Embed Size (px)

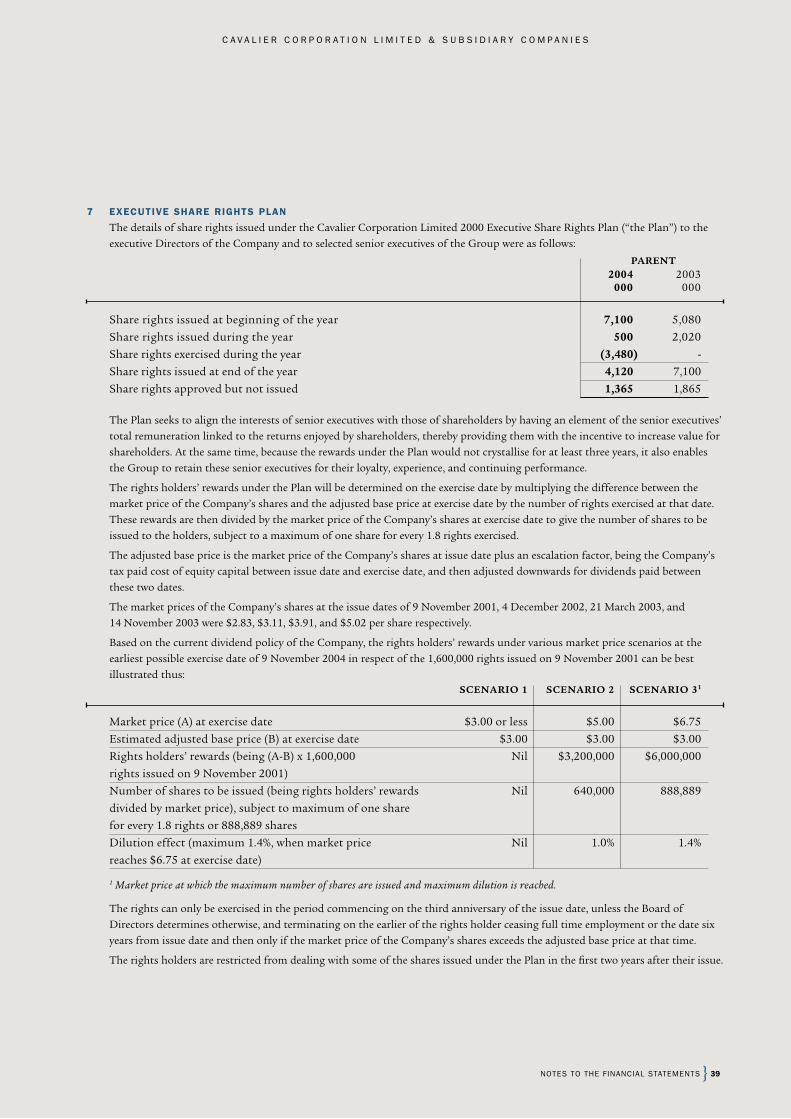

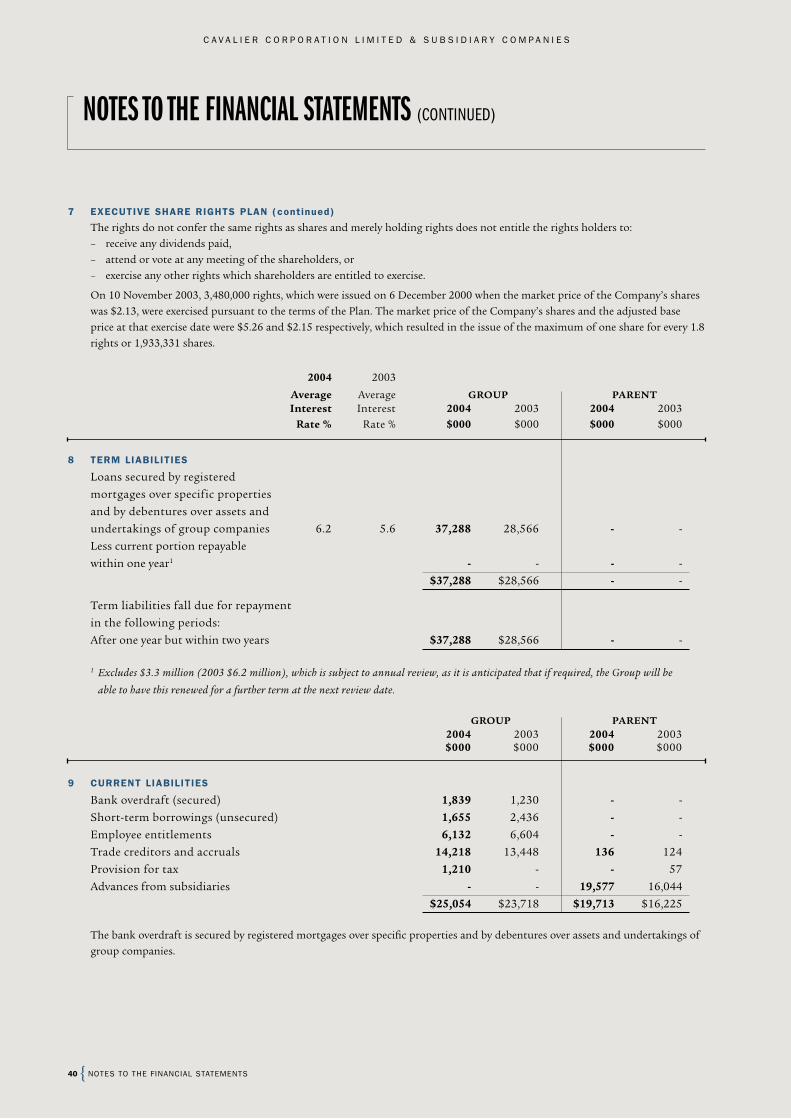

Citation preview

— Jerome Abelardo — Bevan Abraham — Jared Adam — Janine Adams — Pauline Afaese — Agaimalo Afoa — Derek Ainge — Dean Aitken

— Ajang Ajang — Shamina Ali — Thwahir Ali — Margaret Ali-Khan — Ezio Allemano — Murray Allen — Elaine Allsop — Michael Alogi — Victoria Alogi — Malama Amituanai — Tiana Amosa — Colin Anderson — Andy Anderson — Makalio Antonio — Sarah Apuwai — Jason Araia — Neil Archibald — Tangata Arioka — Shaun Armstrong — Malcolm Arnold — Trevor Arnold — Terry Arnott — Dale Arrowsmith — Fiona Aston — Kava Atitoa — John Attwood — Jarmilla Bailey — Gerard Baillache — Carol Baillie — Peter Baker — Debbie Baker — Dorethy Band — Shane Bannon — Tony Barclay — Ian Barnes — Richard Barnes — Kevin Barritt — Robert Barron — Seneuefa Barry — Jennifer Bartle — James Bartlett — Anthony Bates — Kenneth Battiste — Mark Beck — Jeffrey Bee — Sue Beguely — Janet Belcher — Ian Bell — David Bell — Cham Ben — Wayne Bennett — Damon Bennett — Joanne Bennison — Anne-Maria Bergman — Natalie Beuth — Valarie Beuvink — Sally Biddle — Glen Bidlake — Grant Biel — Basil Birch — Jennifer Bird — Deborah Bishop — Trent Blackwell — Virginia Blake — Dave Blakemore — Roy Blood — Darrin Bognuda — Gabriella Bombaci — Douglas Boniface — Brian Borg — Dennis Boston — Vera Bowey — Grant Bradley — Donald Breckenridge — Michael Bristol — Kerry Bromell — Alan Brough — Mary Brougham — Grace Brown — Nicholas Brown — Lyn Brown — David Brown — Arthur Brown — Barry Bruce — Mark Bryant — Mark Bryant — David Bryson — Leslie Buckley — Rossana Bueno — Johannes Buiter — Bronwyn Bullock — Simon Burgess — Allan Burgess — Sarah Burke — Michael Burn — Darren Burns — Matthew Burton — Kym Butcher — Micheal Butcher — Nicholas Carboon — David Carter — Graeme Catt — Paul Chaplow — Craig Chapman — Helen Charles — Warren Charleston — Carl Charlie — Tangikore Charlie — John Cheyne — Que Chieng — Noel Chilton — Greg Chinnery — Stephen Christensen — Leif Christensen — Claeton Christie — Michelle Christison — Wayne Chung — Mark Clark — Jodie Clark — Dorothy-Ann Clark — David Clark — Garth Clarke — Cindy Cliffe — Eugene Coker — Lance Collelo — Stephen Collie — Leslie Collier — Pheoia Collier — Nigel Collinson — Jim Columb — Clive Commerer — Daniel Comp — Edward Connell — Ian Cook — Trevor Cook — Ron Cooper — Renee Cooper — Sheryl Cooper — Licia Cooze — Bridget Copeland — Mary Corliss — Godfrey Corry — Roland Cotter — Leo Cotterall — David Cotton — Kirsty Courtney — Cowie Crapp — Allan Crawford — Steven Crawford — James Crawley — Steven Croawell — Phillip Crockett — Bruce Culver — Shona Cumming — Ian Cunningham — Kevin Dalby — Thomas Daniel — Joseph Dansey — Benjamin Davey — Virginia Davis — Pamela Dawson — Miranda de Boer — John Delautour — Richard Delmarter — David Derrett — Paratene Dewes — Billie Dewhirst — Stefano Di Giovani — Mark Dockary — Robin Dolan — Russell Donaldson — William Doody — John Dowling — Maxwell Downey — Jim Drake — Steven Draper — Brian Drinkwater — Robert Drinkwater — Victor Drollet — Graeme Drummond — Steve Duncan — Lionel Dunkerton — Darren Dunkerton — Peter Duxfield — Shane Eades — Michael Earl — Richard Ebbett — Kirstin Eccles — Wayne Eddington — Lydia Edmonds — Phillip Edwards — Shane Eketone — Pauline Elliott — Khaled Elshall — Leonard Ernst — Gordon Evans — Matthew Ewart — Senio Faasau — Gary Fairweather — David Falanaki — Naofetalaiga Faleapuna — Eapesi Faofua — Akuhata Farmer — Kevin Farquhar — Ross Fata — Michael Fawssett — Tusi Feagaimalii — Brian Ferguson — Avis Ferguson — Anthony Ferguson — Kenneth Ferguson — William Fisher — Cyril Fletcher — Te Aroha Fletcher — Ian Ford — Douglas Forman — Paul Fornusek — Brian Foster — Hiki Fotofili — Nigel Foubister — Maurice Fouhy — Bruce Fright — Jeanette Gardiner — Frank Gardiner — Wayne Garnett — Ben Garnham — Alan Geeves — Joseph George — Stephen Georgiou — Adam German — John German — Myshell Gibbs — Lezanne Gibbs — Daniel Gilbertson — Stuart Gill — Gail Gill — Eliza Gilmour — Elizabeth Godfrey — Louis Godfrey — Bruce Goldsack — David Goodgame — Warren Goodman — Wade Goomes — Darren Gore — Satya Gounder — Alan Graham — Darryl Grant — Richard Grant — Alwyn Grantham — Samuel Green — Wayne Greenall — Sandra Griffin — Gary Griffiths — Rogelio Gultiano — Margaret Haami — Deborah Haddon — Tony Halas — Amokura Halbert — Jay Hales — Nigel Hales — Rodney Hall — Graeme Hall — Nathan Hanaray — Lindsay Hancox — Tony Hand — Gerald Hannan — Kristian Hansen — Tamsyn Hansen-Hill — Sally Hardie — Robert Haren — Mervyn Harrington — David Harris — Steve Harris — Brent Harrison — Steve Harrison — Malcolm Hartley — Brent Hartley — Douglas M. Hastings — Douglas E. Hastings — Pauline Hatch — Karena Hawea — Murray Hawkes — Graeme Hawkins — Jonathan Hawkins — Graham Hazelwood — Jill Heal — Danny Healey — Leanne Hearfield — Darron Heke — Larry Hellyer — Julia Hennessey — Leonard Henwood — Sharon Henwood — Toni Henwood — Nathaniel Heron — James Hetaraka — Vaughn Higgs — Denise Hiku — Shiree Hina — Marcus Hinsley — Michael Hintze — Kate Hodges — Trevor Hofmann — Roger Hofmann — Dianne Hofmann — Paul Hogenesch — Robert Holland — Robert Holland — Mark Holleron — John Holmes — Melissa Hong — Malcolm Hooker — Carl Hoskin — Sharon Howe — D’Jaye Howe — Cathy Howitt — Geoffrey Hucker — Kelvin Hunt — Ake Hunter — Te Koki Hura — Michelle Hutchinson — Geoffrey Ingram — Rodney Jack — Glen Jackson — Alan James — Lisa-Marie Jamieson — Andrew Jellyman — Neil Jenkinson — Clive Jensen — Philip Jermy — Luke Jessop-Smith — Walter Joe — Jan Johnson — Brian Johnston — Lee Jones — Ron Jones — Kevin Jones — Louella Joseph — Aaron Jury — Siuaki Kaafi — William Kabakaba — Pemika Kaewsomnuk — Sagar Kakade — Andrew Karl — Jasbir Kaur — Harpreet Kaur — Alvin Keen — Zane Keen — Edward Keil — Derek Kelly — Kurt Kelsey — Michael Kemp — Anne Kendal — John Kerekere — Daniel Kersten — Geoff Kessick — Dianne King — Maria King — Vernon King — Verna Kingi — Jan Kingi — Adrian Kiwara — Jonathan Kroeger — Ashwin Kumar — Mirek Kuncl — Alwyn Ladd — Motusaga Laga’aia — Paepae Lalogafau — Fagaofiti Lalogafau — Laurence Lambert — John Lane — Nicholas Largent — Anthony Larosa — Noel Larsen — Aneti Laulu — Leo Lauofo — Evo Lave — Mark Lawrence — Hazel Lawrence — Tui Lazarus — Tanginoa Leaaemanu — Armando Lecaros — Talaave Leilua — Tilia Leilua — Ngok Leon — Lealofi Leota — Keke Lesa — Susan Leslie — Taunese Letalu — Rita Leungwai — Phil Leyland — John Liang — Brendan Lingard — Stuart Little — Gary Lockwood — Keith Lodge — Andy Loncar — Brian Lorge — Stephen Loudoun — Shona Luke — Brian Luty — Alison MacDonald — Allan MacErlich — Ian MacKenzie — David Mackie — Winton MacKintosh — Peter Mael — Alfredo Maiquilla — Denis Maniapoto — Felauai Mariota — James Markham — Robin Marshall — Reuben Marsters — Emily Martin — Gary Martin — Suafa Masaga — Marlene Mason — Fualuga Mataituli — Aperahama Matenga — Bill Mathews — Peter Matterson — Gavin Matthews — Jade Matthews — Telesia Matulino — Tony Maurice — Kevin McBrearty — Trevor McBrearty — Regan McCarthy — Peter McClelland — Shane McClure — Barbara McCulloch — Kevin McEldowney — Mark McElroy — Geoffrey McFadzean — Wayne McGillen — James McIlroy — Belinda McInerney — Colin McKenzie — Doreen McKeown — Stephen McKeown — John McKillop — Ross McKimmon — Samantha McLean — Linda McNatty — David McNaughton — Margaret Mead — Valerie Mead — Terence Meenehan — Eleni Meimaris — Jane Meleisea — Adrian Merrall — Michael Merrick — James Metekingi — James Mfula — Kevan Miles — Rochell Miller — Kym Milne — Tanya Milne — Rima Mitchell — Arthur Mitchell — Daniel Mitchell — Michael Mitchell — Sherry Moevao — John Monroe — Graham Moore — Alan Morris — Wayne Morris — Cameron Morris — Owen Morrison — Kathryn Morton — Salujean Mua — Luisa Mulipola — France Mulvey — Allan Munro — Sharon Murdoch — Stewart Murphy — Colin Murray — Alexander Murray — Sitina Nansen — Stewart Nash — Paki Neels — Pania Neels — Graham Neilson — Tita Ng Shiu — Tasesa Ng Shiu — John Ngchok — Taolima Ngchok — Moeroa Nia — Tony Nicholson — Karen Nielson — Rodney North — Adam Northcroft — Michael O’Leary — Keelan O’Connell — Trina Ormsby — Lonsean Ouk — Rim Ourng — Terrence Owen — William Owen — Gay Owen — Louise Page — Neil Palmer — Arnulfo Palmon — Michele Panchartek — Letitia Paparoa — Ashok Parbhu — Murray Parker — Stephen Parker — Perry Parnham — Allen Parsons — Emily Parsons — Craig Partridge — Nayna Patel — Tony Patmore — Chris Pattison — Russell Paul — Michael Payne — Efi Peapea — Coran Pemberton — Noeun Peng — Fiona Pentecost — John Pepper — Matai Pere — Richard Pereniko — Dion Perry — Douglas Perston — John Pervan — Raymond Peters — Grant Peterson — David Philippe — Reginald Phillips — Allan Pierce — Talosaga Pio — Jolene Pitman — Bowman Ponga — Gordon Porter — Ruisa Potoru — Mata Potoru — Jim Pouros — Panapa Poutawa — Rodney Powell — Michael Powell — Nicole Prampromis — Stephen Prichard — Foalele Pritchard-Apulu — William Puhara — Daniel Puhara — Tuatea Punua — Hera Puohotaua — Marianne Putairi — Gregory Pye — Gary Raison — Melissa Randall — Ross Rapson — Tamati Rarere — Peter Raymond — Brian Reeder — Lynette Reeve — William Rerekura — Sheryn Rerekura — Dean Reti — Mohi Reti — Haimona Reweti — Samuel Rewi — Donna Reyes — Andrew Richardson — Kula Ridd — Mataiapo Rima — Barry Ritchie — Janice Ritchie — Riki Ritchie — Doreen Roache — Rhonda Roberts — Thomas Robertson — Garry Robertson — Henrietta Robinson — Tony Robinson — Frank Rochat — Alan Rodda — Michael Rodda — John Rodgers — Rosa Roebeck — Joy Rollinson — Ian Rollinson — Carol Rosewarne — Rachael Ross — Colleen Ross — Jan Ross — Duncan Ross — Charles Ross — John Ross — Gregory Routh — Shannon Routh — David Rowlinson — Tangata Ruatoe — Tuapikepike Ruatoe — Richard Rumpler — Susan Rusbridge — Stuart Rush — Catherine Russell — Graham Rutledge — Edward Ryan — James Ryan — Bobby Sadaraka — Graeme Sage — Meafou Saleupolu — Filifili Samuelu — Darryl Sandri — Elisapeta Sanele — Abundio Sarsonas — Cheval Sauer — Selwyn Savage — Stuart Scott — Nadine Scott — Brian Scott — Judith Sellar — Chunthea Sey — Ann Shadbolt — Peter Shaw — Irene Shaw — Aaron Shears — Rehana Shekhumia — Janeen Shepherd — Dean Sherwood — Aaron Sherwood — Peter Shuker — Janice Simpson — David Sinclair — Janhom Sirikhun — Jeremy Small — Robert Smith — Ian Smith — Brent Smith — Gordon Smith — Gavin Smith — Donald Smith — Stephen Smithard — Christina Soga — Kruy Sok — Melinda Soo — Ben Sorenson — Somchanh Souksavong — Somphone Souksavong — Mark Spence — Mary Spillane — Christine Spooner — Paul Spooner — Raey Stairmand — Shane Stampa — Philip Stent — Abraham Stephens — Peter Stevens — Hayden Stevenson — Antoinette Stewart — Susan Stewart — Blair Stitson — Dominie Stock — Karolyn Stok — Susan Stow — Cindy Stuart — Sam Suksavong — Leon Summerfield — Huo Sun — Adrian Sundman — Karen Sundman — David Tahana — Sydney Taiaroa — Faamao Taiivao — James Tait — Dorothy Takerei — David Takiaho — Sesilia Talivaa — Victor Tan — Susana Taugaai — Atahere Taurima — Rangitere Taurima — Tracy Teague — Maria Temu — Lukin Tengu — Nooroa Terei — Linda Terongomau — Vanessa Tewaa — Van Thai — Curtis Thin — Kane Thomas — Kenneth Thomas — Sarah Thompson — Lavinia Thompson — John Thompson — Alan Thompson — Ivan Thomson — Keith Thorpe — Riwaru Tihema — Inano Tikinau — Tony Timpson — Eddie Timu — Luke Tither — Elisala Toai — Aranui Toatoa — Anarosa Tofaeono — Dorothy Togiatau — Matapakia Tom — Andrew Toohey — Gary Topless — Thoung Tran — Dale Transom — Keriann Trask — Karen Travers — Hamish Tristram — Andrew Tristram — Toe Tua — Misitopa Tuala — Jeremy Tuck — Salatielu Tupuono — Eunike Tupuono — Sina Turner — Kenneth Turner — Terry Tusani — Mereana Tutira — Henry Tyler — Anne Ualiu — Raera Umaki — Peter Vear — David Vernall — Prasad Vinay — Gerry Voskamp — Joshua Wakefield — Anthony Walker — Andrew Walker — Raewyn Wallace — Selwyn Wallace — Phillip Walsh — Lindsay Ward — Michael Ward — Patrick Warren — Anthony Waters — Bruce Watson — Peter Watterson — Lynley Webb — Warren Welch — Malcolm Wells — Donna Whatu — Lynette Wheeler — Alan Whittaker — Noel Wilkins — Gareth Williams — Mikayla Williams — John Williams — Atapana Williams — Patrick Williams — David Williams — Joyce Williamson — Ian Williamson — Robert Wilson — Kevin Wilson — John Wilson — Bruce Wilson — Vanessa Wilson — Alan Wilson — Grant Wilson — Trish Wilson — Melody Winiata — Nicolas Winter — Daniel Withers — Shane Wood — Craig Woolford — Nigel Worthington — Fiona Worthington — Fraser Wright — Grant Wrightson — Peter Yandall — Tony Yee — Stanley Yee — Jimmy Yee — Michael York — Chris Young — Douglas Young — Phillip Young

CAVALIER CORPORATION IS PROUD OF ITS PEOPLE

AND THANKS THEM FOR THEIR CONTRIBUTION

CA

VALIER

CO

RP

OR

ATION

LIMITED

— A

NN

UA

L REP

OR

T 20

04

ANNUAL REPORTFOR THE YEAR ENDED 30 JUNE 2004

C A V A L I E R C O R P O R A T I O N L I M I T E D

CAVALIER CORPORATION KNOWS CONSISTENT

FINANCIAL RESULTS ARE NOT ACHIEVED IN ISOLATION.

THEY ARE PART OF A WHOLE — THE RESULT OF MANY

EVENTS AND DECISIONS, MANY CONNECTIONS

CONNECTED WITH SUCCESSINTRODUCTIONANNUAL REPORT 2004

Cavalier’s ongoing success is no accident. It is the result of many connected events and

decisions, all of which contribute to a company with a solid performance history and a bright

future. The members of Cavalier’s management team have a strong working relationship. They

know the challenges and potential in their industries because these are industries they have

helped shape. The most important connection is the one that happens out in the marketplace.

Our customers connect with our brands, and they connect these brands with success.

THE 2004 ANNUAL REPORT OF CAVALIER CORPORATION LIMITED is presented in a single document

containing both the Annual Review and the Financial Statements and Other Disclosures. As

required by section 211(1)(k) of the Companies Act 1993, this document is signed on behalf of the

Board on 17 September 2004 by :

A M JAMES — CHAIRMAN W K CHUNG — MANAGING DIRECTOR

MANAGING DIRECTOR’S

REVIEWPg.4 CAVALIER

AND THE ENVIRONMENT

Pg.8 HEALTH & SAFETY

AT CAVALIERPg.10

CORPORATE:

Managing Director W K Chung

Finance Director and Company Secretary V T S Tan

Information Services Manager M N McElroy

CARPET OPERATIONS:

CAVALIER BREMWORTH:

Australian General Manager D M Cotton

Australian National Sales Manager K R Battiste

Australian Finance and Administration Manager M O Hintze

New Zealand General Manager Sales S J Duncan

Market Planning Manager C Anderson

Group Marketing Manager D W Philippe

General Manager Manufacturing C A McKenzie

Tufting Plant Manager G J M Voskamp

Wanganui Spinning Plant Manager D J Blakemore

Napier Spinning Plant Manager P N Shuker

Product Development Manager P A Leyland

New Zealand Financial Controller J C Johnson

KNIGHTSBRIDGE CARPETS:

Manager B R Smith

KIMBERLEY CARPETS:

Manager M A Bryant

ONTERA MODULAR CARPETS:

General Manager E Allemano

Commercial Manager G A McFadzean

WOOL OPERATIONS:

HAWKES BAY WOOLSCOURERS:

General Manager N R Hales

CANTERBURY WOOLSCOURERS:

General Manager S J Harrison

ELCO DIRECT:

General Manager R P Cooper

C A V A L I E R C O R P O R A T I O N L I M I T E D & S U B S I D I A R Y C O M P A N I E S

1##FOOTER##

C A V A L I E R C O R P O R A T I O N L I M I T E D

TABLE OF CONTENTSANNUAL REVIEW FINANCIAL STATEMENTS AND OTHER DISCLOSURES

PERFORMANCE HIGHLIGHTS 2

MANAGING DIRECTOR’S REVIEW 4

MANAGING DIRECTOR’S QUESTION AND ANSWER 13

DIRECTORS’ REPORT 16

BOARD OF DIRECTORS 20

CORPORATE GOVERNANCE 21

SHAREHOLDER INFORMATION 24

CONTENTS 27

AUDIT REPORT 28

DIRECTORS’ RESPONSIBILITY STATEMENT 29

STATEMENT OF ACCOUNTING POLICIES 30

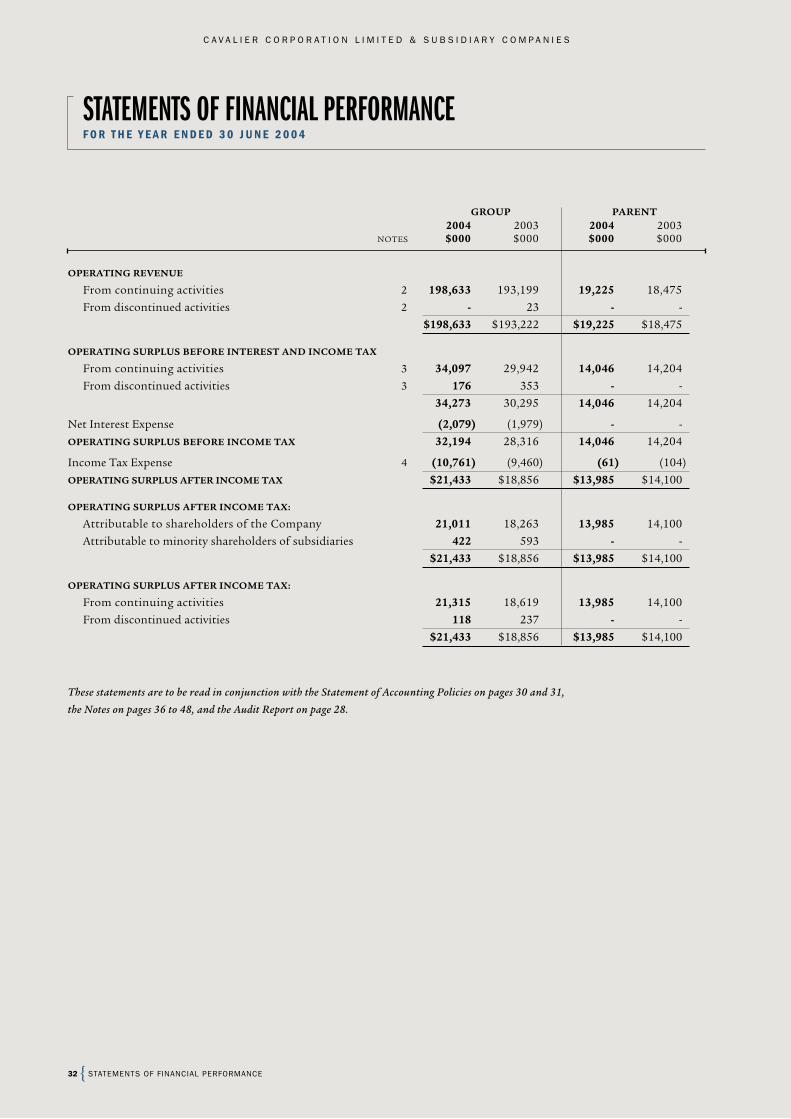

STATEMENTS OF FINANCIAL PERFORMANCE 32

STATEMENTS OF MOVEMENTS IN EQUITY 33

STATEMENTS OF FINANCIAL POSITION 34

STATEMENTS OF CASH FLOWS 35

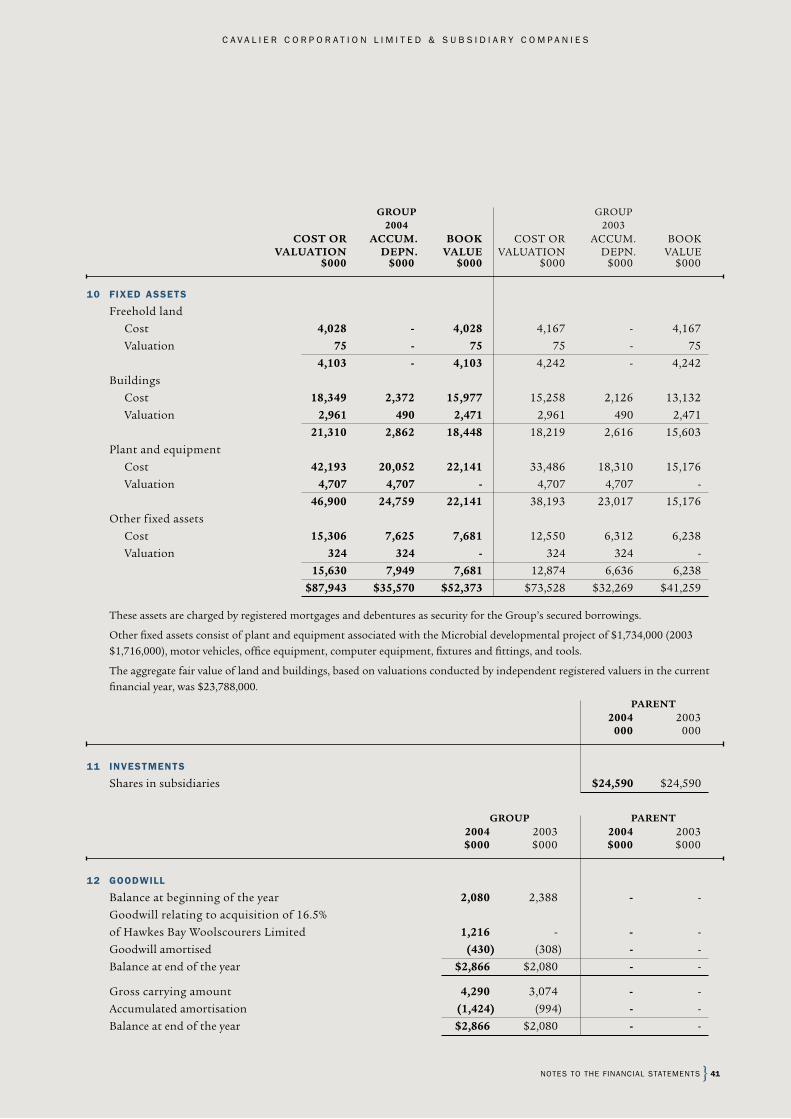

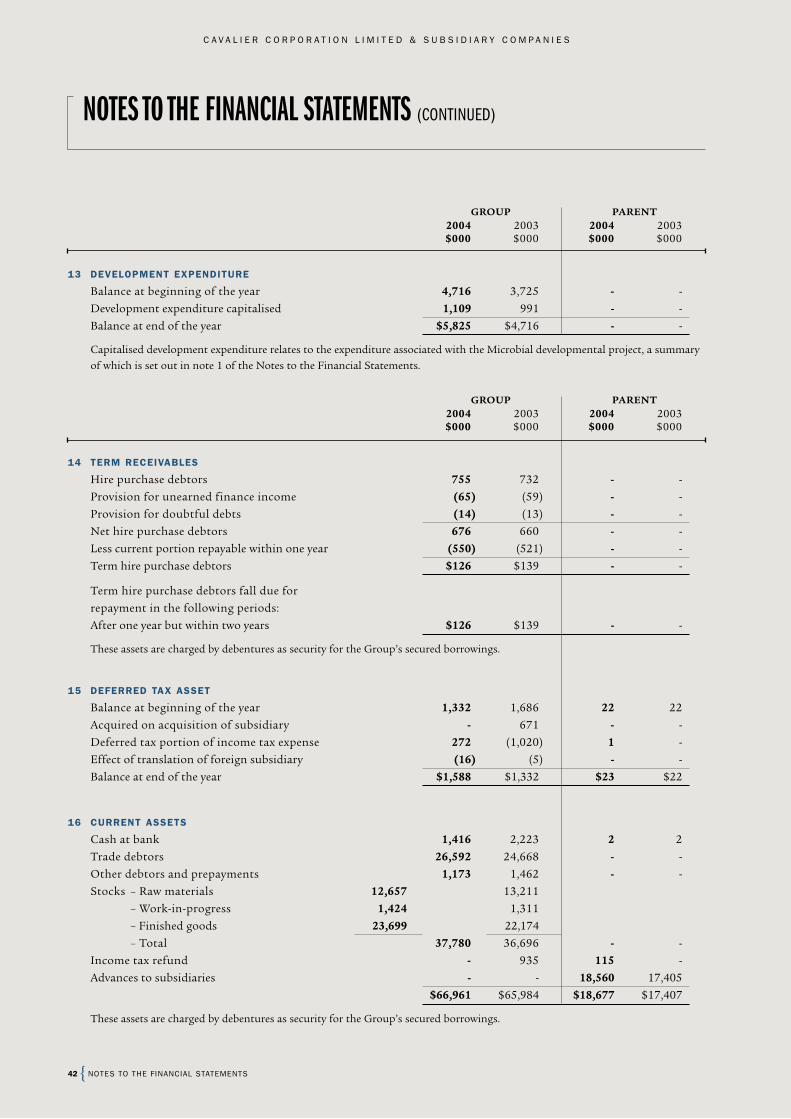

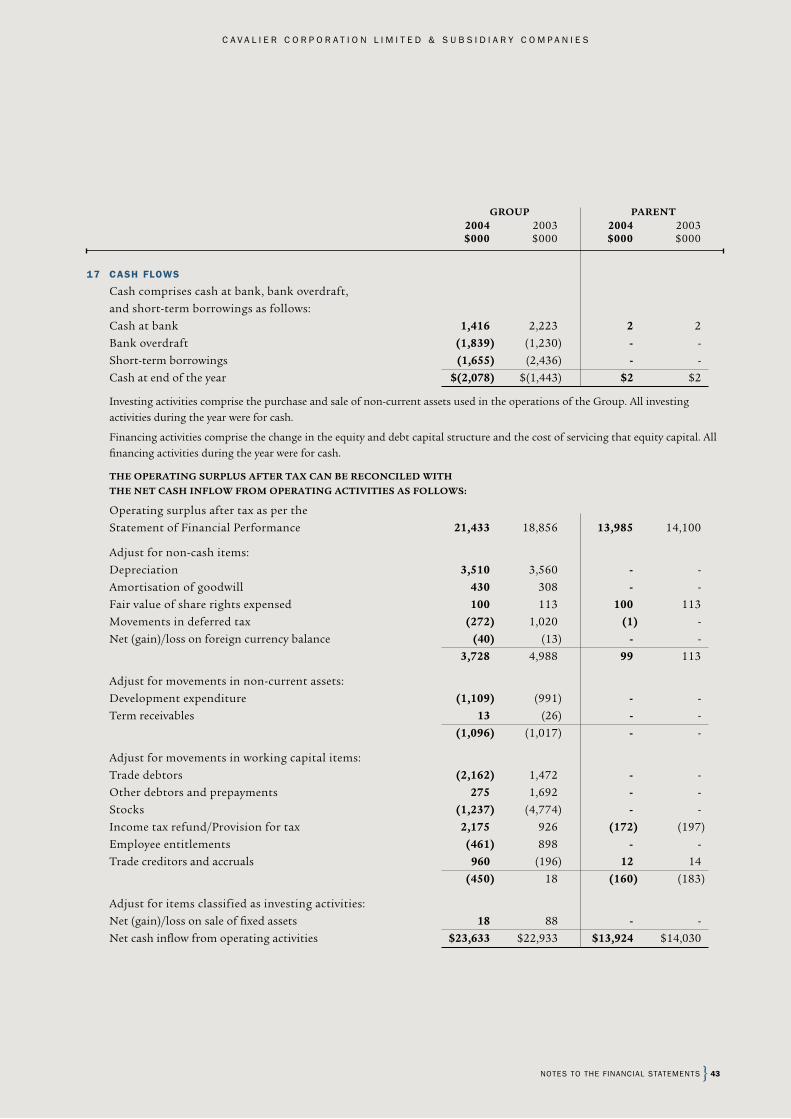

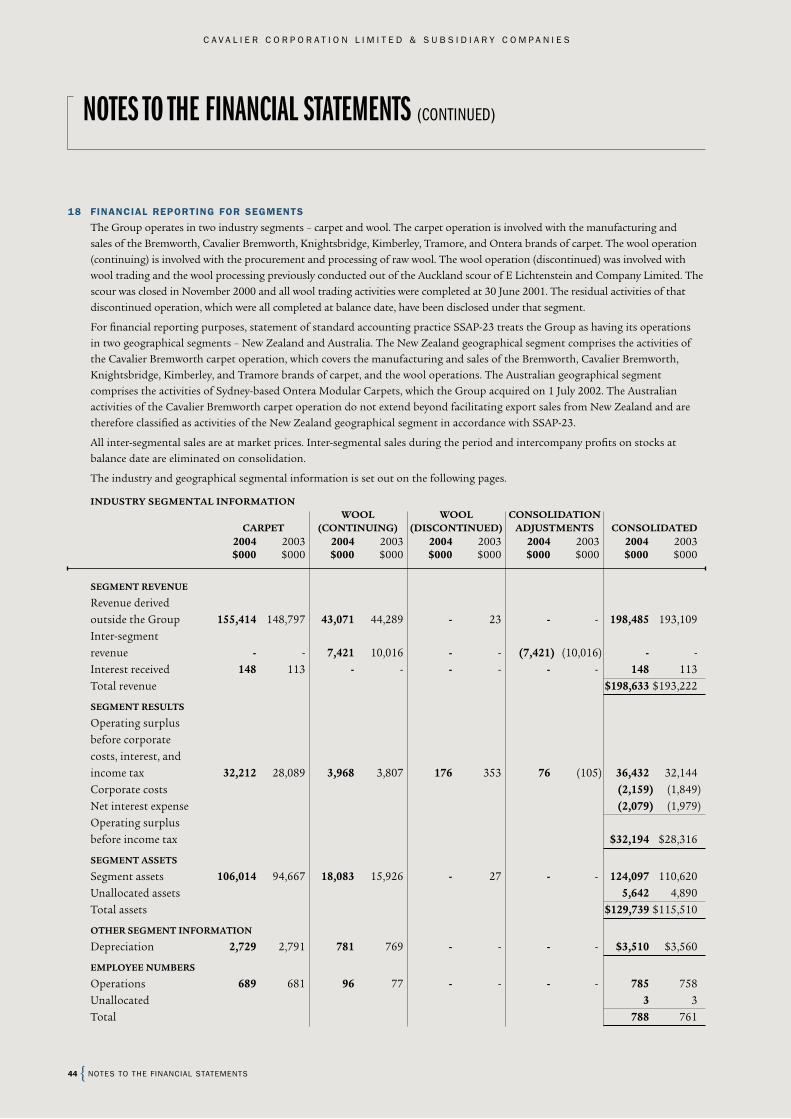

NOTES TO THE FINANCIAL STATEMENTS 36

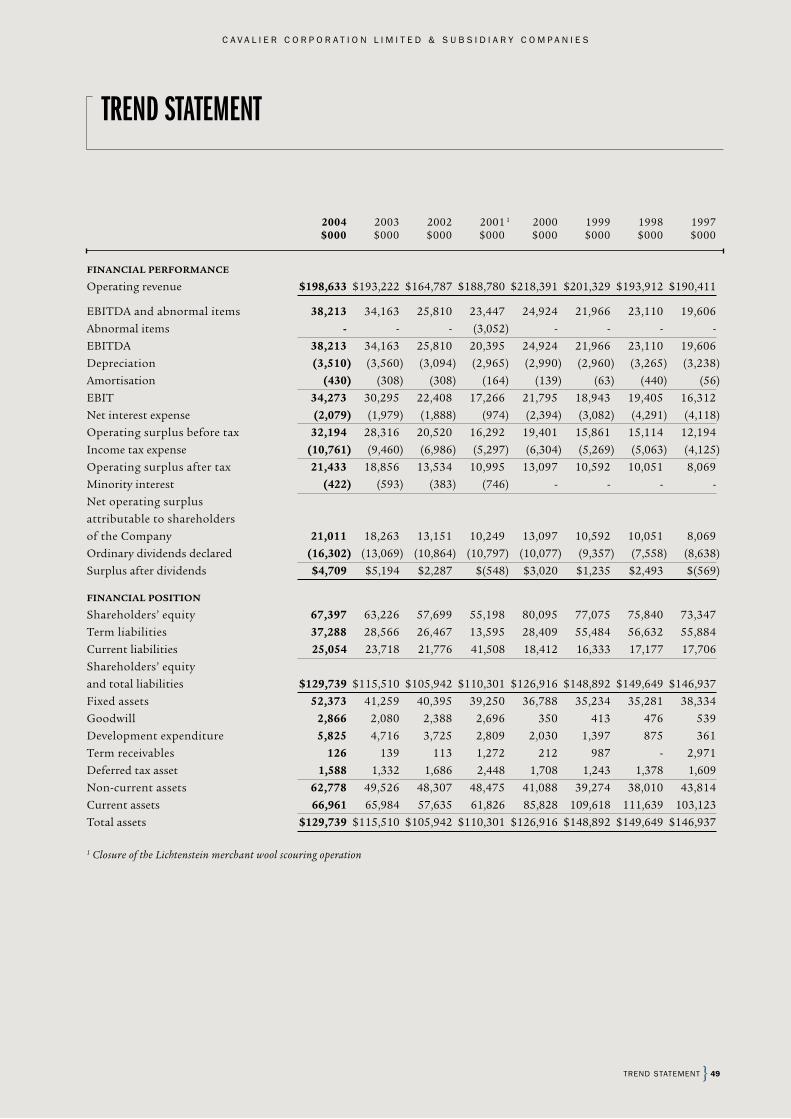

TREND STATEMENT 49

GLOSSARY OF FINANCIAL TERMS 51

OTHER DISCLOSURES 52

CORPORATE DIRECTORY 60

MANAGING DIRECTOR’S

Q&APg.13 DIRECTORS’

REPORTPg.16

134.5

8

SHAREHOLDER INFORMATION

Pg.24

C A V A L I E R C O R P O R A T I O N L I M I T E D

2

Record operating surplus after tax

and minority interest of $21 million

— 15% up on the previous year’s

$18.3 million — on operating revenue

of $198.6 million

RECORD OPERATING

SURPLUS

$21MILLION

S T R A T E G I C V I S I O N S H A R E H O L D E R V A L U E

PERFORMANCEHIGHLIGHTS

Acquisition, just after balance date,

by 92.5%-owned subsidiary, Hawkes

Bay Woolscourers, of 50% interest in

Canterbury Woolscourers, a company

formed to acquire and consolidate two

South Island scours based in Winchester

and Washdyke

WOOLSCOURINGPURCHASE

%50OF CANTERBURYWOOLSCOURERS

Earnings per share of 32.7 cents,

compared with 29.0 cents a year ago

IMPROVEDEARNINGS

PER SHARE ¢3.7INCREASE

Return on funds employed of 21.4%,

compared with 21.6% a year ago and

16.4% and 12.4% for the two years

preceding that year — with each to

be compared against the Group’s

estimated weighted average cost of

capital of 10%

RETURN ON FUNDSEMPLOYED 21.4

PERCENT

Record contribution to Group’s pre-tax

operating surplus by the Cavalier

Bremworth broadloom carpet business

and the Ontera modular carpet

operation of $28.7 million and

$3.5 million respectively

RECORD CARPET

RESULTS32.2MILLIONCOMBINED

Capital spends of $15.2 million,

including the semi-worsted yarn plant

at Wanganui, the new carpet tufting

equipment at Cavalier Bremworth’s

Auckland site and the state-of-the-art

dye-injection machinery at Ontera’s

Sydney plant

STRATEGICCAPITALSPENDS

Record fully imputed dividends

authorised for the year of 27 cents

per share, an increase of 8% on

the 25 cents per share for the

previous year

INCREASE INDIVIDENDSPER SHARE

$23.6 million net cash inflow from

operating activities, up from $22.9

million the previous year

OPERATINGNET CASH

INFLOWReturn on average shareholders’ equity

of 32.8%, compared with 31.2% and

24.0% for the immediately preceding

two years

RETURN ONSHAREHOLDERS’

EQUITY 32.8PERCENT

8PERCENT

$23.6MILLION

$ $15.2MILLION

PERFORMANCE HIGHLIGHTS

3

C A V A L I E R C O R P O R A T I O N L I M I T E D

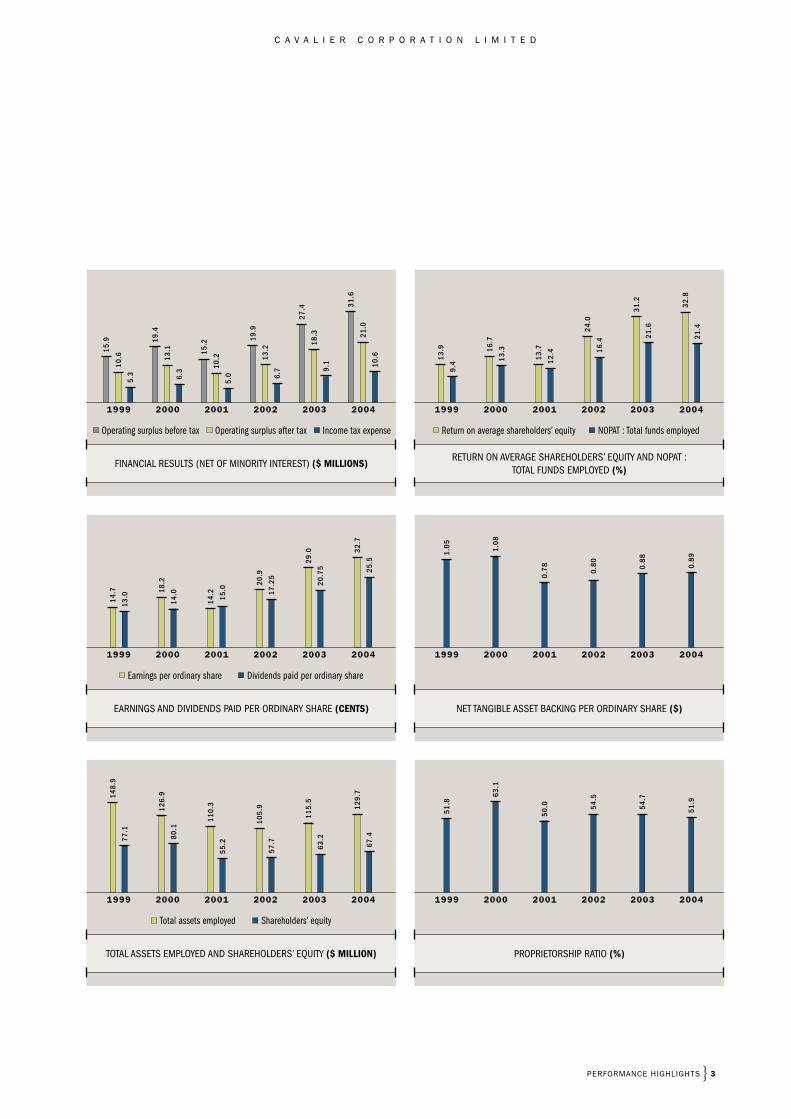

1999

15.9

10.6

5.3

2001

15.2

10.2

5.0

2002

19.9

13.2

6.7

2003

27.4

18.3

9.1

2004

31.6

21.0

10.6

2000

19.4

13.1

6.3

1999

13.9

9.4

2001

13.7

12.4

2002

24.0

16.4

2003

31.2

21.6

2004

32.8

21.4

2000

16.7

13.3

FINANCIAL RESULTS (NET OF MINORITY INTEREST) ($ MILLIONS)RETURN ON AVERAGE SHAREHOLDERS’ EQUITY AND NOPAT :

TOTAL FUNDS EMPLOYED (%)

1999 2001 2002 2003 20042000

NET TANGIBLE ASSET BACKING PER ORDINARY SHARE ($)

1999

14.7

13.0

2001

14.2

15.0

2002

20.9

17.2

5

2003

29.0

20.7

5

2004

32.7

25.5

2000

18.2

14.0

EARNINGS AND DIVIDENDS PAID PER ORDINARY SHARE (CENTS)

1.05

0.78 0.

80 0.88

0.89

1.08

1999

148.

9

77.1

2001

110.

3

55.2

2002

105.

9

57.7

2003

115.

5

63.2

2004

129.

7

67.4

2000

126.

9

80.1

TOTAL ASSETS EMPLOYED AND SHAREHOLDERS’ EQUITY ($ MILLION)

1999 2001 2002 2003 20042000

PROPRIETORSHIP RATIO (%)

51.8

50.0 54

.5

54.7

51.9

63.1

Operating surplus before tax Income tax expenseOperating surplus after tax Return on average shareholders’ equity NOPAT : Total funds employed

Earnings per ordinary share Dividends paid per ordinary share

Total assets employed Shareholders’ equity

PERFORMANCE HIGHLIGHTS

C A V A L I E R C O R P O R A T I O N L I M I T E D

4

A product might be the finest

available, but unless it connects

with the customer’s needs and

expectations, it will never fully

realise its potential.

E X P E R I E N C E S U C C E S S

MANAGING DIRECTOR’S REVIEWF O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 4

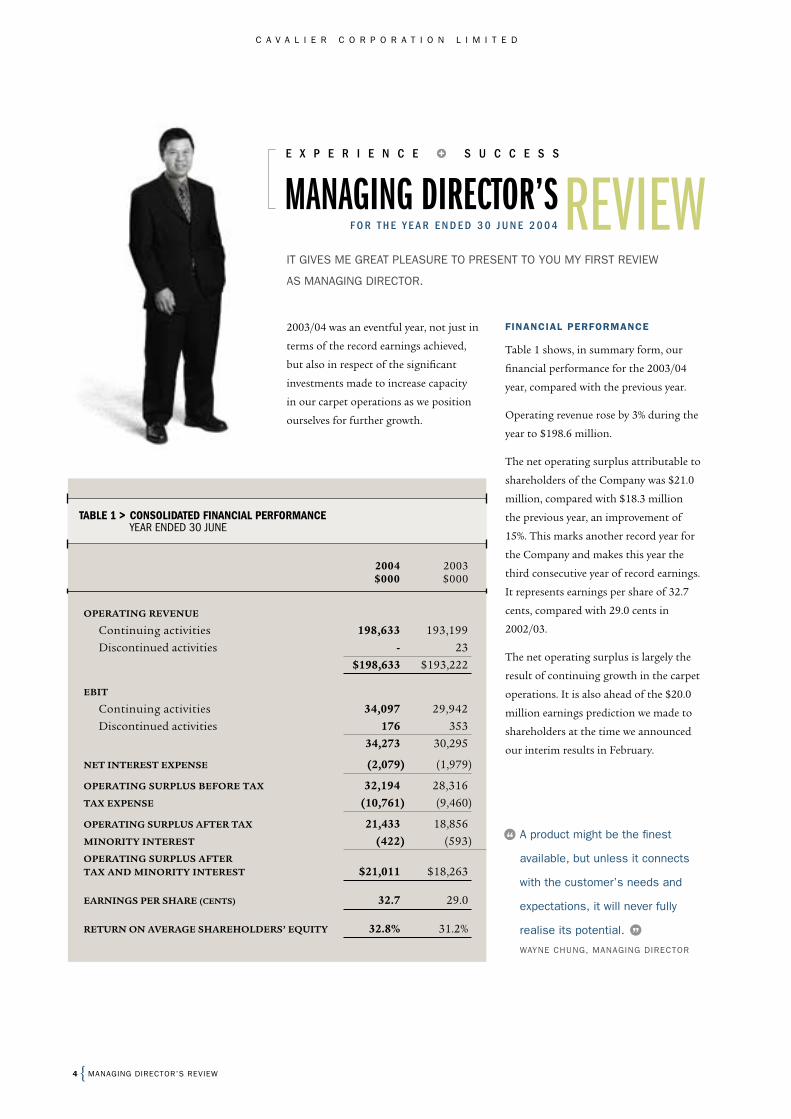

IT GIVES ME GREAT PLEASURE TO PRESENT TO YOU MY FIRST REVIEW

AS MANAGING DIRECTOR.

2003/04 was an eventful year, not just in

terms of the record earnings achieved,

but also in respect of the significant

investments made to increase capacity

in our carpet operations as we position

ourselves for further growth.

FINANCIAL PERFORMANCE

Table 1 shows, in summary form, our

financial performance for the 2003/04

year, compared with the previous year.

Operating revenue rose by 3% during the

year to $198.6 million.

The net operating surplus attributable to

shareholders of the Company was $21.0

million, compared with $18.3 million

the previous year, an improvement of

15%. This marks another record year for

the Company and makes this year the

third consecutive year of record earnings.

It represents earnings per share of 32.7

cents, compared with 29.0 cents in

2002/03.

The net operating surplus is largely the

result of continuing growth in the carpet

operations. It is also ahead of the $20.0

million earnings prediction we made to

shareholders at the time we announced

our interim results in February.

MANAGING DIRECTOR’S REVIEW

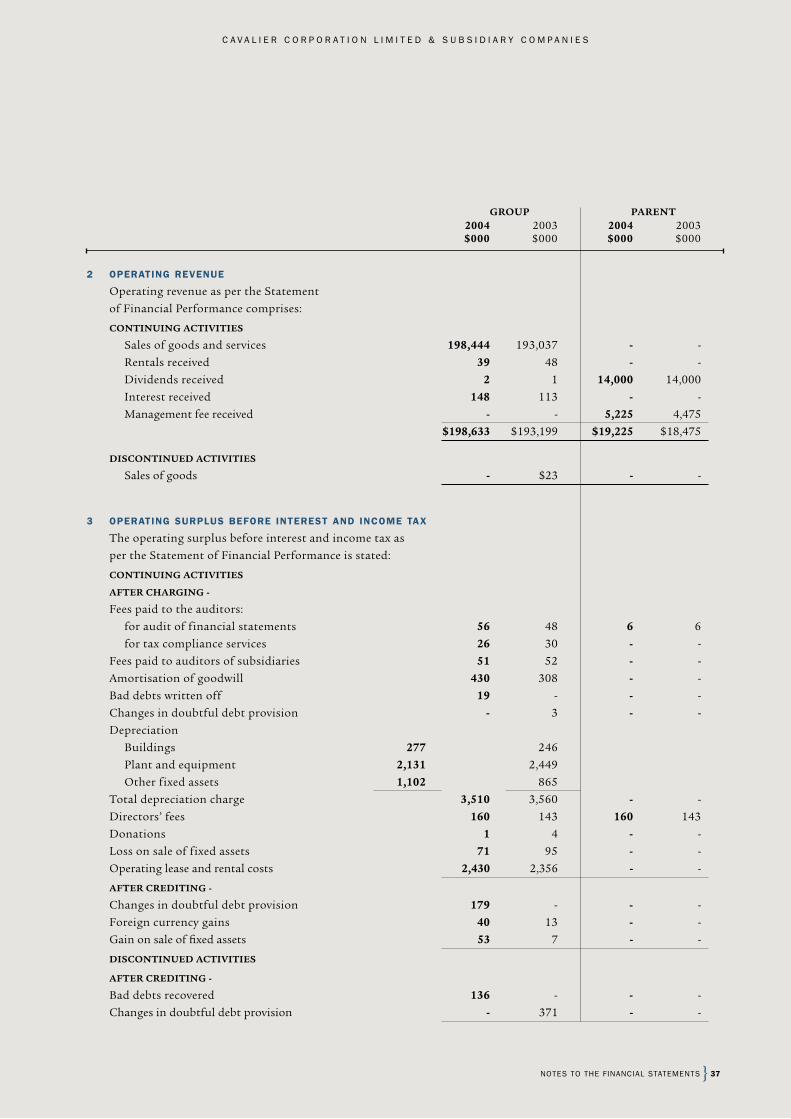

2004 2003 $000 $000

OPERATING REVENUE

Continuing activities 198,633 193,199

Discontinued activities - 23

$198,633 $193,222

EBIT

Continuing activities 34,097 29,942

Discontinued activities 176 353

34,273 30,295

NET INTEREST EXPENSE (2,079) (1,979)

OPERATING SURPLUS BEFORE TAX 32,194 28,316

TAX EXPENSE (10,761) (9,460)

OPERATING SURPLUS AFTER TAX 21,433 18,856

MINORITY INTEREST (422) (593)OPERATING SURPLUS AFTER TAX AND MINORITY INTEREST $21,011 $18,263

EARNINGS PER SHARE (CENTS) 32.7 29.0

RETURN ON AVERAGE SHAREHOLDERS’ EQUITY 32.8% 31.2%

TABLE 1 > CONSOLIDATED FINANCIAL PERFORMANCE YEAR ENDED 30 JUNE

“

WAYNE CHUNG, MANAGING DIRECTOR

”

5##FOOTER##

C A V A L I E R C O R P O R A T I O N L I M I T E D

I N V E S T M E N T

G R O W T H

STRATEGIC CAPITAL EXPENDITURE

OF $15 MILLION IN CAPACITY AND

TECHNOLOGY

POSITIONS THE CARPET OPERATIONS

FOR COST-EFFICIENCIES AND

FURTHER GROWTH IN MARKET SHARE

C A V A L I E R C O R P O R A T I O N L I M I T E D

6

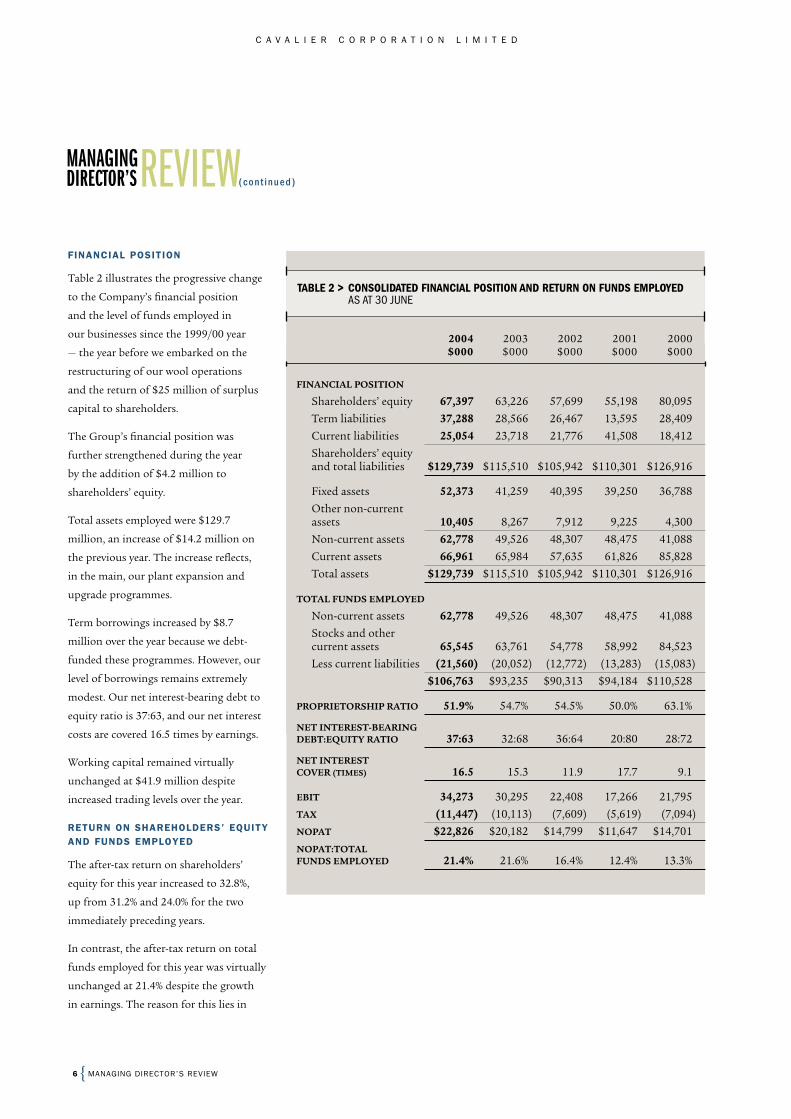

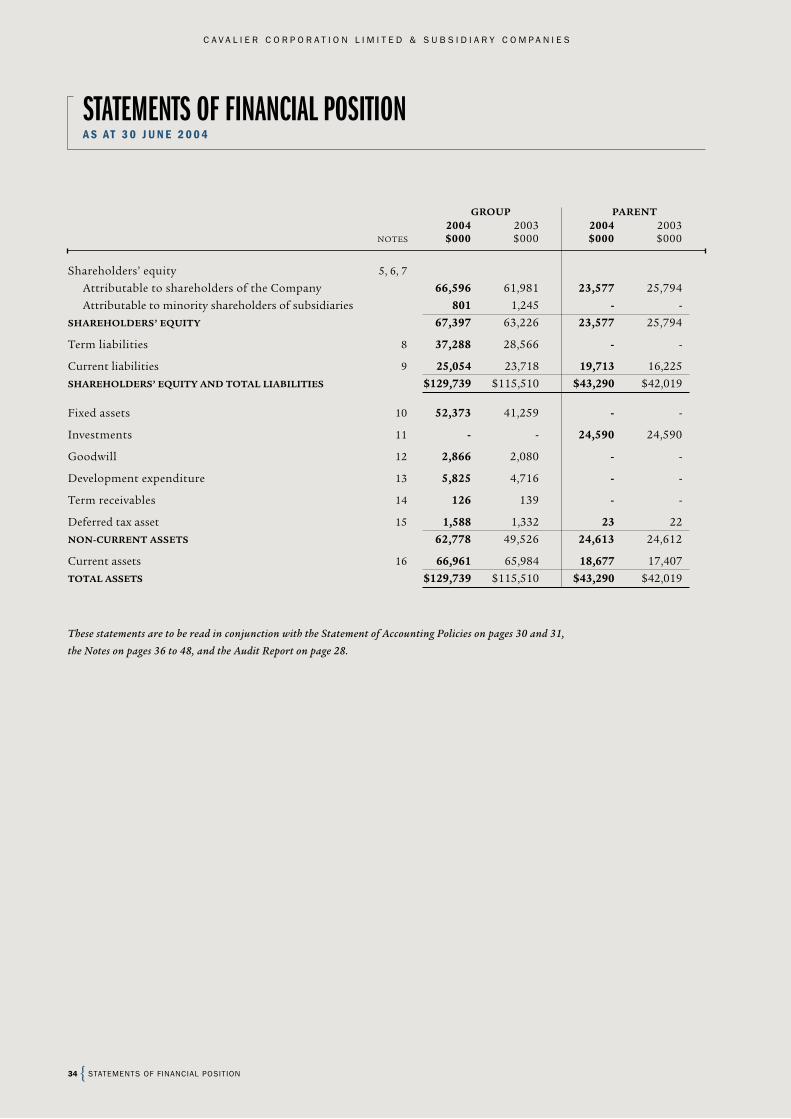

FINANCIAL POSITION

Table 2 illustrates the progressive change

to the Company’s financial position

and the level of funds employed in

our businesses since the 1999/00 year

— the year before we embarked on the

restructuring of our wool operations

and the return of $25 million of surplus

capital to shareholders.

The Group’s financial position was

further strengthened during the year

by the addition of $4.2 million to

shareholders’ equity.

Total assets employed were $129.7

million, an increase of $14.2 million on

the previous year. The increase reflects,

in the main, our plant expansion and

upgrade programmes.

Term borrowings increased by $8.7

million over the year because we debt-

funded these programmes. However, our

level of borrowings remains extremely

modest. Our net interest-bearing debt to

equity ratio is 37:63, and our net interest

costs are covered 16.5 times by earnings.

Working capital remained virtually

unchanged at $41.9 million despite

increased trading levels over the year.

RETURN ON SHAREHOLDERS’ EQUITY AND FUNDS EMPLOYED

The after-tax return on shareholders’

equity for this year increased to 32.8%,

up from 31.2% and 24.0% for the two

immediately preceding years.

In contrast, the after-tax return on total

funds employed for this year was virtually

unchanged at 21.4% despite the growth

in earnings. The reason for this lies in

MANAGING DIRECTOR’S REVIEW

MANAGING DIRECTOR’SREVIEW(cont inued)

TABLE 2 > CONSOLIDATED FINANCIAL POSITION AND RETURN ON FUNDS EMPLOYED AS AT 30 JUNE

2004 2003 2002 2001 2000 $000 $000 $000 $000 $000

FINANCIAL POSITION

Shareholders’ equity 67,397 63,226 57,699 55,198 80,095

Term liabilities 37,288 28,566 26,467 13,595 28,409

Current liabilities 25,054 23,718 21,776 41,508 18,412

Shareholders’ equity and total liabilities $129,739 $115,510 $105,942 $110,301 $126,916

Fixed assets 52,373 41,259 40,395 39,250 36,788

Other non-current assets 10,405 8,267 7,912 9,225 4,300

Non-current assets 62,778 49,526 48,307 48,475 41,088

Current assets 66,961 65,984 57,635 61,826 85,828

Total assets $129,739 $115,510 $105,942 $110,301 $126,916

TOTAL FUNDS EMPLOYED

Non-current assets 62,778 49,526 48,307 48,475 41,088

Stocks and other current assets 65,545 63,761 54,778 58,992 84,523

Less current liabilities (21,560) (20,052) (12,772) (13,283) (15,083)

$106,763 $93,235 $90,313 $94,184 $110,528

PROPRIETORSHIP RATIO 51.9% 54.7% 54.5% 50.0% 63.1%

NET INTEREST-BEARING DEBT:EQUITY RATIO 37:63 32:68 36:64 20:80 28:72

NET INTEREST COVER (TIMES) 16.5 15.3 11.9 17.7 9.1

EBIT 34,273 30,295 22,408 17,266 21,795

TAX (11,447) (10,113) (7,609) (5,619) (7,094)

NOPAT $22,826 $20,182 $14,799 $11,647 $14,701

NOPAT:TOTAL FUNDS EMPLOYED 21.4% 21.6% 16.4% 12.4% 13.3%

7

C A V A L I E R C O R P O R A T I O N L I M I T E D

the $8 million worth of debt-funded, but

as yet incomplete, capital expenditure

programmes that are yet to yield a return.

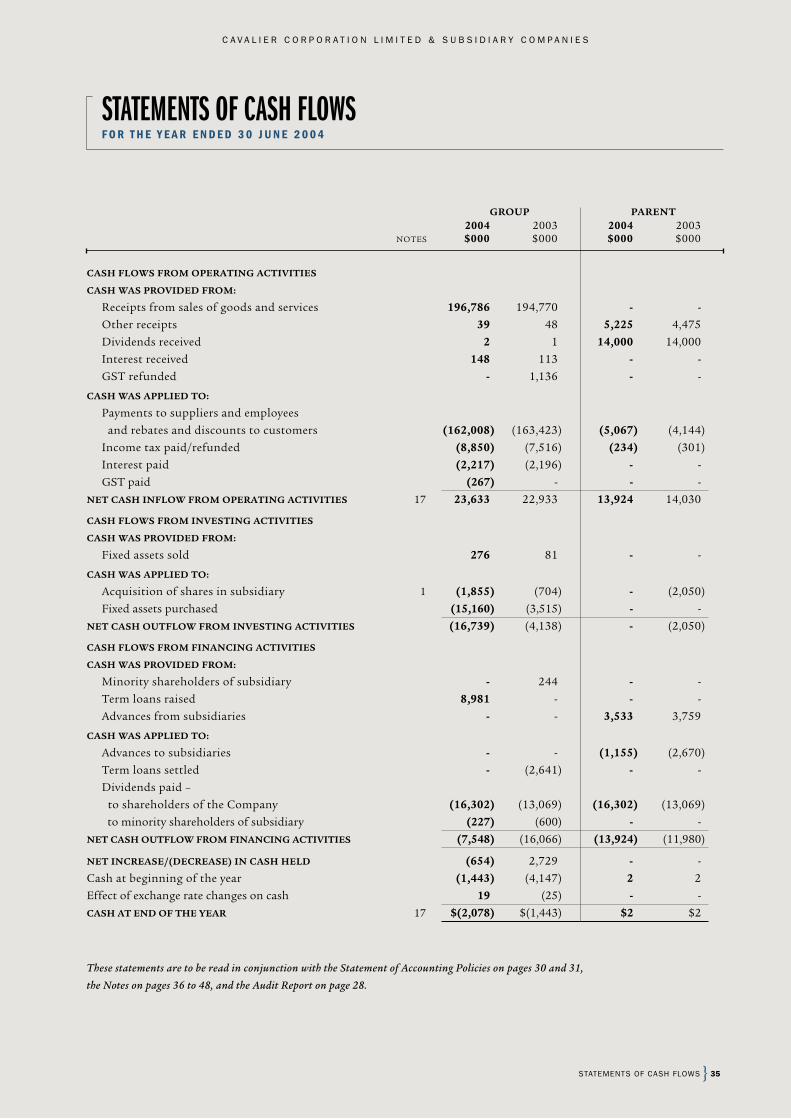

CASH FLOWS

Net cash flows from operating, investing,

and financing activities were a positive

$23.6 million, a negative $16.7 million,

and a negative $7.5 million respectively.

The net cash outflow from investing

activities was much higher than in

previous years due to some large one-off

capital spends which were required to

increase manufacturing capacity. These

included the following:

¬ $7.0 million on providing more yarn

capacity for carpet manufacturing

¬ $1.5 million on upgrading the carpet

tile dye-injection equipment

¬ $1.7 million on increasing facilities at

Hawkes Bay Woolscourers

On top of that, there was the $1.9 million

we spent on increasing our stake in

Hawkes Bay Woolscourers from 76% to

92.5%.

OPERATIONS

Cavalier reports in terms of two industry

segments — carpets and wool.

Within carpets, there are two distinct

areas of operations, broadloom carpets

and carpet tiles. The New Zealand-based

broadloom carpet operation is Cavalier’s

main core business. It manufactures

and markets 100% New Zealand wool

carpets under the Bremworth, Cavalier

Bremworth, Knightsbridge, Kimberley,

and Tramore brands. The carpet tile

business, Ontera Modular Carpets, is

based in Sydney and markets its carpet

tiles to the commercial sector under

the Ontera brand. It is 89.5% owned

by Cavalier, with the balance owned by

Ontera management.

The wool segment comprises the wool

scouring and wool acquisition businesses.

The wool scouring business operates

through 92.5%-owned subsidiary, Hawkes

Bay Woolscourers. Its scour is based in

Napier, and it is one of two independent

commission woolscourers in the North

Island. The wool acquisition business,

which operates through Elco Direct,

acquires wool direct at the farm-gate.

Both of these businesses have Cavalier

as a customer, but the majority of their

business is with external customers.

CARPET OPERATIONS

Broadloom Carpet Operation

The broadloom carpet operation enjoyed

very favourable market conditions in

its main markets of New Zealand and

Australia in the year under review. The

housing sectors in these markets, fuelled

by the low interest rates prevailing in the

last few years, were extremely buoyant.

New houses were built at unprecedented

levels, as were real estate resales, and both

of these factors had a favourable impact

on our broadloom carpet operation.

Sales for the year were $127.9 million,

up $7.4 million or 6% on the previous

year. We would have achieved much

higher sales had it not been for our yarn

manufacturing constraints. However,

we believe that we more than held our

share in those market segments in which

we operate — after having achieved

significant market share increases over

previous years.

WOOL (22%) $43.1 MILLION

CARPET (78%) $155.5 MILLION

FIGURE 1 > CONTRIBUTION TO GROUP OPERATING REVENUE

WOOL (11%) $4.0 MILLION

CARPET (88%) $32.2 MILLION

OTHER (1%)$0.2 MILLION

FIGURE 2 > CONTRIBUTION TO GROUP OPERATING SURPLUS

BEFORE CORPORATE COSTS, INTEREST, AND INCOME TAX

New houses were built at unprecedented levels, as were real estate resales, and

both of these factors had a favourable impact on our broadloom carpet operation.

“

”WAYNE CHUNG, MANAGING DIRECTOR

MANAGING DIRECTOR’S REVIEW

C A V A L I E R C O R P O R A T I O N L I M I T E D

8

Earnings before corporate costs, interest,

and tax were $28.7 million, a 13% increase

on the previous year’s $25.4 million. This

is most pleasing.

We have embarked on a programme to

further increase our yarn manufacturing

capacity by some 25%. This will allow

us to capture important synergistic

benefits within our two carpet operations.

There will be yarn for Ontera, which

currently purchases some $5 million

of spun yarn from external sources. It

will also allow our broadloom carpet

operation to bridge the current gap

between supply and demand for its

products in the market place.

We have also purchased a new tufting

machine at a cost of $2.5 million. This

machine incorporates all the latest

technology available and will enable us

to produce carpets to another dimension.

We plan to have carpet from this machine

sampled and ready for sale later this year.

We have been experiencing some growing

pains at our carpet-manufacturing

site at Auckland. As a result of record

production levels, space has been at a

premium. To alleviate the situation, we

are planning to relocate the distribution

centre to a 5,300 square metre purpose-

built warehouse close by.

Carpet Tile Operation

We acquired the carpet tile operation,

Ontera Modular Carpets, on 1 July

2002, so this year marks the completion

of Ontera’s second year under our

management.

Last year, Ontera achieved a very good

maiden result. This year, we are pleased

to again report that the momentum

has continued, even though sales, at

$27.6 million, were 3% down on the

MANAGING DIRECTOR’S REVIEW

The Group has always been conscious of

its obligations to protect the environment

and, in this regard, works to ensure that

all relevant regulatory requirements are

complied with at all times. Where such

requirements do not exist, best industry

practices are adhered to.

The Group is also committed to

continuous improvement, and this

year saw both the Cavalier Bremworth

broadloom carpet operation and the

Ontera modular carpet tile operation

— both of which account for 78% of

the Group’s operating revenue — gain

ISO 14001 environmental management

system accreditation.

ISO 14001 is based on a set of

standards published by the International

Standards Organisation and will fur ther

enhance the Group’s environmental

commitment.

More and more, purchasing decisions

made by organisations in both the public

and the private sectors are based not

only on the product and its quality and

price, but also on the environmental

per formance of the manufacturer,

and the accreditation of both Cavalier

Bremworth and Ontera should put us in

good stead for the future.

ENVIRONMENTAL CASE STUDY

For many years, Ontera has recognised

the social and economic importance

of environmental consciousness.

Recently, it introduced a programme

called “Commitment to Environmental

Excellence” which will spearhead its

ongoing drive towards sustainability.

A key aspect of this initiative, which

is unique to the flooring industry, calls

for all Ontera modular carpet to be

engineered to withstand the rigours of

a renewal process called EarthPlus®

— a three-step recovery process where

used carpet modules are super-cleaned,

re-textured and re-styled — to give the

product a new appearance and a

new life.

This Ontera EarthPlus® initiative

fitted per fectly with the ANZ Bank’s

environmental best practices

requirements in its recent fit-out of

its premises at 530 Collins Street,

Melbourne. This was a project where

product recovered from the 1989

installation of the QV1 Building, St

Georges Terrace, Perth went through the

EarthPlus® renewal process to provide

the ANZ Bank with 1,053 m2 of fully

re-used EarthPlus® product — the first

significant installation of this type in

Australia.

What is perhaps relevant and significant

from the environmental perspective

is the diversion of approximately 5.4

tonnes of used product from landfill or

incineration — a win-win solution that

both the ANZ Bank and Ontera can

justifiably feel proud of.

CAVALIER CORPORATION

THE ENVIRONMENT

MANAGING DIRECTOR’SREVIEW(cont inued)

9##FOOTER##

C A V A L I E R C O R P O R A T I O N L I M I T E D

E N V I R O N M E N T

S U S T A I N A B I L I T Y

‘ISO 14001 ENVIRONMENTAL

MANAGEMENT SYSTEM’ ACCREDITATION

FOR OUR CARPET OPERATIONS

INCREASES AWARENESS OF NEED

TO ‘REDUCE, REUSE AND RECYCLE’

AND REINFORCES THE GROUP’S

ENVIRONMENTAL COMMITMENT

C A V A L I E R C O R P O R A T I O N L I M I T E D

10

previous year. The year began slowly.

Many commercial refurbishments were

put on hold because of uncertainties

arising from the SARS outbreak in

Asia. However, as the year progressed,

confidence returned, and Ontera finished

the year very strongly.

Earnings before corporate costs, interest,

and tax were $3.5 million, up 29% on the

previous year’s $2.7 million despite the

inclusion in the previous year’s results of

a one-off gain of $0.6 million associated

with the purchase of the business. Thus,

the like-for-like comparison with the

previous year indicates an improvement

of 67%, from $2.1 million to $3.5 million.

This year, we spent considerable sums

of money to provide Ontera with a solid

platform for future growth.

We successfully upgraded the Milliken

dye-injection equipment to incorporate

the latest technology available at a

considerable spend of $1.5 million. This

should provide Ontera with much better

productivity as well as new product

capabilities and should significantly

enhance its competitiveness.

We have also successfully implemented

new information systems that will

strengthen Ontera’s management

controls and customer service capabilities.

The current outlook for Ontera’s business

is very positive. It is enjoying the buoyant

market conditions that are currently

prevailing in the commercial building

markets in Australasia, and we expect to

see this continue into the 2004/05 year.

WOOL OPERATIONS

Our wool scouring operation, Hawkes Bay

Woolscourers, enjoyed a very successful

year. Our earlier decision to upgrade

equipment there produced enormous

benefits, both in terms of output and

quality. It achieved a significant growth in

market share and, in the process, scoured

what we believe to be the highest volume

ever by a commission wool scourer in any

one year. This has come about from its

well-earned reputation for quality and

service — one that is unmatched in the

industry. This is what Cavalier stands for

across all of its businesses and is the very

reason for its success today.

Acquiring wool privately at the farm-gate

is a very competitive and unpredictable

business where sellers and buyers

generally have little regard to anything

else but price.

Even though sales and earnings for

Elco Direct for the year were down

slightly on the previous year, mainly

as a result of lower wool prices, Elco

Direct continues to successfully operate

in this market by providing its customers

with excellent service.

The number of people employed by

the Group now stands in excess of

800 (760 in 2003).

We strive to be an employer of choice,

and in this regard, we will continue to:

¬ maintain and build on the good

industrial relations we currently

have with the unions that represent

our people

¬ invest in on-the-job training, not only

to better equip our people to do their

jobs, but also to help them in their

personal development

¬ place utmost importance on their

health and safety in the workplace

¬ improve on their working environment

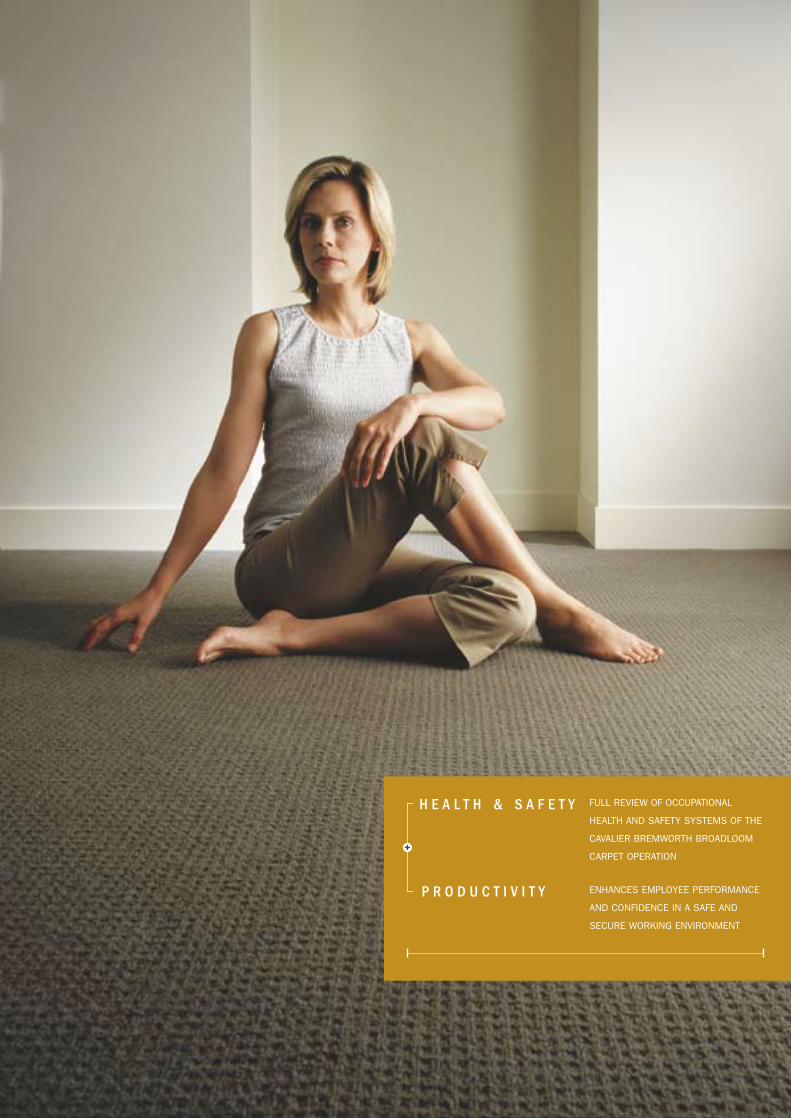

Our commitment to health and safety in

the workplace led to a full review of the

occupational health and safety systems

of the Cavalier Bremworth broadloom

carpet operation, which employs 79%

of the Group’s employees. This review

culminated in the operation being

awarded “primary status” under the

Accident Compensation Commission’s

Accredited Employer Programme

— a three-way partnership between

employer, employees, and the ACC

— which enables Cavalier to take direct

responsibility for managing hazards in

the workplace.

We have quantifiable per formance

targets in the area of health and

safety in the workplace as part of our

commitment to continuous improvement,

and we will strive to do better.

CAVALIER CORPORATION

HEALTH & SAFETY

MANAGING DIRECTOR’S REVIEW

MANAGING DIRECTOR’SREVIEW(cont inued)

11##FOOTER##

C A V A L I E R C O R P O R A T I O N L I M I T E D

H E A L T H & S A F E T Y

P R O D U C T I V I T Y

FULL REVIEW OF OCCUPATIONAL

HEALTH AND SAFETY SYSTEMS OF THE

CAVALIER BREMWORTH BROADLOOM

CARPET OPERATION

ENHANCES EMPLOYEE PERFORMANCE

AND CONFIDENCE IN A SAFE AND

SECURE WORKING ENVIRONMENT

C A V A L I E R C O R P O R A T I O N L I M I T E D

12

Sales for the wool operation overall for

this year were $43.1 million, down $1.2

million or 3% on the previous year. The

lower sales reflect, in the main, lower wool

prices in our wool-acquisition operation

and are not an indicator of reduced

operating activity.

The more important indicator is

earnings. In the year, our wool operation

contributed $4.0 million of earnings

before corporate costs, interest, and tax,

which is 4% up on the previous year’s $3.8

million. This is a credible performance

in a highly competitive business

environment where there is no pricing

premium.

The outlook for the wool operation

is positive. It expects to hold on to its

earnings in the coming year which would

represent an outstanding return on funds

employed.

2004/05 OUTLOOK

The Group’s performance in the 2004/05

year will hinge upon the performance of

our carpet operations.

Some slowdown in building activity and

consumer spending has been widely

predicted on both sides of the Tasman

for sometime now. The extent to which

the slowdown might affect our own

businesses will depend largely on whether

the respective Reserve Banks can engineer

a “soft landing” as against a more radical

slowdown.

In preparing our budgets for the 2004/05

year, we have allowed for some downturn

in the carpet market, but with offsetting

gains in market share associated with our

increased capacity and our new tufting

technology. We are also anticipating cost

reduction associated with our expanded

yarn-manufacturing capacity. Budget is

for tax-paid earnings of $22.5 million, an

increase of 7% on the 2003/04 year.

We will keep shareholders informed as

the year progresses.

MICROBIAL TECHNOLOGIES

Development work on our bio-product

continues.

A busy programme of product

development and field trial work

has produced mixed results — some

outstanding and some less so — and has

signalled the need for further formulation

refinements.

Commercial interest in the product

is very high, but the extraction of

commercial value is dependent upon

our ability to demonstrate consistent,

repeatable field performance.

We have made a lot of progress, and we

are tantalisingly close, but we are not

there yet. Commercialisation is taking far

longer than we originally envisaged, and

we are disappointed about that.

Nevertheless, we retain confidence in the

market potential of this technology, and

we are continuing to invest in it.

We will update shareholders as we move

forward.

W K CHUNG MANAGING DIRECTOR

20 August 2004

1999 2001 2002 2003 2004

34.3

2.1

16.5

30.3

2.0

15.3

22.4

1.9

11.9

17.3

1.0

17.7

18.9

3.1

2000

21.8

2.4

9.1

6.1

EARNINGS BEFORE INTEREST AND TAX, NET INTEREST EXPENSE, AND NET INTEREST COVER

Earnings before interest and tax ($ millions) Net interest cover (times)Net interest expense ($ millions)

MANAGING DIRECTOR’S REVIEW

MANAGING DIRECTOR’SREVIEW(cont inued)

13

C A V A L I E R C O R P O R A T I O N L I M I T E D

Q U E S T I O N A N S W E R

MANAGING DIRECTOR’SQ&A

A N I N T E R V I E W W I T H W AY N E C H U N G

THE FOLLOWING INTERVIEW WITH CAVALIER’S MANAGING DIRECTOR,

WAYNE CHUNG, TOOK PLACE ON 17 SEPTEMBER 2004.

You have previously indicated that the

bulk of the Group’s overseas earnings are

denominated in AUD, so is the current

strength of the NZD:AUD a concern?

Not right now because we have some

five months of the 2004/05 year’s AUD

receivables covered at around .86.

Obviously, it would become a concern

if the NZD:AUD remains at, or goes

above, the current .94 into next year. We

believe that the current strength of the

NZD is driven by the current interest rate

differentials between NZ and Australia

and that we should see a reversal once

the Reserve Bank gets to the end of

its tightening cycle. And going by past

experience, there may be opportunities

to increase prices when the Australian

manufacturers we compete against try to

pass on higher import costs flowing on

from the weak AUD.

The earnings growth of Ontera of 67% on

a like-for-like basis is impressive. Where

to from here for Ontera?

I am confident about the potential for

further earnings growth in Ontera. At

the time of our acquisition, Ontera

was grossly undercapitalised and had

never really been given the chance to

demonstrate just what it was capable of.

The first thing we did back in 2002 was to

put it on a sound financial footing.

Going forward, there are also synergies

between Ontera and our broadloom

carpet operation, principally in the

sharing of the semi-worsted yarn capacity

coming onstream.

So, yes, I am very excited about the

prospects at Ontera, especially in the

current buoyant market for commercial

installations on both sides of the Tasman.

A lot of progress seems to have been

made in your commitment to the

environment and in the area of workplace

health and safety. Can you expand on

these?

We have always had an environmental

policy, and the health and safety of our

people have always been paramount.

Continuous improvement is very much

a part of our organisational culture, and

the developments you see in these areas

are really just continuous improvement

at work. And I must say that I am

thrilled with the results — the ISO 14001

accreditation at both carpet operations

and Cavalier Bremworth’s entry into the

ACC Accredited Employer Programme.

You have made significant investments

in capital projects in the last 12 months.

What are some of the major ones and

how do you see them affecting the

business going forward?

Capital expenditure for the 2003/04

year totalled $15 million which is about

three to four times the amount we would

normally spend in a year. I’ve already

covered some of the more significant

spends in my review.

MANAGING DIRECTOR’S Q&A

C A V A L I E R C O R P O R A T I O N L I M I T E D

14

The bulk of this year’s expenditure is for

increasing our capacity and capability and

should see us well placed to capitalise on

growth opportunities going forward.

For instance, the $7 million expansion at

our Wanganui yarn spinning plant is to

provide much-needed yarn for our carpet

operations. When fully operational, it will

increase our yarn manufacturing capacity

by 25%. Approximately 30% of this will go

towards replacing the yarn which Ontera

currently purchases externally, and the

balance has been ear-marked for growth

in our broadloom carpet business. This

project — which started in December

2003, but will not be fully operational

until December this year — is a major

project for us, and it will take some time

before all the expected benefits can be

realised. We expect some of the benefits to

start coming through in the second half

of the 2004/05 financial year.

Shareholders should note that the

majority of our capital expenditure

programmes (other than those for

compliance and for occupational health

and safety) have been benchmarked

against our internal rate of return of

15% per annum tax-paid, which, when

compared against the Company’s

estimated tax-paid cost of capital of 10%,

should be shareholder value positive.

The Company’s balance sheet remains

very conservatively geared and, with a

debt to equity ratio of 37:63 and net

interest expense covered 16.5 times by

EBIT, we have been able to accommodate

these capital expenditures through

increased borrowing.

Finding projects that match or exceed

our hurdle rate has never been easy

and, in many ways, I feel excited for the

Company and for our shareholders that

we have been able to identify so many

opportunities to grow shareholder wealth.

Where does wool scouring fit into the

Group’s overall strategy?

Scouring is one of the key processes wool

from the sheep’s back has to go through

in its journey from the farm gate to our

range of woollen carpets, and our direct

involvement allows us to retain control of

the consistency of quality so crucial to the

end product.

We have, quite naturally, also been

able to provide that same standard of

quality to the wool industry at large and

that, coupled with our commitment to

outstanding customer service, has made

Hawkes Bay Woolscourers (“HBWS”) the

commission woolscourer of choice in the

North Island.

So, in a lot of ways, it is now core business

for us.

And hence the decision to expand into

the South Island through Hawkes Bay

Woolscourers’ 50% interest in Canterbury

Woolscourers?

Most definitely.

This is a strategic acquisition that will

see the consolidation of two separate

scouring operations currently based

at Winchester and Washdyke in the

Canterbury region. At the same time, we

will also be increasing and upgrading the

existing facilities at Washdyke, where we

will ultimately end up, to make

the scour amongst the most modern and

sophisticated in the country. This project

will take nine months. When completed,

Canterbury Woolscourers (“CWS”) will

have total assets employed of around $13

million and projected EBIT of around

$4.5 million.

HBWS will take a direct management role

in CWS to ensure that all key objectives

are met and to see that CWS is modelled

on the very same HBWS platform and

strategies.

What is the Microbial project and how

long has the Company been involved?

The Microbial project involves bringing

to market a natural remedy for the

prevention of flystrike and the control

of lice infestation in sheep. This remedy

(which we have named Biovine) involves

a natural biological insecticide, bacillus

thuringiensis (Bt), and is potentially of

great significance to the wool industry

world-wide. Existing remedies are toxic,

eco-toxic or both, and chemical pesticide

residues in wool have become a major

issue. The emergence of resistant strains

of blowfly and lice, rendering existing

remedies ineffective, is also a major

issue. The remedy under development is

effective and yet completely non-toxic,

safe, and environmentally benign. It is

what the industry is desperately waiting

for at the moment.

We have been involved in the project

for eight years now and have spent $5.8

million on development and $1.7 million

on a pilot plant.

MANAGING DIRECTOR’SQ&A

MANAGING DIRECTOR’S Q&A

(cont inued)

15

C A V A L I E R C O R P O R A T I O N L I M I T E D

Eights years is a long time, isn’t it?

Commercialisation is definitely taking far

longer than we had originally thought,

and that is disappointing. But when

one looks at that in the context of the

product that we are attempting to bring

to market, maybe the eight years is not

that long a time.

Over that time we have made a great deal

of progress in all the key areas of product

development, regulatory clearance, and

commercial-scale manufacture. We have

also demonstrated that the product has

the potential to control scab mite, and

that has greatly enhanced its potential

commercial value.

Commercial interest in the product has

also been very high, but the extraction of

commercial value is obviously dependent

upon our ability to demonstrate

consistent, repeatable field performance.

We are tantalisingly close, but we are not

yet there, and that is frustrating.

A busy programme of product

development and field trial work over

the last 12 months has produced mixed

results — some outstanding and some

less so — and has signalled the need for

further formulation refinements. We

now believe we know what is required to

produce the necessary level of consistency

and repeatability, but further trial work is

going to be required to prove that.

Where to from here for the project?

We still need more time and work before

we are able to bring Biovine to market.

We are now at a very critical stage of the

development work, and if we pull it off,

the potential post-commercialisation

returns will be significant. However,

there is still the risk — difficult to

quantify, but nevertheless material — that

commercialisation may never occur.

The project is a developmental project

where the risks are high, but the potential

rewards are just as high. The Directors

remain committed to the project, but

are ever conscious of the amount of

development expenditure that has been

accumulating in the Company’ balance

sheet. The true value of this project is

extremely difficult to ascertain because

there is, on the one hand, still the

possibility that the project may come

to nothing. On the other hand, there

are significant potential rewards if it

comes off.

The Directors note that the $5.8 million

of development work and $1.7 million

of pilot plant spends thus far represent

approximately 8% (after tax) of the

equity attributable to shareholders

of the Company, and whilst any

write-offs would obviously affect our

reported results, there would be no

impact whatsoever on our cash flows,

our borrowings, or our ability to pay

dividends.

What are some of the challenges you see

facing the various business units at the

present time and what is your outlook for

these units?

The Cavalier Bremworth broadloom

carpet business is our main core business,

and we are looking to it to continue

to deliver improved earnings in an

increasingly difficult environment.

Some of the potential negatives are

the strength of the NZD on our AUD

denominated receivables, the more

subdued business environment in

Australia, and the impact higher interest

rates in New Zealand may have on

consumer confidence and consumer

demand. But there are positives. The

business has never been in better shape.

We have worked hard on positioning

ourselves for the future. And we believe

we have the strategies to continue to grow

our business.

The Ontera carpet tile business is

well positioned, as is Hawkes Bay

Woolscourers, to make the most of

the opportunities available to them.

And we are also looking forward to the

contribution, in time, of Canterbury

Woolscourers.

As I indicated at the time of the release of

the 2003/04 results, we are budgeting for

a $22.5 million operating surplus after

tax and minority interest for 2004/05

which would be 7.5% up on the record of

2003/04.

MANAGING DIRECTOR’S Q&A

C A V A L I E R C O R P O R A T I O N L I M I T E D

16

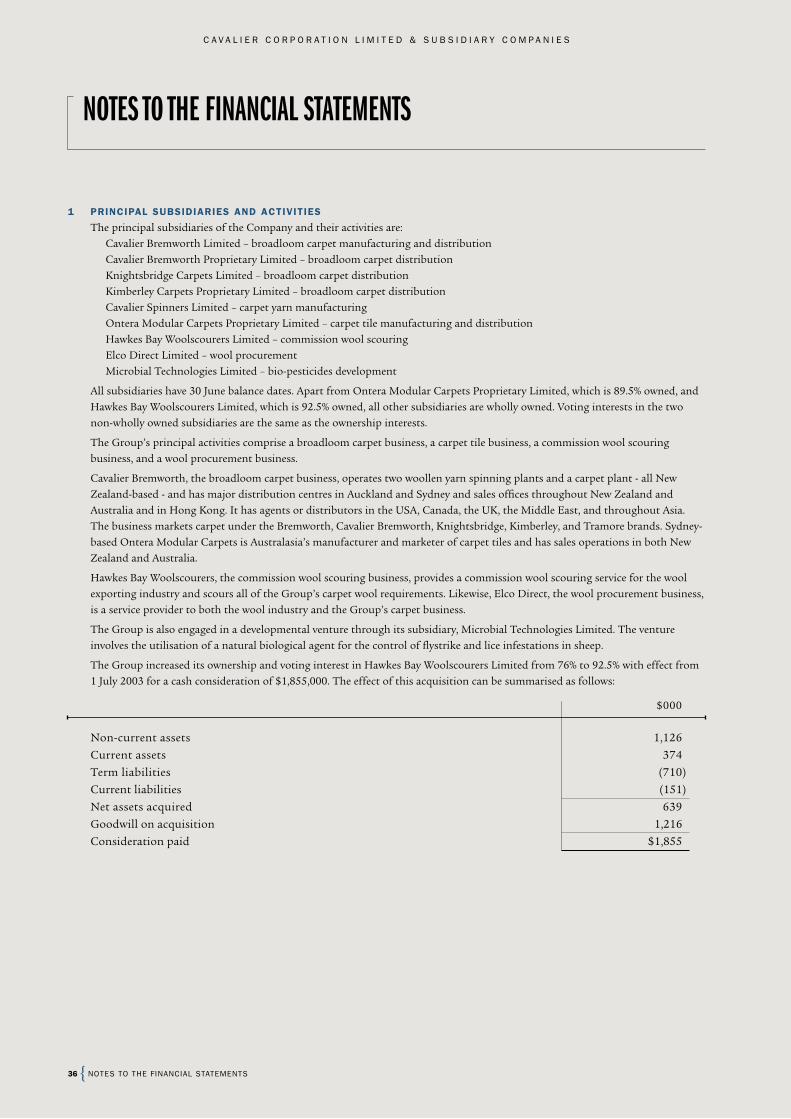

GROUP ACTIVITIES

The Group’s principal activities comprise

the Cavalier Bremworth broadloom carpet

business, the Ontera Modular carpet tile

operation, commission wool scouring,

and a wool procurement business.

The Cavalier Bremworth broadloom

carpet business — which markets

carpet under the Bremworth, Cavalier

Bremworth, Knightsbridge, Kimberley,

and Tramore brands — operates two

woollen yarn spinning plants and a carpet

plant in New Zealand and has major

distribution centres in Auckland and

Sydney and sales offices throughout New

Zealand and Australia. It is represented

in the USA, Canada, the UK, the Middle

East, and throughout Asia by agents or

distributors.

The Ontera Modular carpet tile

operation is based in Sydney and is

one of Australasia’s leading carpet tile

manufacturers.

Hawkes Bay Woolscourers, the

commission wool scouring business,

provides a commission wool scouring

service for the wool exporting industry

and scours all of the Group’s carpet wool

requirements. The Group acquired, on

31 August 2004 through 92.5%-owned

Hawkes Bay Woolscourers, a 50% interest

in Canterbury Woolscourers, a company

formed to acquire and consolidate two

South Island scours based in Winchester

and Washdyke.

Elco Direct, the wool procurement

business, is also a service provider to

both the wool industry and the Group’s

carpet business.

The Group is also engaged in a

developmental venture through its

subsidiary, Microbial Technologies

Limited. The venture involves the

utilisation of a natural biological agent

for the control of flystrike and lice

infestations in sheep.

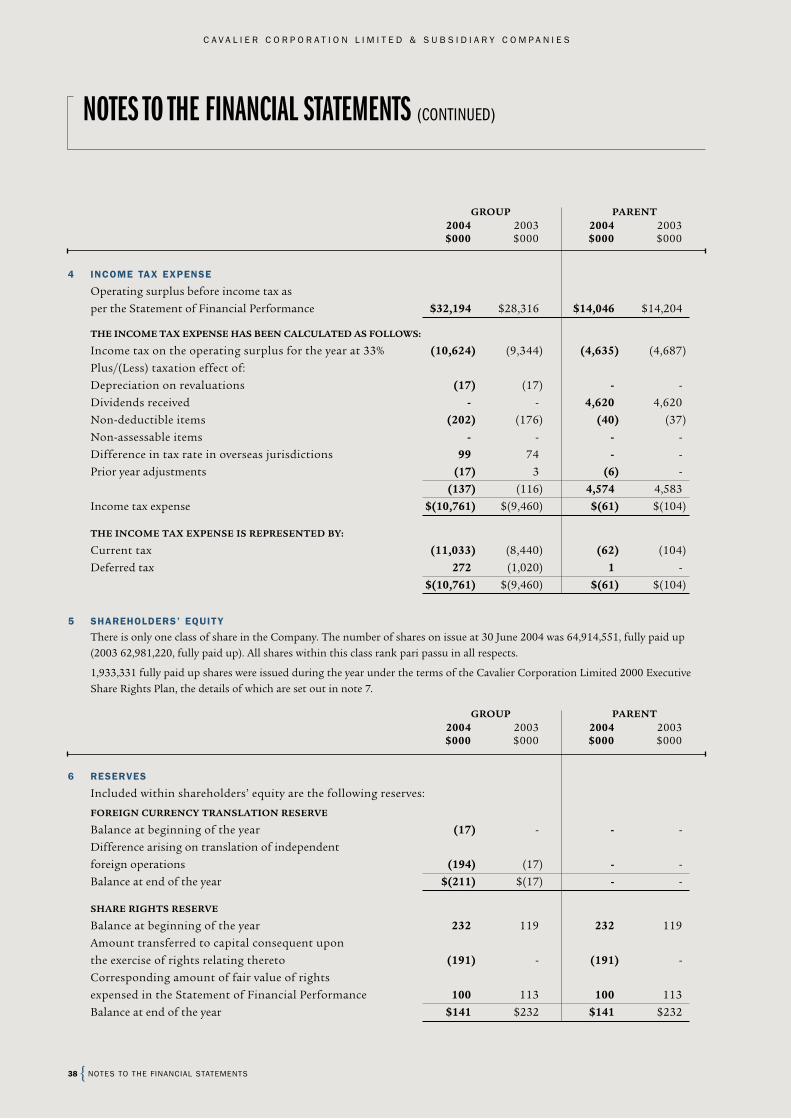

ACCOUNTING POLICIES

Your Directors confirm that there have

been no changes in accounting policies

during the year.

FINANCIAL PERFORMANCE

The Group achieved an operating surplus

after tax and minority interest for the

year of $21,011,000 — 15% up on the

$18,263,000 achieved in the previous year.

This operating surplus is the third record

result in as many years.

2004 2003 $000 $000

Operating revenue $198,633 $193,222

Operating surplus before tax 32,194 28,316

Income tax expense (10,761) (9,460)

Operating surplus after tax 21,433 18,856

Minority interest (422) (593)

Operating surplus after tax and minority interest $21,011 $18,263

REPORTDIRECTORS’DEAR SHAREHOLDERS,

ON BEHALF OF YOUR DIRECTORS, I HAVE PLEASURE IN PRESENTING OUR 2004

ANNUAL REPORT, WHICH INCORPORATES THE AUDITED FINANCIAL STATEMENTS

OF THE COMPANY AND ITS SUBSIDIARIES FOR THE YEAR ENDED 30 JUNE 2004.

L E A D E R S H I P R E S U L T S

FOR THE YEAR ENDED 30 JUNE 2004

ALAN JAMES, CHAIRMAN

The strength of Cavalier comes

not just from the quality of its

core broadloom carpet business,

but also from the synergies

that exist between it and

our other operations.

They connect well together.

DIRECTORS’ REPORT

“

”

17##FOOTER##

C A V A L I E R C O R P O R A T I O N L I M I T E D

E X P A N S I O N

P O T E N T I A L

PURCHASE OF 50% INTEREST IN

CANTERBURY WOOLSCOURERS, A COMPANY

FORMED TO ACQUIRE AND CONSOLIDATE

TWO SOUTH ISLAND WOOL SCOURS

TO PROVIDE THE BASE FOR A NATIONWIDE

WOOL SCOURING OPERATION AND TO

FURTHER ENHANCE SHAREHOLDER VALUEREPORT

C A V A L I E R C O R P O R A T I O N L I M I T E D

18

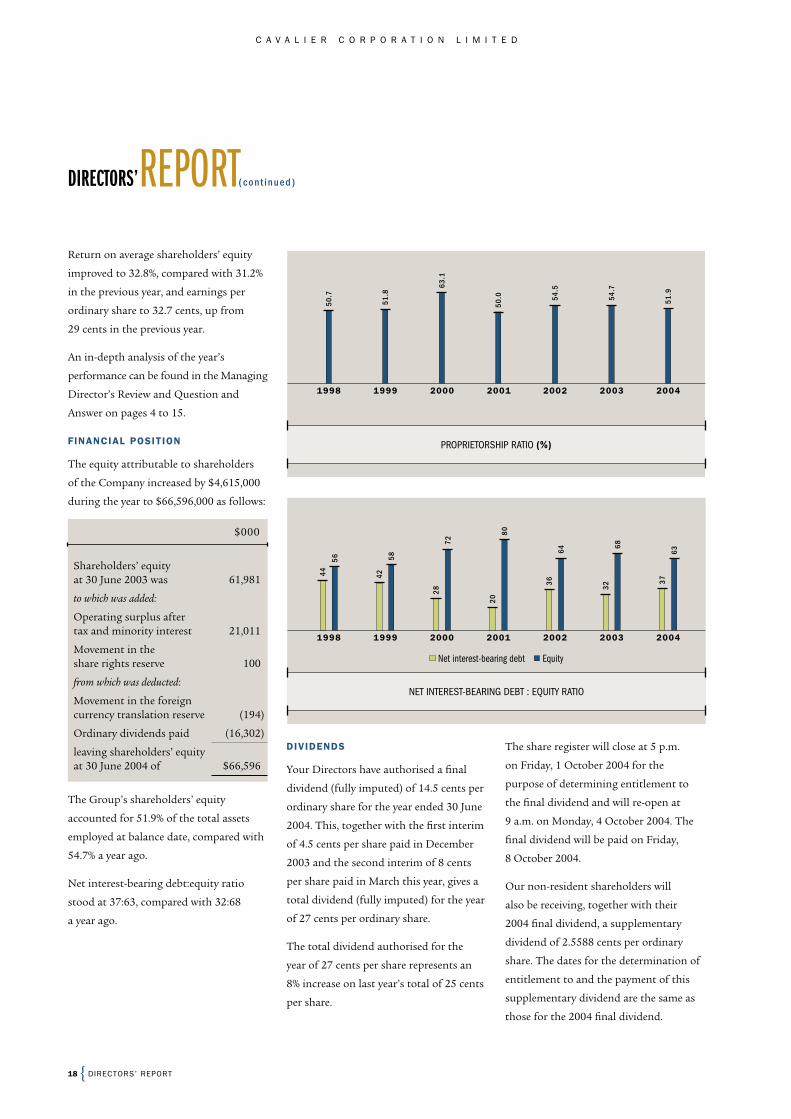

Return on average shareholders’ equity

improved to 32.8%, compared with 31.2%

in the previous year, and earnings per

ordinary share to 32.7 cents, up from

29 cents in the previous year.

An in-depth analysis of the year’s

performance can be found in the Managing

Director’s Review and Question and

Answer on pages 4 to 15.

FINANCIAL POSITION

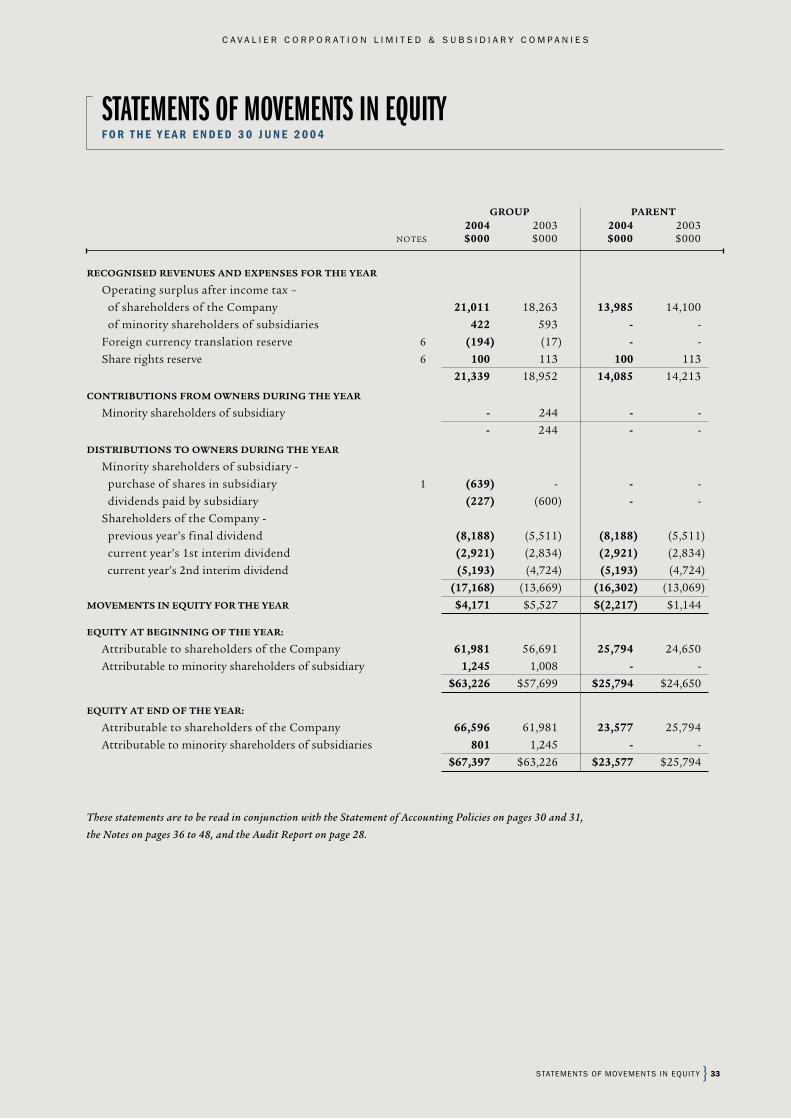

The equity attributable to shareholders

of the Company increased by $4,615,000

during the year to $66,596,000 as follows:

$000

Shareholders’ equity at 30 June 2003 was 61,981

to which was added:

Operating surplus after tax and minority interest 21,011

Movement in the share rights reserve 100

from which was deducted:

Movement in the foreign currency translation reserve (194)

Ordinary dividends paid (16,302)

leaving shareholders’ equity at 30 June 2004 of $66,596

The Group’s shareholders’ equity

accounted for 51.9% of the total assets

employed at balance date, compared with

54.7% a year ago.

Net interest-bearing debt:equity ratio

stood at 37:63, compared with 32:68

a year ago.

DIVIDENDS

Your Directors have authorised a final

dividend (fully imputed) of 14.5 cents per

ordinary share for the year ended 30 June

2004. This, together with the first interim

of 4.5 cents per share paid in December

2003 and the second interim of 8 cents

per share paid in March this year, gives a

total dividend (fully imputed) for the year

of 27 cents per ordinary share.

The total dividend authorised for the

year of 27 cents per share represents an

8% increase on last year’s total of 25 cents

per share.

The share register will close at 5 p.m.

on Friday, 1 October 2004 for the

purpose of determining entitlement to

the final dividend and will re-open at

9 a.m. on Monday, 4 October 2004. The

final dividend will be paid on Friday,

8 October 2004.

Our non-resident shareholders will

also be receiving, together with their

2004 final dividend, a supplementary

dividend of 2.5588 cents per ordinary

share. The dates for the determination of

entitlement to and the payment of this

supplementary dividend are the same as

those for the 2004 final dividend.

DIRECTORS’REPORT

1998 2000

28

72

44

56

2003

32

68

2002

36

64

1999 2004

37

63

42

58

2001

20

80

NET INTEREST-BEARING DEBT : EQUITY RATIO

EquityNet interest-bearing debt

DIRECTORS’ REPORT

(cont inued)

PROPRIETORSHIP RATIO (%)

199951

.82001 2002

54.5

2003

54.7

2004

51.9

20001998

50.7

50.0

63.1

19

C A V A L I E R C O R P O R A T I O N L I M I T E D

DIRECTORS

Mr Keith Thorpe was appointed a non-

executive Director of the Company with

effect from 23 February 2004. Mr Thorpe

was a long-term senior executive with

Lion Nathan and is a former chief

executive officer and a former chairman

of New Zealand Wines and Spirits

Limited. He is currently chairman of Swift

and Moore Pty Limited and a director of

Zespri Group Limited. Mr Thorpe has

a strong marketing and international

business background, and his experience,

qualifications, and skills will complement

those of the existing Directors.

Long-time Finance Director, Mr Wayne

Chung, was appointed to the position

of Managing Director on my retirement

from that executive role on 13 April

2004. Shareholders would be aware that

this change was to enable me to succeed

Mr Anthony Timpson as Chairman. At the

same time, the Directors also appointed

Mr Victor Tan, Company Secretary, to the

position of Finance Director.

Your Directors advise that Mr Chung

was selected from a short-list of

candidates put forward by the

Nominations Committee of the Board

after an Australasian-wide search

designed to ensure that all internal

candidates were benchmarked against

the best available externally.

Pursuant to the Constitution of the

Company, Mr Anthony Timpson and

I retire by rotation at the next Annual

Meeting scheduled for 4 November 2004

and, being eligible, offer ourselves for

re-election.

Mr Timpson was last re-elected to the

Board in November 2001, whereas I was

elected to the Board in October 1993.

Mr Keith Thorpe and Mr Victor Tan,

being Directors appointed by the Board

in between Annual Meetings, hold office

until the next Annual Meeting and, being

eligible, offer themselves for election.

There have been no other nominations.

AUDITORS

KPMG have indicated their willingness

to continue in office in accordance with

section 200 of the Companies Act 1993

(“the Act”). A resolution authorising your

Directors to fix the remuneration of the

auditors will be put to shareholders at the

Annual Meeting.

NON-AUDIT SERVICES AND AUDITOR INDEPENDENCE

Your Directors confirm that KPMG

also provided the Group with taxation

compliance services during the year.

The fees charged for these services

were $26,000.

Your Directors note that the provision

of taxation services by the external

auditors is permitted by the International

Federation of Accountants guidelines

and are satisfied that the independence

of the external auditors has not been

compromised.

KPMG did not provide the Group with

any other non-audit services during the

year.

DIRECTORS’ DISCLOSURES

The various disclosures required of your

Directors under the Act are set out on

pages 52 to 54.

OTHER STATUTORY DISCLOSURES

The other statutory disclosures required

of the Company under the Act are set out

on pages 55 and 56.

MANAGEMENT AND STAFF

On behalf of your Directors, I take

this opportunity to acknowledge

the contributions of Mr Chung, his

management team, and all our staff over

the past year.

A M JAMES CHAIRMAN

17 September 2004

The equity attributable to shareholders of the Company

increased by $4,615,000 during the year to $66,596,000.

“

”ALAN JAMES, CHAIRMAN

DIRECTORS’ REPORT

C A V A L I E R C O R P O R A T I O N L I M I T E D

20

I N D I V I D U A L S T R E N G T H T E A M F O C U S E D

TOTAL YEARS INDUSTRY

EXPERIENCE

*INDEPENDENT DIRECTORSON BOARD

CURRENT & EX-MDS

ON BOARD3 3 181

BOARD OF DIRECTORS1 2 3 4

5 6 7 8

BOARD OF DIRECTORS

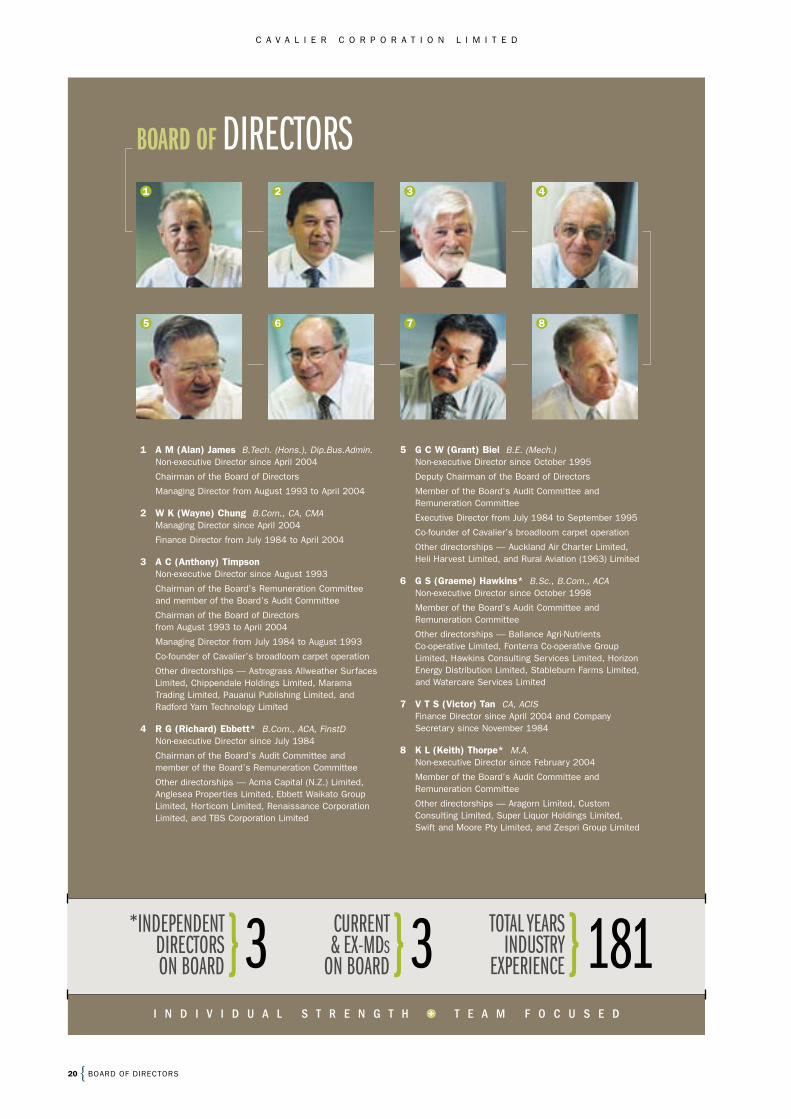

1 A M (Alan) James B.Tech. (Hons.), Dip.Bus.Admin.Non-executive Director since April 2004

Chairman of the Board of Directors

Managing Director from August 1993 to April 2004

2 W K (Wayne) Chung B.Com., CA, CMAManaging Director since April 2004

Finance Director from July 1984 to April 2004

3 A C (Anthony) TimpsonNon-executive Director since August 1993

Chairman of the Board’s Remuneration Committee and member of the Board’s Audit Committee

Chairman of the Board of Directors from August 1993 to April 2004

Managing Director from July 1984 to August 1993

Co-founder of Cavalier’s broadloom carpet operation

Other directorships — Astrograss Allweather Surfaces Limited, Chippendale Holdings Limited, Marama Trading Limited, Pauanui Publishing Limited, and Radford Yarn Technology Limited

4 R G (Richard) Ebbett* B.Com., ACA, FinstDNon-executive Director since July 1984

Chairman of the Board’s Audit Committee and member of the Board’s Remuneration Committee

Other directorships — Acma Capital (N.Z.) Limited, Anglesea Properties Limited, Ebbett Waikato Group Limited, Horticom Limited, Renaissance Corporation Limited, and TBS Corporation Limited

5 G C W (Grant) Biel B.E. (Mech.)Non-executive Director since October 1995

Deputy Chairman of the Board of Directors

Member of the Board’s Audit Committee and Remuneration Committee

Executive Director from July 1984 to September 1995

Co-founder of Cavalier’s broadloom carpet operation

Other directorships — Auckland Air Charter Limited, Heli Harvest Limited, and Rural Aviation (1963) Limited

6 G S (Graeme) Hawkins* B.Sc., B.Com., ACANon-executive Director since October 1998

Member of the Board’s Audit Committee and Remuneration Committee

Other directorships — Ballance Agri-Nutrients Co-operative Limited, Fonterra Co-operative Group Limited, Hawkins Consulting Services Limited, Horizon Energy Distribution Limited, Stableburn Farms Limited, and Watercare Services Limited

7 V T S (Victor) Tan CA, ACISFinance Director since April 2004 and Company Secretary since November 1984

8 K L (Keith) Thorpe* M.A.Non-executive Director since February 2004

Member of the Board’s Audit Committee and Remuneration Committee

Other directorships — Aragorn Limited, Custom Consulting Limited, Super Liquor Holdings Limited, Swift and Moore Pty Limited, and Zespri Group Limited

21

C A V A L I E R C O R P O R A T I O N L I M I T E D

Cavalier Corporation’s systems

ensure that:

¬ business strategies, plans, and budgets

are reviewed and approved

¬ performances against business

objectives are monitored

¬ significant business risks are identified,

monitored, and mitigated

¬ the multitude of laws that affect the

Company and its business activities are

complied with

¬ such matters as significant acquisitions

and disposals, delegated authority

limits, and executive remuneration are

reviewed and approved

¬ all matters of importance are brought

to its attention through a system of

prompt and comprehensive reporting.

In discharging its responsibility, the

Board exercises, on behalf of the

shareholders who appointed it, all the

powers of the Company not otherwise

required by law or the Constitution to be

exercised by shareholders.

Responsibility for the day-to-day

operation and administration of the

Company is delegated to the Managing

Director, who is accountable to the Board.

COMPOSITION OF THE BOARD

The Board currently comprises six

non-executive Directors (including the

Chairman and the Deputy Chairman) and

two executive Directors (the Managing

Director and the Finance Director).

The Board comprises Directors with a

broad range of experience and expertise

and whose core competencies include

accounting and finance, business

judgement, management, industry

knowledge, strategic vision, and

information technology.

The profile of the Directors can be found

on page 20.

One-third, or the number nearest to

one-third, of the Directors (excluding

any Director appointed by the Board

in between Annual Meetings) retire by

rotation at each Annual Meeting. The

Directors to retire are those who have

been longest in office since their last

election. Directors retiring by rotation are

eligible for re-election at that meeting.

A Director appointed by the Board in

between Annual Meetings holds office

only until the next meeting, but is eligible

for election at that meeting.

CORPORATE GOVERNANCETHE BOARD OF DIRECTORS IS RESPONSIBLE FOR THE MANAGEMENT AND

SUPERVISION OF THE BUSINESS AND AFFAIRS OF THE COMPANY. THE BOARD

DISCHARGES THIS RESPONSIBILITY BY ENSURING THAT ADEQUATE SYSTEMS

ARE IN PLACE. THESE SYSTEMS ARE BUILT AROUND SOUND AND PROVEN

PROCEDURES, POLICIES, AND GUIDELINES.

CORPORATE GOVERNANCE

C O N F I D E N C ET R A N S P A R E N C Y

WITHIN THE FRAMEWORK OUTLINED HERE, THE BOARD IS COMMITTED TO:

> Maximising returns to

shareholders by achieving

superior profit performance in

our businesses and by investing

at returns in excess of the cost

of capital

> Maintaining market leadership

by focusing on brand values,

superior product quality and

innovation, and outstanding

customer service

> Fostering an organisational

culture dedicated to continuous

improvement and cost efficiency

and being the most preferred

supplier in all markets and

market segments in which we

operate

> Conducting business with

consistency and absolute

integrity at all times

C A V A L I E R C O R P O R A T I O N L I M I T E D

22

Shareholders may nominate persons

for election to the Board at an Annual

Meeting by giving notice in writing to the

Company within the time notified by the

Company each year accompanied by the

consent in writing of that person to the

nomination.

BOARD MEETINGS

The Board has nine scheduled meetings

a year, but will also meet as and when

required to deal with any specific matters

that may arise between scheduled

meetings.

Details of attendances at the nine Board

meetings held during the year ended 30

June 2004 were:

G C W Biel . . . . . . . . . . . . . . . . . . . . . . 9/9

W K Chung . . . . . . . . . . . . . . . . . . . . . . 9/9

R G Ebbett . . . . . . . . . . . . . . . . . . . . . . 9/9

G S Hawkins. . . . . . . . . . . . . . . . . . . . . 8/9

A M James . . . . . . . . . . . . . . . . . . . . . . . 9/9

V T S Tan 1. . . . . . . . . . . . . . . . . . . . . . . 2/2

K L Thorpe 2 . . . . . . . . . . . . . . . . . . . . . 2/3

A C Timpson . . . . . . . . . . . . . . . . . . . . 9/9

1 Appointed on 13 April 20042 Appointed on 23 February 2004

REMUNERATION OF DIRECTORS

Unless specifically provided for in the

Constitution, the Board may not exercise

the power conferred by section 161 of

the Companies Act 1993 to authorise any

payment of remuneration to the Directors

in their capacity as such without the prior

approval of shareholders having first been

obtained.

Shareholders have previously resolved

that the total remuneration to be paid to

the non-executive Directors be fixed at a

sum not exceeding $250,000 per annum,

such sum to be divided amongst them

in such proportions and in such manner

as they may determine. The Directors

advise that the total remuneration paid to

the non-executive Directors for the year

ended 30 June 2004 was $160,115.

The remuneration packages of the

executive Directors, who are not entitled

to any remuneration in their capacity

as Directors, are fixed by the Board’s

Remuneration Committee, which is

composed entirely of the non-executive

Directors. The executive Directors do not

participate in decisions affecting their

own remuneration packages.

The remuneration of the Directors can be

found on page 54.

COMMITTEES OF THE BOARD

The Board has two standing committees

— one for audit and the other for

executive remuneration.

Audit Committee

The Board’s Audit Committee is

charged with, amongst other things, the

responsibility of reviewing the financial

statements. It is also responsible for

ensuring that adequate internal control

systems are in place to provide the

Board with reasonable assurance that

the Company’s assets are safeguarded,

transactions are recorded and reported

appropriately, and policies are followed.

This Committee meets as and when

required, but at least twice a year, with

management, the independent auditors,

and other internal auditors appointed

from time to time. These meetings are to

enable the Committee to review the work

of each of these groups and to satisfy

itself that they are discharging their

respective responsibilities adequately.

It is a policy of the Board that the

independent auditors have unrestricted

access to the Audit Committee, and it is

standard practice for the Committee to

meet twice a year with the independent

auditors in the absence of executives.

Details of attendances at the two Audit

Committee meetings held during the year

ended 30 June 2004 were:

G C W Biel . . . . . . . . . . . . . . . . . . . . . . 2/2

R G Ebbett . . . . . . . . . . . . . . . . . . . . . . 2/2

G S Hawkins. . . . . . . . . . . . . . . . . . . . . 2/2

A C Timpson . . . . . . . . . . . . . . . . . . . . 2/2

Executive Directors are not members

of the Audit Committee, and their

attendances at Audit Committee

meetings are by invitation and then only

in their capacity as executives.

The members of the Audit Committee

as at 30 June 2004 were Messrs

R G Ebbett (Chairman), G C W Biel,

G S Hawkins, A M James, K L Thorpe,

and A C Timpson. Messrs R G Ebbett

and G S Hawkins have accounting

backgrounds and are members of the

Institute of Chartered Accountants of

New Zealand. Messrs A M James and

K L Thorpe were not members of the

Audit Committee at the time the two

Audit Committee meetings were held

during the year ended 30 June 2004.

CORPORATEGOVERNANCE

CORPORATE GOVERNANCE

(cont inued)

23

C A V A L I E R C O R P O R A T I O N L I M I T E D

Remuneration Committee

The Remuneration Committee meets

as and when required, but at least once

a year, to consider and recommend to

the Board the remuneration packages of

the executive Directors and to approve

those of other senior executives of the

Company. In considering or approving

the remuneration packages of the