Embed Size (px)

Citation preview

C) Option markets and contracts

identify the basic elements and describe the characteristics of option contracts;

An option is a contract. It gives one party (the holder of the option) the right

to choose, during a specified period of time, to buy (or sell, respectively) a specified quantity of a specified asset (for instance a stock) at a given price.

The other contract party (the writer of the option) has the obligation to fulfill the holder's right.

Put Option Call Option

Long-

Buyer of Put-

Holder

Short-

Seller of Put-

Writer

Long-

Buyer of Put-

Holder

Short-

Seller of Put-

Writer

define European option, American option, money ness, payoff, intrinsic value, andtime value

American option: may be exercised at any time up to and including the contracts expiration date

European option: can be exercised only on the contract’s expiration period.

At expiration an American and an European on the same asset and the same strike price are equal

define European option, American option, money ness, payoff, intrinsic value, andtime value.. Contd ..

If 2 options are identical in all respects, except that one is American and the other is European, tha value of an American option will equal or exceed the value of European option

Options Terminologies.

In-the-money: At-the money Out of Money

CALL OPTION BUY PUT OPTION SELL160 ITM SP 160 OTM162 ITM SP 162 OTM164 MP 164 MP166 OTM SP 166 ITM168 OTM SP 168 ITM170 OTM SP 170 ITM

Intrinsic Value of an Option.. An option’s intrinsic value is the

amount by which the option is in-the money. It is the amount that an option owner would receive if the option were exercised.

An option has a zero intrinsic value if it is it is at the money or out of money, regardless of whether it is a call or put

Intrinsic Value of an Option..contd Lets look at the value of a call option

at expiration. If the expiration date date price of the stock exceeds the strike price of the option. The call owner will exercise the option and receive S-X. if the price of the stock is less that the strike price, the call holder will let the option expire and get nothing.

Intrinsic Value of an Option..contd The intrinsic value of the call option

at expiration is the greater of (S-X) or 0. That is C= max(0, S-X)

Value

Stock price at expiration X=50 X=55

0

-5

5

Strike Price of 50 Long Call

Short Call

Put Option pay off

Value

Stock price at expiration

X=50X=40

0

-10

10

Strike Price of 50

Long put

Short Put

Call Option pay off

Time Value The time value of an option is the

amount by which the option premium exceeds the intrinsic value and is sometimes called the speculative value of the option.Option value= intrinsic value+time value.

As discussed earlier, the intrinsic value of an option is the amount by which the option is in the money

At any point during the life of an option its value will be typically greater than its intrinsic value. This is because there is some probability that the stock price will change in an amount that gives the option a positive pay off at expiration greater that the current (intrinsic) value.

Recall that an option’s intrinsic (to a buyer) is the amount of payoff at expiration and is bounded by zero. When an option reaches expiration there is no time remaining and the time value is zero.

For American options and most cases for European options the longer the time to expiration, the greater the time value and other things being equal, the greater the options premium

Identify different types of options Financial Options Options on futures Commodity Options

Financial Options Bond Options Index Options*cash settled Stock Options

Option on futures Sometimes called futures options, give the holder the

right to buy or sell a specified futures contract on or before a given date enter into a long side of a futures contract at a given futures price. Assume that you hold a call option on a bond future @ 98 % of the face value and at the expiration the future price of the bond is 99. By exercising the call, you can take a long position in the futures contract, and the account is immediately marked to market on the settlement price. Your account will be credited with an cash amount of 1% of the face value of the face value of the bond.

The seller of the exercised call will take a short position in the futures contract and the mark to market value of this position will generate the cash position deposited in your account a

Compare IRO & FRA. IRO are similar to stock options

except that the exercise price is an interest rate and the underlying asset is a reference rate

IRO are also similar to FRA because there is no delivery asset, instead they are settled in cash

Consider a long position in a LIBOR based Interest rate call option with a notional amount of $ 1000000 and a strike rate of 5%.

If at expiration libor is greater than 5% the option can be exercised and the owner will receive 1000000*(LIBOR-5%).

IF Libor is less than 5%, the option expires worthless

Interest rate cap and floor An interest rate cap is a series of interest rate call

option, having expiry dates that corresponds to the reset dates on the floating rate loan. Caps are often used to protect a floating rate borrower from an increase in the interest rates. Caps places a maximum limit on the interest rates on the floating rate

Caps pay when rates rise above the cap rate. In this regard, a cap can be viewed as a series of interest rate call options which strike equals to the cap rate. Each option in a cap is called a caplet.

Interest rate cap and floor An interest rate floor is a series of interest rate put

option, having expiry dates that corresponds to the reset dates on the floating rate loan. Floors are often used to protect a floating rate lender from an decline in the interest rates. Floors places a minimum limit on the interest rates on the floating rate

Floors pay when rates fall below the floor rate. In this regard, a floor can be viewed as a series of interest rate put options which strike equals to the floor rate. Each option in a floor is called a floor let

Example

In the event that LIBOR rises above 10%, the cap will make a payment to the cap buyer to offset any interest expenses in excess of an annual rate of 10%

Reset 90 daysReference Rate LIBOR

Cap 10%Floor 5%

Loan Rate

10% cap

5% floor

Loan rate without caps or Floors

LIBOR

5%

10%

5% 10%

Received by cap owner

Received by floor owner

Identify the minimum and maximum values of European and American Options

St=price of underlying stock at time t

x = exercise price of the optionT = time to expiry

ct= price of european call at time t, at any time t prior to expiration

ct=price of Auropean call at time t, at any time t prior to expiration

pt=price of european put at time t, at any time t prior to expiration

Pt=price of American pur at time t, at any time t prior to expirationRFR

Lower case letters are used to denote European style options

Lower bounds for Options (Call & Put) for both American and European options.

Theoretically no option will sell for less than its intrinsic value and no option can take a negative value.

This means that the lower bound for any any option is zero for both Americans and European options

Upper bounds for call Options (American and European )

The maximum value of either an American or European call option at any time t is the time t share price of the underlying stock. This makes sense because no one would pay a price for a right to buy an asset that exceeds the assets value. It would be cheaper to simply buy the underlying stock

At time t=0, the upper boundary condition can be expressed respectively for American and European call option is

American Option C0 <= S0 European Option C0 <= S0

Upper bounds for PUT Options (American and European )

The price for an American put option cannot be more than its strike price. This is the exercise value in the event the underlying stock price goes below zero. However, since the European puts cannot be exercised prior to expiration, the maximum value is the PV of the exercise price discounted at the RFR.

Upper bounds for PUT Options (American and European )

Even if the exercise price goes to zero and is expected to stay zero, the intrinsic value X, will not be received until expiration date. At time t=0, the upper boundary condition can be expressed for American and European option can be expressed as

P0<=X and p0 <=X/1+( RFR) ^ t

Option Strategies. Basic Options Strategy:-Long on call-Short on call-Long on Put-Short on put

Spread Strategies-Bull spread.(Buy call-Sell call @ Higher Exercise

Price)-Market view Bullish-Bear spread. (Buy call-Sell call @ Lower Exercise

Price).-market view Bears

Option Strategies. Straddle-market View Mixed(volatile)-Long Straddle -Short Straddle Strangle -market View Mixed(Range

bound)-Long Straddle -Short Straddle

Spread Strategy

Bull SpreadMarket View Action Profit potential Loss Potentail

Bullish Limited LimitedBuy Call, Sell call @ higher strike

Bull Call Spread

340 360Bull Call Spread -16 9

Net P/LBuy call 340;

Prem16Sell call 360; Prem 9

Spot300 -7 -16 9310 -7 -16 9320 -7 -16 9330 -7 -16 9340 -7 -16 9350 3 -6 9360 13 4 9370 13 14 -1380 13 24 -11390 13 34 -21400 13 44 -31

This involves purchase and sale of Call options at different exercise prices but with the same exercise date. The purchase call shud have a Lower Exercise

Payoff diagram of bull spread

-10

-5

0

5

10

15

Reliance price

Pro

fit/

Lo

ss

Net P/L

Bull Spread

Spread Strategy

Bear SpreadMarket View Action Profit potential Loss Potential

Bearish Limited Limited

Bear Call Spread

Buy Call, Sell call @ Lower strike

Bear Call Spread

360 340Bear Call Spread -9 16

Net P/LBuy call 360; Prem

9Sell call 340; Prem 16

Spot300 7 -9 16310 7 -9 16320 7 -9 16330 7 -9 16340 7 -9 16350 -3 -9 6360 -13 -9 -4370 -13 1 -14380 -13 11 -24390 -13 21 -34400 -13 31 -44

This involves purchase and sale of Call options at different exercise prices but with the same exercise date. The purchase call shud have a Higher Exercise

-15

-10

-5

0

5

10

Spot 300 310 320 330 340 350 360 370 380 390

Reliance stock price

Pro

fit/

Lo

ss

Net P/L

Bear Spread

Straddle-market View Mixed

340

Spot Net P/L1 Call buy : Prem:

16 1 Put buy; Prem: 13290 21 -16 37300 11 -16 27310 1 -16 17320 -9 -16 7330 -19 -16 -3340 -29 -16 -13350 -19 -6 -13360 -9 4 -13370 1 14 -13380 11 24 -13390 21 34 -13

Buy Call, Buy Put @ same Strike

Strike: 340

LONG Straddle Long Straddle Pay PrmMarket View Action Profit Potential Loss PotentialMixed Unlimited limitedBuy call Buy Put

@ same Exercise

Payoff structure for Long Straddle

-40

-20

0

20

40

290 300 310 320 330 340 350 360 370 380 390

Reliance stock price

Pro

fit/L

oss

Short Straddle

Short straddle I M receiving Prm

Sold/short on call Sold/short on putStrike: 340

340Spot Net P/L Call : Prem: 16 Put Prem: 13

290 -21 16 -37300 -11 16 -27310 -1 16 -17320 9 16 -7330 19 16 3340 29 16 13350 19 6 13360 9 -4 13370 -1 -14 13380 -11 -24 13390 -21 -34 13

sell Call, sell Put @ same Strike

Short StraddelMarket View Action Profit Potential Loss PotentialMixed limited UnlimitedSell call Sell Put

@ same Exercise

Payoff structure for short straddle

-30

-20

-10

0

10

20

30

40

290 300 310 320 330 340 350 360 370 380 390

Reliance stock price

Pro

fit/

Lo

ss

Buy Call Buy PUTPremium: 12 Premium: 10Strike 350 Strike 330

Spot Net P/L Call:Prem 12 Put: Prem 10-12 -10350 330

280 28 -12 40290 18 -12 30300 8 -12 20310 -2 -12 10320 -12 -12 0330 -22 -12 -10340 -22 -12 -10350 -22 -12 -10360 -12 -2 -10370 -2 8 -10380 8 18 -10390 18 28 -10400 28 38 -10

Long Strangle I PAY PRM

Market View Action Profit Potential Loss Potential

VolatileBuy Call, Buy Put -Buy

Call at higher SP

Payoff structure for Long Strangle

-30

-20

-10

0

10

20

30

40

280

300

320

340

360

380

400

Reliance

Pro

fit/

Lo

ss

Short Strangle I Recv PRM

Market View Action Profit Potential Loss Potential

VolatileSell Call, Sell Put -

Sell Call at higher SP

Sell Call Sell PutPremium: 12 Premium: 10Strike 350 Strike 330

Spot Net P/L Call:Prem 12 Put: Prem 1012 10350 330

280 -28 12 -40290 -18 12 -30300 -8 12 -20310 2 12 -10320 12 12 0330 22 12 10340 22 12 10350 22 12 10360 12 2 10370 2 -8 10380 -8 -18 10390 -18 -28 10400 -28 -38 10

Short strangle payout structure

-40

-30

-20

-10

0

10

20

30

280

300

320

340

360

380

400

Reliance stock price

Pro

fit/

Lo

ss

INTRINSIC VALUE

For a call option:Intrinsic value = Price of the underlying - Exercise price

For a put option: Intrinsic value = Exercise price - Price of the underlying

FACTORS AFFECTING PREMIA There are five major factors affecting

the Option premium: Price of Underlying Exercise Price Time to Maturity Volatility of the Underlying

And two less important factors: Short-Term Interest Rates Dividends

Intuition would tell us that the spot price of the underlying, exercise price, risk-free interest rate, volatility of the underlying, time to expiration and dividends on the underlying(stock or index) should affect the option price.

OPTION Pricing

Black and Scholes start by specifying a simple and well–known equation that models the way in which stock prices fluctuate. This equation called Geometric Brownian Motion, implies that stock returns will have a lognormal distribution, meaning that the logarithm of the stock’s return will follow the normal (bell shaped) distribution.

The Black-Scholes (1973) option pricing formula prices European put or call options on a stock that does not pay a dividend or make other distributions

Part I of the model In order to understand the model

itself, we divide it into two parts. The first part, SN(d1), derives the expected benefit from acquiring a stock outright. This is found by multiplying stock price [S] by the change in the call premium with respect to a change in the underlying stock price [N(d1)].

Part II of the model The second part of the model, Ke(- t)N(d2),

gives the present value of paying the exercise price on the expiration day.

The fair market value of the call option is then calculated by taking the difference between these two parts.

Assumptions of the Black and Scholes Model:

The stock pays no dividends during the option's life

European exercise terms are used Markets are efficient No commissions are charged Interest rates remain constant and

known Returns are log normally distributed

Value of PUT Option

P=Ke^-rt N(D2) – S N (D1)

Binomial tree A useful and very popular technique

for pricing an option or other derivatives involves constructing what is know as Binomial tree

One step Binomial tree We start by considering a very

simple situation where a stock price is currently $ 20 and it is known that at the end of 3 months the stock price will be either $22 or $ 18

We suppose that the stock pays no dividend and that we are interested in valuing a European call option to buy the stock @ 21 in 3 months

Stock Price $22

Option Price $1

Stock Price $18

Option Price $0

Stock Price $20

Simple binomial tree

One step Binomial tree

We set up a portfolio of the stock and the option in such a way that there is no uncertainty about the value of the portfolio at the end of 3 months.

We also argue that since the portfolio has no risk, the return must be equal to the RFR. This enables to work out the cost of setting up the portfolio and therefore the option price. Since there are 2 securities ( the stock and stock option) and only 2 possible outcomes, it is always possible to set a riskless portfolio

One step Binomial tree Consider a portfolio consisting of a long position in

delta shares of the stock and a short position in one call option.

We will calculate the value of delta that makes the portfolio risk less.

IF the stock price moves from 20 to 22, the value of the shares is Delta 22 and the value of the option is 1, so that the value of the portfolio is Delta 22-1

If the stock price moves down from 20 to 18, the value of the shares is Delta 18 and the value of the option is 0, so that the total value of the portfolio is delta 18

One step Binomial tree The portfolio is risk less if the value of delta

is chosen so that the final value of the portfolio is the same for both the alternative stock prices.

This means: 22Delta –1 = 18 delta Delta = 0.25A risk less portfolio is therefore Long 0.25 share Short = 1 option

One step Binomial tree If the stock price moves up to 22, the

value of the portfolio is 22*0.25-1=4.5 If the value of the stock moves to 18, the

value of the portfolio is 18*0.25 = 4.5 Note: regardless of whether the stock

price moves up or down the value of the portfolio is always 4.5 at the end of the life of the option

One step Binomial tree Risk less portfolio must, in the absence of

arbitrage opportunity earn a RFR. Suppose in this case the RFR is 12%. It follows that the value of the portfolio today must be the PV of 4.5 or

4.5 e ^ -0.12*0.25= 4.367The value of the stock price today is known to be

20. The value of the portfolio today is therefore ,20*0.25-F = 5 – FTherefore F = 0.633

One step Binomial tree This shows that in the absence of

arbitrage opportunity the value of the option is 0.633

Interpreting volume and open interest

While volume alone is not a useful determinant of market direction, used in conjunction with other data it can be very beneficial - especially to longer term traders - in identifying whether a continuation of or reversal in the prevailing trend is likely.

Most traders incorporate Open Interest data with their volume analysis. Open Interest is the net number of open bullish positions in a futures market.

Volume at low levels reflects uncertainty regarding the future direction of the market in question. Conversely, high volume suggests a high level of confidence in the future direction

Low levels of Open Interest reflect a market lacking in liquidity and, therefore, one which will be relatively more susceptible to being moved by a trade than a more liquid counterpart. When there are high levels of Open Interest, deals are likely to be rapidly swallowed up by the market - due to the fact that there will be a vast array of participants eager to open new positions or take profits - and consequently have far less impact on the current price.

Interpreting volume and open interest

Interpreting volume and open interest If volume is relatively high while the market is going up

and remains relatively low during corrections, the inference is that the market is in a strong uptrend, which should continue.

both open interest and prices are increasing, then new buyers are being brought into the market with a strong technical picture unfolding. Expect the uptrend to continue

In the event of open interest declining while prices are also slipping, liquidation by long positions is the implication, therefore suggesting a technically strong market overall. In other words, the market is strong as open interest declining suggests no new aggressive shorts, as this would entail an increase in open interest.

Risk Measures- Delta Delta Hedging Delta is defined as the rate of change of its price with

respect to the price of the underlying asset.It is the slope of the curve that relates the derivatives price to the underlying asset price.

For example, the price of a call option with a hedge ratio of 40 will rise 40% (of the stock-price move) if the price of the underlying stock increases. Typically, options with high hedge ratios are usually more profitable to buy rather than write since the greater the percentage movement - relative to the underlying's price and the corresponding little time-value erosion - the greater the leverage. The opposite is true for options with a low hedge ratio.

Theta The theta of a portfolio of a derivative,

is the rate of change of the value of the portfolio with respect to time with all else remaining the same.

Some times referred to as time decay

Gamma The gamma of the portfolio of

derivatives on an underlying asset is the rate of change of the portfolio;s delta with respect to the price of the underlying asset

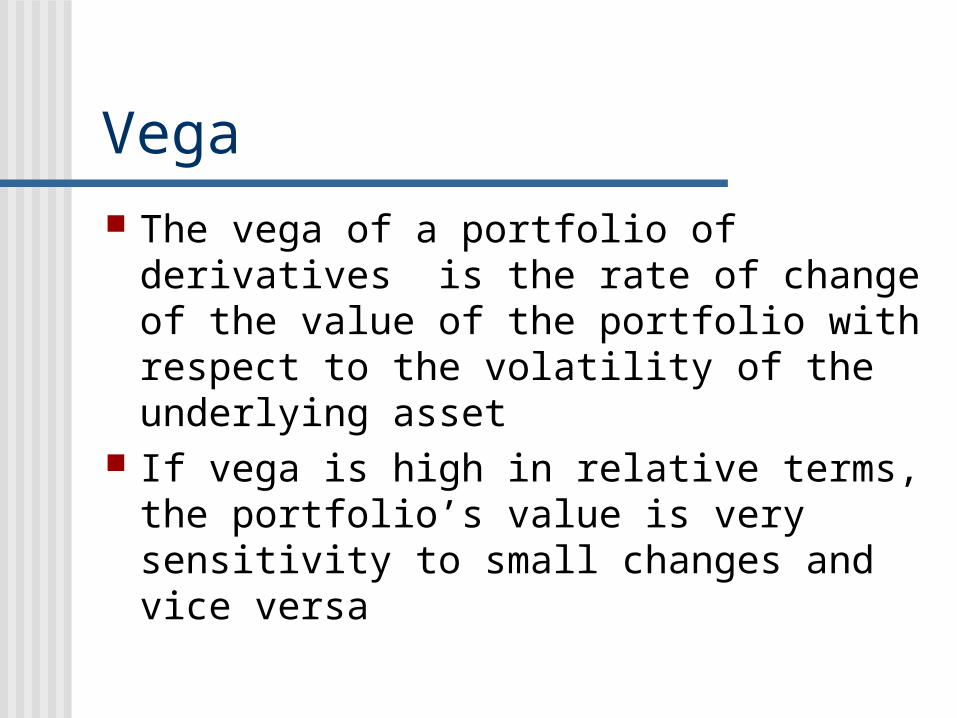

Vega The vega of a portfolio of derivatives is

the rate of change of the value of the portfolio with respect to the volatility of the underlying asset

If vega is high in relative terms, the portfolio’s value is very sensitivity to small changes and vice versa

Rho The rho of a portfolio of derivative is

the rate of change of the value of the portfolio with respect to interest rates.

It measures the sensitivity of the value of the portfolio with respect to interest rates

Exotic options Derivatives with more complex pay offs

than the standard American or European options are sometimes referred to as exotic options

Most exotics are traded over the counter and are structured by Financial institutions

Types of Exotics Packages Non standard American option s Forward Start Options Compound options As you like it option Barrier options Look back options Asian options

Package A package is portfolio consisting of

standard European options call, standard European puts, forward contracts and cash

Non standard American Option In Americans option exercise can take place

at any time during the life of the option and the exercise price will be the same

One type of non standard American option is known as Bermudan option. In this early exercise is restricted to certain dates during the life of the option. An example of a Bermudan option would be an American swap option that can be exercised only on dates when swap payments are exchanged

Compound Options Compound options are options on options 4 main types of compound options, call on call,

call on put, put on put and put on call Example call on call: on the first exercise date,

the holder of the compound option is entitled to pay the first strike price and receive a call option. The call option gives the holder the right to buy the underlying asset for the second strike price on the second exercise date. The compound option will be exercised on the first exercise date only if the value of the option on that date is greater than the first strike price

“As you like it “ An as you like it option (sometimes referred

to as a choosers option), has the feature that after a specified period of time, the holder can choose whether the option is a call or a put option.

Suppose that the time at which the charge is made is t1, the value of the as you like it option is max (c,p)

Where c is the value of call Where p is the value of the put option

Barrier option Barrier option are options where the

payoff depends on whether the underlying assets price reaches a certain level during a certain period of time

One of the product is CAPS

Binary options Binary options are options with

discontinuous pay offs A simple example of binary option is a

cash or nothing call. This pays off nothing if the stock price ends up below the strike price and pays a fixed amount, if it ends up above the strike price

“Look back” options The pay offs from look back options depend

upon the maximum or minimum stock price reached during the life of the option.

The pay off from a European style look back call option is the amount by which the final stock price exceeds the minimum stock stock price achieved during the life of the option

The pay off from a European style look back put option is the amount by which the maximum stock price achieved during the life of the option exceeds the final stock price.

Asian Options Asian pay offs are options where the

pay off depends on the average price of the underlying assets during at least some part of the life of the option