Embed Size (px)

Citation preview

Bureau of Economic Geology, The University of Texas at Austin

The elusive optimal fiscal regime for an extra- heavy oil resource: a case study

©CEE, Bureau of Economic Geology, UT Austin, 2

Outline

• Background• Evolution of fiscal regime• Uncertainty• Final comment

©CEE, Bureau of Economic Geology, UT Austin, 3

The Faja• The Faja is one of the largest oil deposits in the

Western Hemisphere and is now economically viable, over 70 years after its discovery.

• Hydrocarbon ranges from 5 to 12 API and 125m to 1600m of depth.

• Why did production finally take off?

©CEE, Bureau of Economic Geology, UT Austin, 4

Development of Unconventional Resources

• Geostatistical and production uncertainty– Where should wells be located?– How much will wells cost to build?– How will they perform?– For how long?– How much oil? Gas? Water? Sand?

• And let us not forget– For how much will the oil be sold?

• Historically blended with lighter crude oil.

©CEE, Bureau of Economic Geology, UT Austin, 5

Impact of Fiscal Regime

• 1976– Royalty Relief: No– Long run royalty: 16.67%– Taxes: 66.7%– Private participation: No

• 1990’s– Royalty Relief: 1% – Long run royalty: 16.67%– Taxes: 34%– Private participation: 50%

• Price Level– $8-$20 per barrel

©CEE, Bureau of Economic Geology, UT Austin, 6

HEAVY OIL PRODUCTION

200600

1200

2000

3000

0

500

1000

1500

2000

2500

3000

3500

1980 1985 1990 1995 2000

Initi

al P

rodu

ctio

n <B

PD

>

VERTICAL WELLS. IGP, OHGP BASAL

SANDS

BETTER SUCKER-ROD

PUMPS

HORIZONTAL WELLS 1500’,

ESP AND DILUENT

INJECTION

HORIZONTAL WELLS 4000 - 5000’, HIGH

CAPACITY ESP AND PCP

MULTIPHASE PUMPS

MULTILATERAL WELLS

$5000/BPDi

$1666/BPDi

$400/BPDi

©CEE, Bureau of Economic Geology, UT Austin, 8

Original Production Plan of the Faja

092 108 129 129 129 129 129 129

0

79105

105 105 116 116 116 116 116

0

0

130150 154 159 186 186 186 186

0

0

08

170 170170 180 208 208

129

169

317

461507

622 639671 681

711 711

0

100

200

300

400

500

600

700

800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Synt

hetic

Cru

de <

KB

PD>

AmerivenSincorOCNPetrozuataCrude Oil

639

©CEE, Bureau of Economic Geology, UT Austin, 9

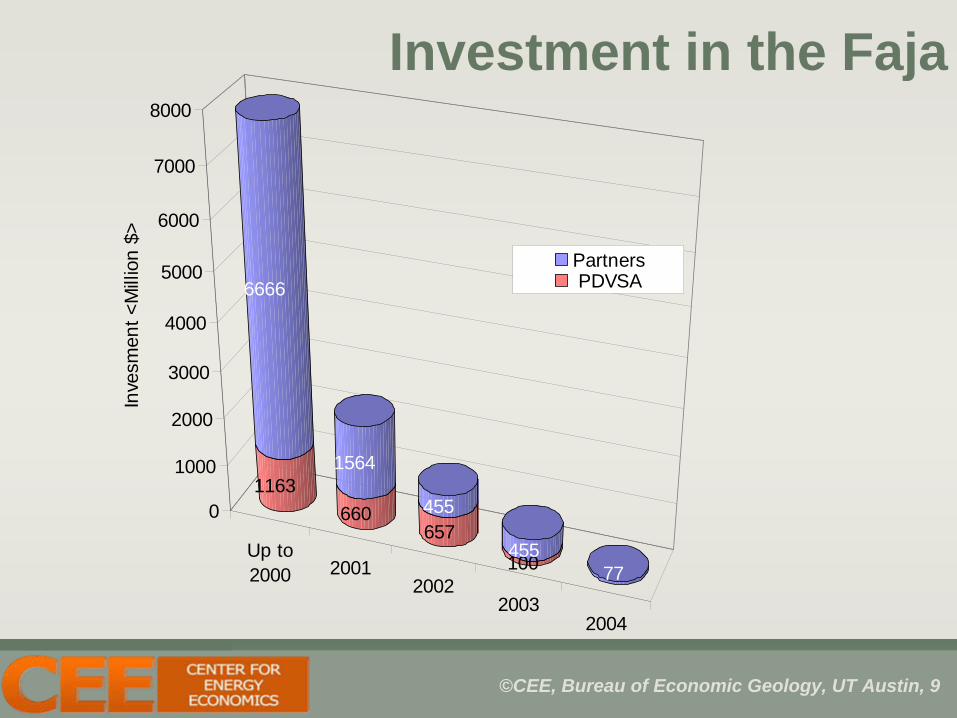

Investment in the Faja

Up to2000 2001

20022003

2004

1163

6666

660

1564

657455

100455

77

0

1000

2000

3000

4000

5000

6000

7000

8000In

vesm

ent <

Mill

ion

$>

Partners PDVSA

©CEE, Bureau of Economic Geology, UT Austin, 10

HORIZONTAL WELLS

Courtesy of Petrozuata

©CEE, Bureau of Economic Geology, UT Austin, 11

LATERAL FISHBONES

Courtesy of Petrozuata

©CEE, Bureau of Economic Geology, UT Austin, 12

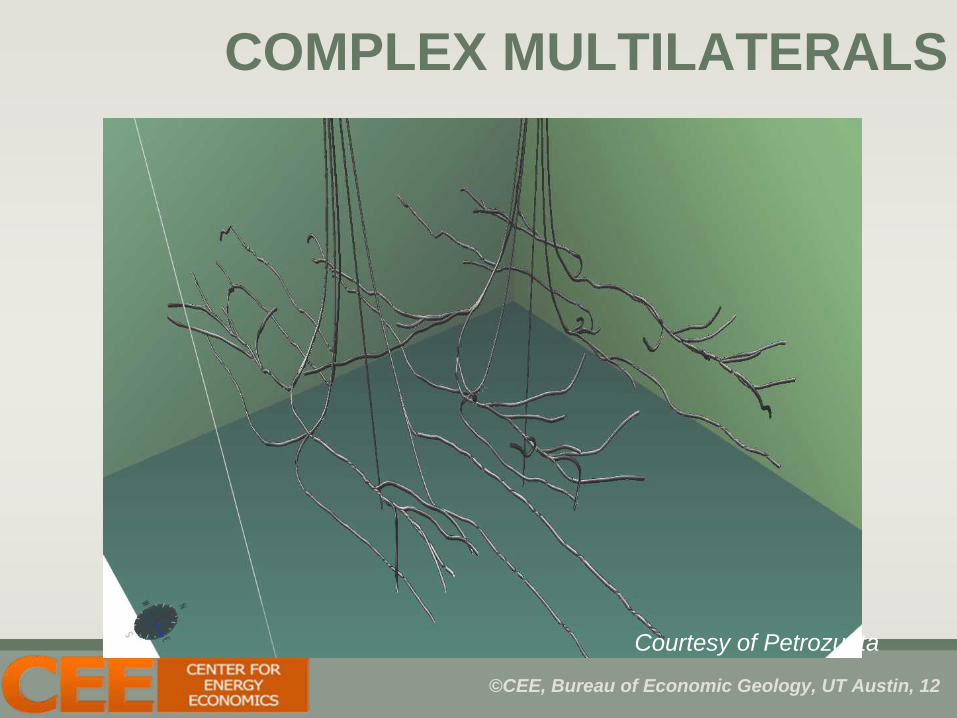

COMPLEX MULTILATERALS

Courtesy of Petrozuata

©CEE, Bureau of Economic Geology, UT Austin, 13

WELLS OF PETROZUATA

Courtesy of Petrozuata

©CEE, Bureau of Economic Geology, UT Austin, 15

Tax – Royalty with depreciation schedule

• In the simple case– Company pays royalty– Company pays taxes on

profits after considering depreciation

Revenue

Royalty

Costs

Cash Flow=(Revenue – Royalty – OPEX – Dep.) * ( 1 - tax) + Dep.

TaxableDepre.

TaxTax

Net Profit

©CEE, Bureau of Economic Geology, UT Austin, 18

Expected Project Value 1998

P50 $815.12

©CEE, Bureau of Economic Geology, UT Austin, 19

Expected Project Value 1998

©CEE, Bureau of Economic Geology, UT Austin, 20

Expected Project Value 2006 (1998 $)

P50 $7,786.79

Considers price evolution between 1998 and 2006.

©CEE, Bureau of Economic Geology, UT Austin, 21

Expected Project Value 2006 (1998 $)

©CEE, Bureau of Economic Geology, UT Austin, 22

Expected Value in 1998 vs 2006

©CEE, Bureau of Economic Geology, UT Austin, 26

How was the value distributed?

• 1990’s– Royalty Relief: 1% – Long run royalty: 16.67%– Taxes: 34%– Private participation: 50%

©CEE, Bureau of Economic Geology, UT Austin, 27

How was the value distributed?

©CEE, Bureau of Economic Geology, UT Austin, 28

In 2006 Temptation wins!

• 1990’s– Royalty Relief: 1% – Long run royalty: 16.67%– Taxes: 34%– Private participation: 50%

• Price Level– $8 - $12 per barrel

• 2006– Royalty Relief: None– Royalty: 33%– Taxes: 50%– Private participation: 50%

• Price Level– $50-60 per barrel

©CEE, Bureau of Economic Geology, UT Austin, 29

How much value would a company lose?

©CEE, Bureau of Economic Geology, UT Austin, 30

And what happens if prices go down?

©CEE, Bureau of Economic Geology, UT Austin, 31

What is the status today?

• Incumbents did not add investments during transition of fiscal regime and some have been removed

• Add on investments still seem attractive– Lessons learned are in jeopardy of being lost– New operators versus Associations

• New projects will need market for Syncrude– Brasil will likely be the likely market for next project

©CEE, Bureau of Economic Geology, UT Austin, 32

Final Comments and Open Questions

• The value of the Faja is mostly untapped and will likely not be tapped in the short term. And Alberta?

• Should royalty change once uncertainty is resolved? Low initial royalty and then one that captures extra rents? Wouldn’t a corporate tax do the same?