Embed Size (px)

Citation preview

Dave Cotton, CPA, CFE, CGFM Cotton & Company LLP

Alexandria, Virginia www.cottoncpa.com

The Good, the Bad, & the Ugly: Case Studies in

Contractor Corruption and Fraud

2014 GOVERNMENT CONTRACTORS' CONFERENCE September 18, 2014

DAVID L. COTTON, CPA, CFE, CGFM COTTON & COMPANY LLP CHAIRMAN

Dave Cotton is chairman of Cotton & Company LLP, Certified Public Accountants. Cotton & Company is headquartered in Alexandria, Virginia. The firm was founded in 1981 and has a practice concentration in assisting Federal and State government agencies, inspectors general, and government grantees and contractors with a variety of government program-‐related assurance and advisory services. Cotton & Company has performed grant and contract, indirect cost rate, financial statement, financial related, and performance audits for more than two dozen Federal inspectors general as well as numerous other Federal and State agencies and programs. Cotton & Company’s Federal agency audit clients have included the U.S. Government Accountability Office, the U.S. House of Representatives, the U.S. Capitol Police, the U.S. Small Business Administration, the U.S. Bureau of Prisons, the Millennium Challenge Corporation, the U.S. Marshals Service, and the Bureau of Alcohol, Tobacco, Firearms and Explosives. Cotton & Company also assists numerous Federal agencies in preparing financial statements and improving financial management, accounting, and internal control systems. Dave received a BS in mechanical engineering (1971) and an MBA in management science and labor relations (1972) from Lehigh University in Bethlehem, PA. He also pursued graduate studies in accounting and auditing at the University of Chicago, Graduate School of Business (1977 to 1978). He is a Certified Public Accountant (CPA), Certified Fraud Examiner (CFE), and Certified Government Financial Manager (CGFM). Dave served on the Advisory Council on Government Auditing Standards (the Council advises the United States Comptroller General on promulgation of Government Auditing Standards—GAO’s yellow book) from 2006 to 2009. He served on the Institute of Internal Auditors (IIA) Anti-‐Fraud Programs and Controls Task Force and co-‐authored Managing the Business Risk of Fraud: A Practical Guide. He served on the American Institute of CPAs Anti-‐Fraud Task Force and co-‐authored Management Override: The Achilles Heel of Fraud Prevention. He is the past-‐chairman of the AICPA Federal Accounting and Auditing Subcommittee and has served on the AICPA Governmental Account-‐ing and Auditing Committee and the Government Technical Standards Subcommittee of the AICPA Professional Ethics Executive Committee. He authored the AICPA’s 8-‐hour continuing professional education course, Joint and Indirect Cost Allocations—How to Prepare and Audit Them. Dave served on the board of the Virginia Society of Certified Public Accountants (VSCPA) and on the VSCPA Litigation Services Committee, Professional Ethics Committee, Quality Review Committee, and Governmental Accounting and Auditing Committee. He is member of the Greater Washington Society of CPAs (GWSCPA) and serves on the GWSCPA Professional Ethics Committee. He is a member of the Association of Government Accountants (AGA) and past-‐advisory board chairman and past-‐president of the AGA Northern Virginia Chapter. He is also a member of the Institute of Internal Auditors and the Association of Certified Fraud Examiners.

Dave has testified as an expert in governmental accounting, auditing, and fraud issues before the United States Court of Federal Claims and other administrative and judicial bodies. Dave has spoken frequently on cost accounting, professional ethics, and auditors’ fraud detection responsibilities under SAS 99, Consideration of Fraud in a Financial Statement Audit. He has been an instructor for the George Washington University masters of accountancy program (Fraud Examination and Forensic Accounting), and instructs for the George Mason University Small Business Development Center (Fundamentals of Accounting for Government Contracts). Dave was the recipient of the AGA’s 2006 Barr Award (“to recognize the cumulative achievements of private sector individuals who throughout their careers have served as a role model for others and who have consistently exhibited the highest personal and professional standards”) as well as AGA’s 2012 Educator Award (“to recognize individuals who have made significant contributions to the education and training of government financial managers”).

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Ø The Case of the Ostensible Subcontractor Ø The Case of the Maryland Ostensible Subcontractor Ø The Case of the Corporation-Creating Couple Ø The Case of the Khan Con of “Historic Proportions” Ø The Case of Hizzoner’s Corrupt Spouse Ø The Case of the Profitable Internal Service Center

The Good, the Bad, & the Ugly: Case Studies in Contractor Corruption and Fraud

What were the Fraud risk factors?

Fraud Risk Factor: A characteristic that provides a motivation/pressure or opportunity for fraud to occur; a rationalization/attitude supportive of fraud; or an indicator that fraud might have occurred or might be occurring

Case Analysis

Motive Pressure

Attitude rationalization

opportunity

FRAUD

2014 GOVERNMENT CONTRACTORS' CONFERENCE

It can’t happen here

Remember: Four words have preceded EVERY fraud that has ever been committed …

We didn’t think it could happen to us

Remember: Eight words have followed EVERY fraud that has ever been discovered …

2014 GOVERNMENT CONTRACTORS' CONFERENCE

The Case of the Ostensible Subcontractor

Case Study

Case Study The Case of the Ostensible

Subcontractor 13 CFR 121.103 (h)(4) …. An ostensible subcontractor is a subcontractor that performs primary and vital requirements of a contract, or of an order under a mul=ple award schedule contract, or a subcontractor upon which the prime contractor is unusually reliant. …

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Ostensible

Subcontractor ü Keith Hedman, an executive at Arlington, VA security

consulting Company A illegally controlled another Arlington, VA security consulting Company B that was 8(a) certified

ü Company B’s 8(a) certification was based on its “titular head” Dawn Hamilton

ü Michael Brian Dunkel agreed to pay Hedman and Company B a fee for allowing Dunkel to use Company B’s 8(a) status to obtain contracts

Source: http://oig.nasa.gov/press/pr2014-D.pdf

Case Study The Case of the Ostensible

Subcontractor ü Company B was required to perform at least 50% of the

contract work

ü No Company B employees did ANY of the work under the contracts

ü Dunkel and others did all of the work as independent contractors and concealed this from the government

ü Dunkel submitted fraudulent proposals and invoices to hide the scheme, used a 3rd party FEIN to prevent reporting of his income to the IRS, and failed to pay any taxes on his Company B income

Source: http://oig.nasa.gov/press/pr2014-D.pdf

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Ostensible

Subcontractor ü Seven defendants, including Hedman and Hamilton pled

guilty to and were sentenced for participation in this fraud scheme and related bribery case before Dunkel pled guilty

ü Dunkel pled guilty on 23 May 2013 to fraudulently obtaining $4.4+ million in government contract payments that should have gone to disadvantaged small businesses

ü Dunkel was sentenced on 28 February 2014 to 60 months in prison and ordered to pay a $12,500 fine and $2,960,697 in forfeiture

Source: http://oig.nasa.gov/press/pr2014-D.pdf

Case Study The Case of the Ostensible

Subcontractor

FRAUD

opportunity

Motive Pressure

Attitude rationalization

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Ostensible

Subcontractor Fraud risk factors/indicators

The Case of the Maryland Ostensible Subcontractor

Case Study

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Maryland Ostensible Subcontractor

ü Vernon Smith was owner/officer of Capitol Contractors, a roofing and construction contractor

ü Majority owner of Capitol was a Native American

ü Capitol received its 8(a) certification in March 1993 but “graduated” from the set-aside program in March 2002

ü Vernon Smith bought the Native American’s interest in Capitol just before Capitol graduated; and Smith became sole owner

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

Case Study The Case of the Maryland Ostensible Subcontractor

ü In 1999, Vernon Smith arranged for Anthony Wright, an African-American former Capitol project manager, to establish Platinum One Contracting in Maryland

ü Wright was president and owned 60% of Platinum; Vernon Smith’s son owned the remaining 40%

ü Vernon Smith actually exercised complete control over Platinum operations, day-to-day management, and long-term decisionmaking

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Maryland Ostensible Subcontractor

ü Vernon Smith directed Wright to apply for 8(a) certification; but the application failed to disclose that Vernon Smith:

ü exercised control over Platinum

ü Previously supervised Wright

ü Owned Capitol Contractors

ü Was related to an owner of Platinum

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

Case Study The Case of the Maryland Ostensible Subcontractor

ü Vernon Smith caused Platinum to submit false annual updates to the SBA from 2004 through 2010 and failed to disclose that:

ü Platinum was not controlled by a socially/economically disadvantaged individual

ü Non-disadvantaged individuals received more compensation than Wright (payments to Vernon Smith and others far exceeded Wrights compensation from 2004 to 2009)

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Maryland Ostensible Subcontractor

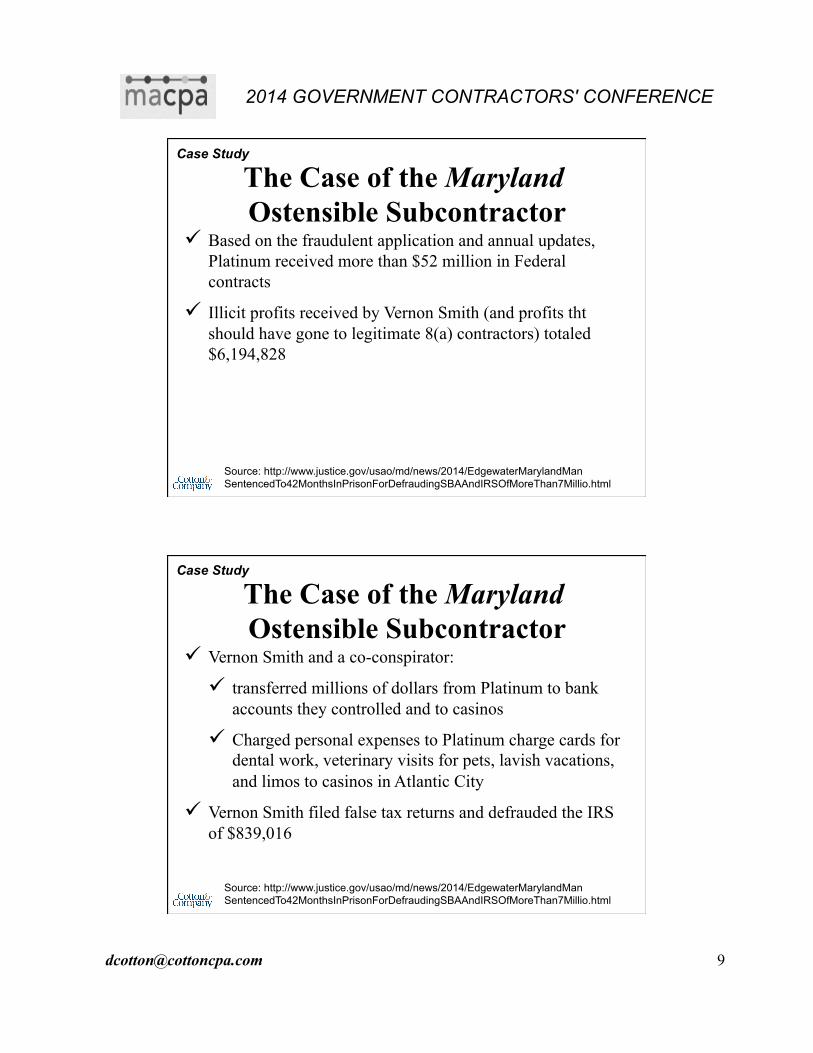

ü Based on the fraudulent application and annual updates, Platinum received more than $52 million in Federal contracts

ü Illicit profits received by Vernon Smith (and profits tht should have gone to legitimate 8(a) contractors) totaled $6,194,828

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

Case Study The Case of the Maryland Ostensible Subcontractor

ü Vernon Smith and a co-conspirator:

ü transferred millions of dollars from Platinum to bank accounts they controlled and to casinos

ü Charged personal expenses to Platinum charge cards for dental work, veterinary visits for pets, lavish vacations, and limos to casinos in Atlantic City

ü Vernon Smith filed false tax returns and defrauded the IRS of $839,016

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Maryland Ostensible Subcontractor

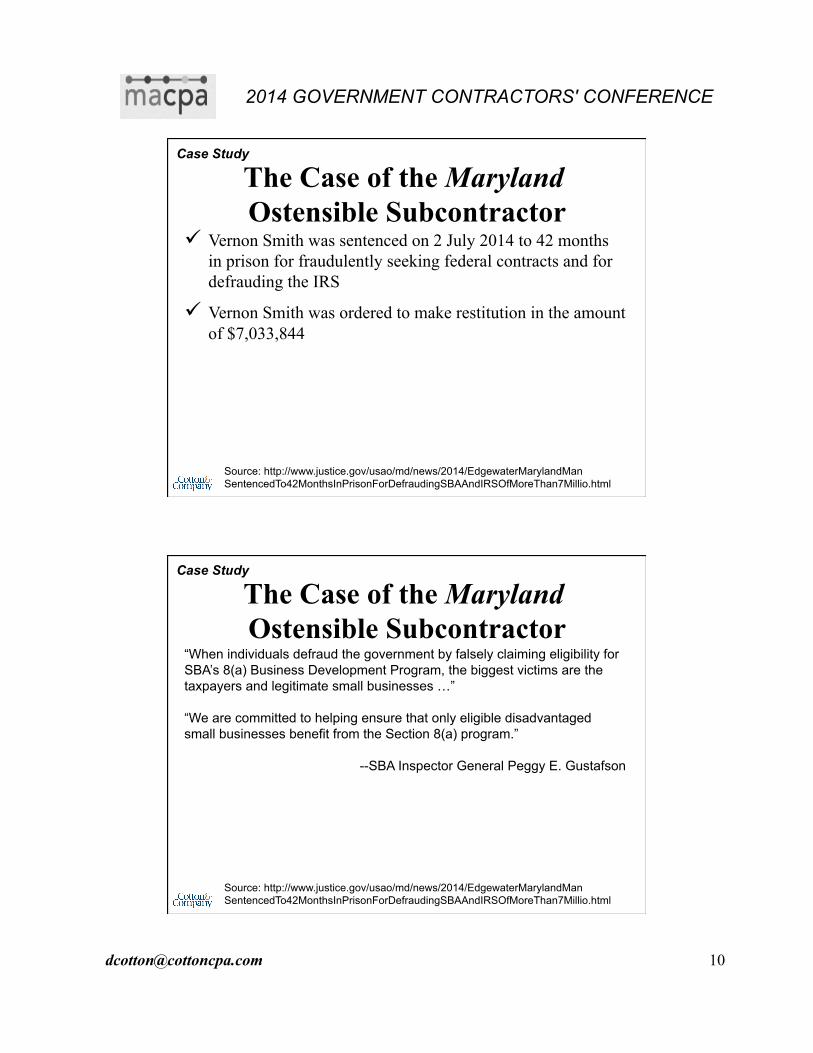

ü Vernon Smith was sentenced on 2 July 2014 to 42 months in prison for fraudulently seeking federal contracts and for defrauding the IRS

ü Vernon Smith was ordered to make restitution in the amount of $7,033,844

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

Case Study The Case of the Maryland Ostensible Subcontractor

“When individuals defraud the government by falsely claiming eligibility for SBA’s 8(a) Business Development Program, the biggest victims are the taxpayers and legitimate small businesses …” “We are committed to helping ensure that only eligible disadvantaged small businesses benefit from the Section 8(a) program.”

--SBA Inspector General Peggy E. Gustafson

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study The Case of the Maryland Ostensible Subcontractor

“Americans were victimized twice by the greed of Vernon Smith. Not only did Smith decide not to pay his fair share of federal taxes and ultimately defraud the IRS out of $839,016, his actions also denied legitimate business owners of socially and disadvantaged groups the opportunity to receive government contracts to which they were entitled ...” “Today’s sentencing should put corrupt business owners, like Vernon Smith, on notice that the government will get to the truth no matter how they may try to conceal their involvement and income.”

--Thomas J Kelly, Special Agent in Charge, IRS Criminal Investigation, Washington D.C. Field Office.

Source: http://www.justice.gov/usao/md/news/2014/EdgewaterMarylandMan SentencedTo42MonthsInPrisonForDefraudingSBAAndIRSOfMoreThan7Millio.html

Case Study The Case of the Maryland Ostensible Subcontractor

FRAUD

opportunity

Motive Pressure

Attitude rationalization

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

Fraud risk factors/indicators

The Case of the Maryland Ostensible Subcontractor

The Case of the Corporation-Creating Couple

Case Study

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü Co-conspirators Christopher Johnson (age 36) and Larayne Whitehead (age 35) created at least 15 bogus businesses in MD, DE, GA, NE, NC, and TN; e.g.: ü The Encompass Group

ü The Crescant Group

ü The Taylor Hailey Group

ü The United Partners Consulting Group

ü Worldwide Industries

ü The Global Synergy Group

ü The Parktech Group Sources: http://www.justice.gov/usao/md/news/2014/ ConspiratorSentencedTo PrisonIn 2.3MillionGovernmentContractFraudScheme.html; http://www.fbi.gov/baltimore/press-releases/2014/clinton-woman-sentenced-in-2.3-million-government-contract-fraud-scheme

The Case of the Corporation-Creating Couple

Case Study

ü They bid on government contracts to provide goods (books, snowmobiles, plants, paint) to government agencies

ü They used the on-line federal marketplace (FedBid) and bid extremely low prices

ü Johnson and Whitehead then enticed other, legitimate (victim) businesses to provide the goods based on their promise to pay after the federal government paid them

ü The Feds paid Johnson and Whitehead; but, they kept the money and did not pay the real suppliers

Sources: http://www.justice.gov/usao/md/news/2014/ ConspiratorSentencedTo PrisonIn 2.3MillionGovernmentContractFraudScheme.html; http://www.fbi.gov/baltimore/press-releases/2014/clinton-woman-sentenced-in-2.3-million-government-contract-fraud-scheme

The Case of the Corporation-Creating Couple

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü Johnson and Whitehead used a front company until that company either was disqualified by FedBid or until it became encumbered with lawsuits and liens

ü Then, they simply continued the scheme using a newly-registered business name

ü Johnson and Whitehead initially used their true identities to set up the bogus businesses; but later used aliases to conceal their true identities

Sources: http://www.justice.gov/usao/md/news/2014/ ConspiratorSentencedTo PrisonIn 2.3MillionGovernmentContractFraudScheme.html; http://www.fbi.gov/baltimore/press-releases/2014/clinton-woman-sentenced-in-2.3-million-government-contract-fraud-scheme

The Case of the Corporation-Creating Couple

Case Study

ü Between 50 and 250 legitimate businesses were victimized

ü Total take: 42.3 million

ü Sentences:

ü Johnson: 18 months in prison; restitution of $2,393,579

ü Whitehead: 18 months in prison; forfeiture of $2,393,579 and a car

Sources: http://www.justice.gov/usao/md/news/2014/ ConspiratorSentencedTo PrisonIn 2.3MillionGovernmentContractFraudScheme.html; http://www.fbi.gov/baltimore/press-releases/2014/clinton-woman-sentenced-in-2.3-million-government-contract-fraud-scheme

The Case of the Corporation-Creating Couple

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

FRAUD

opportunity

Motive Pressure

Attitude rationalization

The Case of the Corporation-Creating Couple

Case Study

Fraud risk factors/indicators

The Case of the Corporation-Creating Couple

2014 GOVERNMENT CONTRACTORS' CONFERENCE

The Case of the Khan Con of “Historic Proportions”

Case Study

Case Study

ü Kerry Khan was a program manager for the Army Corps of Engineers (COE)

ü Khan was the “ringleader” of the “largest domextic bribery and bid-rigging scheme in the history of federal contracting”

ü Khan was paid $12+ million through the bribery scheme from 2007 to 2011

ü Just before his arrest, Khan was in the process of steering a $1 billion contract to a favored company

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

Khan’s Alexandria, VA house (WashPost Photo Courtesy of Department of Jus=ce)

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

Case Study

ü Khan started working at the COE in 1994

ü Rose to program manager and contracting officer’s technical representative with the Directorate of Contingency Operations

ü Had authority to place orders for products and services; and had authority to certify completion of work under contracts

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü Khan’s co-conspirators (all have plead guilty): ü Michael Alexander, another COE manager

ü Harold Babb, director of contracts at Eyak Technology LLC, an Alaska Native-owned small business

ü Alex Cho, chief technology officer at Nova Datacom LLC

ü Larry Corbett, owner of Core Technology LLC

ü Robert McKinney, president of Alpha Technology Group

ü James Edward Miller, owner of Big Surf Construction Management LLC

ü Nick Park, employee of Nova Datacom LLC

ü Lee Khan, Kerry Khan’s son

ü Nazim Khan, Kerry Kahn’s brother Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

Case Study

ü Khan’s co-conspirators (all have plead guilty): ü Nova Datacom LLC

ü Min Jung Cho, president of Nova Datacom

ü Theodoros Hallas, executive VP of Nova Datacom

ü John Han Lee, co-founder of Unisource Enterprise Inc.

ü King Everett Johnson, Unisource Enterprise employee, founder of Integrated Business and Technology Solutions LLC

ü Oh Sung Kwon (aka Thomas Kwon), co-founder and CEO of Avenciatech Inc.

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü In 2006, Kerry Khan and Michael Alexander began steering COE contracts to corrupt companies in return for bribes

ü Khan, Alexander and Harold Babb of EyakTek used EyakTek Alaska-Native-owned small business status as the vehicle to channel COE contracts to others in the scheme

ü EyakTek subs submitted fraudulently inflated or fictitious invoices to Khan and Alexander, then kicked back parts of the payments to Khan and Alexander

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

Case Study

ü In most cases, the corrupt subs provided the equipment and services called for under the contracts, but also billed for inflated or fictitious equipment and services

ü Khan referred to the fraudulently inflated amounts as “overhead”

ü Khan, Alexander, and the subcontractors split the “overhead”

ü Khan obtained $12 million through the scheme; and at the time of his arrest, he had an additional $14 million in “overhead” receivables

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

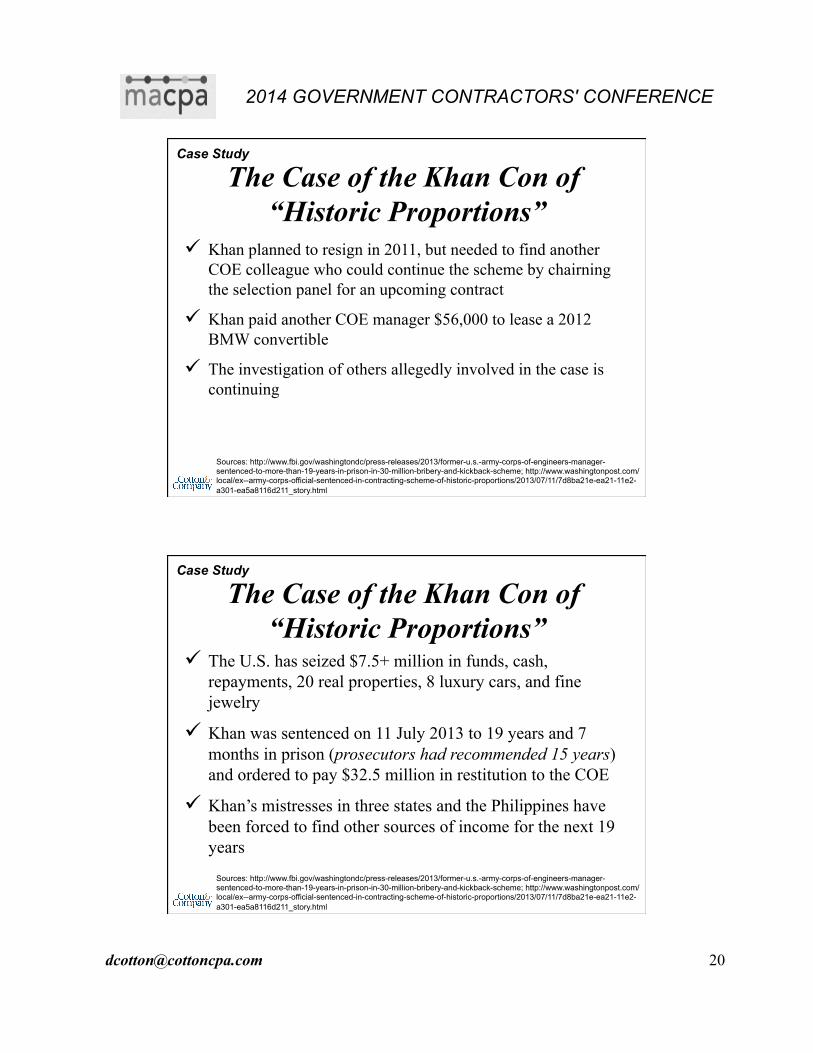

ü Khan planned to resign in 2011, but needed to find another COE colleague who could continue the scheme by chairning the selection panel for an upcoming contract

ü Khan paid another COE manager $56,000 to lease a 2012 BMW convertible

ü The investigation of others allegedly involved in the case is continuing

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

Case Study

ü The U.S. has seized $7.5+ million in funds, cash, repayments, 20 real properties, 8 luxury cars, and fine jewelry

ü Khan was sentenced on 11 July 2013 to 19 years and 7 months in prison (prosecutors had recommended 15 years) and ordered to pay $32.5 million in restitution to the COE

ü Khan’s mistresses in three states and the Philippines have been forced to find other sources of income for the next 19 years

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü How was Khan’s con discovered?

ü Investigators were looking into an unrelated fraud at Nova Datacom

ü Nova Datacom’s founder, Young N. “Alex” Cho “tipped off” investigators about Khan and agreed to wear a wire to help develop the case against Khan and the others

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

Case Study

“The business of our town is government, and with government comes government contracts — lots of government contracts,” Assistant U.S. Attorney Michael Atkinson told the judge Thursday, urging him to send a message to thousands of public officials and contractors who must decide daily “whether to give in to the temptation of government corruption.”

Sources: http://www.fbi.gov/washingtondc/press-releases/2013/former-u.s.-army-corps-of-engineers-manager-sentenced-to-more-than-19-years-in-prison-in-30-million-bribery-and-kickback-scheme; http://www.washingtonpost.com/ local/ex--army-corps-official-sentenced-in-contracting-scheme-of-historic-proportions/2013/07/11/7d8ba21e-ea21-11e2-a301-ea5a8116d211_story.html

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

FRAUD

opportunity

Motive Pressure

Attitude rationalization

The Case of the Khan Con of “Historic Proportions”

Case Study

Fraud risk factors/indicators

The Case of the Khan Con of “Historic Proportions”

2014 GOVERNMENT CONTRACTORS' CONFERENCE

The Case of Hizzoner’s Corrupt Spouse

Case Study

Case Study

ü Darlene Mathis-Gardner, wife of D.C. Superior Court Judge Wendell Gardner, was sentenced on 13 July 2011 to 18 months in prison and ordered to pay $389,738 in restitution to Immigration and Customs Enforcement (ICE)

ü Mathis-Gardner submitted false information about her company’s background and qualifications and created fictitious past performance information in order to obtain a $1.3 million contract for interior design work on ICE’s headquarters building

Source: http://www.justice.gov/opa/pr/2011/July/11-at-915.html

The Case of Hizzoner’s Corrupt Spouse

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

ü After fraudulently obtaining the contract, Mathis-Gardner knowingly submitted invoices that overstated hours worked resulting in $389,738 of overcharges

Source: http://www.justice.gov/opa/pr/2011/July/11-at-915.html

The Case of Hizzoner’s Corrupt Spouse

Case Study

FRAUD

opportunity

Motive Pressure

Attitude rationalization

The Case of Hizzoner’s Corrupt Spouse

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

Fraud risk factors/indicators

The Case of Hizzoner’s Corrupt Spouse

The Case of the Profitable Internal Service Center

Case Study

2014 GOVERNMENT CONTRACTORS' CONFERENCE

ICF-Kaiser International, Inc

ü In the late 1980s and early 1990s ICF was a major Federal government contractor

ü ICF used an internal service center to provide computer services to its divisions and their employees

ü The computer center charged “customers” at “commercial equivalent” rates

ü Each year, the center reconciled its actual costs with its billings to “customers”

True Story

ICF-Kaiser International, Inc

ü The difference (always an excess of revenues over costs) should have been either (a) credited back to “customers” or (b) credited to an indirect cost pool

ü Instead of booking these credits, ICF recorded the difference as a “contingency”

ü Cotton & Company was the EPA-OIG-assigned cognizant audit firm during the early 1990s

ü During an audit of ICF’s indirect cost rates, C&C asked for and obtained access to ICF’s financial statement auditor’s workpapers

True Story

2014 GOVERNMENT CONTRACTORS' CONFERENCE

ICF-Kaiser International, Inc

ü In reviewing these workpapers, C&C noted the computer service center adjustment included in a workpaper supporting the corporation’s contingent liabilities note disclosure

ü The outside auditors had noted, on this workpaper, that once the government auditors had completed the audit of each year’s indirect cost rates, if they had failed to find the adjustment, that year’s adjustment would be reversed to retained earnings

ü Cotton & Company referred this matter to the EPA IG’s investigators

True Story

ICF-Kaiser International, Inc

ü The EPA IG investigation was completed in 2000

True Story

2014 GOVERNMENT CONTRACTORS' CONFERENCE

From the EPA-IG’s March 2003 Semmiannual Report

During this reporting period, a final estimate of the value of the September 2000 settlement agreement between ICF Kaiser International, Inc., and the United States Attorney’s Office, Eastern District of Virginia, was computed. Based upon the documentation provided by ICF and their representations during the settlement negotiations, the total value of the settlement was placed at $391,061,944.

Under the terms of the settlement agreement, ICF agreed to waive these cost claims, which in turn allowed the government to deobligate retained funds and avoid contract closing costs.

True Story

From the EPA-IG’s March 2003 Semmiannual Report

The settlement agreement was the culmination of a lengthy investigation that disclosed that ICF may have billed government contracts for computer center costs in excess of the costs actually incurred. The EPA and 17 other federal departments/agencies were affected by this settlement.

True Story

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Case Study

FRAUD

opportunity

Motive Pressure

Attitude rationalization

The Case of the Profitable Internal Service Center

Case Study

Fraud risk factors/indicators

The Case of the Profitable Internal Service Center

2014 GOVERNMENT CONTRACTORS' CONFERENCE

Corruption and Fraud—Recommended Additional Reading ü Frankensteins of Fraud: The 20th Century's Top 10 White-Collar Criminals, By Joseph T.

Wells, CFE, CPA [www.marketplace.cfenet.com]

ü Occupational Fraud and Abuse, By Joseph T. Wells, CFE, CPA [www.marketplace.cfenet.com]

ü The Informant: A True Story, By Kurt Eichenwald

ü The Smartest Guys in the Room: The Amazing Rise and Scandalous Fall of Enron, By Bethany McLean and Peter Elkind

ü Conspiracy of Fools: A True Story, By Kurt Eichenwald

ü Final Accounting: Ambition, Greed and the Fall of Arthur Andersen, By Barbara Ley Toffler

ü Inside Arthur Andersen: Shifting Values, Unexpected Consequences, By Susan E. Squires

ü Unaccountable: How the Accounting Profession Forfeited a Public Trust, By Mike Brewster

ü Enron : The Rise and Fall, By Loren Fox

ü Power Failure: The Inside Story of the Collapse of Enron, By Mimi Swartz and Sherron Watkins

ü 24 Days: How Two Wall Street Journal Reporters Uncovered the Lies that Destroyed Faith in Corporate America, By Rebecca Smith and John R. Emshwiller

ü Disconnected: Deceit and Betrayal at WorldCom, By Lynne W. Jeter

The Good, the Bad, & the Ugly: Case Studies in

Contractor Corruption and Fraud

Dave Cotton, CPA, CFE, CGFM Cotton & Company LLP

Alexandria, Virginia www.cottoncpa.com

2014 GOVERNMENT CONTRACTORS' CONFERENCE September 18, 2014