Embed Size (px)

Citation preview

1.Firstfilloutyourfederalincometaxreturn—U.S.Form1120.YouwillneedinformationfromyourfederalreturntocompleteyourColoradoreturn.

2.Ifyouowethestate,makeyourcheckormoneyorderpayabletotheColoradoDepartmentofRevenue.Pleaseprintthecorporation’sColoradoaccountnumberand“Form112”onthecheckormoneyorder.

3.MailthereturntotheColoradoDepartmentofRevenue,Denver,Colorado80261-0006.Returnsareduethreeandone-halfmonthsafterthecloseofthetaxableyear.

CONTENTS: ColoradoCcorporationincometaxreturn,Form112Corporationcreditschedule,Form112CRPaymentvoucherforextensionoftimeforfiling,Form158C

C COrpOraTiON 2009 iNCOME TaX

FOrMS aND iNSTrUCTiONS

(10/07/09)

Modernized e-File (MeF) Corporation Electronic FilingBoth Federal and Colorado returnsFor information and availability, see

www.revenue.state.co.us/corporationefileColorado Online Tax Payments

For information and availability, seewww.colorado.gov/paytax

Coloradoincometaxreturnsareduetobefiledthreeandone-halfmonthsafterthecloseofthetaxyear.

Anautomaticsix-monthextensionoftimeforfilingtheColoradocorporationincometaxreturnisallowedforalltaxpayers.However,anextensionoftimetofileisnotanextensionoftimetopaythetax.Ifatleast90percentofthenettaxliabilityisnotpaidbytheoriginalduedateofthereturn,penaltyandinterestwillbeassessed.If90percentormoreofthenettaxliabilityispaidbytheoriginalduedateofthereturnandthebalanceispaidwhenthereturnisfiledbythelastdayoftheextensionperiod,onlyinterestwillbeassessed.

Ifaftertheoriginalduedateofthereturnitisfoundthattheamountpaidisinsufficienttomeetthe90percentrequirement,additionalpaymentshouldbemadeassoonaspossibletoreducefurtheraccumulationofpenaltyandinterest.Despitebeingmadeaftertheduedate,thispaymentshouldberemittedasanextensionpayment.

AfederalextensionoftimeforfilingwillnotbeacceptedforColoradopurposes.

Besuretoroundyourpaymenttothenearestdollar.Youmustenter00afterthedecimalpoint.Theamountonthecheckandtheamountenteredonthepaymentvouchermustbethesame.Thiswillhelpmaintainaccuracyinyourtaxaccount.

ONliNE TaX payMENTSYoumaymakeyourextensionpaymentbyusinganecheckorcreditcardatwww.colorado.gov/paytax. Pleasenotethereisanadditionalfeeifyoudecidetousethiselectronicpaymentmethod.ThisfeeispaidtoathirdpartywhoprovidestheseservicesforColorado.gov.Taxpaymentsremittedviaecheck,adirectdebitfromyourcheckingaccount,willbesubjecttoa$1.00administrativeprocessingfee.Theprocessingfeeforcreditcardtransactionsis2.25%ofthetaxpaymentmade,plusanadditional$0.75pertransaction.

Ifpayingbycheck,submitForm158Cwithpaymentto:

ColoradoDepartmentofRevenue, Denver,Colorado80261-0008.

DO NOT SUbMiT FOrM 158C wiThOUT a payMENT.

EXTENSiON OF TiME FOr FiliNg a COlOraDO C COrpOraTiON iNCOME TaX rETUrN

DETACH FORM ON THIS LINE

rETUrN ONly ThE lOwEr pOrTiON OF ThiS pagE wiTh yOUr payMENT

(0029) Form158C(09/25/09)COlOraDO DEparTMENT OF rEVENUE

www.TaxColorado.com

2009 payment Voucher for Extension of Time for Filing a Colorado C Corporation income Tax return

Vendor iD

70

ReturnthisvoucherwithcheckormoneyorderpayabletotheColoradoDepartmentofRevenue,Denver,Colorado80261-0008.WriteyourColoradoAccountNumberand“2009Form158C”onyourcheckormoneyorder.Donotsendcash.Enclose,butdonotstapleorattach,yourpaymentwiththisvoucher.Fileonlyifyouaremakingapayment.CorporationName ColoradoAccountNumber

Address FederalEmployerIdentificationNumber

City State ZIP

iF NO payMENT iS DUE, DO NOT FilE ThiS FOrM. yOU MUST rOUND TO ThE NEarEST DOllarTheStatemayconvert your check toaone timeelectronicbanking transaction.Yourbankaccountmaybedebitedasearlyas the sameday receivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

aMOUNT OF payMENT

$.DO NOT wriTE iN SpaCE bElOw (08)

For the calendar year 2009 or the fiscal year: Start Date:__________________,2009,End Date: _________________ .

Page3

DETACH FORM ON THIS LINE

rETUrN ONly ThE lOwEr pOrTiON OF ThiS pagE wiTh yOUr payMENT

(0021) Form0900C(09/25/09) COlOraDO DEparTMENT OF rEVENUE

www.TaxColorado.com

2009 C Corporationincome Tax payment Voucher

Vendor iD

70

For the calendar year 2009 or the fiscal year: Start Date:__________________,2009,End Date: ________________ .ReturnthisvoucherwithcheckormoneyorderpayabletotheColoradoDepartmentofRevenue,Denver,Colorado80261-0008.WriteyourColoradoAccountNumberand“2009Form112”onyourcheckormoneyorder.Donotsendcash.Enclose,butdonotstapleorattach,yourpaymentwiththisvoucher.Fileonlyifyouaremakingapayment.CorporationName ColoradoAccountNumber

Address FederalEmployerIdentificationNumber

City State ZIP

iF NO payMENT iS DUE, DO NOT FilE ThiS FOrM. yOU MUST rOUND TO ThE NEarEST DOllarTheStatemayconvert your check toaone timeelectronicbanking transaction.Yourbankaccountmaybedebitedasearlyas the sameday receivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

aMOUNT OF payMENT

$.DO NOT wriTE iN SpaCE bElOw (08)

rETUrN ONly ThE lOwEr pOrTiON OF ThiS pagE wiTh yOUr payMENT

(0029) Form158C(09/25/09)COlOraDO DEparTMENT OF rEVENUE

www.TaxColorado.com

2009 payment Voucher for Extension of Time for Filing a Colorado C Corporation income Tax return

Vendor iD

70

ReturnthisvoucherwithcheckormoneyorderpayabletotheColoradoDepartmentofRevenue,Denver,Colorado80261-0008.WriteyourColoradoAccountNumberand“2009Form158C”onyourcheckormoneyorder.Donotsendcash.Enclose,butdonotstapleorattach,yourpaymentwiththisvoucher.Fileonlyifyouaremakingapayment.CorporationName ColoradoAccountNumber

Address FederalEmployerIdentificationNumber

City State ZIP

iF NO payMENT iS DUE, DO NOT FilE ThiS FOrM. yOU MUST rOUND TO ThE NEarEST DOllarTheStatemayconvert your check toaone timeelectronicbanking transaction.Yourbankaccountmaybedebitedasearlyas the sameday receivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

aMOUNT OF payMENT

$.DO NOT wriTE iN SpaCE bElOw (08)

form0900C(09/25/09)COlOraDO DEparTMENT OF rEVENUEDENvERCO80261-0008www.TaxColorado.com

See instructions below

print the completed form and submit with your payment.

2009 C COrpOraTiON iNCOME TaX payMENT VOUChEr

UseForm0900Cbelowtosubmityourpaymentifyou:• fileusinganyelectronicfilingmethod,• fileareturncontainingabarcode,• orare,forsomeotherreason,sendingyour

paymentseparatefromyourreturn.• Besuretoroundyourpaymenttothenearestdollar.

Youmustenter00afterthedecimalpoint.Theamountonthecheckandtheamountenteredonthepaymentvouchermustbethesame.Thiswillhelpmaintain accuracyinyourtaxaccount.

DO NOTsendanothercopyofyourtaxreturnwithyour paymentbecausetheForm0900Ccontainsalltheinformationrequiredtomatchyourpaymentwithyourreturn.

Rather than mailing a check, you can nowpayusinganelectroniccheckorcreditcardat www.colorado.gov/paytax

Thisonlineserviceincludesanadministrativefee thatallowsColorado.govtodeliverthisandotherimportantservices.ThisfeeispaidtoathirdpartythatprovidestheseservicesforColorado.govatlittleornocosttothetaxpayersofColorado.Forcreditcardtransactions,theadministrativeprocessingfeeistheamountduemultipliedby2.25%plusanadditional$0.75.However,ifyouchoosetopaywithcashintheformofanecheck,theadministrativeprocessingfeeisdiscountedto$1.00pertransaction.

Page4

Filing requirements:Every corporation doing business in Colorado or derivingincomefromColoradosourcesmustfileacorporationincometaxreturnwithColorado.AnycorporationthatisexemptfromfederalincometaxisexemptfromColoradoincometaxandfromfilingaColorado income tax returnexcept that itshallnotbesoexemptif itmustfileafederalreturnofunrelatedbusinessincome.Anyinsurancecompanysubjecttothetaximposedongrosspremiumsby§10-3-209,C.R.S.isexemptfromtheColoradoincometaxandfromfilingColoradoincometaxreturns.

Time and place for Filing:Returnsaredueonthe15thdayofthefourthmonthfollowingthecloseofthetaxableyear.Acorporationisgrantedanautomaticsixmonthextensionoftimeforfiling.SeeForm158Cformoreinformationonanextension.

Mailyourreturnto:ColoradoDepartmentofRevenue,Denver,Colorado80261-0006.

Declaration of Estimated Tax:EveryCcorporationsubjecttotheColoradoincometaxmustfileadeclarationofestimatedincometax,Form112EP,ifitstaxliabilityisexpectedtoexceed$5,000plusestimatedcredits.

additional information available:TheColoradoTax Information Index,whichprovideseasyaccesstoforms,FYIs,statutes,regulationsandotherinformationorganizedbysubject,isavailableatwww.TaxColorado.comoryoucancallforinformationat(303)238-SERv(7378).

accounting period and Method:Thecorporation’saccountingperiodandmethodforColoradoincometaxpurposesmustbethesameasforfederalincometaxpurposes.

Colorado account Number:TheColoradoaccountnumberisa7-digitnumberthatmustbeincludedinadditiontothefederalemployeridentificationnumber.TheColoradoincometaxaccountnumberisthesameasthecorporation’ssalestaxorwagewithholdingaccountnumber.

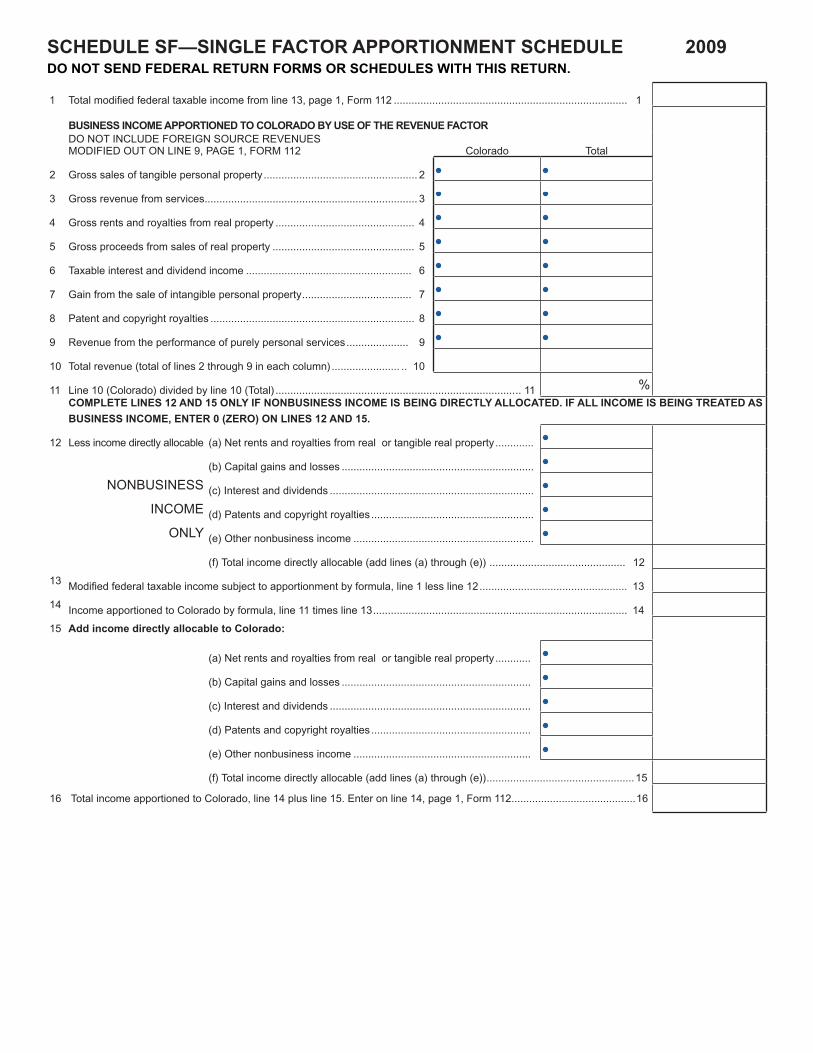

Section a: apportionment Of income:Acorporationdoingbusiness inmore thanone statemustapportionitstaxableincometoanystatesinwhichthecorporationisdoingbusiness.Thisensurestaxispaidtothestateinwhichtheincomeisearnedandtaxable. 59.Income is generally apportioned based upon a single salesfactor,amethodnewtoColoradoin2009:Corporationsmay not apportionincomeusingeitherthetwoorthreefactormethodsallowedinprioryears.

Not apportioning income —ACcorporationdoingbusinessonlyinColoradowillcomputeitstaxon100percentoftheColoradotaxableincome.

Single Sales Factor —Allbusinessincomemustbeapportionedusingasinglefactor:sales.Nonbusinessincomemayeitherbedirectlyallocatedtotheappropriatestateortreatedasbusiness

income,subjecttothesinglesalesfactorapportionment.CompleteandattachScheduleSFtoyourreturnifyouareapportioningincomeusingthesinglesalesfactorapportionmentmethod.

gross receipts Tax —ACcorporationthatperformsnoColoradoactivitiesotherthanmakingsales,doesnotownorrentrealestateinColorado,andgeneratesannualgrosssalesinColoradoof$100,000orlessmayelecttopayataxofone-halfpercentoftheannualgrossreceiptsderivedfromthesalesinColoradoinlieuofpayingthenormalincometax.Enterannualgrossreceiptsonline16,andthe.5%taxonline17.Enter“grossreceiptstax”onthedottedlineonlines16and17. 58.

Other apportionment Methods —If the apportionmentprovisionsdonotfairlymeasuretheColoradosourceincome,thecorporationmayrequest,ortheDepartmentmayrequire,analternativemethodtobeused.

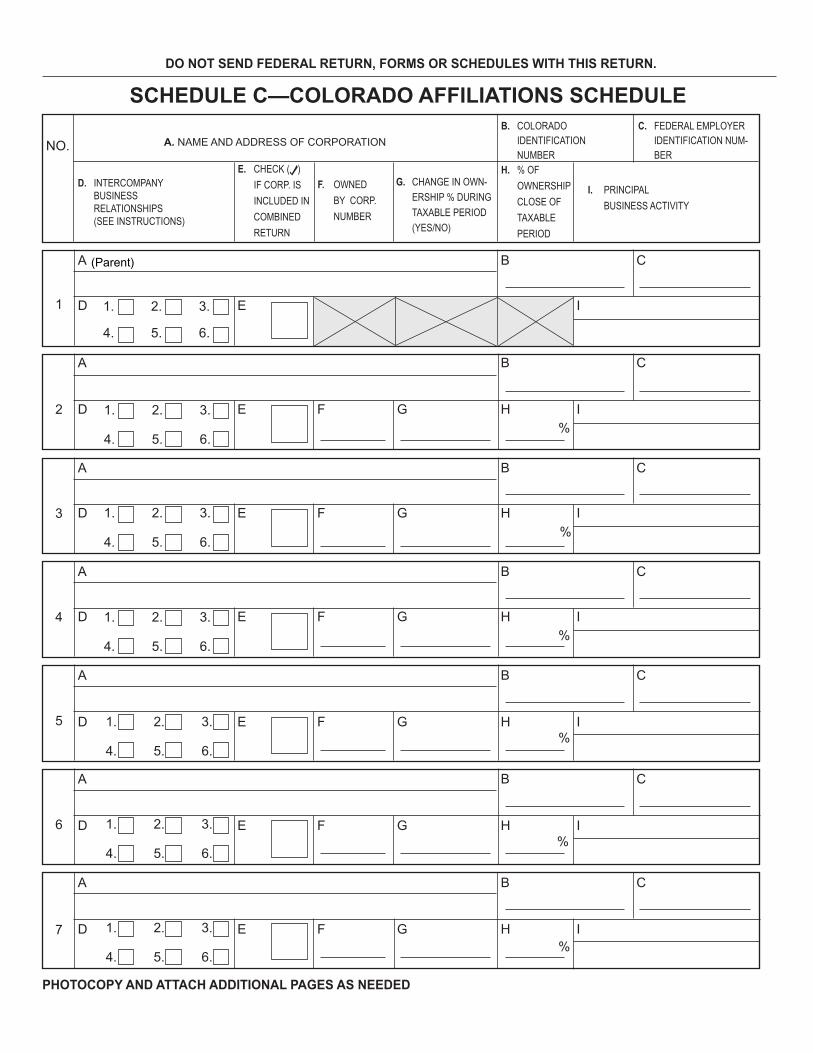

Section b: Separate, Consolidated Or Combined Filing:

TherearefourpossiblefilingalternativesforCcorporations.Thealternativesareseparate,consolidated,combined,andcombined/consolidatedfiling. 60.

Separate Filing —Asinglecorporation,evenifitisamemberofanaffiliatedgroup,mayelecttofileaseparatereturn.Asinglecorporationmaynotfileaseparatereturnifitelectstobepartofaconsolidatedreturn,orisrequiredtobeincludedinacombinedfiling.

Consolidated Filing —Members of an affiliated group ofcorporations,asdefinedin§1504oftheInternalRevenueCode,may elect to file a consolidatedColorado income tax return.However, only members of the consolidated group that aredoingbusiness inColorado canbe included in theColoradoconsolidatedfiling.

AnelectiontofileaconsolidatedreturnisbindingforfouryearsandrequirestheconsentofthemembersoftheaffiliatedgroupthatweredoingbusinessinColorado.Themakingofaconsolidatedreturnshallbeconsideredsuchconsent.

Example:PCompany,aparentcorporationfilingafederalconsolidatedreturn,hasfoursubsidiaries,A,B,C,andD.TheparentandthefirstthreesubsidiariesalldobusinessinColorado.DdoesbusinessonlyinNebraska.PCompanyanditssubsidiaries,A,BandC,mayelecttofileaconsolidatedColorado income tax return. D may not be part of theconsolidatedreturn.

Combined Filing—Anaffiliatedgroupofcorporations,asdefinedin§39-22-303oftheColoradoRevisedStatutesthatmeetsthreeormorepartsofthesix-partintercompanybusinessrelationshiptestforthecurrentyearandtheprecedingtwoyears,mustfileacombinedreport.Combined/Consolidated Filing – If anaffiliatedgroupfilingacombinedreporthasamemberwhofilesafederalconsolidatedreturnwithanothercorporation,and thatothercorporation isdoingbusinessinColoradobutisnoteligibletobeincludedinthecombinedreport,theaffiliatedmemberscanelecttofileacombined/consolidatedfiling.

Example:PCompany,aparentcorporationfilingafederalconsolidatedreturn,hasfoursubsidiaries,A,B,C,andD.P

iNSTrUCTiONS FOr 2009 COlOraDOC COrpOraTiON iNCOME TaX rETUrN, FOrM 112

(S COrpOraTiONS FilE FOrM 106)

Page5

andthefirstthreesubsidiariesalldobusinessinColorado.AwasacquiredonJanuary1,2009andDdoesbusinessonlyinNebraska.PCompanymeetsthesix-parttestforfilingacombinedreportwithB,C,andD.Thus,P,B,C,andDmustfileacombinedreport.A,however,doesnotqualifyforthecombinedreportbecauseithasnotbeenownedfortherequisitetwoyears.PCompanymayelecttofileaconsolidatedreturnwithA.Thus,Pwillbefilingacombined/consolidatedreturn:combinedwithB,C,andD,andconsolidatedwithA.

Federal Taxable income:liNE 1: Enterthefederaltaxableincome(orloss)fromfederal

Form1120.liNE 2: Enterthefederaltaxableincome,totheextentincluded

inline1,ofcorporationsthatarenotincludedinthisconsolidatedand/orcombinedreturn.

liNE 3: Reflectsthefederaltaxableincomeofthefederalpro-formareturnforthecompaniesincludedintheColoradoreturn.

additions: liNE 4: Enter any federal net operating loss deduction

claimed in the computation of the federal taxableincome. 19.

liNE 5: EnteranyColoradoincometaxclaimedasadeductioninthecomputationofthefederaltaxableincome.

liNE 6: Enterallotheradditions: 58. • All interest income (less bond premium

amortization) of the corporation from state ormunicipal obligations that is not included infederal taxable income. Do not include interestincome from any bond or other obligation ofthe State of Colorado or a political subdivisionthereof issued on or after May 1, 1980. Theinteresttobeenteredshallbenetofanyexpenserequired to be allocated thereto by the InternalRevenueCodeforfederalincometaxpurposes.

52. • Any income,warprofits,orexcessprofits taxes

paidoraccruedtoanyforeigncountryortoanypossessionoftheUnitedStatesthatwereclaimedasadeductiononthefederalreturn. 58.

• Anycharitablecontributiondeductionclaimedin2009forthedonationofaconservationeasementthatqualifiedforthegrossconservationeasementcredit.

39.

Subtractions:liNE 8: Enter, to the extent included in federal taxable

income, any United States government bondinterest and any interest or dividend incomeon obligations or securities of any authority, commission, or instrumentality of the UnitedStates to the extent such interest or dividendincome is exempt from state taxation by federallaw. 20.

liNE 9: Enter, to the extent included in federal taxableincome, that part of foreign income that qualifies as excludable foreign source income.Excludable foreign source income means taxableincomefromsourceswithouttheUnitedStatesasusedinsection862oftheInternalRevenueCodeasdeterminedbelow:

• Ifforfederalincometaxpurposesthecorporationhaselectedtoclaimforeigntaxespaidoraccruedasadeduction,excludableforeignsourceincomeshallbeanamountequaltosuchdeduction.

• Ifforfederalincometaxpurposesthecorporationhaselectedtoclaimforeigntaxpaidoraccruedas a credit, excludable foreign source incomeshall be an amount equal to foreign sourceincome(excludingsection78dividendgrossup)multipliedbyafraction,thenumeratorofwhichisthefederalforeigntaxcredit,andthedenominatorofwhich is theforeignsource income(includingsection78dividendgrossup)timestheeffectivefederal corporation income tax rate (federalcorporateincometaxdividedbyfederalcorporate taxableincome).Excludableforeignsourceincomemaynotexceedtotalforeignsourceincomeexcludingsection78dividendgrossup.Foreignsourceincomefromaforeigncorporationwithinanaffiliatedgroupof corporations shall be determined without regard to section 882(a)(2) of the Internal RevenueCode.

ExcludableforeignsourceincomeshallalsobeomittedindeterminingtheColoradosalesfactor(ScheduleSF).

58.liNE 10: Enter,totheextentincludedinfederaltaxableincome,

theamountofcapitalgainincomeearnedfrom: • Thesaleofrealortangiblepersonalpropertylocated

inColorado,or • Thesaleofstockoranownershipinterest ina

Coloradocompanythathas50percentormoreofitspropertyandpayrollwithinColorado,

thatwasacquiredonorafterMay9,1994andheldcontinuouslyforat leastfiveyearspriortothedateofthetransactionfromwhichthecapitalgainsarise.You must attach Form DR1316 to the return toexplainhowtheseassetsqualifyforthesubtraction.

15.liNE 11: Enterallothersubtractions. 58. • To the extent included in federal taxable

income,anyrefundofColoradoincometax. • Any amount included in federal taxable

incomeby reasonof thegross-upprovisionsofsection78oftheInternalRevenueCode.

• TheamountofanysalaryorwageexpensenotallowedasadeductiononthefederalincometaxreturnduetotheprovisionsoftheIndianemploymentcredit,workopportunitycredit,empowermentzoneemploymentcredit,orphandrugcredit,creditforincreasingresearchactivities,employeeretentioncredit,welfare-to-workcreditorminerescueteamtrainingcredit.

Taxable income:liNE 13: Enterthenetamountofline7minusline12.Thisisthe

modifiedfederaltaxableincomethatwillbetheColoradotaxable income to be entered on line 14 for thosecorporationsnotpermittedtoapportionincomeawayfrom Colorado. For those corporations that do apportionincome,entertheamountfromline13online1ofScheduleSF.

liNE 15: Enter the Colorado net operating loss deduction. The Colorado net operating loss

Page6

deduction is computed in the same manneras is the federal net operating loss deductionexcept that in the case of a corporation apportioning income, it is that part of the federalnetoperatingloss,asmodified,thatisfromColorado sources.Colorado operating lossesmaybecarriedforward20yearsfortaxyearsbeginningonorafterAugust6,1997.Theymaynotbecarriedback.Federallimitationsoncarryoverlossesbetweenpredecessor and successor corporations apply forColoradoincometaxpurposes. 19.

TaxliNE 17: TheColoradotaxrateiscurrently4.63%.

CreditsliNES 18 – 26:EnterthecreditsfromForm112CR.liNE 29: If the corporation is required to recapture

federal investment credit with respect to Colorado assets, a recapture of the “old” Colorado investment credit may be required.Include any investment credit recapture, historic property preservation credit recapture, lowincomehousingcreditrecaptureoranyothercreditrecaptureonthisline.Attachascheduletothereturndetailingthecomputationoftherecaptureamount.

liNE 31: Enterallprepaymentcredits. • Anyestimatedtaxpaymentsmadefor2009, • Thatpartofthe2008overpayment,ifany,thatwas

appliedto2009, • Anyamountpaidwitha2009extensionoftimefor

filingvoucher, • AnyColoradotaxwithheldonthesaleofColorado

realestateduringthetaxyearonForm1079.

penalties and interestliNE 32: Thedelinquentfilingorpaymentpenaltyis5%ofthe

balanceoftaxdueforthefirstmonthorfractionthereofplusanadditional1/2%foreachadditionalmonthorfractionthereof,notexceeding12%intheaggregate.Theminimumpenaltyis$5.00.

liNE 33: Interestaccruesonanybalanceoftaxdueduring2010atarateof3%perannumexceptthatwithrespecttoanyassessmentnotpaidwithin30daysofdateofbilling,interestwillbedueatan6%annualrate.

liNE 34: If the corporation is assessing itself an estimatedtaxpenaltyattachacopyofForm205tothereturn.

Includepenaltyandinterestamountsfromlines32-34intheamountowedonline35.

refundliNE 37: Entertheamountofanyoverpaymentyouwishtohave

creditedtothecorporation’s2009estimatedtaxes.liNE 38: Enter theamountofanyoverpaymentyouwish to

haverefunded.

TheDepartmentcandeposityourrefunddirectlyintoyouraccountataU.S.bankorotherfinan-cialinstitution(suchasamutualfund,brokeragefirm,orcreditunion)intheUnitedStates.

Direct Deposit?•Fasterrefund•Saferrefund—Nochecktogetlost.•Convenient—Notriptothebank.

your return aND use Direct Deposit. get your refund in two weeks.

how do i use Direct Deposit?Completetheroutingnumber,typeofaccountandaccountnum-berboxesonline38.The routing numbermust be nine digits.The first two digitsmustbe01through12or21through32.Onthesamplecheck,theroutingnumberis123456780.Yourcheckmaystatethatitispayablethroughabankdifferentfromthefinancialinstitutionatwhichyouhaveyourcheckingaccount.Ifso,donotusetherouting number on that check. Instead, contact your financial institutionforthecorrectroutingnumbertoenteronthisline.Theaccount numbercanbeupto17characters(bothnum-bersandletters).Includehyphensbutomitspacesandspecialsymbols.Enterthenumberfromlefttorightandleaveanyun-usedboxesblank.Onthesamplecheck,theaccountnumberis12312345.Donotincludethechecknumber.

Youshouldcontactyourfinancial institutiontomakesureyourdepositwill beacceptedand toobtain thecorrect routingandaccountnumbers.Thisisespecially importantifyouwantyourrefunddepositedtoasavingsaccountatacreditunion.TheColo-radoDepartmentofRevenueisnotresponsibleforalostrefundifyouenterthewrongaccountinformation.Anyrefundclaimthat,foranyreason,cannotbedepositedintotheaccountspecifiedwillbeissuedandmailedincheckforminstead.

Sections C–g: Corporate informationEnter the requested corporate information on lines C throughG.

SignaturesThelawrequiresthereturntobesignedunderthepenaltiesofperjurybythepresident,vice-president,treasurer,assistanttreasurer,chiefaccountingofficer,orotherofficerdulyauthorizedtoact.Incaseswherereceivers,trusteesinbankruptcy,orassigneesareoperatingthepropertyorbusinessofcorporations,suchreceivers,trustees,orassigneesshallmakereturnsforsuchcorporationsinthesamemannerandformascorporationsarerequiredtomakereturns.

Changes in Federal incomeAny adjustment made by federal amended returns must bereportedandtheColoradoincometaxadjustedaccordinglyonForm112X,theamendedcorporationincometaxreturn.Likewise,anyadjustmentsmadebytheInternalRevenueServicemustbereportedtoColoradoonForm112X.Ifthecorporationoperatesintwoormorestates,tosimplifytheamendedreturnfilingrequirement,thecorporationcanmail therevenueagent’sreportseparately(mustnotbeattachedtothereturn)totheColoradoDepartmentofRevenue,Denver,Colorado80261-0005.IncludetheColoradoaccountnumberonthereport.Thestatuteoflimitationswillnotapplyifthetaxpayerfailstodiscloseanyadjustmentsmadeonfederalreturnsandfailstosubmitcopiesofthefederalagent’sreports.

Page7

DEPARTMENTALUSEONLY

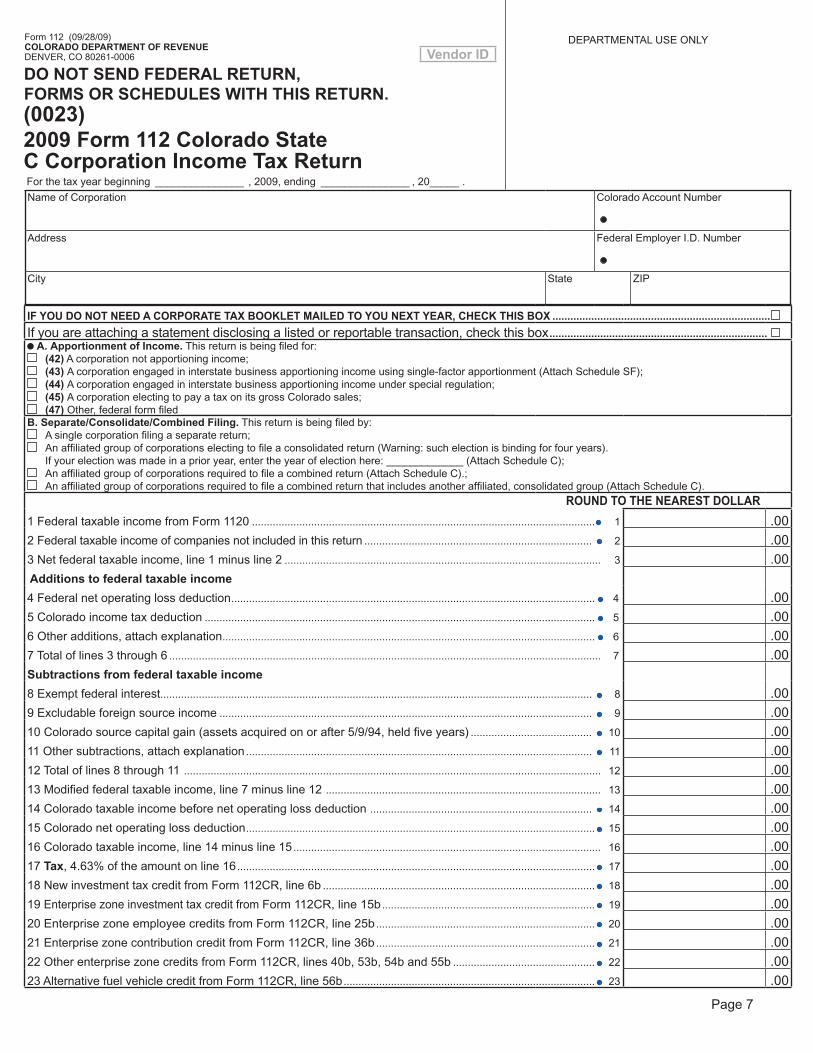

(0023)2009 Form 112 Colorado State C Corporation income Tax returnForthetaxyearbeginning _______________ ,2009,ending _______________ ,20_____.

DO NOT SEND FEDEral rETUrN, FOrMS Or SChEDUlES wiTh ThiS rETUrN.

iF yOU DO NOT NEED a COrpOraTE TaX bOOKlET MailED TO yOU NEXT yEar, ChECK ThiS bOX .........................................................................

Ifyouareattachingastatementdisclosingalistedorreportabletransaction,checkthisbox ......................................................................... a. apportionment of income.Thisreturnisbeingfiledfor: (42)Acorporationnotapportioningincome; (43) Acorporationengagedininterstatebusinessapportioningincomeusingsingle-factorapportionment(AttachScheduleSF); (44) Acorporationengagedininterstatebusinessapportioningincomeunderspecialregulation; (45) AcorporationelectingtopayataxonitsgrossColoradosales; (47) Other,federalformfiled_____________________________________________________

b. Separate/Consolidate/Combined Filing.Thisreturnisbeingfiledby: Asinglecorporationfilingaseparatereturn; Anaffiliatedgroupofcorporationselectingtofileaconsolidatedreturn(Warning:suchelectionisbindingforfouryears). Ifyourelectionwasmadeinaprioryear,entertheyearofelectionhere:_____________(AttachScheduleC);

Anaffiliatedgroupofcorporationsrequiredtofileacombinedreturn(AttachScheduleC).; Anaffiliatedgroupofcorporationsrequiredtofileacombinedreturnthatincludesanotheraffiliated,consolidatedgroup(AttachScheduleC).

rOUND TO ThE NEarEST DOllar

1 FederaltaxableincomefromForm1120 .................................................................................................................... 1 .00

2Federaltaxableincomeofcompaniesnotincludedinthisreturn ............................................................................. 2 .00

3 Netfederaltaxableincome,line1minusline2 ........................................................................................................... 3 .00

additions to federal taxable income .004Federalnetoperatinglossdeduction ........................................................................................................................... 4

5Coloradoincometaxdeduction .................................................................................................................................... 5 .00

6Otheradditions,attachexplanation .............................................................................................................................. 6 .00

7Totaloflines3through6 .................................................................................................................................................. 7 .00

Subtractions from federal taxable income

.008 Exemptfederalinterest.................................................................................................................................................. 8

9Excludableforeignsourceincome .............................................................................................................................. 9 .00

10Coloradosourcecapitalgain(assetsacquiredonorafter5/9/94,heldfiveyears) ......................................... 10 .00

11 Othersubtractions,attachexplanation ..................................................................................................................... 11 .00

12Totaloflines8through11 .............................................................................................................................................12 .00

13 Modifiedfederaltaxableincome,line7minusline12 ............................................................................................. 13 .00

14Coloradotaxableincomebeforenetoperatinglossdeduction ........................................................................... 14 .00

15Coloradonetoperatinglossdeduction ...................................................................................................................... 15 .00

16Coloradotaxableincome,line14minusline15 ........................................................................................................ 16 .00

17Tax,4.63%oftheamountonline16 ......................................................................................................................... 17 .00

18NewinvestmenttaxcreditfromForm112CR,line6b ............................................................................................ 18 .00

19EnterprisezoneinvestmenttaxcreditfromForm112CR,line15b ........................................................................ 19 .00

20EnterprisezoneemployeecreditsfromForm112CR,line25b .......................................................................... 20 .00

21EnterprisezonecontributioncreditfromForm112CR,line36b .......................................................................... 21 .00

22OtherenterprisezonecreditsfromForm112CR,lines40b,53b,54band55b ................................................ 22 .00

23AlternativefuelvehiclecreditfromForm112CR,line56b ..................................................................................... 23 .00

NameofCorporation ColoradoAccountNumber

Address FederalEmployerI.D.Number

City State ZIP

Form112(09/28/09)COlOraDO DEparTMENT OF rEVENUEDENvER,CO80261-0006 Vendor iD

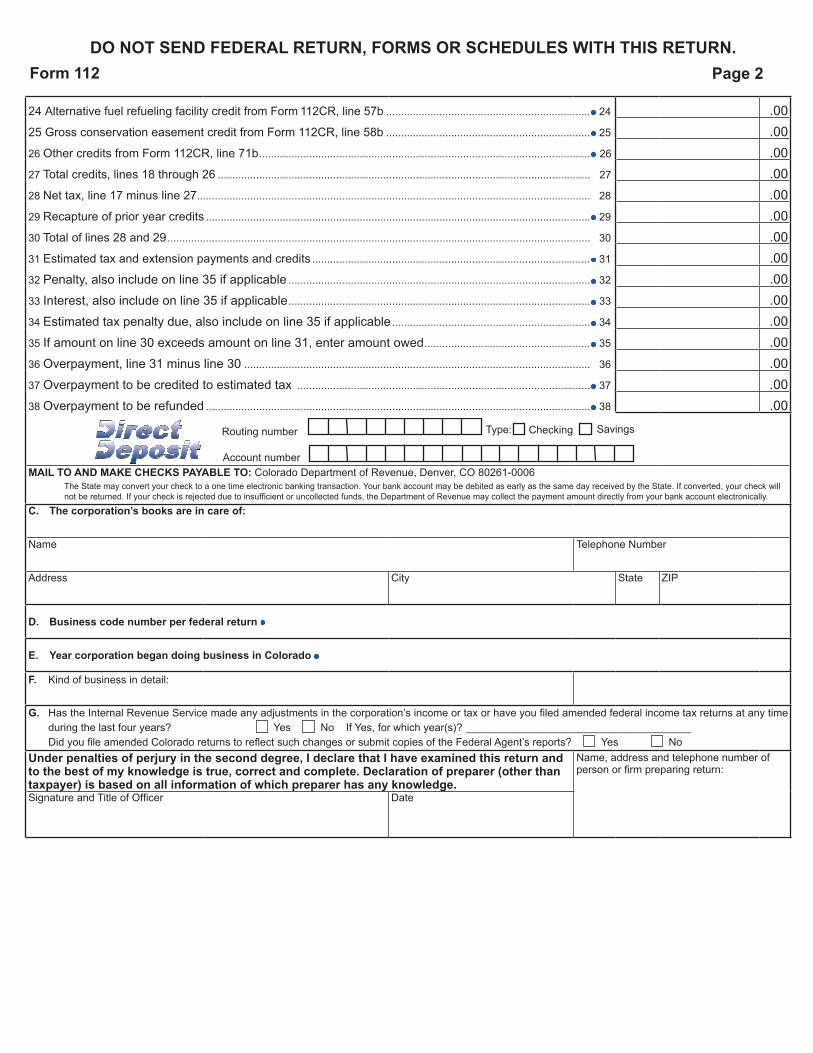

DO NOT SEND FEDEral rETUrN, FOrMS Or SChEDUlES wiTh ThiS rETUrN.

Form 112 page 2

24AlternativefuelrefuelingfacilitycreditfromForm 112CR,line57b ..................................................................... 24 .00

25GrossconservationeasementcreditfromForm112CR,line58b ..................................................................... 25 .00

26OthercreditsfromForm112CR,line71b ................................................................................................................ 26 .00

27Totalcredits,lines18through26 ..............................................................................................................................27 .00

28Nettax,line17minusline27 .....................................................................................................................................28 .00

29Recaptureofprioryearcredits .................................................................................................................................. 29 .00

30Totaloflines28and29 ............................................................................................................................................... 30 .00

31 Estimatedtaxandextensionpaymentsandcredits .............................................................................................. 31 .00

32 Penalty,alsoincludeonline35ifapplicable ...................................................................................................... 32 .00

33 Interest,alsoincludeonline35ifapplicable ...................................................................................................... 33 .00

34Estimatedtaxpenaltydue,alsoincludeonline35ifapplicable ................................................................... 34 .00

35Ifamountonline30exceedsamountonline31,enteramountowed ........................................................ 35 .00

36Overpayment,line31minusline30 .....................................................................................................................36 .00

37Overpaymenttobecreditedtoestimatedtax ................................................................................................... 37 .00

38Overpaymenttoberefunded .................................................................................................................................. 38 .00

Type: Checking SavingsRoutingnumber

AccountnumberMail TO aND MaKE ChECKS payablE TO: ColoradoDepartmentofRevenue,Denver,CO80261-0006

TheStatemayconvertyourchecktoaonetimeelectronicbankingtransaction.YourbankaccountmaybedebitedasearlyasthesamedayreceivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

C. The corporation’s books are in care of:

Name TelephoneNumber

Address City State ZIP

D. business code number per federal return

E. year corporation began doing business in Colorado

F. Kindofbusinessindetail:

g. HastheInternalRevenueServicemadeanyadjustmentsinthecorporation’sincomeortaxorhaveyoufiledamendedfederalincometaxreturnsatanytimeduringthelastfouryears? Yes NoIfYes,forwhichyear(s)? ______________________________________

DidyoufileamendedColoradoreturnstoreflectsuchchangesorsubmitcopiesoftheFederalAgent’sreports? Yes No

Under penalties of perjury in the second degree, i declare that i have examined this return and to the best of my knowledge is true, correct and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Name,addressandtelephonenumberofpersonorfirmpreparingreturn:

SignatureandTitleofOfficer Date

SChEDUlE SF—SiNglE FaCTOr appOrTiONMENT SChEDUlE 2009DO NOT SEND FEDEral rETUrN FOrMS Or SChEDUlES wiTh ThiS rETUrN.

1 Totalmodifiedfederaltaxableincomefromline13,page1,Form112 ............................................................................... 1

bUSiNESS iNCOME appOrTiONED TO COlOraDO by USE OF ThE rEVENUE FaCTOrDONOTINCLUDEFOREIGNSOURCEREvENUES MODIFIEDOUTONLINE9,PAGE1,FORM112 Colorado Total

2 Grosssalesoftangiblepersonalproperty ....................................................2

3 Grossrevenuefromservices........................................................................ 3

4 Grossrentsandroyaltiesfromrealproperty ............................................... 4

5 Grossproceedsfromsalesofrealproperty ................................................ 5

6 Taxableinterestanddividendincome ........................................................ 6

7 Gainfromthesaleofintangiblepersonalproperty ..................................... 7

8 Patentandcopyrightroyalties ..................................................................... 8

9 Revenuefromtheperformanceofpurelypersonalservices ..................... 9

10 Totalrevenue(totaloflines2through9ineachcolumn) ....................... ..10

11 Line10(Colorado)dividedbyline10(Total) ................................................................................... 11 %COMplETE liNES 12 aND 15 ONly iF NONbUSiNESS iNCOME iS bEiNg DirECTly allOCaTED. iF all iNCOME iS bEiNg TrEaTED aS

bUSiNESS iNCOME, ENTEr 0 (ZErO) ON liNES 12 aND 15.

12 Lessincomedirectlyallocable (a)Netrentsandroyaltiesfromrealortangiblerealproperty .............

NONBUSINESS

INCOME

ONLY

(b)Capitalgainsandlosses .................................................................

(c)Interestanddividends .....................................................................

(d)Patentsandcopyrightroyalties .......................................................

(e)Othernonbusinessincome .............................................................

(f)Totalincomedirectlyallocable(addlines(a)through(e)) .............................................. 12

13 Modifiedfederaltaxableincomesubjecttoapportionmentbyformula,line1lessline12 .................................................. 13

14 IncomeapportionedtoColoradobyformula,line11timesline13 ...................................................................................... 14

15 add income directly allocable to Colorado:

(a)Netrentsandroyaltiesfromrealortangiblerealproperty ............

(b)Capitalgainsandlosses ................................................................

(c)Interestanddividends ....................................................................

(d)Patentsandcopyrightroyalties ......................................................

(e)Othernonbusinessincome ............................................................

(f)Totalincomedirectlyallocable(addlines(a)through(e)) ..................................................15

16 TotalincomeapportionedtoColorado,line14plusline15.Enteronline14,page1,Form112 ..........................................16

DO NOT SEND FEDEral rETUrN, FOrMS Or SChEDUlES wiTh ThiS rETUrN.

D E I

a. NAMEANDADDRESSOFCORPORATION

C. FEDERAL EMPLOYER IDENTIFICATION NUM-BER

NO.

B. COLORADO IDENTIFICATION NUMBER

G. ChANgE IN OwN-

ERshIP % DURINg

TAxABLE PERIOD

(YEs/NO)

E. ChECk ( )

IF CORP. Is

INCLUDED IN

COMBINED

RETURN

H. % OF

OwNERshIP

CLOsE OF

TAxABLE

PERIOD

I. PRINCIPAL

BUsINEss ACTIVITY

1

D E F G H I

A B C

2%

D E F G H I

A B C

3%

D E F G H I

A B C

4%

D E F G H I

A B C

5%

D E F G H I

A B C

D E F G H I

A B C

6

7

%

%

(Parent)

phOTOCOpy aND aTTaCh aDDiTiONal pagES aS NEEDED

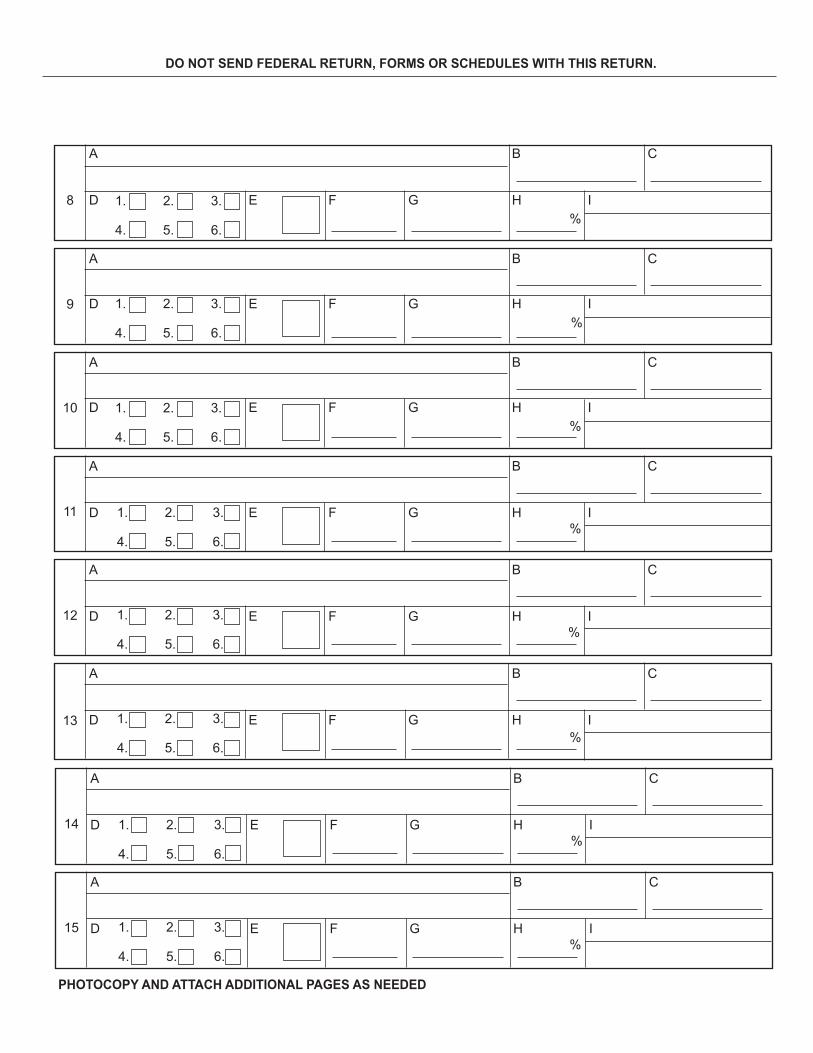

SChEDUlE C—COlOraDO aFFiliaTiONS SChEDUlE

D. INTERCOMPANY BUsINEss RELATIONshIPs (sEE INsTRUCTIONs)

F. OwNED

BY CORP.

NUMBER

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

A B C

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

DO NOT SEND FEDEral rETUrN, FOrMS Or SChEDUlES wiTh ThiS rETUrN.

D E F G H I

A B C

8%

D E F G H I

A B C

9%

D E F G H I

A B C

10%

D E F G H I

A B C

11%

D E F G H I

A B C

D E F G H I

A B C

12

13

%

%

phOTOCOpy aND aTTaCh aDDiTiONal pagES aS NEEDED

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

D E F G H I

A B C

14%

D E F G H I

A B C

15%

1. 2. 3.

4. 5. 6.

1. 2. 3.

4. 5. 6.

ScheduleCmustbecompletedifthecorporationforwhichthereturnisfiledowneda)morethan50percentofthestockofanothercorporationor,b)morethan50percentofthestockofthecorporationforwhichthereturnisfiledwasownedbyanothercorporation.

Enterinformationforthecommonparentonline1.Lines2through15areforsubsidiarycorporations.Photocopyandattachadditionalsheetsifnecessary.

Columns a Through C:Enterthecorporation’sname,address,ColoradoIDnumberandfederalemployerIDnumber.

Column D:Taxpayerswhoareaffiliatedcorporations,asdescribedabove,andwhohavemorethan20percentoftheirpropertyandpayrolllocatedwithintheUnitedStatesmustcompleteColumnD.

Theblocks inColumnDarenumberedfromone(1) tosix(6)andcorrespondtothesixnumberedintercompanybusinessrelationshipsdescribedbelow.ForeachaffiliatelistedonScheduleC,markyes(Y)orno(N)intheblocksofColumnD, to indicatewhether the below describedintercompanybusinessrelationshipsdidordidnotexistduringthetaxyearandthetwoprecedingtaxyears.

intercompany business relationships:1.Is50percentormoreofthecorporation’sgross

receiptsfromsalesorleasestootheraffiliatesoris50percentormoreofthecorporation’scostofgoodssoldorleasedfromotheraffiliates?

2.Doesthecorporationreceive50percentormoreofthetotalannualvalueofeachoffiveormoreof the following services from other affiliates:advertisingandpublicrelations;accountingandbookkeeping;legal;personnel;sales;purchasing;

researchanddevelopment;insurance;employeebenefitprograms?Donotcountserviceswhichareprovidedat an “arm’s length charge.” (SeeU.S.TreasuryRegulation1.482(b)(3).)

3.Is20percentormoreofthecorporation’slong-termdebtowedtoorguaranteedbyotheraffiliates?Is20percentormoreofanyotheraffiliateslong-termdebtowedtoorguaranteedbythecorporation?

4.Does the corporation use patents, trademarks,servicemarks, logos, trade secrets, copyrightsor other proprietary materials owned by otheraffiliates? Does the corporation own patents,trademarks,servicemarks,logos,tradesecrets,copyrights,orotherproprietarymaterialsthatareusedbyotheraffiliates?

5.Are50percentormoreof themembersof thecorporation’sboardofdirectorsalsomembersoftheboardofdirectorsorcorporateofficersofotheraffiliates?

6.Are25percentormoreof thecorporation’s20(twenty) highest ranking officers alsomembersoftheboardofdirectorsorcorporateofficersofotheraffiliates?

Column E: ChecktheblockinColumnEifthecorporationisincludedinacombinedreport.Corporationsincludedinacombinedreportmusthaveansweredyes(Y)tothreeormoreofthe intercompany business relationships referred to inColumnD.

Columns F through i:Entercorporation’sownernumber,whetherornottherewasachangeinownership,ownershippercentageandprincipalbusinessactivity.

iNSTrUCTiONS FOr FOrM 112Cr

priority Of CreditsThelawprovidesthatthenewInvestmentTaxCredit(ITC)is limitedtothetax liabilityremainingafter theoldITC.Otherwise, the taxpayer may choose the sequence inwhichthecreditsareclaimed.Particularattentionshouldbepaid to thecarrybackandcarryover featuresof thevariouscredits.

The New investment Tax CreditAnewColoradoITCisallowedinanamountequalto1percentof the totalqualified investmentasdeterminedundersection46(c)oftheinternalrevenuecodeinqualifiedpropertyasdefinedinsection48oftheinternalrevenuecode as such sections existed prior to the RevenueReconciliationActof1990. 11.

ThenewITCisbasically10percentofwhatthefederalregularpercentageITCwouldbeifitwerestillineffect.

ThenewITCislimitedto$1,000reducedbytheamountoftheoldITCclaimedforthesametaxyear.

AnyexcessnewITCremainingmaybecarriedforwardforaperiodofthreeyears.Itmaynotbecarriedbacktoanearlieryear.

The newColorado ITC is allowed onlywith respect toassets locatedwithinColorado. Ifqualifyingproperty islocatedbothwithinandwithoutColoradoduringthetaxyear,thecreditshallbeapportionedbasedonthetimeofusageofsuchpropertyinColoradoduringthetaxyearascomparedwiththetotaltimeofusageofsuchpropertyeverywhereduringthetaxyearunlessthetaxpayercanjustifyamoreequitableapportionmentmethod.

All InternalRevenueCodesection46 (assuchsectionexistedpriorto1990)restrictionsonqualifiedinvestmentapplyforpurposesofthenewITC.Forexample,onlyafractionofthebasisorcostofassetsthathaveausefullifeoflessthansevenyearsqualifiesforthecredit,only$150,000ofusedpropertymayqualifyforthecredit,andanyamountsexpensedundersection179oftheInternalRevenueCodedonotqualify.

Page12

iNSTrUCTiONS FOr SChEDUlE C

Form112CR(11/17/09)

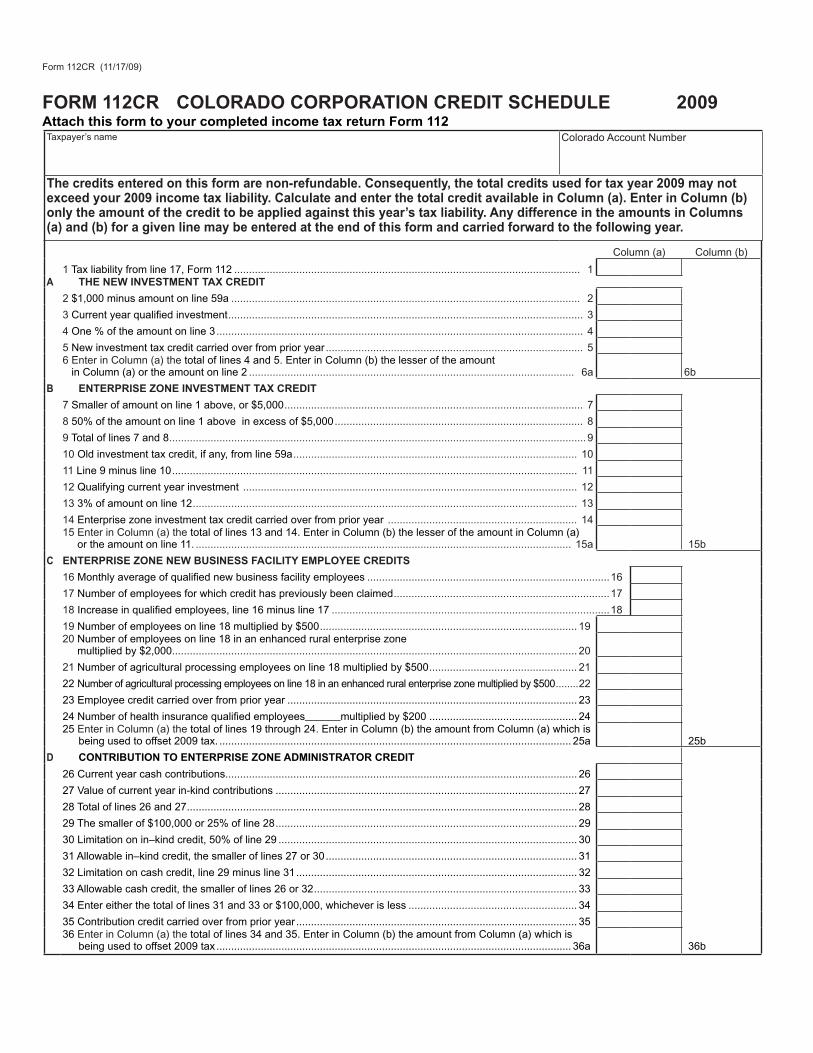

FOrM 112Cr COlOraDO COrpOraTiON CrEDiT SChEDUlE 2009attach this form to your completed income tax return Form 112

Column(a) Column(b)

1 Taxliabilityfromline17,Form112 ..................................................................................................................... 1a ThE NEw iNVESTMENT TaX CrEDiT

2$1,000minusamountonline59a ...................................................................................................................... 2

3 Currentyearqualifiedinvestment ........................................................................................................................ 3

4One%oftheamountonline3 ............................................................................................................................ 4

5Newinvestmenttaxcreditcarriedoverfromprioryear ....................................................................................... 56EnterinColumn(a)thetotaloflines4and5.EnterinColumn(b)thelesseroftheamount inColumn(a)ortheamountonline2 .............................................................................................................. 6a 6b

b ENTErpriSE ZONE iNVESTMENT TaX CrEDiT

7Smallerofamountonline1above,or$5,000 ..................................................................................................... 7

8 50%oftheamountonline1aboveinexcessof$5,000 .................................................................................... 8

9Totaloflines7and8 .............................................................................................................................................9

10Oldinvestmenttaxcredit,ifany,fromline59a ................................................................................................ 10

11 Line9minusline10 ......................................................................................................................................... 11

12Qualifyingcurrentyearinvestment ................................................................................................................. 12

13 3%ofamountonline12 .................................................................................................................................. 13

14Enterprisezoneinvestmenttaxcreditcarriedoverfromprioryear ................................................................ 1415EnterinColumn(a)thetotaloflines13and14.EnterinColumn(b)thelesseroftheamountinColumn(a)ortheamountonline11. ............................................................................................................................... 15a 15b

C ENTErpriSE ZONE NEw bUSiNESS FaCiliTy EMplOyEE CrEDiTS

16Monthlyaverageofqualifiednewbusinessfacilityemployees ..................................................................................16

17Numberofemployeesforwhichcredithaspreviouslybeenclaimed .........................................................................17

18Increaseinqualifiedemployees,line16minusline17 ..............................................................................................18

19Numberofemployeesonline18multipliedby$500 .......................................................................................1920Numberofemployeesonline18inanenhancedruralenterprisezone

multipliedby$2,000.........................................................................................................................................20

21Numberofagriculturalprocessingemployeesonline18multipliedby$500 ..................................................21

22Numberofagriculturalprocessingemployeesonline18inanenhancedruralenterprisezonemultipliedby$500 ........22

23Employeecreditcarriedoverfromprioryear ..................................................................................................23

24Numberofhealthinsurancequalifiedemployees______multipliedby$200 ..................................................2425EnterinColumn(a)thetotaloflines19through24.EnterinColumn(b)theamountfromColumn(a)whichis

beingusedtooffset2009tax. .......................................................................................................................25a 25b

D CONTribUTiON TO ENTErpriSE ZONE aDMiNiSTraTOr CrEDiT

26Currentyearcashcontributions.......................................................................................................................26

27valueofcurrentyearin-kindcontributions ......................................................................................................27

28Totaloflines26and27 ....................................................................................................................................28

29Thesmallerof$100,000or25%ofline28 ......................................................................................................29

30Limitationonin–kindcredit,50%ofline29 .....................................................................................................30

31Allowablein–kindcredit,thesmalleroflines27or30 ..................................................................................... 31

32Limitationoncashcredit,line29minusline31 ...............................................................................................32

33Allowablecashcredit,thesmalleroflines26or32 ......................................................................................... 33

34Entereitherthetotaloflines31and33or$100,000,whicheverisless .........................................................34

35Contributioncreditcarriedoverfromprioryear ...............................................................................................3536EnterinColumn(a)thetotaloflines34and35.EnterinColumn(b)theamountfromColumn(a)whichis

beingusedtooffset2009tax ........................................................................................................................36a 36b

Taxpayer’sname ColoradoAccountNumber

The credits entered on this form are non-refundable. Consequently, the total credits used for tax year 2009 may not exceed your 2009 income tax liability. Calculate and enter the total credit available in Column (a). Enter in Column (b) only the amount of the credit to be applied against this year’s tax liability. any difference in the amounts in Columns (a) and (b) for a given line may be entered at the end of this form and carried forward to the following year.

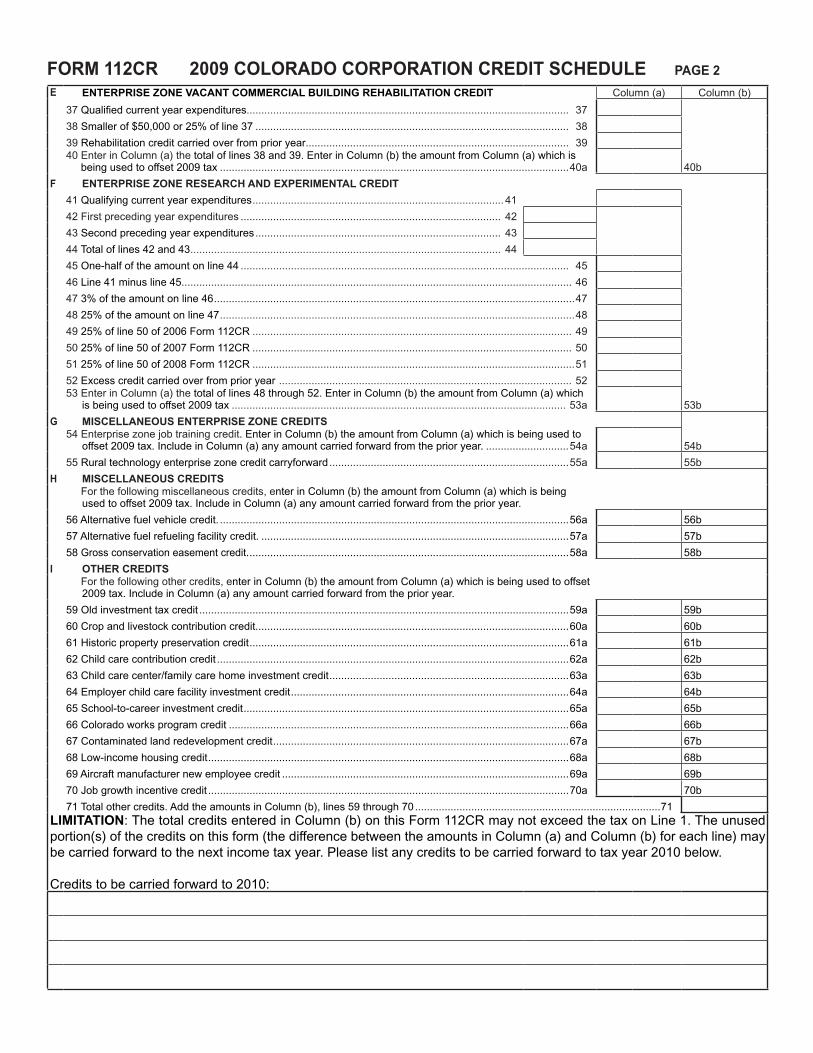

FOrM 112Cr 2009 COlOraDO COrpOraTiON CrEDiT SChEDUlE pagE 2

E ENTErpriSE ZONE VaCaNT COMMErCial bUilDiNg rEhabiliTaTiON CrEDiT Column(a) Column(b)

37Qualifiedcurrentyearexpenditures.............................................................................................................37

38Smallerof$50,000or25%ofline37 ..........................................................................................................38

39Rehabilitationcreditcarriedoverfromprioryear......................................................................................... 3940EnterinColumn(a)thetotaloflines38and39.EnterinColumn(b)theamountfromColumn(a)whichis

beingusedtooffset2009tax ......................................................................................................................40a 40b

F ENTErpriSE ZONE rESEarCh aND EXpEriMENTal CrEDiT

41Qualifyingcurrentyearexpenditures .....................................................................................41

42Firstprecedingyearexpenditures ........................................................................................ 42

43Secondprecedingyearexpenditures ................................................................................... 43

44Totaloflines42and43 ......................................................................................................... 44

45One-halfoftheamountonline44 ...............................................................................................................45

46Line41minusline45....................................................................................................................................46

47 3%oftheamountonline46 ..........................................................................................................................47

4825%oftheamountonline47 ........................................................................................................................48

4925%ofline50of2006Form112CR ............................................................................................................49

5025%ofline50of2007Form112CR ............................................................................................................50

5125%ofline50of2008Form112CR .............................................................................................................51

52Excesscreditcarriedoverfromprioryear ................................................................................................... 5253EnterinColumn(a)thetotaloflines48through52.EnterinColumn(b)theamountfromColumn(a)which

isbeingusedtooffset2009tax .................................................................................................................53a 53b

g MiSCEllaNEOUS ENTErpriSE ZONE CrEDiTS54Enterprisezonejobtrainingcredit.EnterinColumn(b)theamountfromColumn(a)whichisbeingusedto

offset2009tax.IncludeinColumn(a)anyamountcarriedforwardfromtheprioryear. ............................54a 54b

55Ruraltechnologyenterprisezonecreditcarryforward .................................................................................55a 55b

h MiSCEllaNEOUS CrEDiTS57 Forthefollowingmiscellaneouscredits,enterinColumn(b)theamountfromColumn(a)whichisbeing

usedtooffset2009tax.IncludeinColumn(a)anyamountcarriedforwardfromtheprioryear.

56Alternativefuelvehiclecredit. ......................................................................................................................56a 56b

57Alternativefuelrefuelingfacilitycredit. ........................................................................................................57a 57b

58Grossconservationeasementcredit. ............................................................................................................58a 58b

i OThEr CrEDiTS57 Forthefollowingothercredits,enterinColumn(b)theamountfromColumn(a)whichisbeingusedtooffset

2009tax.IncludeinColumn(a)anyamountcarriedforwardfromtheprioryear.

59Oldinvestmenttaxcredit .............................................................................................................................59a 59b

60Cropandlivestockcontributioncredit..........................................................................................................60a 60b

61Historicpropertypreservationcredit ............................................................................................................61a 61b

62Childcarecontributioncredit .......................................................................................................................62a 62b

63Childcarecenter/familycarehomeinvestmentcredit .................................................................................63a 63b

64Employerchildcarefacilityinvestmentcredit ..............................................................................................64a 64b

65School-to-careerinvestmentcredit ..............................................................................................................65a 65b

66Coloradoworksprogramcredit ...................................................................................................................66a 66b

67Contaminatedlandredevelopmentcredit ....................................................................................................67a 67b

68Low-incomehousingcredit ..........................................................................................................................68a 68b

69Aircraftmanufacturernewemployeecredit .................................................................................................69a 69b

70Jobgrowthincentivecredit ..........................................................................................................................70a 70b

71Totalothercredits.AddtheamountsinColumn(b),lines59through70 ...................................................................................71liMiTaTiON:ThetotalcreditsenteredinColumn(b)onthisForm112CRmaynotexceedthetaxonLine1.Theunusedportion(s)ofthecreditsonthisform(thedifferencebetweentheamountsinColumn(a)andColumn(b)foreachline)maybecarriedforwardtothenextincometaxyear.Pleaselistanycreditstobecarriedforwardtotaxyear2010below.

Creditstobecarriedforwardto2010:

Page15

Enterprise ZonesAn enterprise zone is an economically distressed areaofColorado inwhich special tax incentives are offered tobusinessesthatexpandorlocateinthezone.Thepurposeofthetaxincentivesistocreatenewjobsandinvestmentsinthezone.See General6forinformationregardingthelocationoftheenterprisezones.

Enterprise Zone investment Tax CreditIn lieuof theoldColorado investment taxcredit(ITC)withrespecttosuchproperty,thereshallbeallowedtoanypersonaColorado income taxcredit inanamountequal to threepercentofthequalifiedinvestment(asdefinedinsection46oftheinternalrevenuecode)insection38property(definedinsection48oftheinternalrevenuecode)assaidsections46and48existedpriortotheenactmentofthefederalRevenueReconciliationActof1990totheextentsuchpropertywasusedsolelyandexclusively inaColoradoenterprisezoneduringthefirsttwelvemonthsofownershipofsuchpropertybythetaxpayer.

Section38property isbasically tangiblepersonalpropertywhichiseither(federal)recoverypropertyorotherdepreciableoramortizablepropertyhavingausefullifeofthreeyearsormoreusedinthetaxpayer’stradeorbusiness.Only60percentoftheinvestmentin3-yearrecoverypropertyqualifiesforthecredit.Thequalifiedinvestmentinusedpropertyislimitedto$150,000peryear,andanyamountsexpensedundersection179oftheinternalrevenuecodedonotqualifyforthecredit.Undercertaincircumstancesthetaxpayermayclaimthecreditonleasedproperty.

TheenterprisezoneITCmaybeclaimedinanamountequalto thefirst$5,000of tax liabilityplus50percentof thetaxliabilityinexcessof$5,000.EnterprisezoneITCearnedintaxyearsbeginningonorafterJanuary1,1996maybecarriedback3yearsand forward12.Enterprisezone ITCearnedintaxyearspriortoJanuary1,1996maybecarriedback3yearsandforward7.

AnytaxpayerclaiminganenterprisezoneITCof$450ormoremustsubmitwithitsincometaxreturnacertificatefromthezoneadministrator(FormDR0074)totheeffectthatthetaxpayer‘sbusinessislocatedintheenterprisezone. 11.

Enterprise Zone New business Facility Employee CreditsOnlytaxpayerswhoestablishanewbusinessfacilityorexpandanexistingfacilityinanenterprisezonemayclaimthenewbusinessfacilityemployeecredits.Thesecreditsmaynotbeclaimedwithrespecttofacilitiesthatwereinplacepriortotheestablishmentofthezoneexceptforaqualifiedexpansion.

• basic employee credit.Taxpayerswhichestablishanewbusinessfacilitymayclaimacreditof$500forthefirst twelvemonthperiod theyemployaqualifiednewbusinessfacilityemployee.Forsubsequenttaxperiods,theyareallowedtoclaimthiscreditwithrespecttotheincreaseintheaveragenumberofenterprisezonenewbusinessfacilityemployees.Anadditional$2,000creditfor each new business facility employee is availabletobusinesseslocatedinanenhancedruralenterprisezone.

• agricultural processing employee credit. Any taxpayerwhooperatesabusinesswithinanenterprisezone which adds value through manufacturing or

processing to agricultural commodities can claim an additional$500employeecredit.Anadditional$500credit

for each new business facility agricultural processingemployee is available to businesses located in anenhancedruralenterprisezone.Onlybusinessesdirectlyengaged in manufacturing or processing agriculturalcommoditiesintosomeformotherthanthatwhichentersnormalagriculturalcommoditymarketingchannelsqualifyforthisspecialincentive.Harvesting,cleaning,packaging,storing,transporting,wholesaling,retailing,orotherwisedistributingproductswithoutchangingtheirformdonotqualify.

• health insurance credit.Anenterprisezonetaxpayercanqualifyforacreditof$200foreachnewbusinessfacilityemployeewhoisinsuredunderahealthinsuranceplan or program provided through the employer.Anyhealth insurance, health maintenance organization,orprepaidhealthplanwhichisapprovedbytheStateInsuranceCommissionerforsaleinColoradoqualifies.Theemployermustcontribute50percentormoreofthetotalcostoftheplan.Aqualifyingtaxpayermayclaimthiscreditforthefirsttwofullincometaxyearsafterthefacilityiscompletedoracquiredwithinanenterprisezone.

Inorder toclaimtheenterprisezonenewbusinessfacilityemployeecredits, thetaxpayermustsubmitwith itsreturnacertificationfromthezoneadministrator(FormDR0074).

10.

Contributions To Enterprise Zone administrator CreditThecreditforcontributionstoanenterprisezoneadministratortofurthertheeconomicdevelopmentplanofthezoneisallowedat25percentforcashcontributions,12.5percentforin-kindcontributions,andablendedpercentageforcombinedcash/in-kindcontributions. 23.Thecertificate(s)ofcontribution(FormDR0075)furnishedtoyoubythezoneadministratorortheprogram,projectororganizationwillshowtheamountofyourcontributionsthatqualifyforthe25percentcash–12.5percentin-kindcredit.FormDR0075mustbeattachedtoForm112.

Thecontributioncreditissubjecttothefollowingrules:

1. Theamountofcreditgeneratedinanyonetaxyearmaynotexceed$100,000.

2. Theamountofcreditgeneratedinexcessofthecreditclaimedmaybecarriedforwardforupto5years.

3. Thecreditislimitedto25percentofthetotalvalueofthecontribution.

4. Credit for in-kind contributions are limited to one-halfthe credit allowed for cash contributions of the samevalue.

5. Ifataxpayerhasbothcashandin-kindcontributionsduringataxyear,creditforcashcontributionsmaybeallowedatupto100percentbutonlytotheextentnecessarytobringthetotalcreditupto25percentofthevalueofthecombinedcontributions.

6. Creditwillnotbeallowedforcontributionsthatdirectlybenefitthecontributororthatarenotdirectlyrelatedtojobcreation,jobpreservation,child-carepromotionorfortemporary,emergencyortransitionalhousingprogramswhichpromoteemploymentforhomelesspersons.

Page16

Fyis are available at www.TaxColorado.com

COlOraDO DEparTMENT OF rEVENUEDENvERCO80261-0006www.TaxColorado.com

PRSRTSTDU.S.POSTAGE

paiDCOLORADODEPTOFREvENUE

Enterprise Zone Vacant Commercial building rehabilita-tion CreditA25percentcreditisavailableforrehabilitatingcommercialbuildingsinanenterprisezonewhichareatleast20yearsoldandwhichhavebeenvacantforatleasttwoyears. 24.

Enterprise Zone research and Experimental activities CreditTaxpayerswhomakeresearchandexperimentalexpendituresinanenterprisezoneareentitledtoacreditintheamountof3percentofsuchcurrentyearexpendituresinexcessoftheaverageofsuchexpendituresforthetwoprecedingtaxyears. 22.

Enterprise Zone Job Training CreditAcreditof10percentof the total currentyear investmentin a qualified job training program for employeesworkingpredominantlywithinanenterprisezoneisavailable. 31.

rural Technology Enterprise Zone Credit CarryforwardCredits from1999-2004 inexcessof the taxduecanbecarriedforwardfor10years. 36.

alternative Fuel refueling Facility CreditA 50 percent credit is available for the construction,reconstructionoracquisitionofanalternativefuelrefuelingfacility. 9.

gross Conservation Easement CreditAcreditbasedonthevalueofadonatedconservationeasementinColoradoisavailable.AttachacopyofFormDR1305toForm112whenclaimingthiscredit.Additionaldocumentationisrequiredifthecorporationdonatedtheeasementduringthetaxyear. 39.

The Old investment Tax CreditTheoldinvestmenttaxcreditisthesumoftheoldinvestmenttax credit carry over, the current year old investment taxcredit and the old investment tax credit carry back. Thecurrentyearcreditis10percentofthefederalcurrentyearrehabilitation,energyandreforestationinvestmentcreditonassetslocatedinColorado.Thecreditislimitedtothefirst$5,000oftaxliabilityplus25percentofthetaxinexcessof$5,000.Excesscreditmaybecarriedbackthreeyearsandforwardseven. 11.

Crop and livestock Contribution CreditA25percentcreditisavailableforthedonationofcropsorlivestocktoacharitableorganization. 57.historic property preservation CreditAcreditof20percentofthecostofrestoringcertifiedhistoricpropertyinColoradoisavailable. 1.

Child Care Contribution CreditA50percentcredit isavailable forqualifyingcontributionsmadetopromotechildcareinColorado. 35.

Child Care Facility investment CreditA20percentinvestmentcreditisavailableforcertaintangiblepersonalpropertyusedintheoperationofachildcarecenter,afamilychildcarehome,orafostercarehome. 7.

Employer Child Care Facility investment CreditA 10 percent investment credit is available for employersponsoredchildcarefacilityinvestment. 7.

School-to-career investment CreditA credit of 10 percent of the current year investment inaqualifiedschool-to-careerprogram isavailable. 32.

Colorado works program CreditAcreditof20percentofanemployer’sexpenditurestoemployrecipientsofpublicassistanceisavailable. 34.

Contaminated land redevelopment CreditA20percent–50percentcreditisavailableforexpendituresmade to redevelop contaminated land in Colorado. 42.

low-income housing CreditA credit is available for owners of qualified low-incomehousingdevelopments.YoumustattachacopyofyourcreditcertificationfromtheColoradoHousingandFinanceAuthoritytoclaimthiscredit. 46.

aircraft Manufacturer New Employee CreditA credit is available to qualified aircraft manufacturers locatedinanaviationdevelopmentzone. 62.

Job growth incentive CreditCreditsareapprovedandcertifiedbytheColoradoEconomicDevelopment Commission. A credit certificate issued by theCommissionmustbeattachedtoanyreturnclaimingthiscredit.