Embed Size (px)

Citation preview

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 1/8

CASH BUDGETING

2007-08-15 Cash Budgeting 2

The Cash Budget

What is a cash budget?

• A forecasting tool that tracks all cash receipts

and cash disbursements.

• Done on a shorter time frame than other

statements (i.e., month-by-month or even

week-by week).

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 2/8

2007-08-15 Cash Budgeting 3

The Cash Budget

Why is a cash budget important?

• Allows companies to predict possible cash

shortages and take corrective action before a

crisis occurs.

• Allows companies to see if large sums of

excess cash are lying idle—could be put to

better use.

2007-08-15 Cash Budgeting 4

Cash Budgeting

Disregard the principles of accrual accountingwhen developing a cash budget:

• Instead of matching EXPENSES with REVENUES in the

period in which they are incurred, now we are

concerned with matching CASH INFLOWS and CASH

OUTFLOWS in the periods in which they are incurred.

• All cash items, regardless of their classification

(expense, asset, fixed cost, variable cost, etc.), are

accounted for in a cash budget. Non-cash items (such

as amortization) never appear.

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 3/8

2007-08-15 Cash Budgeting 5

Cash Budgeting

REMEMBER: A business that is

UNPROFITABLE can SURVIVE but INSOLVENCY

(i.e., insufficient cash to pay debts) could mean

BUSINESS FAILURE.

2007-08-15 Cash Budgeting 6

Cash Budgeting

Example:

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 4/8

2007-08-15 Cash Budgeting 7

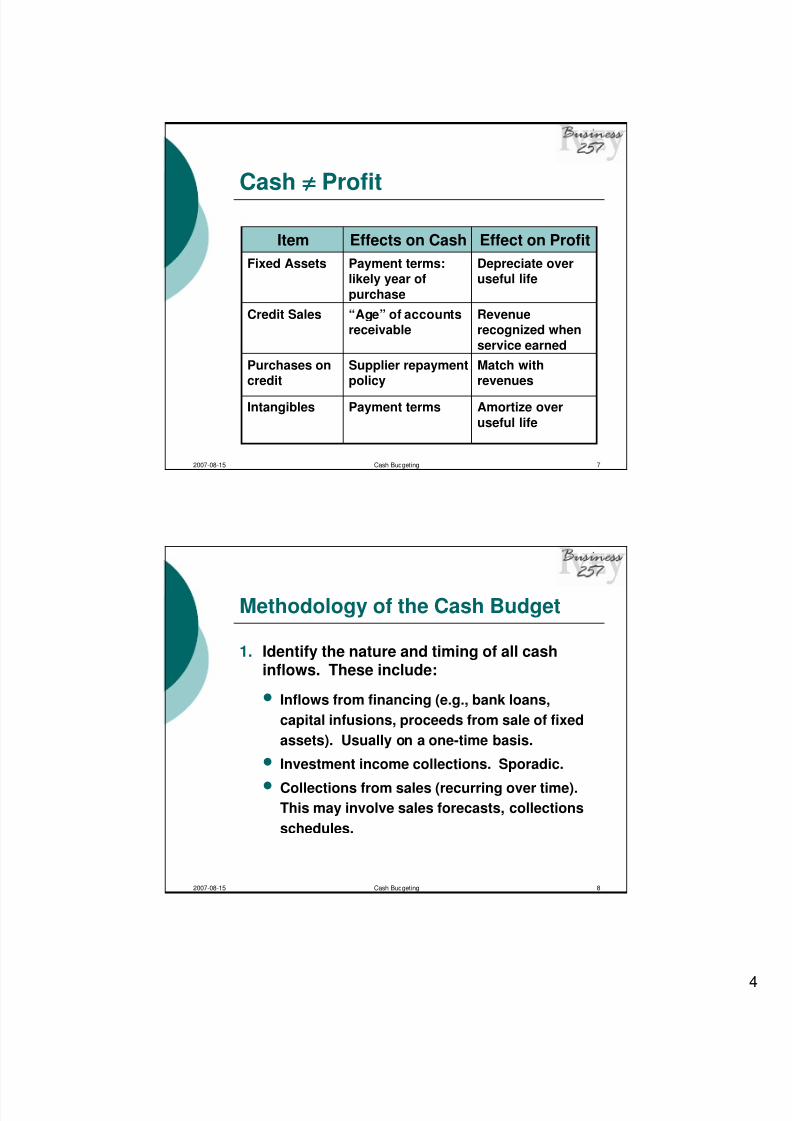

Cash ≠≠≠≠ Profit

Match withrevenues

Supplier repaymentpolicy

Purchases oncredit

Amortize over

useful life

Payment termsIntangibles

Revenuerecognized when

service earned

“Age” of accountsreceivable

Credit Sales

Depreciate overuseful life

Payment terms:likely year of

purchase

Fixed Assets

Effect on ProfitEffects on CashItem

2007-08-15 Cash Budgeting 8

Methodology of the Cash Budget

1. Identify the nature and timing of all cashinflows. These include:

• Inflows from financing (e.g., bank loans,

capital infusions, proceeds from sale of fixed

assets). Usually on a one-time basis.

• Investment income collections. Sporadic.

• Collections from sales (recurring over time).This may involve sales forecasts, collections

schedules.

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 5/8

2007-08-15 Cash Budgeting 9

Methodology of the Cash Budget

Useful tools when forecasting sales:

• Management estimates

• Historical sales patterns

• Industry trends

• Competitor's sales

2007-08-15 Cash Budgeting 10

Methodology of the Cash Budget

2. Identify the nature and timing of allcash outflows. These include:

• Cash operating expenditures

• Capital expenditures

• Financial commitments

• Equity reductions

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 6/8

2007-08-15 Cash Budgeting 11

Methodology of the Cash Budget

3. Subtract outflows from inflows to getnet cash flow for the period (either asurplus or deficit).

4. Add (subtract) cash flow for the periodto the ending balance in cash from theprevious period to get new ending

balance.

2007-08-15 Cash Budgeting 12

Uses of Cash Budgeting

Schedule timing of cash flows to:

• Make efficient use of cash

• Analyze solvency

• Forecast financial requirements

• Prioritize and plan payments of outstandingaccounts

• Perform SENSITIVITY to plan contingency

action• Categorize type of financing requirements

Note: Cash budgeting involves a FUTUREorientation

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 7/8

2007-08-15 Cash Budgeting 13

Uses of Cash Budgeting

Implications:

• KEY VARIABLES highlighted

• Constant fine tuning

• Not perfect

2007-08-15 Cash Budgeting 14

Questions that Might be AskedFollowing a Cash Budget Analysis

1. What is the maximum cash requirement?

In what month is it needed?

Can we secure this much financing?

7/29/2019 cash-budgeting-lecture-1204182808584514-4

http://slidepdf.com/reader/full/cash-budgeting-lecture-1204182808584514-4 8/8

2007-08-15 Cash Budgeting 15

Questions that Might be Asked

Following a Cash Budget Analysis

2. Is the overall cash flow + or – ?

If it is negative, what can be done?

3. Which variables have the biggest

impact on the cash flow?

What happens if these variables change(sensitivity)?

2007-08-15 Cash Budgeting 16

Questions that Might be AskedFollowing a Cash Budget Analysis

4. If a negative cash flow results, what is themain cause?

What is the best type of financing toalleviate the problem?

Is it a long-term or short-term problem?