Embed Size (px)

DESCRIPTION

Real Option Valuation of Early Stage Technology

Citation preview

Real Option Valuation of Technology

Application of Precision Tree

Palisade Risk Conference 2011

Michael Brand

© 2011Captum Capital Limited

2

Valuation of Real Options

§ What are Real Options?

§ How are they valued?

§ Precision Tree models

3

Amsterdam – in year 1637

Bubble Tulips by Nancy Ethiel

4

The Viceroy Tulip

Source: Wikipedia

5

Tulip prices escalated x 20

Source: Wikipedia

6

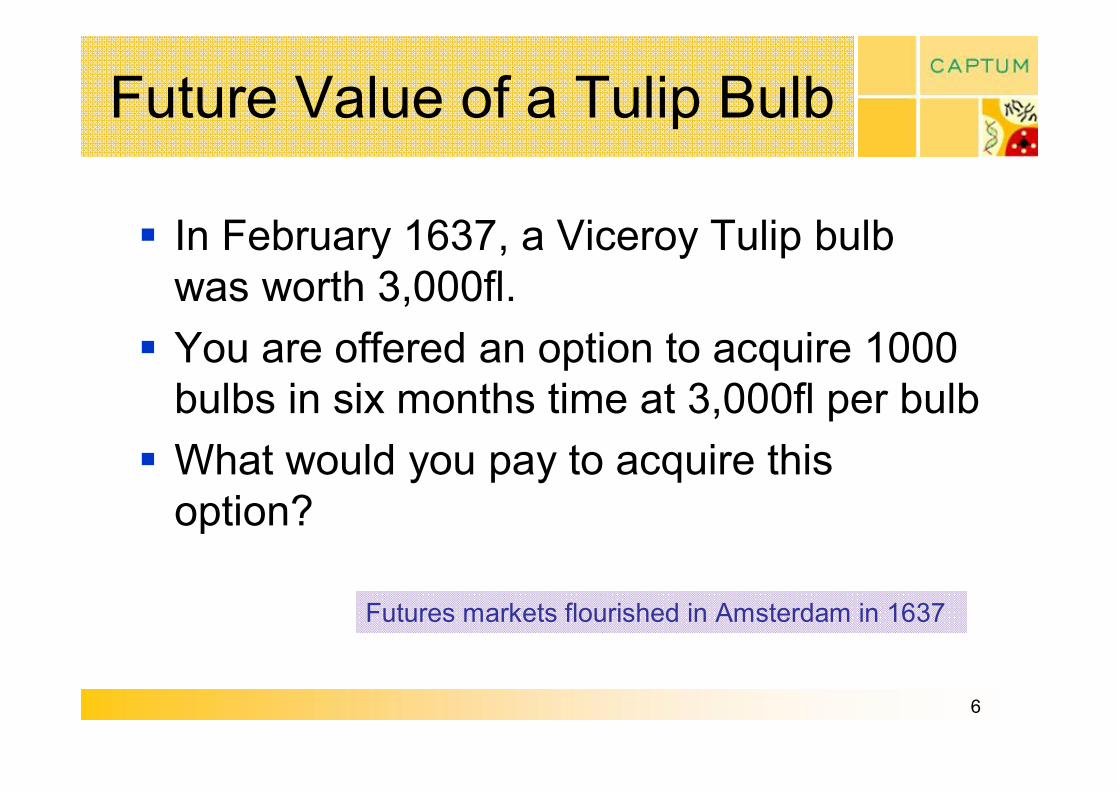

Future Value of a Tulip Bulb

§ In February 1637, a Viceroy Tulip bulb was worth 3,000fl. § You are offered an option to acquire 1000 bulbs in six months time at 3,000fl per bulb § What would you pay to acquire this option?

Futures markets flourished in Amsterdam in 1637

7

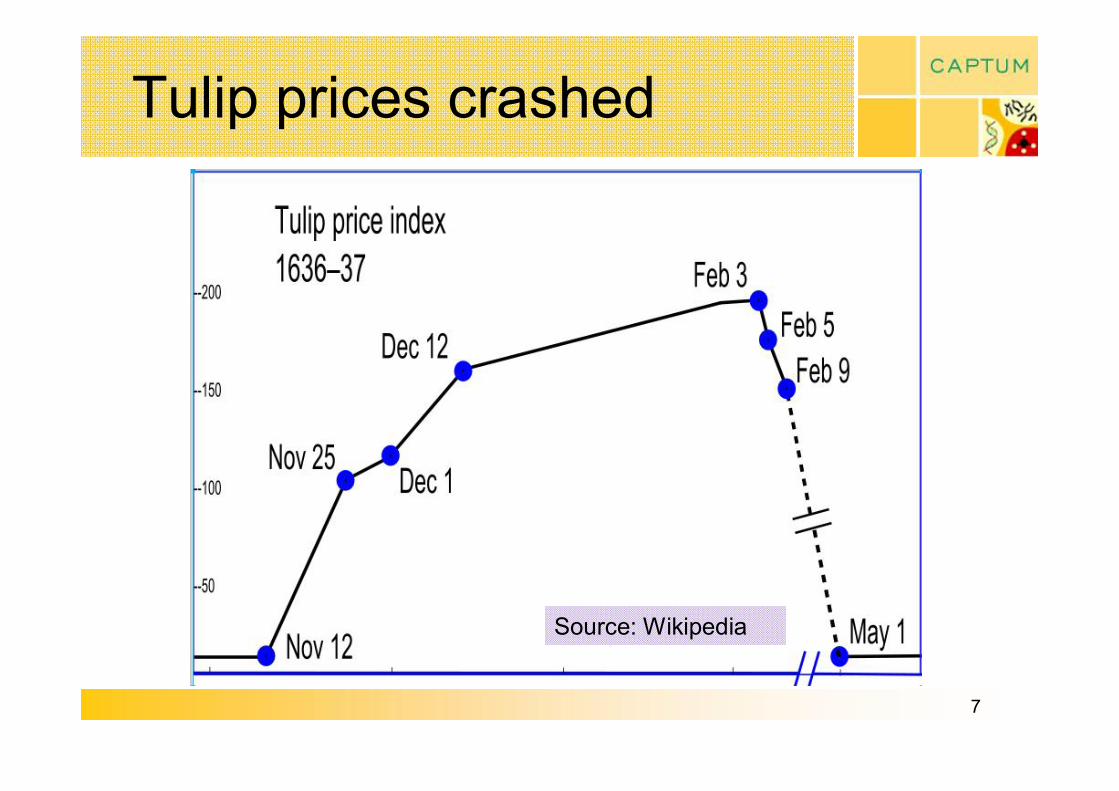

Tulip prices crashed

Source: Wikipedia

8

Future Options are Risky

Newton lost £20,000 of his own money in the South Sea Bubble of 1720

9

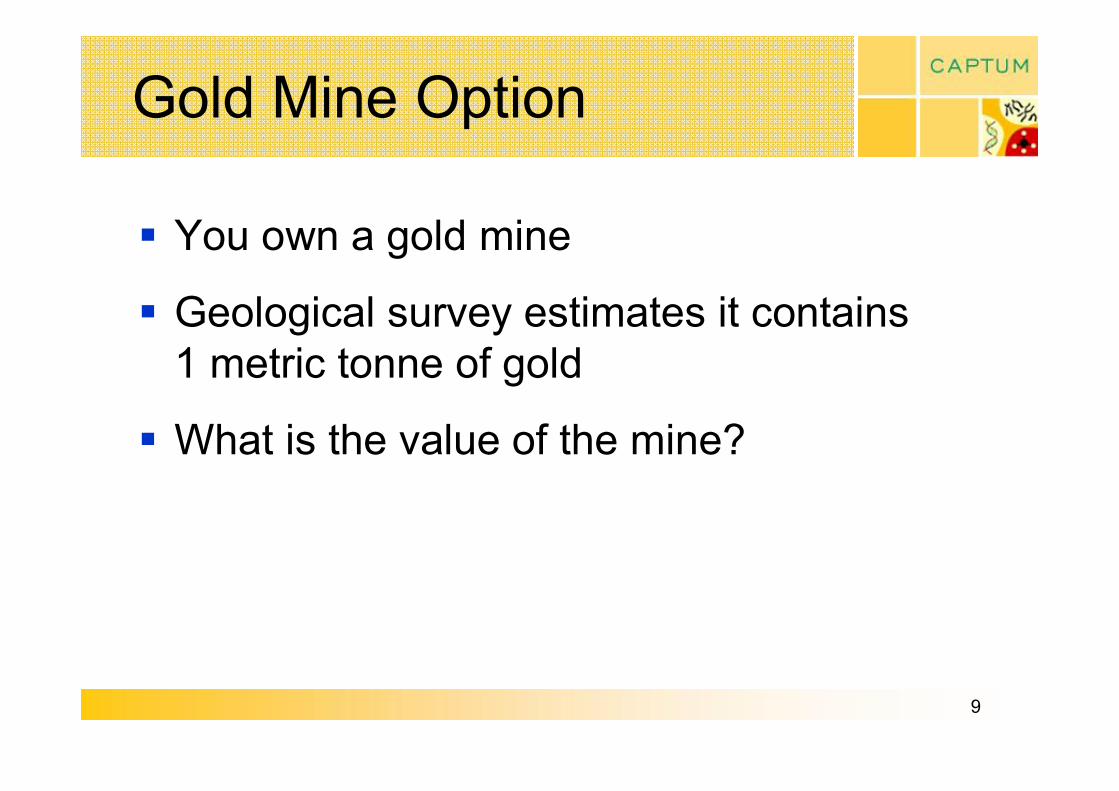

Gold Mine Option

§ You own a gold mine

§ Geological survey estimates it contains 1 metric tonne of gold

§ What is the value of the mine?

10

Value of Gold Mine

§ Its value depends on the price of gold § Risk

§ You can start or stop mining depending on the price of gold § Flexibility in outcome

This is a classic Real Option

11

Historic Gold Price Trends

12

Real Options

§ Risk or Uncertainty in the…outcome

§ Nonlinearity: flexibility to react in different ways…so that a new set of outcomes is achieved

Source: Michael Rees, Financial Modelling in Practice (2008)

13

Technology Development

R&D Project

Fund

Failure

Success Commercial Development

Fund

Option Price

Option Exercise Price

14

Risk Adjusted NPV

∑ + = t

t t

R C P rNPV ) 1 (

rNPV depends on 3 factors:

•Probability, P

•Cash Flow, C

•Discount Rate, R

Most commonly used method for valuing technology

15

Technology Project Value

10000 1000 100 PV

0.5x0.9 0.5 1 P

15735 0 1255 0 100 Cash Flow

4 3 2 1 0 Year

rNPV = 100 + 0.5 x 1000 + 0.45 x 10000 = £3,900,000

Cash Flow in £000s

Discount Rate R = 12%

16

Decision Tree Value Cash Flow in £000s

Discount Rate R = 12%

All Cash Flows discounted to PV

17

Real Option Valuation

§ Key variables § Underlying Asset Value – Enterprise Value § Exercise Price § Term to Exercise § Volatility of Underlying Asset § Discount Rate

18

RO Valuation Methods

§ Black Scholes OptionPricing Model*

§ Binomial Model*

§ Monte Carlo Simulation

§ Decision Tree

* Developed for financial option valuation

19

Black Scholes Equation

Present Value of a Call Option: ) ( ) ( 2 1 d N EXe d PN PV t r f − − =

where:

t t t r EX P

d f

σ σ 2 / ) / log(

1

2 + + =

t

t t r EX P d t

σ

σ 2 / ) / log( 2

2 − +

=

= variance on return σ

= price of security P

= time to exercise t

= exercise price EX = normal probability function N(d)

1 ) ( 2

_

− −

= N P P

r f = risk free rate

20

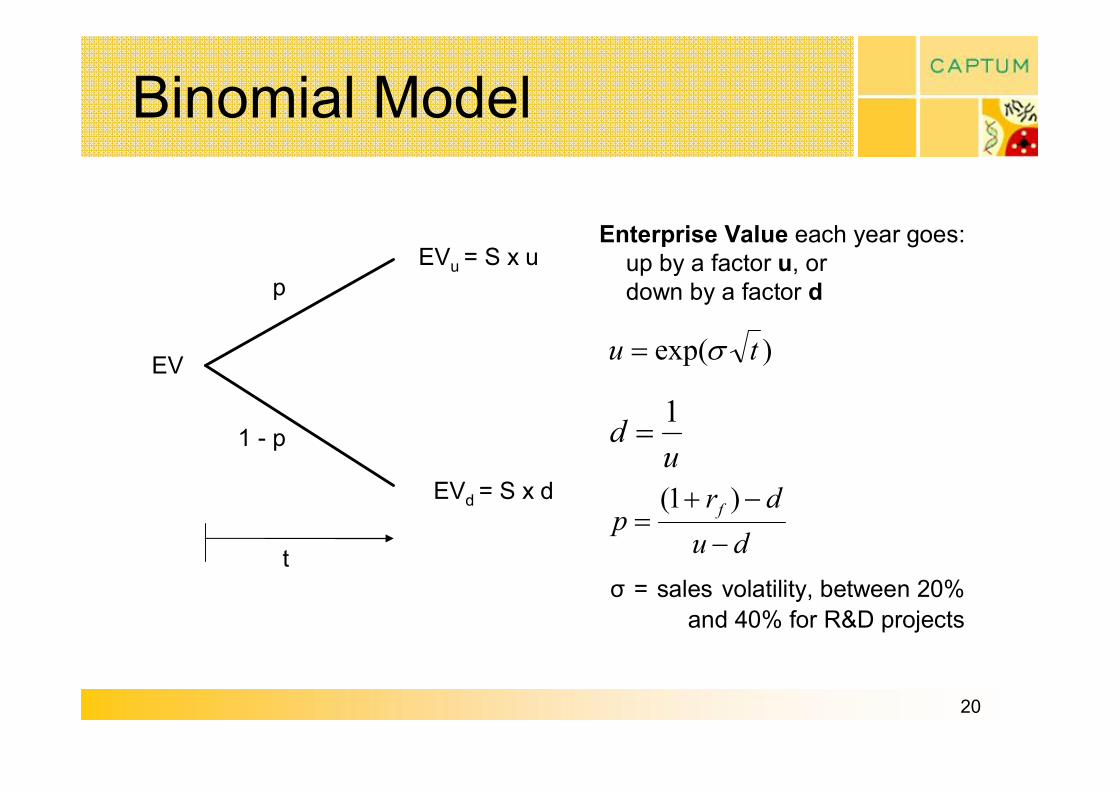

Binomial Model

) exp( t u σ =

u d 1

=

EV

EV u = S x u

EV d = S x d

t

p

1 p

Enterprise Value each year goes: up by a factor u, or down by a factor d

d u d r

p f

−

− + =

) 1 (

σ = sales volatility, between 20% and 40% for R&D projects

21

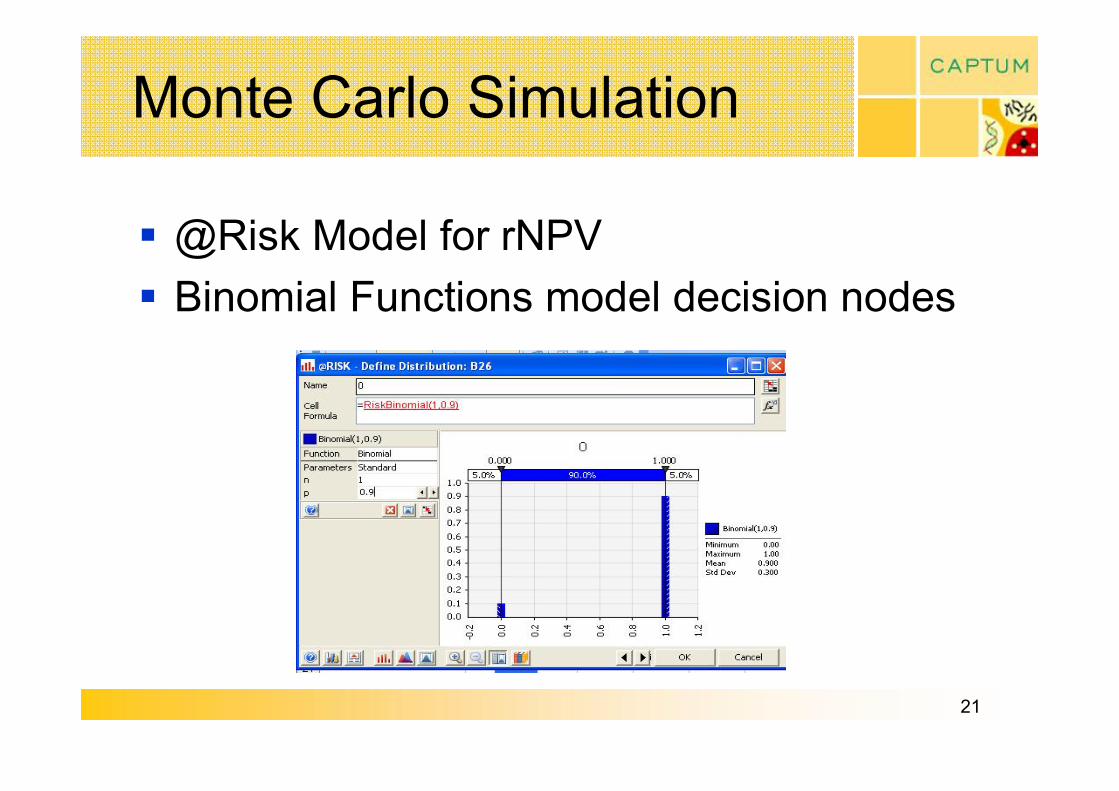

Monte Carlo Simulation

§ @Risk Model for rNPV § Binomial Functions model decision nodes

22

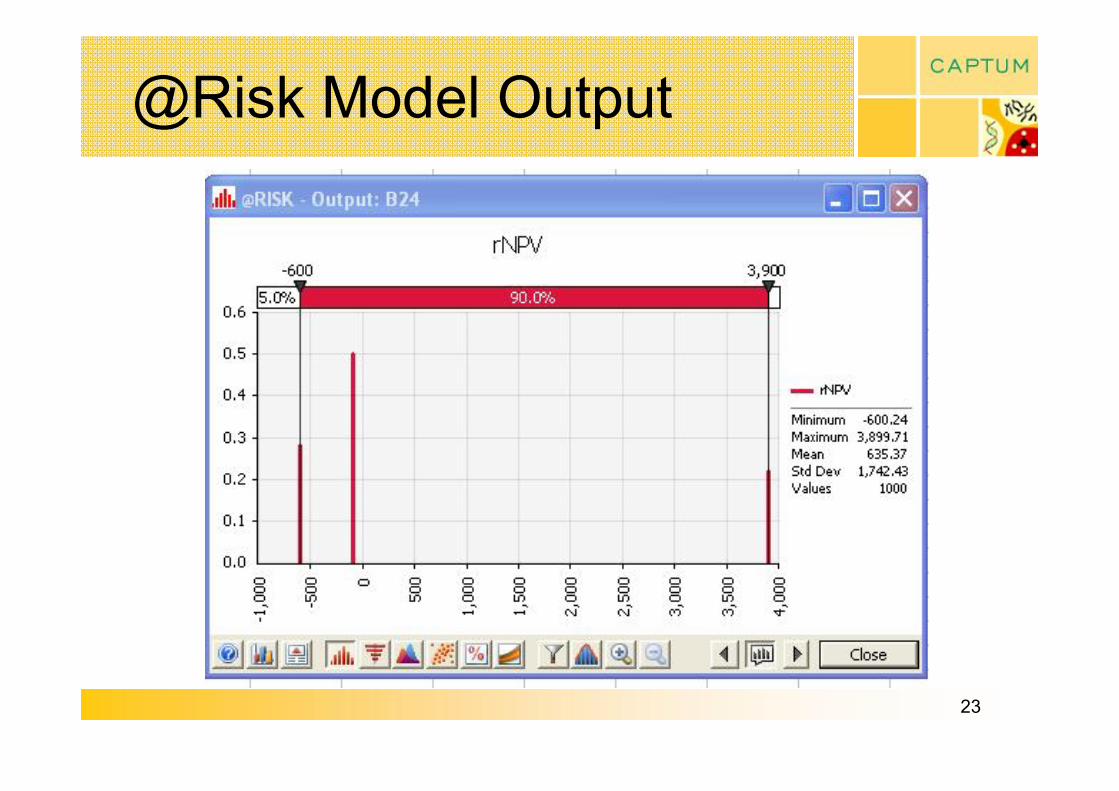

@Risk Model

23

@Risk Model Output

24

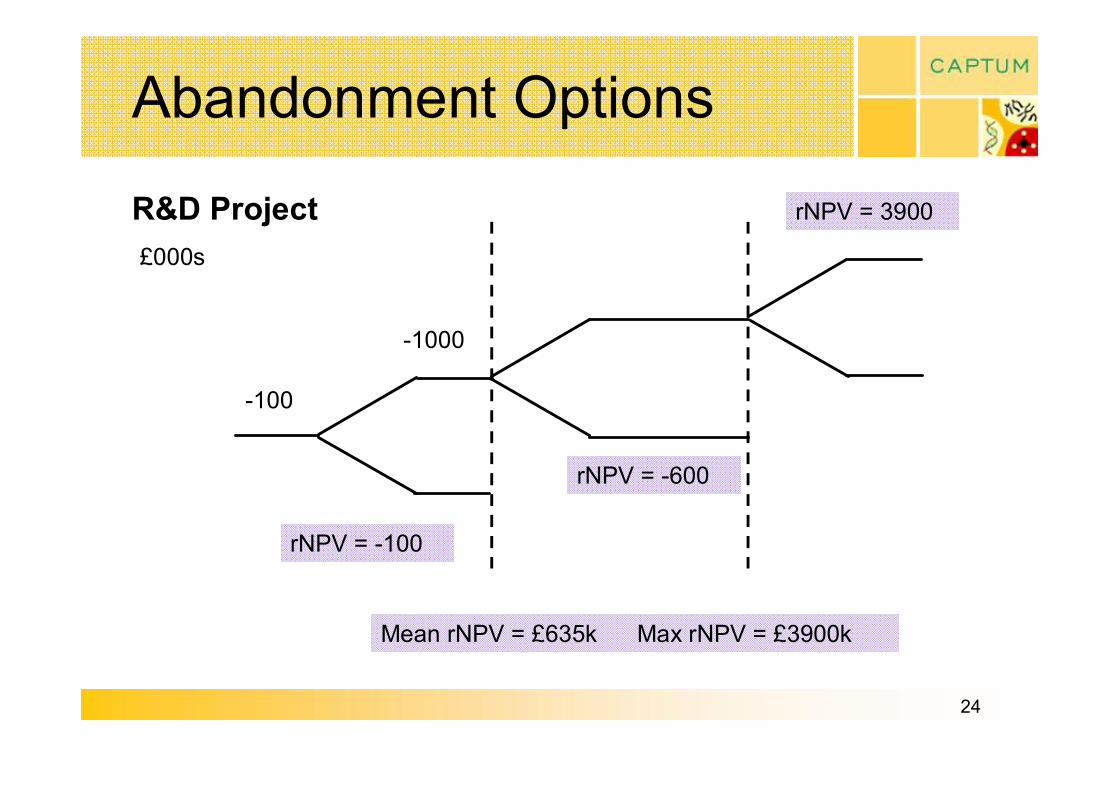

Abandonment Options

R&D Project

100

rNPV = 100

1000

rNPV = 600

rNPV = 3900

Mean rNPV = £635k Max rNPV = £3900k

£000s

25

Strategic Decision Options

§ Defer Investment § Default § Expand § Contract § Shut Down and Restart § Abandon

Lenos Trigeorgis, Real Options (1996)

26

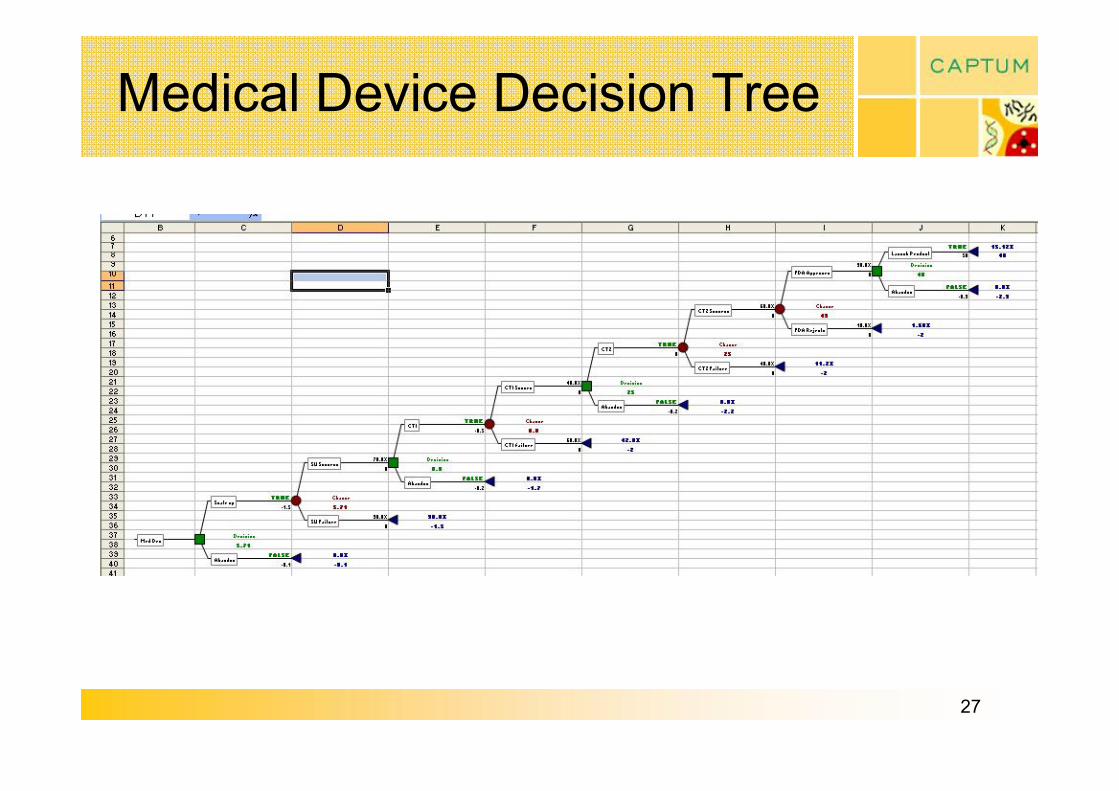

Multiple Milestones

FDA CT2 CT1 Scale up

0.7

0.4

0.6

0.9

1.5

0.1

0.5

0.2

0

0.2

4.5

0.3

Cash Flow £m

Medical Device Development Project

27

Medical Device Decision Tree

28

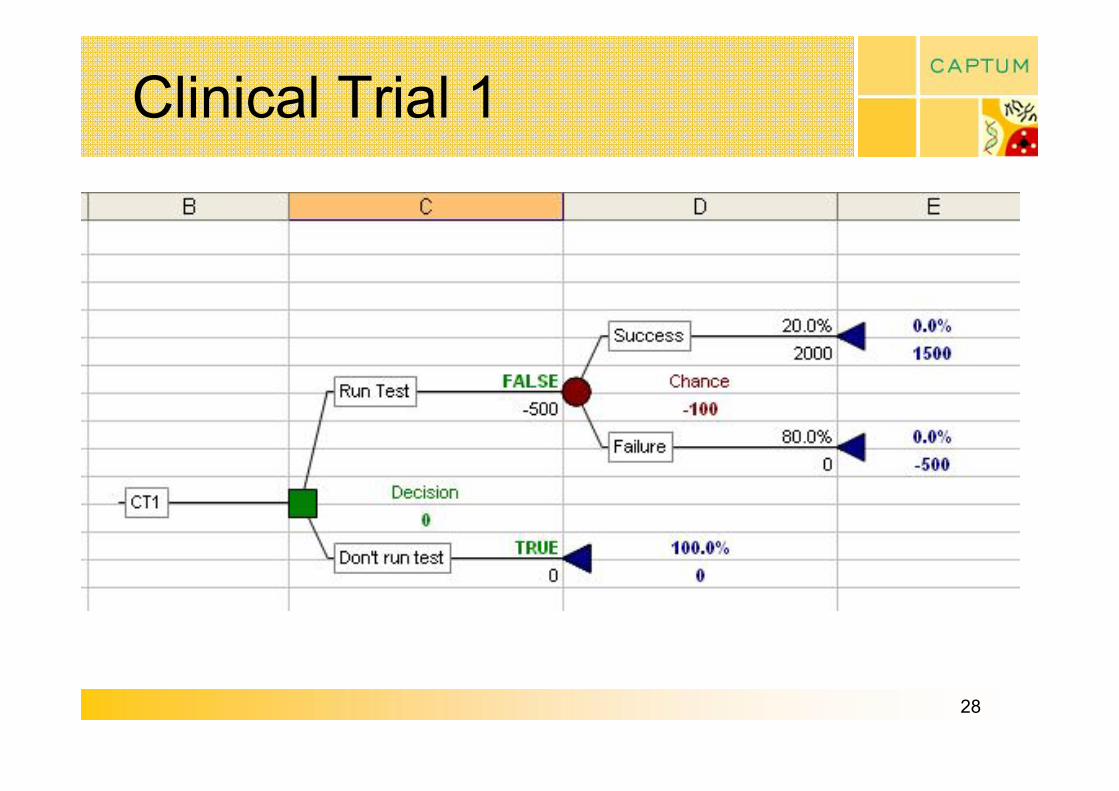

Clinical Trial 1

29

Exercise Options

1. Invest in further R&D

2. Rerun test

30

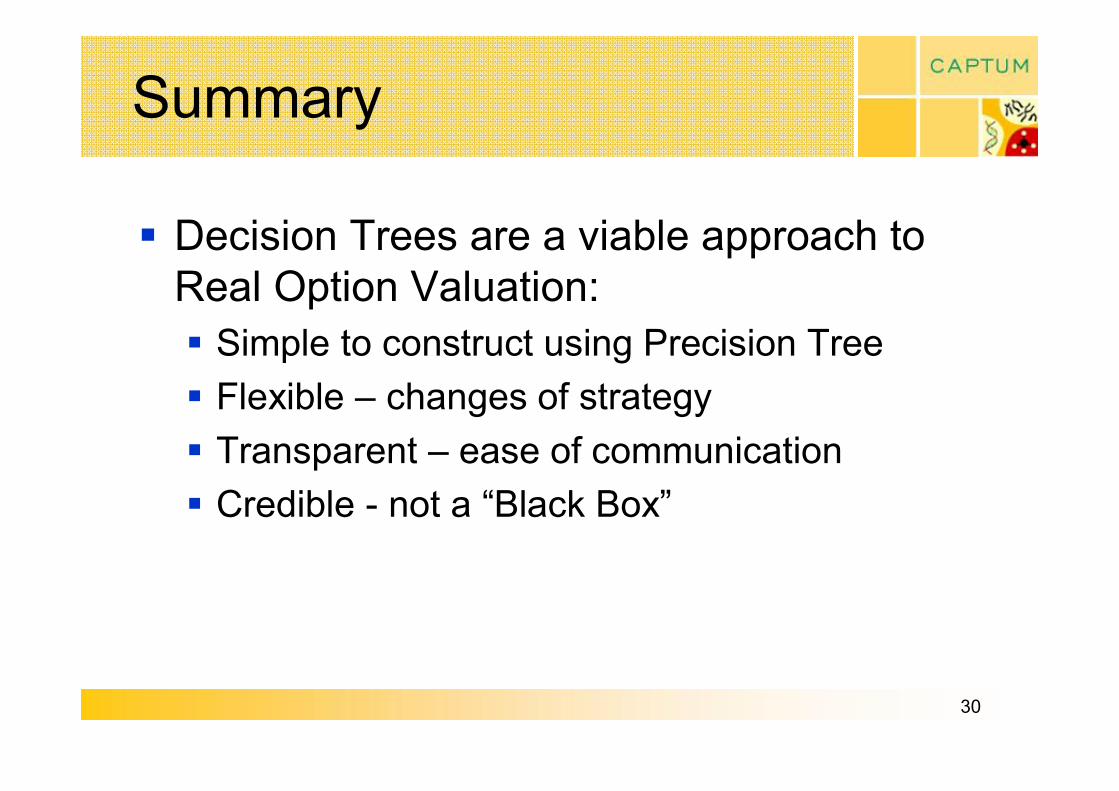

Summary

§ Decision Trees are a viable approach to Real Option Valuation: § Simple to construct using Precision Tree § Flexible – changes of strategy § Transparent – ease of communication § Credible not a “Black Box”

31

About Captum…

§ Formed in 2004 § Transatlantic presence § Life science sector consulting: § Business development, valuation, partnering

§ MasterClasses: § Valuation Masterclass attended by over 500 executives in UK and Europe

§ Internet virtual communities § Sensor100

32

Coming Events

§ MasterClass: Company Valuation London, 25 th May 2011

§ Workshop: Evaluating Technology LES International Conference London, 8 th June 2011

33

Captum Growth Series

Valuing Technology

2 nd edition

To be published May 2011

34

Contact

Michael Brand e: [email protected] t: +44 (0) 115 988 6154 m: +44 (0) 7980 257 241

Captum Capital Limited Cumberland House 35 Park Row Nottingham NG1 6EE United Kingdom

www.captum.com