Embed Size (px)

Citation preview

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 1/42

Buy It Now

eBay shares are undervalued

May 26, 2010

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 2/42

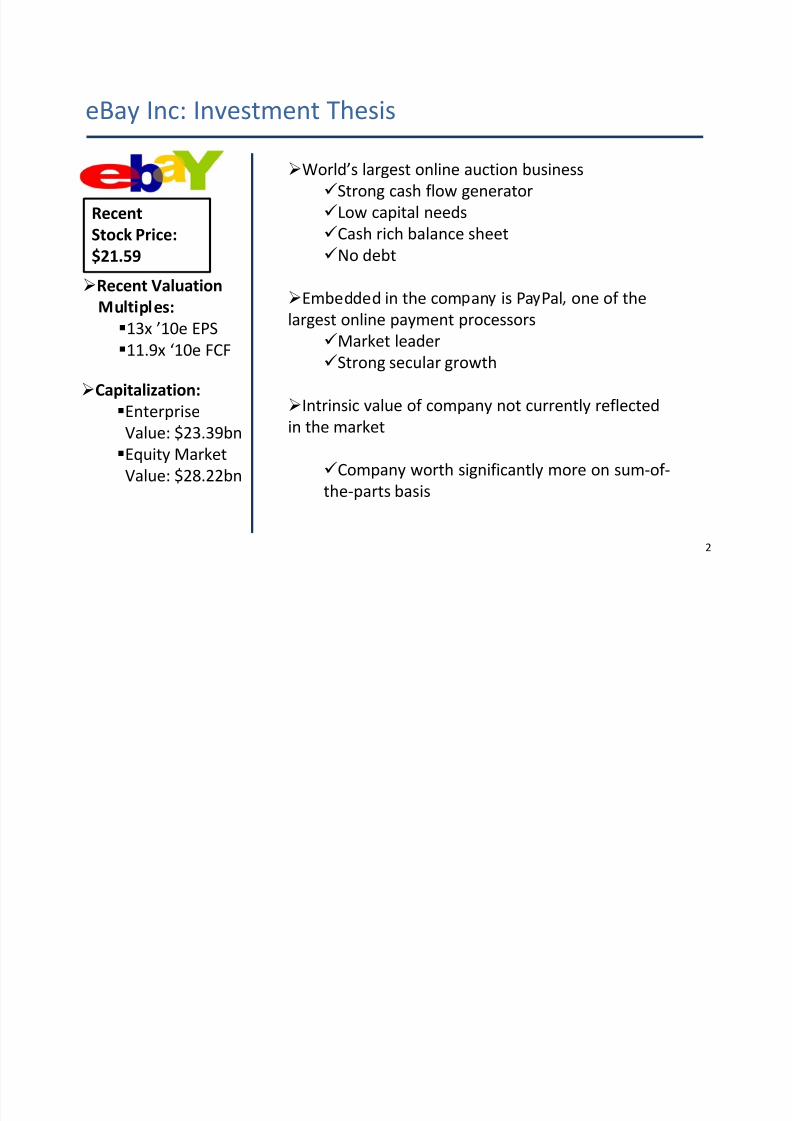

RecentStock Price:

$21.59

Recent Valuation

World’s largest online auction business

Strong cash flow generator

Low capital needsCash rich balance sheet

No debt

Embedded in the com an is Pa Pal one of the

eBay Inc: Investment Thesis

Capitalization:

Enterprise

Value: $23.39bnEquity Market

Value: $28.22bn

u p es:

13x ’10e EPS

11.9x ‘10e FCF

largest online payment processorsMarket leader

Strong secular growth

Intrinsic value of company not currently reflected

in the market

Company worth significantly more on sum-of-

the-parts basis

2

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 3/42

eBay is misunderstood by The Street...

•eBay is still viewed as a tech company,

although it should be viewed as both a

“retailer”/auctioneer and a payment processor

within the eBay portfolio, the company is not being

priced appropriately

• On a sum-of-the-parts basis, eBay remains

significantly undervalued by 33-52% over twoyears

3

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 4/42

Opportunities for value creation

• As eBay’s share price has continued to

stagnate, the case for shareholder activismgrows

Separation of Marketplace and Payments

us nesses Factor loan receivables to eliminate credit risk

Improve transparency on payments business

Return cash to shareholders via dividend or share

buyback program

4

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 5/42

A brief background on eBay

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 6/42

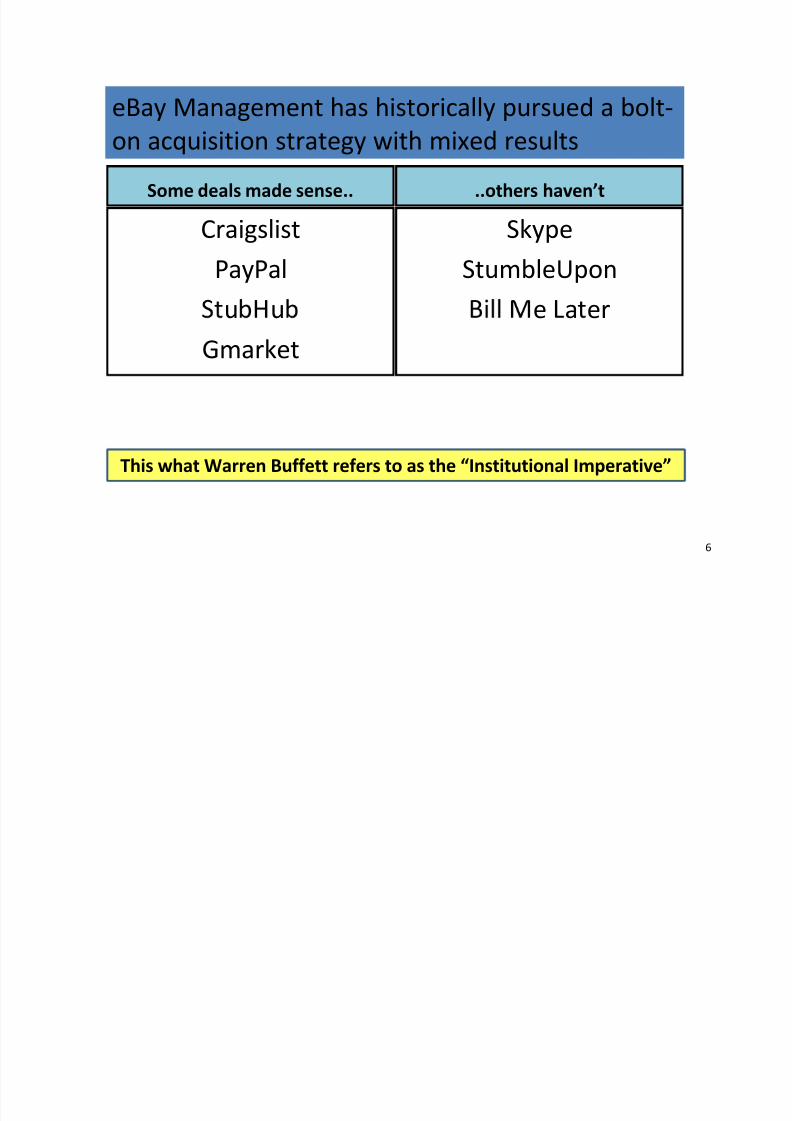

eBay Management has historically pursued a bolt-on acquisition strategy with mixed results

Craigslist

PayPal

Skype

StumbleUpon

..others haven’tSome deals made sense..

u uGmarket

e a er

6

This what Warren Buffett refers to as the “Institutional Imperative”

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 7/42

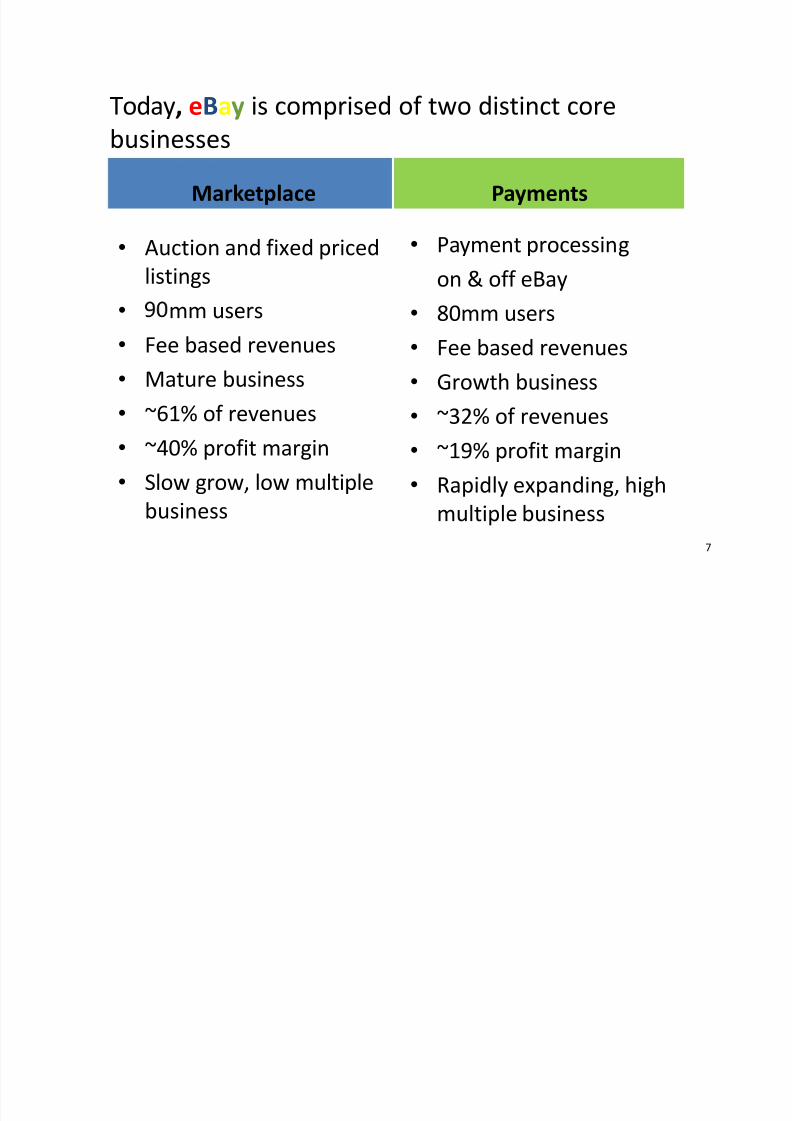

Today, eBay is comprised of two distinct corebusinesses

• Auction and fixed priced

listings

• Payment processing

on & off eBay

Marketplace Payments

• mm users• Fee based revenues

• Mature business

• ~61% of revenues

• ~40% profit margin

• Slow grow, low multiple

business

• 80mm users• Fee based revenues

• Growth business

•~32% of revenues

• ~19% profit margin

• Rapidly expanding, high

multiple business

7

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 8/42

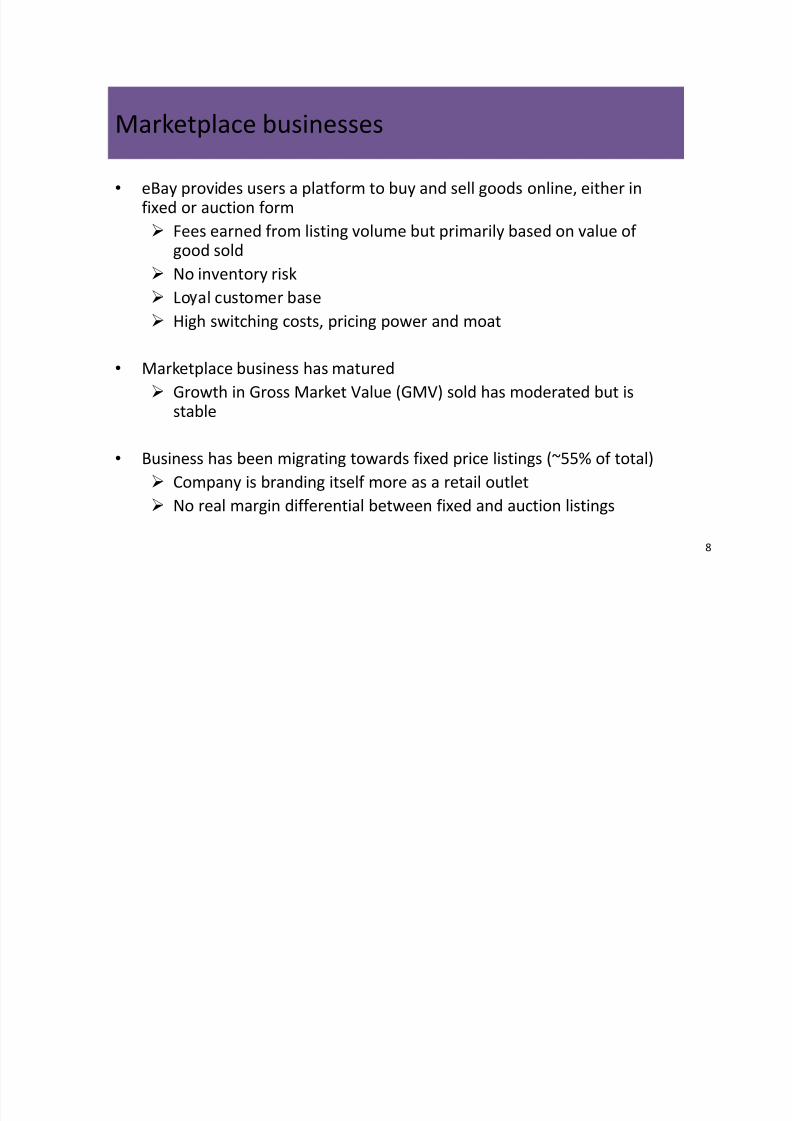

• eBay provides users a platform to buy and sell goods online, either in

fixed or auction form Fees earned from listing volume but primarily based on value of

good sold

No inventory risk

Lo al customer base

Marketplace businesses

High switching costs, pricing power and moat

• Marketplace business has matured

Growth in Gross Market Value (GMV) sold has moderated but isstable

• Business has been migrating towards fixed price listings (~55% of total)

Company is branding itself more as a retail outlet

No real margin differential between fixed and auction listings

8

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 9/42

The Marketplace business is in the midst of

a multi-year turnaround

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 10/42

eBay’s turnaround story

• eBay began to have difficulty attracting sellers

and buyers due to fee adjustments and pooruser experience

The company has since taken a number of steps as part of it’s 3-year plan to

Attracting sellers by offering lower insertion fees,

higher final value fees

Improving search algorithms, web interfaceProviding top seller discounts

Introducing buyer protection

10

rig t t e s ip

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 11/42

The Marketplace business is on its way tobecoming stronger than ever

eBay remains one of the top shopping destinations on the web

The eBay brand is synonymous with value, selection and security

Sticky customer base as many sellers rely on eBay for their livelihood in an industry with no real competitor

Increasingly frugal consumer will come to eBay in search of good prices

Core auction business remains one-of-a-kind

e ay ne wor commun y s a mos mposs e o rep ca e, g v ng e company a w e moa

11

eBay should be thought of in many respects as a royalty business, offeringcustomers access to it’s platform and it’s invaluable outlet to the world’s

buyers for a fee.

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 12/42

Payments business

• PayPal facilitates payments betweenbuyers and sellers for purchases on andoff eBayAllows bu ers to kee sensitive information

secure and private while shopping onlineProvides for convenient paying and buyer

protection

Fosters incremental sales at lower costs to

merchants due to trust and convenience PayPaloffers

12

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 13/42

PayPal is a unique and valuable asset

Dominant market leader in rapidly expanding online

payment industry Secular tailwind in the form of increased e-

commerce and use of plastic

network of users and merchantsAdoption growing quickly outside the US

Takes virtually no credit risk*

Earns float on +2bn customer balances

Earns fees primarily based on market value of transaction

13

*see slide on “Bill Me Later”

PayPal is slowing becoming the crown jewel of eBay but the value of the business is not currently

reflected in the company’s share price

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 14/42

eBay’s other revenue generators

• Advertising

(12% revenue; Marketplace/PayPal mix)

• Skype (equity interest)

•

• Other web properties (shopping.com,

rent.com)

14

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 15/42

eBay’s two core business are worth more today

than is currently reflected in it’s share price

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 16/42

Proposal I: Spin-off PayPal

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 17/42

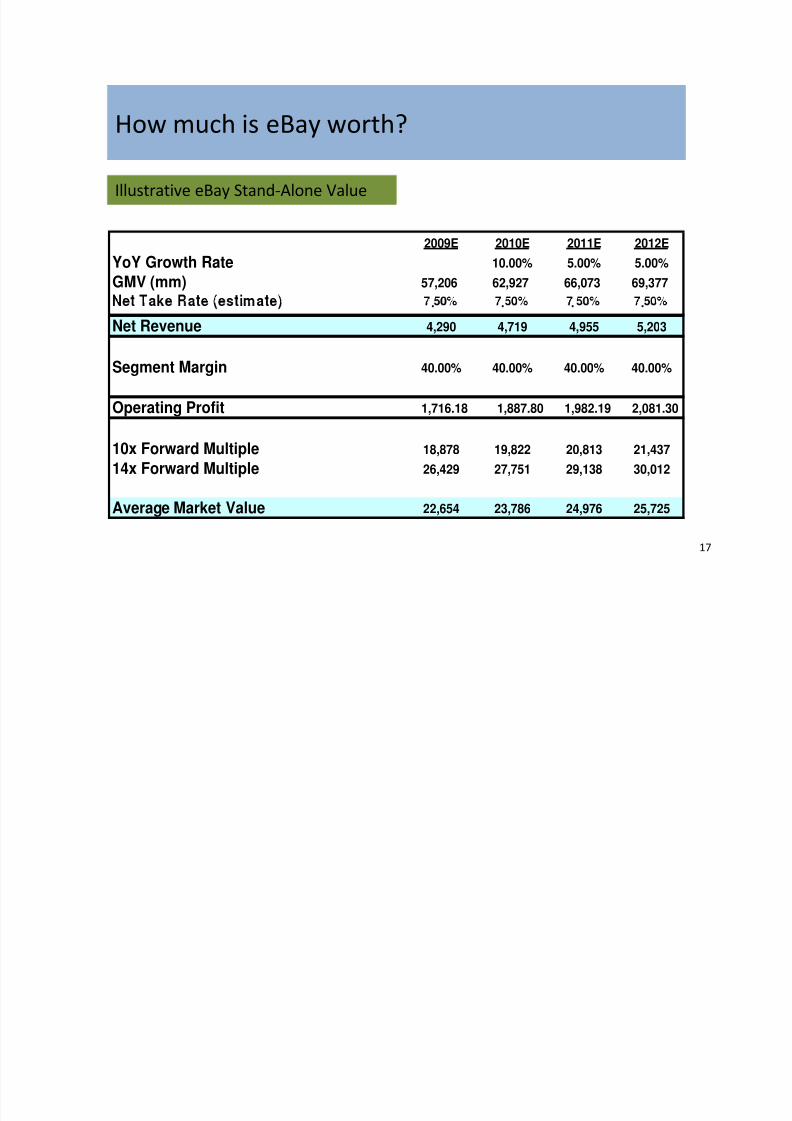

How much is eBay worth?How much is eBay worth?

Illustrative eBay Stand-Alone Value

2009E 2010E 2011E 2012E

YoY Growth Rate 10.00% 5.00% 5.00%

GMV (mm) 57,206 62,927 66,073 69,377

17

. . . .

Net Revenue 4,290 4,719 4,955 5,203

Segment Margin 40.00% 40.00% 40.00% 40.00%

Operating Profit 1,716.18 1,887.80 1,982.19 2,081.30

10x Forward Multiple 18,878 19,822 20,813 21,437

14x Forward Multiple 26,429 27,751 29,138 30,012

Average Market Value 22,654 23,786 24,976 25,725

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 18/42

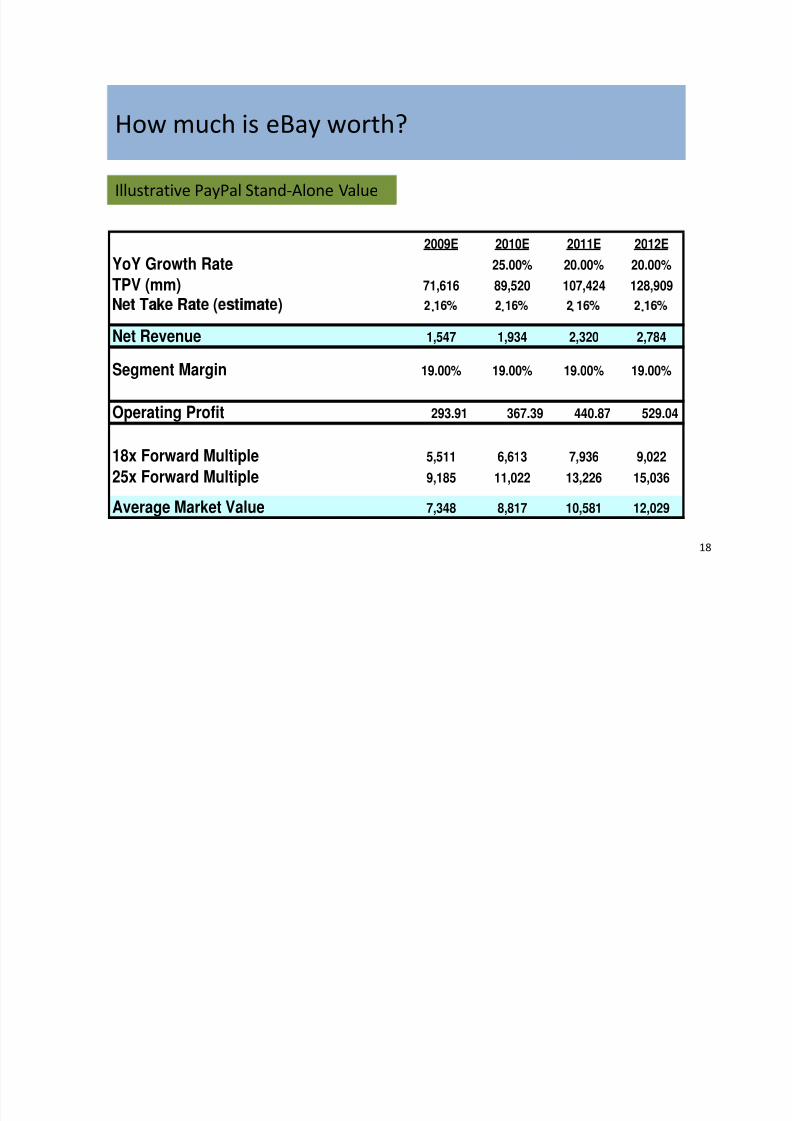

Illustrative PayPal Stand-Alone Value

How much is eBay worth?

2009E 2010E 2011E 2012E

YoY Growth Rate 25.00% 20.00% 20.00%

TPV (mm) 71,616 89,520 107,424 128,909

18

. . . .

Net Revenue 1,547 1,934 2,320 2,784

Segment Margin 19.00% 19.00% 19.00% 19.00%

Operating Profit 293.91 367.39 440.87 529.04

18x Forward Multiple 5,511 6,613 7,936 9,022

25x Forward Multiple 9,185 11,022 13,226 15,036

Average Market Value 7,348 8,817 10,581 12,029

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 19/42

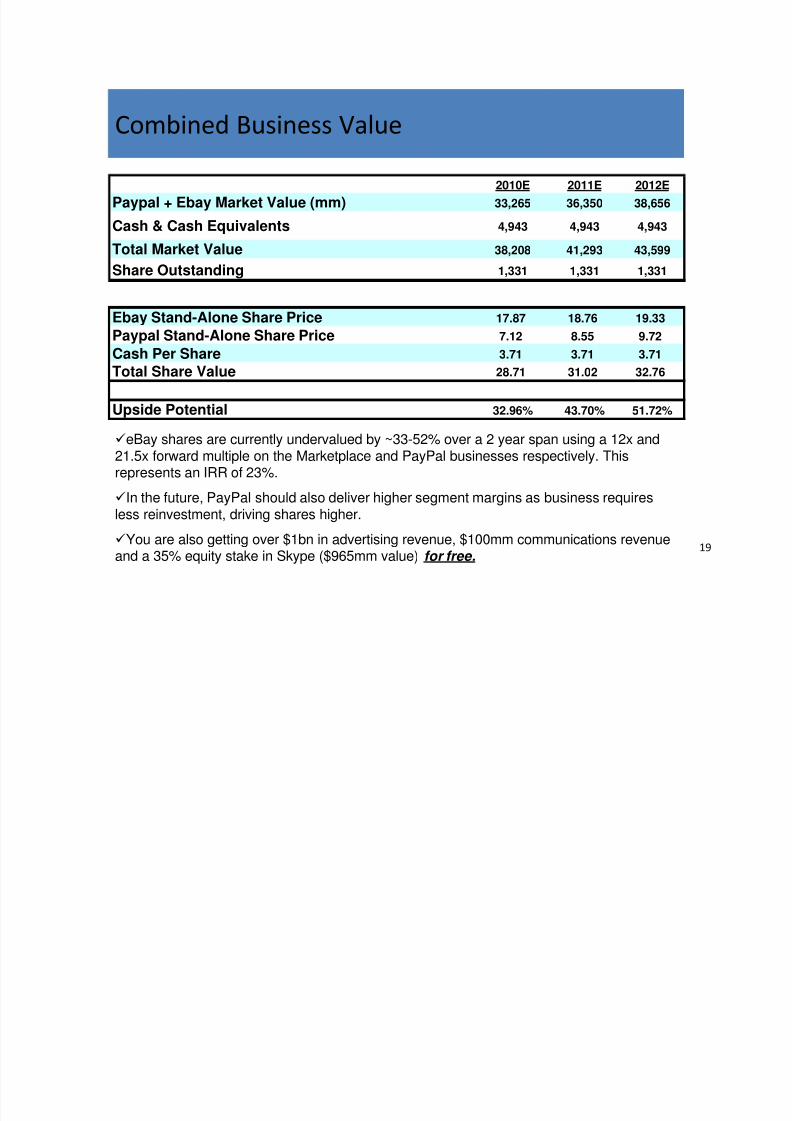

Combined Business Value

2010E 2011E 2012E

Paypal + Ebay Market Value (mm) 33,265 36,350 38,656

Cash & Cash Equivalents 4,943 4,943 4,943

Total Market Value 38,208 41,293 43,599

Share Outstanding 1,331 1,331 1,331

eBay shares are currently undervalued by ~33-52% over a 2 year span using a 12x and21.5x forward multiple on the Marketplace and PayPal businesses respectively. Thisrepresents an IRR of 23%.

In the future, PayPal should also deliver higher segment margins as business requiresless reinvestment, driving shares higher.

You are also getting over $1bn in advertising revenue, $100mm communications revenueand a 35% equity stake in Skype ($965mm value) for free.

19

Ebay Stand-Alone Share Price 17.87 18.76 19.33Paypal Stand-Alone Share Price 7.12 8.55 9.72

Cash Per Share 3.71 3.71 3.71

Total Share Value 28.71 31.02 32.76

Upside Potential 32.96% 43.70% 51.72%

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 20/42

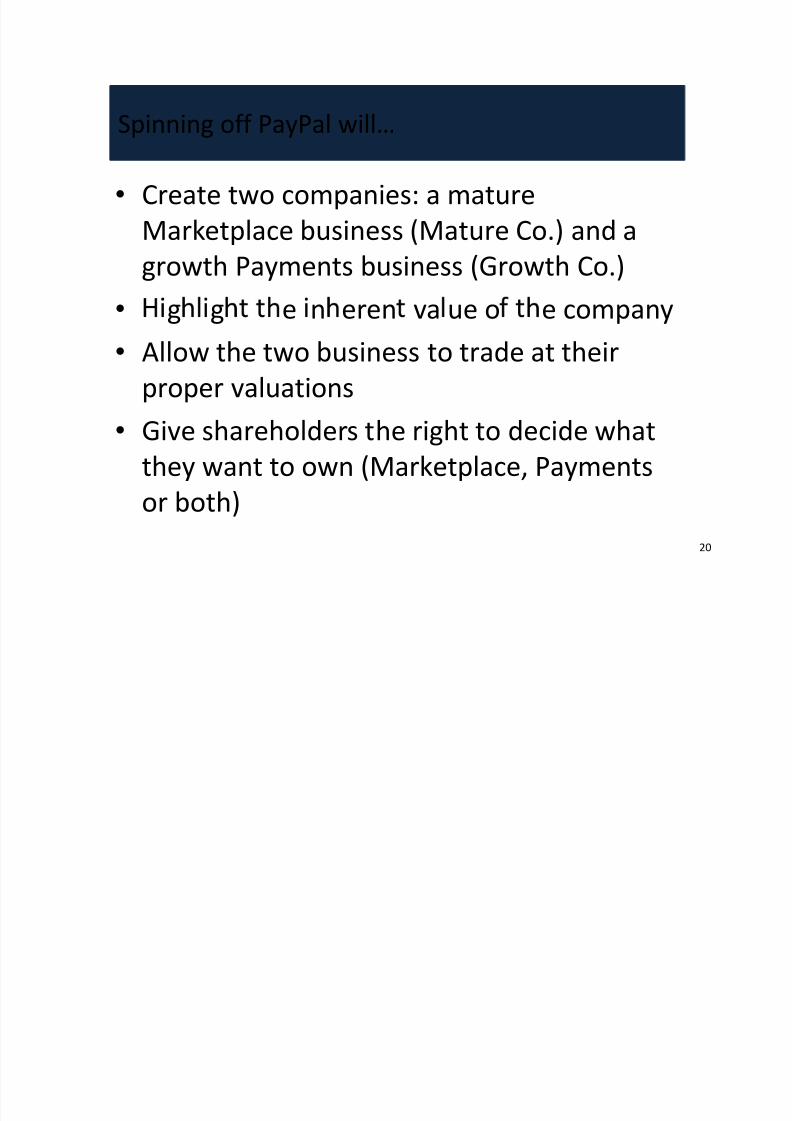

Spinning off PayPal will…

• Create two companies: a mature

Marketplace business (Mature Co.) and a

growth Payments business (Growth Co.)

•

g g e n eren va ue o e company

• Allow the two business to trade at their

proper valuations

• Give shareholders the right to decide whatthey want to own (Marketplace, Payments

or both)

20

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 21/42

Seems simple enough, so what’s theproblem?

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 22/42

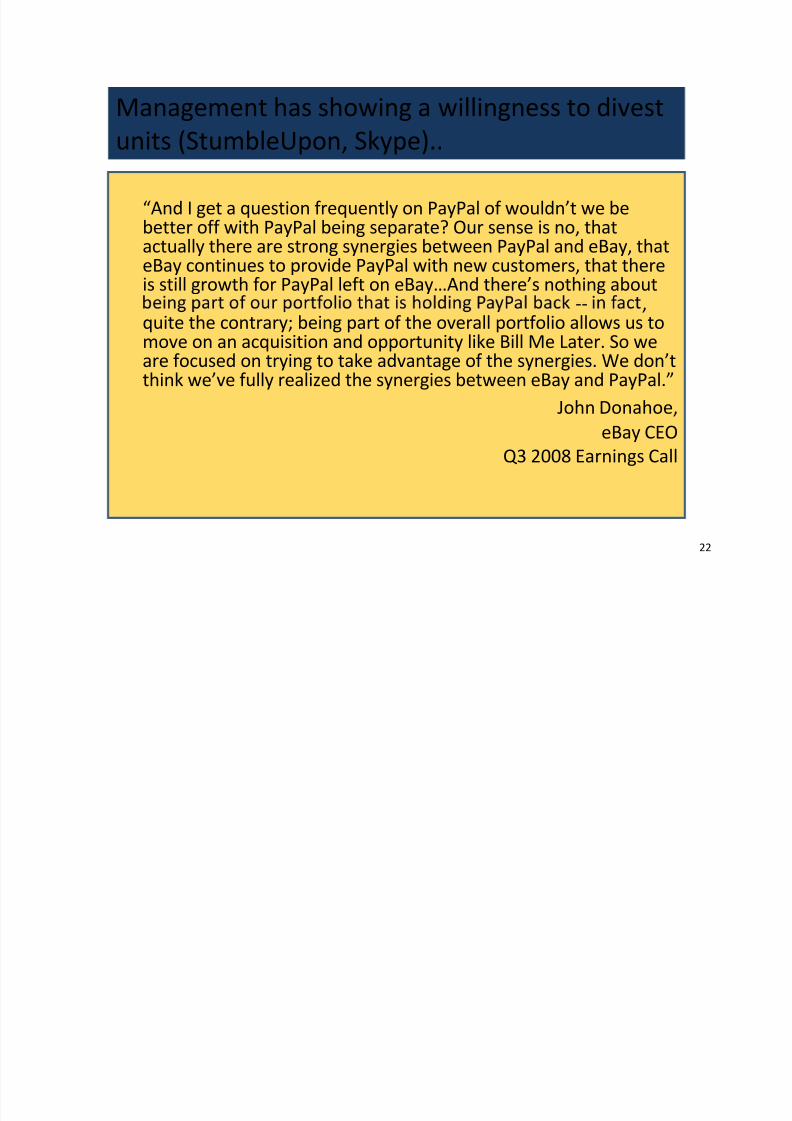

Management has showing a willingness to divestunits (StumbleUpon, Skype)..

“And I get a question frequently on PayPal of wouldn’t we bebetter off with PayPal being separate? Our sense is no, thatactually there are strong synergies between PayPal and eBay, thateBay continues to provide PayPal with new customers, that thereis still growth for PayPal left on eBay…And there’s nothing about

-- ,

quite the contrary; being part of the overall portfolio allows us tomove on an acquisition and opportunity like Bill Me Later. So weare focused on trying to take advantage of the synergies. We don’tthink we’ve fully realized the synergies between eBay and PayPal.”

John Donahoe,

eBay CEOQ3 2008 Earnings Call

22

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 23/42

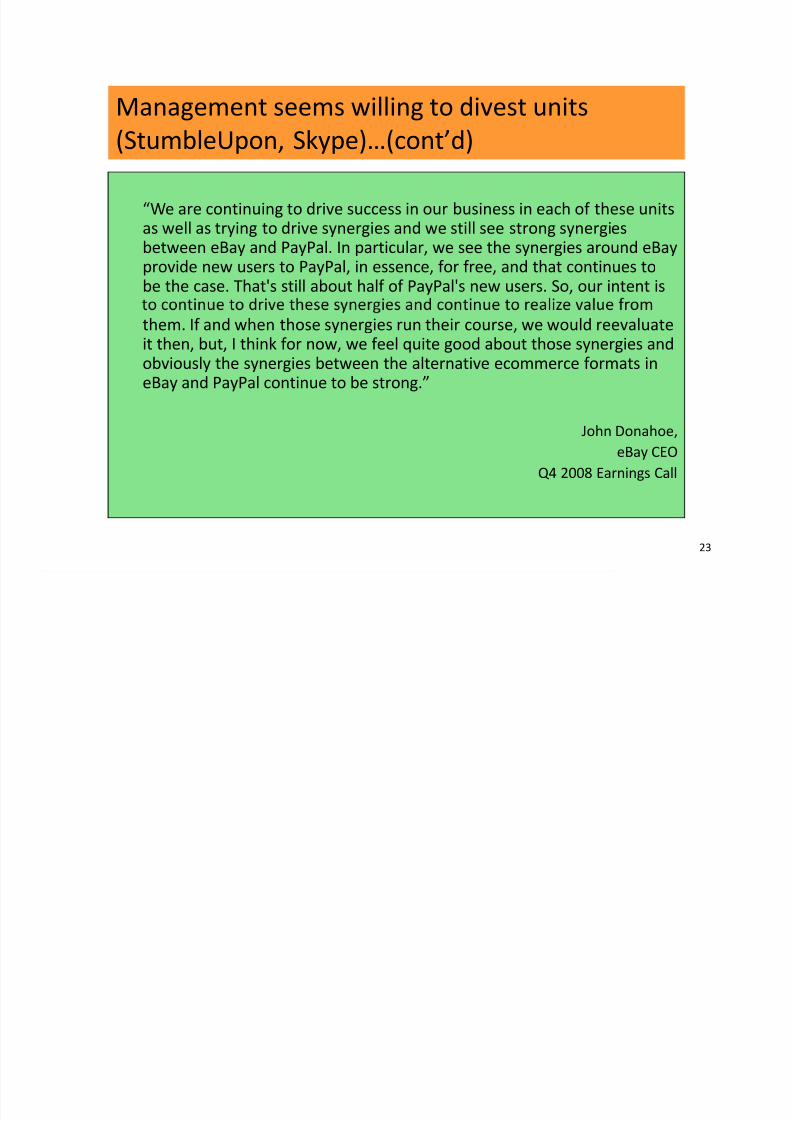

Management seems willing to divest units(StumbleUpon, Skype)…(cont’d)

“We are continuing to drive success in our business in each of these unitsas well as trying to drive synergies and we still see strong synergiesbetween eBay and PayPal. In particular, we see the synergies around eBayprovide new users to PayPal, in essence, for free, and that continues tobe the case. That's still about half of PayPal's new users. So, our intent is

them. If and when those synergies run their course, we would reevaluateit then, but, I think for now, we feel quite good about those synergies andobviously the synergies between the alternative ecommerce formats ineBay and PayPal continue to be strong.”

John Donahoe,eBay CEO

Q4 2008 Earnings Call

23

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 24/42

Management seems willing to divest units(StumbleUpon, Skype)…(cont’d)

“ Is everything on the table? Yes, in the following sense. We viewour job as to drive maximum value for our shareholders. We

believe the best way we can do that is to have strong core

businesses that have synergies we’re extracting and we grow

those businesses and strengthen them over time and that willdeliver the best value to shareholders.”

John Donahoe,

eBay CEO

Q1 2009 Earnings Call

24

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 25/42

…but remains hesitant when it comes to PayPal

“ There continues to be strong synergies between eBayand PayPal. You saw that in the increased penetrationPayPal has had on eBay…eBay continues to provide a

for free and eBay Inc.’s balance sheet allows us toinvest in PayPal’s business and make investments likeBill Me Later that further its position.”

John Donahoe,

eBay CEO

Q1 2010 Earnings Call

25

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 26/42

It’s time to spin-off PayPal

• 18 months later, the situation is worth revisiting

• Management’s rationale for retaining PayPal is no longer justified(i.e., tapping eBay as a source of “free growth”, use of eBay

balance sheet) and relies heavily upon on “synergies"

PayPal has already captured ~60+% of the eBay market (potential$60 GMV

-

PayPal has likely generated enough cash flow of its own to grow the businessgoing forward

As a public company, PayPal would also be able to raise capital of its own

• The view that eBay is “not holding back” PayPal’s

growth is inaccurate and irrelevant PayPal would gain wider acceptance if it weren’t under a

“competitor’s” umbrella

The sole goal of management is the maximization of shareholder

value, which would be accomplished via a PayPal Spin-off 26

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 27/42

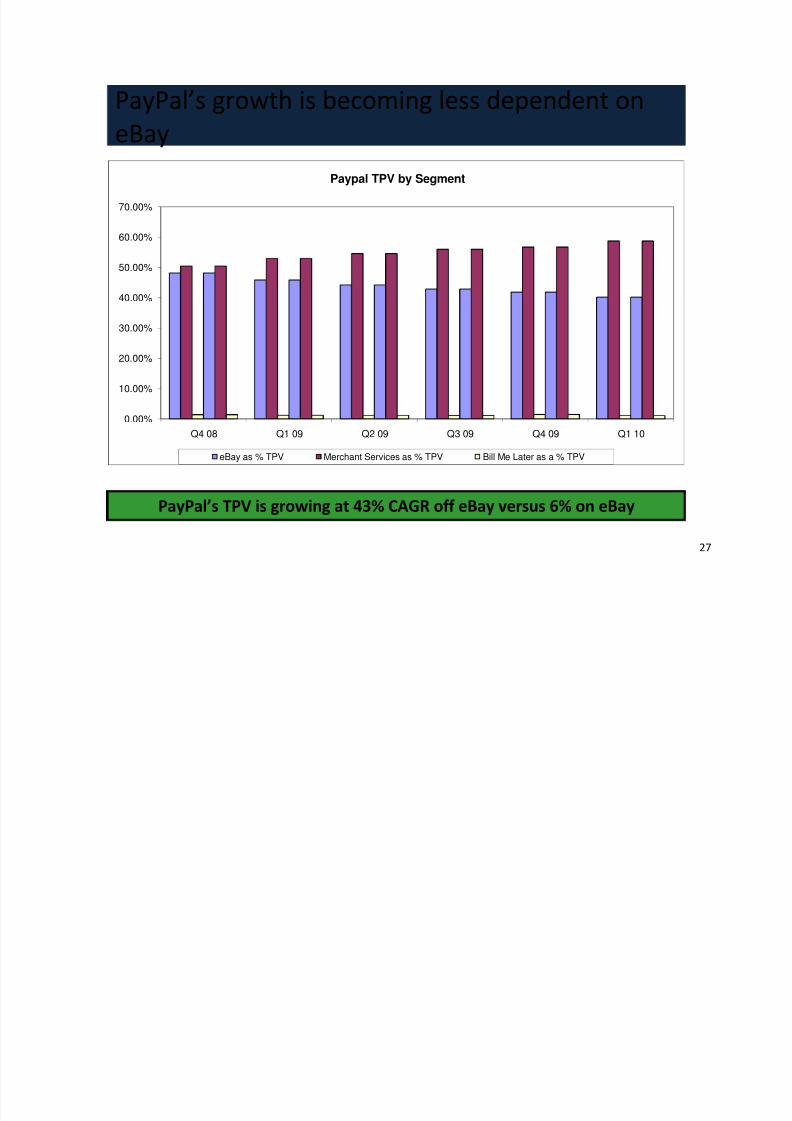

PayPal’s growth is becoming less dependent oneBay

40.00%

50.00%

60.00%

70.00%

Paypal TPV by Segment

0.00%

10.00%

20.00%

30.00%

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10

eBay as % TPV Merchant Services as % TPV Bill Me Later as a % TPV

27

PayPal’s TPV is growing at 43% CAGR off eBay versus 6% on eBay

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 28/42

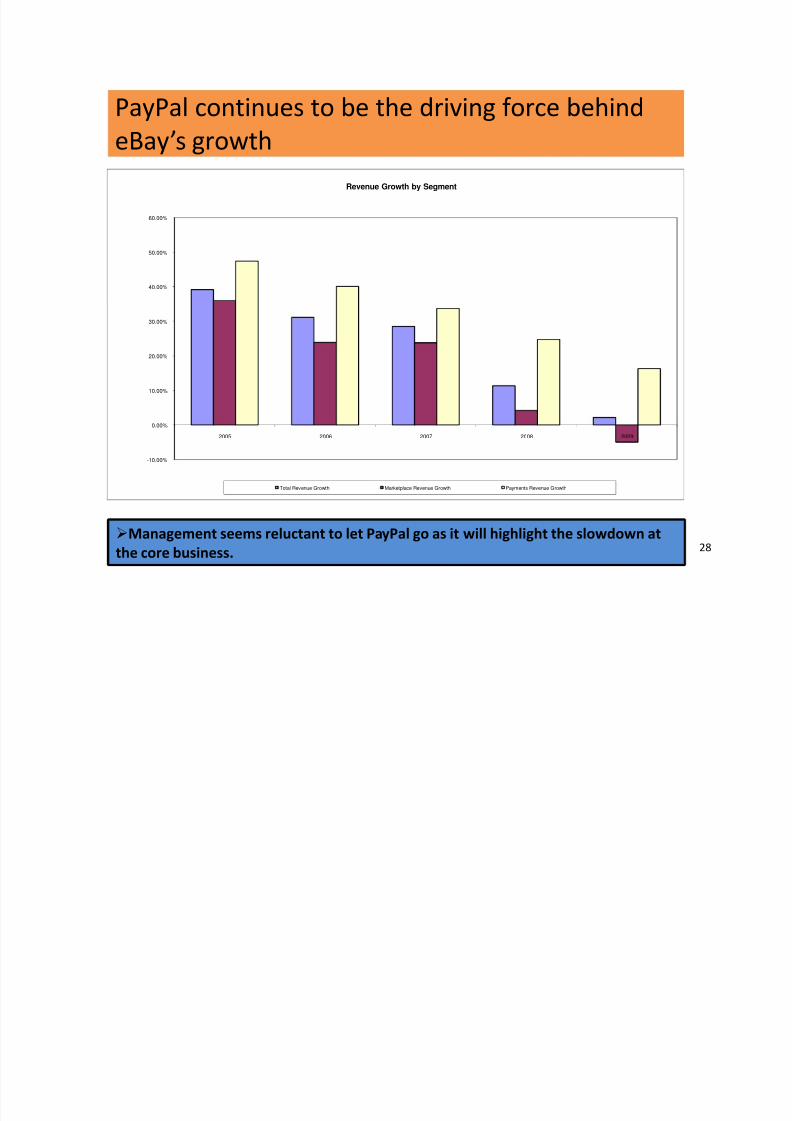

PayPal continues to be the driving force behindeBay’s growth

40.00%

50.00%

60.00%

Revenue Growth by Segment

-10.00%

0.00%

10.00%

20.00%

30.00%

2005 2006 2007 2008 2009

Total Revenue Growth Marketplace Revenue Growth Payments Revenue Growth

28

Management seems reluctant to let PayPal go as it will highlight the slowdown atthe core business.

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 29/42

It’s time to spin-off PayPal..(cont’d)

• However, the proposal has merits:

Allows eBay to focus on fixing its core business

Allows PayPal to grow without being hampered by

eBay’s ongoing restructuring

Allows the market to properly value two distinctbusinesses

Opens up strategic deals with eBay’s rival

merchants which previously were not willing to deal

with PayPal

29

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 30/42

Proposal 2: Sell “Bill Me Later” Receivables,

Improve Transparency

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 31/42

Bill Me Later

• Business acquired by eBay under the PayPal

umbrella in late 2008 for $1.2bn• Provides transactional credit to customers, both

PayPal and non-PayPal purchases

• Loans are extended by CIT and repurchased byeBay

• Current loan book stands at $641mm

• Businesses don’t seem to have synergies with theexception of cross-selling

31

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 32/42

Acquisition Rationale

“On Bill Me Later..the intention was to take the number

one – PayPal – and the number two alternative onlinepayment businesses with very complementary skillsand put them together, leveraging the complements.

,

presence; PayPal with a very strong, small sole-proprietor SMB kind of presence. With thecombination of the product, the platform and the salesforce that we would be able to increase our presence

with large and small merchants…”John Donahoe,

eBay CEO

Q3 2009 Earnings Call

32

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 33/42

Bill Me Later loans are likely of questionablequality

• While cross selling opportunities may make

strategic sense, retaining credit risk does not

Consumers financing eBay and other purchases through BillMe Later likely have poor credit scores and lack alternative

means of procuring credit

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 34/42

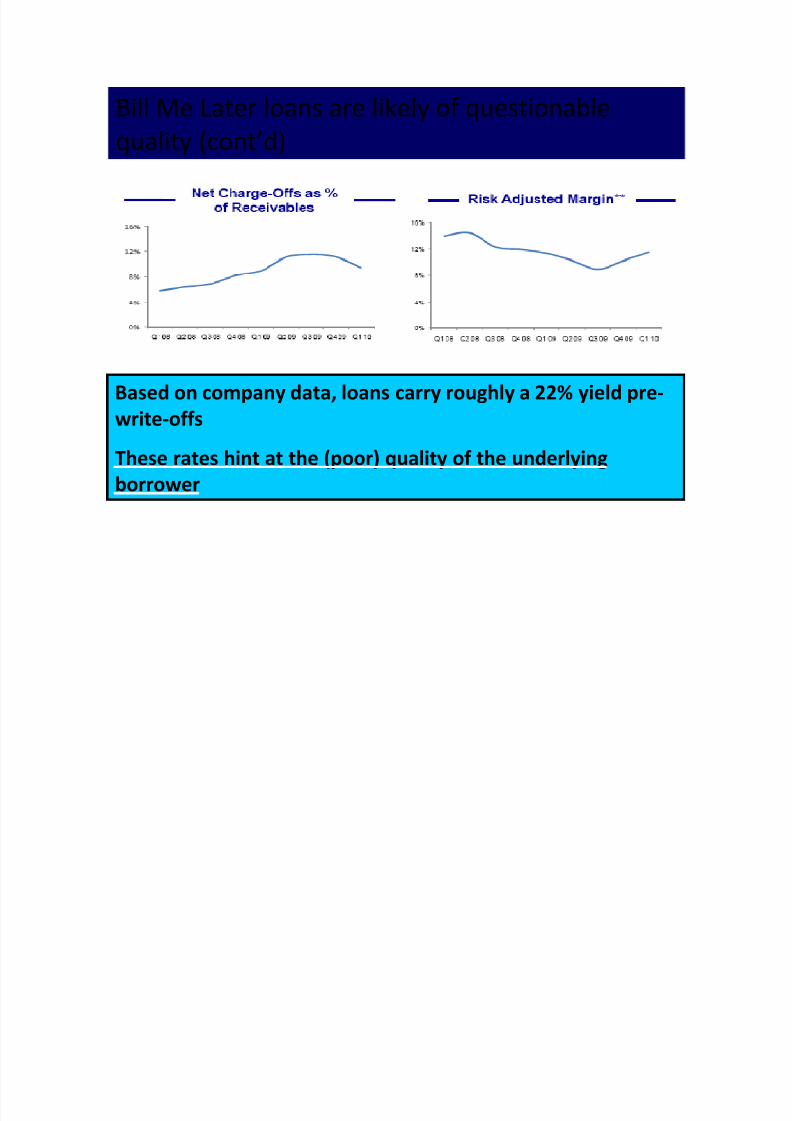

Bill Me Later loans are likely of questionablequality (cont’d)

Based on company data, loans carry roughly a 22% yield pre-

write-offs

These rates hint at the (poor) quality of the underlying

borrower

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 35/42

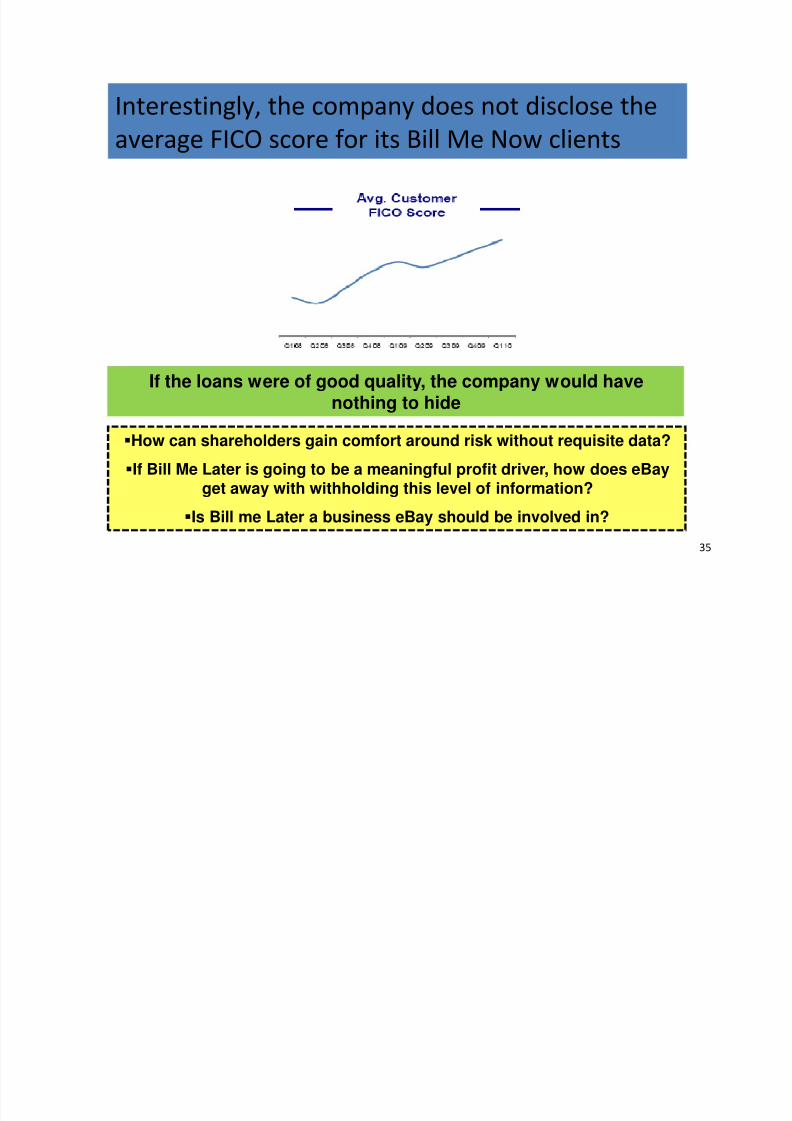

Interestingly, the company does not disclose theaverage FICO score for its Bill Me Now clients

35

If the loans were of good quality, the company would havenothing to hide

How can shareholders gain comfort around risk without requisite data?

If Bill Me Later is going to be a meaningful profit driver, how does eBayget away with withholding this level of information?

Is Bill me Later a business eBay should be involved in?

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 36/42

Why is PayPal taking credit risk?Why is PayPal taking credit risk?

• Classic example of corporate style drift

• eBay is not in the credit assessment

business

are they investing in them?

• eBay’s core competencies are auctions and

payments; they should leave the loan

underwriting and investing business to

consumer finance companies and other

investment vehicles36

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 37/42

PayPal would be more attractive to investorswithout the credit risk

• Credit card networks without credit

exposure (V, MA) trade at premiums to

those who do have credit exposure (AXP)

• The same logic applies to paymentprocessors

37

Given PayPal’s access to supplemental borrower data and the attractiveyields of the loans, eBay can easily find an appropriate buyer for this risk

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 38/42

Proposal III: Initiate Dividend/Share

Buyback

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 39/42

Management has cited future acquisitions and the tax

penalties associated with moving cash to keep from returnmonies to shareholders..

“As you know, the reality of that cash is about $400

million sits here in the U.S. and the rest of it off-shore,so the inherent flexibility we have to use our strongbalance sheet and our strong cash flows here

associated with it…and from a more macroperspective, I would say we always look at our inherentcapital structure and the best way to maintain ourfinancial flexibility to invest and grow while

redeploying our capital to shareholders, and we’llcontinue to do that.”John Donahoe,

eBay CEO

Q3 2008 Earnings Call

39

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 40/42

..but more recently has stated it would considerreturning cash to shareholders

“ … we will continue to look for acquisitions

that will strengthen our two core businessesand we will look to opportunistically

don’t believe the value of the firm isadequately reflected in the stock price. That’s

what we have been doing over the last couple

of years and we’ll continue to do that.”John Donahoe,

eBay CEO

Q3 2009 Earnings Call

40

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 41/42

Mature Co. will have enough cash to meet it’s goals of reinvesting in

the business while still returning cash to shareholders

• eBay has over 4bn of cash on its balance sheet

• As a mature, high cash-flow generative business,Mature Co. should initiate a dividend/sharebuyback to return excess cash to shareholders

• Management pre ers to reinvest in t e usinessand has occasionally bought back shares

• Given the companies’ mixed acquisition historyand growth profile of the Marketplace business,

shareholders would be well served with a returnof capital

41

8/8/2019 Buy It Now

http://slidepdf.com/reader/full/buy-it-now 42/42

Conclusion: Buy It Now • eBay is comprised of a maturing but profitable auction

business and a high growth payments business

• Company boasts a fortress balance sheet, great

customer loyalty and strong cash flow generation

• n a sum-o - e-par s as s, s ares are s gn can y

undervalued

• Potential catalysts to unlock value:

Spin-off payments business

Eliminate credit risk/improve transparency Initiate dividend/buyback program

42

Upside potential: 33-52% over two years