Embed Size (px)

Citation preview

Cash Flow, Profit, Your Lender and You

by Dr. Arnold Oltmans, Associate ProfessorAgricultural and Resource Economics,

NC State University.January 11, 2011

Summer Green Show of NCNLA, Greensboro, NC

If I paid my bills on time and had as much (or more) cash at the end as I had at the beginning, I guess I

had a good year!!

• Is that a good way to measure or evaluate business performance?

If I had more debt at the end than I had at the beginning and less cash than I started with, I must

have had a bad year!!

• Is that a good way to measure or evaluate business performance?

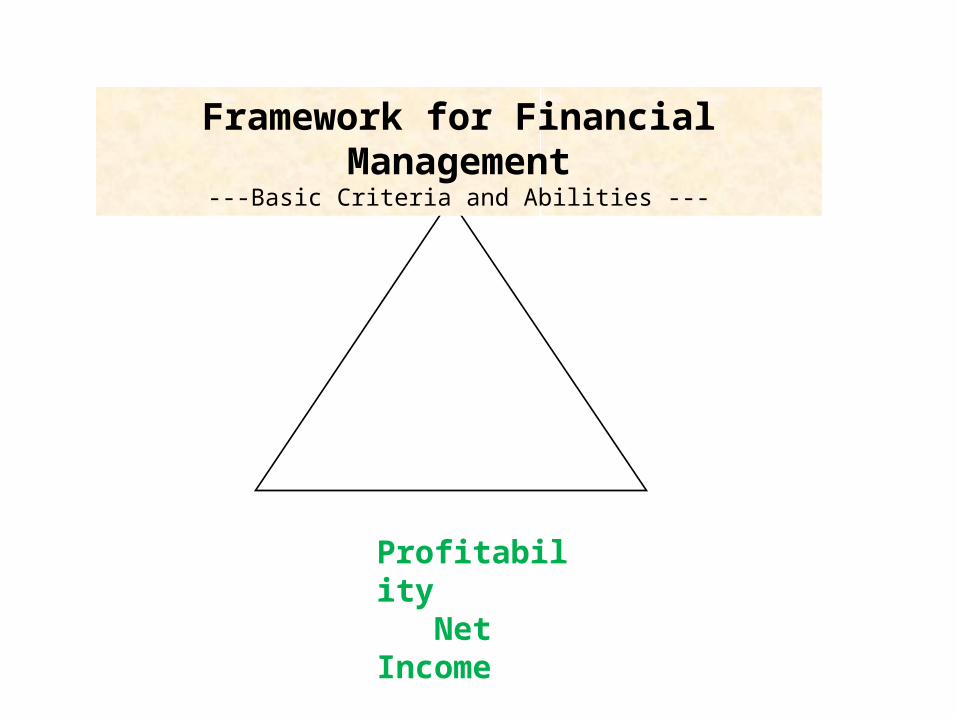

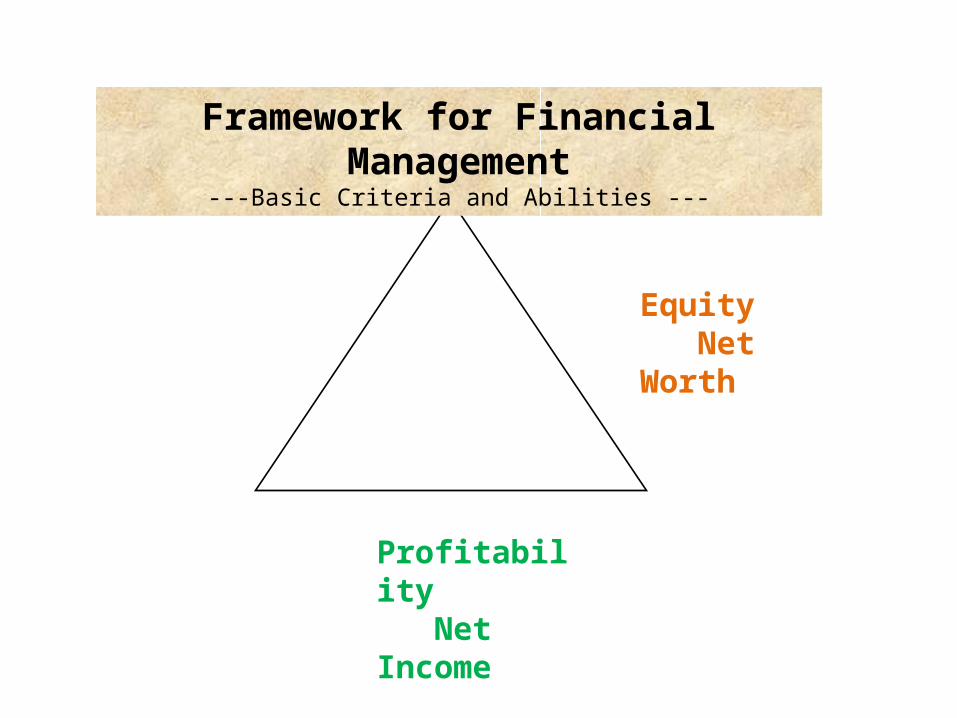

Framework for Financial Management---Basic Criteria and Abilities ---

Profitability Net Income

Equity Net Worth

Framework for Financial Management---Basic Criteria and Abilities ---

Profitability Net Income

Equity Net Worth

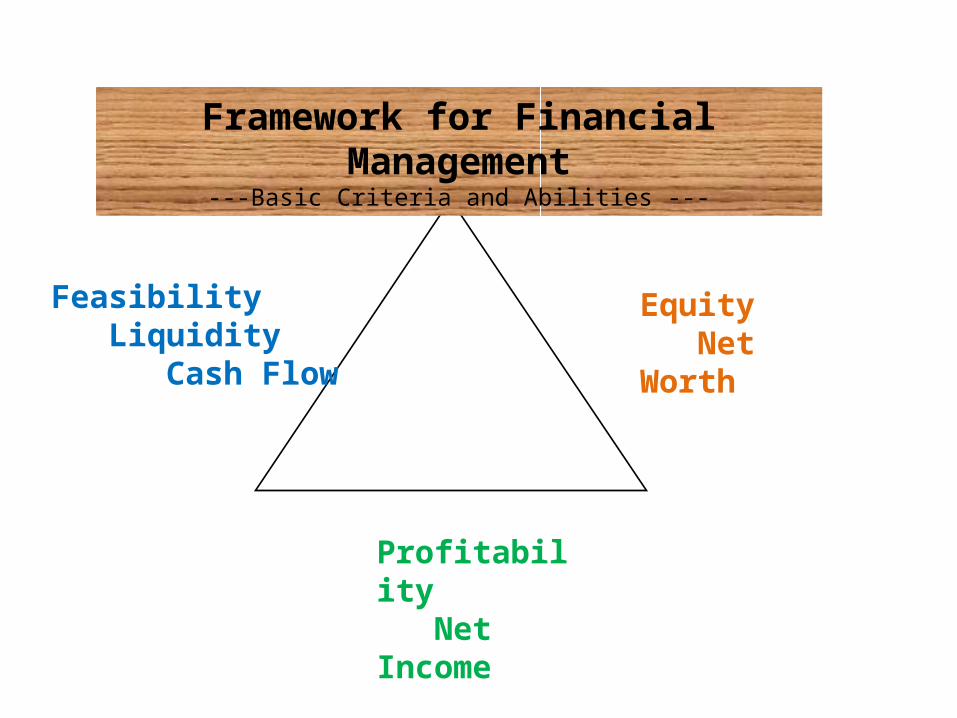

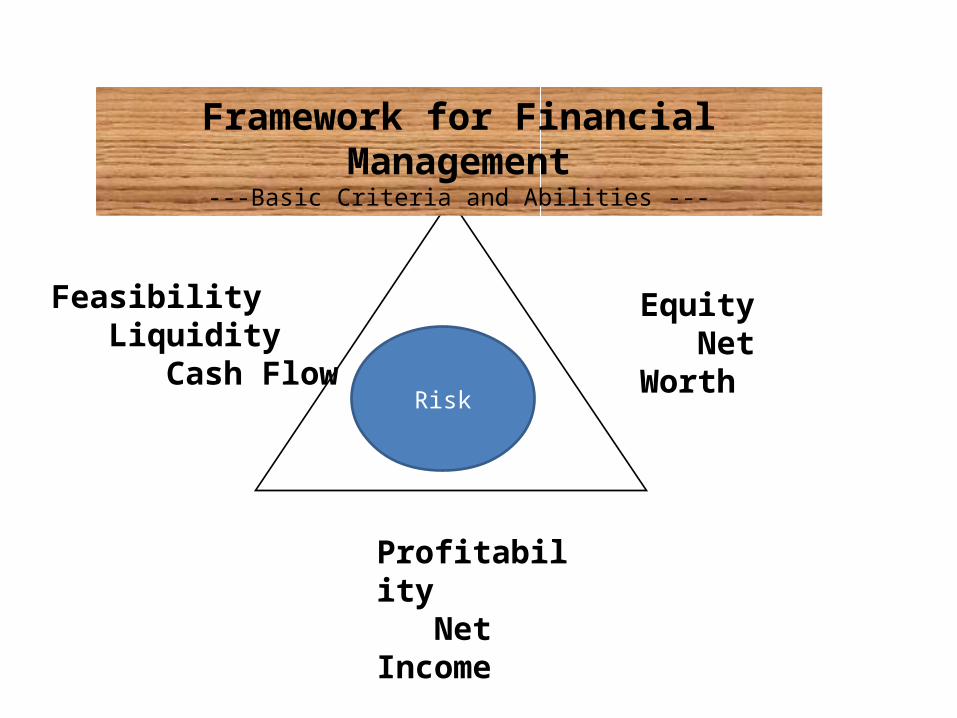

Framework for Financial Management---Basic Criteria and Abilities ---

Feasibility Liquidity Cash Flow

Profitability Net Income

Risk

Equity Net Worth

Framework for Financial Management---Basic Criteria and Abilities ---

Feasibility Liquidity Cash Flow

Profitability Net Income

Financial Management Challenge

• Understand this basic financial framework and interactions

• Properly analyze the business financially• Keep the financial triangle in balance as the

sides tug and pull on each other.

• A never ending challenge---the triangle is never in perfect balance

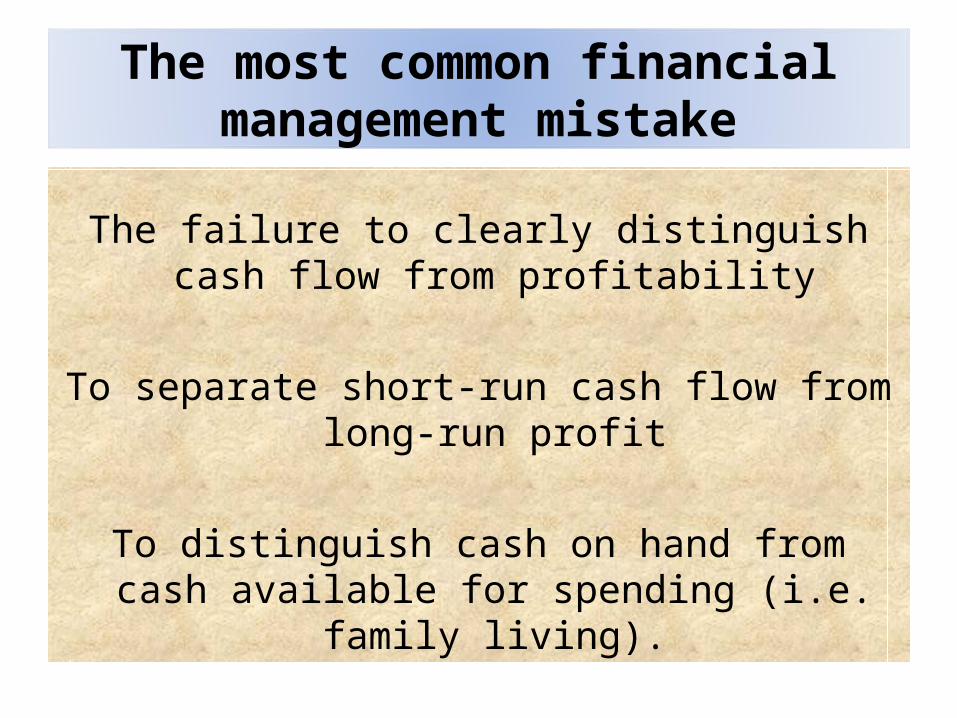

The most common financial management mistake

The failure to clearly distinguish cash flow from profitability

To separate short-run cash flow from long-run profit

To distinguish cash on hand from cash

available for spending (i.e. family living).

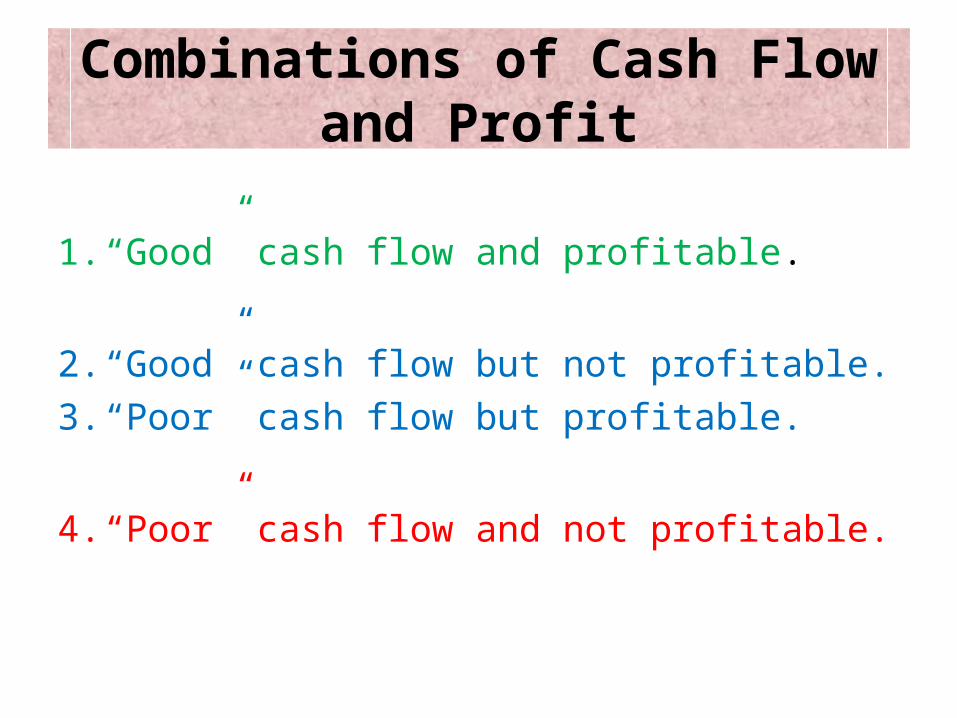

Combinations of Cash Flow and Profit

1. “Good” cash flow and profitable.

2. “Good” cash flow but not profitable.3. “Poor” cash flow but profitable.

4. “Poor” cash flow and not profitable.

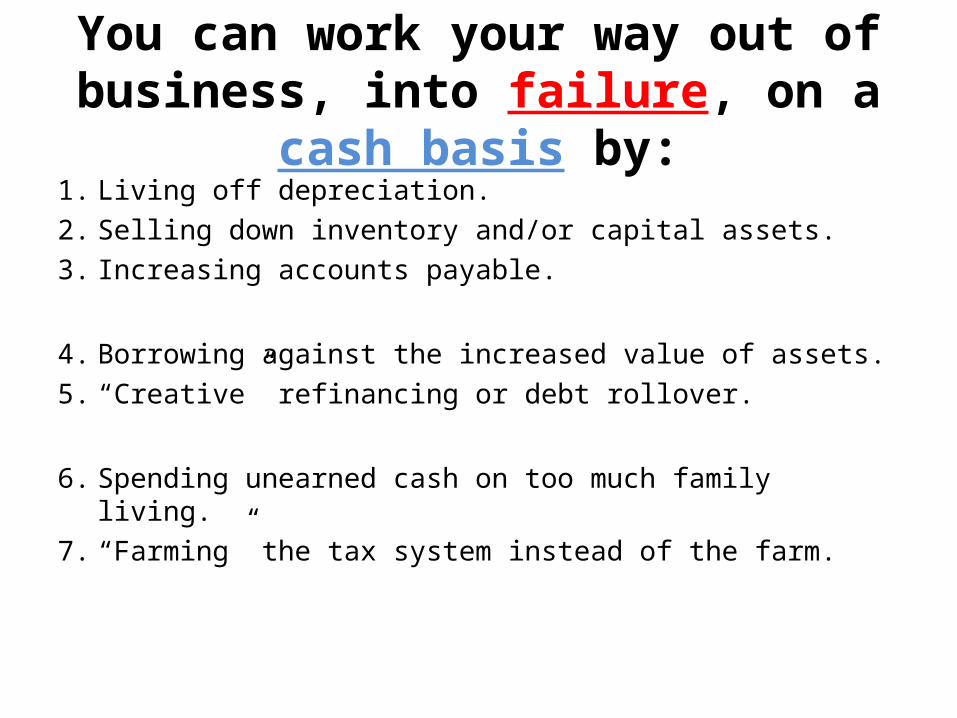

You can work your way out of business, into failure, on a cash basis by:

1. Living off depreciation.2. Selling down inventory and/or capital assets.3. Increasing accounts payable.

4. Borrowing against the increased value of assets.5. “Creative” refinancing or debt rollover.

6. Spending unearned cash on too much family living.7. “Farming” the tax system instead of the farm.

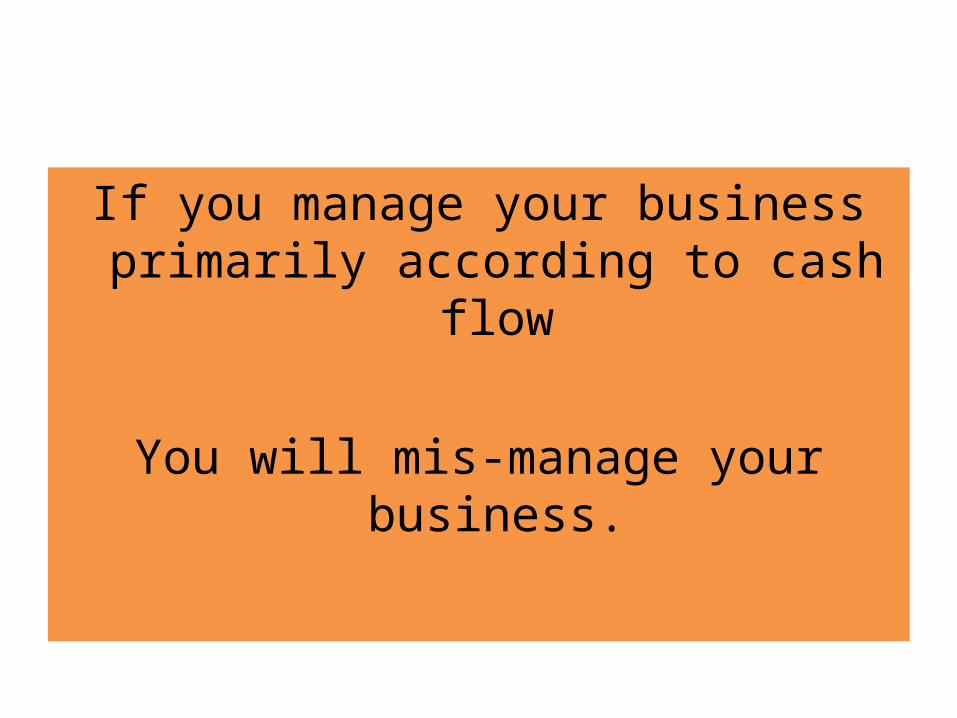

If you manage your business primarily according to cash flow

You will mis-manage your business.

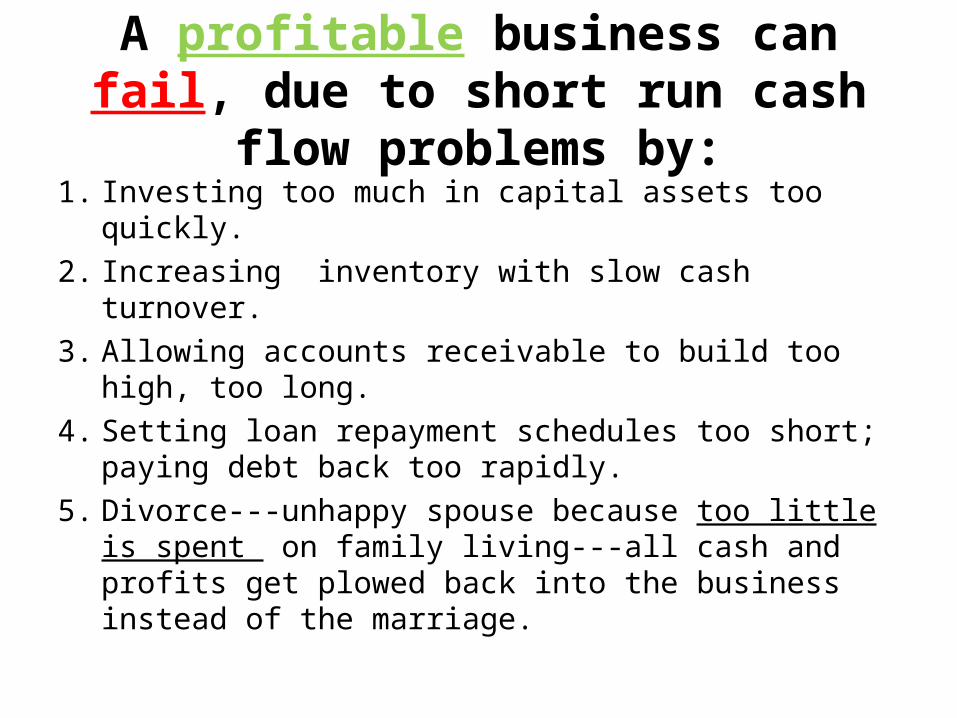

A profitable business can fail, due to short run cash flow problems by:

1. Investing too much in capital assets too quickly.2. Increasing inventory with slow cash turnover.3. Allowing accounts receivable to build too high, too

long.4. Setting loan repayment schedules too short; paying

debt back too rapidly.5. Divorce---unhappy spouse because too little is spent

on family living---all cash and profits get plowed back into the business instead of the marriage.

Equity, Balance Sheets, Your Lender and You

by Dr. Arnold Oltmans, Associate ProfessorAgricultural and Resource Economics,

NC State University.January 11, 2011

Summer Green Show of NCNLA, Greensboro, NC

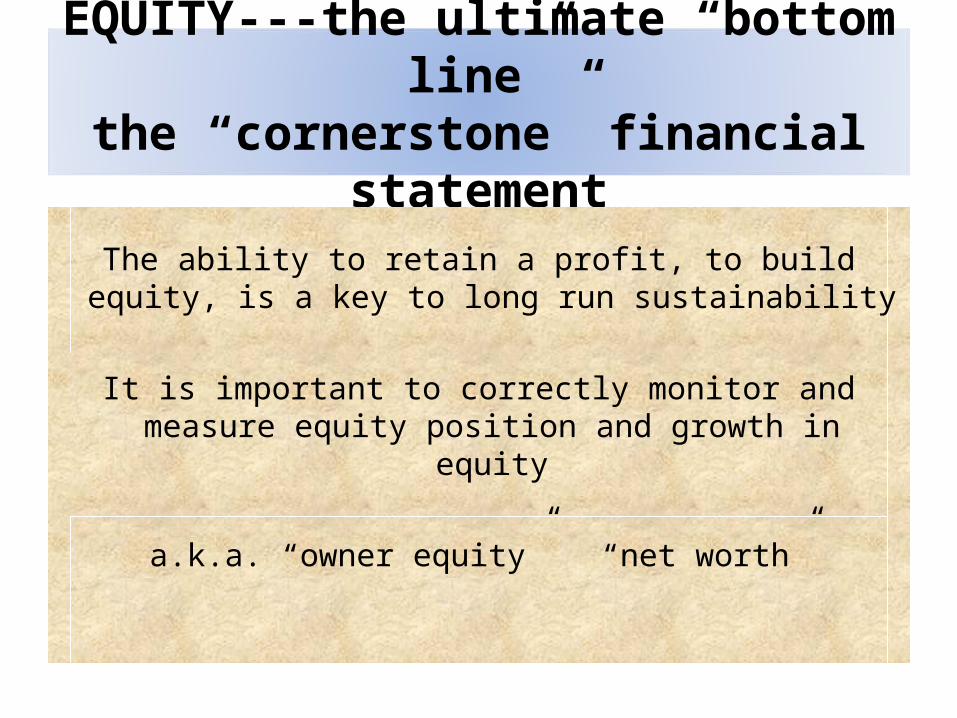

EQUITY---the ultimate “bottom line”the “cornerstone” financial statement

The ability to retain a profit, to build equity, is a key to long run sustainability

It is important to correctly monitor and measure equity position and growth in equity

a.k.a. “owner equity” “net worth”

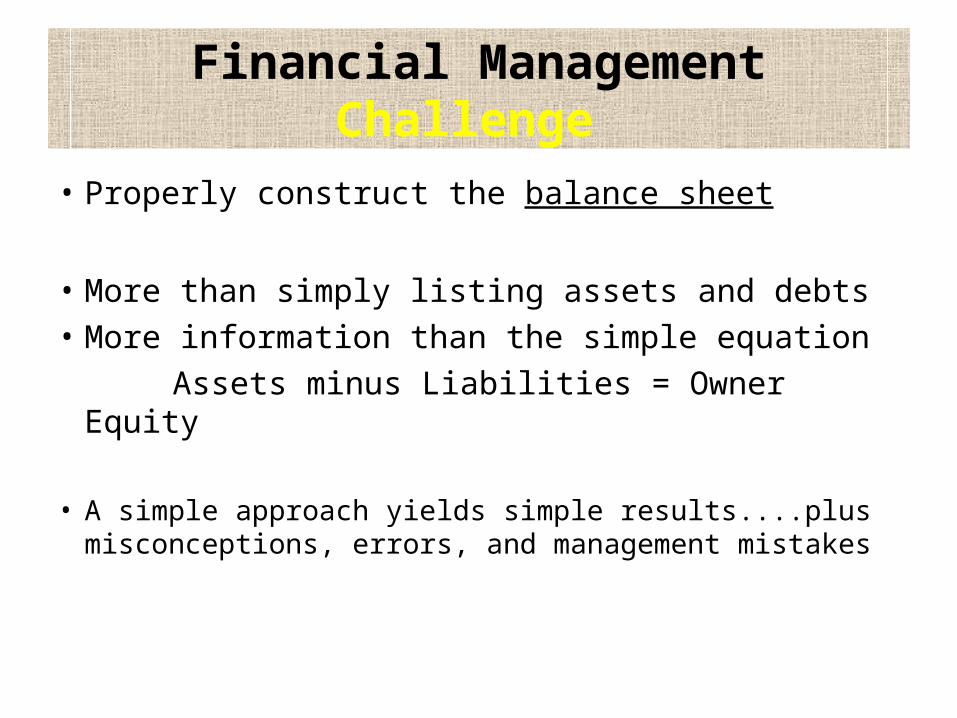

Financial Management Challenge

• Properly construct the balance sheet

• More than simply listing assets and debts• More information than the simple equation Assets minus Liabilities = Owner Equity

• A simple approach yields simple results....plus misconceptions, errors, and management mistakes

Balance Sheet– Key Concepts

1. Balance sheets are done primarily for management purposes---not for lenders.

2. Timing is important.---need to be done consistently—same time each

year---staggered dates can yield misinformation---December 31 or other year-end = necessary

Balance Sheet– Key Concepts

3. Should contain both Cost and Market Value information on assets.

---Asset valuation and interpretation is the toughest and most important part of balance sheet preparation.

(recall the financial crash of 2008-2009—trillions of dollars of mistakes---and the farm financial crisis of 1980s)

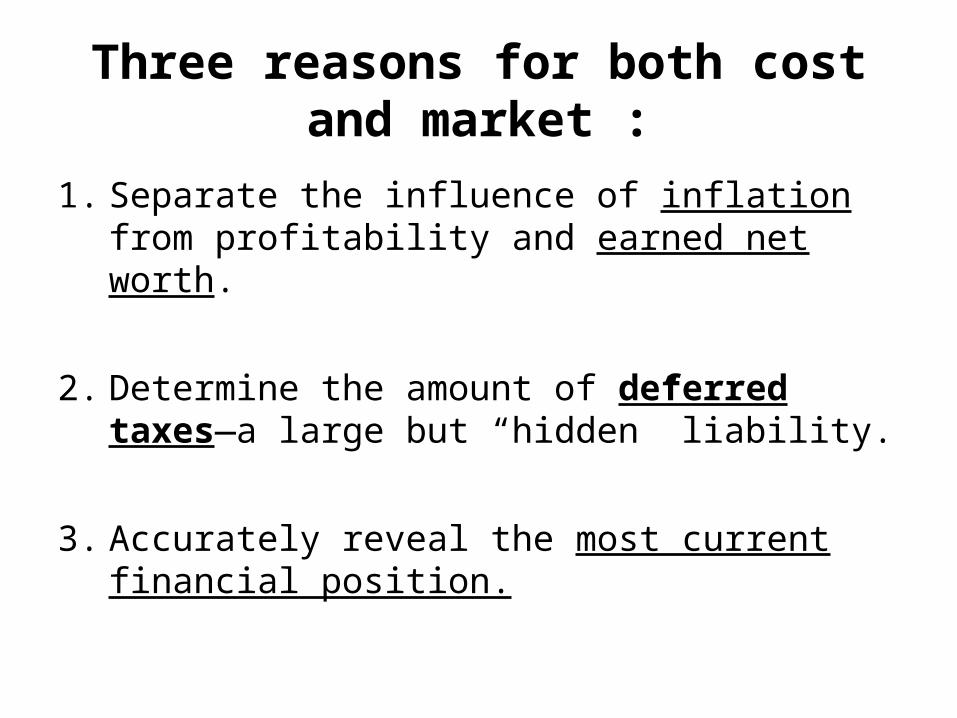

Three reasons for both cost and market :

1. Separate the influence of inflation from profitability and earned net worth.

2. Determine the amount of deferred taxes—a large but “hidden” liability.

3. Accurately reveal the most current financial position.

Balance Sheet– Key Concepts

4. Business and Personal financial information should be separated.

---identify business progress apart from outside personal activity.

5. Current and non-current categories are needed.---in order of declining liquidity

Balance Sheet– Key Concepts

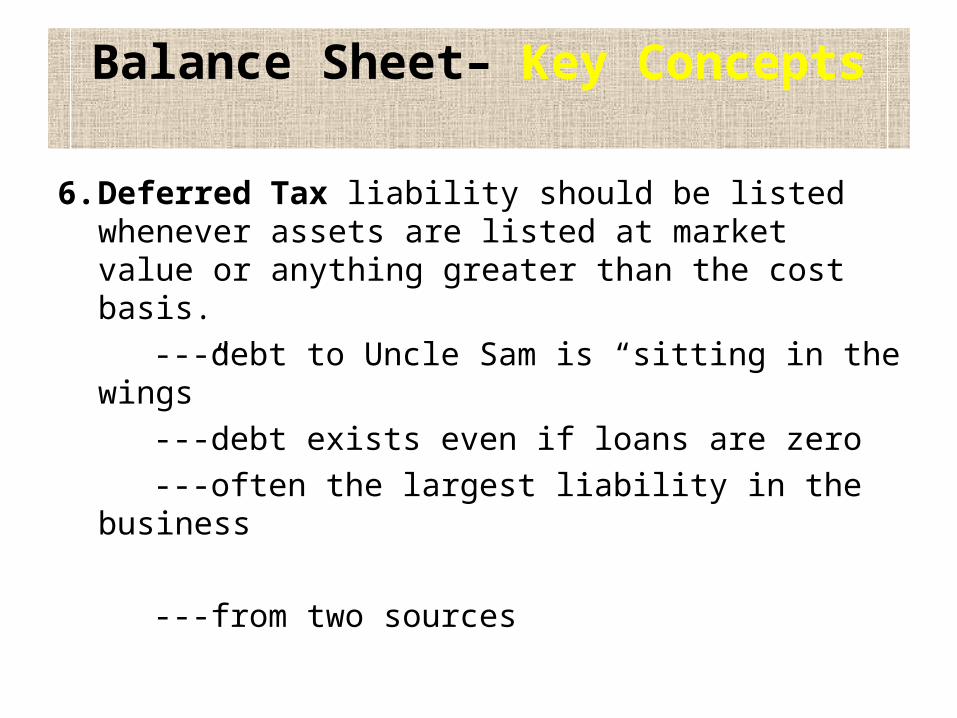

6. Deferred Tax liability should be listed whenever assets are listed at market value or anything greater than the cost basis.

---debt to Uncle Sam is “sitting in the wings” ---debt exists even if loans are zero ---often the largest liability in the business

---from two sources

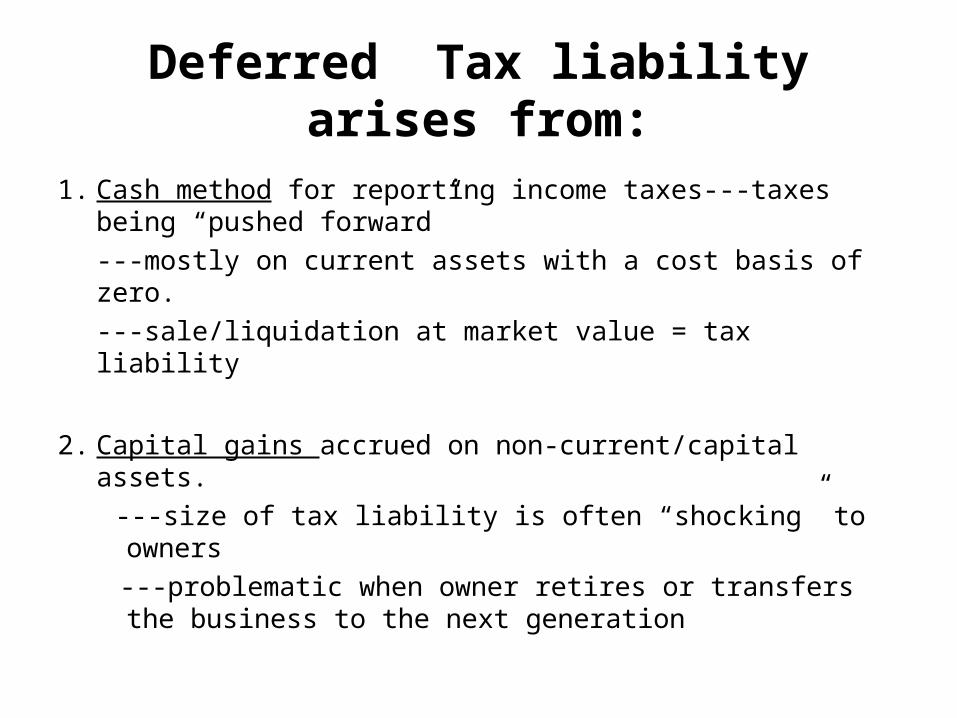

Deferred Tax liability arises from:

1. Cash method for reporting income taxes---taxes being “pushed forward”---mostly on current assets with a cost basis of zero.---sale/liquidation at market value = tax liability

2. Capital gains accrued on non-current/capital assets. ---size of tax liability is often “shocking” to owners ---problematic when owner retires or transfers the

business to the next generation

Balance Sheet– Key Concepts

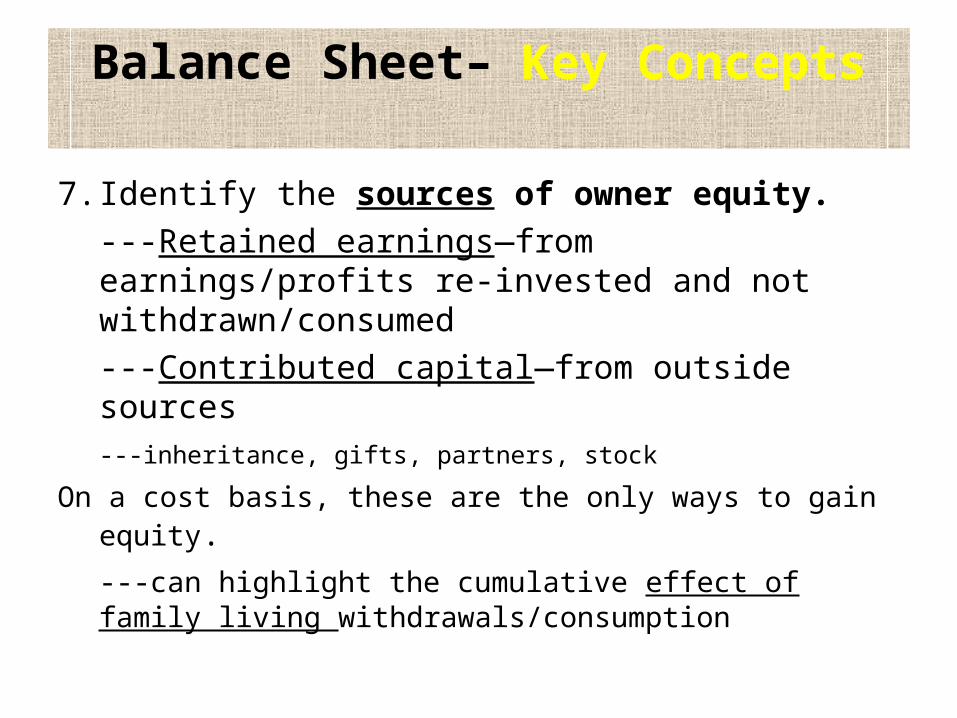

7. Identify the sources of owner equity.---Retained earnings—from earnings/profits re-invested and not withdrawn/consumed---Contributed capital—from outside sources

---inheritance, gifts, partners, stock

On a cost basis, these are the only ways to gain equity.---can highlight the cumulative effect of family living withdrawals/consumption

Balance Sheet– Key Concepts

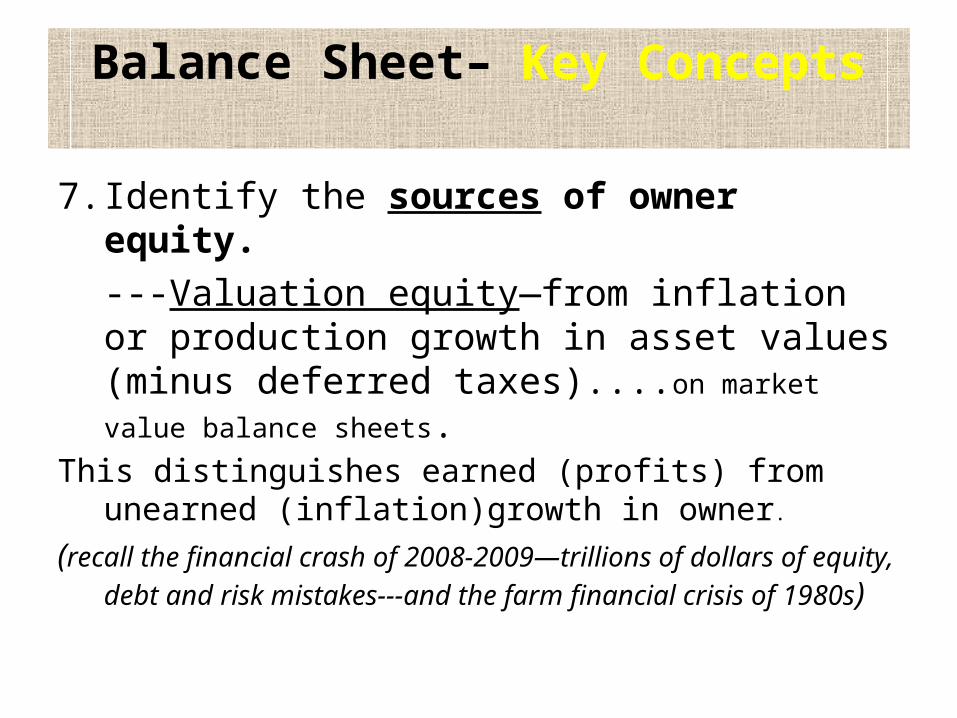

7. Identify the sources of owner equity.---Valuation equity—from inflation or production growth in asset values (minus deferred taxes)....on market value balance sheets.

This distinguishes earned (profits) from unearned (inflation)growth in owner.

(recall the financial crash of 2008-2009—trillions of dollars of equity, debt and risk mistakes---and the farm financial crisis of 1980s)

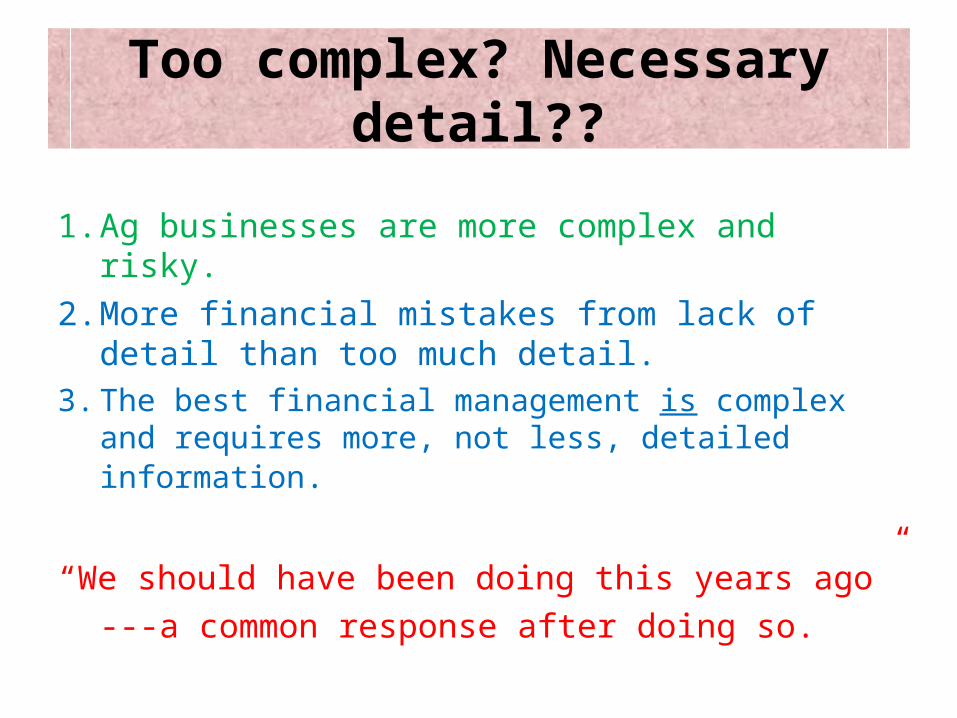

Too complex? Necessary detail??

1. Ag businesses are more complex and risky.2. More financial mistakes from lack of detail

than too much detail.3. The best financial management is complex and

requires more, not less, detailed information.

“We should have been doing this years ago”---a common response after doing so.