Embed Size (px)

Citation preview

By A.AMARNATH, A.LE LAN, C.SANCHIS and J .TSIATENGY

1. HIGH END BABY MARKET

1. Creation of the market : 1990s

2. Origine : Usa, Manahattan and Beverllihills

3. Size of the luxury kids wear segment :

-> 3% of the global clothing market which represents 24.6 Billion Euros

• 2012 : 7.38 Billion Euros

• 2015 : 8.466 Billion Euros

• 2013 -> 2017 : 6% growth

4. Luxury baby segments : baby product / accessories / clothes / shoes

5. Major playors and new

comers :

• 2009 : First and major playors

: Ralph Lauren, Buberry and

Christian Dior ( Baby Dior :

1967)

-> Burberry sold in 2011 for 65

Million Euros with a growth of

+23 %

• 2011 : New comers : Dolce

&Gabana, Prada, John

Galliano, Lanvin, Stella Mac

Cartney, Versace ….

• 2013 : New comers : Oscar

de la Renta, Marc Jacobs,

Phillip Lim and Roberto Cavalli

2. CONSUMERS

-> very popular in Asia ( Chinese and Japanese market) :

« In Hong Kong high society wives are often seen as

ornmental showpieces….their baby are accessories and

they are willing to spend a lot of money on them »

• Henrys and HNWI

• Not price sensitive at all

• Need for self projection : Mini-me

• Status seeking

• Not many children / of first child

3. COMPETITIVE ARENA

2. LUXURY SEGMENT

• Gucci

• Fendi

• Cavalli

• Dolce and Gabana

• Chloé

• Versace

• Marc Jacobs

• Prada

• Armani

• Ferragamo

• Oscar de la renta….

3. AFFORDABLE LUXURY

• Ralph Lauren

• Marni

• Stella Mac Cartney

1. ULTRA LUXURY

SEGMENT

• Christian Dior

• Lanvin

• Burberry

• Jonh Galliano

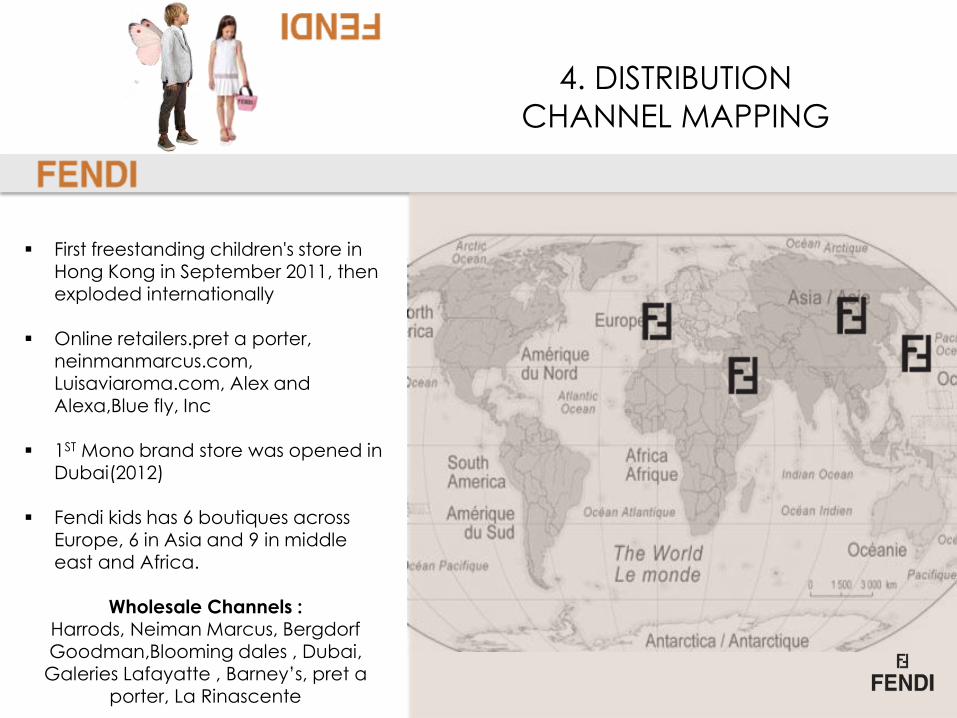

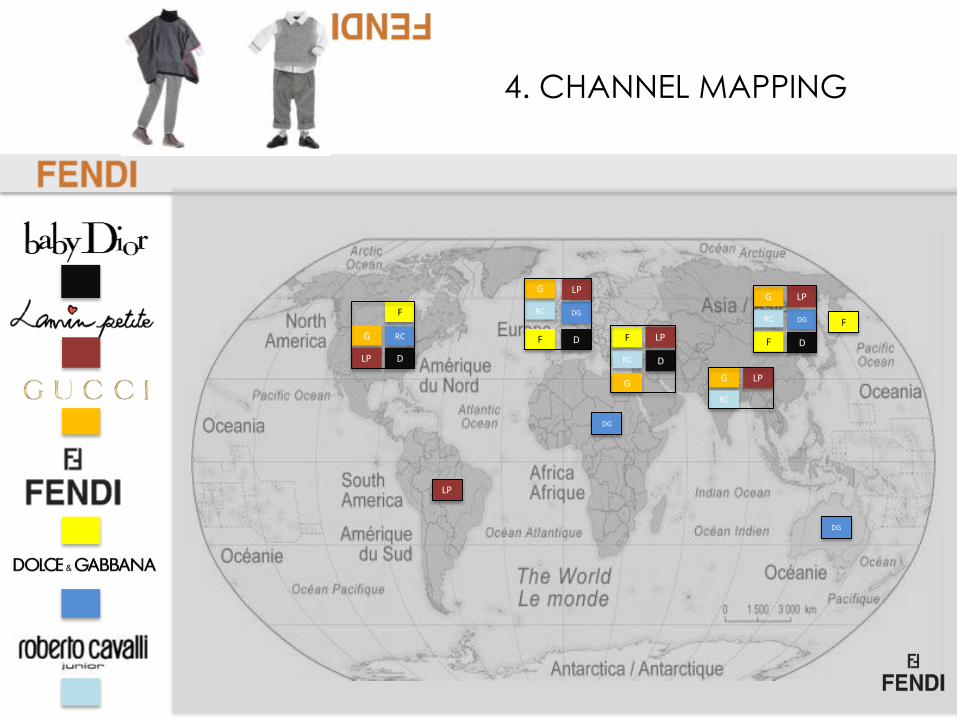

First freestanding children's store in Hong Kong in September 2011, then exploded internationally

Online retailers.pret a porter,

neinmanmarcus.com, Luisaviaroma.com, Alex and Alexa,Blue fly, Inc

1ST Mono brand store was opened in

Dubai(2012)

Fendi kids has 6 boutiques across Europe, 6 in Asia and 9 in middle east and Africa.

Wholesale Channels :

Harrods, Neiman Marcus, Bergdorf Goodman,Blooming dales , Dubai,

Galeries Lafayatte , Barney’s, pret a

porter, La Rinascente

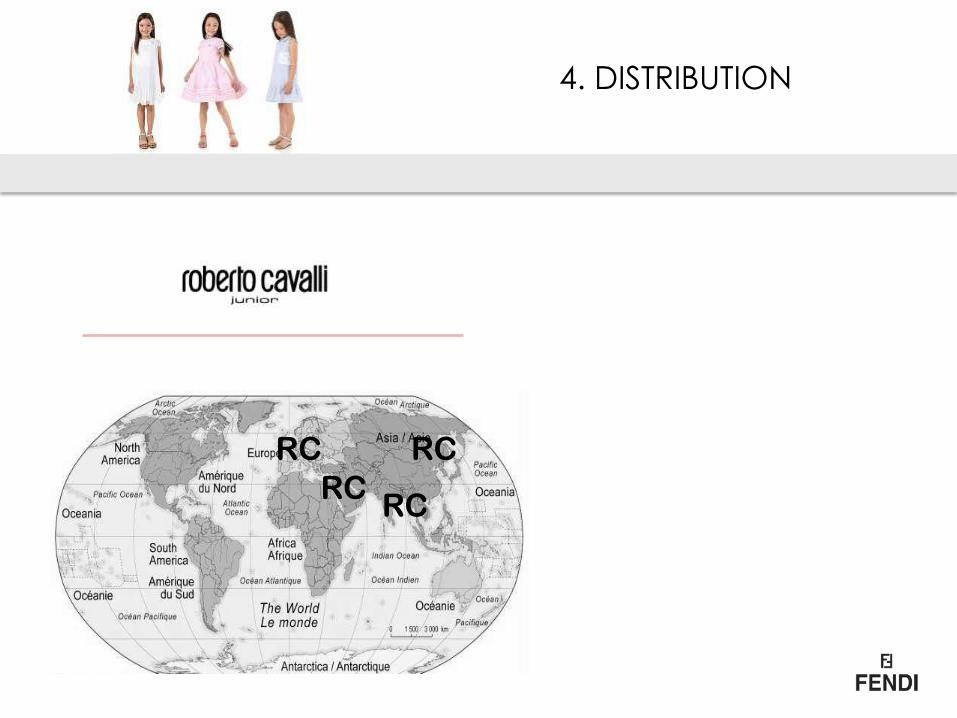

4. DISTRIBUTION

CHANNEL MAPPING

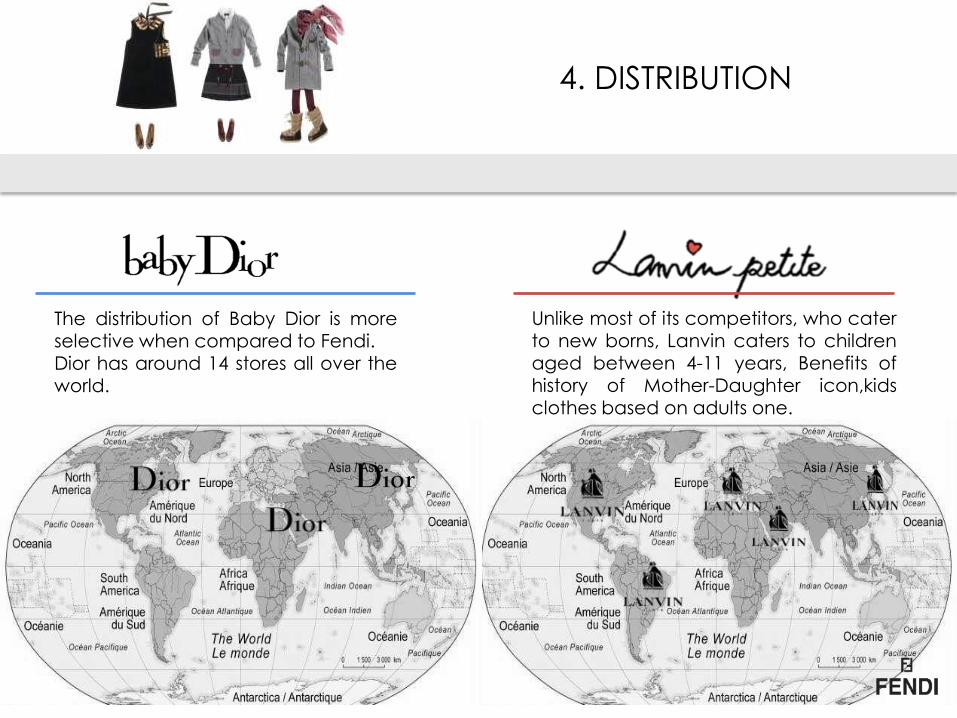

The distribution of Baby Dior is more selective when compared to Fendi.

Dior has around 14 stores all over the world.

Unlike most of its competitors, who cater

to new borns, Lanvin caters to children aged between 4-11 years, Benefits of history of Mother-Daughter icon,kids clothes based on adults one.

4. DISTRIBUTION

Gucci was also the first brand to open an exclusive children’s store on 5th Avenue in New York.

The brand posted images on Facebook of its Britain store showing its store decorations for Christmas.( Fendi used an email campaign

“Winterland Adventures” to publicize its fall/winter 2013-14 children’s collection)

4. DISTRIBUTION

D&G

D&G D&G

D&G

D&G

4. DISTRIBUTION

RC RC

RC RC

4. CHANNEL MAPPING

RC

G

LP

RC

D

F

LP

DG

DG

D

LP G

RC

F F

G

LP

D

LP G

RC

F

F D

RC DG

G LP

DG

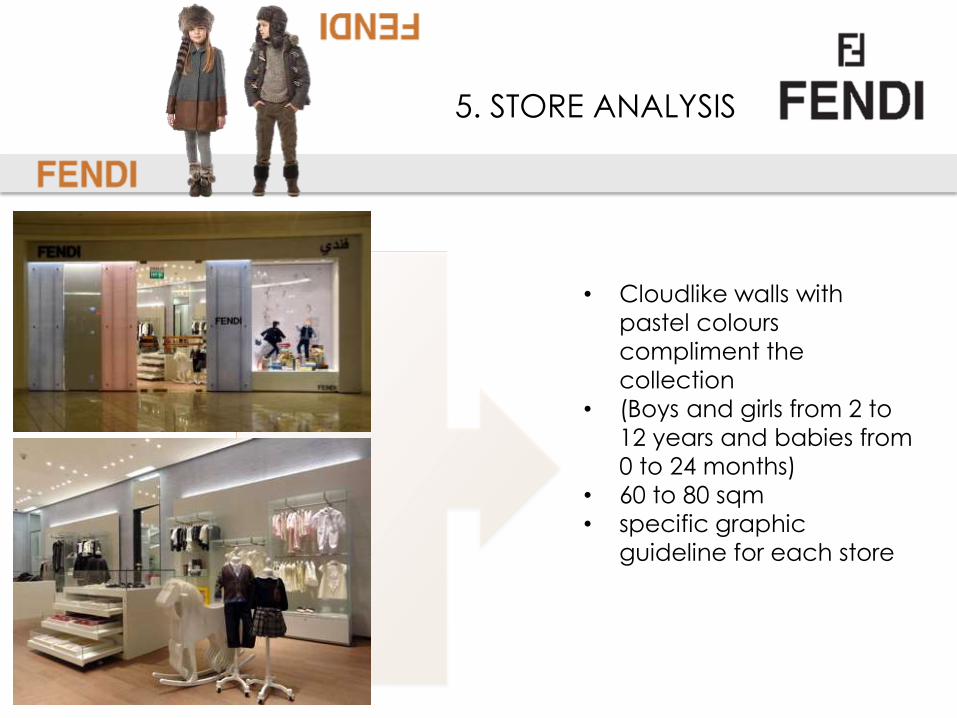

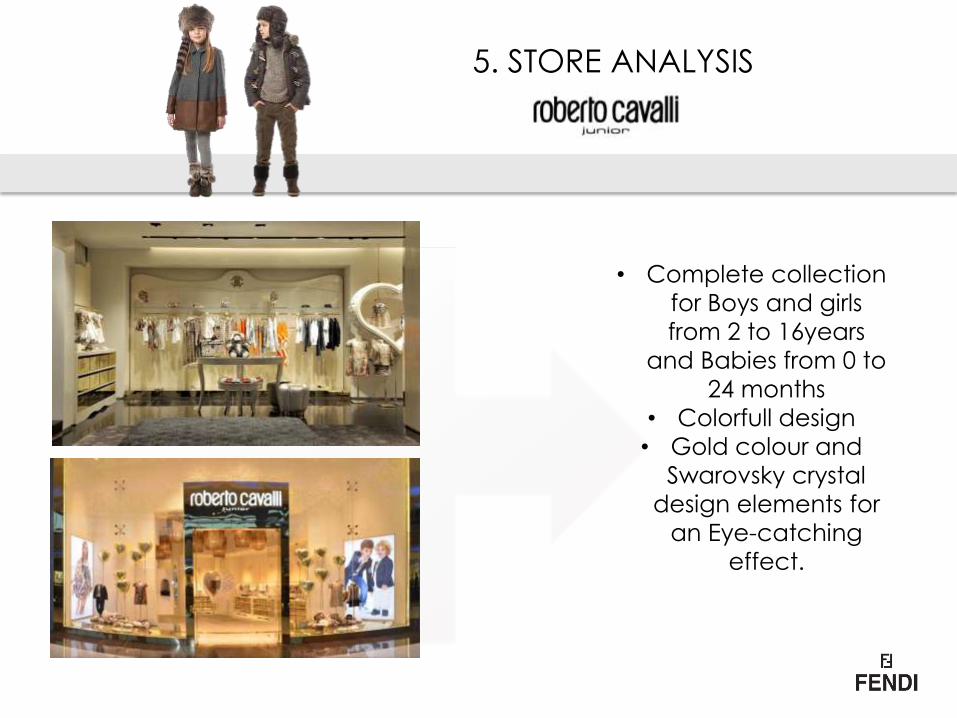

5. STORE ANALYSIS

• Cloudlike walls with

pastel colours

compliment the

collection

• (Boys and girls from 2 to

12 years and babies from

0 to 24 months)

• 60 to 80 sqm

• specific graphic

guideline for each store

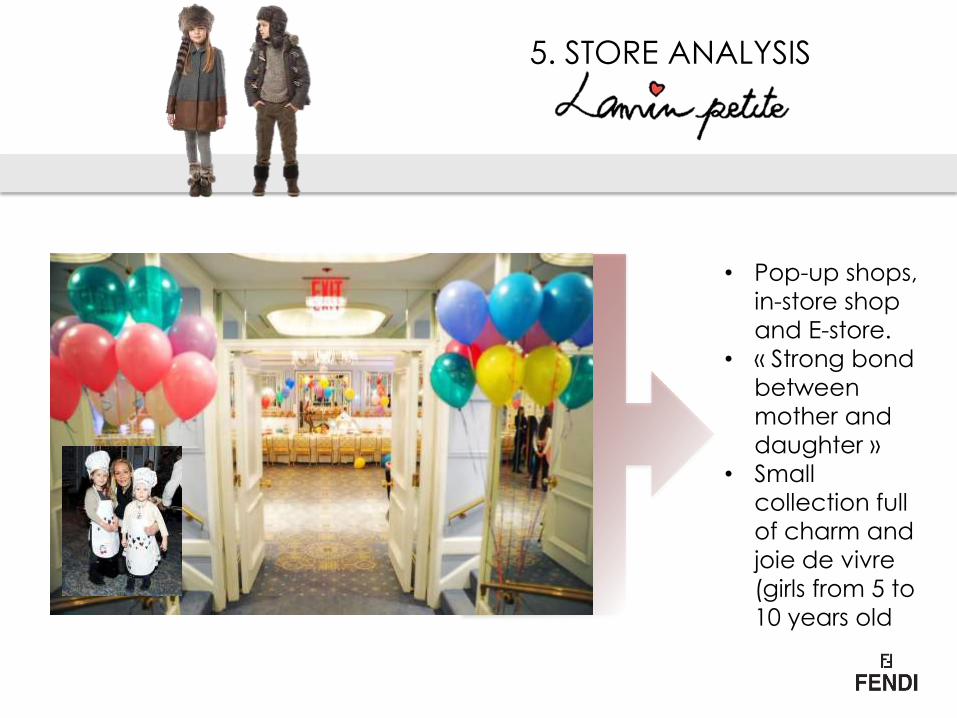

• Pop-up shops,

in-store shop

and E-store.

• « Strong bond

between

mother and

daughter »

• Small

collection full

of charm and

joie de vivre

(girls from 5 to

10 years old

5. STORE ANALYSIS

• Simple

structure in

frontage and

lavish Fabrics

inside.

• High ceiling

with bright

light

• Decoration

retro which

reminds the

extravagant

but simple

chic from the

60’s

5. STORE ANALYSIS

• Front of the store

painted in ivory

• Somptuous but cool and

funky for D&G Baby,

D&G Junior, and D&G

Teen on 70 sq

• Interior design

champagne with

lacquered wood.

• Walls are made of soft

beige velvet.

• Curtains and walls are

made of soft beige

velvet.

5. STORE ANALYSIS

• Complete collection

for Boys and girls

from 2 to 16years

and Babies from 0 to

24 months

• Colorfull design

• Gold colour and

Swarovsky crystal

design elements for

an Eye-catching

effect.

5. STORE ANALYSIS

• Glamour, fashionable

and timeless place

• Miniature furniture

• Eco-friendly teddy

bears

• Sophisticated interior

design mirror

Clothings, apparels

and accessories for

babies to 8 years old

children.

6. STORE ANALYSIS

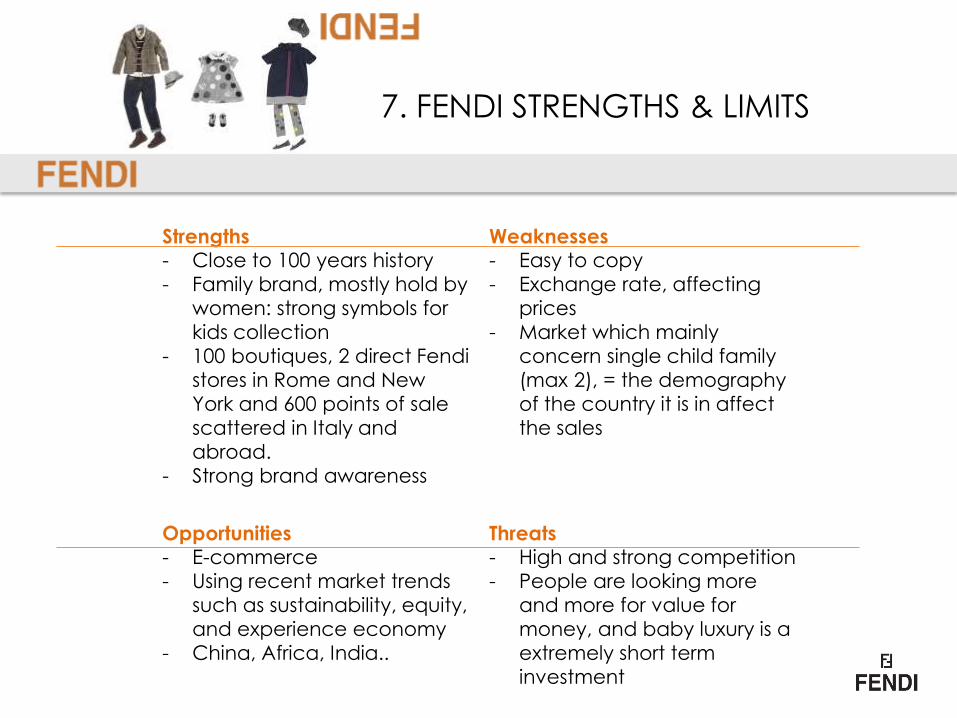

Strengths - Close to 100 years history

- Family brand, mostly hold by

women: strong symbols for

kids collection

- 100 boutiques, 2 direct Fendi

stores in Rome and New

York and 600 points of sale

scattered in Italy and

abroad.

- Strong brand awareness

Weaknesses - Easy to copy

- Exchange rate, affecting

prices

- Market which mainly

concern single child family

(max 2), = the demography

of the country it is in affect

the sales

Opportunities - E-commerce

- Using recent market trends

such as sustainability, equity,

and experience economy

- China, Africa, India..

Threats - High and strong competition

- People are looking more

and more for value for

money, and baby luxury is a

extremely short term

investment

7. FENDI STRENGTHS & LIMITS

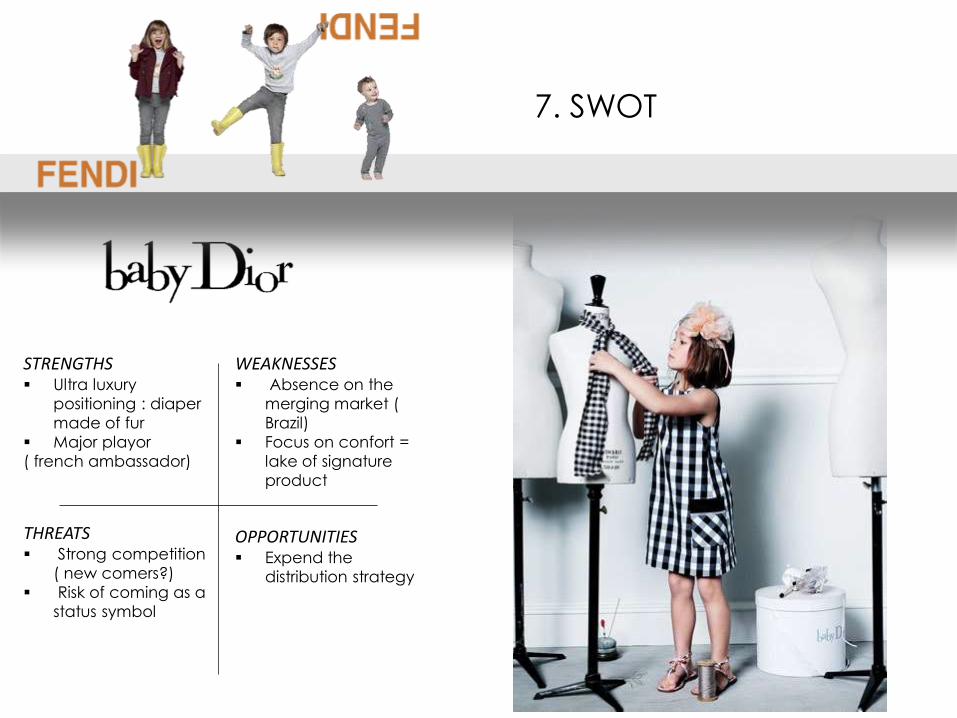

7. SWOT

THREATS Strong competition

( new comers?)

Risk of coming as a

status symbol

STRENGTHS Ultra luxury

positioning : diaper

made of fur

Major playor

( french ambassador)

WEAKNESSES Absence on the

merging market (

Brazil)

Focus on confort =

lake of signature

product

OPPORTUNITIES Expend the

distribution strategy

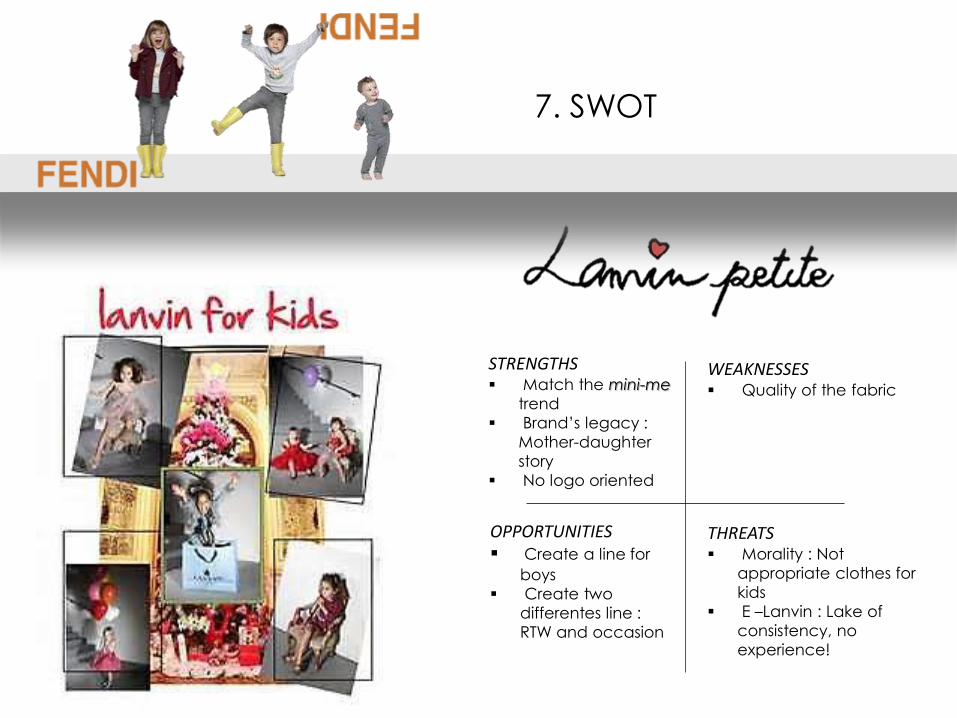

7. SWOT

THREATS Morality : Not

appropriate clothes for

kids

E –Lanvin : Lake of

consistency, no

experience!

STRENGTHS Match the mini-me

trend

Brand’s legacy :

Mother-daughter

story

No logo oriented

WEAKNESSES Quality of the fabric

OPPORTUNITIES Create a line for

boys

Create two

differentes line :

RTW and occasion

7. SWOT

:

STRENGTHS Strong identity and

symbol ( golden

teddy bear)

Major playor

WEAKNESSES Agressive

distribution

strategy

OPPORTUNITIES Reduce the

number of stores :

keep the brand’s

exclusivity

THREATS Strong

competition within

this segment

(Fendi,

Dolce&Gabana,

Roberto Cavalli…)

7. SWOT

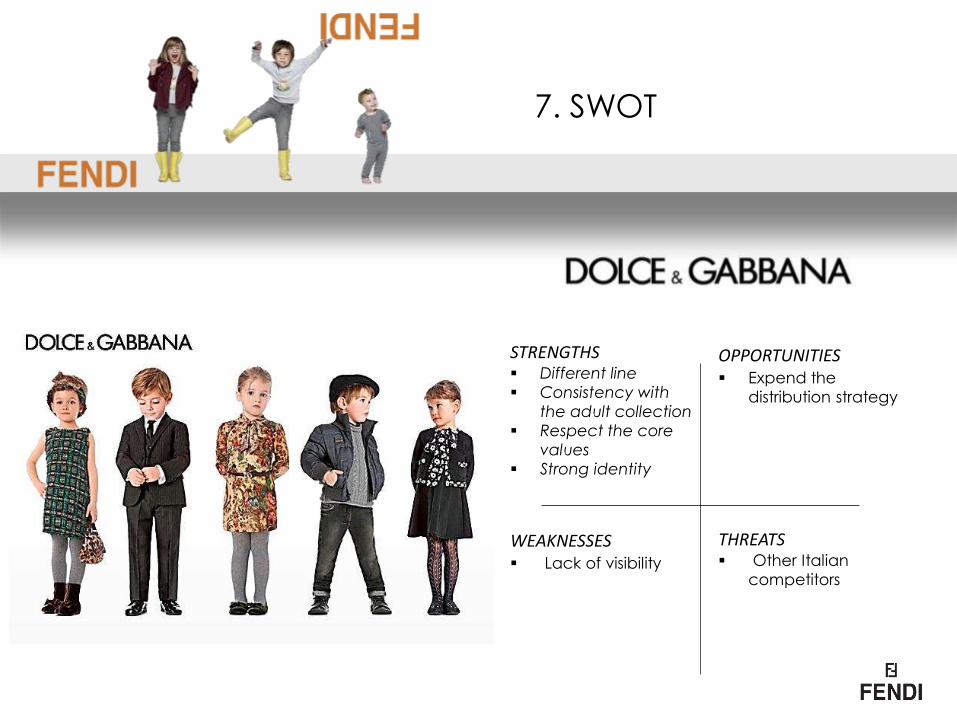

THREATS Other Italian

competitors

STRENGTHS Different line

Consistency with

the adult collection

Respect the core

values

Strong identity

WEAKNESSES Lack of visibility

OPPORTUNITIES Expend the

distribution strategy

7. SWOT

STRENGTHS Strong identity

WEAKNESSES Strong identity

Morality : Not

appropriate

clothes for kids

OPPORTUNITIES Expend the

distribution

strategy

THREATS Other Italian

competitors

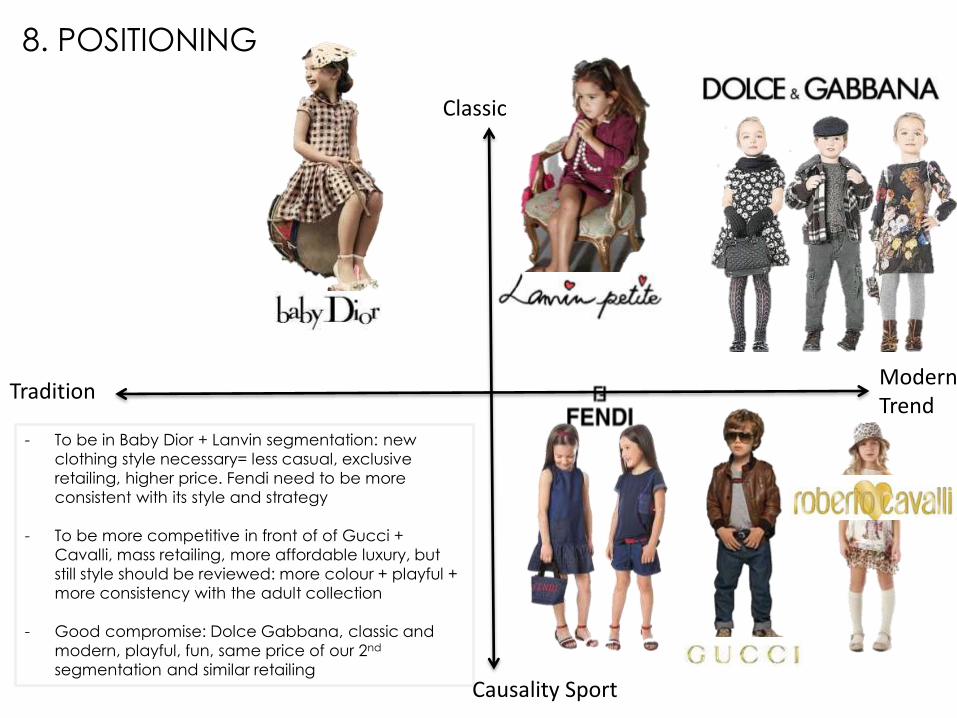

- To be in Baby Dior + Lanvin segmentation: new

clothing style necessary= less casual, exclusive

retailing, higher price. Fendi need to be more

consistent with its style and strategy

- To be more competitive in front of of Gucci +

Cavalli, mass retailing, more affordable luxury, but

still style should be reviewed: more colour + playful +

more consistency with the adult collection

- Good compromise: Dolce Gabbana, classic and

modern, playful, fun, same price of our 2nd

segmentation and similar retailing

Classic

Modern Trend

Tradition

Causality Sport

8. POSITIONING

9. NEW TARGET MARKET : Brazil !

- The size of the luxury market represents only 1% of the population size -35 % of the brazlian luxury market corresponds to foreign brands - Foreign brand make 70% of their revenue by the retail - The Brazilian market is much stronger when it comes to food and beverages, hospitality the foreigner are more successful in the other sectors : fashion, cosmetics, automobiles… - The main market in Brazil are the shoes ( 19%) and the clothing apparel ( 18%) - Very dynamic market since everything can be produced internally - The luxury market is driven by the bourgeoisie - 60% of the population is under 39 years old = digital channel is growing exponentially

BRAZIL

The size of the luxury market

represents only 1% of the population

size

Foreign brand make 70% of their

revenue by the retail

The main market in Brazil are the

shoes ( 19%) and the clothing

apparel ( 18%)

Very dynamic market

The luxury market is driven by the

bourgeoisie

Digital channel is

10. COMPETITORS

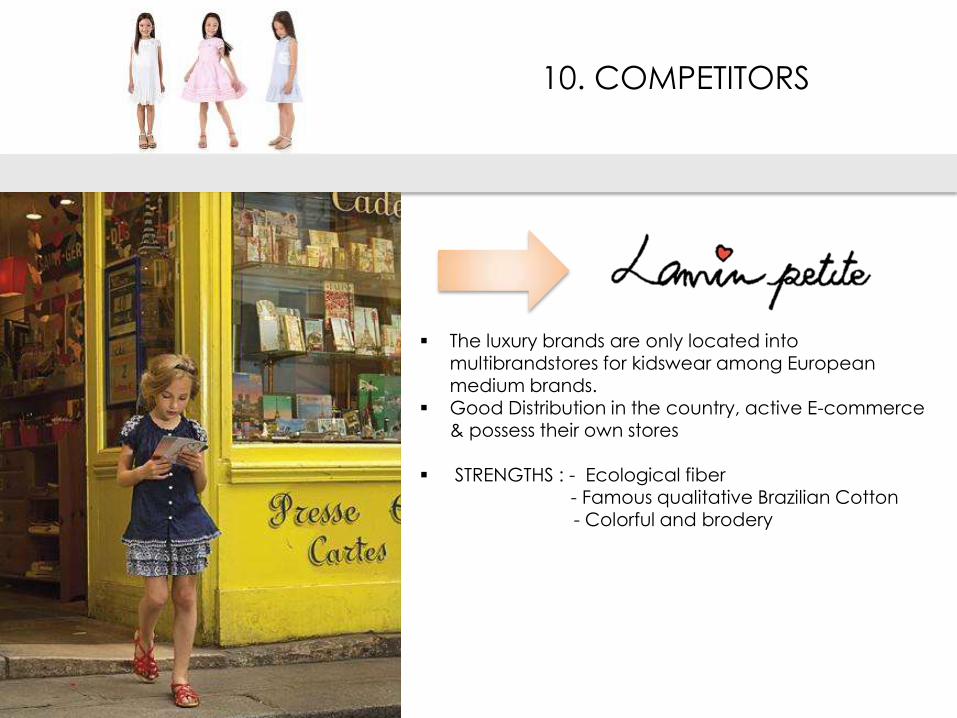

The luxury brands are only located into multibrandstores for kidswear among European medium brands.

Good Distribution in the country, active E-commerce & possess their own stores

STRENGTHS : - Ecological fiber - Famous qualitative Brazilian Cotton - Colorful and brodery

11. CONSUMER PROFIL

Attracted by the luxury

landscape

1/3 of the 165 Brazilian millionaire

have under 35 years old

Get used to shop within

shopping males

Close relationship with sales

people ( CRM tools! )

Focus on Fashion European

brands

No « luxury education »

Attracted by the luxury

landscape

1/3 of the 165 Brazilian millionaire

have under 35 years old =

Potential target

Get used to shop within

shopping males

Got strong and close relationship

with sales people who are more

personal consultant = the

customer relationship is the key of

this market + CRM

They mainly appreciate the

foreign brand = focus on Fashion

European brands

No « luxury education »

12. PRODUCT STRATEGY

Yellow Oilskin : Inlay piece of lambskin

for print, the collar and cuffs. Knitted Cardigan

Silk Crepe Skirt : Safran silk crepe belt & Plissé silk crepe navy

Kimono sleeve Tshirt: Safran silk crepe & serigraphy printed with Palms brode with square sequins

1. Capsule collection for entering the

market

It shows that Fendi knows the market

and the Brazilian consumers : Colors,

shape, fabric…

Create brand’s awareness

2. Current pieces with European style :

introduce the FENDI style there

« Mini moi » strategy

Product endorsment ( Strategy)

Focus on customer elationship and

brand ambassador

In house production : Take advantage of

the natural ressources

13. DISTRIBUTION

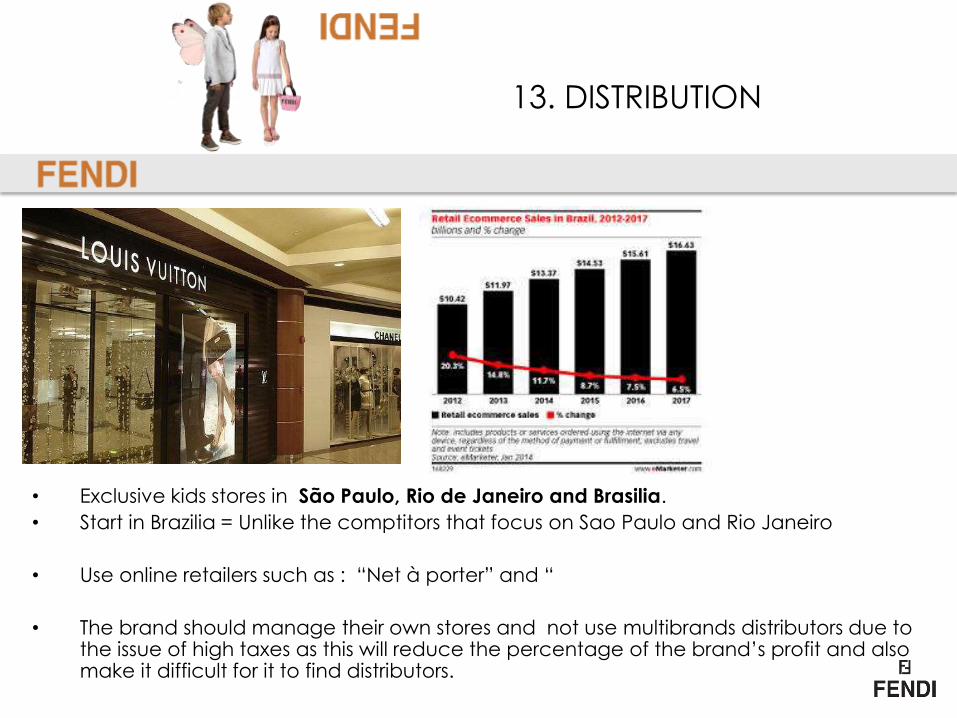

• Exclusive kids stores in São Paulo, Rio de Janeiro and Brasilia.

• Start in Brazilia = Unlike the comptitors that focus on Sao Paulo and Rio Janeiro

• Use online retailers such as : “Net à porter” and “

• The brand should manage their own stores and not use multibrands distributors due to the issue of high taxes as this will reduce the percentage of the brand’s profit and also make it difficult for it to find distributors.

• Exclusive kids stores in São Paulo, Rio de Janeiro and Brasilia. Sao Paulo being the economic capital of the city and Rio de Janeiro is part of the top ten travel destination list.

• Use online retailers such as netaporter and saksfifth avenue to reach this market as they are one the most widely used channel by many brands.

• Can also set up a floor in the existing flagship store

• The brand should manage their own stores and not use distributors due to the issue of high taxes as this will reduce the percentage of the brand’s profit and also make it difficult for it to find distributors.

14. PRICING

• Very high taxation policy – this means double or triple the European or American purchase price.

• A comparison between prices in the Brazil and in Spain on basic

pieces find differences from 11% to 76%. This indicates the low level

of profits and the reason some goods are considered premium

goods

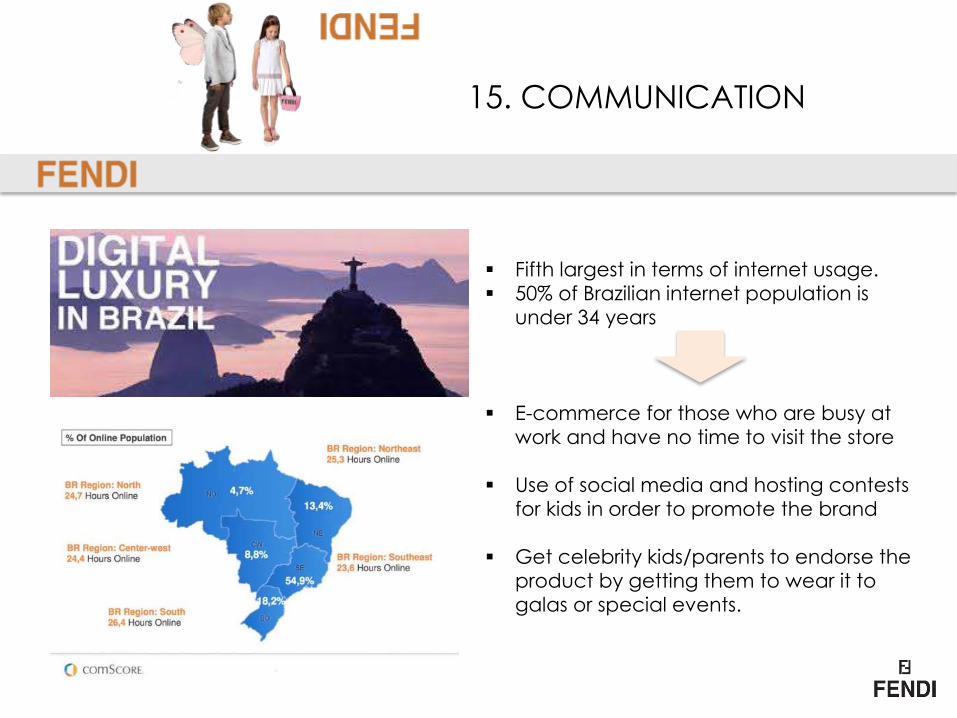

15. COMMUNICATION

Fifth largest in terms of internet usage.

50% of Brazilian internet population is

under 34 years

E-commerce for those who are busy at

work and have no time to visit the store

Use of social media and hosting contests

for kids in order to promote the brand

Get celebrity kids/parents to endorse the

product by getting them to wear it to

galas or special events.

16. CRM

Loyalty based programs (as Brazilians

are very loyal to brands they like)

CRM

Strategies: Offer direct contact,

develop relationship with tourists,

referral programmes, organize baby

shower for special/loyal clients or her

friends. Send customers offers/

updates only based on the gender

of their child

Use of website and mobile

marketing to reach tech savvy

consumers.

17. Brazil ! STRENGTHS & LIMITS

OPPORTUNITIES : -New city for the distribution such as : Brazilia, Curitiba -Luxury brand invest directly in the country ( Eg: Prenium cars) - Create specific collection for this market - The 2014 Wolrd Cup

THREATS : -Local luxury brands ( Alenxander Herchcovich, Salinas and Osklen) - Luxury distribution in the shopping malls ( Cannibalisme)

Strengths Weaknesses

Opportunities Threats

-1/3 of the millionaire are under 35 years old - Strong relationship with sales

people -Fastly growing market ( luxury) - 70% of the revenue of the foreign luxury bran is done by the retail - Main position in the apareal market - Fully integrated supply chain

-High level of taxes : Tax burden ( x2 or x3 the initial price) - Bureaucraty - Size of the market / size of the population = 1%

- Educate cosummers about luxury

-Local luxury brands

-Luxury distribution in the shopping malls ( Cannibalisme)

-New city for the distribution such as : Brazilia, Curitiba -Luxury brand invest directly in the country ( Eg: Prenium cars) - Create specific collection for this market

18. STRATEGIES

• « Mi-me trend » -> They should find inspiration in their

adult collection for the kids clothes which looks more

younger

• The monogram should be more silent for the kid’s line

• More leather in their products

• Etablish signature products + creation of a graphic

guideline : Promote « Fantasy and joie de vivre »

• Fendi has to Embdodies the Italian identity !

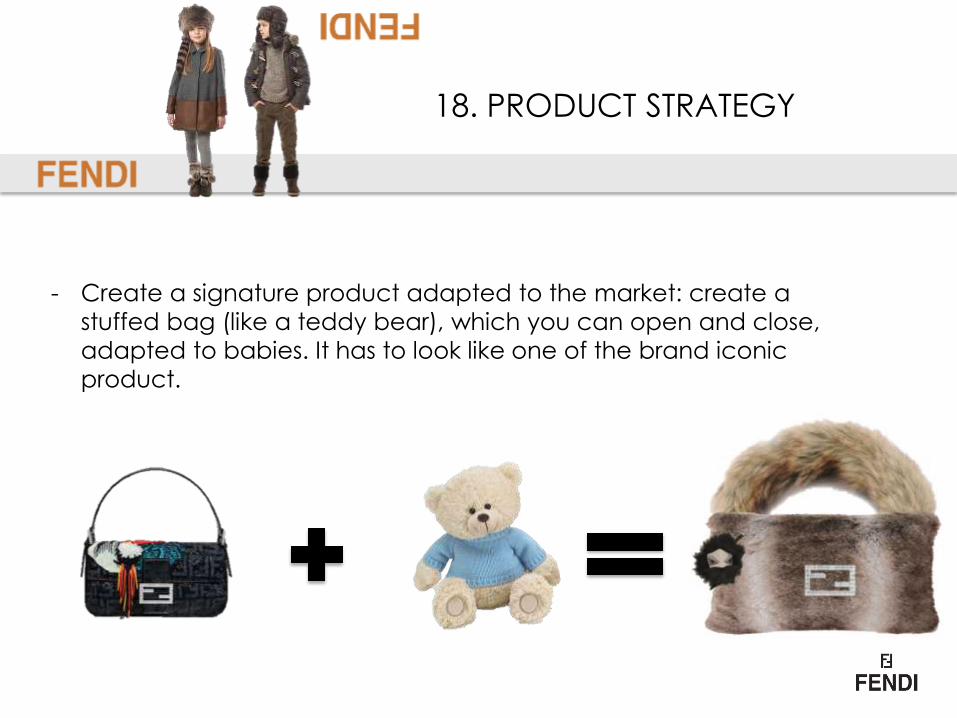

- Create a signature product adapted to the market: create a

stuffed bag (like a teddy bear), which you can open and close,

adapted to babies. It has to look like one of the brand iconic

product.

18. PRODUCT STRATEGY

18. PRODUCT STRATEGY

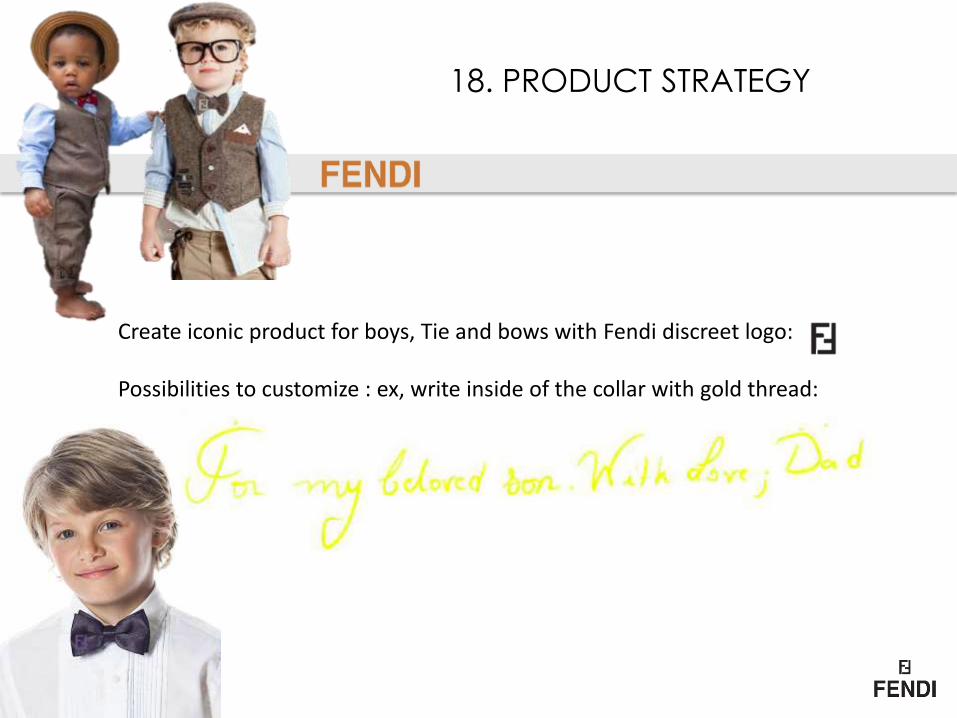

Create iconic product for boys, Tie and bows with Fendi discreet logo: Possibilities to customize : ex, write inside of the collar with gold thread:

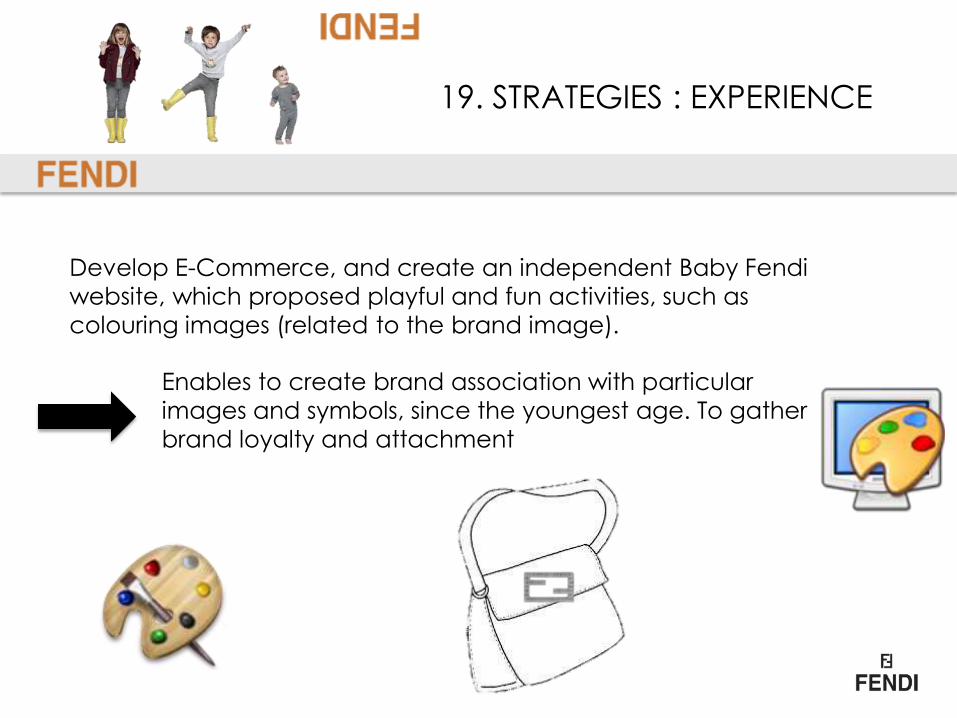

Develop E-Commerce, and create an independent Baby Fendi

website, which proposed playful and fun activities, such as

colouring images (related to the brand image).

Enables to create brand association with particular

images and symbols, since the youngest age. To gather

brand loyalty and attachment

19. STRATEGIES : EXPERIENCE

• Create Experience ! Comité Colbert was aimed to promote

French lifestyle internationally, Fendi could create structure

accepting children and cheering them, in activities around the

Italian culture and its attributes, promoting Italia.

• Will be based in key location, enabling parents to shop while

their children are entertained in a playful and intellectual

manner.

• Activities example: Cooking activities, mix and match: learn

how to dress with style, artistic based activities, music..

19. STRATEGIES : EXPERIENCE

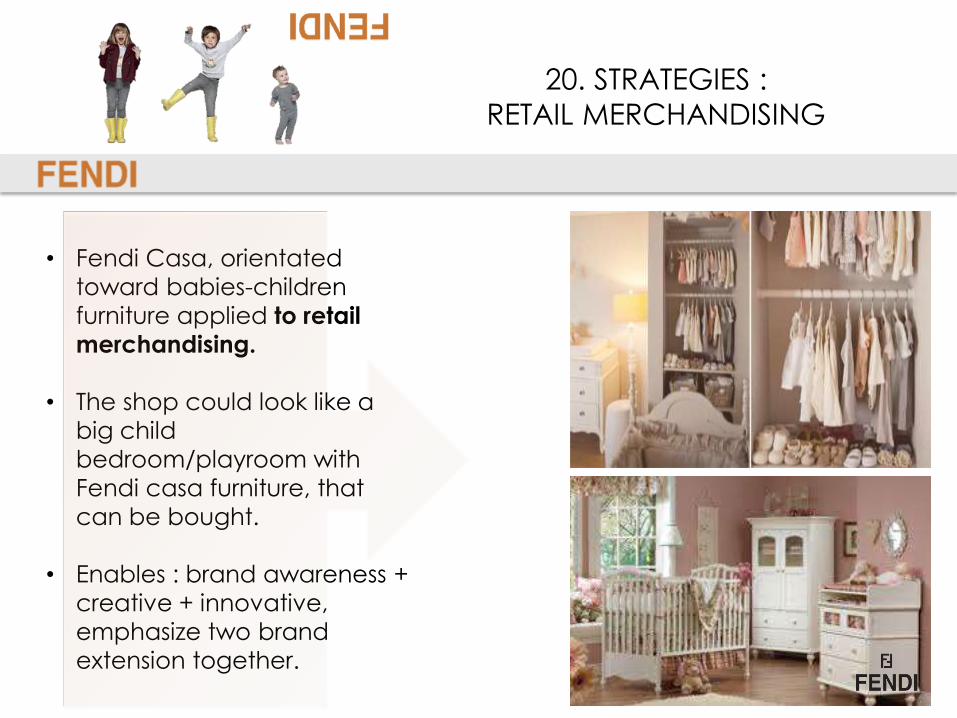

• Fendi Casa, orientated

toward babies-children

furniture applied to retail

merchandising.

• The shop could look like a

big child

bedroom/playroom with

Fendi casa furniture, that

can be bought.

• Enables : brand awareness +

creative + innovative,

emphasize two brand

extension together.

20. STRATEGIES :

RETAIL MERCHANDISING

• Make available in Sims store,

baby Fendi clothes + Children

furniture.

• Product placement + brand

awareness, target all ages

(mostly females).

• Diesel already made collection

available to buy on add on for

the game.

• All the babies/children clothes

and furniture collection in the

game or add on are a bit

disappointing.

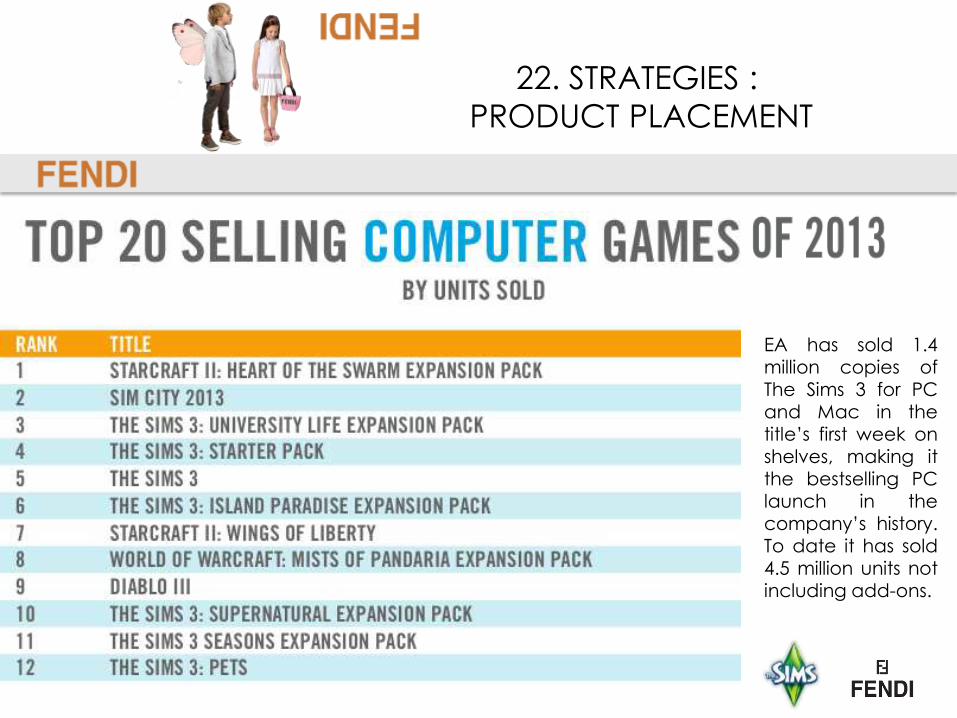

21. STRATEGIES :

PRODUCT PLACEMENT

22. STRATEGIES :

PRODUCT PLACEMENT

EA has sold 1.4 million copies of

The Sims 3 for PC and Mac in the title’s first week on shelves, making it the bestselling PC launch in the company’s history. To date it has sold

4.5 million units not including add-ons.

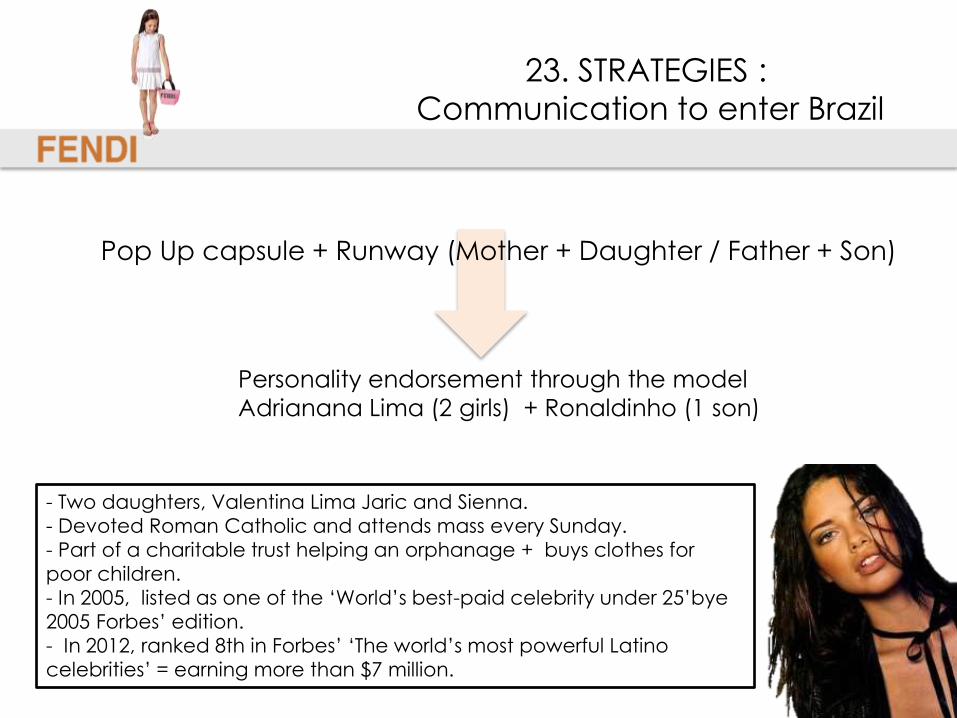

23. STRATEGIES :

Communication to enter Brazil

Pop Up capsule + Runway (Mother + Daughter / Father + Son)

Personality endorsement through the model

Adrianana Lima (2 girls) + Ronaldinho (1 son)

- Two daughters, Valentina Lima Jaric and Sienna.

- Devoted Roman Catholic and attends mass every Sunday.

- Part of a charitable trust helping an orphanage + buys clothes for

poor children.

- In 2005, listed as one of the ‘World’s best-paid celebrity under 25’bye

2005 Forbes’ edition.

- In 2012, ranked 8th in Forbes’ ‘The world’s most powerful Latino

celebrities’ = earning more than $7 million.

9. PRODUCT IMPROVEMENT &

OPPORTUNITIES

By A.AMARNATH, A.LE LAN, C.SANCHIS and J .TSIATENGY

THANK YOU FOR

YOUR ATTENTION !

![Notes for Wireless LAN Users - Ricohsupport.ricoh.com/bb_v1oi/pub_e/oi/0001048/0001048163/VJ0276645/J... · 1 Notes for Wireless LAN Users ... Easy Setup 6. Press the [] ... see Notes](https://img.pdfslide.net/doc/110x75/5b7289d17f8b9ae54f8ccada/notes-for-wireless-lan-users-1-notes-for-wireless-lan-users-easy-setup.jpg)