Embed Size (px)

Citation preview

The Pennsylvania State University

The Graduate School

CASE STUDY: AFFECTIVE LEARNING OBJECTIVES WITHIN A WORKFORCE

FINANCIAL LITERACY PROGRAM

A Dissertation in

Workforce Education and Development

by

Brad Lee Yeckley

© 2021 Brad Lee Yeckley

Submitted in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

August 2021

ii

The dissertation of Brad Lee Yeckley was reviewed and approved by the following:

David L. Passmore

Distinguished Professor, Emeritus, of Education

Dissertation Advisor

Chair of Committee

Mark D. Threeton

Associate Professor of Education

Cynthia Pellock

Teaching Professor of Education

Cathy Bowen

Professor of Agricultural and Extension Education

Heather Zimmerman

Director of Graduate Studies

Department of Learning and Performance Systems

iii

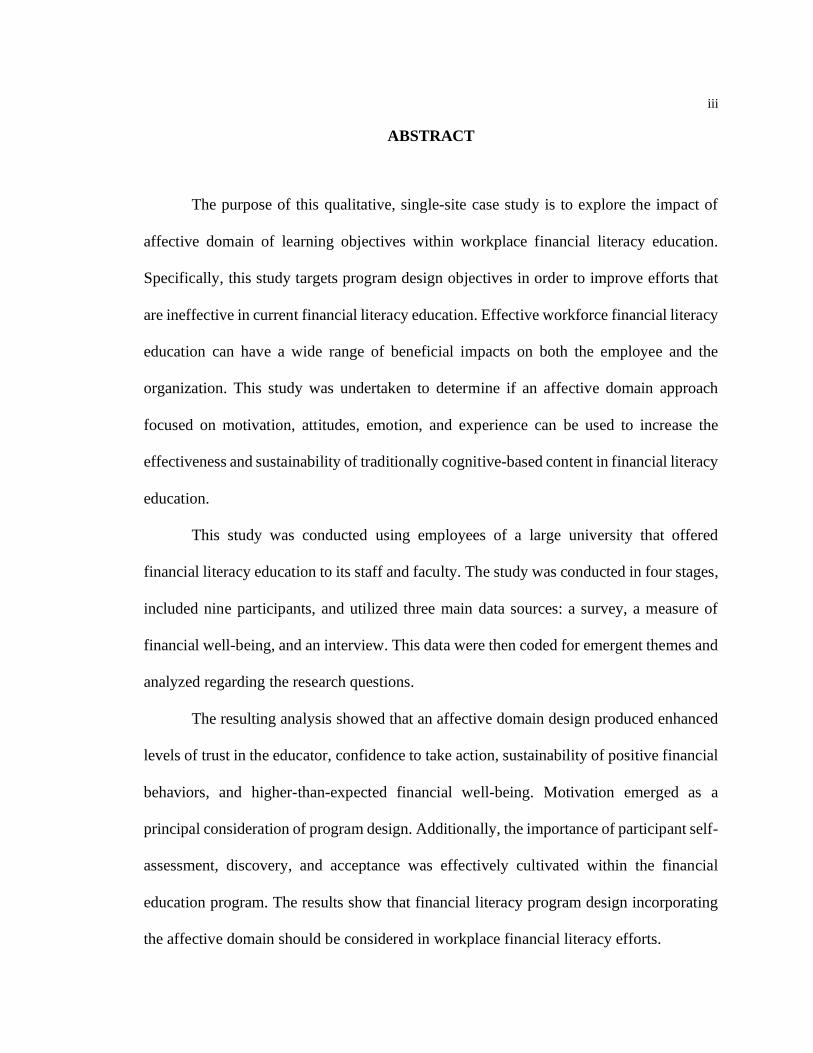

ABSTRACT

The purpose of this qualitative, single-site case study is to explore the impact of

affective domain of learning objectives within workplace financial literacy education.

Specifically, this study targets program design objectives in order to improve efforts that

are ineffective in current financial literacy education. Effective workforce financial literacy

education can have a wide range of beneficial impacts on both the employee and the

organization. This study was undertaken to determine if an affective domain approach

focused on motivation, attitudes, emotion, and experience can be used to increase the

effectiveness and sustainability of traditionally cognitive-based content in financial literacy

education.

This study was conducted using employees of a large university that offered

financial literacy education to its staff and faculty. The study was conducted in four stages,

included nine participants, and utilized three main data sources: a survey, a measure of

financial well-being, and an interview. This data were then coded for emergent themes and

analyzed regarding the research questions.

The resulting analysis showed that an affective domain design produced enhanced

levels of trust in the educator, confidence to take action, sustainability of positive financial

behaviors, and higher-than-expected financial well-being. Motivation emerged as a

principal consideration of program design. Additionally, the importance of participant self-

assessment, discovery, and acceptance was effectively cultivated within the financial

education program. The results show that financial literacy program design incorporating

the affective domain should be considered in workplace financial literacy efforts.

iv

TABLE OF CONTENTS

LIST OF FIGURES ..................................................................................................... vi

LIST OF TABLES ....................................................................................................... vii

ACKNOWLEDGEMENTS ......................................................................................... viii

Chapter 1 Introduction ................................................................................................ 1

Historical Perspective ........................................................................................... 2 Statement of the Problem ...................................................................................... 7 Purpose of the Study ............................................................................................. 10 Research Questions ............................................................................................... 12 Summary ............................................................................................................... 12

Chapter 2 Review of Related Literature ..................................................................... 14

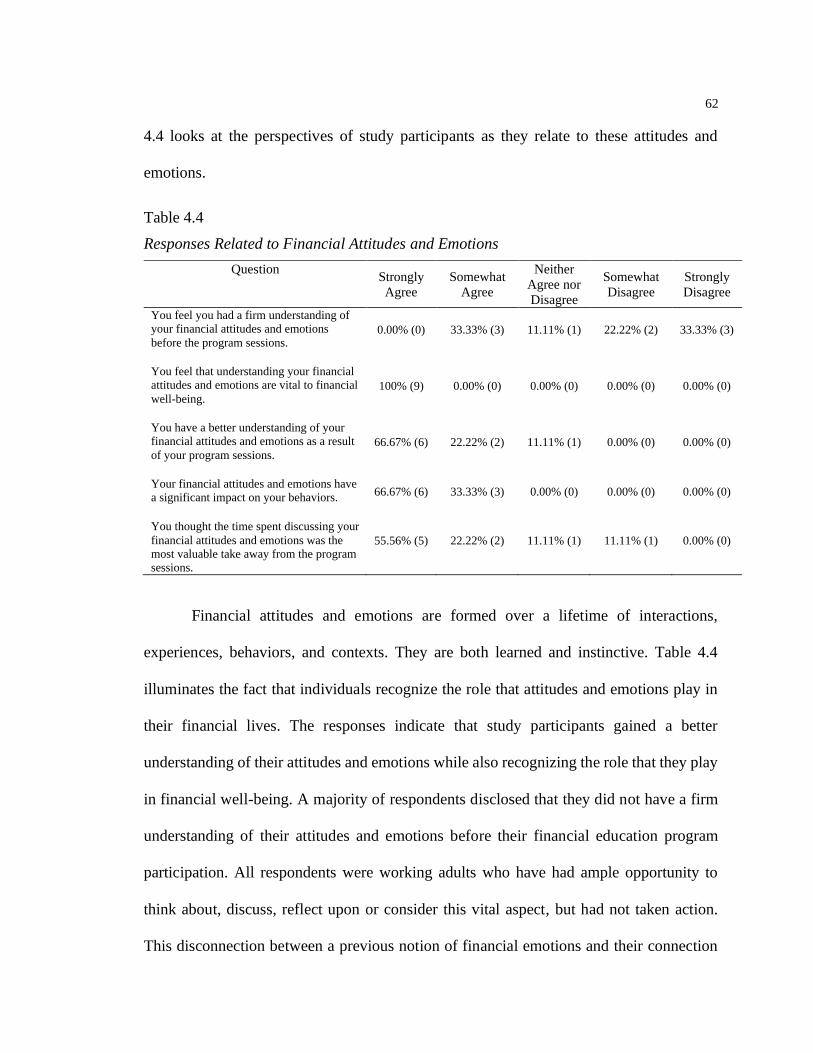

The Need for Workforce Financial Literacy Education ....................................... 14 Evaluation of Existing Financial Literacy Education Efforts ............................... 15 Developmental Psychology and Financial Decision-Making ............................... 17 Cognitive and Affective Domain Learning Outcomes ......................................... 19 Summary ............................................................................................................... 22

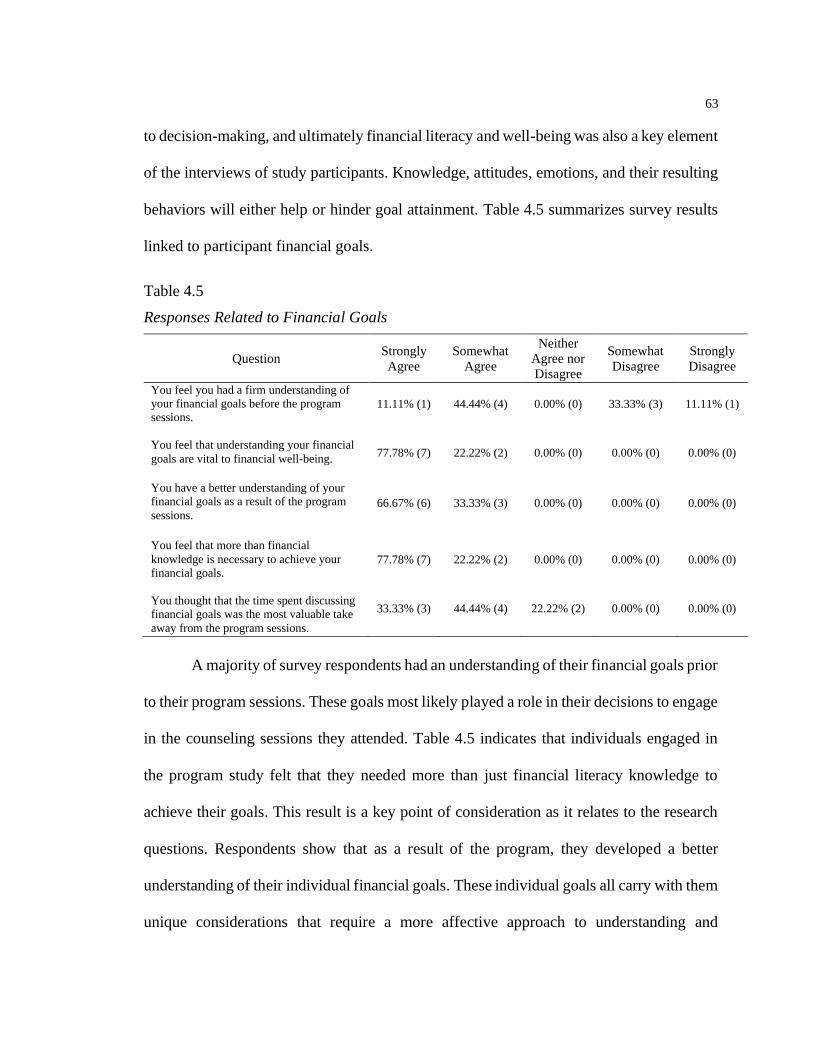

Chapter 3 Method ....................................................................................................... 23

Qualitative Overview ............................................................................................ 23 Study Design ......................................................................................................... 24 Research Study Project Template ......................................................................... 27 Data Collection Procedures .................................................................................. 28 Participants and Sampling .................................................................................... 30 Process of Data Analysis ...................................................................................... 31 Validity and Reliability Concerns of Qualitative Inquiry ..................................... 34 Credibility and Trustworthiness ........................................................................... 36 Reflexivity ............................................................................................................ 37 Limitations ............................................................................................................ 38 Summary ............................................................................................................... 39

Chapter 4 Findings ...................................................................................................... 41

Description of the Program Setting ...................................................................... 42 Study Participants ................................................................................................. 44

Participant 1 ................................................................................................... 44 Participant 2 ................................................................................................... 47

v

Participant 3 ................................................................................................... 47 Participant 4 ................................................................................................... 48 Participant 5 ................................................................................................... 51 Participant 6 ................................................................................................... 52 Participant 7 ................................................................................................... 54 Participant 8 ................................................................................................... 55 Participant 9 ................................................................................................... 57

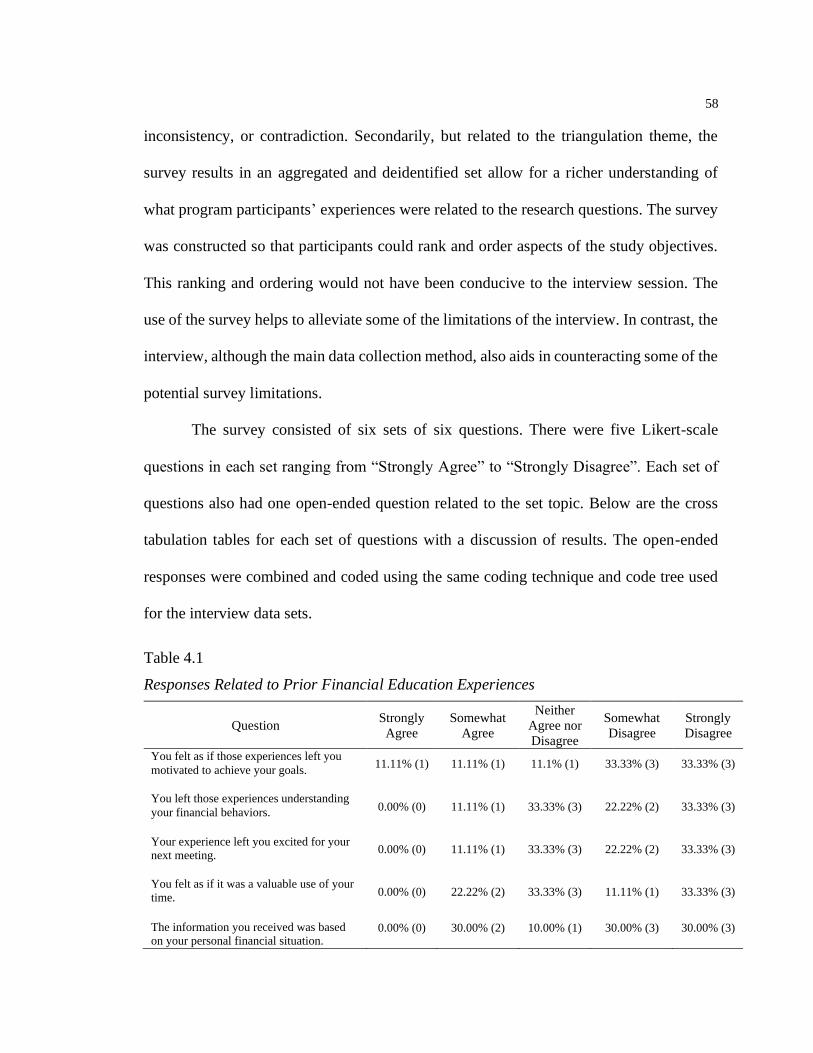

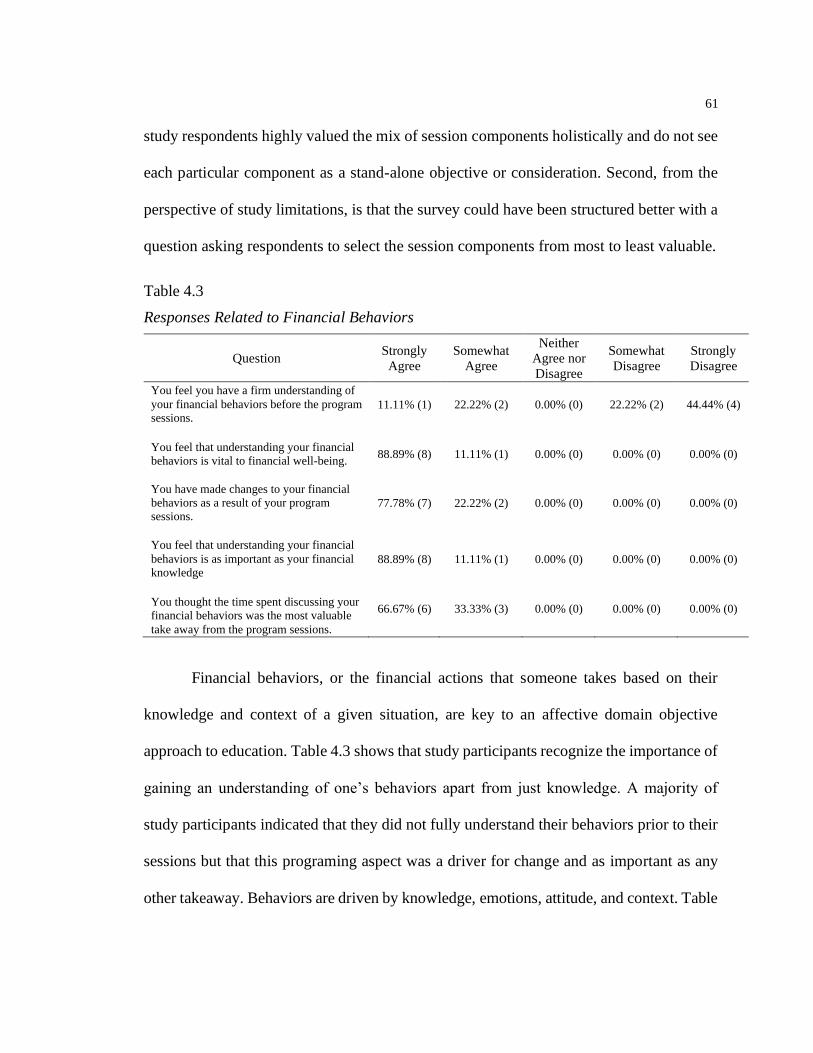

Aggregated Survey Results ................................................................................... 57 Theme 1: Participant Perspectives About Understanding Financial Behaviors

and Habits and the Impact on Financial Well-being ..................................... 65 Theme 2: Participant Reactions About the Financial Education Program and

the Effect on Consumers Financial Protection Bureau Financial Well-

Being Questionnaire Score ............................................................................ 70 Theme 3: Participant Perspectives About Motivation in Financial Literacy

and Well-being Education ............................................................................. 74 Summary ............................................................................................................... 79

Chapter 5 Discussion, Recommendations, and Conclusion........................................ 81

Discussion ............................................................................................................. 82 Theme 1: Behavior ........................................................................................ 82 Theme 2: Well-being Measurement .............................................................. 86 Theme 3: Motivation ..................................................................................... 89

Recommendations ................................................................................................. 92 Recommendation 1: Include a behavioral finance component in

programs ................................................................................................. 92 Recommendation 2: Limit knowledge-based content to what is a current

priority .................................................................................................... 93 Recommendation 3: Make personalized motivation a priority of the

experience ............................................................................................... 94 Recommendation for Future Research ................................................................. 95 Conclusion ............................................................................................................ 96

References .................................................................................................................... 99

Appendix A CFPB Long Form Financial Wellness Questionnaire ............................ 105

Appendix B Interview Protocol .................................................................................. 108

Appendix C Code Tree ............................................................................................... 113

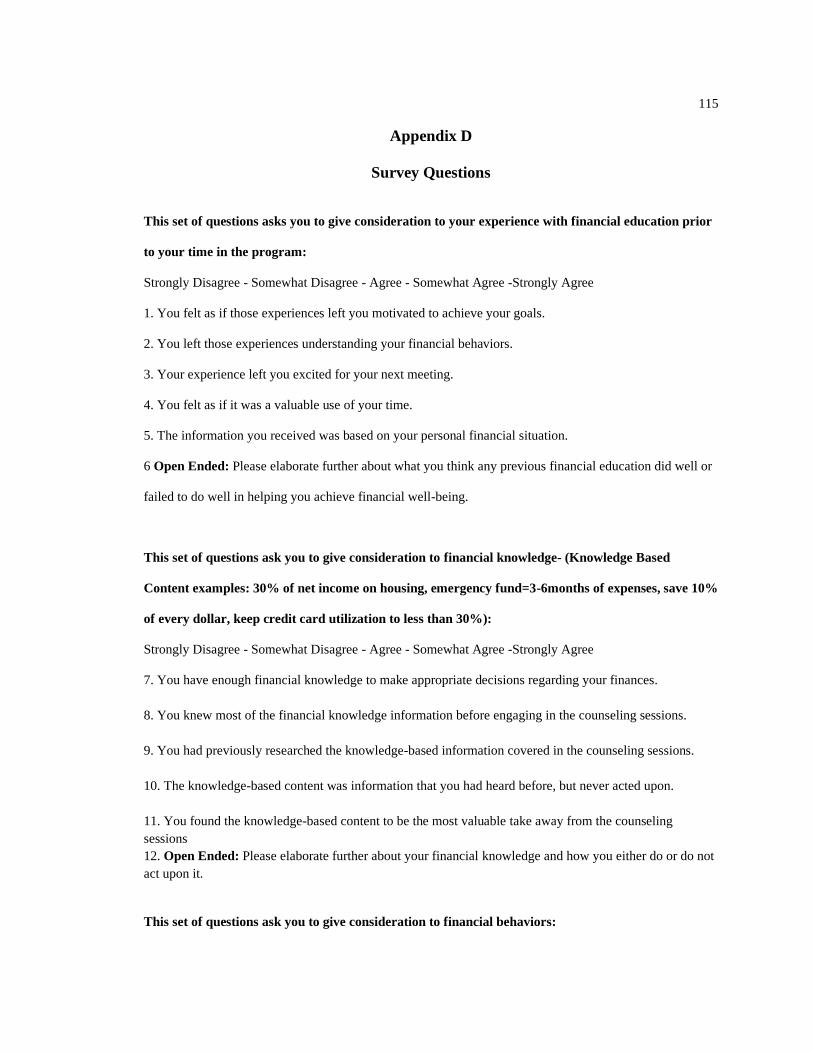

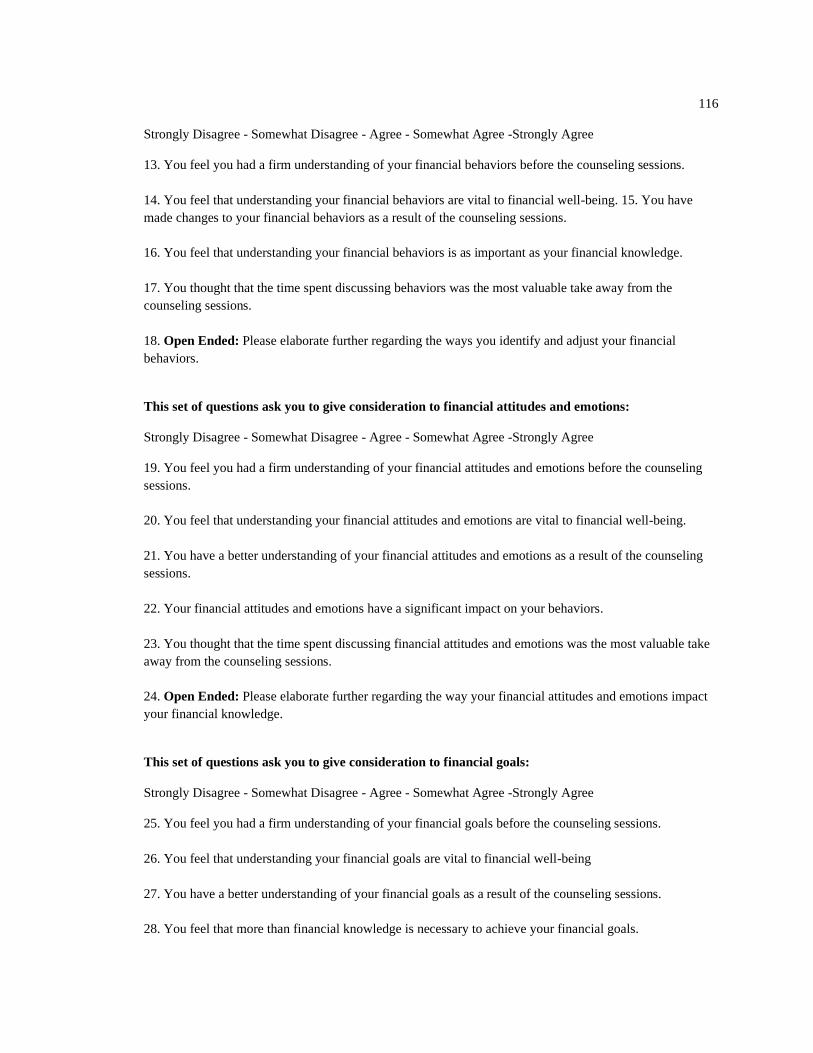

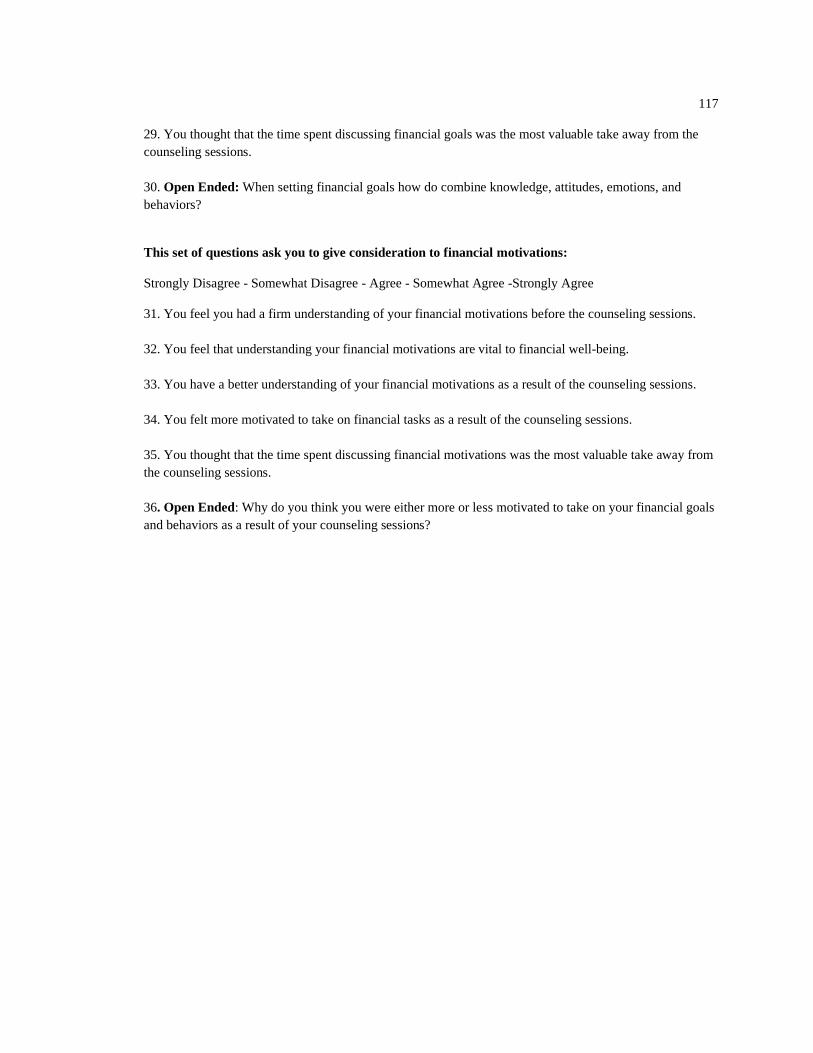

Appendix D Survey Questions.................................................................................... 115

Appendix E Institutional Review Board Determination ............................................. 118

vi

LIST OF FIGURES

Figure 1.0. Multi-step process of workforce financial literacy education. .................. 9

Figure 2.0. Ecological Model for Financial Literacy Education (Adapted from

Way, 2014, p. 29). ................................................................................................ 21

Figure 3.0. Basic Types of Designs for Case Studies (Adapted from Yin, 2012, p.

8) ........................................................................................................................... 26

vii

LIST OF TABLES

Table 4.1 Responses Related to Prior Financial Education Experiences..................... 58

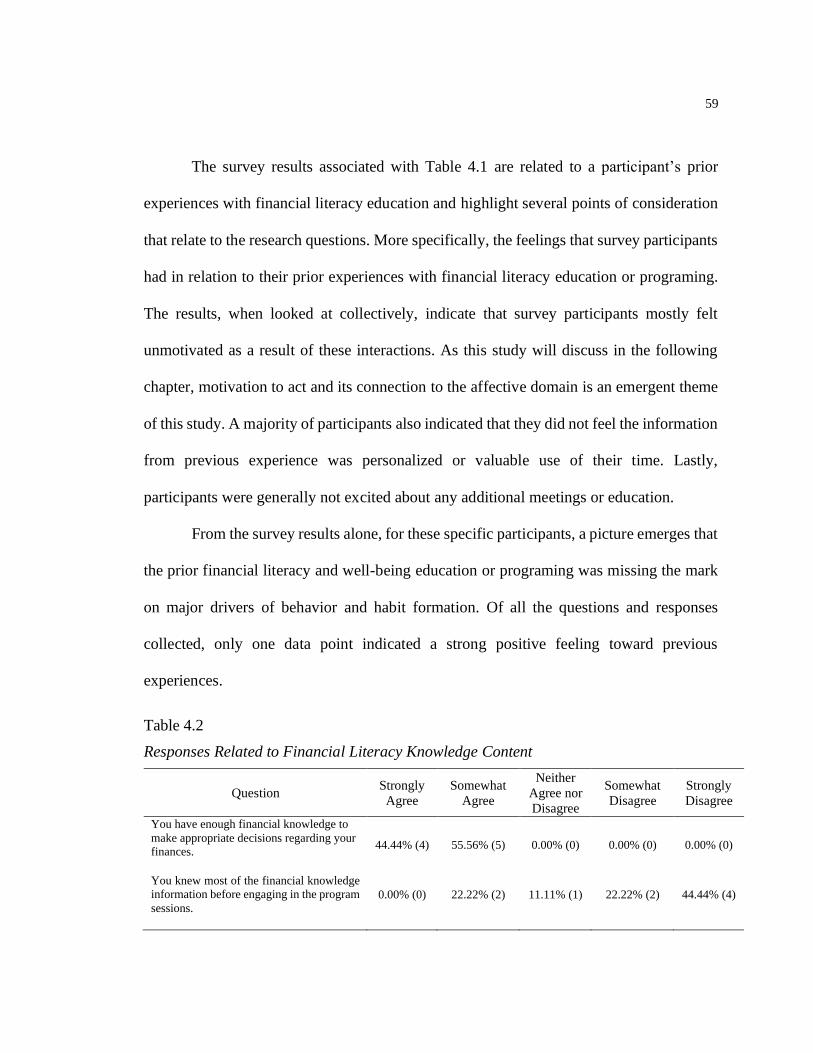

Table 4.2 Responses Related to Financial Literacy Knowledge Content .................... 59

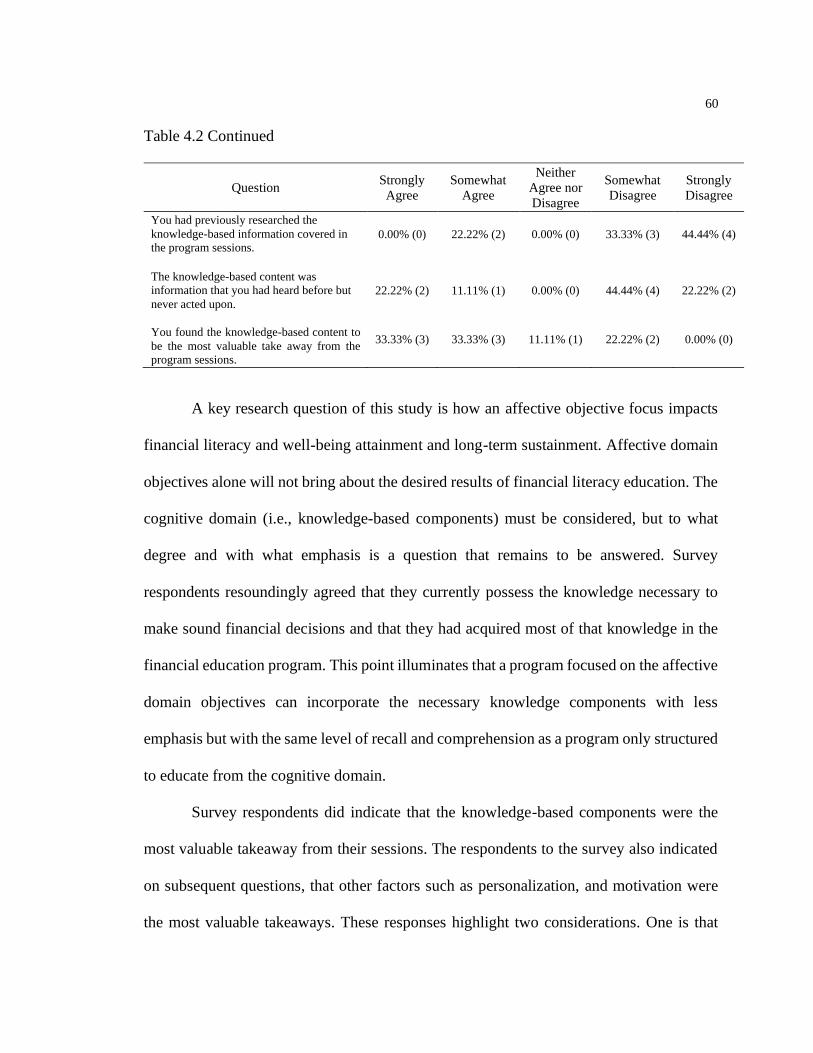

Table 4.3 Responses Related to Financial Behaviors .................................................. 61

Table 4.4 Responses Related to Financial Attitudes and Emotions............................. 62

Table 4.5 Responses Related to Financial Goals ......................................................... 63

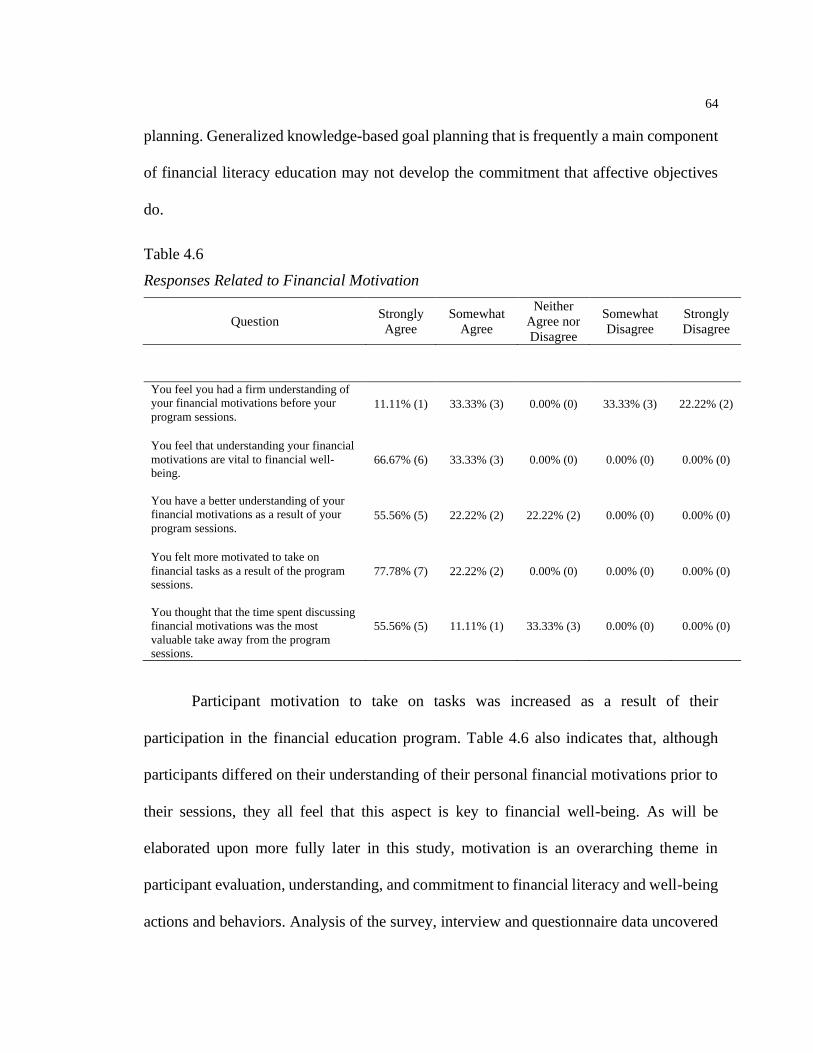

Table 4.6 Responses Related to Financial Motivation................................................. 64

viii

ACKNOWLEDGEMENTS

I would like to express my deepest gratitude to the Pennsylvania State University

and the University of North Carolina Charlotte: two institutions that provided the space to

develop programs that are designed a bit differently than most.

To my committee, I want to say thank you. Dr. Pellock, your commitment to CTE

work provided me the curiosity to explore financial literacy outside of the higher education

setting. Dr. Threeton, without a serendipitous meeting with you, I may have never even

considered the affective domain. Thank you for putting the theory to my vision. Dr. Bowen,

the respect I have for you cannot be overstated. You have been in my corner from the start

and have always been an inspiration. Lastly, Dr. Passmore. Your steadfast commitment to

making sure that I find my own answers has allowed me to do more than I imagined. Thank

you for the nudges, redirections, and reminders to stay with the grind.

To Allie and Lex, thank you for believing in my vision of how a program should

look and for your commitment to the possibility that we could do better.

Lastly, to Katie and Mia, I want to say more than thank you. Making the two of you

proud is always on my mind. But more so than that, your encouragement, sacrifices,

guidance, humor, help, and commitment allowed me to do this. This dissertation is as much

yours as it is mime.

1

Chapter 1

Introduction

This chapter elaborates upon the historical underpinnings of the need for financial

literacy education and how financial literacy education and programing have been

delivered. Explanation of the factors that lead to the effectiveness of such education is

considered and then developed into a set of research questions that guided the study.

Financial literacy education and programing are any intervention designed,

deployed, and evaluated to help individuals make decisions and adjust behaviors that, in

turn, lead to higher levels of personal financial security and wellness. Education consists

of the concepts, competencies, and skills necessary to make financial decisions.

Programing is the method of delivering that education to participants. In a U.S.

Government Accountability Office Highlights publication from 2011, it was found that

employers are positioned such that they can impact not only individuals but increase

organizational effectiveness through financial literacy education and programing.

Organizational commitment to a more financially fit workforce, coupled with effective

programing efforts, may be part of the solution to an issue that has been gaining steam for

some time now, coupling individual and organizational well-being. This research posits

that the development and deployment of these impactful programing efforts be explored in

greater detail.

2

Historical Perspective

Many factors, including employee satisfaction, drive organizational effectiveness

and company profitability. Kim and Garman (2004) report that employees experiencing

financial stress at work have lower overall levels of satisfaction and more negatively

skewed attitudes toward the organizations in which they work. These facts highlight the

relationship between employee satisfaction and successful financial literacy education.

Successful financial literacy programs are ones that have measurable outcomes, stimulate

behavioral change, are comprehensive in scope, and engage participants in ways that

produce long-term habits. Implementing effective and sustainable workforce financial

literacy programing and education has the potential to positively affect organizational

effectiveness, productivity, profitability, engagement, turnover, health, loyalty, and

organizational culture (Joo & Garman, 1998; Kadlec, 2012; Kim & Garman, 2004). These

potential positive effects ultimately become drivers of employees’ safety, job performance,

retention, and health care costs. The employee engagement gap alone, according to Saks

(2006), “is costing U.S. businesses $300 billion a year in lost productivity” (p. 600). While

the engagement gap is only one measure that improved financial literacy may help to offset,

it is one that could make better financial literacy education and programing a value-added

employee benefit. Remund (2010) conceptualizes financial literacy by stating:

Financial literacy is a measure of the degree to which one understands key

financial concepts and possesses the ability and confidence to manage

personal finances through appropriate, short-term decision-making and

sound, long-range financial planning, while mindful of life events and

changing economic conditions. (p. 284)

3

This definition serves well to explain the desired outcomes and behaviors associated with

financial literacy programing, education, and assessment. Throughout the United States,

these outcomes are pursued by schools, universities, employers, community organizations,

and financial service providers. The direct and opportunity costs of this programing could

be in the billions of dollars. However, verifiable costs on a national scale are currently not

available. The effectiveness of this programing and education has been marginally

successful at best, showing “that interventions to improve financial literacy explain only

0.1% of the variance in financial behaviors studied” (Fernandes, Lynch, & Netemeyer,

2014, p. 1). The meta-analysis conducted by Fernandes, Lynch, and Netemeyer (2014)

studying the effectiveness of financial literacy programing and education and covering

10,650 articles, 168 published papers, and 201 non-redundant studies further states that

“What is unclear is why educational interventions investigated thus far have been

unsuccessful” (p. 30).

There exist substantial research and literature regarding financial literacy concepts,

knowledge, programing, education, and assessment (both intervention-based and

measurement-based). A deficiency does, however, exist in determining the most beneficial

methodology for effective and sustainable financial literacy skill acquisition and

deployment. The existing research addresses what should be taught but falls short on how

it should be taught. Standard financial literacy programing and education typically focus

on rote learning of financial literacy content and what Bloom, Englehart, Furst, Hill, and

Krathwohl (1956) defined as the cognitive domain of learning. These two areas attend to

knowledge and concrete concepts related to financial literacy and have been the foundation

of most programing and education. Reliance on only the knowledge necessary to make

4

informed decisions, its deployment, and its measurement without consideration of the

emotional and attitudinal aspects of the learning process may limit the effectiveness of

financial education and programing efforts.

Goodwin, Harris, Nelson, Roach, and Torras (2019) explain that the neoclassical

view of rational choice theory contends that an individual given an economic decision will

always make prudent decisions giving them the highest level of benefit. With the growth

and development of the field of behavioral economics, rational choice theory has been

widely disputed. As Zeckhauser (1986) points out, “Nonrational behavior in economics is

a bit like an optical illusion. Just as you cannot always trust your eyes, you cannot always

trust your behavior to be rational” (p. s440). Examples abound of individuals, groups, and

organizations making irrational economic choices. Whether they are in the pursuit of

immediate gratification, rely too heavily on heuristics, or have skewed intrinsic value

judgments, greed, or apathy, these decisions are made even though the needed knowledge

and concrete concepts are available. By combining knowledge with attention to the

emotional and attitudinal orientation of those receiving instruction, financial literacy

instruction potentially becomes more impactful.

The need for increased levels of financial literacy is not a new topic, but it is

increasingly becoming more imperative across the United States, as studies have shown

that financial literacy among the general population is lacking. Numerous organizations

and non-profits, including the President’s Advisory Council on Financial Literacy (2008),

have come to the same conclusion; that Americans lack the basic skills necessary to make

sound financial decisions. These skills are necessary for successful navigation of everyday

life and become even more critical in times of economic or organizational downturn.

5

This governmental thinking is nothing new. A letter to Thomas Jefferson, dated

August 23, 1787, shows that, over 200 years ago, John Adams recognized the need for

financial literacy: “All the perplexities, confusions, and distresses in America arise, not

from defects in their constitution or confederation, not from a want of honor or virtue, so

much as from downright ignorance of the nature of coin, credit, and circulation” (To

Thomas Jefferson, 1787). These sentiments echo today. Organizations had looked the other

way when it comes to providing employees a base of individual financial literacy and,

finally, it seems as though these times are changing.

Much like the paradigm shift that began to take place after World War II in thinking

about employees’ physical and emotional health, organizations have begun to pay attention

to the cost of having a financially "unfit" workforce. Is this financial literacy education

happening correctly, though? Large-scale organizational losses can happen in the smallest

of increments. For example, lost productivity and time slippage have an effect on all

organizations. Kadlec (2012) estimates that American workers may be spending twenty-

eight hours per month researching personal financial topics while at work. Each of these

lost labor hours has a direct impact on organizational effectiveness and profitability.

Additionally, Financial Stress Research (Financial Finesse, 2016) reported that

85% of employees surveyed in the United States are experiencing at least some financial

stress and that 25% feel that their stress is overwhelming. This report uses a data set “based

primarily on the analysis of 35,703 financial wellness assessments completed January 1,

2014, through December 31, 2015” (Financial Finesse, 2016, p. 16). Given the list of

detrimental outcomes associated with even moderate stress levels, it is not a reach to

conclude that organizations and employers should be making the reduction of financial

6

stress a priority moving forward. As Calnan (2014) found in a survey of employers in the

United Kingdom, over half of the employers do not provide financial literacy education,

even though 73% of the employees have stated that it boosts productivity, and more than

half of those surveyed stated that they had requested some kind of financial education at

work.

A deficiency exists given the history of financial literacy education, the current

methods for deployment of that education, and the research concerning the marginally

effective outcomes associated with such programing. Research focused on the outcomes

and sustainability of a model focused on individual attitudes, emotions, motivations, and

internalizations may help fill in gaps in the existing literature. This research may also

improve not only individual and organizational outcomes but may serve as a best practice

holistically.

The development of best practices becomes increasingly important when a current

intervention or outcome-based educational program is failing to deliver desired outcomes.

The documented level of financial illiteracy among diverse groups has shown that this

indeed is the case. As early as 2005, the Organization for Economic Co-operation and

Development (OECD) had been working to address the pervasive levels of financial

illiteracy by publishing and analyzing policy issues surrounding the effectiveness of

international financial literacy education programs. Numerous other studies have also

concluded that Americans especially are not equipped to or lack the commitment to making

sound financial decisions (Chen & Volpe, 1998; Volpe, Chen, & Liu, 2006; Volpe, Chen,

& Pavlicko, 1996). These findings highlight a need to explore in more detail what may be

7

causing continued low levels of financial literacy during a period where the need for and

access to education has been made a priority.

Statement of the Problem

Although there may be several potential reasons for the inability of traditional

financial literacy interventions to increase the measurable outcomes desired, this

dissertation research is focused on one reason in particular. This research concentrates on

the distinction between cognitive-based learning outcomes and affective-based learning

outcomes associated with financial literacy education and programing in a workforce

setting. As Bloom, Krathwohl, and Masia (1964) point out in the early categorizations of

learning domains and how they impact the study of educational programs as a whole:

If programs have similar objectives, do they involve similar or different

learning experiences? The classifications could be used as tools in clarifying

and organizing educational research results. What types of educational

experiences produce what types of educational development? What types

of educational development are well retained and what types are not? (pp.

5-6)

By focusing on the learning domains and their respective learning outcomes within the

context of financial literacy education, and comparing the results of the differing

perspectives, there may be room for the development of, and adherence to, a set of best

practices and recommendations. This new focus allows for a more uniform approach to

financial literacy education. Even if these distinctions can be drawn, it is difficult to draw

conclusions that are generalizable due to the fact that “relatively few evidence-based

evaluations of financial literacy programs have been conducted, limiting what is known

about which specific methods and strategies are most effective” (Government

8

Accountability Office, 2011). Lending significance to the study of how affective domain

learning outcomes can impact the effectiveness of educational objectives is the tendency

for a majority of evaluated learning objectives to fall into the cognitive domain, as they are

easier to measure. Krathwohl et al. (1964) point out that when looking at cognitive domain

objectives that “the largest proportion of educational objectives fell into this domain” (p.

6). Additionally, the Consumer Financial Protection Bureau (CFPB) (2015) stated:

With rare exceptions, financial knowledge has typically been defined only

in terms of factual knowledge of specific financial concepts or as specific

levels of numeracy. Only a handful of studies have looked at how different

types of financial knowledge influence financial behavior or what

circumstances either limit or catalyze the translation of financial knowledge

into behaviors conducive to financial well-being. Overall, we found

understanding of financial well-being to be very limited. (p. 14)

Given the lack of research and literature that explicitly targets financial literacy education

programs that highlight objectives outside of the cognitive domain, there exists a gap in

the current understanding of financial literacy programs.

This gap can only be addressed by first outlining the differences between the two

domains of learning. The cognitive domain traditionally has been based on a learner’s

capacity to remember and process information while the affective domain relies more

heavily on the learner’s attitudes and feelings that are part of the learning process. It could

be argued that without cognitive-based knowledge objectives, affective objectives focused

on attitudes, feelings, and internalized motivations do not matter. It does no good to

motivate an individual to shift their attitude toward keeping a weekly budget or managing

their credit rating if they are not, in conjunction, provided with the concepts, facts, and

knowledge to carry out these newly developed attitudes. This fact is not the argument

presented in this research. The focus of this research leans more heavily on the potential

9

shift toward affective objectives as the precursor to the cognitive ends. This shift may

potentially engage the learner in a manner that instills sustainability and internalization of

responsibility, motivation, and accountability for financial behaviors. Krathwohl et al.

(1964) point out:

As viewed from the cognitive pole, the student may be treated as an

analytical machine, a “computer” that solves problems. In contrast, viewed

from the affective pole, we take greater cognizance of the motivation, drive,

and emotions that are factors bringing about achievement of cognitive

behavior. (p. 57)

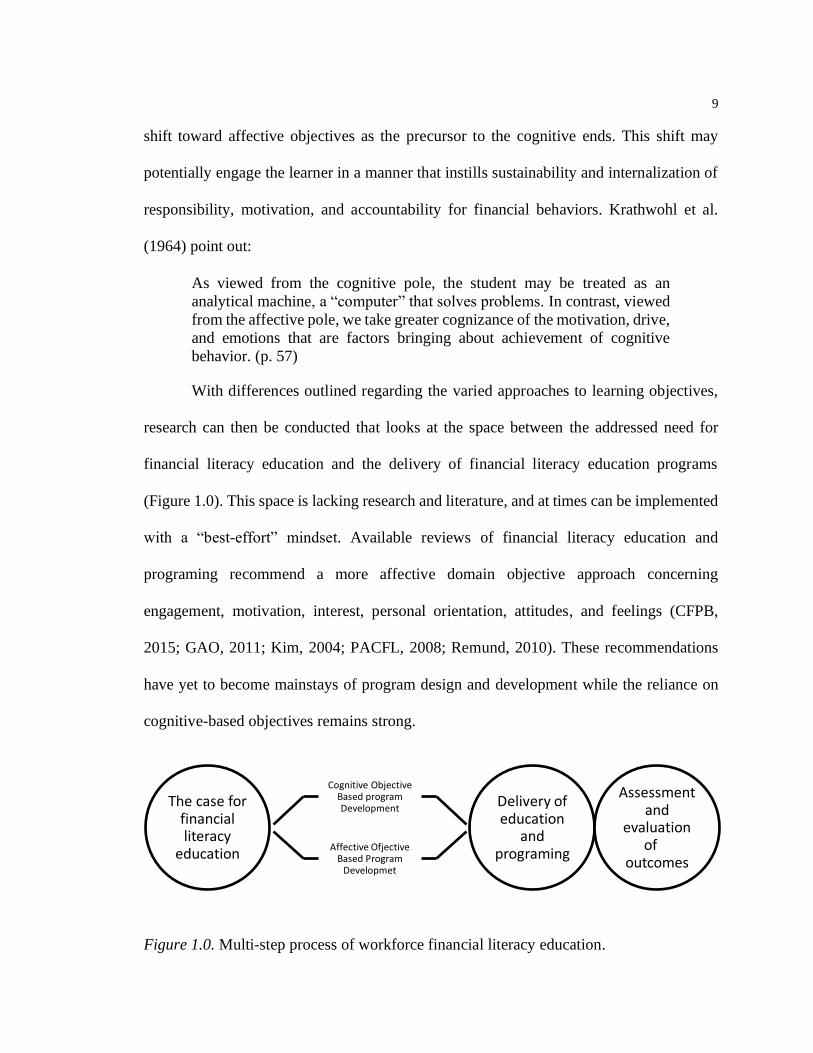

With differences outlined regarding the varied approaches to learning objectives,

research can then be conducted that looks at the space between the addressed need for

financial literacy education and the delivery of financial literacy education programs

(Figure 1.0). This space is lacking research and literature, and at times can be implemented

with a “best-effort” mindset. Available reviews of financial literacy education and

programing recommend a more affective domain objective approach concerning

engagement, motivation, interest, personal orientation, attitudes, and feelings (CFPB,

2015; GAO, 2011; Kim, 2004; PACFL, 2008; Remund, 2010). These recommendations

have yet to become mainstays of program design and development while the reliance on

cognitive-based objectives remains strong.

Figure 1.0. Multi-step process of workforce financial literacy education.

The case for financial literacy

education

Cognitive Objective Based program Development

Affective Ofjective Based Program

Developmet

Delivery of education

and programing

Assessment and

evaluation of

outcomes

10

By breaking down this space between the need for and the delivery of education

and programing, a comparison can then be drawn based on results of already available data

regarding traditionally cognitive objective-based education and programs that have taken

a more affective domain objective approach. The resulting research could then be used to

determine the best design methodology for financial education programs that are being

considered or that are in the development stage.

The CPFB (2015) found that personal attitudes and beliefs, non-cognitive skills,

and personality traits all influence financial behavior and play a role in mediating the

connection between knowledge and behavior. Research and evaluation should be

undertaken that aids in the illumination of these factors that influence behavior and aids in

the synthesis of knowledge, financial skills, and behavior. Without a body of research and

literature addressing these factors and how they integrate into the development of financial

literacy education programs, a blind spot may continue to exist, inhibiting the enhancement

of and efficacy of this type of educational programing.

Purpose of the Study

This research intends to explore and examine the dynamics associated with a

financial literacy education program that includes affective learning objectives as a critical

driver of success. This study involves financial literacy program participants at an

organization that provides optional financial literacy education to their employees.

Through analysis of interview, survey, and questionnaire responses of a criterion sample

of program participants, a narrative was then constructed with regard to program

11

effectiveness, efficacy, and sustainability. The resulting outcomes can then be used to aid

in the development and implementation of financial literacy education programing.

Financial literacy education has multiple sets of standards surrounding what should

be taught and what outcomes should be set as goals. The Institute for Financial Literacy

(IFL), Department of Treasury, The JumpStart Coalition, Council for Economic Education,

Programme for International Student Assessment (PISA), and the National Endowment for

Financial Education (NEFE) have all provided definitions of financial literacy and

standards based on content, competencies, and materials. None have yet developed

comprehensive suggestions regarding how to deliver their recommendations effectively.

Only the National Financial Educators Council (NFEC) (2018) has advocated for

implementing a psychological component to their overall definition of financial literacy

education. The NFEC states that the direct link between a person’s money and their

emotional state justifies inclusion of this component in the definition of financial literacy.

The body of existing literature covering not only program design and delivery, but

the type of learning objectives these programs intend to deliver, is limited at best. This

limitation was addressed and analyzed within this research study. An evaluation of

outcomes associated with a more affective objective learning approach is also provided by

attempting to gain insight and knowledge centered on three main research questions. By

attempting to answer these three research questions, this study works to uncover and reveal

a narrative with regard to how affective learning objectives impact the delivery and efficacy

of financial literacy education.

12

Research Questions

Three research questions were undertaken during this study. One is based on a broader

conceptualization of the program being studied, while the remaining two are more focused

in nature.

1. What are the perspectives of individuals who have been engaged in an

affective learning objective-based financial literacy education program

with regard to financial knowledge, behaviors, and decision-making?

2. How do the individuals who have been part of an affective learning

objective program score on a nationally recognized measure of financial

well-being and how do they interpret their results?

3. Does a focus on the affective learning outcomes change the attitudes,

emotions, and motivations that participants have regarding financial

tasks and goals?

Summary

This chapter serves to highlight the existing efforts being put forth in the

advancement of a more financially literate and educated public, while also lending

credibility to the fact that these efforts may be designed and implemented in a less than

optimal manner. Also discussed was an introduction to a way of looking at desired

outcomes that have been generally overlooked. Finally, three research questions

surrounding the exploration of these desired outcomes with regard to attitudes, emotions,

motivations, and internalizations were presented. Chapter 2 takes these components and

13

applies them to the existing literature and research in order to build a case for further

exploration of the research questions.

14

Chapter 2

Review of Related Literature

When building a case for this study it is important to consider three areas of existing

literature that play a role in the proposed research. First, the overall need for financial

literacy will be reviewed, and the effectiveness of existing financial literacy efforts will be

discussed. Focus will then shift to two areas specific to the research questions and the

proposed focus on attitudes, emotions, motivations, and internalizations. An exploration of

developmental psychology and financial decision-making is a central tenant of this study

and is also reviewed. Lastly, a comparison between the cognitive and affective learning

domains is discussed and expanded upon.

The Need for Workforce Financial Literacy Education

Financial literacy is an important factor for anyone interested in increased

productivity, engagement, and efficiencies of labor markets for several reasons. As

Michaud (2017) points out, there are considerations to be made when a particular labor

market suffers from financial illiteracy. Workers in these labor markets may be financially

distressed. This then leads to losses in productivity and increases in absenteeism. Workers

may have to work longer to accumulate retirement income, and they may not fully

understand an organization or firm’s financial situation during downturns. Garman, Camp,

Kim, Bagwell, Redican, and Baffi (1999) find that individuals who are dealing with

financial strains or stressors often also report that their health is suffering as a result. These

health consequences manifest in many ways, including depression, mood swings, apathy,

15

physical maladies, and emotional irregularities (Goetzel & Ozminkowski, 1999). Kim

(2004) goes further in noting that “financial stress has been shown to have a number of

negative effects on individual and family well-being. Specifically, financial strain has been

linked to depression, anxiety, marital conflict, alcoholism, and drug abuse” (p. 2). These

adverse outcomes associated with financial stress can play a direct role in employee

performance, engagement, and productivity. Estimates are that between ten and fifteen

percent of the American workforce is experiencing a reduction in productivity due to

financial stress (Brown, 1993; Garman, Leech, & Grable, 1996).

Evaluation of Existing Financial Literacy Education Efforts

Kim (2004) discussed the increased need for a more robust examination of

workplace financial education efforts:

There is currently a strong need for more empirical research examining the

impact of different types of workplace financial education on employees’

personal finances. Existing studies have been limited primarily to the effects

of financial programs on investments or retirement savings as their

programs are often limited to such topics. Most of the studies in this area

investigated one or two one-time retirement seminars provided by

employers. (p. 3)

Reviews of the existing literature available that directly assess the outcomes or effects of

financial literacy education efforts carry limitations when considered from a delivery and

development perspective. Typical examination of the impact of this type of education does

produce recommendations that fall in line with affective learning objectives (attitudes,

emotions, interests, and motivations). However, they are usually presented as future

considerations or recommendations, not as a direct and purposeful analysis of the learning

outcomes or objectives of the program. Lusardi and Mitchell (2014) have produced a

16

summary of existing education efforts and have determined that little has been learned

about the effectiveness of financial education programs, despite widespread popularity.

Hogarth (2006) and Martin (2007) presented a slightly more optimistic view of financial

literacy education in their reviews of available studies, although both cautiously contained

their optimism that education efforts were effective.

Other reviews of prior literature and studies carry with them a less favorable

evaluation. It has been contended in a number of studies that there is little evidence that

financial education affects behavior, that more rigorous evaluation is needed, and that

many programs carry design flaws resulting in weak effectiveness (Caskey, 2006;

Hathaway & Khatiwada, 2008; Willis 2008a, 2008b). The issues arising from program

design flaws are of value to this research study. By focusing on the program design and not

just content, effectiveness may be greatly increased. Collins and O’Rourke (2010)

conducted a large-scale evaluation of financial education programs and found that only

eleven out of forty-one addressed any predetermined theory or framework.

The current standard for financial literacy measurement is the Lusardi and Mitchell

questionnaire developed in 2004. This measurement tool specifically addresses the topics

of interest, inflation, and risk and is a good measure of knowledge, but not necessarily

behavior. As Hastings, Madrian, and Skimmyhorn (2013) have expressed:

Although Lusardi & Mitchell’s Big Three questions from the 2004 HRS

have quickly become an international standard in assessing financial

literacy, there is remarkably little evidence on whether this set of survey

questions is the best approach, or even a superior approach, to measuring

financial literacy. The question of how best to assess the desired behavioral

capabilities remains open. (p. 355)

Given the lack of consensus regarding the outcomes associated with financial

literacy education, the unknown best practices in program development, and concerns

17

regarding the current methods of measuring financial literacy, it could be concluded that

there is room for research and evaluation at every level of financial literacy education.

Mandell and Klein (2009) point out that research efforts should be focused on the

understanding and determination of teaching methods that elicit the most desirable

financial decision-making capabilities. This proposal now turns its focus to the financial

decision-making process and its psychological underpinnings.

Developmental Psychology and Financial Decision-Making

With available research and evaluation regarding financial literacy education

having determined that achievement of desirable behavioral outcomes is limited at best, it

becomes advantageous to look at the development and design of these education programs.

A financial literacy program should begin with an understanding of developmental

psychology and financial decision-making processes. As Collins and O’Rourke (2010)

indicated, there is a lack of guiding theory in the literature, and most studies fail to carry

with them sound theoretical underpinnings.

Mitigating the shortcomings found in current educational programs starts with an

approach that more adequately addresses components of developmental psychology and

financial decision-making. As Tokar (2015) points out, “what is clear from the analysis,

however, is that financial literacy encapsulates more than just numeracy knowledge” (p.

114). In the same study, Tokar proposed that confidence is as necessary as the knowledge

component within any financial literacy education program and that this realization can

lead to better financial decision-making.

18

If an understanding of the differences between the current focus of financial literacy

education programs and the proposition that more focus should be applied to

developmental psychology and the financial decision-making process can be reached,

successful outcomes can be realized. As Zeckhauser (1986) stated in his findings on the

matter, “Success will mean that we can systematically employ our understanding of

psychology to make nonobvious predictions about behavior in a range of problems of

economic import” (p. s449). There has been a paradigm shift from the neoclassic model

that states that profit maximization and perfectly competitive markets determine economic

outcomes. From this perspective, the rational choice theory, which contends that an

individual will make decisions that maximize utility and self-interest, took hold. With this

theory holding court in the minds of financial educators, a new school of thought has started

to take hold, namely behavioral economics. As Goodwin, Harris, Nelson, Roach, and

Torras (2019) highlight, the last few decades have seen a shift from the neo-classic view

to an alternative embracing of behavioral economics. This shift takes into consideration

social and psychological aspects that had previously been left out of financial literacy

education. They go on to then expand on this idea by suggesting that a more sophisticated

model of human motivation is required to understand why people make the financial

decisions that they do, sometimes in direct objection to their own self- interest.

Given this alternative in how individuals make decisions, a more refined focus on

these behavioral and developmental components of financial literacy education could

enhance the effectiveness of programing. Holden (2010) has examined this phenomena and

postulates that:

Financial education material and approaches are often developed by

practitioners based on the assumption that, if individuals are presented with

19

knowledge and financial tools, then they will better be able to assess the

relative advantages of known financial options and choose what is most

likely to achieve their financial goals. (p. 1)

Holden goes on to state that there is not a singular theory of development that can

adequately explain how financial decisions are made, but that there is a myriad of

individualized components that lead an individual to a particular financial decision. Given

this stance, it is postulated that a focus on only the core components of knowledge, while

not attending to attitudes, emotions, motivations, and internalizations may result in

undesirable results.

The preceding sections of this chapter were meant to provide an understanding

relating to what has been happening in this sphere of education and how the psychology of

financial decision-making can impact success. Attention will now be given to the two

domains of learning that this study intends to address by focusing on how they have

historically been used, and could be utilized, to improve program effectiveness.

Cognitive and Affective Domain Learning Outcomes

Cognitive objectives are those which place emphasis on recall, recollection, and

achievement of various topic-specific intellectual tasks. The affective objectives rely more

solely on matters of emotion, motivation, attitudes, values, and interest (Anderson &

Krathwohl, 2009). This study intends to expand upon participant affective objective

description and development.

Emphasis is placed overwhelmingly on knowledge objectives or other cognitive-

based outcomes at the expense of or detriment to the development of the ability to

adequately value or deploy that knowledge (Bloom, Krathwohl, & Masia, 1964). It is the

20

development of these abilities that this study intends to focus on. In adherence to a more

crystalized focus on the affective domain outcomes, traditional processes are better

understood, and new processes can be implemented. As Bloom, Krathwohl, and Masia

(1964) point out:

It seems clear that the cognitive approach to affective objectives is a

frequently traveled route. What about the reverse? One of the main kinds of

affective-domain objectives which are sought as a means to cognitive ends

is the development of interest and motivation. (p. 57)

By taking a more detailed look at how the affective-based objectives impact learning in the

context of a financial literacy education program, this study intends to add a depth of

knowledge to the research. This depth manifests in the emphasis on the learning tasks,

processes, and delivery of content with consideration of attitudes, emotions, motivations,

and internalizations.

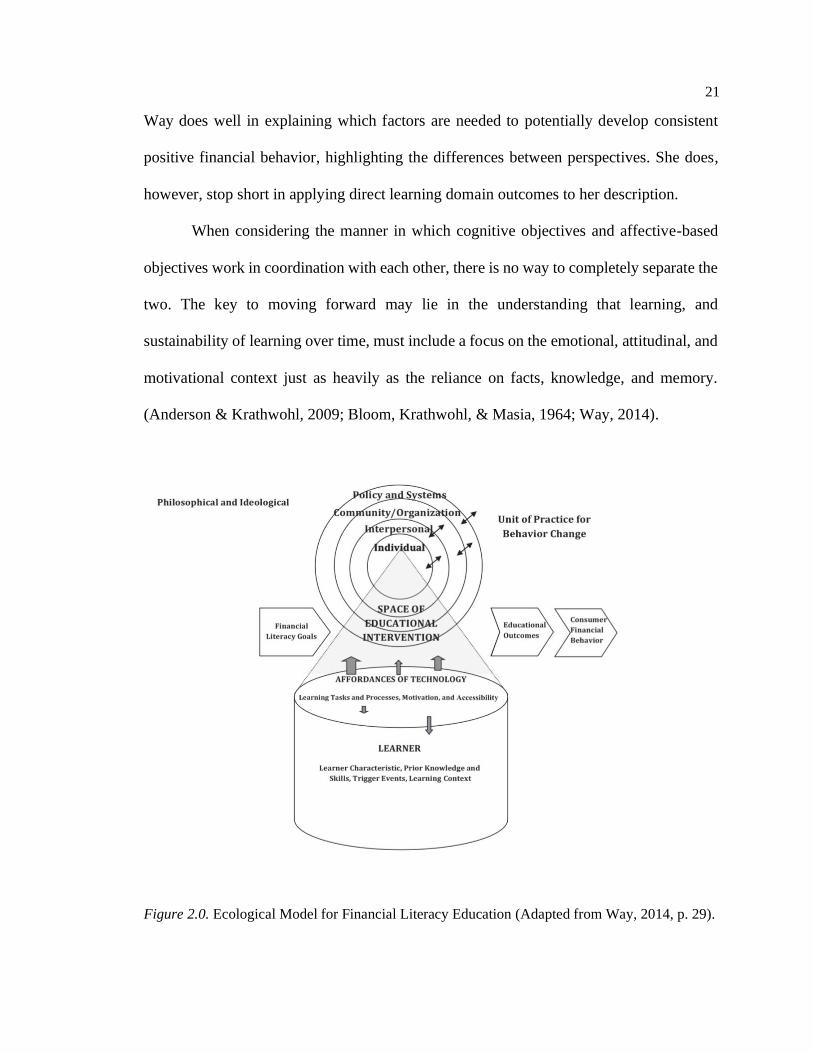

Figure 2.0 (Way, 2014) can be considered one of the more comprehensive financial

literacy education models available, and within the model, there is attention paid to what

can be considered affective outcomes. This model mimics many others where the

recommendations address motivation, attitudes, beliefs, emotions, values, and

internalization. What is not clear from the review of the literature is if there has yet to be a

comprehensive study conducted that uniquely addresses the development and deployment

of programing focused on the affective-based outcomes. As Way (2014) points out:

Financial behavior is not just a function of factual knowledge and skills, but

also a complex array of other personal, interpersonal, and environmental

factors, such as intentions, beliefs and attitudes, self-efficacy and self-

regulatory ability, resources derived through authentic experiences, social

interaction, and self-reflection. While either behaviorist or constructivist

approaches to learning may be useful in developing knowledge and “how-

to” skills, the other important determinants of positive behavior may

arguably be more likely to develop through constructivist approaches. (p.

30)

21

Way does well in explaining which factors are needed to potentially develop consistent

positive financial behavior, highlighting the differences between perspectives. She does,

however, stop short in applying direct learning domain outcomes to her description.

When considering the manner in which cognitive objectives and affective-based

objectives work in coordination with each other, there is no way to completely separate the

two. The key to moving forward may lie in the understanding that learning, and

sustainability of learning over time, must include a focus on the emotional, attitudinal, and

motivational context just as heavily as the reliance on facts, knowledge, and memory.

(Anderson & Krathwohl, 2009; Bloom, Krathwohl, & Masia, 1964; Way, 2014).

Figure 2.0. Ecological Model for Financial Literacy Education (Adapted from Way, 2014, p. 29).

22

Summary

The aim of Chapter 2 was to inform the reader of the context in which a majority

of financial literacy education and programing is taking place. It is important to point out

at this juncture that the existing literature, research, and efforts are not incorrect or to be

deemed completely ineffective. In the realm of financial literacy education, cognitive

objective-based programing is far and away better than no programing at all. The intent is

to show that there is a gap in what currently exists that should be addressed. In the following

chapter the methods that are used to explore the affective domain learning objectives are

outlined and developed.

Chapter 3

Method

The transformation of knowledge, ideas, or phenomena into accepted academic

research or theory necessitates that care was taken in the development of the methods used

to conduct research. This chapter outlines the methods deployed in this study while also

giving an overview of the specific protocols and procedures that were implemented. The

chapter ends with a description of the overall project plan and addresses potential

limitations of the study.

Qualitative Overview

Methodology use is determined by a number of factors, including what is to be

studied and the research questions proposed within the study (Yin, 2012). Given the nature

of this research study, a qualitative research design is best suited for the exploration of the

proposed research questions. Qualitative researchers are interested in discovering the

meaning that people attribute to a particular phenomenon, the way they experience the

phenomenon, and how they integrate the phenomenon into their way of understanding the

world (Merriam, 1998). As Rallis and Rossman (2016) elaborated, qualitative research

begins with questions, and the purpose of undertaking this type of study is learning. This

study was undertaken with the intention of learning more so than proving or substantiating

a causal effect. This study began with questions regarding the design methodology of

financial literacy programs and their learning objectives. The resulting data were used to

24

inform and expand upon the research questions. The knowledge derived from this study

can be used to create potential new understandings of how financial literacy education is

delivered in the workplace and beyond.

Since the aim of the study is to evaluate the perspectives of individuals engaged in

a financial literacy program, and because this study uses interview responses and other

documentation that are not strictly quantitative or numerical in nature, a qualitative design

is preferable. Qualitative data allows for exploration of the research questions focused on

decision-making, motivation, emotions, attitudes, and well-being. The data generated from

this study consisted of survey responses, interviews, a questionnaire, and other

documentation/field notes that shed light on the delivery of financial literacy education to

employees within a workforce setting. Data interpretation took place in order to uncover

emergent themes regarding affective learning outcomes and their role in enhancing

financial literacy education. The research questions this study not only lend to a qualitative

study but, more specifically, a case study design.

Study Design

This research employs an embedded case study design. A case study is:

A qualitative approach in which the investigator explores a real-life,

contemporary bounded system (a case) or multiple bounded systems (cases)

over time, through detail, in-depth data collection involving multiple

sources of information (e.g., observations, interviews, audiovisual material,

and documents and reports), and reports a case description and case themes.

(Creswell, 2013, p. 97)

Given that the desired data from this study focuses on aspects of emotion, attitude,

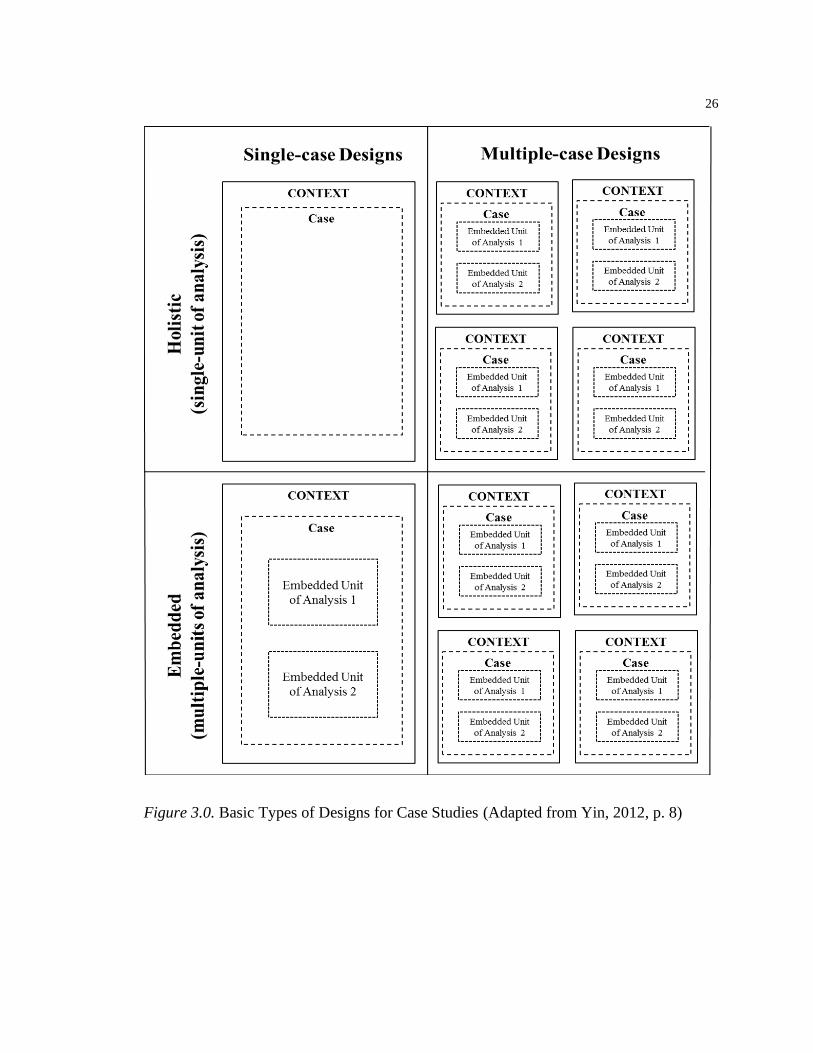

motivation, and values, a case study design is best suited. Yin (1994) asserts that a case

25

study is best suited for “how” and “why” types of research questions, and this study is

precisely that. In particular, this study aims to illuminate why financial education programs

should consider affective objectives and how to develop and implement them. Within a

case study design, a number of factors need to be considered in order to determine the best

variation of case study to be utilized. Figure 3.0 illustrates the differences that need to be

considered when selecting a case study design. Additionally, Yin (1994) categorizes case

studies as explanatory, exploratory, or descriptive. The selection of one type of case study

design over the other is dependent upon the overall purpose of the study.

For this study, a single-site, exploratory, embedded design was utilized. Yin (2012)

states that this type of study is used in the linking of program implementation with program

effects or outcomes, a main consideration of this study. This design also sought to uncover

the potential causal links in real-life interventions. This study design allows for an in-depth

evaluation and exploration of the particular phenomena to be studied. In this case study,

that phenomenon is a workplace financial education program at a large American

university that focuses effort on affective domain learning objectives. These objectives are

undertaken in order to engage participants more readily in the areas of attitudes, emotions,

motivations, and internalizations. By utilizing embedded units of analysis as seen in Figure

3.0, the overall phenomena can be explored from multiple perspectives, thus allowing for

greater validity and reliability in the resulting data analysis. In this case, each embedded

unit is a study participant.

26

Figure 3.0. Basic Types of Designs for Case Studies (Adapted from Yin, 2012, p. 8)

27

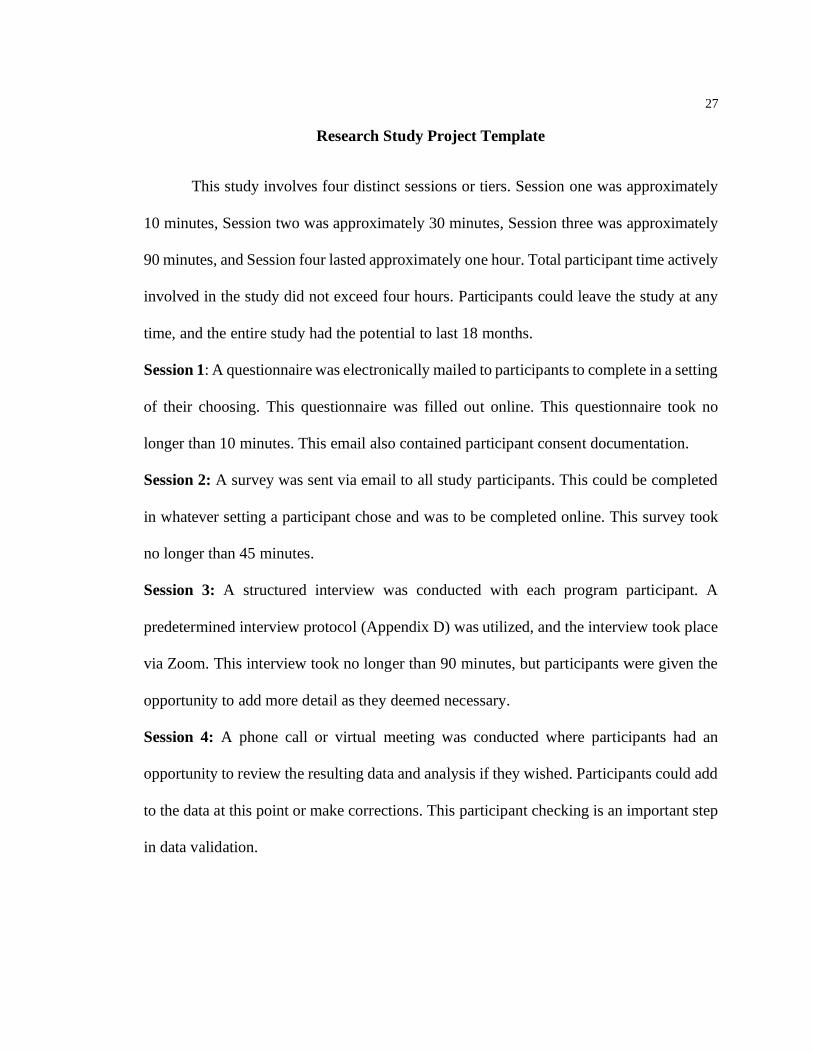

Research Study Project Template

This study involves four distinct sessions or tiers. Session one was approximately

10 minutes, Session two was approximately 30 minutes, Session three was approximately

90 minutes, and Session four lasted approximately one hour. Total participant time actively

involved in the study did not exceed four hours. Participants could leave the study at any

time, and the entire study had the potential to last 18 months.

Session 1: A questionnaire was electronically mailed to participants to complete in a setting

of their choosing. This questionnaire was filled out online. This questionnaire took no

longer than 10 minutes. This email also contained participant consent documentation.

Session 2: A survey was sent via email to all study participants. This could be completed

in whatever setting a participant chose and was to be completed online. This survey took

no longer than 45 minutes.

Session 3: A structured interview was conducted with each program participant. A

predetermined interview protocol (Appendix D) was utilized, and the interview took place

via Zoom. This interview took no longer than 90 minutes, but participants were given the

opportunity to add more detail as they deemed necessary.

Session 4: A phone call or virtual meeting was conducted where participants had an

opportunity to review the resulting data and analysis if they wished. Participants could add

to the data at this point or make corrections. This participant checking is an important step

in data validation.

28

This study utilized a project management plan in which all participants had access

to data for viewing and commenting. This plan was available electronically throughout the

research study.

Data Collection Procedures

For this study, multiple forms of data were collected and evaluated. Interview,

survey, and questionnaire responses were the primary data collected. Erickson (1986)

spoke to the necessity of multiple data collection procedures. He stated that each collection

method has weaknesses and strengths, but that a combination of methods leads to

triangulation and more accurate findings. Each participant took a nationally available

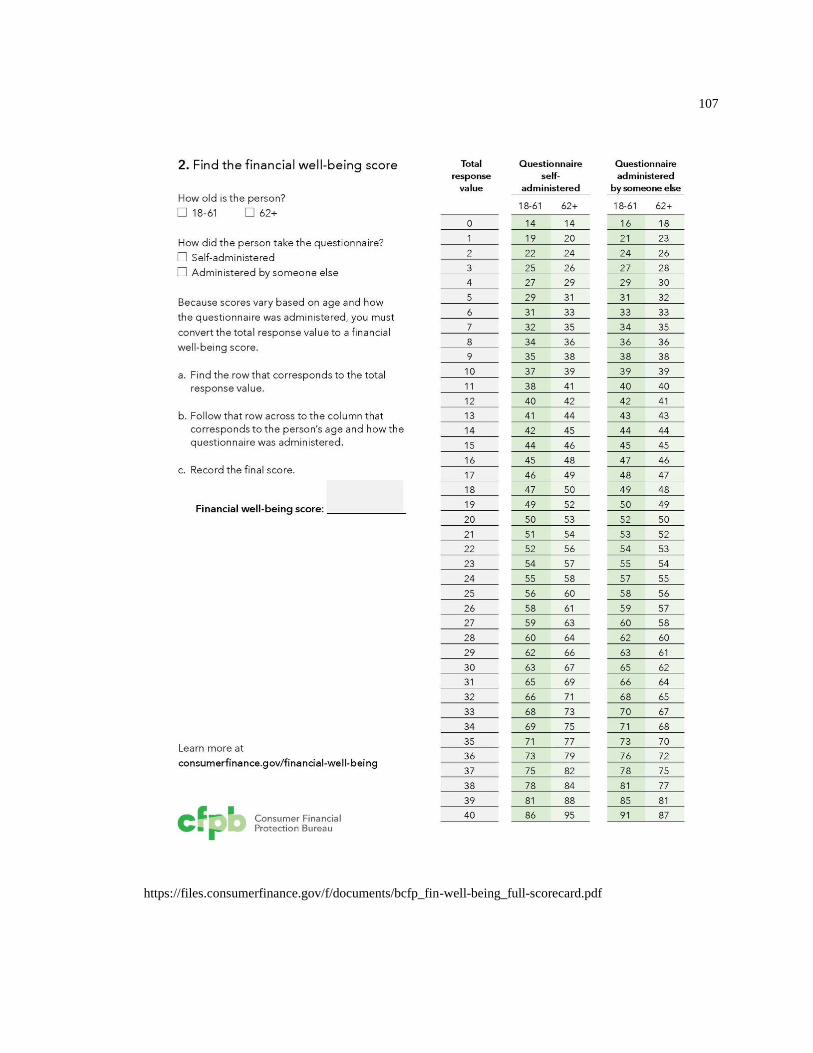

assessment of financial well-being: The Consumer Financial Protection Bureau Financial

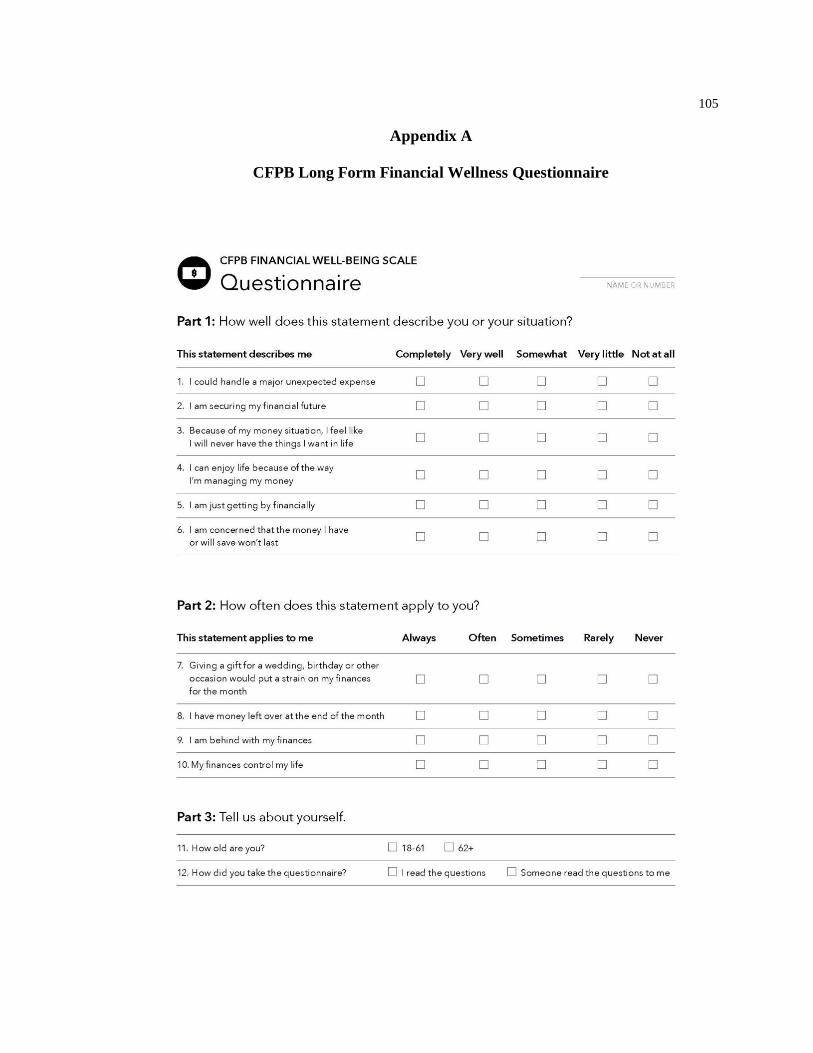

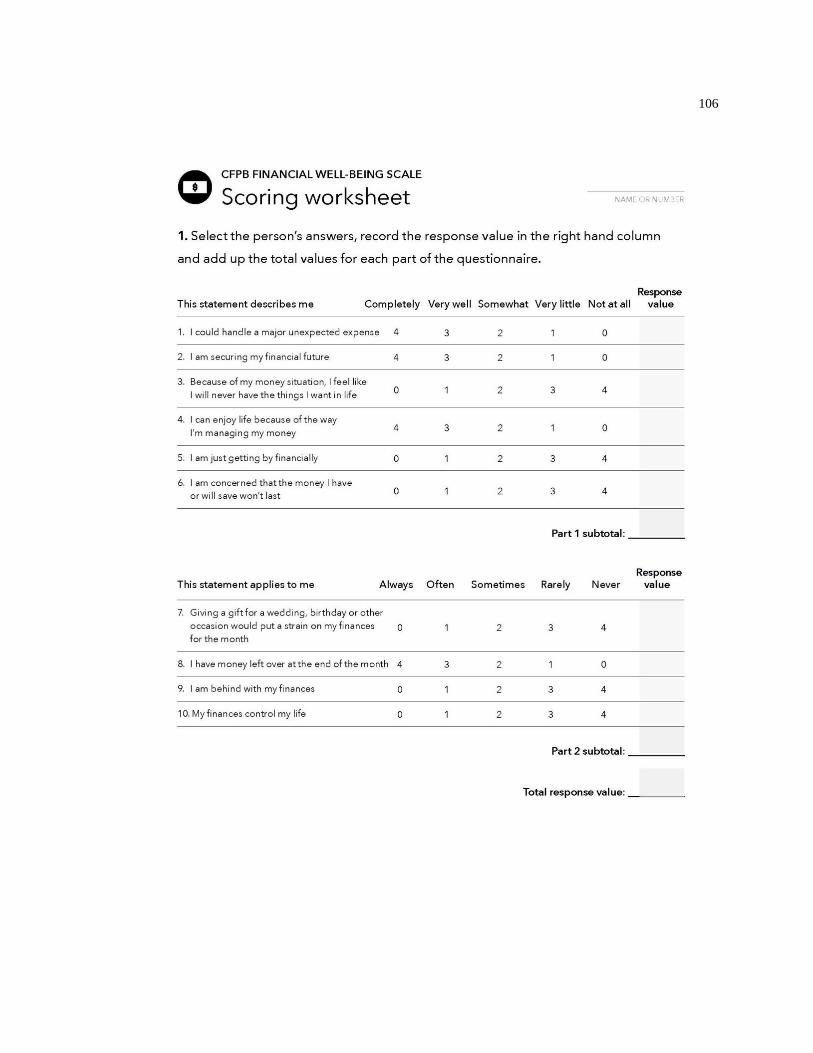

Well-Being Long Form Questionnaire (Appendix A) (Measuring Financial Well-Being: A

Guide to Using the CFPB Financial Well-Being Scale, n.d.). This questionnaire measures

a participant’s financial well-being as it relates to four measures. These measures are the

ability to meet day-to-day financial obligations, enjoyment of one’s life, the capacity to

absorb financial shock, and being on track to meet goals. This questionnaire was delivered

via email along with the implied consent documentation. If a potential participant returned

their score on the questionnaire, they were then moved into the next stage of the study.

Interview data and results of the CFPB questionnaire were analyzed on the

individual level. The results of the survey were aggregated in total and analyzed as a set of

responses without being identified on an individual basis. This served as a separate avenue

to explore the research questions while also giving participants the opportunity to give their

29

perspectives more openly, and anonymously, as the researcher was also the main contact

within the financial literacy education program. This anonymity allows for greater

creditability in the study. All data collected were de-identified in the final study results and

participants were assigned a participant ID.

The interviews, conducted after the questionnaire and survey, were structured and

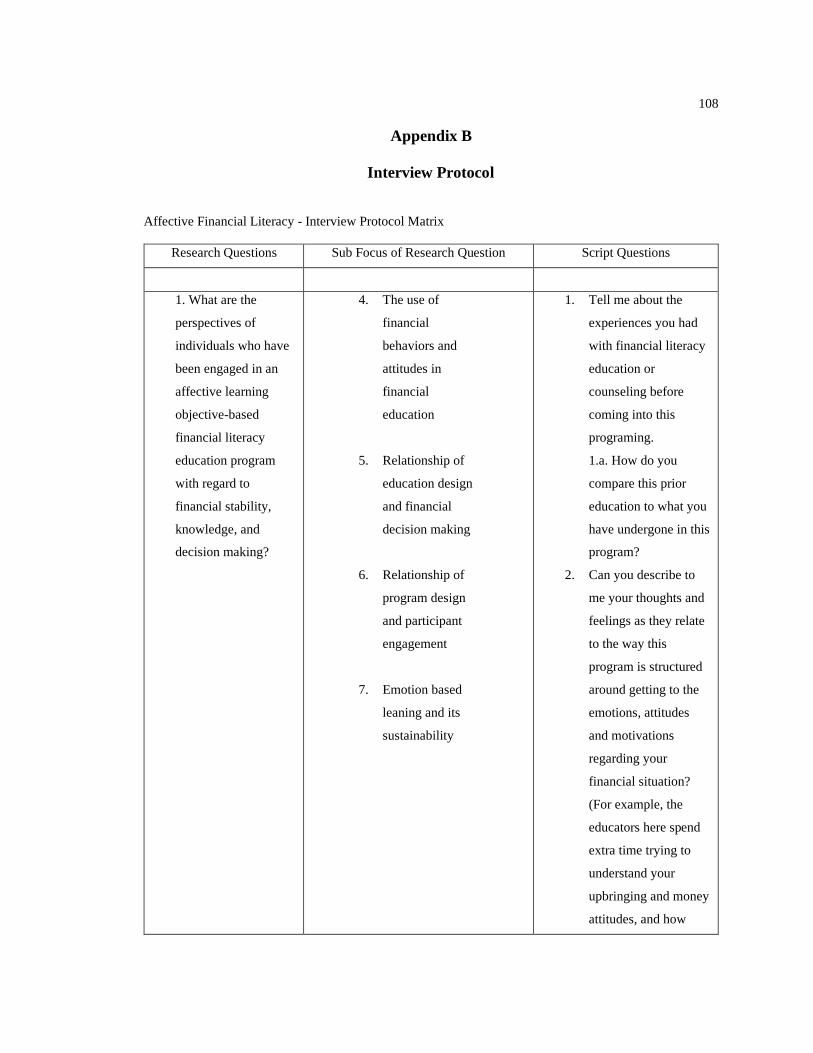

followed a defined and prescribed interview protocol (Appendix B). The questions

followed a sequence that aligned with the research questions. Structuring this way allows

for consistency in the data collected and for the focus to remain on the research questions

being explored. All of these interviews were conducted over Zoom (https://www.zoom.us/)

and were recorded, transcribed, and stored. As Creswell (2014) points out, this is a useful

approach because direct observation behaviors of the participants cannot take place outside

of the program setting, and it gives the researcher control over the line of questioning.

The survey (Appendix D) given to study participants was developed to collect

information in six distinct areas that help to answer the study’s research questions. Each

section of the survey had five Likert-scale questions and one open-ended response

question. The Likert-scale range was presented as: Strongly Disagree - Somewhat Disagree

- Agree - Somewhat Agree -Strongly Agree. Participants selected the scale measure they

felt matched their perspective and the presented data were displayed according to the

number and percentage of selections. The administration of the survey to participates

provides an additional source of data that helps to identify and describe the impact of

affective domain objectives as they relate to the research questions. The survey was

delivered and completed electronically by program participants through Qualtrics

(https://www.qualtrics.com/).

30

The selected participants have participated in a minimum of three educational

sessions within the program setting, and the educator during these sessions collected notes

and observations related to the research questions of this study. These documents contain

source data that is representative of an individual’s demographics, beliefs, attitudes,

motivations, and worldview, thus describing an individual’s perspective (Merriam, 2015).

These documents were reviewed and field memos created.

Participants and Sampling

Creswell (2014) discussed that “the idea behind qualitative research is to

purposefully select participants or sites (or documents or visual materials) that will best

help the researcher understand the problem and the research questions” (p. 189). For this

research study, a criterion sampling technique was employed. Patton (2002) states that this

approach studies all cases that meet a predetermined criterion. It is essential in this study

that criterion sampling is utilized in order to ensure that participants have had sufficient

exposure to the phenomenon of interest (i.e., participation in the financial literacy program

that is being evaluated). An existing file of program participants was evaluated to

determine those candidates who meet the criteria for the study. There were 33 employees

who met the eligibility requirements for the study. Once identified, participant email

addresses were available on the intake documents. At initial participant selection, the

inclusion criteria entailed the following: Adult 18 years of age or older, University

employee who participated in 1-hour counseling/education sessions, and no less than three

sessions completed. Creswell (2014) contends that case studies should include four to five

31

cases. From the eligible potential participates, 27 potential participants received the

informed consent email with the CFPB questionnaire included. Of the 27 potential

participants, 11 individuals replied with their questionnaire scores. These 11 participants

were then sent the survey for completion. Of the 11 participants, nine responded to the

survey and, ultimately, seven individuals were interviewed. This sample size allows for the

interviews, documentation review, and follow-up conversations to be completed in a timely

fashion while giving ample time and data to reach a depth of understanding concerning the

research questions (Creswell, 2014).

Process of Data Analysis

Analysis of qualitative data is a robust and creative process that must include both

inductive and deductive reasoning, along with creative thinking. Creswell (2014) points

out that data analysis will naturally coincide with other aspects of the study, but that there

is a process to follow that is interactive in nature. Due to the emergent nature of qualitative

research, and specifically the design of this study, care was taken to gain a richer

understanding of all data collected and to distill this data into the most relevant themes.

All data were compiled using case study methods of notetaking, interview

transcripts, questionnaire results, and survey results. Resulting data were analyzed and

coded for inductive, emergent, and apparent themes. The data were then interpreted and

analyzed as they pertained to research questions. First, the interviews were transcribed and

reviewed for accuracy; at the same time, documents and observation notes were cataloged.

The researcher then reviewed and annotated relevant discoveries and potential themes. This

32

step “provides a general sense of the information and an opportunity to reflect on its overall

meaning” (Creswell, 2014, p. 197).

All interviews were transcribed in a timely fashion to ensure accuracy. All

transcripts were then read while listening to the original recording. Transcripts were then

downloaded into Deedoose (https://www.dedoose.com/), a qualitative data analysis

software platform. The use of this software allows for a more simplified coding process.

As Creswell (2014) points out, coding allows for an organization of the data into usable

chunks that can be labeled and categorized according to emergent themes. This making

sense of the data and coding it for meaningful themes relevant to the research questions

allows for a step-by-step analysis that can uncover a deeper understanding of the data as a

whole.

The coding process used in this study took place in three distinct stages following

the structure of the study. These stages evolved from an inductive to a combination

inductive/deductive approach, finally resulting in the construction of relevant categories

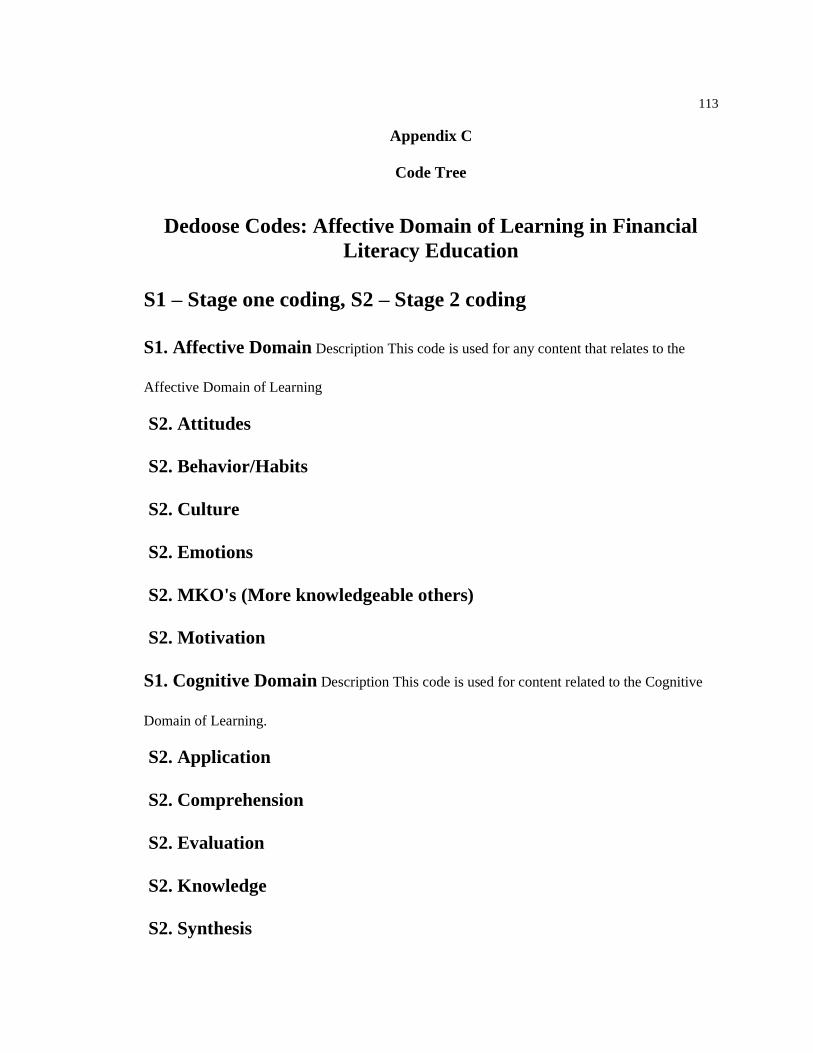

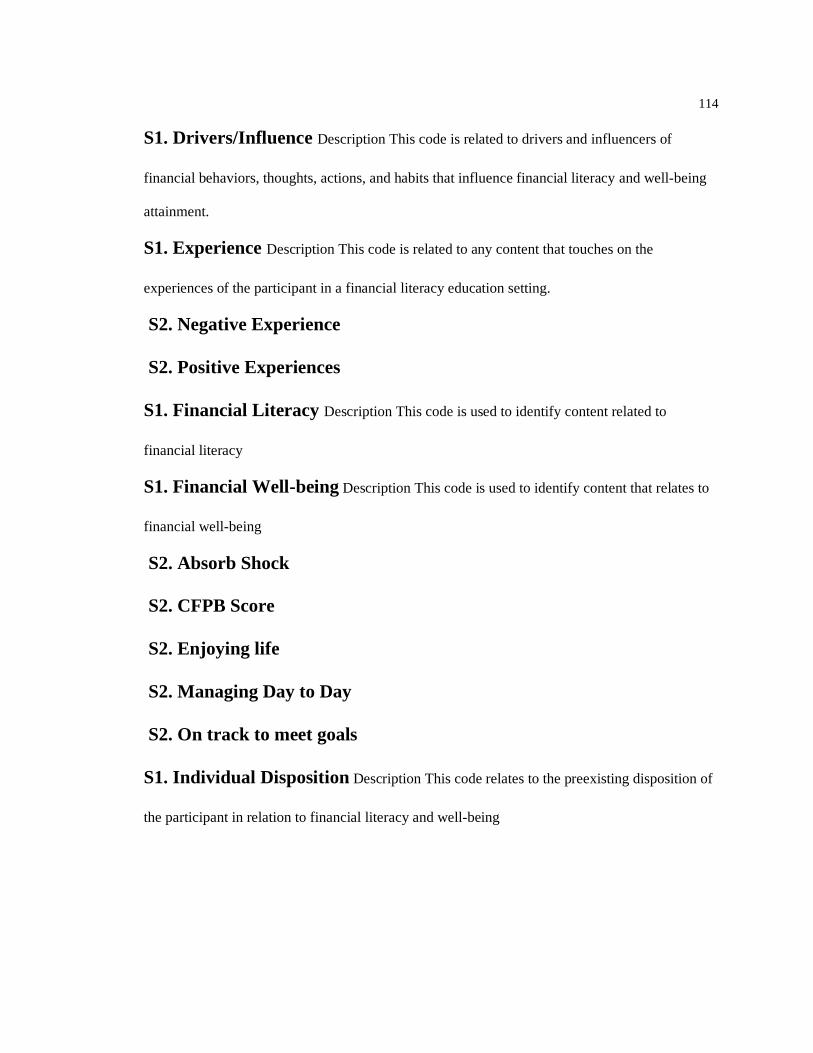

and themes that assisted in the addressing of the research questions. Stage one of the coding

process was by definition a deductive or concept-driven approach that followed a top-down

strategy, a research theory leading to a hypothesis. Appendix C lists all stage one and stage

two codes used in this study. Observation and analysis were then used to confirm or refute

the leading theory. Stage one coding for this study began with the creation of main themes

or categories as they related to the research questions. There were seven initial codes that

were created for the first pass deductive coding (Affective Domain, Cognitive Domain,

Influences, Experience, Financial Literacy, Financial Well-being, and Individual

Disposition). Using these seven codes, the data was chunked into excerpts that were

33

relevant to individual codes. These chunks were mainly in sentence or paragraph format.

Constant comparison to previous coding was used throughout this process in order to help

in the consistency, validity, and credibility of the coding. These code chunks were then

examined for ideas, themes, and any emergent observations. All coding was conducted by

the primary researcher.

Stage two of the coding process was a thematic analysis that employed both an

inductive and deductive approach. This was largely a latent approach in that the meaning

behind the actual text was given priority consideration over the absolute text or language.

This approach allowed for a deeper dive into the experience of the study participants,

particularly their discussion of personal finances. This stage of coding happened in

sequential order. First, the data was read again with stage one coding applied. Second, stage

two inductive codes were created based on the research questions; there were an additional

eighteen codes created. These additional eighteen codes can be found in Appendix C. After

this round of coding, categories were created and themes were generated to help explain

and address the research questions. These themes were reviewed through constant

comparison and triangulation of data. Finally, the resulting themes were defined. From the

results of the coding process, several significant findings were uncovered that were

analyzed to answer and elaborate on the research questions.

The survey data was analyzed to address participant perceptions within each of six

defined areas: previous education, knowledge, behavior, attitude and emotions, goals, and

motivation. The data was compiled and analyzed for frequency and type of response. Given

the small sample size and qualitative nature of this study, no additional statistical analysis

was conducted. The survey, however, could be used in future research in which more robust

34

statistical analysis may be warranted. The open-ended questions that were included in the

survey were aggregated and coded along with the interview transcripts but were not

attached to any descriptor variable and were not identified by participant in any way.

The CFPB Long Form Questionnaire was used to help uncover perceived levels of

financial well-being of the study participants. These results not only give a measure of

overall level of financial well-being of program participants but are also used to draw

comparisons to the available data of individuals who have completed the questionnaire

nationally and at the state level.

These findings and their relevance to the research questions are then presented in a

detailed discussion. These discussions are presented as a description of participant

experiences, attitudes, and emotions as they pertain to the financial literacy program and

the research questions as a whole. Creswell (2014) states that the last step in the qualitative

research process should include making an interpretation. For this particular study, the

researcher tied the results of the study to the larger realm of financial literacy education

and how programs are designed, developed, and deployed in the workforce.

Validity and Reliability Concerns of Qualitative Inquiry

Regardless of the type of research, validity and reliability are concerns that

can be approached through careful attention to a study’s conceptualization

and the way in which the data are collected, analyzed, and interpreted and

the way in which the findings are presented. (Merriam, 2015, p. 238)

Creswell (2014) stated that one of the strengths of qualitative research is its validity. This

validity can be achieved through the accuracy of the resulting descriptions from the

researchers, participants, and readers’ accounts. In order to ensure the validity of the data

35

collected in this study, complete written transcripts of interviews and narrative descriptions

are provided to participants so that they were afforded the opportunity to clarify and review

all data. This participant checking aids in determining the accuracy of the researcher’s

findings. Additionally, in order to increase the validity of this study, triangulation of the

data sources took place. Triangulation between the interviews, session notes/documents,

and observations is a critical step in the validation of codes and themes uncovered in data

analysis.

To further enhance the credibility and validity of the study, a section of this chapter

and the discussion chapter is dedicated to the clarification of potential researcher bias.

“This self-reflection creates an open and honest narrative that will resonate well with

readers” (Creswell, 2014, p. 202). For this study, in particular, it is vital to address the

reflexivity of the researcher, as the researcher is also a key facilitator of the financial

literacy education program being studied.

The reliability of a particular study is the ability to replicate that study. This

standard, however, can be problematic in qualitative research. Creating an entirely accurate

recreation of a qualitative inquiry is not possible. Merriam (2015) suggests that “rather than

demanding that outsiders get the same result, a researcher wishes outsiders to concur that,

given the data collected, the results make sense – they are consistent and dependable” (p.

251). This study provides results that very well may be some of the first of its kind when

considering the specific research questions. Reliability, in its truest form, may or may not

come as a result of other research undertaking the same or similar phenomena. Creswell

(2014) and Yin (2012) have addressed that in order to ensure this consistency and

dependability, the researcher needs to be vigilant in the documentation of all procedures

36

that take place within the study and that a detailed case study protocol and database be

constructed. Heightened diligence affords other researchers the transparency needed to

understand how the study was conducted and how the data was analyzed.

Credibility and Trustworthiness

Any sound research is done in such a manner that the researcher is acting from an

ethical perspective in hopes of concluding with a trustworthy and credible result. Yin

(2009) referenced that good case study research should utilize different perspectives and

give sufficient evidence within the resulting reporting. When this stance is taken in

combination with the strategies proposed by Merriam (2002) regarding triangulation,

participant checks, reflexivity, and rich description, the credibility, and trustworthiness of

the study are enhanced.

This study utilized triangulation and participant checks in order to verify the

accuracy of data and confirm the emergent theme discoveries. Additionally, by providing

a rich description of participant thoughts and feelings as they related to the research

questions and this study’s methodology, credibility and trustworthiness of the results are

strengthened. Merriam (2002) explained that taking this approach allows future readers of

the study to decide if their experience matches the resulting research.

37

Reflexivity

In any qualitative study it is imperative that the researchers recognize and reflect

on the role that they play in the research process. This reflection on oneself and the role

that the researcher’s background, experiences, and culture play in the study all have the

potential to guide and characterize the data and results (Creswell, 2014). Reflexivity does

not happen in one instance but must be continually considered and noted throughout the

research process. Merriam (1998) ascertained that with any qualitative research the

researcher’s biases and personal orientation will ultimately have an impact on the outcome

of the study. This impact on the outcome of the study is not necessarily a deficit or a

limitation of the study, as long as the researcher undertakes an ongoing and formalized

approach to explicitly recognizing and documenting biases, impactful views, and

dispositions. When biases are identified and accounted for there remains a potential for a

skew of subjectivity. This study in particular carried with it a potential for a high degree of

researcher subjectivity, given that I was the primary counselor in the financial education

program while also being the primary researcher. Peshkin (1988) addressed the issue by

stating that, “one’s subjectivities could be seen as virtuous, for bias is the basis from

which researchers make a distinctive contribution, one that results from the unique

configuration of their personal qualities and joined to the data they have collected” (p. 18).

In an effort to fully address potential bias and/or subjectivity considerations, I will

now discuss my experiences and dispositions in relation to this study. I have spent the last

twenty years working in some capacity helping individuals, families, and businesses to

achieve financial security and well-being. I grew up in a poor household where my parents

38

lacked the knowledge and, more importantly, the motivation and behaviors necessary to

ensure their financial success. For the last eight years of my professional career, I have

developed and delivered financial literacy and well-being programing aimed at connecting

and intertwining the knowledge, behaviors, and emotions needed to codify financial

success. As the assistant director of the financial education program, I intentionally

designed program aspects to more deliberately tie these aspects together. It was only after

witnessing the financial education program’s success, while also understanding that a

majority of other programs were failing to meet expectations, that I decided to conduct this

study. I have identified that I am indeed biased in regard to program design, and this study

is an attempt to more fully understand if this type of program design can have a meaningful

and lasting impact.

Limitations

There are limitations to this study. As described above, there exists a potential for

a degree of researcher bias and subjectivity. Care was taken to identify the potential biases