Embed Size (px)

Citation preview

Business Confidence Survey

July 2014

Economic Affairs and Research Division Page 2

Business Confidence Survey

Highlights

FICCI’s latest Business Confidence Survey reflects signs of rebound in the economy. A clear mandate in elections, followed by a slew of announcements undertaken by the government has lifted the spirits of industry members. However, going ahead it will be imperative to back these announcements with speedy and timely action. The Overall Business Confidence Index (OBCI) inched up 8 notches in the current survey vis-a-vis the previous round. This is the third consecutive time we have seen an increase in the confidence level. The OBCI value climbed to 69.0 in the current survey, up from 60.8 in the last survey round. An improvement was noted in both Current Conditions Index and Expectations Index. The respondents are clearly more upbeat about the near term prospects and this is true for expected performance at all the three levels – economy, industry and firm level. In fact, a whopping majority of 93% participants said that they expect the overall economic situation to be ‘moderately to substantially better’ in the coming six months.

The Union Budget is one of the most eagerly awaited exercises in India. The respondents indicated that they are looking forward to the first Union Budget of the current government. The participating companies maintained that they expect the Budget to be pro-growth giving due focus on ironing out the issues faced by the industry and investors. Some of the recommendations made by the companies participating in the survey are listed below-

Further, results pertaining to key operational parameters including sales, profits, investments, employment and exports indicated an improvement. The participating companies indicated that most of these parameters are steering towards an upturn. A discernible improvement was noted in the outlook of the respondents with regard to profits. The net response pertaining to profits jumped to 34 in the present survey, up from the corresponding figure of 4 in the previous survey round.

Key focus areas for the Union Budget 2014-15

Simplifying Taxes Implement GST as soon as possible Review Direct Tax Code Do away with retrospective taxation

Boost Infrastructure Quantum increase in infrastructure investments

Allocate greater funds for power projects

Contain Inflation Indicate development of seamless supply side infrastructure

Incentivize/Encourage states to amend and implement APMC Act

Look at a Comprehensive Agriculture policy

Contain fiscal deficit Check Subsidies Relook at MNREGA Draw up a focussed Disinvestment

Plan Promote Manufacturing Promote MSME units

Promote Skill development Enhance exports Give fresh impetus to Special

Economic Zones

Economic Affairs and Research Division Page 3

Business Confidence Survey

The investor sentiment which had taken a sharp hit in the past few quarters also seemed to be recuperating. According to the current survey results, a plunge was noted in the percentage of participating companies anticipating investments to decline in near term. About 6 percent of the respondents indicated lower investments over the next two quarters. The corresponding figure was 20 percent last time. Also, 40 percent companies said that they foresee higher investments over the next two quarters, vis-à-vis 24 percent stating likewise in the last round.

Outlook of the participating companies with regard to employment and exports also noted an improvement. The net responses pertaining to employment increased to 21 in the current survey from 6 in the last survey round. While net responses pertaining to exports increased to 35 in the present survey, the corresponding figure was 31 in the previous round.

Among the key factors affecting business prospects, weak demand was reported to be a constraining factor by a majority of respondents. Nearly 74 percent of the participating companies in the present survey pointed out that demand situation continues to be weak. In the previous survey round 70 percent companies had stated likewise. However, about 72 percent of the respondents said that they expect their order book position to recover over the next six months.

Further, the situation with regard to availability and cost of credit seems to be easing. The proportion of respondents citing availability of credit as a concern area declined to 25 percent in the present survey round from 40 percent last time. In addition, the proportion of respondents stating high cost of credit as a concern area declined for the third consecutive quarter.

Economic Affairs and Research Division Page 4

Business Confidence Survey

Survey Profile The current survey drew responses from companies with a wide sectoral and geographical spread. The survey drew responses from about 180 companies with a turnover ranging from Rs 1 crore to Rs 2,40, 000 crore. The participating companies belonged to a wide array of sectors such as textiles, cement, consultancy services, chemicals, steel and steel products, construction, food processing, electrical equipment and machinery, paper and paper products. The survey was conducted during May and June 2014. Detailed Survey Findings

Almost 50% of the participating companies indicate improvement in overall economic condition vis-à-vis last six months….

Current performance vis-à-vis the performance in last six months

*percentage of respondents

The results of FICCI’s latest Business Confidence Survey indicate an improvement in the overall situation vis-à-vis last six months. This was specifically true at the economy and industry level, with a higher proportion of respondents citing ‘moderately to substantially better’ performance compared to last two quarters. About 48 percent of the respondents reported that the overall economic situation has improved vis-a-vis last six months. This was 23 points higher than the proportion of respondents saying likewise in the last survey round. At the industry level, 34 percent of the companies indicated ‘moderately to substantially better’ performance vis-à-vis last six months. The corresponding figure in the last survey round was 23 percent. However, at the firm level the proportion of respondents citing improved performance remained the same as in the last survey. Nonetheless, a substantive decline was noted in percentage of participants reporting a worsening of situation. Further, about half of the respondents indicated no change in the

Economic Affairs and Research Division Page 5

Business Confidence Survey

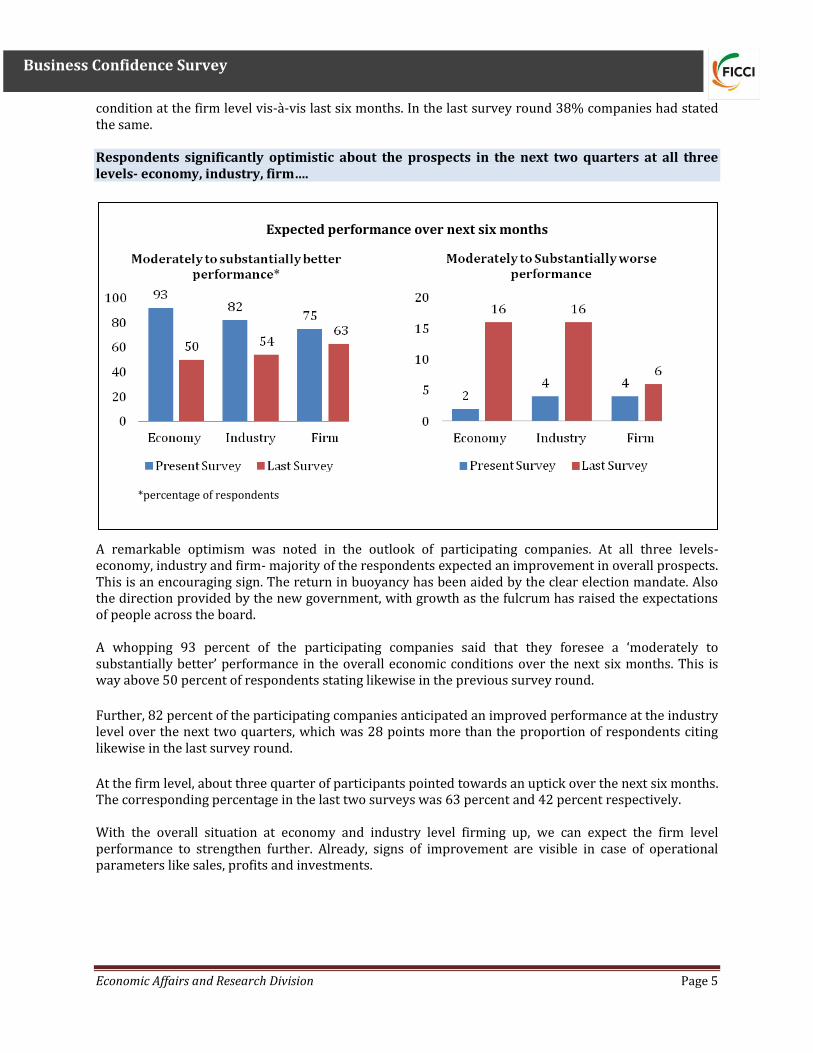

condition at the firm level vis-à-vis last six months. In the last survey round 38% companies had stated the same. Respondents significantly optimistic about the prospects in the next two quarters at all three levels- economy, industry, firm….

Expected performance over next six months

*percentage of respondents

A remarkable optimism was noted in the outlook of participating companies. At all three levels- economy, industry and firm- majority of the respondents expected an improvement in overall prospects. This is an encouraging sign. The return in buoyancy has been aided by the clear election mandate. Also the direction provided by the new government, with growth as the fulcrum has raised the expectations of people across the board. A whopping 93 percent of the participating companies said that they foresee a ‘moderately to substantially better’ performance in the overall economic conditions over the next six months. This is way above 50 percent of respondents stating likewise in the previous survey round.

Further, 82 percent of the participating companies anticipated an improved performance at the industry level over the next two quarters, which was 28 points more than the proportion of respondents citing likewise in the last survey round.

At the firm level, about three quarter of participants pointed towards an uptick over the next six months. The corresponding percentage in the last two surveys was 63 percent and 42 percent respectively. With the overall situation at economy and industry level firming up, we can expect the firm level performance to strengthen further. Already, signs of improvement are visible in case of operational parameters like sales, profits and investments.

Economic Affairs and Research Division Page 6

Business Confidence Survey

Operational Parameters: investments, profits, exports and employment seen picking up….

Operational parameters including sales, profits, investments, exports and employment which had reported deterioration in the last survey seem to have climbed back on the recovery path. The participating companies indicated that most of these parameters are steering towards an upturn.

Operational Parameters – Net Responses (Expectations over the next six months)

Note: Net responses are measured as the differential between the companies reporting positive and negative responses.

Responses indicating status quo are not reckoned

Net responses pertaining to sales rose to 62 in the present survey round. About 67 percent of participating companies said that they foresee an increase in sales in near term. The corresponding figure in the previous survey round was 56 percent. In addition, a decline was noted in the percentage of respondents expecting sales to remain same over the next two quarters or lower further. Just about 5 percent of the participants expected lower sales over next two quarters. A discernible improvement was also noted in the outlook of the respondents with regard to profits. The net response pertaining to profits jumped to 34 in the present survey round, up from the corresponding figure of 4 in the last survey. While on one hand an increase was noted in the proportion of respondents expecting profits to go up in near term, on the other, the percentage of respondents expecting lower profits witnessed a perceptible decline. The investor sentiment which had taken a sharp hit in the past few quarters seems to be recuperating. According to the current survey results, a plunge is noted in the percentage of participating companies anticipating investments to decline in near term. About 6 percent of respondents indicated lower investments over the next two quarters. The corresponding figure was 20 percent last time. Also, 40 percent companies said that they foresee higher investments over the next two quarters, vis-à-vis 24 percent stating likewise in the last round. Net response improved to 34 in the present survey from 4 in the last survey round.

Economic Affairs and Research Division Page 7

Business Confidence Survey

Prospects for next six months (All figures are in % and refer to proportion of respondents)

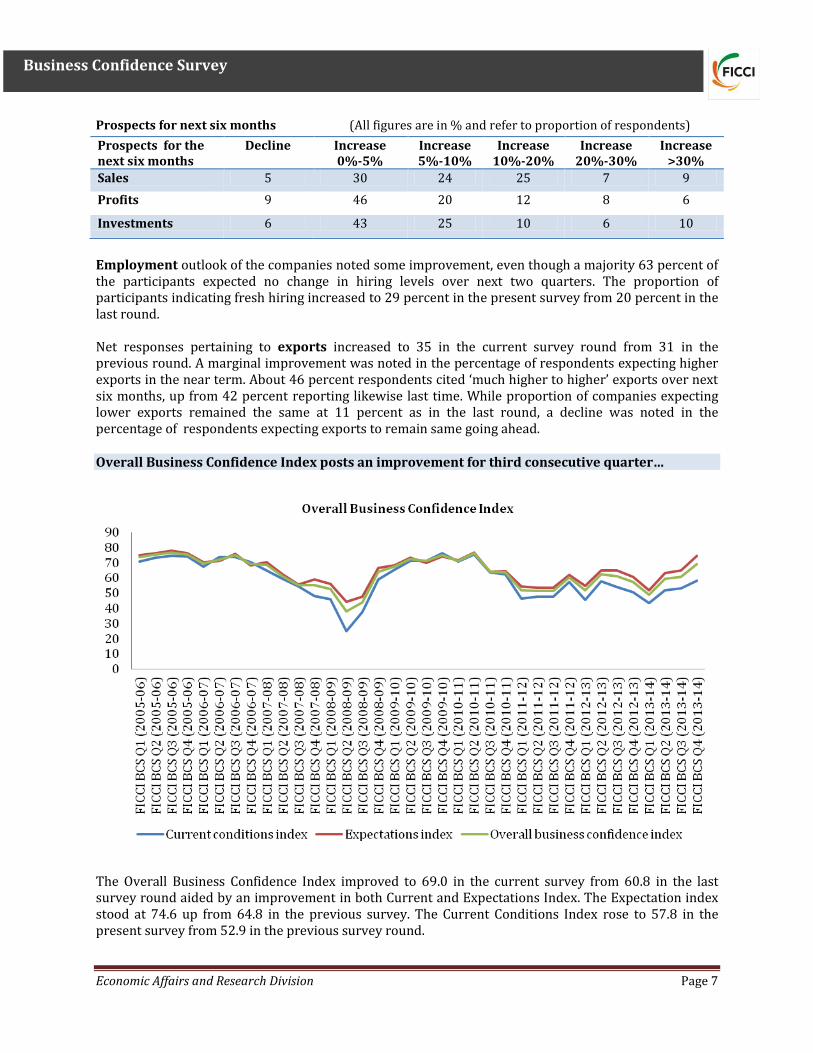

Employment outlook of the companies noted some improvement, even though a majority 63 percent of the participants expected no change in hiring levels over next two quarters. The proportion of participants indicating fresh hiring increased to 29 percent in the present survey from 20 percent in the last round. Net responses pertaining to exports increased to 35 in the current survey round from 31 in the previous round. A marginal improvement was noted in the percentage of respondents expecting higher exports in the near term. About 46 percent respondents cited ‘much higher to higher’ exports over next six months, up from 42 percent reporting likewise last time. While proportion of companies expecting lower exports remained the same at 11 percent as in the last round, a decline was noted in the percentage of respondents expecting exports to remain same going ahead. Overall Business Confidence Index posts an improvement for third consecutive quarter…

The Overall Business Confidence Index improved to 69.0 in the current survey from 60.8 in the last survey round aided by an improvement in both Current and Expectations Index. The Expectation index stood at 74.6 up from 64.8 in the previous survey. The Current Conditions Index rose to 57.8 in the present survey from 52.9 in the previous survey round.

Prospects for the next six months

Decline Increase 0%-5%

Increase 5%-10%

Increase 10%-20%

Increase 20%-30%

Increase >30%

Sales 5 30 24 25 7 9

Profits 9 46 20 12 8 6

Investments 6 43 25 10 6 10

Economic Affairs and Research Division Page 8

Business Confidence Survey

Key factors constraining growth of businesses….. First and foremost, weak demand was reported to be a constraining factor by a majority of respondents. Nearly 74% of the participating companies in the present survey round pointed out that demand situation continues to be frail and is a major concern for them. In the previous survey round 70% companies had stated likewise.

However, that said the participants also expected an improvement in their order book position over near term. About 72 percent of the respondents anticipated a better order book position over the next six months. This is considerable improvement from 46 percent companies reporting likewise in the previous round. Further, while 22 percent participants expected no change in the order book position, the remaining 6 percent anticipated worsening. Two, as pointed out in the survey, the situation with regard to availability and cost of credit seems to be easing. The proportion of respondents citing availability of credit as a concern area declined to 25 percent in the present survey round from 40 percent last time. In addition, the proportion of respondents stating high cost of credit as a concern area declined for the third consecutive quarter. In the current survey round, 47 percent of the participants felt that cost of credit was high. In the previous survey 53 percent of the participating companies had reported likewise.

Average interest rate charged by the banks on working capital and term loan

Working Capital Loan Term Loan

At present Six months

back

One year

Back

At present Six months

back

One year

back

Turnover up to 500 crore

12.9 13.1 13.0 12.3 12.8 12.6

Turnover over 500 crore

13.7 14.2 14.1 11.1 11.4 11.2

Economic Affairs and Research Division Page 9

Business Confidence Survey

Lastly, a sharp drop was noted in the proportion of respondents stating rising cost of raw materials to be a bothering factor. About 37 percent of the participants in the survey said raw material costs were a constraining factor for them. The corresponding number in the last survey was 65%. However, given the recent volatility in crude oil prices and impending tensions in Iraq, we might once again see pressure arising on raw material costs.

Top Expectations from the forthcoming Union Budget

In the present survey we asked the participants to indicate their top expectations from the forthcoming Union Budget. This Budget will be the first one for the current government and will be announced amidst high expectations. Following are some of the key suggestions/expectations put across by a majority of companies participating in the survey.

The need to simplify the existing tax structure was indicated to be a prerequisite for assuring ease of doing business. It was unanimously felt by the participants that Goods and Services Tax should be implemented as soon as possible. The respondents also pointed out that retrospective amendment in taxation is detrimental for the investment climate of the country and any such legislation should be a rare exception. The participants also indicated the need to review direct tax code. A majority of the participants said that there is a need for quantum increase in investments in infrastructure sector, be it roads, ports, airports or railways. This would have a multiplier effect on the economy and will give a push to other sectors as well. The respondents also felt that unavailability of quality power supply is a major concern for the industry. The government should allocate greater funds for power generation projects in the Budget. Inflation has been one of the key factors impeding India’s growth prospects. The participants said that it is very important to target the root cause to address the issue of inflation. Food prices have been soaring and what is required is a seamless supply side infrastructure. Also, encouraging/incentivising states to amend and implement APMC Act is imperative. It was also felt that there is a need to take a relook at the agricultural strategy. We should look at greater crop diversification and encourage food processing and ancillary industries. In fact FICCI has also suggested the need to chalk out a comprehensive agriculture policy covering production, productivity, water management, soil and seed health, market access and insurance for farmers. India’s subsidy bill has increased over time and the companies participating in the survey pointed out that we urgently need to check this trend.

Simplifying Taxes

Boost Infrastructure

Contain Inflation

Contain fiscal deficit

Economic Affairs and Research Division Page 10

Business Confidence Survey

The participants felt that increasing spend on critical sectors like education, healthcare and housing is imperative but it should be assured that the money allocated is being spent judiciously and efficiently. It was also said that the government should indicate a disinvestment plan in the forthcoming budget. The respondents also felt that the government should take a relook at MNREGA The participating companies said that giving a push to the manufacturing sector is the need of hour. The government should promote faster clearances and investments. Further, some respondents felt that MSME sector should be promoted with greater vigour. There is a need to review the MSME exemption limits and the sector should be provided finance at lower costs. Promote skill development. With a view to boost exports, participants suggested that a fresh impetus should be given to Special Economic Zones.

Promote Manufacturing

Encourage Exports

Economic Affairs and Research Division Page 11

Business Confidence Survey

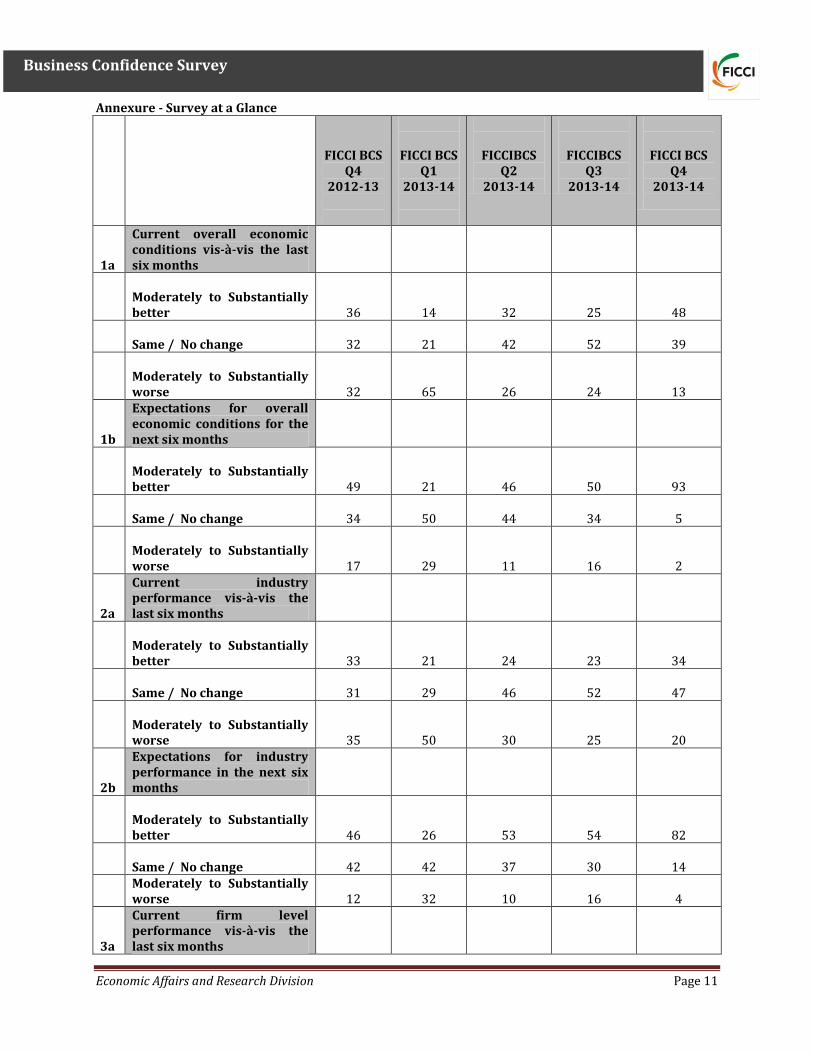

Annexure - Survey at a Glance

FICCI BCS Q4

2012-13

FICCI BCS Q1

2013-14

FICCIBCS Q2

2013-14

FICCIBCS Q3

2013-14

FICCI BCS Q4

2013-14

1a

Current overall economic conditions vis-à-vis the last six months

Moderately to Substantially better 36 14 32 25

48

Same / No change 32 21 42 52

39

Moderately to Substantially worse 32 65 26 24

13

1b

Expectations for overall economic conditions for the next six months

Moderately to Substantially better 49 21 46 50

93

Same / No change 34 50 44 34

5

Moderately to Substantially worse 17 29 11 16

2

2a

Current industry performance vis-à-vis the last six months

Moderately to Substantially better 33 21 24 23

34

Same / No change 31 29 46 52

47

Moderately to Substantially worse 35 50 30 25

20

2b

Expectations for industry performance in the next six months

Moderately to Substantially better 46 26 53 54

82

Same / No change 42 42 37 30

14

Moderately to Substantially worse 12 32 10 16

4

3a

Current firm level performance vis-à-vis the last six months

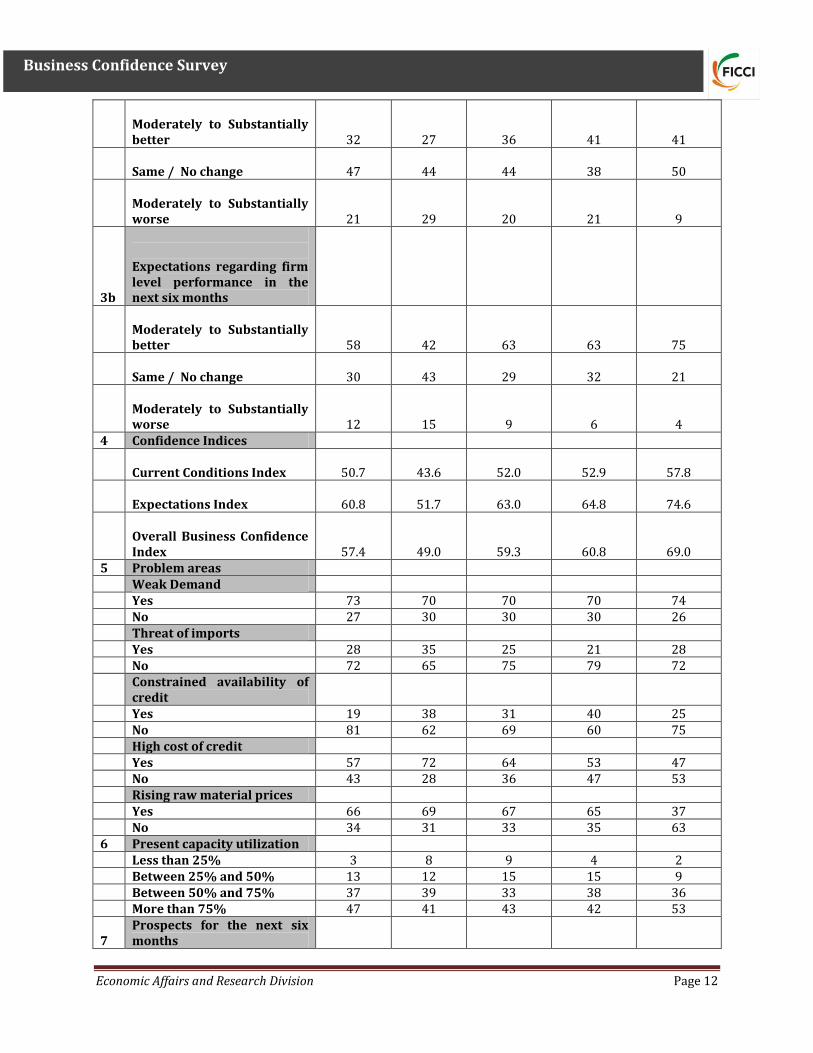

Economic Affairs and Research Division Page 12

Business Confidence Survey

Moderately to Substantially better

32

27 36 41

41

Same / No change 47 44 44 38

50

Moderately to Substantially worse 21 29 20 21

9

3b

Expectations regarding firm level performance in the next six months

Moderately to Substantially better 58 42 63 63

75

Same / No change 30 43 29 32

21

Moderately to Substantially worse 12 15 9 6

4 4 Confidence Indices

Current Conditions Index 50.7 43.6 52.0 52.9

57.8

Expectations Index 60.8 51.7 63.0 64.8

74.6

Overall Business Confidence Index 57.4 49.0 59.3 60.8

69.0 5 Problem areas

Weak Demand

Yes 73 70 70 70 74

No 27 30 30 30 26

Threat of imports

Yes 28 35 25 21 28

No 72 65 75 79 72

Constrained availability of credit

Yes 19 38 31 40 25

No 81 62 69 60 75

High cost of credit

Yes 57 72 64 53 47

No 43 28 36 47 53

Rising raw material prices

Yes 66 69 67 65 37

No 34 31 33 35 63

6 Present capacity utilization

Less than 25% 3 8 9 4 2

Between 25% and 50% 13 12 15 15 9

Between 50% and 75% 37 39 33 38 36

More than 75% 47 41 43 42 53

7 Prospects for the next six months

Economic Affairs and Research Division Page 13

Business Confidence Survey

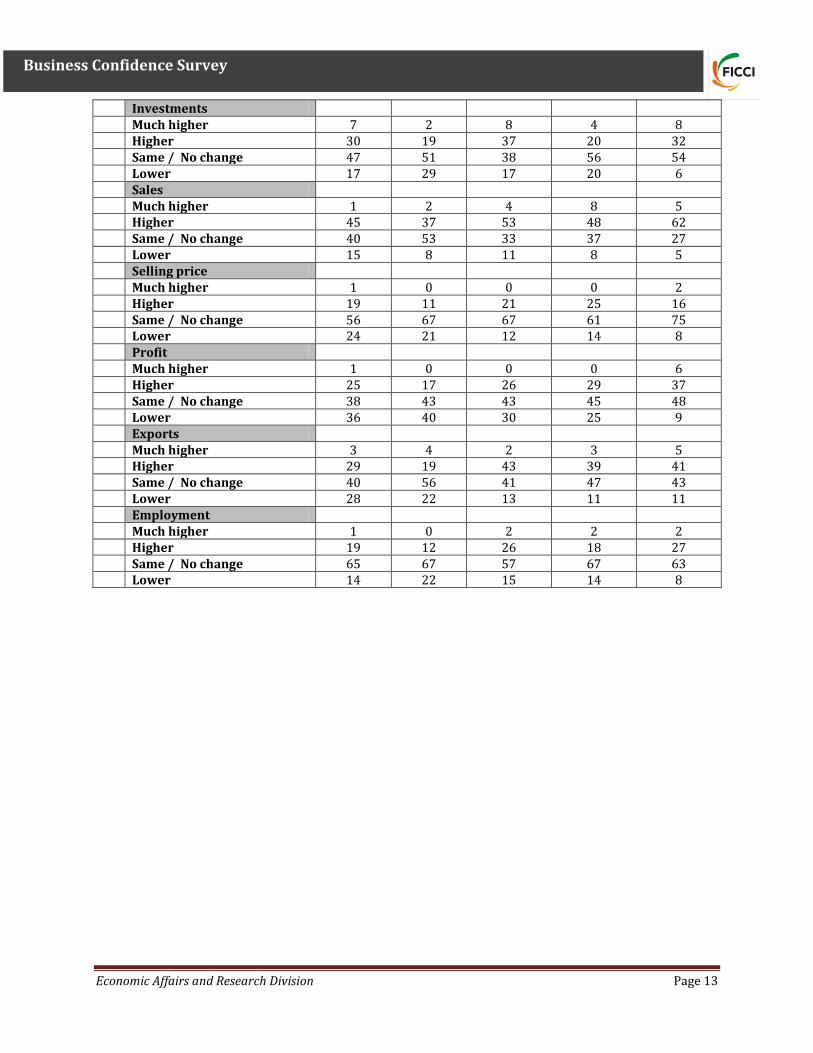

Investments

Much higher 7 2 8 4 8

Higher 30 19 37 20 32

Same / No change 47 51 38 56 54

Lower 17 29 17 20 6

Sales

Much higher 1 2 4 8 5

Higher 45 37 53 48 62

Same / No change 40 53 33 37 27

Lower 15 8 11 8 5

Selling price

Much higher 1 0 0 0 2

Higher 19 11 21 25 16

Same / No change 56 67 67 61 75

Lower 24 21 12 14 8

Profit

Much higher 1 0 0 0 6

Higher 25 17 26 29 37

Same / No change 38 43 43 45 48

Lower 36 40 30 25 9

Exports

Much higher 3 4 2 3 5

Higher 29 19 43 39 41

Same / No change 40 56 41 47 43

Lower 28 22 13 11 11

Employment

Much higher 1 0 2 2 2

Higher 19 12 26 18 27

Same / No change 65 67 57 67 63

Lower 14 22 15 14 8