Embed Size (px)

Citation preview

Carving a path for ReformA Review of the Green Paper

www.pwc.com/jm

Brian J. Denning, Partner

Tax Reform for JamaicaA Review of the Green Paper

PwC

Phased Implementation

Proposed Implementation of Tax Reform

Green Paper proposes implementation in three phases:

1. Reform of International Trade & Indirect Taxes (SCT and GCT)

2. Corporate & Personal Income Taxes

3. Payroll Taxes

In the short-term, implementation of:

• specific tax policy reform measures (across each category)

• tax administrative reform measures

32 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Reform of International Trade &Indirect Taxes (SCT & GCT)

42 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Customs Duty

Reform of International Trade Taxes

Current Regime

Imposes customs duty at various rates (0% - 100%) on the customs valueof goods imported into Jamaica

Minimum rates on various categories of goods set by the CommonExternal Tariff (CET) – requires CARICOM approval to alter/suspend

Relief from duty given to various sectors (tourism, manufacturing,agriculture etc.)

Extensive ministerial waivers of duties

Perception that system is complex, inefficient and facilitates corruption

In 2009/10 - import duties collected (J$18 billion) were 3.7% of thevalue of the goods imported (J$486 billion)

Tariff codes imposing duty of 20% or less generate highest yields

52 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Customs Duty

Reform of International Trade Taxes

Matalon Report

Indicated preference for unification of statutory rate with collected rate

Somewhere between 5% - 10%

Recognised CARICOM CET obligations represent a hurdle to reform

Green Paper

Proposes a maximum tariff rate (permitted by CET) of either:

• 20% - if Customs Administration Fee (CAF) is 5%

• 25% - if CAF is set at 3%

Care needs to be taken to evaluate each affected tariff heading todetermine whether there remains a legitimate basis for retaining a highercustoms duty rate (e.g. local market protection)

62 September 2011Carving the Path for Jamaica's Tax Reform

PwC

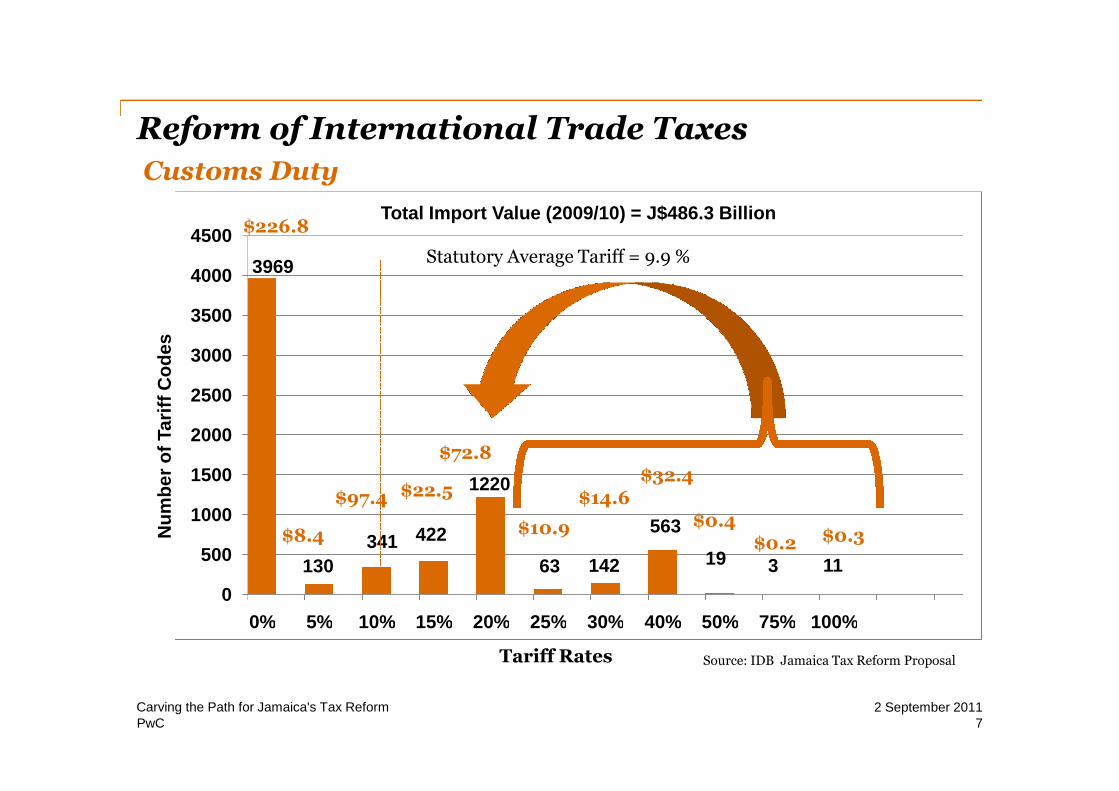

Reform of International Trade Taxes

Customs Duty

3969

130

341 422

1220

63 142

563

19 3 11

0

500

1000

1500

2000

2500

3000

3500

4000

4500

0% 5% 10% 15% 20% 25% 30% 40% 50% 75% 100%

Total Import Value (2009/10) = J$486.3 Billion

$8.4

$97.4 $22.5

$10.9

$14.6$32.4

$0.4$0.2 $0.3

Statutory Average Tariff = 9.9 %

$226.8

Tariff Rates

$72.8

Nu

mb

er

of

Tari

ffC

od

es

Source: IDB Jamaica Tax Reform Proposal

72 September 2011Carving the Path for Jamaica's Tax Reform

PwC

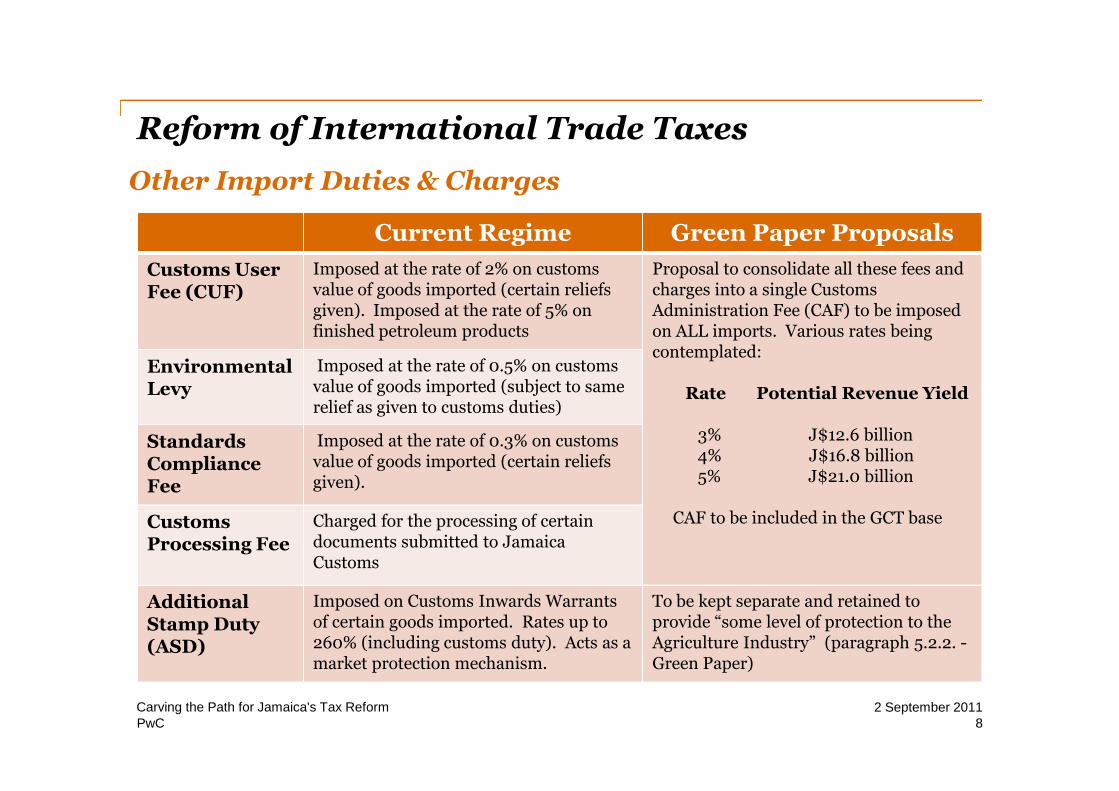

Other Import Duties & Charges

Reform of International Trade Taxes

Current Regime Green Paper Proposals

Customs UserFee (CUF)

Imposed at the rate of 2% on customsvalue of goods imported (certain reliefsgiven). Imposed at the rate of 5% onfinished petroleum products

Proposal to consolidate all these fees andcharges into a single CustomsAdministration Fee (CAF) to be imposedon ALL imports. Various rates beingcontemplated:

Rate Potential Revenue Yield

3% J$12.6 billion4% J$16.8 billion5% J$21.0 billion

CAF to be included in the GCT base

EnvironmentalLevy

Imposed at the rate of 0.5% on customsvalue of goods imported (subject to samerelief as given to customs duties)

StandardsComplianceFee

Imposed at the rate of 0.3% on customsvalue of goods imported (certain reliefsgiven).

CustomsProcessing Fee

Charged for the processing of certaindocuments submitted to JamaicaCustoms

AdditionalStamp Duty(ASD)

Imposed on Customs Inwards Warrantsof certain goods imported. Rates up to260% (including customs duty). Acts as amarket protection mechanism.

To be kept separate and retained toprovide “some level of protection to theAgriculture Industry” (paragraph 5.2.2. -Green Paper)

82 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Other Import Duties & Charges

Reform of International Trade Taxes

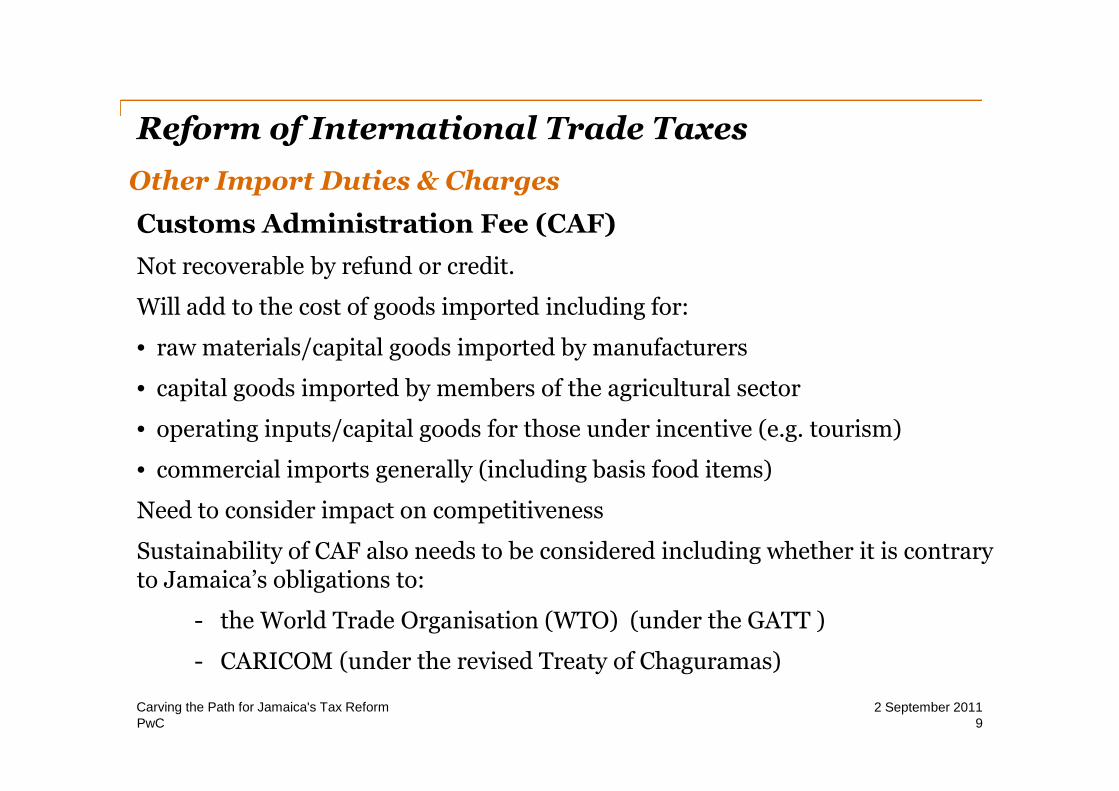

Customs Administration Fee (CAF)

Not recoverable by refund or credit.

Will add to the cost of goods imported including for:

• raw materials/capital goods imported by manufacturers

• capital goods imported by members of the agricultural sector

• operating inputs/capital goods for those under incentive (e.g. tourism)

• commercial imports generally (including basis food items)

Need to consider impact on competitiveness

Sustainability of CAF also needs to be considered including whether it is contraryto Jamaica’s obligations to:

- the World Trade Organisation (WTO) (under the GATT )

- CARICOM (under the revised Treaty of Chaguramas)

92 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Other Import Duties & Charges

Reform of International Trade Taxes

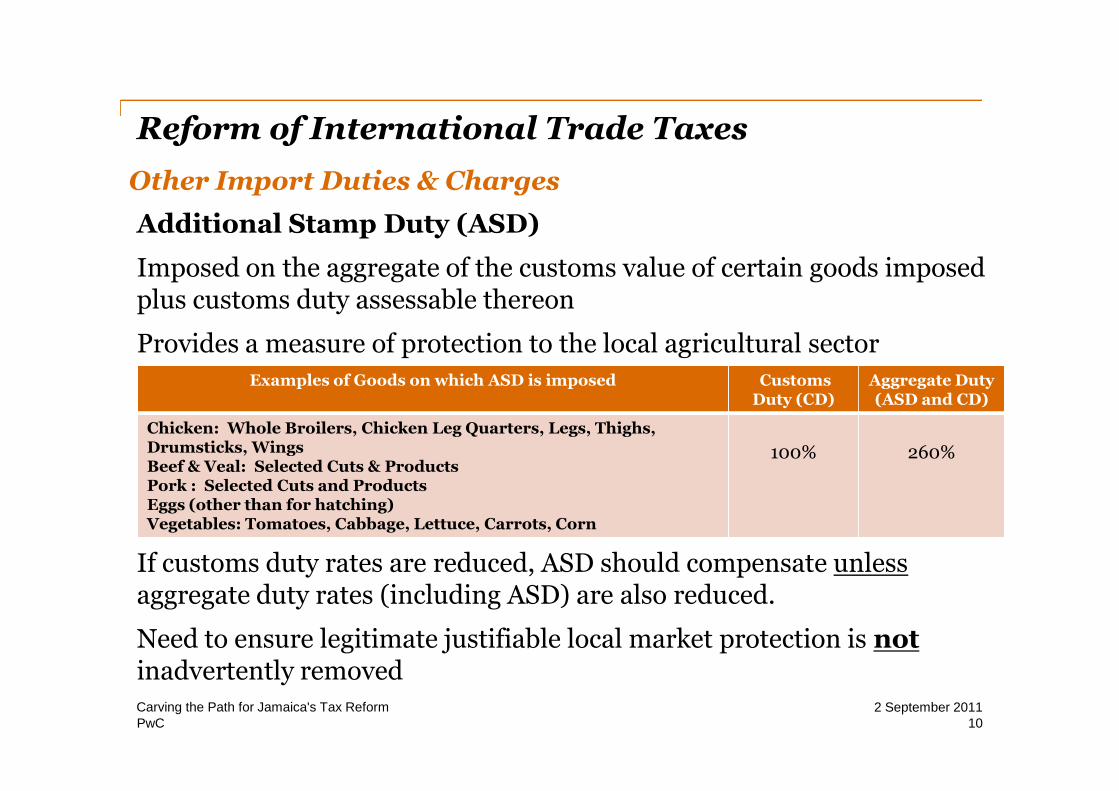

Additional Stamp Duty (ASD)

Imposed on the aggregate of the customs value of certain goods imposedplus customs duty assessable thereon

Provides a measure of protection to the local agricultural sector

If customs duty rates are reduced, ASD should compensate unlessaggregate duty rates (including ASD) are also reduced.

Need to ensure legitimate justifiable local market protection is notinadvertently removed

Examples of Goods on which ASD is imposed CustomsDuty (CD)

Aggregate Duty(ASD and CD)

Chicken: Whole Broilers, Chicken Leg Quarters, Legs, Thighs,Drumsticks, WingsBeef & Veal: Selected Cuts & ProductsPork : Selected Cuts and ProductsEggs (other than for hatching)Vegetables: Tomatoes, Cabbage, Lettuce, Carrots, Corn

100% 260%

102 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Other Import Duties & Charges

Reform of International Trade Taxes

Current Regime Green Paper Proposals

AdvanceGeneral

ConsumptionTax

(GCT)

Imposed at the rate of 5% on GCTtaxable goods imported by commercialimporters excluding:• petroleum products;• capital goods;• goods imported under the GCT

deferment scheme e.g. raw materialsfor the purpose of manufacturing;

• goods that are zero rated or exemptfrom GCT;

• telephone instruments; and• goods imported on which an uplift fee

is chargeable under the GCT Act.

In effect GCT is collected at the port atthe rate of 22.5% [17.5% + 5%]. May beclaimed as a GCT input tax credit whereappropriate

Proposal to impose on ALL commercialimports (excluding bauxite and petroleum)

To be creditable against any tax type(excluding the CAF). Consideration beinggiven that it would be creditable but notrefundable.

Various rates being contemplated.

Rate Potential Net* Revenue Yield

3% J$2.6 billion4% J$3.5 billion5% J$4.3 billion

* assuming 80% recovered by way of credit

112 September 2011Carving the Path for Jamaica's Tax Reform

PwC

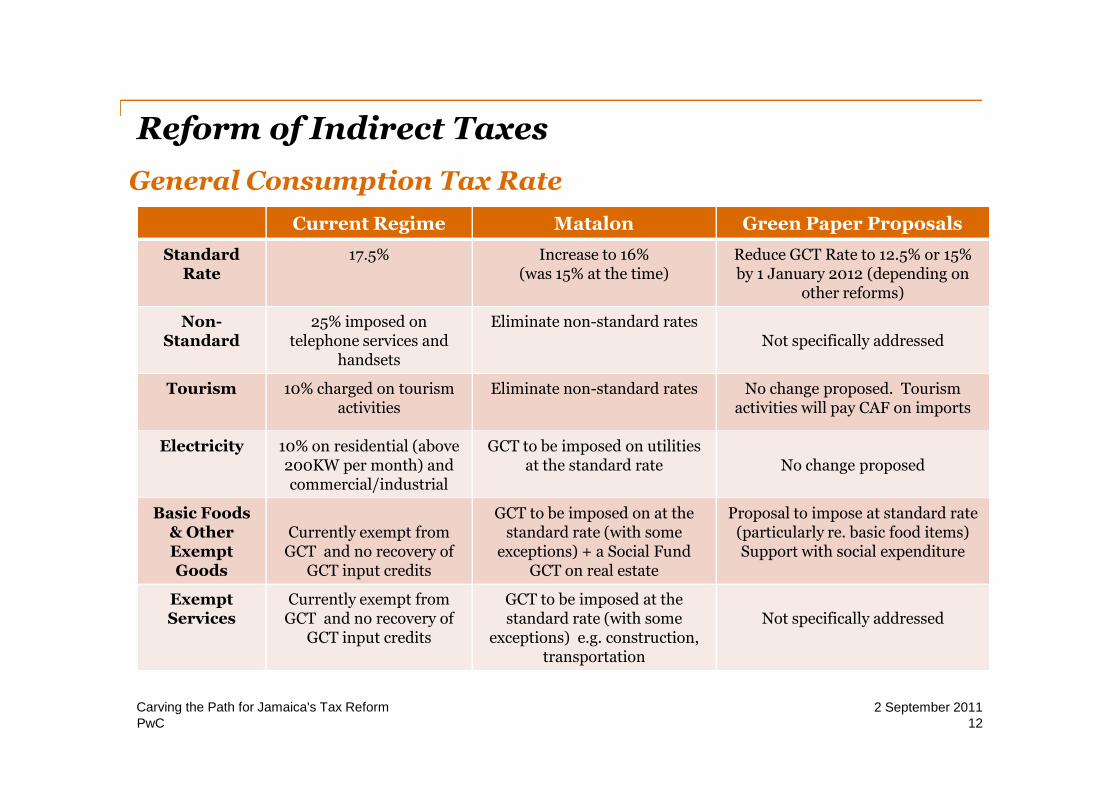

General Consumption Tax Rate

Reform of Indirect Taxes

Current Regime Matalon Green Paper Proposals

StandardRate

17.5% Increase to 16%(was 15% at the time)

Reduce GCT Rate to 12.5% or 15%by 1 January 2012 (depending on

other reforms)

Non-Standard

25% imposed ontelephone services and

handsets

Eliminate non-standard ratesNot specifically addressed

Tourism 10% charged on tourismactivities

Eliminate non-standard rates No change proposed. Tourismactivities will pay CAF on imports

Electricity 10% on residential (above200KW per month) andcommercial/industrial

GCT to be imposed on utilitiesat the standard rate No change proposed

Basic Foods& OtherExemptGoods

Currently exempt fromGCT and no recovery of

GCT input credits

GCT to be imposed on at thestandard rate (with some

exceptions) + a Social FundGCT on real estate

Proposal to impose at standard rate(particularly re. basic food items)Support with social expenditure

ExemptServices

Currently exempt fromGCT and no recovery of

GCT input credits

GCT to be imposed at thestandard rate (with some

exceptions) e.g. construction,transportation

Not specifically addressed

122 September 2011Carving the Path for Jamaica's Tax Reform

PwC

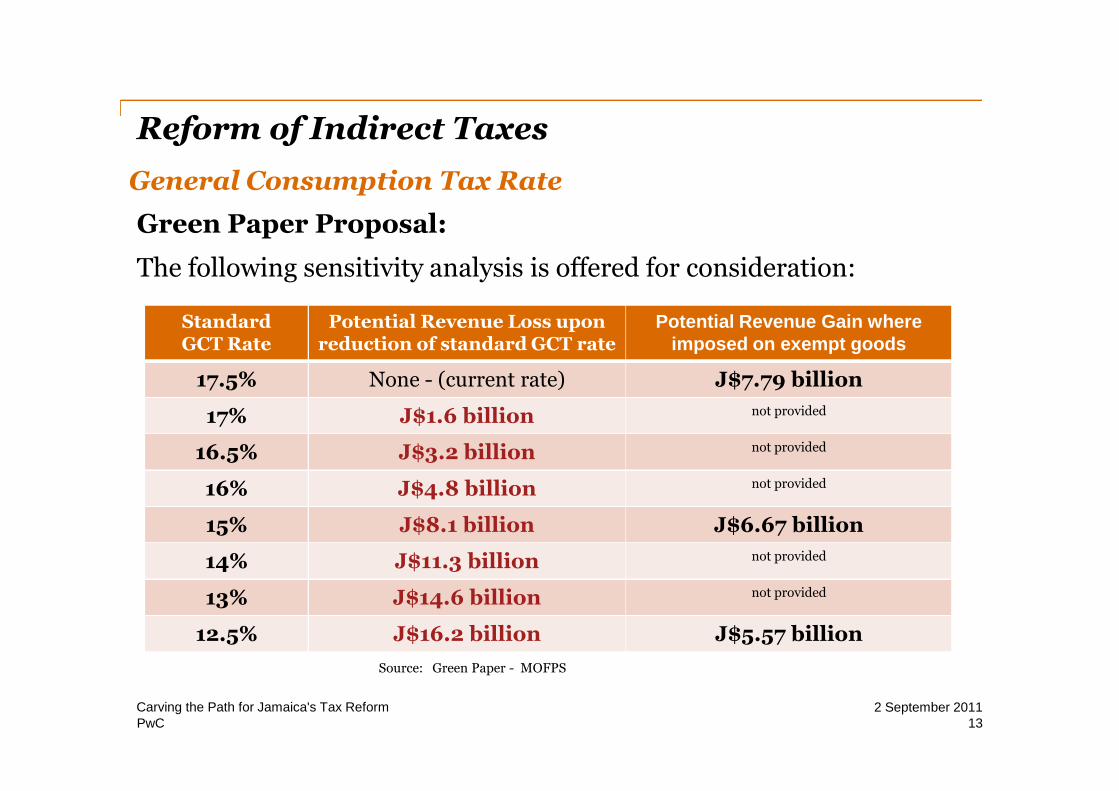

General Consumption Tax Rate

Reform of Indirect Taxes

Green Paper Proposal:

The following sensitivity analysis is offered for consideration:

StandardGCT Rate

Potential Revenue Loss uponreduction of standard GCT rate

Potential Revenue Gain whereimposed on exempt goods

17.5% None - (current rate) J$7.79 billion

17% J$1.6 billion not provided

16.5% J$3.2 billion not provided

16% J$4.8 billion not provided

15% J$8.1 billion J$6.67 billion

14% J$11.3 billion not provided

13% J$14.6 billion not provided

12.5% J$16.2 billion J$5.57 billion

Source: Green Paper - MOFPS

132 September 2011Carving the Path for Jamaica's Tax Reform

PwC

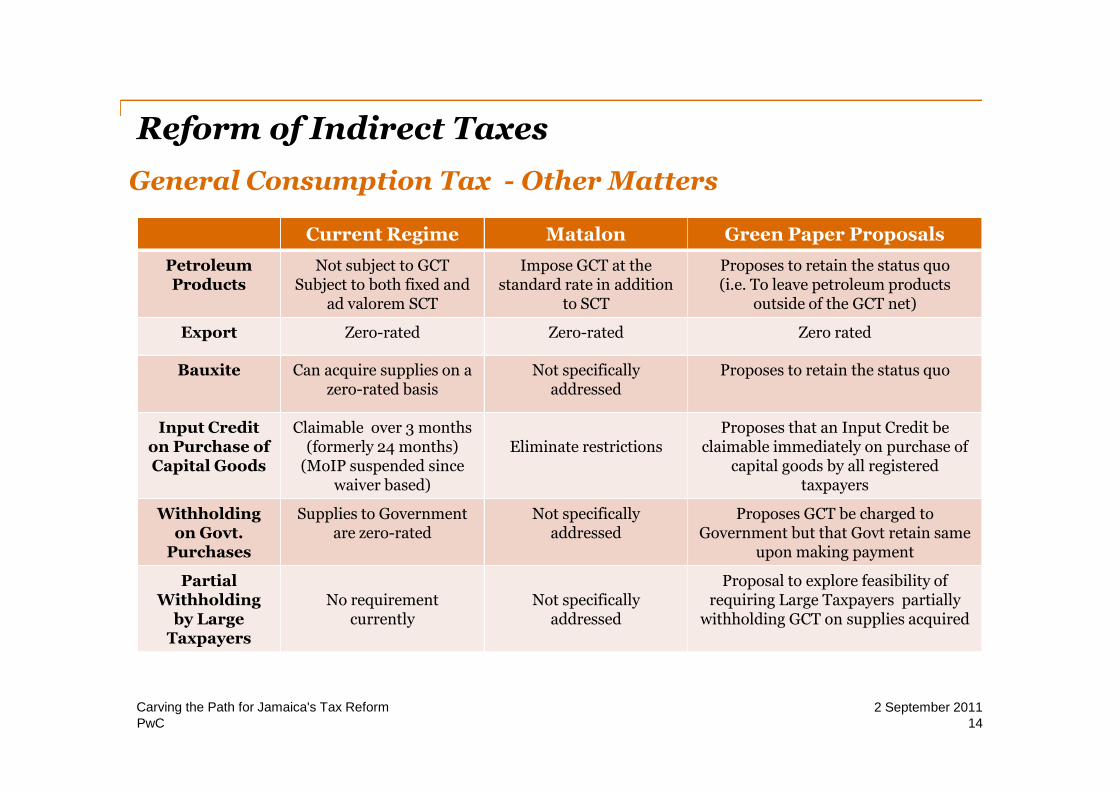

General Consumption Tax - Other Matters

Reform of Indirect Taxes

Current Regime Matalon Green Paper Proposals

PetroleumProducts

Not subject to GCTSubject to both fixed and

ad valorem SCT

Impose GCT at thestandard rate in addition

to SCT

Proposes to retain the status quo(i.e. To leave petroleum products

outside of the GCT net)

Export Zero-rated Zero-rated Zero rated

Bauxite Can acquire supplies on azero-rated basis

Not specificallyaddressed

Proposes to retain the status quo

Input Crediton Purchase ofCapital Goods

Claimable over 3 months(formerly 24 months)

(MoIP suspended sincewaiver based)

Eliminate restrictionsProposes that an Input Credit be

claimable immediately on purchase ofcapital goods by all registered

taxpayers

Withholdingon Govt.

Purchases

Supplies to Governmentare zero-rated

Not specificallyaddressed

Proposes GCT be charged toGovernment but that Govt retain same

upon making payment

PartialWithholding

by LargeTaxpayers

No requirementcurrently

Not specificallyaddressed

Proposal to explore feasibility ofrequiring Large Taxpayers partially

withholding GCT on supplies acquired

142 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Reform of Corporate & PersonalTaxes

152 September 2011Carving the Path for Jamaica's Tax Reform

PwC

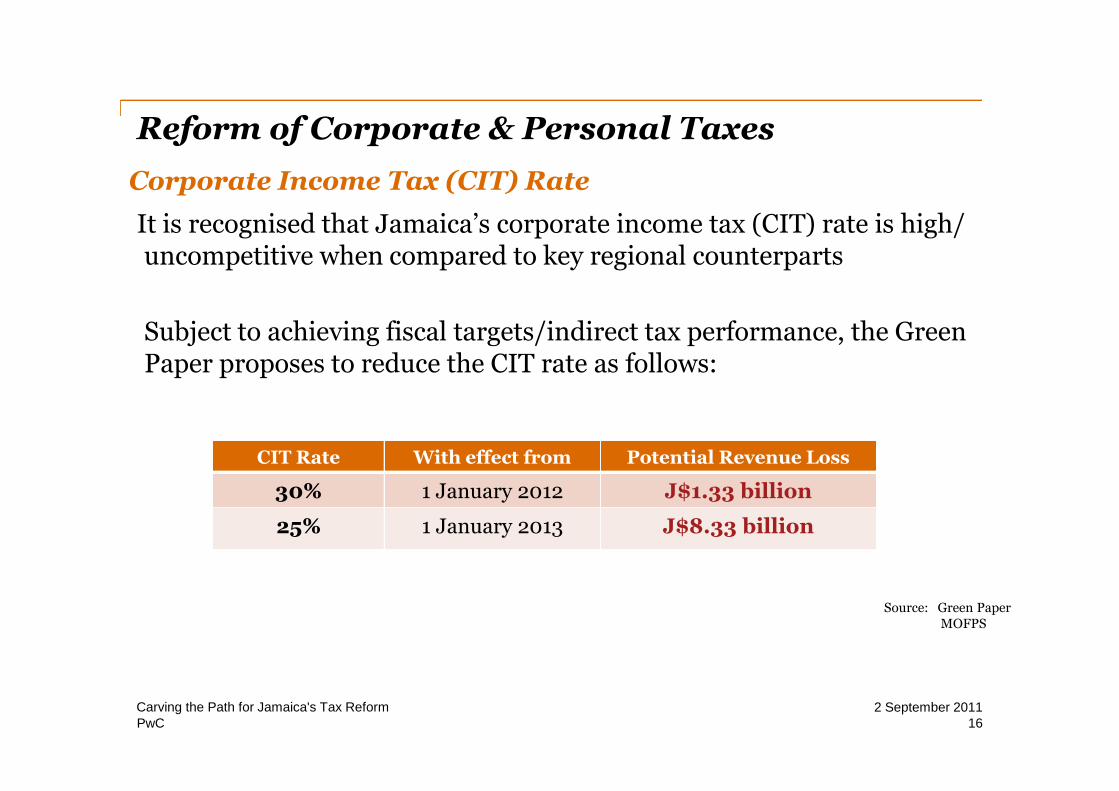

Corporate Income Tax (CIT) Rate

Reform of Corporate & Personal Taxes

It is recognised that Jamaica’s corporate income tax (CIT) rate is high/uncompetitive when compared to key regional counterparts

Subject to achieving fiscal targets/indirect tax performance, the GreenPaper proposes to reduce the CIT rate as follows:

CIT Rate With effect from Potential Revenue Loss

30% 1 January 2012 J$1.33 billion

25% 1 January 2013 J$8.33 billion

Source: Green PaperMOFPS

162 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Incentives

Reform of Corporate & Personal Taxes

Current Regime:

Contains a myriad of tax preferences, sectoral incentives and waivers

Effectiveness of our suite of incentives has been questionable

Has resulted in a narrowing of the taxable base

Matalon Report suggested that an incentive study be undertaken

Green Paper:

Proposes:

• An Omnibus Tax Code;

• A Tax Incentive Act (which will contain all incentives offered)

• Significant reduction in waivers and institution of rules-basedframework (including dollar limitations) for exceptional cases

172 September 2011Carving the Path for Jamaica's Tax Reform

PwC

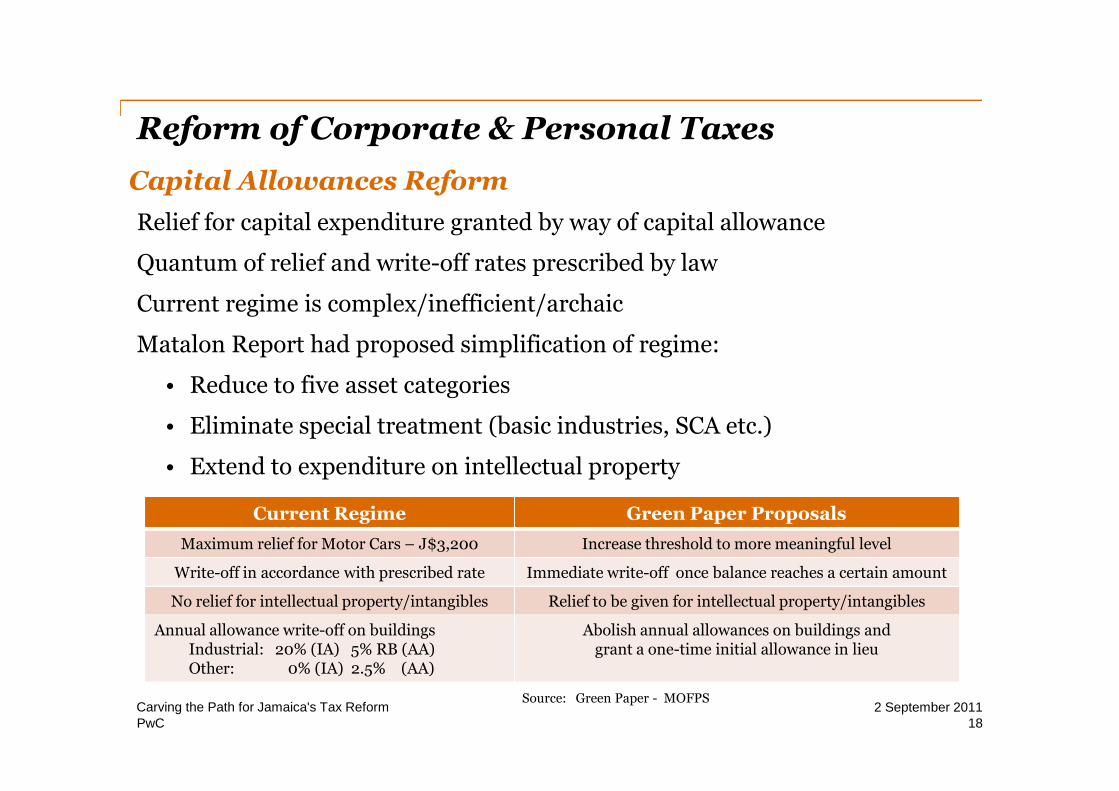

Capital Allowances Reform

Reform of Corporate & Personal Taxes

Relief for capital expenditure granted by way of capital allowance

Quantum of relief and write-off rates prescribed by law

Current regime is complex/inefficient/archaic

Matalon Report had proposed simplification of regime:

• Reduce to five asset categories

• Eliminate special treatment (basic industries, SCA etc.)

• Extend to expenditure on intellectual property

Current Regime Green Paper Proposals

Maximum relief for Motor Cars – J$3,200 Increase threshold to more meaningful level

Write-off in accordance with prescribed rate Immediate write-off once balance reaches a certain amount

No relief for intellectual property/intangibles Relief to be given for intellectual property/intangibles

Annual allowance write-off on buildingsIndustrial: 20% (IA) 5% RB (AA)Other: 0% (IA) 2.5% (AA)

Abolish annual allowances on buildings andgrant a one-time initial allowance in lieu

Source: Green Paper - MOFPS

182 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Minimum Business Tax

Reform of Corporate & Personal Taxes

Current Regime:

Current regime does not impose any minimum business tax

Authorities are concerned with taxpayers who make losses or minimalprofits on an ongoing basis

Matalon Report suggested that an Alternative Minimum Tax (AMT)warranted consideration in light of poor CIT performance

Green Paper:

Proposes to introduce a minimum business tax which will be payableirrespective of profitability

Doesn’t specify how it will be determined (e.g. whether on revenues etc.)

Also proposes to eliminate various trade license fees.

192 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Other

Reform of Corporate & Personal Taxes

Asset Tax:

Currently imposed on the value of the assets of Jamaican registeredcompanies – returns must be filed annually

Considered a nuisance tax and difficult to administer

Green Paper proposes abolition of Asset Tax

Contractors Levy:

Currently the levy is creditable (but not refundable) against income taxliability in the year it is suffered – no carry forward mechanism

Challenges being experienced by construction sector

Green Paper proposes to permit carry forward of unutilised credit for upto five years

202 September 2011Carving the Path for Jamaica's Tax Reform

PwC

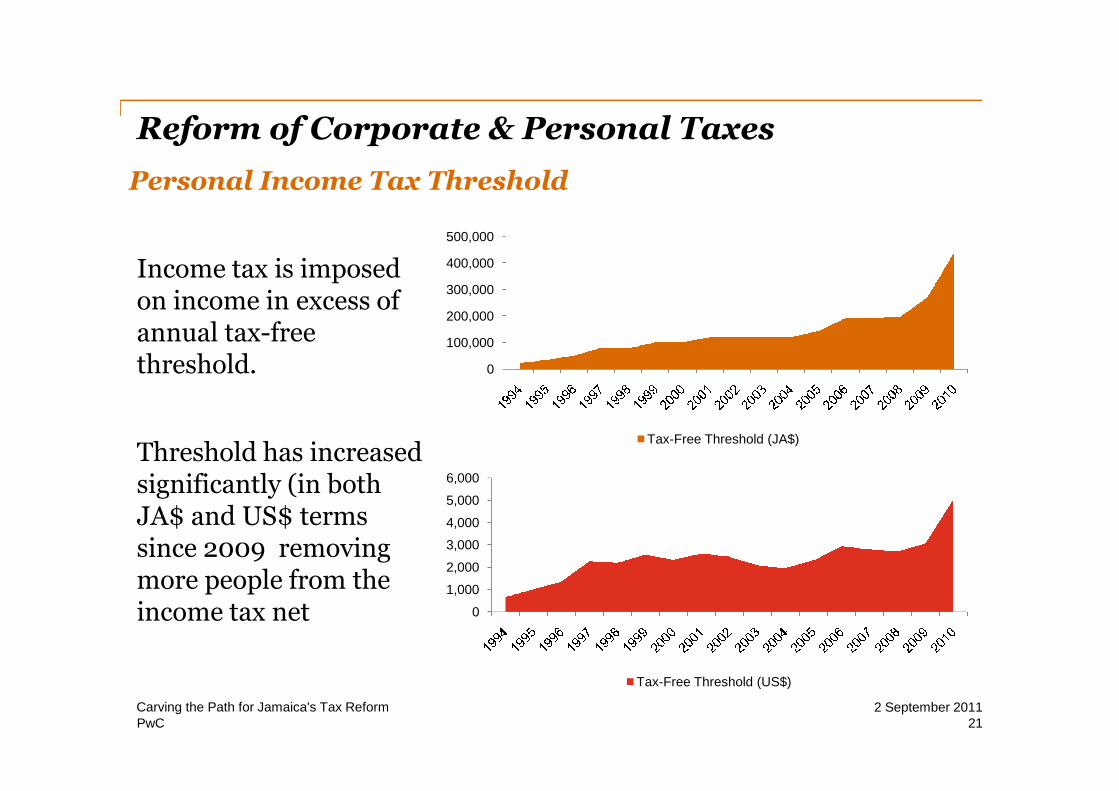

Reform of Corporate & Personal Taxes

Income tax is imposedon income in excess ofannual tax-freethreshold.

Threshold has increasedsignificantly (in bothJA$ and US$ termssince 2009 removingmore people from theincome tax net

0

100,000

200,000

300,000

400,000

500,000

Tax-Free Threshold (JA$)

0

1,000

2,000

3,000

4,000

5,000

6,000

Tax-Free Threshold (US$)

Personal Income Tax Threshold

212 September 2011Carving the Path for Jamaica's Tax Reform

PwC

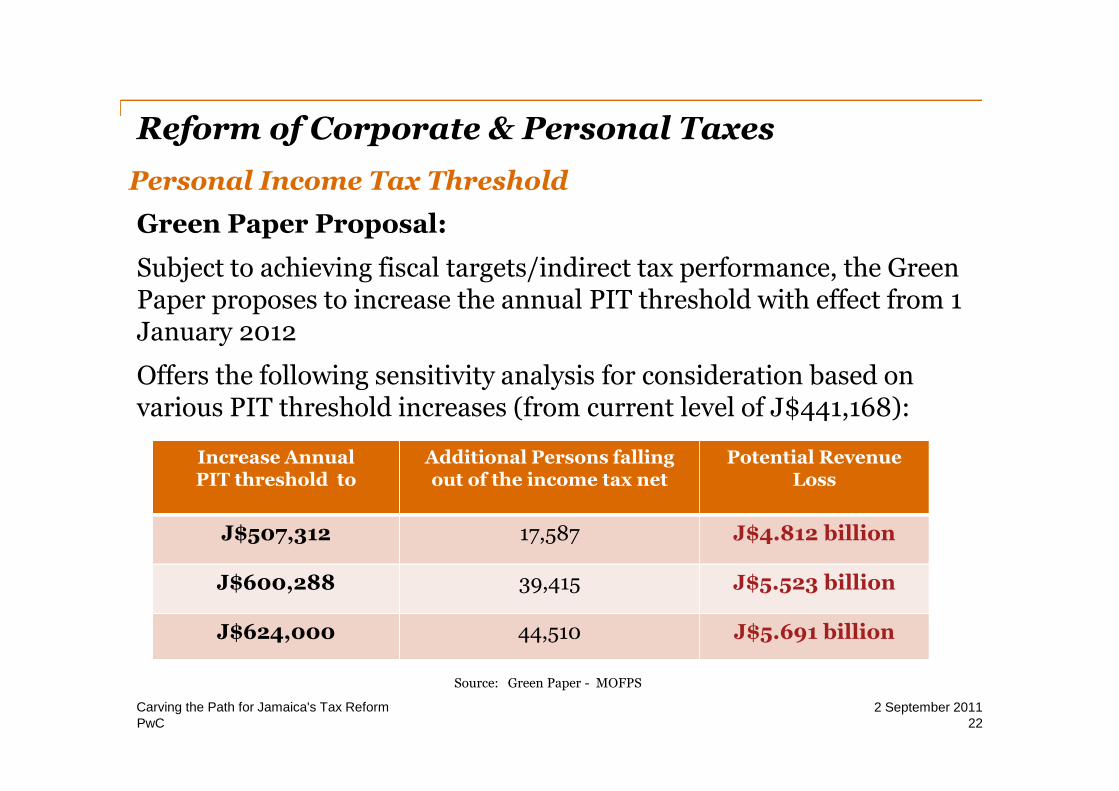

Personal Income Tax Threshold

Reform of Corporate & Personal Taxes

Green Paper Proposal:

Subject to achieving fiscal targets/indirect tax performance, the GreenPaper proposes to increase the annual PIT threshold with effect from 1January 2012

Offers the following sensitivity analysis for consideration based onvarious PIT threshold increases (from current level of J$441,168):

Increase AnnualPIT threshold to

Additional Persons fallingout of the income tax net

Potential RevenueLoss

J$507,312 17,587 J$4.812 billion

J$600,288 39,415 J$5.523 billion

J$624,000 44,510 J$5.691 billion

Source: Green Paper - MOFPS

222 September 2011Carving the Path for Jamaica's Tax Reform

PwC

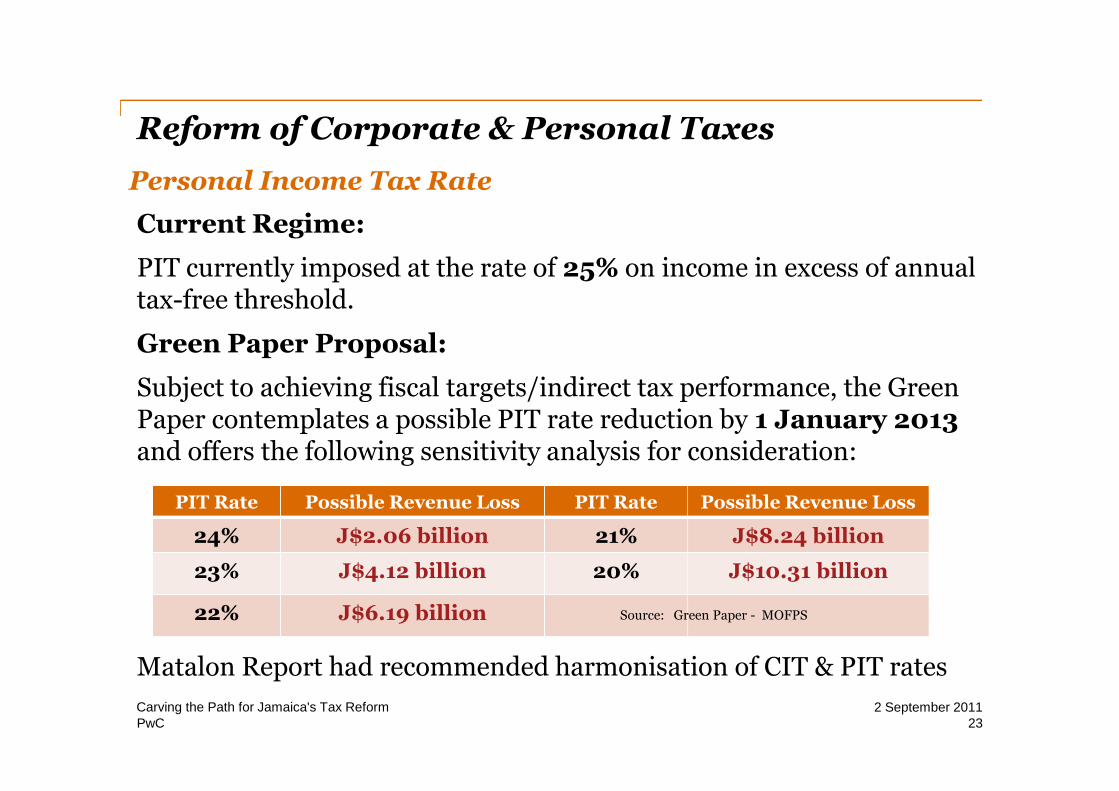

Personal Income Tax Rate

Reform of Corporate & Personal Taxes

Current Regime:

PIT currently imposed at the rate of 25% on income in excess of annualtax-free threshold.

Green Paper Proposal:

Subject to achieving fiscal targets/indirect tax performance, the GreenPaper contemplates a possible PIT rate reduction by 1 January 2013and offers the following sensitivity analysis for consideration:

Matalon Report had recommended harmonisation of CIT & PIT rates

PIT Rate Possible Revenue Loss PIT Rate Possible Revenue Loss

24% J$2.06 billion 21% J$8.24 billion

23% J$4.12 billion 20% J$10.31 billion

22% J$6.19 billion Source: Green Paper - MOFPS

232 September 2011Carving the Path for Jamaica's Tax Reform

PwC

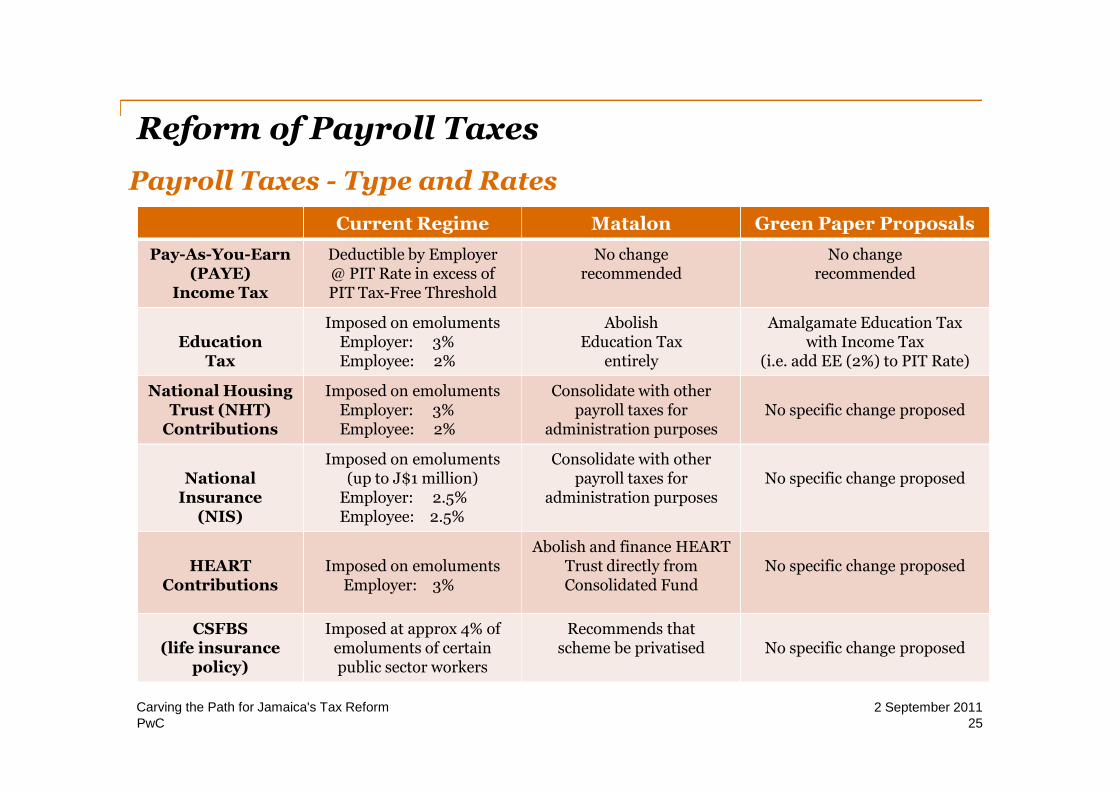

Reform of Payroll Taxes

242 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Payroll Taxes - Type and Rates

Reform of Payroll Taxes

Current Regime Matalon Green Paper Proposals

Pay-As-You-Earn(PAYE)

Income Tax

Deductible by Employer@ PIT Rate in excess ofPIT Tax-Free Threshold

No changerecommended

No changerecommended

EducationTax

Imposed on emolumentsEmployer: 3%Employee: 2%

AbolishEducation Tax

entirely

Amalgamate Education Taxwith Income Tax

(i.e. add EE (2%) to PIT Rate)

National HousingTrust (NHT)

Contributions

Imposed on emolumentsEmployer: 3%Employee: 2%

Consolidate with otherpayroll taxes for

administration purposesNo specific change proposed

NationalInsurance

(NIS)

Imposed on emoluments(up to J$1 million)

Employer: 2.5%Employee: 2.5%

Consolidate with otherpayroll taxes for

administration purposesNo specific change proposed

HEARTContributions

Imposed on emolumentsEmployer: 3%

Abolish and finance HEARTTrust directly fromConsolidated Fund

No specific change proposed

CSFBS(life insurance

policy)

Imposed at approx 4% ofemoluments of certainpublic sector workers

Recommends thatscheme be privatised No specific change proposed

252 September 2011Carving the Path for Jamaica's Tax Reform

PwC

Administrative Reform

26Carving the Path for Jamaica's Tax Reform 2 September 2011

PwC

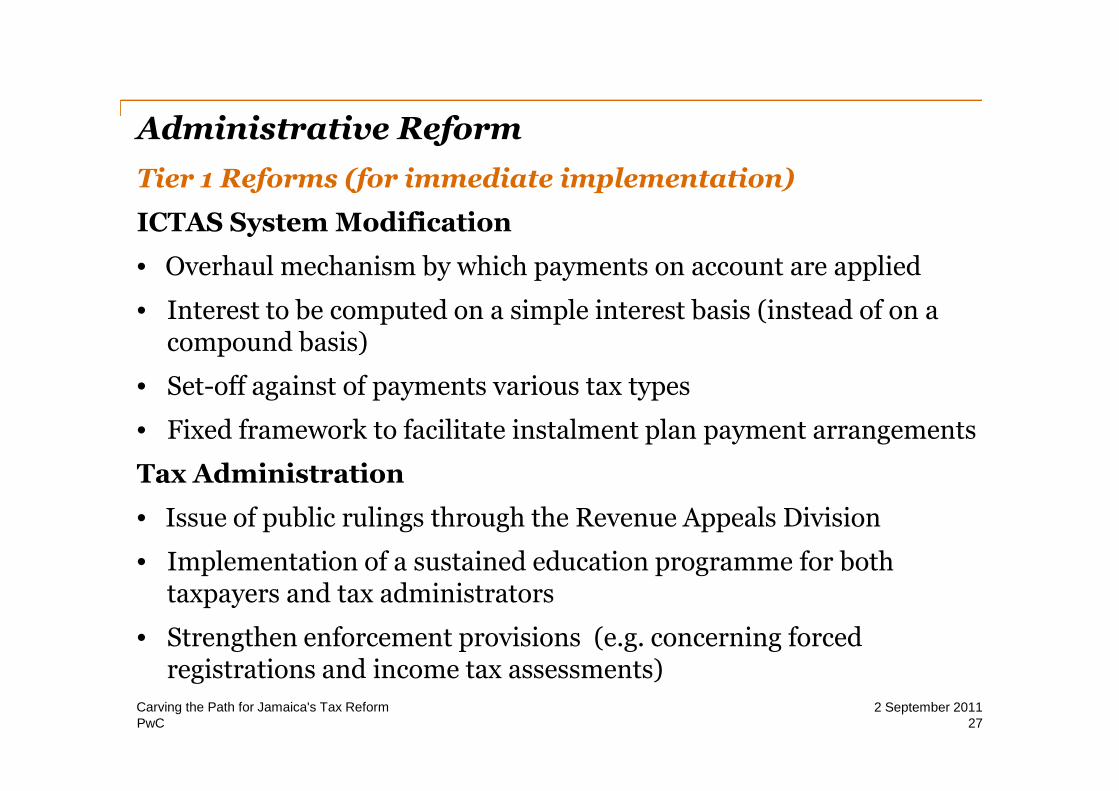

Administrative Reform

Tier 1 Reforms (for immediate implementation)

ICTAS System Modification

• Overhaul mechanism by which payments on account are applied

• Interest to be computed on a simple interest basis (instead of on acompound basis)

• Set-off against of payments various tax types

• Fixed framework to facilitate instalment plan payment arrangements

Tax Administration

• Issue of public rulings through the Revenue Appeals Division

• Implementation of a sustained education programme for bothtaxpayers and tax administrators

• Strengthen enforcement provisions (e.g. concerning forcedregistrations and income tax assessments)

27Carving the Path for Jamaica's Tax Reform 2 September 2011

PwC

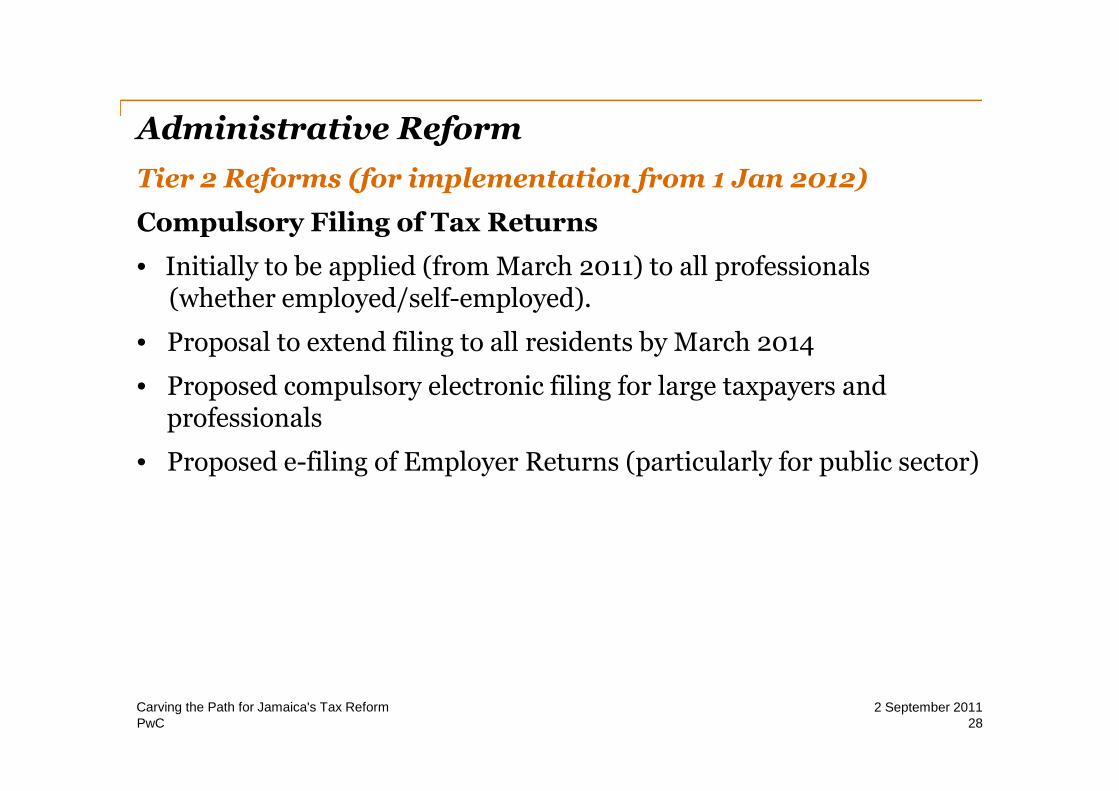

Administrative Reform

Tier 2 Reforms (for implementation from 1 Jan 2012)

Compulsory Filing of Tax Returns

• Initially to be applied (from March 2011) to all professionals(whether employed/self-employed).

• Proposal to extend filing to all residents by March 2014

• Proposed compulsory electronic filing for large taxpayers andprofessionals

• Proposed e-filing of Employer Returns (particularly for public sector)

28Carving the Path for Jamaica's Tax Reform 2 September 2011

Questions?

www.pwc.com/jm

This publication has been prepared for general guidance on matters of interest only, and does notconstitute professional advice. You should not act upon the information contained in this publicationwithout obtaining specific professional advice. No representation or warranty (express or implied) is givenas to the accuracy or completeness of the information contained in this publication, and, to the extentpermitted by law, PricewaterhouseCoopers Jamaica, its members, employees and agents do not accept orassume any liability, responsibility or duty of care for any consequences of you or anyone else acting, orrefraining to act, in reliance on the information contained in this publication or for any decision based onit.

© 2011 PricewaterhouseCoopers Jamaica. All rights reserved. In this document, “PwC” refers toPricewaterhouseCoopers Jamaica which is a member firm of PricewaterhouseCoopers InternationalLimited, each member firm of which is a separate firm or legal entity.

Kingston:Scotiabank CentreDuke StreetKingston

Tel: 1 876 922 6230Fax: 1 876 922 7581

Montego Bay:Fairview Office Park, Unit 10Alice Eldemire DriveMontego BaySt. James

Tel: 1 876 952 5065Fax: 1 876 952 1273

http://www.pwc.com/jm

Eric Crawford, Tax Services LeaderDirect Line: (876) 932 8323Email: [email protected]

Brian Denning, PartnerDirect Line: (876) 932 8423Email: [email protected]

Viveen A Morrison, DirectorDirect Line: (876) 932 8336Email: [email protected]

Paul Cobourne, Senior ManagerDirect Line (876) 932 8350Email: [email protected]

Kimblian Batson, ManagerDirect Line: (876) 932 8378Email: [email protected]

Venneshia Sinanan Forde, ManagerDirect Line: (876) 932 8377Email: [email protected]

If you require specific advice on the implications of the information provided inthis publication or if you need any further information, please contact your usualPwC contact or one of our tax team members noted below: