Embed Size (px)

Citation preview

TXT e-Solutions Alla frontiera dell’innovazione:

Cloud Managed Services

nel Business Plan di TXT Retail e di TXT Next

Borsa Italiana – April 2016

2

Revenues: 61.5 m€ (+13.1%)

Net Income (Norm.) 3.9 m€ (+17.4%)

Free Cash Flow 8.4% of Rev.

NFP: 8.3 m€

FY 2015 Results

5 years CAGR +11% p.a.

FY 2015

3

The TXT Opportunity

Fashion, Luxury & Specialty Retail

• 1.000+ Tier 1 and Tier 2 Companies

World-wide;

• 2.500+ Tier 3

• «Digital Transformation» of the Retail

Industry is the driving force behind the

Omni-channel revolution

• Omni-channel challenges drive a growing

demand for End-to-End Lifecycle

Management Solutions

• A global market opportunity of 1.2+ b€,

growing 8+% CAGR till 2020

Aerospace, Automotive & Transport

• 200+ Global Aerospace & Aviation large

Groups;

• 200+ Automotive & Rail global Tier-1

• A consolidated industry, posted for long-term

growth at 5% CAGR till 2033, despite short-

term fluctuations

• High R&D and Engineering budgets, under

the pressure of products differentiation,

emerging technologies and environmental &

regulatory challenges

• 230+ b€ externalised R&D & Engineering

services across the entire Product Lifecycle,

growing at 6% CAGR till 2020

40%

60%+12.4% vs. 2014

+14.2% vs. 2014

4

Aerospace & Aviation

5-Years Strategy

5

TXT Next: Changing Gears in International Development

6

TXT Next + Pace: Well Positioned to Capture the Market Opportunity

25+ Years Working with Industry Leaders World-wide

OEMs – Fixed & Rotary Wings Airlines & Lessors1st Tier Suppliers & MROs

Academia & Research

7

TXT Next + Pace: Well Positioned to Capture the Market Opportunity

Deep Knowledge of the Aerospace & Aviation Industry, spanning the entire Product Life-cycle

AIRBORNE

SOFTWARE

FLIGHT

SIMULATION

DIGITAL

MANUFACTURING

DESIGN &

ENGINEERING

MARKETING &

PROCUREMENT

OPERATIONS

SUPPORT

PACETXT Next

Inside our Customers’ PRODUCTS Inside our Customers’ CORE PROCESSES

8

TXT Next + Pace: Well Positioned to Capture the Market Opportunity

Delivering GloballySelling Globally

TEAMS:• Milano (I)• Torino, Genova (I)• Berlin (D)• Munich (D)• Touluse (F)• Yeovil (UK)• Sassenheim (NL)

• Seattle (USA)

70+ Customers

300+Engineers

9

TXT Next 5-years Strategic Plan: Accelerate International Growth …

• … as «Engineering Solution» Partner, leveraging the «People + IP» paradigm:

– Exploiting complementary TXT-PACE domain knowledge, technology skills & software

assets across a single, global Customer Base;

– Organically …

– … and through further Acquisitions

BENEFIT TO THE CLIENTS

BENEFIT TO PROVIDERS

• Time To Market • Cross-industry Fertilization• Increased Efficiency• Cost Competitiveness

• Reusability / Productivity• Pricing Power / Margins• Barriers to Entry• Competitive Differentiators

10

TXT Next 5-years Strategic Plan: Accelerate International Growth …

• … Investing in innovative Software Products:Airborne Software, Simulation & Operations Support

Digital Manufacturing

Design, Marketing & Operations Support

PACE TXT Next

11

TXT Next 5-years Strategic Plan: Accelerate International Growth …

• … investing in innovative Cloud-based models to deliver Solutions & Managed Services;

Some examples …

CLOSED-LOOP FLIGHT

PLANNING, FLIGHT OPTIM.

& DATA ANALYSIS SERVICE

…..Managed Services for Centralized Management

(preparation, update, etc.) & Analysis of Airborne Systems

Operational Data, according to DO200 regulations

Managed Service for Software Maintenance of a Fleet of

Simulators provided by means of a Cloud-Based Health

Monitoring & Fix / Deploy System

Managed Services for Cloud-based post-flight analysis of

flight performance “big data” to feedback flight planning and

flight performance optimisation activities

AIRBORNE

NAVDATA MANAGEMENT

MANAGED SERVICE

SIMULATOR FLEETS

LONGTERM REMOTE

MAINTENANCE SERVICE

Fashion, Luxury & Specialty Retail

5-Years Strategy

TXT Retail Target Processes: The «Merchandise Lifecycle»

The Omnichannel Retailers’ «Merchandise Lifecycle»:

A strategic & complex End-to-End process that involves many actors that real-time collaborate to

generate growth & profit by cost-effectively selling compelling customer focused collections

across multiple interacting retail channels

How Industry Transformation impacts Omnichannel Retailers’ Key Business Processes?

13

TXT Retail: Unique Customer Base of 350+

- 15+ New Major Customers and 50+ Go-Lives of Major Projects, each Year …- … across all Segments, Business Models & Geographies

Mixed Goods

Luxury Global Brands Fast Fashion Specialty

Luxury Global Brands Fast Fashion Mixed Goods

Department Store

TXT Retail: Focused on the End-to-End Merchandise Lifecycle

15

Core to Retailers’ competitive

differentiation is the

Merchandise Lifecycle, the

end-to-end process that

encompasses:

- Understanding customer

needs and opportunities,

- Devising a brand and product

strategy,

- Developing and sourcing a

compelling collection,

- Optimizing the assortment

across markets and channels,

- Buying and delivering the

products

- Managing the sell out to

optimise the return on

merchandise investment.

Common DataModel

Integration ServicesWorkflow

Management

Calendar

ManagementReporting

• Strategic Plan

• Merchandise Plan

• Channel Plan

• OTB Management

• Plan by Attribute

• Assortment Strategy

• Channel Distribution

• Item Lifecycle Mgmt

• Item Plan

• Order Creation

• Trend R & D

• Concept & Design

• Collection Mgmt

• Industrialization

• Costing/Sourcing

• Forecasting

• Allocation

• Store Replenishment

• DC Replenishment

• Promos & Markdowns

• Initial Pricing

• Fashion S&OP

• Plan & Schedule

• Delivery Mgmt

• Vendor Collaboration

TXT Retail Services

End-to-end Merchandise Lifecycle Management

TXT Retail: Well Positioned to Capture the Global Market Opportunity

Software43%

Services57%

Italy11%

Germany21%

France21%

UK & Nordics21%

APAC8%

Spain2% North Am.

16%

TXT Retail 5-years Strategic Plan: Global Leadership

17

Execution

• Geography: Global Leadership

– Consolidate Europe

– Expand in North America

– Start-up Asia-Pacific

• Industry: from mainly Lower Tier-1 and Upper Tier-

2, Fashion & Luxury, to:

– A growing range of Retail Segments

– Super Tier 1 and Lower-Tier 2 and Tier 3 Retailers

Vision & Innovation

• The Offering: Cloud-based Managed Services & Cloud Deployment

• Customer Dimension: Capturing wider & deeper customer attributes in

Merchandise Lifecycle Management

• The Software: Another leapfrog jump ahead of competitors in Technology

• AgileFit: Extending breadth of process coverage & depth of verticalisation

From Software VendorTo Transformational Enablerin the Omni-channel Journeyof Global Retailers

TXT Retail Strategy Pillars: Leading-edge Technology

TXT Retail enables Customer-

driven Merchandising Excellence

through an End-to-End

Merchandise Lifecyle

Management Software featuring:

- A unified database that informs

the End-to-End Merchandise

processes

- Real-time integration across all

Merchandise Lifecycle processes

- Collaboration across all actors in

the Merchandise Lifecycle

processes, blending art, science &

mobility as appropriate

- Productivity enhancing UI: “2

hours adoption” thanks to the right

UI for each User & Task.

- Flexible configuration: it helps

you adopting business process best

practices, and flexes as the market

& your organization change

The 1st & onlyEnd-to-End Merchandise Lifecycle Management Software

TXT Retail Strategy Pillars: AgileFit - Business Best Practices «Ready to Go»

MitigateProject

Risk

Reduce Project Costs

Faster Time to Benefits

HigherROI

Workbook DesignSolution Design Interface Specification

Performance TestsReference Application Project Deliverables

22

TXT Retail Strategy Pillars: Cloud-based Solutions & Services

• Extend Value Proposition to include Cloud-based Managed Services and Merchandise Lifecycle

Management Cloud Services (SAAS)

• This reduces TCO of TXT Retail & strengthens TXT Retail’s position as “Transformational Enabler” for

its Customers

20

Cloud Managed Services

system

Man

ag

ed

Serv

ices

Customer

Merchandise Cloud Services (SAAS)

SaaS

Customer

Customersystem

ApplicationManagement

Assistance

System Administration

Infrastructure management

(VMs)

Infrastructure

Customer

ApplicationManagement

Assistance

System Administration

Infrastructure management

(VMs)

Infrastructure

Merchandise Lifecycle Management Cloud Strategy

Industry Segment Fashion, Luxury and Apparel Solution Areas Potential

Customer Tier

N. of Companies*

Cloud StrategyTarget Revenue

ModelSupply Chain Collaboration

Collection Lifecycle

Management

Store Forecasting and Replenishment

Merchandise Financial Planning

Assortment Planning and

Buying

Tier1 23Cloud Managed

Services

License,Maintenance,

Services

Tier2 233Cloud Managed

Services

License,Maintenance,

Services

Tier3 1500Merchandise

Lifecycle SAASSet Up plus

Recurring Fees

TXT Retail Strategy Pillars: Cloud-based Solutions & Services

*TXT Management Estimates 24

Market Mature, TXT Ready

Early Adopters, TXT Ready for Pilot Customers

Market Maturing, TXT Preparing for Pilots

Market Not Ready

TXT Retail Strategy Pillars: The Customer Dimension

22

Sales Budgeting:Multi-Channel Sales Budget

TXT Retail

• Partnerships, e.g. FirstInsight for Consumer Collaboration on Product Evaluation

• Customer Projects, e.g. Starboard to drive better Assortments using Consumer Demographic Information

• Customer-driven Pilots, to experiment new ideas and approaches

TXT Retail 5-years Global Leadership Goal

23

Tier 1

Tier 2

Tier 3

REVENUE BY CUSTOMER TIER

APAC

Continental Europe

North America

UK&Nordics

REVENUE BY REGION

Luxury

Brand

Specialty Fashion

Specialty Others

Department Store/Travel

Retail

REVENUE BY INDUSTRY SEGMENT

Packaged Solutions

300M$

ERP Extensions, Custom, Maintenance of Obsolete

Applications 900M$

IT SPEND FOR MERCHANDISE LIFECYCLE

Confidential & Proprietary

TXT Retail: The End-to-End Merchandise Lifecycle Opportunity

24

Competitive Differentiation and Enablers for Customer Success

Gain MarketshareExpand

Market

TXT Management Estimates

TXT10%

Others90%

IT SPEND BY TYPE OF SOLUTIONS

Summary & Financial Details

25Confidential & Proprietary

Management

Alvise Braga Illa – Chairman

After graduating at the Polytechnic Institute in Milan, Mr Braga Illa was for 10 years in research and teaching at theLincoln Laboratory and Massachusetts Institute of Technology, innovating in satellite technology, opticalcommunication and network systems. He directed the R&D Labs at Italtel, founded Zeltron S.p.A. and managed therestructuring of Ducati Energia as General Manager. Mr. Braga Illa founded TXT Automation Systems, later sold to ABB(1997), and TXT e-solutions (1989).

Marco Guida – CEO

Graduated in Electronic Engineering, Marco Guida managed innovative IT projects in various areas of themanufacturing operations of Pirelli Group until 1994, when he joined TXT e-solutions. Initially responsible for AdvancedInformation Systems, in January 2000 promoted to Vice President. As Director of International Operations hesuccessfully led the transformation of TXT e-solutions from an Italian to an International Group. Since 2009 he is ChiefExecutive Officer of TXT Group.

Paolo Matarazzo – CFO

After graduating from Milan’s Bocconi University and majoring in business administration at the University of San Diego(California), has had significant experience in the financial world. He was initially an analyst in London for three yearsand then worked for the Recordati Group for seven years, with responsibility for treasury management. In the followingseven years he was Head of Finance, Administration & Control in Europe for Eurand, a company listed on NASDAQ. Hejoined TXT in May 2007 as Group CFO.

The Basis for Success

• TXT Retail

– Global Retail Industry is large, growing & dynamic: e-commerce, new business models, new players

– Planning is a «big niche» & a growing investment area for Retailers

– TXT has a unique offering and a solid competitive position, sustained by constant innovation

– Large, world-wide base of happy global customers.

– Global presence with the opportunity to further expand in North America and APAC markets.

• TXT Next + PACE

– Large, innovative & healthy target markets, with long-term positive trends

– Highly fidelised customer base

– Solid team with 30+ years of domain expertise

– Specialised know-how consolidated in Sw assets: differentiation, competitive advantage and margins

– Leader with the opportunity to continue growing in Europe, both organically and through targeted

acquisition, and to accelerate international development

27

Why Invest in TXT?

• International profile: >55% of Revenues from Int’l markets, and growing

• Growth in Revenue, Profit & Cash

• Large fidelised customer base of 350+ blue-chip customers: a key asset in good & bad

times, hard to replicate for new competitors

• Solid presence in large, healthy markets with very high growth potential

• Upside growth potential: opportunity to capitalize existing product & know how in other

industries

• Innovation is in our DNA: historically a «1° mover» in many markets

• Solid & stable management team, who are shareholders of TXT

• Cash & Stock Dividend policy

• Expanding Shareholder base: co-workers & management; private & retail; institutional

investors

• Financially solid and self-sustainable

2015 – Growth of Revenues and development investments

29

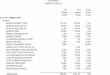

€ thousand 2015 % 2014 (1)2014 non

recurring

2014

Normalized

(2)

%Var %

vs 2014

Var % vs 2014

Normalized

REVENUES 61.540 100,0 55.878 (1.468) 54.410 100,0 10,1 13,1

Direct costs 29.189 47,4 26.455 (407) 26.048 47,9 10,3 12,1

GROSS MARGIN 32.351 52,6 29.423 (1.061) 28.362 52,1 10,0 14,1

Research and Development costs 5.118 8,3 4.698 4.698 8,6 8,9 8,9

Commercial costs 12.681 20,6 11.094 11.094 20,4 14,3 14,3

General and Administrative costs 7.893 12,8 6.839 6.839 12,6 15,4 15,4

EBITDA before Stock Grant 6.659 10,8 6.792 (1.061) 5.731 10,5 (2,0) 16,2

Stock Grant 740 1,2

EBITDA 5.919 9,6 6.792 (1.061) 5.731 10,5 (12,9) 3,3

Amortization, depreciation 1.124 1,8 1.325 1.325 2,4 (15,2) (15,2)

OPERATING PROFIT (EBIT) 4.795 7,8 5.467 (1.061) 4.406 8,1 (12,3) 8,8

Financial income (charges) (151) (0,2) (249) (249) (0,5) (39,4) (39,4)

EARNINGS BEFORE TAXES (EBT) 4.644 7,5 5.218 (1.061) 4.157 7,6 (11,0) 11,7

Taxes (762) (1,2) (1.046) 197 (849) (1,6) (27,2) (10,2)

NET PROFIT 3.882 6,3 4.172 (864) 3.308 6,1 (7,0) 17,4

(1) Official Financial Reporting.

(2) Income Statement 2014 includes non-recurring income of 1.468k€ and non-recurring costs of 407k€. In order to compare

performance w ith current year, f inancial results 2014 have been "Normalized" excluding non-recurring Revenues and Costs. Taxes

have been calculated pro-rata.

Strong Balance Structure

30

€ thousand 31.12.2015 31.12.2014 Var

Intangible assets 14.692 15.079 (387)

Tangible assets 1.361 1.249 112

Other fixed assets 2.079 1.692 387

Fixed Assets 18.132 18.020 112

Inventories 2.075 1.821 254

Trade receivables 25.032 18.571 6.461

Other short term assets 2.759 2.197 562

Trade payables (1.422) (1.540) 118

Tax payables (1.291) (1.117) (174)

Other payables and short term liabilities (16.090) (13.606) (2.484)

Net working capital 11.063 6.326 4.737

Severance and other non current liabilities (3.830) (3.841) 11

Capital employed 25.365 20.505 4.860

Shareholders' equity 33.624 28.970 4.654

Net financial debt (8.259) (8.465) 206

Financing of capital employed 25.365 20.505 4.860

Dividends & Shareholder‘s Return in the last 5 Years

• Dividends•2011: 1 € /share (extraordinary, rebased) •2012: Free Share Distribution 1:1•2013: 0.20 € /share (rebased)•2014: Free Share Distribution 1:1•2014: 0.25 € / share•2015: Free Share Distribution 1:10•2015: 0.25 € / share•2016: 0.25 € / share

•Share Price•31.12.2010: 1.51€/share (rebased for free share distribution)•29.2.2016: 7.76€ /share

TXT Market Capitalization (m€)

Free share distribution 1:1

32

Free share distribution 1:10

Free share distribution 1:1

Dividend 2.6m€

Dividend 2.6m€

Dividend 2.1m€

Dividend 10.3m€

Shareholding Structure – December 2015

33

Market42,4%

Treasury Shares10,3%

E-Business Consulting25,6%

A. Braga Illa13,8%

Management7,9%

![Budget 2014: Budget plan [French]](https://img.pdfslide.net/doc/110x75/55cf9902550346d0339afd61/budget-2014-budget-plan-french.jpg)