Embed Size (px)

Citation preview

Pergamon Stand. J. Mgmt, Vol. 12, No. 4, pp. 359-387, 1996

Copyright © 1996 Elsevier Science Ltd Printed in Great Britain. All rights reserved

0956-5221/96 $15.00 + 0.00 S0956-5221(96)00021-8

BUSINESS COMMUNITIES IN THE EUROPEAN CONFECTIONERY SECTOR: A U.K.-FINLAND COMPARISON

PAIVI ERIKSSON,* CAROLYN FOWLER,t RICHARD WHIPPt and KEIJO RASANEN~

*University of Tarnpere, Finland, t Cardiff Business School, Cardiff, U.K. and SHelsinki School of Economics, Helsinki, Finland

(First received September 1995: accepted in revised form May 1996)

Abstract - - This paper is based on the early stages of an international collaborative project investigating the structural changes of the confectionery sectors in Finland and the U.K. over the past two decades. An institutional perspective is used to extend conventional understandings of industries via the development of the sector concept. The network and community constructs are shown to be important devices for understanding the institutional character of a sector. Accordingly, the paper reveals the similarities and differences between the two national examples. An explanation is offered of the way domestic networks persist in both countries while contrasting community profiles are apparent. Copyright © 1996 Elsevier Science Ltd

Key words: Sector, confectionery, Finland, U.K., institutional perspective, network, community, international, comparative.

1. INTRODUCTION

This paper offers a preliminary exploration of the structural changes of the confectionery sectors in Finland and in the U.K. over the past two decades and the inter-organisational relationships which result. The sector concept is employed to embrace the entire value chain (suppliers, dis- tributors, regulators and servers - - R~is~J_nen and Whipp, 1992). The main emphasis of the paper is on the confectionery manufacturers and the competitive and collaborative relationships among them and the other actors operating within the confectionery sector. Based on the early stages of a collaborative research project, the paper examines similarities and differences in the patterns of structural change within a sector but seen from two different national contexts. The paper also highlights the relevance of the social dimensions of structural change by applying key elements of organisational and sociological literatures to two empirical cases.

The next section of the paper outlines the broad dimensions used in the study to describe the basic patterns of structural change: these include the economic and social context, the character- istics of the manufacturers and other major actors in ways which are consistent with traditional Industrial Organisation (IO) frames of reference. However, the section goes on to outline the way alternative institutional orientations may be used to establish a fuller conception of a sector. This will involve the identification of a range of competitive/collaborative relationships, including the network and community forms.

359

360 P. ERIKSSON et al.

Sections 3 and 4 present the two empirical cases. The confectionery sectors in Finland and the U.K. are of very different sizes, both in terms of the number of companies and the volume of production. The relationships between the confectionery companies and their suppliers (raw materials, technology, machinery) seem more similar in these two countries than the relationships between the companies and their distributors. The Finnish companies also seem to have developed a somewhat closer relationship to the state than the U.K. companies. The social rela- tionships among the confectionery manufacturers appear to be more complex in the U.K. case compared to the Finnish case. The group of multinational companies within the U.K. market cross national borders in their networks and collaborative relationships. Yet, in both countries domestic networks based on localities, families and social elites persist. Contrasting community profiles are apparent.

Having offered an initial sketch of the different types of relationships between the confec- tionery companies and the other actors within the sector, the U.K. and Finnish accounts raise the question of how these relationships have been established and maintained over time. Has there been any considerable change as to the base of the relationships over time? Which forces and fac- tors have accounted for the change in each country? An interesting feature of the comparison is that one case country has been a member of the European Union (EU) for two decades, whereas the other case country only joined the EU in January 1995.

Overall, the paper will be concerned with the character of cooperation and conflict within inter-organisationai settings. The aim will be to capture, for the first time, both the historical trajectories of such structures and the contrasting patterns of contemporary development. The paper will be unusual in bringing together evidence from food industries with contrasting back- grounds and which, hitherto, have seldom been the subject of direct comparison. In conceptual terms the piece will seek to make a specific contribution. In short, the paper will offer a recon- structed notion of the sector as a means of mobilising sociological and economic literatures in order to understand inter-organisational relationships.

2. ON STUDYING SECTORS

The sector has long been one of the major building blocks of modem social science. Given its centrality, it is unsurprising perhaps that different academic sub-disciplines have employed con- trasting analytical frameworks in order to understand the sector. Alternative models abound (cf. Kay, 1993). Such diversity offers a creative opportunity to those seeking to comprehend the emerging forms of the confectionery sector. The contention of this paper is that the use of com- posite approaches, drawn from different academic specialisms, may be a productive means of decoding such contemporary relationships. In order to substantiate this claim, a review of the rel- evant orientations and conceptual apparatus is required. This entails a brief inspection of the growth of the institutional approach in general and, more particularly, the way it has given rise to the sector concept which draws on a range of socio-economic literatures. For the purposes of this paper, such an overview provides the opportunity to inspect the relevance of the community and the network in the sector context.

The dominant approach to studying a sector has been long-established by the IO tradition within economics. The assumptions of the IO writers were derived from the tenets of neo-classi- cal economics. Consequently, the basic concepts of perfect competition, monopoly or oligopoly used to describe an industry relied on the rational, profit-maximising behaviour of economic agents. Little space was devoted to chronic information problems, the routine ignorance shown

THE EUROPEAN CONFECTIONERY SECTOR 361

by firms, or anything which might distort the movement of economic relations to equilibrium states of rest (Hodgs.on, 1988, pp. 4-21). The last decade or so has seen the emergence of a set of key constructs by IO writers which are now widely used to describe the operation of sectors. These include the notions of strategic capability based on a firm's uniqueness (Lenz, 1980), the extended competitive rivalry among firms, suppliers and buyers (Porter, 1980, 1985), and basic frameworks for classifying an industry according to the balance of the competitive relations it contains (Barney, 1986).

Clearly, the IO tradition has established fundamental ways of describing an industry (some of which will be used in the following sections on confectionery). However, debates within eco- nomics and related disciplines have produced alternative means of comprehending industry struc- tures, and not least, their operation. The contribution of the "new institutional economists" stands out (see, for example, Langlois, 1986). These writers see market and industry relations as essen- tially the product of human experience. Above all, these relations are informed by a variety of social institutions - - that is, agreed forms of behaviour which specify appropriate conduct in recurrent situations. Institutions are the particular sets of assumptions, conventions and proce- dures shown by members of a particular group. Institutionalists seek to explain the influence of such institutions on behaviour and, conversely, the evolution of institutions as an unintended con- sequence of behaviour. This approach is especially uncomfortable for orthodox economics. In the words of Brian Loasby (1987, p. 7): "institutions provide the bounds [to behaviour and choice], and are themselves susceptible to reasonable explanation. They are not, however, gen- erally amenable to precise definition; and this lack of precision is crucial":

Broadly speaking, the institutionalists have found common cause with a number of like- minded scholars from outside the strict confines of economics. The common denominator has been a shared concern with the often intangible rules (Pettigrew and Whipp, 1991) of conduct which guide actions within an industry. Productive examples include Abernathy et al . 's (1983) demonstration of how technological innovation within firms could be facilitated by shaping such implicit rules. Similarly, Elbaum and Lazonick (1986) argued that social institutions in the U.K. (notably family-controlled firms and the separation of finance and industry) constrained the growth of mass production techniques in the first half of the 20th century. Recent attention to the rise of "national innovation systems" and "national business systems" (Whitley, 1992) has extended the use of the institutional perspective further.

This stream of institutional research has energised some alternative approaches to not just the sector but also strategic behaviour at firm and inter-firm level (for an overview, see Whipp, 1996). Huff (1982) and Spender (1989) established the existence of "dominant logics" and "recipe knowledge" which limited decision-making in the firm. In turn, Porac and Thomas (1992) argue that managerial cognitive structures contain the consensually-held beliefs within an industry. If the structures stabilise, they become interpretive frames which shape the way managers make sense of circumstances outside the firm. Three examples stand out: "boundary beliefs", concern- ing who is included in the membership of an industry; "strategic paradigms", which underlie the resource allocation decisions of managers; and "reputational orderings"; as actors evaluate the relative strength of firms within the industry. Recent work by Durand (1993) has applied these constructs to reveal the "technology maps" which businesses use to guide their innovations paths.

As the subsequent sections will show, our investigation of confectionery is informed by the institutional perspective in both the general and more immediate senses. Overall, the sector con- cept outlined below rests on the way the assumptions and conventional procedures found in a sec- tor arise from the interaction of an extensive potential set of actors. In detail however, the oper- ation of the confectionery sector has come to rely on a number of institutional forms, as will be

362 P. ERIKSSON et al.

seen in the tacit rules concerning recruitment, or the cognitive structures which underpin the perceived status of key firms or individual functions (see Section 4).

The term "sector" is widely used, often interchangeably with the label industry. General famil- iarity with the word has reduced its precision. Yet the concept may be construed in a way which releases many of the possibilities of institutional analysis (cf. Whipp and Clark, 1986, Chapter l; Child, 1988). The research on which this paper is based regards a sector as an historical forma- tion of coevolving business activities. It is often, but not uniquely, attached to specific locations, as in the case of a region or country. The core of the sector idea is that it includes organisations which provide similar goods or services along with those who regularly transact with them in supplying, servicing, regulatory or customer roles (R~is~inen and Whipp, 1992, p. 47). It differs from the term industry (perpetually reinforced by government classifications such as the U.K.'s SIC) which confines itself to direct/indirect competitors centred on a common product.

A sector may generate a variety of social and economic relations but we believe its ability to coordinate them may be limited. Sectors should not be assumed to contain simple or dominant governance structures. Rather, sectors are best regarded as arenas where cooperation and com- petition coexist simultaneously. The sector is an accomplishment of multiple actors with naturally diverse logics of action, beliefs and paradigms. Indeed, views of the precise boundaries and membership of a sector may well be contested (cf. Knights and Morgan, 1991). Temporally speak- ing, the sector is routinely in a state of relative impermanence. Tensions persist between constantly emerging alternative economic and organisational solutions. In spite of the force of global economic imperatives, differences in national sectors appear to remain important - - and hence the motivation to compare the confectionery sector in two national settings (cf. Porter, 1990).

Conceived in these terms, the sector offers a promising site to link economic, sociological and cognitive perspectives. The institutional orientation raises the prospect of more challenging accounts of structural relations between members of a sector. This paper highlights two particu- lar expressions of these types of relations: first, social and commercial networks and second, community forms. The main assumption behind this study is that mapping the networks in a sector is useful but that it is not sufficient for gaining an understanding of the social structures involved. The meaning and use of the network connections, that is the social relations among the actors, can only be interpreted by reference to the communities within which these relationships are being socially constructed and reconstructed.

Sector analysts have shown an increasing interest in networks as a manifestation of institu- tional relations. Network structures have maintained an enduring presence within the social sciences. A network is classically defined as a specific type of relation linking a limited set of persons or events. The set of persons on which a networks rests are often termed actors.

The location of individual actors in the network has important perceptual and behavioural consequences for both individuals and the system as a whole (Knoke and Kuklinski, 1982). Historians have highlighted the role of subcontracting networks in the operation of manufactur- ing and textiles throughout the past two centuries (Dobb, 1963). Trust and cooperation are shown to have existed alongside profit maximisation (Thompson, 1991, p. 171).

Subsequent application of the network idea to management has led to challenging results. Network theorists question the idea of the firm as an easily isolated entity and as a dominant economic actor. To them a network is "the totality of inter-organisational relationships, direct and indirect, that a firm is involved in" (Araujo and Easton, 1995, p. 22). Those within the firm are therefore embedded in structured sets of exchange relationships that are both enabling and constraining. Actors are able to convert local knowledge and resources in to general purpose, relational knowledge. Networks are vital sources of organisational learning. Moreover, Johanson

THE EUROPEAN CONFECTIONERY SECTOR 363

and Mattson (1985) consider the firm's position in its network as an intangible asset, the result of the coordination of complementary investments by the firm and its exchange partners. In the mature U.K. confectionery sector, such assets have become so well established as to be almost taken for granted. Forthcoming studies of business networks could also make use of the sociologically more advanced actor-network approaches, where the development of material artefacts are analysed in relation to the building of networks of complementary actors. These kind of views already apply in the field of science and technology studies and await application in sector studies (Latour, 1987).

The second manifestations of institutional relations, the community concept, occupies one of the central positions in the pantheon of sociological thought. Recent political initiatives in the U.S.A. and Europe have re-invented the term. A new political force has been added to the work via its related connotation of "communitarianism" (Etzioni, 1995). Leaving these innovations to political analysts, the concem here is with the sociological construction of community; this may have practical relevance to the study of sectors. A community is composed of individuals/groups who share a common economic position. This is, in turn, reinforced by a range of possible joint social attachments. A community is composed of mutually dependent actors. Anthropologists such as Calhoun (1982) go further. He emphasises not only commonality of purpose but self-reg- ulation. Moral obligation is the essence of a community for him. Communities contain many types of interdependence based on, for example, economic ties, location, religion or even kinship. The paramount characteristic is that community ties do not allow individuals or groups to act wholly independently. Roles and standards are generated within communities and help to define appropriate action in the face of new circumstances (Whipp, 1985, p. 775).

In one respect, communities identified by sociologists may provide an exceptionally strong example of Loasby' s institutions which set bounds to behaviour and choice but which, at the same time, are not amenable to precise definition (see above). Whilst considerable effort has been devoted to the study of scientific communities (Kuhn, 1970) research on commercial or indus- trial communities has tended to be specialised around a geographical focus (see, for example, Piore and Sabel, 1984). Danish management writers though have confirmed the community to be of clear relevance to understanding a number of their industrial sectors. Borum shows how the Danish information technology sector, for example, operates in relation to six identifiable com- munities. These include an "IBM community", a "systems programmers community" and a "technical community" of hardware suppliers (Borum, 1990, p. 191). Borum's and colleagues' work indicates how a sector may be dominated by a single community with practitioners united by common recruitment patterns and joint understandings of methods, ideals and relations to other communities. Conversely, it is possible for such dimensions to appear only weakly, or not at all, in other sectors. The aim of the subsequent sections of this paper is to mount an exploratory inspection of the confectionery sector in order to discover the apparent strength of community forms.

At this early stage of our research, it is not possible to do justice to the full rosta of issues raised by either the specialist literatures on communities or networks. However, it may well be possible to discover the existence of these institutional forms in the confectionery sector, to detect their outlines and to begin to register the comparisons between different national locations. The aim is explorative, in the spirit of a pilot study. Accordingly the method employed has been induc- tive with a reliance on interviews with key actors, triangulated with documentary and secondary sources during 1994. The outcome at this point is a useful clarification of the strong differences in the institutional character of two distinct parts of the international confectionery sector.

In general, the orientation of the study has been towards the qualitative. The choice was

364 P. ERIKSSON et al.

logical since the phenomenon of communities in the confectionery sector had not been studied previously. Such an approach enabled the use of a range of sources with no prior assumption of the superiority of any one type of evidence. The aim was to use a set of probes in order to discover if community forms existed. It is important to distinguish this approach from a deductive method: the project was not seeking to test existing theories or positions. In addition, the intention was to remain sensitive to many of the subtleties which surround inter- organisational relationships.

This composite approach has relied therefore on a mix of sources which are appropriate to an institutional analysis. In other words, the primary and secondary sources are employed to capture the intangible qualities of sector relationships. The concern was with uncovering the assumptions and core values which inform the actions of those across the sector. The need for such a range of sources is reinforced by the attempt to reveal both the structural and processual aspects of inter-organisational forms. Moreover, the muiti-faceted construction of the sector, described in the previous pages, demanded that adequate attention be devoted to a comparable spread of evidential material.

The result has been an attempt to triangulate three main types of data: documentary, secondary and interview-based. The documentary category included a variety of sources, internal to the focal organisations, and which had not been published (such as company communications, mem- oranda, reports and incidental material). The interview evidence (recorded or noted) was not just derived from managers in the main firms; importantly, they deliberately embraced sector specialists (such as technology experts or machinery consultants), suppliers, distributors and those who played servicing or regulatory roles. Inevitably, given the exploratory character of the study, interviews were held with other academic researchers given their role in interpreting and constructing sector recipes and practice. The secondary data sources covered commercial research reports, the publications of key associations and 10 electronic databases.

It should be noted that triangulation between these three types of evidence had two main objectives. First, to minimise reliance on any single type of data; and second, to produce a deliberate tension between them which would generate second order questions to direct the research process. The contradictions between published statements, practice and underlying beliefs provide the basis for some of the major findings reported in this paper. The process was highly iterative. Each of the three categories of evidence was visited repeatedly as research questions and fieldwork opportunities arose. Observational data, of a limited kind, was generated unintentionally as the chance to attend major exhibitions appeared. Such a spread of evidence gave rise to a rich set of concerns which reflected the broad institutional approach of the authors.

The aim of the following sections is to examine not only the economic connections within each sector but also to establish the existence of network and community forms. The attempt to dis- cover the relevance of these inter-organisational relations was guided by a set of questions derived from the preceding discussion. The core questions in the economic sphere centred on determining the established actors, their modes of competition and the extent to which coopera- tion was facilitated by an economic logic. In respect of networks, the inquiry was concerned with: the character and scope of interactions between individuals and groups; the extent to which social, technical and professional networks exist beyond the routine commercial connections found across the value chain; the role of language; and how far network relations constrain or enable the actions of managers. In the community domain our concerns were with identifying the existence of commonly-accepted values and norms which regulate behaviour, the strength of rules of mutual obligation, and how far such community forms have developed by comparison to

THE EUROPEAN CONFECTIONERY SECTOR 365

other sectors in Europe. The preliminary responses to these questions are summarised in the following sections.

3. THE U.K. CONFECTIONERY SECTOR: ECONOMIC, NETWORK AND COMMUNITY FORMS

3.1. The value chain Before explaining the inter-organisational relationships, the first task is to describe the value

chain of the confectionery sector in the U.K. and the confectionery manufacturers and their competitive and cooperative strategies. The U.K. confectionery market is one of the largest in the world, with consumers currently spending over £4.4 billion on confectionery each year. Chocolate confectionery accounts for £3 billion and sugar confectionery £1.4 billion (Nestl6-Rowntree, 1994). The U.K. market is fragmented not only by different tastes for choco- late (white, milk and dark chocolate) but also according to the purpose of the purchase. In the U.K. confectionery is popular with men, women and children (Mintel, 1993a, pp. 17-22). This is supported by an abundance of market research information which has influenced the manu- facturers' product range and brand positioning (Mintel, 1993a; Mintel, 1993b; Trebor-Bassett, 1994; Nestlr-Rowntree, 1994). Confectionery is purchased primarily on impulse, however it is becoming increasingly rationalised with the increased purchasing of multi-packs from super- markets where consumption is planned for a future date (Mintel, 1993a). Overall, the U.K. choco- late market is distinctive in several ways, not least, because of questions of taste which were shaped in the last century and also because of its established own label segment in both the mass and luxury areas of the market (cf. Sutton, 1991; Eriksson, 1994b).

The major raw materials of the industry are cocoa, sugar, milk and fats, together with machin- ery and packaging. Cocoa is the most important raw material in chocolate production and is sourced predominantly from West Africa (Economic Intelligence Unit, 1989, p. 41). The U.K. chocolate industry has benefited greatly from the historical Commonwealth links with the cocoa bean producing countries. This has resulted in manufacturers, such as Cadbury, becoming closely involved with their source of supply by setting up a processing plant in Nigeria. Cadbury and NestlE-Rowntree both import and grind their own beans. Mars, on the other hand, does very little grinding and instead purchases cocoa butter (UNCTAD, 1991, p. 39). Intermediate cocoa products, which are often made to a manufacturer's specific recipe, are available directly from a few U.K. companies or else are purchased from European companies. Continental Europe is also the main source of machinery for the sector (Voipio, 1993, p. 120). The German, Swiss and Italian machinery manufacturers are important actors in the sector and aid in the transfer of information and production technology. Many of these machines are purchased through sales agents located in the U.K.

Wholesalers are important in the distribution of confectionery. They handle approximately 55% of all production (Trebor-Bassett, 1994, p. 25). Their biggest customers are the independent grocery retailers (63% of sales) and caterers. The supermarket chains are also a key group, accounting for 23% of all confectionery sales. In the U.K., own label products have grown with the chain retailers. They are important to the retailer because they have lower advertising costs, lower packaging costs and higher gross margins. The growth of own label products has directly resulted in the increased advertising expenditure of the branded manufacturers (Trebor-Bassett, 1994).

There are many who provide service roles in the sector, including the Biscuit, Cake, Chocolate

366 P. ERIKSSON et al.

and Confectionery Alliance (BCCCA). A spokeperson for the BCCCA regarded the organisation as "the voice of the industry". Eighty-four confectionery companies belong to the BCCCA, and it is in their interest that the Alliance works, for example, to remove legislative obstacles and pro- mote training. Other servers include consultants. These are predominantly technical specialists who have gained experience at one or several of the confectionery companies or their suppliers. These people often have an unparalleled knowledge due to their access to numerous production sites (production manager). Advertising companies and the confectionery press are amongst the other servers. There are two major confectionery magazines in Britain: Confectionery Production and Kennedy's Confection. The first provides broad information on the technology for the indus- try. The second reports on developments in the sector, such as company mergers, new product launches and the career moves of managers. It is seen as important by managers in the industry for enabling personnel to keep in touch with past colleagues. The regulators of the sector are agents of the U.K. government and the EU. The manufacturers must adhere to strict hygiene, packaging, labelling and quality of raw material regulations as specified by the EU. Government departments also serve the sector by funding agencies that promote confectionery products abroad. The confectionery companies are frequently recognised by the British government for export achievements and their importance within the British economy (Nestlr-Rowntree, 1992).

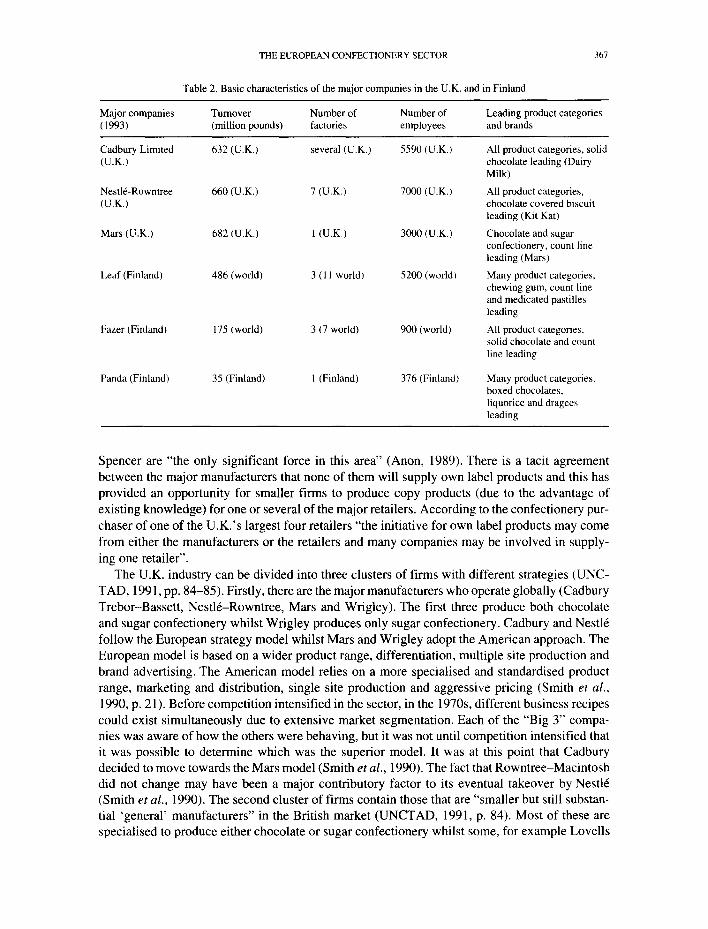

3.2. Confectionery companies and their competitive and cooperative strategies The U.K. sector is dominated by three manufacturers - - the British company Cadbury

Trebor-Bassett (29%), the Swiss company Nestlr-Rowntree (21%) and the American company Mars (17%) (Nestlr-Rowntree, 1994, p. 1). Characteristics of the major confectionery compa- nies and the U.K.sector are shown in Tables 1 and 2. There are, in total, over 100 companies man- ufacturing confectionery in the U.K., however the "Big 3", together with 15 smaller finns, account for virtually all of the production. The ownership of the production facilities has become increasingly concentrated with the number of companies producing confectionery falling by 60% in the U.K. since 1950 (Smith et al., 1990, p. 27). Chocolate confectionery is more concentrated than sugar confectionery due to its more expensive start-up costs, the technological barrier and extensive advertising for branded products (cf. Sutton, 1991). Branding is far more important in the chocolate market than it is in the sugar confectionery market where approximately 38% of confectionery is unbranded and is produced by comparatively small companies (Mintel, 1993b). In contrast, less than 4% of chocolate confectionery is sold under an own label and Marks and

Table 1. Basic characteristics of the confectionery sectors in the U.K. and Finland

Characteristics of the sector (1993) U.K. Finland

Number of companies Consumption (volume)/capita Degree of internationalisation Degree of concentration Status of the sector Industry sub-groupings

112 13.5 kg high high high 1. Large international companies,

"The Big 3" (European and U.S. models)

2. Middle-sized companies (own labels)

3. Small local companies (luxury and novelty products)

6 8 kg moderate/increasing high peripheral/increasing I. Large and middle-sized Finnish-

owned companies (European model) 2. Small Finnish companies (special

products) 3. Foreign sales companies (European

and U.S. models)

THE EUROPEAN CONFECTIONERY SECTOR

Table 2. Basic characteristics of the major companies in the U.K. and in Finland

367

Major companies Turnover Number of Number of Leading product categories (1993) (million pounds) factories employees and brands

Cadbury Limited 632 (U.K.) several (U.K.) 5590 (U.K.) All product categories, solid (U.K.) chocolate leading (Dairy

Milk)

Nestlr-Rowntree 660 (U.K.) 7 (U.K.) 7000 (U.K.) All product categories, (U.K.) chocolate covered biscuit

leading (Kit Kat)

Mars (U.K.) 682 (U.K.) 1 (U.K.) 3000 (U.K.) Chocolate and sugar confectionery, count line leading (Mars)

Leaf (Finland) 486 (world) 3 (11 world) 5200 (world) Many product categories, chewing gum, count line and medicated pastilles leading

Fazer (Finland) 175 (world) 3 (7 world) 900 (world) All product categories, solid chocolate and count line leading

Panda (Finland) 35 (Finland) 1 (Finland) 376 (Finland) Many product categories. boxed chocolates, liquorice and dragees leading

Spencer are "the only significant force in this area" (Anon, 1989). There is a tacit agreement between the major manufacturers that none of them will supply own label products and this has provided an opportunity for smaller firms to produce copy products (due to the advantage of existing knowledge) for one or several of the major retailers. According to the confectionery pur- chaser of one of the U.K.'s largest four retailers "the initiative for own label products may come from either the manufacturers or the retailers and many companies may be involved in supply- ing one retailer".

The U.K. industry can be divided into three clusters of firms with different strategies (UNC- TAD, 1991, pp. 84-85). Firstly, there are the major manufacturers who operate globally (Cadbury Trebor-Bassett, Nestlr-Rowntree, Mars and Wrigley). The first three produce both chocolate and sugar confectionery whilst Wrigley produces only sugar confectionery. Cadbury and Nestl6 follow the European strategy model whilst Mars and Wrigley adopt the American approach. The European model is based on a wider product range, differentiation, multiple site production and brand advertising. The American model relies on a more specialised and standardised product range, marketing and distribution, single site production and aggressive pricing (Smith et al., 1990, p. 21). Before competition intensified in the sector, in the 1970s, different business recipes could exist simultaneously due to extensive market segmentation. Each of the "Big 3" compa- nies was aware of how the others were behaving, but it was not until competition intensified that it was possible to determine which was the superior model. It was at this point that Cadbury decided to move towards the Mars model (Smith et al., 1990). The fact that Rowntree-Macintosh did not change may have been a major contributory factor to its eventual takeover by Nestl6 (Smith et al., 1990). The second cluster of firms contain those that are "smaller but still substan- tial 'general' manufacturers" in the British market (UNCTAD, 1991, p. 84). Most of these are specialised to produce either chocolate or sugar confectionery whilst some, for example Loveils

368 P. ERIKSSON et al.

Confectionery, produce both. Some companies, such as Gerber Confectionery, compete for the highly valued contracts to produce own label products for the national supermarket chains (Bresnen and Fowler, 1996). Marks and Spencer, for instance, purchase their own label confec- tionery for the U.K. market from an estimated 35 confectionery manufacturers according to one confectionery buyer. Thirdly, there is the group of specialist manufacturers, who are either sugar or chocolate confectionery manufacturers, who produce a small product range, operating on a smaller and sometimes more local level, for example Pollard's of the South West of England. Many of these companies are not in direct competition with the larger firms but are instead pro- ducing luxury or novelty items (possibly for the cheap children's market). Some of these may also join together to market, package and distribute their products, as in the case of Sweetmate (Anon, 1991).

Throughout the history of confectionery production in Britain there has been inter-firm co- operation. During the 1920s there were close links between Cadbury, Fry and Rowntree. These firms cooperated on issues such as purchasing cocoa, advertising, pricing and agreeing not to poach employees (Voipio, 1993). In 1934, Nestl6 and Terry were also included in these informal agreements (Smith et al., 1990, p. 74). Until the 1970s, Cadbury supplied chocolate to Mars for their count line product and Cadbury consciously decided not to enter this segment of the market from fear of losing this profitable deal (Smith et al., 1990).

The largest manufacturers have grown organically and then by acquisition and mergers, including Rowntree-Macintosb (1969), Cadbury-Schweppes (1969) and Nestlr-Rowntree (1988) and Cadbury and Trebor-Bassett (1989) (UNCTAD, 1991, pp. 76-79). The 1960s were characterised by diversification as well as signifying the start of the merging of chocolate and sugar confectionery companies (Rowlinson, 1995, p. 126). This was also when power began to shift within the sector from the manufacturers to the retailers. The main reasons were the abolition of the Resale Price Maintenance, increased concentration of the retailers, the onset of own label products and the introduction of advanced point of sale information technology (Hyde et al., 1991). Since this time the supermarket chains have been able to demand strict specifica- tions from the manufacturers, for example - - packaging requirements, and often refuse to stock slow moving lines according to two purchasers from the major supermarkets.

The frequency of the mergers and acquisitions amongst the confectionery manufacturers, since the 1960s, can be partly explained by market saturation. It has become increasingly difficult for established companies to increase their market share by either promoting their existing brands or developing new ones. Instead, it is more efficient for a company to purchase market share. This saturation also led to increased exporting, particularly in the 1970s. The U.K. is currently the largest European exporter of sugar confectionery (see, for example, Sutton, 1991 and Eriksson, 1994b). Since the early 1980s many manufacturers retrenched into their core confectionery business and core brands, in some cases abandoning the low-earning sections of their product portfolio (Smith et al., 1990). Simultaneously some companies have attempted to grow by using their established brand image with new products, for example Mars ice-cream bars. These brand extensions have involved new forms of cooperation between food manufacturers, for example ice-cream and confectionery companies (Nestlr-Rowntree, 1994, p. 2).

Historically there have been U.K. chocolate centres in Birmingham, Leeds and Bristol. Manufacturers in these areas maintained contact points through local colleges or night schools that provided training for the industry. More recently there has been greater movement of operatives between confectionery companies in the same area, as in the three in the Bristol area (production manager Bendicks). Since the 1980s interaction between the manufacturers in

THE EUROPEAN CONFECTIONERY SECTOR 36!)

general has increased; this has occurred for a variety of reasons, some of which are discussed in the following section.

3.3. Evidence of network relationships It is by no means straightforward to display the network relationships that exist within the con-

fectionery sector. The primary need is to examine the interaction between managers of firms of different sizes within both sugar and chocolate confectionery as well as the central role of the BCCCA within the confectionery sector.

The U.K. confectionery sector contains networks that are both formal and informal, and that are fragmented between chocolate and sugar confectionery companies. Even after the extensive mergers and acquisitions, which have brought both activities into one company, the businesses are frequently left as separate divisions, operating on different sites and with different labour mar- kets. This has resulted in the continued divide between the sugar and chocolate confectionery net- works. Even though the BCCCA, which is a major meeting point for the sector's members, rep- resents both chocolate and sugar confectionery, here too the separation persists.

Figure 1 is a schematic representation of the social networks operating between individuals in the different confectionery manufacturers. The data collection process for this diagram originated with a detailed search of published articles and reports as well as company documentation. This was supplemented with interviews with senior managers of a wide variety of confectionery manufacturers, from the "Big 3", medium-sized branded and own label manufacturers and smaller more local manufacturers. In addition, interviews were conducted with 10 importers in order to gain a different perspective of the U.K. confectionery sector. The nodes portray individual managers and the number of nodes is not precisely equivalent to the number of actors within the sector. The linkages represent exchanges between the managers of different organisa- tions, which are predominantly of a social and informal nature even though they are frequently founded upon an economic basis.

Interaction in the sector is very separate between sugar and chocolate confectionery managers and in the case of sugar confectionery can be broken down between different types of sugar con- fectionery, for example boiled sweets and toffees. The chocolate confectionery network is far denser and it is generally considered in the industry that the network has matured to the point where "there are people in every chocolate factory in Britain who will know people in most other choco- late factories (in Britain)" (a chocolate confectionery Managing Director). Connections between the sugar confectionery firms are not as widespread, largely due to the greater number of firms involved but also because of the more fragmented nature of the market. In general, both sugar and chocolate confectionery networks are seen to be more informal between the employees of smaller firms, compared to the links between the larger firms. Most relationships are between companies that are similar in both size and product type. The situation is illustrated in Fig. 1.

The contact between the largest firms is more formal and centres around the BCCCA. This was evident from the committee structures at the BCCCA (BCCCA Annual Review 1994, pp. 37-41). During fieldwork it was found that employees of the largest firms were more likely to interact with managers of medium-sized firms within their product grouping, i.e. chocolate or sugar confectionery. There was little evidence of relationships between employees of the largest and smallest confectionery manufacturers. Where this did occur it was most likely to follow an acquisition, for example the Trebor-Bassett purchase of Lion Confectionery. The strongest informal interaction occurred between managers of medium-sized companies. It was in these companies that managerial mobility was highest, so enabling the development of numerous social relationships between both past and present colleagues.

370 P. ERIKSSON et al.

Ch an1

Chocolate Chocolate e.g.

relationship between individuals or groups within different companies

O chocolate confectionery company

( ~ sugar and chocolate confectionery company

sugar confectionery company

Fig. 1. A schematic representation of networks of individuals/groups in the U.K. confectionery sector.

It is not unusual for employees to work all their lives within the confectionery sector, if not within one firm. This was commented upon by nine different managers. However, our findings showed that it was not uncommon for the senior managers, particularly of medium-sized com- panies, to have gained experience with three or four different firms, although it was rare for employees to move between sugar and chocolate confectionery manufacturers. Even when they transferred to a manufacturer that produced both they continued to work within the same product group.

In the smallest firms, contact was primarily less formally structured and again was between personnel of companies producing a similar product. Interaction was most likely to have been initiated at an exhibition or similar function. Connections between medium and small manufac- turers were common because many of the smallest manufacturers had been established by man- agers with previous experience of one or several medium-sized confectionery companies. Within the confectionery sector there were some medium-sized companies that produced both chocolate and sugar confectionery and it was their managers that had links in the two separate networks.

Interviews with both domestic manufacturers and importers revealed that importers are peripheral players in the U.K. sector and on the whole are not well connected to the U.K.-based manufacturers. However, some importers do have close links with staff of U.K. manufacturers,

THE EUROPEAN CONFECTIONERY SECTOR 371

for example some managers have left manufacturing companies to work for an importer of finished confectionery. Some importers have close ties but these are between companies that are most likely to be situated in the same country and which have a history of interaction within their domestic market.

All of the senior managers that were interviewed agreed that it used to be the convention that if one worked for a major confectionery company then transferring to a competitor was highly unlikely. This was thought to have existed until competition increased in the 1970s. However, since then there has been a change in the operations of the sector's social and commercial net- work and a reduction in the formal cooperative behaviour. At one level secrecy has increased between the manufacturers and it is no longer possible for employees of one company to visit another within the U.K., instead it has become more likely that staff of a U.K. manufacturer would travel abroad (especially to Europe) to view another confectionery manufacturer. This has dra- matically affected the transfer of knowledge in the sector.

In order to compensate, firms began to recruit personnel from their competitors, for example when Cadbury recruited Mars personnel (Smith et al., 1990, p. 322). The frequent takeovers in the industry have also meant that the sector's network has developed through easy access to other manufacturing establishments and techniques which had been acquired into the group, as in the case of Cadbury in France and the U.K. More recently, people have moved within the confectionery industry through competitive recruitment policies, "Previously this would have been completely unheard of and definitely frowned upon but then there would have been much greater loyalty shown towards the employee. Nowadays, they are reducing their staff" (chocolate confectionery Managing Director, 1995). The increased movement of staff between firms is seen as a direct response to the reduction in loyalty of the employers as witnessed by the job losses and rationalisation programmes. It used to be very rare for people to leave, especially from the shop-floor. However, in the 1980s redundancies in the confectionery industry became commonplace. Employee movement is also thought to have increased because of disenchantment with the new "foreign" management styles following a takeover or merger. Such approaches are seen not to fit with the previous family ownership and paternalistic management. This has resulted in companies losing technologists and craft expertise.

The research findings reveal that fewer informal relationships have developed between the largest manufacturers due to there being comparatively less movement of staff out of these firms. The result is managers in these organisations being more orientated towards their own company and having fewer links with the other manufacturers in the sector. The explanation lies in these organisations having the scope to offer sufficient career opportunities within their group. The greater movement of personnel between the medium- and small-sized companies explains why it is their managers that are more likely to have broader personal networks within the confectionery sector.

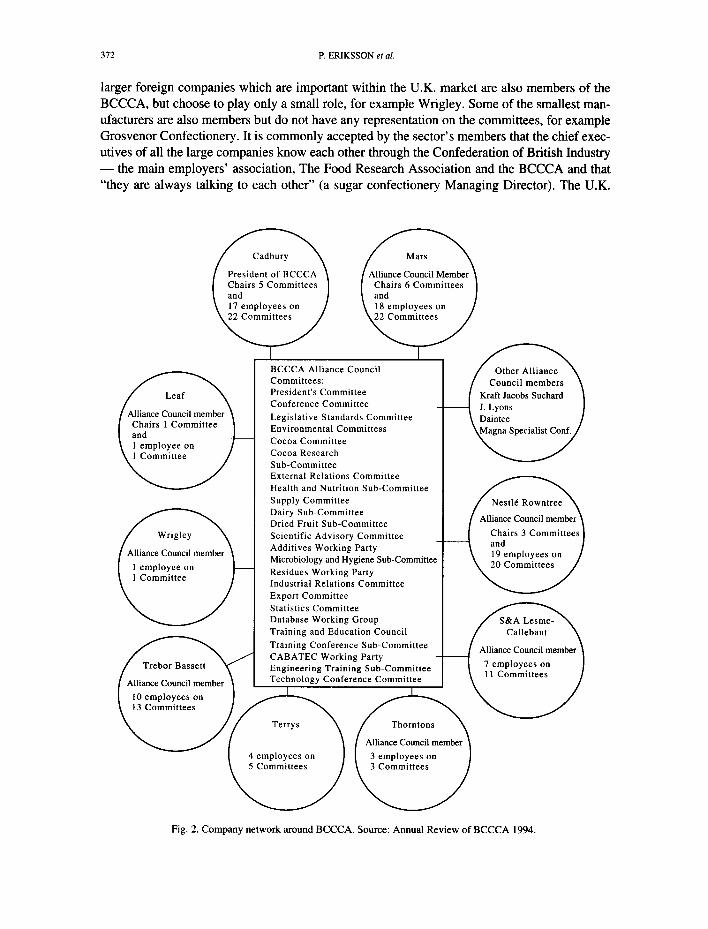

The BCCCA is a central feature of the confectionery sector and acts as an important meeting point for representatives of the industry. The Alliance has 24 different committees and these are comprised of staff from 59 different organisations, mostly manufacturers. They are predomi- nantly middle and senior managers who have closely related areas of expertise. The ties amongst the Alliance's members are based around personal and social interaction as well as the formal committee membership and are strengthened by the sharing of experiences, values and knowl- edge. The largest manufacturers have the strongest presence in the association through their high level of committee membership (see Fig. 2). This diagram was derived from the information supplied by the BCCCA (For example, the Annual Reviews of 1993, 1994 and 1995). Some

372 P. ERIKSSON et al.

larger foreign companies which are important within the U.K. market are also members of the BCCCA, but choose to play only a small role, for example Wrigley. Some of the smallest man- ufacturers are also members but do not have any representation on the committees, for example Grosvenor Confectionery. It is commonly accepted by the sector's members that the chief exec- utives of all the large companies know each other through the Confederation of British Industry - - the main employers' association, The Food Research Association and the BCCCA and that "they are always talking to each other" (a sugar confectionery Managing Director). The U.K.

BCCCA Alliance Council / nrh,r t, ll~o,., \ ~ Committees:

President's Committee Conference Committee Legislative Standards Committee Environmental Committess Cocoa Committee Cocoa Research Sub-Committee External Relations Committee Health and Nutrition Sub-Committee f ~ Supply Committee Dairy Sub-Committee Dried Fruit Sub-Committee Scientific Advisory Committee Additives Working Party Microbiology and Hygiene Sub-Committee Residues Working Party Industrial Relations Committee Export Committee Statistics Committee Database Working Group f S&A Lesme- ~ Training and Education Council / Callebaut \ Training Conference Sub-Committee [ Alliance Council member \

J CABATEC Working Party - '- '---"l "7 ~mnl . . . . . . . . [ Engineering Training Sub-Committee ~ ~ l~'ae~.~;~'~" ] Technology Conference Committee

Fig. 2. Company network around BCCCA. Source: Annual Review of BCCCA 1994.

THE EUROPEAN CONFECTIONERY SECTOR 373

networks are sufficiently developed that if one company wanted to sell part of its operations, the information would be passed to all likely buyers in the industry "like wild-fire" (a chocolate con- fectionery Managing Director). The sale of Bendicks in 1988, was a case-in-point. These net- works can be viewed as a resource. If a manager is considering changing a source of supply, they routinely contact another firm requesting that firm' s experiences of that supplier.

Members of the chocolate network feel that the sugar specialists do not have the same cama- raderie due to their products being more fragmented and more peripheral to the U.K. confec- tionery sector. In spite of this, there was evidence of very close commercial cooperation between some smaller sugar confectionery manufacturers who produce some products for each other as well as helping out when they are busy or are experiencing mechanical problems. No evidence of this type of relationship was found in the chocolate confectionery sector due to the more sophisticated nature of the product and the greater secrecy of recipes. However, in chocolate con- fectionery there were instances of"borrowing" raw materials from fellow manufacturers if stocks were low and suppliers could not deliver on time.

Economic relationships in the sector (between a manufacturer and a supplier) ~'start as totally professional and develop in time to become social. This is part of the importance of the relationship because when things go wrong you've got to be able to trust the person on the other end of the phone" (chocolate confectionery Managing Director). The inter-firm nel- works in the sector do tend to be based primarily around an employee 's function. This is because employees from a similar function have the opportunity to meet at national exhibi- tions (for example, marketing and sales personnel) or training courses (for example, produc- tion or engineering personnel). Conferences can also prove important. When reporting on the 41st Alliance Technology Conference, the BCCCA wrote "It commands a faithful audience of regulars" (BCCCA Annual Review 1994, p. 36). These relationships are strengthened by the ready identification of shared experiences and common technical problems within the U.K. sector.

The suppliers of intermediate cocoa products are also an important link in the economic net- work, especially for the smaller firms. These suppliers employ confectionery experts who have a detailed knowledge of food chemistry, for example chocolate, and when this is combined with their routine interactions with chocolate factories around the world, they become vital informa- tion conduits in the confectionery sector. As one Managing Director said "they act as remarkably good channels for communication". They are seen as central, not only for their knowledge of con- fectionery production processes but also for their contacts and their own personal links with con- fectionery experts which they have built up. They are often used as a communication channel when a manager wishes to change jobs within the industry.

The recent increased movement between confectionery firms has extended the confectionery networks and made the sector more open. In Nestlr-Rowntree there has been a steady two-way flow of personnel between the U.K. and Switzerland since 1988. Currently, more than a quarter of the staff at Nestlr 's major confectionery research centre in York are from outside Britain (Lorenz, 1994). In another chocolate company one Director talked of his previous colleagues in four different confectionery firms in the following terms: "they would all talk to me as if I saw them yesterday, whereas it is more likely to have been at least 2 years." The familiarity within the sector is undoubtedly increased by there being comparatively few people within the special- ist technical or managerial bands in the sector's employment hierarchy. This is especially true for the specialist functions such as chocolate chemists or trained sugar boilers. "You tend to know all of them, and you tend to talk to all of them from time to time" (chocolate confectionery Managing Director).

374 P..ERIKSSON et al.

Although movement of personnel within confectionery has increased within the sector, strong loyalty to a product area persists. The divide between the sugar and chocolate confectionery net- works can be witnessed in the distinctive languages of professional expertise which are used by the sugar and chocolate confectionery actors in the U.K. sector. These are common to English- speaking sugar and chocolate confectionery sectors across the world.

3.4. Evidence of community relationships The managers within the confectionery sector studied in this research believed that there was

a confectionery community within the U.K. and that it was predominantly divided between sugar and chocolate confectionery manufacturers. Older and more experienced managers in the sector thought there was a confectionery community, because of the "allegiance" that so many employ- ees have to the sector. One of the dominant norms of the community is the long career paths within one or several confectionery companies.

The nature of the two communities appears to be different. The chocolate community is smaller and more united (probably due to its higher concentration) resulting in its ready identifi- cation by its members. One of the most important issues for the chocolate manufacturers has been to maintain their high product integrity. Chocolate production was considered to be a craft which needed to be mastered and there were thought to be only a few "chocolate masters" in Britain. These were managers or food technicians that had received extensive formal training in conti- nental Europe. Interestingly, the majority of manufacturers were agreed in their view that the "Big 3", even with their domination in the U.K. and world markets were not chocolate masters but instead were experts at manufacturing "clever" chocolate by using cheaper raw materials and advanced technology. In spite of this, the large manufacturers are important within the commu- nity, because of their high profile in the external relations of the sector and also because of their central role within the BCCCA. The BCCCA is seen as having a central role for the community by providing a fulcrum point, "One of the joys of going to these functions [at the BCCCA] is that you are guaranteed of knowing two or three people in the room that you may not have seen for 10 or 15 years" (chocolate confectionery Managing Director).

In contrast, the sugar community was more fragmented and there were signs of lower company and sector loyalty; this was confirmed by lower interaction between the manufacturers and the propensity of the managers to leave sugar confectionery to work in other areas of the food sector. This is interesting, considering that it is chocolate that, as a raw material, has the wider use within food manufacturing. It may be that there is less loyalty in sugar confectionery because of it having a lower craft status and requiring fewer specialist skills.

Where economic links did exist between sugar confectionery manufacturers they appeared to be closer, for example, in sharing production or packaging facilities (Production Manager, sugar confectionery). This may be because there are more opportunities for economic coopera- tion due to the need for less secrecy regarding production techniques within the industry. Even recipes for different types of sugar confectionery are published in the industry magazine (Kennedy's, 1994, pp. 36--39). However, the social network was more fragmented and the com- munity less tangible, this was commented upon by representatives from 15 different sugar con- fectioners. Nevertheless, amongst the smaller manufacturers, particularly of the higher quality sugar confectionery, there was typically a closer social network and a greater awareness of the confectionery community.

An important feature of the confectionery sector in the U.K., is the historical tradition of the firms' "moral" behaviour and pride in their welfare management principles (Voipio, 1993; Nestlr, 1993). The major confectionery companies, have throughout their history, been involved

THE EUROPEAN CONFECTIONERY SECTOR 375

in and supportive of the areas where their plants are located, as in the well-known case of Cadbury building houses for its employees. The major British manufacturers have been in continuous contact with each other over issues concerning their sector's environment and have established norms of behaviour and mutual obligation (marketing manager, Cadbury). Examples include agreements not to recruit directly from each other and not to supply own label products. However, as loyalty has fallen and the sector has been opened to a greater number of actors so the commu- nity norms have been threatened. This has resulted in behavioural changes, including more competitive recruitment practices. However, for the larger manufacturers life-long employment in one company persists.

Rules of behaviour exist, especially in respect for "professional" boundaries, particularly amongst the older managers. Experienced managers who are connected socially but who work for rival firms will "never discuss some issues (for example, production techniques), you just wouldn't ask the question" (chocolate chemist). This is also true for prior colleagues of the same firm who would not even discuss how they used to manufacture confectionery. Even though movement across the sector has increased there are still signs of mutual obligation between companies and individuals. Some managers reported that when they had left one confectionery company and gone to work for a rival, they had not recorded the recipes of their previous employer nor had they been asked to, even though they had the necessary knowledge "it would not be appropriate to do so, it was theirs [the previous employer], they had worked hard for it" (chocolate chemist).

Mutual obligation and shared values also exist within the confectionery community. For example, according to industry consultants, there was a shared interest to maintain positive company images, especially for the largest manufacturers. Cadbury and Nestl6-Rowntree both wish to preserve their paternalistic image whilst Mars and Wrigley are both intensely secretive and their employees keep a low public profile. Alternatively, Cadbury is more open and its employees work hard to maintain a strong public face. Other shared ideals in the sector included raising awareness of "quality" confectionery, this was particularly true for the medium- and small-size chocolate producers. Evidence was also found of trust between companies currently manufacturing products for each other.

Managers reported that the nature of the community has been changing due, in part, to environmental pressures, such as increasing international competition, changing consumer tastes, a shifting of power within the sector towards the retailers, and changing employment profiles (Smith et al., 1990). Some of these changes were seen to result in diminishing loyalty. Currently, the younger managers seemed to associate more closely with their function and showed less loyalty towards their company or sector.

The major market for most companies in the U.K. sector is the domestic one (Mintel, 1993a, b). However, an international awareness has emerged in recent years as the number of foreign companies acquiring U.K. production units has increased together with the size of the U,K.'s confectionery exports. This has had an effect on the community. A confectionery buyer for one of the major U.K. supermarket chains, felt that Rowntree has changed its priorities since the Nestl6 takeover. She thought that they were now far more globally orientated and were less inter- ested in their U.K. customers. This was shown by the supermarket having to cope with stock shortages whilst Nestl6-Rowntree were launching their products in new foreign markets and the resulting strain put upon domestic commercial networks.

Practices of inclusion and exclusion seemed to be operating within the U.K. community. Companies operating outside of the U.K. were not thought of as being included in the U.K. con- fectionery community (although some obviously are involved in the commercial networks,

376 P. ERIKSSON et al.

particularly suppliers). From interviews with staff of 10 Belgian, French and German manu- facturers, the authors conclude that importers, especially the small luxury Continental companies, were not thought of as being included. This is because they are distant from and critical of U.K. production techniques, training and raw materials. A foreign manufacturer has a greater chance of being included in the U.K. community if they are producing within the U.K. This is because they are more likely to be seen as British, due to employing British staff when acquiring a British company.

4. THE FINNISH CONFECTIONERY SECTOR: ECONOMIC, NETWORK AND COMMUNITY FORMS

4.1. The value chain As in the U.K., the most important raw materials used in confectionery production in Finland

are sugar, milk (powder), cocoa, fats, and flour (for liquorice). Sugar, milk (powder) and flour have been domestic monopolies because of the Finnish agricultural policy. This is changing now that Finland is a member of the EU (e.g. Tukiainen, 1994). The largest confectionery company, Fazer, buys cocoa powder and cocoa fat through intermediaries in Holland, Germany and the U.K. (Donner, 1991, p. 46). According to industry experts all the other Finnish companies no longer grind their own cocoa beans. Each of the companies have developed their own relation- ships with cocoa and other raw material suppliers over time (Donner, 1991, p. 48; Volk and Mikkola, 1994, p. 37) and, according to managers, the companies hardly use the same interme- diaries. Production machinery is supplied by foreign suppliers, German and Italian producers, for example (Volk and Mikkola, 1994, p. 43). However, the managers interviewed reported that each manufacturer usually remodels the machinery for their own use.

Distributors are amongst the most important actors within the confectionery sector (cf. Peltola, 1991; Kuparinen, 1992; Volk and Mikkola, 1994). Because of the concentrated retail trade in Finland, the manufacturers have to sell their products on a yearly basis to four large wholesale organisations, who distribute them to retail shops, kiosks, cafrs and petrol stations. Despite the power of wholesale organisations over manufacturers (Lindqvist, 1983) and the problems in the cooperative relationships, this intensive inter-relationship is also mutually beneficial. According to managers, wholesale organisations carry part of the stock, they transport the goods to the retail- ers and give considerable marketing support to the manufacturers. The wholesale organisations have some own label confectionery products but this segment has not yet grown important (cf. Eriksson, 1999; Holtari, 1993). During recent years, each company has developed its own distri- bution channels (Kinturi, 1981; J~ms~i, 1993; Vaalavirta, 1994) and respective networks abroad (for an example, see Hyv/Snen and Vihma, 1995, p. 34). They have also made agreements with the emerging European-wide retail alliances (Sahiluoma, 1992; Korhonen, 1993). Tax-free trade is an important distribution channel for one of the largest Finnish companies, Fazer (cf. Kauhanen, 1993).

The Finnish state and the EU are the most important regulators of the Finnish confectionery sector (Volk and Mikkola, 1994, p. 27 and p. 32). One of the servers, the Finnish Food Industries Federation (FIF), is an important intermediator between the confectionery companies and the reg- ulators (including state and trade unions) (cf. FIF Annual Reports; Alanen, 1992). Others who play service roles include consultants, advertising and market agencies and financial institutions. According to industry experts, the large companies use the same international consultant and market agencies but each tend to have their own advertising agencies and financial arrangements.

THE EUROPEAN CONFECTIONERY SECTOR 377

Finnish consumers eat less confectionery, particularly chocolate, than consumers in many other countries (Eriksson, 1994a, see also Table 1 ). However, the Finns spend approximately the same amount of money on confectionery as the British consumers. Confectionery is more expen- sive in Finland, but according to respondents, the Finns also prefer higher quality. Local tastes are deeply rooted (Eriksson and Pantzar, 1992), which is reflected in the relatively high con- sumption of liquorice-based confectionery products in Finland, for example. According to mar- ket research, most of the confectionery in Finland is eaten by children, teenagers and women and is bought on impulse.

4.2. Confectionery. companies and their competitive and cooperative strategies There has been a strong trend of concentration within the Finnish confectionery sector since

World War II. In 1994, there were only six domestic confectionery companies. The three largest are Fazer Confectionery (part of Fazer Companies, owned by the Fazer family), Leaf Finland (part of the international Leaf Group owned by the Finnish Huhtam~iki Corporation) and Panda (former cooperative, bought by three managers in 1988) (see Table 2, also Eriksson, 1994a). These companies have almost 70% of the domestic market. The other three companies are very small, accounting for about 5% of the market. In addition, there are a number of large interna- tional confectionery companies in the Finnish market, such as Mars, Marabou and Nestl6 (Voipio, 1993, p. 121). These operate through their own sales offices or agents but have no pro- duction in Finland. Imports account for almost 30% of the Finnish confectionery market but exports are almost twice the amount of imports (FIF).

Traditionally, the Finnish confectionery companies have produced a wide range of products. Each of the large companies have a variety of well-established core brands but each of them also introduce experimental brands (cf. Eriksson and Pantzar, 1992; Teirisalo, 1990). New brands gen- erate more profit, but they do not usually have a long life cycle (cf. Peltola, 1991, p. 14; see also Eriksson, 1991). Typically for a mature industry, the companies fight for rather small changes in domestic market shares. Since the increasing imports from the early 1970s, companies have made efforts to rationalise and modemise their production processes and product ranges with varying success (e.g. Monto, 1973, 1975; Nevalainen, 1986; Eriksson, 1991). However, according to the managers interviewed, none of the Finnish companies have yet adopted the U.S. model of narrow product range and standardised production (Saastamoinen, 1992; Jaakkola, 1996).

Fazer Confectionery (including Chymos range) is the market leader, being particularly strong in chocolate with their high quality Swiss-type milk chocolate brand for which they have devel- oped a technology of their own using fresh milk. Fazer also has leading brands and a good mar- ket share in count lines, pastilles and candies (Teirisalo, 1990; Eriksson and Pantzar, 1992). Leaf Finland has specialised in chewing gum, count lines and medicated pastilles, in which groups it has several "number one" brands (Teirisalo, 1990). It is emphasised in Annual Reports and Company Newsletters that Leaf's strategy has an emphasis on health issues. They developed a manufacturing technology using a new sweetener, Xylitol (which is mostly used in chewing gum), in cooperation with another Finnish food industry company (e.g. Isosaari, 1994). They have also launched a low calorie count line brand. Panda used to have a very wide product range, which was sold exclusively in cooperative retail shops (cf. Kinturi, 1989; Vaalavirta, 1994). Since the management buy-out, Panda has rationalised its product range and is specialising in assorted chocolates, liquorice and dragees, in which groups it has a larger market share than its competi- tors (Ohrnberg, 1994). Panda has developed its own technology for liquorice production, which is based on all natural ingredients (cf. Wessman, 1990; Volk and Mikkola, 1994, p. 44).

The Finnish confectionery companies are situated geographically apart, which supports the

378 P. ERIKSSON et al.

statements by managers that there are few cooperative relationships based on locality, such as movement of labour and staff between the companies. According to a labour union representa- tive, the Finnish confectionery companies are considered to be the best employers within the food sector. They have better remuneration packages, offer better training and life-long employment. When managers or workers have left a company, they have usually taken new employment out- side the confectionery sector.

Linking interviews with managers and industry experts with their public statements has revealed little cooperative activities between the domestic companies (see also Volk and Mikkola, 1994, p. 47). However, the large confectionery companies have developed some cooperation when they have identified a common threat or an opportunity, such as the increasing imports in the 1970s and the issues concerning Finland's membership in the EU in the 1990s. According to managers, rising imports forced the large domestic manufacturers to discuss the future of the industry and to make an industry rationalisation agreement (see also Monto, 1973, 1975). There has also been some cooperation in the form of product exchange and some joint export efforts (Karkk~iinen, 1976; Jonsson, 1992). However, these cooperative relationships have never been industry-wide. The Panda cooperative was left out of the industry rationalisa- tion agreement and Fazer stayed outside joint export efforts in the 1970s (Eriksson, 1991). Campaigning for the EU membership made Fazer and Leaf work together more closely for 2 years (Donner, 1991; Tukiainen, 1994). However, these, or any other forms of cooperation, have not been widespread. For example, Peter Fazer has been the key figure in the EU membership and the related domestic raw-material monopoly discussions but Leaf and Panda management have remained in the background (for examples, see Alanen, 1992; Hertsi, 1993a, b). On the other hand, the large companies have developed their own network relationships both within and outside the Finnish market. These will be discussed in more detail in the next section.

4.3. Evidence of network relationships In this section, we will first discuss the fragmented nature of networks within the Finnish con-

fectionery sector and provide an example of one of the separate company networks: the innova- tion network of Leaf Finland. Secondly, we will investigate the recent activities within the net- work of the domestic confectionery companies evolving around the industry association, the FIF.

In general, both formal and informal networks within the Finnish confectionery sector seem to be rather fragmented and separate. Historically, each of the major companies have developed their own domestic and international networks based on their own strategic interests within the confectionery sector (cf. Eriksson, 1994a). This is even more true outside of confectionery in areas such as cooperative retailing, pharmaceuticals, packaging, cleaning services, construction and other food industries. Geographical distance between the confectionery companies, high loy- alty and low mobility of labour and staff, and, according to industry experts, a general attitude of competitiveness and secrecy have advanced this development of building networks outside the confectionery sector.

The research findings reveal that the current networks are built around broader divisions, some of which are also found in other sectors of the Finnish economy (for divisions in the whole Finnish economy, see Alestalo, 1985, p. 180, for example). Fazer Group is one of the old and well respected corporations within the Swedish-speaking economic circles in Finland (cf. Hoving, 1951; Leikola, 1985). It has bought firms and made cooperative agreements primarily with companies in other Nordic countries, and more recently in the Baltic countries (Korhonen, 1992; Kauhanen, 1993). It has also divided its production between the Nordic countries. Leaf Group has acquired companies and made cooperative agreements in North and South America,

THE EUROPEAN CONFECTIONERY SECTOR 379

Europe and China (Korhonen, 1990; Asikainen, 1993). Leaf has developed relationships with the innovative food technology companies, such as Cultor and Xyrofin (Isosaari, 1994), which can be explained by the interests of the whole HuhtamLki corporation in innovative businesses, i.e. pharmaceutical and packaging businesses (Hurri, 1994). Panda used to be a cooperative until the late 1980s with good networks within the cooperative movement; it had its own exclusive distri- bution channel, for example (cf. Kinturi, 1989; Vaalavirta, 1994).

These divisions and respective differences in company strategies may have implications for the language and vocabulary used within the largest companies and their networks. As profes- sional magazines show, a common language of manufacturing expertise, for example, is well developed within the world confectionery sector. However, due to the Swedish-speaking culture of Fazer (and the company's initial links to the Russian and French confectionery making and recipes), the earlier manufacturing experts created a manufacturing vocabulary of their own in this company. According to Fazer's manufacturing and product development management, some of this vocabulary was still in use in the 1980s. In a similar way, we may assume that innovation- related language and vocabulary is richer in Leaf Finland's networks compared to Fazer' s. Panda has probably started to enrich the language related to marketing and distribution since it became independent from the cooperative governance in 1988 (cf. Kinturi, 1989).

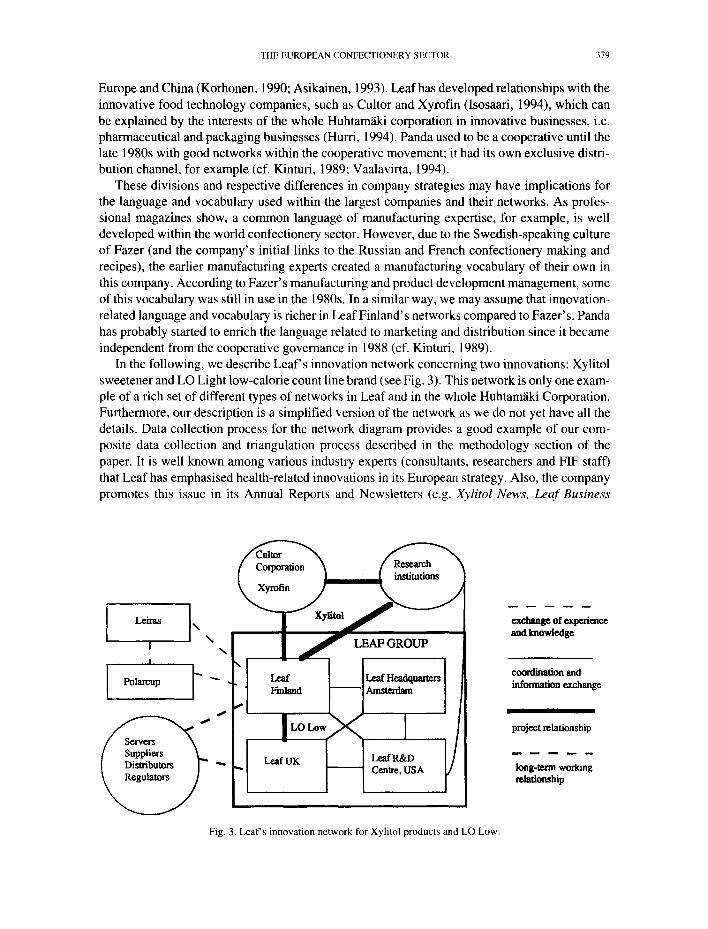

In the following, we describe Leaf's innovation network concerning two innovations: Xylitol sweetener and LO Light low-calorie count line brand (see Fig. 3). This network is only one exam- ple of a rich set of different types of networks in Leaf and in the whole Huhtam~iki Corporation. Furthermore, our description is a simplified version of the network as we do not yet have all the details. Data collection process for the network diagram provides a good example of our com- posite data collection and triangulation process described in the methodology section of the paper. It is well known among various industry experts (consultants, researchers and FIF staff) that Leaf has emphasised health-related innovations in its European strategy. Also, the company promotes this issue in its Annual Reports and Newsletters (e.g. Xylitol News, Leaf Business

-- Leaf I L~f H~dqu~ers I

Fig. 3. Leaf's innovation network for Xylitol products and LO Low.

exchange of ~xperie.ce and knowledge

coordination and informalion exchange

project relationship

long-~'m working r~.hfionship

380 P. ERIKSSON et al.

Background and Huhtamigki Review) and in public statements, such as published interviews of Leaf managers in newspapers and professional magazines. Data provided by these sources gave us an initial indication of the relevance of the issue and prompted another round of data collec- tion and triangulation from primary and secondary sources and some informal discussions with industry experts.