Embed Size (px)

Citation preview

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 1/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Greetings from FundsIndia!

Hope you had a happy Diwali. Our equity markets certainly did and we are offto a rocking start to the new (traditional) Indian financial year with new indexhighs. It is a little too early to say if this rally is real and if it will find suste-nance from earnings reports. Our view on the market, however, has been tonot get too low with the downs nor get too high with the ups. Our goal is to roll

with the curves and trust that the long investment term will take care of the returns.

So, we turn our attention to what's happening in your favourite investment platform -FundsIndia.com. Some of you may have already seen it - we have made a couple of en-hancements to how SIPs are managed (now you can change the scheme and amount of

your SIP directly online) and added an ability to create notes for your portfolio. We've alsotweaked the annualized returns calculation to show IRR data for investments that are lessthan a year old.

You can find details about these changes in the blog post—Three Changes, or by simply

logging into your account. We are working on more changes that you will see as this month progresses. We are con-tinuing to enhance the way we show mutual fund data for your investments, and I'm confi-dent that you will find these useful.

All these changes are results of suggestions from our investors, so big props to folks who

have been sending in valuable feedback about improving our services and platform.

It is also the season for tax savings. Before your HR department (or your tax attorney) reminds you to do so, please goahead and make your 80-c tax saving mutual fund investment as soon as possible.

Choosing a good tax fund has never been easier – our research has produced a small list of the best tax funds that youcan choose from.

Please read Vidya Bala’s article in this newsletter (or in our blog) to see what these funds are. Remember, we can send you the mutual fund account statement for your tax saving investment as soon as the investment has been completed.

Happy (tax-saving) Investing!

06—Nov —2013

Volume 6, Issue 11

Inside this issue:

‘T is the Season of

Change —SrikanthMeenakshi

1

Tax-saving fundsthat made an im-pression - VidyaBala

2

Equity Recommen-dations- B. Kr ishna Kumar

3

Financial PlanningEducation Series

5

The Un-Diwal i In-vestment Strategy

—Dhirendra Kumar

6

'Tis the Season of Change

Srikanth Meenakshi

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 2/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

With the tax season on, it may be time for you to scout for tax-saving funds to benefit from tax deductions under Section 80C of the In-

come Tax Act up to Rs 1 lakh.

Franklin India Taxshield, Religare Invesco Tax Plan, Canara Robeco Equity Tax Saver and ICICI Pru Tax Plan have been

our select list of funds in the tax-saving category. These are well-established funds and have developed a consistent track record of perfor-

mance although they may not always turn out to be chart busters.

But there have been other funds in this category that have been conspicuous in the performance chart in recent times, although they do

not have a very long track record. We take a look at 3 of these funds that have hogged the limelight.

Axis Long Term Equity Fund

Having been launched in the beginning of 2010, this fund has been in the limelight since its first year. Its three-year return is superior to

even established peers. But 2 factors have worked in the fund’s favour since its launch.

One, for the first 3 years (almost until early 2013), the fund would not have seen any redemptions as it has a 3-year lock-in as an ELSS

fund. That could well have helped contain declines, especially in a turbulent market such as the one in 2011. The fund fell just 14.8% that year even as its benchmark, BSE 200 fell 27%.

Two, the fund does not hesitate to get into cash to protect downside. In 2011, its equity holdings went lower than 90%. In 2013 too, it re-

duced equity exposure in March but quickly ramped it up. That the fund also has higher exposure to large-cap stocks also means that it

does not bear the mid-cap brunt as much as a few other funds. Its average market cap for instance, is much higher than ICICI Pru Tax

Plan.

The fund’s performance provides comfort for a ‘buy’ but given that it is only one year since the fund has corpus that are open for redemp-

tion, you will do well to keep exposure to the fund limited. Completion of a 5-year record, with similar colours would make this fund a core

part of a tax-saving portfolio.

BNP Paribas Tax Advantage

BNP Paribas Tax Advantage has changed hands since its launch under the ABN Amro AMC stable in early 2006 (which limits us fromgranting it the benefit of a long track record).

Its performance during its life time is therefore a bit chequered, with the fund beating its benchmark less than 50% of the times on a roll-

ing one-year return basis since launch. But this has significantly improved in the last 2 years since takeover by fund manager Shreyash

Devalker.

The fund appears to position itself as a scheme with large-cap bias in recent times, given that its large-cap holding (above Rs 10,000 crore

market cap) is higher than many peers. That means, in a mid-cap driven rally, its participation may be a bit capped, if it continues its cur-

rent strategy.

That it seeks to contain downside is also evident by the way it holds underweight position (in relation to its benchmark BSE 200) in sec-

tors such as finance, which took a knock in the last few quarters.

This fund managed to cross the Rs 100-crore AUM about a year ago but is still much smaller than Axis Long Term Equity.

IDFC Tax Advantage (ELSS)

Launched a year before Axis Long Term Equity, this fund can claim to have gone through slightly longer market cycles than the former.

The fund is what one would call a typical ELSS fund, with higher exposure to mid-cap stocks than the other two mentioned above.

But that also means that this fund can take a sharp knock in market falls. In 2011, for instance, the fund fell a good 7 percentage points

more than larger peers such as Franklin India Taxshield. But it adequately made up for this in 2012 with higher returns that year.

Although laden with slightly more midcaps than the other two, the fund has played its sectors cautiously; with higher exposure to IT and

Page 2 Volume 6, Issue 11

Tax-saving funds that made an impression

Vidya Bala

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 3/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

pharma and lower weight to finance.

This fund too has a small asset size of close to Rs 150 crore.

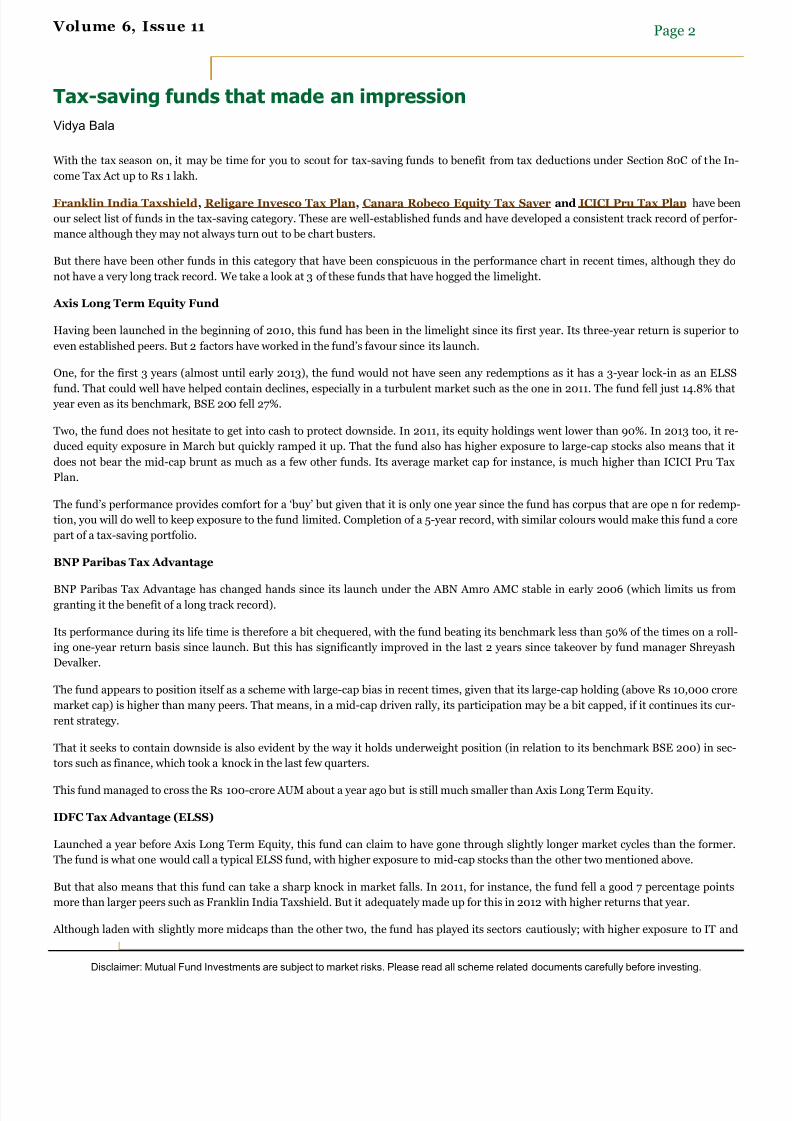

Which should you choose?

If you are investing in equity funds for the first time and have tax-saving in mind, the established funds (mentioned in the beginning)

should be your first choice.

If you already own some of the established ELSS funds then you may

consider limited exposure to one of the 3 funds mentioned above. Of

them, IDFC Tax Advantage is suitable for a slightly aggressive investor;

the fund could capitalise on a mid-cap rally. Axis Long Term Equity for

a moderate-risk investor and BNP Paribas Tax Advantage for a value-

focused investor.

Vidya Bala is the Head of Mutual Fund Research at FundsIndia. She

writes for our monthly newsletter on topics including mutual fund,

personal finance and equity markets. Vidya Bala can be reached at

The stock market sentiment was distinctly positive in October. Both the Sensex and the Nifty inched closer towards their life-time high last

month. While the Sensex has moved past its all-time high recently, the Nifty is still within the striking distance of the high at 6,358.

The Rupee has appreciated from its record low of close to the 70-mark to the US Dollar ,while consumer inflation still remains at lofty

levels. The Reserve Bank of India has hiked interest rates, which has resulted in an upward revision in base lending rates by the banking

sector.

The high interest rate regime is a dampener for corporate sector growth as well as retail investor participation in the stock market. Inves-

tors still seem comfortable parking their surplus either in risk-free term deposits or FMPs. The overwhelming response to the recent tax-

free deposits from public sector entities is a testimony to this observation.

From a positive perspective, the earnings scorecard from the companies thus far has not been disappointing. Companies across a diverse

set of industries have reported their earnings and most of them have been either in-line or marginally better than expectations.

Buying interest is visible in beaten down sectors such as public sector banks, realty and infrastructure. Technically, we remain cautiously

optimistic on the near term outlook for the stock market. There are still quite a few key events that could influence market sentiment.

The major factor could be the US Federal Reserve’s decision on tapering their quantitative easing program. Any decision on th is front

would have a big influence on almost all asset classes. The next major event would be the outcome of the elections in key states in India,

including Delhi.

Investors may adopt a SIP kind of approach to investment. Buying index ETFs on weakness would not be such a bad idea. We maintain the

positive view on the Nifty as long as the index trades above the key support at 5,700.

(Continued on page 4 . . . )

Page 3 Volume 6, Issue 11

The Month Ahead - Equity Recommendations

B. Krishna Kumar

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 4/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

As long as the support at 5,700 holds, we would

expect the Nifty to touch 6,650-6,700 soon. We

expect the interest rate sensitive sectors such as

banking, realty and automobile to drive the index

to higher levels. We are also positive on the met-

als space, with Tata Steel being the preferredpick.

This month, we cover the outlook for Dabur In-

dia and Chambal Fertiliser. We are positive on

both these stocks and expect 8-10% appreciation

from a short-term perspective. Investors may

accumulate these stocks at the current levels as

well as on declines.

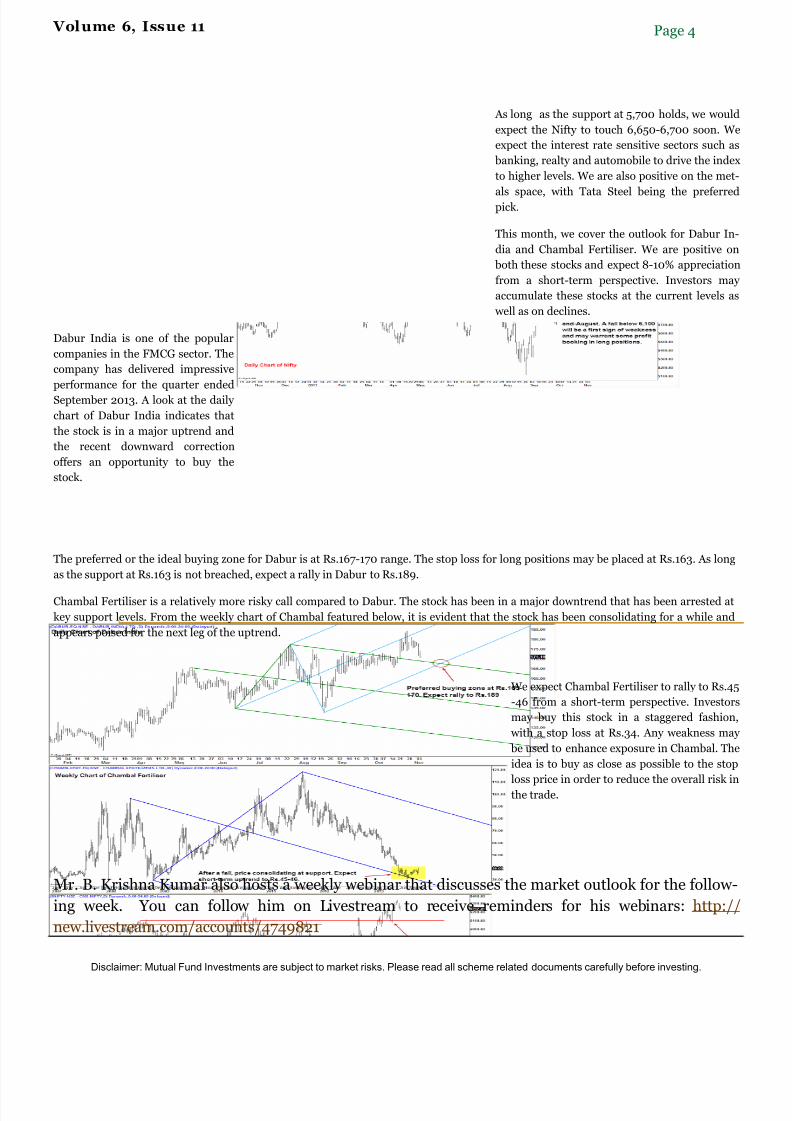

Dabur India is one of the popular

companies in the FMCG sector. The

company has delivered impressive

performance for the quarter ended

September 2013. A look at the daily

chart of Dabur India indicates that

the stock is in a major uptrend and

the recent downward correction

offers an opportunity to buy the

stock.

The preferred or the ideal buying zone for Dabur is at Rs.167-170 range. The stop loss for long positions may be placed at Rs.163. As long

as the support at Rs.163 is not breached, expect a rally in Dabur to Rs.189.

Chambal Fertiliser is a relatively more risky call compared to Dabur. The stock has been in a major downtrend that has been arrested at

key support levels. From the weekly chart of Chambal featured below, it is evident that the stock has been consolidating for a while and

appears poised for the next leg of the uptrend.

We expect Chambal Fertiliser to rally to Rs.45

-46 from a short-term perspective. Investors

may buy this stock in a staggered fashion,

with a stop loss at Rs.34. Any weakness may

be used to enhance exposure in Chambal. The

idea is to buy as close as possible to the stop

loss price in order to reduce the overall risk in

the trade.

Mr. B. Krishna Kumar also hosts a weekly webinar that discusses the market outlook for the follow-

ing week. You can follow him on Livestream to receive reminders for his webinars: http://

new.livestream.com/accounts/4749821

Page 4 Volume 6, Issue 11

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 5/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Financial planning is a systematic approach to create a roadmap in order to reach your goals. It helps you

identify and quantify your current financial needs in order to judge how much money you will need for the

future.

With financial planning, you can set important milestones such as your child’s education, your child’s mar-

riage, your retirement, or the purchase of a new asset, and start saving for them.

Here is how a financial planner can help you:

It is simple. A financial planner will help you determine and quantify your goals, and then evaluate your

income and expenses to see how to allocate funds towards your goals in a way that your financial objec-

tives are accomplished.

Once a plan is created by taking all your personal financial goals into account, you can start investing to-

wards reaching your goals.

Financial planning is not only for the wealthy. It is essential that individuals who are just starting out on

their career path also receive good financial advice in order to ensure that they are not reckless with their

money.

As each individual’s needs are unique, you will need a tailor made financial plan that fits your require-

ments. Of course, the financial planner would charge a nominal fee for developing an independent com-

prehensive financial plan that suits you.

Investment products are varied and complex in nature. Every product has its own advantages; but it may

also be unsuitable for a few. A financial planner would help identify a product that could be suitable to

your objectives rather than just picking a product.

A financial planner has a vital role to play in aiding you to achieve your desired financial goals. And rest

assured, the presence of a competent, experienced and honest financial planner can ensure that your fi-

nancial process becomes an easy task.

Mr. S. Sridharan is the Head of Financial Planning at FundsIndia. You can reach Mr. Sridharan at sri-

Page 5 Volume 6, Issue 11

The Advantages of Financial Planning

S. Sridharan—Head - Financial Planning

8/10/2019 Capital Letter November 2013 - Fundsindia.com

http://slidepdf.com/reader/full/capital-letter-november-2013-fundsindiacom 6/6

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

The best way to invest this Diwali (or indeed, any Diwali) is to pretend that it's not Diwali. In other words, to

have an un-Diwali investment strategy. I realise that this may sound sort of sacrilegious--perhaps it is--butinvestments are serious business and it's never a good idea to make investing decisions based on custom or

habit or ceremony.

Diwali, like all other festivals, is a great time to celebrate, to be with friends and family and to conduct whatev-

er rituals and traditions that are customary for your community. However, unlike many other festivals, Diwali

is intertwined with wealth and investments and prosperity which gives it an additional aspect of being an aus-

picious time to invest.

However, any rational analysis as an investor would perforce lead one to the conclusion that there is no rea-

son to treat a date--any date--as special. Whether the date is a calendar new year like January 1, or a tradition-

al new year like Diwali, or the start of a new decade, it has no more significance to how you invest than yourown birthday.

Therefore, just like one does for these other 'round number dates', I'd say that the investment strategy to be

followed should depend entirely on what your needs are, and not on what the calendar shows. However, that

immediately brings up the question of dealing with what your needs are and how to map them on to the in-

vestments you make.

The trick here is to divide your investments into specific financial goals, a goal being defined as the combina-

tion of a target amount and a target date. For example, you'll need money for your daughter's higher educa-

tion after three years. You'd like to buy a house at least ten years before retirement. You'd like to go on a vaca-

tion to Europe after two years. You'd like Rs 2 lakh to always be available for emergencies.

Each of these goals is very precise. The risk you can take with it, as well as the amount of money needed can

be quantified quite precisely. Therefore, it is relatively easy to decide what kind investments should be made

for each of them. Instead each individual must have many portfolios, one for each financial goal. And then can

you tune each portfolio's level of conservativeness or aggressiveness to the right level by choosing the right

kind of assets.

Syndicated from Value Research Online. Read the article online here: http://www.valueresearchonline.com/story/

h2_storyview.asp?str=23875

Page 6 Volume 6, Issue 11

The Un-Diwali Investment Strategy

By Dhirendra Kumar | Nov 4th, 2013

Wealth India Financial Services Pvt. Ltd.,H.M. Centre, Second Floor,

29, Nungambakkam High Road,Nungambakkam,Chennai - 600 034

Phone: (0) 7667 166 166Email: [email protected]