Embed Size (px)

Citation preview

Capital in Life Insurance Companies

21 May 2002

Patrick Edwards, Head of Capital Management

The material that follows is a presentation of general

background information about the Bank’s activities

current at the date of the presentation 21 May 2002. It

is information given in summary form and does not

purport to be complete. It is not intended to be relied

upon as advice to investors or potential investors and

does not take into account the investment objectives,

financial situation or needs of any particular investor.

These should be considered, with or without

professional advice when deciding if an investment is

appropriate.

Disclaimer

Speaker’s Notes

Speaker’s notes for these presentations

are attached below each slide.

To access them, you may need to save

the slides in PowerPoint and view/print

in “notes view.”

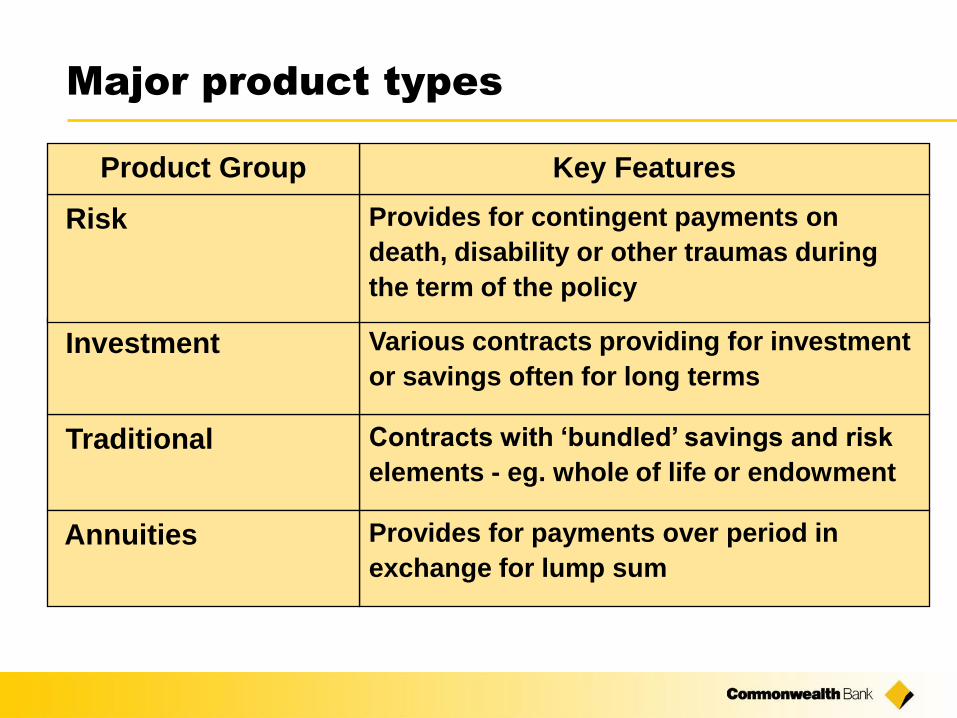

Major Product types

Risks

Business Currently Being Written

Life Insurance Regulation

Australian Life Companies

Overseas Life Companies

Conclusion

Agenda

Major product types

Contracts with ‘bundled’ savings and risk

elements - eg. whole of life or endowment

Traditional

Various contracts providing for investment

or savings often for long terms

Investment

Provides for payments over period in

exchange for lump sum

Annuities

Provides for contingent payments on

death, disability or other traumas during

the term of the policy

Risk

Key FeaturesProduct Group

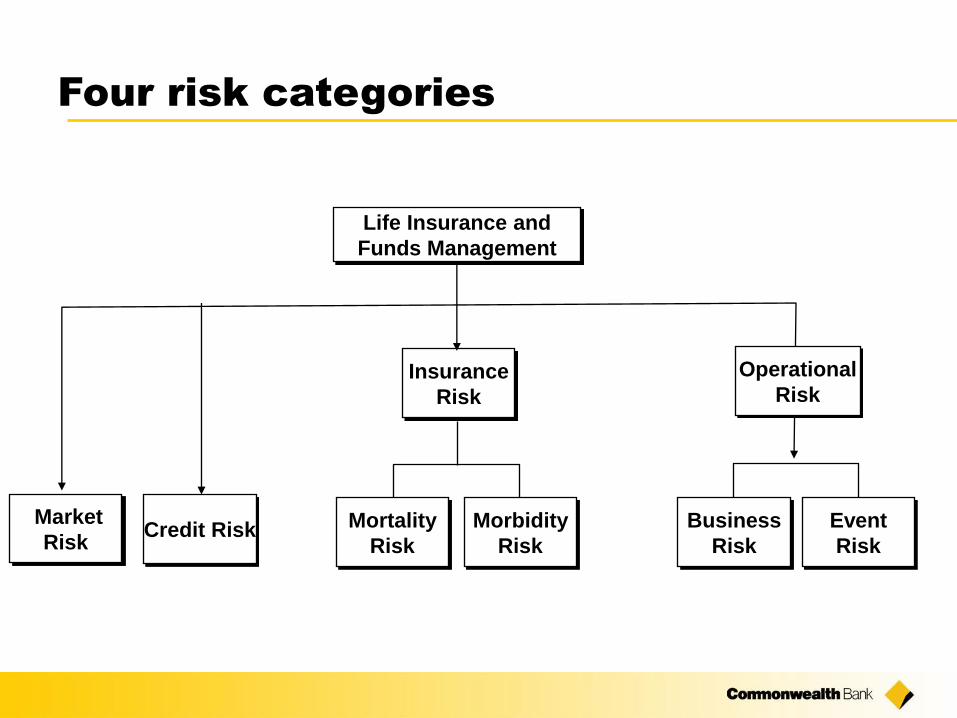

Life Insurance and

Funds Management

Insurance

Risk

Market

RiskCredit Risk Mortality

Risk

Morbidity

Risk

Business

Risk

Event

Risk

Four risk categories

Operational

Risk

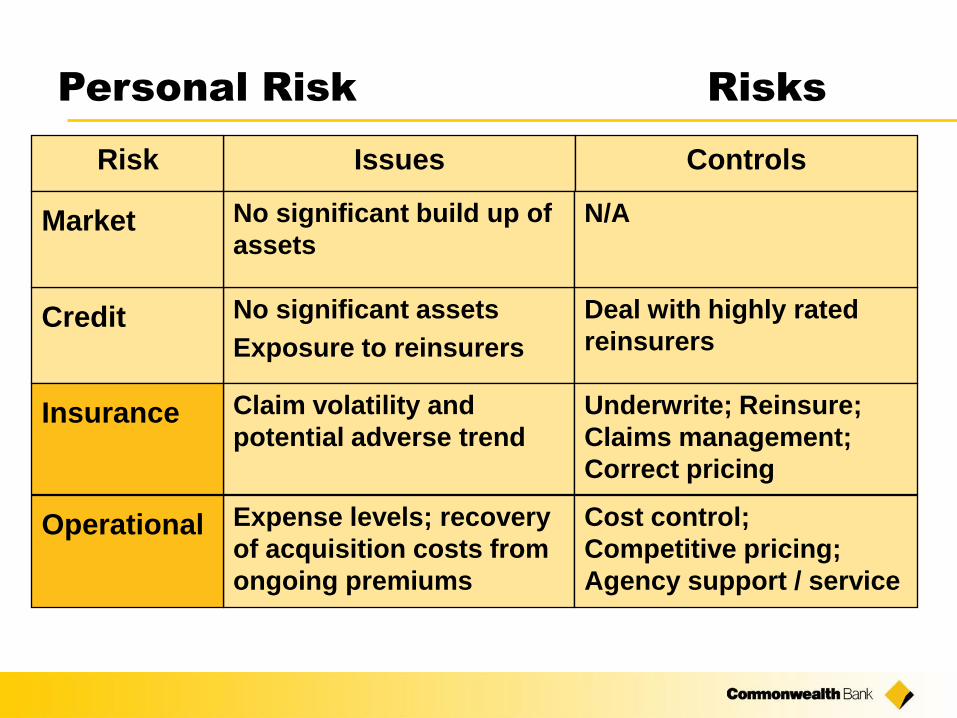

Personal Risk Risks

IssuesRisk

No significant assets

Exposure to reinsurersCredit

Controls

Deal with highly rated

reinsurers

Claim volatility and

potential adverse trendInsurance Underwrite; Reinsure;

Claims management;

Correct pricing

Expense levels; recovery

of acquisition costs from

ongoing premiums

Operational Cost control;

Competitive pricing;

Agency support / service

No significant build up of

assetsMarket N/A

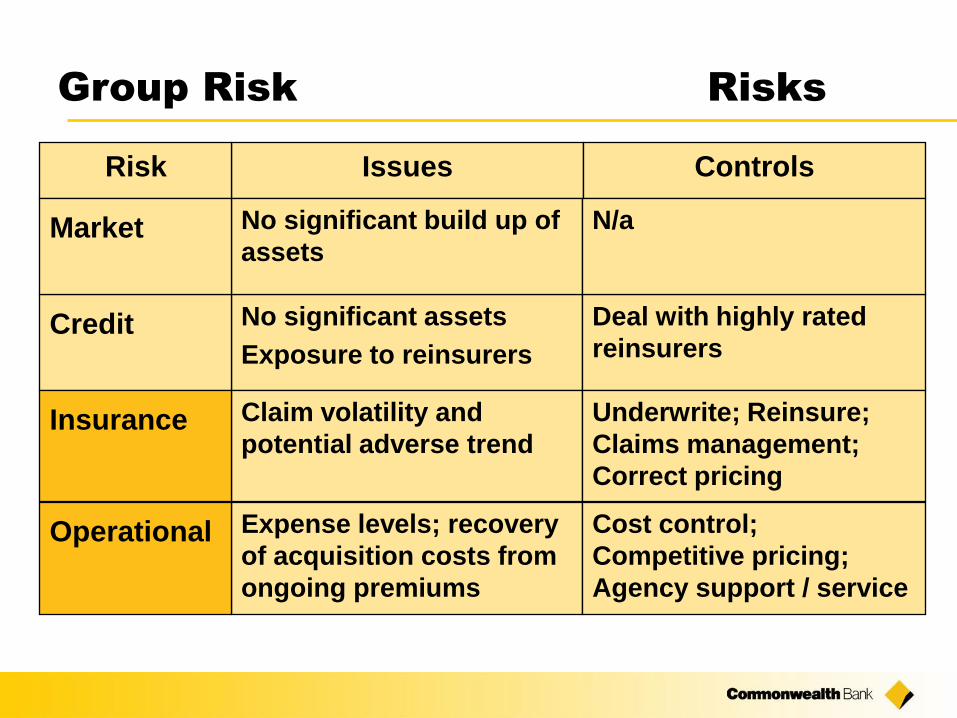

Group Risk Risks

IssuesRisk

No significant assets

Exposure to reinsurersCredit

Controls

Deal with highly rated

reinsurers

Claim volatility and

potential adverse trendInsurance Underwrite; Reinsure;

Claims management;

Correct pricing

Expense levels; recovery

of acquisition costs from

ongoing premiums

Operational Cost control;

Competitive pricing;

Agency support / service

No significant build up of

assetsMarket N/a

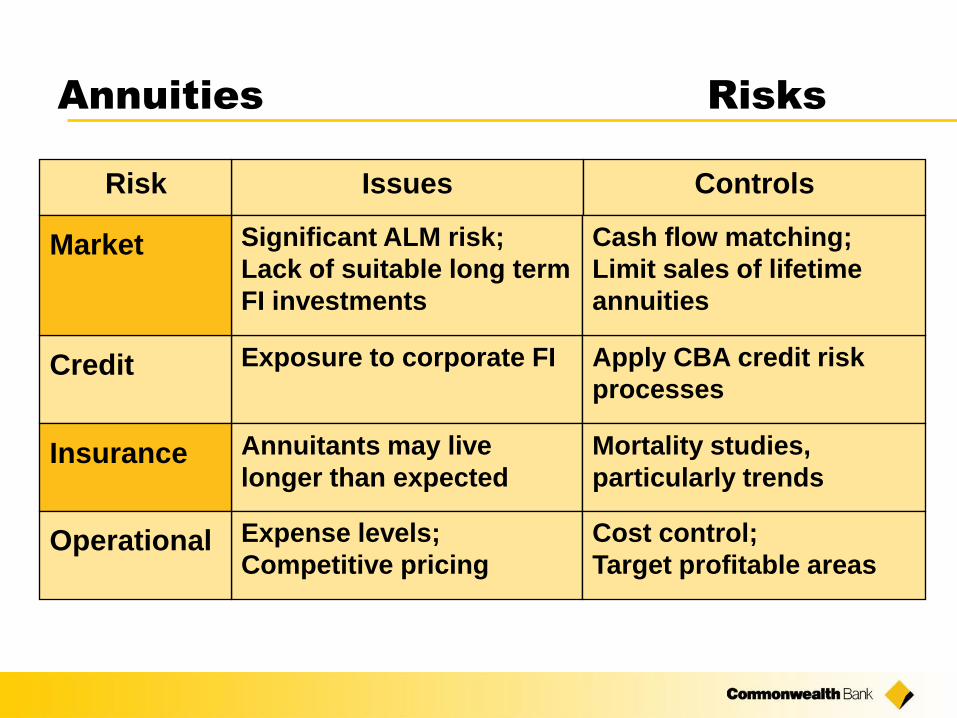

Annuities Risks

IssuesRisk

Exposure to corporate FICredit

Controls

Apply CBA credit risk

processes

Annuitants may live

longer than expectedInsurance Mortality studies,

particularly trends

Expense levels;

Competitive pricingOperational Cost control;

Target profitable areas

Significant ALM risk;

Lack of suitable long term

FI investments

Market Cash flow matching;

Limit sales of lifetime

annuities

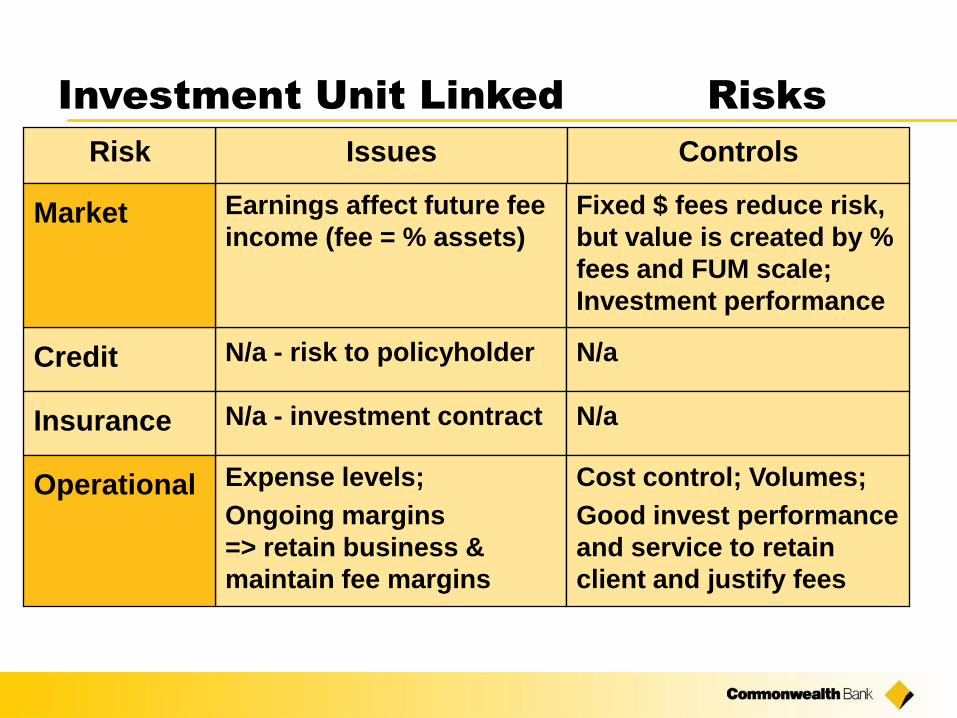

Investment Unit Linked Risks

IssuesRisk

N/a - risk to policyholderCredit

Controls

N/a

N/a - investment contractInsurance N/a

Expense levels;

Ongoing margins

=> retain business &

maintain fee margins

Operational Cost control; Volumes;

Good invest performance

and service to retain

client and justify fees

Earnings affect future fee

income (fee = % assets)Market Fixed $ fees reduce risk,

but value is created by %

fees and FUM scale;

Investment performance

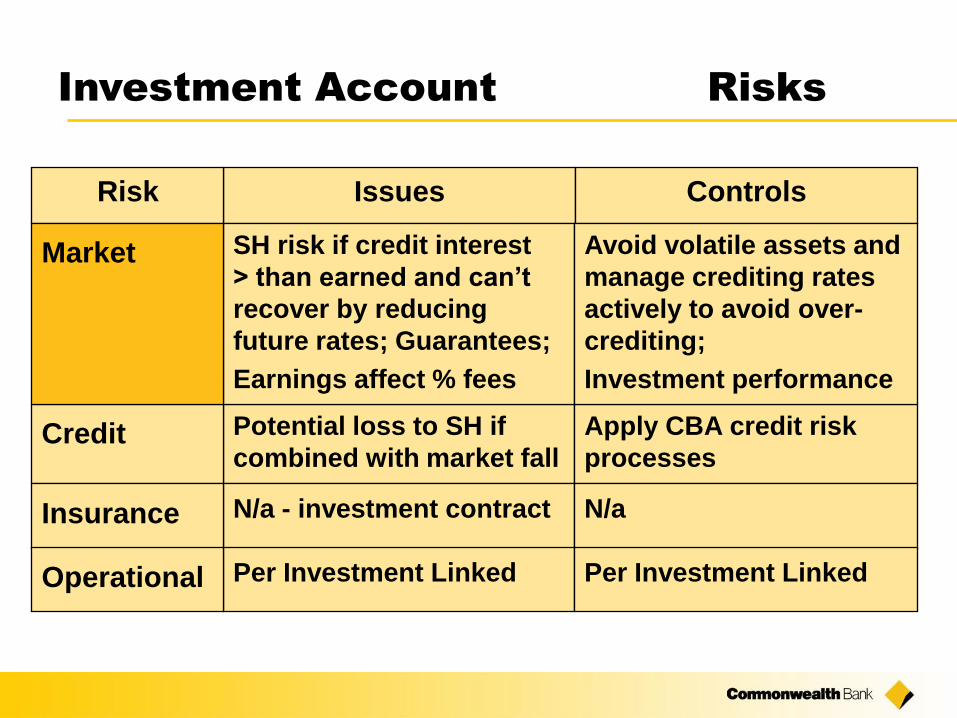

Investment Account Risks

IssuesRisk

Potential loss to SH if

combined with market fallCredit

Controls

Apply CBA credit risk

processes

N/a - investment contractInsurance N/a

Per Investment LinkedOperational Per Investment Linked

SH risk if credit interest

> than earned and can’t

recover by reducing

future rates; Guarantees;

Earnings affect % fees

Market Avoid volatile assets and

manage crediting rates

actively to avoid over-

crediting;

Investment performance

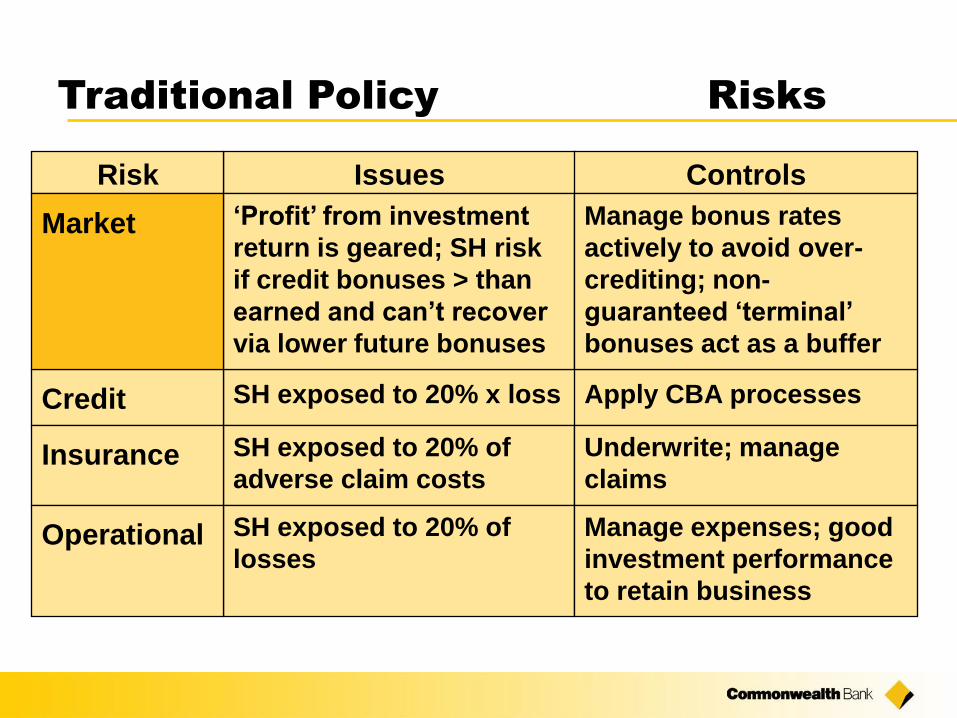

Traditional Policy Risks

IssuesRisk

SH exposed to 20% x lossCredit

Controls

Apply CBA processes

SH exposed to 20% of

adverse claim costsInsurance Underwrite; manage

claims

SH exposed to 20% of

lossesOperational Manage expenses; good

investment performance

to retain business

‘Profit’ from investment

return is geared; SH risk

if credit bonuses > than

earned and can’t recover

via lower future bonuses

Market Manage bonus rates

actively to avoid over-

crediting; non-

guaranteed ‘terminal’

bonuses act as a buffer

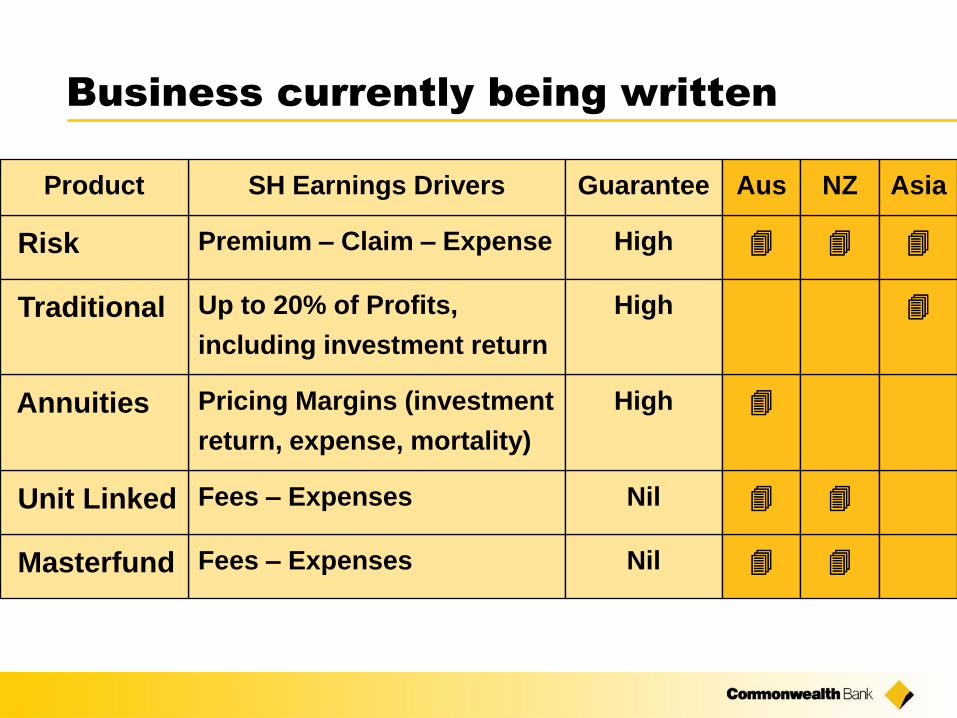

Business currently being written

Fees – ExpensesMasterfund

Fees – ExpensesUnit Linked

Premium – Claim – ExpenseRisk

SH Earnings DriversProduct

Pricing Margins (investment

return, expense, mortality)

Annuities

Nil

Nil

High

Guarantee

High

Up to 20% of Profits,

including investment return

Traditional High

Aus

NZ

Asia

Life insurance regulations in Australia

• Life Insurance Act 1995

• Australian Prudential Regulation Authority (APRA)

• Regulatory capital is calculated by statutory fund, not

by company

• Two tier test: solvency (published) and capital

adequacy (unpublished)

• Capital Adequacy Liability

• Other Liabilities

• Resilience Reserve

• Inadmissible Assets Reserve

• New Business Reserve

Capital adequacy

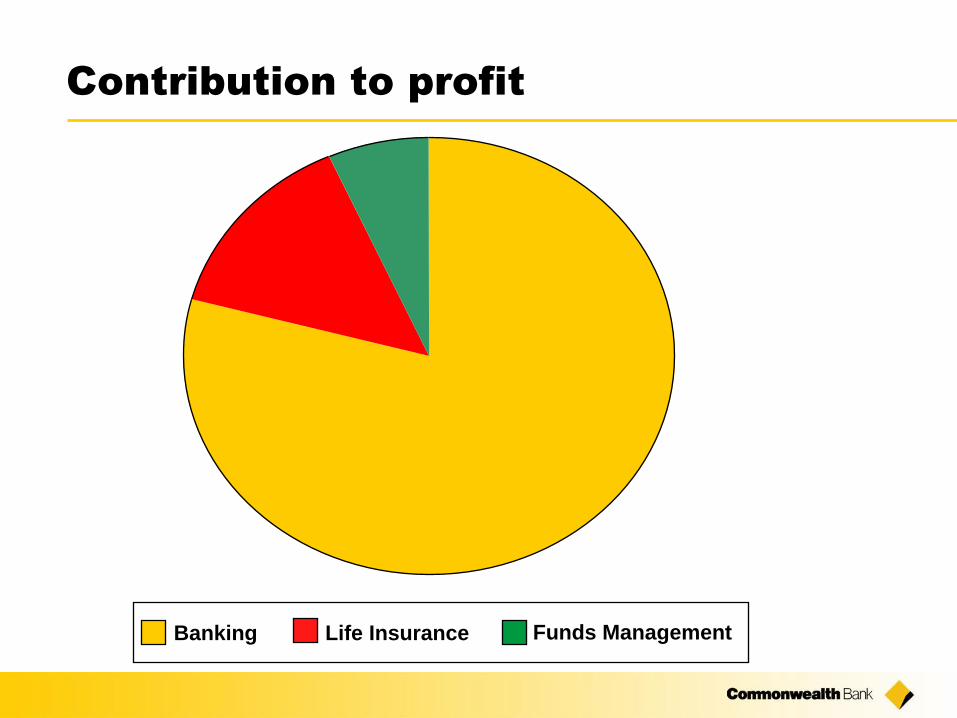

Contribution to profit

Banking Life Insurance Funds Management

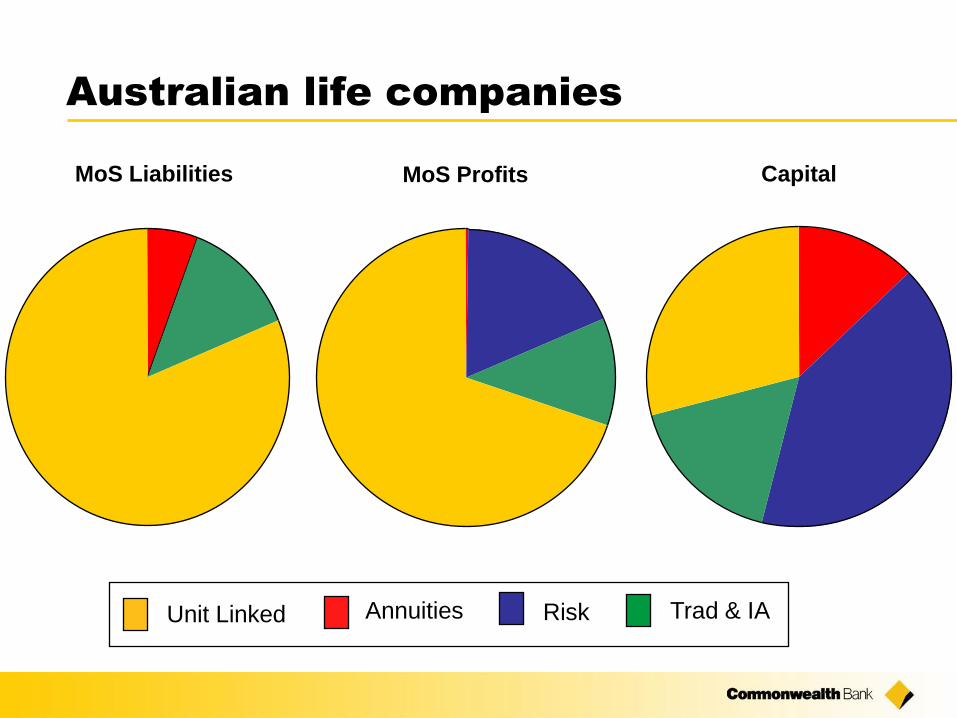

Australian life companies

Unit Linked Annuities Risk Trad & IA

MoS Liabilities MoS Profits Capital

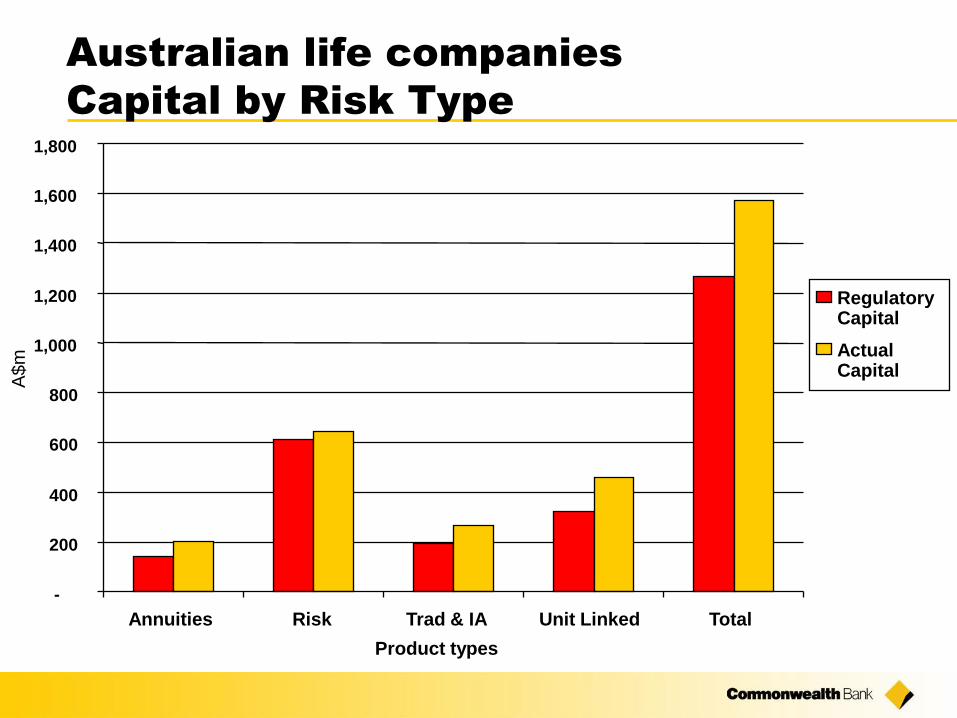

Australian life companies

Capital by Risk Type

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Annuities Risk Trad & IA Unit Linked Total

Product types

A$m

RegulatoryCapital

ActualCapital

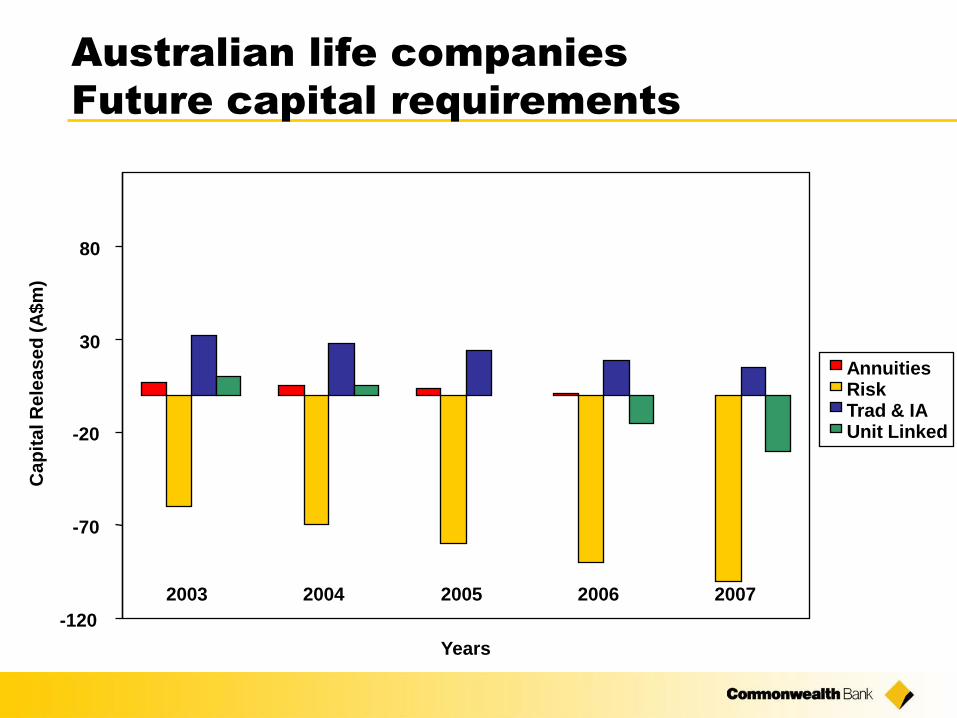

Australian life companies

Future capital requirements

-120

-70

-20

30

80

2003 2004 2005 2006 2007

Years

Ca

pit

al R

ele

as

ed

(A

$m

)

AnnuitiesRiskTrad & IAUnit Linked

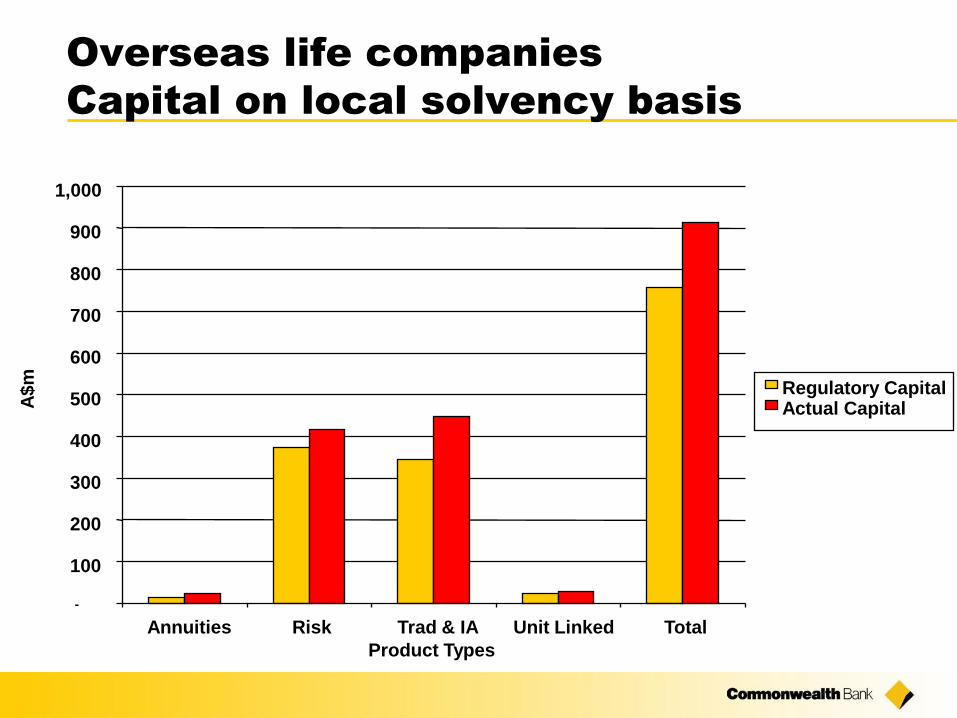

Overseas life companies

Capital on local solvency basis

-

100

200

300

400

500

600

700

800

900

1,000

Annuities Risk Trad & IA Unit Linked Total

Product Types

A$

m Regulatory CapitalActual Capital

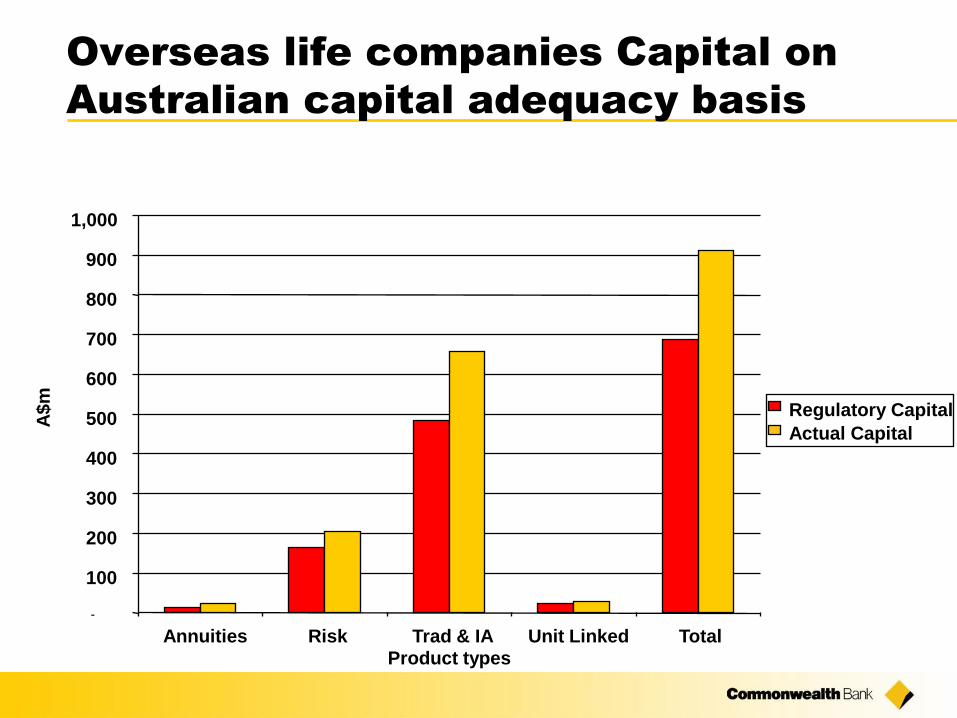

Overseas life companies Capital on

Australian capital adequacy basis

-

100

200

300

400

500

600

700

800

900

1,000

Annuities Risk Trad & IA Unit Linked Total

Product types

A$

m

Regulatory Capital

Actual Capital

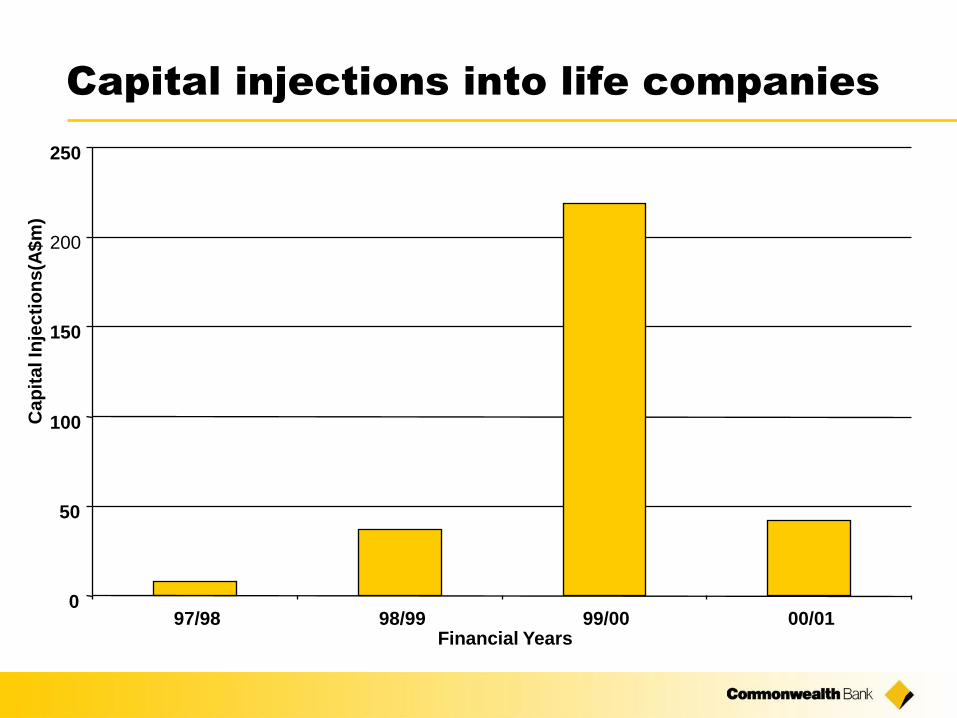

Capital injections into life companies

0

50

100

150

200

250

97/98 98/99 99/00 00/01Financial Years

Ca

pit

al In

jec

tio

ns(A

$m

)

Conclusions

Risks identified, measured and managed

APRA has realistic regulatory capital requirements

Overseas regulatory capital requirements are more arbitrary

In the near term, growth of risk business will absorb

more capital than is released by closed book

Capital in Life Insurance Companies

21 May 2002

Patrick Edwards, Head of Capital Management