Embed Size (px)

Citation preview

Capital Project FundsWASB Joint Convention

January 21, 2015

Capital Projects Funds - WUFAR FUND 4x

Capital Project Funds account for financial resources used for capital facilities.● Fund 41 is used for projects financed by a special tax

levy. (72 Districts)● Fund 46 is used for projects financed with funds

transferred from the General Fund. (Seven Districts)● Fund 49 is used for projects financed with borrowed

funds.

ESTABLISHING A SCHOOL CAPITAL EXPANSION FUND (Power of the Annual Meeting)

RESOLUTION CREATING A CAPITAL EXPANSION FUNDAND LEVYING A TAX IN CONNECTION THEREWITH

BE IT RESOLVED by the electors of the __________ School District that a Capital Expansion Fund is hereby created pursuant to Section 120.10(10m) of the Wisconsin Statutes for the purpose of financing building and site capital expenditures related to [propose/use/specific projects] ; and BE IT FURTHER RESOLVED that a tax in the amount of $X be levied for the 20xx-20xx school year to be deposited in the Capital Expansion Fund created above to be used only for the purposes specified above.

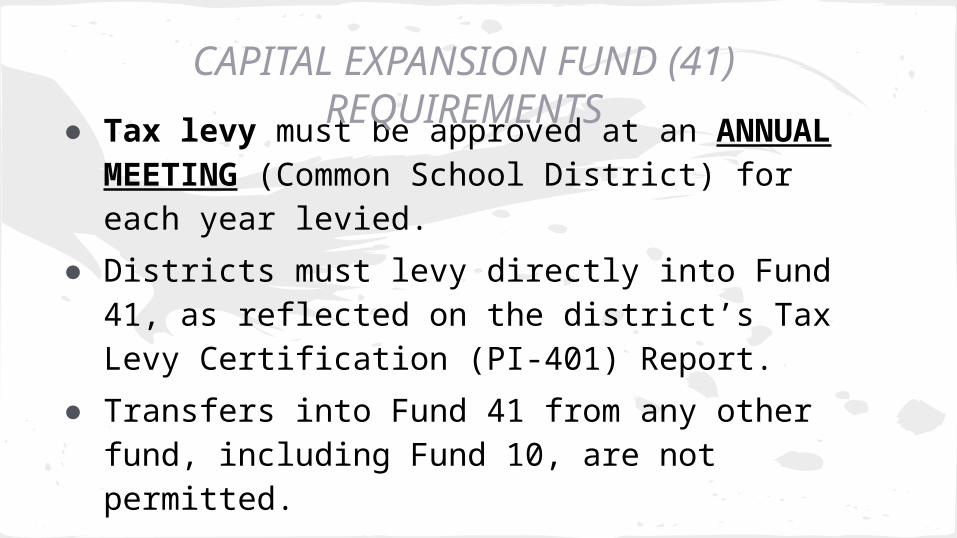

● Tax levy must be approved at an ANNUAL MEETING (Common School District) for each year levied.

● Districts must levy directly into Fund 41, as reflected on the district’s Tax Levy Certification (PI-401) Report.

● Transfers into Fund 41 from any other fund, including Fund 10, are not permitted.

CAPITAL EXPANSION FUND (41) REQUIREMENTS

CAPITAL EXPANSION FUND (41)REQUIREMENTS and RESTRICTIONS

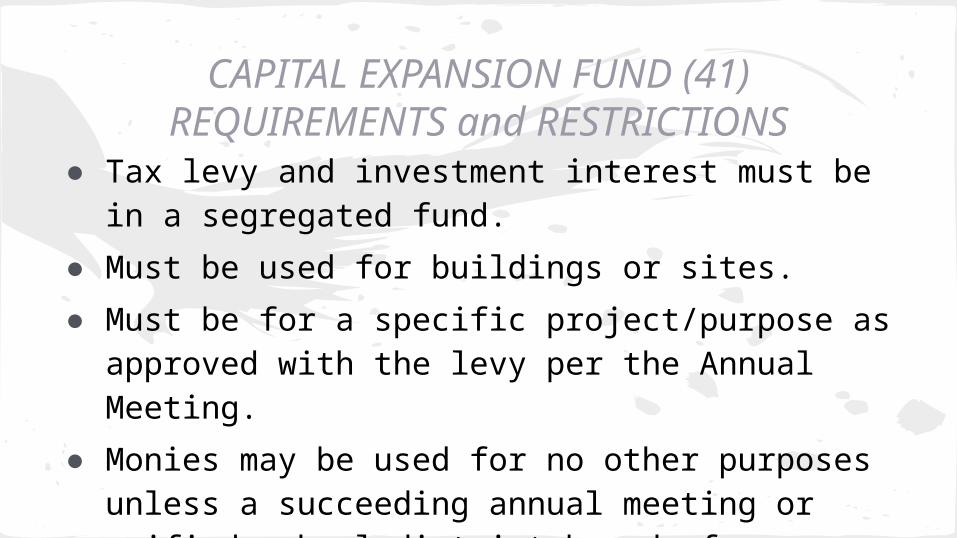

● Tax levy and investment interest must be in a segregated fund.

● Must be used for buildings or sites.

● Must be for a specific project/purpose as approved with the levy per the Annual Meeting.

● Monies may be used for no other purposes unless a succeeding annual meeting or unified school district board of education votes to change the purpose.

CAPITAL EXPANSION FUND REPORTING

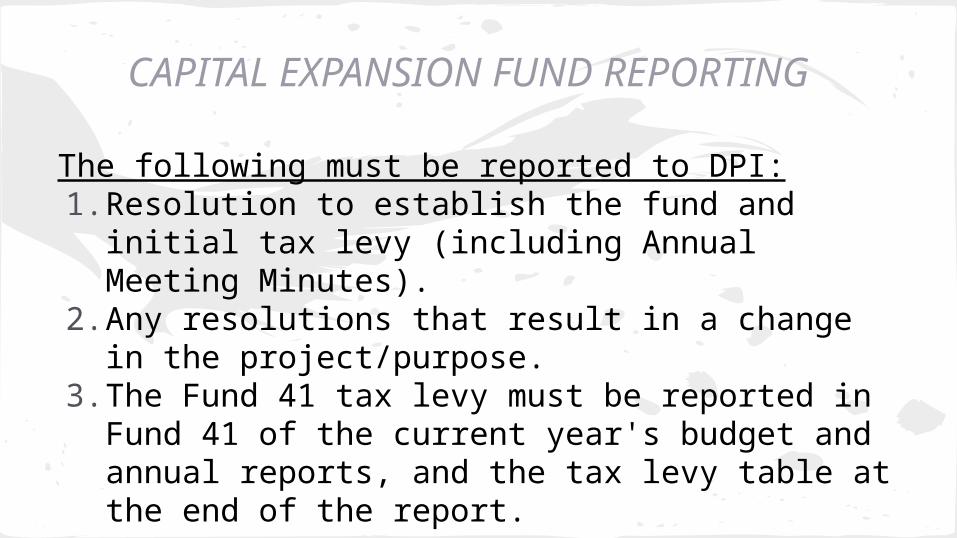

The following must be reported to DPI:1. Resolution to establish the fund and initial tax levy

(including Annual Meeting Minutes).2. Any resolutions that result in a change in the

project/purpose.3. The Fund 41 tax levy must be reported in Fund 41 of

the current year's budget and annual reports, and the tax levy table at the end of the report.

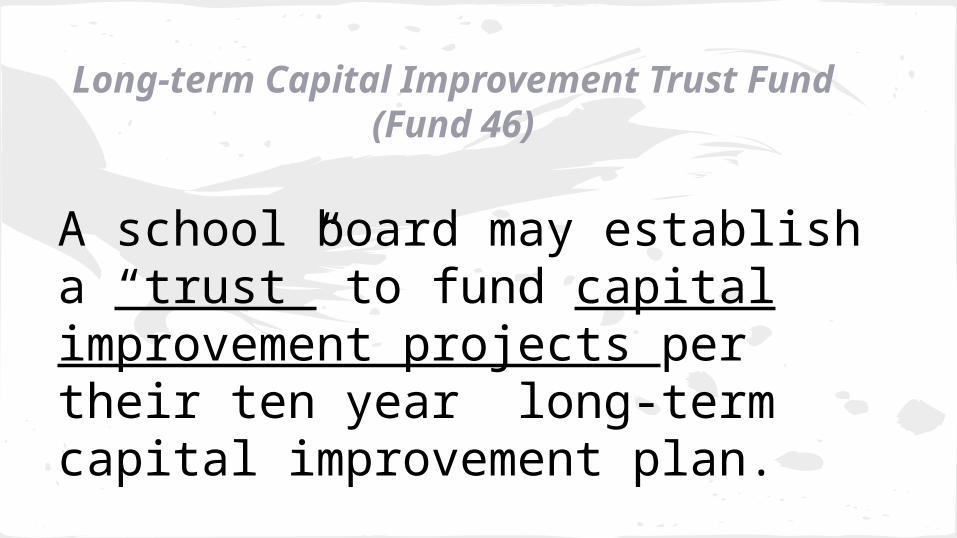

Long-term Capital Improvement Trust Fund (Fund 46)

A school board may establish a “trust” to fund capital improvement projects per their ten year long-term capital improvement plan.

Long-term Capital Improvement Trust Fund (46)

REQUIREMENTS - Getting Started

�1. Board approved 10 year capital improvement plan.2. Board resolution to establish a trust.3. Creation of a segregated bank account.

Long-term Capital Improvement Trust Fund (46)

REQUIREMENTS and RESTRICTIONS● �Funds may only be accessed five years after the

establishment of the “trust” fund.● �Funds must be physically deposited and held in a

segregated bank/investment (separate and distinct from other district accounts) until they are expended for capital improvement projects per the district’s plan.

● �Funds invested as per sec. 66.0603, Wis. Stats.

Long-term Capital Improvement Trust Fund (46)

REQUIREMENTS and REPORTINGThe following must be reported to DPI:

1. Official Board minutes approving the long-term capital improvement plan.

2. Signed resolution creating the Long-term Capital Improvement Trust Fund or official minutes documenting the creation of the fund.

3. Documentation that confirms the existence of a segregated bank/investment account.

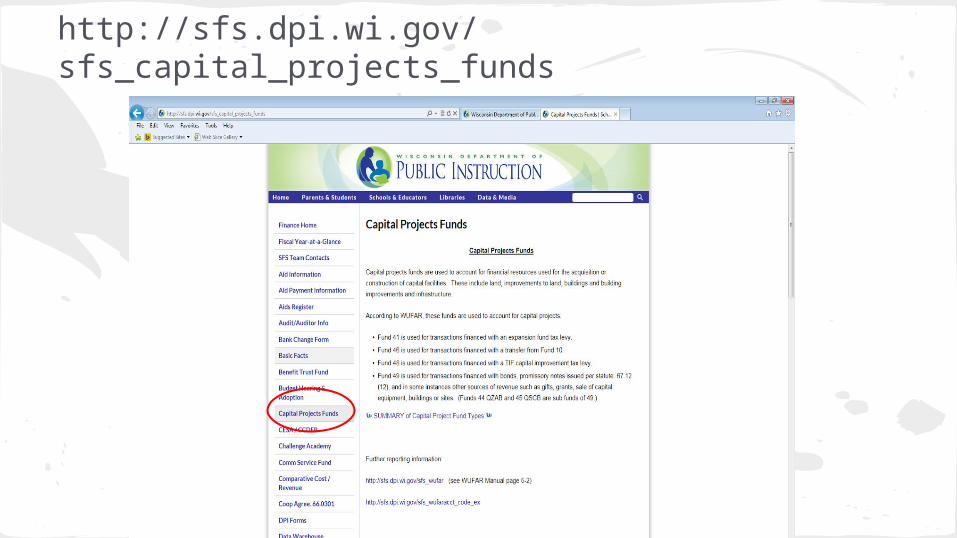

http://sfs.dpi.wi.gov/sfs_capital_projects_funds

Carey Bradley, DPI SFS Consultant, 608-267-3752