Embed Size (px)

Citation preview

[email protected] July 2013

- On a restructuring mode- On a restructuring mode

Theme for growth

• Branch expansion• Capital Infusion• Restructuring the balance sheet profile

Analyst - Sanjeev JainPhone - 033-3051-2174Email Id - [email protected]

1

BuyPRICE TARGET - `1458

Initiating Coverage Report

Contents Pages

Investment & Valuation Brief 03

Company Background 04-05

Management Background 06

Business Model 07

Banking Sector Outlook 08

Investment Rationale 09-23

Peers Analysis 24

Valuations & Recommendations 25

Financial Projections 26

Ratio Analysis 27

Key Concerns 28

Analyst Page 29

Research Performance 30

Disclaimer 31

2

22nd July 2013

BUY Axis Bank Ltd

Source: Company, ACE Equity, Microsec Research

Axis Bank is the third largest Private Sector Bank (in terms of business andprofitability) to have begun operations in 1994. As on 31st March 2013, theBank’s balance sheet size crossed over INR3.4 trillions with strong distributionnetwork of 1947 branches and 11245 ATMs spread across the country. It alsohas overseas offices in Singapore, Hong Kong, Shanghai, Colombo, Dubai andAbu Dhabi. It differentiated itself from other players in the industry through itsexcelling in customer delivery through insight, empowered employees andinnovative use of technology coupled with its ubiquitous branches and ATMs.Axis Bank is one of the few Indian Banks, which has smartly managed totransform itself into a true financial conglomerate with its presence in corebanking besides, Insurance, Asset Management, Mutual Fund, Broking, HomeFinance etc.

We Initiate Coverage on Axis Bank with a BUY rating. Our rating underpinsthe Bank’s strong business growth momentum, diversified revenue stream,healthy low cost deposits (CASA) base which leads to improve in Net InterestMargin (NIM), improving core income with healthy profitability, strong riskmanagement, improving asset quality with healthy Provision Coverage Ratio(PCR), in-depth assessment of capital with strong Capital Adequacy Ratio(CAR), improving cost efficiency, healthy Return Ratios and last but not least,well aligned bank with the regulator’s guideline.

Axis Bank has managed to keep return ratios healthy. Among its peers it isbetter placed in terms of strong return ratios. It has delivered ROE and ROA of~19% and 1.7% respectively in FY13. We believe that Axis is likely to maintainits return ratios over the next couple of years and may deliver ~1.6% and ~18%ROA and ROE respectively in FY15E .

On the basis of P/BV, Axis Bank is trading at lower valuation amongst top fivePrivate Banks. At the CMP of INR1190, the stock is trading at FY13 P/BV of1.68x. The current valuation of 1.46x FY14E and 1.27x FY15E Book Value looksattractive. We recommend a BUY on the stock with a target price of INR1458(1.55x FY15E BV) with an upside potential of ~23% from the current level withan investment horizon of 12-15 months.

Sector- Banking

3

[email protected] July 2013

Source: Company, Microsec Research

Company Background Axis Bank is one of the first new generation Private Sector Bank to have begunoperations in 1994. The Bank was promoted in 1993, jointly by Specified Undertaking ofUnit Trust of India (SUUTI) (then known as Unit Trust of India), Life InsuranceCorporation of India (LIC), General Insurance Corporation of India (GIC), NationalInsurance Company Ltd., The New India Assurance Company Ltd., The OrientalInsurance Company Ltd. and United India Insurance Company Ltd. The Bank was set upwith a capital of INR115 crores, with UTI contributing INR100 crores, LIC - INR7.5crores and GIC and its four subsidiaries contributing INR1.5 crores each.

Presently, Axis Bank is the third largest Private Sector Bank in terms of business andprofitability. As on 31st March 2013, the Bank’s balance sheet size crossed over INR3.4trillions with strong distribution network of 1947 branches and 11245 ATMs spreadacross the country. It also has overseas offices in Singapore, Hong Kong, Shanghai,Colombo, Dubai and Abu Dhabi. It differentiated itself from other players in the industrythrough its excelling in customer delivery through insight, empowered employees andinnovative use of technology coupled with its ubiquitous branches and ATMs. The Bankoffers a wide range of banking products and financial services to corporate and retailcustomers through a variety of delivery channels and through its specialized subsidiariesin the areas of Investment Banking, Insurance, Mutual Fund, Broking, Home Finance etc.

Axis Bank Milestones

Axis Bank opens itsRegistered Office andCorporate Office.

Bank inauguratedits first branch atAhmadabad.

“Axis” the FirstIndian Bank launchedtravel currency card.

Bank gets listedon London stockexchange.

Launched creditcard business.

Launched India's firstand only Indiancurrency prepaid travelcard for foreignnationals.

Reached 2 lakh installedEDC machines – thehighest for any bank inIndia

4

[email protected] July 2013

5Source: Company, Microsec Research

Key Subsidiaries

Key Subsidiaries

Axis Capital Ltd.

Axis Private Equity Ltd.

Axis Trustee Services Ltd.

Axis Asset Management

Company Ltd.

Axis Mutual Fund Trustee

Ltd.

Axis Bank UK Ltd.

Axis Finance Ltd.

As on 31st March 2013, the Bank has seven subsidiaries through which it offers a wide range of banking products andfinancial services to corporate and retail customers.

[email protected] July 2013

6

Board of Directors & Management

Shikha Sharma

K. N. Prithviraj

V. R. Kaundinya

S. B. Mathur

Prasad R. Menon

R. N. Bhattacharyya

Samir K. Barua

A. K. Dasgupta

Som Mittal

Sanjiv Misra

Ireena Vittal

Rohit Bhagat

Chairman

MD & CEO

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

[email protected] July 2013

7

•Corporate lender

•Corporate deposits

• Slow growth

Phase 1: upto FY03

•Developed CASA franchise• Fee income – diversity in revenue• Period of very high growth inbusiness and network

Phase 2: FY04-09 • Predictable, consistent

profitable growth• Reduced risk concentration• Increase share of customer wallet• Improve operating leverage• Better placed in industry growth.

Phase 3: FY10 onwards

Evolution of Axis Bank’s Business Model

Continue to build and strengthenRetail Banking franchise .

Leverage strengths in CorporateBanking & Infrastructure linkedFinancial services Banking franchise

Build a full-service offering to SMEcustomers Banking franchise .

Capture end-to-end opportunities inPayments across customer segmentsBanking franchise .

Axis’s BusinessStrategy

Bank’s Business Strategy Along Four Key Themes

[email protected] July 2013

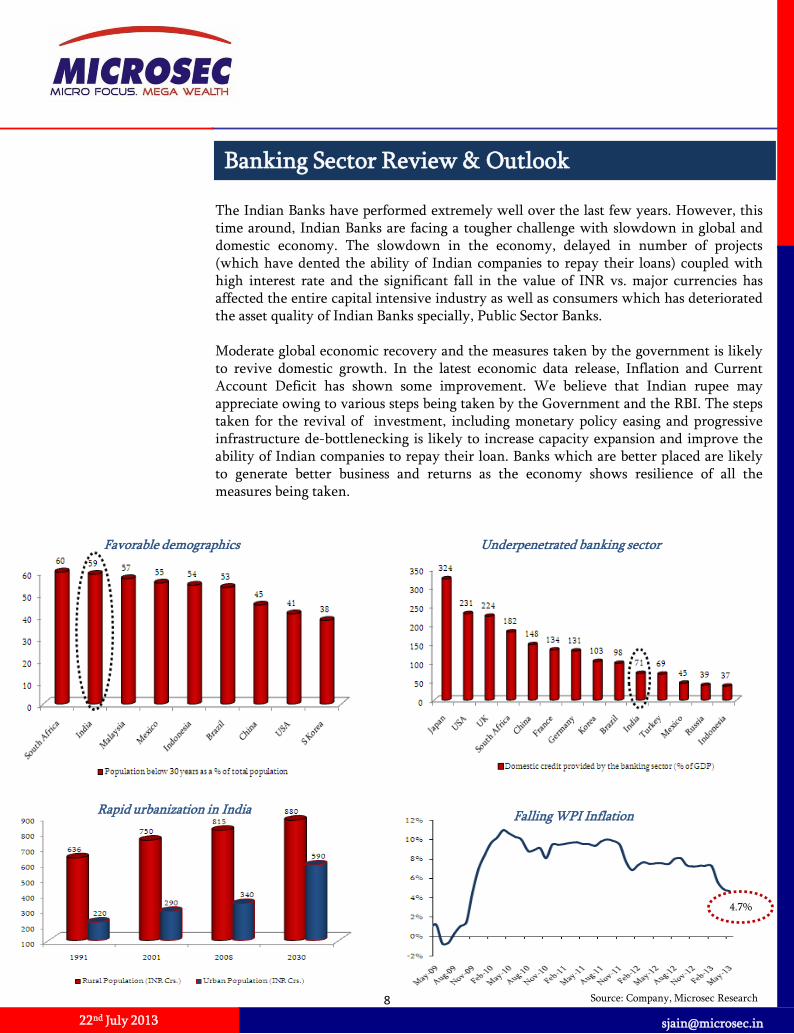

Banking Sector Review & Outlook

The Indian Banks have performed extremely well over the last few years. However, thistime around, Indian Banks are facing a tougher challenge with slowdown in global anddomestic economy. The slowdown in the economy, delayed in number of projects(which have dented the ability of Indian companies to repay their loans) coupled withhigh interest rate and the significant fall in the value of INR vs. major currencies hasaffected the entire capital intensive industry as well as consumers which has deterioratedthe asset quality of Indian Banks specially, Public Sector Banks.

Moderate global economic recovery and the measures taken by the government is likelyto revive domestic growth. In the latest economic data release, Inflation and CurrentAccount Deficit has shown some improvement. We believe that Indian rupee mayappreciate owing to various steps being taken by the Government and the RBI. The stepstaken for the revival of investment, including monetary policy easing and progressiveinfrastructure de-bottlenecking is likely to increase capacity expansion and improve theability of Indian companies to repay their loan. Banks which are better placed are likelyto generate better business and returns as the economy shows resilience of all themeasures being taken.

Favorable demographics

Rapid urbanization in India

8

Falling WPI Inflation

Underpenetrated banking sector

4.7%

Source: Company, Microsec Research

[email protected] July 2013

Microsec Research

7

30th October 2012

Investment Rationale Advances growth continues to surpass industry loan growth

Despite challenging environment, Axis has maintained its advances growth above theindustry advances growth over the past few years. Bank’s advances have grown at aCAGR of ~20% over the period of FY10-13. In FY13, the Bank has reported a 16.03%YoY advances growth to INR196966 crores while industry reported a 15.79% YoYadvances growth. Out of the Bank’s total advances, Retail and Large and Mid corporateadvances contained ~27% (~INR53200 crores) and ~50% (~INR98500 crores)respectively. The Bank’s strong relation with the corporates, focus more towards retailbusiness, diversified product portfolio, the Bank’s ubiquitous branches and hassle freecustomer services and strong risk management has pushed up the Bank’s advancesgrowth above the industry.

We believe, the Bank’s focus towards retail business along with the offtake of past projectsanctions and working capital demand by the corporate may help it to deliver theiradvances growth of ~19% and ~21% in FY14E and FY15E respectively while, industrymay grow by ~16% and 17% in the same period.

Focus towards retailbusiness along with theofftake of past projectsanctions going forwardmay boost the Bank’s loanbook growth.

Axis Bank ‘s Advances Growth Trend

Source: Ace Equity, Company, Microsec Research10

Industry Vs. Axis Bank

Quarterly Advances Growth Trend

Private Banks Vs. Axis Bank

22nd July 2013

11

Break up of advances, increasing focus towards Retail Banking

Source: Company, Microsec Research

Axis Bank has reduced its exposure from Large &Mid corporate from ~54% in FY11 to 50% in FY13owing to the risk from the slowdown in theeconomy. Furthermore, ~62% of corporateadvances have rating of at least ‘A’ in March 2013and looks healthy. Moreover, the Bank hasincreased its exposure towards retail business andthe retail loan portfolio continues to be focused onsecured products. As on 31st March 2013, theBank’s retail loan portfolio contribution to its totalloan portfolio stood at 27%, of which securedloans accounted for ~87% of the total retail loans.In addition, SME and Agriculture loan bookcontributed 15% and 8% respectively.

[email protected] July 2013

12 Source: Company, Microsec Research

Axis Bank is now focusing more on retail segmentwith a strong risk management. Out of the total retailloan book, the Bank has increased focus on its securedretail loan portfolio such as home loans whilereducing its exposure from unsecured retail loanssuch as personal loans. As on 31st March 2013,secured loans accounted for ~87% of the total retailloans and also, the Bank has reduced its exposure topersonal loans significantly to 7% from 14% in March2011. Moreover, it has also increased its exposure toauto loans by 300bps to 14% in March 2013 from 11%in March 2011.

Break up of retail loan portfolio

[email protected] July 2013

13 Source: Company, Microsec Research

Healthy loan portfolio

Rating Distribution : Large and Mid Corporate

Rating Distribution : Small & Medium Enterprise

62% of corporate advanceshave rating of at least ‘A’ inMarch 2013

80% of SME advances haverating of at least ‘SME3’ inMarch 2013

[email protected] July 2013

14

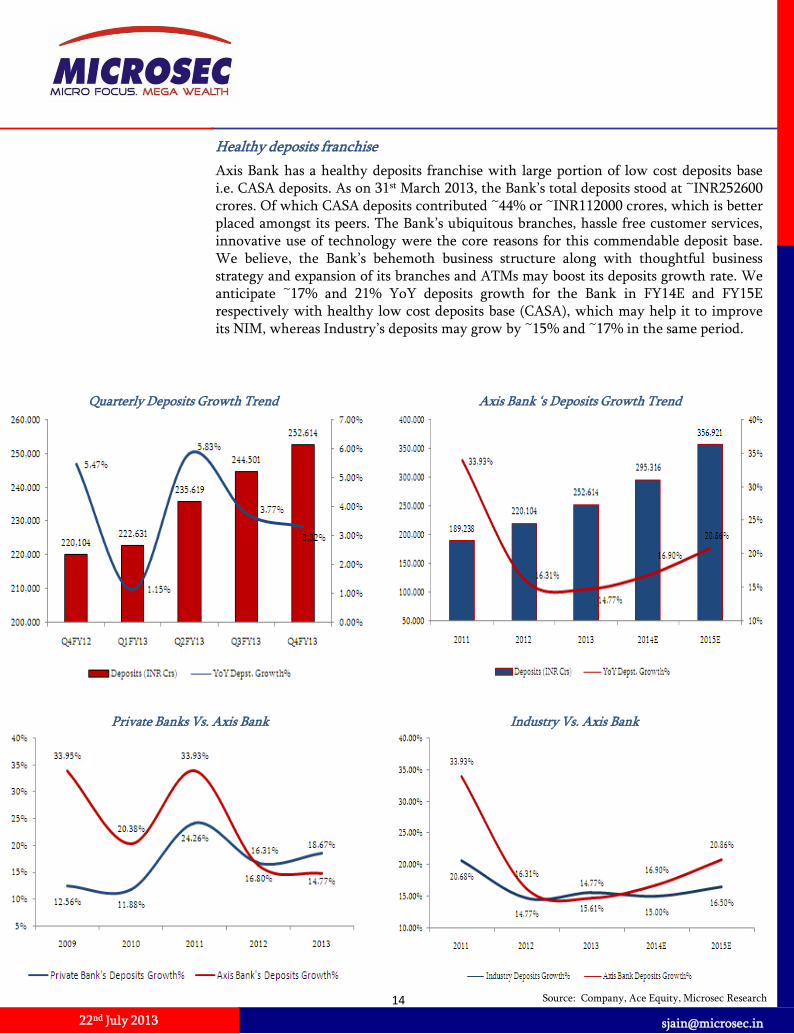

Axis Bank has a healthy deposits franchise with large portion of low cost deposits basei.e. CASA deposits. As on 31st March 2013, the Bank’s total deposits stood at ~INR252600crores. Of which CASA deposits contributed ~44% or ~INR112000 crores, which is betterplaced amongst its peers. The Bank’s ubiquitous branches, hassle free customer services,innovative use of technology were the core reasons for this commendable deposit base.We believe, the Bank’s behemoth business structure along with thoughtful businessstrategy and expansion of its branches and ATMs may boost its deposits growth rate. Weanticipate ~17% and 21% YoY deposits growth for the Bank in FY14E and FY15Erespectively with healthy low cost deposits base (CASA), which may help it to improveits NIM, whereas Industry’s deposits may grow by ~15% and ~17% in the same period.

Healthy deposits franchise

Axis Bank ‘s Deposits Growth Trend

Quarterly Deposits Growth Trend

Source: Company, Ace Equity, Microsec Research

Industry Vs. Axis Bank Private Banks Vs. Axis Bank

22nd July 2013

Customer convenience andhigh quality services throughstrong distribution andinnovative use of technologycontinued to be the bedrockof the Bank’s growthstrategy.

Strong CASA deposits underpins low-cost deposits franchise The Bank has improved its low cost deposits base from ~41% in FY11 to ~44% in FY13.Bank’s behemoth business structure along with thoughtful business strategy, focus moretowards Retail Banking and capturing salary accounts with providing high class andhassle free services to its customers and continued expansion of its branches and ATMshelped it to boost its CASA portfolio. Bank’s key priority towards healthy growth inCurrent & Savings account deposits has helped it to cross CASA deposit of over ~INR1.12 trillions in FY13. We anticipate that the Bank will maintain its CASA ratio of ~44%in FY14E and FY15E. Customers convenience and high quality services through strongdistribution and innovative use of technology continued to be the bedrock of the Bank’sgrowth strategy.

Source: Company, Ace Equity, Microsec Research

CASA growth continues to rise

Bank’s branch expansion continues to rise CASA per branch continues to rise

15

[email protected] July 2013

16

Net Interest Income continues to rise

Axis Bank has consistently maintained its Net Interest Income (NII) growth above theindustry. Bank’s NII has grown at a CAGR of ~21% whereas, Industry's NII grew at aCAGR of ~14% over the period of FY11-13. Moreover, NII contribution to its totalrevenue was ~60% in FY13 as against ~58% in FY11. It is mainly because of its focusedefforts on both the asset and liability sides of the balance sheet with rebalanced itsfunding mix and focus towards retail deposits base (CASA) with stable assets quality.

We expect ~19% and ~22% YoY growth of NII in FY14 and FY15E respectively. TheBank’s focus towards retail banking business with rising low cost deposits base and inanticipation of improvement in corporate balance sheet with stable asset quality provideus confidence on our valuation.

Axis Bank’s NII growth trend

Source: Company, Ace Equity, Microsec Research

Axis Bank Vs. Industry

Contribution of NII to Total Income is on the rise Rising interest income

[email protected] July 2013

18

Higher CASA deposits supports Margin stabilityThe Bank’s NIM has consistently been higher than the industry’s averagenotwithstanding challenging environment. In FY13, its NIM improved by 5bps to3.18% against industry’s decline by 8bps to ~2.5% primarily because of the Bank’s lowcost deposits base (CASA) which has improved from ~41% in 2011 to ~44% (~INR1.12trillions) in 2013. As on 31st March 2013 Bank’s retail contribution to the loan booksstood at 27% or ~INR53200 crores, of which secured loans accounted for ~87% of thetotal retail loans.

We anticipate the Bank’s margin may be in the range of 3.25-3.30% in FY15E,supported by reduction in deposits cost owing to increase in low cost deposit base andexpectation of improvement in domestic economy.

Quarterly Net Interest Margin Trend

Improving low costdeposits base and shiftingfocus towards retailbanking boosted margin.

Source: Ace Equity, Microsec Research

Improving Net Interest Margin (NIM)

Improving Cost of funds boosted NIM.

17

[email protected] July 2013

Improving asset quality; Strong coverage ratioIn the current challenging environment, where the banking sector is suffering from assetquality problems, Axis Bank has been able to improve its asset quality. Over the past fewquarters, the Bank has improved its NNPA and GNPA ratios. In Q4FY13, its GNPA andNNPA stood at 1.06% and 0.32% as against 1.10% and 0.33% in Q3FY13 respectively. Itis better placed amongst its peers in term of superior asset quality. Moreover, it is wellpositioned to tame time liabilities with ~79% of its Provision Coverage Ratio (PCR) and itis in third position amongst its peers in terms of high PCR. The Bank’s thoughtfulbusiness strategy and strong risk management with in-depth analysis of borrowers’profile enabled it to improve its asset quality problems.

The Bank possesses high rated loan books, around 62% of corporate advances have ratingof at least ‘A’ and ~80% of SME advances have rating of at least ‘SME3’ in March 2013.Moreover, the Bank has reduced its credit risk exposure from the top five stress sectorslike Infrastructure, Power etc by 209bps to ~27% in FY13 from ~29% in FY12. Itssuperior asset quality with reducing credit risk exposure from stress sector boosted ourconfidence on it. The following graphs depicts the Credit Risk exposure of top fivesectors.

We expect that the Bank is likely to maintain itsasset quality going forward backed by the reversal ininterest cycle, improvement in economic conditionand the Bank’s strong risk management with healthyloan portfolio and also government’s persistentsupport to ailing sectors. The management soundspositive it term of asset quality and confident on theoverall business growth.

Reducing fund and non fund based Credit Risk exposure of top 5 sectors

Banks thoughtful businessstrategy and strong riskmanagement with in-depthanalysis of borrowers’ profileenabled it to improve itsasset quality problems.

The management soundspositive it term of assetquality and confident on theoverall business growth.

Source: Company, Microsec Research 18

22nd July 2013

Asset quality trend Quarterly asset quality trend.

Healthy asset quality amongst its peers

Healthy Provision Coverage Ratio (PCR) Provision Coverage is better than its peers

19 Source: Company, ACE Equity, Microsec Research

NPAs’ recovery & Write-offs trend

[email protected] July 2013

Well capitalized Private Bank

Axis Bank is in well position to support its growth trajectory with 17% of CapitalAdequacy Ratio (CAR), which is well above the benchmark requirement of 9% stipulatedby Reserve Bank of India (RBI). Of this, Tier-I capital stood at 12.23%, while Tier-IIcapital stood at 4.77% as on 31st March 2013. The Bank’s CAR is better placed amongst itspeers. The Bank actively manages its capital to meet regulatory norms and current andfuture business needs considering the risks in its businesses, expectation of ratingagencies, share holders and investors, and the available options of raising capital.

In FY13, the Bank raised capital in the form of equity and debt to support future growth.It raised Tier I capital in the form of equity capital through a Qualified InstitutionalPlacement (QIP) and a preferential allotment of equity shares to the promoters of theBank. The Bank mobilized an aggregate of INR5537.47 crores through this offering, byissuing 34000000 equity shares through a QIP offering and 5837945 shares to promoters.Capital infusion of INR5537.47 crores has increased the Bank’s net worth by ~24% andadded ~INR55/share to the book value. Post this, the Bank’s ROE remained healthy at~18%. Moreover, Axis’s current capital structure meets the RBI’s Basel III norm.

Axis Bank’s healthy capital base

22

One of the best CAR amongst its peers

Source: Company, ACE Equity, Microsec Research

Shareholding pattern as on 31st March 2013

Bank’s recent Capitalinfusion of ~INR5537 croreshas increased the Bank’s networth by ~24% and added~INR55/share to the bookvalue.

Basel III RequirementA minimum common equitytier I capital of 5.5%, aminimum tier 1 capital ratioof 7.0% of risk weightedassets, a capital conservationbuffer of 2.5% comprisingonly common equity capitaland a minimum overallcapital adequacy ratio of9.0%.

The Basel III regulationswould be implemented inphases beginning from 1st

April 2013 and would befully implemented by March31, 2018.

20

[email protected] July 2013

Superior profitability growth continues to remain

The Bank’s operating profit has grown at a CAGR of ~21% whereas, Profit After Tax(PAT) grew at a CAGR of ~24% over the period of FY11-13. It is driven by robust growthin its Net Interest Income and Other Income at a CAGR of ~21% and 19% respectivelyover the same period. The Bank’s strong relation with the corporate, focus more towardsretail business, diversified product portfolio, Hassle free customer services through itsubiquitous branches and ATMs and stable asset quality are the core reasons for thisrobust performance. We anticipate that the Bank will maintain its growth rate over thenext couple of years supported by strong risk management with stable asset quality andfocus towards retail business portfolio.

21Source: Company, ACE Equity, Microsec Research

Operating Profit to grow at a CAGR of ~21% over FY13-15E

Other Income/Total Income

PAT to grow at a CAGR of ~18% over FY13-15E

Other Income to grow at a CAGR of ~18% over FY13-15E

[email protected] July 2013

13

Growing profitability boosted Return ratios

In the present challenging environment, where macro and micro economic environmentled to higher stress, Axis Bank has managed well and kept return ratios healthy. In FY13,its Return on Assets (ROA) was at historical high of 1.7% and Return on Equity (ROE)stood at 18.5% despite recent capital infusion of ~INR5537 crores. Moreover, it is betterplaced amongst its top four private peers in terms of high returns The Banks rapidbusiness expansion along with growing profitability and its active management ofcurrent and future business needs considering the risks in its businesses was the corereason of this achievement.

We believe that the Bank is likely to maintain its returns ratios over the next couple ofyears. We anticipate ~1.6% and ~18% ROA and ROE for FY15E respectively.

22

Healthy Return Ratios amongst its peers

Balance sheet growth is on the rise

The Bank’s balance sheet has grown at a CAGR of~18% to ~INR3.4 trillions over the period of FY11-13.We anticipate ~19% CAGR growth over the period ofFY13-15E.

Source: Company, ACE Equity, Microsec Research

Axis Bank’s ROE & ROA trend

22nd July 2013

Operationally efficient bank

Axis Bank well managed its cost efficiency reflected in itsCost/Income ratio which decreased by 210bps to 42.6% inFY13 despite the addition of 6163 new employees.Improvement in low cost deposits (CASA) coupled with focustowards retail segment and also its behemoth businessstructure helped it to improve its cost efficiency. The Bankhas consistently improved its cost/Income ratio from 2008despite significant scale-up in branches and employeestrength. Moreover, its initiative to recruitment of young andtalented employees have boosted the productivity of theBank. The Bank’s employee cost contributed 34.38% in itstotal operating expenses and the PAT contributed peremployee was ~INR14 lakh in FY13. We anticipate, theBank’s Cost/Income ratio may come down to ~41% in FY15E.

Improving Cost/Income ratio

Stable employee cost Business/employee likely to improve (INR Crs.)

Profitability/employee is on the rise (INR Crs.)

23

Assets/employee is on the rise (INR Crs.)

[email protected] July 2013

24 Source: Ace Equity, Microsec ResearchNote:- All figures are as on 31st March 2013, Return summary till 18th July 2013

[email protected] July 2013

Valuation and Recommendation Axis Bank has managed to keep return ratios healthy. It is better placed amongst its top four privatepeers in terms of strong return ratios. It has delivered ROE and ROA of ~19% and 1.7% respectivelyin FY13. We believe that the Bank may maintain its return ratios over the next couple of years andmay deliver ~1.6% and ~18% ROA and ROE respectively in FY15E .

P/BV BandValuation looks attractive

On the basis of P/BV, Axis Bank is trading at lower valuation amongst top five Private Banks. Atthe CMP of INR1190, the stock is trading at FY13 P/BV of 1.68x. The current valuation of 1.46xFY14E and 1.27x FY15E Book Value looks attractive. We recommend a BUY on the stock with atarget price of INR1458 (1.55x FY15E BV) with an upside potential of ~23% from the current levelwith an investment horizon of 12-15 months.

TTM P/BV; Valuation is inexpensive as compared to its peers

25 Source: ACE Equity, Microsec Research

22nd July 2013

26

Financials & Projections

Source: Company, Ace Equity, Microsec Research

[email protected] July 2013

Key Concerns

Glimpse of Axis Bank’s Branch

Further downturn in economic activities and growth may act as a vicious cycle oninvestment in Capex and consumer income and spending, which may impact the earnings ofthe Bank and its asset quality.

Recent increment in provision on restructuring as per the RBI new guideline may impact theprofitability.

Issuing of new Banking license may increase competition which may affect the Bank’smargin.

[email protected] July 2013

29

Recommendation

Strong Buy >20%

Buy between 10% and 20%

Hold between 0% and 10%

Underperform between 0% and -10%

Sell < -10%

Expected absolute returns (%) over 12 months

MICROSEC RESEARCH IS ALSO ACCESSIBLE ON BLOOMBERG AT <MCLI>

Microsec Research: Phone No.: 91 33 30512100 Email: [email protected]

Ajay Jaiswal: President, Investment Strategies, Head of Research: [email protected]

Fundamental Research

Name Sectors Designation Email ID

Nitin Prakash Daga IT, Telecom & Entertainment AVP-Research [email protected]

Naveen Vyas Midcaps, Market Strategies AVP-Research [email protected]

Sutapa Roy Economy Research Analyst [email protected]

Sanjeev Jain BFSI Research Analyst [email protected]

Neha Majithia Metal, Mineral & Mining Research Analyst [email protected]

Soumyadip Raha Mid Cap Executive Research [email protected]

Saroj Singh Mid Cap Executive Research [email protected]

Kapil Bhati Mid Cap Executive Research Associate [email protected]

Technical & Derivative Research

Vinit Pagaria Derivatives & Technical Senior VP [email protected]

Ranajit Saha Technical Research Sr. Manager [email protected]

Institutional Desk

Puja Shah Institutional Desk Dealer [email protected]

Abhishek Sharma Institutional Desk Dealer [email protected]

PMS Division

Siddharth Sedani PMS Research AVP [email protected]

Ketan Mehta PMS Sales AVP [email protected]

Research: Financial Planning Division

Shrivardhan Kedia FPD Products Manager Research [email protected]

Research-Support

Subhabrata Boral Research Support Asst. Manager Technology [email protected]

[email protected] July 2013

Microsec Research

34

7th December’ 2010

Microsec Research

35

7th December’ 2010

![PassBy[ME] - Bugzilla integration on CentOS 6.5 … · 5 PassBy[ME] - Bugzilla integration on CentOS 6.5 operating sytem Copyright Microsec Ltd. – 2014. 2 Installation of Bugzilla](https://img.pdfslide.net/doc/110x75/5b72a9aa7f8b9a58028d89c5/passbyme-bugzilla-integration-on-centos-65-5-passbyme-bugzilla-integration.jpg)

![PassBy[ME] - Bugzilla integration on CentOS 6.5 · PDF filePassBy[ME] - Bugzilla integration on CentOS 6.5 operating sytem Copyright Microsec Ltd. – 2014.](https://img.pdfslide.net/doc/110x75/5a7520f37f8b9a93088c25bb/passbyme-bugzilla-integration-on-centos-65-passbyme-bugzilla-integration.jpg)