Embed Size (px)

Citation preview

RESULTS REVIEW 4QFY17 28 APR 2017

Kotak Mahindra Bank BUY

Countdown to growth KMB delivered yet another broad-based, strong performance with (1) Sequential loan growth of 5%, (2) Fee uptick of 24% YoY, (3) Healthy CASA expansion ~200bps, (4) Fat NIM of 4.6%, +10bps, (5) Opex growth curtailed at 2%, with C-I ratio down 220bps to ~46% and (6) Superior asset quality, despite the marginal GNPA rise. Lending subs (KMP and KMI) reported strong growth. K-Sec continued to display strong earnings momentum, while AMC profits were impacted by up-front expenses.

Post the e-VYSB integration (and demonetisation disruption), we sense KMB is at the cusp of high growth. All levers are in place : healthy Tier I (15%+, without factoring a likely fund raise), its recent mass-digital thrust, wider spread and an impeccable fix on asset quality. Consequently, RoAA will improve ~22bps to ~1.9% over FY17-19E (after the 27bps rise in FY17) led by steady NIMs, robust fee growth,

improving oplev and moderating LLP. Maintain BUY with SOTP of Rs 1,013 (4.5x FY19E core ABV of Rs 183 + subs. value of Rs 189).

Highlights of the quarter

Loan momentum continues, strong CASA growth: Broad-based loan growth was driven by Agri (+15%), CV (+12%), and business banking (+8%), while the corp loans remained stable. With improving growth trends, we have factored in 19% loan CAGR over FY17-19E. CASA (44%, +200bps) was driven by continued traction in SA (+41/8% YoY).

With improving efficiencies at e-VYSB branches and higher SA rate offerings, we believe that the robust SA growth should continue.

Near-term outlook: The stock should remain buoyant, given a consistent performance and improving growth outlook.

Financial Summary (Rs mn) 4QFY17 4QFY16 YoY (%) 3QFY17 QoQ (%) FY16 FY17P FY18E FY19E Net Interest Income 21,613 18,572 16.4% 20,503 5.4% 69,004 81,262 99,133 115,214 PPOP 17,020 11,942 42.5% 15,277 11.4% 40,411 59,848 73,226 85,586 PAT 9,765 6,958 40.3% 8,798 11.0% 20,898 34,115 43,052 51,471 EPS (Rs) 5.3 3.8 39.8% 4.8 10.8% 11.4 18.5 23.4 28.0 Core ROAE (%)

11.0 13.2 15.0 15.6

Core ROAA (%)

1.41 1.68 1.86 1.90 Core Adj. BVPS (Rs)

119.5 136.4 157.4 183.0

P/E (x)#

69.9 41.4 31.9 25.8 P/ABV (x)#

6.66 5.63 4.74 3.94

Source: Bank, HDFC sec Inst Research; Note: # adjusted for embedded value of subs.

INDUSTRY BANKS CMP (as on 27 Apr 2017) Rs 915 Target Price Rs 1,013 Nifty 9,342

Sensex 30,030

KEY STOCK DATA

Bloomberg KMB IN

No. of Shares (mn) 1,881

MCap (Rs bn) / ($ mn) 1,680/26,305

6m avg traded value (Rs mn) 1,907

STOCK PERFORMANCE (%)

52 Week high / low Rs 921/690

3M 6M 12M

Absolute (%) 16.8 13.6 28.7

Relative (%) 9.1 6.1 13.4

SHAREHOLDING PATTERN (%)

Promoters 32.1

FIs & Local MFs 5.41

FPIs 40.9

Public & Others 21.5

Source : BSE

Darpin Shah [email protected] +91-22-6171-7328 Pranav Gupta [email protected] +91-22-6171-7337

HDFC securities Institutional Research is also available on Bloomberg HSLB <GO> & Thomson Reuters

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

Healthy PPOP growth: Led by a superior NIM performance (4.6%, +10bps QoQ), healthy fee growth of 24% (driven by third party distribution income), and higher recoveries and controlled opex (+2% QoQ), PPOP grew 43/11% YoY/QoQ. Oplev. was visible with C-I improvement of 220bps to 46%. A stable NIM (4.6%), steady traction in fees (17% CAGR) and controlled opex (15%) will drive efficiencies. We expect core C-I improvement of 300bps to ~47% over FY17-19E.

Low stressed assets: Managements cautious stance to recognise std. stressed SME exposures (from the e-VYSB book), led to ~13% QoQ rise in GNPA (Rs 36bn, 2.6%). However, with a 460bps drop in PCR (52%), NNPAs jumped ~25% QoQ to Rs 17bn (1.26%). Despite this, KMB’s stressed exposures remain minuscule, with a restructured book of 7bps, SMA II of 10bps and no utilisation of RBI dispensation. With no major pain in asset quality and e-VYSB, led provisions already made, we have factored in LLP of 52bps over FY17-19E vs. 66bps in FY17.

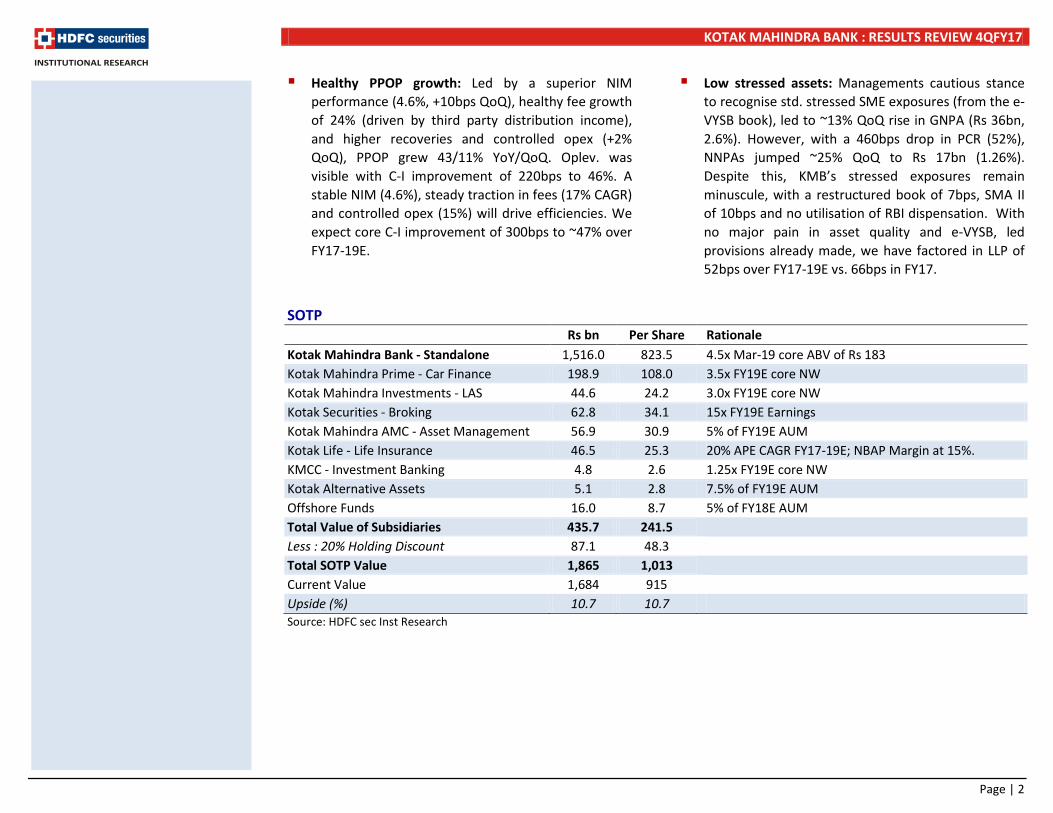

SOTP

Rs bn Per Share Rationale

Kotak Mahindra Bank - Standalone 1,516.0 823.5 4.5x Mar-19 core ABV of Rs 183 Kotak Mahindra Prime - Car Finance 198.9 108.0 3.5x FY19E core NW Kotak Mahindra Investments - LAS 44.6 24.2 3.0x FY19E core NW Kotak Securities - Broking 62.8 34.1 15x FY19E Earnings Kotak Mahindra AMC - Asset Management 56.9 30.9 5% of FY19E AUM Kotak Life - Life Insurance 46.5 25.3 20% APE CAGR FY17-19E; NBAP Margin at 15%. KMCC - Investment Banking 4.8 2.6 1.25x FY19E core NW Kotak Alternative Assets 5.1 2.8 7.5% of FY19E AUM Offshore Funds 16.0 8.7 5% of FY18E AUM Total Value of Subsidiaries 435.7 241.5

Less : 20% Holding Discount 87.1 48.3

Total SOTP Value 1,865 1,013

Current Value 1,684 915

Upside (%) 10.7 10.7 Source: HDFC sec Inst Research

Page | 2

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

Five Quarters At A Glance Rs mn 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17 YoY Growth QoQ Growth Net Interest Income 18,572 19,191 19,954 20,503 21,613 16.4% 5.4% Non Interest Income 6,819 7,332 8,311 9,102 10,027 47.0% 10.2% Fee Income 6,100 5,640 6,300 7,250 7,570 24.1% 4.4% Operating Income 25,392 26,523 28,265 29,605 31,640 24.6% 6.9% Operating Expenses 13,450 13,373 13,864 14,328 14,620 8.7% 2.0% Pre provision Profits 11,942 13,150 14,401 15,277 17,020 42.5% 11.4% Provisions 2,004 1,795 1,978 1,921 2,674 33.4% 39.2%

NPA Provisions 1,704 1,671 1,415 1,370 2,519 47.8% 84.0% PBT 9,937 11,355 12,423 13,356 14,346 44.4% 7.4% Provision For Tax 2,980 3,936 4,290 4,558 4,582 53.8% 0.5% PAT 6,958 7,420 8,133 8,798 9,765 40.3% 11.0% Balance Sheet items/ratios Deposits (Rs bn) 1,386 1,400 1,410 1,494 1,574 13.5% 5.4%

CASA (%) 38.1 37.4 39.0 42.0 44.0 593 bps 196 bps Advances (Rs bn) 1,187 1,208 1,260 1,293 1,361 14.7% 5.3%

CV And CE (%) 6.3 6.6 6.9 7.5 8.0 167 bps 49 bps Agri Finance (%) 15.2 13.9 14.1 12.8 13.9 -122 bps 116 bps Mortgage Loans (%) 19.4 19.4 19.4 19.4 19.2 -19 bps -18 bps PL (%) 12.6 12.2 12.6 12.2 12.8 18 bps 57 bps Business Banking (%) 15.2 14.1 13.8 12.9 13.1 -202 bps 28 bps Corp Banking (%) 29.5 31.5 30.7 32.9 30.6 118 bps -229 bps Others (%) 1.9 2.3 2.5 2.4 2.3 42 bps -2 bps

CD ratio (%) 85.6 86.2 89.3 86.5 86.4 85 bps -11 bps CAR (%) 16.3 16.34 16.8 16.0 16.8 50 bps 80 bps

Tier I (%) 15.3 15.8 15.7 14.9 15.2 -10 bps 30 bps Profitability Calc. Yield On Advances (%) 11.0 11.0 10.9 10.7 10.15 -81 bps -51 bps Calc. Cost Of Funds (%) 6.2 6.2 6.1 5.9 5.25 -96 bps -64 bps NIM (%) 4.30 4.37 4.47 4.49 4.60 30 bps 11 bps Cost-Income Ratio (%) 53.0 50.4 49.1 48.4 46.2 -676 bps -219 bps Tax Rate (%) 30.0 34.7 34.5 34.1 31.9 195 bps -219 bps Asset Quality Gross NPA (Rs bn) 28.4 30.6 31.8 31.8 35.8 26.1% 12.6% Net NPA (Rs bn) 12.6 14.7 15.2 13.8 17.2 36.1% 24.6% Gross NPAs (%) 2.4 2.5 2.5 2.4 2.6 23 bps 17 bps Net NPAs (%) 1.1 1.2 1.2 1.1 1.3 20 bps 19 bps Coverage Ratio (%) 55.5 52.0 52.3 56.6 52.0 -354 bps -461 bps Restructured Book (%) 0.26 0.13 0.12 0.11 0.07 -18 bps -4 bps Source: HDFC sec Inst Research

Slightly ahead of estimates driven by sequential NIM improvement of 10bps

Fees were driven by strong third party distribution income; recoveries were higher at ~Rs 1bn

KMB has recognised entire stress inherited from e-VYSB

Led by strong SA growth of 41% YoY and CA growth of 19% YoY

Share of CASA and TD sweep together constitutes ~50% of deposits

Led by a sharp drop in CoF; Avg SA rate at 5.5%, stable QoQ

Due to one-off tax benefits

~8% QoQ growth was a positive

We have not factored in fund raise

Lowest amongst peers, SMA II stood at a mere 10bps

Page | 3

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

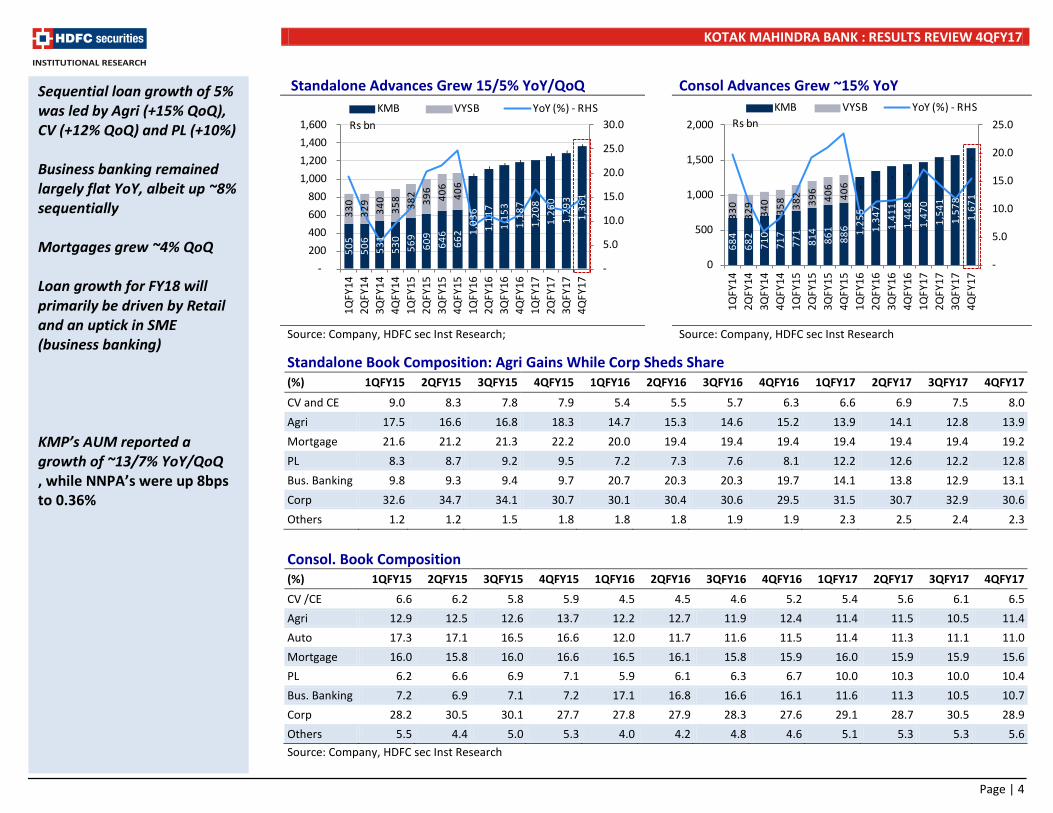

Standalone Advances Grew 15/5% YoY/QoQ Consol Advances Grew ~15% YoY

Source: Company, HDFC sec Inst Research; Source: Company, HDFC sec Inst Research

Standalone Book Composition: Agri Gains While Corp Sheds Share (%) 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

CV and CE 9.0 8.3 7.8 7.9 5.4 5.5 5.7 6.3 6.6 6.9 7.5 8.0

Agri 17.5 16.6 16.8 18.3 14.7 15.3 14.6 15.2 13.9 14.1 12.8 13.9

Mortgage 21.6 21.2 21.3 22.2 20.0 19.4 19.4 19.4 19.4 19.4 19.4 19.2

PL 8.3 8.7 9.2 9.5 7.2 7.3 7.6 8.1 12.2 12.6 12.2 12.8

Bus. Banking 9.8 9.3 9.4 9.7 20.7 20.3 20.3 19.7 14.1 13.8 12.9 13.1

Corp 32.6 34.7 34.1 30.7 30.1 30.4 30.6 29.5 31.5 30.7 32.9 30.6

Others 1.2 1.2 1.5 1.8 1.8 1.8 1.9 1.9 2.3 2.5 2.4 2.3

Consol. Book Composition (%) 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

CV /CE 6.6 6.2 5.8 5.9 4.5 4.5 4.6 5.2 5.4 5.6 6.1 6.5

Agri 12.9 12.5 12.6 13.7 12.2 12.7 11.9 12.4 11.4 11.5 10.5 11.4

Auto 17.3 17.1 16.5 16.6 12.0 11.7 11.6 11.5 11.4 11.3 11.1 11.0

Mortgage 16.0 15.8 16.0 16.6 16.5 16.1 15.8 15.9 16.0 15.9 15.9 15.6

PL 6.2 6.6 6.9 7.1 5.9 6.1 6.3 6.7 10.0 10.3 10.0 10.4

Bus. Banking 7.2 6.9 7.1 7.2 17.1 16.8 16.6 16.1 11.6 11.3 10.5 10.7

Corp 28.2 30.5 30.1 27.7 27.8 27.9 28.3 27.6 29.1 28.7 30.5 28.9

Others 5.5 4.4 5.0 5.3 4.0 4.2 4.8 4.6 5.1 5.3 5.3 5.6 Source: Company, HDFC sec Inst Research

Sequential loan growth of 5% was led by Agri (+15% QoQ), CV (+12% QoQ) and PL (+10%) Business banking remained largely flat YoY, albeit up ~8% sequentially Mortgages grew ~4% QoQ Loan growth for FY18 will primarily be driven by Retail and an uptick in SME (business banking) KMP’s AUM reported a growth of ~13/7% YoY/QoQ , while NNPA’s were up 8bps to 0.36%

505

506

531

530

569

609

646

662 1,

036

1,11

7 1,

153

1,18

7 1,

208

1,26

0 1,

293

1,36

1

330

329

340

358

382

396

406

406

-- - -

- - -

-

5.0

10.0

15.0

20.0

25.0

30.0

-

200

400

600

800

1,000

1,200

1,400

1,600

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

KMB VYSB YoY (%) - RHS

Rs bn

684

682

710

717

771

814

861

886 1,

255

1,34

7

1,41

1

1,44

8

1,47

0

1,54

1

1,57

8

1,67

1

330

329

340

358

382

396

406

406 -

- - -

-

-

5.0

10.0

15.0

20.0

25.0

0

500

1,000

1,500

2,000

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

KMB VYSB YoY (%) - RHSRs bn

Page | 4

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

KMP Book: Total Advances Grew 13/7%YoY/QoQ LAS Customer Assets Continues Momemtum

Source: Bank, HDFC sec Inst Research Source: Bank, HDFC sec Inst Research

Deposits Growth Was Strong At 14% CASA Ratio Grew 31/10% YoY/QoQ Led by SA

Source: Bank, HDFC sec Inst Research; Source: Bank, HDFC sec Inst Research

Deposits Break-up (%) 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

CA 13.1 13.9 14.6 17.6 14.9 16.5 15.0 16.8 15.6 15.6 15.2 17.6

SA 17.9 17.2 16.9 18.7 19.5 19.8 20.3 21.3 21.8 23.4 24.2 26.4

TD 69.0 68.9 68.5 63.6 65.7 63.8 64.7 61.9 62.6 61.0 60.6 56.0 Source: Company, HDFC sec Inst Research

KMP’s car loans grew ~13% YoY, and other advances saw a string growth of ~25/13% YoY/QoQ KMI (LAS business) AUM grew 44/16% YoY/QoQ SA growth was strong at 41/8% YoY/QoQ, yielding an improved CASA ratio at 44% (+590bps YoY and 200bps QoQ) KMB to continue its higher rate offerings in SA deposits TD sweep deposits form ~6.4% vs. 7.3% QoQ of total deposits

-2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0

0

50

100

150

200

250

300

2QFY

14

3QFY

14

4QFY

14

1QFY

15

2QFY

15

3QFY

15

4QFY

15

1QFY

16

2QFY

16

3QFY

16

4QFY

16

1QFY

17

2QFY

17

3QFY

17

4QFY

17

Total Loans Car Loans

Total Loans YoY Car Loans YoY

Rs bn %

7.4 11

.7

15.6

23.8

23.6

30.2

32.7

34.3

40.2

47.6

48.0

48.7

55.3

59.6

69.1

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2QFY

14

3QFY

14

4QFY

14

1QFY

15

2QFY

15

3QFY

15

4QFY

15

1QFY

16

2QFY

16

3QFY

16

4QFY

16

1QFY

17

2QFY

17

3QFY

17

4QFY

17

Rs bn

525

526

547

591

614

681

731

749 1,

168

1,23

2

1,30

9

1,38

6

1,40

0

1,41

0

1,49

4

1,57

4

409

400

390

412

423 44

7

460

460 0 0 0 0

0

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

0

500

1,000

1,500

2,000

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

KMB VYSB YoY (%) - RHS

Rs bn

151

154

163

188

190

212

231

272 40

1

447

462 52

8

524

550 62

8 693

123

130

135

138

126 14

8

146 14

6 -

- -

-

-

-

10.0

20.0

30.0

40.0

50.0

-

100

200

300

400

500

600

700

800

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

KMB VYSB YoY (%) - RHS

Rs bn

Page | 5

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

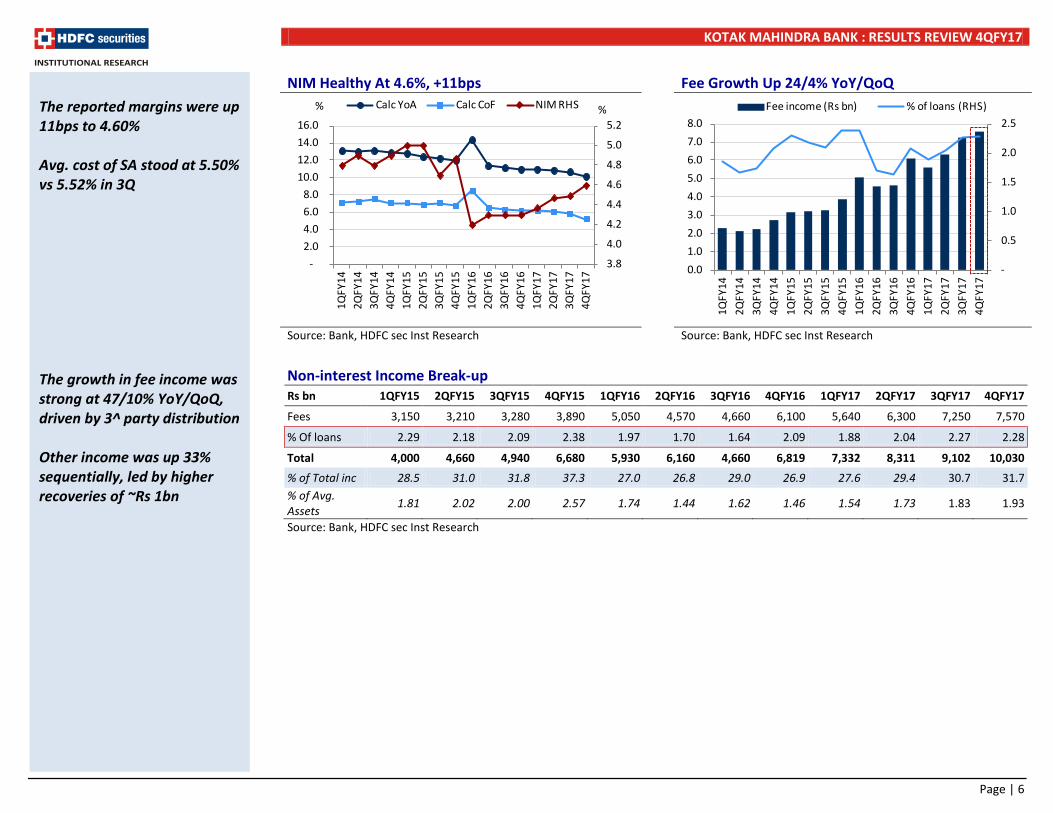

NIM Healthy At 4.6%, +11bps Fee Growth Up 24/4% YoY/QoQ

Source: Bank, HDFC sec Inst Research Source: Bank, HDFC sec Inst Research

Non-interest Income Break-up Rs bn 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

Fees 3,150 3,210 3,280 3,890 5,050 4,570 4,660 6,100 5,640 6,300 7,250 7,570

% Of loans 2.29 2.18 2.09 2.38 1.97 1.70 1.64 2.09 1.88 2.04 2.27 2.28

Total 4,000 4,660 4,940 6,680 5,930 6,160 4,660 6,819 7,332 8,311 9,102 10,030

% of Total inc 28.5 31.0 31.8 37.3 27.0 26.8 29.0 26.9 27.6 29.4 30.7 31.7 % of Avg. Assets

1.81 2.02 2.00 2.57 1.74 1.44 1.62 1.46 1.54 1.73 1.83 1.93

Source: Bank, HDFC sec Inst Research

The reported margins were up 11bps to 4.60% Avg. cost of SA stood at 5.50% vs 5.52% in 3Q The growth in fee income was strong at 47/10% YoY/QoQ, driven by 3^ party distribution Other income was up 33% sequentially, led by higher recoveries of ~Rs 1bn

3.8

4.0

4.2

4.4

4.6

4.8

5.0

5.2

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

Calc YoA Calc CoF NIM RHS% %

-

0.5

1.0

1.5

2.0

2.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1QFY

14

2QFY

14

3QFY

14

4QFY

14

1QFY

15

2QFY

15

3QFY

15

4QFY

15

1QFY

16

2QFY

16

3QFY

16

4QFY

16

1QFY

17

2QFY

17

3QFY

17

4QFY

17

Fee income (Rs bn) % of loans (RHS)

Page | 6

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

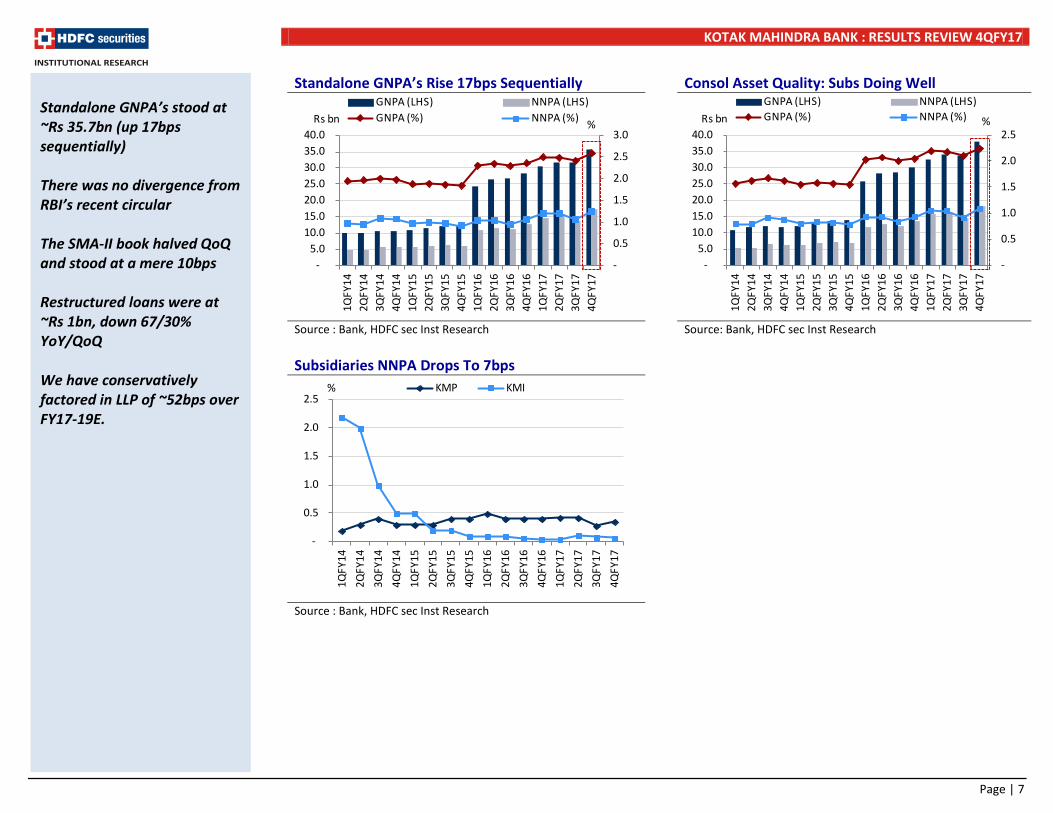

Standalone GNPA’s Rise 17bps Sequentially Consol Asset Quality: Subs Doing Well

Source : Bank, HDFC sec Inst Research Source: Bank, HDFC sec Inst Research Subsidiaries NNPA Drops To 7bps

Source : Bank, HDFC sec Inst Research

Standalone GNPA’s stood at ~Rs 35.7bn (up 17bps sequentially) There was no divergence from RBI’s recent circular The SMA-II book halved QoQ and stood at a mere 10bps Restructured loans were at ~Rs 1bn, down 67/30% YoY/QoQ We have conservatively factored in LLP of ~52bps over FY17-19E.

-

0.5

1.0

1.5

2.0

2.5

3.0

-5.0

10.0 15.0 20.0 25.0 30.0 35.0 40.0

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

GNPA (LHS) NNPA (LHS)GNPA (%) NNPA (%)Rs bn %

-

0.5

1.0

1.5

2.0

2.5

-5.0

10.0 15.0 20.0 25.0 30.0 35.0 40.0

1QFY

142Q

FY14

3QFY

144Q

FY14

1QFY

152Q

FY15

3QFY

154Q

FY15

1QFY

162Q

FY16

3QFY

164Q

FY16

1QFY

172Q

FY17

3QFY

174Q

FY17

GNPA (LHS) NNPA (LHS)GNPA (%) NNPA (%)Rs bn %

-

0.5

1.0

1.5

2.0

2.5

1QFY

14

2QFY

14

3QFY

14

4QFY

14

1QFY

15

2QFY

15

3QFY

15

4QFY

15

1QFY

16

2QFY

16

3QFY

16

4QFY

16

1QFY

17

2QFY

17

3QFY

17

4QFY

17

KMP KMI%

Page | 7

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

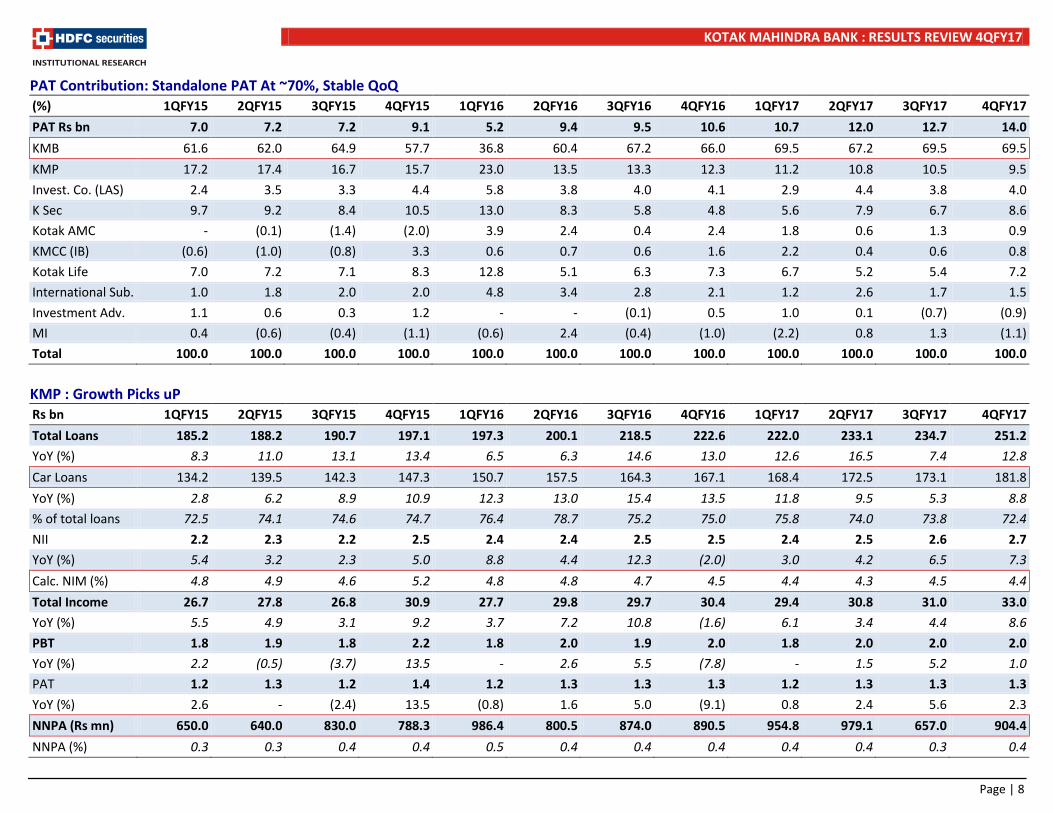

PAT Contribution: Standalone PAT At ~70%, Stable QoQ (%) 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

PAT Rs bn 7.0 7.2 7.2 9.1 5.2 9.4 9.5 10.6 10.7 12.0 12.7 14.0

KMB 61.6 62.0 64.9 57.7 36.8 60.4 67.2 66.0 69.5 67.2 69.5 69.5

KMP 17.2 17.4 16.7 15.7 23.0 13.5 13.3 12.3 11.2 10.8 10.5 9.5

Invest. Co. (LAS) 2.4 3.5 3.3 4.4 5.8 3.8 4.0 4.1 2.9 4.4 3.8 4.0

K Sec 9.7 9.2 8.4 10.5 13.0 8.3 5.8 4.8 5.6 7.9 6.7 8.6

Kotak AMC - (0.1) (1.4) (2.0) 3.9 2.4 0.4 2.4 1.8 0.6 1.3 0.9

KMCC (IB) (0.6) (1.0) (0.8) 3.3 0.6 0.7 0.6 1.6 2.2 0.4 0.6 0.8

Kotak Life 7.0 7.2 7.1 8.3 12.8 5.1 6.3 7.3 6.7 5.2 5.4 7.2

International Sub. 1.0 1.8 2.0 2.0 4.8 3.4 2.8 2.1 1.2 2.6 1.7 1.5

Investment Adv. 1.1 0.6 0.3 1.2 - - (0.1) 0.5 1.0 0.1 (0.7) (0.9)

MI 0.4 (0.6) (0.4) (1.1) (0.6) 2.4 (0.4) (1.0) (2.2) 0.8 1.3 (1.1)

Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

KMP : Growth Picks uP Rs bn 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

Total Loans 185.2 188.2 190.7 197.1 197.3 200.1 218.5 222.6 222.0 233.1 234.7 251.2

YoY (%) 8.3 11.0 13.1 13.4 6.5 6.3 14.6 13.0 12.6 16.5 7.4 12.8

Car Loans 134.2 139.5 142.3 147.3 150.7 157.5 164.3 167.1 168.4 172.5 173.1 181.8

YoY (%) 2.8 6.2 8.9 10.9 12.3 13.0 15.4 13.5 11.8 9.5 5.3 8.8

% of total loans 72.5 74.1 74.6 74.7 76.4 78.7 75.2 75.0 75.8 74.0 73.8 72.4

NII 2.2 2.3 2.2 2.5 2.4 2.4 2.5 2.5 2.4 2.5 2.6 2.7

YoY (%) 5.4 3.2 2.3 5.0 8.8 4.4 12.3 (2.0) 3.0 4.2 6.5 7.3

Calc. NIM (%) 4.8 4.9 4.6 5.2 4.8 4.8 4.7 4.5 4.4 4.3 4.5 4.4

Total Income 26.7 27.8 26.8 30.9 27.7 29.8 29.7 30.4 29.4 30.8 31.0 33.0

YoY (%) 5.5 4.9 3.1 9.2 3.7 7.2 10.8 (1.6) 6.1 3.4 4.4 8.6

PBT 1.8 1.9 1.8 2.2 1.8 2.0 1.9 2.0 1.8 2.0 2.0 2.0

YoY (%) 2.2 (0.5) (3.7) 13.5 - 2.6 5.5 (7.8) - 1.5 5.2 1.0

PAT 1.2 1.3 1.2 1.4 1.2 1.3 1.3 1.3 1.2 1.3 1.3 1.3

YoY (%) 2.6 - (2.4) 13.5 (0.8) 1.6 5.0 (9.1) 0.8 2.4 5.6 2.3

NNPA (Rs mn) 650.0 640.0 830.0 788.3 986.4 800.5 874.0 890.5 954.8 979.1 657.0 904.4

NNPA (%) 0.3 0.3 0.4 0.4 0.5 0.4 0.4 0.4 0.4 0.4 0.3 0.4

Page | 8

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

Kotak Sec Snapshot: Healthy PAT Growth Rs mn. 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

K Sec Vol (bn) 60.53 66.21 73.78 83.72 78.13 75.93 64.81 74.03 76.72 73.29 87.43 104.34

Market Share (%) 2.9 2.7 2.8 2.9 2.7 2.7 2.7 2.3 2.4 2.3 2.2 2.2

Total Income 2230 2240 2230 2890 2500 2700 2280 2250 2380 2940 2870 3660

YoY (%) 51.7 47.4 32.7 80.6 12.1 20.5 2.2 (22.1) (4.8) 8.9 25.9 62.7

Yield (calc.) 0.06 0.06 0.05 0.06 0.05 0.06 0.06 0.05 0.05 0.07 0.05 0.06

PBT 1030 1000 910 1470 1020 1200 830 750 920 1440 1250 1820

YoY (%) 114.6 66.7 28.2 167.3 (1.0) 20.0 (8.8) (49.0) (9.8) 20.0 50.6 142.7

PAT 680 660 600 960 670 780 550 510 600 960 850 1210

YoY (%) 119.4 65.0 30.4 118.2 (1.5) 18.2 (8.3) (46.9) (10.4) 23.1 54.5 137.3

Kotak AMC Snapshot: Earnings Growth Arrested By Up Fronting Of Expenses Rs mn 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

AUM (Rs bn) 666 657 714 806 942 960 957 1022 1109 1207 1331 1414

Debt (%) 47.0 43.0 40.0 36.0 41.0 39.0 42.5 38.3 41.1 42.9 44.7 43.1

Equity (%) 7.0 9.0 10.0 12.0 14.0 14.0 13.7 14.3 14.5 16.0 16.8 19.6

Alt assets (%) 9.0 9.0 9.0 7.0 6.0 6.0 6.0 11.1 10.3 9.0 8.2 5.1

Offshore Funds (%) 18.0 19.0 22.0 26.0 23.0 25.0 22.1 20.7 19.0 17.3 16.5 17.4

Insurance (%) 18.0 19.0 18.0 18.0 18.0 15.0 15.4 15.2 14.6 14.2 13.0 13.7

PMS (%) 1.0 1.0 1.0 1.0 1.0 1.0 0.4 0.4 0.4 0.6 0.8 1.1

PBT 0 0 -90 -160 210 240 130 320 290 110 240 200

YoY (%) (100.0) (100.0) (150.0) (420.0) #DIV/0! #DIV/0! (244.4) (300.0) 38.1 (54.2) 84.6 (37.5)

PAT 0 -10 -10 -180 200 230 40 250 190 70 160 130

YoY (%) (100.0) (105.9) (108.3) (550.0) #DIV/0! (2,400.0) (500.0) (238.9) (5.0) (69.6) 300.0 (48.0)

Page | 9

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

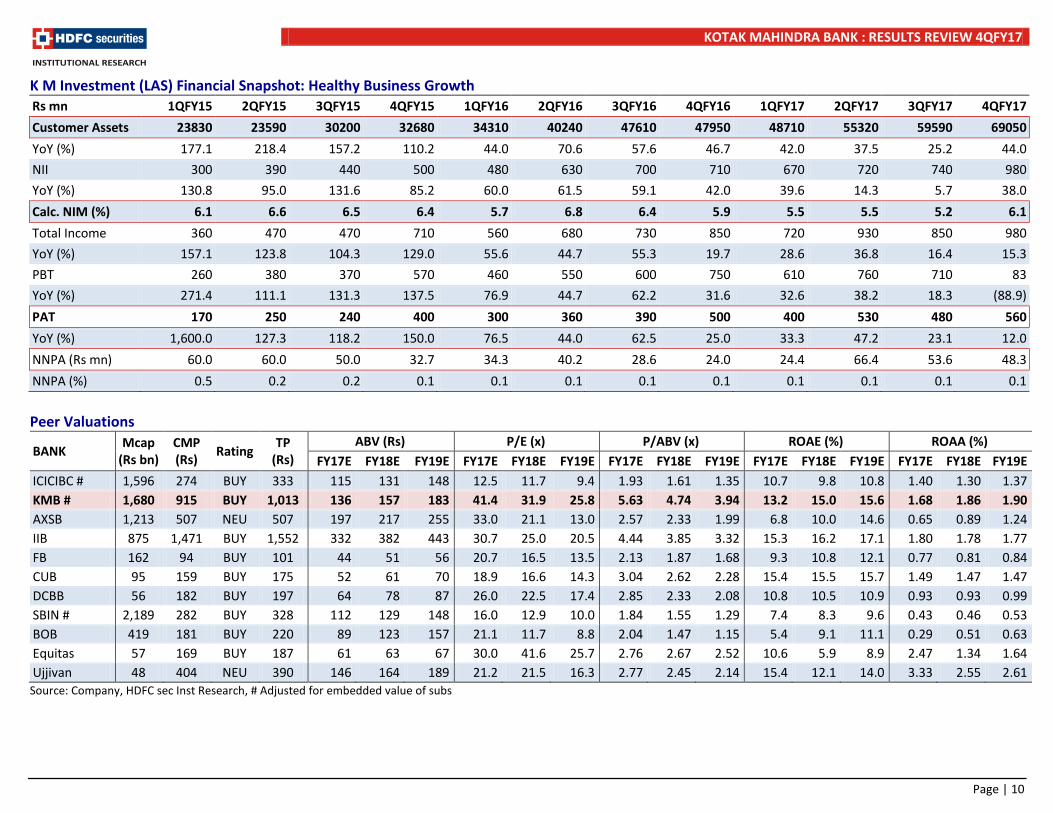

K M Investment (LAS) Financial Snapshot: Healthy Business Growth Rs mn 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

Customer Assets 23830 23590 30200 32680 34310 40240 47610 47950 48710 55320 59590 69050

YoY (%) 177.1 218.4 157.2 110.2 44.0 70.6 57.6 46.7 42.0 37.5 25.2 44.0

NII 300 390 440 500 480 630 700 710 670 720 740 980

YoY (%) 130.8 95.0 131.6 85.2 60.0 61.5 59.1 42.0 39.6 14.3 5.7 38.0

Calc. NIM (%) 6.1 6.6 6.5 6.4 5.7 6.8 6.4 5.9 5.5 5.5 5.2 6.1

Total Income 360 470 470 710 560 680 730 850 720 930 850 980

YoY (%) 157.1 123.8 104.3 129.0 55.6 44.7 55.3 19.7 28.6 36.8 16.4 15.3

PBT 260 380 370 570 460 550 600 750 610 760 710 83

YoY (%) 271.4 111.1 131.3 137.5 76.9 44.7 62.2 31.6 32.6 38.2 18.3 (88.9)

PAT 170 250 240 400 300 360 390 500 400 530 480 560

YoY (%) 1,600.0 127.3 118.2 150.0 76.5 44.0 62.5 25.0 33.3 47.2 23.1 12.0

NNPA (Rs mn) 60.0 60.0 50.0 32.7 34.3 40.2 28.6 24.0 24.4 66.4 53.6 48.3

NNPA (%) 0.5 0.2 0.2 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1

Peer Valuations

BANK Mcap

(Rs bn) CMP (Rs)

Rating TP

(Rs) ABV (Rs) P/E (x) P/ABV (x) ROAE (%) ROAA (%)

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E ICICIBC # 1,596 274 BUY 333 115 131 148 12.5 11.7 9.4 1.93 1.61 1.35 10.7 9.8 10.8 1.40 1.30 1.37 KMB # 1,680 915 BUY 1,013 136 157 183 41.4 31.9 25.8 5.63 4.74 3.94 13.2 15.0 15.6 1.68 1.86 1.90 AXSB 1,213 507 NEU 507 197 217 255 33.0 21.1 13.0 2.57 2.33 1.99 6.8 10.0 14.6 0.65 0.89 1.24 IIB 875 1,471 BUY 1,552 332 382 443 30.7 25.0 20.5 4.44 3.85 3.32 15.3 16.2 17.1 1.80 1.78 1.77 FB 162 94 BUY 101 44 51 56 20.7 16.5 13.5 2.13 1.87 1.68 9.3 10.8 12.1 0.77 0.81 0.84 CUB 95 159 BUY 175 52 61 70 18.9 16.6 14.3 3.04 2.62 2.28 15.4 15.5 15.7 1.49 1.47 1.47 DCBB 56 182 BUY 197 64 78 87 26.0 22.5 17.4 2.85 2.33 2.08 10.8 10.5 10.9 0.93 0.93 0.99 SBIN # 2,189 282 BUY 328 112 129 148 16.0 12.9 10.0 1.84 1.55 1.29 7.4 8.3 9.6 0.43 0.46 0.53 BOB 419 181 BUY 220 89 123 157 21.1 11.7 8.8 2.04 1.47 1.15 5.4 9.1 11.1 0.29 0.51 0.63 Equitas 57 169 BUY 187 61 63 67 30.0 41.6 25.7 2.76 2.67 2.52 10.6 5.9 8.9 2.47 1.34 1.64 Ujjivan 48 404 NEU 390 146 164 189 21.2 21.5 16.3 2.77 2.45 2.14 15.4 12.1 14.0 3.33 2.55 2.61

Source: Company, HDFC sec Inst Research, # Adjusted for embedded value of subs

Page | 10

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

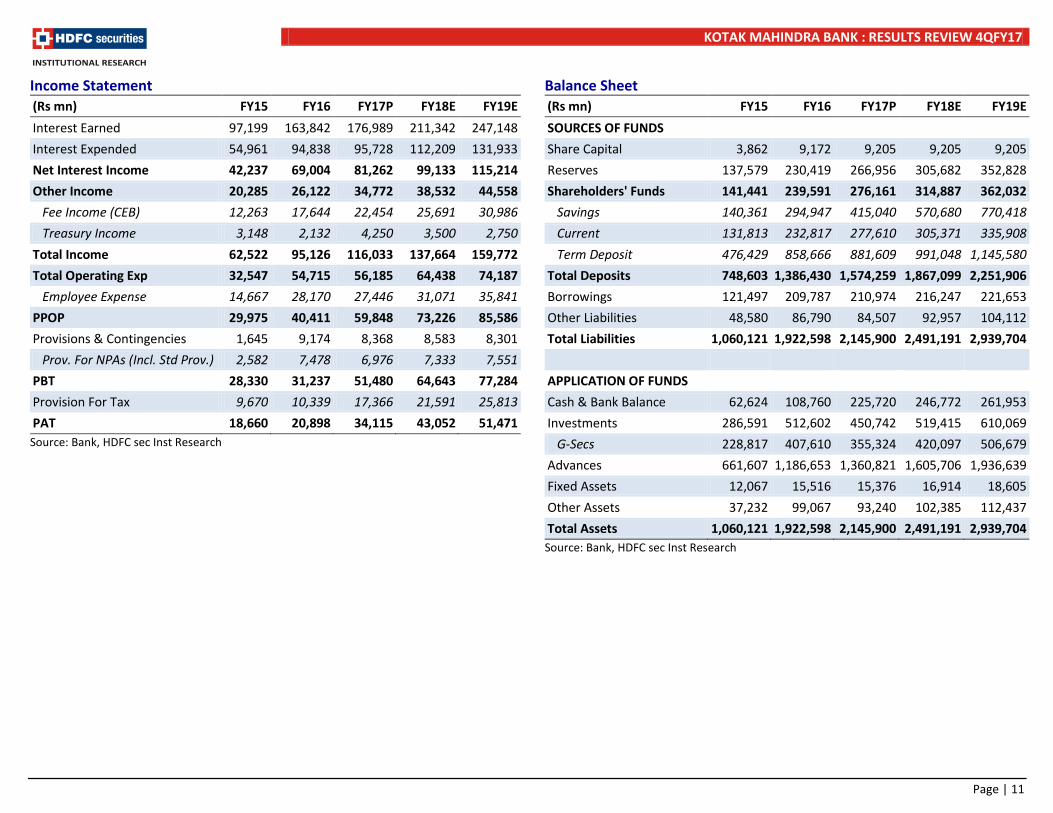

Income Statement (Rs mn) FY15 FY16 FY17P FY18E FY19E

Interest Earned 97,199 163,842 176,989 211,342 247,148

Interest Expended 54,961 94,838 95,728 112,209 131,933

Net Interest Income 42,237 69,004 81,262 99,133 115,214

Other Income 20,285 26,122 34,772 38,532 44,558

Fee Income (CEB) 12,263 17,644 22,454 25,691 30,986

Treasury Income 3,148 2,132 4,250 3,500 2,750

Total Income 62,522 95,126 116,033 137,664 159,772

Total Operating Exp 32,547 54,715 56,185 64,438 74,187

Employee Expense 14,667 28,170 27,446 31,071 35,841

PPOP 29,975 40,411 59,848 73,226 85,586

Provisions & Contingencies 1,645 9,174 8,368 8,583 8,301

Prov. For NPAs (Incl. Std Prov.) 2,582 7,478 6,976 7,333 7,551

PBT 28,330 31,237 51,480 64,643 77,284

Provision For Tax 9,670 10,339 17,366 21,591 25,813

PAT 18,660 20,898 34,115 43,052 51,471 Source: Bank, HDFC sec Inst Research

Balance Sheet (Rs mn) FY15 FY16 FY17P FY18E FY19E

SOURCES OF FUNDS

Share Capital 3,862 9,172 9,205 9,205 9,205

Reserves 137,579 230,419 266,956 305,682 352,828

Shareholders' Funds 141,441 239,591 276,161 314,887 362,032

Savings 140,361 294,947 415,040 570,680 770,418

Current 131,813 232,817 277,610 305,371 335,908

Term Deposit 476,429 858,666 881,609 991,048 1,145,580

Total Deposits 748,603 1,386,430 1,574,259 1,867,099 2,251,906

Borrowings 121,497 209,787 210,974 216,247 221,653

Other Liabilities 48,580 86,790 84,507 92,957 104,112

Total Liabilities 1,060,121 1,922,598 2,145,900 2,491,191 2,939,704

APPLICATION OF FUNDS

Cash & Bank Balance 62,624 108,760 225,720 246,772 261,953

Investments 286,591 512,602 450,742 519,415 610,069

G-Secs 228,817 407,610 355,324 420,097 506,679

Advances 661,607 1,186,653 1,360,821 1,605,706 1,936,639

Fixed Assets 12,067 15,516 15,376 16,914 18,605

Other Assets 37,232 99,067 93,240 102,385 112,437

Total Assets 1,060,121 1,922,598 2,145,900 2,491,191 2,939,704 Source: Bank, HDFC sec Inst Research

Page | 11

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

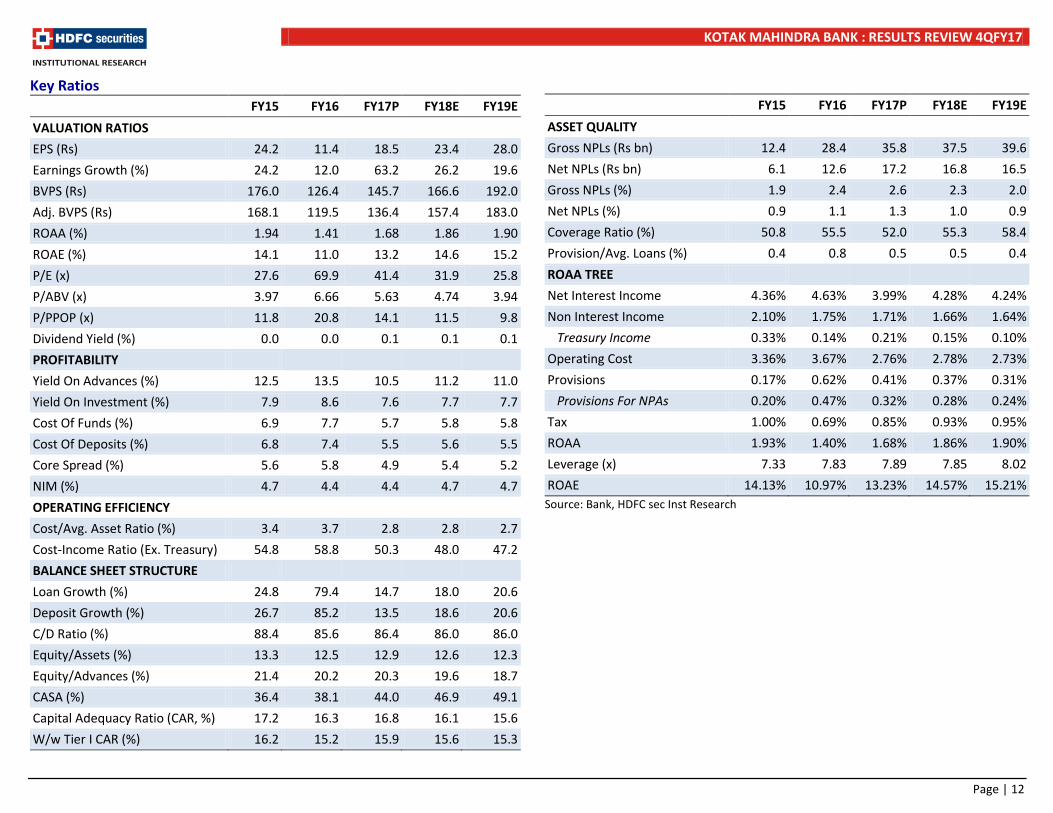

Key Ratios

FY15 FY16 FY17P FY18E FY19E

VALUATION RATIOS

EPS (Rs) 24.2 11.4 18.5 23.4 28.0

Earnings Growth (%) 24.2 12.0 63.2 26.2 19.6

BVPS (Rs) 176.0 126.4 145.7 166.6 192.0

Adj. BVPS (Rs) 168.1 119.5 136.4 157.4 183.0

ROAA (%) 1.94 1.41 1.68 1.86 1.90

ROAE (%) 14.1 11.0 13.2 14.6 15.2

P/E (x) 27.6 69.9 41.4 31.9 25.8

P/ABV (x) 3.97 6.66 5.63 4.74 3.94

P/PPOP (x) 11.8 20.8 14.1 11.5 9.8

Dividend Yield (%) 0.0 0.0 0.1 0.1 0.1

PROFITABILITY

Yield On Advances (%) 12.5 13.5 10.5 11.2 11.0

Yield On Investment (%) 7.9 8.6 7.6 7.7 7.7

Cost Of Funds (%) 6.9 7.7 5.7 5.8 5.8

Cost Of Deposits (%) 6.8 7.4 5.5 5.6 5.5

Core Spread (%) 5.6 5.8 4.9 5.4 5.2

NIM (%) 4.7 4.4 4.4 4.7 4.7

OPERATING EFFICIENCY

Cost/Avg. Asset Ratio (%) 3.4 3.7 2.8 2.8 2.7

Cost-Income Ratio (Ex. Treasury) 54.8 58.8 50.3 48.0 47.2

BALANCE SHEET STRUCTURE

Loan Growth (%) 24.8 79.4 14.7 18.0 20.6

Deposit Growth (%) 26.7 85.2 13.5 18.6 20.6

C/D Ratio (%) 88.4 85.6 86.4 86.0 86.0

Equity/Assets (%) 13.3 12.5 12.9 12.6 12.3

Equity/Advances (%) 21.4 20.2 20.3 19.6 18.7

CASA (%) 36.4 38.1 44.0 46.9 49.1

Capital Adequacy Ratio (CAR, %) 17.2 16.3 16.8 16.1 15.6

W/w Tier I CAR (%) 16.2 15.2 15.9 15.6 15.3

FY15 FY16 FY17P FY18E FY19E

ASSET QUALITY

Gross NPLs (Rs bn) 12.4 28.4 35.8 37.5 39.6

Net NPLs (Rs bn) 6.1 12.6 17.2 16.8 16.5

Gross NPLs (%) 1.9 2.4 2.6 2.3 2.0

Net NPLs (%) 0.9 1.1 1.3 1.0 0.9

Coverage Ratio (%) 50.8 55.5 52.0 55.3 58.4

Provision/Avg. Loans (%) 0.4 0.8 0.5 0.5 0.4

ROAA TREE

Net Interest Income 4.36% 4.63% 3.99% 4.28% 4.24%

Non Interest Income 2.10% 1.75% 1.71% 1.66% 1.64%

Treasury Income 0.33% 0.14% 0.21% 0.15% 0.10%

Operating Cost 3.36% 3.67% 2.76% 2.78% 2.73%

Provisions 0.17% 0.62% 0.41% 0.37% 0.31%

Provisions For NPAs 0.20% 0.47% 0.32% 0.28% 0.24%

Tax 1.00% 0.69% 0.85% 0.93% 0.95%

ROAA 1.93% 1.40% 1.68% 1.86% 1.90%

Leverage (x) 7.33 7.83 7.89 7.85 8.02

ROAE 14.13% 10.97% 13.23% 14.57% 15.21% Source: Bank, HDFC sec Inst Research

Page | 12

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

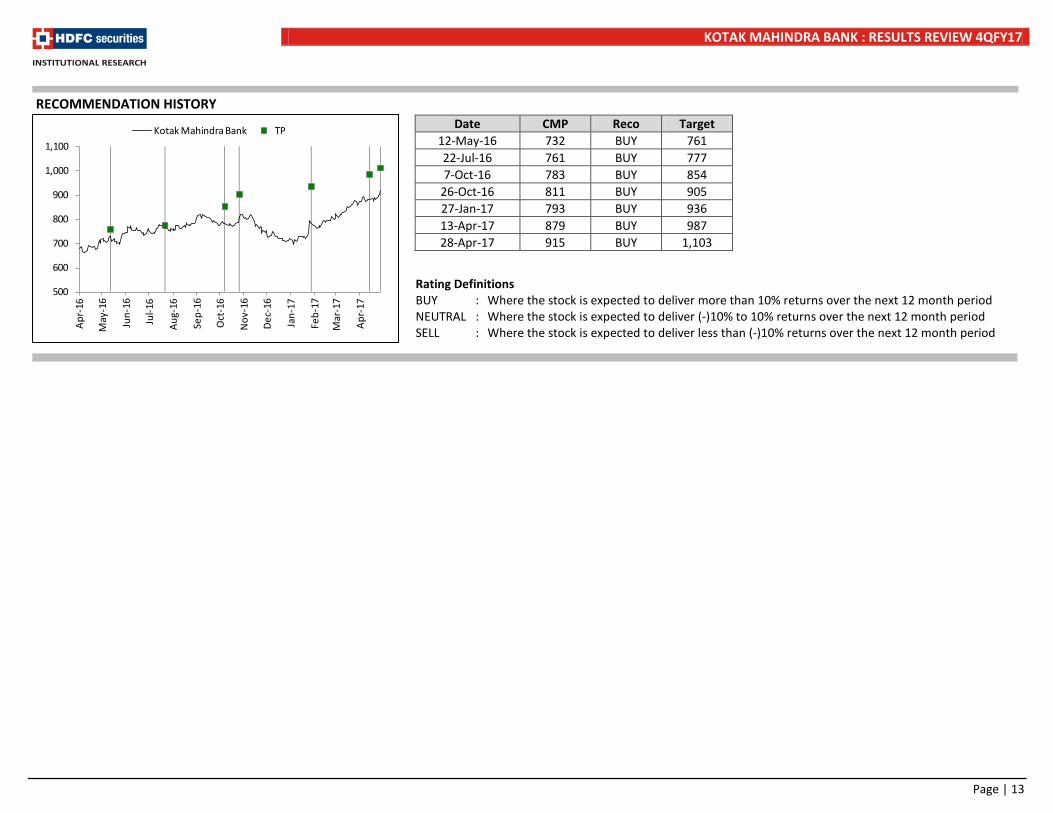

RECOMMENDATION HISTORY

Rating Definitions BUY : Where the stock is expected to deliver more than 10% returns over the next 12 month period NEUTRAL : Where the stock is expected to deliver (-)10% to 10% returns over the next 12 month period SELL : Where the stock is expected to deliver less than (-)10% returns over the next 12 month period

Date CMP Reco Target 12-May-16 732 BUY 761 22-Jul-16 761 BUY 777 7-Oct-16 783 BUY 854

26-Oct-16 811 BUY 905 27-Jan-17 793 BUY 936 13-Apr-17 879 BUY 987 28-Apr-17 915 BUY 1,103

500

600

700

800

900

1,000

1,100

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct

-16

Nov

-16

Dec

-16

Jan-

17

Feb-

17

Mar

-17

Apr

-17

Kotak Mahindra Bank TP

Page | 13

KOTAK MAHINDRA BANK : RESULTS REVIEW 4QFY17

Disclosure: We, Darpin Shah, MBA & Pranav Gupta, ACA authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock – No Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HDFC Securities Ltd or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HDFC Securities Ltd . Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HDFC Securities Ltd may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HDFC Securities and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HDFC Securities Ltd, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HDFC Securities Ltd and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report. HDFC Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HDFC Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HDFC Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HDFC Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HDFC Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report. HDFC Securities Ltd. is a SEBI Registered Research Analyst having registration no. INH000002475

HDFC securities Institutional Equities Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013 Board : +91-22-6171 7330 www.hdfcsec.com

Page | 14