Embed Size (px)

Citation preview

Journal of Macroeconomics, Spring 1997, Vol. 19, No. 2, pp. 1–17 1Copyright � 1997 by Louisiana State University Press0164-0704/97/$1.50

JAMES HARTLEYMount Holyoke College

South Hadley, Massachusetts

KEVIN SALYERSTEVEN SHEFFRIN

University of California, Davis

Davis, California

Calibration and Real Business CycleModels: An UnorthodoxExperiment*

This paper examines the calibration methodology used in real business cycle (RBC) theory. Weconfront the calibrator with data from artificial economies (various Keynesian macroeconomicmodels) and examine whether a prototypical real business cycle model, when calibrated to thesedata sets using standard methods, can match a selected set of sample moments. We find thatthe calibration methodology does constitute a discriminating test in that the calibrated realbusiness cycle models cannot match the moments from all the artificial economies we study.In particular, we find the RBC model can only match the moments of economies whose mo-ments are close to actual U.S. data.

1. Introduction

Nearly a decade ago, Kydland and Prescott (1982) demonstrated thata simple optimal growth model subject to persistent technological shockswould exhibit characteristics that were similar in important respects to actualmacroeconomic data. It is hard to exaggerate the practical importance oftheir finding. Not only did it begin an influential literature on business cycles(i.e., real business cycles) but it transformed the practice of other econo-mists, both theoretical and applied, as well. It has become quite commonnow for many macroeconomists to begin with the real business cycle modelas a basic framework and then use embellishments to highlight additionalfeatures of the data.

Critics of real business cycle models, however, have been uneasy aboutthe empirical methodology used in support of the model. Specifically, these

*We are indebted to Ray Fair, Kevin Hoover, Stephen LeRoy, James Nason, Linda Tesarand Randy Wright for insightful comments and suggestions.

James Hartley, Kevin Salyer and Steven Sheffrin

2

criticisms have focused on the calibration methods used in RBC analysis.The defining characteristics of the calibration approach are: (i) the param-eters of a model are not estimated but instead determined by long-run (i.e.,steady-state) behavior of the economy and (ii) given these parameters, thecharacteristics of the model’s unconditional equilibrium distribution for theendogenous variables are compared to that of the data. This comparisontypically involves a limited set of second moments. Recently, due to thiscriticism, several alternative real business cycles have been estimated ratherthan calibrated.1 Kydland and Prescott (1991), in response to this criticism,strongly defend calibration as a scientific method. In addition, Hoover (1995)also finds some virtues in this approach on philosophical and methodologicalgrounds.

Proponents of estimation point to the possibility of testing overiden-tifying restrictions as a virtue of this method. But Kydland and Prescott haveemphasized the importance of accounting for pervasive measurement errorin economic data. Once one allows for measurement errors, testable over-identifying restrictions can easily disappear. Moreover, a decade of experi-ence of estimating macro models with complex, cross-equation restrictionshas not been comforting. Models often fail these restrictions. When they donot fail these restrictions, it is often because the fit of the model was so poorto begin with that the restrictions do not matter.

Watson (1993) and Canova, Finn, and Pagan (1994) have advocatedalternative strategies for evaluating real business cycle models. Watson es-timates the variance of measurement errors (at different frequencies) whichare necessary to reconcile the models with the data. Canova, Finn, and Paganexamine whether the time series properties of the data (for example, thenumber of co-integrating vectors) match those implied by the model. Bothapproaches provide useful diagnostics and are important contributions toevaluating specific calibrated models.

However, we are still left with a basic question. Is it just an accidentthat calibrated real business cycle models seem to resemble actual econo-mies in important respects or is there something truly fundamental under-lying this correspondence? This paper tries to address this question with anunorthodox experiment using economic models.

We begin by demonstrating that a typical Keynesian model, for whichwe chose the Fairmodel (developed by Ray Fair), will generate sample mo-ments similar to both U.S. data and a real business cycle model calibratedto U.S. data. Furthermore, if real business cycle practitioners were con-fronted with artificial data generated from the Fairmodel, they would chooseparameters similar to those that are chosen to match U.S. data.

1See Altug (1989) and Christiano and Eichenbaum (1992) as examples.

Calibration and Real Business Cycle Models

3

We then use a version of the Fairmodel modified to generate differentaggregate time series. From these time series, we calibrate real businesscycle models using such data as factor shares and the calculated Solow re-siduals. We then ask if the calibrated real business cycle moments matchthe moments of the modified Keynesian model. This experiment addressesthe question of whether real business cycle models can be successfully cal-ibrated to mimic any model.

Our basic finding is that the RBC model and the calibration method-ology does indeed limit the range of data characteristics which can be gen-erated within the model. Specifically, the intertemporal optimization frame-work inherent in all RBC models sharply constrains the relative volatilitiesand correlations among investment, consumption, and output. Moreover,this behavior, as noted by RBC practitioners, is similar to that observed inU.S. data. This result, while comforting to those studying U.S. macroeco-nomic conditions, may prove problematic if RBC models are confronted withdata from other countries. To elaborate on this point, recent research byBackus and Kehoe (1992) has highlighted the variety of correlation prop-erties exhibited in aggregate time-series across countries as well as sampleperiods. Our results suggest that conventional RBC models cannot easilymatch the broad range of data characteristics reported in their study.

The next section describes our simulations with the Fairmodel andreports the estimated sample moments for selected variables. The followingsection uses the simulated data from two versions of the artificial economyto calibrate real business cycle models and determine if they can match themoments of artificial economies. Throughout our discussion we highlight thecritical nature that commonly employed assumptions have in determiningthe goodness of fit of these models.

2. Moments of a Keynesian Macro Model

In this section, we first demonstrate that a typical Keynesian macromodel will generate sample moments similar to those observed in U.S. data.In the following section, we use simulations from this Keynesian model togenerate artificial time series to be used in calibration exercises.

We chose the Fairmodel for our simulations.2 The Fairmodel consistsof 128 equations of which 98 are identities. There are 128 endogenous andover 100 exogenous variables. The 30 behavioral equations were individuallyestimated by two-stage least squares, with the data series starting in the firstquarter of 1954. The model is explicitly Keynesian in design; for example,disequilibrium possibilities are built into the model via a labor constraint

2For a detailed description, see Fair (1990) and Fair (1994).

James Hartley, Kevin Salyer and Steven Sheffrin

4

TABLE 1. Autocorrelation of Output: Actual and Artificial Economies

Leads and Lags

�1 �2 �3 �4

U.S.1 0.84 0.57 0.27 �0.01FM (reaction function) 0.89 0.65 0.39 0.15FM (M1 exog.) 0.92 0.75 0.54 0.34King Plosser, Rebelo2 0.93 0.86 0.80 0.74

NOTES: 1From Kydland and Prescott (1982), Table II, p. 1364.2From King, Plosser, and Rebelo (1988), Table 5, p. 224.

variable. In short, the Fairmodel bears little resemblance to a typical realbusiness cycle model.

To generate artificial data, the Fairmodel was used to produce fore-casts over the period 1968:i to 1977:iv under two assumptions regardingmonetary policy. One set of data was produced under the assumption thatthe monetary aggregate, M1, is exogenous and equal to the historical data.Another was constructed using the Fairmodel’s interest rate reaction func-tion. Given these exogenous time series, the Fairmodel generated time seriesfor the remaining endogenous variables through dynamic simulation. Of the128 endogenous variables in the model, we restrict our attention to thecritical set of output, consumption, investment, and labor input. Specifically,the logarithms of per capita GNP (y), consumption (c), investment (i), andhours worked (n) generated by the model were regressed on a constant anda time trend.3 The residuals from these regressions, which can be interpretedas the percentage deviations from trend, are the series we examine.

We first determine whether the model generates the correct autocor-relations in output. Table 1 contains these values. While the fit appears tobe quite close, as noted earlier, there is no standard metric to gauge thedegree of fit. Hence, for comparison, the output from a real business cyclemodel studied by King, Plosser, and Rebelo (1988) is also reported. Underboth assumptions about monetary policy, the Fairmodel output is less au-tocorrelated than the data from the real business cycle model and matchesquite well the pattern observed in the actual data.

Table 2 compares the cyclical volatility of the Fairmodel series to the

3If the growth model with constant, exogenous technological growth is taken seriously, thenoutput, consumption, and investment should be detrended using a common trend. However,since we are examining only ten years of data, this restriction is too severe. Also, even thoughper-capita labor in the growth model does not have a trend in steady state, we nonethelesslinearly detrended this series as well.

Calibration and Real Business Cycle Models

5

TABLE 2. Descriptive Statistics for U.S. Economy and ArtificialEconomies

ry rc/ry ri/ry rh/ry Corr(y, c) Corr(y, i) Corr(y, h)

U.S. Data1 0.017 0.49 3.02 0.96 0.76 0.80 0.88Fairmodel

(reaction function) 0.012 0.40 2.16 0.70 0.35 0.89 0.80Fairmodel

(M1 exogenous) 0.020 0.65 3.60 0.80 0.79 0.93 0.96Hansen2 0.018 0.29 3.24 0.77 0.87 0.99 0.98Kydland & Prescott3 0.018 0.35 3.58 0.58 0.94 0.80 0.93King, Plosser, Rebelo

Model4 0.043 0.64 2.31 0.48 0.76 0.85 0.73

NOTES: 1From Kydland and Prescott (1990), Tables I and II, p. 10–11.2Hansen (1985) indivisible labor model, see Table 1, p. 321.3Kydland and Prescott (1982) time-to build model, Table III, p. 1364.4Taken from King, Plosser, Rebelo (1988), Table 5, p. 224. Both Hansen and Kydland and

Prescott pass model data through the Hodrick-Prescott filter.

data; in addition the contemporaneous correlations of all variables with out-put are reported for the U.S. and model output. For comparison, the samplemoments from three real business cycle models are also given for compar-ison.4 None of the models matches perfectly the entire set of sample mo-ments, but the Fairmodel seems to do qualitatively as well as the othermodels.5 In particular, output from the model replicates the observed vol-atilities of consumption, investment, and labor relative to that of outputreasonably well.

These results demonstrate that the Fairmodel is able to match a lim-ited set of sample moments at least as well as typical real business cyclemodels. There may be some question, however, as to whether this is par-ticularly surprising. Since the Fairmodel was estimated using data from theactual economy, the parameter values may incorporate these sample mo-ments into the model’s structure.

4Because the cited papers used different detrending procedures on the model data, quanti-tative comparison of the reported sample moments is problematic.

5Because the Fairmodel was used to generate data over a relatively small sample period (9years), the moments reported in Table 2 are somewhat sensitive to the choice of forecast period.For instance, the correlations of consumption, investment and hours with output produced bythe reaction function model over the period 60:i–69:iv are 0.83, 0.90, and 0.90, respectively.Over this period, the same moments under the assumption of exogenous M1 are 0.66, 0.83,and 0.73. However, the relative volatilities, which are the primary focus of the next section, arenot as sensitive to the particular forecasting period.

James Hartley, Kevin Salyer and Steven Sheffrin

6

To be more precise, in some cases, standard econometric methods canbe viewed as “matching moments.” As Bollen (1989) discusses in detail,latent variable models and models with errors of measurement can mosteasily be estimated by matching theoretical and sample covariances. Forsimultaneous equation models, full information maximum likelihood esti-mation is equivalent to minimizing a function of the sample and theoreticalcovariances. Methods-of-moments estimators, of course, also are based on“matching” moments.

Fair, however, estimated his model using single-equation methods,typically, 2SLS with corrections for serially correlated errors. This methodof estimation does not necessarily lead to close fits between actual and sam-ple moments. Moreover, the moments that the real business cycle literatureexamines (and we employ in this paper) are based on detrended data. Thus,there is even less reason to expect a close correspondence between actualand simulated sample moments.

The demonstration that the Fairmodel roughly matches U.S. samplemoments is useful for our purposes. It means that in our base case both theFairmodel and a real business cycle model calibrated to U.S. data producejoint distributions for the endogenous variables that have similar secondmoment characteristics. In the next section, we use the Fairmodel to gen-erate artificial data and then examine the properties of a RBC model cali-brated to this data.

3. Calibrating a RBC Model to the Fairmodel Data

The claim that RBC models should be taken seriously as a useful de-scription of the U.S. economy is often supported by the model’s ability toduplicate two basic characteristics of U.S. time series: investment is two tothree times as volatile as GNP, while consumption exhibits half the volatilityof output. The following quote from a recent article by Hansen and Wright(1992) is typical:

The model predicts that consumption will be less than half as volatileas output, that investment will be about three times as volatile as out-put, and that consumption, investment, and employment will bestrongly positively correlated with output, just as in the postwar U.S.time series. In this sense, the real business cycle approach can bethought of as providing a benchmark for the study of aggregate fluc-tuations (p. 2).

The conviction that these particular features of RBC models constitutetelling evidence of their relevance is reflected in the response of RBC prac-

Calibration and Real Business Cycle Models

7

titioners to the original model’s noted failure in describing labor marketactivity. Specifically, its counterfactual predictions about the correlations be-tween labor supply, productivity, and GNP resulted in modifications to thebasic model (e.g., Hansen’s 1985 introduction of indivisible labor, the mod-eling of government-produced output by Christiano and Eichenbaum 1992and the introduction of a home production sector by Benhabib, Rogerson,and Wright 1991) rather than a refutation of the underlying paradigm.

But how compelling is this evidence? That is, might it be possible thatthe growth model and calibration methodology are sufficiently malleable topermit duplication of these variance-covariance relations from a broad rangeof model economies; in particular, economies whose underlying structure isvastly different from that of the growth model? To put the question morebluntly, Are real business cycles the truth or just truly good chameleons? Toanswer that question, the Fairmodel described in the previous section wasused to generate aggregate time series. We conduct the experiment ofwhether a growth model calibrated to this data can successfully duplicatethe volatilities of consumption, investment and output.

Once again, the Fairmodel was used to generate data over the period68:i–77:iv. For this exercise it was assumed the money stock, M1, was ex-ogenous and determined by the historical record. This produces the sameset of sample moments reported in Table 2; for convenience, these statisticsare repeated in Table 3.

With these characteristics noted, a real business cycle model (identicalto Hansen’s 1985 divisible labor model) was calibrated to the Fairmodeloutput. Specifically, it was assumed that the time path of the economy wascharacterized as the solution to the following social planner problem:

�tmax E b [ln c � A ln (1 � h )] (P)0 � t t� �

t�0

subject to

h 1�hc � k � k k h � k (1 � d) ; (1)t t�1 t t t t

ln k � c ln k � e ; (2)t�1 t t�1

where kt denotes beginning-of-period capital, b is agents’ discount factor, his capital’s share, d the depreciation rate of capital, and A � 0 representsthe importance of leisure in utility. The variable kt � 0 denotes the tech-nology shock; its motion is described by the AR(1) process in Equation (2).It is assumed that es is independently and identically distributed with astandard deviation of re and a mean such that E(kt) � 1.

James Hartley, Kevin Salyer and Steven Sheffrin

8

As is well known, if depreciation is less than 100% then no analyticsolution to problem (P) exists, thus necessitating the use of numerical ap-proximation methods. We employed the approach described in King, Plos-ser, and Rebelo (1988) which involves taking a first-order Taylor series ex-pansion of the necessary equilibrium conditions around the steady state (i.e.,non-stochastic) equilibrium values. The resulting linear expectational differ-ence equations will have a unique solution because of the saddle path prop-erties implied by the typical growth model with constant returns to scale.The solution is represented by a set of functions that express the choicevariables at time t (consumption, labor, and investment) in terms of thecurrent state variables (capital and the technology shock). Moreover, thelinear structure in the approximated economy implies that the solutions willalso be linear. The equilibrium characteristics of the model can then bestudied through simulation methods.

In order to solve for the steady state, the parameter values describingtastes (b, A) and technology (h, d, k, c, rs) must be stipulated. In accordancewith RBC methodology, these were chosen (i.e., calibrated) so that the im-plied steady-state behavior of the artificial economy was similar to the long-run characteristics of the Fairmodel data. Specifically, labor’s share of GNPaveraged 63% in the Fairmodel output implying a value for h of 0.37. Inaddition, agents spent roughly 22% of their time in work activity; this impliesa value for A of 3. The autocorrelation of ln kt and the standard deviationof the residual, rs, were determined by studying the time-series propertiesof the Solow production residual defined as

ln Z � ln y � 0.37 ln k � 0.63 ln h . (3)t t t t

The series ln Zt was linearly detrended and ln kt was defined as the deviationsfrom trend. Assuming the AR(1) process in Equation (2) for this constructedseries produced estimates for c of 0.91 and rs of 0.005. As in virtually allRBC models, the remaining two parameters, b and d, were assumed to be0.99 and 0.025, respectively.6

With these parameter values, the RBC model was used to generateartificial time series. The sample length was assumed to be 2000 observationsin order to minimize spurious behavior of the random technology shock.Since the model implies all series are stationary (and without trend), theartificial data was not detrended. The sample variances and covariances fromthe artificial economy are reported in Table 3.

6Together with h, the parameters b and d determine the steady-state capital output ratio.The implied ratio is roughly 12 (with GNP measured as a quarterly flow) which is consistentwith U.S. data.

Calibration and Real Business Cycle Models

9

TABLE 3. Sample Moments from Fairmodel and Calibrated RBC Model

Variable

Fairmodel

rx rx/ry r(x, y)

RBC model

rx rx/ry r(x, y)

y 0.020 1.00 1.00 0.022 1.00 1.00c 0.013 0.65 0.79 0.013 0.59 0.80i 0.072 3.60 0.93 0.060 2.73 0.93n 0.016 0.80 0.96 0.011 0.50 0.84

It is clear from Table 3 that the calibrated RBC model duplicates quiteclosely the behavior of the Fairmodel as reflected in the reported samplemoments. In addition to the cross-correlations and volatilities relative toGNP, the RBC model also matches the absolute variances of output andconsumption. Based on the success of the calibration exercise it is likely thata RBC theorist, if presented with data from the Fairmodel, would incorrectlyconclude that a stochastic growth model accurately describes the structureof the economy. This potential error, however, is not necessarily a criticismof RBC models and the calibration methodology but, instead, should beinterpreted as a demonstration of observational equivalence. That is, theprevious section showed that the Fairmodel can duplicate the variances andcorrelations of U.S. aggregate time series; and it is well known that RBCmodels exhibit this property as well. Hence, this calibration exercise illus-trates the consistency of these two models. Given this illustration, we arenow ready to engage in the primary test of this paper.

4. The Range of the Real Business Cycle Model

The Fairmodel is now modified in order to generate time series withdifferent characteristics (as reflected in the moments reported in Table 3)than that of U.S. data. The calibration methodology is then used to examinewhether a standard real business cycle model, calibrated to this new data,can produce similar second moments. While this exercise directly tests therange of second moments that a calibrated RBC model can produce, thetest is clearly limited in scope: the RBC model we employ is relatively simpleand only one set of parameter changes in the Fairmodel is studied. Fromthis perspective, our analysis is best viewed as is an illustrative inquiry intothe calibration approach rather than a thorough test; indeed, the alteredparameters were chosen specifically for this purpose.7 That is, we sought

7We examined several different modifications (e.g., changing the parameter which governs

James Hartley, Kevin Salyer and Steven Sheffrin

10

modifications to the Fairmodel that not only produced the desired variationsin model output but also represented a thought experiment familiar to ma-croeconomists; at the same time, we wished to highlight the discriminatingaspects of the calibration methodology.

To generate the new artificial economy, we changed the value of twoimportant coefficients in the Fairmodel. These parameters were chosen inorder to exploit the Keynesian monetary transmission mechanism within theeconomy. This aspect of the model is similar to a textbook IS-LM frameworkin which the real consequences from a change in the money supply dependscritically on the interest rate response induced by the money shock (i.e., theslope of the LM curve) and the corresponding reaction of investment de-mand (the slope of the IS curve). In light of this structure, we dramaticallyincreased the interest rate elasticity of households’ money demand (Equa-tion [9] in the Fairmodel). Specifically, the interest rate coefficient waschanged from �0.0033 to �0.09, a roughly 30-fold increase.8 As a conse-quence of this change, interest rate fluctuations due to variations in themoney supply are greatly reduced. In order to produce fluctuations in in-vestment demand even though interest rates exhibit low volatility, we in-creased the coefficient on interest rates that enters into the demand forconsumer durables (Equation [3]). (The sum of consumer durables, firminvestment, and residential housing is defined as investment). Specifically,this coefficient was changed from �0.0037 to �0.1.9 Within an IS-LMframework, these changes imply a flattening of both the LM and IS curves.

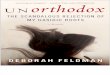

In order to illustrate the impact that these modifications have on equi-librium behavior, some impulse response functions are presented in Figure1. These are constructed in the following manner: the money stock initiallyis assumed to follow its historical path over the sample period (68:iv–77:iv).Under this restriction, the original (denoted FM1) and modified (denotedFM2) Fairmodels are used to generate a forecast for the endogenous vari-

the responsiveness of the price level to output changes) but none produced much variation inthe moments reported in Table 3. This clearly does not imply that the Fairmodel is insensitiveto parameter variation but reflects the limited data characteristics we studied. Our focus on therelative volatilities and contemporaneous correlations of model output is fairly standard in RBCanalysis.

8A change in the interest rate coefficient requires a corresponding change in the equation’sintercept term so that the forecast errors remain centered on zero. If this is not done, theconstructed forecast confounds cyclical behavior with a transition path. The intercept term inEquation (9) was changed, therefore, from 0.0767 to 0.48. We thank Ray Fair for bringing thisissue to our attention; our ignoring it in an earlier draft resulted in our misinterpreting equilib-rium dynamics.

9As noted in the previous footnote, the constant term must also be changed so that the forecasterrors from the model are centered around zero. The constant in Equation (3) was changedfrom �0.000315 to 0.61.

Calibration and Real Business Cycle Models

11

Figure 1.Impulse Response Functions: Original and High Interest Rate Elasticity Models

(1% Change in M1 in 1970:i)

James Hartley, Kevin Salyer and Steven Sheffrin

12

TABLE 4. Sample Moments from Modified (High Interest RateElasticity) Fairmodel and Calibrated RBC Model

Variable

Fairmodel

rx rx/ry r(x, y)

RBC model

rx rx/ry r(x, y)

y 0.019 1.00 1.00 0.022 1.00 1.00c 0.002 0.11 0.51 0.013 0.59 0.80i 0.061 3.21 0.87 0.060 2.73 0.93n 0.018 0.95 0.87 0.011 0.50 0.84

ables. The model is then solved under the assumption that M1 follows thesame path except for an increase of 1% in the first quarter of 1970. Takingthe difference between the forecasts produces the desired impulse responsefunctions. The three graphs in Figure 1 present these impulse responsefunctions from the two economies for a key interest rate (top panel), con-sumption (middle panel), and investment (lower panel). The effects of theincreased interest rate elasticities are fairly dramatic—in the original econ-omy the money shock results in a significant fall in interest rates while in-terest rates are almost constant in the modified economy. This difference isreflected in the behavior of consumption (which is affected by interest ratechanges through implied capital gains) and investment. The greater interestrate elasticity of investment in the modified economy is illustrated in thethird panel. This is reflected in the fact that the investment response due toa money shock is much greater than the interest rate effect. The left-handcolumns of Table 4 present the now familiar set of sample moments that aregenerated from solving the modified Fairmodel. And it is clear from thenumbers that consumption in the new economy is extremely stable; this isreflected in the fact that the standard deviation of consumption is only 11%as large as GNP volatility.

In order for the output from a calibrated RBC model to produce rela-tive volatilities like that observed in the modified Fairmodel, the calibrationexercise must generate different parameter values for the RBC model. How-ever, while the greater interest rate elasticities in the modified economyresult in different equilibrium dynamics, they do not affect the type of equi-librium behavior measured by the RBC parameters. In particular, labor’sshare in the modified economy is still roughly 63% (implying a constant valuefor h of 0.37) and the fraction of time spent in work activity is still about21% so that the parameter A is unchanged. By assumption (b, d) are constantso the only parameters remaining are those describing the stochastic processfor the shock. But again, constructing the Solow residual and analyzing the

Calibration and Real Business Cycle Models

13

TABLE 5. Postwar Volatilities of Consumption and Investment andCorrelations with Output

Country (rc/ry) (ri/ry) r(c, y) r(i, y)

Japan 1.25 2.01 0.65 0.61Norway 2.90 5.50 0.76 0.42Sweden 1.17 2.10 0.52 0.55U.S. 0.65 2.60 0.82 0.88

serial correlation properties of the detrended series shows that the autocor-relation parameter is virtually unchanged (c � 0.92 in the modified economyrather than the original value of 0.91). As a consequence, the relative vola-tilities from a RBC model calibrated to the high interest rate elastic Fair-model output would not mimic that economy but instead generate samplemoments virtually identical to the original calibrated model. For this reason,the moments reported in Table 4 for the RBC model are the same as thosein Table 3.10

This exercise demonstrates that the calibration methodology placesimportant restrictions on the parameter choices for an RBC model; more-over these restrictions imply a limited set of equilibrium characteristicswhich can be duplicated by the calibrated model. A substantial body of re-search has established consistency between the time series characteristics ofthe U.S. economy and the RBC approach. It remains to be seen, however,whether the broad range of volatilities and correlations seen in internationaldata can be produced within this framework. This diversity was reported byBackus and Kehoe (1992); some of their statistics are reproduced below inTable 5 (taken from their Table 3, p. 875).

The low volatility of consumption and highly procyclical nature of con-sumption and investment in the U.S. are clearly not seen in the other coun-tries. Since, as noted above, these features are precisely those which aregenerated within the RBC framework, its ability to match international datais suspect. That is, the properties of the model are determined entirely by

10It is important to note that the method of choosing the parameter values (the calibrationof the model) that we employ is standard; most real business cycle theorists presented with ourdata would choose roughly the same values. This consistency is ensured by the requirementthat the computed steady state of the model replicates the sample averages of key economicvariables; i.e., the steady state of the model mimics the long-run features of the data. For themodel studied here, the sample averages of labor’s share of output, the return on capital, thefraction of time spent working, and the capital-output ratio uniquely determine the preferenceparameters (b, A) and the technology parameters (d, h).

James Hartley, Kevin Salyer and Steven Sheffrin

14

the values of the parameters describing tastes (b, A) and technology (h, d,c, re). Internationally, the time spent working (which determines A) andcapital’s share (h), while different, do not vary dramatically. It is also difficultto justify wide ranges in the rate of depreciation of capital (d). Hence, thevalues for the remaining parameters, i.e., those which describe the autocor-relation (c) and volatility (re) of the technology shock are critical in differ-entiating the equilibrium characteristics across nations. With respect to therelative volatilities of consumption, investment, and output, the most crucialparameter is the autocorrelation of the technology shock. In order to gen-erate greater volatility in consumption (relative to income) than observed inU.S. data, the shock must be significantly less autocorrelated than what isobserved in the U.S. due to the implied income and substitution effects.Recently, Backus, Kehoe, and Kydland (1992) measured this autocorrelationparameter (for a constructed aggregate of European output) to be 0.90 (re-call that the value used for our analysis was 0.91). Hence, while more em-pirical research in this area is necessary, we conclude tentatively that theinternational relevance of the standard RBC approach is questionable.

5. Conclusion

The purpose of this research was to assess the quality of the evidenceoffered in support of real business cycle analysis. This evidence takes theform of a comparison between the second moments implied by an artificialeconomy and those observed in the data; consequently, our assessment wasfrom two different perspectives. We first asked whether a Keynesian artificialeconomy can duplicate the variances and covariances observed in the U.S.economy. Not surprisingly, using the Fairmodel as the artificial economy,we demonstrated that it did. We then calibrated a RBC model to the outputfrom two versions of the Fair model and checked for consistency in termsof the absolute and relative volatilities of GNP and its components. The firstversion used to generate data was the unmodified (i.e., estimated) Fair-model; upon calibrating a growth model to this data set we concluded thatthe RBC model could indeed replicate the volatilities of consumption andinvestment relative to output produced within the Fairmodel. We then mod-ified the Fairmodel so that the resulting output did not have the same char-acteristics as observed in actual data. Calibrating the RBC model to this dataset led to significant inconsistencies.

We are left with the question we started with: Do these results enhanceor diminish one’s confidence in RBC models? While it is premature to an-swer this question definitively, it appears that the permanent income frame-work and implicit intertemporal prices that constitute the core structure ofstandard RBC models do impose fairly stringent restrictions on the prop-

Calibration and Real Business Cycle Models

15

erties of equilibrium. This feature has positive as well as negative aspects.On the one hand, it insures that real business cycle models are not purechameleons—that is, they cannot mimic any model. On the other hand, itmeans that it may be difficult to match the full range of moments and cor-relations from industrialized economies as presented by Backus and Kehoe(1992).

Received: November 1994Final version: February 1996

References

Altug, Sumru. “Time-to-Build and Aggregate Fluctuations: Some New Evi-dence.” International Economic Review 30 (November 1989): 889–920.

Backus, David K., and Patrick J. Kehoe. “International Evidence on theHistorical Properties of Business Cycles.” The American Economic Re-view 82 (1992): 864–88.

Backus, David K., Patrick J. Kehoe, and Finn Kydland. “International RealBusiness Cycles.” Journal of Political Economy 100 (August 1992): 745–75.

Benhabib, Jess, Richard Rogerson, and Randall Wright. “Homework in Mac-roeconomics: Household Production and Aggregate Fluctuations.” Jour-nal of Political Economy 99 (December 1991): 1166–87.

Bollen, Kenneth A. Structural Equations with Latent Variables. New York:John Wiley & Sons, 1989.

Canova, Fabio, Mary Finn, and Adrian Pagan. “Evaluating a Real BusinessCycle Model” In Nonstationary Time Series Analysis and Cointegration,edited by C. Hargreaves. Oxford: Oxford University Press, 1992.

Christiano, Lawrence J., and Martin Eichenbaum. “Current Real-BusinessCycle Theories and Aggregate Labor-Market Fluctuations.” AmericanEconomic Review 82 (June 1992): 430–50.

Fair, Ray C. Fairmodel User’s Guide and Intermediate Workbook. South-borough, Massachusetts: Macro Incorporated, 1990.

Testing Macroeconomic Models. Cambridge, MA: Harvard University Press,1994.

Hansen, Gary D. “Indivisible Labor and the Business Cycle.” Journal ofMonetary Economics 16 (November 1985): 309–28.

Hansen, Gary D., and Randall Wright. “The Labor Market in Real BusinessCycle Theory.” Federal Reserve Bank of Minneapolis Quarterly Review(Spring 1992): 2–12.

Hoover, Kevin D. “Fact and Artifacts: Calibration and the Empirical As-

James Hartley, Kevin Salyer and Steven Sheffrin

16

sessment of Real-Business Cycle Models.” Oxford Economic Papers 47(1995): 24–44.

King, Robert G., Charles Plosser, and Sergio Rebelo. “Production Growthand Business Cycles I: The Basic Neoclassical Model.” Journal of Mon-etary Economics 21 (March/May 1988): 195–232.

Kydland, Finn, and Edward C. Prescott. “Business Cycles: Real Facts and aMonetary Myth.” Federal Reserve Bank of Minneapolis Quarterly Re-view 14 (1990): 3–18.

———. “Time to Build and Aggregate Fluctuations.” Econometrica 50(1982): 1345–70.

———. “The Econometrics of the General Equilibrium Approach to Busi-ness Cycles.” Scandinavian Journal of Economics 93 (1991): 161–78.

Watson, Mark W. “Measures of Fit for Calibrated Models.” Journal of Po-litical Economy 101 (1993): 1011–41.

Data Appendix

All of the data used in this paper was that provided with the Fairmodel.For further information, consult the FAIRMODEL User’s Guide.

The following variables from the Fairmodel were used in oursimulations:

CN � Real consumer expenditures for nondurable goods.CD � Real consumer expenditures for durable goods.

COG � Federal government purchases of goods (Fiscal policyvariable).

CS � Real consumer expenditures for services.GNPD � GNP deflator.

GNP � Nominal gross national product.GNPR � Real gross national product.

HF � Nonresidential fixed investment by firms.IHH � Residential investment by households.IKF � Nonresidential fixed investment by firms.

JF � Number of jobs in the business sector.M1 � Money supply, end of quarter (Monetary policy variable).

POP � Noninstitutional population over 16 years old.PROD � Output per paid for worker hour.

WF � Average hourly earnings excluding overtime of workers inbusiness sector.

The above variables were used to generate the following:

Calibration and Real Business Cycle Models

17

Consumption (C) � ln((CN � CS)/POP)Hours (N) � ln((JF*HF)/POP)

Investment (I) � ln((IKF � IHH � CD)/POP)Real Output (Y) � ln(GNPR/POP)