Embed Size (px)

Citation preview

Syndicate 1 - Umboniswa

Business Case

Can Microfinance be deliverable in a Sustainable Manner from a South African Perspective ?

Team Members: Bobby Madhav

Sipho Silinda

Brigitte Ryder

Zilindile Makapela

id27888703 pdfMachine by Broadgun Software - a great PDF writer! - a great PDF creator! - http://www.pdfmachine.com http://www.broadgun.com

CONSUMER EDUCATION AND ENTERPRISE DEVELOPMENT IN THE SME MARKET PAGE 1

Table of Contents

Introduction����.�����������������������3

1. Background ������������������������.4

1.1 What is microfinance? ����������������������4

1.2 How does microfinance help the poor? ���������������4

1.2.1 Brief background and size of the segment ����������������..4

1.2.2 Demand for microfinance services �������������������...5

2. Methodology �����������������������...6

3. What is the current landscape? ����������������6

3.1 Formal Financial Sector Perspective ����������������6

3.2 Public Sector Perspective ��������������������..8

3.2.1 The Establishment of Khula Enterprise ������������������8

3.2.2 Umsobomvu Fund ��������������������������..9

3.2.3 Mafisa �������������������������������..9

3.3 Regulation ��������������������������...9

3.3.1 Cooperatives Bill and Community Banks �����������������9

3.3.2 Financial Services and Empowerment ���������������� ��9

3.3.3 National Credit Act ������������������������ ��.9

3.4 Public Private Partnerships and Non-government organisation ��� �..9

3.4.1 Urban Foundation ������������������������� �10

3.5 Informal Sector ���������������������� � 10

3.5.1 Stokvels ������������������������������.10

3.5.2 Mashonisa and Pyramid Schemes �������������������.11

4. Global Best Practice ��������������������12

4.1 India �����������������������������12

4.1.1 Credit Delivery Models ������������������������.12

4.1.2 Regulation and Legal forms ����������������������13

4.1.3 Financing Models ��������������������������.13

4.1.4 Growth Strategies ��������������������������.13

4.2 UK Perspective ������������������������.14

4.3 Grameen Bank � Bangladesh������������������.14

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 2

4.4 Bolivia ����������������������������15

5. Business Case Study �������������������..17

5.1 Purpose ���������������������������.17

5.2 Reasons ���������������������������17

5.3 Options ���������������������������..17

5.4 Benefits Expected �����������������������17

5.5 Pricing and Risk ������������������������17

5.6 Cost �����������������������������18

5.7 Characteristics of Model ��������������������..19

5.7.1 Value Proposition ��������������������������.19

5.7.2 Network ������������������������������.19

5.7.3 Solution Offerings and Pricing ���������������������.19

5.7.4 Pre-Finance Education and Aftercare Support/Mentoring ���������...19

6. Conclusion and recommendation ����������..����21

7. Appendices ������������������..�����22

8. Table of references �����������������.��...25

8.1 Books, Articles and Presentations ��...����������..��..25

8.2 Websites ������������������������..��25

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 3

Introduction

Can Microfinance be deliverable in a Sustainable Manner from a South African Perspective ? To date microfinance has earned incredible interest from multilateral lending agencies, bilateral donor agencies, governments of developing and developed countries and nongovernmental organisations all in support for the development of microfinance. The fundamental question to be raised and addressed within the South African context is: Is microfinance viable from a South African banking perspective? And subsequent to that, can microfinance be delivered in a sustainable manner from a South African perspective? About 95 percent of some 16.4 million poor households and unbanked South African citizens have little or no access to institutional financial services, yet according to Paul Hanratty: Managing Director Old Mutual, a Stokvel fund triple to record R33 billion in the past decade and is classified as �grey money� (Business Report, Wednesday, August 29 2007)1 . Grey money consists of funds held by savings clubs, such as stokvels, that circulate outside of the formal financial system. Paul Hanratty indicated that �grey money� was part of the non-traditional savings now fast approaching the R1 trillion mark. In South Africa, government as the policy maker and formal financial institutions recognize that providing efficient microfinance services for this segment of population is important for the following reasons:

Poverty eradication and employment creation strategy thereby enhancing AsgiSA initiatives; Microfinance is an enabler for the poor and low-income earners to actively participate in and benefit

from the development opportunities which the country is realizing towards and beyond 2010; and Microfinance is the key to empowerment of micro enterprise and poor women (providing working

capital) who make up a significant proportion of the poor and suffer disproportionately from poverty especially in the rural areas, to access procurement within medium and large companies as required by the Financial Sector Charter;

In the Asian developing countries, microfinance services have been used to reduce poverty. About 21 percent of the Grameen Bank borrowers and 11 percent of the borrowers of the Bangladesh Rural Advancement Committee, microfinance NGO, managed to lift their families out of poverty within about four years of participation2. Therefore if done correctly and cooperatively within coherence principles, microfinance will change the socioeconomic variables and economic participation from excluded majority into the mainstream of our economy to the benefit of all, the challenge in South Africa is to establish a workable microfinance model. This microfinance model must take into account the dynamic diverse demographic within South Africa rural and metro areas; financial historical background within South Africa and the level of exposure of financial knowledge of this segment as well as its current potential.

1 Hanratty, P. 2007. Wednesday, August 29. Stokvel Funds: Business Report, Business Day 2 Khander, S.R. 1998. Fighting Poverty with Microfinance: Experience in Bangladesh. New York: Oxford University Press

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 4

Section

1 Background

1.1.What is microfinance?

To most, microfinance means providing very poor families with very small loans (micro-credit) to assist them to engage in productive activities or grow their tiny businesses. Microfinance is quickly becoming a popular corner of the capital markets as more investment banks and wealthy philanthropists such as George Soros and eBay co-founder Pierre Omidyar see the business of providing small loans to low-income individuals in poor countries as potentially profitable as well as a powerful tool for development 3. According to Asian Development Bank (ADB: 2000), microfinance is defined as the provision of a broad range of financial services such as deposits, loans, payment services, money transfer, and insurance to poor and low-income households and their micro-enterprise.4 It is critical to note that micro finance services are provided by three types of sources, namely:

Formal institutions, such as rural banks and cooperatives; Semiformal institutions, such as non-government organisations (NGO�s); and Informal sources such as money lenders and shopkeepers.

These three types of sources are common especially in African countries. It is encouraging as stated above that in other countries investment banks are starting to have an interest in this segment, though in South Africa that has not emerged as yet.

1.2.How does microfinance help the poor ?

Eric Thurman suggests that microfinance or micro credit is not a panacea that can solve every problem in the world but, he argues, �it is a proven intervention that works well in many ways significantly outperforms most �top down� antipoverty efforts�5. The concern globally is that currently micro credit is only available to 5 to 10 percent of the people who could benefit from it. In addressing the question, �how does microfinance help the poor?� it is appropriate to give a brief background of the segment and analyse demand for microfinance services, then indicate how microfinance helps the poor.

1.2.1. Brief background and size of the segment

The typical microfinance clients are low-income persons that do not have access to formal financial institutions. Microfinance clients are typically self-employed, often household-based entrepreneurs6. Over 16.4 million people in South Africa live in poverty, most live in rural areas. Most rural poor people are engaged in agricultural activities some as labourers or small scale farmers and variety of microenterprises with little or no access to conventional financial services. In 2005 up to 60 percent of the population were excluded from formal financial services7. Most formal financial institutions do not serve this segment as it is perceived to be high risk, inability to provide collateral and costly to service it as little profits are realized.

3 The Financial Times. 2007. July 30. Microfinance: Boon or bane 4 Asian Development Bank (ADB). 2000. Rural Asia Study: Beyond the Green Revolution. Manila: ADB 5 Thurman, E and Smith, P. 2007. A Billion Bootstraps: Microcredit Barefoot Banking, and the Business Solution for Ending Poverty. New York. McGraw-Hill 6 Reichman, R. and Restrepo, C.E. 1995. Balancing the double day: Women as managers of microenterprises. Somerville, MA, USA. Accion International. 7 Meagher, P. 2005. Microfinance Regulation and Supervision in South Africa.

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 5

1.2.2. Demand for microfinance services

When properly harnessed, microfinance offers a variety of benefits to poor people. Foremost, microfinance initiatives can effectively address material poverty, the physical deprivation of goods and services, and the income to attain them. When properly guided, the material benefits of micro financing can extend beyond the household into community8. At the personal level, microfinance can effectively address issues associated with non-material poverty, which includes social and psychological effects that prevent people from realizing their potential. Poor and low-income households and micro enterprises have a large demand for safe and convenient deposit services. Reason for that is, the poor need to save for emergencies such as death in the family, payments to hospitals; investment; consumption; social obligations; and education of their children. These savings are therefore critical for funding micro enterprises, providing working capital and loans etc. Detail segmented demands are described see (Appendix 1). Analysing the demand for microfinance services, it is then evident that microfinance can help the poor by advancing micro credit , provide micro savings and micro insurance to them. Microfinance, the Grameen way, includes several support systems that contribute greatly to its success. Institutions such as Khula Indemnity Credit Guarantee and Ntsika can help micro enterprises by credit guarantees , business advice and counselling, while clients also provide peer support for each other through solidarity circles. For example, if a client falls ill, her circle helps with her business until she is well. If a client gets discouraged, the support group pulls her through. This contributes substantially to the extremely high repayment rate of loans made to microfinance entrepreneurs9. Microfinance has a positive impact far beyond the individual client. As families cross the poverty line and micro enterprises expand, their communities benefit. Jobs are created, knowledge is shared, civic participation increases, and women are recognized as valuable members of their families and communities.

8 Microfinance in Africa 9 Grameen

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 6

Section

2 Methodology

The methodology followed in researching the business case comprised:

Data and Statistical analysis; Case analysis; Informal discussions held with various financial institutions and Internet research.

Section

3 What is the current landscape ?

3.1.Formal Financial Sector Perspective

Commercial banks traditionally do not serve low-income earners, micro-entrepreneurs and the poor (collectively referred to as the unbanked), chiefly because the high costs involved make it unattractive. The big four of South African banking, between them have a market share in excess of 70 percent. And it is only since the early 1997 that they have given serious thought to entering this market segment, in no small way influenced by the changes in the local political landscape. As a result, access to basic banking services to poorer people is one of the pillars of the proposed Financial Services Charter implementation. The reality is that the Usury Act has a cap on the amount of interest commercial banks can charge on their loans. This was due to a ceiling placed on lending rates by the Usury Act of 1968 to protect borrowers from excessive charges. The transaction cost per rand lent was just too high to make such business profitable. Banks have formerly entered the market but not on the lower end. The market being serviced is loans from R1000-00 and above. This is done in most instances only providing loans to the low-income formally employed. This means if an individual does not have a payslip or security such loans will not be granted. In view of this the so-called 'formal' micro-lending industry (those belonging to the Micro Lending Association of South Africa) outside of the banking sector have mushroomed in a very short span of time. It is important for us to understand the previous experiences of commercial banks in Micro finance and what led to them moving to more profitable lending.

Standard Bank created E Bank (now E Plan) in 1993 to provide basic banking services to the low-income urban population. It, however, only entered the micro-lending market in 1999. Rather than going it alone, it followed a cautious approach by entering into a joint venture with African Investment Bank Limited (Abil), in terms of which Abil's loan products were sold to Standard Bank's E Plan customers through Standard Bank's branch network. The loan book grew to R256 million (Standard Bank Group, 2002:21). Subsequent to this ABIL had terminated its contract with Standard bank and are now one of the Leaders in Microfinance. Nedbank ventured into the low-income market via its Peoples Bank division in 1995, the latter later becoming Nedbank's empowerment subsidiary with its own banking licence. It had a client base of 2 million, primarily low- and middle-income individuals (Nedcor, 2002:45). The focus was originally not on the

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 7

lending side, but two alliances Nedbank had entered into was to position it strategically in the micro-lending market. The alliance with Capital One of the US entered into in 1999, gave Nedbank access to Capital One's expertise in information-based penetration into lower-end lending markets. The first branch of Absa's NuBank division, aiming to serve those that were traditionally regarded as unbankable, was opened in February 1996. In contrast to Peoples Bank and E Plan, NuBank immediately provided both unsecured personal micro-loans and micro-entrepreneur loans. In April 2000, Absa acquired a 51 per cent stake (later increased to 61 per cent) in one of the then market leaders in micro-lending, UniFer, and incorporated NuBank into it. Absa immediately gained a significant share in the micro-lending market and at the same time illustrated its commitment to the development of this market.

Referring to the banks' entrance, the industry suffered a serious setback in 2002.10 It is ironic that the crisis was largely confined to two of the major bank micro-lenders, UniFer of Absa and Saambou, who, in a very competitive environment, indiscriminately expanded their lending books from 2000 onwards. The background to their actions was the government's decision to halt from the second half of 2000 new micro-loans to public servants linked to its payroll deduction system. This had caused a great setback for the commercial banks as most of these loans were paid up vis debit of payroll deductions. In 2001 all agreements were terminated.

For microlenders with a large exposure to public servants, the government's decision was potentially disastrous. UniFer a divison Of ABSA suffered severely from unpaid loans. In March 2002, the shortfall in UniFer's provisions for bad debts was R1,8 billion on a loan book of R4,9 billion and its net asset value R1,3 billion in the red. Other banks in the industry realised the risks involved in making use of brokers and purposefully avoided this route. FNB and Peoples Bank rather used their branch networks, while Abil terminated all its agreements with brokers in March 2000 The other major bank micro-lender who experienced serious problems with its micro-lending business, Saambou, was ultimately put under curatorship in February 2000. Its assets were put up for sale and Abil bought its R2,8 billion micro-loan book. The industry has apparently weathered the storm but this had led to many �Loan sharks� setting up shop and charging ridiculous fees and unscrupulous practices emerged. Hence the MRFC had taken an active role to regulate the industry to build confidence in the industry and the poor.

The big four banks themselves to show their commitment to serving this market, although not at the lower end, decided to attend to the demand for entrepreneurial loans of between R10 000 and R50 000 (since increased to R100 000) In recent years all Commercial Banks have adopted the Financial Services Charter which prescribes to the Bank�s of their commitment in financing the lower end of the chain. The Banks have made great strides in this area. However it still remains to be seen if any bank has exceeded its target. The reality is that if it makes no business sense then there is reluctance to fast forward some of the initiatives. Majority of banks have applied the minimum delivery in terms of the FSC targets. Banks have rather adopted the letter of the Charter and are mainly concentrating on the SMME markets. These companies in most instances will have formal businesses and are in some way running or setting up businesses.

10 MicroFinance Regulatroty council, 2001:4

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 8

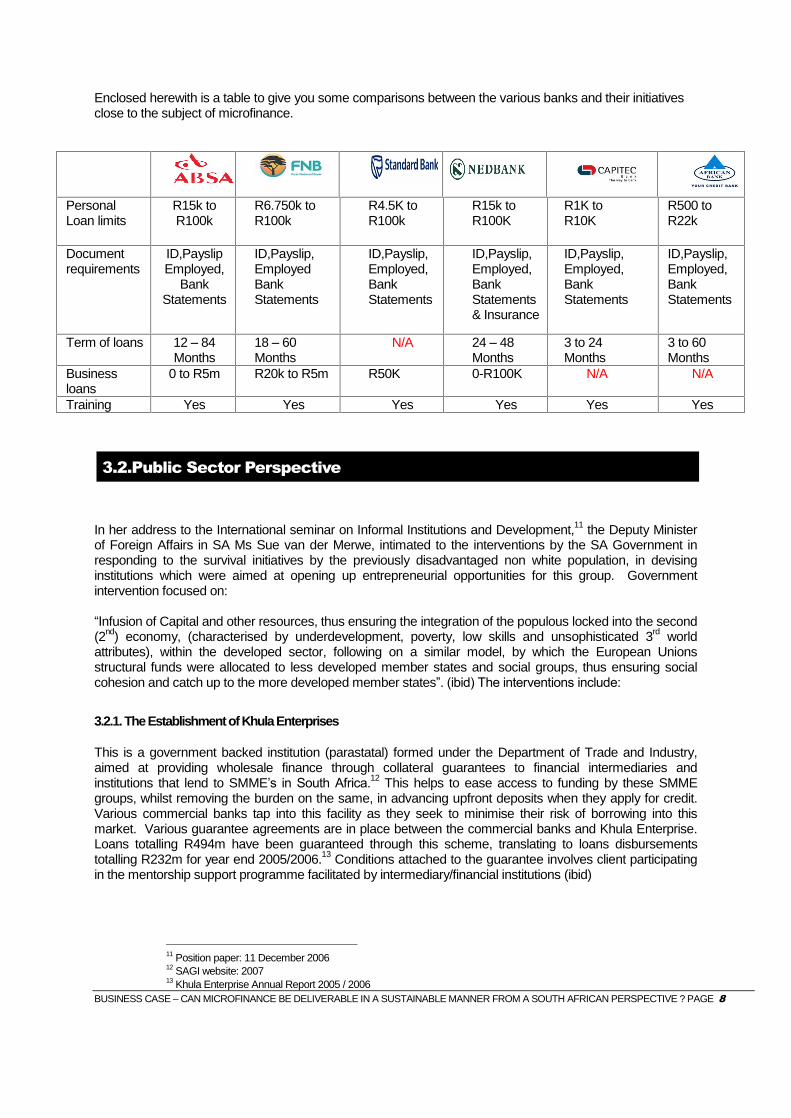

Enclosed herewith is a table to give you some comparisons between the various banks and their initiatives close to the subject of microfinance.

Personal Loan limits

R15k to R100k

R6.750k to R100k

R4.5K to R100k

R15k to R100K

R1K to R10K

R500 to R22k

Document requirements

ID,Payslip Employed,

Bank Statements

ID,Payslip, Employed Bank Statements

ID,Payslip, Employed,Bank Statements

ID,Payslip, Employed,Bank Statements & Insurance

ID,Payslip, Employed,Bank Statements

ID,Payslip, Employed, Bank Statements

Term of loans 12 � 84 Months

18 � 60 Months

N/A 24 � 48 Months

3 to 24 Months

3 to 60 Months

Business loans

0 to R5m R20k to R5m R50K 0-R100K N/A N/A

Training Yes Yes Yes Yes Yes Yes

3.2.Public Sector Perspective

In her address to the International seminar on Informal Institutions and Development,11 the Deputy Minister of Foreign Affairs in SA Ms Sue van der Merwe, intimated to the interventions by the SA Government in responding to the survival initiatives by the previously disadvantaged non white population, in devising institutions which were aimed at opening up entrepreneurial opportunities for this group. Government intervention focused on: �Infusion of Capital and other resources, thus ensuring the integration of the populous locked into the second (2nd) economy, (characterised by underdevelopment, poverty, low skills and unsophisticated 3rd world attributes), within the developed sector, following on a similar model, by which the European Unions structural funds were allocated to less developed member states and social groups, thus ensuring social cohesion and catch up to the more developed member states�. (ibid) The interventions include:

3.2.1. The Establishment of Khula Enterprises

This is a government backed institution (parastatal) formed under the Department of Trade and Industry, aimed at providing wholesale finance through collateral guarantees to financial intermediaries and institutions that lend to SMME�s in South Africa.12 This helps to ease access to funding by these SMME groups, whilst removing the burden on the same, in advancing upfront deposits when they apply for credit. Various commercial banks tap into this facility as they seek to minimise their risk of borrowing into this market. Various guarantee agreements are in place between the commercial banks and Khula Enterprise. Loans totalling R494m have been guaranteed through this scheme, translating to loans disbursements totalling R232m for year end 2005/2006.13 Conditions attached to the guarantee involves client participating in the mentorship support programme facilitated by intermediary/financial institutions (ibid)

11 Position paper: 11 December 2006 12 SAGI website: 2007 13 Khula Enterprise Annual Report 2005 / 2006

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 9

3.2.2. Umsobomvu Fund

Youth fund distributed through Business partners for SMME businesses, with active participation in business operation by business partners and supportive mentorship support. They provide funds ranging from micro, small and up to medium business loans, sometimes accessible through a voucher scheme programme. (ibid) The focus of this intervention is targeted towards the unemployed youth, both the young graduates and the not so highly educated youth, who may have viable business propositions. The approval process and criteria focuses more on sound business plan and sustainability of the venture proposed. 3.2.3. Mafisa

This is an intervention by the Department of Agriculture, aimed at supporting the emerging and developing farmers who have not built a credit worthiness to qualify for the loans with commercial banks 14. These loans are distributed through Land and Agricultural bank at below market interest rates, for amounts ranging from R500 to R100k, with minimal credit requirements. By June 2007, according to the programme director Mr Dlulani for Mafisa in the Department of Agriculture and land Affairs, R323m has been disbursed to developing farmers in the pilot areas.

3.3.Regulation

In the same conference on informal institutions and development, Deputy Minister Sue van der Merwe, highlighted key areas of Regulation which the Government has introduced. She highlights: 3.3.1. Cooperatives Bill and Community Banks

Work done to bring the informal institutions in various sectors, into a regulative regime (Position paper, 2006). Initiatives in this space include the Co-operatives bill which has recently been open for public hearings by the portfolio committee of parliament. This is the instrument that will pave the way for a legislative foundation for the establishment of community/village banks, which will operate along the lines of a co-operative institutional model.

3.3.2. Financial Services and Empowerment

Has been formulated with input from the financial sector, encouraging the formal commercial sector to introduce products which are within reach of the previously unbankable markets. In this space, already progress is showing, especially in the area of basic savings accounts, a joint initiative by the four (4) major banks in South Africa, called Mzansi Account. Over 100 000 accounts were opened for the previously unbanked market, within the first month of roll out in 2004. The regulations outcome targeted by the charter and the accompanying code of ethic, seek to compel the financial sector in addition, to address matters of Employment Equity, management control, Ownership control skill development and procurement process that favour the previously disadvantaged groups.15

3.3.3 National Credit Act

The introduction of this piece of legislation towards the end of the first half of 2007, has been an attempt by Government to steer the financial institutions towards exercising responsible lending to the individual or personal consumer borrowers on loans less than R1m. It seeks to limit and eradicate the application of undue soliciting of lending, by stipulating conditions under which financial institutions should lend in this segment of the market, especially towards low income (micro finance target market) component of this segment. Mr Covadia, the chairman of the Banking Council of South Africa, attests to the immediate slow down in credit extension observed since the act, during the month of June, in his opening remarks during the South African Institute of Bankers� Awards (Nedbank July 2007)

14 Minister of Agriculture Budget Speech, 2005 15 SA Banking Council, Web site 2007 / Patric Meagher Micro finance Regulations and super Vision SA . 5 April 2008

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 10

3.4.Public Private Partnership and Non-governmental Organisation Co-Operatives

Kate Philip in his paper on Co-operatives in South Africa: Their role in job creation and Poverty Reduction (October 2003), highlights some of the few co-operative initiatives that evolved with a specific mission to support their members with micro finance, through initiatives of churches in the Western Cape (Co-op forum), that rolled out a Grahamstown �Bus station�, NGO�s like COPE, SHADE, the Wilgerspruit fellowship centre, ACAT etc. Trade unions on the other hand were supporting Co-ops initiatives as a strategy to deal with dismissal in their industries. These included 3 SAMCOL Workers� Co-ops in Howick, linked to NUMSA, the Zenzeleni Co-op owned by SACTWU and NUM�s network of 30 producer Co-ops in South Africa. (ibid) 3.4.1. Urban Foundation

According to the Urban foundation information bulletin, the body plays its direct role in housing projects (8 January 1980). Formed in December 1976, bringing a wide variety of businessman from a range of political views, this body (which included Afrikaners, English and Blacks) sought to fundraise from the business sector. (Especially those companies listed in the Johannesburg Sock Exchange � JSE) requesting a fraction of their after tax profit (2%) or percentage of their turnover (0.04%).16These funds were lent out on lower rates to the low end of the market, primarily targeted at eradicating informal settlements. Subscription also came from Barclays and Standard bank�s offices in the UK as well as unsolicited funding from the German Government (ibid). Already in its first three years of existence by 1980, of the R20m spent on projects, R15,5m was spent on housing. The best known area of involvement has been the infamous squatter township of crossroads, Cape Town, where lot of its houses were ready by end November 1980 according to Sunday Times Johannesburg, 18 January 1981 (ibid) This body had to work within the agreed terms of the then charged apartheid government, especially in areas of land tenure (99 year lease), zoning and urban planning etc. Though this institutional establishment was received with lukewarm and caution by the said Government, however resolved to work with this institution

3.5.Informal Sector

3.5.1. Stokvels

In their website, Legalcity.net, the online journal defines stokvels as a concept based on traditional African ethos of self-help and mutual support, wherein a group of people join together to pledge regular contributions to a common fund from which each member can draw on rotational basis or at the end of the year, usually for a specific purpose. The online journal traces the origin of this concept to the mid 19th century, arguably from a group of African migrant workers who would set up burial societies to be able to transport their relatives back home for burial when deceased. The national stokvel association of SA (NASASA), the umbrella body co-ordinating various stokvel groupings, describes the organic growth of the stokvel movement into different segments of the Economy, and confirms the foundation as premised on values of ubuntu, trust, support and peer pressure. Evolving from being a pure savings and borrowing mechanism for members, to setting up Joint ventures wherein members would pool together their saving on rotational basis as they qualify for a lump sum payout, which may be used for the purchase of a Taxi/Bus transportation vehicle. This model was even enhanced by members who would host other members when their turn of payout arrive, sell food and liquor on this occasion, with proceeds raised accruing to the host. Though the statistic is not conclusive in this section, which may last the entire weekend With enhancement of the Co-op model, the stokvel system has been adapted by the SCC and Save Act groups in kwaZuly/Natal, by focusing on social and broader economic support to group members, e.g. Financial training, Mutual support and care for HIV affected and infected members, women empowerment

16 Christopher R Hill : Change in South Africa 1983

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 11

and embarking on various civic campaign in the communities.17 . Even though these latter models (SCC and Save act) did not survive through to date, due to the lack of sustainable funds to support the value add functions mentioned above, however the schemes in a revised form still do exist and members intend to use their combined power to negotiate better deposit rates, credit terms and bond investments opportunities with financial institutions. 3.5.2. Mashonisa and Pyramid schemes

Mashonisa are illegal get rich quick schemes that are sometimes operated by notorious individuals in the community, sometimes by unscrupulous business people (shebeen owners, Spaza owners, even by individuals who solely specialize in this sort of lending).18 The target market to this product, are those that have some form of income, i.e. regular wage or salary earners and pensioners / those earning various government grants. The form of credit approval and risk mitigation involves highly irregular terms and conditions, with repayment amounts sometimes twice the original price. Loan advanced, and the borrowers identify documents and savings cards kept as security by the lenders who ensure control of funds as they became available. Pyramid schemes on the other hand promise depositors guaranteed returns above market rates, sometimes up to 300%. The registrar of banks had to intervene by freezing funds of some of these schemes who breached the regulations governing the stokvels maximum limit with a scheme of 53000 members having in excess of R40m to the permissible R9,9 million limit in 1999, having to be frozen by the Banks Registrar (ibid).

17 Elizabeth Dubbeld: the future of Micro credit in Bangladesh and South Africa 18 Legal city, 2007

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 12

Section

4 Global Best Practise

4.1. India

India�s microfinance sector is largely unfettered by tedious regulation and interference. The biggest obstacle until recently was little access to commercial markets and the forbidding cost of capital funds. As private banks, spearheaded by ICICI in 2003, entered the microfinance market, this barrier has partly disappeared and microfinance is growing at a break-neck pace on all fronts viz. loan outstanding, client outreach, product and service diversification or geographic spread. Current issue of concern now focus around skilled human resources, flexible product design, reducing transaction costs, ensuring adequate management information systems, standard credit information, better use of advances in technology, accessing alternative financing, expanding into underserved areas, and dealing with regulatory hurdles and political risks. There is an urgent need for structured long term financing to the sector to fully address these important issues and smoothly transition into a well functioning mature industry.

Currently, roughly 66% of the formal supply is disbursed through the Self Help Group (SHG)-bank linkage route, largely financed by the National Bank for Agriculture and Rural Development (NABARD) while the rest comes from microfinance institutions (MFIs) increasingly backed by commercial banks.19

Despite these efforts, the World Bank estimates that the Indian microfinance activity currently reaches only 4% of the poor.20About 26 percent of 1.1 billion people in India are still under the poverty line. Only an estimated 10 to 12 percent of the poor in India are reached by microfinance including the outreach of SHGs, NGO MFIs, NBFCs, Commercial Banks and Cooperatives.

4.1.1. Credit Delivery Models

The SHG-bank linkage model and the joint liability group model (widely called the Grameen model although Grameen with its particular features is actually a subset of joint liability) are the most prominent microfinance operational models in India. Although some MFIs use one model exclusively, most use both or hybrid models. A SHG is a group of around fifteen to twenty poor individuals�usually women�who provide financial support to one another in the form of pooled savings and internal credit assistance. SHG members generally use the loan for both consumption and productive purposes. Given the fungible nature of money, most MFIs do not scrutinise loan utilisation. The bank issues a loan to the group, after rating them based on their savings and internal credit behaviour. The loans are kept on the bank�s balance sheet. The SHG can also lend internally both before and after the bank linkage takes place. The SHG may choose to keep only part of their savings in the bank account, partly in order to maintain internal financing capability for emergency loans.

19 By this phrase, we mean MFIs operating in partnership with a bank under the ICICI Partnership Model or as Business Correspondents 20 Basu, Priya. Lead Economist, Finance & Private Sector, World Bank. DEBATE: Cap the interest rate on microfinance? The Economic Times. 21 March 2006

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 13

A joint-liability group (JLG) is a small group of borrowers (typically 4-5) who are jointly liable to an external lender (MFI) for a loan that they receive. Unlike the SHG, the sole purpose of existence of a JLG is to receive a group loan from an MFI.

4.1.2. Regulation and Legal Forms

At present, there is not one universal legal definition or form or parliamentary regulation or regulatory authority for what constitutes a MFI in India. The term is broadly applied to an organisation engaged in lending of very small amounts to low-income households previously disconnected from or underserved by the formal banking sector. The organisation may be for or not for profit. It may operate under a variety of legal forms governed by different pieces of legislation and different regulators. There are nine broad legal forms. 4.1.3. Financing Models

Traditionally, civil society organisations financed all operational and capital costs incurred for small lending activity through donor funds. Now, MFIs take on commercial debt for on-lending and raise capital by securitization of assets and portfolio sales. Other avenues available are equity investment, quasi-equity through the partnership model, and loan guarantor funds.

1. On-lending involves the MFI borrowing from banks and then lending that money to clients. On-lending is the predominant model of financing.

2. Securitization: In India, in the absence of a secondary market for microfinance securities, people often use the term synonymously with portfolio sales. The first step of a securitization is the buy-out of a micro-finance loan portfolio against a purchase consideration calculated by computing the net present value of receivables at an agreed discount rate. The originator (MFI) or a third party (such as USAID or Grameen Foundation USA) provides partial credit protection i.e. credit enhancement to the investor (Bank) in the form of a guarantee or over collaterisation etc. amounting to a certain percentage of the receivables under the portfolio by way of a lien on fixed deposit. The MFI continues to service the loan portfolio in exchange for service fees. Although ICICI has purchased several microfinance portfolios, there have been only two securitization deals. In 2004, the largest ever securitization deal in microfinance was signed between ICICI Bank and SHARE Microfin Ltd, a large MFI operating in rural areas of the state of Andhra Pradesh. Technical assistance and the collateral deposit of $325 K (93% of the guarantee required by ICICI) were supplied by Grameen Foundation USA. Under this agreement, ICICI purchased a part of SHARE�s microfinance portfolio against a consideration calculated by computing the Net Present Value of receivables amounting to $4.3 Mn (Rs.215 Mn) at an agreed discount rate. The interest paid by SHARE is almost 4% less than the rate paid in commercial loans.21

3. Few MFIs receive much equity funding, and few large institutions invest in equity. The exception to this latter rule is the Bellwether Fund, which has invested millions of dollars into microfinance start-ups. Foreign private equity funds entering the sector include ACCION Equity Fund and Lok Capital.

4. ICICI Bank created the partnership model .It involves lending money directly to an MFI�s clients, while the MFI services the loan and charges a service fee to the client. Thus the effective interest rate to the client is higher than the ICICI Bank rate as stated on official bank documentation. To incentivize the MFI to efficiently collect repayments, the MFI must repay all the defaults up to a certain limit. This is the dominant mode of financing in India right now.22

5. MFIs receive charitable grants from numerous domestic and international donors. Two types

of grants are used: operating grants which can only be used to meet operating costs, and capital grants which go straight into an MFI�s equity.

21 Duflo, Annie. �ICICI Banks the Poor in India: Demonstrates That Serving Low-Income Segments is Profitable.� Microfinance Matters, Issue 17/October 2005, United Nations Capital Development Fund. 22 Chidambaram P. Government of India Union budget speech 28 February 2006

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 14

4.1.4. Growth Strategies

The SHG movement enjoys immense political and non-government support in India. At the moment, in terms of credit outlay, the sector is divided between bank-linked SHG members and MFI clients at a ratio of 3:1. Both channels are growing rapidly but as the sector penetrates the national consciousness, more investors, entrepreneurs and professionals are attracted to the MFI model. Current trends suggest that the market division between the largely state bank financed SHG and private bank financed MFI route will reverse in the next few years. There are three main expansion strategies for microfinance institutions:

1. Horizontal growth�the MFI chooses plain vanilla products (usually just loans) and replicate across all branches to expand their client base and geographic coverage.

2. Vertical growth�the MFI chooses to maintain a particular client profile and geographic coverage but diversify its products and services instead. Thus catering to changing needs of the customer, the MFI converts itself from a standardized retailer into a full service local financial institution. The MFI is now a �credit+� provider offering insurance, savings, money transfer, remittance, larger loan sizes, individual consumer loans, personal loan products and ancillary business services such as connecting clients to previously non-existent or inaccessible markets and livelihood opportunities.

3. Franchisee�the MFI appoints a local entrepreneur as its franchisee and allows her to conduct business under an established name and methodology.

4.2.UK Perspective

Citigroup, Deutsche Bank, ING, ABN Amro, Standard Chartered Bank, etc. are already supporting microfinance institutions in some form or other like direct financing for loan portfolio growth, catalytic financing through a guarantee mechanism etc. The recently introduced �Growth Guarantee Program� of Grameen Foundation is an example of such support. In the United Kingdom the �Promoting Financial Inclusion� initiative was driven by The National Treasury that �Tackling financial exclusion is the responsibility of financial services providers, working in partnership with the Government and the voluntary and community sector. Working together we can empower individuals to take control of their own finances, access basic financial services and break free of unmanageable debt.� Regulations were put in place to allow everyone access to a banking account - the Universal Banking Services concept announced in the UK in August 2004, providing a cheap, �no frills� bank account which should serve the needs of many who have been excluded from the formal banking sector. In many countries, the Post Office network has the best reach into the community, and can handle simple financial services effectively, leveraging off an existing branch network. Where there is no existing network, it may be possible to use part-time, or mobile units. Historically the communities obtained funding from �Co-operative Banks� which were run along the lines of a saving club concept.

4.3.Grameen Bank - Bangladesh

The concept is the brainchild of Dr Muhammad Yunus of Chittagong University who felt concern at the pittance earned by landless women after a long arduous day's work labouring for other people. He reasoned that if these women could work for themselves instead of working for others they could retain much of the surplus generated by their labours, currently enjoyed by others.

Established in 1976, the Grameen Bank (GB) has over 1000 branches (a branch covers 25-30 villages, around 240 groups and 1200 borrowers) in every province of Bangladesh, borrowing groups in 28,000 villages, 12 lakh borrowers with over 90% being women. It has an annual growth rate of 20% in terms of its borrowers. The most important feature is the recovery rate of loans,

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 15

which is as high as 98%. A still more interesting feature is the ingenious manner of advancing credit without any "collateral security".

The Grameen Bank lending system is simple but effective. To obtain loans, potential borrowers must form a group of five, gather once a week for loan repayment meetings, and to start with, learn the bond rules and "16 Decisions" which they chant at the start of their weekly session. These decisions incorporate a code of conduct that members are encouraged to follow in their daily life e.g. production of fruits and vegetables in kitchen gardens, investment for improvement of housing and education for children, use of latrines and safe drinking water for better health, rejection of dowry in marriages etc. Physical training and parades are held at weekly meetings for both men and women and the "16 Decisions" are chanted as slogans. Though according to the Grameen Bank management, observance of these decisions is not mandatory, in actual practice it has become a requirement for receiving a loan.

A number of groups in the same village are federated into a Centre. The organisation of members in groups and centres serves a number of purposes. It gives individuals a measure of personal security and confidence to take risks and launch new initiatives.

The formation of the groups - the key unit in the credit programme - is the first necessary step to receive credit. Loans are initially made to two individuals in the group, who are then under pressure from the rest of the members to repay in good time. If the borrowers default, the other members of the group may forfeit their chance of a loan. The loan repayment is in weekly instalments spread over a year and simple interest of 20% is charged once at the year end.

The groups perform as an institution to ensure mutual accountability. The individual borrowing member is kept in line by considerable pressure from other group members. Credibility of the entire group and future benefits in terms of new loans are in jeopardy if any one of the group members defaults on repayment.

There have been occasions when the group has decided to fine or expel a member who has failed to attend weekly meetings or wilfully defaulted on repayment of a loan. The members are free to leave the group before the loan is fully repaid, however, the responsibility to pay the balance falls on the remaining group members. In the event of default by the entire group, the responsibility for repayment falls on the centre.

The Grameen Bank has provided an inbuilt incentive for prompt and timely repayment by the borrower i.e. gradual increase in the borrowing eligibility of subsequent loans.

A survey has shown that about 42% of the members had no income earning occupation (though some may have been unpaid family workers in household enterprises) at the time of application of the first loan. Thus, the Grameen Bank has helped to generate new jobs for a large proportion of the members. Only insignificant portion of the loans (6 per cent) was diverted for consumption and other household needs.

About 50 per cent of the loans taken by male members were for the purpose of trading and shopkeeping. 75 per cent of loans given to female members were utilised for livestock, poultry raising, processing and manufacturing activity.

How savings can be a continuous source of adequate financing can be seen from the experience of Grameen Bank which has more money in deposits than in outstanding loans.

4.4.Bolivia

At the end of 1995, two of the five Bolivian microfinance organizations were regulated, and three were NGOs. The three NGOs were Centro de Fomento a Iniciativas Económicas (FIE), Fundación para la

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 16

Promoción y Desarrollo de la Microempresa (PRODEM), and Fundación Sartawi. BancoSol, the best-known microfinance organization in Latin America, is a bank that was split off from PRODEM23. Caja de Ahorro y Préstamo Los Andes is a regulated non-bank (Rock, 1997). The five lenders can be grouped by their lending technology and by their geographic market niche. In lending technology, BancoSol and PRODEM lend to groups, and FIE and Caja Los Andes lend to individuals. Sartawi works through communities to lend to both groups and individuals. In geographic market niche, PRODEM and Sartawi are mostly rural, while BancoSol, FIE, and Caja Los Andes are mostly urban. Thus BancoSol lends to urban groups, PRODEM lends to rural groups, 13 and Caja Los Andes and FIE lend to urban individuals. Sartawi lends to rural groups and rural individuals. The differences in technology and in market niche among the five lenders reflect their history of external support and the forces that spawned their creation. PRODEM lends to groups because, when founded in 1987, it followed the model of the Grameen Bank of Bangladesh. Although PRODEM worked at first in an urban market niche, it later shifted to a rural focus so as not to compete with BancoSol, which inherited most of the urban borrowers of PRODEM when it was split off in 1992. BancoSol was created in part to mobilize large deposits from rich households and firms in order to relieve the constraints on funds that had limited the growth PRODEM, in part to test whether an NGO could become a commercial bank, and in part to mobilize small deposits from poor households and firms. The development of both PRODEM and BancoSol was heavily shaped by technical assistance from the Calmeadow Foundation of Canada and from Acción International, a U.S.-based NGO with links to group lenders in many countries in Latin America. Caja Los Andes was founded in 1992 and has received funds from the Inter- American Development Bank, GTZ of Germany, and the Swiss government. Its individual loans reflect the influence of extensive technical assistance from the German consulting firm Interdizciplinäre Projekt Consult. At first, Caja Los Andes lent mostly for manufacturing in the belief that industry had the greatest effects on employment, but it soon added loans for commerce. When FIE started to make loans in 1988, its clients were urban artisans who had completed classes with a training branch of the NGO. FIE only made loans for manufacturing until 1993, when, like Caja Los Andes, it started to lend for commerce. By 1995, the lending and training arms of FIE were separated. FIE is unique among the lenders studied here because it has not had a single dominant donor nor a major source of technical assistance. Sartawi started to lend to rural communities in part because it already worked with rural communities in non-financial development projects. The bulk of its funds came from Plan Internacional, a rural-development NGO, and from the German Lutheran Church. Like FIE, Sartawi has had little external technical assistance. It separated lending from other activities in 1995. In Aymara, sartawi means to progress. The five lenders have several traits in common. They all work in niches untouched by traditional banks. All five make small loans to first-time borrowers and bigger loans to repeat borrowers. All five charge high prices, and all five keep arrears and loan losses low with various mixes of screening, monitoring, and contract enforcement. All five have received grants, technical assistance, and low-priced loans from USAID and other donors. Still, very little of their success has been due to access to funds from second-tier lenders in Bolivia. Compared with peers, all five have high outreach and sustainability (Microbanking Bulletin, 1998). They all aim to reduce poverty, but none explicitly targets the poor. Bolivia, while sparsely peopled, may have the densest microcredit in the world. The five microfinance organizations studied here are the most important of the about 30 in Bolivia. They account for more than half of both clients and portfolio outstanding (La Razón, 1997).

23 Gonzalez-Vega et al., 1997b; Schreiner, 1997; Mosley, 1996

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 17

Section

5 Business Case Study

5.1.Purpose:

To develop a cost effective model for a co-ordinated rollout of a sustainable microfinance model.

5.2.Reasons

The current industry is fragmented. There is a perception that the microfinance is not a commercially viable business. The cost of loans to individuals is extremely high especially in the informal sector where loan sharks dominate. Lack of financial acumen is prevalent in this sector.

The model will result in the following benefits:

Alleviation of poverty Reduction in Unemployment Sustainable Financial Services Establishment of small social and sustainable economic networks Profitable revenue streams

5.3.Options

To establish a lean cost-effective technologically driven Microfinance Bank utilising franchising principles (including Joint Venture and accreditation with third party institutions) to create the distribution channels and to move away from the traditional bricks and mortar approach of South African banking delivery channels. The principles from the Grameen Bank in Bangladesh are to be implemented whereby funding is done to small groups within a community / geographical area. In Limpopo the Small Enterprise Foundation (SEF) has been running along these principles for a number of years and we have utilised their financial data (see appendix 3) to model our business case and demonstrate that it can become a profitable venture over time.

5.4.Benefits Expected

If done correctly and co-operatively within coherence principles, microfinance will change the socio-economic variables and ensure economic participation, by the excluded majority, into the mainstream of our economy.

5.5.Pricing and Risks

Risk exposure to these loans should be mitigated by setting proper aftercare monitoring, insurance (where economically viable), guarantees that could be sourced from various funds (Government, Donors NGO�s etc.) and market linkages (uptakes) where small business finance is involved.

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 18

This should be accompanied by relaxed forms of credit qualification and vetting process, taking into account the various supporting interventions, which are mentioned above. The following key indicators should be used (Standard chartered bank: microfinance 2006)

Purpose Market sustainability and Business viability Technical knowledge of borrower Possible risk mitigation

The pricing of the loans should be capped at particular margins above the cost of funds. Preferably fixed options should be made available, compared to fluctuating rates. Repayments will also need to be linked to cash flows projected in their business planning.

5.6.Cost

Looking at the SEF experience in South Africa, we have compiled a simplistic financial model utilising an average loan size of R1500-00, funding received at P-2% with some staff expenses, IT and bad debt provisioning which reflects that a positive cashflow could be achieved in year 3 with breakeven being achieved year 5.

However, the present regulatory environment in South Africa does provide challenges and one would need to look at innovative ways of overcoming these. A possibility could be to form a joint venture with the newly formed �Co-operative Bank� and look at �Social Microfinance� options .

Y1 Y2 Y3 Y4 Y5

Loan outstanding 22,500,000 28,125,000 35,156,250 43,945,313 54,931,641

No. loans advanced 15,000 18,750 23,438 29,297 36,621Average loan size 1500 1,500 1,500 1,500 1,500 1,500

Expected Return (30%) 3,375,000 7,593,750 9,492,188 11,865,234 14,831,543Interest Expense (P-2%) 2,587,500 3,234,375 4,042,969 5,053,711 6,317,139Operating Expense 3,932,000 3,932,000 3,932,000 3,932,000 3,932,000Bad debts 0.25% 56,250 70,313 87,891 109,863 137,329Systems 2,000,000 500,000 500,000 500,000 500,000Annual (loss)/profit -5,144,500 -72,625 1,017,219 2,379,523 4,082,404Cummulative (loss)/profit -5,144,500 -5,217,125 -4,199,906 -1,820,383 2,262,021

Assumptions:

Operating Expenses 3932000

Anticipated bad debt 0.25%

Staff compliment 36

Growth of 25% YOY in number of new loans

Expected return calculated at 50% of new loans value to account for disbursements over time.

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 19

5.7.Characteristics of Model

5.7.1.Value proposition

Any application for finance has to be based on sound, sustainable and value adding into the life or existence of the borrower. The measure, and degree of the value added and sustainability thereof will vary according to the purpose of the loan, e.g. the measurement for testing this will take a different set of indicators when looking at a loan to finance a child�s education needs compared to a loan to finance a Spaza shop. Whereas the ability to repay may be a significant indicator to the former case, the availability of the market, the skills of the borrower, may be what comforts the lender in the latter case. Simply borrowing for significantly intangible expenditure (e.g. to entertain friends over drink and braai/barbeque throughout the weekend), may not be sustaining /valuable. 5.7.2.Network Rural and Urban areas: Franchising and JV model will be used thereby banks outsource their loan disbursement services to other agents in order to have a wider outreach to clients in geographical areas. This model can be photocopied to other places within the country. Franchisees or agents will be selected by a bank panel being the Franchisor, proper training be given and the franchisees to work in that particular bank for one month. In the far rural areas people such as chief and church ministers can be used as agents as they are seen being the leaders of the communities and trusted to date by all members of the communities.

In South Africa, branchless banking through retail agents is permitted only for licensed financial institutions. Nonbanks are prohibited from accepting public deposits, broadly defined, so mobile operators interested in branchless banking have created joint ventures with licensed banks to offer cell phone-based banking. WIZZIT, a four-year-old technology firm, became a division of the South African Bank of Athens to be able to offer cell phone- and card-based bank accounts for the unbanked.24 WIZZIT offers deposit, withdrawal, payment, and airtime purchase services through a combination of the mobile phone interface, ATMs, branches of ABSA Bank (South Africa�s largest), and post offices. MTN Banking, a competitor, is a joint venture of a leading mobile operator, MTN, and Standard Bank.25Neither WIZZIT nor MTN Banking uses retail agents (with the exception of post offices) to handle cash on its behalf. Still, South Africa is an important reference case because of network operators� interest in branchless banking and the strict regulatory interpretation that forced joint ventures with banks. 5.7.3.Solution Offerings and Pricing

See appendix 2

5.7.4.Pre-Finance Education and After Care Support / Mentoring

Commercial banks already have shown leadership in the space of low to medium cost housing finance, through the association of mortgage lending customised training towards the first time home loaner buyers. This compulsory type of training is critical to this market, to sensitise the borrower on financial/debt matters. (AML Loan training manual: 1995)

Various NGOs already play in the space of training. The banking industry needs to bring these players in as part of the value chain, on a formalised structured basis. (see the save Act Model Elizabeth Dubbeld paper on: The future of Micro credit in Bangladesh and South Africa).

24 http://www.wizzit.co.za 25 http://www.mtnbanking.co.za

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 20

Similarly the NGOs, established entrepreneurs (e.g. Commercial farmers in agriculture mentorship emerging subsistence farmers) and financial institution�s staff, all should engage in a structured technical support and monitoring role. In cases of rural farming ventures, extension officers who are technical experts on farming practice should be utilised for this role.

.

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 21

Section

6 Conclusion and Recommendation

From a South African perspective Microfinance can be deliverable in a sustainable manner by making funding easily accessible, moving away from the historical brick and mortar delivery channels and encouraging collaborative funding models. Our recommendation is that a funding model utilising a combination of funds from grant and donor monies, wholesale funding ex Banks and deposit monies from lenders be established as a �Microfinance Bank� , based on the Grameen funding principles with delivery channels via franchise principles and or selected JV�s with NGO�s would provide a sustainable solution.

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 22

Section

7 Appendices

Appendix 1 - Demand for Micro Finance Services Source of demand Products and services and characteristics of

demand Households Poor (Rural and Urban Microfarms Fisheries, Livestock and Poultry Enterprise (nonfarm)

Convenient access to safe and liquid deposits facility; Savings with easy withdrawal facility; Return on savings; Term loan with reasonable interest payment; Money transfer services, payment services; Consumption and emergency loans and or burial society

etc; Low cost housing loan; Small loans for livelihood activities; and Low transaction costs Working capital: fertilizer, seeds Term loan: purchasing of tools, machinery, land

improvement, etc; Minimal transactional costs and reasonable interest

rates; Deposit facilities (safe, liquid and convenient); Return on deposits, and Insurance services

(Note: seasonal demand)

Working capital for feed; Term loan: purchasing tools, machinery, livestock,

chicks, etc; Deposit facilities (safe, liquid and convenient); Insurance services

Working capital; Term loan; Deposit services (safe, liquid and convenient); Money transfer, payment services; Insurance and leasing services; and Minimal transaction costs and easy access

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 23

Appendix 2 - Solution Offerings and Pricing

Source of demand Product and Services Suggested Loan size and facility size

Pricing

Micro lending to individual Micro lending to group Small Enterprise and Micro Farms and Medium Enterprise and Medium Farms

1. Personal Loan: household consumption and emergencies;

2. Debit Card no overdraft facility:

transacting, withdrawal; payments and transfers;

3. Savings Account: deposits

services (for saving purpose); 4. Low cost housing loan: buying a

house; and 5. Insurance Services: burial needs:

benefits principal member R6 000 and family member R3000 with hearshe and cemetery being paid for.

1. Club Loan: group size, 5 to 10.

Group project initiatives, end product must be profitable.

1. Working Capital: cash flow and

purchasing of stock; 2. Term Loan: purchasing business

assets; 3. Cheque account: transacting

purpose: withdrawals, payments and transfers facilities;

4. Savings Account/ Deposits

services: (for business saving purpose)

5. Business Insurance: covering

business assets, exposure and livestock

R1000 � R5000 R100 � R1000; R1000 � R15 000; R15 000 upwards R50 000 � R90 000 R50 p.m. minimum R50 000 rural and R100 000 urban Maximum up to R20 000 : Maximum up to R50 000 Maximum up to R150 000 : Maximum up to R300 000 Working capital linked. Up to R10 000; Up to R25 000; Above R50 000. Will depend to the business exposure and asset value

In line with NCA limits Initial fee R20, no charge for usage 3%; 3.5%; and 5%. (will be adjusted as the repo rate changes) In line with NCA limits n/a In line with NCA limits In line with NCA limits In line with NCA limits Working capital linked 4%; 6%; and 8%. (will be adjusted as the repo rate changes) n/a

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 24

Appendix 3 � SEF Financial Information

Dec 2005 (6 months)

Jun-05 Jun-04 Jun-03 Jun-02

Number of loans outstanding 32 054 27 538 22 110 18058 13 387

Loans disbursed since inception R 280 million R 236 million R170 million R124 million R91.5 millionCurrent average loan size disbursed R 1 463 R 1 424 R 1 294 R 1 158 R 1 033Number of loans disbursed since inception 249 436 217 660 167 768 127 276 94 603

Bad Debt rate 0.10% 0.40% 1.40% 1.50% 2.20%Re-scheduled loans (due to illness) R 158 734 R 111 860 R 86 389 R 117 422 R 121 875

Death w rite off for the year R 78 315 R 71 240 R 71 240 R 51 378 R 38 695

Principle outstanding R 31.8 million R 26.4 million R 19.1 million R 13.5 million R 8.0 million

Total savings as held by Clients R 3.0 million R 3.2 million R 3.0 million R 2.5 million R 2.2 million

% w omen clients 98% 98% 99% 99% 98%

Number of clients per loan off ice 254 244 303 296 209

Total staff 170 157 104 101 103

Total Operations staff 143 131 83 83 81

Financial self suff iciency 93% 92% 92% 76% 51%

Source: Small Enterprise Foundation 2006

Financial Indicators for SEF

Dec-03 Jun-03 Jun-02 Percentage change

Loan interest income R 4.64 million R 7.31 million R 4.6 million 58%

Operational expenses R 5.07 million R 9.35 million R 9 million 3.88%

Interest paid R 465 829 R 649 210 R 407 598 59.27%

Investment interest income R 117 353 R 691 408 R 201 716 42.76%

Investments R 2.52 million R 1.3 million R 3.5 million 62.85%

Operational self-suff iciency 91% 78% 51% 52.94%

Source: Small Enterprise Foundation 2006

BUSINESS CASE � CAN MICROFINANCE BE DELIVERABLE IN A SUSTAINABLE MANNER FROM A SOUTH AFRICAN PERSPECTIVE ? PAGE 25

Section

8 Table of References

8.1.Books , Articles and Presentations

1. Microfinance in Bangladesh: Challenges and prospects - Mamun Rashid ,The Daily Star, Vol5.

Num 877 , Wednesday 15th November 2006. 2. CGAP Focus Note No.38 October 2006 : Use of Agents in Branchless Banking for the poor:

Rewards, Risks and Regulation. 3. Is Grameen Bank Different from Conventional Banks ? � Muhammed Yunus , July 2007. 4. Microfinance Regulation in Seven countries � A Comparative Study � Iris Center, University of

Maryland, 31 May 2006. 5. Small Enterprise Foundation � 2006. 6. Banker to the Poor � Yunus Muhammed, The University Press Limited, Dhaka, 2000. 7. State of the Microcredit Summit Campaign Report 2006 :Sam Daley-Harris 8. Standard Chartered � Microfinance Update : Mizinga Melu 9. The Future of Microcredit in Bangladesh and South Africa: The Grameen Bank and Save Act

� Elizabeth Dubbeld 10. Co-operatives in South Africa :Their role in Job Creation and Poverty Reduction : Kate Philip for the

South African Foundation , October 2003 11. Paper delivered by Deputy Minister of Foreign Affairs, Ms Sue Van der Merwe ��Informal

Institutions and Development: What do we know and what can we do?� OECD Development Centre, Paris, 11 December 2006.

12. Business Day, Business Report Stokvel Funds, Wednesday, August 29 , 2007.

8.2.Websites

1. http://www.absa.co.za 2. http://www.fnb.co.za 3. http://www.standardbank.co.za 4. http://www.nedbank.co.za 5. http://www.thedti.org.za 6. http://www.selda.org.za/docs/saveactfinal.doc. 7. http://www.legalcity.net 8. http://www.urbanfoundation.co.za 9. http://www.Dep of Foreign Affairs.co.za