Embed Size (px)

Citation preview

LEARNING OBJECTIVES AND CHAPTER COMPETENCIES

After studying Chapter 10, you should be able to demonstrate the following competencies:

COMPETENCY Know Apply

LO1 UNDERSTAND THE BASICS OF CAPITAL BUDGETING ANALYSIS.

CC1 Describe some business decisions that rely on capital budgeting analysis. •CC2 Explain the distinction between screening decisions and preference

decisions.•

CC3A Compute the present value of a series of cash flows. •CC4 Determine the acceptability of an investment project using the net present

value (NPV) method.•

CC5 Describe the typical cash flows in a capital budgeting analysis without taxes. •CC6 Outline the simplifying assumptions made in a capital budgeting analysis. •CC7 Explain the logic of ignoring financing-related cash flows and the choice of

the appropriate discount rate in capital budgeting analysis.•

LO2 UNDERSTAND AND APPLY ALTERNATIVE METHODS TO ANALYZECAPITAL INVESTMENTS.

CC8 Prepare an NPV analysis of two competing projects using either the total costapproach or the incremental cost approach.

•CC9 Compute the NPV of a project when no revenues are involved. •CC10 Rank projects in order of preference using the profitability index. •CC11 Compute the internal rate of return (IRR) of a project, interpret it, and explain

its use for project selection.• •

CC12 Compare and contrast the IRR and NPV methods in project selection. •CC13 Calculate the payback period of an investment project. •CC14 Explain the payback method and its potential to mislead a manager. •

10Capital Budgeting Decisions

WWW.TEX-CETERA.WS

COMPETENCY Know Apply

CC15 Calculate the simple rate of return (SRR) of an investment project. •CC16 Explain the disadvantages of the SRR method for project selection. •LO3 UNDERSTAND AND INCORPORATE THE EFFECTS OF INFLATION ON

CASH FLOWS IN CAPITAL BUDGETING.

CC17B Explain the distinction between real and nominal cash flows. •CC18B Compute the price index number for a future year given the annual rate of

inflation.•

CC19B Explain the distinction between real and nominal rates of return. •LO4 UNDERSTAND AND INCORPORATE THE EFFECTS OF TAXES ON CASH

FLOWS IN CAPITAL BUDGETING.

CC20C Explain the impact of tax-deductibility of depreciation (i.e., capital costallowance [CCA]).

•CC21C Compute the present value of CCA tax shields. •CC22C Compute the NPV of a project when cash flows related to the ownership and

disposal of depreciable property are included in the analysis.•

Note: The superscripts “A,” “B,” and “C” refer to Appendices 10A, 10B, and 10C respectively; all are available on Connect.

ON THE JOB

A FRAMEWORK FOR SUSTAINABLE GROWTHCapital investments are among the mostimportant decisions a company can make. Theseinvestments both enable a company to continueto operate in the future and position thecompany to exploit new opportunities—calledgrowth opportunities—to anchor its competitiveposition in the marketplace. So how docompanies allocate scarce funds to these twopurposes? The process underlying suchdecisions is the capital budgeting process, andevery company will have its own set of policiesand procedures that managers must follow whenseeking approval and funding for capitalprojects. At Calgary-based Suncor Energy, forexample, the decisions are based on expectedreturns, short-term cash flows, and risk. At CintasCorporation—a supplier of uniforms to variouscorporations—the capital proposals must beaccompanied by a financial analysis thatestimates the project’s cash inflows andoutflows. In addition, the assumptions underlyingthe cash flow estimates are carefully scrutinized

Stockbyte/Getty Images

574 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

so that the company can channel its limited capital funds toward the most profitable opportunities.Capital investments are good news stories because they signal expansions in enterprises. Conversely,in downturns, capital disinvestment occurs. Indeed, following the precipitous fall in oil prices in 2015,Suncor stepped back its capital investments and laid off personnel, as did much of the oil sector inAlberta.

Sources: “Suncor Energy Board Approves 2010 Capital Spending Plan,” press release, November 13, 2009, Suncor Energy

website, http://www.suncor.com/en/newsroom/2418.aspx?id 1076131; personal conversation between Peter C. Brewer and Paul

Carmichael, senior controller, Cintas Corporation.

Critical thinking question Given a number of investment opportunities, how should Suncordecide which projects should receive funding?

Note to student: See Guidance Answers online.

A Look Back A Look at This Chapter A Look Ahead

Chapter 9 presented a basicframework for the decision-makingprocess, centred on the notion ofrelevant costs and benefits, andused it in a wide variety ofsituations.

Chapter 10 expands the coverageof the decision-making process byfocusing on decisions aboutsignificant outlays on long-termprojects. A variety of techniquesused by managers faced withthese decisions are reviewed andillustrated.

Standard costs and varianceanalysis are covered in Chapter 11.This chapter introducesmanagement control andperformance measurement.

T he term capital budgeting is used to describe how managers plan significant outlays on projects that have long-termimplications, such as the purchase of new equipment and the introduction of new products. Most companies havemany more potential projects than can actually be funded. Hence, managers must carefully select those projects that

promise the greatest return. How well managers make these capital budgeting decisions is a critical factor in the long-termprofitability of the company.

Capital budgeting involves investment—a company must commit funds now in order to receive a return in the future.Investments are not limited to shares and bonds. Purchase of inventory or equipment is also an investment. For example,Yum! Brands, Inc. makes an investment when it opens a new Pizza Hut restaurant. Mountain Equipment Co-op makes aninvestment when it installs a new computer to handle customer billing. Chrysler makes an investment when it redesignsa product, such as the Jeep Compass, and has to retool its production lines. Merck & Co. invests in medical research.Amazon.ca makes an investment when it redesigns its website. All of these investments are characterized by a commitmentof funds today in the expectation of receiving a return in the future in the form of additional cash inflows or reduced cashoutflows.

CHAPTER 10: CAPITAL BUDGETING DECISIONS 575

WWW.TEX-CETERA.WS

Capital Budgeting—Planning Investments

Typical Capital Budgeting Decisions

LO1 • Know

CC1: Describe some business decisions that rely on capital budgeting analysis.

The types of business decisions that require capital budgeting analysis are virtually any decisions that involve an outlay now inorder to obtain some return (increase in revenue or reduction in costs) in the future. Typical capital budgeting decisions includethe following:

LO1 • Know

CC2: Explain the distinction between screening decisions and preference decisions.

Capital budgeting decisions tend to fall into two broad categories—screening decisions and preference decisions. Screeningdecisions are those relating to whether a proposed project meets some preset standard of acceptance. For example, a firm mighthave a policy of accepting projects only if they promise a return of, say, 20% on the investment. The required rate of return is theminimum rate of return a project must yield to be acceptable.

Preference decisions, by contrast, are those in which you select from among several competing courses of action. To illustrate,a firm might be considering several different machines to replace an existing machine on the assembly line. The choice of whichmachine to purchase is a preference decision.

In this chapter, we initially discuss ways of making screening decisions. Preference decisions are discussed toward the end ofthe chapter.

The Time Value of MoneyAs stated previously, business investments commonly involve returns that extend over fairly long periods. Therefore, inapproaching capital budgeting decisions, you must employ techniques that recognize the time value of money: (1) A dollartoday is worth more than a dollar a year from now. (2) Projects that promise returns earlier in time are preferable to those thatpromise returns later in time. The capital budgeting techniques that involve discounted cash flows recognize the preceding twocharacteristics of business investments most fully.

We will spend most of this chapter illustrating the use of discounted cash flow methods in making capital budgeting decisions.If you are not already familiar with discounting and the use of present value tables, you should read Appendix 10A on Connectbefore proceeding any further; present value tables are provided in Exhibits 10–1 and 10–2. (Note: Future value tables areavailable in Appendix 10D.)

• Cost reduction decisions: Should new equipment be purchased to reduce costs?• Expansion decisions: Should a new plant, warehouse, or other facility be acquired to increase capacity and sales?• Equipment selection decisions: Which of several available machines would be the most cost effective to purchase?• Lease-or-buy decisions: Should new equipment be leased or purchased?• Equipment replacement decisions: Should old equipment be replaced now or later?

576 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

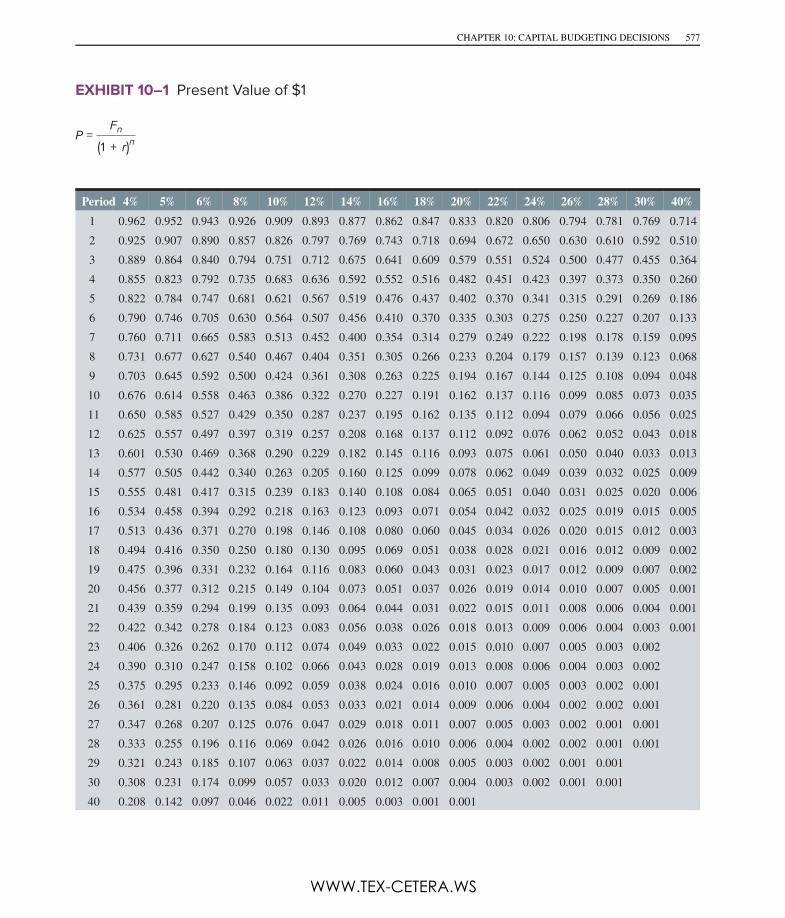

Period 4% 5% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28% 30% 40%1 0.962 0.952 0.943 0.926 0.909 0.893 0.877 0.862 0.847 0.833 0.820 0.806 0.794 0.781 0.769 0.7142 0.925 0.907 0.890 0.857 0.826 0.797 0.769 0.743 0.718 0.694 0.672 0.650 0.630 0.610 0.592 0.5103 0.889 0.864 0.840 0.794 0.751 0.712 0.675 0.641 0.609 0.579 0.551 0.524 0.500 0.477 0.455 0.3644 0.855 0.823 0.792 0.735 0.683 0.636 0.592 0.552 0.516 0.482 0.451 0.423 0.397 0.373 0.350 0.2605 0.822 0.784 0.747 0.681 0.621 0.567 0.519 0.476 0.437 0.402 0.370 0.341 0.315 0.291 0.269 0.1866 0.790 0.746 0.705 0.630 0.564 0.507 0.456 0.410 0.370 0.335 0.303 0.275 0.250 0.227 0.207 0.1337 0.760 0.711 0.665 0.583 0.513 0.452 0.400 0.354 0.314 0.279 0.249 0.222 0.198 0.178 0.159 0.0958 0.731 0.677 0.627 0.540 0.467 0.404 0.351 0.305 0.266 0.233 0.204 0.179 0.157 0.139 0.123 0.0689 0.703 0.645 0.592 0.500 0.424 0.361 0.308 0.263 0.225 0.194 0.167 0.144 0.125 0.108 0.094 0.04810 0.676 0.614 0.558 0.463 0.386 0.322 0.270 0.227 0.191 0.162 0.137 0.116 0.099 0.085 0.073 0.03511 0.650 0.585 0.527 0.429 0.350 0.287 0.237 0.195 0.162 0.135 0.112 0.094 0.079 0.066 0.056 0.02512 0.625 0.557 0.497 0.397 0.319 0.257 0.208 0.168 0.137 0.112 0.092 0.076 0.062 0.052 0.043 0.01813 0.601 0.530 0.469 0.368 0.290 0.229 0.182 0.145 0.116 0.093 0.075 0.061 0.050 0.040 0.033 0.01314 0.577 0.505 0.442 0.340 0.263 0.205 0.160 0.125 0.099 0.078 0.062 0.049 0.039 0.032 0.025 0.00915 0.555 0.481 0.417 0.315 0.239 0.183 0.140 0.108 0.084 0.065 0.051 0.040 0.031 0.025 0.020 0.00616 0.534 0.458 0.394 0.292 0.218 0.163 0.123 0.093 0.071 0.054 0.042 0.032 0.025 0.019 0.015 0.00517 0.513 0.436 0.371 0.270 0.198 0.146 0.108 0.080 0.060 0.045 0.034 0.026 0.020 0.015 0.012 0.00318 0.494 0.416 0.350 0.250 0.180 0.130 0.095 0.069 0.051 0.038 0.028 0.021 0.016 0.012 0.009 0.00219 0.475 0.396 0.331 0.232 0.164 0.116 0.083 0.060 0.043 0.031 0.023 0.017 0.012 0.009 0.007 0.00220 0.456 0.377 0.312 0.215 0.149 0.104 0.073 0.051 0.037 0.026 0.019 0.014 0.010 0.007 0.005 0.00121 0.439 0.359 0.294 0.199 0.135 0.093 0.064 0.044 0.031 0.022 0.015 0.011 0.008 0.006 0.004 0.00122 0.422 0.342 0.278 0.184 0.123 0.083 0.056 0.038 0.026 0.018 0.013 0.009 0.006 0.004 0.003 0.00123 0.406 0.326 0.262 0.170 0.112 0.074 0.049 0.033 0.022 0.015 0.010 0.007 0.005 0.003 0.00224 0.390 0.310 0.247 0.158 0.102 0.066 0.043 0.028 0.019 0.013 0.008 0.006 0.004 0.003 0.00225 0.375 0.295 0.233 0.146 0.092 0.059 0.038 0.024 0.016 0.010 0.007 0.005 0.003 0.002 0.00126 0.361 0.281 0.220 0.135 0.084 0.053 0.033 0.021 0.014 0.009 0.006 0.004 0.002 0.002 0.00127 0.347 0.268 0.207 0.125 0.076 0.047 0.029 0.018 0.011 0.007 0.005 0.003 0.002 0.001 0.00128 0.333 0.255 0.196 0.116 0.069 0.042 0.026 0.016 0.010 0.006 0.004 0.002 0.002 0.001 0.00129 0.321 0.243 0.185 0.107 0.063 0.037 0.022 0.014 0.008 0.005 0.003 0.002 0.001 0.00130 0.308 0.231 0.174 0.099 0.057 0.033 0.020 0.012 0.007 0.004 0.003 0.002 0.001 0.00140 0.208 0.142 0.097 0.046 0.022 0.011 0.005 0.003 0.001 0.001

EXHIBIT 10–1 Present Value of $1

P =Fn

(1 + r)n

CHAPTER 10: CAPITAL BUDGETING DECISIONS 577

WWW.TEX-CETERA.WS

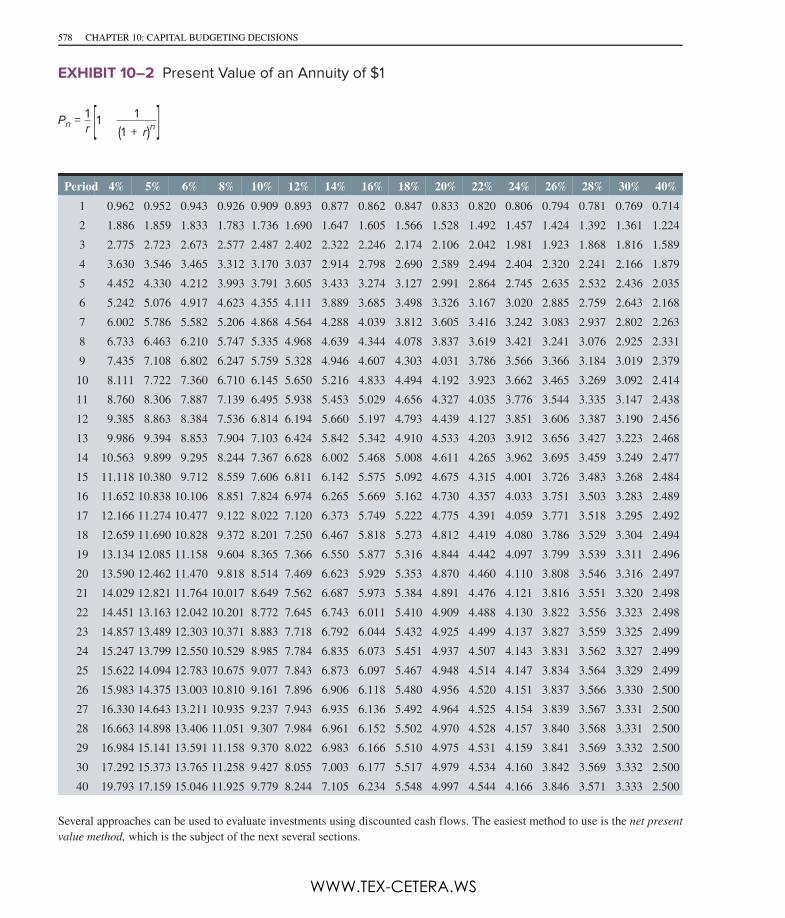

Period 4% 5% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28% 30% 40%1 0.962 0.952 0.943 0.926 0.909 0.893 0.877 0.862 0.847 0.833 0.820 0.806 0.794 0.781 0.769 0.7142 1.886 1.859 1.833 1.783 1.736 1.690 1.647 1.605 1.566 1.528 1.492 1.457 1.424 1.392 1.361 1.2243 2.775 2.723 2.673 2.577 2.487 2.402 2.322 2.246 2.174 2.106 2.042 1.981 1.923 1.868 1.816 1.5894 3.630 3.546 3.465 3.312 3.170 3.037 2.914 2.798 2.690 2.589 2.494 2.404 2.320 2.241 2.166 1.8795 4.452 4.330 4.212 3.993 3.791 3.605 3.433 3.274 3.127 2.991 2.864 2.745 2.635 2.532 2.436 2.0356 5.242 5.076 4.917 4.623 4.355 4.111 3.889 3.685 3.498 3.326 3.167 3.020 2.885 2.759 2.643 2.1687 6.002 5.786 5.582 5.206 4.868 4.564 4.288 4.039 3.812 3.605 3.416 3.242 3.083 2.937 2.802 2.2638 6.733 6.463 6.210 5.747 5.335 4.968 4.639 4.344 4.078 3.837 3.619 3.421 3.241 3.076 2.925 2.3319 7.435 7.108 6.802 6.247 5.759 5.328 4.946 4.607 4.303 4.031 3.786 3.566 3.366 3.184 3.019 2.379

10 8.111 7.722 7.360 6.710 6.145 5.650 5.216 4.833 4.494 4.192 3.923 3.662 3.465 3.269 3.092 2.41411 8.760 8.306 7.887 7.139 6.495 5.938 5.453 5.029 4.656 4.327 4.035 3.776 3.544 3.335 3.147 2.43812 9.385 8.863 8.384 7.536 6.814 6.194 5.660 5.197 4.793 4.439 4.127 3.851 3.606 3.387 3.190 2.45613 9.986 9.394 8.853 7.904 7.103 6.424 5.842 5.342 4.910 4.533 4.203 3.912 3.656 3.427 3.223 2.46814 10.563 9.899 9.295 8.244 7.367 6.628 6.002 5.468 5.008 4.611 4.265 3.962 3.695 3.459 3.249 2.47715 11.118 10.380 9.712 8.559 7.606 6.811 6.142 5.575 5.092 4.675 4.315 4.001 3.726 3.483 3.268 2.48416 11.652 10.838 10.106 8.851 7.824 6.974 6.265 5.669 5.162 4.730 4.357 4.033 3.751 3.503 3.283 2.48917 12.166 11.274 10.477 9.122 8.022 7.120 6.373 5.749 5.222 4.775 4.391 4.059 3.771 3.518 3.295 2.49218 12.659 11.690 10.828 9.372 8.201 7.250 6.467 5.818 5.273 4.812 4.419 4.080 3.786 3.529 3.304 2.49419 13.134 12.085 11.158 9.604 8.365 7.366 6.550 5.877 5.316 4.844 4.442 4.097 3.799 3.539 3.311 2.49620 13.590 12.462 11.470 9.818 8.514 7.469 6.623 5.929 5.353 4.870 4.460 4.110 3.808 3.546 3.316 2.49721 14.029 12.821 11.764 10.017 8.649 7.562 6.687 5.973 5.384 4.891 4.476 4.121 3.816 3.551 3.320 2.49822 14.451 13.163 12.042 10.201 8.772 7.645 6.743 6.011 5.410 4.909 4.488 4.130 3.822 3.556 3.323 2.49823 14.857 13.489 12.303 10.371 8.883 7.718 6.792 6.044 5.432 4.925 4.499 4.137 3.827 3.559 3.325 2.49924 15.247 13.799 12.550 10.529 8.985 7.784 6.835 6.073 5.451 4.937 4.507 4.143 3.831 3.562 3.327 2.49925 15.622 14.094 12.783 10.675 9.077 7.843 6.873 6.097 5.467 4.948 4.514 4.147 3.834 3.564 3.329 2.49926 15.983 14.375 13.003 10.810 9.161 7.896 6.906 6.118 5.480 4.956 4.520 4.151 3.837 3.566 3.330 2.50027 16.330 14.643 13.211 10.935 9.237 7.943 6.935 6.136 5.492 4.964 4.525 4.154 3.839 3.567 3.331 2.50028 16.663 14.898 13.406 11.051 9.307 7.984 6.961 6.152 5.502 4.970 4.528 4.157 3.840 3.568 3.331 2.50029 16.984 15.141 13.591 11.158 9.370 8.022 6.983 6.166 5.510 4.975 4.531 4.159 3.841 3.569 3.332 2.50030 17.292 15.373 13.765 11.258 9.427 8.055 7.003 6.177 5.517 4.979 4.534 4.160 3.842 3.569 3.332 2.50040 19.793 17.159 15.046 11.925 9.779 8.244 7.105 6.234 5.548 4.997 4.544 4.166 3.846 3.571 3.333 2.500

Several approaches can be used to evaluate investments using discounted cash flows. The easiest method to use is the net present

value method, which is the subject of the next several sections.

EXHIBIT 10–2 Present Value of an Annuity of $1

Pn = 1r [1 1

(1 + r)n ]

578 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

HELPFUL HINT

We discount two types of cash flows in this chapter:

IN BUSINESS

ECONOMIC CONDITIONS DICTATE CAPITAL BUDGETSWhen the health of the economy is uncertain, capital spending declines. Rite Aid CEO Mary Sammons cut hercompany’s capital budget by $50 million due to uncertain economic conditions. Estée Lauder tightened its beltby challenging managers to defend what they must have and define what they can give up. Yum! Brands (ownerof Pizza Hut, KFC, and Taco Bell) navigated the difficult economy by abandoning projects that might come true infavour of a must-have capital budgeting mentality.

Look at the recent news stories out of the Canadian oil patch. In 2015–2016, they spell out the woes of theoil firms—including large oil refiners and oil exploration companies, and the many companies that rely on theseenterprises to pull activity and value along the value chain. Emphasis during lean times will be on essentials justsufficient to maintain the enterprise until the turnaround occurs. In some cases companies may indeed exit anindustry entirely.

In contrast to these firms, for companies whose fuel costs are a significant fraction of their total operating costs,the low oil prices represent good news. In February 2016, Air Canada announced plans to purchase 45 C-Seriesjets from Bombardier with options for another 30. For Bombardier, this comes as welcome news because themanufacturer had only 243 firm orders as of early 2016.

Sources: Matthew Boyle, “The Budget Knives Come Out,” BusinessWeek, October 13, 2008, p. 30. For the Air Canada announcement, visit,

for example, http://newssaskatchewan.ca/2016/02/17/air canada says cseries fits into expansion plans/. Note that virtually every business

news outlet reported Air Canada’s announcement.

1. A single sum of money that is received (or paid) at a single point in the future. For example, if a companyexpects to sell a piece of equipment five years from today for $10,000, this amount represents a single sumof money that we assume the company will receive on the last day of the fifth year from now. Exhibit 10–1 isused to discount a single sum of money that will be received or paid in the future to its value as of today, alsoknown as its present value.

2. An annuity. An annuity refers to a series of identical sums of money that will be received or paid inconsecutive future periods. For example, if a company expects to receive $20,000 from customers annuallyfor each of the next five years, this amount represents an annuity that we assume the company will receiveon the last day of five consecutive years. Exhibit 10–2 is used to discount an annuity that will be received orpaid in consecutive future periods to its lump sum value as of today.

CHAPTER 10: CAPITAL BUDGETING DECISIONS 579

WWW.TEX-CETERA.WS

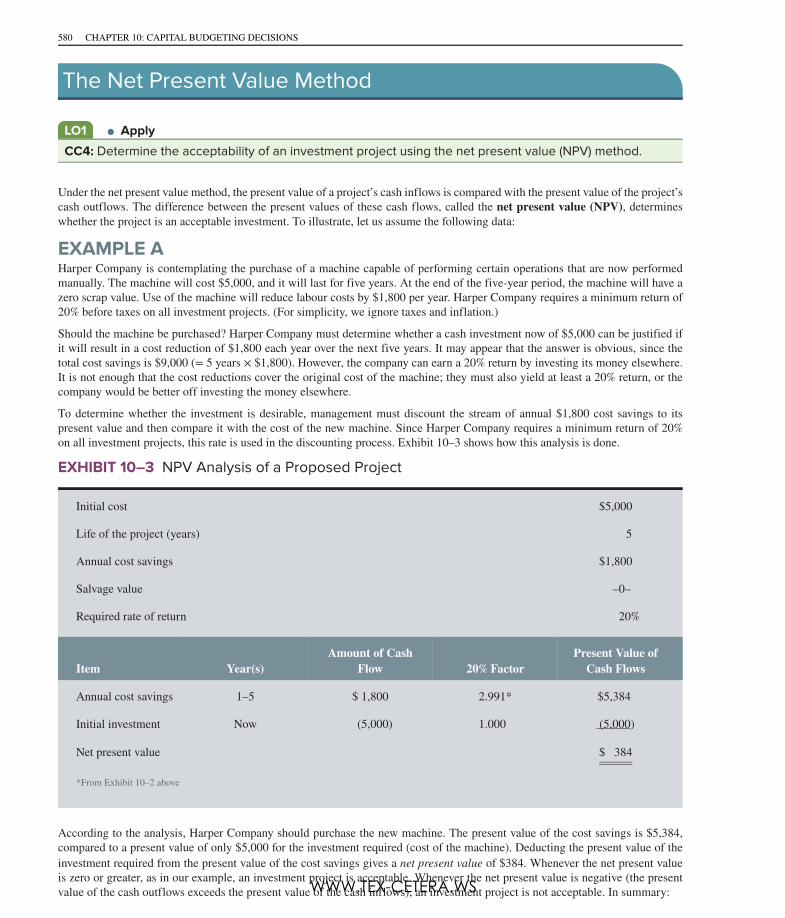

The Net Present Value Method

LO1 • Apply

CC4: Determine the acceptability of an investment project using the net present value (NPV) method.

Under the net present value method, the present value of a project’s cash inflows is compared with the present value of the project’scash outflows. The difference between the present values of these cash flows, called the net present value (NPV), determineswhether the project is an acceptable investment. To illustrate, let us assume the following data:

EXAMPLE AHarper Company is contemplating the purchase of a machine capable of performing certain operations that are now performedmanually. The machine will cost $5,000, and it will last for five years. At the end of the five-year period, the machine will have azero scrap value. Use of the machine will reduce labour costs by $1,800 per year. Harper Company requires a minimum return of20% before taxes on all investment projects. (For simplicity, we ignore taxes and inflation.)

Should the machine be purchased? Harper Company must determine whether a cash investment now of $5,000 can be justified ifit will result in a cost reduction of $1,800 each year over the next five years. It may appear that the answer is obvious, since thetotal cost savings is $9,000 (= 5 years × $1,800). However, the company can earn a 20% return by investing its money elsewhere.It is not enough that the cost reductions cover the original cost of the machine; they must also yield at least a 20% return, or thecompany would be better off investing the money elsewhere.

To determine whether the investment is desirable, management must discount the stream of annual $1,800 cost savings to itspresent value and then compare it with the cost of the new machine. Since Harper Company requires a minimum return of 20%on all investment projects, this rate is used in the discounting process. Exhibit 10–3 shows how this analysis is done.

Initial cost $5,000

Life of the project (years) 5

Annual cost savings $1,800

Salvage value –0–

Required rate of return 20%

Item Year(s)Amount of Cash

Flow 20% FactorPresent Value of

Cash Flows

Annual cost savings 1–5 $ 1,800 2.991* $5,384

Initial investment Now (5,000) 1.000 (5,000)

Net present value $ 384

*From Exhibit 10–2 above

According to the analysis, Harper Company should purchase the new machine. The present value of the cost savings is $5,384,compared to a present value of only $5,000 for the investment required (cost of the machine). Deducting the present value of theinvestment required from the present value of the cost savings gives a net present value of $384. Whenever the net present valueis zero or greater, as in our example, an investment project is acceptable Whenever the net present value is negative (the presentvalue of the cash outflows exceeds the present value of the cash inflows), an investment project is not acceptable. In summary:

EXHIBIT 10–3 NPV Analysis of a Proposed Project

580 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

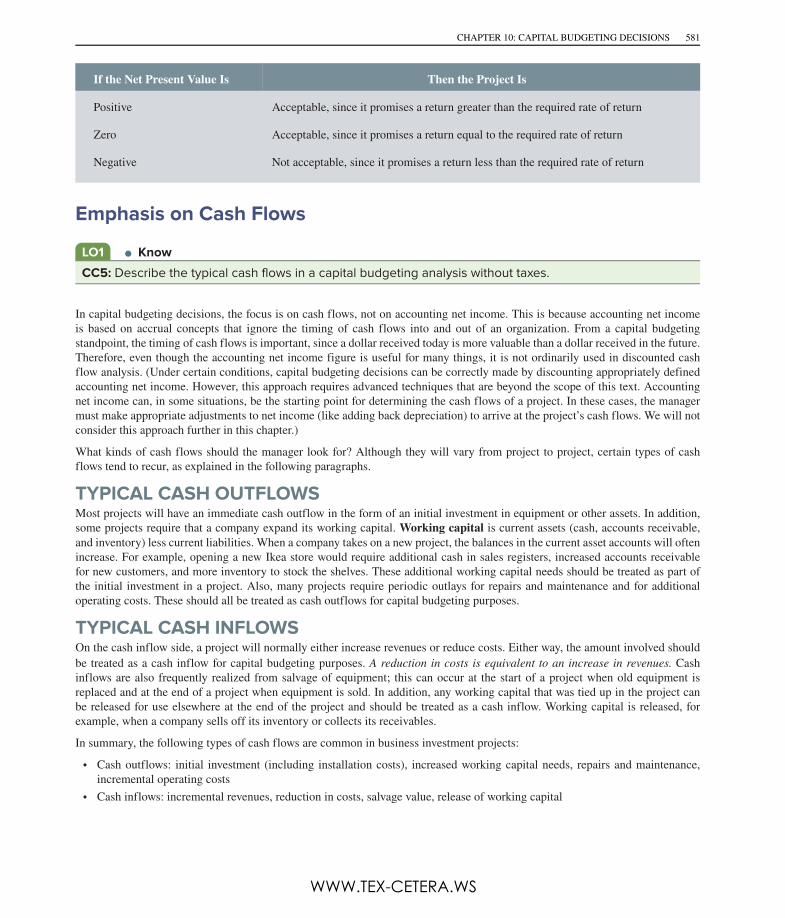

If the Net Present Value Is Then the Project Is

Positive Acceptable, since it promises a return greater than the required rate of return

Zero Acceptable, since it promises a return equal to the required rate of return

Negative Not acceptable, since it promises a return less than the required rate of return

Emphasis on Cash Flows

LO1 • Know

CC5: Describe the typical cash flows in a capital budgeting analysis without taxes.

In capital budgeting decisions, the focus is on cash flows, not on accounting net income. This is because accounting net incomeis based on accrual concepts that ignore the timing of cash flows into and out of an organization. From a capital budgetingstandpoint, the timing of cash flows is important, since a dollar received today is more valuable than a dollar received in the future.Therefore, even though the accounting net income figure is useful for many things, it is not ordinarily used in discounted cashflow analysis. (Under certain conditions, capital budgeting decisions can be correctly made by discounting appropriately definedaccounting net income. However, this approach requires advanced techniques that are beyond the scope of this text. Accountingnet income can, in some situations, be the starting point for determining the cash flows of a project. In these cases, the managermust make appropriate adjustments to net income (like adding back depreciation) to arrive at the project’s cash flows. We will notconsider this approach further in this chapter.)

What kinds of cash flows should the manager look for? Although they will vary from project to project, certain types of cashflows tend to recur, as explained in the following paragraphs.

TYPICAL CASH OUTFLOWSMost projects will have an immediate cash outflow in the form of an initial investment in equipment or other assets. In addition,some projects require that a company expand its working capital. Working capital is current assets (cash, accounts receivable,and inventory) less current liabilities. When a company takes on a new project, the balances in the current asset accounts will oftenincrease. For example, opening a new Ikea store would require additional cash in sales registers, increased accounts receivablefor new customers, and more inventory to stock the shelves. These additional working capital needs should be treated as part ofthe initial investment in a project. Also, many projects require periodic outlays for repairs and maintenance and for additionaloperating costs. These should all be treated as cash outflows for capital budgeting purposes.

TYPICAL CASH INFLOWSOn the cash inflow side, a project will normally either increase revenues or reduce costs. Either way, the amount involved shouldbe treated as a cash inflow for capital budgeting purposes. A reduction in costs is equivalent to an increase in revenues. Cashinflows are also frequently realized from salvage of equipment; this can occur at the start of a project when old equipment isreplaced and at the end of a project when equipment is sold. In addition, any working capital that was tied up in the project canbe released for use elsewhere at the end of the project and should be treated as a cash inflow. Working capital is released, forexample, when a company sells off its inventory or collects its receivables.

In summary, the following types of cash flows are common in business investment projects:

• Cash outflows: initial investment (including installation costs), increased working capital needs, repairs and maintenance,incremental operating costs

• Cash inflows: incremental revenues, reduction in costs, salvage value, release of working capital

CHAPTER 10: CAPITAL BUDGETING DECISIONS 581

WWW.TEX-CETERA.WS

Simplifying Assumptions

LO1 • Know

CC6: Outline the simplifying assumptions made in a capital budgeting analysis.

A number of assumptions underlie our treatment of the NPV method.

TIMING OF CASH FLOWSAll cash flows are assumed to occur at the end of the period. Typically cash flows will occur throughout a period, but ourassumption will make calculations easier.

REINVESTMENT OF CASH INFLOWSAll surplus cash inflows generated by the project are assumed to be immediately reinvested at a rate of return equal to the discountrate, until the end of the project. Without this assumption (e.g., if the cash flows from a project are simply kept locked up in a safeuntil the project ends), the net present value will not be accurate.

PROJECTS ARE CARBON COPIES OF THE FIRMThe risk of investing in a project is assumed to be identical to the risk you would face if you bought the company outright—thatis, if you purchased all of the outstanding securities of the company. This means that projects are basically clones of the companyin so far as risk is concerned. This assumption is very important to the choice of the discount rate in NPV analysis and to theprocedure for handling financing-related cash flows. This is explained below.

TREATMENT OF INFLATIONAlthough this is somewhat unrealistic, inflation is assumed not to be a factor. When inflation exists, we will need to adjust eitherthe cash flows or the discount rate. A brief discussion of these adjustments is provided in Appendix 10B on Connect.

INCOME TAXESThe NPV method usually considers cash flows only on an after-tax basis. This, in turn, requires that we use an after-tax discountrate and that we focus on after-tax cash flows. The effect of income taxes on revenues and costs should be fully reflected in theanalysis. As an example, if we assume a 30% tax rate, the after-tax amount of a cash inflow of $100 is $70 (= $100 × [1 − 0.30]).Similarly, we must also take into account the tax-deductibility of depreciation. Recall that depreciation is an expense item whencalculating income (it may be buried in the cost of goods sold or selling and administrative expenses on an income statement).Therefore, although depreciation in itself is not a cash flow, it is treated as an expense when calculating income taxes and henceresults in tax savings. These tax savings—called tax shields—are cash inflows and must be treated as such in any NPV analysisinvolving depreciable property. In Canada, a complex set of rules governs the calculation of depreciation for tax purposes. Theamount allowed as a deduction is called the capital cost allowance (CCA). These rules, as well as the techniques for calculatingCCA, after-tax discount rates, and after-tax cash flows, are discussed briefly in Appendix 10C on Connect. A more completetreatment can be found in advanced texts on corporate finance.

Choosing a Discount RateThe discount rate should be the company’s minimum required rate of return. What is a company’s minimum required rate ofreturn? The company’s cost of capital is usually regarded as the minimum required rate of return. The cost of capital is the averagerate of return the company must pay to its long-term creditors and to shareholders for the use of their funds. The cost of capital isthe minimum required rate of return, because if a project’s rate of return is less than the cost of capital, the company does not earnenough of a return to compensate its creditors and shareholders. Therefore, any project with a rate of return less than the cost ofcapital should not be accepted.

The cost of capital serves as a screening device in net present value analysis. When the cost of capital is used as the discountrate, any project with a negative net present value does not cover the company’s cost of capital and therefore should bediscarded as unacceptable.

582 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

Financing-Related Cash Flows

LO1 • Know

CC7: Explain the logic of ignoring financing-related cash flows and the choice of the appropriate discountrate in capital budgeting analysis.

A common source of confusion for students is how to handle cash inflows from borrowing and cash outflows for making interestpayments and principal repayments. Given our simplifying assumptions and our choice of the company’s cost of capital for thediscount rate, the rule is very simple: ignore all financing-related cash flows. The impact on the project of the financing decisionsmade to fund the project is captured in the company’s cost of capital—the discount rate. More advanced discussions of this topicwill consider specific cases where our simple rule requires modification. For our purposes, this rule will suffice.

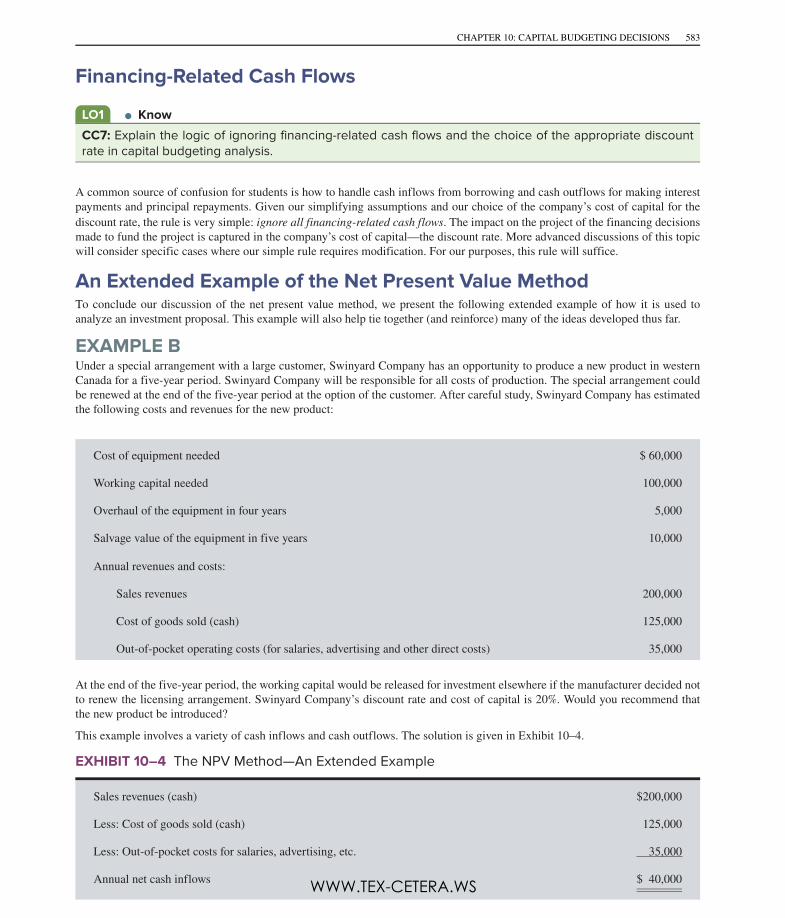

An Extended Example of the Net Present Value MethodTo conclude our discussion of the net present value method, we present the following extended example of how it is used toanalyze an investment proposal. This example will also help tie together (and reinforce) many of the ideas developed thus far.

EXAMPLE BUnder a special arrangement with a large customer, Swinyard Company has an opportunity to produce a new product in westernCanada for a five-year period. Swinyard Company will be responsible for all costs of production. The special arrangement couldbe renewed at the end of the five-year period at the option of the customer. After careful study, Swinyard Company has estimatedthe following costs and revenues for the new product:

Cost of equipment needed $ 60,000

Working capital needed 100,000

Overhaul of the equipment in four years 5,000

Salvage value of the equipment in five years 10,000

Annual revenues and costs:

Sales revenues 200,000

Cost of goods sold (cash) 125,000

Out-of-pocket operating costs (for salaries, advertising and other direct costs) 35,000

At the end of the five-year period, the working capital would be released for investment elsewhere if the manufacturer decided notto renew the licensing arrangement. Swinyard Company’s discount rate and cost of capital is 20%. Would you recommend thatthe new product be introduced?

This example involves a variety of cash inflows and cash outflows. The solution is given in Exhibit 10–4.

Sales revenues (cash) $200,000

Less: Cost of goods sold (cash) 125,000

Less: Out-of-pocket costs for salaries, advertising, etc. 35,000

Annual net cash inflows $ 40,000

EXHIBIT 10–4 The NPV Method—An Extended Example

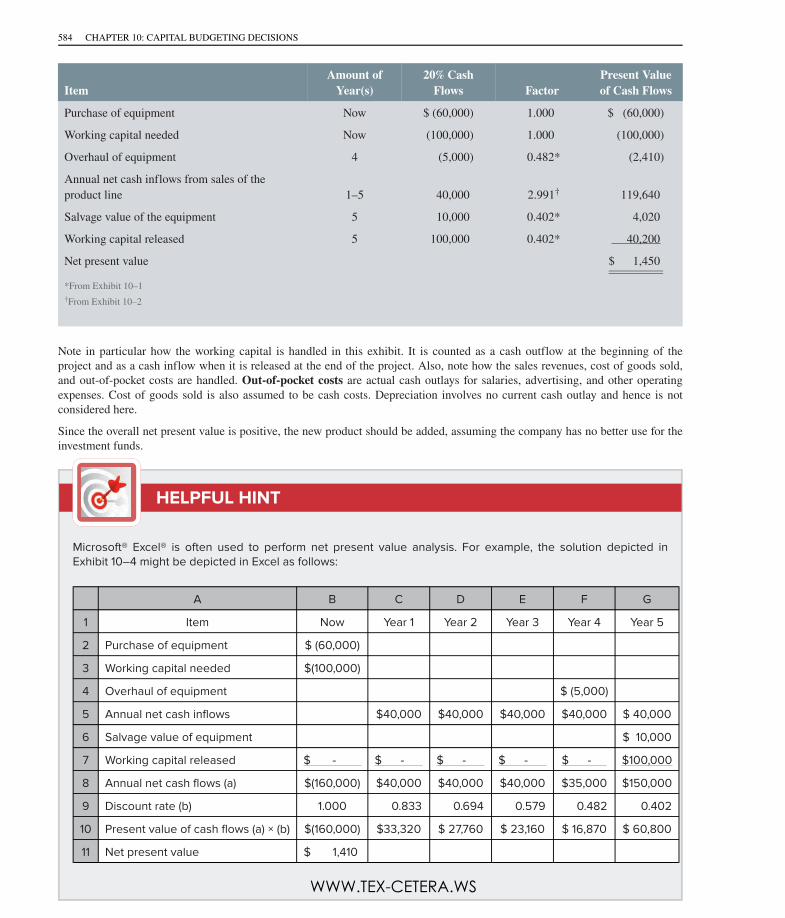

CHAPTER 10: CAPITAL BUDGETING DECISIONS 583

WWW.TEX-CETERA.WS

ItemAmount of

Year(s)20% Cash

Flows FactorPresent Valueof Cash Flows

Purchase of equipment Now $ (60,000) 1.000 $ (60,000)

Working capital needed Now (100,000) 1.000 (100,000)

Overhaul of equipment 4 (5,000) 0.482* (2,410)

Annual net cash inflows from sales of theproduct line 1–5 40,000 2.991† 119,640

Salvage value of the equipment 5 10,000 0.402* 4,020

Working capital released 5 100,000 0.402* 40,200

Net present value $ 1,450

*From Exhibit 10–1†From Exhibit 10–2

Note in particular how the working capital is handled in this exhibit. It is counted as a cash outflow at the beginning of theproject and as a cash inflow when it is released at the end of the project. Also, note how the sales revenues, cost of goods sold,and out-of-pocket costs are handled. Out-of-pocket costs are actual cash outlays for salaries, advertising, and other operatingexpenses. Cost of goods sold is also assumed to be cash costs. Depreciation involves no current cash outlay and hence is notconsidered here.

Since the overall net present value is positive, the new product should be added, assuming the company has no better use for theinvestment funds.

HELPFUL HINT

Microsoft® Excel® is often used to perform net present value analysis. For example, the solution depicted inExhibit 10–4 might be depicted in Excel as follows:

A B C D E F G

1 Item Now Year 1 Year 2 Year 3 Year 4 Year 5

2 Purchase of equipment $ (60,000)

3 Working capital needed $(100,000)

4 Overhaul of equipment $ (5,000)

5 Annual net cash inflows $40,000 $40,000 $40,000 $40,000 $ 40,000

6 Salvage value of equipment $ 10,000

7 Working capital released $ - $ - $ - $ - $ - $100,000

8 Annual net cash flows (a) $(160,000) $40,000 $40,000 $40,000 $35,000 $150,000

9 Discount rate (b) 1.000 0.833 0.694 0.579 0.482 0.402

10 Present value of cash flows (a) × (b) $(160,000) $33,320 $ 27,760 $ 23,160 $ 16,870 $ 60,800

11 Net present value $ 1,410

584 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

This approach creates one column in the spreadsheet for “Now” and one for each year (year 1 through year 5). Allcash flows are inserted into the column of the spreadsheet that corresponds to when they occur. For example, the$60,000 purchase of equipment appears in the “Now” column because the cash outflow takes place immediately.In addition, all cash flows, including annuities, are discounted using the factors from Exhibit 10–1. For example,although the $40,000 annual net cash inflows that are shown above represent an annuity, each of these five$40,000 amounts is discounted using factors from Exhibit 10–1.

The net present value of $1,410 that is shown in cell B11 is computed by adding together cells B10 through G10.This amount is $40 lower than the net present value shown in Exhibit 10–4; however, this difference exists solelybecause the discount factors in Exhibits 10–1 and 10–2 have been rounded to three decimal places.

IN BUSINESS

ASIAN BUSINESSES INVESTING IN CANADAForeign investment in Canada is not new, with many American businesses having set up shop in Canada. Morerecently, the Canadian resource sector has attracted Asian interest. Chinese energy giants CNOOC and Sinopechave expressed interest in investing billions of dollars in the potash, fertilizer, and oil sectors. Quite in contrast tothe resource sector, another group of Chinese investors is planning the development of a mega-mall in Dundurn,Saskatchewan. The proposed mall, when fully constructed, is expected to be larger than the West Edmonton Mallin terms of square footage. As another example, Indian company Central Pulp & Paper Inc. will build a wheatstraw-based paper plant in Manitoba for Winnipeg-based Prairie Pulp & Paper Inc. (PPPI). While the investment willexceed $500 million, it is expected to reduce PPPI’s annual costs by $5 million.

But, in a delicate balancing act, Canada must weigh the influx of capital against loss of control of potentiallystrategic resources which could impact national interest. This was seen by Saskatchewan’s rejection of a bidfor the province’s potash business by BHP Billiton, which abandoned its plan to buy a stake in PotashCorpof Saskatchewan. On the West Coast, Asian interests have flocked to participate in the boom experienced inVancouver’s technology, digital entertainment, interactive, and green-economy sectors. The favourable exchangerate for the Canadian dollar against its US counterpart and a competitive tax regime are a couple of factorscomplementing the strengths in these sectors in Canada.

Sources: Jason Fekte, “Chinese Energy Giants Set Sights on Potash; Documents Show Canada a Target for Investment in Resource Sector,”

The Ottawa Citizen, November 2, 2012, p. A.1, http://www2.canada.com/ottawacitizen/news/story.html?id 30f4c684 b1b5 46a3 8d63

bdfb3659d5cc; Jeff Davis, “Dundurn Mega Mall Plan Gets Official Launch Date,” Leader Post [Regina, Sask], March 16, 2013, p. B.4,

http://www.leaderpost.com/news/Dundurn+megamall+plan+gets+official+launch+date/8108522/story.html; “14 Canada India Deals in the

Spotlight,” CBC News, posted November 5, 2012, http://www.cbc.ca/news/business/story/2012/11/05/pol trade deals india.html. For news of

the fate of Billiton’s plan to buy PotashCorp. see https://search.yahoo.com/yhs/search?p BHP+Billiton+loss+of+Potash+bid&ei UTF 8&

hspart mozilla&hsimp yhs 004. http://www.worldeyereports.com/reports/article/asian business and investment flocks to vancouver/.

CHAPTER 10: CAPITAL BUDGETING DECISIONS 585

WWW.TEX-CETERA.WS

Expanding the Net Present Value Method

LO2 • Know

CC8: Prepare an NPV analysis of two competing projects using either the total cost approach or theincremental cost approach.

So far, our examples have involved only a single investment alternative. We will now expand the NPV method to include twoalternatives. Note that if all projects have a negative net present value, none should be accepted. In addition, we will integrate theconcept of relevant costs into the discounted cash flow analysis.

The NPV method can be used to compare competing investment projects in two ways. One is the total cost approach, and theother is the incremental cost approach. Each approach is illustrated below.

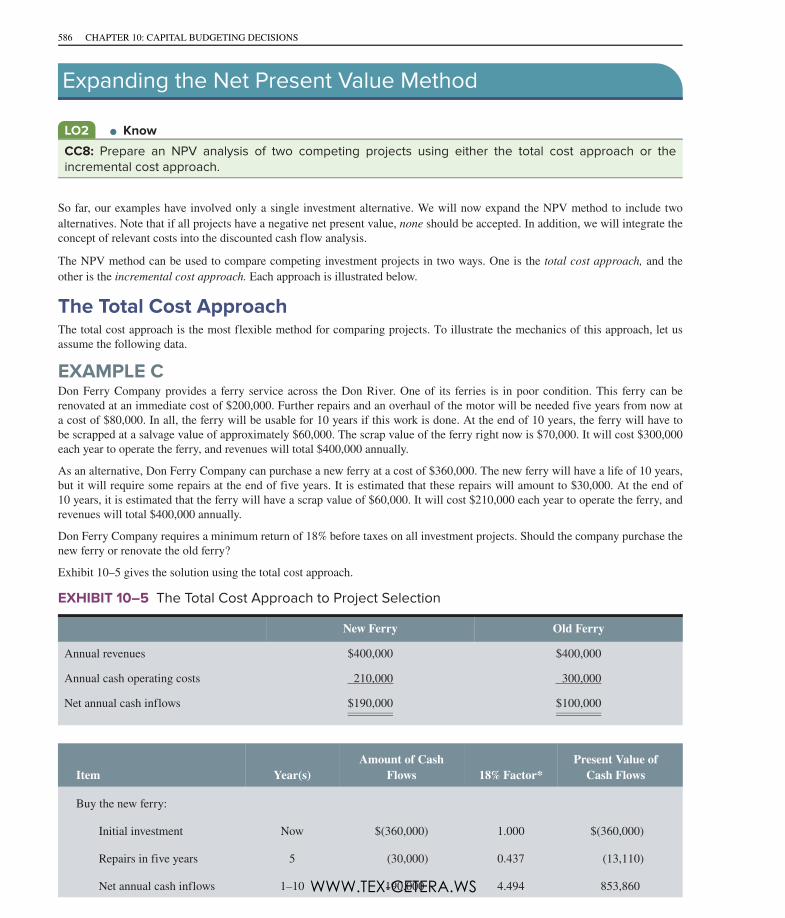

The Total Cost ApproachThe total cost approach is the most flexible method for comparing projects. To illustrate the mechanics of this approach, let usassume the following data.

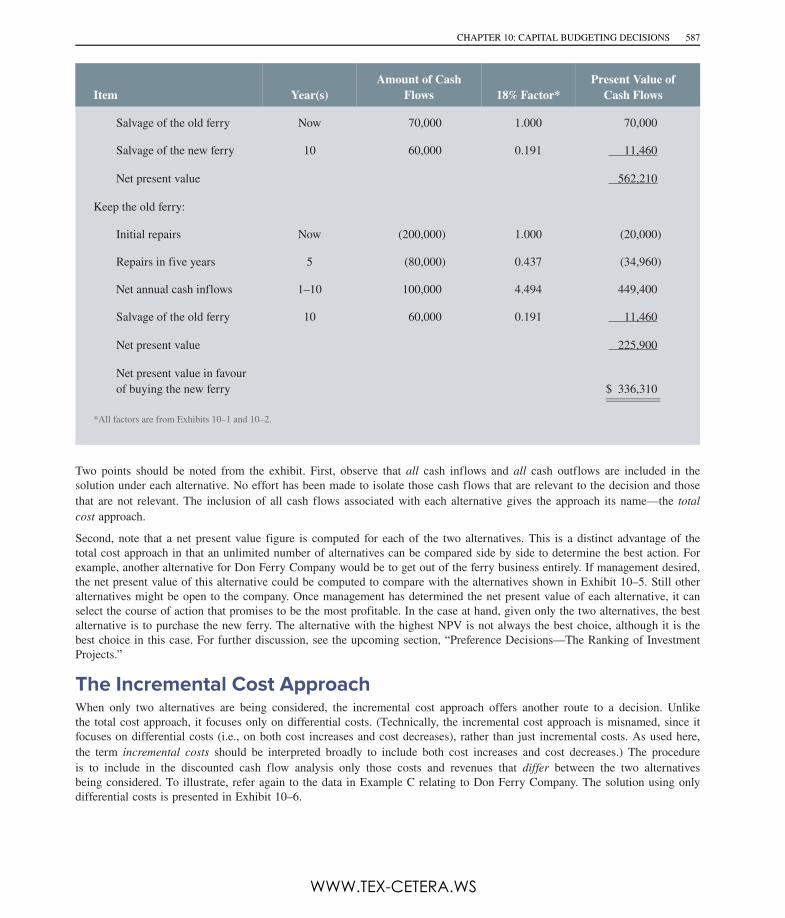

EXAMPLE CDon Ferry Company provides a ferry service across the Don River. One of its ferries is in poor condition. This ferry can berenovated at an immediate cost of $200,000. Further repairs and an overhaul of the motor will be needed five years from now ata cost of $80,000. In all, the ferry will be usable for 10 years if this work is done. At the end of 10 years, the ferry will have tobe scrapped at a salvage value of approximately $60,000. The scrap value of the ferry right now is $70,000. It will cost $300,000each year to operate the ferry, and revenues will total $400,000 annually.

As an alternative, Don Ferry Company can purchase a new ferry at a cost of $360,000. The new ferry will have a life of 10 years,but it will require some repairs at the end of five years. It is estimated that these repairs will amount to $30,000. At the end of10 years, it is estimated that the ferry will have a scrap value of $60,000. It will cost $210,000 each year to operate the ferry, andrevenues will total $400,000 annually.

Don Ferry Company requires a minimum return of 18% before taxes on all investment projects. Should the company purchase thenew ferry or renovate the old ferry?

Exhibit 10–5 gives the solution using the total cost approach.

New Ferry Old Ferry

Annual revenues $400,000 $400,000

Annual cash operating costs 210,000 300,000

Net annual cash inflows $190,000 $100,000

Item Year(s)Amount of Cash

Flows 18% Factor*Present Value of

Cash Flows

Buy the new ferry:

Initial investment Now $(360,000) 1.000 $(360,000)

Repairs in five years 5 (30,000) 0.437 (13,110)

Net annual cash inflows 1–10 190,000 4.494 853,860

EXHIBIT 10–5 The Total Cost Approach to Project Selection

586 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

Item Year(s)Amount of Cash

Flows 18% Factor*Present Value of

Cash Flows

Salvage of the old ferry Now 70,000 1.000 70,000

Salvage of the new ferry 10 60,000 0.191 11,460

Net present value 562,210

Keep the old ferry:

Initial repairs Now (200,000) 1.000 (20,000)

Repairs in five years 5 (80,000) 0.437 (34,960)

Net annual cash inflows 1–10 100,000 4.494 449,400

Salvage of the old ferry 10 60,000 0.191 11,460

Net present value 225,900

Net present value in favourof buying the new ferry $ 336,310

*All factors are from Exhibits 10–1 and 10–2.

Two points should be noted from the exhibit. First, observe that all cash inflows and all cash outflows are included in thesolution under each alternative. No effort has been made to isolate those cash flows that are relevant to the decision and thosethat are not relevant. The inclusion of all cash flows associated with each alternative gives the approach its name—the total

cost approach.

Second, note that a net present value figure is computed for each of the two alternatives. This is a distinct advantage of thetotal cost approach in that an unlimited number of alternatives can be compared side by side to determine the best action. Forexample, another alternative for Don Ferry Company would be to get out of the ferry business entirely. If management desired,the net present value of this alternative could be computed to compare with the alternatives shown in Exhibit 10–5. Still otheralternatives might be open to the company. Once management has determined the net present value of each alternative, it canselect the course of action that promises to be the most profitable. In the case at hand, given only the two alternatives, the bestalternative is to purchase the new ferry. The alternative with the highest NPV is not always the best choice, although it is thebest choice in this case. For further discussion, see the upcoming section, “Preference Decisions—The Ranking of InvestmentProjects.”

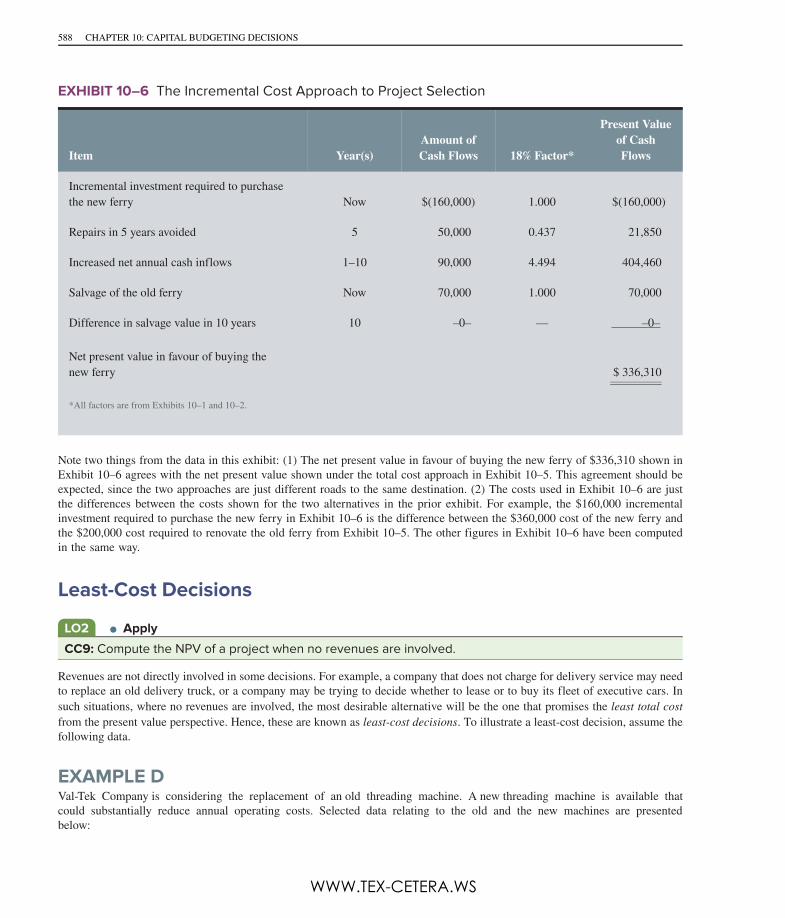

The Incremental Cost ApproachWhen only two alternatives are being considered, the incremental cost approach offers another route to a decision. Unlikethe total cost approach, it focuses only on differential costs. (Technically, the incremental cost approach is misnamed, since itfocuses on differential costs (i.e., on both cost increases and cost decreases), rather than just incremental costs. As used here,the term incremental costs should be interpreted broadly to include both cost increases and cost decreases.) The procedureis to include in the discounted cash flow analysis only those costs and revenues that differ between the two alternativesbeing considered. To illustrate, refer again to the data in Example C relating to Don Ferry Company. The solution using onlydifferential costs is presented in Exhibit 10–6.

CHAPTER 10: CAPITAL BUDGETING DECISIONS 587

WWW.TEX-CETERA.WS

Item Year(s)Amount ofCash Flows 18% Factor*

Present Valueof CashFlows

Incremental investment required to purchasethe new ferry Now $(160,000) 1.000 $(160,000)

Repairs in 5 years avoided 5 50,000 0.437 21,850

Increased net annual cash inflows 1–10 90,000 4.494 404,460

Salvage of the old ferry Now 70,000 1.000 70,000

Difference in salvage value in 10 years 10 –0– — –0–

Net present value in favour of buying thenew ferry $ 336,310

*All factors are from Exhibits 10–1 and 10–2.

Note two things from the data in this exhibit: (1) The net present value in favour of buying the new ferry of $336,310 shown inExhibit 10–6 agrees with the net present value shown under the total cost approach in Exhibit 10–5. This agreement should beexpected, since the two approaches are just different roads to the same destination. (2) The costs used in Exhibit 10–6 are justthe differences between the costs shown for the two alternatives in the prior exhibit. For example, the $160,000 incrementalinvestment required to purchase the new ferry in Exhibit 10–6 is the difference between the $360,000 cost of the new ferry andthe $200,000 cost required to renovate the old ferry from Exhibit 10–5. The other figures in Exhibit 10–6 have been computedin the same way.

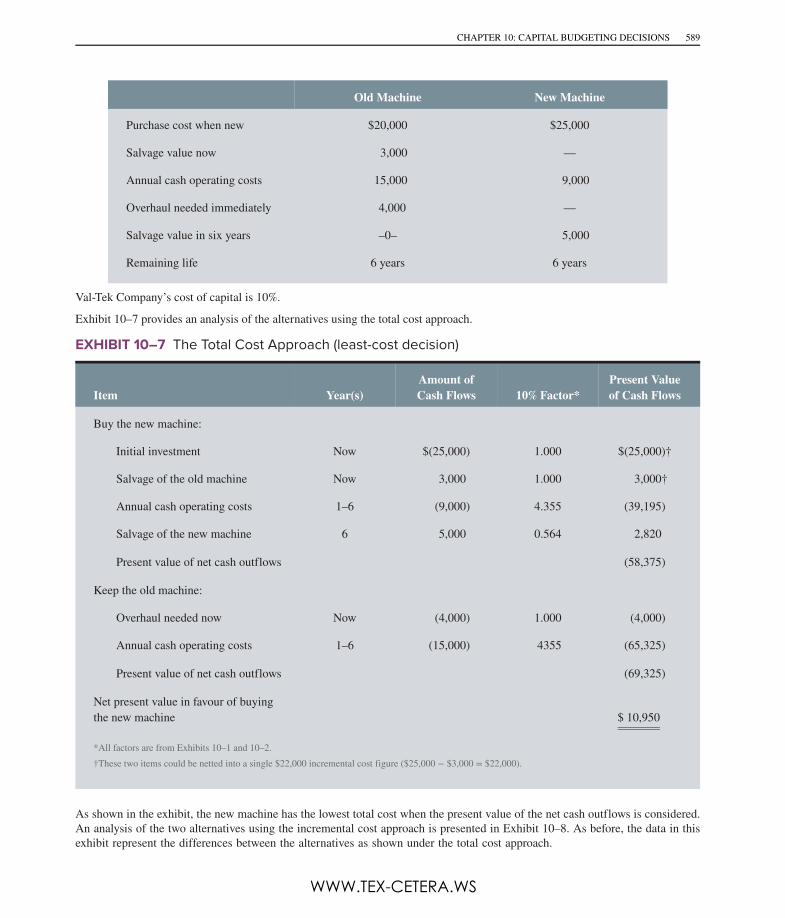

Least-Cost Decisions

LO2 • Apply

CC9: Compute the NPV of a project when no revenues are involved.

Revenues are not directly involved in some decisions. For example, a company that does not charge for delivery service may needto replace an old delivery truck, or a company may be trying to decide whether to lease or to buy its fleet of executive cars. Insuch situations, where no revenues are involved, the most desirable alternative will be the one that promises the least total cost

from the present value perspective. Hence, these are known as least-cost decisions. To illustrate a least-cost decision, assume thefollowing data.

EXAMPLE DVal-Tek Company is considering the replacement of an old threading machine. A new threading machine is available thatcould substantially reduce annual operating costs. Selected data relating to the old and the new machines are presentedbelow:

EXHIBIT 10–6 The Incremental Cost Approach to Project Selection

588 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

Old Machine New Machine

Purchase cost when new $20,000 $25,000

Salvage value now 3,000 —

Annual cash operating costs 15,000 9,000

Overhaul needed immediately 4,000 —

Salvage value in six years –0– 5,000

Remaining life 6 years 6 years

Val-Tek Company’s cost of capital is 10%.

Exhibit 10–7 provides an analysis of the alternatives using the total cost approach.

Item Year(s)Amount ofCash Flows 10% Factor*

Present Valueof Cash Flows

Buy the new machine:

Initial investment Now $(25,000) 1.000 $(25,000)†

Salvage of the old machine Now 3,000 1.000 3,000†

Annual cash operating costs 1–6 (9,000) 4.355 (39,195)

Salvage of the new machine 6 5,000 0.564 2,820

Present value of net cash outflows (58,375)

Keep the old machine:

Overhaul needed now Now (4,000) 1.000 (4,000)

Annual cash operating costs 1–6 (15,000) 4355 (65,325)

Present value of net cash outflows (69,325)

Net present value in favour of buyingthe new machine $ 10,950

*All factors are from Exhibits 10–1 and 10–2.†These two items could be netted into a single $22,000 incremental cost figure ($25,000 − $3,000 = $22,000).

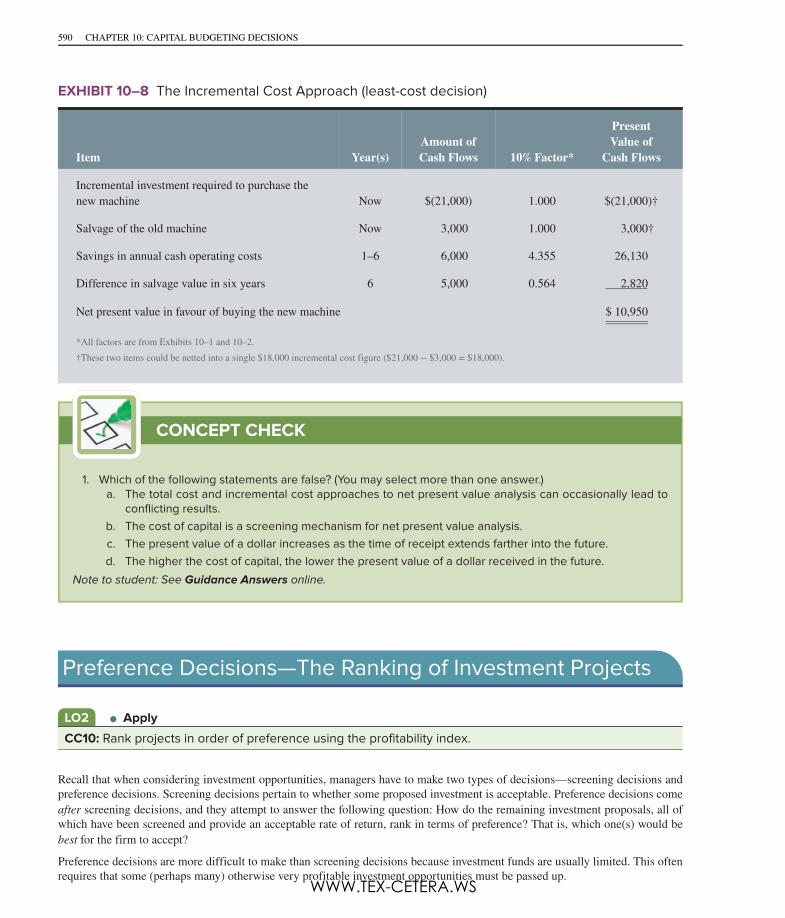

As shown in the exhibit, the new machine has the lowest total cost when the present value of the net cash outflows is considered.An analysis of the two alternatives using the incremental cost approach is presented in Exhibit 10–8. As before, the data in thisexhibit represent the differences between the alternatives as shown under the total cost approach.

EXHIBIT 10–7 The Total Cost Approach (least-cost decision)

CHAPTER 10: CAPITAL BUDGETING DECISIONS 589

WWW.TEX-CETERA.WS

Item Year(s)Amount ofCash Flows 10% Factor*

PresentValue of

Cash Flows

Incremental investment required to purchase thenew machine Now $(21,000) 1.000 $(21,000)†

Salvage of the old machine Now 3,000 1.000 3,000†

Savings in annual cash operating costs 1–6 6,000 4.355 26,130

Difference in salvage value in six years 6 5,000 0.564 2,820

Net present value in favour of buying the new machine $ 10,950

*All factors are from Exhibits 10–1 and 10–2.†These two items could be netted into a single $18,000 incremental cost figure ($21,000 − $3,000 = $18,000).

CONCEPT CHECK

Note to student: See Guidance Answers online.

Preference Decisions—The Ranking of Investment Projects

LO2 • Apply

CC10: Rank projects in order of preference using the profitability index.

Recall that when considering investment opportunities, managers have to make two types of decisions—screening decisions andpreference decisions. Screening decisions pertain to whether some proposed investment is acceptable. Preference decisions comeafter screening decisions, and they attempt to answer the following question: How do the remaining investment proposals, all ofwhich have been screened and provide an acceptable rate of return, rank in terms of preference? That is, which one(s) would bebest for the firm to accept?

Preference decisions are more difficult to make than screening decisions because investment funds are usually limited. This oftenrequires that some (perhaps many) otherwise very profitable investment opportunities must be passed up.

EXHIBIT 10–8 The Incremental Cost Approach (least-cost decision)

1. Which of the following statements are false? (You may select more than one answer.)a. The total cost and incremental cost approaches to net present value analysis can occasionally lead to

conflicting results.b. The cost of capital is a screening mechanism for net present value analysis.c. The present value of a dollar increases as the time of receipt extends farther into the future.d. The higher the cost of capital, the lower the present value of a dollar received in the future.

590 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

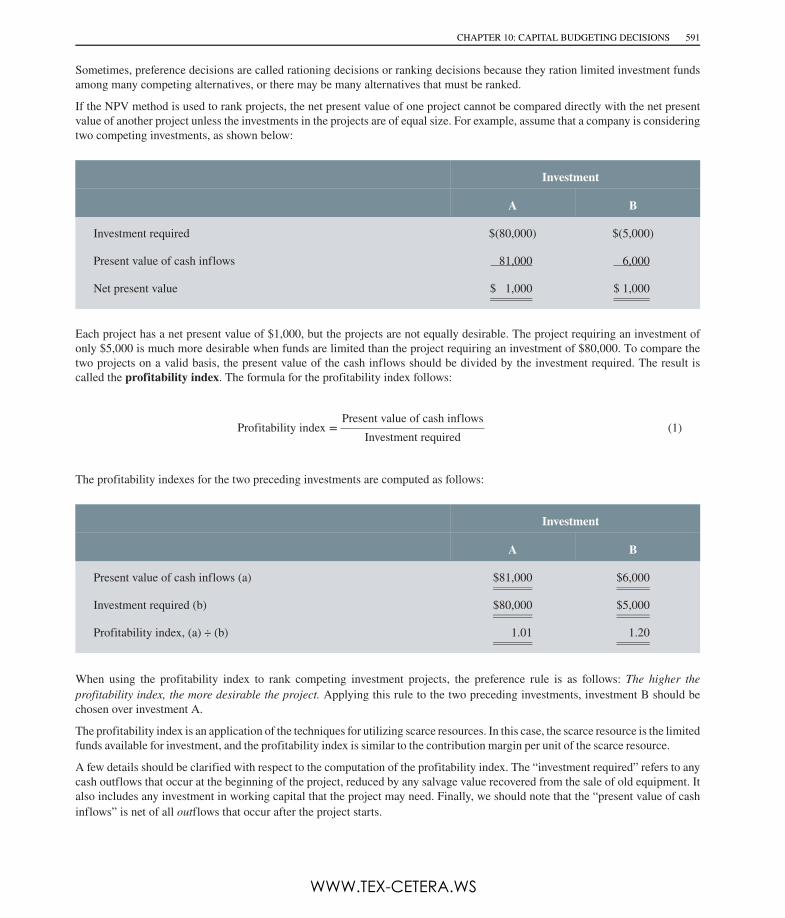

Sometimes, preference decisions are called rationing decisions or ranking decisions because they ration limited investment fundsamong many competing alternatives, or there may be many alternatives that must be ranked.

If the NPV method is used to rank projects, the net present value of one project cannot be compared directly with the net presentvalue of another project unless the investments in the projects are of equal size. For example, assume that a company is consideringtwo competing investments, as shown below:

Investment

A B

Investment required $(80,000) $(5,000)

Present value of cash inflows 81,000 6,000

Net present value $ 1,000 $ 1,000

Each project has a net present value of $1,000, but the projects are not equally desirable. The project requiring an investment ofonly $5,000 is much more desirable when funds are limited than the project requiring an investment of $80,000. To compare thetwo projects on a valid basis, the present value of the cash inflows should be divided by the investment required. The result iscalled the profitability index. The formula for the profitability index follows:

Profitability index =Present value of cash inflows

Investment required(1)

The profitability indexes for the two preceding investments are computed as follows:

Investment

A B

Present value of cash inflows (a) $81,000 $6,000

Investment required (b) $80,000 $5,000

Profitability index, (a) ÷ (b) 1.01 1.20

When using the profitability index to rank competing investment projects, the preference rule is as follows: The higher the

profitability index, the more desirable the project. Applying this rule to the two preceding investments, investment B should bechosen over investment A.

The profitability index is an application of the techniques for utilizing scarce resources. In this case, the scarce resource is the limitedfunds available for investment, and the profitability index is similar to the contribution margin per unit of the scarce resource.

A few details should be clarified with respect to the computation of the profitability index. The “investment required” refers to anycash outflows that occur at the beginning of the project, reduced by any salvage value recovered from the sale of old equipment. Italso includes any investment in working capital that the project may need. Finally, we should note that the “present value of cashinflows” is net of all outflows that occur after the project starts.

CHAPTER 10: CAPITAL BUDGETING DECISIONS 591

WWW.TEX-CETERA.WS

IN BUSINESS

CHOOSING A CATSometimes a long-term decision does not require the use of sophisticated analytical techniques. For example,White Grizzly Cat Skiing of Meadow Creek, British Columbia, needs two snowcats for its powder-skiingoperations—one for shuttling guests to the top of the mountain and one to be held in reserve in case ofmechanical problems with the first. Bombardier of Canada sells new snowcats for $250,000 and used,reconditioned snowcats for $150,000. In either case, the snowcats are good for about 5,000 hours of operationbefore they need to be reconditioned. From White Grizzly’s perspective, the choice is clear. Since both the newand reconditioned snowcats last about 5,000 hours, the latter will result in a higher net present value due to itslower capital investment. Therefore, the reconditioned snowcats are the obvious choice. They may not have all ofthe latest bells and whistles, but they get the job done at a price that a small operation can afford.

Bombardier snowcats do not have passenger cabs as standard equipment. To save money, White Grizzly builds itsown custom-designed passenger cab for about $15,000, using recycled Ford Escort seats and industrial-strengthaluminum for the frame and siding. If purchased retail, a passenger cab would cost about twice as much andwould not be as well suited for snowcat skiing.

Source: Brad and Carole Karafil, owners and operators of White Grizzly Cat Skiing, http://www.whitegrizzly.com.

The Internal Rate of Return Method

LO2 • Know • Apply

CC11: Compute the internal rate of return (IRR) of a project, interpret it, and explain its use for project selection.

The internal rate of return (IRR) of a project is defined as the discount rate that makes the net present value of theproject equal zero. The internal rate of return is sometimes referred to as the yield of the project. It is interpreted as therate of return promised by the project over the project’s useful life. We will consider three aspects of the internal rate ofreturn: (1) its calculation, (2) its interpretation, and (3) its usefulness for decision making about projects as compared withthe net present value rule.

Calculating the Internal Rate of Return of a ProjectTo illustrate the calculation of the internal rate of return, assume the following simplistic data.

EXAMPLE EChantal Enterprises is planning to add a new product line during the summer. The net initial investment will be $142,514. The netcash inflow from the sale of the new product line at the end of one year following the purchase is forecast at $149,700. Determinethe internal rate of return of this project.

The internal rate of return is the discount rate that will make the project’s net present value equal zero. This essentially meansthat the present value of the net cash inflow at the end of one year must equal the net initial investment. We can illustrate thisrelationship as follows:

592 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

From the present value table in Exhibit 10–1, we can see that 0.952 corresponds to a discount rate of 5% (see the first linecorresponding to year 1). We conclude that the proposed investment’s internal rate of return is 5%. The present value of 0.952 canalso be expressed mathematically as follows (the full calculation is presented in Endnote 1 to this chapter):1

1

(1 + IRR)= 0.952

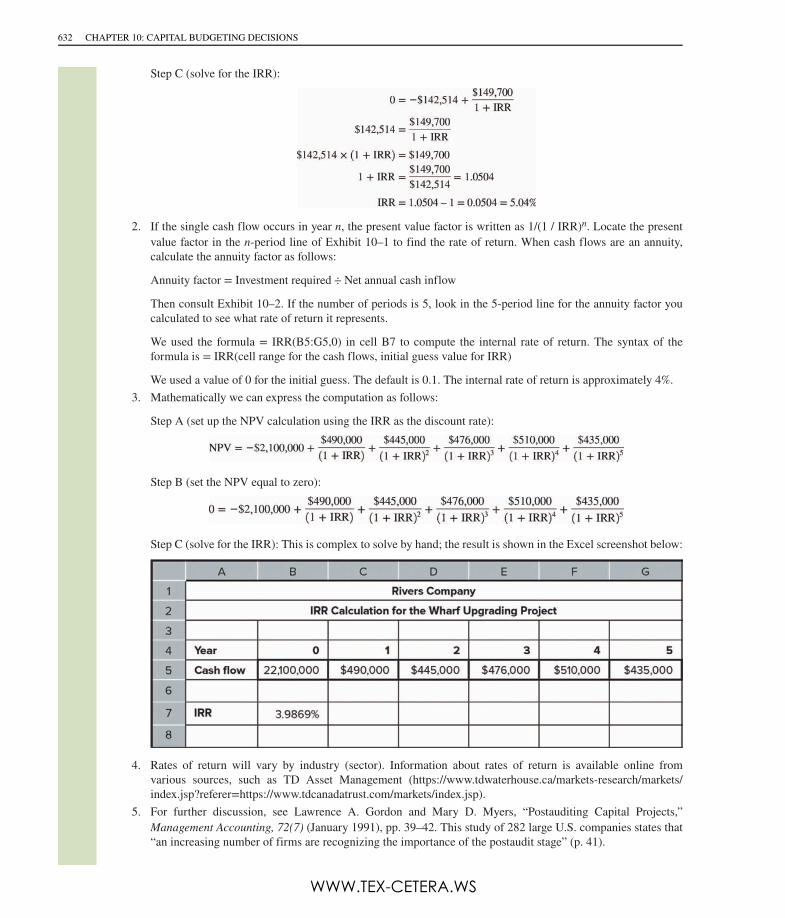

It was simple to solve for the internal rate of return here because the project had a single cash flow occurring in the first year.Moreover, this was a very simple example to illustrate the principle underlying the calculation of the internal rate of return. Thetable method will provide a rough estimate within 1% of the internal rate of return, but it will work only for single cash flowsor annuities.2 In practice, a project can last for several years and have nonconstant cash flows. This complicates the mathematics(step C of the calculation in Endnote 1), but steps A and B will stay the same. Practitioners use computer programs or spreadsheetsto complete step C. To illustrate this, consider the next example.

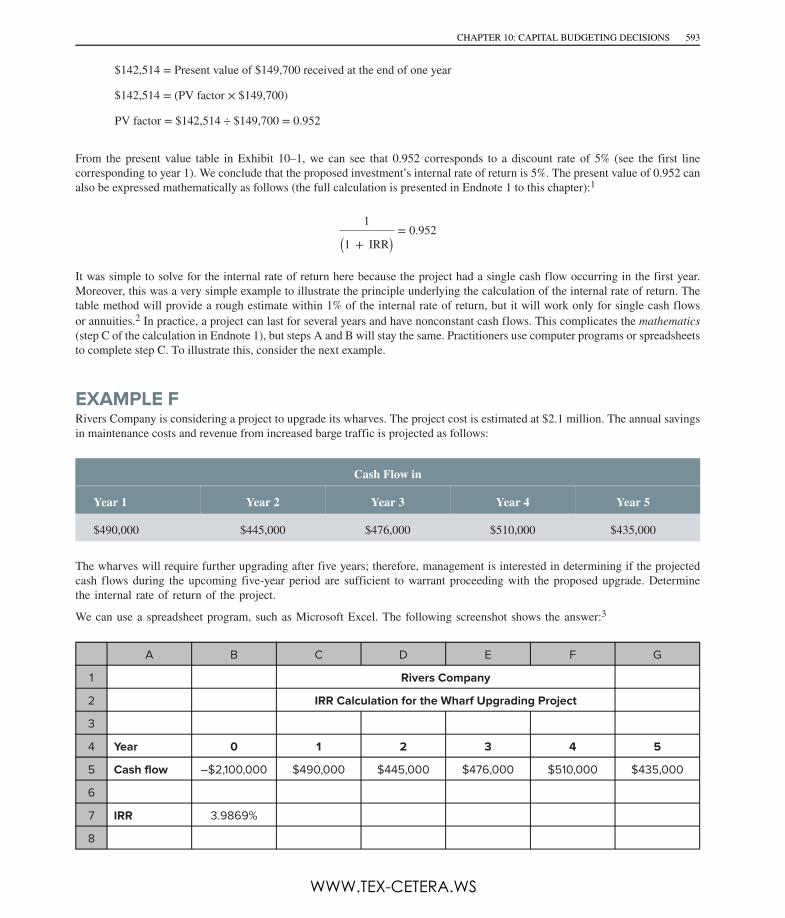

EXAMPLE FRivers Company is considering a project to upgrade its wharves. The project cost is estimated at $2.1 million. The annual savingsin maintenance costs and revenue from increased barge traffic is projected as follows:

Cash Flow in

Year 1 Year 2 Year 3 Year 4 Year 5

$490,000 $445,000 $476,000 $510,000 $435,000

The wharves will require further upgrading after five years; therefore, management is interested in determining if the projectedcash flows during the upcoming five-year period are sufficient to warrant proceeding with the proposed upgrade. Determinethe internal rate of return of the project.

We can use a spreadsheet program, such as Microsoft Excel. The following screenshot shows the answer:3

A B C D E F G

1 Rivers Company

2 IRR Calculation for the Wharf Upgrading Project

3

4 Year 0 1 2 3 4 5

5 Cash flow –$2,100,000 $490,000 $445,000 $476,000 $510,000 $435,000

6

7 IRR 3.9869%

8

$142,514 = Present value of $149,700 received at the end of one year

$142,514 = (PV factor × $149,700)

PV factor = $142,514 ÷ $149,700 = 0.952

CHAPTER 10: CAPITAL BUDGETING DECISIONS 593

WWW.TEX-CETERA.WS

Interpretation and Use of the IRRThe project’s internal rate of return is the rate of return promised by the cash flows of the project. If the wharf project at RiversCompany provides the cash flows that have been forecast for each year, and if each cash flow is immediately reinvested at the rateof about 4% per year, then the net present value of the project at a discount rate of 4% will be equal to 0.

This, however, does not tell you how the internal rate of return can be used to decide if a project is worthwhile. For example,should Rivers Company go ahead with the wharf upgrade? To decide whether to accept a project, the internal rate of return mustbe compared with the company’s cost of capital. The cost of capital will play the role of a hurdle rate (or minimum required rate of

return).4 The logic behind this is that if the project cannot yield at least the cost of the funds tied up in it, it will not be profitable.The decision rule using the internal rate of return can be stated as follows: If the internal rate of return is equal to or greater than

the cost of capital, the project should be accepted. If the internal rate of return is less than the cost of capital, the project should

be rejected.

Suppose the cost of the capital for the wharf project is 5%. Since the internal rate of return of 4% is less than the hurdle rate of5%, Rivers Company will reject the project.

The idea that an acceptable project should earn a rate of return greater than the cost of capital is very appealing. This is the basicprinciple of the internal rate of return method. But the complexity behind the calculation of the internal rate of return can makeit look mysterious. Note that the cost of capital in the internal rate of return method is the hurdle rate. In the net present valuemethod, the cost of capital is the discount rate.

Comparison of the IRR and NPV Methods

LO2 • Know

CC12: Compare and contrast the IRR and NPV methods in project selection.

Many managers wonder if the IRR and NPV methods provide an identical signal about whether projects should be accepted orrejected. We list the strengths and limitations of the two methods in the table below. Although both methods have strengths andlimitations, the net present value will always provide the correct signal regarding acceptance or rejection of a project.

Internal Rate of Return Net Present Value

Strengths IRR is a simple way to communicate informationabout an investment proposal because investorsprefer rates to dollars as a measure of evaluation.

Percentage is a standardized measure; therefore, theIRRs of two different investments can be easilycompared.

It can be calculated without the requirement of apre-established discount rate.

NPV is conceptually superior because it assumesthat cash flows can be reinvested at the discountrate (which ideally should be the opportunity costof capital).

It can be used even when the cash flow pattern isunconventional (i.e., negative cash flows after theinitial investment).

Limitations There is a limiting assumption that cash flows arereinvested at the IRR (which may not be the sameas the opportunity cost of capital).

We cannot easily compute the IRR when the cashflow pattern is unconventional (i.e., negative cashflows after the initial investment).

It may be difficult to compare two investments ofdiffering magnitudes.

It requires establishing the discount rate.

594 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

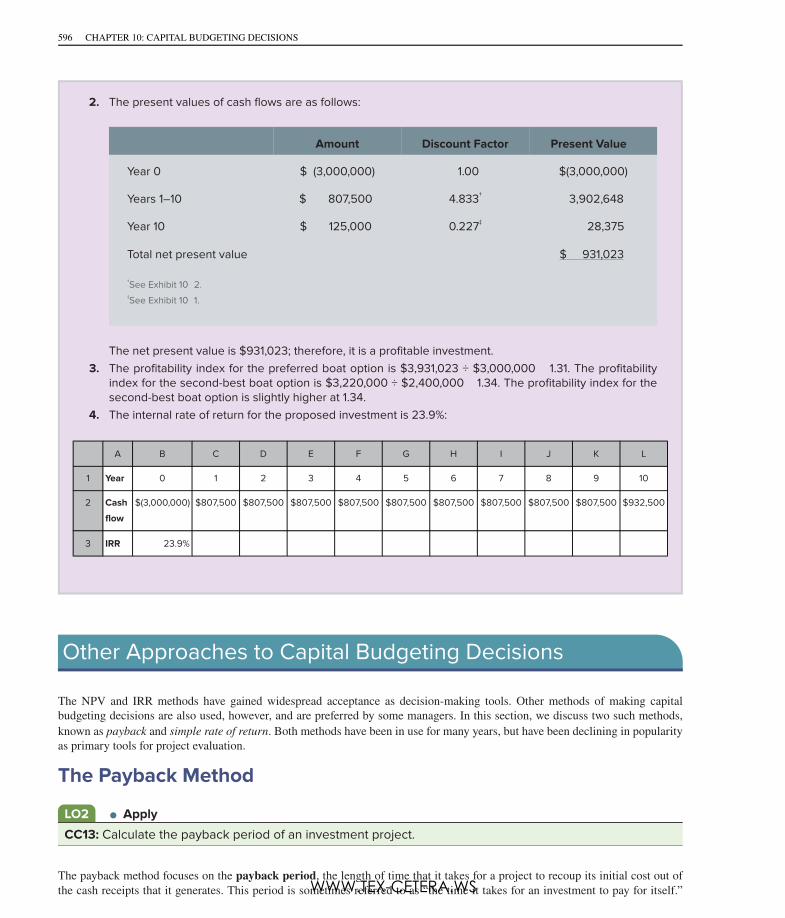

WORKING IT OUT

Max Corporation, a recreational company, is considering investing in a new boat that it can use to offer touristsboat rides. After reviewing the features of six different boats, its estimates for the selected option are as follows:

Investment in the boat $3,000,000

Salvage value after 10 years 125,000

Annual revenue and expense projections:

Sales revenue 6,400,000

Contribution margin 30% of sales revenue

Fixed expenses

Marketing, sales, and promotion $750,000

Administration 450,000

Depreciation 287,500 1,400,000

Required:

SOLUTION TO WORKING IT OUT

1. Compute the cash flows over the 10-year period.2. Using a discount rate of 16%, compute the net present value of the proposed investment. Is this a

profitable investment?3. The second-best boat choice required an investment of $2.4 million and generated a net present value

of $820,000. Compute the profitability index of each option.4. Compute the internal rate of return (IRR) for the company’s preferred investment option.

1. The cash flows are as follows:

Year 0 (now) $3,000,000

Years 1–10 807,500*

Year 10 (salvage value) 125,000

*This amount is calculated as follows:

Contribution margin ( 30% × $6,400,000) $1,920,000

Fixed expenses 1,400,000

Net income $ 520,000

Add back depreciation 287,500

Net annual cash flow $ 807,500

CHAPTER 10: CAPITAL BUDGETING DECISIONS 595

WWW.TEX-CETERA.WS

A B C D E F G H I J K L

1 Year 0 1 2 3 4 5 6 7 8 9 10

2 Cash

flow

$(3,000,000) $807,500 $807,500 $807,500 $807,500 $807,500 $807,500 $807,500 $807,500 $807,500 $932,500

3 IRR 23.9%

Other Approaches to Capital Budgeting Decisions

The NPV and IRR methods have gained widespread acceptance as decision-making tools. Other methods of making capitalbudgeting decisions are also used, however, and are preferred by some managers. In this section, we discuss two such methods,known as payback and simple rate of return. Both methods have been in use for many years, but have been declining in popularityas primary tools for project evaluation.

The Payback Method

LO2 • Apply

CC13: Calculate the payback period of an investment project.

The payback method focuses on the payback period, the length of time that it takes for a project to recoup its initial cost out ofthe cash receipts that it generates. This period is sometimes referred to as “the time it takes for an investment to pay for itself.”

2. The present values of cash flows are as follows:

Amount Discount Factor Present Value

Year 0 $ (3,000,000) 1.00 $(3,000,000)

Years 1–10 $ 807,500 4.833† 3,902,648

Year 10 $ 125,000 0.227‡ 28,375

Total net present value $ 931,023

†See Exhibit 10 2.‡See Exhibit 10 1.

The net present value is $931,023; therefore, it is a profitable investment.3. The profitability index for the preferred boat option is $3,931,023 ÷ $3,000,000 1.31. The profitability

index for the second-best boat option is $3,220,000 ÷ $2,400,000 1.34. The profitability index for thesecond-best boat option is slightly higher at 1.34.

4. The internal rate of return for the proposed investment is 23.9%:

596 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

The basic premise of the payback method is as follows: the more quickly the cost of an investment can be recovered, the moredesirable is the investment.

The payback period is expressed in years. When the net annual cash inflow is the same every year, the following formula can beused to compute the payback period:

Payback period =Investment required

Net annual cash inflow*(2)

*If new equipment is replacing old equipment, this becomes incremental net annual cash inflow.

To illustrate the payback method, assume the following data.

EXAMPLE GYork Company needs a new milling machine. The company is considering two machines: machine A and machine B. Machine Acosts $15,000 and will reduce operating costs by $5,000 per year. Machine B costs only $12,000, but will also reduce operatingcosts by $5,000 per year. Which machine should be purchased according to the payback method?

Machine A payback period =$15,000$5,000

= 3.0 years

Machine B payback period =$ 12,000$ 5,000

= 2.4 years

According to the payback calculations, York Company should purchase machine B, since it has a shorter payback period thanmachine A.

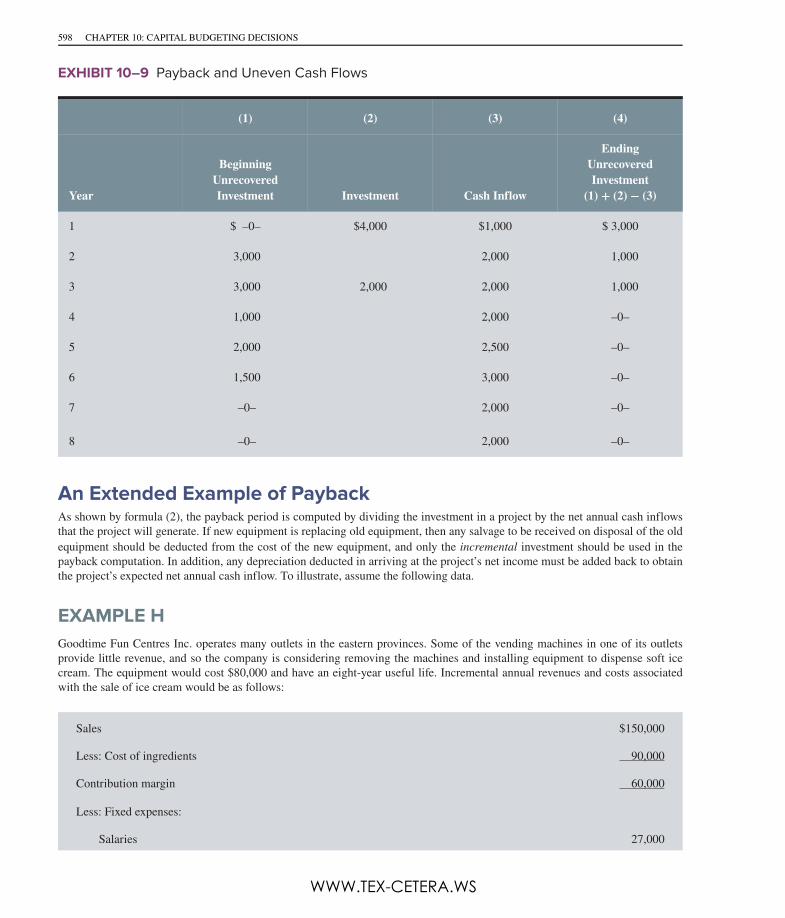

Payback and Uneven Cash FlowsWhen the cash flows associated with an investment project change from year to year, the simple payback formula that we justoutlined is no longer usable, and the computations involved in deriving the payback period can be fairly complex. Consider thefollowing data:

Year Investment Cash Inflow

1 $4,000 $1,000

2 2,000

3 2,000 2,000

4 2,000

5 2,500

6 3,000

7 2,000

8 2,000

What is the payback period on this investment? The answer is 3.5 years, but to obtain this figure, you must track the unrecoveredinvestment year by year. The steps involved in this process are shown in Exhibit 10–9. By the middle of the fourth year, sufficientcash inflows will have been realized to recover the entire investment of $6,000 (= $4,000 + $2,000).

CHAPTER 10: CAPITAL BUDGETING DECISIONS 597

WWW.TEX-CETERA.WS

(1) (2) (3) (4)

Year

BeginningUnrecoveredInvestment Investment Cash Inflow

EndingUnrecoveredInvestment

(1) + (2) − (3)

1 $ –0– $4,000 $1,000 $ 3,000

2 3,000 2,000 1,000

3 3,000 2,000 2,000 1,000

4 1,000 2,000 –0–

5 2,000 2,500 –0–

6 1,500 3,000 –0–

7 –0– 2,000 –0–

8 –0– 2,000 –0–

An Extended Example of PaybackAs shown by formula (2), the payback period is computed by dividing the investment in a project by the net annual cash inflowsthat the project will generate. If new equipment is replacing old equipment, then any salvage to be received on disposal of the oldequipment should be deducted from the cost of the new equipment, and only the incremental investment should be used in thepayback computation. In addition, any depreciation deducted in arriving at the project’s net income must be added back to obtainthe project’s expected net annual cash inflow. To illustrate, assume the following data.

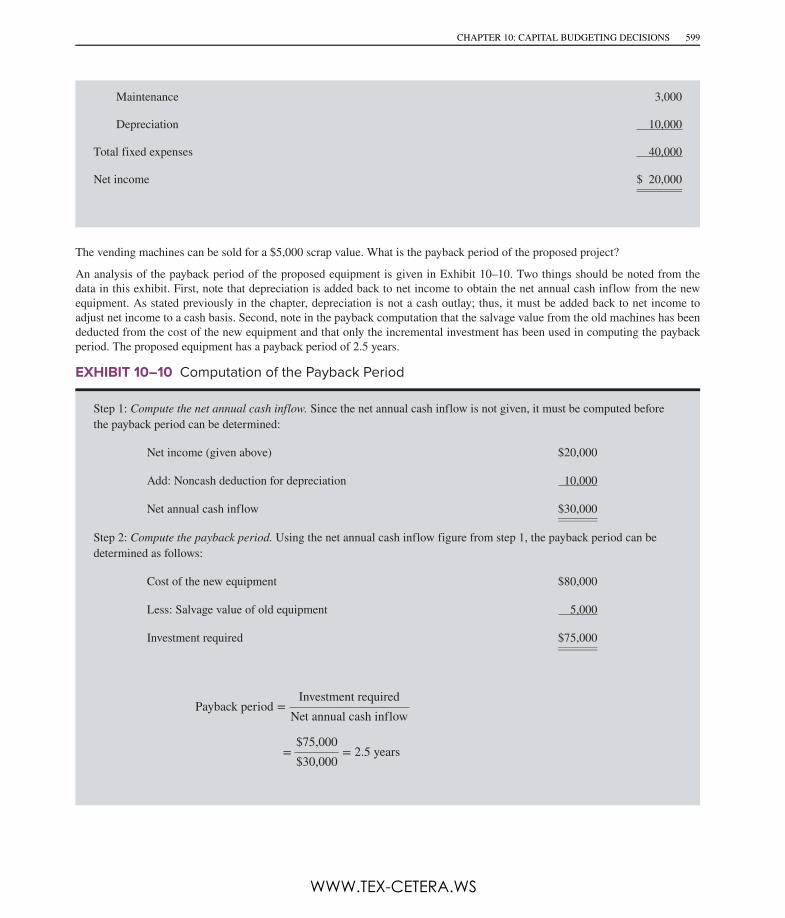

EXAMPLE HGoodtime Fun Centres Inc. operates many outlets in the eastern provinces. Some of the vending machines in one of its outletsprovide little revenue, and so the company is considering removing the machines and installing equipment to dispense soft icecream. The equipment would cost $80,000 and have an eight-year useful life. Incremental annual revenues and costs associatedwith the sale of ice cream would be as follows:

Sales $150,000

Less: Cost of ingredients 90,000

Contribution margin 60,000

Less: Fixed expenses:

Salaries 27,000

EXHIBIT 10–9 Payback and Uneven Cash Flows

598 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

Maintenance 3,000

Depreciation 10,000

Total fixed expenses 40,000

Net income $ 20,000

The vending machines can be sold for a $5,000 scrap value. What is the payback period of the proposed project?

An analysis of the payback period of the proposed equipment is given in Exhibit 10–10. Two things should be noted from thedata in this exhibit. First, note that depreciation is added back to net income to obtain the net annual cash inflow from the newequipment. As stated previously in the chapter, depreciation is not a cash outlay; thus, it must be added back to net income toadjust net income to a cash basis. Second, note in the payback computation that the salvage value from the old machines has beendeducted from the cost of the new equipment and that only the incremental investment has been used in computing the paybackperiod. The proposed equipment has a payback period of 2.5 years.

Step 1: Compute the net annual cash inflow. Since the net annual cash inflow is not given, it must be computed beforethe payback period can be determined:

Net income (given above) $20,000

Add: Noncash deduction for depreciation 10,000

Net annual cash inflow $30,000

Step 2: Compute the payback period. Using the net annual cash inflow figure from step 1, the payback period can bedetermined as follows:

Cost of the new equipment $80,000

Less: Salvage value of old equipment 5,000

Investment required $75,000

EXHIBIT 10–10 Computation of the Payback Period

Payback period =Investment required

Net annual cash inflow

=$75,000$30,000

= 2.5 years

CHAPTER 10: CAPITAL BUDGETING DECISIONS 599

WWW.TEX-CETERA.WS

IN BUSINESS

INVESTING IN AN MBA“What is the value of an MBA?” This is a key question that potential students might ask. The financial benefit ofearning an MBA degree is enhanced earning power; the costs include both tuition and the opportunity cost oflost salary for two years. According to a Forbes magazine study published in 2000, the net present value of anMBA using the first five years of post-degree earnings varies a great deal—ranging from over $100,000 at HarvardUniversity to $1,000 or less at some institutions. The payback period of between 3.3 and 5 years shows lessvariation. This has not changed despite criticisms of the MBA degree. A study published in 2005 suggests that theMBA is still a valuable proposition, providing an average net present value of over $500,000 over one’s lifetime,a payback period of less than nine years, and an internal rate of return of over 17%. Finally, a 2011 article suggeststhat an MBA from a reputable program offers many benefits, including higher compensation, that contribute to ahigh return on investment.

Sources: Kurt Brandenhausen, “The Bottom Line on B Schools,” Forbes, February 7, 2000, pp. 100 104; Antony Davies and Thomas Cline,

“The ROI on the MBA,” BizEd, January/February 2005, pp. 42 45; Denise Deveau, “The ROI of an MBA,” Financial Post, November 29, 2011,

http://business.financialpost.com/2011/11/29/the roi of an mba/.

Evaluation of the Payback Method

LO2 • Know

CC14: Explain the payback method and its potential to mislead a manager.

The payback period only tells a manager how long it will take for a project to recover its investment. It does not say anything

about a project’s profitability. It is possible for a project to have a shorter payback in comparison with another project and not beas profitable. There are three reasons for the payback method to potentially mislead a manager.

DIFFERENT USEFUL LIVESConsider Example G above. Machine B has a shorter payback period than machine A. This suggests that machine B is preferable.However, the example did not provide any data on the useful lives of the machines. Suppose that machine A has a 10-year usefullife, whereas machine B has a five-year useful life. Note that when the useful lives of alternative projects are different, simplecomparisons of their net present value or payback period should not be made. Why? It will take two purchases of machine B toprovide the same service as machine A. If, on the one hand, a manager is going to use a machine for only five years, the analysisshould include the disposal value of machine A. On the other hand, if the manager intends to operate the machine for 10 years,the analysis of machine B should include the cash flow from the second purchase of machine B in year 5. Clearly, an analysis thatrelies only on the payback period will miss these points.

TIME VALUE OF MONEYThe payback period weighs all cash flows equally, regardless of when the cash flows occur. However, we know that cash flowsreceived in a previous period are more valuable than those received in a later period. This flaw in the payback period method cancause a manager to make a wrong decision. Consider the following simple example. Two alternative projects cost $8,000 each.The cash flows from these projects are shown below:

600 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

Both projects have a payback period of five years, but project 2 will return most of its cash flows earlier and is, thus, moredesirable—a point that will be missed if you rely only on the payback period.

CASH FLOWS BEYOND THE PAYBACK CUTOFF DATESometimes, managers specify that projects have to meet a cutoff date criterion for the payback period for the project to beacceptable. Such a policy will discard any project that fails to return its cost by the cutoff date. This can be dangerous, since thecash flows that occur beyond the cutoff date are never considered. Consider the following data:

Now, suppose that projects 1 and 2 both have a cost of $7,000 and that management wants a payback period of four years or less.Project 2, which has a payback of three years, will pass this test, but project 1 will fail the test and be rejected. But a net presentvalue analysis will take into consideration all of the cash flows of both projects. Such an analysis will show that project 1 is moreprofitable than project 2.

In a rapidly changing marketplace, it is not uncommon for managers to demand that projects have small payback periods, becauseif the cash flows do not materialize in the first two years, they are highly unlikely to surface later. Textbook publishing is agood illustration of this concept. Publishers often tell authors that if a textbook is not adopted for use in its first two years afterpublishing, it is unlikely to find a market thereafter. This also explains why textbooks undergo revision once every three or fouryears. But be careful. These instances do not justify the unquestioning use of the payback method. Note that when rapid paybackis suggested, an assumption is made that cash flows beyond the cutoff date are unlikely to be obtained. Therefore, we hope that itis clear to you that the payback method will not always provide the proper signal for project acceptance or rejection and must beused carefully.

The Simple Rate of Return Method

LO2 • Apply

CC15: Calculate the simple rate of return (SRR) of an investment project.

The simple rate of return (SRR) method is another capital budgeting technique that does not involve discounted cash flows. Themethod is also known as the accounting rate of return, the unadjusted rate of return, and the financial statement method.

Unlike the other capital budgeting methods we have discussed, the simple rate of return method does not focus on cash flows.Rather, it focuses on accounting net income. The approach is to estimate the revenues that will be generated by a proposedinvestment and then to deduct from these revenues all of the projected operating expenses associated with the project. This netincome figure is then related to the initial investment in the project, as shown in the following formula:

CHAPTER 10: CAPITAL BUDGETING DECISIONS 601

WWW.TEX-CETERA.WS

(3)

*The investment should be reduced by any salvage from the sale of old equipment.

Or, if a cost reduction project is involved, formula (3) becomes

(4)

*The investment should be reduced by any salvage from the sale of old equipment.

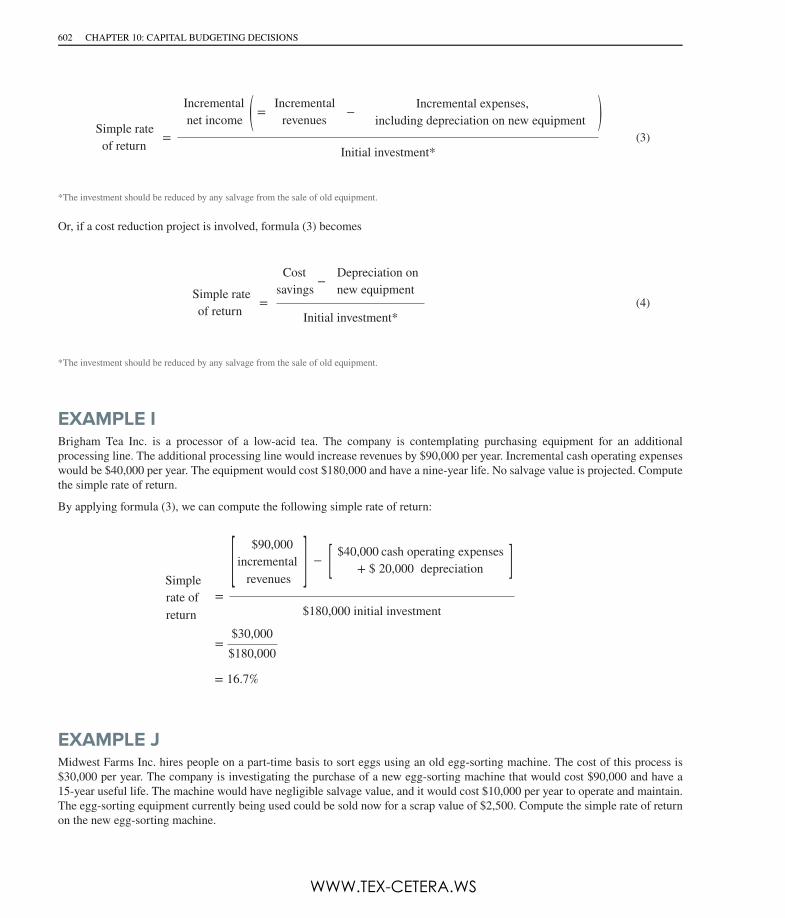

EXAMPLE IBrigham Tea Inc. is a processor of a low-acid tea. The company is contemplating purchasing equipment for an additionalprocessing line. The additional processing line would increase revenues by $90,000 per year. Incremental cash operating expenseswould be $40,000 per year. The equipment would cost $180,000 and have a nine-year life. No salvage value is projected. Computethe simple rate of return.

By applying formula (3), we can compute the following simple rate of return:

EXAMPLE JMidwest Farms Inc. hires people on a part-time basis to sort eggs using an old egg-sorting machine. The cost of this process is$30,000 per year. The company is investigating the purchase of a new egg-sorting machine that would cost $90,000 and have a15-year useful life. The machine would have negligible salvage value, and it would cost $10,000 per year to operate and maintain.The egg-sorting equipment currently being used could be sold now for a scrap value of $2,500. Compute the simple rate of returnon the new egg-sorting machine.

Simple rateof return

=

Incrementalnet income ( =

Incrementalrevenues

− Incremental expenses,including depreciation on new equipment )

Initial investment*

Simple rateof return

=

Costsavings

−Depreciation onnew equipment

Initial investment*

Simplerate ofreturn

=

[ $90,000incremental

revenues ] − [ $40,000 cash operating expenses+ $ 20,000 depreciation ]

$180,000 initial investment

=$30,000$180,000

= 16.7%

602 CHAPTER 10: CAPITAL BUDGETING DECISIONS

WWW.TEX-CETERA.WS

A cost reduction project is involved in this situation. By applying formula (4), we can compute the simple rate of return as follows:

Simple rate of return =$20,000 * cost savings − $6,000 † depreciation on new equipment

$90,000 − $2,500

= 16.0%*$30,000 − $10,000 = $20,000 cost savings†$90,000 ÷ 15 years = $6,000 depreciation

Criticisms of the SRR Method

LO2 • Know

CC16: Explain the disadvantages of the SRR method for project selection.