Embed Size (px)

Citation preview

BOARD OF DIRECTORS

California Housing Finance Agency

Board of Directors

December 12, 2017

Bank of the West Tower

500 Capitol Mall

Conference Center, 18th Floor

Sacramento, California

(916) 326-8000 (CalHFA Receptionist)

10:00 a.m.

1. Roll Call.

2. Chairman/Executive Director comments.

3. Approval of the minutes of the October 12, 2017 Board of Directors meeting..............................01

4. Discussion, recommendation and possible action to increase the Area Median Income (AMI) for

Single Family Program eligibility to 150% in all counties and to adopt a single household size

adjustment, Resolution No. 17-24 (Tim Hsu) ................................................................................04

5. Discussion, recommendation, and possible action regarding the adoption of a resolution

enacting the Agency’s bond issuance and compliance monitoring policies as required by the

California Debt Limit Allocation Committee, Resolution No. 17-25 (Michael Carroll) ..............11

6. Reports:

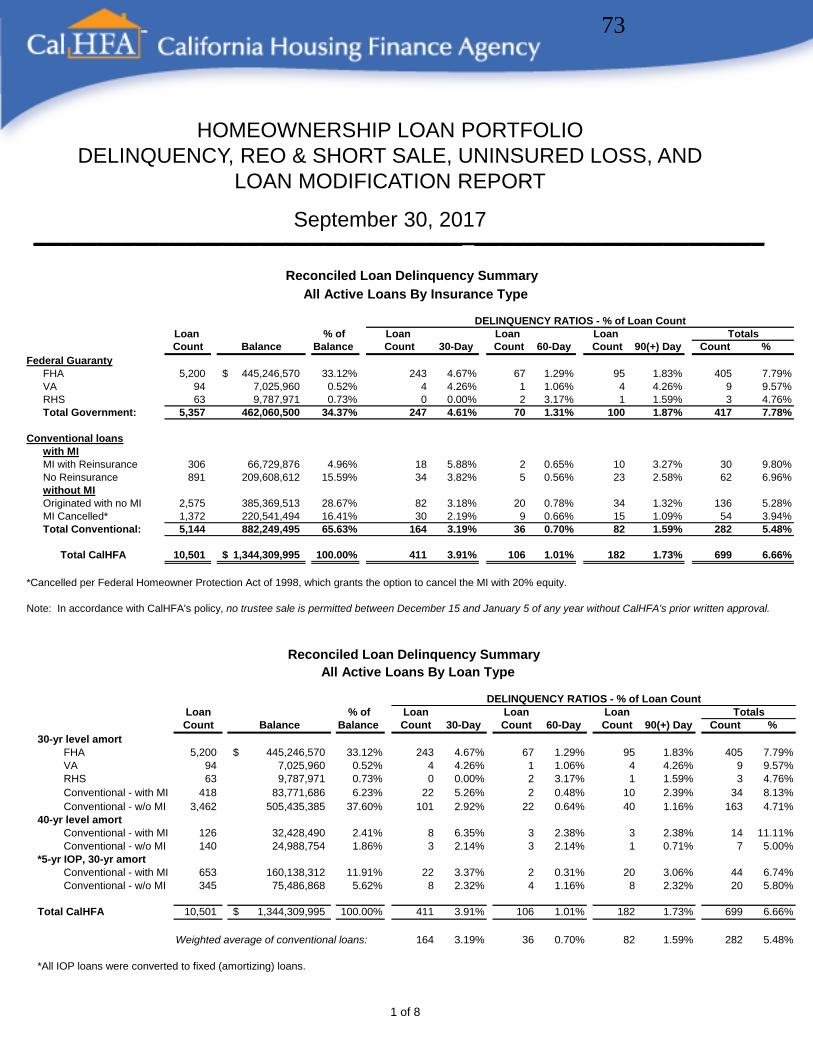

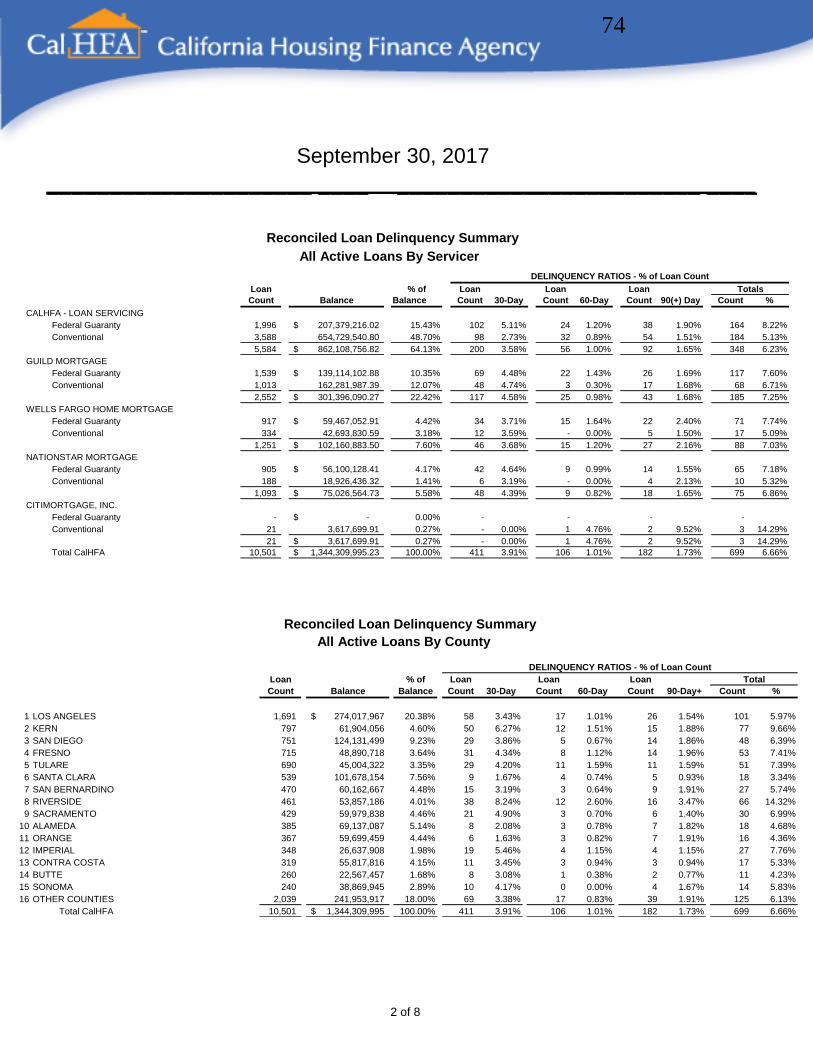

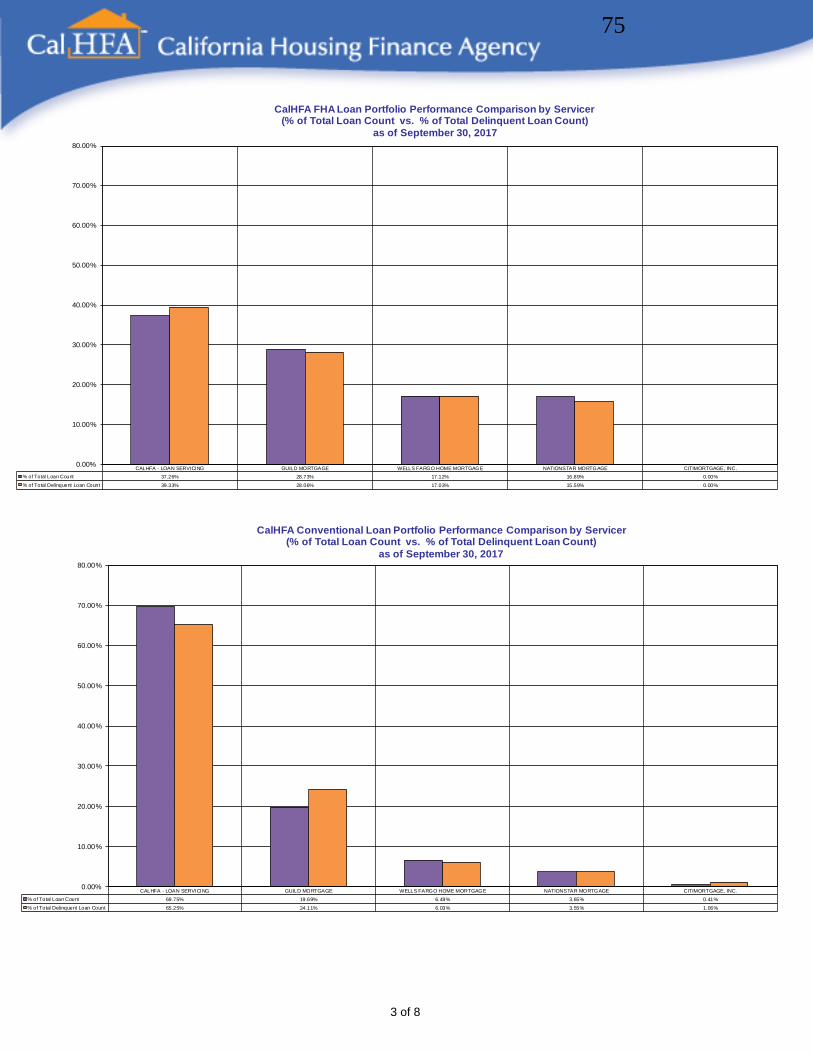

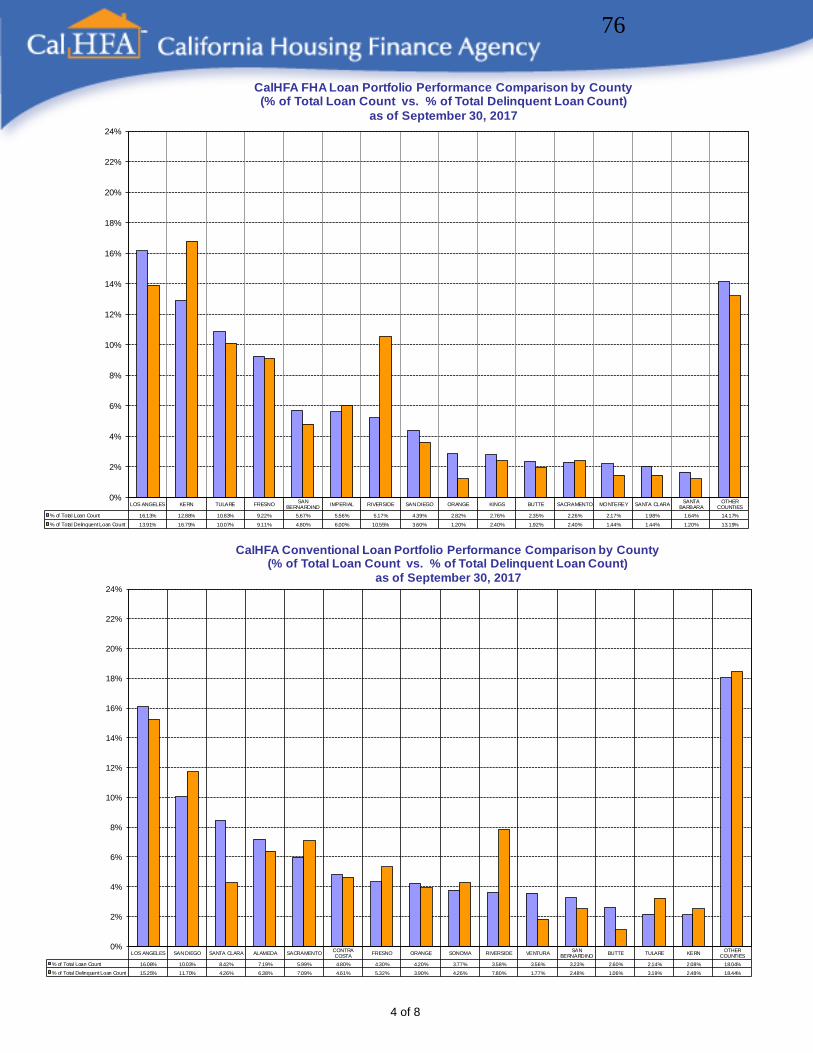

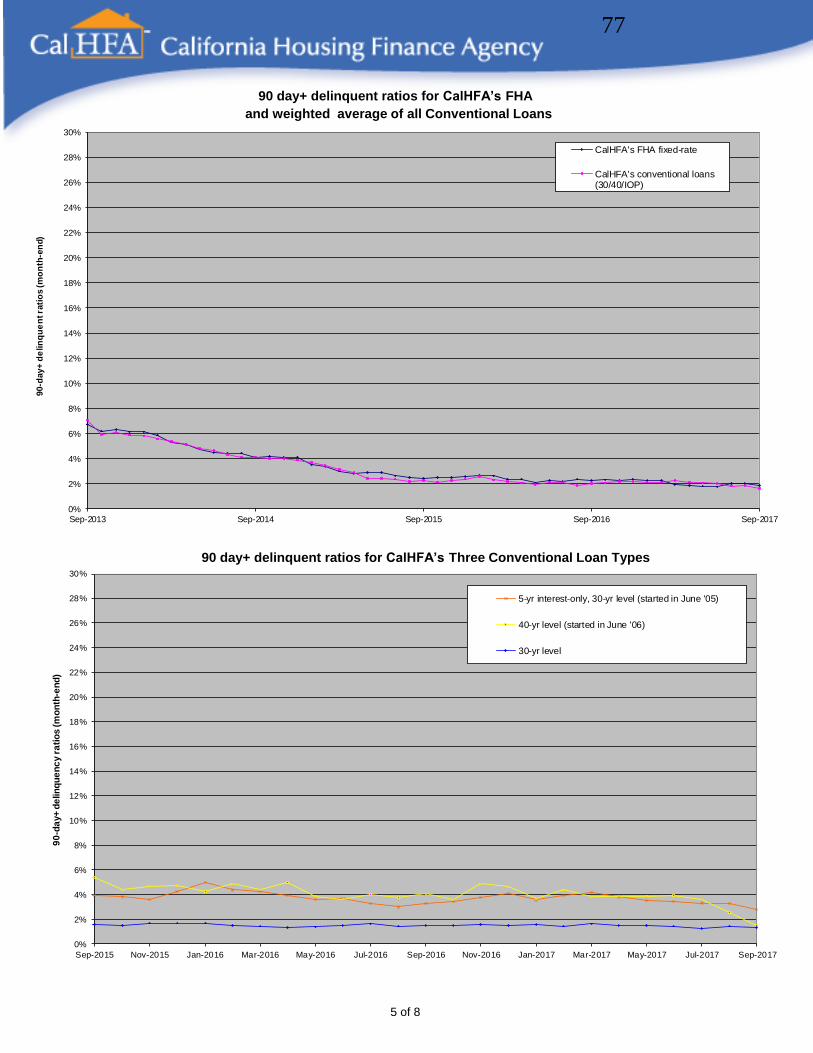

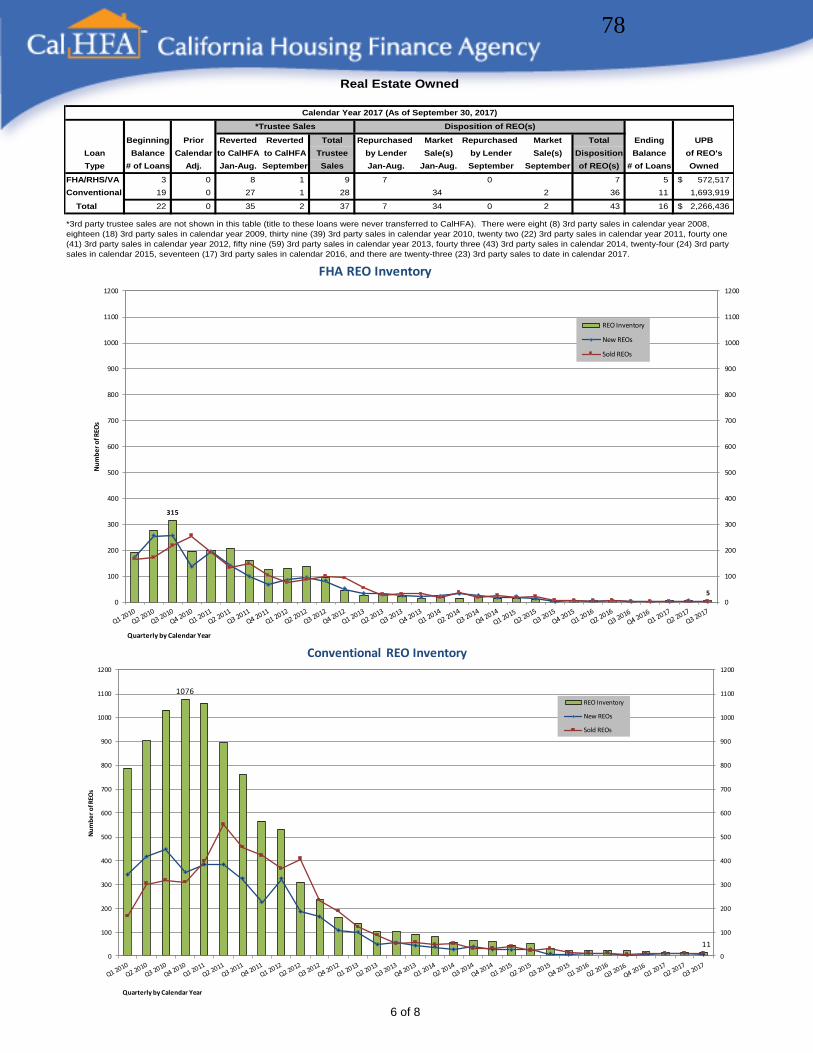

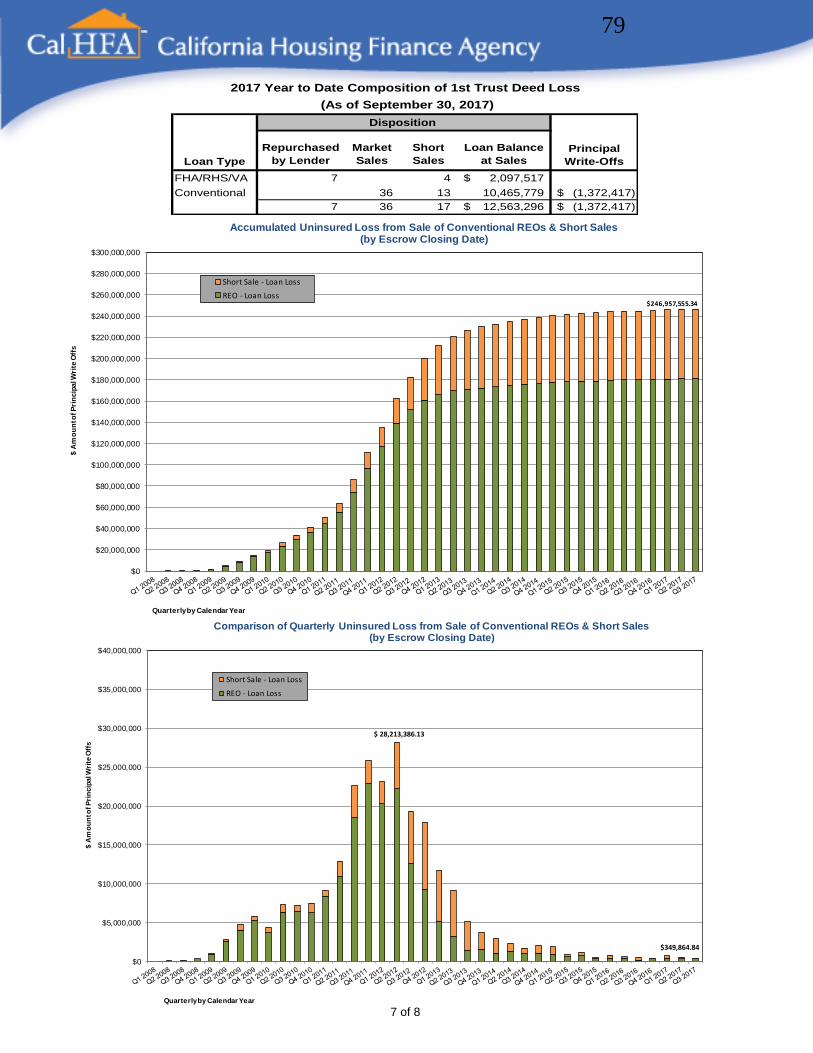

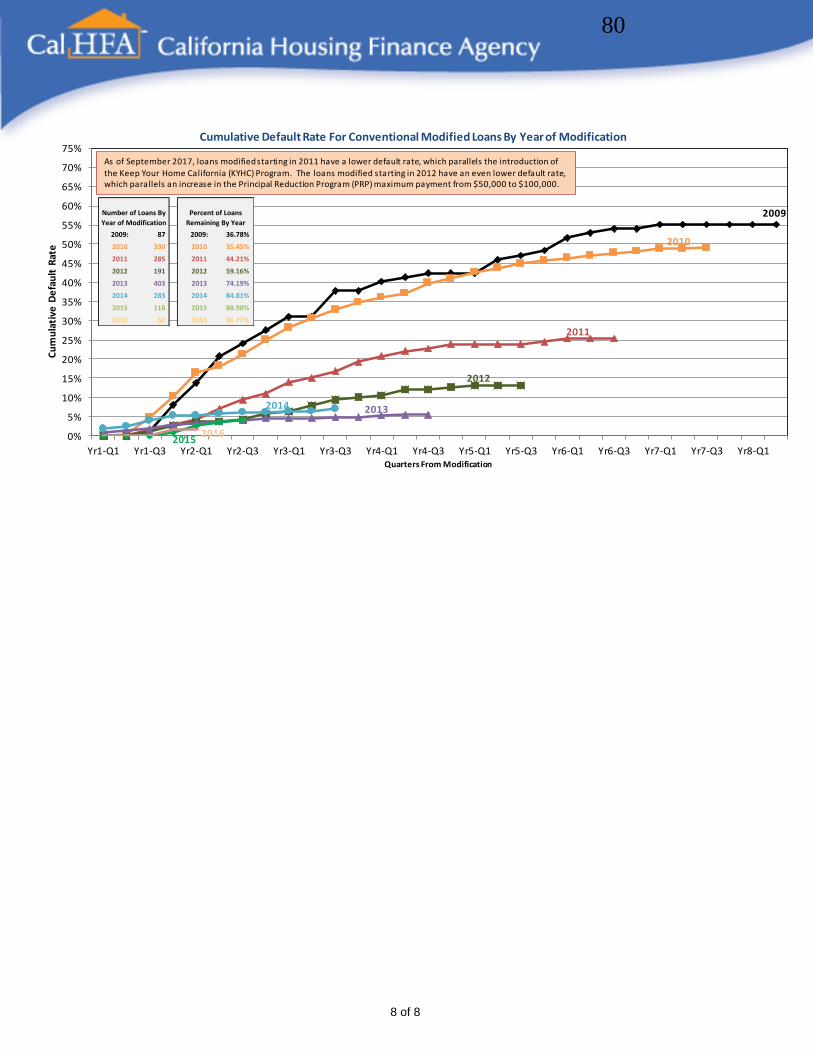

A. Homeownership Loan Portfolio Update ...................................................................................72

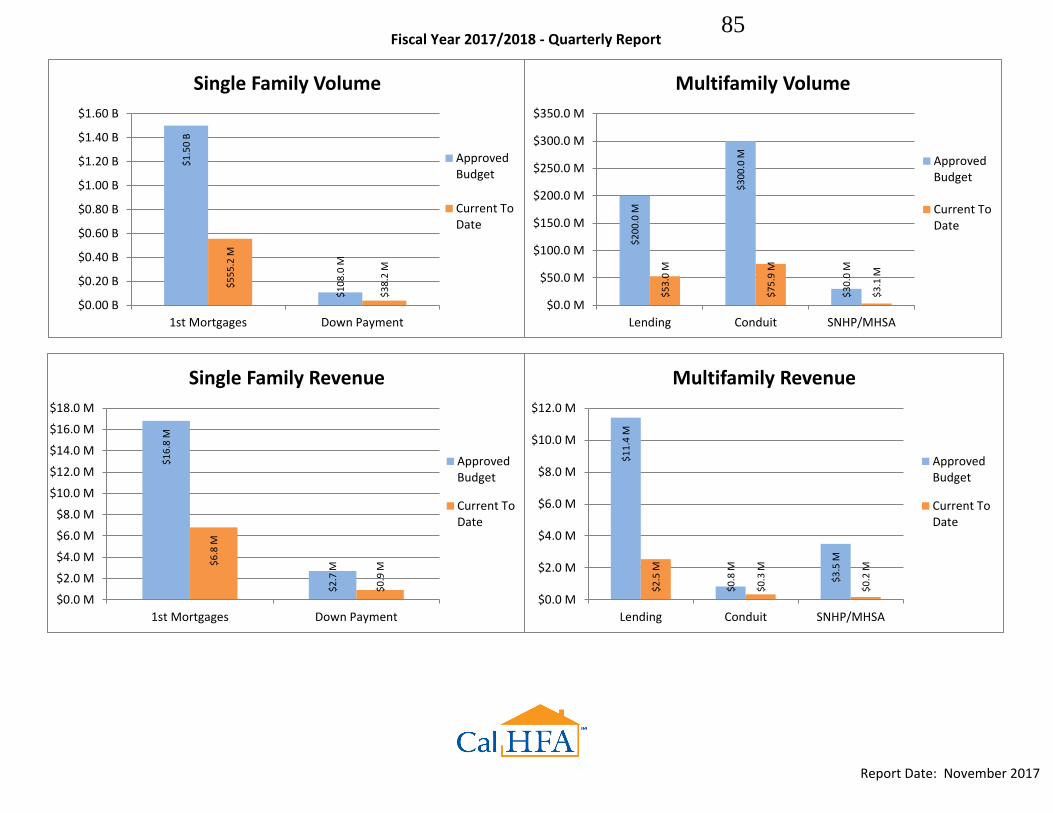

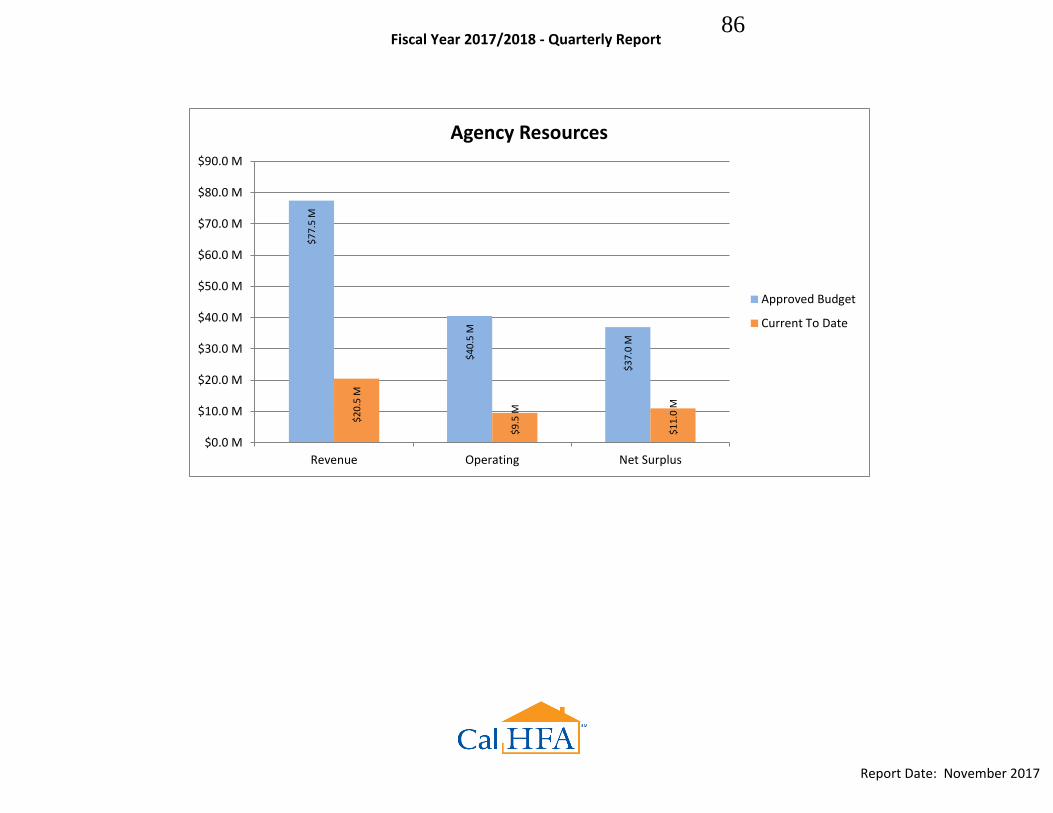

B. 2017-18 Quarterly Report .........................................................................................................81

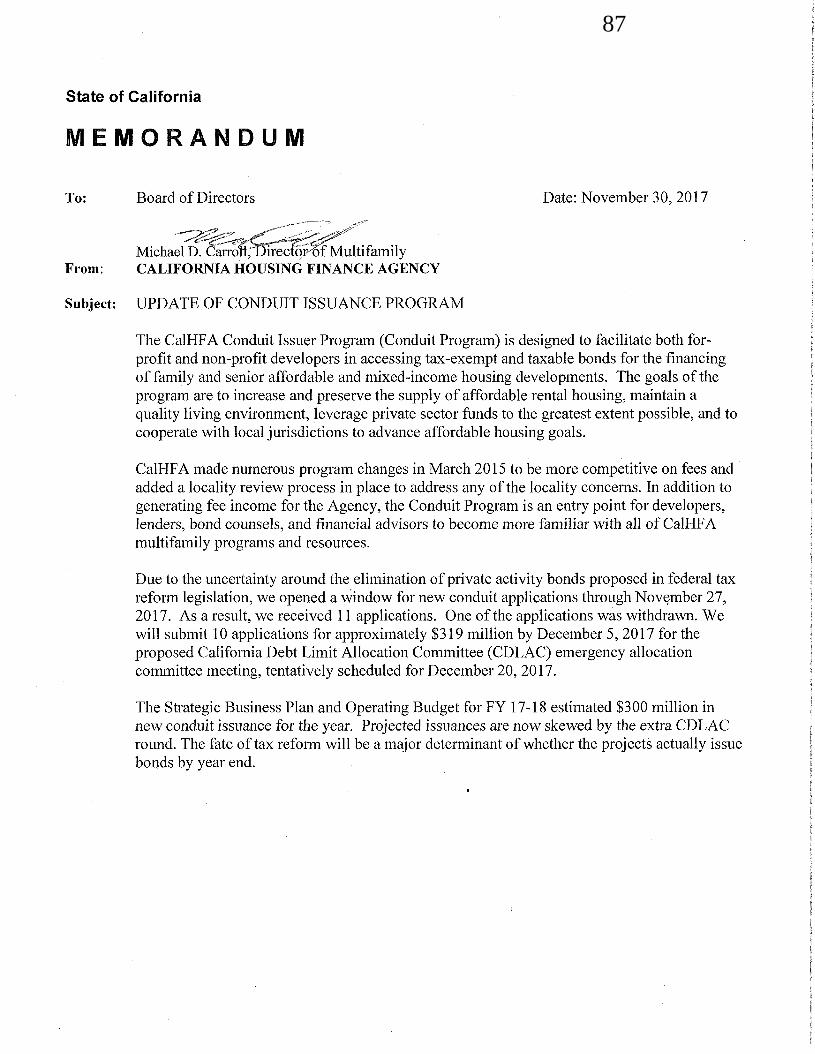

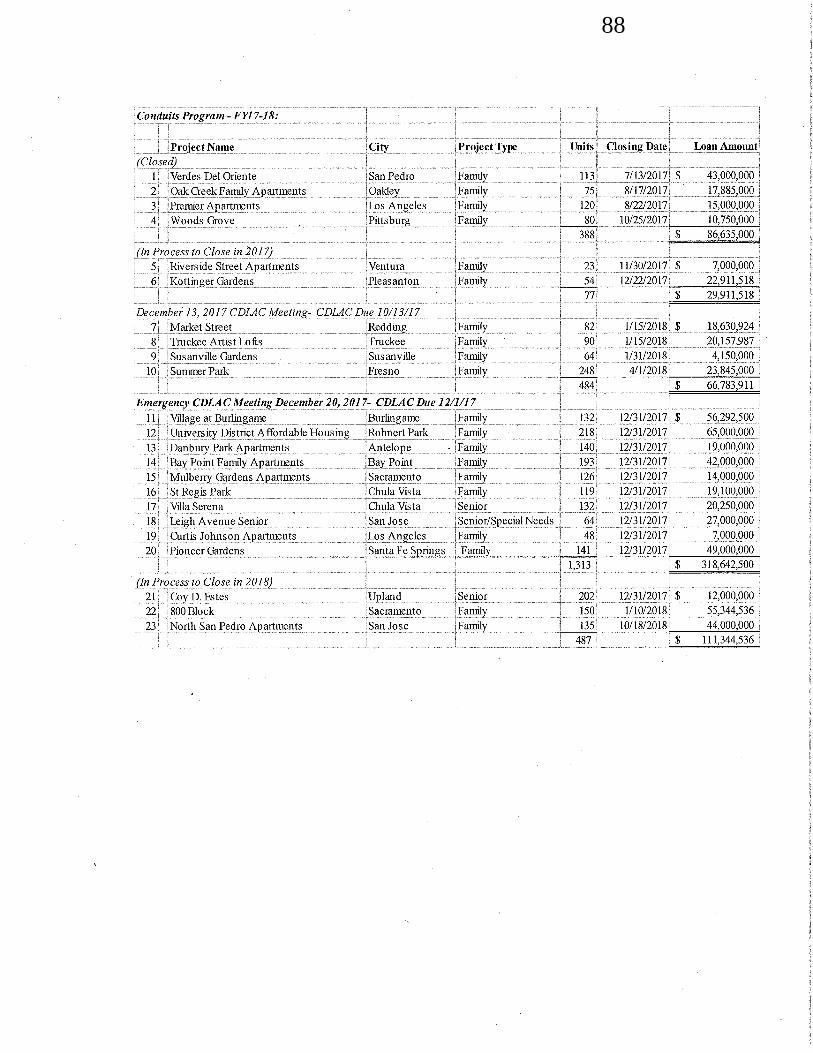

C. Conduit Issuance Program Update ............................................................................................87

D. Final Report of the 2017 Legislative Session ...........................................................................89

7. Discussion of other Board matters.

8. Public testimony: Discussion only of other matters to be brought to the Board’s attention.

(NEXT)

9. Adjournment.

10. Handouts.

NOTES**

PARKING: Public parking at Bank of the West

Tower – Entrance at 5th and N Streets. Public parking:

1) Bank of the West Parking structure ($1.75 per 20 minutes,

$18 maximum); 2) Street parking available via meter ranging

from 2 hours to 10 hours; 3) Other nearby parking structures.

REFRESHMENTS: Available for purchase at Specialty’s

Café in the lobby.

FUTURE MEETING DATE: Next CalHFA Board

of Directors Meeting will be January 16, 2018, location

TBA.

10/12/17 Board Minutes

1

MINUTES

California Housing Finance Agency (CalHFA)

Board of Directors Meeting

October 12, 2017

Meeting noticed on September 29, 2017

1. ROLL CALL

The California Housing Finance Agency Board meeting was called to order at 10:01 a.m. by

Acting Chair Gunning. A quorum of members was present.

MEMBERS PRESENT: Avila Farias, Brown (for Chiang), Gunn (for Imbasciani),

Gunning, Johnson-Hall, Ortega (for Cohen), Prince, Sotelo,

Russell, von Koch-Liebert (for Podesta), Boatman Patterson.

MEMBERS ARRIVING Gallagher, Metcalf.

AFTER ROLL CALL:

MEMBERS ABSENT: Alex, Falk, Hunter.

STAFF PRESENT: Thomas O. Freeburger, Don Cavier, Michael Carroll, Ruth Vakili,

Tony Sertich, Liane Rhodes, Melissa Flores.

2. APPROVAL OF MINUTES – September 14, 2017

The minutes were approved by unanimous consent of members present.

3. CHAIRMAN/EXECUTIVE DIRECTOR COMMENTS

Executive Director comments:

a) Reported on the passage of the Legislative Housing Package – SB2 includes an estimate of

$30-40 million annually to support Multifamily Programs low to moderate and mixed

income housing;

b) Reported that the staff appreciation picnic was held on October 11th and was brought

indoors due to the poor air quality as a result of the devastating wildfires burning in

California. She offered prayers to those impacted by the catastrophic effects of the

wildfires;

c) Reported on the achievement of Agency goals; i) replaced our federal temporary line of

credit with a private bank by December 31, 2015, ii) enhanced efficient delivery of

affordable housing through single family and multifamily lending programs, iii)

strengthened our formal collaboration with HCD to assist us in becoming a lender with a

purpose and aligned our lending activities with other state housing models;

1

10/12/17 Board Minutes

2

Prince recognized the successful accomplishments and suggested that the hard work of the staff be acknowledged by the Board. Gunning said that he would follow up on this request.

d) Announced that she will be chairing the Fannie Mae Advisory Council Meeting, of which

she is a member, on October 18, 2017 in Washington, D.C.;

e) Informed the Board that November and December Board meetings will be scheduled due to

business need.

4. REPORT OF THE CHAIR OF THE AUDIT COMMITTEE

Committee Chair Gunning reported that the Audit Committee met earlier this morning. The

Committee heard informational presentations by:

Liane Rhodes, Director of IT, reported on cyber security, security assessments and

results, oversight requirements, and current & future initiatives.

Tony Sertich, Director of Enterprise Risk Management, gave an update on the

implementation of the new Enterprise Risk Management unit. Committee Chair Gunning

asked that the Audit committee in their Agency oversight role work closely with Tony

and his unit.

BUSINESS ITEMS:

5. Final Loan Commitment for Kottinger Gardens Phase 2, No. 17-016-A/N for 54 Units

located in Pleasanton/Alameda – Resolution No. 17-23.

Presented by Carroll and Vakili.

On a motion by Sotelo, the Board approved staff recommendation for Resolution 17-23. The

votes were as follows:

AYES: Avila Farias, Brown (for Chiang), Gallagher, Gunn (for Imbasciani), Gunning,

Johnson-Hall, Metcalf, Prince, Sotelo, Russell, von Koch-Liebert (for Podesta).

NOES: None.

ABSTAIN: None.

ABSENT: Falk, Hunter.

6. DISCUSSION OF OTHER BOARD MATTERS

None.

2

10/12/17 Board Minutes

3

7. PUBLIC TESTIMONY: DISCUSSION ONLY OF OTHER MATTERS TO BE

BROUGHT TO THE BOARD’S ATTENTION

None.

8. ADJOURNMENT

As there was no further business to be conducted, Acting Chair Gunning adjourned the meeting

at 10:33 a.m.

___________________________________

3

1

State of California

M E M O R A N D U M To: Board of Directors Date: December 12, 2017

TIM HSU, Acting Director of Single Family Lending

From: California Housing Finance Agency

Subject: RECOMMENDATION FOR CHANGING INCOME LIMITS CALCULATION ON CALHFA

MORTGAGE PRODUCTS

Recommendations:

In an effort to more closely align income limit calculations with existing housing authority law and recent

statutory changes to more efficiently serve individuals and families seeking homeownership in California

when using Single Family Lending’s TBA financing model, CalHFA staff recommends the Board formally

adopt the following income limit calculations on all CalHFA non-Mortgage Revenue Bond (MRB) mortgage

products:

(1) High Cost Areas. Increase CalHFA’s income limits to 150% of the area median

income (AMI) in all 58 California counties; and

(2) Household Size Adjustment. Adopt a single household size adjustment factor of

8, regardless of actual household size.

Note: Though CalHFA Single Family Lending is currently not using MRB financing for its lending products,

CalHFA would need to follow federal MRB income limit guidelines if or when MRBs are utilized by CalHFA

Single Family Lending in the future.

Background – High Cost Areas:

The California Housing Finance Agency’s legislation authorizes CalHFA to finance loans to persons and

families of low and moderate income. California Health and Safety Code (HSC) section 50093 defines

moderate income as income not exceeding 120% of AMI, adjusted for family size.

HSC section 50093 further authorizes CalHFA, jointly with HCD, or with the concurrence of the Secretary of

the Business, Consumer Services and Housing Agency, to use higher income limits in designated geographic

areas of the state, upon a determination that the 120% of the median income in the particular geographic areas

is too low to qualify a substantial number of persons and families of low or moderate income who can

otherwise afford a home purchase financed by CalHFA.

Previously, a 2015 Legislative Analyst Office report entitled “California’s High Housing Costs – Causes and

Consequences” (LAO Report) found that even California’s least expensive housing markets are about or more

expensive than the U.S. average.1 Accordingly, CalHFA designated 35 counties as “high cost” pursuant to

1 https://www.acgov.org/cda/hcd/documents/lao_report-on-high-housing-costs2015.pdf

4

2

CalHFA Board Resolution 16-02 and began calculating moderate income as income not exceeding 140% of

AMI.

More recently, the California Association of Realtors’ (CAR) 2017 – Q3 market data showed that California’s

First Time Buyer Housing Affordability Index (FTB-HAI)2 has dropped almost 10% over the last 33 months

since CalHFA adopted the 140% AMI limit for the current 35 high costs counties. In other words, almost

20,000 of California’s 200,000 first time homebuyer population that were potentially eligible for their first

home in 2015 can no longer afford the median sale priced home in their county.3

Recommendation Assessment – High Cost Areas:

CalHFA staff has determined that the 140% AMI limit remains too low a figure to qualify a substantial

number of persons and families of moderate income in those 35 designated counties, much less the remaining

23 counties using 120% of AMI, and believes home prices in all communities throughout California are

higher than what the median income household can afford. Under this standard, all counties in California

could be designated “high cost.”

The LAO Report further recommended, among other things, to put all policy options on the table to address

California’s high housing costs. Accordingly, CalHFA staff recommends that the Board increase CalHFA’s

income limits to 150% of AMI in all 58 California counties because current income limits remain too low to

qualify a substantial number of persons and families of low or moderate income who can otherwise afford a

home purchase financed by CalHFA and to align with the income limits established under existing California

housing authority law as well as the recently enacted 2017 Building Homes and Jobs Act (SB 2; HSC section

50470(b)(2)(D)(ii)).4

Background – Household Size Adjustment:

In further response to the LAO Report’s recommendation to put all policy options on the table, CalHFA staff

also recommends changing the manner in which income limits are adjusted based upon household size.

As previously discussed, borrowers must not exceed the limit of what is considered moderate income in a

particular county to be eligible for a CalHFA single-family mortgage product. CalHFA relies upon HCD’s

published figures for establishing California’s moderate income limit levels. HCD sets the maximum

moderate income limit to equal 120% of the county’s AMI. After calculating the 4-person AMI limit for a

particular county, income limits are adjusted for household size so that larger households have higher income

2 http://www.car.org/marketdata/data/ftbhai/ 3 https://fred.stlouisfed.org/series/CAHOWN 4 While the county median income in some California counties might not be higher than the national average,

the LAO Report makes clear that there are other significant financial impediments to owning a home in

California, regardless of location, including the fact that the overall home ownership rate in California is at a

30 year low. For those reasons and the sake of efficiency, CalHFA staff is recommending all counties move

to 150% AMI.

5

3

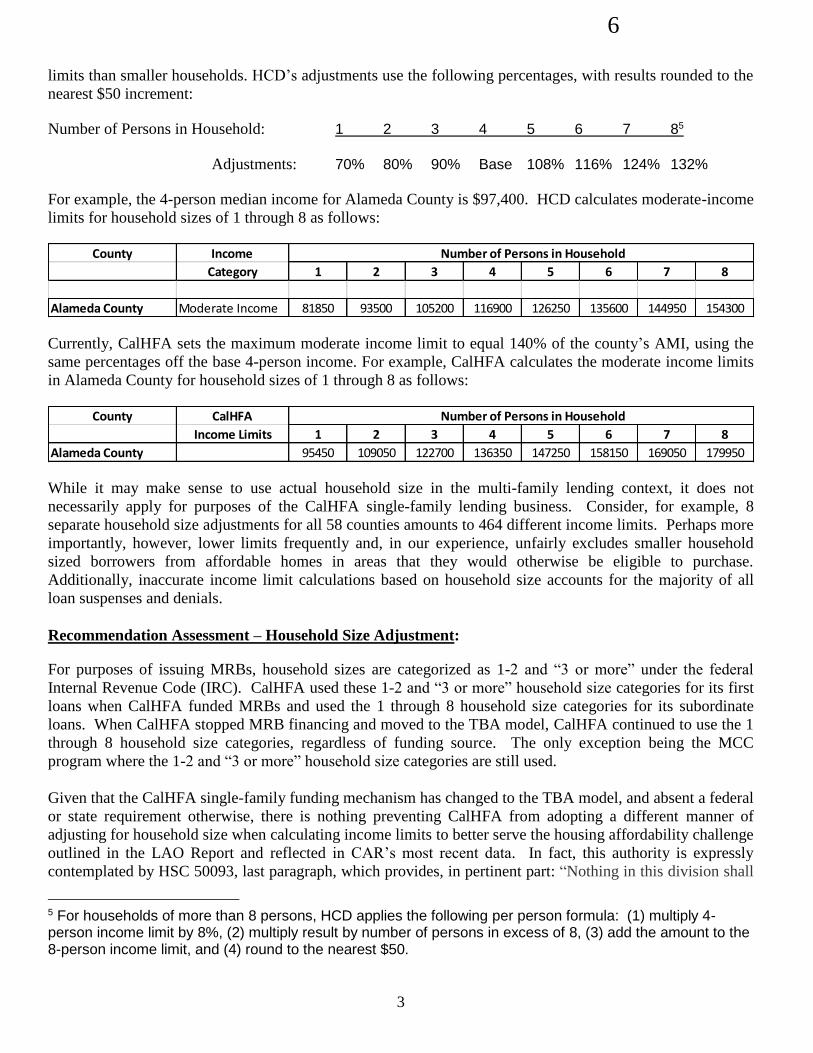

limits than smaller households. HCD’s adjustments use the following percentages, with results rounded to the

nearest $50 increment:

Number of Persons in Household: 1 2 3 4 5 6 7 85

Adjustments: 70% 80% 90% Base 108% 116% 124% 132%

For example, the 4-person median income for Alameda County is $97,400. HCD calculates moderate-income

limits for household sizes of 1 through 8 as follows:

Currently, CalHFA sets the maximum moderate income limit to equal 140% of the county’s AMI, using the

same percentages off the base 4-person income. For example, CalHFA calculates the moderate income limits

in Alameda County for household sizes of 1 through 8 as follows:

While it may make sense to use actual household size in the multi-family lending context, it does not

necessarily apply for purposes of the CalHFA single-family lending business. Consider, for example, 8

separate household size adjustments for all 58 counties amounts to 464 different income limits. Perhaps more

importantly, however, lower limits frequently and, in our experience, unfairly excludes smaller household

sized borrowers from affordable homes in areas that they would otherwise be eligible to purchase.

Additionally, inaccurate income limit calculations based on household size accounts for the majority of all

loan suspenses and denials.

Recommendation Assessment – Household Size Adjustment:

For purposes of issuing MRBs, household sizes are categorized as 1-2 and “3 or more” under the federal

Internal Revenue Code (IRC). CalHFA used these 1-2 and “3 or more” household size categories for its first

loans when CalHFA funded MRBs and used the 1 through 8 household size categories for its subordinate

loans. When CalHFA stopped MRB financing and moved to the TBA model, CalHFA continued to use the 1

through 8 household size categories, regardless of funding source. The only exception being the MCC

program where the 1-2 and “3 or more” household size categories are still used.

Given that the CalHFA single-family funding mechanism has changed to the TBA model, and absent a federal

or state requirement otherwise, there is nothing preventing CalHFA from adopting a different manner of

adjusting for household size when calculating income limits to better serve the housing affordability challenge

outlined in the LAO Report and reflected in CAR’s most recent data. In fact, this authority is expressly

contemplated by HSC 50093, last paragraph, which provides, in pertinent part: “Nothing in this division shall

5 For households of more than 8 persons, HCD applies the following per person formula: (1) multiply 4-person income limit by 8%, (2) multiply result by number of persons in excess of 8, (3) add the amount to the 8-person income limit, and (4) round to the nearest $50.

County Income Number of Persons in Household

Category 1 2 3 4 5 6 7 8

Alameda County Moderate Income 81850 93500 105200 116900 126250 135600 144950 154300

County CalHFA Number of Persons in Household

Income Limits 1 2 3 4 5 6 7 8

Alameda County 95450 109050 122700 136350 147250 158150 169050 179950

6

4

prevent the agency or the department from adopting separate family size adjustment factors or programmatic

definitions of income to qualify households, persons, and families for programs of the agency or department,

as the case may be.” A fact acknowledged by HCD’s “State Income Limits for 2017” which provides, in

pertinent part: “Applicability of these State Income Limits is subject to particular programs as program

definitions of such factors as income, family, and household size, etc. vary…” Of course, if there were a

federal statutory (i.e., MCC) or programmatic requirement to adjust for household size, CalHFA would have

to comply.

Additional research by CalHFA also has shown other state HFAs have adopted the use of one single income

limit, regardless of actual household size, when they are utilizing TBA financing. CalHFA staff believes a

single household size of 8 for all single-family loan products not otherwise required by a federal law or

program, regardless of actual household size, should be used because it is more inclusive for all eligible first-

time homebuyers.6

6 With respect to households of over 8 persons, an analysis of the origination history since relaunching the

single-family lending business in 2013 shows that only 9 loans out of over 27,700 reservations actually

needed household income in excess of 8 persons in order to qualify.

7

-1-

BOARD OF DIRECTORS 1

OF THE CALIFORNIA HOUSING FINANCE AGENCY 2

3

RESOLUTION NO. 17-24 4

5

RESOLUTION SUPPORTING INCREASED INCOME LIMITS AND OTHER 6

CHANGES FOR HOMEOWNERSHIP PROGRAMS IN CALIFORNIA 7

8

WHEREAS, the California Housing Finance Agency (the “Agency”) has 9

determined that there exists a need in California for providing financial assistance to persons and 10

families of low or moderate income to enable them to purchase moderately priced single family 11

residences; 12

13

WHEREAS, the Agency has determined that it is in the public interest for the 14

Agency to provide such financial assistance by means of ongoing programs (collectively, the 15

“Homeownership Program”); 16

17

WHEREAS, pursuant to Resolution No. 16-02, the Agency made a determination 18

that in particular “high cost” geographic areas of California, the Agency’s current income limits 19

were too low to qualify a substantial number of persons or families of low or moderate income 20

and therefore subsequently modified the Homeownership Program to increase income limits in 21

those particular geographic areas of California as a means of furthering the Agency’s mission of 22

promoting housing opportunities for low to moderate income Californians; 23

24

WHEREAS, the Agency has made a new determination that the Agency’s current 25

income limits continue to remain too low to qualify a substantial number of persons or families 26

of low or moderate income in all geographic areas of California thereby prohibiting otherwise 27

qualified buyers from qualifying for the Agency’s loan products; 28

29

WHEREAS, the Secretary of Business, Consumer Services, and Housing and the 30

Director of the Department of Housing and Community Development (“HCD”) concur with the 31

Agency in the use of higher income limitations in all geographic areas of California; 32

33

WHEREAS, the Agency has historically adjusted income limits for purposes of 34

qualifying persons or families of low or moderate income based upon household size. For 35

purposes of issuing Mortgage Revenue Bonds (“MRB”), the Agency used 1-2 and “3 or more” 36

household size categories for its first loans and used one (1) through eight (8) household size 37

categories for the Agency’s subordinate loans. When the Agency stopped MRB financing and 38

moved to the TBA model, the Agency continued to use the one (1) through eight (8) household 39

size categories, regardless of funding source, so that larger households had higher income limits 40

than smaller households; 41

42

WHEREAS, in order to lower loan suspense and denial rates, and provide 43

additional homeownership opportunities to persons or families of low or moderate income with 44

smaller household sizes, the Agency staff recommended that income limits for each county in 45

California as published annually by HCD be adjusted using a single household size of eight (8) 46

in accordance with California Health and Safety Code section 50093; 47

8

-2-

WHEREAS, the Board supports this action to modify the Homeownership 1

Program to further the Agency’s mission of promoting housing opportunities for low to moderate 2

income Californians. 3

4

NOW, THEREFORE, BE IT RESOLVED by the Board of Directors (the 5

“Board”) of the California Housing Finance Agency as follows: 6

7

Section 1. Authorization to Increase Income Limits. As soon as is practicable, 8

the Agency shall increase income limits to a maximum of one hundred fifty percent (150%) of 9

the area median income in all geographic areas of California. 10

11

Section 2. Authorization to Adjust Household Size. As soon as is practicable 12

or as otherwise required by federal law, the Agency shall adjust income limits in each county of 13

California as published annually by HCD for purposes of qualifying persons or families of low 14

or moderate income for the Homeownership Program based upon a household size of eight (8), 15

regardless of the actual number of members of a household. 16

17

Section 3. Authorization to Modify Income Limits in Response to GSE and 18

other Federal Requirements. The Agency may, as necessary, in response to Government 19

Sponsored Entity or other Federal Regulatory entity, such as the Department of Housing and 20

Urban Development, modify income limits in conformance with those federal requirements. 21

22

Section 4. Authorization of Related Actions and Agreements. The officers of 23

the Agency, or the duly authorized deputies thereof, are hereby authorized and directed, jointly 24

and severally, to do any and all things and to execute and deliver any and all agreements and 25

documents which they may deem necessary or advisable in order to effectuate the purposes of 26

this resolution, including but not limited to satisfying in the best interests of the Agency. 27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

9

-3-

SECRETARY'S CERTIFICATE 1

2

I, Thomas O. Freeburger, the undersigned, do hereby certify that I am the duly 3

authorized Acting Secretary of the Board of Directors of the California Housing Finance 4

Agency, and hereby further certify that the foregoing is a full, true, and correct copy of 5

Resolution No. 17-24 duly adopted at a regular meeting of the Board of Directors of the 6

California Housing Finance Agency duly called and held on the 12th day of December 2017, at 7

which meeting all said directors had due notice, a quorum was present and that at said meeting 8

said resolution was adopted by the following vote: 9

10

AYES: 11

12

NOES: 13

14

ABSTENTIONS: 15

16

ABSENT: 17

18

IN WITNESS WHEREOF, I have executed this certificate hereto this ___th day 19

of ____________ 20___. 20

21

22

ATTEST: 23

THOMAS O. FREEBURGER 24

Acting Secretary of the Board of Directors of the 25

California Housing Finance Agency 26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

10

State of California

M E M O R A N D U M

To: Board of Directors Date: November 28, 2017

Tony Sertich, Director of Enterprise Risk Management & Compliance From: CALIFORNIA HOUSING FINANCE AGENCY

Subject: CALHFA BOND ISSUANCE & POST-ISSUANCE COMPLIANCE POLICY

On December 15, 2016, the California Debt Limit Allocation Committee (“CDLAC”) adopted

Regulation 5031(c), which requires all private activity bond Issuers to submit a Bond Issuance

and Post-Issuance Compliance Policy (“Policy”) to CDLAC by December 31, 2017. The

Policy must be approved by the Issuer’s governing Board.

CalHFA has had a bond policy and an asset management handbook for several years.

However, we have not had an overall bond issuance and compliance policy with specific focus

on CDLAC compliance. The attached policy documents our current practices, which already

align with CDLAC’s requirements.

Formal approval of the Policy is requested from the Board.

11

California Housing Finance Agency

Bond Issuance & Post-Issuance Compliance Policy

November 27, 2017

12

DEBT ISSUANCE POLICY

AUTHORITY

Authority to Issue Bonds

The California Housing Finance Agency (“Agency” or “CalHFA”) is authorized to issue Bonds

for financing housing in California pursuant to Parts 1 through 4 of Division 31 of the California

Health and Safety Code.

Single Family Bond Resolutions

Annually the Director of Financing will prepare a resolution, and obtain Board approval,

authorizing the Agency’s single family bond indentures, the issuance of single family bonds,

credit facilities for homeownership purposes, and related financial agreements and contracts for

services.

Multifamily Bond Resolutions

Annually the Director of Financing will prepare a resolution, and obtain Board approval,

authorizing the financing of the Agency’s multifamily housing program, the issuance of

multifamily bonds, the Agency’s multifamily bond indentures, credit facilities for multifamily

purposes, and related financial agreements and contracts for services.

Approval to Submit Applications to the California Debt Limit Allocation Committee

(“CDLAC”)

Annually the Director of Financing will prepare a resolution, and obtain Board approval,

authorizing the summiting of an application(s) to CDLAC for private activity bond allocations to

be used in connection with the issuance of all or a portion of Agency bonds, in order for interest

on such Bonds to be excludable from gross income for federal income tax purposes. The

Resolution states the aggregate amount authorized to be allocated for the calendar year. The

Resolution may be amended and increased during the year if demand requires additional

authority.

APPLICATION

Agency Application

The Agency will not submit applications to CDLAC for bond allocation on qualified residential

rental projects (“QRRP”) until the borrower has provided CalHFA with a complete Agency

application and full application fee. The Agency’s application includes a project description,

sources and uses, proposed project income and rent restrictions, partnership and borrower

information, and details on the entities involved in the development.

CDLAC Applications

For tax-exempt bonds, prior to the issuance of bonds, the Agency must apply for and receive an

allocation of bond issuance authority from CDLAC. To receive such an allocation the Agency

must document its readiness to issue the bonds promptly and meet other CDLAC requirements.

13

Applications for Bonds shall include evidence of a performance deposit equal to one-half of one

percent (.5%) of the allocation requested, not to exceed $100,000. In the case of a multifamily

project, such evidence may include, but is not limited to a copy of a check or certified funds from

the developer to the Agency. In the case where the application is for a single family housing

program, a copy of a general ledger statement evidencing that funds have been reserved for this

purpose, and a fully executed Performance Deposit Certification that certifies the required

deposit has been made and is being held by the Agency on the behalf of the CDLAC.

The Agency will maintain the performance deposit until a written release is received from

CDLAC. A written authorization releasing the performance deposit or refund of deposits, if paid

to CDLAC, will occur upon CDLAC’s receipt of a properly completed Report of Action. If the

financing does not close within the time allowed by CDLAC, and CDLAC requires that the

deposit be forfeited, then the deposit will be remitted to or retained by CDLAC.

Tax Equity and Fiscal Responsibility Act (“TEFRA”) Hearing

When the Agency proposes to issue Single Family or Multifamily Bonds, Federal tax law (in

order for the interest on the bonds to be tax-exempt) imposes a requirement that a public hearing

be held by which the Treasurer of the State of California will approve the Bond issue. Public

notice of the hearing must be published at least two weeks prior to the hearing. The TEFRA

Hearing purpose is to allow interested persons an opportunity to express their views for or

against the issuance of the Bonds. Information (dates and times) of the Agency’s scheduled

TEFRA hearings are posted on the Agency’s webpage. (www.calhfa.ca.gov) TEFRA hearings

are conducted in the Agency’s Sacramento offices.

Request for Proposals for Advice and Recommendations (“RFP”)

The Agency will periodically post to its website a RFP to notify all interested and qualified

investment banking firms, brokers, dealers, and financial services entities that it wishes them to

provide advice and recommendations in connection with a municipal financial product and/or the

issuance of municipal securities.

Derivative Financial Products (“Hedges”)

The Agency may enter into Hedges in connection with management of the Agency’s Single

Family and Multifamily loan commitments. The Agency’s Executive Director and Director of

Financing are authorized to enter into Hedges consistent with the Agency’s normal management

process. The Hedges allow the Agency to mitigate the risk of its exposure to movements in

interest rates as part of managing the Agency’s programs.

The circumstances where Hedges may be used, the methods and guidelines to be employed when

Hedges are used and the management and reporting responsibilities of staff and others is set-

fourth in the Agency’s Board Approved Master Hedge Policy. (See Exhibit #1)

14

BOND CHARACTERISTICS

Types of Bonds

The Board approved Single Family and Multifamily resolutions give the Agency its authority to

issue debt pursuant to Parts 1 through 4 of Division 31 of the California Health and Safety Code.

The Agency may issue either tax-exempt or taxable bonds. Tax-exempt bonds require an

allocation of bond authority from CDLAC. Taxable bonds are not exempt from federal taxation,

therefore, do not require an allocation of bond authority from CDLAC. If a bond is a tax-exempt

refunding bond, the bond may require an allocation of bond authority from CDLAC.

Negotiated Sales, Private Placements, and Bonds Issued on Behalf of a Nongovernmental

Borrower (“Conduit Financings”).

Bonds can be either publicly sold, privately placed, or financed on behalf of a nongovernment

borrower.

Negotiated Sale

The Agency typically issues bonds via a negotiated sale. In a negotiated sale the Agency will

use a managing underwriter. The responsibilities and selection criteria of the managing

underwriter is summarized below, under the “Bond Issuance Team” section.

Privately Placed Bonds

The Agency will privately place bonds if the Executive Director and the Financing Director

determine that it would be in the best interest of the Agency. If a decision is made to do a private

placement, the Financing Director, after consulting with the Executive Director will appoint an

underwriter/placement agent. The placement agent acts as agent for the Agency in selling bonds

to a private placement purchaser, and as such does not purchase the bonds.

Conduit Financings for Nongovernmental Borrowers

The Agency is authorized to issue bonds and lend the proceeds to one or more nongovernmental

borrowers to finance Multifamily Housing, the development of which is deemed to be a public

purpose. In each case, the criteria for qualification as a borrower are derived from state

constitutional and statutory criteria, the Agency’s own policy requirements, and in the case of

federally tax-exempt bonds, federal tax requirements. Generally, the nongovernmental borrower

and any credit enhancement provided by or on its behalf, are the only sources of revenues for

repayment of the bonds. The role the nongovernmental borrower takes varies, however, in all

cases the Agency is the central figure in the financing.

15

Bond Ratings

The bonds issued under the single family and multifamily programs should generally be rated

double -A or its equivalent, with the minimum rating being single-A, or its equivalent, from at

least one of the following nationally recognized rating agencies: Moody’s Investors Service,

Standard & Poor’s Corporation or Fitch Investors Inc. Where feasible, the rating Services of

Moody’s and Standard & Poor’s should be used. The same rating requirement applies in the

case of a substitution of existing credit facility for bonds that are outstanding.

Bond ratings are not required for private placements and Conduit Financings.

Bond Authority Limitation

Currently, the Agency has authority to have outstanding bonds or notes, at any one time in the

aggregate principal amount of $13,500,000,000 excluding refunding issues and certain taxable

securities. This authority is statutory (CA Health & Safety Code 51350), and is increased as

necessary.

Interest Rate

Each financing will be structured to ensure the lowest possible cost of funds for the bonds in the

current market. This takes into account the bond interest rate, bond fees, and risk structure of the

bonds.

Bond Denominations

Typically, the Agency’s publicly offered bonds will be sold in $5,000 denominations. Most

privately placed bonds, including Conduit Financings, will be sold in $0.01 denominations. In

no case, shall the bond denominations exceed $100,000.

Credit Enhancements

For certain bonds (e.g. variable rate bonds), the preferred method of obtaining the required rating

on the bonds is through the provision of additional outside credit support for the bond issue by

rated, financially strong private institutions, such as bond insurance companies; domestic and

foreign banks and insurance companies; saving and loans, and loan-level insurance, etc. The

rating on the bonds is determined by the credit worthiness of the participating credit

enhancement provider.

Rated Bonds without Credit Enhancement

Fixed rate bonds can be issued without credit enhancement if the proposed financing structure

results in the required and desired rating on the bonds.

Liability for Repayment of Bonds

Bonds issued by the Agency are special limited obligations of the Agency, payable solely from

the revenues, assets and properties pledged under the respective indentures. The Agency has no

taxing power. The Bonds issued by the Agency do not constitute a debt or liability of the State

of California or any political subdivision thereof, other than the Agency, or a pledge of the faith

and credit of the State of California or any such political subdivision, other than the Agency.

16

Use of Bond Proceeds

The Agency uses the proceeds of single family mortgage revenue bonds to assist low to

moderate income homebuyers in California purchase a home and multifamily bond proceeds to

provide acquisition/rehabilitation and permanent financing to preserve, improve, maintain and

increase the affordability of rental housing for very low, low, and moderate income families in

California.

No more than five percent (5%) of the net bond proceeds may be used for private business use or

trade or business activity unrelated to the Agency’s purpose. In addition no proceeds of the

bonds will be used to finance or refinance any airplane, skybox or other private luxury box,

health club facility, facilities primarily used for gambling or any store the principal business of

which is the sale of alcoholic beverages for consumption.

FEES

Cost of Issuance (“COI”)

The COI of Bonds financed with proceeds of such Bonds (including premium and transferred

proceeds allocable to the bonds), shall not exceed two percent (2%) of the proceeds of the

obligations. On Conduit Financings, the borrower is responsible for paying the entire COI.

Application Fees

The Agency’s application fees are outlined in each program’s term sheet. The fee is small and

covers initial administrative costs.

CDLAC Fees

For QRRP applications, the CDLAC filing fee will be paid by the borrower. The borrower will

pay for any additional fees and deposits required by CDLAC unless explicitly stated in

CalHFA’s term sheets.

Issuance Fees

Conduit Financings require an issuer fee to be paid to the Agency. The Conduit Issuer Program

Term sheet will govern the fees due to the Agency, including the Issuer Fee. (See Exhibit #2)

Administrative Fees

For Homeownership bond issuances, the Agency may, but is not required to, charge an annual

administrative fee for administering the bond programs of the Agency. The Administrative Fee

calculations for each bond program is described in the applicable indenture.

For Multifamily bond issuances where the Agency is the lender, the administrative fee will be

paid through the loan interest rate. For Conduit Financings, the Conduit Issuer Program Term

Sheet will govern the fees due to the Agency, including the Annual Administrative Fee. The

Annual Administrative Fee is priced to cover the Agency’s cost of monitoring the property. (See

Exhibit #2)

17

BOND ISSUANCE TEAM

The Bond offering process is a coordinated effort among various professionals. If it is

determined by the Agency’s Executive Director and Director of Financing that there is a need to

issue either multifamily or single family debt (“Transaction”) a Financing Team is established, to

develop offering documents, prepare for information for rating agencies, market the bonds to

investors, price the bonds and close the Transaction. The team members vary depending on the

type and complexity of the Transaction.

Appointment of a Transaction Manager

The Director of Financing appoints a lead person to manage the Transaction (“Transaction

Manager”). The Transaction Manager is responsible for coordinating the efforts of the financing

team and keeping the Transaction on schedule. The Transaction Manager is also responsible for

ensuring all aspects of the financing plan have been reviewed, which includes all documents and

the financing structure.

Appointment of Bond Counsel

After consulting with the Agency’s Executive Director, the Financing Director will appoint a

Bond Counsel to the Transaction. The Bond Counsel will prepare the necessary legal documents

and provide an opinion regarding the validity of the bonds and their tax exemption. The Bond

Counsel will also provide legal advice on all relevant issues to best protect the interest of the

Agency and ensure compliance with federal and state securities law. The Bond Counsel

specifically represents the interest and concerns of the Agency in ensuring the integrity of the

bond transaction.

The Bond Counsel is to be a nationally recognized firm experienced in Public Finance Law.

Approval criteria will include the experience of the firm and staff as well as the cost of services.

Periodically, the Agency will conduct a RFP to ensure that the most qualified and cost-effective

Bond Counsel are retained.

Appointment of Bond/Disclosure Counsel

After consulting with the Agency’s Executive Director, the Financing Director will appoint a

Disclosure Counsel to the Transaction. Customarily the Disclosure Counsel is also the Bond

Counsel. The Disclosure Counsel will draft the bond financing documents including but not

limited to the indenture, the Preliminary Official Statement (“POS”), the Official Statement

(“OS”), the Tax Certificate, the Continuing Disclosure Agreement as well as other closing

documents.

Approval criteria will include the experience of the firm and staff as well as cost of services.

18

Appointment of a Managing Underwriter/Remarketer and Underwriting Syndicate/Selling Group

After consulting with the Agency’s Executive Director, the Director of Financing will appoint a

Managing/Senior underwriter (“Underwriter”) and, in most cases, an underwriting/selling team

to the Transaction. The Underwriter is to be a nationally recognized firm experienced in

underwriting mortgage revenue bond issuances. Approval criteria will include the experience of

the firm and staff, cost of services, underwriting abilities and financial qualifications and

abilities.

The Underwriter will work with the Agency in determining the financing structure and plan of

finance. The Underwriter will also review bond documents, manage the pricing process, execute

pre-sale marketing, provide preliminary pricing indications, work with the Agency to determine

how orders are filled from the bond pricing order period, execute the bond purchase agreement,

and provide proceeds at closing.

The Underwriter customarily will appoint an underwriter’s counsel to represent the underwriter’s

interests, draft the purchase contract and assist in undertaking the due diligence review.

Typically the underwriter’s counsel’s fees are paid by the Underwriter from the underwriting

expense portion of their spread.

Appointment of Bond Trustee/Paying Agent

A bank will be designated by the Agency as the custodian of funds and official representative of

bondholders. After consulting with the Agency’s Executive Director, the Director of Financing

will appoint a Bond Trustee to the transaction. In addition to acting in a fiduciary role, the

Trustee will also maintain records on behalf of the Agency to identify the registered owners of

the bonds and transmit principal and interest payments from the Agency to the bondholders. The

Trustee will also provide required notices to bondholders and protect the interests of bondholders

by monitoring compliance with covenants of the indentures. Approval criteria of the Trustee

will include the experience of the firm and staff, cost of services and financial qualifications and

abilities. The Trustee’s on-going expenses are paid from the revenues of the applicable

indenture.

The Trustee customarily will appoint a bank/trustee counsel to represent the Trustee’s interests.

Typically, the Trustee’s counsel’s fees are paid by the Agency, a component of the COI.

Appointment of Credit Rating Agency(ies)

After consulting with the Agency’s Executive Director the Director of Financing may appoint

one or more credit rating agencies to the Transaction. If the Transaction is part of a parity

indenture, the rating agency may already be determined. The rating agency will give an

independent credit quality rating to the Transaction. The rating agency is part of the Transaction

team and therefore, has access to all documents, however, once the structure is in reasonably

final form, the Underwriter will provide the rating agency with additional information, such as

cash-flow projections or other financial analysis. The rating agency will assess the credit quality

of the Bonds and assign a rating to the bond issue.

19

Underwriters and investors rely upon the credit quality judgement made by the rating agency.

Some mutual funds, institutions and investment trusts are restricted by law or by the terms of

their organizational documents to buying securities at or above specified credit ratings.

Ratings are reviewed periodically by the rating agency(ies) whether or not requested by the

Agency. Such a review may result in the upgrading or downgrading of an existing rating. To

perform such a review, the Agency will periodically provide the rating agency(ies) with financial

statements and other reports relating to the status of the Transaction.

Appointment of a Credit Enhancement Provider

If applicable (e.g. variable rate debt), after consulting with the Agency’s Executive Director, the

Director of Financing will appoint a credit enhancement provider to the Transaction.

The credit enhancement provider typically is a bank providing a Letter of Credit or a bond

insurer providing a Bond Insurance policy. The credit enhancement provider may be a savings

and loan association, a mortgage insurer, a federal agency or a private guarantor. In each case

the purpose of the credit enhancement is to provide, for a fee, additional security for the bonds

that improves the credit rating of the bonds and thereby lowers the borrowing costs to the

Agency. The Agency will make the determination to use credit enhancement when the savings

from the credit enhancement exceed the cost of the credit enhancement or where the credit

enhancement facilitates the sale of a bond issue that would not otherwise be possible.

Approval criteria of the credit enhancement provider will include the experience of the firm and

staff, as well as costs associated with providing credit enhancement.

Auditor

Typically, the auditor that is contracted to perform the Agency’s annual audit is appointed to the

Transaction team. The Auditor performs procedures (which are agreed upon by the Underwriter)

on financial data in the POS and OS and provides the Underwriter or Underwriter’s counsel with

a comfort letter. The fees associated with providing a comfort letter is customarily paid by the

Agency as a component of the COI; however, the fees associated with the comfort letter are

negotiated with the auditor’s at the time they awarded the auditing contract.

20

Disclosure Oversight Committee

The Agency has established a Disclosure Oversight Committee (the “Committee”). The

members of the committee are as follows:

Executive Director

General Counsel

Director of Financing

Director of Enterprise Risk Management and Compliance

Comptroller

Programs Administrator

Housing Finance Chief – Single Family Lending

Housing Finance Chief –Single Family Portfolio Management

Housing Finance Chief-Loan Servicing

Housing Finance Chief-Asset Management

Housing Finance Chief-Multifamily Programs

Agency’s Disclosure Representative; and

A Housing Finance Officer Representative from the Agency’s Financing Division.

The Committee may also retain and consult with outside legal counsel.

The primary responsibilities of the Committee are:

i. meet annually to review SEC Rule 15c2-12 disclosure requirements with respect to

outstanding bonds

ii. meet annually with the Financial Statement Disclosure Review Committee (the “FS

Committee”) to discuss the annual financial statement’s disclosure reporting, and

iii. meet as necessary to promote best practices regarding all Agency disclosure reporting

The Agency’s Disclosure representative, currently the Agency’s Director of Financing, is a

major participant in the preparation and review of the Agency’s Bond disclosure documents.

Financial Advisor

Typically, the Agency does not utilize the services of a Financial Advisor, but reserves the right

to appoint one to the Transaction team, if the Executive Director and the Director of Financing

deems it would be beneficial to the Agency.

Printing and Disseminating Services

Typically, the Agency uses a service to house and disseminate documents as well as print and or

provide online access of the POS and OS. Currently the Agency is utilizing Elabra to perform

these services.

21

TRANSACTION PROCESS

Preparation of an Interested Parties Distribution List

The Transaction Manager will prepare an interested parties distribution list identifying all parties

to the Transaction, their e-mail address and their telephone numbers. The distribution list will be

posted to Elabra by the Transaction Manager. The distribution list must include (but is not

limited to) the following individuals or representatives from the following areas (“Working

Group”) (the Working Group will receive notifications of all postings related to the Transaction).

Working Group

Director of Financing

Director of Enterprise Risk Management and Compliance

Transaction Manager

Financing Associate (or person responsible for document management)

Back-up Transaction Manager

Agency’s Legal Division

State of California’s Treasurer’s Office

Office of the Attorney General of the State of California

Agency’s Outside Bond Counsel

Disclosure Counsel

The Bond Trustee for the Transaction

Counsel to the Trustee

Underwriter/Manager for the Transaction

Underwriter’s Counsel

Rating Agencies

Credit Enhancement Provider (s) , if applicable

Preparation of a Timeline/Schedule

The Transaction Manager will prepare a timeline/schedule identifying when the disclosure

documents will be distributed, who will be responsible for the preparation of the draft

documents, when comments are due and when the final documents are due. The Transaction

Manager will post the timeline/schedule to Elabra.

Preparation of a Budget

The Transaction Manager will prepare a budget for the Transaction, ensuring that the total COI

does not exceed 2% of the related proceeds. The breakdown of the fees associated with each

issuance is negotiated with the Underwriter and is based on the then current industry standards.

Preparation of the POS and OS

As required by securities law, the Agency prepares a POS and OS when issuing municipal debt.

The POS is the preliminary prospectus of a bond issue. Investors use the POS as one of their

primary resources for investment decisions. After the bonds are sold and the bond structure is

finalized, the POS is updated to create the OS.

22

The Agency utilizes the services of a Bond Counsel and Disclosure Counsel to prepare the POS

and OS and to assist and advise the Agency on disclosure obligations. However, the material

accuracy of the POS and OS is the Agency’s responsibility.

Disclosure Review and Information Gathering for the POS and OS

In addition to the above mentioned working group, the Transaction Manager will identify any

additional contributors and reviewers of the POS and OS. The Transaction Manager will contact

them as soon as possible to inform them that their assistance is needed in either providing

information or reviewing information in the POS and OS and will let them know what they need

to provide/review and when the information is needed. The Transaction Manager will send out a

contributor’s memorandum. The Transaction Manager will maintain a checklist of all

individuals that were requested to contribute or review the information in the POS and OS and

follow-up with them if the Transaction Manager has not heard from them by the due date. Upon

receipt of the information the Transaction Manager will review and send the information to the

Disclosure Counsel. The Disclosure Counsel will update the POS or OS and distribute the

information to the Working Group, via Elabra.

Requirements for Offering Materials or Disclosure Documents

Customarily both the multifamily and single family POS and OS consists of two sections

(“Parts”). Part I provides information concerning the Agency’s Offered Bonds. Additional

information concerning the Agency, security for the Bonds, the Program and the Agency’s other

financing programs is contained in Part 2 of the POS and OS.

Part 1 primarily provides, but is not limited to, information concerning:

Introduction (information about the bonds being issued)

Application of Funds

Tax Matters

Litigation

Ratings

Continuing Disclosure

Underwriters

Part 1 usually contains, but is not limited to, the following appendices:

Proposed Form of Legal Opinion

Summary/Form of Continuing Disclosure Agreement

Part 2 primarily provides, but is not limited to, certain information concerning:

The Agency

Security for the Bonds

The Program

Other Programs of the Agency

Certain Investor Considerations

Summary of Certain Provisions of the General Indenture, if applicable

23

Part 2 usually contains, but is not limited to, the following appendices, if applicable (e.g. a parity

indenture):

Single Family

o Agency Audited Financial for the latest Fiscal Year End

o Bonds under the Indenture

o Counterparties

o Mortgage Loan Portfolio

o GNMA Mortgage-Backed Securities

o Fannie Mae Mortgage-Backed Securities

Multifamily

o Agency Audited Financial for the latest Fiscal Year End

o Description of Developments and loans allocable to the Offered Bonds

o Developments and loans financed by prior series of bonds

o Certain Agency financial Information and Operating Data

Conduit Disclosure Requirements

The disclosure obligations for conduit bond issuances are the responsibility of the developer.

Bond Counsel will notify the Agency if the requirements are not being met and the Agency will

take appropriate action as directed by Bond Counsel. This may include reporting the disclosure

failures to the Securities and Exchange Commission.

Review Procedures and Requirements for Financing Structure

The financing structure will be prepared by the Underwriter with input from the Agency. In

designing the structure, the Underwriter will take into consideration the Agency’s needs as well

as the needs of municipal investors. Before finalizing the financing structure, the structure will

be reviewed by the Director of Financing, the Transaction Manager and Bond Counsel.

Report of Any Significant Disclosure Issues

The Transaction Manager will report any significant disclosure issues and concerns to the

Disclosure Representative and if the Disclosure Representative believes they are material, will

convene a meeting of the Disclosure Committee. The Disclosure Committee will address the

issue and make a decision as soon as possible. The Transaction Manager will notify the Working

Group of the Disclosure Committee’s decision. The Disclosure Counsel will update the POS,

OS or other documents, if necessary, and distribute to the Working Group, via Elabra.

Due Diligence by Underwriter

The Transaction Manager will work with the Disclosure Counsel and Underwriter to set up a

formal due diligence meeting/call prior to the issuance of the POS.

Disclosure Checklist and Working Documentation

Prior to signing off on the POS the Transaction Manager will go through their checklist to make

sure that all the requested information has been updated and all comments have been addressed

and that the updates and comments have been posted to Elabra. The checklist and all supporting

documents will become part of the bond files.

24

POS – “Substantially Final” Certificate

SEC Rule 15c-2-12 requires that prior to making any offers or sales, the underwriters must

receive a certificate from the issuer stating that the POS is ‘substantially final”. Underwriter’s

Counsel prepares this certificate and submits it to the Transaction Manager. The Transaction

Manager will have the Director of Financing sign the certificate. Note that obtaining the

certificate is the underwriter’s responsibility not the Agency’s.

Approve and Distribute POS

The timeline will indicate the date in which the POS will need to be approved and distributed.

The Transaction Manager will coordinate the OS approvals. The Transaction Manager is the last

person to approve the POS and will not approve until all comments have been resolved and

posted to Elabra. The Director of Financing signs the final POS authorizing its execution and

delivery.

Ratings Affirmed

A few days prior to the date upon which the ratings need to be provided, the Transaction

Manager will contact the rating agency(ies) to ensure each has everything needed to provide a

rating on the transaction in accordance with the timeline.

Pre-Pricing Call

Typically the Underwriter, the Agency, and the State Treasurer’s Office (“STO”), the Agency’s

Agent for sale, will have a pre-pricing call in which the UW provides the Agency and the STO

with a summary of market conditions and investors responses to the transaction. At this time the

Agency and the STO will have an opportunity to ask questions and make decisions regarding

pricing.

Pricing Call

At this time the Underwriter provides a final summary of the market and preliminary sales.

During the call a verbal award is usually authorized.

Sign Purchase Contract/Deliver Good Faith Deposit

After the pricing call the purchase contract is signed, and typically the Underwriter will deliver a

Good Faith Deposit to the STO.

Distribute Draft Closing Documents

Draft closing documents are posted to Elabra for review by the Working Group.

Approve the OS

The timeline will indicate the date in which the OS will need to be approved. The Transaction

Manager will coordinate the OS approvals. The Transaction Manager is the last person to

approve and will not approve until all comments have been resolved and posted to Elabra. The

Director of Financing signs the final OS authorizing its execution and delivery.

25

Pre-Close All Bonds

The day prior to closing the transaction, a pre-close conference is scheduled, typically via a

conference call, to confirm there are no outstanding issues and all signatures for all documents

have been obtained.

Close All Bonds

On the day of closing, the Underwriter wires the bond proceeds to the STO and upon verification

of receipt of the proceeds the Bond Trustee, upon written request of the Agency, authenticates,

registers, and delivers the bonds to the purchaser and the transaction is closed.

Investment of Bond Proceeds

The bond proceeds will be invested in accordance with the Agency’s Board Approved

Investment Policy. (See Exhibit #3)

QUALIFIED RESIDENTIAL RENTAL PROJECT (“QRRP”) REQUIREMENTS

Loan Amount

There is no minimum or maximum loan amount for QRRP applicants.

Loan-to-Value (“LTV”)

The maximum LTV for the Agency’s lending programs is governed by the program term sheets.

The maximum LTV for projects that desire tax-exempt Private Activity Bonds to be issued is

100%.

Debt Service Coverage Ratio (“DCR”)

The minimum DCR for the Agency’s lending programs is governed by the program term sheets.

The minimum DCR for projects that desire tax-exempt Private Activity Bonds to be issued is

1.00.

Affordability Requirements

The Agency requires a minimum of either a) 20% of the units to be restricted to renters earning a

maximum of 50% of the county’s Area Median Income (AMI) or b) 40% of the units to be

restricted to renters earning a maximum of 60% of the county’s AMI with 10% of the units

restricted to renters earning a maximum of 50% of the county’s AMI. The rents will be

restricted to no more than 30% of the restricted AMI less the utility allowance.

Developer Fee Limitations

All developer fee limitations imposed by CDLAC will be enforced by the Agency. If the

Agency is providing any subordinate financing, the developer fee must be deferred or

contributed to match the subsidy fund amount, up to 50% of the total allowable developer fee.

Local Review

The Agency will request input from local governments prior to issuing bonds through its Conduit

Issuer Program. The feedback will be incorporated into the Senior Loan Committee approval

package.

26

Partnership Entity

The partnership entity must have a complete LP-1 filing. The partnership must be a single-asset

entity.

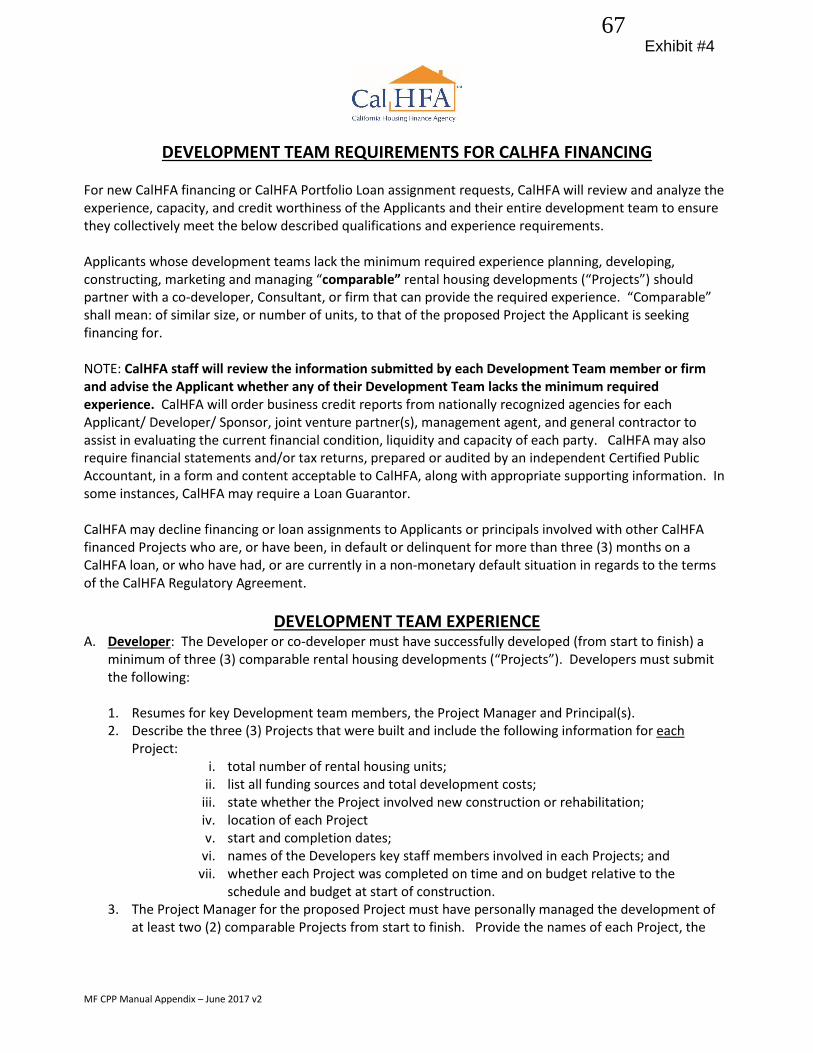

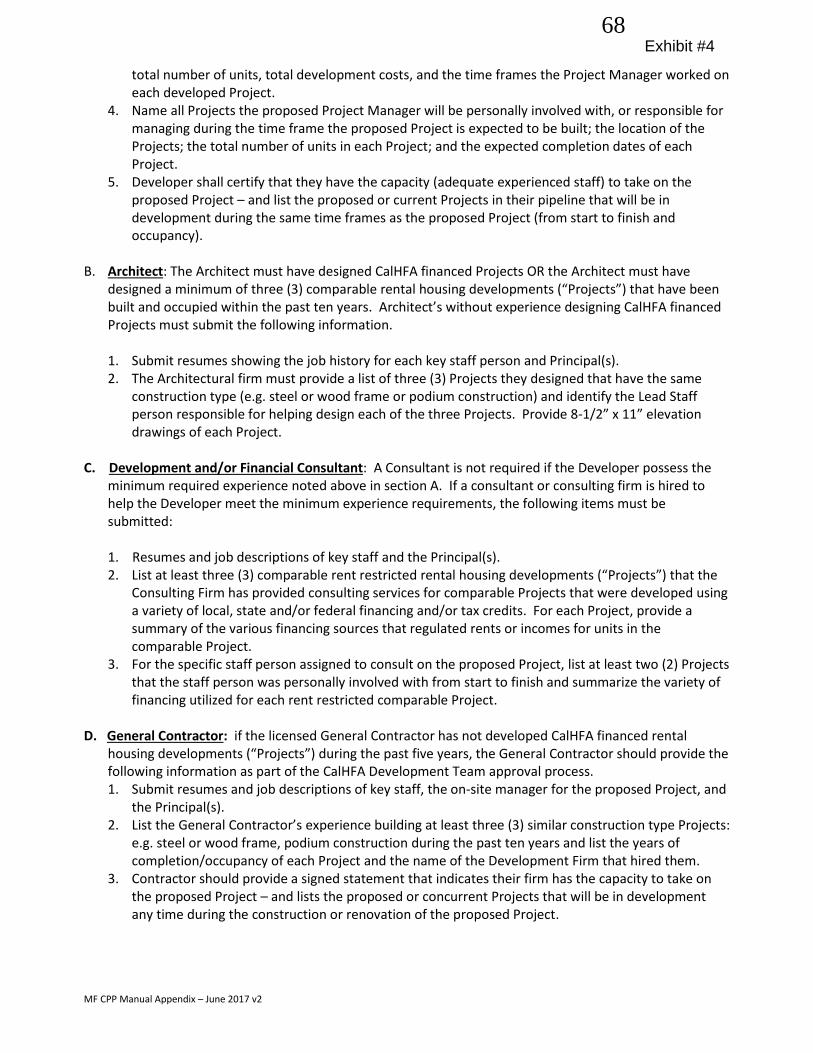

Developer Team Requirements

Each of the following members of the development team must have the required experience in

affordable housing, as detailed in the Agency’s “Development Team Requirements for CalHFA

Financing”. (See Exhibit #4)

Developer

Architect

Development and/or Financial Consultant

General Contractor

Management Company

EXCEPTIONS AND OVERSIGHT

On-Going Review

All Agency Board Approved Policies are reviewed periodically, and if material changes are

needed they will be brought to the Board for approval.

Exceptions & Waivers

An Exceptions and Waivers to this policy must be approved by Senior Loan Committee and, if

necessary, the Board of Directors. The exceptions will be noted in project approval requests

distributed prior to Senior Loan Committee and Board of Director meetings. The Board of

Directors will be notified of any exceptions that are approved by the Senior Loan Committee.

27

POST ISSUANCE COMPLIANCE POLICY

BOND POST ISSUANCE COMPLIANCE

Bond Compliance

The Agency consults with bond counsel and other legal counsel and advisors, as needed,

throughout the Bond issuance process to identify requirements and to establish procedures

necessary or appropriate so that the tax-exempt Bonds will continue to qualify for tax-exempt

status. The requirements and procedures are documented in the tax certificate and agreement

(“Tax Certificate”) and/or other documents finalized at or before issuance of the tax-exempt

Bonds. The requirements and procedures includes future compliance with applicable arbitrage

rebate requirements and certain other applicable post-issuance requirements of federal tax law

throughout (and in some cases beyond) the term of the tax-exempt Bonds.

The Agency also consults with bond counsel and other legal counsel and advisors, as needed,

following issuance of the tax-exempt Bonds to ensure that all applicable post-issuance

requirements are met. The Agency engages expert outside advisors (“Rebate Service Provider”)

or prepares in-house, the calculation of arbitrage rebate payable with respect to the investment of

Bond proceeds. Unless otherwise provided by the indenture relating to the Bonds, unexpended

Bond proceeds are held by a trustee or other financial institution, and the investment of Bond

proceeds are managed by the Agency, in accordance with the Agency’s Investment Policy. (See

Exhibit #3)

Continuing Disclosure

SEC Rule 15c-2-12 requires that underwriters participating in most bond offerings obtain from

the issuer of the bonds a written Continuing Disclosure Agreement (CDA) to provide continuing

disclosure with respect to the bonds being issued as long as they remain outstanding.

The continuing disclosure element of the Rule requires the issuer (either by itself or through a

trustee or other dissemination agent) to provide two separate disclosures:

i. Once a year, an annual financial report including the issuer’s audited financial

statements for the most recently completed fiscal year, and updating of other financial

and operating information which was included in the original official statements.

ii. Notice of the occurrence of certain material events with respect to the bonds, within ten

(10) business days of such occurrence.

The commitment to provide these continuing disclosures is set forth in detail in a Master CDA

for each indenture. The Agency’s processes and procedures for ensuring these obligations are

met is described in the Agency’s Board Approved Disclosure Policy. To ensure that these

obligations are performed timely the Agency maintains a Responsible Parties List and Timeline.

28

Conduit Continuing Disclosure Requirements

Any continuing disclosure obligations for conduit bond issuances are the responsibility of the

developer. Bond Counsel will notify the Agency if the requirements are not being met and the

Agency will take appropriate action.

Bond Document Retention Requirements

Bond documents, including tax certificates, opinions, offering statements, and other closing and

monitoring documents, will be retained for 7 years after the bonds are fully redeemed.

ARBITRAGE COMPLIANCE

Non-Purpose Investments

The Agency’s Fiscal Services Division will complete all non-purpose investment arbitrage

calculations in accordance with Internal Revenue Service (“IRS”) rules. In certain cases, these

calculations will be conducted by a qualified third party. Any excess investment earnings will be

rebated to the IRS.

Mortgage Yield Compliance

The Agency’s Financing Division will conduct all mortgage yield compliance calculations for

purpose investment arbitrage. Any excess earnings on purpose investments will either be

returned to the borrower or rebated to the IRS.

SINGLE-FAMILY COMPLIANCE

The Financing Division will annually certify to CDLAC through the online compliance

verification system that the Agency’s single-family bond allocations are in compliance with the

CDLAC resolution. This will include verifying the income targets have been met.

QRRP COMPLIANCE

CDLAC Requirements & Timing

The Agency, as the Bond Issuer, is required by CDLAC to ensure that all multifamily projects

are in compliance with CDLAC Regulations. In addition, the Agency ensures that the projects

are in compliance with the Regulatory Agreement (“RA”) requirements. The self-certification

must be submitted by the Agency to CDLAC no later than March 1 of each year.

Prior to Conversion to Permanent

The Multifamily Lending Division will collect the sponsor’s certification and report to CDLAC

through the online compliance verification system that the project is still under construction or

rehabilitation.

At Conversion to Permanent

The Multifamily Lending Division will collect verification that minimum sustainable building

standards were utilized during construction or rehabilitation. The Multifamily Lending Division

will also verify that any additional sustainable building methods required by CDLAC were met

and/or completed.

29

The project will be transferred to the Asset Management Division for all on-going compliance.

The Asset Management Division will ensure compliance with all other applicable requirements

of the CDLAC resolution.

Projects Receiving Allocation Prior to December 31, 2016

Each January, the Asset Managers (AM) will be responsible for obtaining all documents

required by CDLAC from the Sponsor in order to verify compliance with the CDLAC

Resolution.

o Project Sponsors’ Certification of Compliance I on sponsor’s letterhead

(applicable for projects awarded allocation after 2000).

o In addition, Project Sponsors are required to provide all supporting documentation

as back up to the Certificates of Compliance for services provided and income

requirements as listed on the Resolution, such as flyers, calendars of events,

service contracts, rent rolls, Tenant Income Certification (“TIC”), Project Status

Report (“PSR”) and annual Tenant Verification Lists (“TVL”).

The Agency monitor the income and rent restrictions annually, as per the requirements in

the RA, until the end of the qualified project period.

o Project Sponsors are required to provide information, via the TVL, on qualified

tenants annually no later than August 15 (with information as of June 30) via the

agency’s online Web Compliance Management System (“WCMS”).

o Copies of such certifications shall be retained in the Borrower’s files for a period

of three (3) years and shall be available for inspection by the Agency or its agents

upon request.

Audited Financial Statements submitted at the end of Sponsor’s fiscal year and reviewed

by the AM.

After the AM has received all documentation from the Sponsor, the AM will review and

then submit the Annual Applicant and Public Benefits and Ongoing Compliance Self-

Certification to CDLAC, via the online compliance certification system no later than

March 1.

The Applicant shall complete and submit the Annual Applicant Public Benefits and On-

going Compliance Self Certification, via the online compliance certification system

annually for the longer of the period the bonds remain outstanding or the period of

restriction for QRRP projects outlined in Section 5192 of the CDLAC Regulations.

Projects Receiving Allocation after December 31, 2016

Each January, the AM will be responsible for obtaining all documents required by

CDLAC from the Sponsor in order to verify compliance with the CDLAC Resolution.

o Project Sponsors’ Certification of Compliance II on sponsor’s letterhead

(applicable for projects awarded allocation after December 31, 2016).

o Certificate of Completion for Qualified Residential Rental Projects.

o In addition, Project Sponsors are required to provide all supporting documentation

as back up to the Certificates of Compliance for services provided and income

requirements as listed on the Resolution, such as flyers, calendars of events,

service contracts, rent rolls, TIC, PSR and TVL.

30

The Agency monitors the income/rent restriction annually, as per the requirements in the

RA, until the end of the qualified project period.

o Project Sponsors are required to provide information, via the TVL, on qualified

tenants annually no later than August 15 (with information as of June 30th) via

WCMS.

Copies of such certifications shall be retained in the Borrower’s files for a period of three

(3) years and shall be available for inspection by the Agency or its agents upon request.

Audited Financial Statements submitted at the end of Sponsor’s fiscal year and reviewed

by the AM.

After the AM has received all documentation from the Sponsor, the AM will review and

then complete and submit The Annual Applicant Public Benefits and On-going

Compliance Self Certification to CDLAC, via the online compliance certification system

by March 1 of every year until the termination of the Regulatory Period and/or

Compliance Period.

All Multifamily Projects

The Agency’s Inspectors conduct site inspections (every 1 to 3 years as required) of the

units and the projects’ exterior to ensure the projects are being maintained in the

standards established by State and local housing quality standards and code requirements

and the existence of any change in amenities. Once the inspection has been completed the

inspectors will send the borrower an inspection report identifying items that have failed

or are in need of repair/replacement. The borrower is required to submit a report noting

corrective actions taken to the Agency.

Change in Ownership/Management Company – The borrower is required to notify the

AM of any change in ownership, Management Company or project name. Once the AM

is notified of the change the AM will contact the borrower and request submission of the

documentation required by CDLAC and the Agency for the change.

o CDLAC form - Part V – Legal Status of Project Sponsor and Developer

(Ownership Change)

o CDLAC form - Attachment W-1 – Information on Project Sponsor (Ownership

Change)

o Organizational Chart (Ownership Change)

o CDLAC form - Attachment X – Information on Proposed Management Company

(Management Company Change)

AM will review all documentation and then complete and submit:

o All the above required CDLAC forms

o Request to Revise Resolution (completed for either a change in ownership and/or

Management Company) to CDLAC at the time of change.

31

Penalty for Non-Compliance

When there is a violation of the CalHFA Regulatory Agreement the borrower is given a

thirty (30) day notice to correct deficiency or non-compliance. If correction is not

completed CalHFA will notify other involved lenders/compliance agency of our intention

to force a cure or issue pre-NOD and or NOD if the situation warrants.

o If there is a CDLAC violation – for example, a tenant’s rental income exceeds

that allowed under the Exhibit A (CDLAC Resolution) the Sponsor is notified to

give a notice to move the resident to a unit whose rental amount conforms to

CDLAC requirement or given a notice to seek other rental accommodations.

o If there is a violation of the property’s Exhibit A (CDLAC Resolution) with

regard to amenities, then the property must provide alternative amenities (if not

actually seeking a revision of its Resolution) within a reasonable time, or reinstall

amenity.

Should the Sponsor not comply within the time provided and prior to March 1,

notification will be given to the Sponsor that they are out of compliance and notice will

be sent to CDLAC notifying of the non-compliant issue(s).

EXCEPTIONS AND OVERSIGHT

On-Going Review

All Agency Board Approved Policies are reviewed periodically, and if material changes are

needed they will be brought to the Board for approval.

Exceptions & Waivers

An Exceptions and Waivers to this policy must be approved by Senior Loan Committee and, if

necessary, the Board of Directors. The exceptions will be noted in project approval requests

distributed prior to Senior Loan Committee and Board of Director meetings. The Board of

Directors will be notified of any exceptions that approved by the Senior Loan Committee.

32

Page 1 of 10

California Housing Finance Agency

MASTER HEDGE POLICY

I. Purpose

The purpose of this Master Hedge Policy (the “Policy”) is to establish guidelines for the

use and management of various derivative financial products (“Hedges”) in conjunction

with the California Housing Finance Agency’s (“CalHFA” or the “Agency”)

management of its loan commitment pipeline.

The Policy and its contemplated Hedges are intended to cover only future hedging

activities of the Agency’s loan commitments. This policy is not intended to encompass

the Agency’s existing portfolio of interest rate swaps. This policy is not intended to

completely eliminate the Agency’s interest rate risk. For example, the Agency will

continue to bear some interest rate risk in situations where the closing of loans and/or

delivery of mortgage-backed securities precede the issuance of bonds.

The use of Hedges allows CalHFA to mitigate the risk of its exposure to movements in

interest rates as part of managing the Agency’s single family and multifamily loan

commitment pipelines. The short-term goal of the Policy is to ensure a pre-defined target

profit on loan originations. The long-term goal of the Policy is to generate a stable profit

margin range for the Agency’s lending activities.

The Policy sets forth a framework for the utilization of Hedges with particular emphasis

on their content and execution. As a framework, the intent of the Policy is to set forth

guidance while maintaining the flexibility needed to effectively use and manage Hedges

under changing market conditions.

II. Scope

The Policy describes the circumstances where Hedges may be used, the methods and

guidelines to be employed when Hedges are used and the management and reporting

responsibilities of staff and others necessary in carrying out the Policy.

III. Legal Authority

A. Authority

CalHFA may enter into Hedges in order to reduce the amount of interest rate risk.

CalHFA has statutory authority to enter into Hedge.

Exhibit #1 33

Page 2 of 10

B. Approval

CalHFA may enter into Hedges in connection with management of the Agency’s

loan commitments. The Agency’s Executive Director, Director of Financing and

Financing Risk Manager are authorized to enter into Hedges consistent with the

Agency’s normal management process.

The Policy shall govern CalHFA’s use and management of all Hedges. While

adherence to the Policy is required in applicable circumstances, the Agency

recognizes that changes in the capital markets, Agency programs, and other

unforeseen circumstances may from time to time produce situations that are not

covered by the Policy and will require modifications or exceptions to achieve

policy goals. In these cases, management flexibility is appropriate, provided the

Board is informed of any significant departures from previous practice.

The Policy shall be reviewed and updated periodically and presented to the Board

for approval. The Director of Financing is the designated administrator of the

Policy, and shall have the day-to-day responsibility and authority for structuring,

implementing, and managing Hedges.

CalHFA shall be authorized to enter into Hedges only with qualified Hedge