Embed Size (px)

Citation preview

Building Material Shortages: Joint

Results from Home Builder and

Lumber Dealer Surveys

June 2013

1

In May of 2013, the National Association of Home Builders (NAHB) and National Lumber and Building

Material Dealers Association (NLBMDA) undertook a joint effort to survey their respective members on

building material shortages and prices.

The NAHB survey took the form of special questions appended to the monthly survey that serves as

the basis for the NAHB/Wells Fargo Housing Market Index (HMI). The HMI survey is sent to a panel of

builders primarily to gauge the overall strength of the single-family housing market, but also often

includes a set of special questions on a topic of current interest to the housing industry. Since 1994 the

survey has periodically included special questions on the availability of building materials. In 2011

these material questions were expanded to cover price changes over the past six months, and the

expanded questions were the ones included on the May 2013 questionnaire.

In that same month, NLBMDA partnered with NAHB to conduct a similar survey of NLBMDA members.

To the extent possible given the nature of the businesses, the questions on the NLBMDA survey were

the same as those on the NAHB survey. NLBMDA’s members operate single or multiple lumber yards

and component plants serving the residential construction industry, so they deal in many of the same

products single-family builders purchase, but are one step upstream in the distribution channel.

Survey data were collected from both NAHB builders and NLBMDA dealers during the first half of May.

Over that approximately two-week span, 383 builders and 230 dealers provided responses.

Highlights of the results include the following:

Reflecting the modest recovery in the housing industry, lumber and building material dealers

reported an average 6.9 percent increase in the volume of their sales over the past six months

(Exhibit 1).

As a class, the lumber dealers handle all of the 24 products purchased by single family builders

that were covered in the two surveys.

Dealers are much more likely to handle some products than others. For example, 95 to 96

percent of them handle framing lumber, OSB and plywood; but only 12 percent handle HVAC

equipment (Exhibit 2).

Among builders, the highest incidence of shortages was for OSB (with 22 percent of builders

reporting shortages), followed by gypsum wall board (20 percent), framing lumber (18 percent)

and plywood (also 18 percent).

Except for wall board, the incidence of shortages for these products was higher among dealers,

with 27 to 28 percent reporting shortages of OSB and plywood, and 36 percent reporting a

shortage of framing lumber (Exhibit 3). Dealers are a step upstream in the distribution channel,

so this may reflect advance knowledge of shortages before they are experienced by home

builders.

For most of the 24 products and materials covered by the survey, the share of builders reporting

a shortage was much higher in May of 2013 than it was in 2011 or 2012. The only exceptions

were copper wire, vinyl siding, HVAC, insulation, and SIPs (Exhibit 8).

2

For example, the share of builders reporting a shortage of framing lumber jumped from 3 to 4

percent in 2011 and 2012 to 18 percent in May of 2013 (Exhibit 4). The share had been as high

as 24 percent in October of 2004, but starts at that time were over 2 million.

Similarly, the share of builders reporting a shortage of gypsum wall board increased from 6

percent in 2011 to 11 percent in 2012 and 20 percent in May of 2013 (Exhibit 5). The share had

been as high as 34 percent in May of 2006, but starts were near 2 million at that time.

The share of builders reporting a shortage of OSB jumped from 3 to 4 percent in 2011 and 2012

to 22 percent in May of 2013 (Exhibit 6). The share had been as high as 52 percent in October

of 2003, when starts were 1.9 million.

The share of builders reporting a shortage of plywood jumped from 2 to 3 percent in 2011 and

2012 to 18 percent in May of 2013 (Exhibit 7). The share had been as high as 39 percent in

October of 2003.

The increase in the incidence of shortages in May of 2013 is surprising at this early stage of

the housing recovery, with total housing starts just now edging up to a rate of million a year—

about the level of starts in the industry’s worst post-war recession before 2008.

Ninety to 92 percent of single-family builders reported that prices of OSB, framing lumber and

plywood had increased. The percentages were even higher (95 to 96) among the lumber and

building material dealers.

With the exception of 3 concrete-related products, a larger share of lumber dealers than builders

reported price increases (Exhibit 9).

On average, builders reported a 5.17 percent increase in the materials that go into a house over

the past six months. For the lumber dealers, an average couldn’t be calculated, because most

of them checked the upper ended category “10 percent or more” (Exhibit 10).

The greater average price increase reported by the lumber dealers could in part reflect advance

knowledge by businesses upstream in the distribution channel, but it is also likely a result of the

product mix differences shown in Exhibit 2.

In May of 2013, the share of builders reporting that prices had increased over the past 6 months

was higher than in either 2011 or 2012 for every building product or material, except vinyl siding,

roofing, and cooper wiring (Exhibit 11).

These results are discussed in more detail in the subsequent section. Following that, Appendix IA

shows detailed tables for single-family builders who responded to NAHB’s May 2013 survey, with

results broken down by region of the country and number of units started. Appendix IB shows detailed

tables for the lumber and building material dealers who responded to NLBMDA’s May 2013 survey, with

results broken down by gross sales volume. Appendix II reproduces the questionnaires used in the two

surveys.

3

Increase in Market Activity

In response to questions about the total volume of their sales, 21 percent of NLBMDA members said

sales had stayed about the same of the past 6 months, 16 percent said sales had increased at least 10

but less than 15 percent, and 15 percent said sales had increased at least 5 but less than 10 percent

(Exhibit 1). On average across all lumber and building material dealers responding to the survey, sales

over the past six months increased 6.9 percent.

*Calculated assuming the midpoint of each category, with the highest and lowest values restricted to

stay within the top and bottom 15 percent of the observations, a procedure called “Winsorizing” that is

designed to limit the influence of extreme values. Because Winsorizing uses more of the information

available in the data, statisticians generally consider it preferable to the median for this purpose.

This reflects a general increase in home building activity over that same period, as the housing industry

is in the process of recovering from a historic trough. The monthly starts series has been volatile,

especially in the last months before the builder and lumber dealer surveys were conducted, but the

number of units under construction at any one time (which is probably a better indication of demand for

building materials than starts) has been rising consistently every month.

In October of 2012, the seasonally adjusted number of housing units under construction was 520,000.

In April of 2013 it was 605,000—a 16 percent increase. This is above the average increase in sales

reported by lumber dealers in general, although the larger dealers seem to have done somewhat better.

The average increase in sales over the past six months was 10.9 percent for dealers with $10 to $20

million in annual gross revenue and 12.8 percent for those with over $30 million (Appendix IB).

14%

21%

14%

15%

16%

6%

6%

8%

Declined

Stayed about the same

Increased by less than 5%

Increased 5% to 10%

Increased 10% to 15%

Increased 15% to 20%

Increased 20% to 30%

Increased 30% or more

Exhibit 1. CHANGE IN SALES VOLUME FOR LUMBER DEALERS PAST SIX MONTHS

Average=6.9%*

4

Evidence of Shortages

Before investigating shortages for particular building products and materials, it’s necessary to consider

the mix of products purchased by home builders and lumber dealers. Both the builder and dealer

surveys asked about the same 24 distinct categories of products. Three quarters of these products are

purchased by the vast majority (over 80 percent) of single-family builders. Not surprisingly, virtually all

builders reported buying products such as roofing materials, wall board, windows and doors, and

framing lumber (Exhibit 2).

Many of these products are bought and sold by the vast majority lumber dealers as well. For example,

95 to 96 percent of lumber dealers purchase framing lumber, OSB and plywood. Considered as a

class, lumber dealers sell all 24 building products covered in the survey, but some products are sold by

a relatively small share. The leading example is HVAC equipment—a product line for only 12 percent

of the dealers.

These results are consistent with a recent NAHB survey that asked builders about where they go to buy

various products. Over 80 percent of single-family builders said they usually buy sawn lumber, plywood

and OSB from lumber yards, but only 1 percent cited lumber yards as the main source for HVAC

equipment. (See the HousingEconomics.com Special Study for November 2012 “Buying Products for

Home Building & Remodeling: Who and Where” for the complete breakdown.)

Exhibit 3 shows the shares of home builders and lumber dealers who reported shortages of each of the

24 building products, based only on the builders and dealers who actually purchase these products.

The percentages in the exhibit are builders and dealers who reported either “some” or a “serious”

shortage for a particular product. Relatively few respondents classified any of the shortages as serious

(see Exhibit 8, Appendix IA and Appendix IB for separate some/serious percentages).

For the home builders’ perspective, shortages of OSB are the most widespread of any building material

(with 22 percent of builders reporting some or serious shortages), followed by gypsum wall board (20

percent), framing lumber (18 percent) and plywood (also 18 percent).

A smaller share of lumber dealers reported a shortage of wall board, but 27 to 28 percent of the dealers

reported shortages of OSB and plywood—and 36 percent reported a shortage of framing lumber.

These numbers are higher than the share of builders reporting shortages of any product or material.

Substantial numbers of lumber dealers also reported shortages of roofing material and millwork—29

and 21 percent, respectively, much higher than the share of home builders who were experiencing a

shortage of these items.

Shortage is a relative term, and we have no history on how the building material dealers reacted to past

cycles. So it’s unclear whether they are actually experiencing worse shortages than builders, reacting

to the shortages that do exist with greater concern, or witnessing trends earlier because they are

upstream in the distribution channel.

5

14%

24%

35%

30%

57%

25%

57%

82%

58%

95%

37%

96%

58%

50%

12%

56%

40%

25%

85%

95%

92%

90%

86%

80%

61%

32%

37%

62%

66%

74%

83%

87%

88%

89%

93%

95%

95%

96%

96%

97%

97%

97%

98%

99%

99%

99%

99%

99%

Other

Structural Insulated Panels

Steel (Lightweight)

Steel Beams

Vinyl siding

Clay brick

Concrete brick and block

Trusses

Cement

Plywood

Copper wiring

Orient Strand Board (OSB)

Ready-mix concrete

Hardwood flooring

HVAC equipment

Cabinets

Plumbing fixtures & fittings

Ceramic Tiles

Insulation material

Framing lumber

Windows and Doors

Millwork

Gypsum wall board

Roofing materials

BUILDERS

DEALERS

Exhibit 2. SHARE WHO PURCHASE VARIOUS MATERIALS

6

17%

0%

2%

2%

2%

2%

3%

4%

9%

1%

4%

4%

10%

21%

4%

9%

4%

29%

5%

10%

27%

36%

12%

28%

11%

3%

4%

5%

6%

6%

6%

6%

6%

7%

7%

8%

8%

8%

9%

9%

10%

12%

13%

14%

18%

18%

20%

22%

Other

HVAC equipment

Vinyl siding

Cement

Ceramic Tiles

Plumbing fixtures & fittings

Steel Beams

Copper wiring

Insulation material

Ready-mix concrete

Concrete brick and block

Steel (Lightweight)

Hardwood flooring

Millwork

Cabinets

Windows and Doors

Structural Insulated Panels

Roofing materials

Clay brick

Trusses

Plywood

Framing lumber

Gypsum wall board

Orient Strand Board (OSB)

BUILDERS

DEALERS

Exhibit 3. SHARE REPORTING A SHORTAGE (EITHER SERIOUS OR SOME)

Based on Builders and Dealers Who Purchase the Materials

7

The Shortages in Historical Perspective

As mentioned in the introduction, the HMI has included questions on building materials for over

a decade, so history is available on shortages reported by builders. Between May 2006 and

June of 2011, the home building industry was either in severe decline or lying near the bottom

of a historically low trough, so material shortages were not an issue that needed to be

addressed in the survey. In June 2011 the questions on building materials were revised

slightly, primarily by expanding the list to include 24 distinct products, and the revised versions

of the questions were repeated in April of 2012 and, most recently, in May of 2013.

In 2011 and 2012, the residential construction industry had not recovered very far yet, and,

where the data were comparable, the share of builders reporting shortages was near historic

lows. But in May of 2013 a modest housing recovery was under way, and the share of builders

reporting a shortage in most cases rose substantially above the 2001-2012 levels. The only

exceptions were copper wire and vinyl siding (availability of which improved modestly since

2011), HVAC and insulation materials (which stayed about the same), and structural insulated

panels (availability of which was worse in 2013 than in 2012, but about the same as in 2011).

The increase in the incidence of shortages reported by builders was strongest in gypsum wall

board and various lumber categories. Over the longer term, shortages of these materials have

at times been more widespread, but the current shortages are surprisingly at this early stage of

the housing recovery. Total housing starts are just now edging up to a rate of million a year,

about the level of starts in the industry’s worst post-war recession before 2008.

Exhibit 4 compares the percentage of builders reporting a shortage of framing lumber to the

seasonally adjusted annual rate of housing starts since 2001. The share reporting a shortage

jumped from 3 to 4 percent in 2011 and 2012 to 18 percent in May of 2013. The share had

been as high as 24 percent in October of 2004, when starts were over 2 million. So 18 percent

is a surprisingly high incidence of shortages given the current starts rate of under 1 million. In

comparison, 36 percent of lumber dealers reported a shortage of framing lumber in May of

2013.

Exhibit 5 compares the percentage of builders reporting a shortage of gypsum wall board to

the seasonally adjusted annual rate of housing starts since 2001. The share reporting a

shortage increased from 6 percent in 2011 to 11 percent in 2012 and 20 percent in May of

2013. The share had been as high as 34 percent in May of 2006, when starts were near 2

million. So 20 percent is a surprisingly high incidence of shortage given the current starts rate

of under 1 million. In comparison, only 12 of lumber dealers reported a shortage of wall board

in May of 2013.

8

0

0.05

0.1

0.15

0.2

0.25

0

500

1,000

1,500

2,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Shortage Starts

Exhibit 4. HOUSING STARTS (AREA) AND

FRAMING LUMBER SHORTAGE (BARS)

0

0.05

0.1

0.15

0.2

0.25

0.3

0

500

1,000

1,500

2,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Shortage Starts

Exhibit 5. HOUSING STARTS (AREA) AND

GYPSUM WALLBOARD SHORTAGE (BARS)

9

Exhibit 6 compares the percentage of builders reporting a shortage of OSB to the seasonally

adjusted annual rate of housing starts since 2001. The share reporting a shortage jumped

from 3 to 4 percent in 2011 and 2012 to 22 percent in May of 2013. The share had been as

high as 52 percent in October of 2003, when starts were 1.9 million. So a surge to 22 percent

is surprising given the current starts rate of under 1 million. In comparison, 28 of lumber

dealers reported a shortage of OSB in May of 2013.

Exhibit 7 compares the percentage of builders reporting a shortage of plywood to the

seasonally adjusted annual rate of housing starts since 2001. The share reporting a shortage

jumped from 2 to 3 percent in 2011 and 2012 to 18 percent in May of 2013. The share had

been as high as 39 percent in October of 2003, when starts were 1.9 million. So 18 percent is

a surprisingly high incidence of shortages given the current starts rate of under 1 million. In

comparison, 27 of lumber dealers reported a shortage of plywood in May of 2013.

Exhibit 8 shows the complete history of responses to the HMI question on shortages of

building materials.

10

0

0.1

0.2

0.3

0.4

0

500

1,000

1,500

2,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Shortage Starts

Exhibit 7. HOUSING STARTS (AREA) AND

PLYWOOD SHORTAGE (BARS)

0

0.1

0.2

0.3

0.4

0.5

0

500

1,000

1,500

2,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Shortage Starts

Exhibit 6. HOUSING STARTS (AREA) AND

OSB SHORTAGE (BARS)

11

Exhibit 8. Current Availability of Materials – HISTORY (Percent of Respondents)

No

Shortage

Some

Shortage

Serious

Shortage

Cement/Ready-mix concrete+

May-13 94% 6% 0%

Apr-12 98% 2% 0%

Jun-11 97% 3% 0%

May-06 75% 23% 1%

Nov-05 68% 28% 4%

Oct-05 64% 29% 7%

Jul-05 71% 25% 5%

Jan-05 71% 24% 4%

Oct-04 61% 34% 4%

Jul-04 59% 34% 7%

May-04 88% 8% 3%

Mar-04 96% 3% 0%

Oct-03 98% 2% 0%

Oct-02 98% 2% 0%

Jun-01 96% 4% 0%

Jul-00 89% 11% 0%

Jan-00 90% 10% 0%

Mar-99 87% 13% 0%

Jun-98 86% 10% 4%

Dec-96 90% 8% 2%

Sep-94 90% 8% 2%

Ready-mix concrete

May-13 93% 7% 0%

Apr-12 97% 3% 0%

Jun-11 98% 2% 0%

Jul-05 70% 26% 3%

Jan-05 73% 24% 3%

12

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage

Some

Shortage

Serious

Shortage

Concrete brick and block

May-13 94% 6% 0%

Apr-12 96% 4% 0%

Jun-11 96% 2% 0%

May-06 83% 16% 1%

Nov-05 75% 23% 2%

Oct-05 73% 24% 5%

Jul-05 80% 18% 2%

Jan-05 80% 15% 6%

Oct-04 73% 23% 6%

Jul-04 75% 20% 4%

May-04 88% 10% 2%

Mar-04 93% 7% 0%

Oct-03 96% 4% 0%

Oct-02 96% 4% 0%

Jun-01 88% 12% 0%

Jul-00 76% 20% 5%

Jan-00 80% 18% 2%

Mar-99 91% 8% 1%

Jun-98 92% 6% 2%

Clay brick

May-13 86% 14% 0%

Apr-12 95% 5% 0%

Jun-11 96% 4% 0%

May-06 74% 21% 5%

Nov-05 71% 25% 4%

Oct-05 72% 21% 6%

Jul-05 70% 27% 4%

Jan-05 70% 25% 5%

Oct-04 59% 33% 8%

Jul-04 63% 30% 7%

May-04 77% 20% 2%

Mar-04 77% 22% 1%

Oct-03 91% 9% 0%

Oct-02 88% 12% 0%

Jun-01 69% 27% 4%

Jul-00 50% 34% 16%

Jan-00 40% 39% 21%

Mar-99 77% 20% 3%

Jun-98 87% 12% 1%

13

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage

Some

Shortage

Serious

Shortage

Vinyl siding

May-13 97% 3% 0%

Apr-12 96% 3% 0%

Jun-11 94% 4% 0%

Insulation material

May-13 95% 6% 0%

Apr-12 95% 5% 0%

Jun-11 94% 5% 0%

May-06 80% 18% 2%

Nov-05 87% 12% 1%

Oct-05 86% 13% 1%

Jul-05 90% 10% 0%

Jan-05 86% 13% 0%

Oct-04 80% 19% 2%

Jul-04 80% 19% 1%

May-04 87% 12% 0%

Mar-04 89% 10% 0%

Oct-03 96% 3% 1%

Oct-02 94% 6% 0%

Jun-01 98% 2% 0%

Jul-00 80% 20% 0%

Jan-00 61% 37% 1%

Mar-99 58% 34% 7%

Jun-98 88% 10% 2%

Structural Insulated Panels (SIP)

May-13 91% 9% 0%

Apr-12 97% 3% 0%

Jun-11 91% 9% 0%

May-06 92% 8% 0%

Nov-05 94% 3% 0%

Oct-05 91% 9% 0%

Oct-04 87% 8% 5%

Jul-04 89% 8% 3%

May-04 88% 7% 5%

Mar-04 95% 5% 3%

14

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage

Some

Shortage

Serious

Shortage

Steel (Lightweight for framing)

May-13 92% 8% 0%

Apr-12 95% 7% 0%

Jun-11 93% 7% 2%

May-06 93% 5% 0%

Nov-05 79% 19% 2%

Oct-05 87% 10% 3%

Oct-04 71% 24% 5%

Jul-04 74% 19% 5%

May-04 68% 25% 8%

Mar-04 86% 13% 2%

Steel Beams

May-13 94% 6% 0%

Apr-12 96% 4% 0%

Jun-11 95% 5% 2%

May-06 91% 9% 0%

Nov-05 88% 10% 1%

Oct-05 90% 9% 1%

Oct-04 79% 16% 4%

Jul-04 81% 18% 1%

May-04 76% 20% 4%

Mar-04 86% 10% 4%

Trusses

May-13 86% 13% 1%

Apr-12 98% 2% 0%

Jun-11 97% 2% 0%

May-06 94% 6% 0%

Nov-05 93% 7% 0%

Oct-05 88% 11% 1%

Jul-05 95% 4% 0%

Jan-05 92% 7% 0%

Oct-04 86% 12% 2%

Jul-04 90% 9% 0%

May-04 92% 7% 0%

Mar-04 93% 5% 0%

15

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage Some

Shortage Serious

Shortage

Framing lumber

May-13 82% 16% 2% Apr-12 97% 3% 0% Jun-11 96% 4% 0%

May-06 95% 5% 0% Nov-05 88% 11% 1%

Oct-05 80% 18% 2% Jul-05 95% 5% 0% Jan-05 88% 12% 0%

Oct-04 76% 23% 1% Jul-04 84% 13% 2%

May-04 81% 17% 2% Mar-04 79% 20% 1% Oct-03 84% 14% 2%

Oct-02 99% 1% 0% Jun-01 96% 4% 0%

Jul-00 92% 8% 0% Jan-00 90% 9% 1% Mar-99 90% 9% 1%

Jun-98 93% 7% 0% Dec-96 78% 21% 1%

Sep-94 81% 18% 1%

Gypsum wall board

May-13 80% 18% 2% Apr-12 89% 11% 0%

Jun-11 94% 6% 0% May-06 66% 29% 5% Nov-05 71% 26% 3%

Oct-05 73% 23% 3% Jul-05 78% 21% 1%

Jan-05 83% 16% 1% Oct-04 73% 25% 1% Jul-04 75% 24% 1%

May-04 81% 17% 2% Mar-04 83% 16% 0%

Oct-03 89% 11% 0% Oct-02 92% 8% 0% Jun-01 91% 9% 0%

Jul-00 72% 26% 2% Jan-00 31% 61% 8%

Mar-99 40% 41% 18% Jun-98 84% 15% 1% Dec-96 73% 23% 3%

Sep-94 76% 23% 1%

16

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage

Some

Shortage

Serious

Shortage

Orient Strand Board (OSB)

May-13 78% 19% 3%

Apr-12 96% 4% 0%

Jun-11 97% 3% 0%

May-06 89% 11% 1%

Nov-05 73% 25% 2%

Oct-05 68% 26% 6%

Jul-05 91% 9% 0%

Jan-05 77% 22% 0%

Oct-04 63% 33% 3%

Jul-04 69% 26% 5%

May-04 70% 22% 7%

Mar-04 55% 40% 6%

Oct-03 47% 37% 15%

Oct-02 98% 2% 0%

Jun-01 97% 3% 0%

Plywood

May-13 81% 16% 2%

Apr-12 97% 3% 0%

Jun-11 98% 2% 0%

May-06 89% 10% 0%

Nov-05 76% 21% 2%

Oct-05 71% 23% 5%

Jul-05 90% 10% 0%

Jan-05 82% 16% 1%

Oct-04 69% 29% 2%

Jul-04 76% 22% 3%

May-04 72% 22% 7%

Mar-04 63% 33% 4%

Oct-03 61% 29% 10%

Oct-02 98% 2% 0%

Jun-01 96% 4% 0%

Jan-00# 90% 10% 0%

Cabinets

May-13 91% 7% 1%

Apr-12 97% 3% 0%

Jun-11 98% 2% 0%

17

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage Some

Shortage Serious

Shortage

Millwork

May-13 92% 8% 0% Apr-12 97% 3% 0% Jun-11 95% 4% 0%

Windows and Doors

May-13 91% 9% 0%

Apr-12 98% 2% 0% Jun-11 96% 4% 0%

May-06 93% 6% 1% Nov-05 94% 5% 1%

Oct-05 93% 5% 1% Jul-05 95% 4% 0% Jan-05 95% 6% 0%

Oct-04 93% 7% 0% Jul-04 96% 4% 0%

May-04 96% 3% 0% Mar-04 96% 3% 0% Oct-03 97% 2% 1%

Oct-02 98% 2% 0% Jun-01 96% 4% 0%

Jul-00 90% 10% 0%

Hardwood flooring

May-13 94% 6% 1% Apr-12 97% 3% 0%

Jun-11 99% 1% 0%

Ceramic Tiles

May-13 95% 5% 1% Apr-12 94% 5% 0% Jun-11 96% 3% 1%

Roofing materials

May-13 88% 11% 1% Apr-12 91% 8% 1% Jun-11 89% 10% 1%

May-06 81% 17% 2% Nov-05 78% 19% 2%

Oct-05 75% 18% 6% Jul-05 81% 14% 5% Jan-05 81% 14% 6%

Oct-04 79% 19% 3% Jul-04 88% 10% 1%

May-04 90% 9% 1% Mar-04 91% 9% 0% Oct-03 95% 4% 1%

18

Exhibit 8. Current Availability of Materials – HISTORY (continued) (Percent of Respondents)

No

Shortage Some

Shortage Serious

Shortage

Roofing materials - continued

Oct-02 96% 4% 0% Jun-01 95% 5% 0% Jul-00 89% 10% 0%

Jan-00 88% 12% 0% Mar-99 90% 9% 1%

Plumbing fixtures & fittings

May-13 94% 6% 0%

Apr-12 96% 3% 0%

Jun-11 97% 3% 0%

HVAC equipment

May-13 97% 3% 0%

Apr-12 98% 1% 0%

Jun-11 97% 2% 0%

Copper wiring

May-13 95% 4% 1%

Apr-12 93% 6% 0%

Jun-11 90% 9% 1%

Notes: (+) Prior to Jan. '05 Cement and ready-mix concrete were combined.

(#) Plywood/OSB.

19

Price Changes

For the same 24 categories of building products and materials, the two surveys also asked if prices

over the past 6 months had increased, declined, or remained unchanged. In May of 2013, very few

respondents reported that prices for any product or material had declined recently (Appendix IA and

IB).

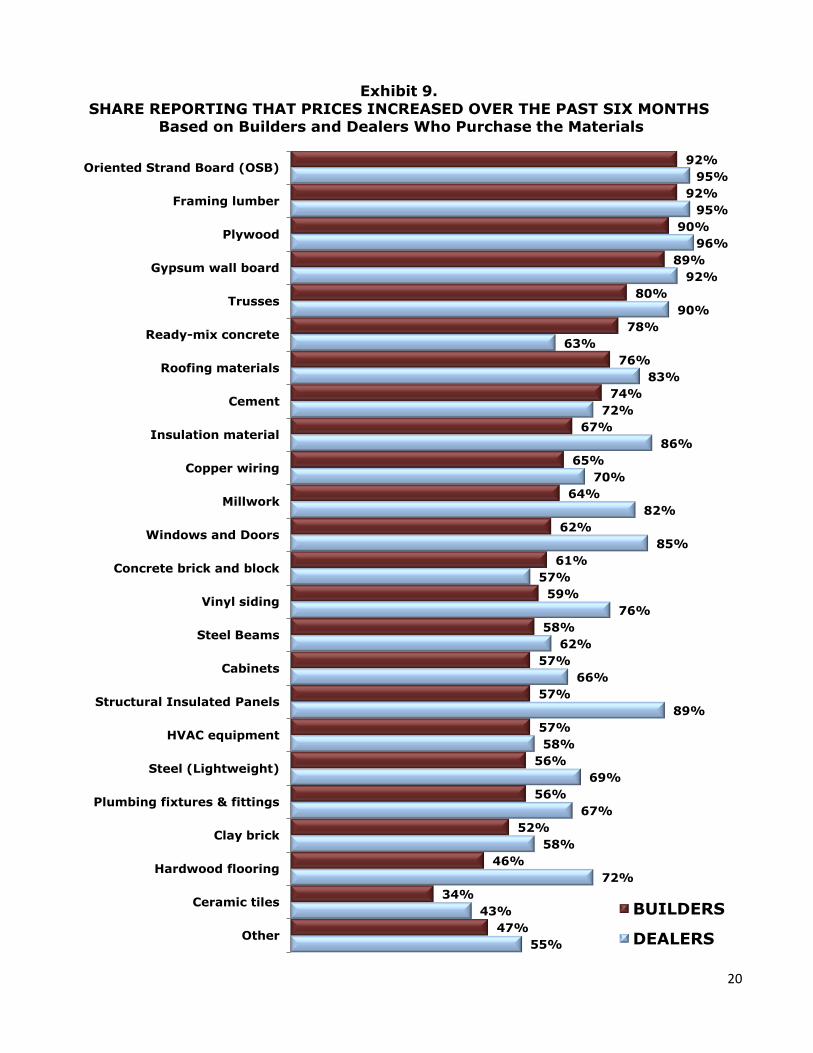

Exhibit 9 shows the share who reported prices had increased (again, based on home builders and

lumber dealers who purchased the products). Ninety to 92 percent of single-family builders reported

that prices of OSB, framing lumber and plywood had increased. The percentages were even higher (95

to 96) among the lumber and building material dealers. With the exception of the 3 concrete-related

products (cement, ready-mix concrete and concrete brick and block), more lumber dealers than

builders reported price increases. The dealer-builder differences were particularly strong for insulation

materials, millwork, windows and doors, vinyl siding, SIPs, and hardwood flooring. Note that, in most of

these cases, the vast majority of lumber and building material dealers were reporting price increases

even though relatively few of them were reporting shortages for the same materials.

That still leaves the question of how quickly prices are rising. To get a rough idea, the two surveys

asked over the past six month how prices had changed overall, either for materials that go into a house

(for home builders) or for all products sold (for lumber and building material dealers). On average

builders reported a 5.17 percent increase in the materials that go into a house over the past six months.

For the lumber dealers, an average couldn’t be calculated, because most of them checked the upper

ended category “10 percent or more” (Exhibit 10).

The greater average price increase reported by the lumber dealers could in part reflect advance

knowledge by businesses in the distribution channel, but it is likely also a result of the product mix

differences shown in Exhibit 2. Lumber dealers tend to be engaged in selling products like OSB,

framing lumber, plywood and wallboard, where the incidence of shortages and price increases are

disproportionately high.

Limited history on price changes is available from the HMI survey of single-family builders (Exhibit 11).

The 24-item price question was asked in its current form in June of 2011 and April of 2012. In May of

2013, the share of builders reporting that prices had increased over the past 6 months was higher than

in either 2011 or 2012 for every building product or material, except vinyl siding, roofing, and cooper

wiring.

20

55%

43%

72%

58%

67%

69%

58%

89%

66%

62%

76%

57%

85%

82%

70%

86%

72%

83%

63%

90%

92%

96%

95%

95%

47%

34%

46%

52%

56%

56%

57%

57%

57%

58%

59%

61%

62%

64%

65%

67%

74%

76%

78%

80%

89%

90%

92%

92%

Other

Ceramic tiles

Hardwood flooring

Clay brick

Plumbing fixtures & fittings

Steel (Lightweight)

HVAC equipment

Structural Insulated Panels

Cabinets

Steel Beams

Vinyl siding

Concrete brick and block

Windows and Doors

Millwork

Copper wiring

Insulation material

Cement

Roofing materials

Ready-mix concrete

Trusses

Gypsum wall board

Plywood

Framing lumber

Oriented Strand Board (OSB)

BUILDERS

DEALERS

Exhibit 9.

SHARE REPORTING THAT PRICES INCREASED OVER THE PAST SIX MONTHS Based on Builders and Dealers Who Purchase the Materials

21

*Calculated assuming the midpoint of each category, with the highest and lowest values restricted to

stay within the top and bottom 18 percent of the observations, a procedure called “Winsorizing” (see

footnote to Exhibit 2).

0%

3%

10%

30%

26%

13%

5%

14%

0%

1%

1%

9%

15%

12%

7%

54%

Decreased

Stayed about the same

Increased less than 2%

Increased 2% to 4%

Increased 4% to 6%

Increased 6% to 8%

Increased 8% to 10%

Increased 10% or more

Exhibit 10.

OVERALL CHANGE IN MATERIAL PRICES PAST 6 MONTHS For Same House/Across All Products Sold

BUILDERS

DEALERS

Average Increase:

BUILDERS=5.17%*

DEALERS= Over 10%

22

Exhibit 11. Change in prices now vs. 6 months ago – HISTORY

(Percent of Respondents)

Based on builders who purchase the materials only

June 2011 April 2012 May 2013

Cement

Increased 60 67 74

Decreased 3 1 0

No change 37 33 26

Ready-mix concrete

Increased 64 70 78

Decreased 5 1 0

No change 31 29 22

Concrete brick and block

Increased 42 51 61 Decreased 2 1 0 No change 56 48 39

Clay brick

Increased 35 35 52 Decreased 2 3 0 No change 63 61 48

Vinyl siding

Increased 62 60 59 Decreased 2 1 0 No change 37 38 41

Insulation material

Increased 49 59 67 Decreased 3 1 1 No change 48 40 32

Structural Insulated Panels

Increased 42 40 57 Decreased 4 1 0 No change 54 59 43

Steel (Lightweight)

Increased 53 45 56 Decreased 1 2 0 No change 46 53 44

Steel Beams

Increased 56 55 58 Decreased 2 2 1 No change 42 43 41

Trusses

Increased 37 51 80 Decreased 8 5 1 No change 55 44 19

23

Exhibit 11. Change in prices now vs. 6 months ago – HISTORY (continued)

(Percent of Respondents)

June 2011 April 2012 May 2013

Framing lumber

Increased 43 58 92

Decreased 18 6 1

No change 39 36 8

Gypsum wall board

Increased 56 79 89

Decreased 5 3 1

No change 40 19 10

Oriented Strand Board (OSB)

Increased 41 61 92

Decreased 12 4 0

No change 47 35 8

Plywood

Increased 45 62 90

Decreased 10 3 1

No change 45 34 10

Cabinets

Increased 32 40 57

Decreased 5 4 2

No change 63 57 41

Millwork

Increased 35 43 64

Decreased 4 4 1

No change 61 53 35

Windows and Doors

Increased 47 51 62

Decreased 5 3 1

No change 48 46 37

Hardwood flooring

Increased 28 30 46

Decreased 6 6 3

No change 66 64 51

Ceramic tiles

Increased 24 26 34

Decreased 4 6 4

No change 71 68 62

24

Exhibit 11. Change in prices now vs. 6 months ago – HISTORY (continued)

(Percent of Respondents)

June 2011 April 2012 May 2013

Roofing materials

Increased 76 77 76 Decreased 3 4 2

No change 21 19 22

Plumbing fixtures & fittings

Increased 47 49 56

Decreased 2 4 2 No change 52 47 42

HVAC equipment

Increased 49 54 57

Decreased 3 4 3

No change 48 42 40

Copper wiring

Increased 72 69 65 Decreased 1 3 4

No change 26 28 32

Other

Increased 36 30 47

Decreased 5 0 5 No change 59 70 49

25

Appendix IA:

Detailed Tables from the Builders Survey

26

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE

(Percent of Respondents)

Total Region

No. of For-Sale Units Started

in 2012

NE MW S W <25 25-99 100+

Cement

No shortage 95 100 99 92 94 95 97 80

Some shortage 5 1 8 6 5 3 20

Serious shortage

Responses 319 29 75 161 54 247 35 20

Ready-mix concrete

No shortage 93 100 97 89 92 93 95 80

Some shortage 7 3 11 8 7 5 20

Serious shortage

Responses 348 33 79 174 62 269 39 20

Concrete brick & block

No shortage 93 100 99 89 96 93 97 89

Some shortage 7 1 11 4 7 3 11

Serious shortage

Responses 303 26 68 160 49 239 32 18

Clay brick

No shortage 87 86 95 81 100 88 86 82

Some shortage 13 14 5 19 12 14 18

Serious shortage

Responses 265 21 64 152 28 205 29 17

Vinyl siding

No shortage 96 100 97 96 91 96 100 100

Some shortage 4 3 4 9 4

Serious shortage

Responses 239 31 68 118 22 189 24 12

Insulation material

No shortage 94 100 95 93 92 94 97 86

Some shortage 6 5 7 8 6 3 14

Serious shortage

Responses 355 34 80 178 63 273 39 22

27

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Region

No. of For-Sale Units Started

in 2012

NE MW S W <25 25-99 100+

Structural Insulated

Panels (SIP)

No shortage 90 100 92 88 89 90 100 83

Some shortage 9 6 12 11 10 17

Serious shortage 1 3

Responses 115 10 36 50 19 88 14 6

Steel (Lightweight for

framing)

No shortage 92 100 94 93 85 92 100 100

Some shortage 8 6 7 15 8

Serious shortage

Responses 130 17 33 54 26 106 13 5

Steel Beams

No shortage 94 96 95 92 92 93 96 100

Some shortage 6 4 5 8 8 7 4

Serious shortage

Responses 219 28 63 92 36 172 26 12

Trusses

No shortage 86 90 91 85 83 89 75 85

Some shortage 13 10 9 13 17 10 25 15

Serious shortage 1 2 1

Responses 315 30 74 148 63 243 36 20

Framing lumber

No shortage 82 82 83 82 80 80 83 91

Some shortage 16 18 16 16 14 17 17 4

Serious shortage 2 1 2 6 3 4

Responses 362 34 82 182 64 276 42 23

Gypsum wall board

No shortage 80 81 82 76 87 79 90 83

Some shortage 18 19 17 21 10 18 10 13

Serious shortage 2 1 2 3 2 4

Responses 356 32 83 178 63 272 41 23

28

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Region

No. of For-Sale Units

Started in 2012

NE MW S W <25 25-99 100+

Oriented Strand Board

(OSB)

No shortage 78 73 82 77 79 78 81 77

Some shortage 19 27 14 18 21 18 19 23

Serious shortage 3 4 5 4

Responses 346 33 78 173 62 263 42 22

Plywood

No shortage 82 76 86 83 75 82 78 84

Some shortage 16 24 11 13 25 15 22 16

Serious shortage 2 3 4 3

Responses 321 33 71 161 56 249 37 19

Cabinets

No shortage 91 97 96 87 94 93 93 74

Some shortage 8 3 4 11 6 6 8 22

Serious shortage 1 2 1 4

Responses 352 34 82 174 62 270 40 23

Millwork

No shortage 92 100 95 90 87 90 98 91

Some shortage 8 5 9 13 10 2 4

Serious shortage 0 1 4

Responses 359 33 83 182 61 275 41 23

Windows and Doors

No shortage 91 97 96 86 95 91 90 87

Some shortage 9 3 4 14 5 9 10 13

Serious shortage 0 1 0

Responses 361 34 82 183 62 276 42 23

Hardwood flooring

No shortage 93 97 94 93 90 93 95 91

Some shortage 7 3 6 7 8 7 5 5

Serious shortage 1 1 2 0 5

Responses 352 33 81 179 59 271 39 22

29

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Region

No. of For-Sale Units Started in

2012

NE MW S W <25 25-99 100+

Ceramic tiles

No shortage 94 97 95 93 95 94 95 91

Some shortage 5 3 5 6 5 6 5 9

Serious shortage 1 1 1

Responses 350 33 77 179 61 269 39 23

Roofing materials

No shortage 88 97 88 84 94 87 95 83

Some shortage 11 3 12 14 5 12 5 13

Serious shortage 1 2 2 1 4

Responses 357 33 81 180 63 274 41 23

Plumbing fixtures &

fittings

No shortage 94 100 97 93 90 94 92 91

Some shortage 6 3 7 10 6 8 9

Serious shortage

Responses 349 33 78 175 63 271 39 22

HVAC equipment

No shortage 97 100 99 95 97 96 100 95

Some shortage 3 1 5 3 4 5

Serious shortage

Responses 349 33 79 177 60 270 39 22

Copper wiring

No shortage 95 100 96 93 93 95 95 95

Some shortage 5 4 5 7 4 5 5

Serious shortage 1 1 1

Responses 333 30 77 168 58 257 38 20

Other

No shortage 89 100 96 82 88 88 90 83

Some shortage 9 4 15 6 10 17

Serious shortage 2 3 6 1 10

Responses 89 6 27 39 17 68 10 6

30

Q1. Change in prices now vs. 6 months ago

(Percent of Respondents)

Total Region

No. of For-Sale Units Started

in 2012

NE MW S W <25 25-99 100+

Cement

Increased 74 69 71 76 76 74 76 84

Decreased

No change 26 31 29 24 24 26 24 16

Responses 301 26 70 156 49 232 34 19

Ready-mix concrete

Increased 78 77 74 79 78 76 76 100

Decreased

No change 22 23 26 21 22 24 24

Responses 327 31 73 165 58 252 37 20

Concrete brick and

block

Increased 61 59 54 61 69 61 53 65

Decreased 0 1 3

No change 39 41 46 38 31 39 43 35

Responses 272 22 59 149 42 214 30 17

Clay brick

Increased 52 65 44 54 48 54 33 44

Decreased 0 1 4

No change 48 35 56 45 52 46 63 56

Responses 236 17 57 137 25 180 27 16

Vinyl siding

Increased 59 79 65 55 35 60 48 50

Decreased 0 1 1

No change 41 21 35 45 65 39 52 50

Responses 221 28 63 110 20 174 23 12

Insulation material

Increased 67 67 64 65 75 67 57 73

Decreased 1 2 1

No change 32 33 36 33 25 32 43 27

Responses 327 30 76 164 57 250 37 22

31

Q1. Change in prices now vs. 6 months ago - continued

(Percent of Respondents)

Total Region

No. of For-Sale Units

Started in 2012

NE MW S W <25 25-99 100+

Structural Insulated

Panels (SIP)

Increased 57 50 52 68 44 57 30 83

Decreased

No change 43 50 48 33 56 43 70 17

Responses 93 6 31 40 16 72 10 6

Steel (Lightweight for

framing)

Increased 56 58 56 56 55 57 44 60

Decreased

No change 44 42 44 44 45 43 56 40

Responses 106 12 27 45 22 87 9 5

Steel Beams

Increased 58 60 60 54 66 61 46 64

Decreased 1 2 1 1 9

No change 41 40 38 45 34 38 54 27

Responses 195 25 58 80 32 151 24 11

Trusses

Increased 80 73 81 80 80 80 75 85

Decreased 1 1 1 0 3

No change 19 27 17 18 20 19 22 15

Responses 296 26 70 141 59 227 36 20

Framing lumber

Increased 92 91 91 91 95 91 93 96

Decreased 1 1 2 1 4

No change 8 9 9 8 3 8 7

Responses 346 32 77 177 60 262 42 23

Gypsum wall board

Increased 89 93 86 91 88 90 82 91

Decreased 1 2 1

No change 10 7 14 8 12 9 18 9

Responses 336 30 78 169 59 258 39 23

32

Q1. Change in prices now vs. 6 months ago – continued

(Percent of Respondents)

Total Region

No. of For-Sale Units Started in

2012

NE MW S W <25 25-99 100+

Oriented Strand Board

(OSB)

Increased 92 93 93 91 90 91 93 90

Decreased 0 2 5

No change 8 7 7 9 8 9 8 5

Responses 331 29 76 167 59 252 40 21

Plywood

Increased 90 93 91 88 92 90 91 94

Decreased 1 1 2 1

No change 9 7 9 11 6 10 9 6

Responses 298 28 67 153 50 231 35 18

Cabinets

Increased 57 67 54 58 55 59 49 45

Decreased 2 1 3 2

No change 41 33 45 39 45 39 51 55

Responses 328 27 76 165 60 251 39 22

Millwork

Increased 64 54 60 67 66 65 60 59

Decreased 1 1 1 1

No change 35 46 38 32 34 34 40 41

Responses 335 26 78 172 59 255 40 22

Windows and Doors

Increased 62 76 56 60 67 63 56 50

Decreased 1 1 2 2

No change 37 24 42 38 33 35 44 50

Responses 337 29 78 170 60 257 41 22

Hardwood flooring

Increased 46 45 47 46 47 50 36 25

Decreased 3 3 5 3 3

No change 51 55 50 49 53 47 61 75

Responses 322 29 74 166 53 249 36 20

33

Q1. Change in prices now vs. 6 months ago - continued

(Percent of Respondents)

Total Region

No. of For-Sale Units

Started in 2012

NE MW S W <25 25-99 100+

Ceramic tiles

Increased 34 36 35 33 37 36 22 27

Decreased 4 4 5 2 4 3

No change 62 64 61 62 61 60 76 73

Responses 324 28 72 167 57 248 37 22

Roofing materials

Increased 76 80 79 74 76 76 70 73

Decreased 2 1 3 2 3 9

No change 22 20 19 23 24 22 28 18

Responses 338 30 77 172 59 259 40 22

Plumbing fixtures &

fittings

Increased 56 48 56 54 65 57 54 43

Decreased 2 3 2 2 3

No change 42 52 41 43 35 42 43 57

Responses 325 29 73 166 57 252 37 21

HVAC equipment

Increased 57 55 56 59 52 58 47 48

Decreased 3 4 4 2 3 3

No change 40 45 40 37 46 38 50 52

Responses 323 29 72 166 56 250 36 21

Copper wiring

Increased 65 58 68 64 63 67 50 58

Decreased 4 4 5 2 4 6

No change 32 42 28 31 35 29 44 42

Responses 299 24 72 151 52 230 34 19

Other

Increased 47 0 46 50 40 43 50 50

Decreased 5 0 15 6

No change 49 0 38 50 60 51 50 50

Responses 43 0 13 20 10 35 2 4

34

Q2. Overall, how have total material costs for the same house changed over the past 6 months?

(Percent of respondents)

Total Region

No. of For-Sale Units Started

in 2012

NE MW S W <25 25-99 100+

Declined

Stayed about the same 2.67 2.86 1.18 4.28 3.15

Increased by less than 2% 9.60 20.00 14.12 5.88 8.82 9.79 6.82 8.70

Increased 2% to 3.99% 30.13 40.00 30.59 27.27 32.35 30.77 43.18 13.04

Increased 4% to 5.99% 25.87 28.57 23.53 27.27 23.53 24.83 22.73 47.83

Increased 6% to 7.99% 12.53 2.86 17.65 12.83 10.29 13.99 6.82 13.04

Increased 8% to 9.99% 5.07 4.71 5.35 7.35 4.20 11.36

Increased 10% or more 14.13 5.71 8.24 17.11 17.65 13.29 9.09 17.39

Average* 5.17 3.29 4.69 5.40 5.38 4.76 4.95 5.61

Responses 375 35 85 187 68 286 44 23

*Calculated assuming the midpoint of each category and Winsorizing 18 percent of the responses at the top and bottom.

35

Appendix IB:

Detailed Tables from the Lumber Dealers Survey

36

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Cement

No shortage 98 97 100 94

Some shortage 2 3 6

Responses 131 73 39 18

Ready-mix concrete

No shortage 99 100 97 100

Some shortage 1 3

Responses 131 78 34 18

Concrete brick and block

No shortage 96 95 100 94

Some shortage 4 5 6

Responses 127 73 37 16

Clay brick

No shortage 95 94 100 89

Some shortage 5 6 11

Responses 56 34 12 9

Vinyl siding

No shortage 98 96 100 100

Some shortage 2 4

Responses 128 69 37 20

Insulation material

No shortage 91 89 97 88

Some shortage 9 11 3 12

Responses 192 98 59 33

Structural Insulated Panels (SIP)

No shortage 96 96 95 100

Some shortage 4 4 5

Responses 53 26 19 8

37

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Steel (Lightweight for framing)

No shortage 96 95 95 100

Some shortage 4 5 5

Responses 76 40 21 15

Steel Beams

No shortage 97 100 91 100

Some shortage 3 9

Responses 65 32 22 11

Trusses

No shortage 90 89 89 94

Some shortage 10 11 11 6

Responses 185 97 53 34

Framing lumber

No shortage 64 68 65 54

Some shortage 35 30 34 46

Serious shortage 1 2 2

Responses 217 110 65 41

Gypsum wall board

No shortage 88 91 90 76

Some shortage 12 9 10 24

Responses 197 102 60 34

Oriented Strand Board (OSB)

No shortage 71 72 65 83

Some shortage 27 27 32 18

Serious shortage 1 1 3

Responses 217 110 66 40

38

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Plywood

No shortage 73 74 69 79

Some shortage 26 25 31 21

Serious shortage 1 2

Responses 217 110 68 38

Cabinets

No shortage 96 95 97 96

Some shortage 4 5 3 4

Responses 124 60 38 24

Millwork

No shortage 79 85 75 64

Some shortage 20 14 23 33

Serious shortage 1 1 2 3

Responses 206 107 61 36

Windows and Doors

No shortage 91 88 95 91

Some shortage 9 12 5 9

Responses 206 109 61 34

Hardwood flooring

No shortage 90 95 87 83

Some shortage 9 5 10 17

Serious shortage 1 3

Responses 112 58 30 23

Ceramic tiles

No shortage 98 100 100 91

Some shortage 2 9

Responses 54 28 15 11

39

Q1. Current Availability of Materials : WITHOUT DO NOT PURCHASE - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Roofing materials

No shortage 70 68 75 66

Some shortage 28 30 25 31

Serious shortage 1 1 3

Responses 179 92 53 32

Plumbing fixtures & fittings

No shortage 98 98 95 100

Some shortage 2 2 5

Responses 87 53 20 14

HVAC equipment

No shortage 100 100 100 100

Responses 26 15 6 5

Copper wiring

No shortage 96 100 90 89

Some shortage 4 10 11

Responses 80 50 21 9

Other

No shortage 83 100 100 25

Some shortage 6 25

Serious shortage 11 50

Responses 18 10 4 4

40

Q1. Change in prices now vs. 6 months ago

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Cement

Increased 72 75 67 71

No change 28 25 33 29

Responses 125 71 36 17

Ready-mix concrete

Increased 63 70 48 65

Decreased 1 3

No change 36 30 48 35

Responses 120 69 33 17

Concrete brick and block

Increased 57 59 52 60

Decreased 1 3

No change 42 41 45 40

Responses 115 68 31 15

Clay brick

Increased 58 56 64 56

No change 42 44 36 44

Responses 53 32 11 9

Vinyl siding

Increased 76 75 74 82

Decreased 3 3 12

No change 20 22 26 6

Responses 118 65 34 17

Insulation material

Increased 86 87 85 83

Decreased 3 1 6 3

No change 11 12 9 13

Responses 175 91 53 30

41

Q1. Change in prices now vs. 6 months ago - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Structural Insulated Panels (SIP)

Increased 89 91 88 86

No change 11 9 12 14

Responses 46 22 17 7

Steel (Lightweight for framing)

Increased 69 71 67 64

Decreased 6 14 7

No change 26 29 19 29

Responses 70 35 21 14

Steel Beams

Increased 62 58 63 70

Decreased 2 4

No change 37 38 38 30

Responses 52 26 16 10

Trusses

Increased 90 86 94 97

Decreased 1 2

No change 9 12 6 3

Responses 172 91 49 31

Framing lumber

Increased 95 92 98 95

Decreased 3 4 2 3

No change 2 4 3

Responses 205 104 61 39

Gypsum wall board

Increased 92 93 91 94

Decreased 1 2

No change 7 7 7 6

Responses 186 96 58 31

42

Q1. Change in prices now vs. 6 months ago - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Oriented Strand Board (OSB)

Increased 95 93 97 97

Decreased 3 4 3 3

No change 1 3

Responses 208 105 63 39

Plywood

Increased 96 95 97 97

Decreased 3 3 3 3

No change 1 2

Responses 209 107 64 37

Cabinets

Increased 66 63 71 61

No change 34 37 29 39

Responses 116 57 34 23

Millwork

Increased 82 79 81 91

Decreased 2 2 2 3

No change 16 19 17 6

Responses 195 100 58 35

Windows and Doors

Increased 85 87 81 88

Decreased 2 3

No change 13 11 19 12

Responses 197 104 58 33

Hardwood flooring

Increased 72 66 69 89

No change 28 34 31 11

Responses 92 47 26 18

43

Q1. Change in prices now vs. 6 months ago - continued

(Percent of Respondents)

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Ceramic tiles

Increased 43 36 54 50

Decreased 2 8

No change 54 64 38 50

Responses 46 25 13 8

Roofing materials

Increased 83 86 82 75

Decreased 2 1 4

No change 15 13 14 25

Responses 167 87 50 28

Plumbing fixtures & fittings

Increased 67 70 68 44

Decreased 1 5

No change 32 30 26 56

Responses 72 44 19 9

HVAC equipment

Increased 58 69 50 40

No change 42 31 50 60

Responses 24 13 6 5

Copper wiring

Increased 70 73 59 75

Decreased 4 2 12

No change 26 24 29 25

Responses 70 45 17 8

Other

Increased 55 60 33 67

No change 45 40 67 33

Responses 11 5 3 3

44

Q2. On average across all product lines, how have prices for the materials you sell changed over the

past 6 months?

(Percent of respondents)

Percent

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Stayed about the same 0.88 0.89 0.00 2.22

Increased by less than 2% 1.32 1.79 1.47 0.00

Increased 2% to 3.99% 9.25 14.29 4.41 4.44

Increased 4% to 5.99% 14.98 16.96 10.29 15.56

Increased 6% to 7.99% 11.89 10.71 11.76 15.56

Increased 8% to 9.99% 7.49 7.14 5.88 8.89

Increased 10% or more 54.19 48.21 66.18 53.33

Responses 227 112 68 45

Q3. Over the past 6 months, how has the total volume of your sales changed?

(Percent of respondents)

Percent

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Declined 14.47 25.44 5.97 0.00

Stayed about the same 21.05 28.95 13.43 11.11

Increased by less than 5% 13.6 14.04 13.43 13.33

Increased 5% to 9.99% 15.35 13.16 19.4 13.33

Increased 10% to 14.99% 16.23 10.53 20.9 24.44

Increased 15% to 19.99% 5.70 2.63 2.99 17.78

Increased 20% to 29.99% 5.70 1.75 8.96 11.11

Increased 30% or more 7.89 3.51 14.93 8.89

Average* 6.90 2.72 10.90 12.78

Responses 228 114 67 45

*Calculated assuming the midpoint of each category and Winsorizing 15 percent of the responses at the top and bottom (26 percent

for respondents with under $10 million in gross revenue)

Q4. Approximately how much is your annual gross revenue

(Percent of respondents)

Percent

Total Annual Gross Revenue

Under $10

million

$10 million to Over $30

million $30 million

Under $10 million 50.22 100

$10 million to $29.99 million 29.96 100

$30 million to $59.99 million 9.69 48.89

$60 million to $89.99 million 4.85 24.44

$90 million or more 5.29 26.67

Responses 227 114 68 45

45

Appendix II:

Questionnaires

46

NAHB: HMI Survey Special Questions for May 2013

1. How would you describe the current availability of the following materials, as well as changes in their prices now

vs. 6 months ago?

Current Availability Changes in Prices Now vs. 6

months ago

No

shortage

Some

shortage

Serious

shortage

Do not

Purchase Increased Decreased

No

change

Cement

Ready-mix concrete

Concrete brick and block

Clay brick

Vinyl siding

Insulation material

Structural Insulated Panels (SIP)

Steel (Lightweight for framing)

Steel Beams

Trusses

Framing lumber

Gypsum wall board

Oriented Strand Board (OSB)

Plywood

Cabinets

Millwork

Windows and Doors

Hardwood flooring

Ceramic tiles

Roofing materials

Plumbing fixtures & fittings

HVAC equipment

Copper wiring

Other(Specify) ____________________

2. Overall, how have total material costs for the same house changed over the past 6 months?

Declined Increased 4 to 5.99%

Stayed about the same Increased 6 to 7.99%

Increased by less than 2% Increased 8 to 9.99%

Increased 2 to 3.99% Increased 10% or more

THANK YOU

47

Survey of National Lumber and Building Material Dealers

1. How would you describe the current availability of the following materials, as well as changes in their prices now

vs. 6 months ago?

Current Availability Changes in Prices Now vs. 6

months ago

No

shortage

Some

shortage

Serious

shortage

Do not

Purchase Increased Decreased

No

change

Cement

Ready-mix concrete

Concrete brick and block

Clay brick

Vinyl siding

Insulation material

Structural Insulated Panels (SIP)

Steel (Lightweight for framing)

Steel Beams

Trusses

Framing lumber

Gypsum wall board

Oriented Strand Board (OSB)

Plywood

Cabinets

Millwork

Windows and Doors

Hardwood flooring

Ceramic tiles

Roofing materials

Plumbing fixtures & fittings

HVAC equipment

Copper wiring

Other(Specify) ________________

2. On average across all product lines, how have prices for the materials you sell changed over the past 6 months?

Declined Increased 4 to 5.99%

Stayed about the same Increased 6 to 7.99%

Increased by less than 2% Increased 8 to 9.99%

Increased 2 to 3.99% Increased 10% or more

3. Over the past 6 months, how has the total volume of your sales changed?

Declined Increased 10 to 14.9%

Stayed about the same Increased 15 to 19.9%

Increased by less than 5% Increased 20 to 29.9%

Increased 5 to 9.9% Increased 30% or more

4. Approximately how much is your annual gross revenue?

Under $10 million $60 million to $89.9 million

$10 million to $29.9 million $90 million or more

$30 million to $59.0 million

THANK YOU!