Embed Size (px)

Citation preview

IATA Economics www.iata.org/economics 1

CARGO E-CHARTBOOK Q2 2013 OVERVIEW Operating conditions for airline cargo businesses deteriorated over recent months, but the outlook looks a bit

more positive. Over recent months airlines saw air freight volumes stall, load factors weaken and yields

continue the steady decline seen over the past two years. These developments have largely resulted from the

pause in business confidence improvement and continued slowing in world trade growth. Having said that

though, current levels of business confidence continue to indicate a modest pick-up in economic growth this

year, and consumer confidence in Europe and the US has made some progress, both of which should

provide support to air freight demand in the months ahead. Finally, although current conditions are tough,

cargo heads surveyed in April are optimistic, saying they expect both volumes and yields to improve this year.

Economic Situation – global economic growth in 2013 is expected to improve slightly on 2012, but

significant regional variation is resulting in a three-speed economic recovery. Looser monetary policy is

helping emerging economies expand at a much faster pace than advanced economies, and looser bank

lending standards in the US have supported faster growth there than in Europe (page 2)

Traffic Growth – the growth trend in air freight volumes has flattened over recent months in line with the stall

in business confidence, after showing signs of a pick-up at the end of 2012 (page 2)

Demand Environment – has weakened over recent months. World trade growth continues to slow,

hampered by weakness in advanced economies, and the earlier rise in business confidence has now stalled.

On the positive side, however, there is also no sign of an inventory overhang (page 3)

Demand Drivers – have shown some improvement compared to Q1, but remain weak overall. European and

US consumer confidence has improved further over recent months, but this has not been enough to sustain

the pick-up in air freight volumes in late 2012, as indicated by the recent slip in semi-conductor shipments

(page 3)

Capacity – load factors weakened over recent months as the growth trend in air freight markets lost

momentum. Fleet expansion has added to downward pressure on aircraft utilization rates, and that is likely to

continue as delivery of new aircraft with belly hold capacity is set to expand the existing widebody fleet by 6%

this year. Air freight rates remain weak (page 4)

Competition – sea freight rates have plunged over recent months reflecting weakening demand. Container

shipping volumes have declined in several regions, and have even contracted in Latin America and North

Europe (page 4)

Revenue and Yields – air freight yields started to show some improvement toward the end of 2012,

supported by stronger demand and load factors, but have since returned to the mostly flat trend seen over

the past 2 years (page 5)

Costs – jet fuel prices have eased over the past several months, with prices in May about 15% lower than

the most recent peak in February. This has reduced some of the downward pressure on cargo profitability,

as has the decline in nominal wage rates (page 5)

Profitability outlook – remains optimistic, with an increase in volumes expected over the next 12 months

according to heads of cargo surveyed in April. Air freight yields are also expected to improve (page 5)

IATA Economics: www.iata.org/economics 2

Cargo eChartbook – Q2 2013

Economic Outlook & Traffic Growth

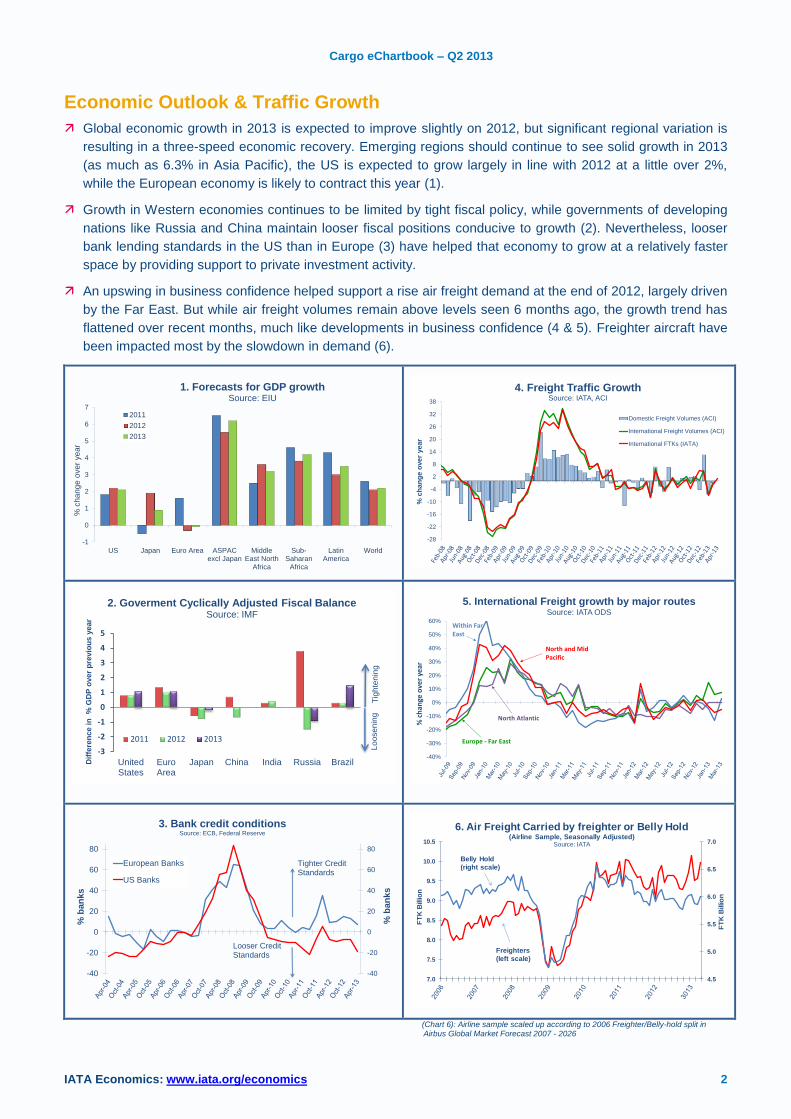

Global economic growth in 2013 is expected to improve slightly on 2012, but significant regional variation is

resulting in a three-speed economic recovery. Emerging regions should continue to see solid growth in 2013

(as much as 6.3% in Asia Pacific), the US is expected to grow largely in line with 2012 at a little over 2%,

while the European economy is likely to contract this year (1).

Growth in Western economies continues to be limited by tight fiscal policy, while governments of developing

nations like Russia and China maintain looser fiscal positions conducive to growth (2). Nevertheless, looser

bank lending standards in the US than in Europe (3) have helped that economy to grow at a relatively faster

space by providing support to private investment activity.

An upswing in business confidence helped support a rise air freight demand at the end of 2012, largely driven

by the Far East. But while air freight volumes remain above levels seen 6 months ago, the growth trend has

flattened over recent months, much like developments in business confidence (4 & 5). Freighter aircraft have

been impacted most by the slowdown in demand (6).

-1

0

1

2

3

4

5

6

7

US Japan Euro Area ASPACexcl Japan

MiddleEast North

Africa

Sub-Saharan

Africa

LatinAmerica

World

% c

hange o

ver

year

1. Forecasts for GDP growth Source: EIU

2011

2012

2013

-28

-22

-16

-10

-4

2

8

14

20

26

32

38

% c

ha

ng

e o

ve

r ye

ar

4. Freight Traffic GrowthSource: IATA, ACI

Domestic Freight Volumes (ACI)

International Freight Volumes (ACI)

International FTKs (IATA)

-3

-2

-1

0

1

2

3

4

5

UnitedStates

EuroArea

Japan China India Russia BrazilDif

fere

nce i

n %

GD

P o

ver

pre

vio

us y

ear

2011 2012 2013

2. Goverment Cyclically Adjusted Fiscal BalanceSource: IMF

Tig

hte

nin

gL

oo

se

nin

g

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

% c

han

ge o

ver

year

5. International Freight growth by major routesSource: IATA ODS

Within Far East

Europe - Far East

North Atlantic

North and Mid Pacific

-40

-20

0

20

40

60

80

-40

-20

0

20

40

60

80

% b

an

ks

% b

an

ks

3. Bank credit conditionsSource: ECB, Federal Reserve

European Banks

US Banks

Tighter Credit Standards

Looser Credit Standards

4.5

5.0

5.5

6.0

6.5

7.0

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

FT

K B

illio

n

FT

K B

illio

n

6. Air Freight Carried by freighter or Belly Hold(Airline Sample, Seasonally Adjusted)

Source: IATA

Freighters

(left scale)

Belly Hold

(right scale)

(Chart 6): Airline sample scaled up according to 2006 Freighter/Belly-hold split in Airbus Global Market Forecast 2007 - 2026

IATA Economics: www.iata.org/economics 3

Cargo eChartbook – Q2 2013

Demand Environment & Drivers

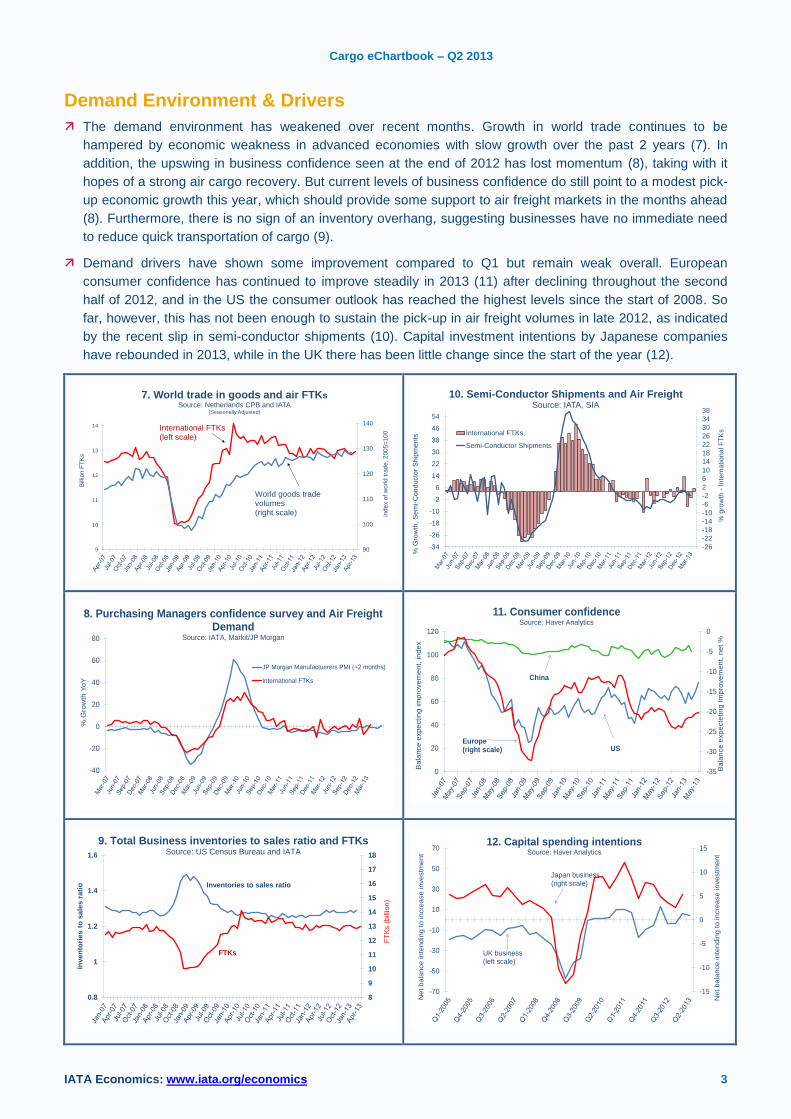

The demand environment has weakened over recent months. Growth in world trade continues to be

hampered by economic weakness in advanced economies with slow growth over the past 2 years (7). In

addition, the upswing in business confidence seen at the end of 2012 has lost momentum (8), taking with it

hopes of a strong air cargo recovery. But current levels of business confidence do still point to a modest pick-

up economic growth this year, which should provide some support to air freight markets in the months ahead

(8). Furthermore, there is no sign of an inventory overhang, suggesting businesses have no immediate need

to reduce quick transportation of cargo (9).

Demand drivers have shown some improvement compared to Q1 but remain weak overall. European

consumer confidence has continued to improve steadily in 2013 (11) after declining throughout the second

half of 2012, and in the US the consumer outlook has reached the highest levels since the start of 2008. So

far, however, this has not been enough to sustain the pick-up in air freight volumes in late 2012, as indicated

by the recent slip in semi-conductor shipments (10). Capital investment intentions by Japanese companies

have rebounded in 2013, while in the UK there has been little change since the start of the year (12).

90

100

110

120

130

140

9

10

11

12

13

14

index o

f w

orld t

rade, 2005=

100

Bill

ion F

TK

s

7. World trade in goods and air FTKsSource: Netherlands CPB and IATA

(Seasonally Adjusted)

International FTKs(left scale)

World goods trade volumes(right scale)

-26

-22

-18

-14

-10

-6

-2

2

6

10

14

18

22

26

30

34

38

-34

-26

-18

-10

-2

6

14

22

30

38

46

54

% g

row

th -

Inte

rna

tio

na

l F

TK

s

% G

row

th,

Se

mi-

Co

nd

ucto

r S

hip

me

nts

10. Semi-Conductor Shipments and Air FreightSource: IATA, SIA

International FTKs

Semi-Conductor Shipments

-40

-20

0

20

40

60

80

% G

row

th Y

oY

JP Morgan Manufactuerers PMI (+2 months)

International FTKs

8. Purchasing Managers confidence survey and Air Freight Demand

Source: IATA, Markit/JP Morgan

-35

-30

-25

-20

-15

-10

-5

0

0

20

40

60

80

100

120

Bala

nce e

xpecte

ting im

pro

vem

ent,

net %

Bala

nce e

xpecting im

pro

vem

ent,

index

11. Consumer confidenceSource: Haver Analytics

China

Europe(right scale) US

8

9

10

11

12

13

14

15

16

17

18

0.8

1

1.2

1.4

1.6

FT

Ks (

bill

ion

)

Inve

nto

rie

s t

o s

ale

s r

ati

o Inventories to sales ratio

FTKs

9. Total Business inventories to sales ratio and FTKsSource: US Census Bureau and IATA

-15

-10

-5

0

5

10

15

-70

-50

-30

-10

10

30

50

70

Net

bala

nce inte

ndin

g to incre

ase investm

ent

Net

bala

nce inte

ndin

g to incre

ase investm

ent

12. Capital spending intentionsSource: Haver Analytics

UK business(left scale)

Japan business(right scale)

IATA Economics: www.iata.org/economics 4

Cargo eChartbook – Q2 2013

Capacity & Competition

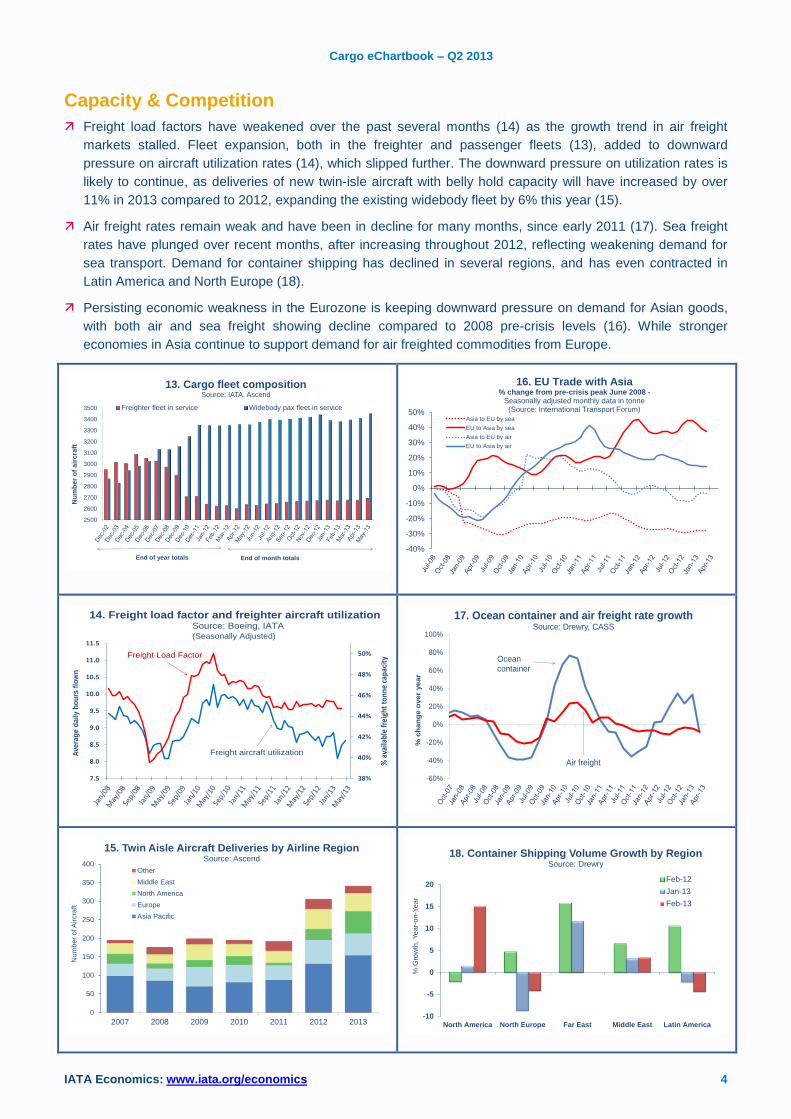

Freight load factors have weakened over the past several months (14) as the growth trend in air freight

markets stalled. Fleet expansion, both in the freighter and passenger fleets (13), added to downward

pressure on aircraft utilization rates (14), which slipped further. The downward pressure on utilization rates is

likely to continue, as deliveries of new twin-isle aircraft with belly hold capacity will have increased by over

11% in 2013 compared to 2012, expanding the existing widebody fleet by 6% this year (15).

Air freight rates remain weak and have been in decline for many months, since early 2011 (17). Sea freight

rates have plunged over recent months, after increasing throughout 2012, reflecting weakening demand for

sea transport. Demand for container shipping has declined in several regions, and has even contracted in

Latin America and North Europe (18).

Persisting economic weakness in the Eurozone is keeping downward pressure on demand for Asian goods,

with both air and sea freight showing decline compared to 2008 pre-crisis levels (16). While stronger

economies in Asia continue to support demand for air freighted commodities from Europe.

2500

2600

2700

2800

2900

3000

3100

3200

3300

3400

3500

Nu

mb

er

of

air

cra

ft

13. Cargo fleet compositionSource: IATA, Ascend

Freighter fleet in service Widebody pax fleet in service

End of month totalsEnd of year totals

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%Asia to EU by sea

EU to Asia by sea

Asia to EU by air

EU to Asia by air

16. EU Trade with Asia% change from pre-crisis peak June 2008 -

Seasonally adjusted monthly data in tonne(Source: International Transport Forum)

38%

40%

42%

44%

46%

48%

50%

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

% a

vaila

ble

frei

ght

tonn

e ca

paci

ty

Avera

ge d

aily h

ou

rs f

low

n

Freight Load Factor

Freight aircraft utilization

14. Freight load factor and freighter aircraft utilizationSource: Boeing, IATA (Seasonally Adjusted)

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

% c

ha

ng

e o

ver

yea

r

17. Ocean container and air freight rate growthSource: Drewry, CASS

Ocean container

Air freight

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013

Num

ber

of A

ircra

ft

15. Twin Aisle Aircraft Deliveries by Airline RegionSource: Ascend

Other

Middle East

North America

Europe

Asia Pacific

-10

-5

0

5

10

15

20

North America North Europe Far East Middle East Latin America

% G

row

th, Y

ear-

on-Y

ear

18. Container Shipping Volume Growth by RegionSource: Drewry

Feb-12

Jan-13

Feb-13

IATA Economics: www.iata.org/economics 5

Cargo eChartbook – Q2 2013

Revenues, Costs & Profits

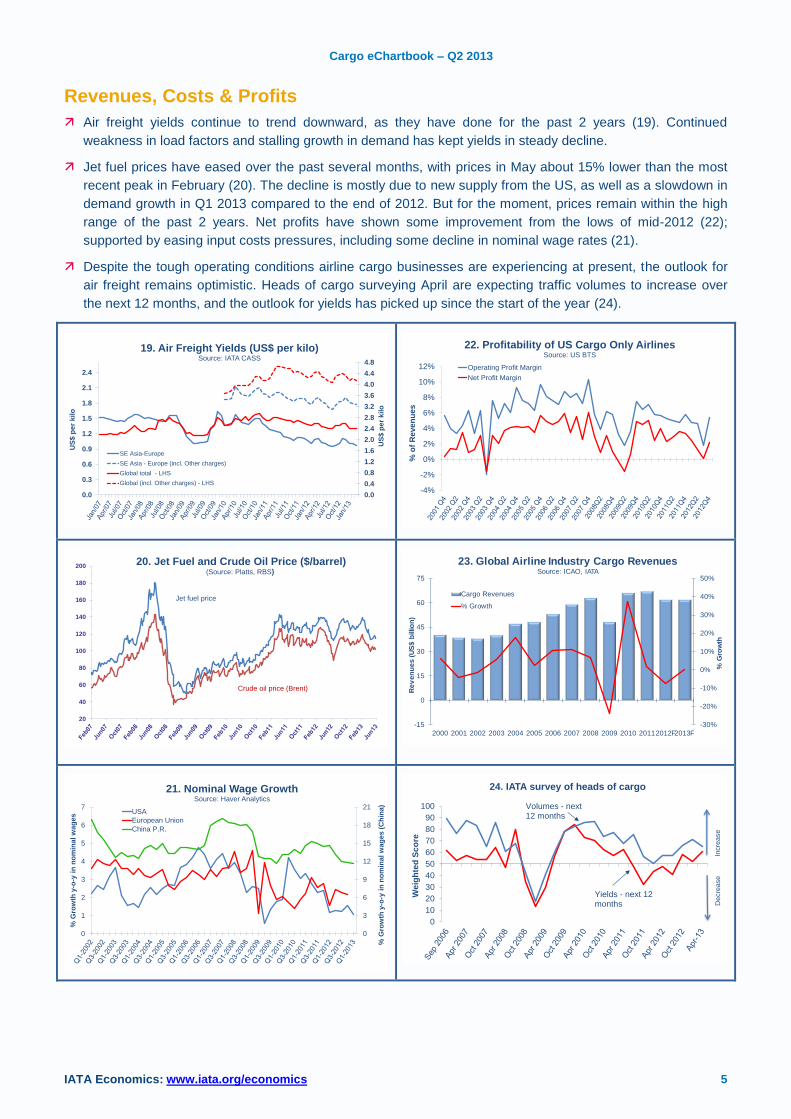

Air freight yields continue to trend downward, as they have done for the past 2 years (19). Continued

weakness in load factors and stalling growth in demand has kept yields in steady decline.

Jet fuel prices have eased over the past several months, with prices in May about 15% lower than the most

recent peak in February (20). The decline is mostly due to new supply from the US, as well as a slowdown in

demand growth in Q1 2013 compared to the end of 2012. But for the moment, prices remain within the high

range of the past 2 years. Net profits have shown some improvement from the lows of mid-2012 (22);

supported by easing input costs pressures, including some decline in nominal wage rates (21).

Despite the tough operating conditions airline cargo businesses are experiencing at present, the outlook for

air freight remains optimistic. Heads of cargo surveying April are expecting traffic volumes to increase over

the next 12 months, and the outlook for yields has picked up since the start of the year (24).

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

3.6

4.0

4.4

4.8

US

$ p

er

kil

o

US

$ p

er

kil

o

19. Air Freight Yields (US$ per kilo)Source: IATA CASS

SE Asia-Europe

SE Asia - Europe (incl. Other charges)

Global total - LHS

Global (incl. Other charges) - LHS

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

% o

f R

eve

nu

es

22. Profitability of US Cargo Only AirlinesSource: US BTS

Operating Profit Margin

Net Profit Margin

20

40

60

80

100

120

140

160

180

20020. Jet Fuel and Crude Oil Price ($/barrel)

(Source: Platts, RBS)

Jet fuel price

Crude oil price (Brent)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-15

0

15

30

45

60

75

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20112012F2013F

% G

row

th

Re

ve

nu

es

(U

S$

billio

n)

23. Global Airline Industry Cargo RevenuesSource: ICAO, IATA

Cargo Revenues

% Growth

0

3

6

9

12

15

18

21

0

1

2

3

4

5

6

7

% G

row

th y

-o-y

in

no

min

al

wag

es (

Ch

ina)

% G

row

th y

-o-y

in

no

min

al

wag

es

21. Nominal Wage GrowthSource: Haver Analytics

USA

European Union

China P.R.

0

10

20

30

40

50

60

70

80

90

100

We

igh

ted

Sc

ore

24. IATA survey of heads of cargo

Volumes - next 12 months

Yields - next 12 months

Incre

ase

Decre

ase

IATA Economics: www.iata.org/economics 6

Cargo eChartbook – Q2 2013

Air Freight Routes and Direction

Table 1. International Freight Volume Growth by Route Area (Source: IATA ODS statistics)

% Growth in Freight Tonnes, year-on-year

Route Area Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13

Africa - Middle East 5.7% 17.4% 20.0% 3% 0% 6%

Europe - Africa -2.8% 10.2% 4.5% -2% 3% -6%

Europe - Far East -2.0% 5.3% 1.3% -3% -5% -3%

Europe - Middle East 6.5% 1.9% 6.3% 15% 6% 7%

Far East - Southwest Pacific -5.3% 0.4% 1.9% -6% -10% -2%

Mid Atlantic -5.8% -2.5% -7.3% 3% 13% -11%

Middle East - Far East 9.6% 13.9% 9.5% 5% -6% 5%

North America - Central America

-19.6% -11.5% -18.1% -27% 1% -32%

North America - South America

3.0% 9.2% 18.2% 4% -5% 6%

North and Mid Pacific -5.7% 1.6% 2.4% -3% -7% -5%

North Atlantic -8.4% -0.7% -4.7% 2% 8% 0%

South Atlantic -9.3% -7.5% -6.9% 3% 5% -1%

South Pacific -17.4% -16.7% -9.0% 18% 27% -7%

Within Africa -4.6% 14.5% -2.3% 0% -2% -6%

Within Europe -6.2% -1.1% -5.7% 6% 8% -2%

Within Far East -0.4% 1.0% -0.7% -4% -13% 3%

Within North America -27.0% -9.5% -11.9% 0% -4% 4%

Within South America 6.2% 8.7% 14.2% 8% -9% -2%

Table 2. Outbound CASS Market Revenues (excl. fuel surcharges)

US$m Q4 2012

% Growth in Air Freight Revenues, year-on-year

Origin Region 2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1

Africa 50.2 -10.9 -15.5 -23.3 -7.9 1.9 -2.6

Caribbean 6.8 2.4 33.6 16.5 43.4 34.0 4.1

Central America 58.2 -11.1 -12.9 -3.4 -0.9 -4.7 -1.4

Europe 1465.5 0.8 -5.4 -13.1 -5.9 -0.5 2.6

Japan & Korea 503.6 -22.1 -18.3 -25.4 -22.8 -26.0 -29.7

Middle East 83.3 -6.1 5.7 1.9 10.7 17.9 20.0

North America 723.0 -0.9 -4.1 -7.9 -8.3 -7.5 -6.4

South America 273.8 4.8 0.2 -8.3 1.7 -5.5 -1.7

South East Asia 960.5 -25.1 -9.4 -11.1 -7.3 2.1 -11.1

Table 3. Inbound CASS Market Revenues (excl. fuel surcharges)

US$m Q4 2012

% Growth in Air Freight Revenues, year-on-year

Destination Region 2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1

Africa 323.7 5.3 0.6 -6.3 -5.6 -5.3 -3.7

Caribbean 29.4 -5.1 -7.0 -10.4 -10.4 -8.1 -2.5

Central America 103.6 3.2 1.6 -13.6 -8.4 -6.7 -13.1

Europe 898.2 -25.6 -18.6 -22.4 -18.1 -12.6 -15.1

Japan & Korea 289.2 -7.7 -6.8 -11.0 -8.2 -6.2 -9.0

Middle East 334.3 2.5 5.6 -2.4 -1.9 2.3 1.0

North America 790.3 -18.9 -8.8 -18.8 -6.6 0.5 -9.9

South America 414.3 5.1 -1.3 -7.4 -5.2 -6.5 -0.6

South East Asia 706.0 -1.2 -6.7 -7.3 -3.1 -1.3 0.5

IATA Economics: www.iata.org/economics 7

Cargo eChartbook – Q2 2013

Glossary

ACI: Airports Council International

AFTK: Available Freight Tonne Kilometers

European CB: European Central Bank

EIU: Economist Intelligence Unit

CASS: Cargo Accounts Settlement System

FT: Financial Times

FTK: Freight Tonne Kilometers

PMI: Purchasing Managers Index

Netherlands CPB: Netherlands Bureau for Economic Policy Analysis

ODS: Origin-Destination Statistics

SIA: Semiconductors Industry Association

US BTS: US Bureau of Transportation Statistics

M-o-m Month over month percentage change

Y-o-y Year over year percentage change

IATA Economics

10th

June 2013