Embed Size (px)

Citation preview

Bumrungrad Hospital Public Company Limited

The Presentation for Debenture Issuance

Financial Advisor

Joint Lead Underwriters

11 November 2011

• The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for any securities of Bumrungrad Hospital Public Company Limited (the "Company“ or “BH”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in connection with, any contract or commitment whatsoever.

• This presentation is being communicated only to persons who have professional experience in matters relating to investments and/or to persons to whom it is lawful to communicate it under the laws of applicable jurisdictions. Other persons should not rely or act upon this presentation or any of its contents.

• Certain information and statements made in this presentation contain the Company's forward-looking statements. All forward-looking statements are the Company's current expectation of future events and are subject to a number of factors that could cause actual results to differ materially from those described in the forward-looking statements. Prospective investors should take care with respect to such statements and should not place undue reliance on any such forward-looking statements.

• This presentation has been prepared by the Company solely for the use at this presentation. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the Company, any of its affiliates or any of their respective agents, advisors or representatives, shall have any liability (in negligence or otherwise) for any loss or damage howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. The information presented or contained in this presentation is current as of the date hereof and is subject to change without notice and its accuracy is not guaranteed. None of the Company, any of its affiliates or any of their respective agents, advisors or representatives, makes any undertaking to update any such information subsequent to the date hereof.

• This presentation should not be construed as legal, tax, investment or other advice. No part of this presentation shall be relied upon directly or indirectly for any investment decision-making or for any other purposes. Prospective investors should undertake their own assessment with regard to any investment and should obtain independent advice on any such investment’s suitability, inherent risks and merits and any tax, legal and accounting implications which it may have for them.

• Certain data in this presentation were obtained from various external data sources, and none of the Company, any of its affiliates or any of their respective agents, advisors or representatives have verified such data with independent sources. Accordingly, the Company makes no representation as to the accuracy or completeness of those data, and such data involve risks and uncertainties and are subject to change based on various factors.

Disclaimer

1

Table of Contents

2

1. Company Information / Q3 Update Financials

2. Key Investment Highlights / Debenture Issue / Potential Key Covenants

3. Key Timeline

Overview

Bumrungrad International Hospital, Bangkok

Agenda

3

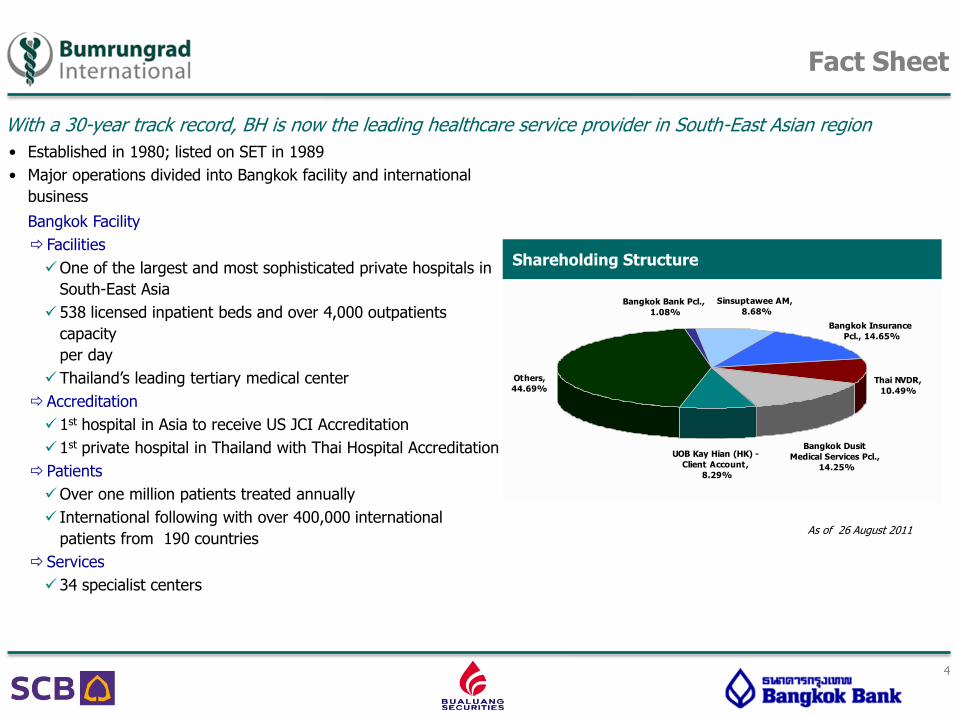

• Established in 1980; listed on SET in 1989

• Major operations divided into Bangkok facility and international

business

Bangkok Facility

Facilities

One of the largest and most sophisticated private hospitals in

South-East Asia

538 licensed inpatient beds and over 4,000 outpatients

capacity

per day

Thailand’s leading tertiary medical center

Accreditation

1st hospital in Asia to receive US JCI Accreditation

1st private hospital in Thailand with Thai Hospital Accreditation

Patients

Over one million patients treated annually

International following with over 400,000 international

patients from 190 countries

Services

34 specialist centers

With a 30-year track record, BH is now the leading healthcare service provider in South-East Asian region

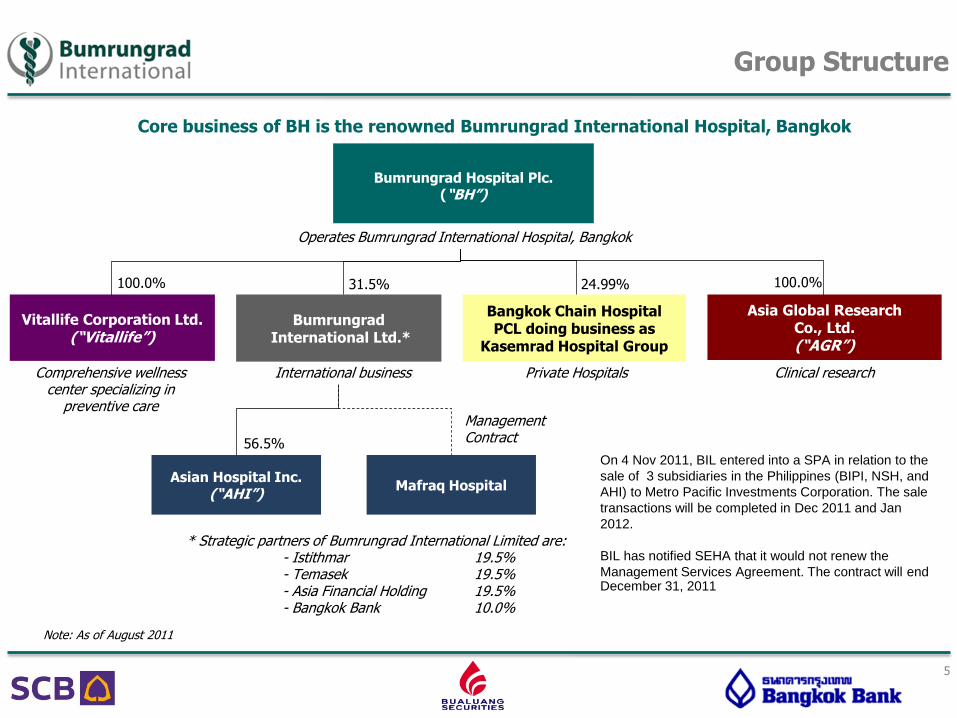

Shareholding Structure

Bangkok Insurance

Pcl., 14.65%

Sinsuptawee AM,

8.68%Bangkok Bank Pcl.,

1.08%

Thai NVDR,

10.49%

Bangkok Dusit

Medical Services Pcl.,

14.25%

UOB Kay Hian (HK) -

Client Account,

8.29%

Others,

44.69%

Fact Sheet

4

As of 26 August 2011

Note: As of August 2011

Private Hospitals Comprehensive wellness center specializing in

preventive care

Vitallife Corporation Ltd. (“Vitallife”)

100.0% 31.5%

Asian Hospital Inc. (“AHI”)

56.5%

* Strategic partners of Bumrungrad International Limited are: - Istithmar 19.5% - Temasek 19.5% - Asia Financial Holding 19.5% - Bangkok Bank 10.0%

Mafraq Hospital

Management Contract

International business

Bumrungrad International Ltd.*

100.0%

Asia Global Research Co., Ltd. (“AGR”)

Clinical research

Bumrungrad Hospital Plc. (“BH”)

Bangkok Chain Hospital PCL doing business as

Kasemrad Hospital Group

Operates Bumrungrad International Hospital, Bangkok

24.99%

Core business of BH is the renowned Bumrungrad International Hospital, Bangkok

Group Structure

5

On 4 Nov 2011, BIL entered into a SPA in relation to the

sale of 3 subsidiaries in the Philippines (BIPI, NSH, and

AHI) to Metro Pacific Investments Corporation. The sale

transactions will be completed in Dec 2011 and Jan

2012.

BIL has notified SEHA that it would not renew the

Management Services Agreement. The contract will end December 31, 2011

BH’s management team comprises individuals with extensive experience in healthcare management

K. Linda Lisahapanya Managing Director

Mr. Dennis Brown CEO

Bumrungrad International Ltd.

Mr. Mack Banner CEO

Bumrungrad International, Bangkok

Mr. Anthony Tan CEO

Vitallife Corporation Ltd.

Dr. Suthipong Treeratana CEO

Asia Global Research Co., Ltd.

Dr. Sinn Anuras Group Medical Director

Mr. Dennis Brown Corporate CEO

Management Team

6

Overview

Bumrungrad International Hospital, Bangkok

Agenda

7

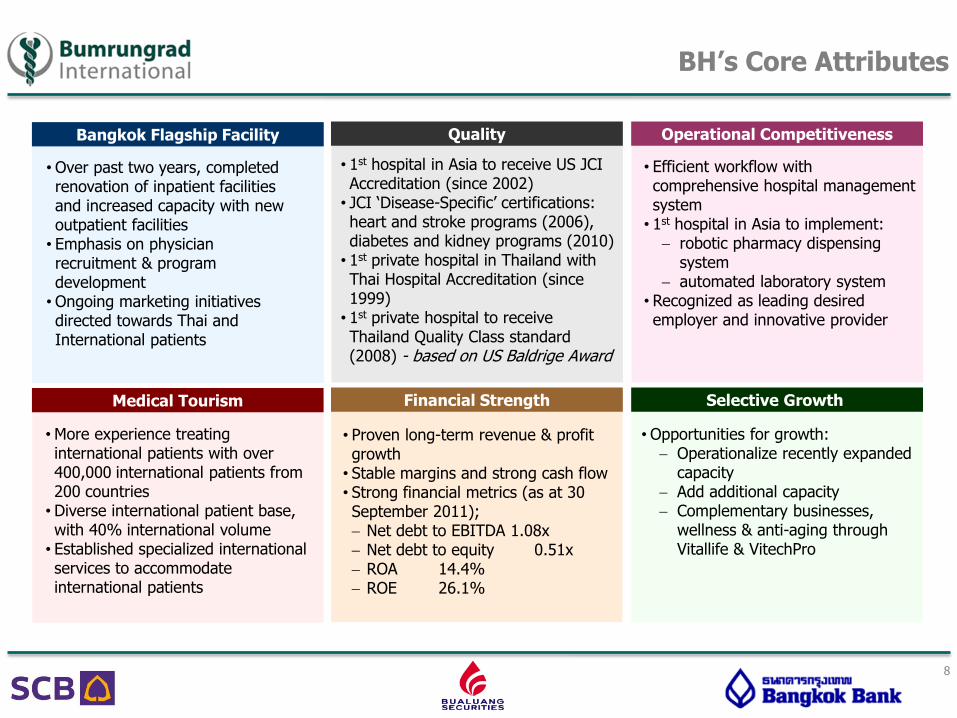

Bangkok Flagship Facility

Medical Tourism

Quality

Financial Strength

Operational Competitiveness

Selective Growth

• 1st hospital in Asia to receive US JCI Accreditation (since 2002)

• JCI ‘Disease-Specific’ certifications: heart and stroke programs (2006), diabetes and kidney programs (2010)

• 1st private hospital in Thailand with Thai Hospital Accreditation (since 1999)

• 1st private hospital to receive Thailand Quality Class standard (2008) - based on US Baldrige Award

• Efficient workflow with comprehensive hospital management system

• 1st hospital in Asia to implement: robotic pharmacy dispensing

system automated laboratory system

• Recognized as leading desired employer and innovative provider

•More experience treating international patients with over 400,000 international patients from 200 countries

• Diverse international patient base, with 40% international volume

• Established specialized international services to accommodate international patients

• Proven long-term revenue & profit growth

• Stable margins and strong cash flow • Strong financial metrics (as at 30 September 2011); Net debt to EBITDA 1.08x Net debt to equity 0.51x ROA 14.4% ROE 26.1%

•Opportunities for growth: Operationalize recently expanded

capacity Add additional capacity Complementary businesses,

wellness & anti-aging through Vitallife & VitechPro

•Over past two years, completed renovation of inpatient facilities and increased capacity with new outpatient facilities

• Emphasis on physician recruitment & program development

•Ongoing marketing initiatives directed towards Thai and International patients

BH’s Core Attributes

8

Ce

rtif

ica

tio

ns a

nd

Aw

ard

s

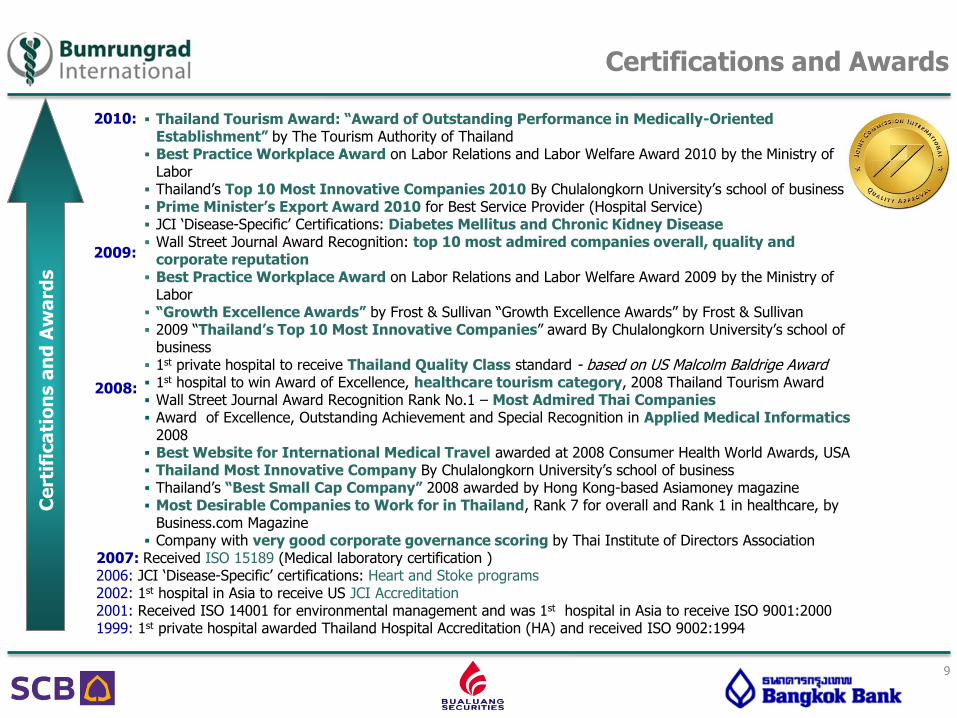

Thailand Tourism Award: “Award of Outstanding Performance in Medically-Oriented Establishment” by The Tourism Authority of Thailand

Best Practice Workplace Award on Labor Relations and Labor Welfare Award 2010 by the Ministry of Labor

Thailand’s Top 10 Most Innovative Companies 2010 By Chulalongkorn University’s school of business Prime Minister’s Export Award 2010 for Best Service Provider (Hospital Service) JCI ‘Disease-Specific’ Certifications: Diabetes Mellitus and Chronic Kidney Disease Wall Street Journal Award Recognition: top 10 most admired companies overall, quality and

corporate reputation Best Practice Workplace Award on Labor Relations and Labor Welfare Award 2009 by the Ministry of

Labor “Growth Excellence Awards” by Frost & Sullivan “Growth Excellence Awards” by Frost & Sullivan 2009 “Thailand’s Top 10 Most Innovative Companies” award By Chulalongkorn University’s school of

business 1st private hospital to receive Thailand Quality Class standard - based on US Malcolm Baldrige Award 1st hospital to win Award of Excellence, healthcare tourism category, 2008 Thailand Tourism Award Wall Street Journal Award Recognition Rank No.1 – Most Admired Thai Companies Award of Excellence, Outstanding Achievement and Special Recognition in Applied Medical Informatics

2008 Best Website for International Medical Travel awarded at 2008 Consumer Health World Awards, USA Thailand Most Innovative Company By Chulalongkorn University’s school of business Thailand’s “Best Small Cap Company” 2008 awarded by Hong Kong-based Asiamoney magazine Most Desirable Companies to Work for in Thailand, Rank 7 for overall and Rank 1 in healthcare, by

Business.com Magazine Company with very good corporate governance scoring by Thai Institute of Directors Association

2007: Received ISO 15189 (Medical laboratory certification ) 2006: JCI ‘Disease-Specific’ certifications: Heart and Stoke programs 2002: 1st hospital in Asia to receive US JCI Accreditation 2001: Received ISO 14001 for environmental management and was 1st hospital in Asia to receive ISO 9001:2000 1999: 1st private hospital awarded Thailand Hospital Accreditation (HA) and received ISO 9002:1994

2008:

2009:

2010:

Certifications and Awards

9

Inpatient experience offers hotel-like ambience and room design Priority on patient safety Less “clinical” feeling Warm and restful environment

World Class Inpatient Facilities Renovation of all rooms completed in May 2010

10

Ground Floor Lobby

Sky Lobby

Clinic area design enhances privacy, in a pleasant and calming environment, with efficient workflows

Welcome Center New Clinics

Expanded Outpatient Facilities New OPD Tower with similar high quality ambience opened in June 2008

11

• Focus on physician recruitment and targeted specialties

• Domestic marketing efforts include advertisements, fairs, and packages

• International marketing through multiple channels

• Proven growth with increasing penetration in referral markets

• Selectively pursuing overseas expansion – Bumrungrad International Limited

• Extend success in wellness, anti-aging and other complementary business lines

Strategy

12

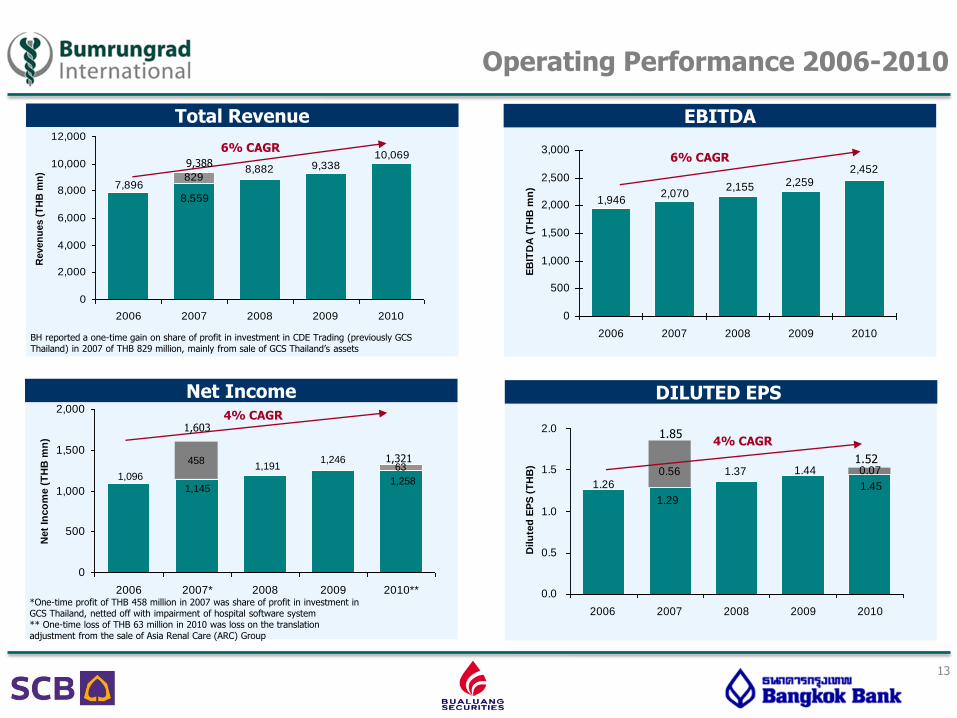

Total Revenue

Net Income

EBITDA

1,9462,070

2,155 2,2592,452

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008 2009 2010

EB

ITD

A (

TH

B m

n)

6% CAGR

8297,896

8,559

8,882 9,33810,069

0

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010

Reven

ues (

TH

B m

n)

6% CAGR

458

1,145

1,0961,191

1,246

1,258

63

0

500

1,000

1,500

2,000

2006 2007* 2008 2009 2010**

Net

Inco

me (

TH

B m

n)

4% CAGR

DILUTED EPS

1.26

1.29

1.37 1.44

1.45

0.56 0.07

0.0

0.5

1.0

1.5

2.0

2006 2007 2008 2009 2010

Dilu

ted

EP

S (

TH

B)

4% CAGR

*One-time profit of THB 458 million in 2007 was share of profit in investment in GCS Thailand, netted off with impairment of hospital software system ** One-time loss of THB 63 million in 2010 was loss on the translation adjustment from the sale of Asia Renal Care (ARC) Group

9,388

BH reported a one-time gain on share of profit in investment in CDE Trading (previously GCS Thailand) in 2007 of THB 829 million, mainly from sale of GCS Thailand’s assets

1,603 1.85

1.52 1,321

Operating Performance 2006-2010

13

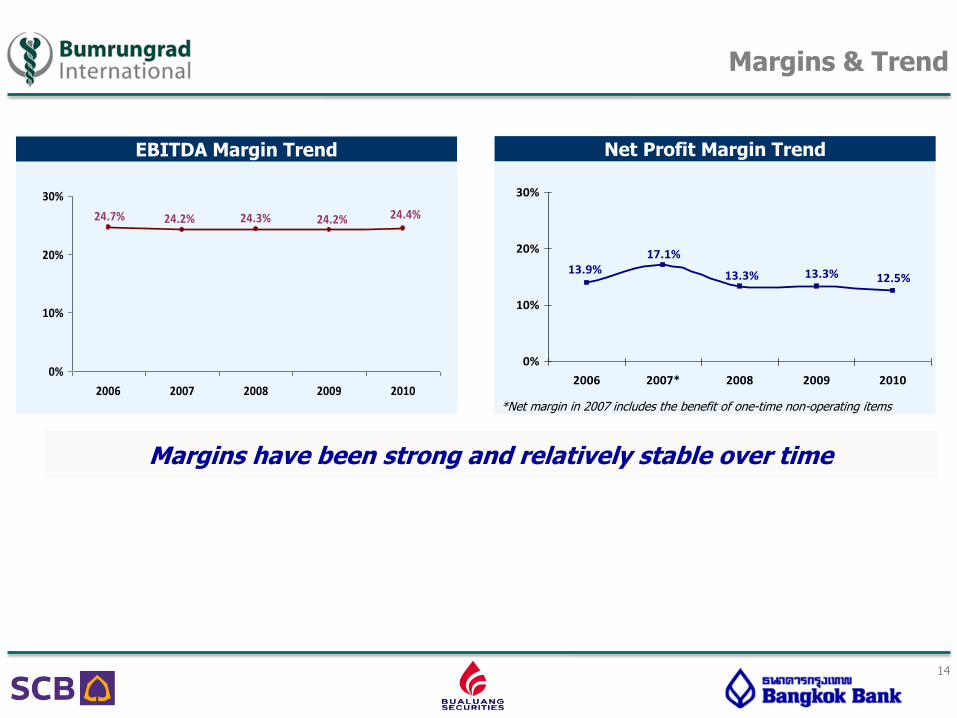

Margins have been strong and relatively stable over time

Net Profit Margin Trend

13.3% 12.5%13.3%

17.1%13.9%

0%

10%

20%

30%

2006 2007* 2008 2009 2010

*Net margin in 2007 includes the benefit of one-time non-operating items

EBITDA Margin Trend

24.2%24.7% 24.3% 24.2% 24.4%

0%

10%

20%

30%

2006 2007 2008 2009 2010

Margins & Trend

14

2,2751,818

24.2%26.1%

0

1,000

2,000

3,000

4,000

YTD Sep'10 YTD Sep'11

0%

10%

20%

30%

40%

EBITDA

EBITDA Margin

Total Revenue

7,521

8,730

7,000

7,500

8,000

8,500

9,000

YTD Sep'10 YTD Sep'11

EBITDA

Net Income

THB million THB million

THB million

63

50977

1,264

12.2%13.8%

14.4%13.0%

0

200

400

600

800

1,000

1,200

1,400

YTD Sep'10 YTD Sep'11

5%

10%

15%

20%

25%

Net Profit excl extra itemsNet Profit Net Profit Margin excl extra itemsNet Profit Margin

Higher growth of net profit compared to growth of total revenues was driven by a lower rate of increase in cost of hospital operations and administrative expenses.

16%

29%

25.2%

33% 1,214

914

9M11 Update

15

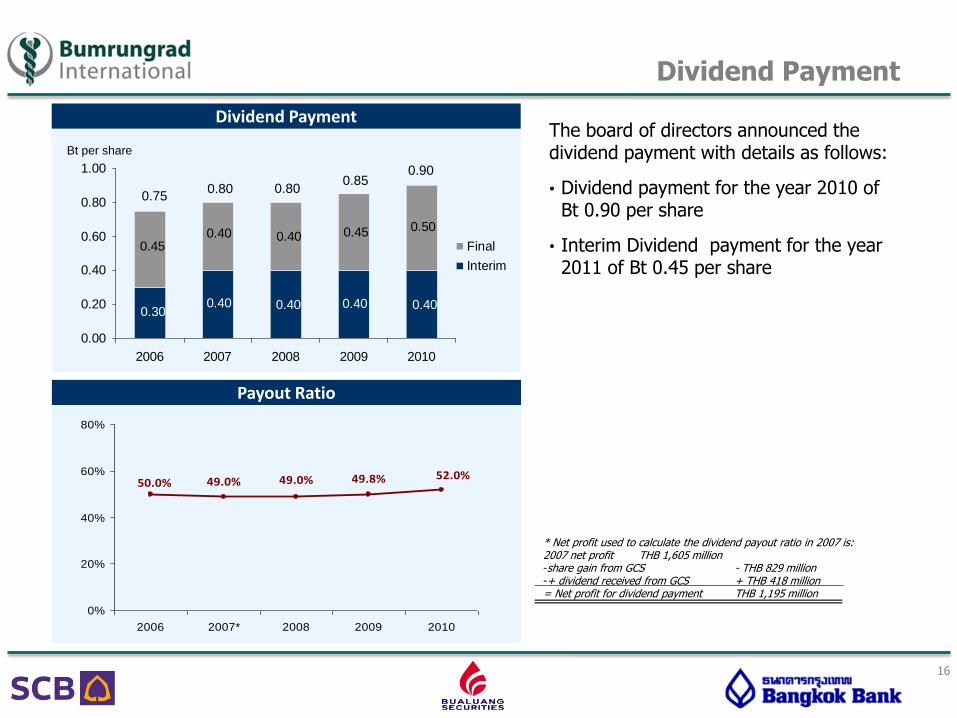

Dividend Payment

Dividend Payment

0.400.400.400.400.30

0.450.40 0.40 0.45 0.50

0.00

0.20

0.40

0.60

0.80

1.00

2006 2007 2008 2009 2010

Final

Interim

Bt per share

Payout Ratio

49.0%50.0% 49.0% 49.8% 52.0%

0%

20%

40%

60%

80%

2006 2007* 2008 2009 2010

The board of directors announced the dividend payment with details as follows:

• Dividend payment for the year 2010 of Bt 0.90 per share

• Interim Dividend payment for the year 2011 of Bt 0.45 per share

0.75 0.80

0.85 0.80

* Net profit used to calculate the dividend payout ratio in 2007 is: 2007 net profit THB 1,605 million -share gain from GCS - THB 829 million -+ dividend received from GCS + THB 418 million = Net profit for dividend payment THB 1,195 million

0.90

16

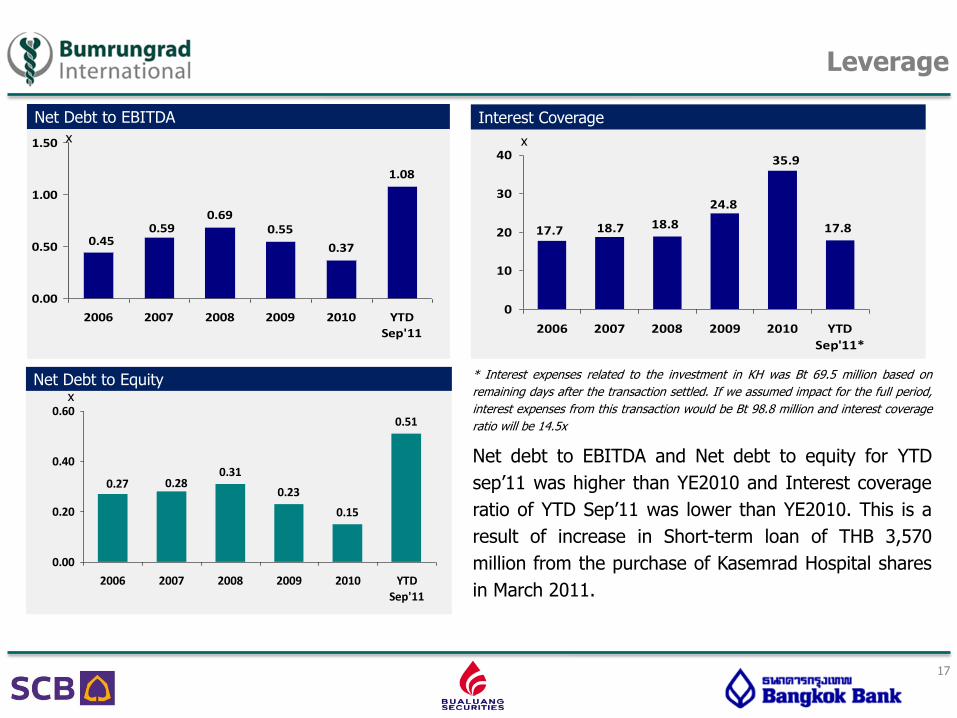

x Interest Coverage

18.8 17.8

35.9

24.8

17.7 18.7

0

10

20

30

40

2006 2007 2008 2009 2010 YTD

Sep'11*

x

0.690.55

0.37

1.08

0.590.45

0.00

0.50

1.00

1.50

2006 2007 2008 2009 2010 YTDSep'11

Net Debt to EBITDA

x

Net Debt to Equity x

0.31

0.23

0.15

0.51

0.27 0.28

0.00

0.20

0.40

0.60

2006 2007 2008 2009 2010 YTDSep'11

* Interest expenses related to the investment in KH was Bt 69.5 million based on

remaining days after the transaction settled. If we assumed impact for the full period,

interest expenses from this transaction would be Bt 98.8 million and interest coverage

ratio will be 14.5x

Net debt to EBITDA and Net debt to equity for YTD

sep’11 was higher than YE2010 and Interest coverage

ratio of YTD Sep’11 was lower than YE2010. This is a

result of increase in Short-term loan of THB 3,570

million from the purchase of Kasemrad Hospital shares

in March 2011.

Leverage

17

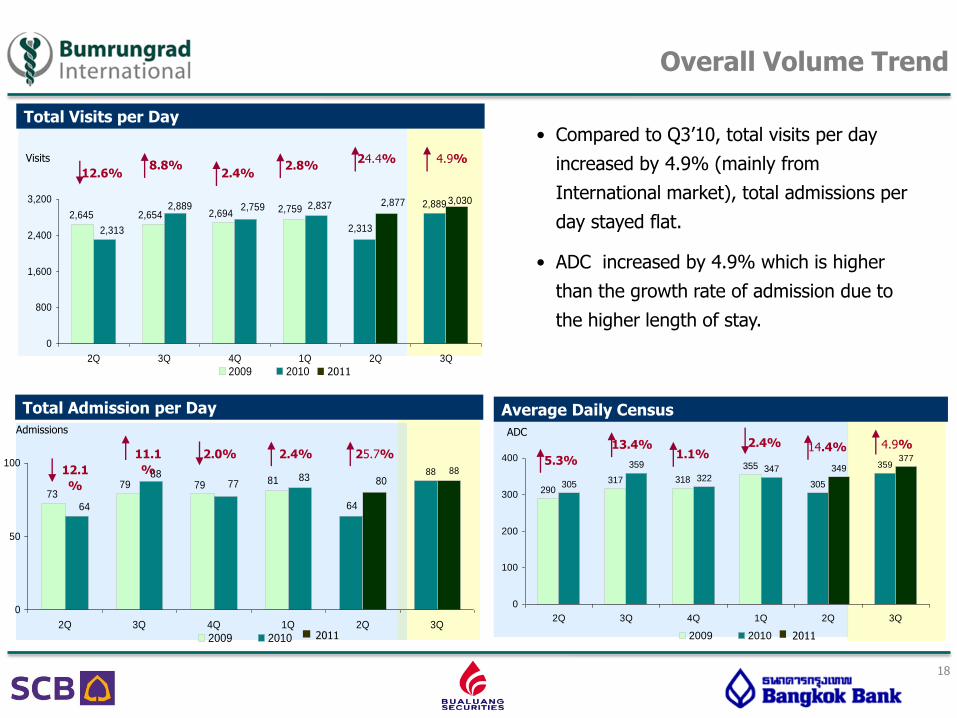

Overall Volume Trend

• Compared to Q3’10, total visits per day

increased by 4.9% (mainly from

International market), total admissions per

day stayed flat.

• ADC increased by 4.9% which is higher

than the growth rate of admission due to

the higher length of stay.

Total Visits per Day

Visits

12.6% 8.8%

2.4%

2,889

2,313

2,7592,6942,6542,645

3,0302,8772,8372,7592,889

2,313

0

800

1,600

2,400

3,200

2Q 3Q 4Q 1Q 2Q 3Q

2009 2010 2011

4.9%

7379 79 81

64

88

64

8877

83 8088

0

50

100

2Q 3Q 4Q 1Q 2Q 3Q

2009 2010 2011

12.1

%

11.1

%

2.0% 2.4%

Average Daily Census

ADC

290317 318

355

305

359

305

359

322347 349

377

0

100

200

300

400

2Q 3Q 4Q 1Q 2Q 3Q

2009 2010

5.3%

13.4% 1.1%

Admissions

4.9%

2011

Total Admission per Day

2.8%

2.4%

24.4%

25.7% 14.4%

18

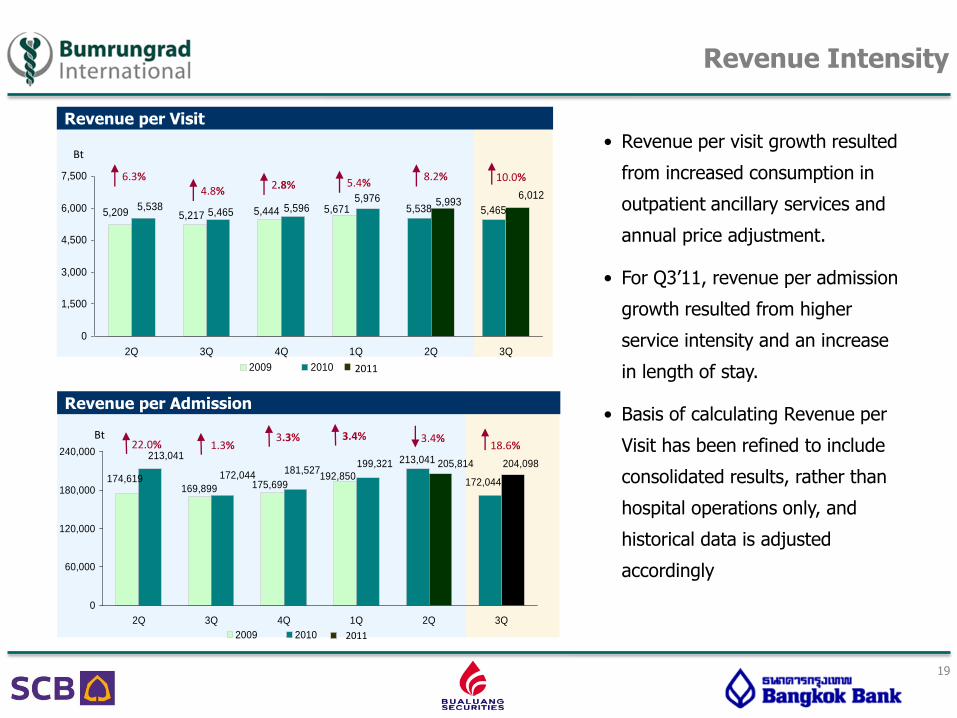

• Revenue per visit growth resulted

from increased consumption in

outpatient ancillary services and

annual price adjustment.

• For Q3’11, revenue per admission

growth resulted from higher

service intensity and an increase

in length of stay.

• Basis of calculating Revenue per

Visit has been refined to include

consolidated results, rather than

hospital operations only, and

historical data is adjusted

accordingly

Revenue Intensity

Revenue per Admission

Revenue per Visit

6.3%

Bt

Bt

4.8% 2.8% 5.4%

22.0% 1.3%

10.0%

3.3%

2011

174,619169,899 175,699

192,850

213,041

172,044

213,041

172,044181,527

199,321 205,814 204,098

0

60,000

120,000

180,000

240,000

2Q 3Q 4Q 1Q 2Q 3Q

2009 2010 2011

3.4%

8.2%

3.4%

5,209 5,217 5,444 5,671 5,538 5,4655,5385,465 5,596

5,976 5,9936,012

0

1,500

3,000

4,500

6,000

7,500

2Q 3Q 4Q 1Q 2Q 3Q

2009 2010

18.6%

19

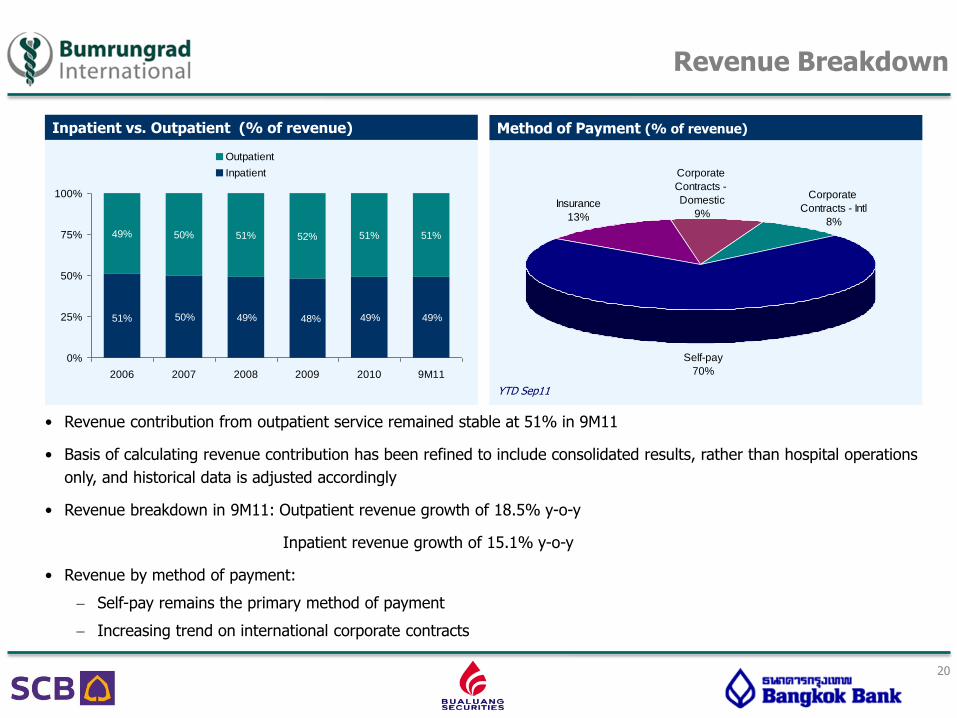

Revenue Breakdown

Inpatient vs. Outpatient (% of revenue) Method of Payment (% of revenue)

YTD Sep11

• Revenue contribution from outpatient service remained stable at 51% in 9M11

• Basis of calculating revenue contribution has been refined to include consolidated results, rather than hospital operations

only, and historical data is adjusted accordingly

• Revenue breakdown in 9M11: Outpatient revenue growth of 18.5% y-o-y

Inpatient revenue growth of 15.1% y-o-y

• Revenue by method of payment:

Self-pay remains the primary method of payment

Increasing trend on international corporate contracts

Insurance

13%

Corporate

Contracts - Intl

8%

Corporate

Contracts -

Domestic

9%

Self-pay

70%

49% 50% 51% 52% 51% 51%

49%51% 50% 49% 48% 49%

0%

25%

50%

75%

100%

2006 2007 2008 2009 2010 9M11

Outpatient

Inpatient

20

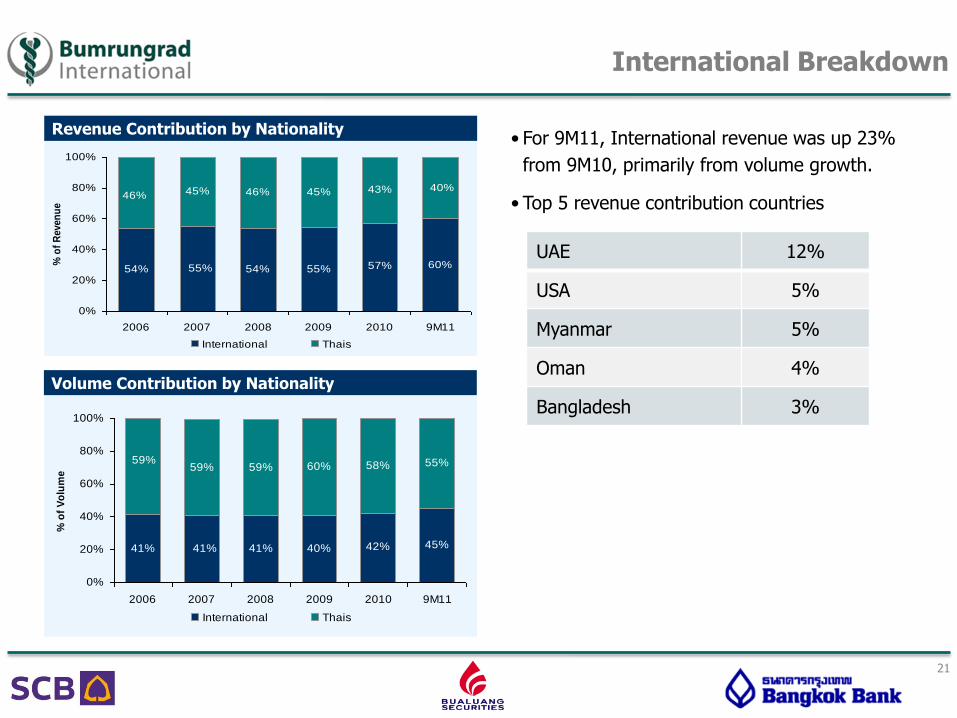

International Breakdown

21

Volume Contribution by Nationality

Revenue Contribution by Nationality

54% 54% 55%

45% 46% 45%

60%57%55%

43% 40%46%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 9M11

% o

f R

even

ue

International Thais

41% 41% 40%

59% 59% 60%

45%41% 42%

58% 55%59%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 9M11

% o

f V

olu

me

International Thais

• For 9M11, International revenue was up 23%

from 9M10, primarily from volume growth.

• Top 5 revenue contribution countries

UAE 12%

USA 5%

Myanmar 5%

Oman 4%

Bangladesh 3%

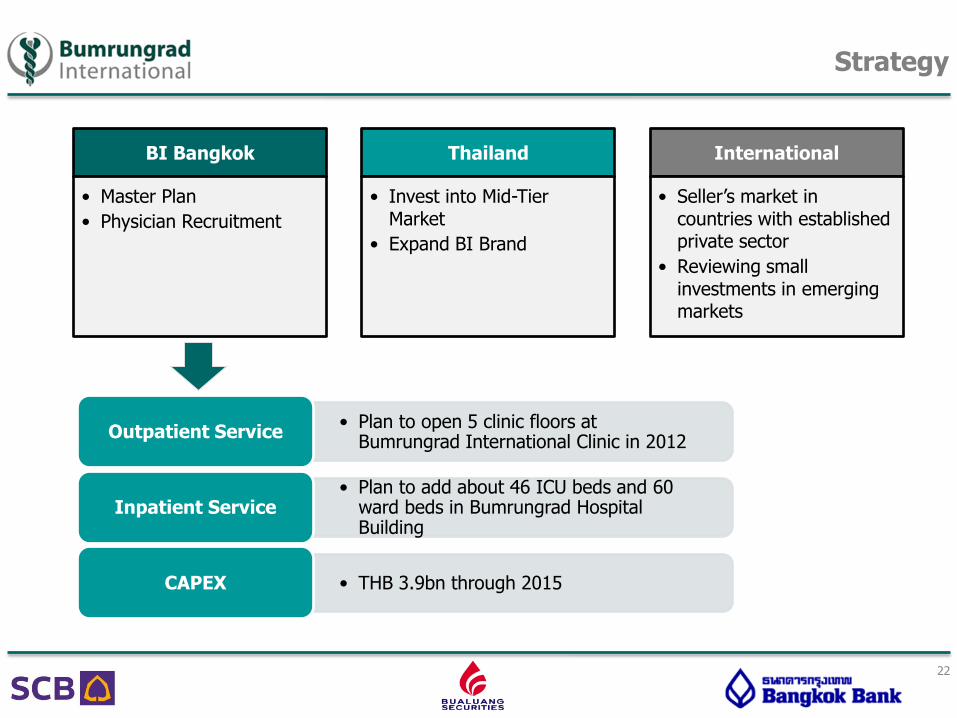

Strategy

BI Bangkok

• Master Plan

• Physician Recruitment

Thailand

• Invest into Mid-Tier Market

• Expand BI Brand

International

• Seller’s market in countries with established private sector

• Reviewing small investments in emerging markets

• Plan to open 5 clinic floors at Bumrungrad International Clinic in 2012

Outpatient Service

• Plan to add about 46 ICU beds and 60 ward beds in Bumrungrad Hospital Building

Inpatient Service

• THB 3.9bn through 2015 CAPEX

22

Master Plan CAPEX

Million THB Y11* Y12* Y13 Y14 Y15 Total

Est. Capital Investment

794 924

1,273 888

49 3,928

Capital Type Est. Capital Costs (THB mm)

Land 625

New Building Construction 1,186

Construction 1,306

Special Medical Equipment 248

General Medical Equipment 396

General Equipment 57

IT Equipment 90

Vitallife Expansion 20

Total Costs 3,928

Note: * CAPEX for years 2011 and 2012 have been approved by the Board. The remaining year will require approval in each subsequent years budget submission.

23

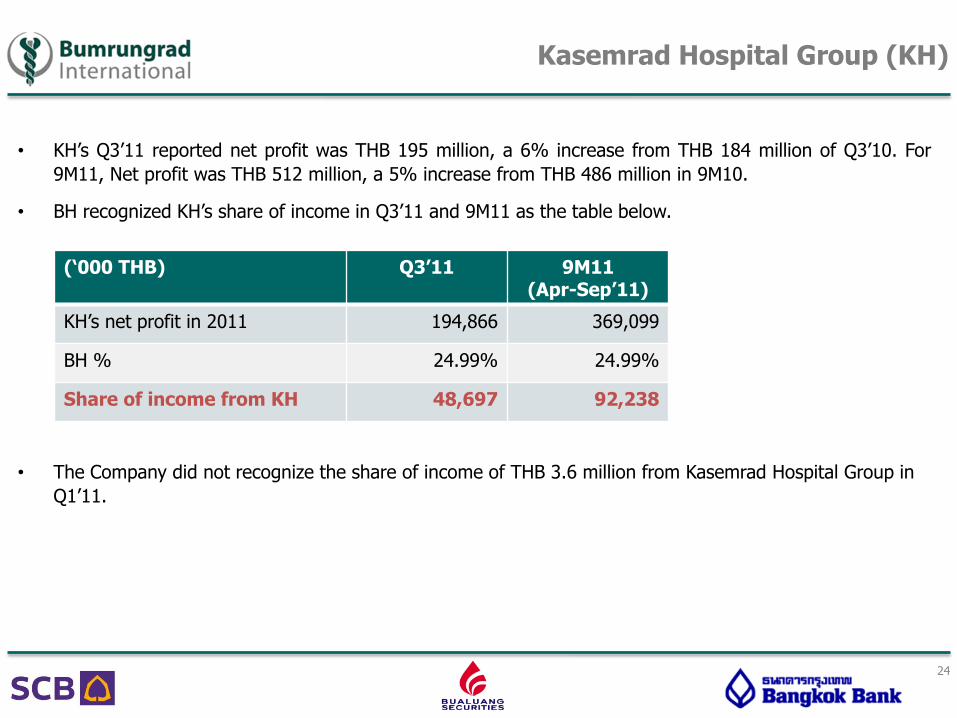

• KH’s Q3’11 reported net profit was THB 195 million, a 6% increase from THB 184 million of Q3’10. For

9M11, Net profit was THB 512 million, a 5% increase from THB 486 million in 9M10.

• BH recognized KH’s share of income in Q3’11 and 9M11 as the table below.

• The Company did not recognize the share of income of THB 3.6 million from Kasemrad Hospital Group in

Q1’11.

(‘000 THB) Q3’11 9M11 (Apr-Sep’11)

KH’s net profit in 2011 194,866 369,099

BH % 24.99% 24.99%

Share of income from KH 48,697 92,238

Kasemrad Hospital Group (KH)

24

Table of Contents

25

1. Company Information / Q3 Update Financials

2. Key Investment Highlights / Debenture Issue / Potential Key Covenants

3. Key Timeline

Key Investment Highlights

Leading position and strong brand recognition among both domestic and international hospitals

Experienced management team

Solid medical profile in attracting competent medical team

Strong financial profile

26

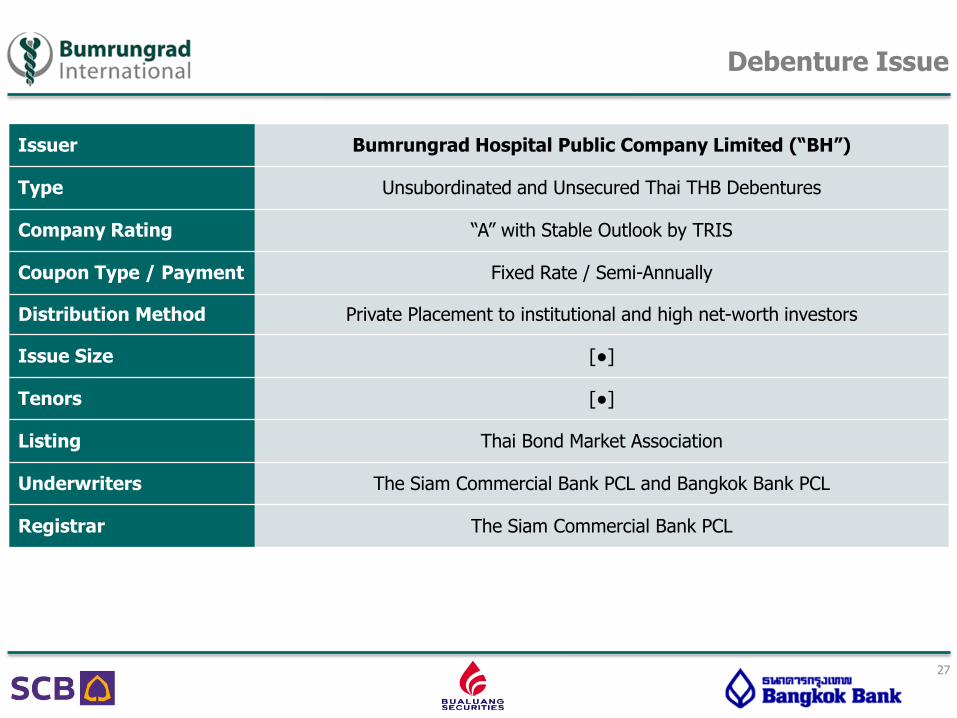

Debenture Issue

27

Issuer Bumrungrad Hospital Public Company Limited (“BH”)

Type Unsubordinated and Unsecured Thai THB Debentures

Company Rating “A” with Stable Outlook by TRIS

Coupon Type / Payment Fixed Rate / Semi-Annually

Distribution Method Private Placement to institutional and high net-worth investors

Issue Size [●]

Tenors [●]

Listing Thai Bond Market Association

Underwriters The Siam Commercial Bank PCL and Bangkok Bank PCL

Registrar The Siam Commercial Bank PCL

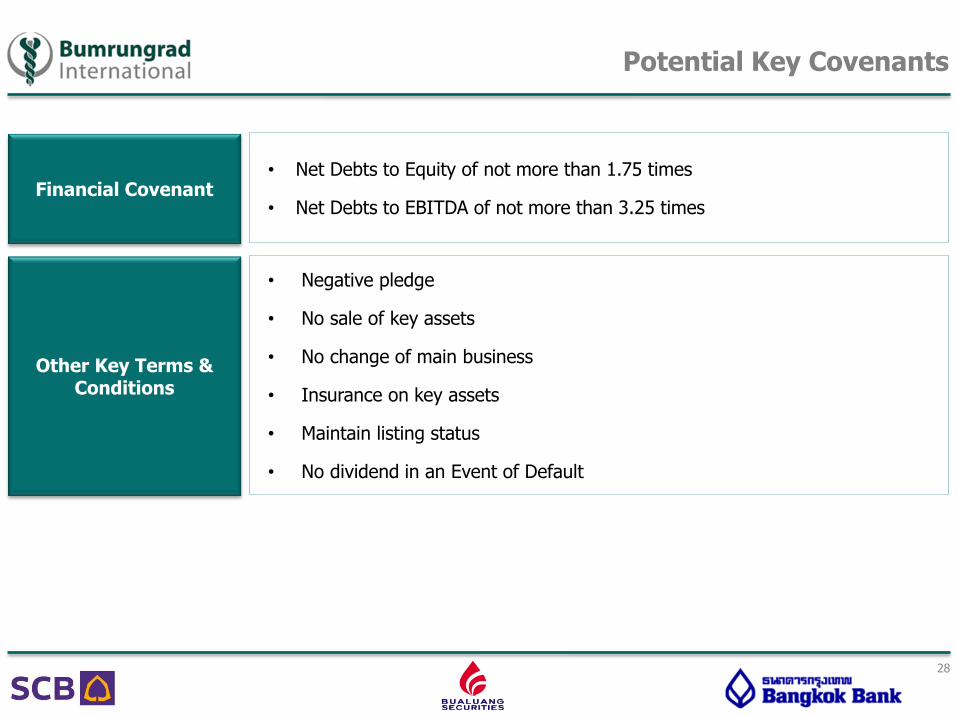

Potential Key Covenants

28

• Net Debts to Equity of not more than 1.75 times

• Net Debts to EBITDA of not more than 3.25 times Financial Covenant

• Negative pledge

• No sale of key assets

• No change of main business

• Insurance on key assets

• Maintain listing status

• No dividend in an Event of Default

Other Key Terms & Conditions

Table of Contents

29

1. Company Information / Q3 Update Financials

2. Key Investment Highlights / Debenture Issue / Potential Key Covenants

3. Key Timeline

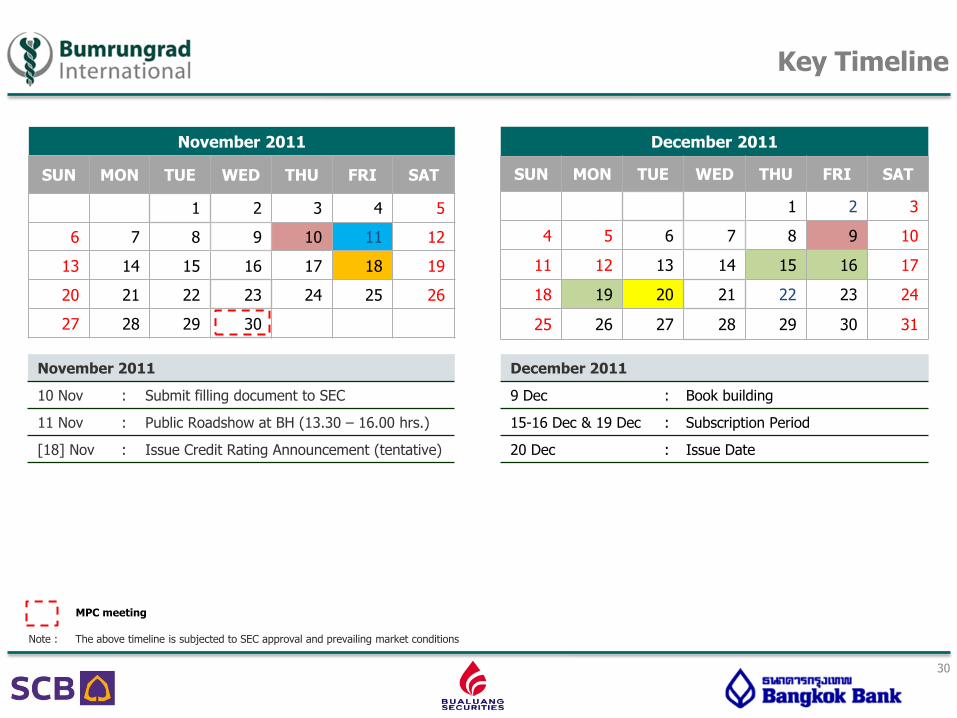

Key Timeline

30

November 2011

SUN MON TUE WED THU FRI SAT

1 2 3 4 5

6 7 8 9 10 11 12

13 14 15 16 17 18 19

20 21 22 23 24 25 26

27 28 29 30

December 2011

SUN MON TUE WED THU FRI SAT

1 2 3

4 5 6 7 8 9 10

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 27 28 29 30 31

Note : The above timeline is subjected to SEC approval and prevailing market conditions

MPC meeting

November 2011

10 Nov : Submit filling document to SEC

11 Nov : Public Roadshow at BH (13.30 – 16.00 hrs.)

[18] Nov : Issue Credit Rating Announcement (tentative)

December 2011

9 Dec : Book building

15-16 Dec & 19 Dec : Subscription Period

20 Dec : Issue Date