Embed Size (px)

Citation preview

Strictly Confidential. For Team Members’ use only.

Business & Investment Guidance-April’2011

Branch Channel Business Group

Page 2Strictly Confidential. For Team Members’ use only.

Most Important Message from our Vice Chairman and MD’s OfficeDear Team members

Heartiest congratulations on India winning 'World Cup'. Indeed it was a glorious and much awaited victory.

Friends wish you a very happy 'New Financial year 2011-12'. As always, last financial year was an eventful year - full of leanings. We initiated lot of new practices in 2010-11 to move towards our Vision 2013. Few of them are :

· Bottom up approach by introducing 'Game Plan' targets· Financial Planning 'version 2'· Launch of 'Daily Activity Report'- DAR Platform· 3 by 3 Client/Volume Matrix to track business· 'Personal Aspiration' of all Sales team members· Chairman's Club· 'Client Search Engine'and many more..............................

The clear objective of these processes are, to not only realize your full potential but to help you grow into COMPLETE FINANCIAL PLANNERS.

Friends, in last 3 month of financial year 2010-11, I was able to connect with most of the team members on 'Ground'. After taking lot of inputs from 'YOU', we now have now a 'ear to ground' action plan for this year. I am confident with your wholehearted participation, we will set new benchmarks of Client Satisfaction and resultant Business Performance this year.

We take inspiration from Coca Cola brand , who had once 10-15 years lost way and were in risk of losing their No. 1 spot to Pepsi. What was wrong ? They had changed their original, 1935 formula too many times and consumers were losing connect with the brand. Solution ? Go back to original 1935 Coke formula and brand it as 'Coke Classic'- results were phenomenal, consumers immediately 'reconnected' with the brand and they regained their leadership position

Page 3Strictly Confidential. For Team Members’ use only.

BAJAJ CAPITAL CLASSIC

Time has come for us to launch 'Bajaj Capital Classic' by reverting to the 'original formula' that made our company successful in first place. We were a simple one product company but still following Financial Planning approach. We were catering to a basic need of society of 1960s and 70s- higher return than Bank with adequate safety. Each team member was Volume focused doing Rs 40-50 lacs FD Volume per month through 125-150 transactions from 50-60 clients each. We had respect of companies and used to command premium rates (a lot of it used to come back as rewards and incentives for team.

Bajaj Capital of today is catering to a young- urban population in age group of 30-45 besides older generation of clients comprising of pre-retirees and retirees.

While needs of older generation remain same as above. This young breed is very unique combination of traditional and modern. Their aspiration is to get a taste of India Growth Story without taking undue risks. DO WE HAVE ANY PRODUCTS TO CATER TO ASPIRATION OF THIS CLASS ? We believe we have ideal products in form of Capital Protection for this audience where 85% of your money gives you Bank FD returns, 7%+ post tax and 15% of your money gives you a flavor of markets and potentially 3-4% higher return giving a total return of 11-12% which is just right to meet Financial Goals like Child's Future, Retirement. If someone has a 2-5 year horizon they can choose products from Mutual Fund stable and if the goal is 5-10 years away, they can take same product from Life Insurance platform.

If we go by simple, Bajaj Capital Classic sales process- a team member can achieve 40-50 lacs p.m Volume in MF Capital Protection and 10 lacs p.m Volume new generation Capital Protection plans in ULIP platform. Just these two products can generate following Revenue per team member;

MF CPOF- 40 lacs * 3% = 1.2 lacsLI CPOF- 10 lacs * 12% = 1.2 lacsTOTAL- 2.4 lacs p.m just from these two Product lines vis a vis 1.1 lac average needed to achieve JFM 2011 target from a confusing range of 0+ products presently !

This, of course, is a simplistic example and does not include crucial Financial Planning products like Mutual Fund SIP, Health Insurance, Term Insurance, Traditional Plans, FMPs, Fixed Deposits which cater to needs of a wider set of investors.

Page 4Strictly Confidential. For Team Members’ use only.

What I am saying is that a FOCUS on 8 odd products which gives a team member 80% of his Margin. Balance 20% margin can come from 50 odd other products.

LONG TERM SIP

This will work in conjunction with a Long Term SIP Development Plan where every branch will SIP (SIMPLY IMPLEMENT PLAN) of 50 new SIPs each month and each ANG active Adviser giving 5 SIPs each month. At an average of Rs 2600 per SIP, we will add some Rs 450 cr Equity AUM each year. When we stick to this Plan for 3 years, in the 4th year our Trail will be Rs 4.5 cr from MF SIP itself.

SIPs will contribute to our current year Strategy also because its a great communication starter and helps us stay in monthly touch with clients giving them an opportunity to pitch second, third and Fourth product. We should make it a rule- "ONLY A PERSON WHO HAS SIP THROUGH US IS CONSIDERED A CLIENT".

We should make the term of SIP perpetual so team members don't have to repeat the hard work time and again. We have tested that some of the most successful new Advisers have become successful due to SIP strategy.

POWER OF FINANCIAL PLANNING

In last four months of financial year 2011-12, we have sacrificed current Revenue for future Revenue by focusing on 80CCCF Bond issues. What these issues have given us in turn is a 'RIPE' client base of 30,000 new highest tax bracket investors in the age group of 35-45 ready to be harvested. Imagine we are able to implement a Financial Plan for each of these clients- we would generate a whopping Rs 45 cr Revenue (30,000 * 15,000 average Financial Planning margin per client). This would result in a profit of Rs 25 cr in Q1 itself. How do we get our team to step up Financial Planning implementation ? I believe its a combination to Training and Reward.

We need to restart Case Study based training where teams come together and 'role play' Financial Planning pitches to clients. In Rewards, I like the idea of 20% Bonus incentives on implementation of 4/4 clients on audited Financial Plan which has been verified over phone for Client satisfaction.

MOTOR PLANGI Team's plan to collect database of all active clients' car insurance details is a great one. Motor Insurance is a great way to build relationship with client. Only this plan itself can get us more GI Margin than all GI products put together last year if we manage to insure 30,000 of 82,000 active clients who transacted through us last year

Page 5Strictly Confidential. For Team Members’ use only.

CLIENT ENGAGEMENT

We all know our real mantra for success is 'CROSS SELL'- how can we add second, third and fourth products into a clients' portfolio ? We now have tools like Financial Planning version 2.0, Portfolio Review and now Client Search Engine which empower a team member to study gaps in Client Portfolio and make them suitable recommendations. Its like the good old days when Renewals were an icing on the cake of fresh deposits.While we empower our teams to 'keep in touch' with clients- its important that we directly engage clients also. We will launch our much awaited INVESTORS CLUB were clients will be engaged on Four Pillars of- Be Informed, Plan, Insure, Invest and Refer. Our aim is to involve Clients in the process of securing their future and achieve 4/4 client portfolios by engaging them. Team Members helping us in this endeavor will earn extra rewards.

FINANCIAL PLANNING PACKAGESMany of our clients are now looking for 'ready made' Portfolios which they can buy and don't have to exercise their own mind in selection and regular re- shuffling from time to time. In a snap survey in Coimbatore HNI investors conference recently- 35 of 70 Clients' present polled that they would consider investing in a Model Portfolio if fees structure is reasonable. This would be a new step in positioning of brand Bajaj Capital- this resonates with our very first positioning of Retire and Prosper, Make your Children Lakhpati which we used in 60s and 70s and offered fulfillment of these needs through Company FDs. We will initially launch Mutual Fund scheme based Portfolios but will go on too add ULIPs, Fixed Income, Health Insurance in due course. We are ready to roll out Model Portfolios from April 1, 2011.

So what I want from you are your ideas on following points :· Can you do 40 lacs MF CPOF and 10 lacs LI CPOF ?· Can you Implement 15 financial plan per/mth with average revenue of 15000/- ?· Can you Sell Motor Insurance to your existing clients ?· Can you Implement Financial Plan for new clients acquired in 80CCCF bonds ?· Can you do 50 MF Perpetual SIPs per month ?

Send your responses directly to me on my email id [email protected].

Page 6Strictly Confidential. For Team Members’ use only.

We will work on a 'SPIRIT OF EXCELLENCE' in all areas. Remember you may heat up the water to 211 degrees F but it will still not release steam. Take it up to 212 degree F and water will boil. What is the lesson for us here ? We all work super hard but we need to that 1 degree extra this year to reach the 'boiling point' of performance. Remember even at at 90% target achievement your Branch contributes ZERO profit to company and all of us lose our Rewards in turn ( incl. me on my dividend as a shareholder in the company).

Dear team members let's work together & realize our full potential. Nothing less than 100% is going to satisfy us.

All the best and God speed !

Rajiv Deep Bajaj

Vice Chairman & Managing Director

Page 7Strictly Confidential. For Team Members’ use only.

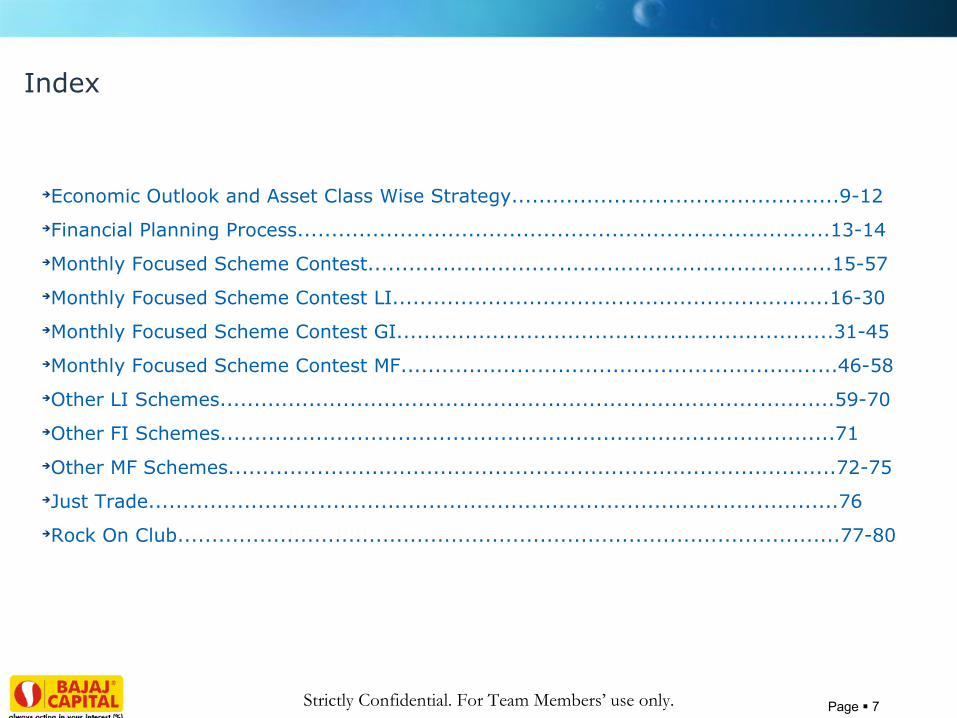

Index

➔Economic Outlook and Asset Class Wise Strategy................................................9-12

➔Financial Planning Process..............................................................................13-14

➔Monthly Focused Scheme Contest....................................................................15-57

➔Monthly Focused Scheme Contest LI................................................................16-30

➔Monthly Focused Scheme Contest GI................................................................31-45

➔Monthly Focused Scheme Contest MF................................................................46-58

➔Other LI Schemes..........................................................................................59-70

➔Other FI Schemes..........................................................................................71

➔Other MF Schemes.........................................................................................72-75

➔Just Trade.....................................................................................................76

➔Rock On Club.................................................................................................77-80

Page 8Strictly Confidential. For Team Members’ use only.

Economic Outlook

- Asset Class wise Strategy

Page 9Strictly Confidential. For Team Members’ use only.

Econ

omy

Economic Outlook

Economic growth remained robust in the 3rd quarter of FY11 coming in at 8.2% after back to back growth of 8.9% in the first two quarters of this fiscal. However, going ahead, Indian economy is likely to see a mid-cycle moderation in growth on the back of high inflation and rising interest rates as they impact consumption as well as investment sentiments. While high inflation and interest rates have already started impacting consumption, investment growth is still far from being robust as seen from the low growth in output of capital goods. Government spending, another contributor to growth is also likely to remain restrained going ahead amid worries on the high fiscal deficit. The target real growth rate of 9% for 2011-12 thus seems difficult to be met. RBI, in its mid-quarter review of monetary policy on March 17, 2011, raised repo and reverse repo rates by 0.25% each, largely in line with expectations. The policy stance remained hawkish with RBI focusing primarily on controlling inflation amid concerns over the structural nature of inflation and fears that high food inflation might already be spilling over to wages and price of manufactured products. Though RBI admitted that monetary policy has limited impact in controlling structural food inflation, it nevertheless hinted that interest rate hikes might continue simply to contain the feared spillover or generalization of food inflation. Meanwhile, industrial growth continued to remain weak in Jan 2011 coming in at 3.7%, even though core sector growth remained unusually robust at approx. 7%. Other indicators of industrial and service sector activity such as growth in indirect tax collections mainly excise duty, bank non-food credit growth, manufacturing PMI, etc however continued to expand, as per the RBI. The silver lining was however the revision in RBI's target for current account deficit for 2010-11 from 3.5% to 2.5% on the back of an expected surge improvement in net exports. Meanwhile, primary article inflation including food and non-food inflation continued to remain stubbornly high, raising fears that interest rates might continue to harden for some time. Liquidity deficit in the banking system continued to ease in March with the daily average coming in at Rs. 52000Cr as compared to Rs. 76000Cr in Feb 2011 and 94000cr in Jan 2011. It is expected to continue easing in April as government spending starts and money comes back into the banking system after the financial year end. The April – June period is traditionally an easy liquidity period in a year.

Econ

omy

Equi

ty

Last month we had revised our outlook on equities from 'Underweight' to 'NEUTRAL' expecting a range bound movement in markets in the near term and that time was ripe to start accumulating stocks over the next 3-4 months. This was based on our view that equity market valuations had fallen in line with long term averages, the Union Budget had been better than expected and the fact that most of the negatives were priced into stock prices. Since then, major stock indices have actually gone up by 8-9% in the month of March 2011. While in the near term, there might be some profit booking in the markets, we believe that time is still ripe to keep accumulating stocks with a long term horizon by investing in select diversified equity fund schemes by way of SIP and/or STP.

Page 10Strictly Confidential. For Team Members’ use only.

Economic Outlook Contd…..

Equi

ty

After the recent upside, Sensex is now trading at more than 16 times its expected FY12 EPS. Valuations have thus moved into the fair value plus zone relative to the expected earnings growth of 15%. Macro economic fundamentals categorized by high inflation, large deficits, rising interest rates and slowing growth still do not support a singular bull run in Indian equities. We believe Indian equities will continue to trade in a range bound manner before starting the next leg of the bull run, thereby giving an opportunity to long term equity investors. Going ahead, corporate earnings for the fourth quarter of FY11, due in April, is likely to provide the trigger for FY12 earnings upgrade or downgrade thereby giving short term direction to the markets. We expect them to remain largely in line with expectations with a few negative surprises. Oil prices continue to remain uncomfortably high and might pose a key risk in the near term. We thus maintain our NEUTRAL outlook on Equities without ruling out some profit booking in the near term.

Deb

t

Long Term Debt: 10 year g-sec yields continued to hover above 8% levels (8.13% G-Sec, 2022) after the borrowing plan for the first half of the fiscal was announced. High inflation and fears of rise in the borrowing program are likely to restrict downside in yields whilst continuing to put upward pressure in the near term. Any further rise in oil prices or even if they remain at these levels for sometime can be detrimental for bonds. We expect 10 year g-sec yields to remain range bound between 7.8% - 8.5% in the near term. As such, the risk reward is not favorable for investing in long term debt funds at this point in time. Hence, we remain UNDERWEIGHT on market linked long term debt instruments.

Short Term Debt: One year bank CD rates continue to rule near the 10% mark, though they have moderated slightly from levels of 10.25% in February. Even the 3 month and 6 month Bank CDs are available at yields in excess of 9.5%. This has resulted in a spread of 300-350 bps between overnight rates and 6 month / 1 year rates, which is not sustainable. Moreover, the period of April-June is traditionally an easy liquidity period as lot of government spending comes during this period. We expect short term yields to moderate from the present levels over the next quarter as liquidity eases in the system. This should lead to mark to market gains from short term debt funds and thereby enhance their returns. Select Short term debt funds today are carrying a portfolio yield between 9.5-10.0% p.a. with average maturity of 1-1.2 years and duration of less than 1 year. This presents a very attractive risk-reward as compared to long term debt funds. Hence, we remain OVER WEIGHT on short term debt funds with an investment horizon of at least six months.

Page 11Strictly Confidential. For Team Members’ use only.

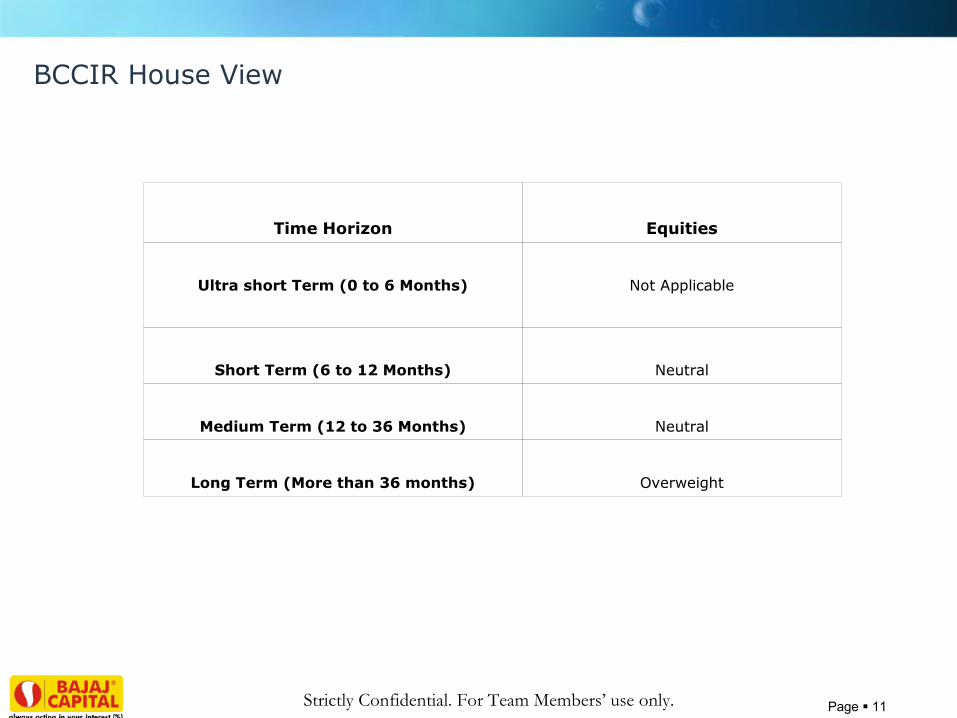

Time Horizon Equities

Ultra short Term (0 to 6 Months) Not Applicable

Short Term (6 to 12 Months) Neutral

Medium Term (12 to 36 Months) Neutral

Long Term (More than 36 months) Overweight

BCCIR House View

Page 12Strictly Confidential. For Team Members’ use only.

Long Term Debt Funds – Underweight – either avoid or restrict exposure to 25% of the debt portfolio with a minimum 1.5-2 years investment horizon Short Term Debt Funds – Overweight – exposure should be between 75-100% of debt portfolio depending upon risk appetite of investor

Equity

Investment Strategy

Debt

Gold

We maintain our NEUTRAL stance on Gold. Gold is an excellent portfolio insurance against financial crises and currency depreciation. However, we believe that with real interest rates likely to move upwards, returns from Gold should not be much different than debt. We recommend a 5-7% exposure to Gold in every portfolio by way of a mix of Gold ETFs and Gold Funds (such as the Reliance Gold Savings Fund). .

In terms of investment strategy for equities, investors should invest in equities through Systematic Transfer Plans (STPs) over the next 3-4 months. One can also put in lumpsum amounts on dips of 7-8% from these levels. Focus should be on pure large cap or flexicap funds. Infrastructure sector seems particularly attractive after the budget and in light of the fact that after the recent correction, the valuation of infrastructure related stocks has also turned attractive.

Recommended Sub-Asset Allocation in equities - Large Cap Funds: 50%; Flexicap funds: 20%; Infrastructure funds: 10%; Value Style funds: 20%

Page 13Strictly Confidential. For Team Members’ use only.

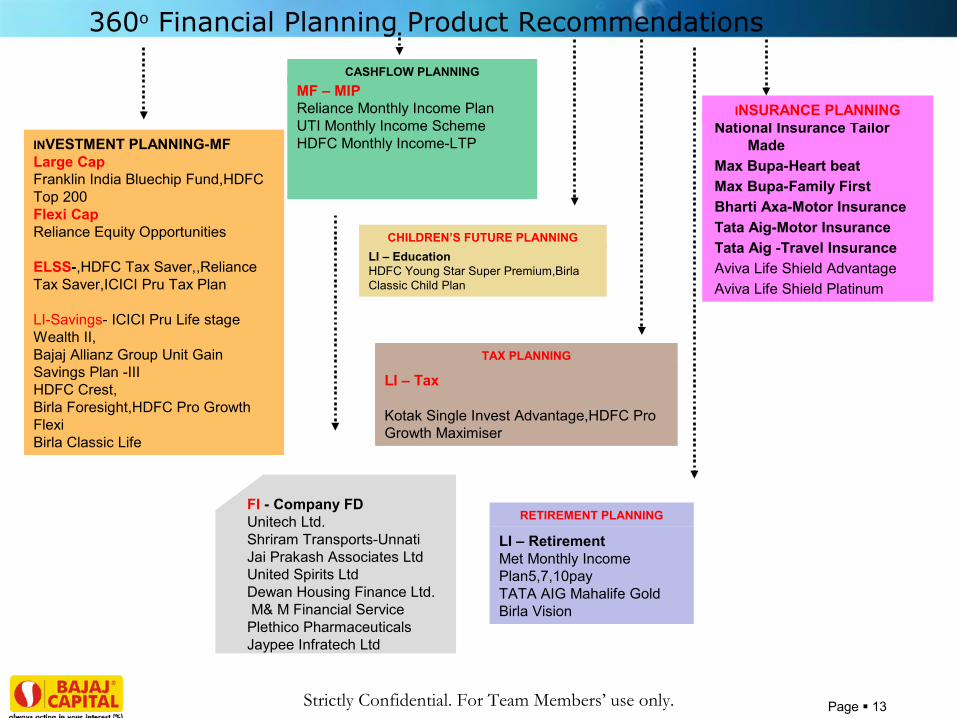

RETIREMENT PLANNING

LI – RetirementMet Monthly Income Plan5,7,10payTATA AIG Mahalife GoldBirla Vision

FI - Company FDUnitech Ltd.Shriram Transports-UnnatiJai Prakash Associates LtdUnited Spirits LtdDewan Housing Finance Ltd. M& M Financial ServicePlethico PharmaceuticalsJaypee Infratech Ltd

LI – Tax

Kotak Single Invest Advantage,HDFC Pro Growth Maximiser

TAX PLANNING

INVESTMENT PLANNING-MFLarge CapFranklin India Bluechip Fund,HDFC Top 200Flexi CapReliance Equity Opportunities

ELSS-,HDFC Tax Saver,,Reliance Tax Saver,ICICI Pru Tax Plan

LI-Savings- ICICI Pru Life stage Wealth II,Bajaj Allianz Group Unit Gain Savings Plan -IIIHDFC Crest,Birla Foresight,HDFC Pro Growth FlexiBirla Classic Life

CHILDREN’S FUTURE PLANNINGLI – Education HDFC Young Star Super Premium,Birla Classic Child Plan

MF – MIP Reliance Monthly Income PlanUTI Monthly Income SchemeHDFC Monthly Income-LTP

CASHFLOW PLANNING

National Insurance Tailor Made

Max Bupa-Heart beatMax Bupa-Family FirstBharti Axa-Motor InsuranceTata Aig-Motor InsuranceTata Aig -Travel InsuranceAviva Life Shield AdvantageAviva Life Shield Platinum

INSURANCE PLANNING

360o Financial Planning Product Recommendations

Page 14Strictly Confidential. For Team Members’ use only.

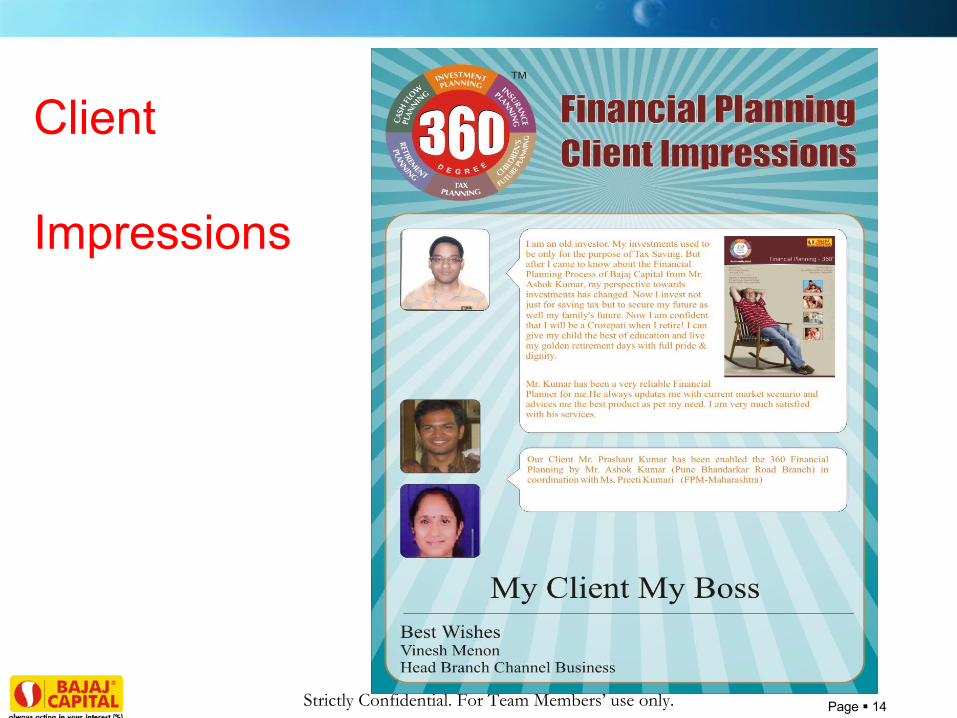

Client Impressions

Client Impressions

Page 15Strictly Confidential. For Team Members’ use only.

Monthly Focused Schemes Contest

Page 16Strictly Confidential. For Team Members’ use only.

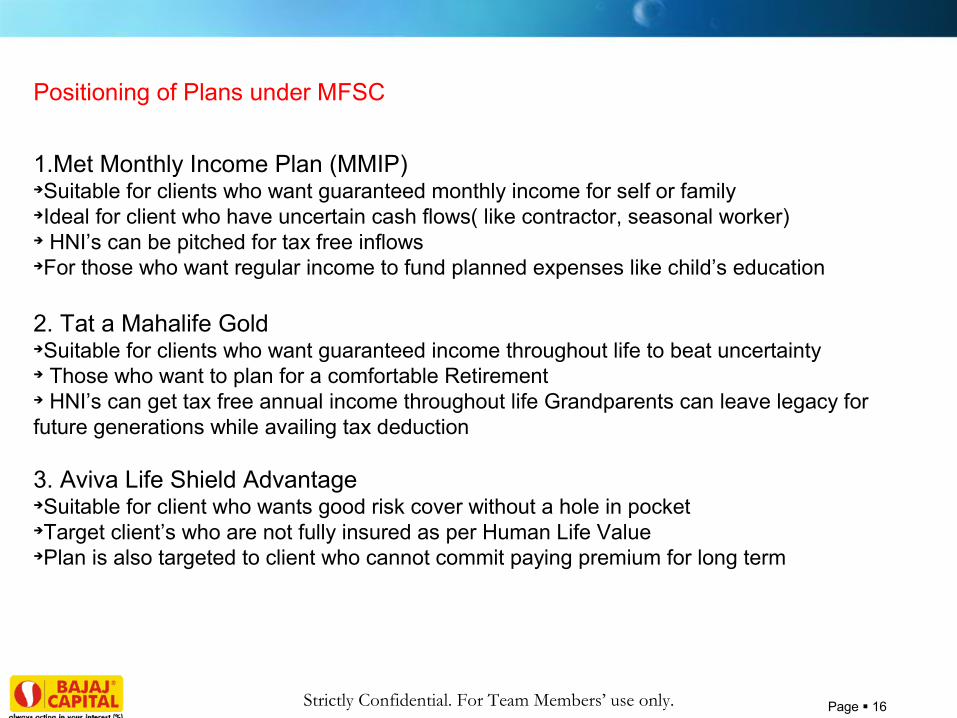

1.Met Monthly Income Plan (MMIP)Suitable for clients who want guaranteed monthly income for self or familyIdeal for client who have uncertain cash flows( like contractor, seasonal worker) HNI’s can be pitched for tax free inflowsFor those who want regular income to fund planned expenses like child’s education

2. Tat a Mahalife GoldSuitable for clients who want guaranteed income throughout life to beat uncertainty Those who want to plan for a comfortable Retirement HNI’s can get tax free annual income throughout life Grandparents can leave legacy for future generations while availing tax deduction

3. Aviva Life Shield AdvantageSuitable for client who wants good risk cover without a hole in pocketTarget client’s who are not fully insured as per Human Life ValuePlan is also targeted to client who cannot commit paying premium for long term

Positioning of Plans under MFSC

Page 17Strictly Confidential. For Team Members’ use only.

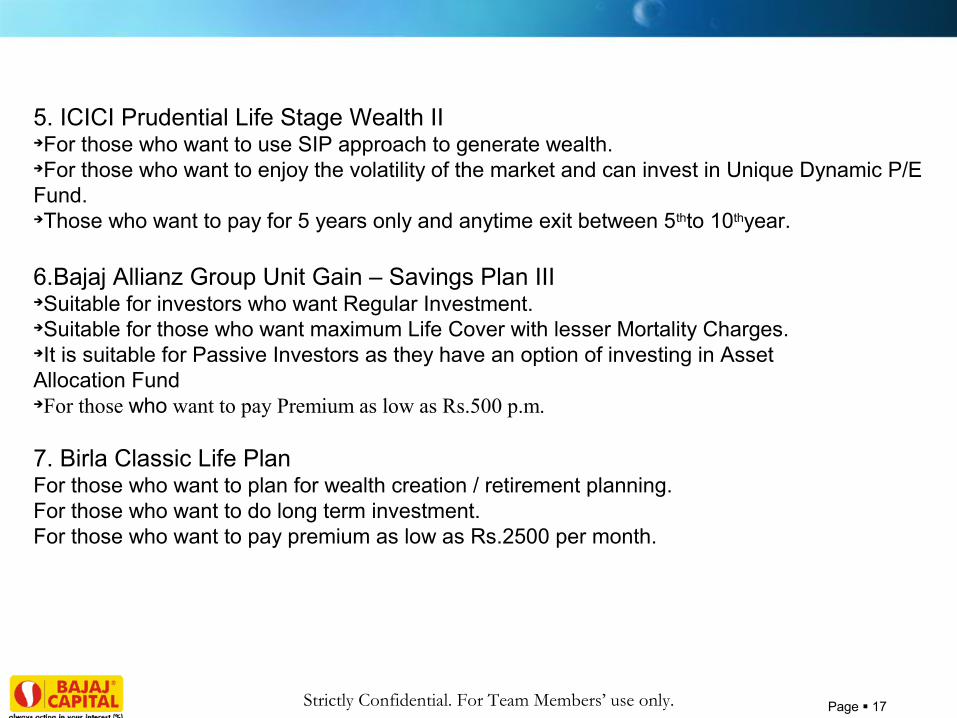

5. ICICI Prudential Life Stage Wealth IIFor those who want to use SIP approach to generate wealth.For those who want to enjoy the volatility of the market and can invest in Unique Dynamic P/E Fund.Those who want to pay for 5 years only and anytime exit between 5thto 10thyear.

6.Bajaj Allianz Group Unit Gain – Savings Plan IIISuitable for investors who want Regular Investment.Suitable for those who want maximum Life Cover with lesser Mortality Charges.It is suitable for Passive Investors as they have an option of investing in AssetAllocation FundFor those who want to pay Premium as low as Rs.500 p.m.

7. Birla Classic Life PlanFor those who want to plan for wealth creation / retirement planning.For those who want to do long term investment.For those who want to pay premium as low as Rs.2500 per month.

Page 18Strictly Confidential. For Team Members’ use only.

8.HDFC Pro Growth MaximiserA Single Premium Plan with tax free maturity benefits (in case of 5 times risk cover).For Clients looking for Debt + Returns i.e. who are looking for equity linked returns subject to a minimum guarantee. For HNI’s who want equity exposure along with capital protection, who are very conservative and who doesn't want to play with capital while looking for inflation adjusted returns.For those investors who understand the dynamics of equity & debt market and who like to take the market opportunity by switching the money aggressively between equity & debt.

9.Kotak Single Invest AdvantageA tax free Single Premium Plan with 1.25 times of Risk Cover from 2nd year.To be positioned with Classic Opportunity Fund & Dynamic Floor Fund II to the investors.

Page 19Strictly Confidential. For Team Members’ use only.

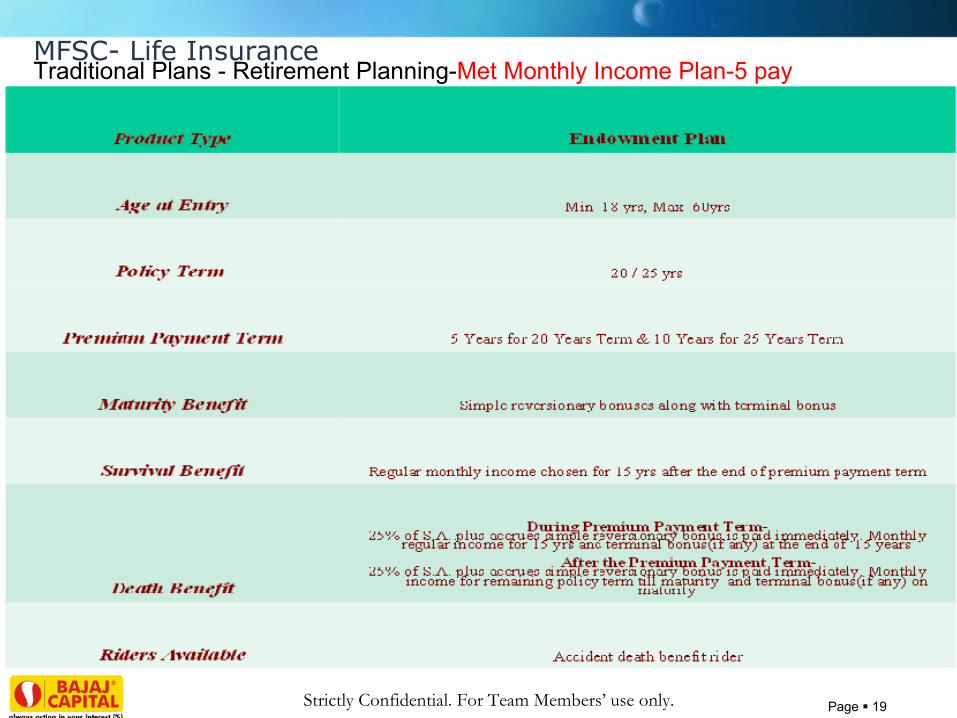

MFSC- Life InsuranceTraditional Plans - Retirement Planning-Met Monthly Income Plan-5 pay

Page 20Strictly Confidential. For Team Members’ use only.

Tata AIG Mahalife Gold

Product Type Endowment - Whole Life

Age at Entry Min- 30 days ; Max- 60

Policy Term Whole life

Maturity Benefit Sum Assured

Survival BenefitAnnual Cash Div (Based on co. performance). from 6th policy anniversary onwards, Guaranteed annual cash payment of 5%

of S.A. from 10th policy anniversary onwards.

Death Benefit Sum Assured

Riders AvailableAccident Benefits, Disability Benefits, Term Benefits or

Critical Illness benefits to this plan at nominal extra cost. Also Payor Benefit rider for juvenile cases

Page 21Strictly Confidential. For Team Members’ use only.

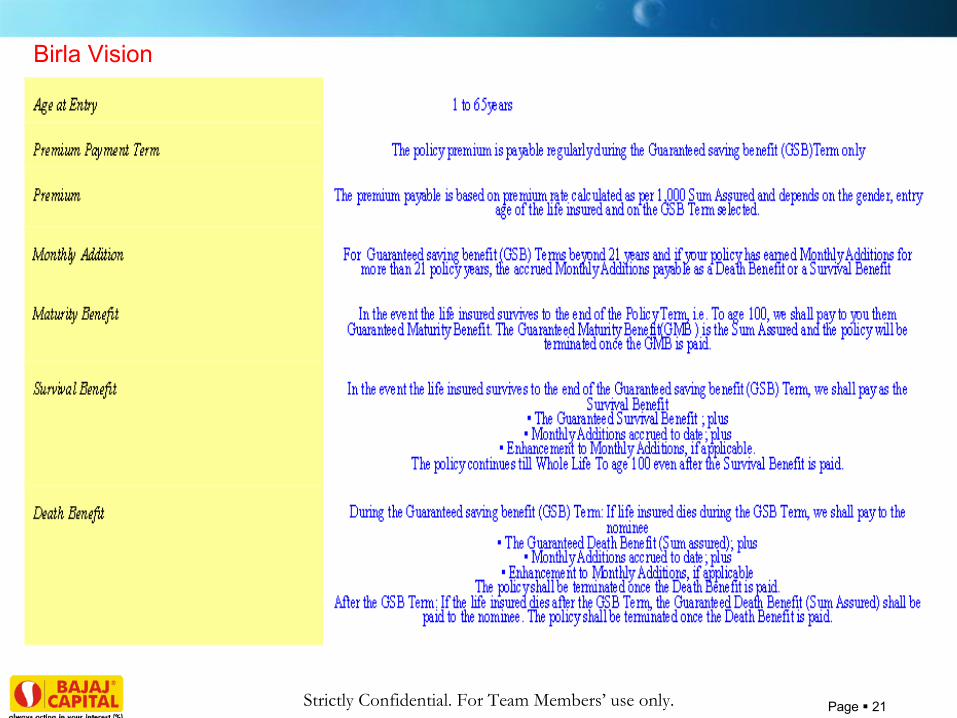

Birla Vision

Page 22Strictly Confidential. For Team Members’ use only.

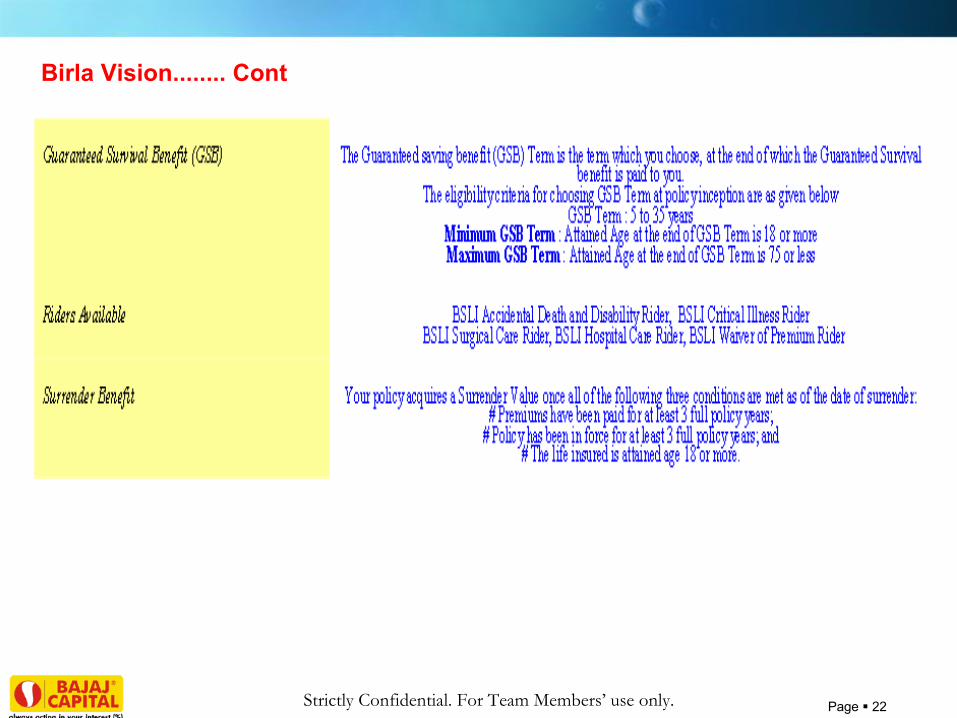

Birla Vision........ Cont

Page 23Strictly Confidential. For Team Members’ use only.

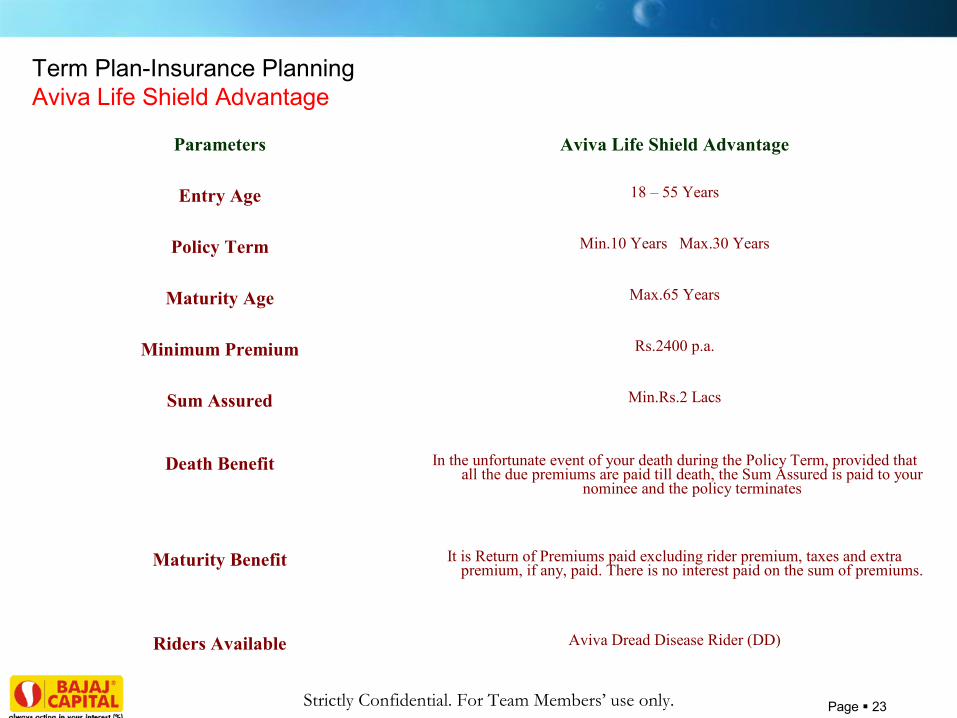

Term Plan-Insurance Planning Aviva Life Shield Advantage

Parameters Aviva Life Shield Advantage

Entry Age 18 – 55 Years

Policy Term Min.10 Years Max.30 Years

Maturity Age Max.65 Years

Minimum Premium Rs.2400 p.a.

Sum Assured Min.Rs.2 Lacs

Death Benefit In the unfortunate event of your death during the Policy Term, provided that all the due premiums are paid till death, the Sum Assured is paid to your

nominee and the policy terminates

Maturity Benefit It is Return of Premiums paid excluding rider premium, taxes and extra premium, if any, paid. There is no interest paid on the sum of premiums.

Riders Available Aviva Dread Disease Rider (DD)

Page 24Strictly Confidential. For Team Members’ use only.

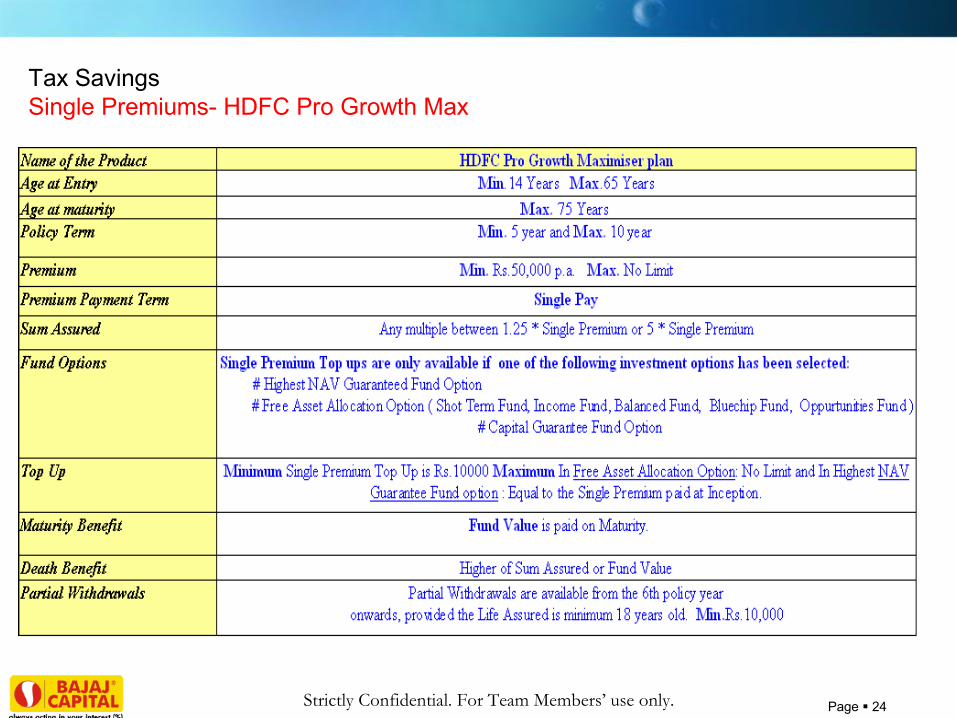

Tax SavingsSingle Premiums- HDFC Pro Growth Max

Page 25Strictly Confidential. For Team Members’ use only.

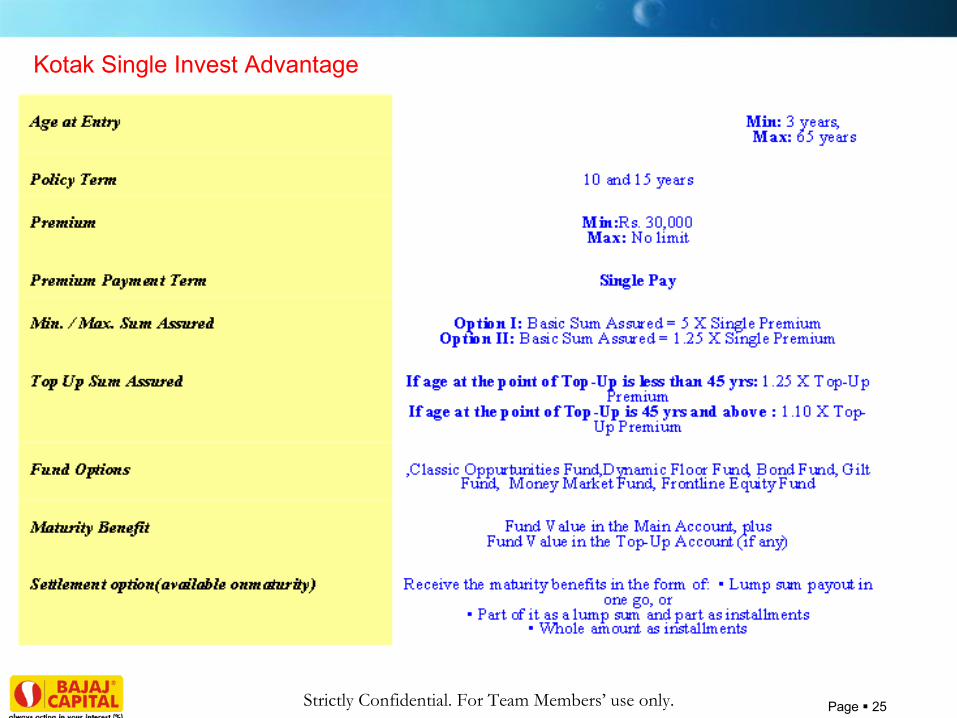

Kotak Single Invest Advantage

Page 26Strictly Confidential. For Team Members’ use only.

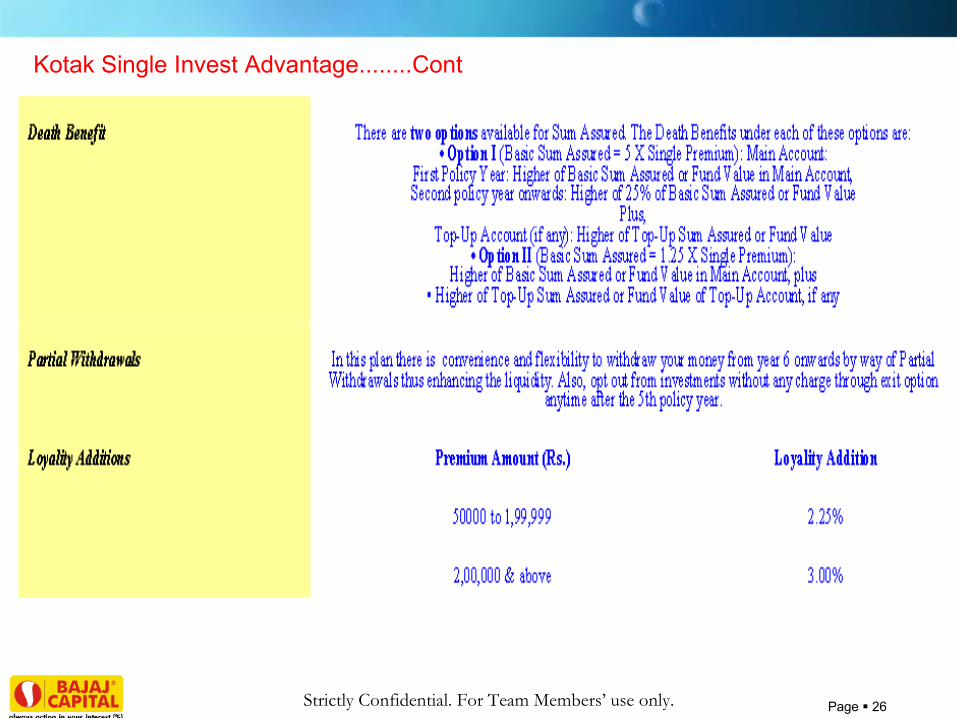

Kotak Single Invest Advantage........Cont

Page 27Strictly Confidential. For Team Members’ use only.

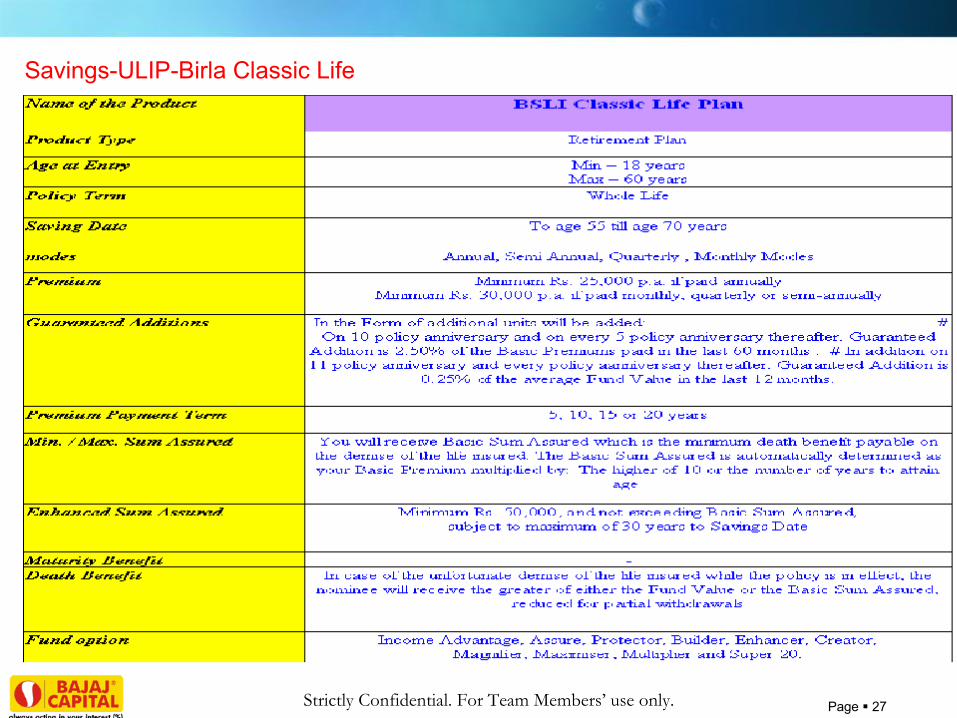

Savings-ULIP-Birla Classic Life

Page 28Strictly Confidential. For Team Members’ use only.

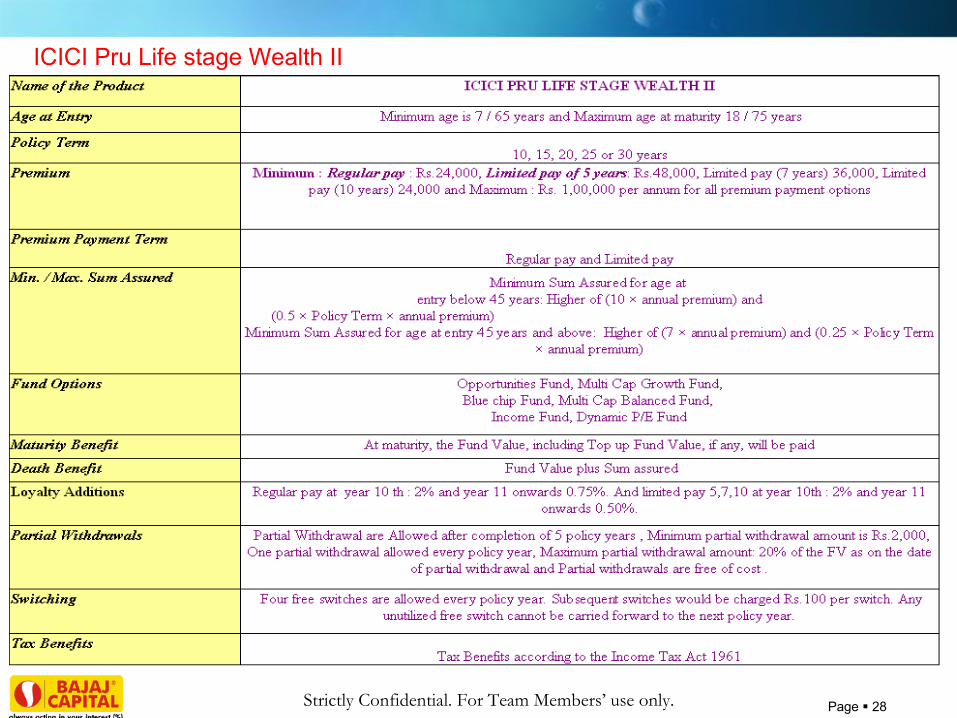

ICICI Pru Life stage Wealth II

Page 29Strictly Confidential. For Team Members’ use only.

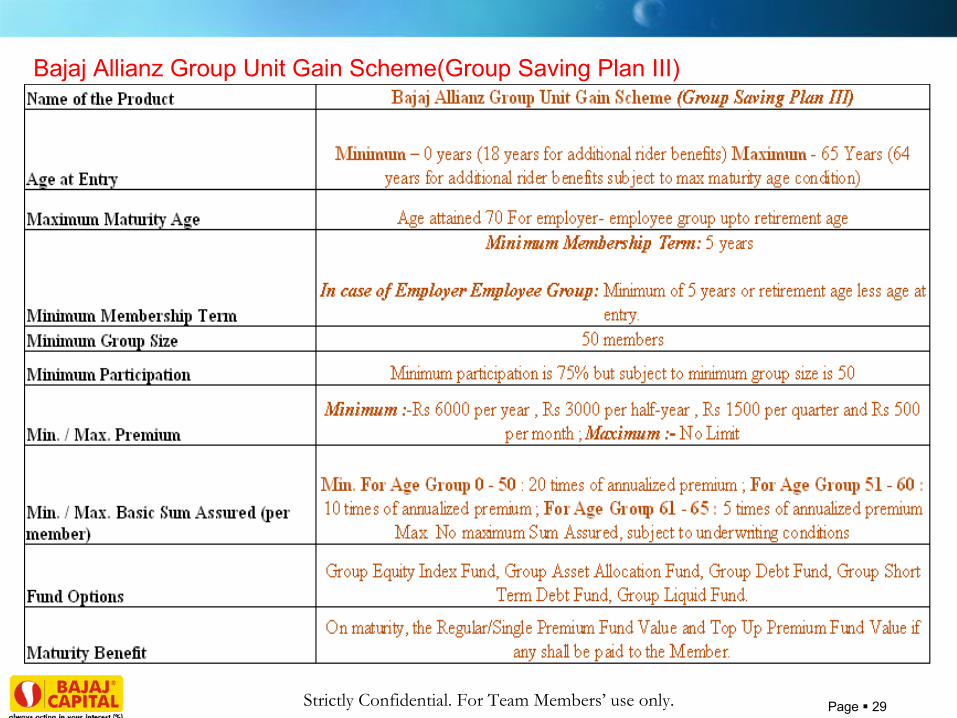

Bajaj Allianz Group Unit Gain Scheme(Group Saving Plan III)

Page 30Strictly Confidential. For Team Members’ use only.

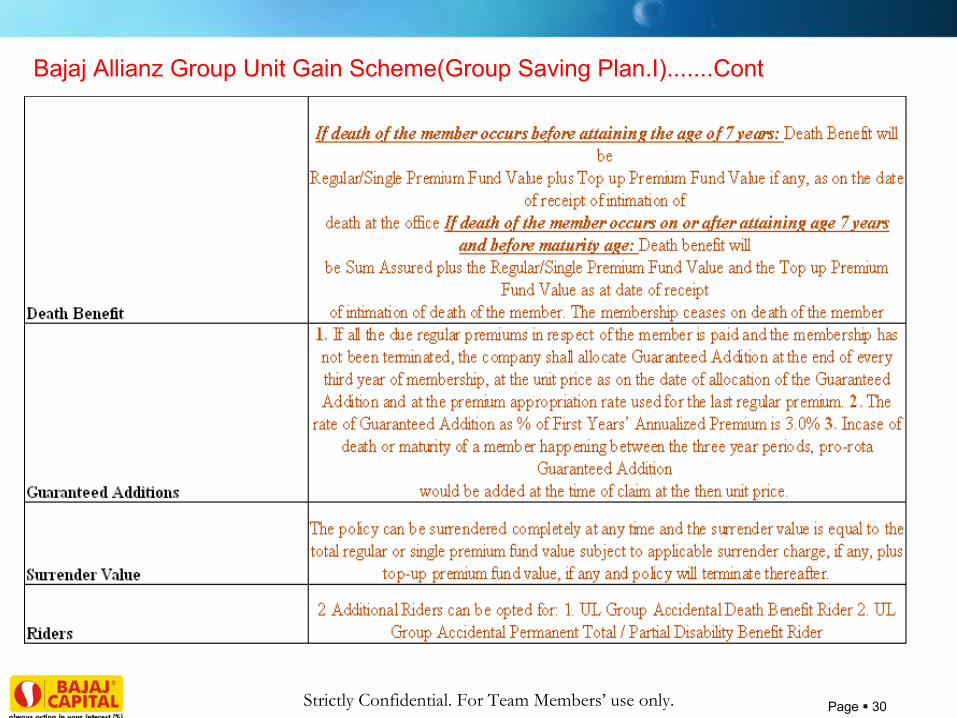

Bajaj Allianz Group Unit Gain Scheme(Group Saving Plan.I).......Cont

Page 31Strictly Confidential. For Team Members’ use only.

MFSC- General InsuranceNational Insurance -Tailor Made PolicyFocus Clientele :- Focus on all our clientele who have taken LI from us in March-April 2010.

Any persons aged between 5 months and 80 years, residing in India ,can take this insurance.Salient Features:Entry age ranges from 1 to 65 years and 0 days. An individual of upto 65 years can propose for the cover also, benefit of renewals till the age of 80 years is also there.No pre-insurance medical tests requirements till the age of 65years.All unknown pre-existing illness are covered after 30 days of policy inception, except Cancer, Kidney ,Heart diseases, Joint Replacements of all kind, Major Organ transplants, like kidney, pancreas, bone marrow, etc, Paralysis & Blindness, Neurological Disorder. However the diseases mentioned above will be covered after four continuous claim free policy years.

Maternity benefit upto 10 % of the Sum Insured with 9 month waiting period.

30 days pre-hospitalization and 60 days post hospitalization expenses are covered

Ambulance referral facility, Along with air rescue where ever needed.Coverage option ranges from Rs. 2,00,000 to Rs.10,00,000Choose cover for your self (individual) or for your family (floater) from a wide range of coverage options

Premium paid for the policy qualifies for tax benefit under section 80D of Income Tax act.

Cashless hospitalization facility at over 1400 hospitals TPA – East West Assist

Page 32Strictly Confidential. For Team Members’ use only.

Max Bupa – Heartbeat Health Insurance

Focus Clientele :- Any adult(18 years) individual can take this plan. No age capping limit.

Family Floater Plan : Maximum of 2 Adults + 2 Children.

Sum Insured in case of Heartbeat Individual or Family Floater plan ranges from Rs. 2 lacs to Rs. 50 lacs depending on the plan you choose

Heartbeat Silver Plan, Gold Plan, Platinum Plan.

Max Bupa is the only company to provide coverage of Rs.50 lacs.

Heartbeat Silver : 2 lacs, & 3 lacs. ~ Individual & Family Floater HeartbeatGold : 5 lacs, 7.5 lacs, & 10 lacs. ~ Individual & Family Floater Heartbeat Platinum : 15 lacs, 20 lacs & 50 lacs. ~ Individual & Family Floater

USP :-Direct Settlement of Claims : No TPA(Third Party Administrators)for Claims. We have an in-house claims processing unit to give customers a seamless claims experience.

Cashless Facility : In our State-of-the-art network hospitals.

Complete Reimbursement for our Out of Network Hospital.

Assured Renewal for Life: Once the policy is issued, the customer can renew the policy for life without any medical tests.

Page 33Strictly Confidential. For Team Members’ use only.

Maternity & Child Care Benefit : Maternity cover upto 2 deliveries along with vaccinations for the child.

Silver and Gold policies: customer avails the Maternity benefit, then we will cover the vaccination charges a of the new born for free – Upto 1year. Platinum policies:- Upto to the age of 12 yrs (Subject to renewal). Cover expenses towards consultation for a a nutrition and growth to the child during a visit for vaccination

New Born Baby Benefit : Free coverage for the Baby upto Renewal. !!

No Age restriction for enrollment : People of any age can take Max Bupa policy. However there is a co-pay of 20% for people over the age of 65yrs for both Network and Out of Network Hospitals.

Out-Patient Benefit : Covered upto 20000 for our Platinum Customers.

Domiciliary Treatment : Medical expenses of treatment taken at home covered under the policy. Covered upto 250000 !! *

No Waiting Period for Emergencies & Zero Waiting Period on renewal. : We cover Accidents and emergencies from day policy starts. However there is a waiting period of 90 days for all Planned hospitalization applicable only for the first year of the policy.

No Limit on Number of Claims: Any number of incidents of covered medical conditions are insured in the given policy year (subject to sum insured)

24x7 In house Customer Service: Direct access to the company in case of medical emergency

Page 34Strictly Confidential. For Team Members’ use only.

Relationship Manager : Assured Visit By Company Executive (a Doctor) during hospitalization – Gold & Platinum. The customer can focus on family or self medical need rather than running around for administrative requirements

Free health check up is a Renewal benefit : Everyone named in the policy is eligible for this benefit.

Unique Loyalty Program: Health services and products up to 10% of renewal premium will be available. Vouchers with catalogue are sent to the customer at renewal. Policy Holder can choose any services & products from the catalog and redeem them by submitting vouchers during the year.

E-Opinion: A second e-opinion for a life threatening condition can be arranged for our Elite Platinum Customer.

Tax benefit u/s 80D.

Page 35Strictly Confidential. For Team Members’ use only.

Max Bupa – Heartbeat Family First

Heartbeat Family First is an Extended Family Floater cover called Family First provide an opportunity to our customer to insure their extended family under the one Health Insurance policy.

Family First Policy means a Policy in terms of which, two or more persons of the Family are named in the Schedule as Insured Persons. In a Family First Policy, Family means Policyholder and the persons listed below who is/are related to the Policyholder in the following manner:

Legally married spouse as long as he or she continues to be married to the proposer

Son

Daughter-in-law

Daughter

Father

Mother

Father-in-law as long as the proposers spouse continues to be married to him/her

Mother-in-law as long as the proposers spouse continues to be married to him/her

Grandfather

Grandmother

Grandson,Grand daughter

Page 36Strictly Confidential. For Team Members’ use only.

Heartbeat Family First” caters to the family floater as well as individual segments. Sum Insured in case of Family First is flexible, the proposer can choose a fixed amount for each member of the extended family (one amount chosen for all family members), as well as, a floating amount that can be utilized once the sum Insured per person is consumed. This provides flexibility for families to decide their optimal cover. The premium for Family First policies depends on the individual age and sum insured of each insured customer in the Extended Family and the amount of floater cover chosen.

Sum Insured Family First : 1 lac to 5 lacs for Individual and 3 lacs to 15 lacs for Floater. Variants based on Benefits of Heartbeat Family First - Silver Plan and Gold Plan.

Family First Silver & Gold: 1 lac, 2 lacs 3 lacs, 4 lacs, & 5 lacs.~ Individual AND 3lacs, 4 lacs, 5 lacs,10 lacs & 15 lacs ~ Floater.

Coverages

Unique Comprehensive Health Insurance Cover for You and Your Extended Family!.

Direct Settlement of Claims : No TPA(Third Party Administrators)for Claims. We have an in-house claims processing unit to give customers a seamless claims experience.

Cashless Facility : In our State-of-the-art network hospitals.

Complete Reimbursement for our Out of Network Hospital.

Assured Renewal for Life: Once the policy is issued, the customer can renew the policy for life without any medical tests.

No Age restriction for enrollment : People of any age can take Max Bupa policy. However there is a co-pay of 20% for people over the age of 65yrs for both Network and Out of Network Hospitals

No Waiting Period for Emergencies & Zero Waiting Period on renewal. : We cover Accidents and emergencies from day policy starts. However there is a waiting period of 90 days for all Planned hospitalization applicable only for the first year of the policy.

Page 37Strictly Confidential. For Team Members’ use only.

No Limit on Number of Claims: Any number of incidents of covered medical conditions are insured in the given policy year (subject to sum insured)

Co-pay: If any Insured Person is 65 years of age or over on the date of commencement of the current Policy Period, then the Company will only pay 80% of any amount assessed for payment or reimbursement in respect of any claim made by that Insured Person and the balance will be borne by the Insured Person.

24x7 In house Customer Service: Direct access to the company in case of medical emergency

Free health check up is a Renewal benefit : The Policy covers the cost of a health check-up once in two years under Heartbeat Family First Silver plan and annually under Heartbeat Family First Gold plan.

Unique Loyalty Program: Health services and products up to 10% of Last paid premium will be available. Vouchers with catalogue are sent to the customer at renewal. Policy Holder can choose any services & products from the catalog and redeem them by submitting vouchers during the year.

Tax benefit u/s 80D.

Page 38Strictly Confidential. For Team Members’ use only.

Focus Clientele :- Focus on our existing clientele, add motor details in wealth maker so that they can be tapped once renewal is due.Bharti AXA presents an array of protective plans to suit your personal and business requirements. These embody our commitment to our system of values. Motor Insurance

Your vehicle, whether in parking or driving in a city street or on a highway is at many kinds of risk. Bharti AXA has a policy that offers many kinds of benefit.

SmartDrive Commercial Vehicle Insurance

SmartDrive Private Car Insurance

SmartDrive Two Wheeler Insurance

SMARTDRIVE PRIVATE CAR INSURANCE Steer towards safety with Smart Drive, Bharti AXA’s private car insurance policy. Your vehicle is fully road-ready only when you have insured it against loss or damage. Opt for a policy which is reliable and most easily available.

Simple, yet comprehensive; this defines Bharti AXA's Smart Drive Private Car Insurance Policy. It provides protection for loss or damage to your car arising out of any unfortunate eventuality. It further provides cover for liability, death or property damage of third parties. The Policy covers your motor vehicle used for social, pleasure and domestic purposes as well as professional purpose.

Bharti Axa – Motor Insurance

Page 39Strictly Confidential. For Team Members’ use only.

What does the Policy cover?

This policy provides the following covers 1. Accidental damage to the vehicle due to: Fire, lightning, self-ignition, external explosion, burglary, housebreaking or theft, malicious act. Riot and strike; terrorism; earthquake; flood, cyclone and inundation Whilst in transit by rail, road, air, elevator, lift. 2. Liability covers for: Third party injury or death Third party property damage caused to their property By paying an additional premium, you can opt for extra covers in case of:

Loss or damage to electrical accessories Loss or damage to Non-electrical accessories Personal Accident cover for insured or any named person or unnamed passengers Legal liability to persons employees (paid drivers/cleaners) Legal Liability to employees of the insured (other than paid drivers/cleaners)

What is payable in the event of a claim under a policy?

n the event of a claim under any of the sections, the following becomes payable:

Page 40Strictly Confidential. For Team Members’ use only.

1. Accidental Damage Section: Actual amount spent for repairs / replacement as assessed subject to Sum Insured Garaging and towing charges up to a maximum of Rs.1500/- Damage to tyres. (along with damage to vehicle)* Damage to plastic / rubber parts* Damage to all fibre glass components* Damage to all parts made of glass

2. Liability Section: Compulsory personal accident compensation for owner driver Personal Accident compensation for paid-driver, if opted Death or bodily injury to third parties – as per Motor Vehicles Act Death or bodily injury to any person carried in the car provided they are not Insured’s employees and not carried for hire or reward – As per Motor Vehicles Act Third party property damage – up to Rs.750,000/- All costs and expenses incurred with the Company’s written consent What is not payable in the event of a claim under a policy?Wear and tear, breakdowns. Consequential loss Loss when driving with invalid driving license or under the influence of alcohol. Loss due to war, civil war, etc. Claims arising out of contractual liability. Use of vehicle otherwise than in accordance with `limitations as to use ' (e.g. private car being used as a taxi) War perils, nuclear perils Mechanical and electrical breakdown; failure or breakage.

Page 41Strictly Confidential. For Team Members’ use only.

TATA AIG – Motor Insurance

Focus Clientele :- Focus on our existing clientele, add motor details in wealth maker so that they can be tapped once renewal is due.

What does the Auto Secure Insurance Cover ?

Loss or Damage to your Vehicle: Any partial or total loss to your vehicle arising out of accident or on account of fire and allied perils is covered. Third Party Legal Liability: Covers Third party property damage and Third party Bodily injury.No deduction on count of Salvage value

Green Channel Settlement: Green Channel Settlement is another first in the motor insurance industry. This innovation promises to make accident claims and repairs easier than never before! You get value added propositions through our accredited garages

Auto Restore Warranty: Tata AIG Auto Secure policyholders can enjoy 'Warranty on Accident Repairs' when a customer opts for the 'Green Channel Settlement ADD-ON COVERS

With growing needs and dynamic external factors, the regular car insurance is no longer sufficient. Tata AIG has endeavored to offer evolved benefits giving maximum value additions over and above the basic benefits.

Enhanced protection though 8 unique add on covers.

Page 42Strictly Confidential. For Team Members’ use only.

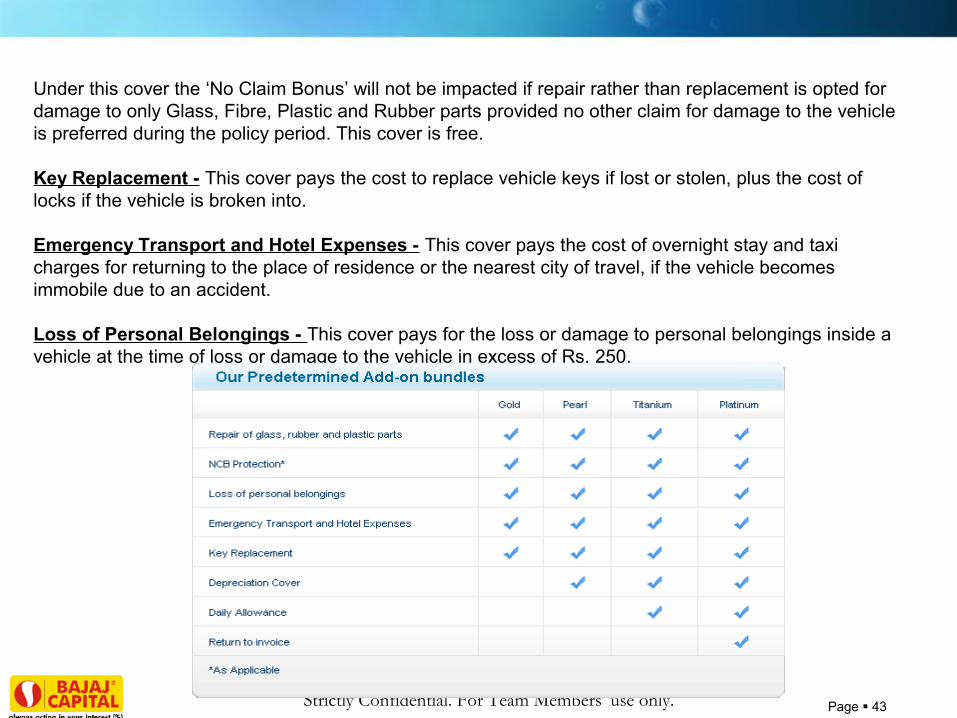

Depreciation Reimbursement - This cover offers full claim without any deduction for depreciation on the value of parts replaced. The cover is available for vehicles up to 3 years old and operates for maximum 2 claims during the policy period.

Return to Invoice - This cover pays the difference between the ‘claim amount receivable’ under the policy and the ‘purchase price of vehicle’ as per invoice in case the vehicle is declared a Total Loss or a Constructive Total Loss.

In case the same vehicle make and model is available at a lower price than the purchase price, then the lower price will be considered for arriving at the differential amount.The cover also pays first time registration charges and road tax on the insured vehicle. Cover is available for vehicles up to 3 years old.

Daily Allowance - This cover pays a fixed sum towards hiring a transport while the vehicle is under repair for a valid claim and the repair time is more than 3 days.The cover will be valid for maximum 10 days and in case of Total Loss / Theft claims, validity will be up to 15 days.Period of Daily Allowance may extend beyond the policy period depending upon the date of loss.

No Claim Bonus Protection - Normally in case of a claim, the ‘No Claim Bonus (NCB)’ component of your car insurance policy gets impacted. However under this cover, the existing NCB can be retained. Such a retention of NCB will be applicable in case of certain claims if the bonus accumulated is 25% or more and there is no claim in the preceding 2 years. NCB Protection is available only if vehicle is renewed with Tata AIG. Repair of Glass, Fibre, Plastic and Rubber Parts -

Page 43Strictly Confidential. For Team Members’ use only.

Under this cover the ‘No Claim Bonus’ will not be impacted if repair rather than replacement is opted for damage to only Glass, Fibre, Plastic and Rubber parts provided no other claim for damage to the vehicle is preferred during the policy period. This cover is free. Key Replacement - This cover pays the cost to replace vehicle keys if lost or stolen, plus the cost of locks if the vehicle is broken into.

Emergency Transport and Hotel Expenses - This cover pays the cost of overnight stay and taxi charges for returning to the place of residence or the nearest city of travel, if the vehicle becomes immobile due to an accident.

Loss of Personal Belongings - This cover pays for the loss or damage to personal belongings inside a vehicle at the time of loss or damage to the vehicle in excess of Rs. 250.

Page 44Strictly Confidential. For Team Members’ use only.

TATA AIG – Travel Insurance

Focus Clientele :- Individuals & families traveling within India for holidays.

Domestic Travel Guard (for Travel within IndiaA holiday is for a great change away from home. But what do you do if you fall ill in a completely new city, if your flight is delayed or baggage is lost! Despair at your helplessness?

Tata AIG Domestic Travel Guard is unique:

Accidental Death and Dismemberment Benefit

Accidental Death and Expense Benefit Missed Departure (Rail / Air): In the event of missing the departure of your booked journey, the cost of your actual ticket (air / rail) will be reimbursed subject to certification by the concerned authority.

Accommodation charges due to trip delay: In the event of the trip delay, the extra accommodation expenses incurred will be reimbursed.

Lost ticket reimbursement: In case of a ticket loss due to which one cannot continue the journey the actual cost of the ticket will be reimbursed. Emergency medical evacuation: In the event of a medical emergency, the arrangements for the evacuation and transportation of the insured for appropriate & quality medical care, shall be covered.

24 x 7 Assistance: Our assistance team will be available round the clock for any assistance or referral services.

Page 45Strictly Confidential. For Team Members’ use only.

Some of the covers included in this policy include :

Repatriation and Personal Liability

What is not Covered ?

This policy does not cover expenses directly or indirectly in respect of : traveling against the advice of a physician, for obtaining treatment, pre-existing ailments & complications arising out of them, suicide or attempted suicide, war, illegal acts, traveling under the influence of drugs, terrorism, dangerous sports etc. Please refer to the Policy wordings for other exclusions.

Page 46Strictly Confidential. For Team Members’ use only.

Mutual Funds-Use Client Search Engine to select right set of clients to pitch SIP's and Sundaram CPOF

SIP: All the investors without any SIP runningAll the existing SIP investors with running SIPs for more than 2 yrs and SIP amount has not increasedAll the investors with SIP renewal

CPOF (Capital Protection Oriented Fund):All the investors with more than 25% unrealized profit in equity schemes (each scheme)All the investors with Income funds or Gilt Funds in their portfolio (holding period more than 1 yr)

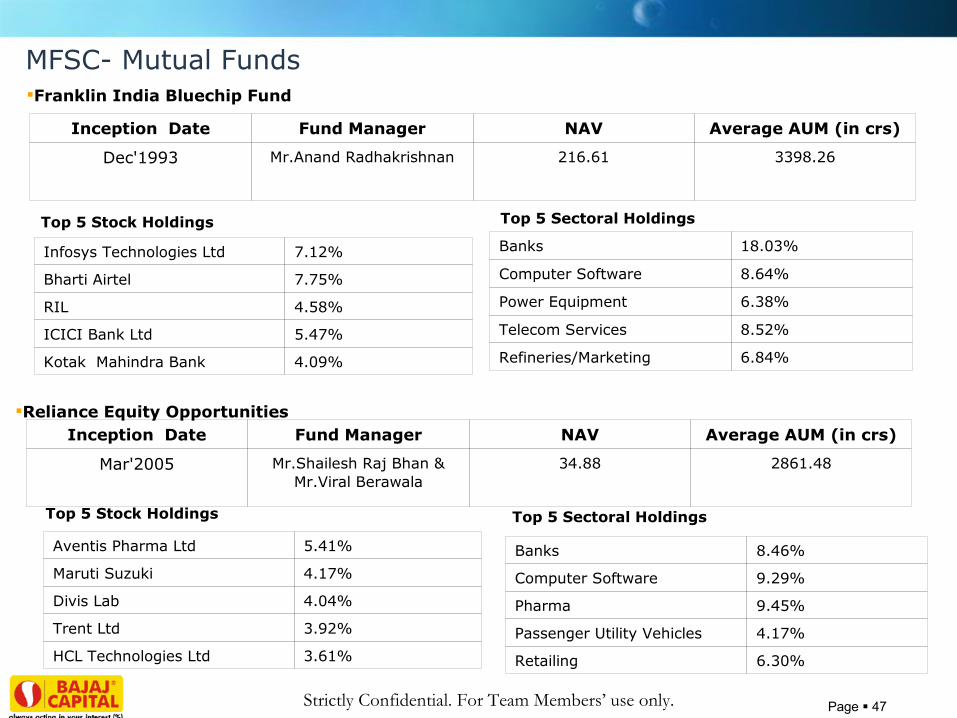

Page 47Strictly Confidential. For Team Members’ use only.

Franklin India Bluechip Fund

Inception Date Fund Manager NAV Average AUM (in crs)

Dec'1993 Mr.Anand Radhakrishnan 216.61 3398.26

Infosys Technologies Ltd 7.12%

Bharti Airtel 7.75%

RIL 4.58%

ICICI Bank Ltd 5.47%

Kotak Mahindra Bank 4.09%

Banks 18.03%

Computer Software 8.64%

Power Equipment 6.38%

Telecom Services 8.52%

Refineries/Marketing 6.84%

Top 5 Stock Holdings Top 5 Sectoral Holdings

MFSC- Mutual Funds

Reliance Equity OpportunitiesInception Date Fund Manager NAV Average AUM (in crs)

Mar'2005 Mr.Shailesh Raj Bhan & Mr.Viral Berawala

34.88 2861.48

Top 5 Stock Holdings Top 5 Sectoral Holdings

Aventis Pharma Ltd 5.41%

Maruti Suzuki 4.17%

Divis Lab 4.04%

Trent Ltd 3.92%

HCL Technologies Ltd 3.61%

Banks 8.46%

Computer Software 9.29%

Pharma 9.45%

Passenger Utility Vehicles 4.17%

Retailing 6.30%

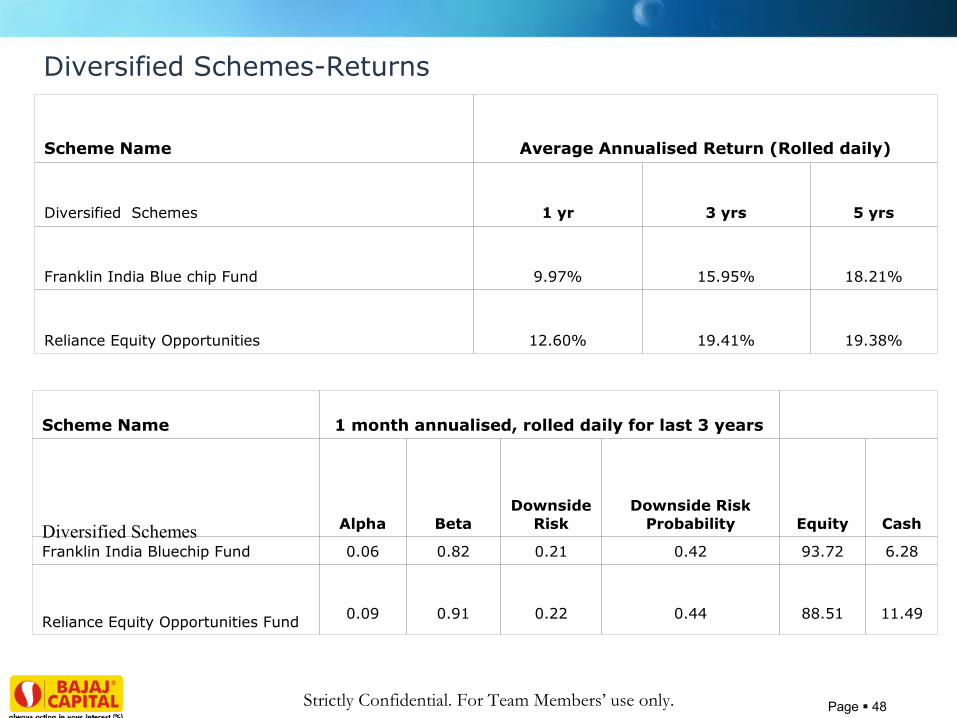

Page 48Strictly Confidential. For Team Members’ use only.

Scheme Name Average Annualised Return (Rolled daily)

Diversified Schemes 1 yr 3 yrs 5 yrs

Franklin India Blue chip Fund 9.97% 15.95% 18.21%

Reliance Equity Opportunities 12.60% 19.41% 19.38%

Scheme Name 1 month annualised, rolled daily for last 3 yearsAsset

Allocation

Diversified Schemes Alpha BetaDownside

RiskDownside Risk

Probability Equity Cash

Franklin India Bluechip Fund 0.06 0.82 0.21 0.42 93.72 6.28

Reliance Equity Opportunities Fund 0.09 0.91 0.22 0.44 88.51 11.49

Diversified Schemes-Returns

Page 49Strictly Confidential. For Team Members’ use only.

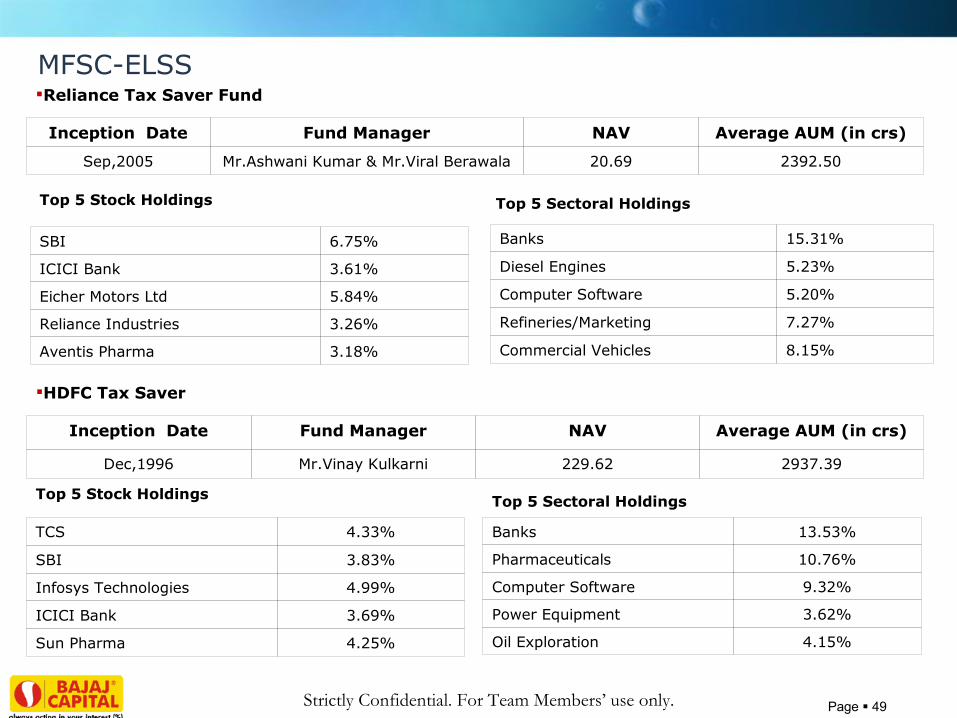

MFSC-ELSSReliance Tax Saver Fund

Inception Date Fund Manager NAV Average AUM (in crs)

Sep,2005 Mr.Ashwani Kumar & Mr.Viral Berawala 20.69 2392.50

SBI 6.75%

ICICI Bank 3.61%

Eicher Motors Ltd 5.84%

Reliance Industries 3.26%

Aventis Pharma 3.18%

Banks 15.31%

Diesel Engines 5.23%

Computer Software 5.20%

Refineries/Marketing 7.27%

Commercial Vehicles 8.15%

Top 5 Stock Holdings Top 5 Sectoral Holdings

HDFC Tax Saver

Inception Date Fund Manager NAV Average AUM (in crs)

Dec,1996 Mr.Vinay Kulkarni 229.62 2937.39

TCS 4.33%

SBI 3.83%

Infosys Technologies 4.99%

ICICI Bank 3.69%

Sun Pharma 4.25%

Banks 13.53%

Pharmaceuticals 10.76%

Computer Software 9.32%

Power Equipment 3.62%

Oil Exploration 4.15%

Top 5 Stock Holdings Top 5 Sectoral Holdings

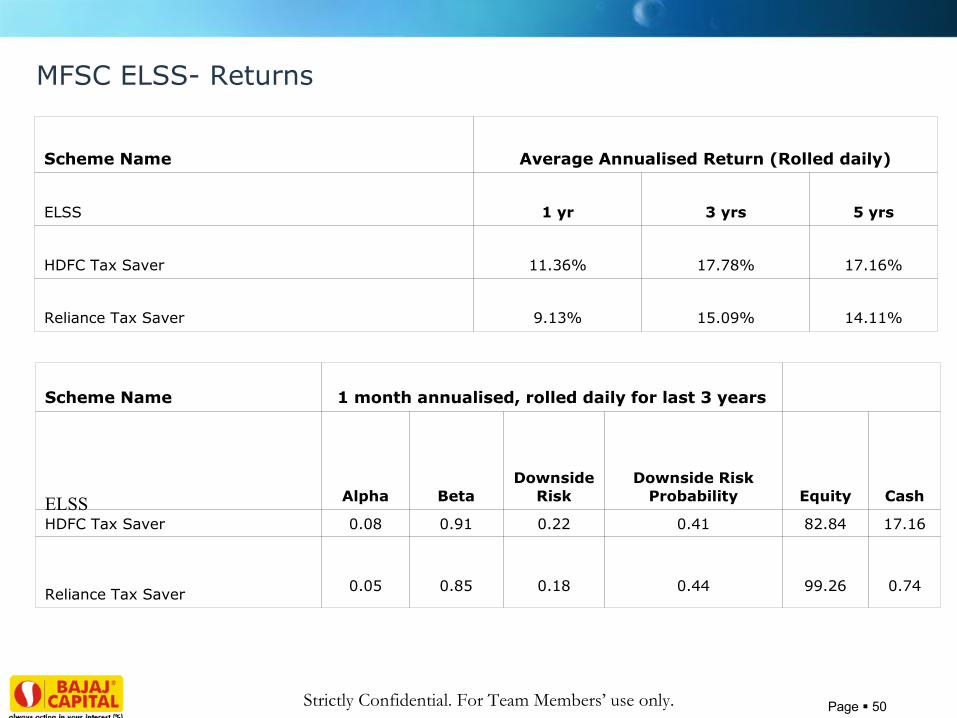

Page 50Strictly Confidential. For Team Members’ use only.

Scheme Name Average Annualised Return (Rolled daily)

ELSS 1 yr 3 yrs 5 yrs

HDFC Tax Saver 11.36% 17.78% 17.16%

Reliance Tax Saver 9.13% 15.09% 14.11%

Scheme Name 1 month annualised, rolled daily for last 3 yearsAsset

Allocation

ELSS Alpha BetaDownside

RiskDownside Risk

Probability Equity Cash

HDFC Tax Saver 0.08 0.91 0.22 0.41 82.84 17.16

Reliance Tax Saver 0.05 0.85 0.18 0.44 99.26 0.74

MFSC ELSS- Returns

Page 51Strictly Confidential. For Team Members’ use only.

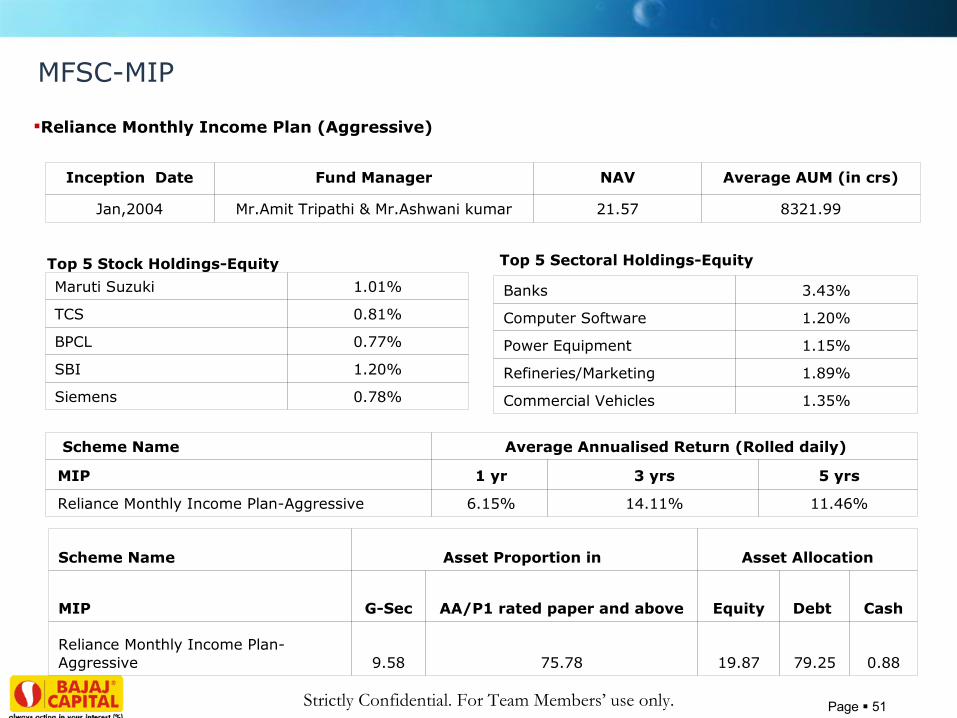

Reliance Monthly Income Plan (Aggressive)

Inception Date Fund Manager NAV Average AUM (in crs)

Jan,2004 Mr.Amit Tripathi & Mr.Ashwani kumar 21.57 8321.99

Top 5 Stock Holdings-Equity Top 5 Sectoral Holdings-Equity

Maruti Suzuki 1.01%

TCS 0.81%

BPCL 0.77%

SBI 1.20%

Siemens 0.78%

Banks 3.43%

Computer Software 1.20%

Power Equipment 1.15%

Refineries/Marketing 1.89%

Commercial Vehicles 1.35%

Scheme Name Average Annualised Return (Rolled daily)

MIP 1 yr 3 yrs 5 yrs

Reliance Monthly Income Plan-Aggressive 6.15% 14.11% 11.46%

Scheme Name Asset Proportion in Asset Allocation

MIP G-Sec AA/P1 rated paper and above Equity Debt Cash

Reliance Monthly Income Plan-Aggressive 9.58 75.78 19.87 79.25 0.88

MFSC-MIP

Page 52Strictly Confidential. For Team Members’ use only.

Capital Protection Oriented Fund These are close ended hybrid funds that invest predominantly (atleast 70%-80%) in debt while simultaneously investing a minor part of the portfolio (atmost 20%-30%) in equity. The benefits are enumerated below:1) Capital protection: As the name suggests, this class of funds are designed for capital protection. If you invest INR 100 in a capital protection oriented fund(CPOF, henceforth), INR 80 will be invested in debt (assuming 80% allocation in debt) and the rest in equity. The fund manager will aim for an interest earning of atleast INR 20 (after factoring in expenses) during its tenure so that total amount received at the end of maturity becomes equal to INR 100 (INR 80 + INR 20). Although it is similar to an MIP in terms of asset allocation, but its close ended nature makes all the difference. Unlike MIP, the fund manager of a CPOF doesn't have to actively manage its debt portfolio. This offsets the probability of mark to market losses due to interest rate changes and ensures capital protection.

2) Bank Fixed deposit plus returns: The CPOF invests in a mix of debt and equity. Debt portion comprises of highest grade debt instruments with a low credit risk. Currently, AAA rated debt instruments with a 3 year maturity are trading at an yield of 9.50%+p.a while bank FD of the same maturity is available at 8.25%p.a. That's a clear gain of 125 bps. The difference widens if one considers post tax returns as shown in the illustration next page. Apart from this, the presence of equity also enhances the probability of capital gain and generating better returns than Bank FD.

3) Tax efficient: CPOFs are tax efficient in the sense that they provide better post tax returns than FD owing to the presence of indexation factor. Capital gains from the fund are taxed as long term capital gains and investor can take Indexation benefit. Tax is levied at the rate of 10% without indexation and 20% with indexation. The benefit is subject to prevailing tax rate and inflation

Page 53Strictly Confidential. For Team Members’ use only.

4) Liquidity: Though these funds are essentially close ended, they are nevertheless listed on stocks exchanges and can be bought or sold there. However, past trends suggest that liquidity in these instruments on the stock exchanges has remained very low. Hence, an investor should invest that part of his/her savings in these funds that he/she will not need during the tenure of the scheme.

In a nutshell, the benefits are:1) Capital protection orientation structure2)Stable returns from debt combined with higher growth potential of equity 3) 3 years tenure gives the fund managers the liberty to execute long term calls4) “Hold till maturity” of debt instruments nullifies the interest rate risk 5) Better tax treatment as against traditional fixed return products6) Indexation benefit7) Inflation beating returns owing to presence of equity

Portfolio composition Debt: Invest in high grade debt instruments with maturity similar to the maturity of the scheme and they are held till maturity. This offsets the interest rate risk . Equity: Normally, these funds invest in diversified portfolio of stocks across market capitalisation. Growth stocks available at attractive valuations are normally included in the portfolio

Page 54Strictly Confidential. For Team Members’ use only.

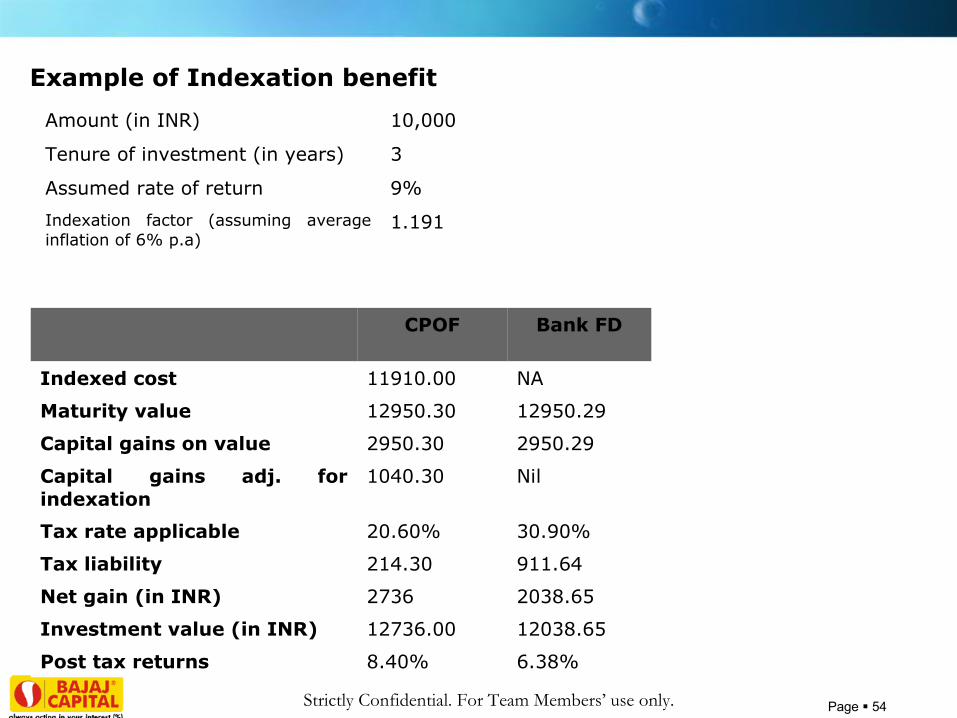

Example of Indexation benefit

Amount (in INR) 10,000

Tenure of investment (in years) 3

Assumed rate of return 9%

Indexation factor (assuming average inflation of 6% p.a)

1.191

CPOF Bank FD

Indexed cost 11910.00 NA

Maturity value 12950.30 12950.29

Capital gains on value 2950.30 2950.29

Capital gains adj. for indexation

1040.30 Nil

Tax rate applicable 20.60% 30.90%

Tax liability 214.30 911.64

Net gain (in INR) 2736 2038.65

Investment value (in INR) 12736.00 12038.65

Post tax returns 8.40% 6.38%

Page 55Strictly Confidential. For Team Members’ use only.

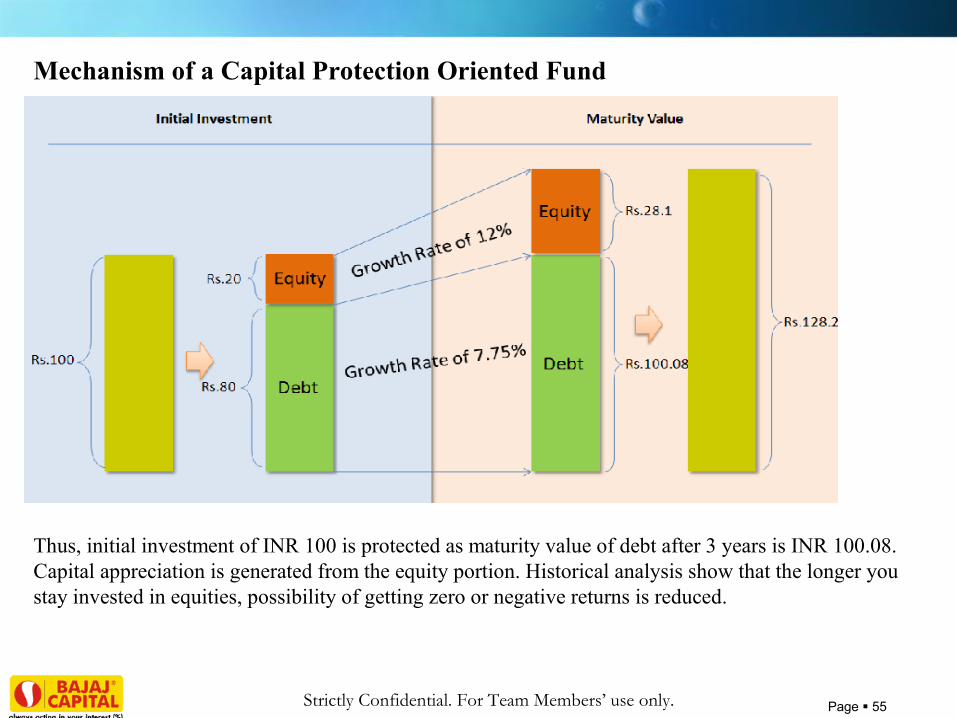

Mechanism of a Capital Protection Oriented Fund Mechanism of a Capital Protection Oriented Fund

Thus, initial investment of INR 100 is protected as maturity value of debt after 3 years is INR 100.08. Capital appreciation is generated from the equity portion. Historical analysis show that the longer you stay invested in equities, possibility of getting zero or negative returns is reduced.

Page 56Strictly Confidential. For Team Members’ use only.

Sundaram Capital Protection Oriented Fund- Series III NFO period: Mar, 29 till Apr 11, 2011

Capital Protection Orientation – Endeavor’s to preserve capital by investing atleast 80% funds in fixed income securities so that, with the interest it grows back to your initial capital value over a 3 year period.Capital Gains – Generates capital appreciation by investing a part of fund (atmost 20%) in equity, it will be a multi-cap equity portfolio which will create scope for attaining higher returns as compared to broad marketHighest CRISIL rating AAA (so) – This rating indicates the highest degree of certainty regarding timely payment of face value of the investment of investors.Tax Efficient – The tax efficiency of this fund is attractive as gains will be taxed as long term capital gains and investor can take Indexation benefit.

Other fund houses expected to launch capital protection oriented funds in Apr, 11

Reliance Mutual FundSBI Mutual Fund

Page 57Strictly Confidential. For Team Members’ use only.

DSP BlackRock Savings Manager FundIt is an aggressive monthly income fund, which picks scrip only from top 100 companies by market capitalisation to build its equity portfolio. While for the debt portfolio fund is focused on high credit quality securities. As per Feb, 2011 portfolio, the fund's equity exposure is 17.53% and the debt exposure is 81.29% of the total portfolio. The debt portfolio is entirely invested in high credit rated debt instruments. The fund is among top quartile performers in terms of risk adjusted returns coupled with the lowest downside side in its category. The fund has generated an alpha of 2.68% in the last 3 years, which speaks about effective management of equity portion of the fund. The fund has generated an average annualised monthly rolling return (rolled daily) of 8.62% in the last 3 years. Please note:DSP BlackRock Savings Manager Fund-Moderate and DSP BlackRock Savings Manager Fund-Conservative merged into DSP BlackRock Savings Manager Fund – Aggressive with effect from Feb 26, 2011. The Merged DSP BlackRock Savings Manager Fund-Aggressive has been renamed to DSP BlackRock Savings Manager Fund.

Franklin India Dynamic PE Ratio Fund of FundIt is a fund of fund with a unique in-built buy-sell discipline based on the market conditions. The fund is rebalanced on the monthly basis based on the prevailing market PE. The equity component of the scheme is invested in Franklin India Bluechip and the debt component is invested in Templeton India Income Fund. It holds 45% exposure in Franklin India Bluechip and 55% exposure in Templeton India Income Fund applicable as on 7th Mar, 2011. It suits the investors, wanting to take advantage of the upside while staying relatively protected on the downside. The ideal investment horizon of the fund is 3 years. It has generated the annualised trialling return of 12.01% in last 3 years.

Page 58Strictly Confidential. For Team Members’ use only.

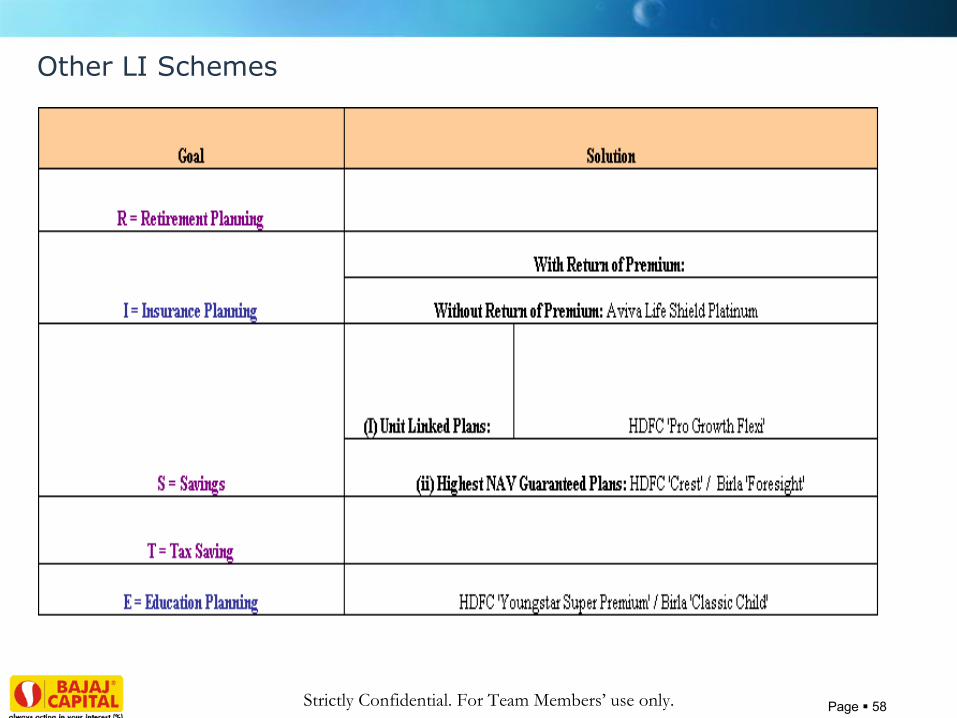

Other LI Schemes

Page 59Strictly Confidential. For Team Members’ use only.

Aviva Life Shield PlatinumUnique protection plan providing protection to the family members of the policyholder in case he is not around.Has differential premium rates as per smoker and non smoker category.

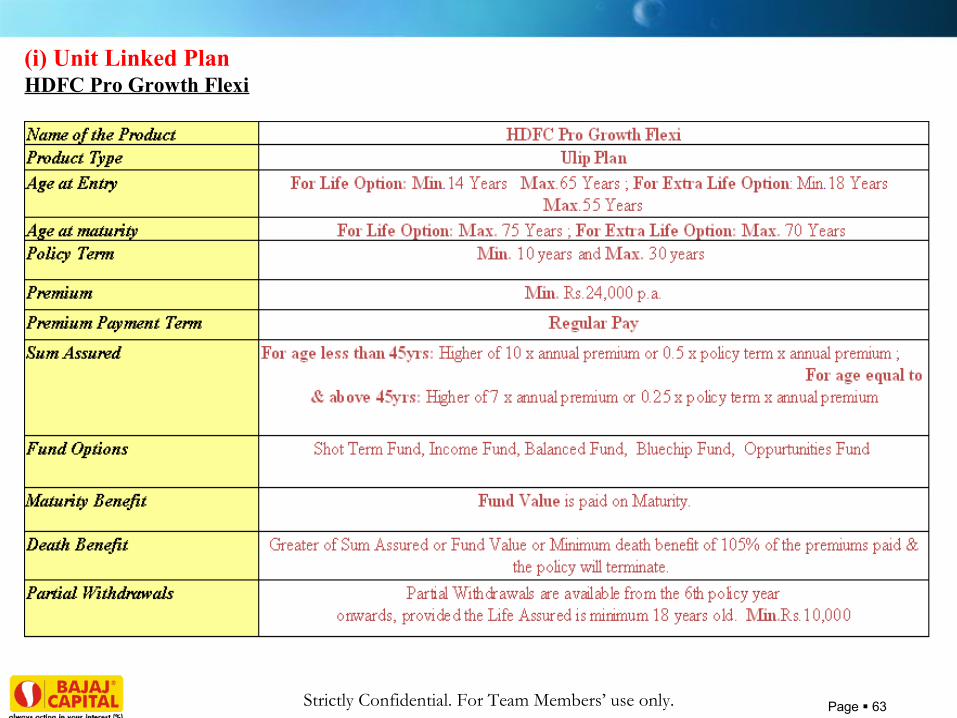

HDFC Pro Growth FlexiPlan suitable for those who want to create wealth for future and accumulate a lump sum amount.For those who want to pay premium as low as Rs.2500 per month.

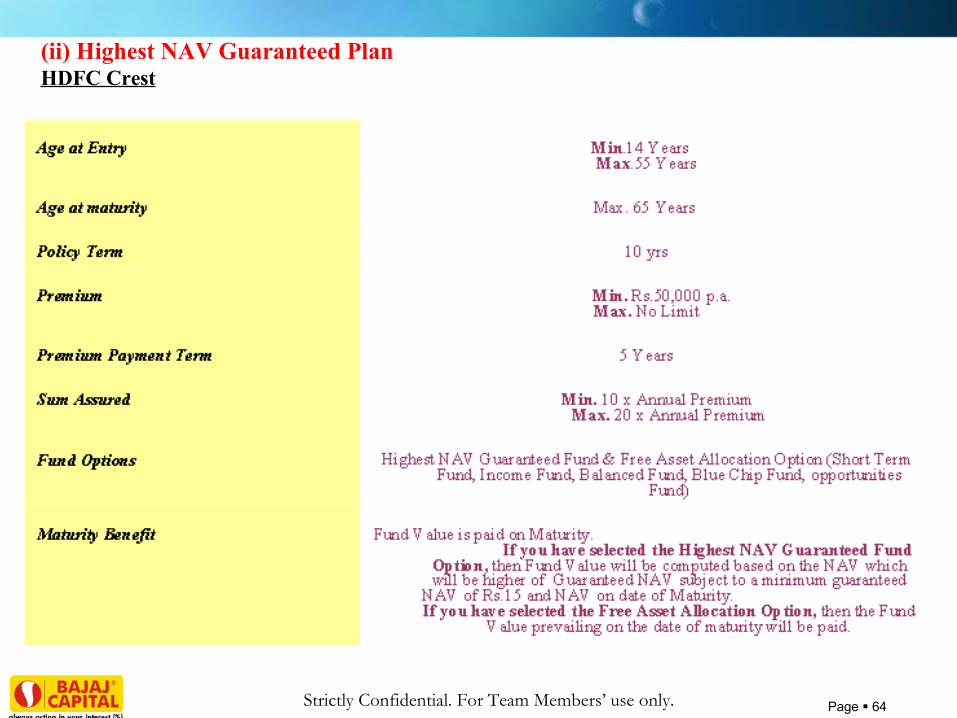

HDFC CrestSuitable for those who want to pay for a Short Term like 5 years.For clients who want to enjoy the benefit of equity market with a minimum guaranteed return.Those who want guarantee as this plan guarantees 50% appreciation in NAV over 10 years.

Birla ForesightSuitable for those who want to optimize their investment in capital markets when they are low and locking in the gains when they are high.For those who want to pay premium only once or for short term of 5 years.

Positioning of Plans

Page 60Strictly Confidential. For Team Members’ use only.

HDFC Youngstar Super PremiumFor those who want to invest in a plan and gic=ve their child a bright and a secured future.For those who do not want to undergo any medical underwritings.

Birla Classic ChildFor those who want to create legacy for their child.

Page 61Strictly Confidential. For Team Members’ use only.

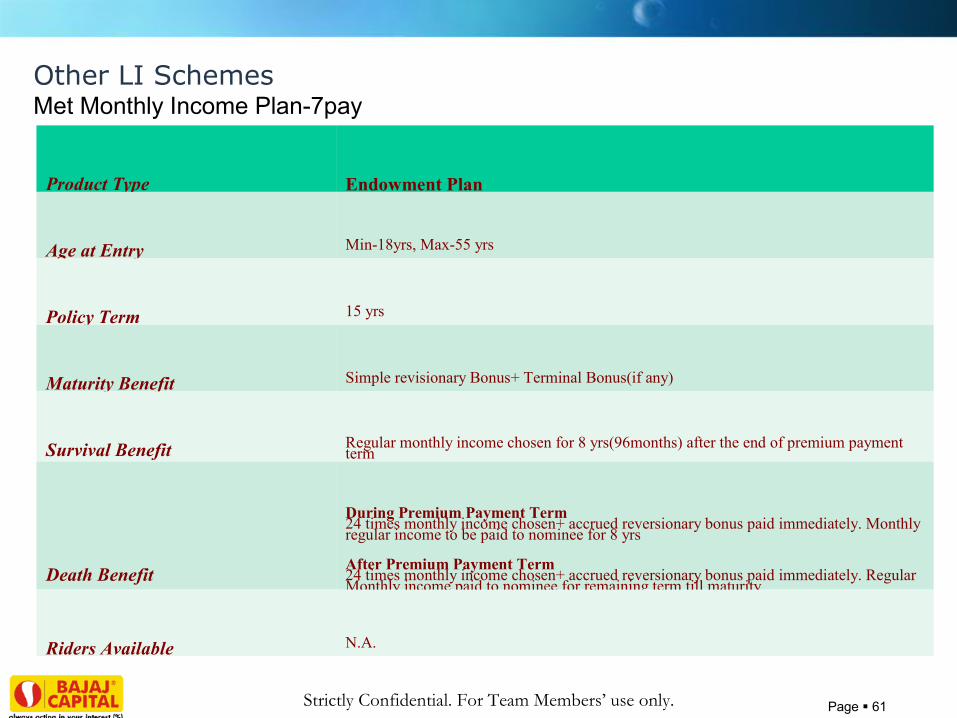

Other LI SchemesMet Monthly Income Plan-7pay

Product Type Endowment Plan

Age at Entry Min-18yrs, Max-55 yrs

Policy Term 15 yrs

Maturity Benefit Simple revisionary Bonus+ Terminal Bonus(if any)

Survival Benefit Regular monthly income chosen for 8 yrs(96months) after the end of premium payment term

Death Benefit

During Premium Payment Term24 times monthly income chosen+ accrued reversionary bonus paid immediately. Monthly regular income to be paid to nominee for 8 yrs

After Premium Payment Term24 times monthly income chosen+ accrued reversionary bonus paid immediately. Regular Monthly income paid to nominee for remaining term till maturity

Riders Available N.A.

Page 62Strictly Confidential. For Team Members’ use only.

Without Return of Premium

(a) Aviva Life Shield Platinum

It is a unique protection plan to help you plan for your family in case you are not around.

This plan has 3 options:

Option A – Life ProtectionChoose this option if you foresee a need for lump sum payment of large sum of money to your family in case you are not around. You can opt for additional health and Accidental Death Benefit rider. We offer differential rates for Smokers, Non-smokers and preferred rates for (Healthy) Non-smokers.

Option B – Income ReplacementChoose this option if you want to provide a regular monthly income to your family in your absence. This amount increases by 5% p.a. compounded annually from the very first year of your policy to beat inflation. Your premium obligation is limited to about 2/3rd of the policy term.

Option C – Loan Protection. Choose this option to cover for higher financial liabilities and family responsibilities in the early years of your life, the Life Cover decreases evenly across the policy term. Your premium obligation is limited to about 2/3rd of the policy term.This Insurance plan offers rebate on your premium for higher levels of Sum Assured

Page 63Strictly Confidential. For Team Members’ use only.

(i) Unit Linked PlanHDFC Pro Growth Flexi

Page 64Strictly Confidential. For Team Members’ use only.

(ii) Highest NAV Guaranteed PlanHDFC Crest

Page 65Strictly Confidential. For Team Members’ use only.

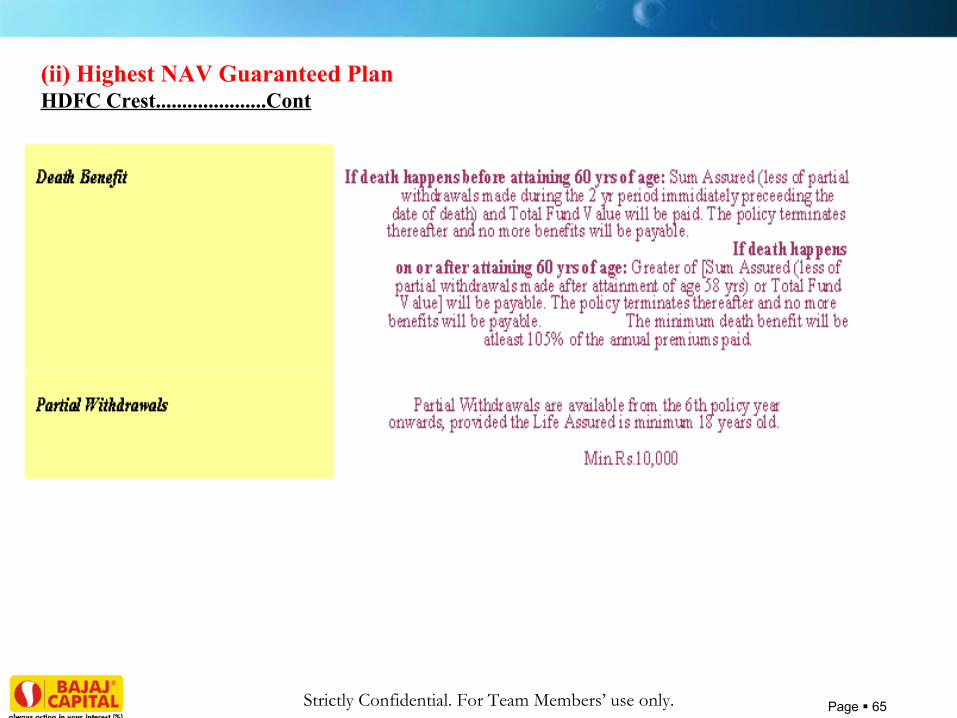

(ii) Highest NAV Guaranteed PlanHDFC Crest.....................Cont

Page 66Strictly Confidential. For Team Members’ use only.

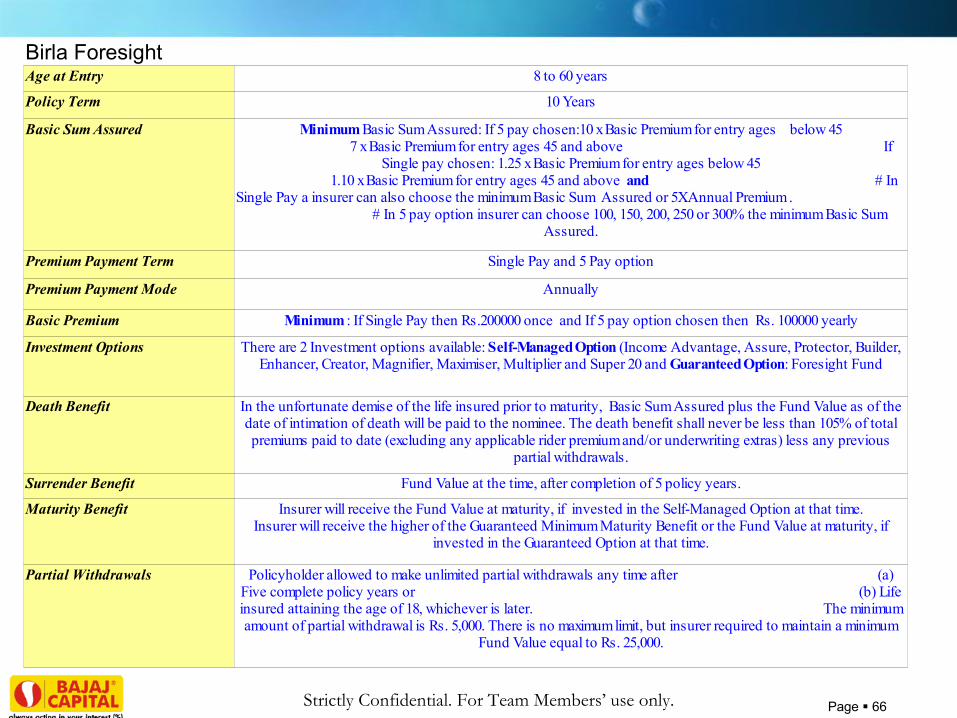

Birla Foresight Age at Entry 8 to 60 years

Policy Term 10 Years

Basic Sum Assured

Premium Payment Term Single Pay and 5 Pay option

Premium Payment Mode Annually

Basic Premium

Investment Options

Death Benefit

Surrender Benefit Fund Value at the time, after completion of 5 policy years.

Maturity Benefit

Partial Withdrawals

Minimum Basic Sum Assured: If 5 pay chosen:10 x Basic Premium for entry ages below 45 7 x Basic Premium for entry ages 45 and above If

Single pay chosen: 1.25 x Basic Premium for entry ages below 45 1.10 x Basic Premium for entry ages 45 and above and # In

Single Pay a insurer can also choose the minimum Basic Sum Assured or 5XAnnual Premium . # In 5 pay option insurer can choose 100, 150, 200, 250 or 300% the minimum Basic Sum

Assured.

Minimum : If Single Pay then Rs.200000 once and If 5 pay option chosen then Rs. 100000 yearly

There are 2 Investment options available: Self-Managed Option (Income Advantage, Assure, Protector, Builder, Enhancer, Creator, Magnifier, Maximiser, Multiplier and Super 20 and Guaranteed Option: Foresight Fund

In the unfortunate demise of the life insured prior to maturity, Basic Sum Assured plus the Fund Value as of the date of intimation of death will be paid to the nominee. The death benefit shall never be less than 105% of total premiums paid to date (excluding any applicable rider premium and/or underwriting extras) less any previous

partial withdrawals.

Insurer will receive the Fund Value at maturity, if invested in the Self-Managed Option at that time.Insurer will receive the higher of the Guaranteed Minimum Maturity Benefit or the Fund Value at maturity, if

invested in the Guaranteed Option at that time.

Policyholder allowed to make unlimited partial withdrawals any time after (a) Five complete policy years or (b) Life insured attaining the age of 18, whichever is later. The minimum amount of partial withdrawal is Rs. 5,000. There is no maximum limit, but insurer required to maintain a minimum

Fund Value equal to Rs. 25,000.

Page 67Strictly Confidential. For Team Members’ use only.

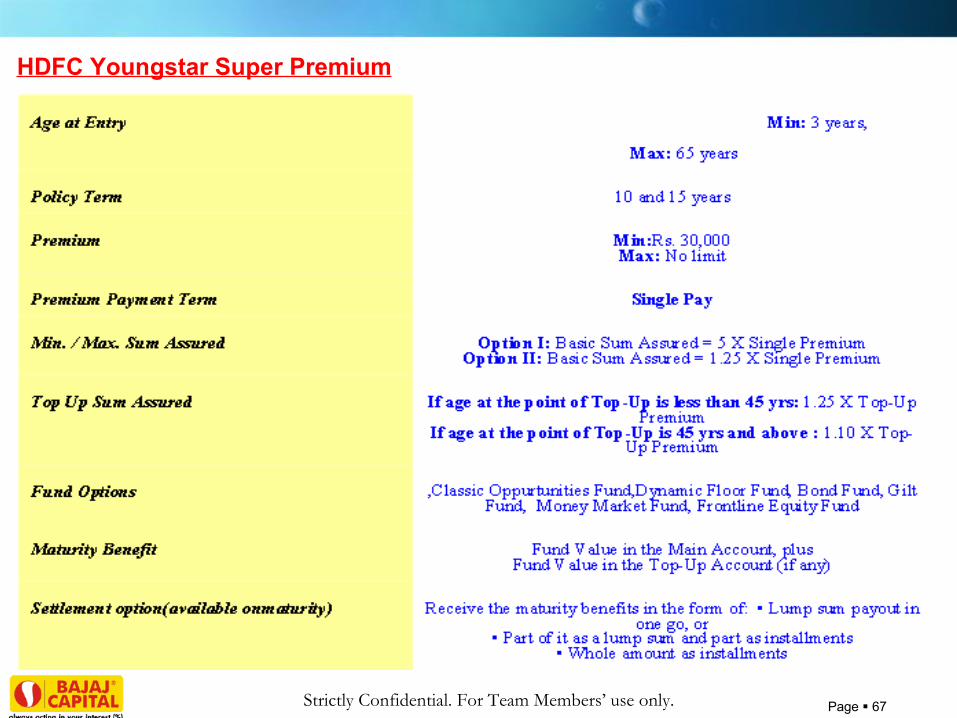

HDFC Youngstar Super Premium

Page 68Strictly Confidential. For Team Members’ use only.

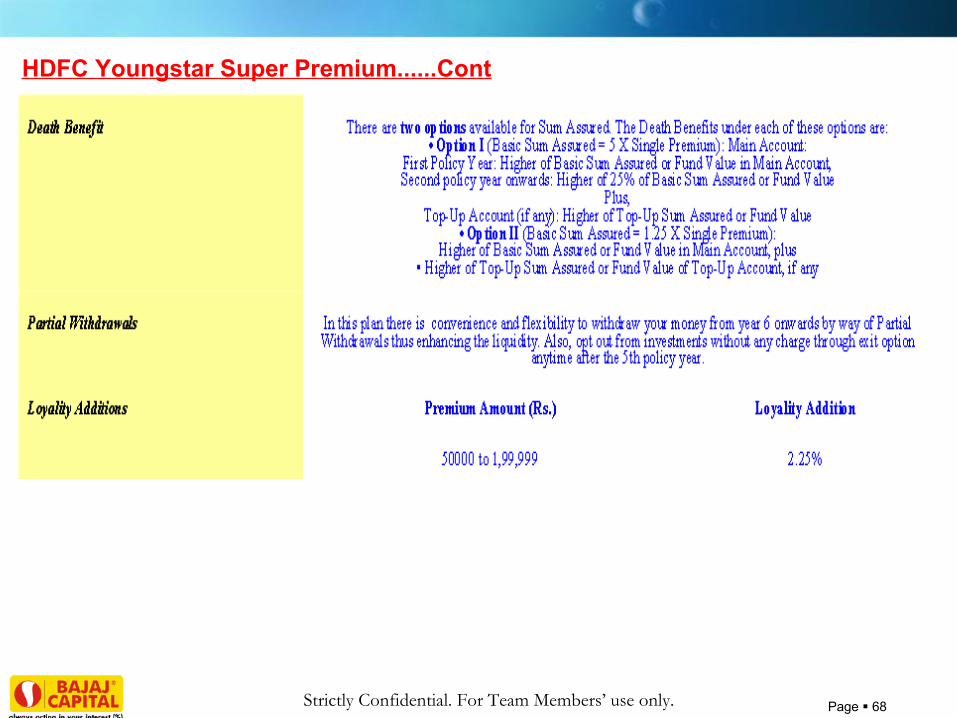

HDFC Youngstar Super Premium......Cont

Page 69Strictly Confidential. For Team Members’ use only.

Birla Classic Child PlanClassic Child Plan is a non-participating unit- linked insurance plan that provides an option to choose the savings date as per your savings objective and also enhance your life cover to increase the financial security for your child.

Features of the Plan:

Entry Age: Parent – 18 to 65 years ; Child – 30 days to 17 years

Policy Term – Savings Date + 20 years

Basic Premium – Rs.25000 annuallyBasic Sum Assured: For entry age below 45 : greater of 10 or (policy term/divided by 2) , For entry ages 45 and above : greater of 7 or (policy term/divided by 4)

Option of Riders to increase protection

Guaranteed Additions - in the form of additional units will be to the policy On the 10th policy anniversary and on every 5th policy anniversary thereafter. Guaranteed Addition is 2.50% of the Basic Premiums paid in the last 60 months. In addition on 11th policy anniversary and every policy thereafter guaranteed addition is 0.25% of the average Fund Value in the last 12 months.

Death Benefit: In the unfortunate event of the death of the primary life insured, the beneficiary will receive the Basic Sum Assured.

Page 70Strictly Confidential. For Team Members’ use only.

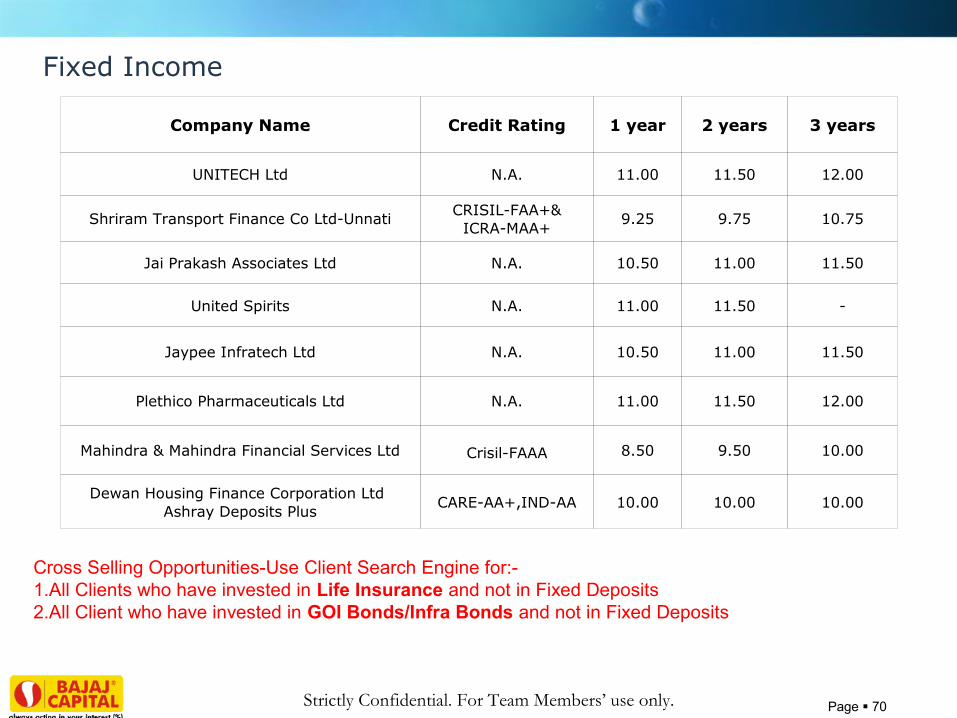

Company Name Credit Rating 1 year 2 years 3 years

UNITECH Ltd N.A. 11.00 11.50 12.00

Shriram Transport Finance Co Ltd-Unnati CRISIL-FAA+& ICRA-MAA+

9.25 9.75 10.75

Jai Prakash Associates Ltd N.A. 10.50 11.00 11.50

United Spirits N.A. 11.00 11.50 -

Jaypee Infratech Ltd N.A. 10.50 11.00 11.50

Plethico Pharmaceuticals Ltd N.A. 11.00 11.50 12.00

Mahindra & Mahindra Financial Services Ltd Crisil-FAAA 8.50 9.50 10.00

Dewan Housing Finance Corporation Ltd-Ashray Deposits Plus

CARE-AA+,IND-AA 10.00 10.00 10.00

Fixed Income

Cross Selling Opportunities-Use Client Search Engine for:-1.All Clients who have invested in Life Insurance and not in Fixed Deposits2.All Client who have invested in GOI Bonds/Infra Bonds and not in Fixed Deposits

Page 71Strictly Confidential. For Team Members’ use only.

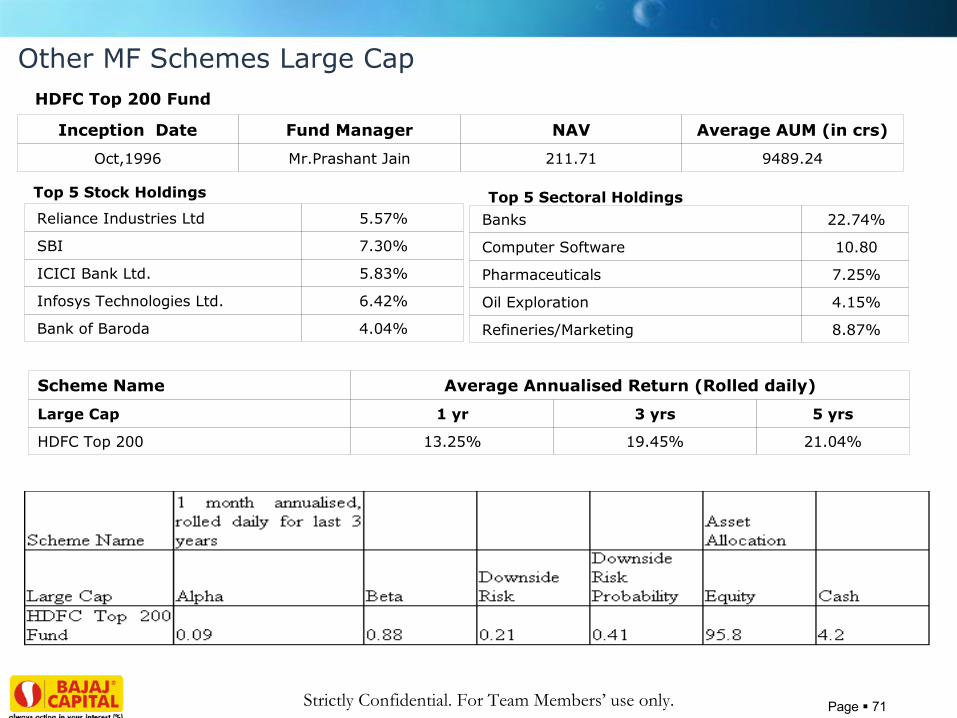

Other MF Schemes Large Cap

Top 5 Sectoral Holdings

Inception Date Fund Manager NAV Average AUM (in crs)

Oct,1996 Mr.Prashant Jain 211.71 9489.24

HDFC Top 200 Fund

Top 5 Stock Holdings

Reliance Industries Ltd 5.57%

SBI 7.30%

ICICI Bank Ltd. 5.83%

Infosys Technologies Ltd. 6.42%

Bank of Baroda 4.04%

Banks 22.74%

Computer Software 10.80

Pharmaceuticals 7.25%

Oil Exploration 4.15%

Refineries/Marketing 8.87%

Scheme Name Average Annualised Return (Rolled daily)

Large Cap 1 yr 3 yrs 5 yrs

HDFC Top 200 13.25% 19.45% 21.04%

Page 72Strictly Confidential. For Team Members’ use only.

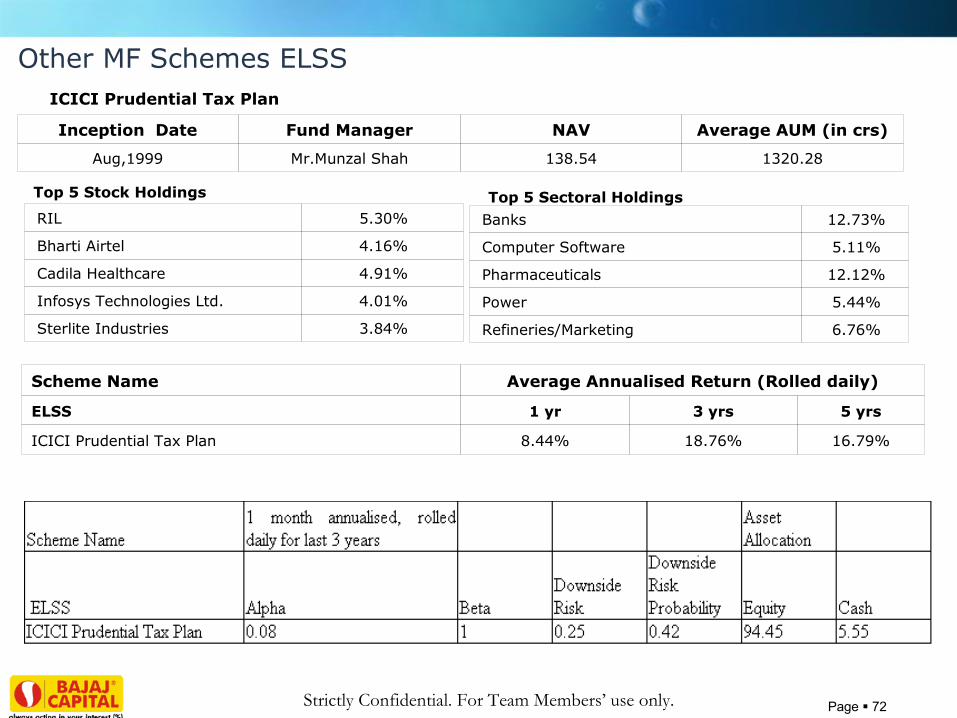

Other MF Schemes ELSS

Top 5 Sectoral Holdings

Inception Date Fund Manager NAV Average AUM (in crs)

Aug,1999 Mr.Munzal Shah 138.54 1320.28

ICICI Prudential Tax Plan

Top 5 Stock Holdings

RIL 5.30%

Bharti Airtel 4.16%

Cadila Healthcare 4.91%

Infosys Technologies Ltd. 4.01%

Sterlite Industries 3.84%

Banks 12.73%

Computer Software 5.11%

Pharmaceuticals 12.12%

Power 5.44%

Refineries/Marketing 6.76%

Scheme Name Average Annualised Return (Rolled daily)

ELSS 1 yr 3 yrs 5 yrs

ICICI Prudential Tax Plan 8.44% 18.76% 16.79%

Page 73Strictly Confidential. For Team Members’ use only.

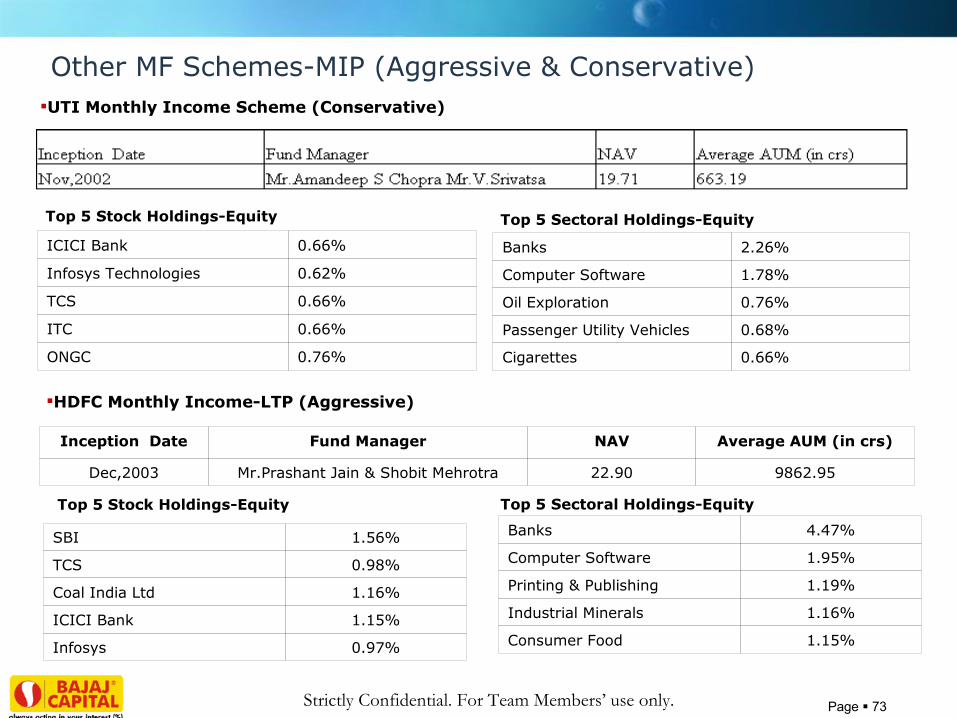

Other MF Schemes-MIP (Aggressive & Conservative)

HDFC Monthly Income-LTP (Aggressive)

Inception Date Fund Manager NAV Average AUM (in crs)

Dec,2003 Mr.Prashant Jain & Shobit Mehrotra 22.90 9862.95

Top 5 Stock Holdings-Equity Top 5 Sectoral Holdings-Equity

SBI 1.56%

TCS 0.98%

Coal India Ltd 1.16%

ICICI Bank 1.15%

Infosys 0.97%

Banks 4.47%

Computer Software 1.95%

Printing & Publishing 1.19%

Industrial Minerals 1.16%

Consumer Food 1.15%

UTI Monthly Income Scheme (Conservative)

Top 5 Stock Holdings-Equity

ICICI Bank 0.66%

Infosys Technologies 0.62%

TCS 0.66%

ITC 0.66%

ONGC 0.76%

Top 5 Sectoral Holdings-Equity

Banks 2.26%

Computer Software 1.78%

Oil Exploration 0.76%

Passenger Utility Vehicles 0.68%

Cigarettes 0.66%

Page 74Strictly Confidential. For Team Members’ use only.

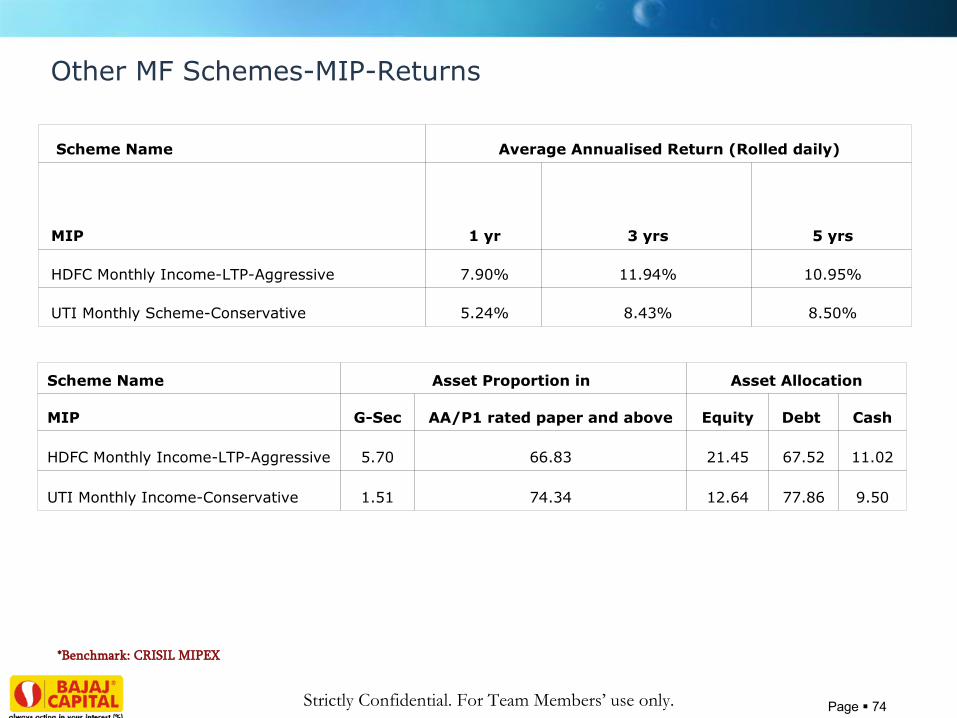

Other MF Schemes-MIP-Returns

Scheme Name Average Annualised Return (Rolled daily)

MIP 1 yr 3 yrs 5 yrs

HDFC Monthly Income-LTP-Aggressive 7.90% 11.94% 10.95%

UTI Monthly Scheme-Conservative 5.24% 8.43% 8.50%

*Benchmark: CRISIL MIPEX

Scheme Name Asset Proportion in Asset Allocation

MIP G-Sec AA/P1 rated paper and above Equity Debt Cash

HDFC Monthly Income-LTP-Aggressive 5.70 66.83 21.45 67.52 11.02

UTI Monthly Income-Conservative 1.51 74.34 12.64 77.86 9.50

Page 75Strictly Confidential. For Team Members’ use only.

Just TradeJust Activ Premier Plus as the name sounds Provide for facility of buying and selling shares, futures, options, mutual funds and applying for IPOs online with little paper work. Just Activ-Premier Plus provides you browser based streaming quotes engine which looks like a dealer terminal.

This A/c is Suitable for: An Activ Trader who trades Heavily in Equity and Derivatives, A computer savvy person, A person who wishes to watch the price movement of a list of shares on one screen Who has the facility to load and run JAVA program in his computer( For Online Trading)Features-Just Activ comes with the following features: Just Activ Premier Plus allows you convenience of executing your trades yourself OR through our Call N Trade Buying and selling shares/F&O of contracts of companies listed in NSE. Buying, redemption and switching of mutual funds schemes in more than 15 top AMCs in India at Zero transaction Fee(SIP Facility also Available) Helps you to place order for more than one mutual fund schemes at a time Apply for IPO’s without filling any form at Zero cost Online Investment Platform fully integrated with DP and bank accounts (HDFC/ICICI/AXIS) for online Transfer of Funds Facility to Call and Trade AND Phone a Fund transaction at no extra cost. First Year Free DP (AMC) Initial Margin Money required-Nil

Just Activ Premier Plus comes with an Annual Charges of Rs 99,999/- towards account activation and Subscription Fee.

Brokerage on buying and selling shares, futures and options beyond the above specified free turnover limits in a day will be chared as given below:

•

*Service Tax on Annual Subscription fee, brokerage, Securities Transaction Tax, Turnover Tax and Stamp duty would be charged separately as applicable. **Available at Select Locations

Free Turnover Limit - Daily Futures & Options and Cash – Intraday squaring Off & Delivery

Rs. 5,00,00,000

Free Turnover Limit - Daily Delivery Rs. 50,00,000

Delivery 0.10%

Non Delivery (cash –intra day and futures & options) 0.01%

Annual Subscription Fees to be paid at the time of opening the account

Rs. 99,999*

Page 76Strictly Confidential. For Team Members’ use only.

F.Y. 2010-11-March-‘Rock on Club’ Branches

Mr.Awadesh Pratap Singh & eam Pune Pimpri

Mr.Vivek Kr.Rai & Team Jalgaon

Mr.Bhushan Kiran Dusane& Team Pune Bhandarkar

Ms. Rupali Manish Salunkhe & Team Mumbai Sion

Mr. Dan Bahadur Yadav & team Nerul

Mr.Narain M Gaekwad & Team Fort

Page 77Strictly Confidential. For Team Members’ use only.

F.Y. 2010-11-March-‘Rock on Club’ Branches

Mr.Pradip Baishya & Team R.G.Barua

Mr.Uday S Indu & Team South Kolkata

Mr.Avradeep Mukherjee & Team Salt Lake V

Mr.Ranjeet Kumar & Team Bhagalpur

Team Garia

Mr.Bikash Ranjan Roy & Team Giwahati B

Page 78Strictly Confidential. For Team Members’ use only.

F.Y. 2010-11-March-‘Rock on Club’ Branches

Mr.Atul Ranjan & Team Gomti Nagar

Mr.Akhilesh Mittal & Team Ajmer

Mr.Gaurav Mehrotra & Team Agra

Mr.Vijendra Kr.Sharma & Team Noida 29

Mr.Tanmay Dixit & Team Kanpur

Mr.Amit Babbar & Team Ashok Vihar

Page 79Strictly Confidential. For Team Members’ use only.

F.Y. 2010-11-March-‘Rock on Club’ Branches

Mr.M Shyam Kumar & Team Secundarabad

Mr.P Radhankrishna Velldi & Team Kukatpally

Mr. S Karthick & Team Salem

Ms.C.K.Vanitha & Team Jaya Nagar

Mr.K.Bhupathi & Team Karur

Ms.Chitra Mondal & Team Kottivakkam

![Seite 1 Titelblatt - Weiach April.pdf · bbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbb)lqdq]hq 'hu *hphlqghudw](https://img.pdfslide.net/doc/110x75/5b9f4c4209d3f2083f8cea1b/seite-1-titelblatt-weiach-aprilpdf-bbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbbblqdqhq.jpg)