Embed Size (px)

Citation preview

Capability Building in Global Markets

Barcelona

8th October 2008

Motivation

• A nice way of combining product and process innovation is to introduce the concept of ‘Capability’

• This allows us to develop a key distinction between productivity and quality

• It also allows us to focus attention on the idea that much of the improvements we see in quatity (and productivity) come from innovations in working practices , rather than from R&D

Sources

• Sutton, Quality,Trade and the ‘Moving Window’, Economic Journal , Nov 2007

• Brandt, Rawski, Sutton, China’s Great Economic Transformation, Cambridge University Press 2008

• Sutton, The auto-component industry in China and India: A Benchmarking Study

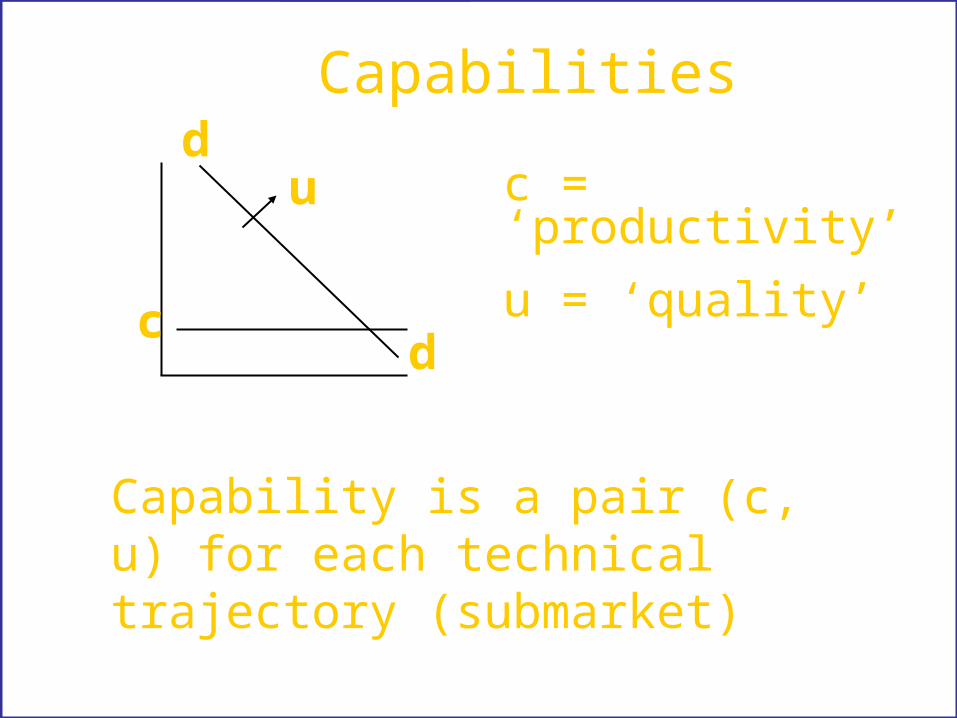

Capabilitiesd

dc

u c = ‘productivity’

u = ‘quality’

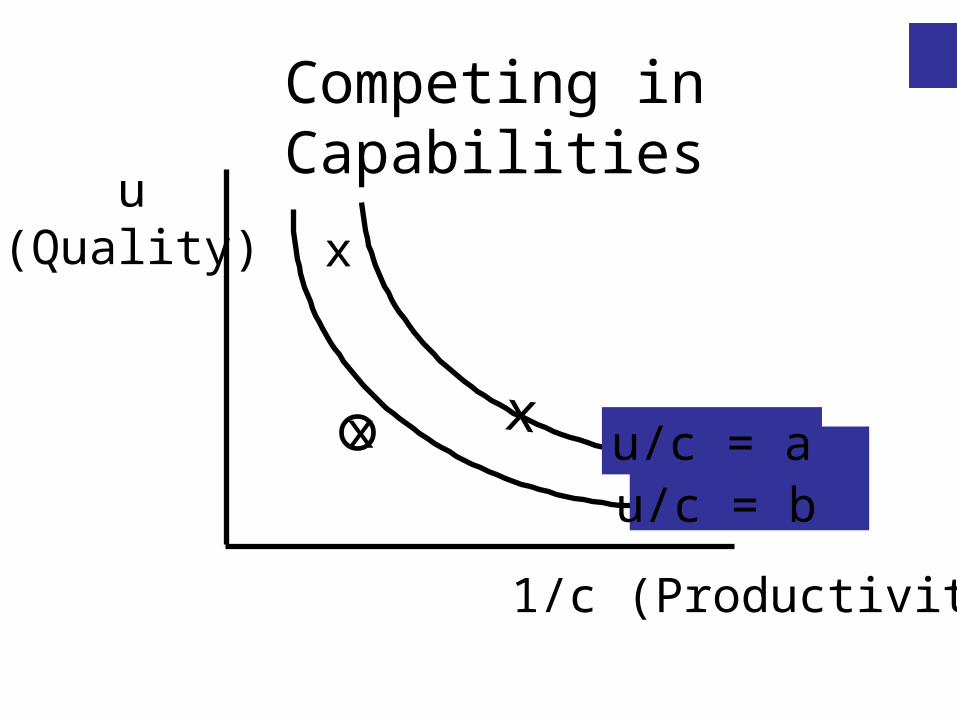

Capability is a pair (c, u) for each technical trajectory (submarket)

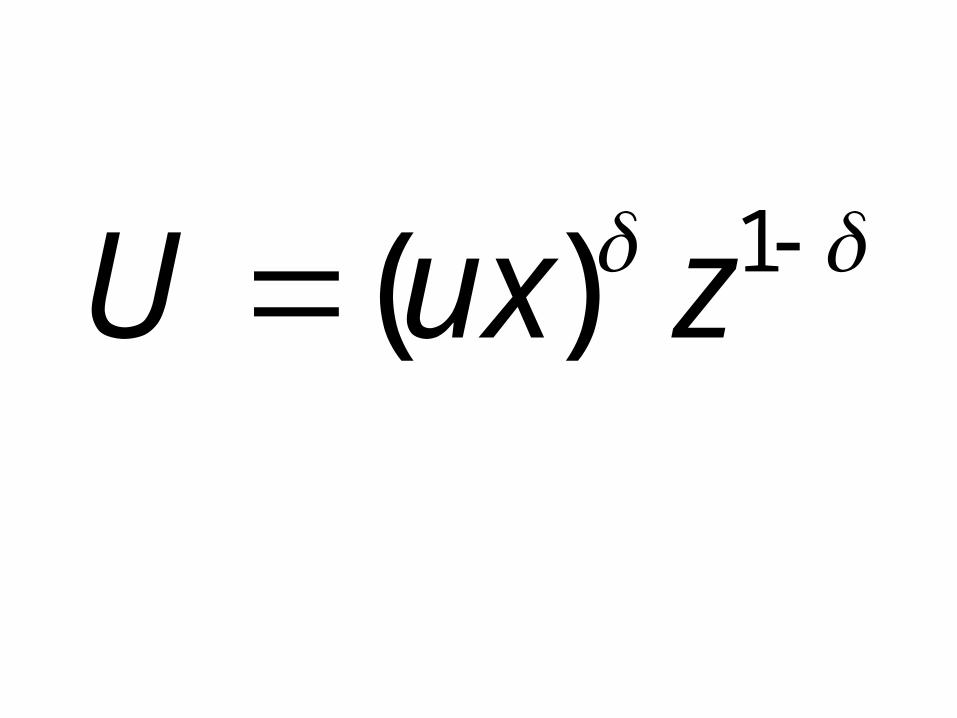

1)( zuxU

Key feature:

The consumers choose products offering the best u/p

Implication: if u>v, the market share of a firm offering u cannot be eroded to zero by any number of firms offering v

Proposition 1

- given any configuration of capabilities

(c1,u1), (c2,u2) . . (cn,un)

there is a lower bound in (c,u) space below which a firm cannot achieve positive sales at equilibrium

(ex. Cournot equilibrium)

xu

(Quality)

1/c (Productivity)

x

u/c = bu/c = ax

Competing in Capabilities

Fixed /Sunk costs

• Iso-elastic response of quality(beta)

• Isoelastic response of labour productivity (gamma)

• Unit variable cost = labour cost + materials cost

Proposition 2

Suppose one element in building capability is the expenditure of fixed outlays (“sunk costs”)

- Then competition in ‘capability building’ will lead to a bound on the number of firms ‘in the window’.

X

X

X

X

X

X

XX

X

X

XX

X

X

XX

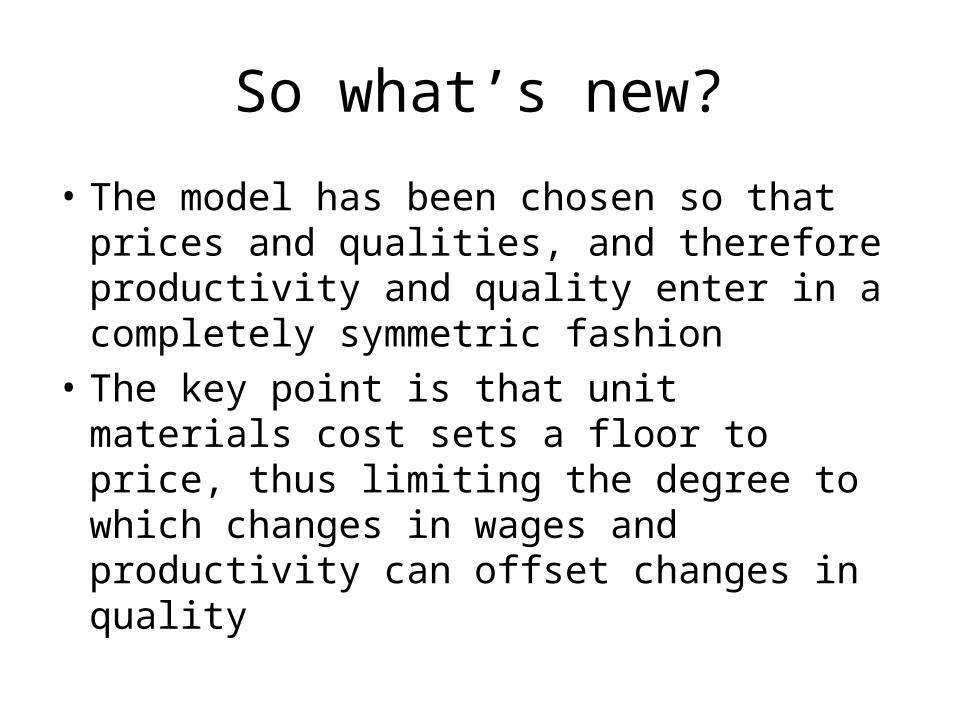

So what’s new?

• The model has been chosen so that prices and qualities, and therefore productivity and quality enter in a completely symmetric fashion

• The key point is that unit materials cost sets a floor to price, thus limiting the degree to which changes in wages and productivity can offset changes in quality

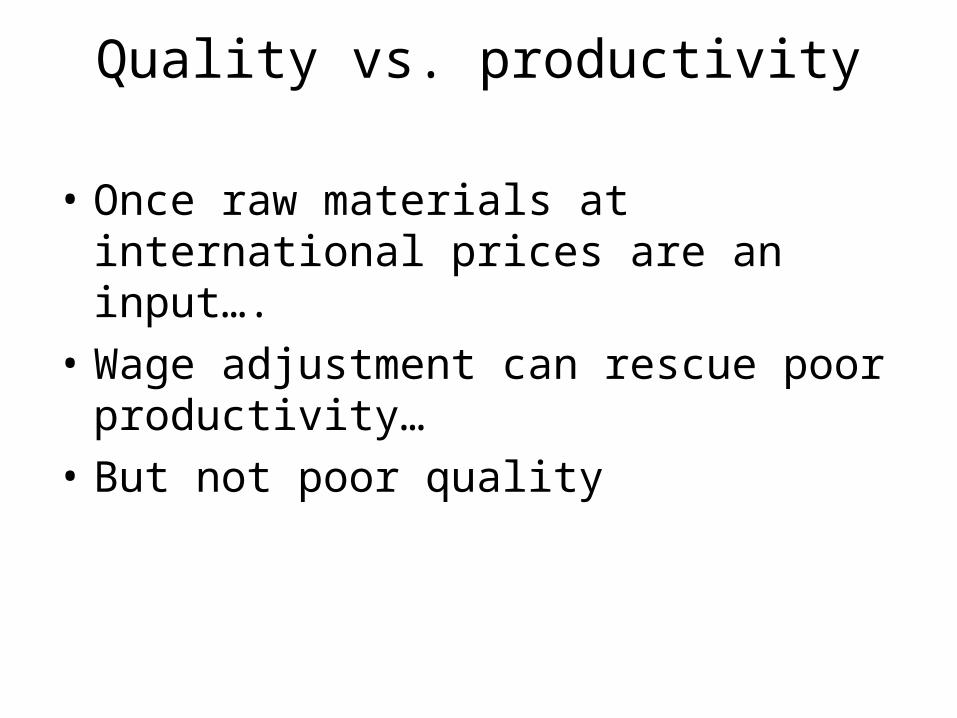

Quality vs. productivity

• Once raw materials at international prices are an input….

• Wage adjustment can rescue poor productivity…

• But not poor quality

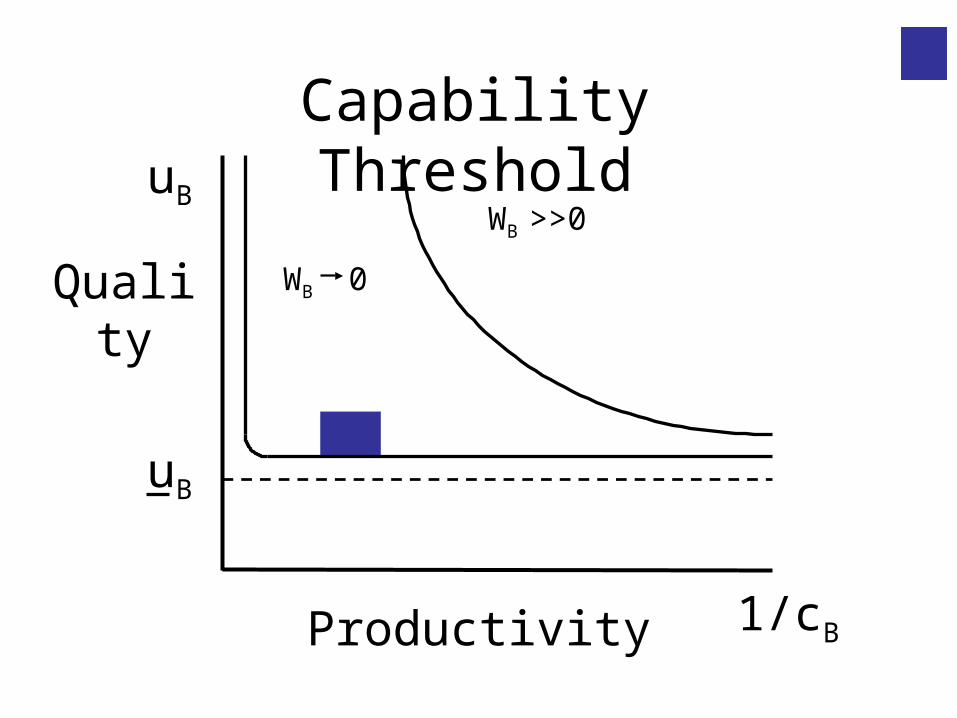

Capability Threshold

Quality

uB

1/cBProductivity

uB

WB 0

WB >>0

A Digression ….

• An extension of the model adds a second parameter (horizontal differentiation)

• This can be further generalized to “linkages between sub-markets”

• This extension is important in providing an explanation for cross-industry differences in market structure

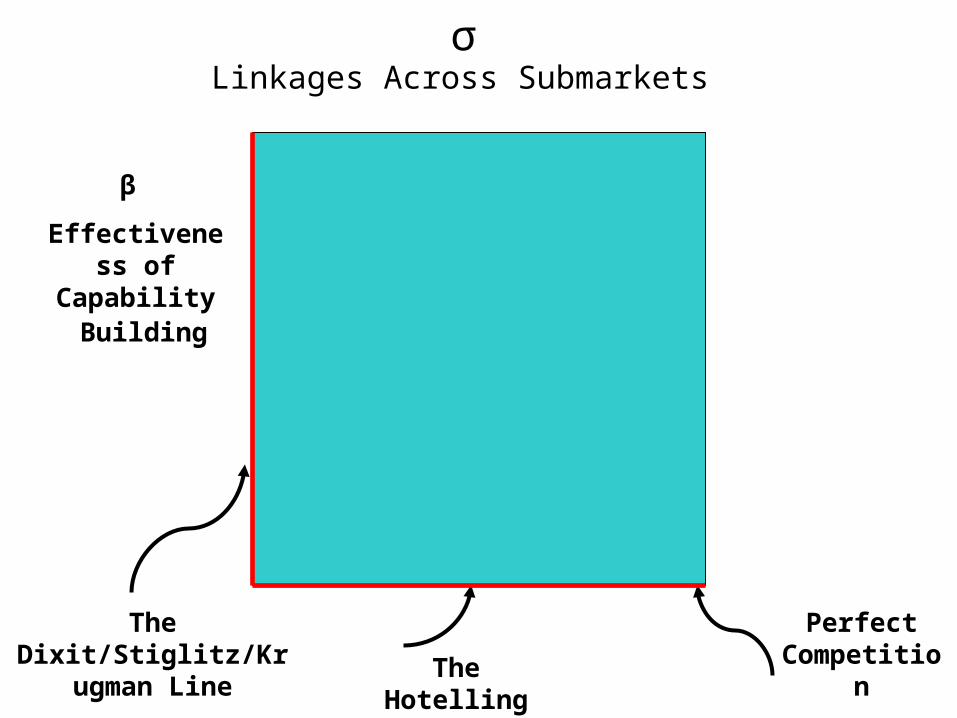

σ Linkages Across Submarkets

The Dixit/Stiglitz/Krugman

LineThe Hotelling

Line

Perfect Competition

β

Effectiveness of Capability

Building

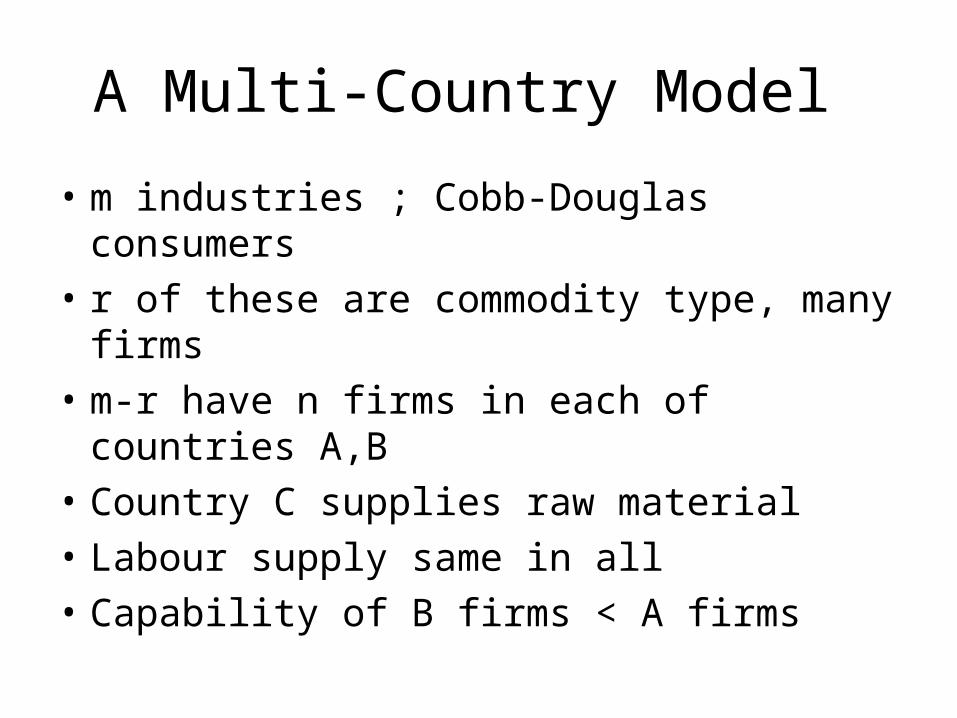

A Multi-Country Model

• m industries ; Cobb-Douglas consumers

• r of these are commodity type, many firms

• m-r have n firms in each of countries A,B

• Country C supplies raw material

• Labour supply same in all

• Capability of B firms < A firms

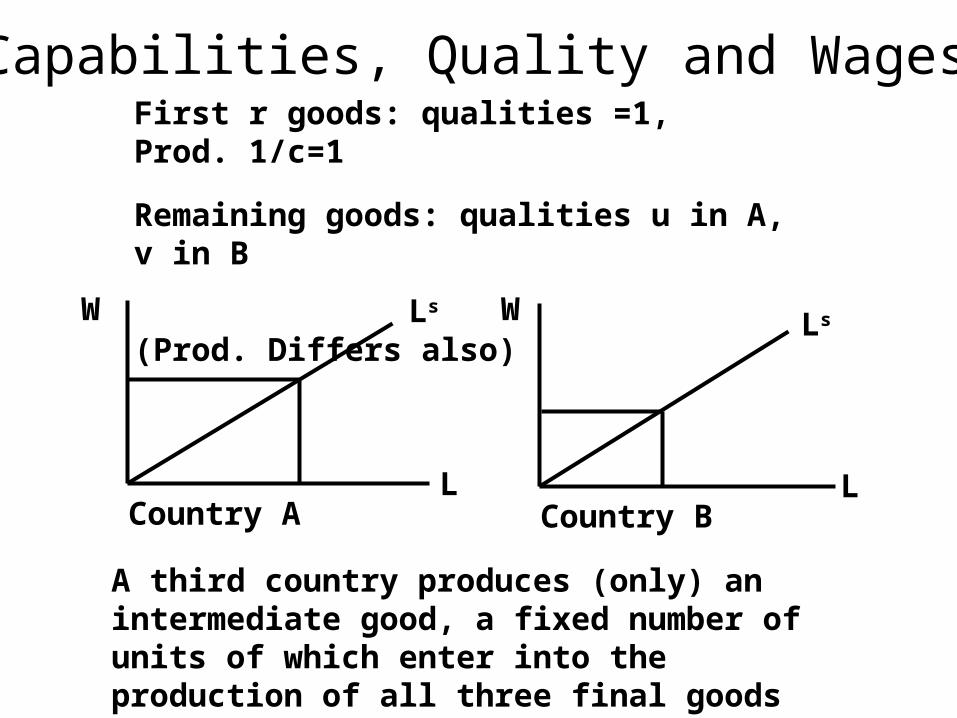

Capabilities, Quality and WagesFirst r goods: qualities =1, Prod. 1/c=1

Remaining goods: qualities u in A, v in B

(Prod. Differs also)

W

L

Ls

Country A

W

L

Ls

Country B

A third country produces (only) an intermediate good, a fixed number of units of which enter into the production of all three final goods

Modelling Pre-Globalisation

• The aim is to exclude competition in “quality” goods, while allowing A and B to source materials from C.

• Two routes:

• (i) Partition country C

• (ii) Unify C but inhabitants are insensitive to quality differences

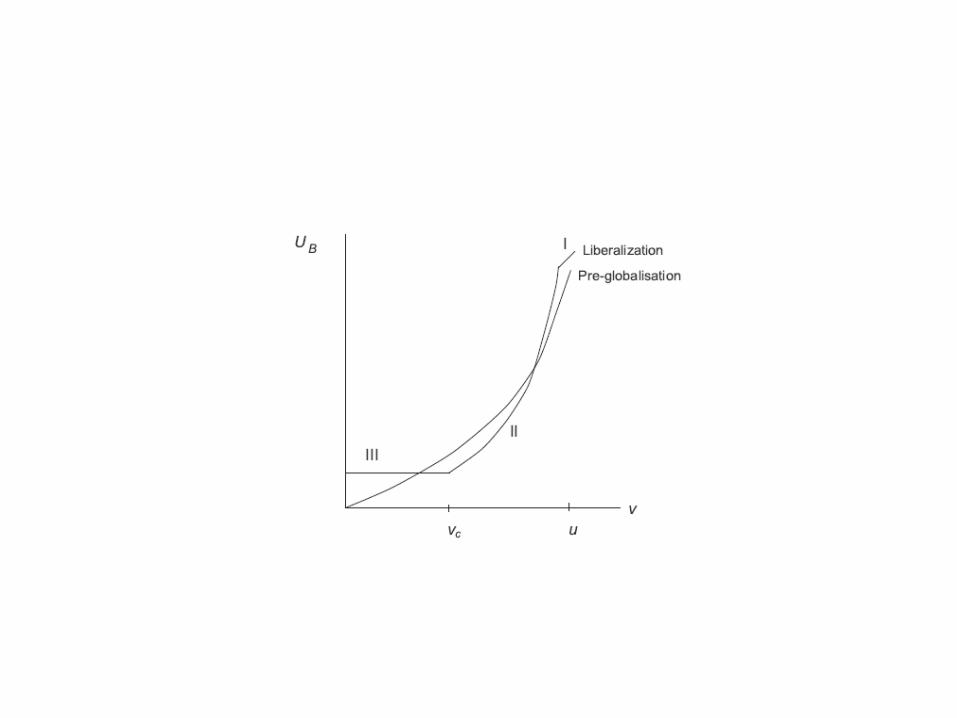

Three Phases

• Phase I: Impact phase…Capabilities given

• Phase II: Transfer phase

• Phase III: Re-investment (escalation) phase

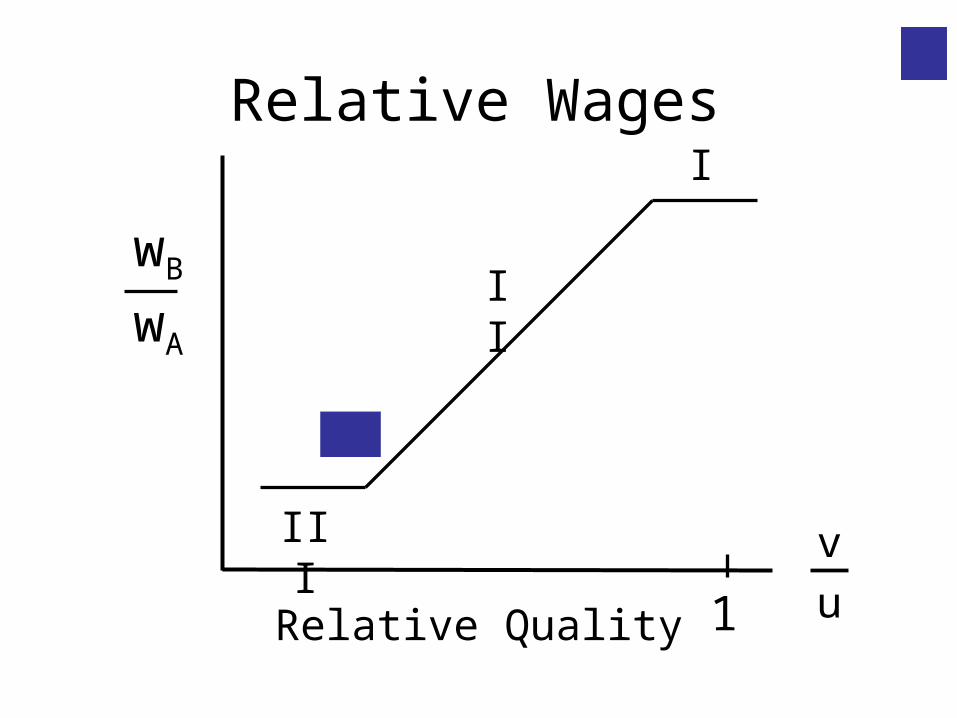

Phase I : Impact

• There are three regimes, depending on the size of the gap in capability

• Regime I….gap ~ 0

• Regime II…..moderate gap

• Regime III….wide gap

Relative Wages

1Relative Quality

wB

v

u

I

II

III

wA

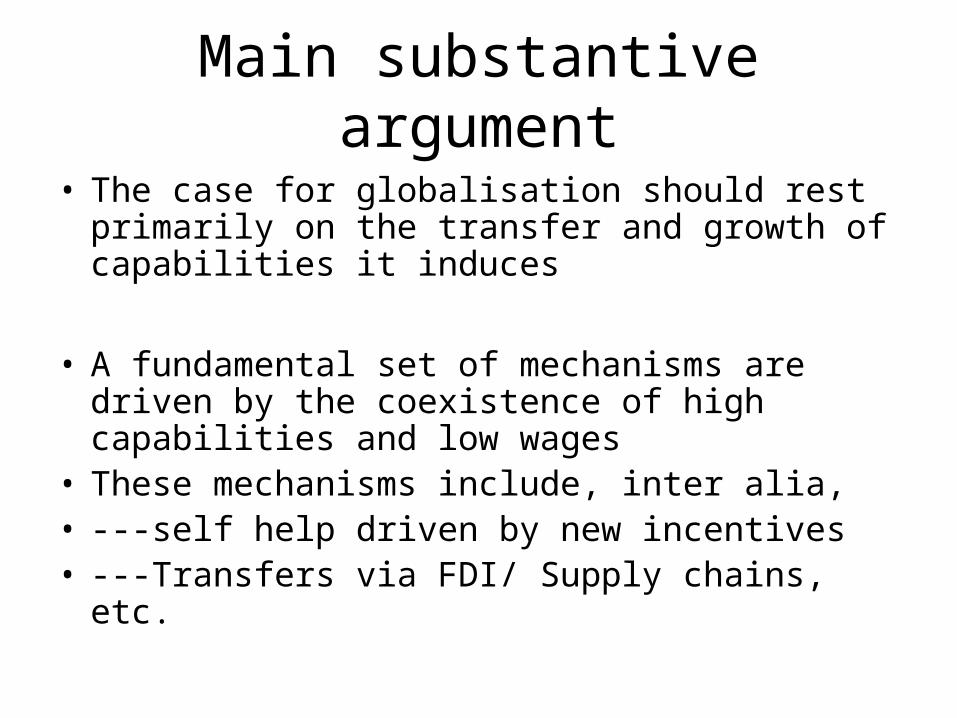

Main substantive argument

• The case for globalisation should rest primarily on the transfer and growth of capabilities it induces

• A fundamental set of mechanisms are driven by the coexistence of high capabilities and low wages

• These mechanisms include, inter alia, • ---self help driven by new incentives• ---Transfers via FDI/ Supply chains, etc.

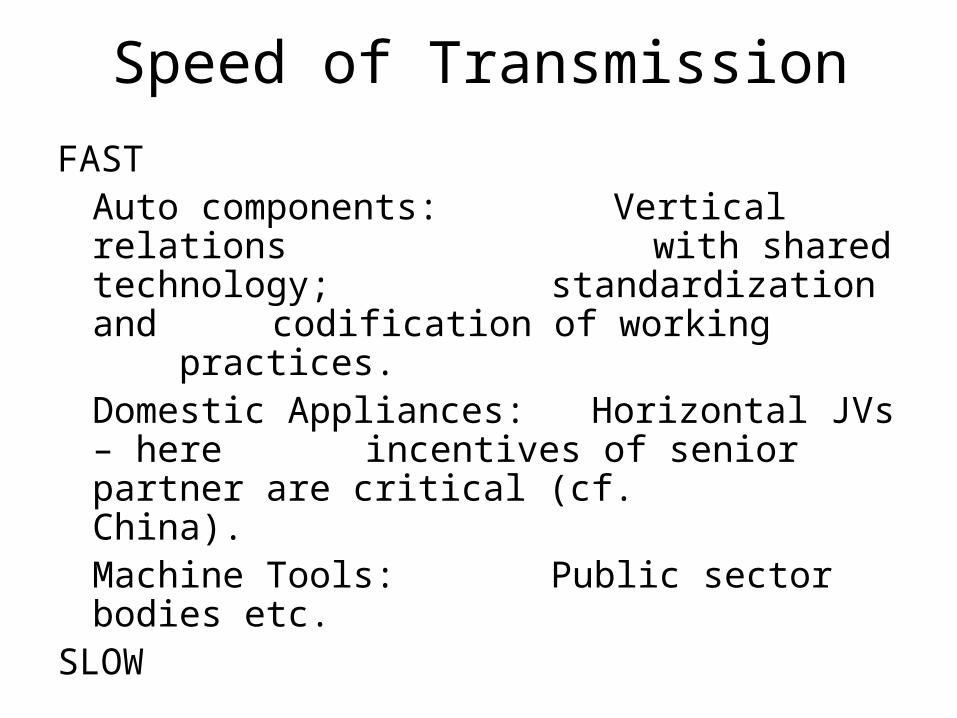

Speed of Transmission

FASTAuto components: Vertical relations

with shared technology; standardization and

codification of working practices.Domestic Appliances: Horizontal JVs – here

incentives of senior partner are critical (cf.

China).Machine Tools: Public sector bodies etc.

SLOW

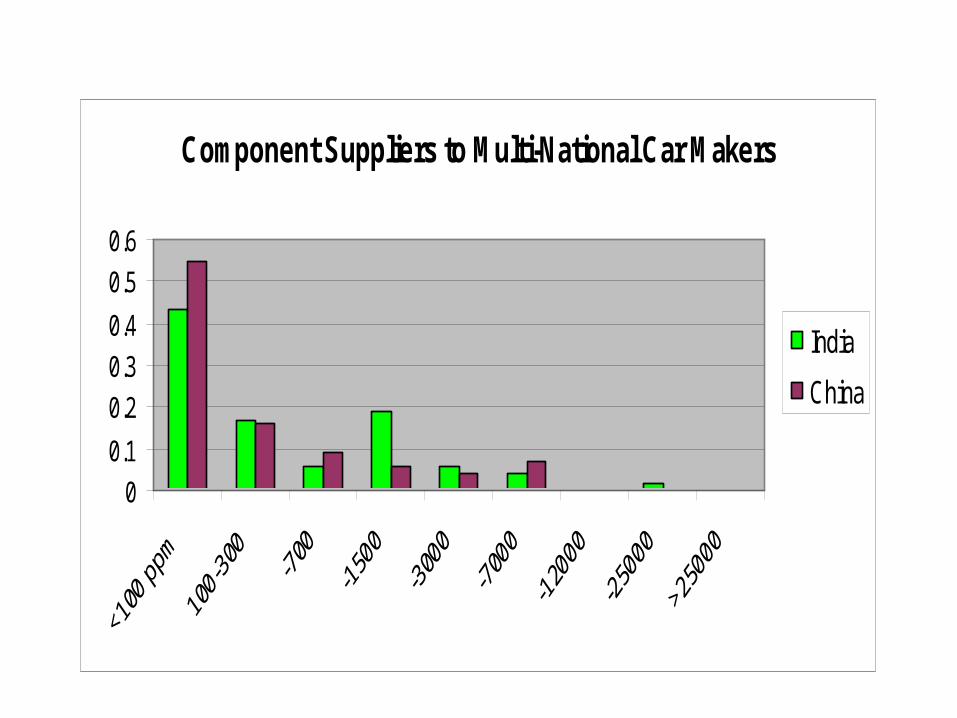

Component Suppliers to Multi-National Car Makers

0

0.1

0.2

0.3

0.4

0.5

0.6

India

China

The Mahindra Story

CNC Machine Tools

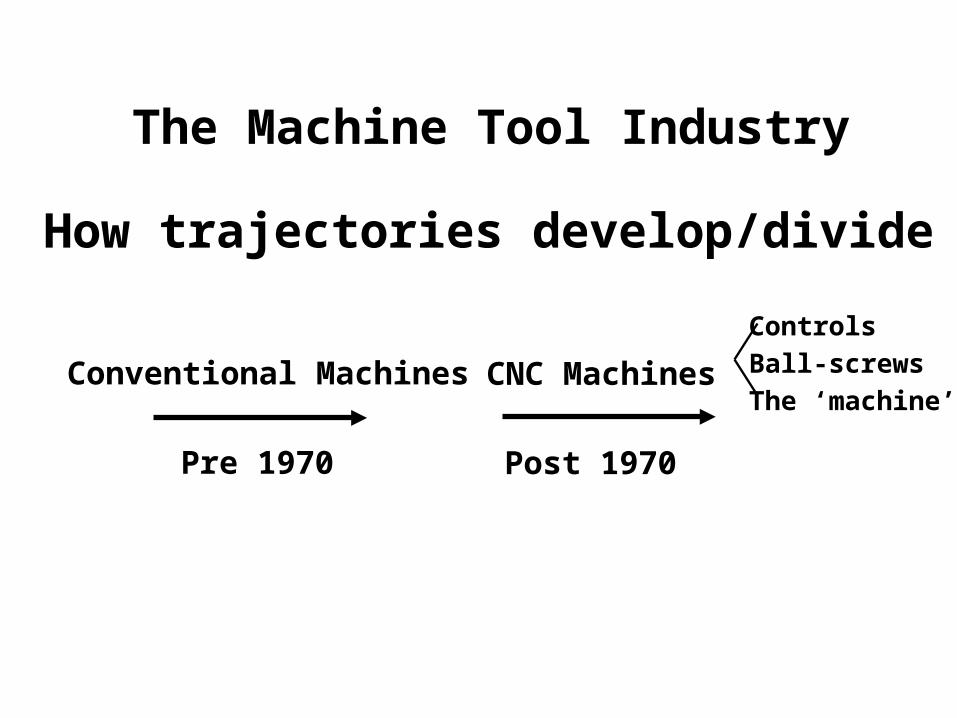

The Machine Tool Industry

How trajectories develop/divide

Conventional Machines CNC Machines

Controls

Ball-screws

The ‘machine’

Pre 1970 Post 1970

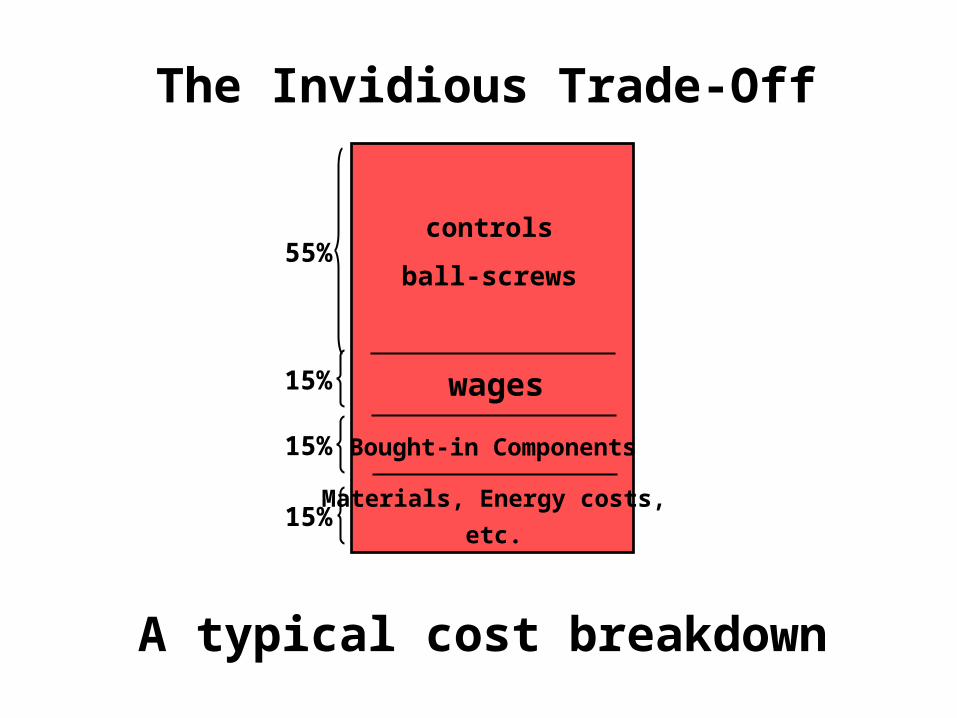

The Invidious Trade-Off

controls

ball-screws

15% wages

Bought-in Components

Materials, Energy costs,

etc.

15%

15%

55%

A typical cost breakdown

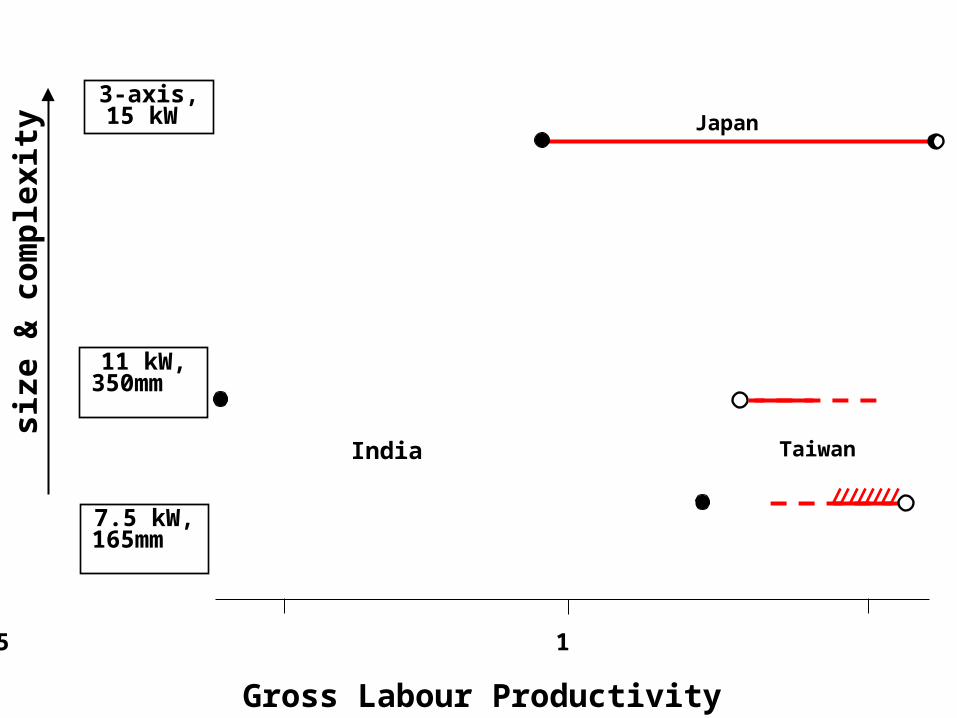

Gross Labour Productivity

3-axis, 15 kW

7.5 kW,165mm

11 kW,350mm

0.25 1 4

size

& c

om

ple

xity

Japan

India Taiwan

Phase III

• Escalation and shakeout

• Outcome depends on initial post-transfer gap

• Under a full transfer regime, shakeout occurs only for low-beta industries

• But…only a sub-set of firms re-invest