Embed Size (px)

DESCRIPTION

t

Citation preview

Module-3

--------------------------------------------------UNIT 1 INVESTMENT DECISIONS---------------------------------------------------------------------------

Objectives

To identify long term investment decisions

To study the significance of Capital Budgeting

To torch on capital budgeting process

Unit outline

3.1.1 Introduction

Classification of investment decisions

Long-term investment decision or capital budgeting and

Short-term decision or Working capital decision.

Expenses comes under capital investment

3.1.2 Meaning of Capital Budgeting

3.1.3 Importance of Capital Budgeting

3.1.4 Capital Budgeting Process

--------------------------------------------------3.1.1 INTRODUCTION

---------------------------------------------------------------------------The investment decision is the most important of the firm's three major

decisions when it comes to the value creation. Investment decision relates to

the determination of total amount of assets to be held in the firm, the

composition of these assets like the amount of fixed assets, current assets

and the extent of business risk involved by the investors.

The investment decisions can be classified in to two groups: (1) Long-

term investment decision or capital budgeting and (2) Short-term decision or

Working capital decision.

In this module the long-term investment decision or capital budgeting is

discussed in detail. The capital budgeting decisions, require comparison of

cost against benefits over a long period. The investment made in capital

assets cannot be recovered in the short run. Such assets will generate

returns ranging from 2 to 20 years or more. Such investment decision

involve a careful consideration of various factors like profitability, safety,

liquidity and solvency etc. a business organisation has to face quite often the

problem of capital investment decisions. Capital investment refers to the

investment in projects whose results would generate revenue or earnings

from alter a year and it will continue for several numbers of years. The

following are the expenses which comes under capital investment are:

a) Replacements of old technology with new technology

ii) Expansion of production activity

iii) Diversification of products due to competition and for growth

iv) Research and Development expenditure

v) Miscellaneous expensed for installation of equipment, pollution control

equipment etc.

-------------------------------------------------- 3.1.2 MEANING OF CAPITAL BUDGETING ---------------------------------------------------------------------------

Capital budgeting is the process of making investment decisions in

capital expenditures. A capital expenditure refers to an expenditure whose

benefits are expected be received over period of time exceeding one year.

Charles T. Horngreen has defined capital budgeting as, "Capital

budgeting is long term planning for making and financing proposed capital

outlays".

Richard and Greenlaw have referred to capital budgeting as "acquiring

inputs with long-run return".

Lynch defines it as "Capital budgeting consists in planning

development of available capital for the purpose of maximising the long term

profitability of the concern."

-------------------------------------------------- 3.1.3 IMPORTANCE OF CAPITAL BUDGETING

---------------------------------------------------------------------------

A capital budgeting or investment decision involves huge capital on

capital assets of the concern. Any wrong decision in capital budgeting will

cost the organisation through its capital loss and also revenue loss of the

company. Hence this decision is so critical and important, the finance

manager should take special care in making these decisions. They are

a) It involves heavy funds. Capital budgeting decisions, generally,

involve large investment of limited funds. These funds are to be

invested properly. Hence it is important to plan and control these

funds.

b) These funds will have long term implications. Since the funds

are limited and also involves huge investments for long term or

permanent basis. Hence it involves more risks, it should be

properly managed.

c) Irreversible decisions. Once the investment is made on capital

assets, it is not possible to reverse the decisions without incurring

heavy losses.

d) Long term impact on profitability. Capital budgeting decisions

will have a long-term and significant effect on the profitability of a

concern. An unwise decision may prove disastrous and greater loss

to the organisation.

e) Difficulties of Investment decisions. The capital budgeting

decisions require an assessment of future events which are

uncertain, hence it is very difficult to estimate the probable events

it is very difficult to asses the probable costs, benefits accurately in

this dynamic environment.

f) It is national important. The investment decision taken by the

individual concern is of national importance because it generates

employment, economic activities and economic growth.

-------------------------------------------------- 3.1.4 CAPITAL BUDGETING PROCESS

---------------------------------------------------------------------------

Capital budgeting involves complex process because it involves

investment of current funds for achieving benefit in future and the future is

always uncertain. However, the following procedure may be adopted in the

process of capital budgeting:

1) Identification of Investment proposal. It is first and important stage in

the capital budgeting process. The proposal or the idea bout potential

investment opportunities may originate from top management or may

come from the any part of organisation structure. The ideas are

analysed by the departmental head in the light of the corporate

objectives and strategies.

2) Screening the proposals. Each proposal received by the department is

screened from various angles to see whether it is technically feasible,

amount of expenditure involved, returns generated, risks involved

etc.,

3) Evaluation of various proposals. the next stage is to evaluate the

various proposals received from the departments by using capital

budgeting techniques.

4) Fixing priorities. After evaluating various proposals, the unprofitable

or uneconomical proposals are rejected. Out of selected proposals

once again are listed on the basis of priorities after considering

urgency, risk and profitability of the proposal.

5) Final approval and preparation of capital expenditure budget. For the

approved proposal in the meeting the capital expenditure budget is

prepared. This budget lays down the amount of estimated expenditure

to be incurred on fixed assets during the budget period.

6) Implementing proposal. While implementing the project or proposal, it

is better to assign responsibilities for completing the project within the

given time frame and cost limit so as to avoid unnecessary delays and

cost over runs. Network techniques used in the project management

such as PERT and CPM can also be applied to control and monitor the

implementation of the projects.

7) Performance review. The last stage in the process of capital budgeting

is the evaluation of the performance of the project. The evaluation is

made through post completion audit by way of comparison of actual

expenditure on the project with the budgeted one. Any unfavourable

variances, if any should be looked into and the causes of the same be

identified so that corrective action may be taken in future.

--------------------------------------------------UNIT 2 METHODS OR TECHNIQUES OF CAPITAL BUDGETING

---------------------------------------------------------------------------

Objective

To understand the various techniques of Capital Budgeting

Unit outline

3.2.1 Technique that recognize Payback of Capital Employed:

Payback Period Method.

3.2.2 Techniques that use Accounting Profit for Project

evaluation:

a. Accounting Rate of Return method.

b. Earning Per Share.

3.2.3 Techniques that recognize Time Value of Money:

a. Net Present Value Method.

b. Internal Rate of Return Method.

c. Net Terminal Value Method.

d. Profitability Index Method.

e. Discounted Payback Period Method.

--------------------------------------------------UNIT 2 METHODS OR TECHNIQUES OF CAPITAL BUDGETING

---------------------------------------------------------------------------

Methods or techniques of capital budgeting or Investment

Appraisal Techniques

The techniques available for appraisal of investment proposal are classified

three heads:

I. Technique that recognize Payback of Capital Employed:

Payback Period Method.

II. Techniques that use Accounting Profit for Project evaluation:

c. Accounting Rate of Return method.

d. Earning Per Share.

III. Techniques that recognize Time Value of Money:

f. Net Present Value Method.

g. Internal Rate of Return Method.

h. Net Terminal Value Method.

i. Profitability Index Method.

j. Discounted Payback Period Method.

-------------------------------------------------------------------------------

3.2.1 Technique that recognize Payback of Capital Employed

---------------------------------------------------------------------------

Payback Period Method.

The term payback refers to the period in which the project will

generate the necessary cash to recover the initial investment. For example,

if a project requires Rs. 30,000 as initial investment and it will generate an

annual cash inflow of Rs. 6,000 for ten years, the pay back period will be 5

years, it is calculated as follows:

Initial InvestmentPay back period = -------------------

Annual Cash Inflow

Rs 30,000= ------------

Rs 6,000

Cash inflow is calculated by taking into profits from the project before depreciation and

after Tax.When the cash inflow is uneven then the payback period is calculated bu cumulative

cash inflows and by interpolation, the exact payback period can be calculated. For example, if

the project requires an initial investment of Rs. 40,000 and the annual cash inflows for 5 years

are Rs. 12,000, Rs, 10,000, Rs. 14,000, Rs. 11,000 and Rs. 9,000 respectively, the pay back

period will be calculated as follows:

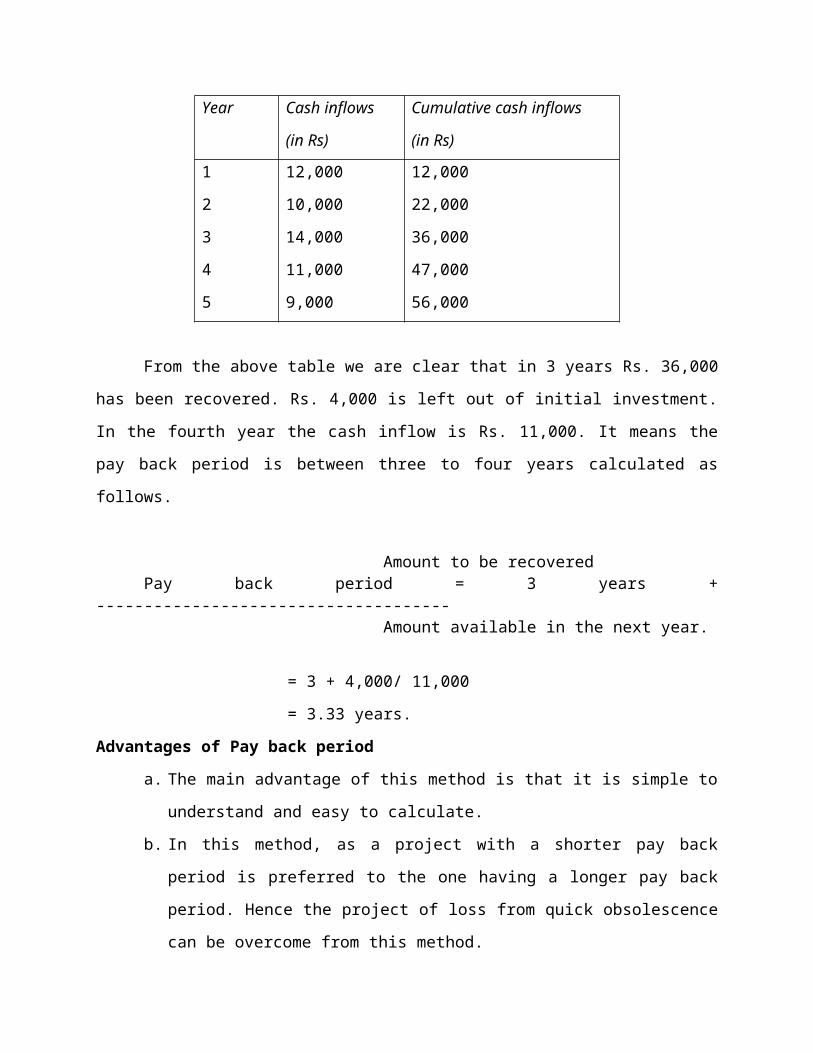

Year Cash inflows

(in Rs)

Cumulative cash inflows

(in Rs)

1

2

3

4

5

12,000

10,000

14,000

11,000

9,000

12,000

22,000

36,000

47,000

56,000

From the above table we are clear that in 3 years Rs. 36,000 has been

recovered. Rs. 4,000 is left out of initial investment. In the fourth year the

cash inflow is Rs. 11,000. It means the pay back period is between three to

four years calculated as follows.

Amount to be recoveredPay back period = 3 years + -------------------------------------

Amount available in the next year.

= 3 + 4,000/ 11,000

= 3.33 years.

Advantages of Pay back period

a. The main advantage of this method is that it is simple to understand

and easy to calculate.

b. In this method, as a project with a shorter pay back period is

preferred to the one having a longer pay back period. Hence the

project of loss from quick obsolescence can be overcome from this

method.

c. This method gives an indication to the prospective investors

specifying when their funds are likely to be repaid.

d. This method is suitable when the future is very uncertain.

Disadvantages

a. This method does not take into account the cash inflows earned

after the pay back period and the true profitability of the projects

cannot be correctly assessed.

b. This method ignores the time value of money and does not

consider the magnitude and timing of cash in flows.

c. It does not take into consideration the cost of capital which is a

very important factor in making sound investment decisions.

d. It treats each asset individually in isolation with other assets which

is not feasible in real practice.

e. This method does not consider the salvage value of an investment.

---------------------------------------------------------------------------

3.2.2 Techniques that use Accounting Profit for Project evaluation

--------------------------------------------------------------------------

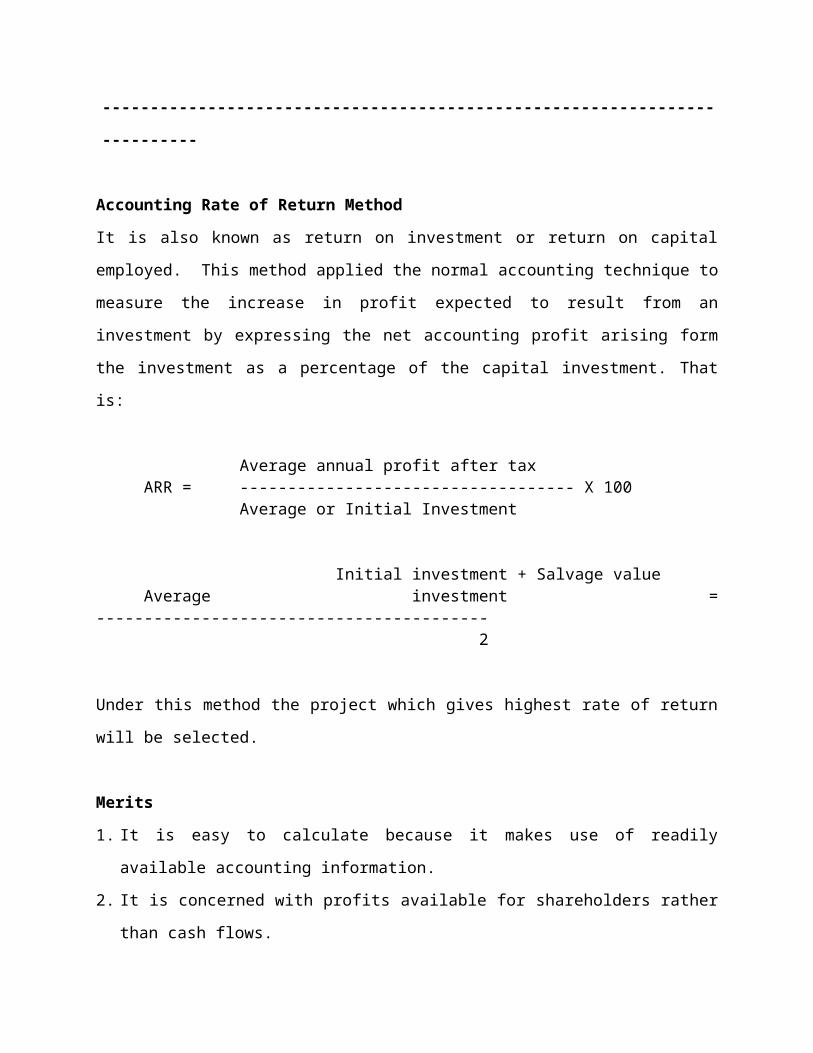

Accounting Rate of Return Method

It is also known as return on investment or return on capital employed. This

method applied the normal accounting technique to measure the increase in

profit expected to result from an investment by expressing the net

accounting profit arising form the investment as a percentage of the capital

investment. That is:

Average annual profit after taxARR = ----------------------------------- X 100

Average or Initial Investment

Initial investment + Salvage valueAverage investment = -----------------------------------------

2

Under this method the project which gives highest rate of return will be

selected.

Merits

1. It is easy to calculate because it makes use of readily available

accounting information.

2. It is concerned with profits available for shareholders rather than cash

flows.

3. This method takes into consideration all the years profit throughout its

life.

4. Quick decision of capital investment proposals is possible.

5. If high profits are required, this is certainly a way of achieving them.

Demerits

1. It does not take into account the time value of money.

2. It uses the straight line method of depreciation. Once this method is

changed the method will not be easy to use.

3. It is biased against short-term projects in the same way that payback is

biased against longer-term ones.

4. There are different methods for calculating the accounting rate of return

due to diverse concepts of investments as well as earnings. Each method

gives different results. This reduces the reliability of the method.

-------------------------------------------------------------------------------

3.2.3 Techniques that recognize Time Value of Money

--------------------------------------------------------------------------

Net present Value Method

This is generally considered to be the best method for evaluating the

capital investment proposals. In this method first cash inflows and cash

outflows associated with each project are worked out. The present value of

these cash inflows and outflows are then calculated at the rate of return

acceptable to the management. This rate of return is considered as the cut-

off rate and is generally determined on the basis of cost of capital adjusted

risk element in the project. The Net Present Value (NPV) is the difference

between the total present value of future cash inflows and the total present

value of future cash outflows.

The Net Present Value can be used as an 'accept or reject' criterion. In

case the NPV is positive the project should be accepted. If the NPV is

negative, the project should be rejected.

Merits

1. It recognises the time value of money and is suitable to be applied ina

situation with uniform or uneven cash inflows even at different periods of

time.

2. It takes into account the earnings over the entire life of the project and

the true profitability of the profit can be evaluated.

3. It takes into consideration the objective of maximum profitability.

Demerits

1. As compared to traditional method, the NPV method is more difficult to

understand and operate.

2. It is not easy to determine an appropriate discount rate.

3. The method is based on the presumption that cash inflow can be invested

at the discounting rate in the new projects. But this presumption does not

always hold good because it all depends upon the available investment

opportunities.

Internal Rate of Return (IRR)

Internal Rate of Return is that rate at which the sum of discounted

cash inflows equals the sum of discounted cash outflows. In other words, it is

the rate which discounts the cash flows to zero. It is also known as time

adjusted rate of return method or trial and error yield method.

Merits

It also takes into account the present value of money.

It considers the profitability of the project for its entire economic life and

hence enables evaluation of true profitability.

The determination of cost of capital is not a pre-requisite for the use of this

method and hence it is better than NPV method where the cost of capital

cannot be determined easily.

It provides for uniform ranking of various proposals due to the percentage

rate of return.

Demerits

1. It is difficult to understand and is the most difficult method of evaluation

of investment proposals.

2. This method is based upon the assumption that the earnings are

reinvested at the internal rate of return for the remaining life of the

project, which is not a justified assumption.

3. The results of NPV method and IRR method may differ when the projects

under evaluation differ in their size, life and timings of cash flows.

Discounted Pay back Period Method.

Under this method the draw back of time value of money not

considered in pay back period is considered. Hence this method is

improvement over the pay back period method. Under this method the

project which gives the greatest post pay-back period may be accepted.

Under this method the present values of all cash outflows and inflows are

computed at an appropriate discount rate. The time period at which the

cumulated present value of cash inflows equals th present value of cash

outflows is known as discounted pay back period.

Profitability Index Method or Benefit Cost Ratio

It is also a time-adjusted method of evaluating the investment proposals.

Profitability index also called as Benefit-Cost Ratio or Desirability factor is the

relationship between present value of cash inflows and present value of cash

outflows. Thus

Present value of cash inflowsProfitability Index = -------------------------

Present value of cash outflows

The proposal is accepted if the profitability index is more than one and

is rejected in case the PI is less than one.

--------------------------------------------------UNIT 3 PROBLEMS ON CAPITAL BUDGETING

---------------------------------------------------------------------------

Objectives

To give practical exposure to the working of capital budgeting

To help in decision making process, in selecting a best method of capital

budgeting

To know the working knowledge of these methods

Unit outline

3.3.1 Problems on capital budgeting

Payback period

Accounting Rate of Return

Net Present Value

Internal Rate of Return

Profitability index

-------------------------------------------------------------------------------

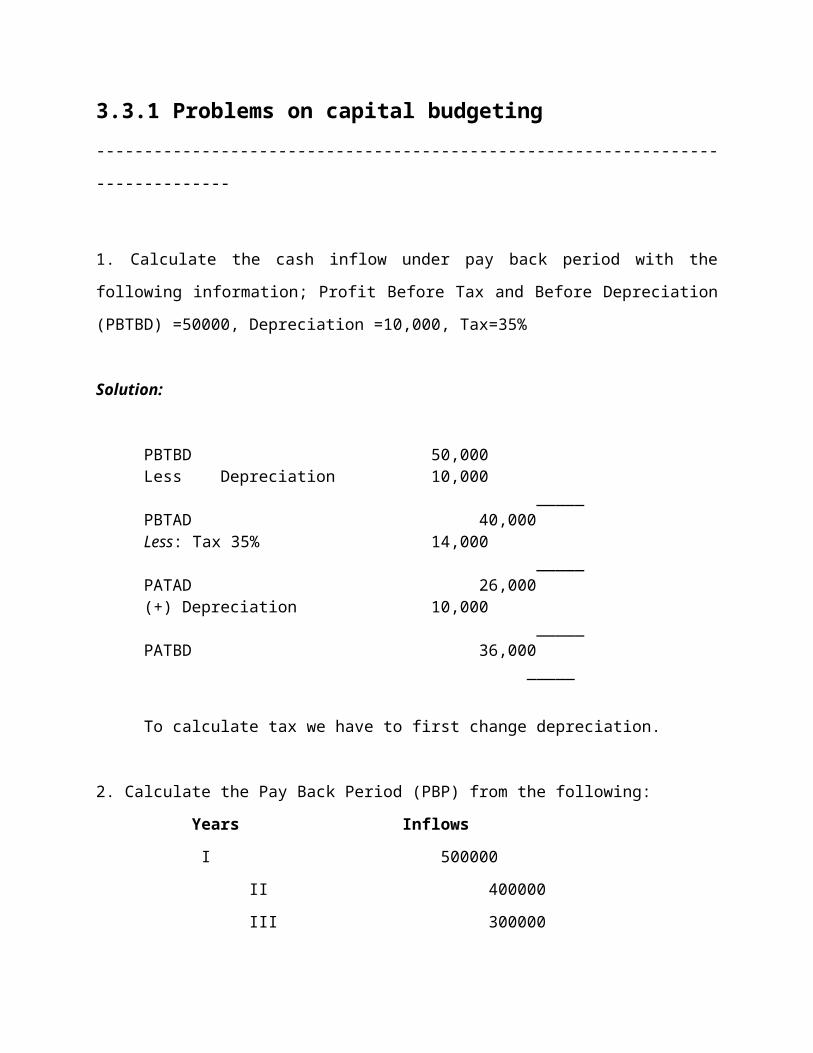

3.3.1 Problems on capital budgeting

-------------------------------------------------------------------------------

1. Calculate the cash inflow under pay back period with the following

information; Profit Before Tax and Before Depreciation (PBTBD) =50000,

Depreciation =10,000, Tax=35%

Solution:

PBTBD 50,000Less Depreciation 10,000

_____PBTAD 40,000Less: Tax 35% 14,000

_____PATAD 26,000(+) Depreciation 10,000

_____PATBD 36,000

_____

To calculate tax we have to first change depreciation.

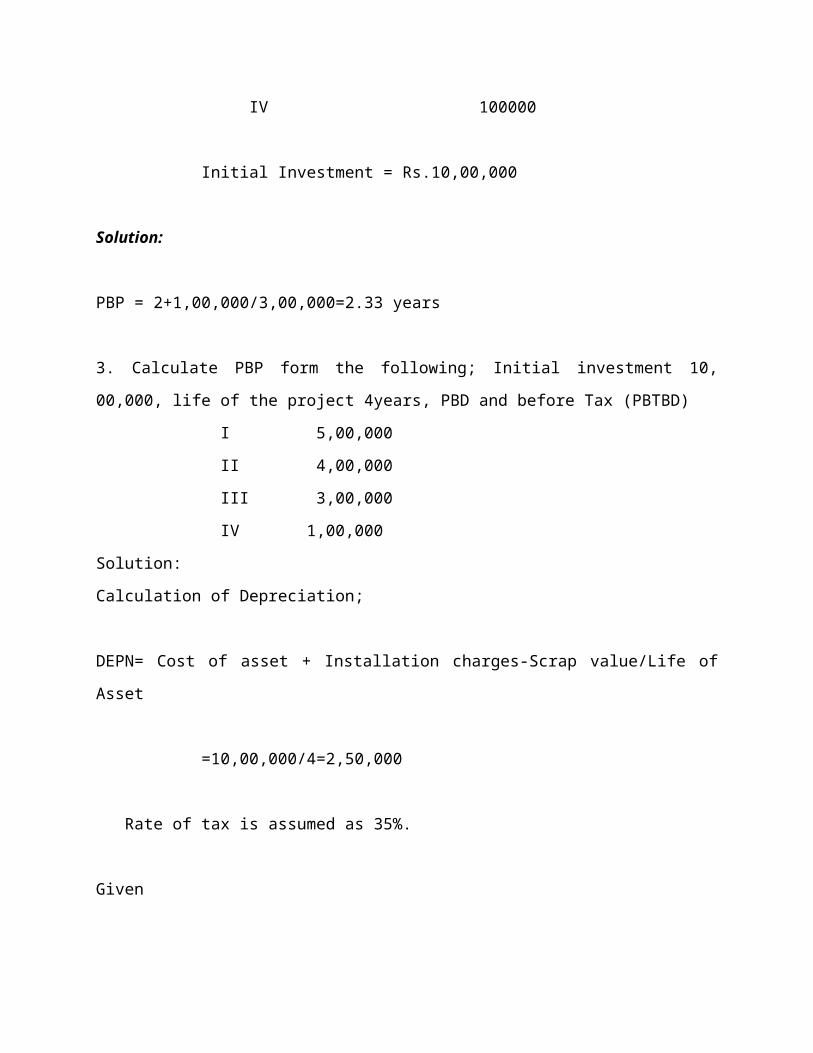

2. Calculate the Pay Back Period (PBP) from the following:

Years Inflows

I 500000

II 400000

III 300000

IV 100000

Initial Investment = Rs.10,00,000

Solution:

PBP = 2+1,00,000/3,00,000=2.33 years

3. Calculate PBP form the following; Initial investment 10, 00,000, life of the

project 4years, PBD and before Tax (PBTBD)

I 5,00,000

II 4,00,000

III 3,00,000

IV 1,00,000

Solution:

Calculation of Depreciation;

DEPN= Cost of asset + Installation charges-Scrap value/Life of Asset

=10,00,000/4=2,50,000

Rate of tax is assumed as 35%.

Given

Year PBTBD (-) Depn. PBTAD (-) Tax 35% PATAD (+)Dep. PATBD

I 500000 250000 250000 87500 162500 250000 412500

II 400000 250000 150000 52500 97500 250000 347500

III 300000 250000 50000 17000 32500 250000 282500

IV 100000 250000 (150000) - (150000) 250000 100000

PBP=2+2,40,000/2,82,500 (2,40,000=10,00,000-7,60,000)

= 2.85 Years

4. A Project involves the investment of Rs. 500000 which yields PADAT as

stated below:

Years PATAD

I 25000

II 37500

III 62500

IV 65000

V 40000

At the end of 5 years the machinery in the project can be sold for 40,000.

The cut-off rate is 8%. Suggest the management whether or not to accept

the proposal based on ARR.

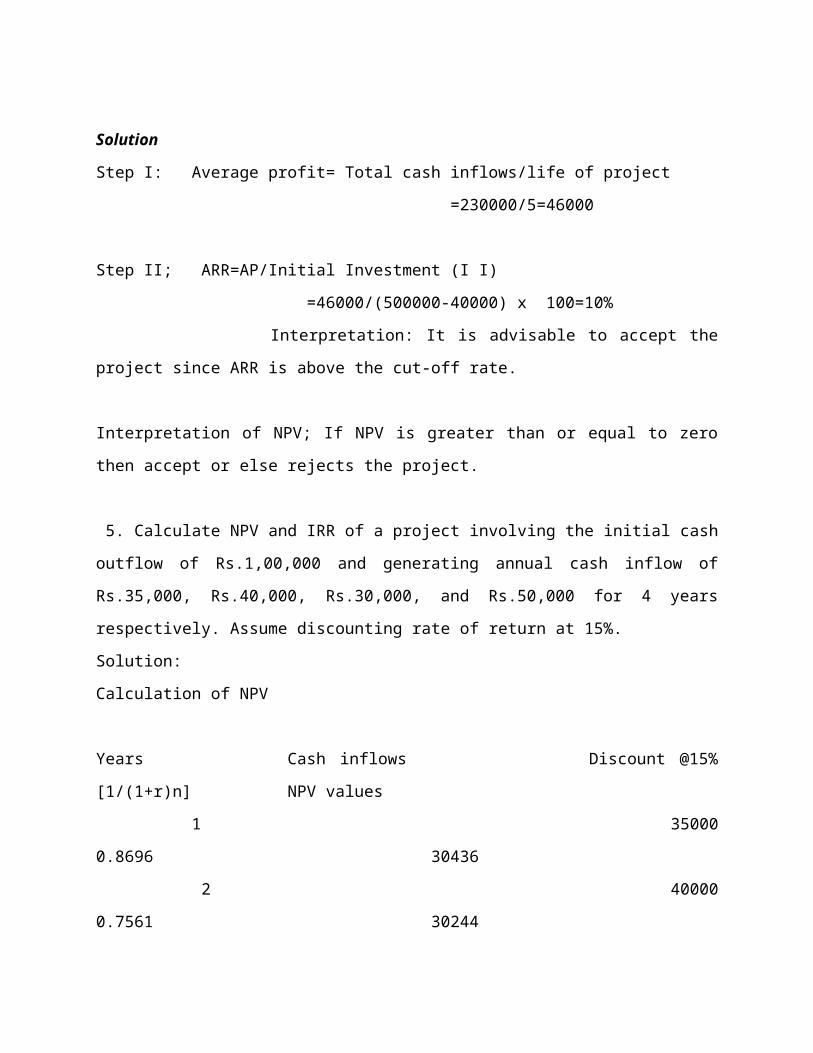

Solution

Step I: Average profit= Total cash inflows/life of project

=230000/5=46000

Step II; ARR=AP/Initial Investment (I I)

=46000/(500000-40000) x 100=10%

Interpretation: It is advisable to accept the project since ARR is

above the cut-off rate.

Interpretation of NPV; If NPV is greater than or equal to zero then accept or

else rejects the project.

5. Calculate NPV and IRR of a project involving the initial cash outflow of

Rs.1,00,000 and generating annual cash inflow of Rs.35,000, Rs.40,000,

Rs.30,000, and Rs.50,000 for 4 years respectively. Assume discounting rate

of return at 15%.

Solution:

Calculation of NPV

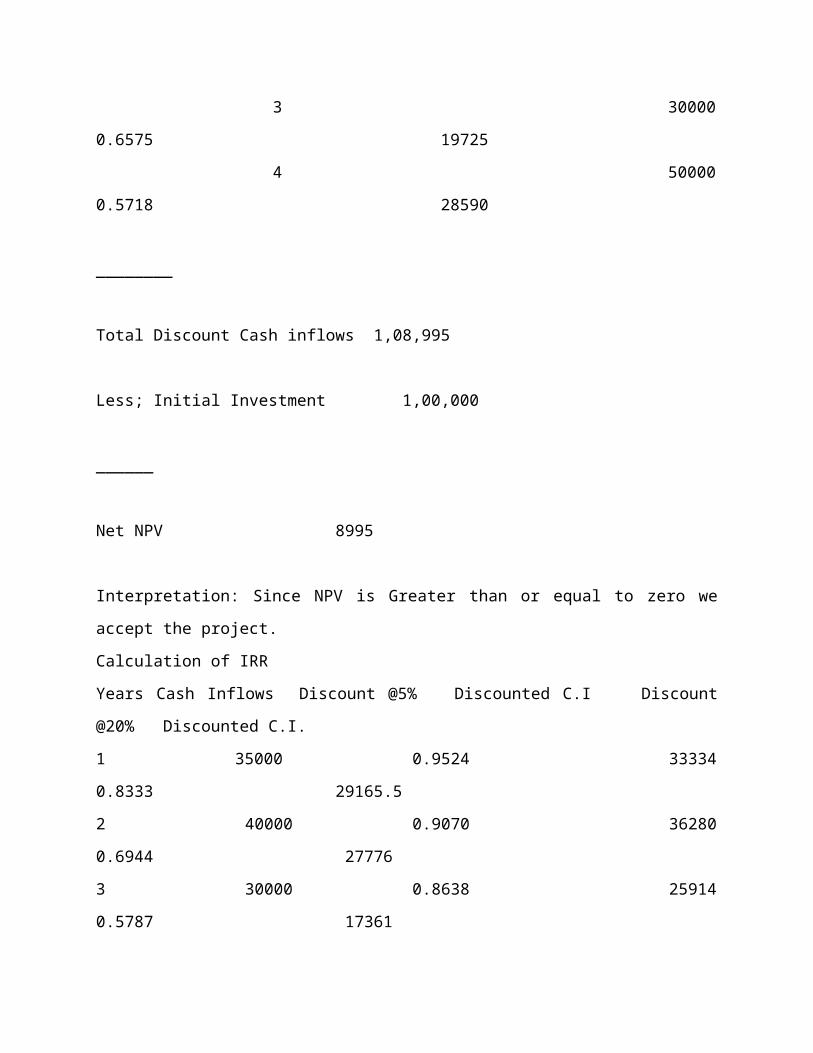

Years Cash inflows Discount @15% [1/(1+r)n] NPV values

1 35000 0.8696 30436

2 40000 0.7561 30244

3 30000 0.6575 19725

4 50000 0.5718 28590

________

Total Discount Cash inflows 1,08,995

Less; Initial Investment 1,00,000

______

Net NPV 8995

Interpretation: Since NPV is Greater than or equal to zero we accept the

project.

Calculation of IRR

Years Cash Inflows Discount @5% Discounted C.I Discount @20% Discounted C.I.

1 35000 0.9524 33334 0.8333 29165.5

2 40000 0.9070 36280 0.6944 27776

3 30000 0.8638 25914 0.5787 17361

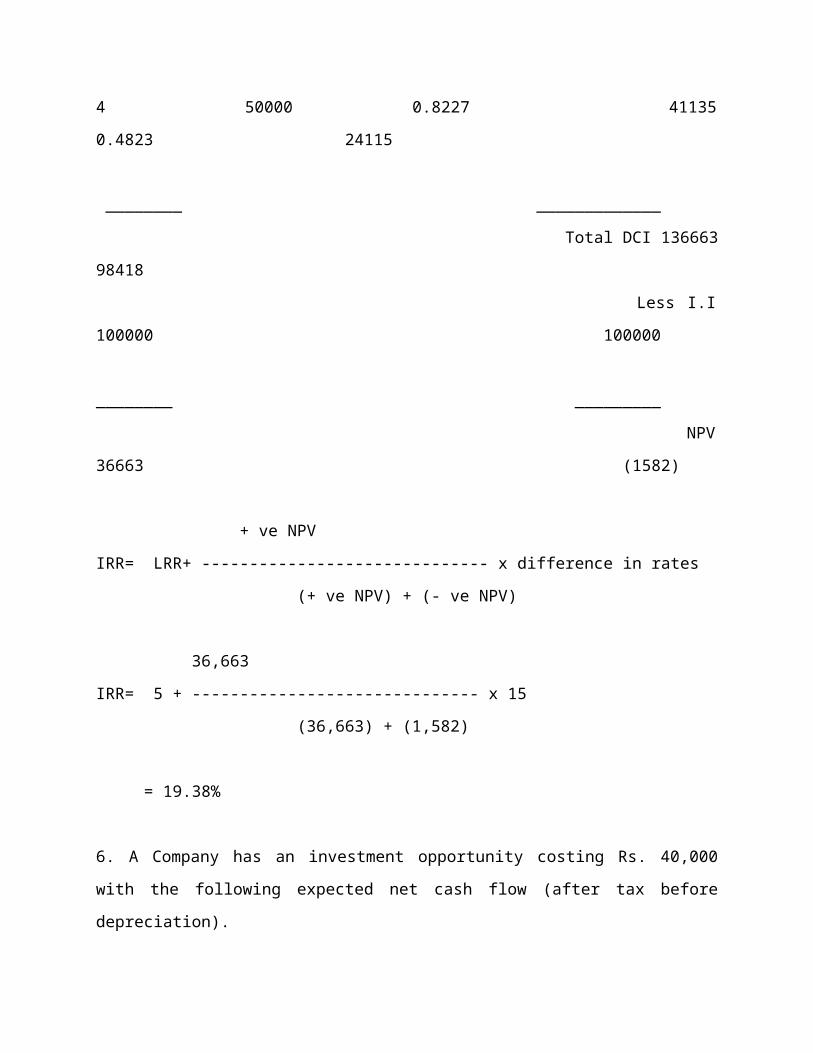

4 50000 0.8227 41135 0.4823 24115

________ _____________

Total DCI 136663 98418

Less I.I 100000 100000

________ _________

NPV 36663 (1582)

+ ve NPV

IRR= LRR+ ------------------------------ x difference in rates

(+ ve NPV) + (- ve NPV)

36,663

IRR= 5 + ------------------------------ x 15

(36,663) + (1,582)

= 19.38%

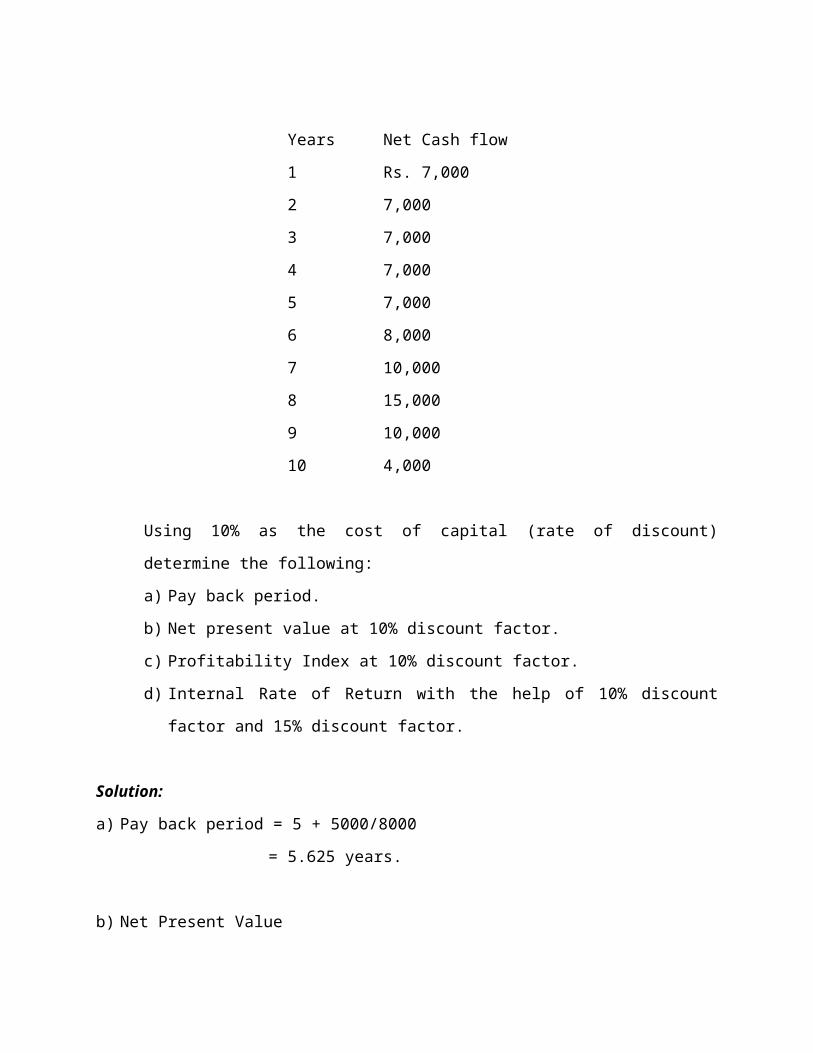

6. A Company has an investment opportunity costing Rs. 40,000 with the

following expected net cash flow (after tax before depreciation).

Years Net Cash flow

1 Rs. 7,000

2 7,000

3 7,000

4 7,000

5 7,000

6 8,000

7 10,000

8 15,000

9 10,000

10 4,000

Using 10% as the cost of capital (rate of discount) determine the

following:

a) Pay back period.

b) Net present value at 10% discount factor.

c) Profitability Index at 10% discount factor.

d) Internal Rate of Return with the help of 10% discount factor and

15% discount factor.

Solution:

a) Pay back period = 5 + 5000/8000

= 5.625 years.

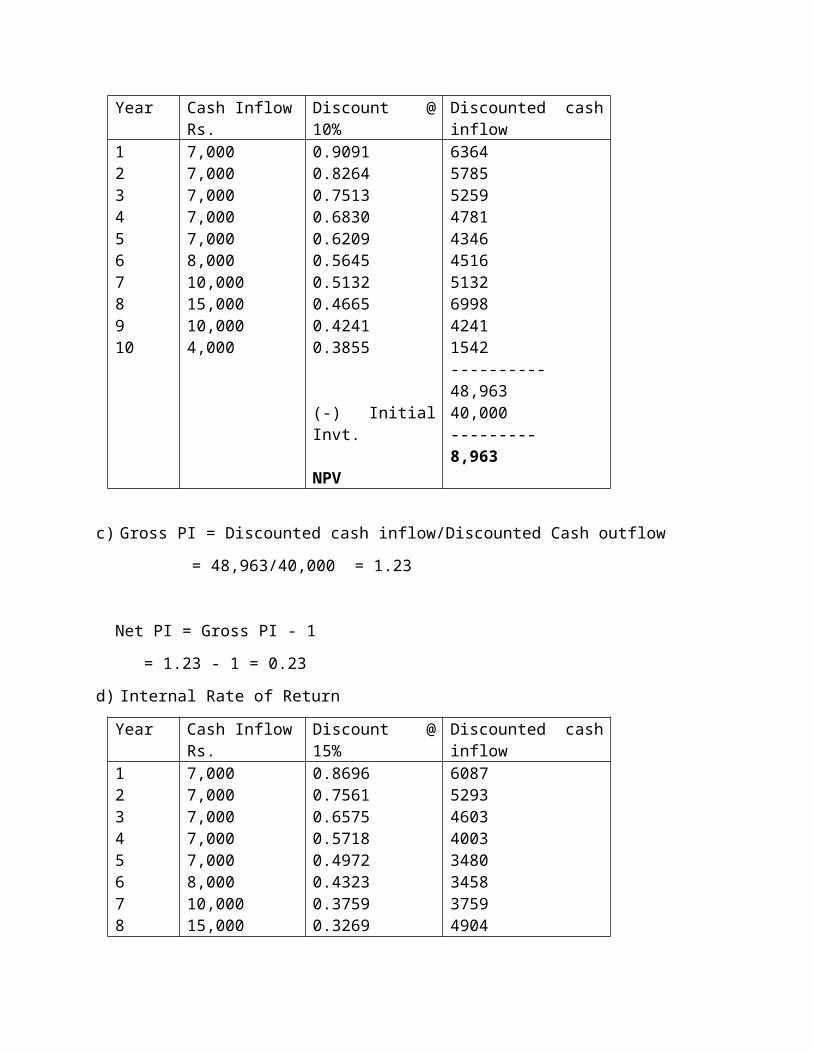

b) Net Present Value

Year Cash Inflow Rs.

Discount @ 10%

Discounted cash inflow

12345678910

7,0007,0007,0007,0007,0008,00010,00015,00010,0004,000

0.90910.82640.75130.68300.62090.56450.51320.46650.42410.3855

(-) Initial Invt.

NPV

6364578552594781434645165132699842411542----------48,96340,000---------8,963

c) Gross PI = Discounted cash inflow/Discounted Cash outflow

= 48,963/40,000 = 1.23

Net PI = Gross PI - 1

= 1.23 - 1 = 0.23

d) Internal Rate of Return

Year Cash Inflow Rs.

Discount @ 15%

Discounted cash inflow

1234567

7,0007,0007,0007,0007,0008,00010,000

0.86960.75610.65750.57180.49720.43230.3759

6087529346034003348034583759

8910

15,00010,0004,000

0.32690.28430.2472

Less Initial Invt.

(-)ve NPV

49042843989--------39,41840,000

--------(-) 582

+ ve NPV

IRR= LRR+ ------------------------------ x difference in rates

(+ ve NPV) + (- ve NPV)

8,963

IRR= 10 + ------------------------------ x (15 - 10)

8,963 + 582

= 14.695 %

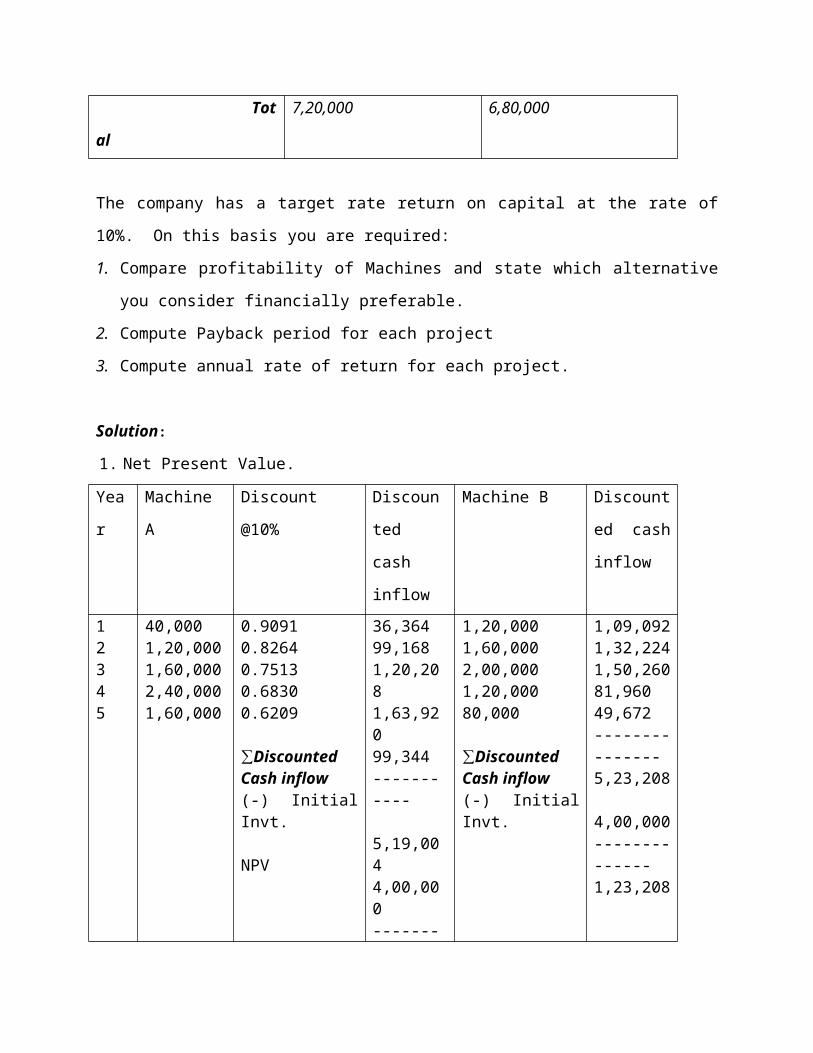

7. The L Company Ltd, is considering the purchase of a new machine. Two

alternative machines (A&B0 have been suggested each costing Rs. 4,00,000.

Earnings after taxation but before depreciation are expected to be as

follows:

Year Machine A Machine B

1

2

3

4

5

Total

40,000

1,20,000

1,60,000

2,40,000

1,60,000

7,20,000

1,20,000

1,60,000

2,00,000

1,20,000

80,000

6,80,000

The company has a target rate return on capital at the rate of 10%. On this

basis you are required:

1. Compare profitability of Machines and state which alternative you

consider financially preferable.

2. Compute Payback period for each project

3. Compute annual rate of return for each project.

Solution:

1. Net Present Value.

Yea

r

Machine

A

Discount

@10%

Discount

ed cash

inflow

Machine B Discount

ed cash

inflow

12345

40,0001,20,0001,60,0002,40,0001,60,000

0.90910.82640.75130.68300.6209

∑Discounted Cash inflow (-) Initial Invt.

NPV

36,36499,1681,20,2081,63,92099,344-----------

5,19,0044,00,000------------1,19,004

1,20,0001,60,0002,00,0001,20,00080,000

∑Discounted Cash inflow(-) Initial Invt.

1,09,0921,32,2241,50,26081,96049,672---------------5,23,208

4,00,000--------------1,23,208

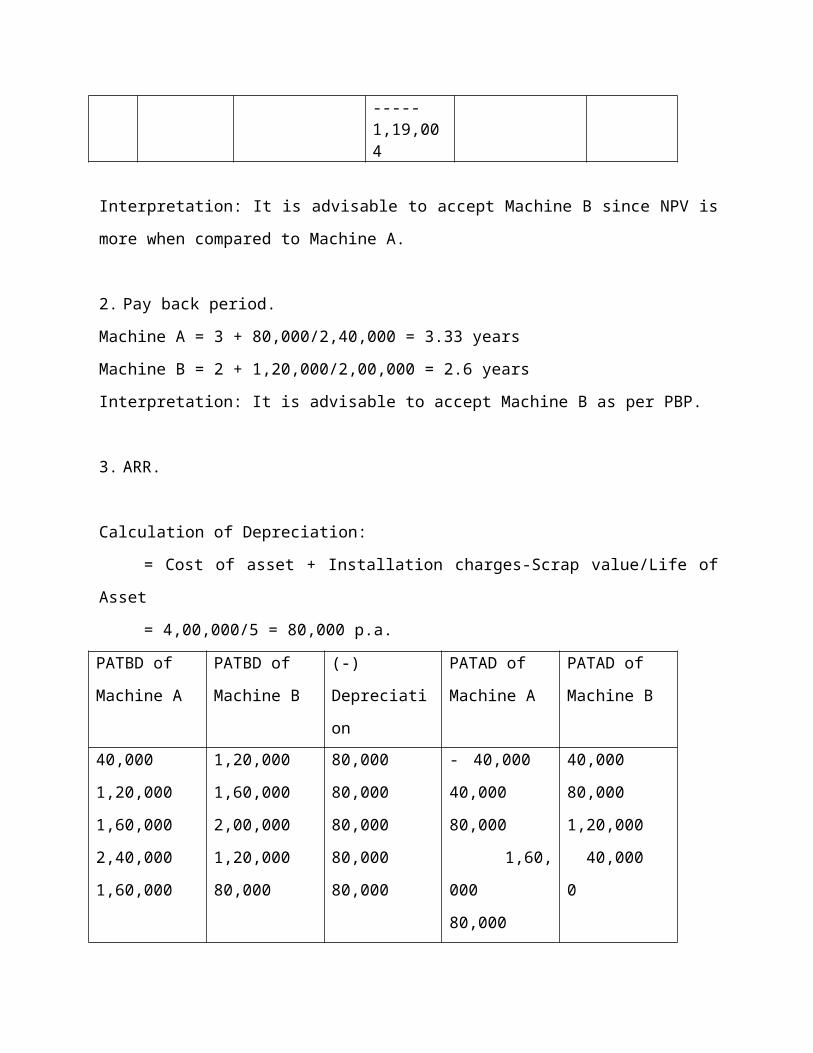

Interpretation: It is advisable to accept Machine B since NPV is more when

compared to Machine A.

2. Pay back period.

Machine A = 3 + 80,000/2,40,000 = 3.33 years

Machine B = 2 + 1,20,000/2,00,000 = 2.6 years

Interpretation: It is advisable to accept Machine B as per PBP.

3. ARR.

Calculation of Depreciation:

= Cost of asset + Installation charges-Scrap value/Life of Asset

= 4,00,000/5 = 80,000 p.a.

PATBD of

Machine A

PATBD of

Machine B

(-)

Depreciation

PATAD of

Machine A

PATAD of

Machine B

40,000

1,20,000

1,60,000

2,40,000

1,60,000

1,20,000

1,60,000

2,00,000

1,20,000

80,000

80,000

80,000

80,000

80,000

80,000

- 40,000

40,000

80,000

1,60,000

80,000

40,000

80,000

1,20,000

40,000

0

Average profit (A) = 3,20,000/5 = 64,000

ARR = 64,000/4,00,000 x 100 = 16%

Average profits (B) = 2,80,000/5 = 56,000

ARR = 56,000/4,00,000 x 100 = 14%

Interpretation: it is advisable to accept Machine A as per ARR

1. The expected cash flows of the project are as follows:

Years Cash flows

0 - 1,00,000

1 20,000

2 30,000

3 40,000

4 50,000

5 60,000

The cost of capital is 12% calculate the following.

a) NPV

b) Benefit cost ratio (GPI)

c) PBP

d) IRR

e) Discounted PBP

Solution:

a) NPV

Year Cash Inflow Discount factor @12%

Discounted Cash inflow

12345

20,00030,000 40,00050,00060,000

0.89290.79720.71180.63550.5674

∑ Cash inflow- Initial invt.

NPV

17,85823,91628,47231,77517,022------------1,19,0431,00,000------------19,043

b) Benefit cost ration (GPI)

= Discounted Cash inflow / Discounted Cash outflow

= 1,19,043 / 1,00,000

= 1.19

c) Pay Back period

= 3 + 10,000 / 50,000

= 3.2 years

d) IRR

Year Cash Inflow Discount factor @20%

Discounted Cash inflow

12345

20,00030,000 40,00050,00060,000

0.83330.69440.57870.48230.4019

∑ Cash inflow- Initial invt.

NPV

16,66620,83223,14824,11512,057------------ 96,8181,00,000------------- 3,182

+ ve NPV

IRR= LRR+ ------------------------------ x difference in rates

(+ ve NPV) + (- ve NPV)

19,043

IRR= 12 + ------------------------------ x (15 - 10)

19,043 + 3,182

= 18.85%

e) Discounted Pay Back period

= 3 + 29,754 / 31,775

= 3.9 years

-------------------------------------------------------------------------------

Unit 4 Risk and Uncertainty in Capital Budgeting -------------------------------------------------------------------------------

Objectives

The objectives of this unit are:

To bring clarity in the concepts of Risk and Uncertainty

To study the methods of accounting the risk in capital budgeting

Unit outline

3.4.1 Risk and Uncertainty in Capital Budgeting

The following methods are suggested for accounting for risk in capital

budgeting.

(i) General Techniques:

(a)Risk adjusted discount rate;

(b)Certainty equivalent coefficient.

(ii) Quantitative Techniques:

(a)Sensitivity analysis

(b)Probability assignment

(c) Standard deviation

(d)Coefficient of variation

(e) Decision tree analysis

-------------------------------------------------------------------------------

3.4.1 Risk and Uncertainty in Capital Budgeting

----------------------------------------------------------------------------

All the techniques of capital budgeting require the estimation of future

cash inflows and cash outflows. The future cash flows are estimated, based

on the following factors:

(1) Expected economic life of the project.

(2) Salvage value of the asset at the end of its life.

(3) Capacity of the project.

(4) Selling price of the product.

(5) Production cost

(6) Depreciation and tax rate

(7) Future demand for the product etc.,

But due to uncertainties about the future most of the above factors

cannot be exact. For example, the product becomes absolute, technology

becomes obsolescence, in these situations taking investment decisions

becomes difficult. But some allowances for the element of risk have to be

provided.

The following methods are suggested for accounting for risk in capital

budgeting.

(i) General Techniques:

(a)Risk adjusted discount rate;

(b)Certainty equivalent coefficient.

(ii) Quantitative Techniques:

(a)Sensitivity analysis

(b)Probability assignment

(c) Standard deviation

(d)Coefficient of variation

(e)Decision tree analysis

Risk adjusted discount rate

The risk adjusted discount rate is based on the presumption that

investors expect a higher rate of return on risky projects as compared to less

risky projects. The rate requires is determined by i) risk free rate and ii) risk

premium rate. Risk free rate is the rate at which the future cash inflows

should be discounted and there been no risk. Risk premium rate is the extra

return expected by the investor over the normal rate on account of the

project being risky. Therefore risk adjusted discount rate is a composite

discount rate that takes into account both the time and risk factors. A higher

discount rate will be used for more risky projects and lower rate for less risky

projects.

From the following data, state which project is better>

Year Cash inflows

Project X Project Y

0 -10,000 -10,000

1 5,000 6,000

2 4,000 6,000

3 2,000 4,000

Riskless discount rate is 5%. Project X is less risky as compared to

Project Y. the management considers risk premium rates at 5% and 10%

respectively appropriate for discounting the cash inflows.

Solution:

Project Risk adjusted discount rate

X 5% + 5% = 10%

Y 5% + 10% = 15%

Year Discounted Cash inflows

Project X Project Y

0 -10,000 -10,000

1 4,545 5,218

2 3,320 4,536

3 1,502 2,630

--------- ---------NPV - 633 2,384

--------- ---------

Project Y is superior to Project X. since NPV is positive it may be accepted.

Sensitivity analysis

Where cash inflows are very sensitive under different circumstances,

more than one forecast of the future cash inflows may be made. These

inflows may be regarded as 'Optimistic', 'Most Likely' and 'Pessimistic'.

Further cash inflows may be discounted to find out the NPV under these

three different situations. If the NPV under the three situations differ widely it

implies that there is a great risk in the project and the investor's decision to

accept or reject a project will depend upon his risk bearing abilities

Illustration

Mr. Tanu is considering tow mutually exclusive projects A and B. You

are required to advise him about the acceptability of the projects from the

following information.

Project A

Rs.

Project B

Rs.

Cost of the Investment

Forecast Cash Inflows per

annum for 5 years

Optimistic

Most Likely

Pessimistic

(The cut-off rate is 15%)

50,000

35,000

25,000

20,000

50,000

40,000

20,000

5,000

Solution

Computation of NPV of cash in flows at a Discount Rate of 15%

(Annuity of Re. 1 for 5 years)

Project A Project B

Annual

cash

inflow

Discou

nt

factor

@ 15%

Present

Value

NPV Annual

cash

inflow

Discou

nt

factor

@ 15%

Present

Value

NPV

Optimistic

Most Likely

35,000

25,000

3.3522

3.3522

1,17,327

83,805

67,327

33,805

40,000

20,000

3.3522

3.3522

1,34,088

67,044

84,088

17,044

Pessimistic 20,000 3.3522 67,044 17,044 5,000 3.3522 16,761 -33,239

The NPV calculated above indicate that Project B is more risky as compared

to Project A. at the same time during favorable conditions, it is more

profitable.

Probability Technique

A probability is a relative frequency with which an event may occur in

the future. When future estimates of cash inflows have different probabilities

the expected monetary values may be computed by multiplying cash inflow

with the probability assigned.

Illustration:

The ABC company Limited has given the following possible cash inflows fro

two of their projects X and Y out of which one they wish to undertake

together with their associated probabilities. Both the projects will require an

equal investment of Rs. 5,000.

You are required to give your considered opinion regarding the

selection of the project.

Project X Project Y

Possible

event

Cash inflows Probability Cash

inflows

Probabilit

y

A

B

C

D

E

4,000

5,000

6,000

7,000

8,000

.10

.20

.40

.20

.10

12,000

10,000

8,000

6,000

4,000

.10

.15

.50

.15

.10

Solution:

Computation of Expected Monetary values for Project X and Project Y

Project X Project Y

Cash Probabilit Expect Cash Probabili Expecte

inflows y ed

value

inflows ty d value

A

B

C

D

E

4,000

5,000

6,000

7,000

8,000

Total

.10

.20

.40

.20

.10

Rs. 400

1,000

2,400

1,400

800

6000

12,000

10,000

8,000

6,000

4,000

Total

.10

.15

.50

.15

.10

1,200

1,500

4,000

900

400

8,000

The expected monetary value of Project Y is higher than the expected

monetary value of Project X. Hence Project Y is preferable to project X.

Decision Tree Analysis

Decision tree anlysis is another technique which is helpful in tackling

risky capital investment proposals. Decision tree is a graphic display of

relationship between a present decision and possible future events, future

decisions and their consequences. The sequence of event is mapped out

over time in a format resembling branches of a tree. In other words, it is a

pictorial representation in tree form which indicates the magnitude,

probability and interrelationship of all possible outcomes.