Embed Size (px)

Citation preview

www.stepstone.com

CAPITAL MARKETS DAY 2016 STEPSTONE - SHAPING THE FUTURE OF E-RECRUITMENT 08.12.2016

RALF BAUMANN

CEO STEPSTONE

www.stepstone.com 2.

TODAY WE ARE GOING TO COVER DIFFERENT TOPICS

1. State of the business ‘Continued growth’

2. Growth elements ‘Various elements drive our growth’

3. Business environment ‘A candidate centric development’

4. StepStone product strategy ‘Our way to an E-Sourcing company’

5. StepStone’s tech and business… ‘We are shaping the future of E-Recruitment’

www.stepstone.com 3.

STEPSTONE – A MARKET LEADING JOB BOARD GROUP

50+

million

VISITS PER MONTH

16

million

SUBSCRIBERS

26

million

CVs

650

thousand

JOBS PER MONTH¹

32%

Ø ANNUAL REVENUE

GROWTH SINCE 2005

2,200+ EMPLOYEES

21 COUNTRIES

130+ COUNTRIES VIA

THE NETWORK

¹ Comprises the entire StepStone Group

www.stepstone.com 4.

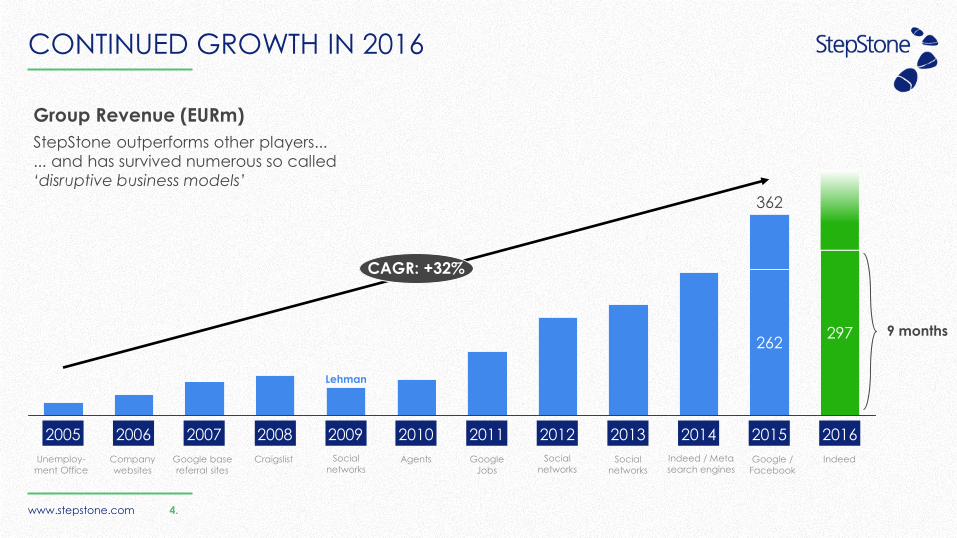

CONTINUED GROWTH IN 2016

297

CAGR: +32%

2015 2016

362

262

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

Group Revenue (EURm)

StepStone outperforms other players...

... and has survived numerous so called

‘disruptive business models’

Lehman

9 months

Unemploy-

ment Office Company

websites

Google base

referral sites

Craigslist Social

networks Agents Google

Jobs

Social

networks Social

networks

Indeed / Meta

search engines Google /

Indeed

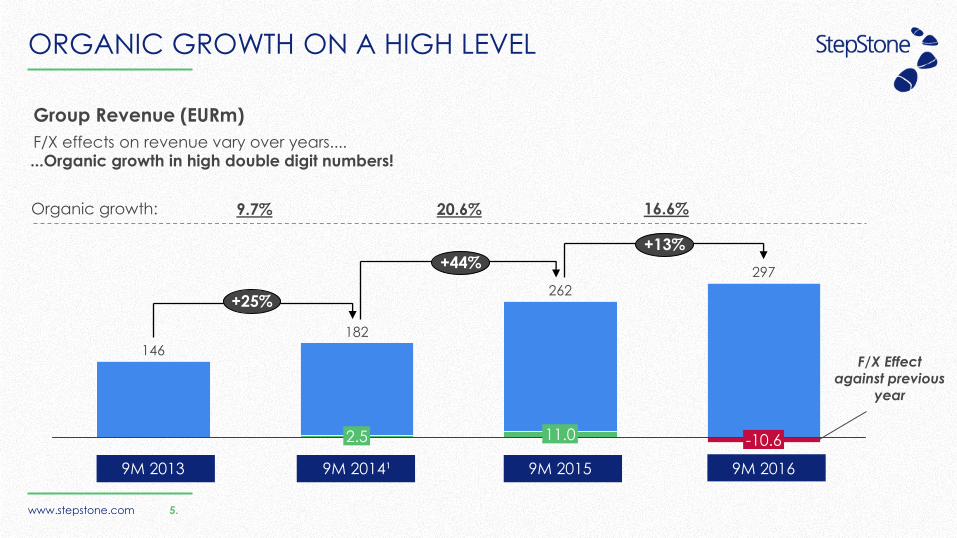

www.stepstone.com 5.

F/X Effect against previous

year

ORGANIC GROWTH ON A HIGH LEVEL

146

11.0 -10.6

+13%

+25%

2.5

182

262

9M 2013 9M 2014¹

+44%

9M 2015 9M 2016

297

9.7%

Group Revenue (EURm)

F/X effects on revenue vary over years....

20.6% 16.6% Organic growth:

...Organic growth in high double digit numbers!

www.stepstone.com

GROWTH ELEMENTS

www.stepstone.com 7.

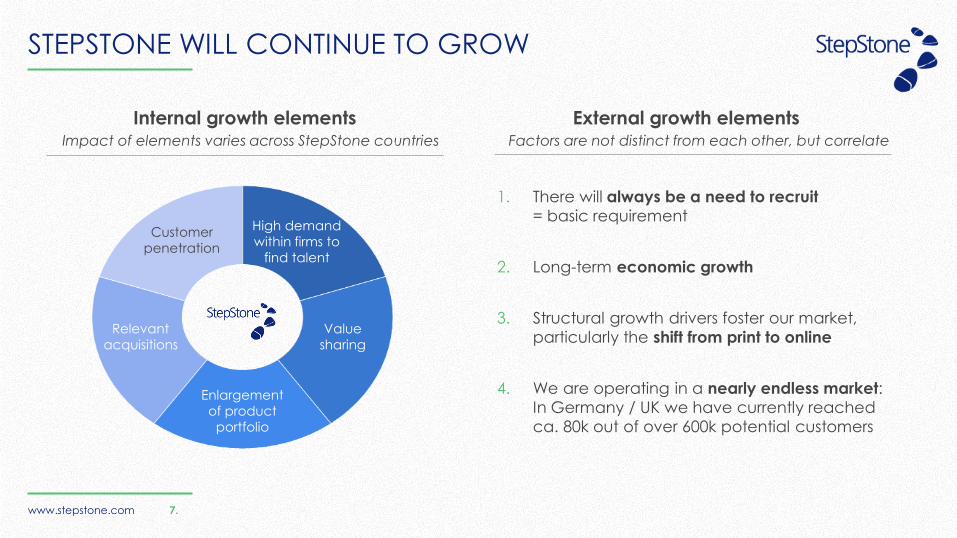

STEPSTONE WILL CONTINUE TO GROW

External growth elements

1. There will always be a need to recruit

= basic requirement

2. Long-term economic growth

3. Structural growth drivers foster our market,

particularly the shift from print to online

4. We are operating in a nearly endless market:

In Germany / UK we have currently reached

ca. 80k out of over 600k potential customers

Internal growth elements Impact of elements varies across StepStone countries Factors are not distinct from each other, but correlate

Customer

penetration

High demand

within firms to

find talent

Value

sharing

Enlargement

of product

portfolio

Relevant

acquisitions

www.stepstone.com 8.

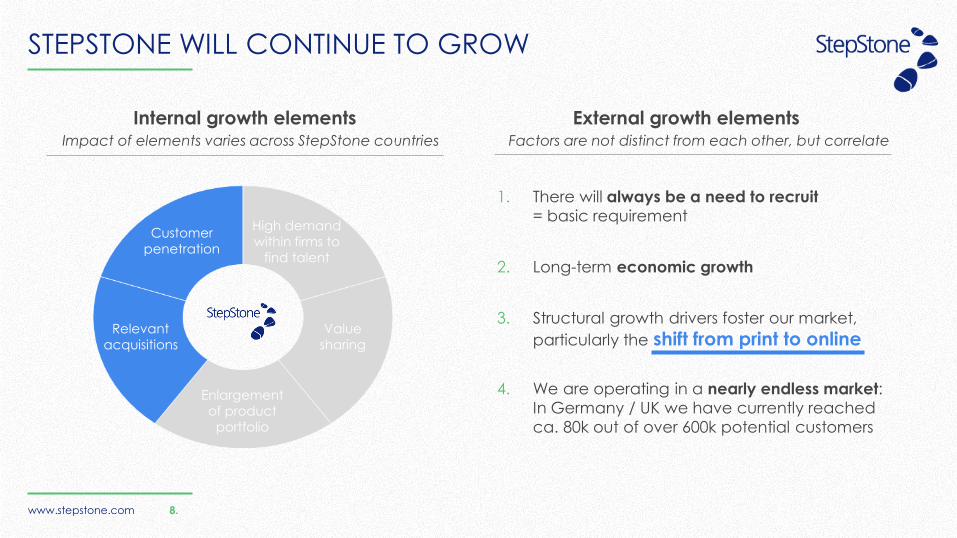

STEPSTONE WILL CONTINUE TO GROW

External growth elements

1. There will always be a need to recruit

= basic requirement

2. Long-term economic growth

3. Structural growth drivers foster our market,

particularly the shift from print to online

4. We are operating in a nearly endless market:

In Germany / UK we have currently reached

ca. 80k out of over 600k potential customers

Internal growth elements Impact of elements varies across StepStone countries Factors are not distinct from each other, but correlate

Customer

penetration

High demand

within firms to

find talent

Value

sharing

Enlargement

of product

portfolio

Relevant

acquisitions

www.stepstone.com 9.

Print Online

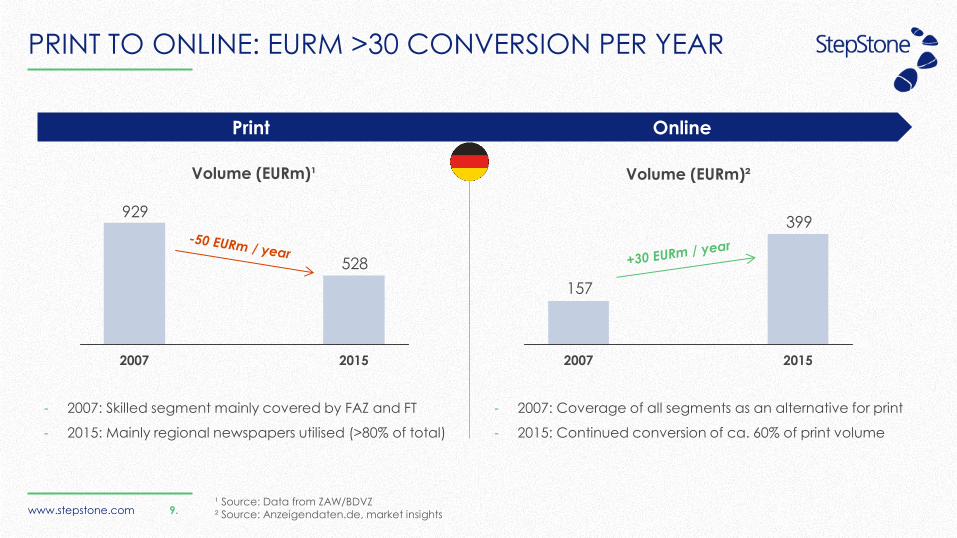

PRINT TO ONLINE: EURM >30 CONVERSION PER YEAR

929

528

2015 2007

157

399

2015 2007

Volume (EURm)¹ Volume (EURm)²

- 2007: Skilled segment mainly covered by FAZ and FT

- 2015: Mainly regional newspapers utilised (>80% of total)

¹ Source: Data from ZAW/BDVZ ² Source: Anzeigendaten.de, market insights

- 2007: Coverage of all segments as an alternative for print

- 2015: Continued conversion of ca. 60% of print volume

www.stepstone.com 10.

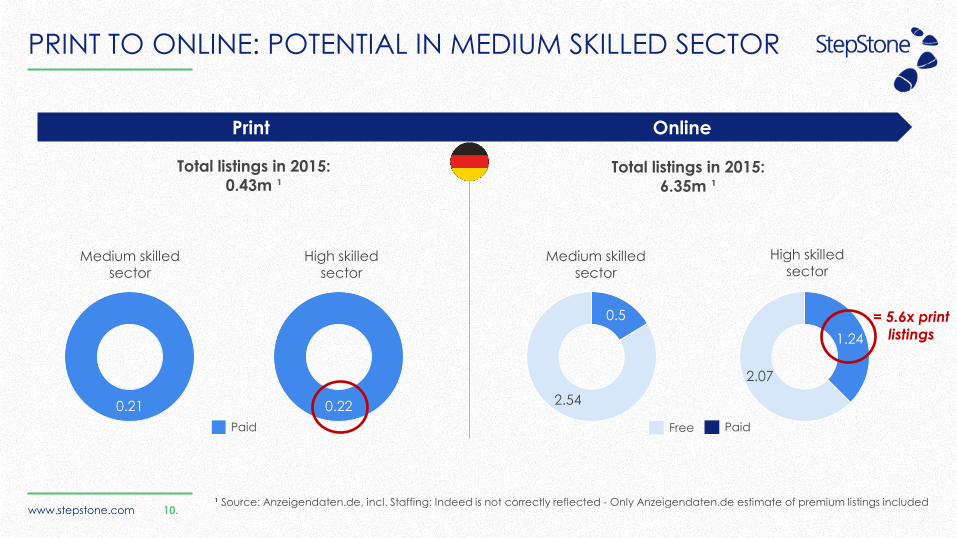

PRINT TO ONLINE: POTENTIAL IN MEDIUM SKILLED SECTOR

Total listings in 2015:

0.43m ¹ Total listings in 2015:

6.35m ¹

¹ Source: Anzeigendaten.de, incl. Staffing; Indeed is not correctly reflected - Only Anzeigendaten.de estimate of premium listings included

0.21 0.22

0.5

2.54

1.24

2.07

Paid Paid Free

= 5.6x print listings

Medium skilled sector

High skilled sector

Medium skilled sector

High skilled sector

Print Online

www.stepstone.com 11.

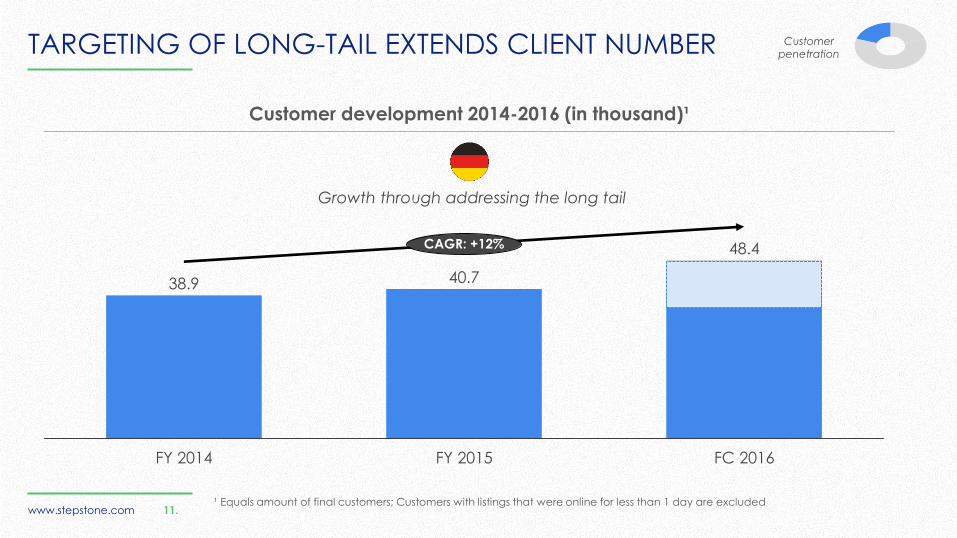

TARGETING OF LONG-TAIL EXTENDS CLIENT NUMBER

Customer development 2014-2016 (in thousand)¹

CAGR: +12%

FC 2016

48.4

FY 2015

40.7

FY 2014

38.9

¹ Equals amount of final customers; Customers with listings that were online for less than 1 day are excluded

Growth through addressing the long tail

Customer penetration

www.stepstone.com 13.

5

10

15

20

25

0.5

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.0

7.5

07/12 04/13

10.3

7.2

10/13 04/11 01/12 07/13 10/12

13.2 13.4

04/12 01/16 04/16 07/16 10/16 10/15 07/15 04/15 01/15 10/14 07/14 04/14 07/11 10/11 01/11

8.2

01/13 01/14

7.9 8.9 8.6

10.9 10.4

8.7 9.8

9.1 8.5

6.5

9.5

11.4 11.3 11.6 11.1

7.4

9.2

6.8

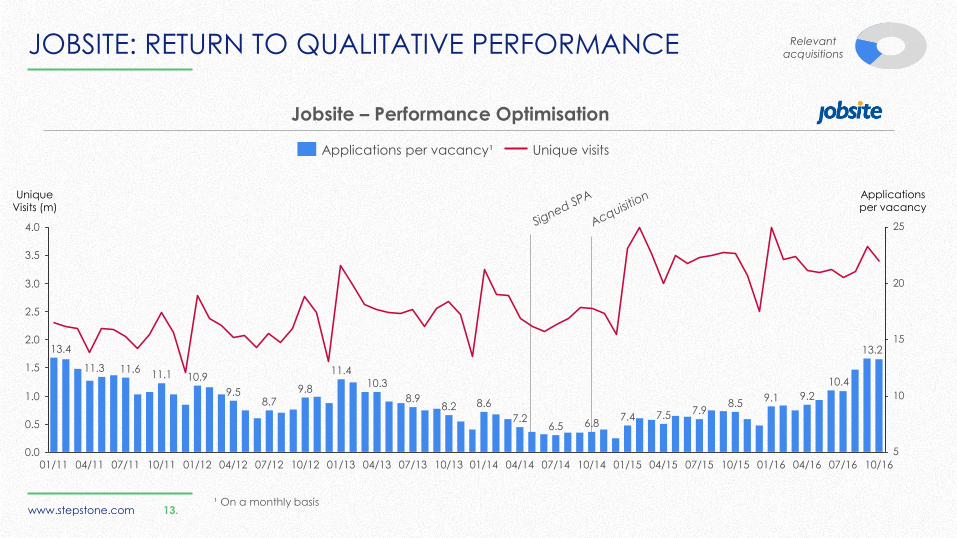

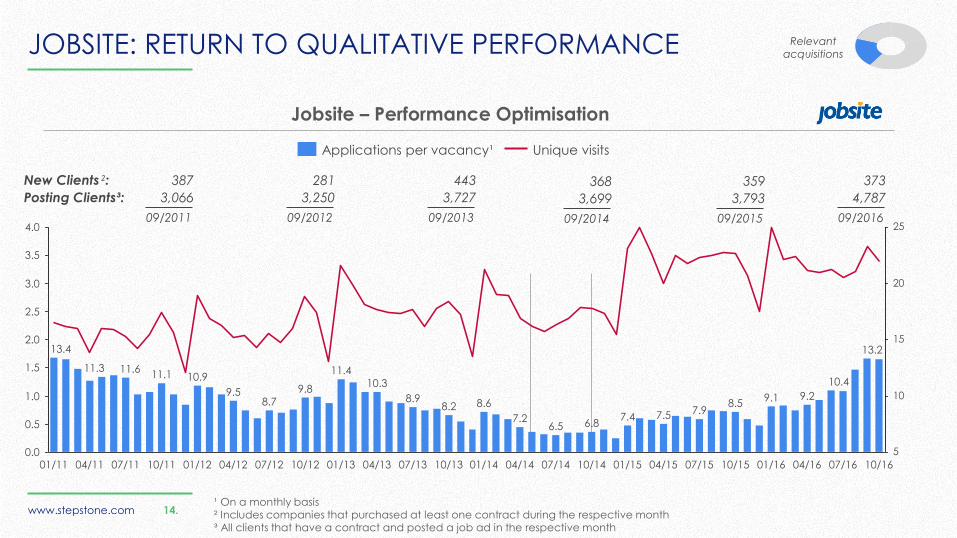

JOBSITE: RETURN TO QUALITATIVE PERFORMANCE Relevant acquisitions

Unique visits Applications per vacancy¹

Applications per vacancy

Jobsite – Performance Optimisation

Unique Visits (m)

¹ On a monthly basis

www.stepstone.com 14.

5

10

15

20

25

0.5

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.0

7.5

07/12 04/13

10.3

7.2

10/13 04/11 01/12 07/13 10/12

13.2 13.4

04/12 01/16 04/16 07/16 10/16 10/15 07/15 04/15 01/15 10/14 07/14 04/14 07/11 10/11 01/11

8.2

01/13 01/14

7.9 8.9 8.6

10.9 10.4

8.7 9.8

9.1 8.5

6.5

9.5

11.4 11.3 11.6 11.1

7.4

9.2

6.8

JOBSITE: RETURN TO QUALITATIVE PERFORMANCE

Jobsite – Performance Optimisation

Relevant acquisitions

Unique visits Applications per vacancy¹

387

3,066

09/2011

New Clients²:

Posting Clients³:

281

3,250

09/2012

443

3,727

09/2013

368

3,699

09/2014

359

3,793

09/2015

373

4,787

09/2016

¹ On a monthly basis ² Includes companies that purchased at least one contract during the respective month ³ All clients that have a contract and posted a job ad in the respective month

www.stepstone.com 15.

2017: Leverage of brand and company potentials

1. Further improvement of candidate delivery

• Usage of technological group competencies

• Increase of candidate reach & product customisation

2. Capitalisation of product performance in sales

• Built up on increased candidate delivery and product performance

• Apply best-in-class sales know-how / group competencies

3. In addition, revitalization of brand awareness:

• Extension of own campaigns to strengthen business position

• Follow the German example: Recently StepStone.de was awarded by Handelsblatt as one of the top 5 most popular online brands together with Skype, WhatsApp, Google+ and Pinterest ¹

¹ Category ‘Digital Life / Social web, Dating & Recruiting Sites’ www.stepstone.com 15.

JOBSITE: RETURN TO PERFORMANCE Relevant acquisitions

www.stepstone.com

BUSINESS ENVIRONMENT

www.stepstone.com 17.

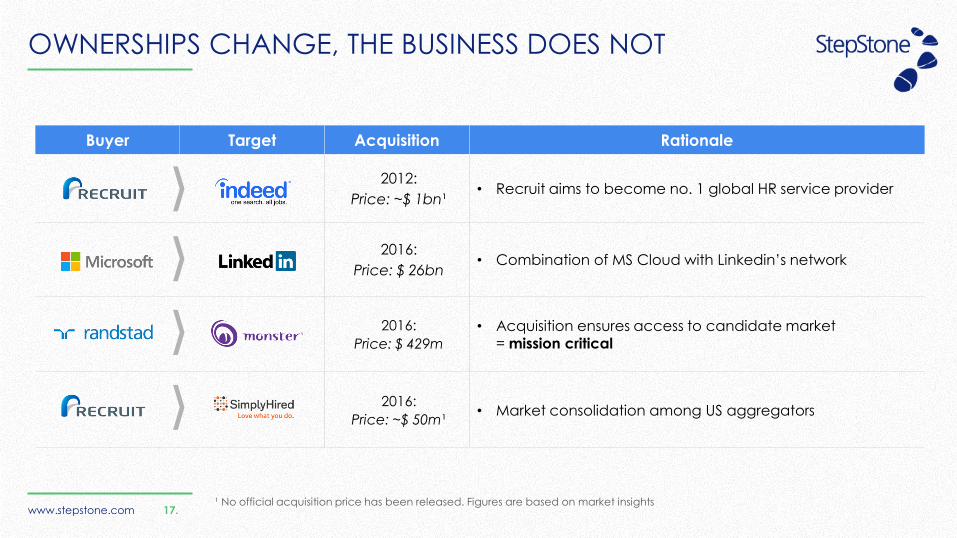

OWNERSHIPS CHANGE, THE BUSINESS DOES NOT

Buyer Target Acquisition Rationale

2012:

Price: ~$ 1bn¹ • Recruit aims to become no. 1 global HR service provider

2016:

Price: $ 26bn • Combination of MS Cloud with Linkedin’s network

2016:

Price: $ 429m

• Acquisition ensures access to candidate market = mission critical

2016:

Price: ~$ 50m¹ • Market consolidation among US aggregators

¹ No official acquisition price has been released. Figures are based on market insights

www.stepstone.com 18.

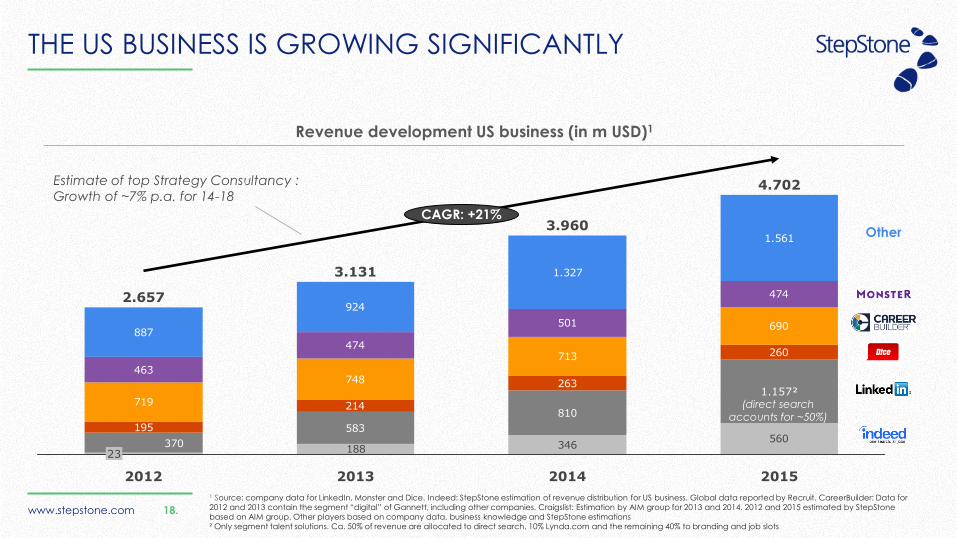

THE US BUSINESS IS GROWING SIGNIFICANTLY

Revenue development US business (in m USD)1

346560

583

810

195

214

263

260

719

748

713

690

463

474

501

474

887

924

1.327

1.561

188370

CAGR: +21%

2015

4.702

1.157²

2014

3.960

2013

3.131

23

2012

2.657

Estimate of top Strategy Consultancy :

Growth of ~7% p.a. for 14-18

1 Source: company data for LinkedIn, Monster and Dice. Indeed: StepStone estimation of revenue distribution for US business. Global data reported by Recruit. CareerBuilder: Data for

2012 and 2013 contain the segment “digital” of Gannett, including other companies. Craigslist: Estimation by AIM group for 2013 and 2014. 2012 and 2015 estimated by StepStone

based on AIM group. Other players based on company data, business knowledge and StepStone estimations

² Only segment talent solutions. Ca. 50% of revenue are allocated to direct search, 10% Lynda.com and the remaining 40% to branding and job slots

Other

(direct search accounts for ~50%)

www.stepstone.com 19.

CANDIDATE CENTRIC TRENDS AND DEVELOPMENT

StepStone learnings

1. Being on-top of core business

2. Drive and capitalise on candidate centric trends

(product and services)

3. Secure long term success by driving on innovations

along E-Recruitment cycle (venture new bets)

Market trends

• Basic principles of job search remain (perfect match)

• Recruiters’ search for talented candidates intensified

• Candidates expect better products & services

• Other players try to solve new recruiter needs

respectively increased candidate expectations

www.stepstone.com

PRODUCT STRATEGY

www.stepstone.com 21.

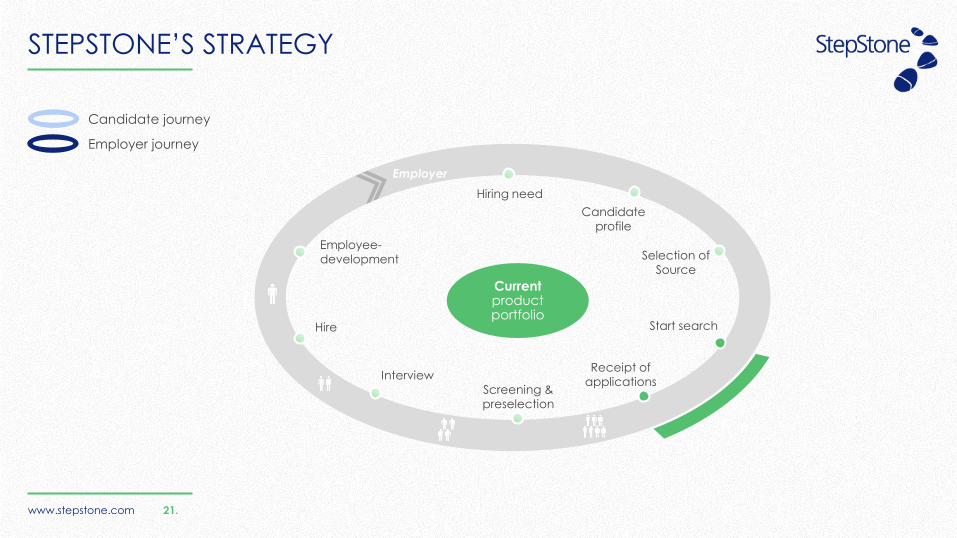

STEPSTONE’S STRATEGY

Hiring need

Candidate

profile

Receipt of

applications Screening &

preselection

Interview

Hire

Employee-

development Selection of

Source

Start search

Employer

Current product portfolio

Candidate journey

Employer journey

www.stepstone.com 22.

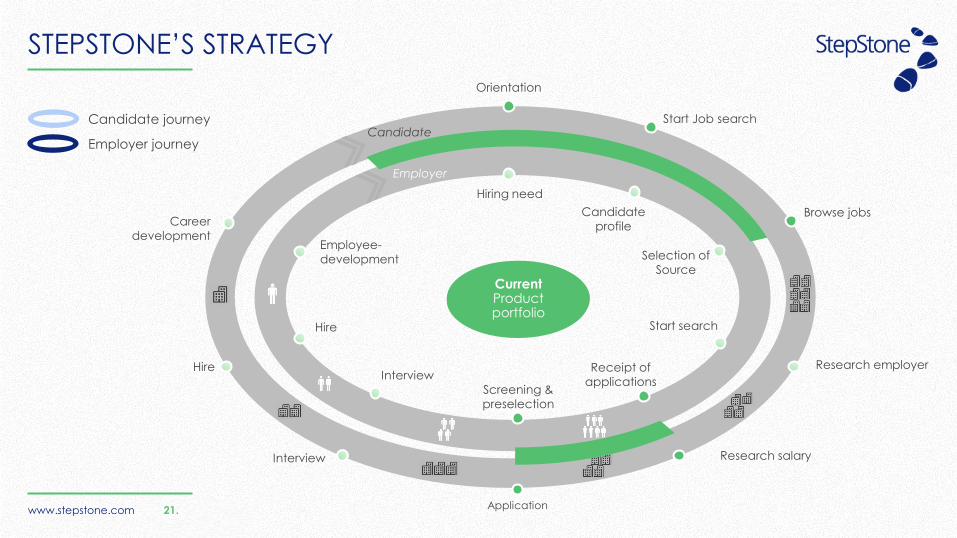

STEPSTONE’S STRATEGY

Hiring need

Candidate

profile

Receipt of

applications Screening &

preselection

Interview

Hire

Employee-

development Selection of

Source

Start search

Employer

Current product portfolio

Orientation

Start Job search

Browse jobs

Research employer

Research salary

Application

Interview

Hire

Career

development

Candidate journey

Employer journey Candidate

Current Product portfolio

21.

www.stepstone.com 23.

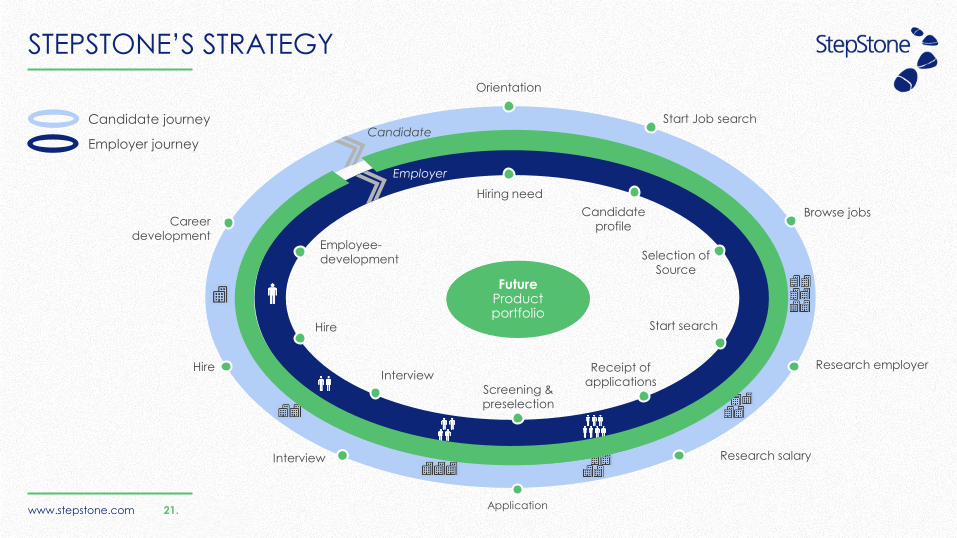

STEPSTONE’S STRATEGY

Hiring need

Candidate

profile

Receipt of

applications Screening &

preselection

Interview

Hire

Employee-

development Selection of

Source

Start search

Employer

Current product portfolio

Orientation

Start Job search

Browse jobs

Research employer

Research salary

Application

Interview

Hire

Career

development

Candidate journey

Employer journey Candidate

Current Product portfolio

Future Product portfolio

21.

www.stepstone.com 22.

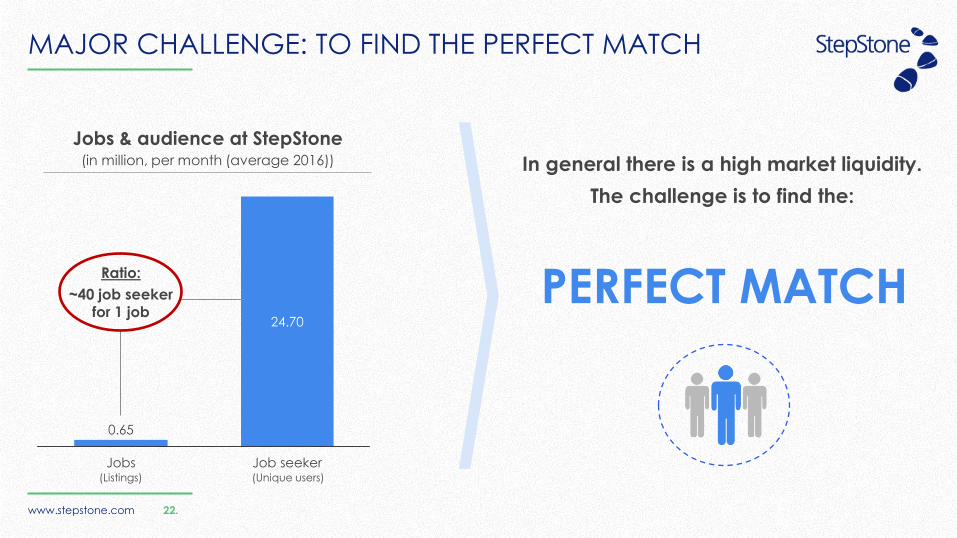

MAJOR CHALLENGE: TO FIND THE PERFECT MATCH

In general there is a high market liquidity.

The challenge is to find the:

PERFECT MATCH

Jobs

24.70

0.65

Job seeker (Unique users) (Listings)

Jobs & audience at StepStone (in million, per month (average 2016))

Ratio:

~40 job seeker for 1 job

www.stepstone.com 23.

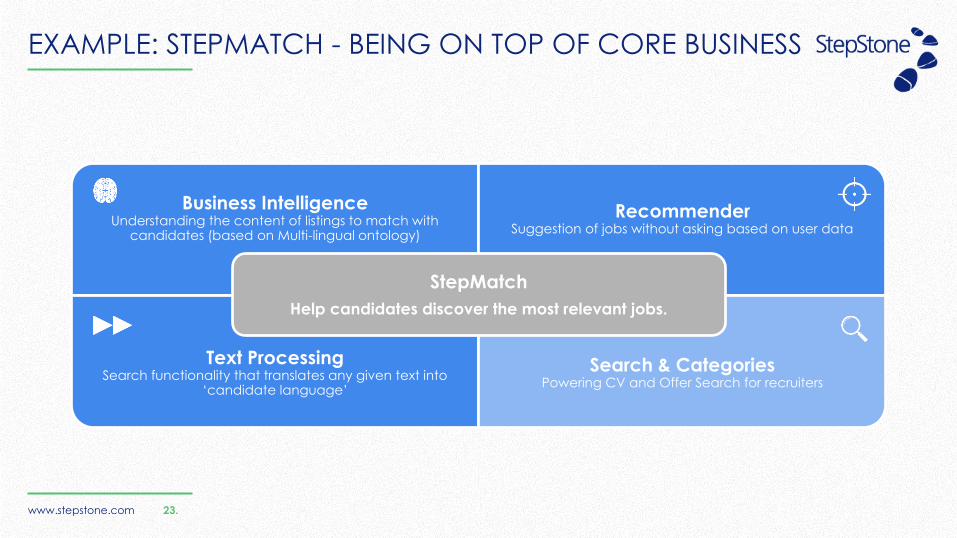

EXAMPLE: STEPMATCH - BEING ON TOP OF CORE BUSINESS

Business Intelligence Understanding the content of listings to match with

candidates (based on Multi-lingual ontology)

Recommender Suggestion of jobs without asking based on user data

Text Processing Search functionality that translates any given text into

‘candidate language’

Search & Categories Powering CV and Offer Search for recruiters

StepMatch

Help candidates discover the most relevant jobs.

www.stepstone.com 24.

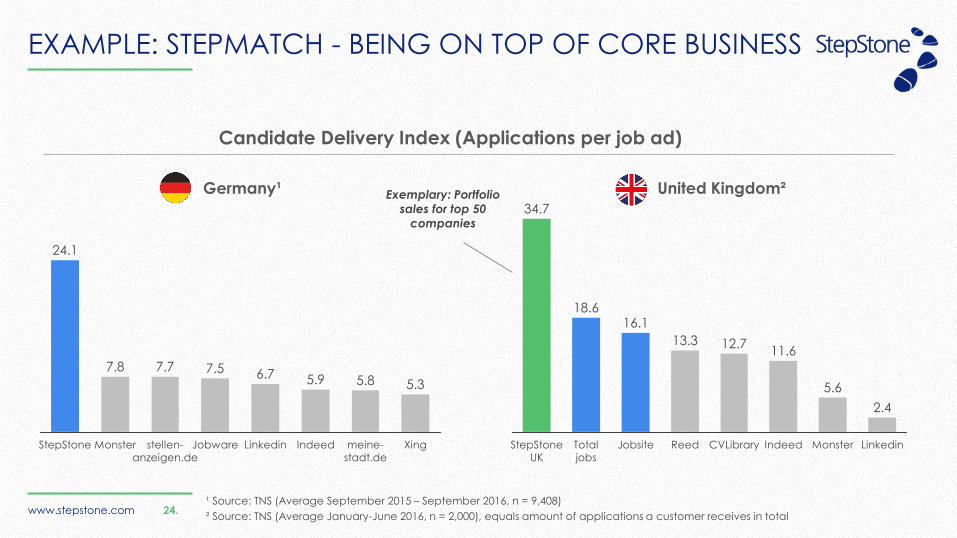

EXAMPLE: STEPMATCH - BEING ON TOP OF CORE BUSINESS

Candidate Delivery Index (Applications per job ad)

2.4

Monster

5.6

Indeed

11.6

CVLibrary

12.7

Reed

13.3

Jobsite

16.1

Total jobs

18.6

StepStone UK

34.7

Germany¹ United Kingdom²

¹ Source: TNS (Average September 2015 – September 2016, n = 9,408)

² Source: TNS (Average January-June 2016, n = 2,000), equals amount of applications a customer receives in total

Exemplary: Portfolio

sales for top 50

companies

5.3

meine-stadt.de

5.8

Indeed

5.9

6.7

Jobware

7.5

stellen-anzeigen.de

7.7

Monster

7.8

StepStone

24.1

www.stepstone.com 25.

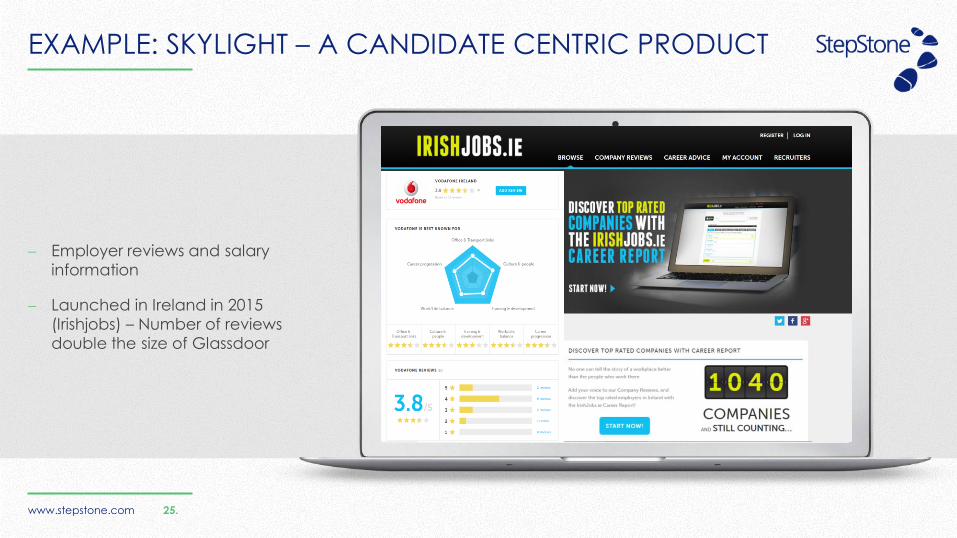

Employer reviews and salary

information

Launched in Ireland in 2015

(Irishjobs) – Number of reviews

double the size of Glassdoor

EXAMPLE: SKYLIGHT – A CANDIDATE CENTRIC PRODUCT

www.stepstone.com 26.

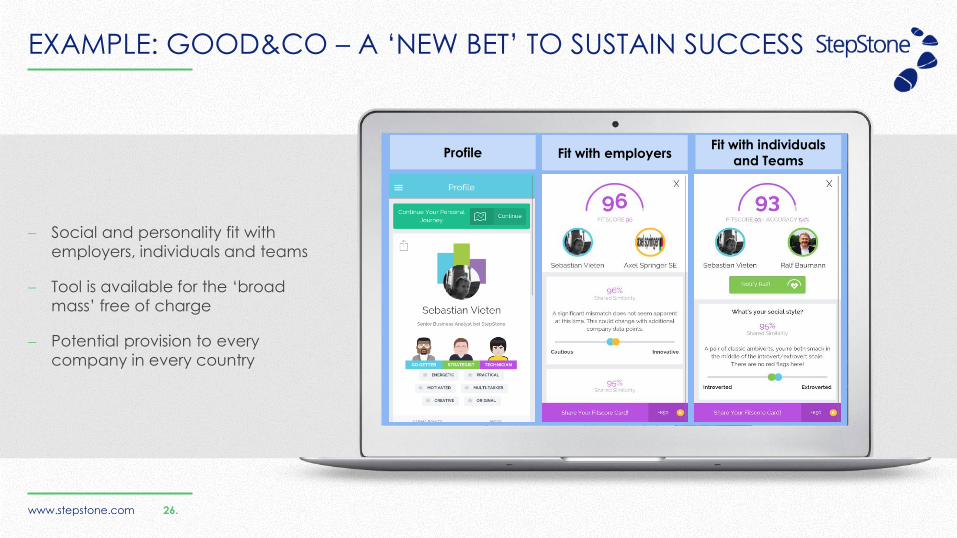

Social and personality fit with

employers, individuals and teams

Tool is available for the ‘broad

mass’ free of charge

Potential provision to every

company in every country

Profile Fit with employers Fit with individuals

and Teams

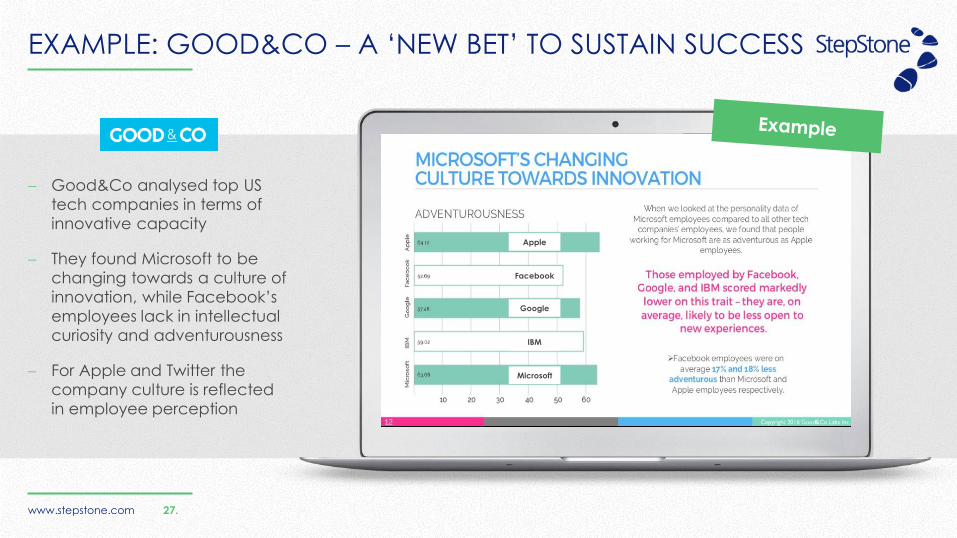

EXAMPLE: GOOD&CO – A ‘NEW BET’ TO SUSTAIN SUCCESS

www.stepstone.com 27.

EXAMPLE: GOOD&CO – A ‘NEW BET’ TO SUSTAIN SUCCESS

Good&Co analysed top US

tech companies in terms of

innovative capacity

They found Microsoft to be

changing towards a culture of

innovation, while Facebook’s

employees lack in intellectual

curiosity and adventurousness

For Apple and Twitter the

company culture is reflected

in employee perception

Apple

IBM

Microsoft

www.stepstone.com

STEPSTONE’S TECH AND BUSINESS

INITIATIVES WILL RESULT IN…

www.stepstone.com 29.

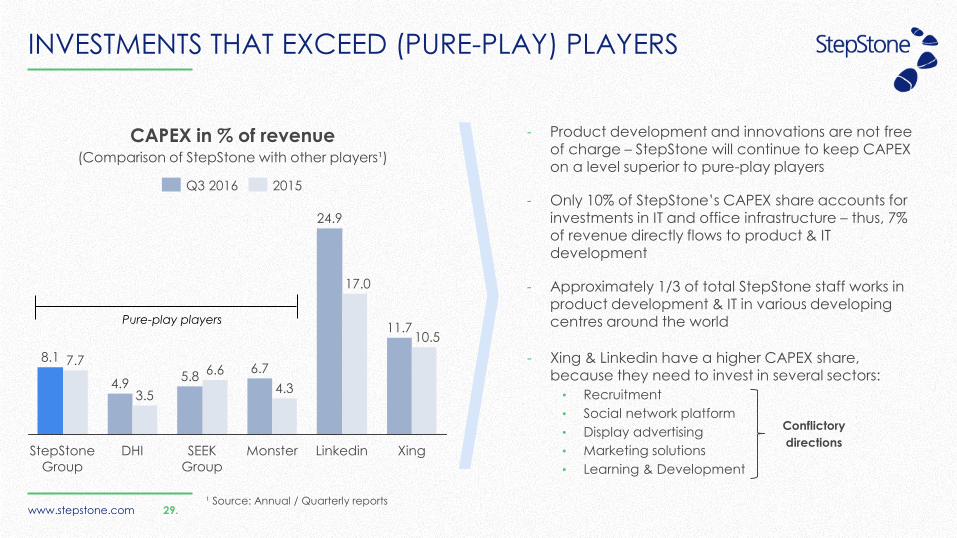

CAPEX in % of revenue (Comparison of StepStone with other players¹)

INVESTMENTS THAT EXCEED (PURE-PLAY) PLAYERS

11.7

Linkedin Xing

10.5

17.0

24.9

Monster

4.3

6.7

SEEK

Group

6.6 5.8

DHI

3.5 4.9

StepStone

Group

7.7 8.1

Q3 2016 2015

- Product development and innovations are not free of charge – StepStone will continue to keep CAPEX on a level superior to pure-play players

- Only 10% of StepStone’s CAPEX share accounts for investments in IT and office infrastructure – thus, 7%

of revenue directly flows to product & IT development

- Approximately 1/3 of total StepStone staff works in product development & IT in various developing centres around the world

¹ Source: Annual / Quarterly reports

Pure-play players

Conflictory

directions

- Xing & Linkedin have a higher CAPEX share, because they need to invest in several sectors:

• Recruitment

• Social network platform

• Display advertising

• Marketing solutions

• Learning & Development

www.stepstone.com 30.

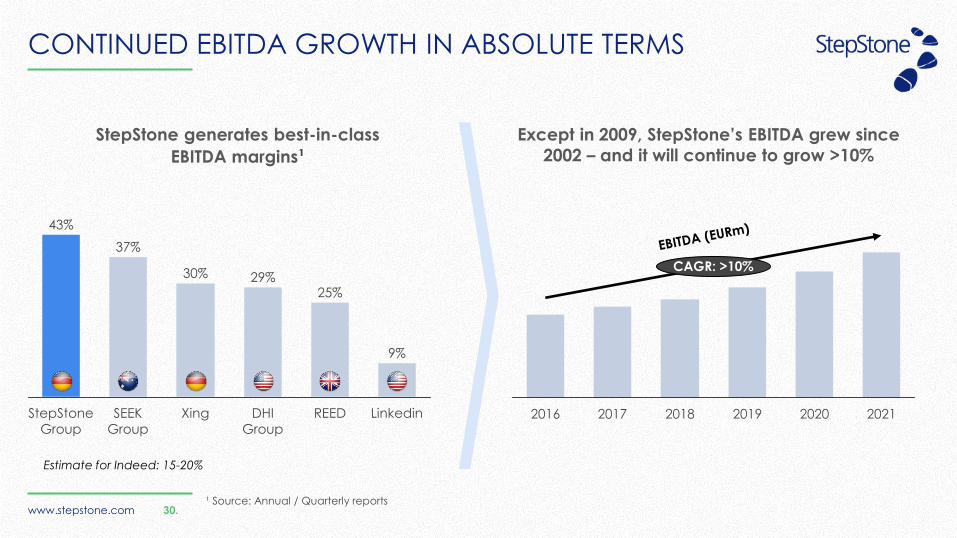

CONTINUED EBITDA GROWTH IN ABSOLUTE TERMS

StepStone generates best-in-class

EBITDA margins¹

25%

REED Linkedin

9%

DHI

Group

29%

30%

SEEK

Group

37%

StepStone

Group

43%

Except in 2009, StepStone’s EBITDA grew since

2002 – and it will continue to grow >10%

Estimate for Indeed: 15-20%

2016 2018 2017 2019 2020 2021

CAGR: >10%

¹ Source: Annual / Quarterly reports

www.stepstone.com 31.

KEY TAKE-AWAYS

Growing and shaping the future of E-

Recruitment!

Business continues to grow, we will invest in growth initiatives and new

applications

EBITDA will continue to grow >10% CAGR