Embed Size (px)

Citation preview

Page 1 of 84

LNALewis Nathan AdvocatesLNALewis Nathan Advocates

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION.

The definitions commencing on page 8 of this Circular apply mutatis mutandis to this document including the cover page.

This Document is neither a prospectus nor an invitation to the public to subscribe for shares in Cavmont Capital Holdings Zambia Plc (“CCHZ” or “the Company”), but is an offer on a claw back basis to existing CCHZ shareholders, to acquire shares in the Company on the terms and conditions set out in this Circular.

Action Required:

This entire Circular is important and should be read with particular attention to page 5 entitled “Action required by CCHZ shareholders” which sets out the action required of them with regard to the Claw‐back Rights Offer;

If you are in any doubt as to the meaning of the contents of this Circular or as to the action you should take, please consult your accountant, bank manager, stockbroker or other professional advisor immediately;

If you no longer hold any shares in CCHZ, then you should send this Circular, as soon as possible, to the stockbroker through whom the sale of your shareholding in CCHZ was effected for onward transmission to the purchaser or transferee of those CCHZ shares;

Letters of Allocation (“LAs”) may only be traded in dematerialised form and accordingly CCHZ has issued all Letters of Allocation in dematerialised form.

CAVMONT CAPITAL HOLDINGS ZAMBIA PLC

(Incorporated in the Republic of Zambia, Company Registration Number: 41902) Share Code: CCHZ

ISIN: ZM0000000227 (“Cavmont” or “the Company”)

CIRCULAR TO SHAREHOLDERS

Regarding a

RENOUNCEABLE CLAW‐BACK RIGHTS OFFER Of 64,285,714,286 ordinary shares of ZMK 1.00 (one Zambian Kwacha) par value each in the share capital of CCHZ (“Claw ‐back Rights Offer

Shares”), at a subscription price of ZMK 1.40 per Claw‐back Rights Offer Share (“Claw‐back Offer Price”), on the basis of 90 (ninety) new

Claw‐back Rights Offer Shares for every 7 (seven) ordinary shares already held as at the Record Date, payable in full on acceptance;

and incorporating:

the information required for a Pre‐Listing Statement for the purposes of providing information to the public on CCHZ which complies with the

Listing Requirements of the LuSE.

JOINT LEAD ADVISERS

STOCKBROKERS ZAMBIA LIMITED

IMARA BOTSWANA LIMITED

Legal Adviser Independent Reporting Accountant

LEWIS NATHAN ADVOCATES DELOITTE & TOUCHE CHARTERED ACCOUNTANTS

Sponsoring Broker Transfer Secretary

STOCKBROKERS ZAMBIA LIMITED

CORPSERVE ZAMBIA

Date of Issue: 16 November 2012

Page 2 of 84

The Directors of CCHZ, whose names are given in section E of this Circular, collectively and individually accept full responsibility

for the accuracy of the information contained in this Circular and confirm that to the best of their knowledge and belief, there

are no other facts the omission of which would make any statement false or misleading, that they have made all reasonable

enquiries to ascertain such facts and that the Circular contains all information required by law.

Each of the Joint Lead Advisers to the Offer and the listing, Sponsoring Broker, Legal Adviser and Independent Reporting

Accountant have consented in writing to act in the capacities stated and to their names being stated and, where applicable, their

reports being included in this Circular.

Copies of this Circular are available in English only and may be obtained during normal business hours between 16 November and

07 December 2012 from the registered office of the Company and the offices of the Sponsoring Brokers, the addresses of which

are set out in the “Corporate Information” section on page 3 of this Circular.

Page 3 of 84

CORPORATE INFORMATION

Company Secretary and Registered Office Issuer

Louis Kabula Cavmont Capital Holdings Zambia Plc

Cavmont Capital Holdings Zambia Plc PwC Place, Plot 2374

PwC Place , Plot 2374 Thabo Mbeki Road

Thabo Mbeki Road P.O. Box 38474

P.O. Box 38474 Lusaka

Lusaka Zambia

Zambia

Joint Lead Adviser Joint Lead Adviser and Sponsoring Broker

Imara Botswana Limited Stockbrokers Zambia Limited (a member of the LuSE)

Plot 117, Millennium Office Park 2nd Floor, Stock Exchange Building

Ground Floor, Block A Unit 2 Central Park

Kgale Hill, P Bag 00186 P.O. Box 38956

Gaborone Lusaka

Botswana Zambia

Legal Advisers Transfer Secretary

Lewis Nathan Advocates Corpserve Share Transfer Agents

The Nathan Park, 758 Independence Avenue Plot 3671

Woodlands House Number 6, Mwaleshi Road

P.O. Box 37268 P.O Box 37522

Lusaka Lusaka

Zambia Zambia

Banker Independent Reporting Accountant

Cavmont Bank Limited Deloitte & Touche Chartered Accountants

PwC Place, Plot 2374 Abacus Square, Plot no. 2374/B

Thabo Mbeki Road Thabo Mbeki road

P.O. Box 38474 P.O. Box 30030

Lusaka Lusaka

Zambia Zambia

Auditors

PricewaterhouseCoopers

PwC Place

Stand No. 2374, Thabo Mbeki Road

P.O. Box 30942

Lusaka

Zambia

Page 4 of 84

CONTENTS

Page

CORPORATE INFORMATION 3

CONTENTS 4

ACTION REQUIRED BY CAVMONT SHAREHOLDERS 5

IMPORTANT INFORMATION 6

SALIENT DATES AND TIMES 7

DEFINITIONS 8

SALIENT FEATURES OF THE CLAW‐BACK RIGHTS OFFER 11

1. THE CLAW‐BACK RIGHTS OFFER 11

2. FINANCIAL EFFECTS OF THE CLAW‐BACK OFFER 11

3. DIRECTORS’ OPINION, RECOMMENDATION AND UNDERTAKING 11

4. PRE‐LISTING STATEMENT 11

CIRCULAR TO SHAREHOLDERS 12

A. PURPOSE OF THIS CIRCULAR 12

B. THE CLAW‐BACK OFFER 13

C. INFORMATION RELATING TO CAVMONT CAPITAL HOLDINGS ZAMBIA PLC 17

D. FINANCIAL INFORMATION 23

E. INFORMATION RELATING TO THE DIRECTORS 25

F. GENERAL INFORMATION 27

ANNEXURE I EXTRACTS FROM THE ARTICLES OF ASSOCIATION 28

ANNEXURE II TABLE OF ENTITLEMENTS 29

ANNEXURE III INFORMATION RELATING TO THE UNDERWRITERS 30

ANNEXURE IV REPORT ON THE FORECAST STATEMENT OF COMPREHENSIVE INCOME AND STATEMENT OF FINANCIAL POSITION 31

ANNEXURE V REPORT OF THE INDEPENDENT REPORTING ACCOUNTANT 35

LETTER OF ALLOCATION AND ACCEPTANCE FORM 81

Page 5 of 84

ACTION REQUIRED BY CAVMONT SHAREHOLDERS

COURSES OF ACTION

Action to be taken by CCHZ Shareholders

In order to participate in the Claw‐back Rights Offer, you need a copy of this Circular and your Letter of Allocation, which indicates your

name, the number CCHZ shares that you held as at the Record Date, which was Friday, 02 November 2012, and the number of Claw‐back

Rights Offer Shares that you are entitled to purchase on the basis of 90 Claw‐back Rights Offer Shares for every 7 ordinary shares held on

Record Date –and then follow the courses of action provided at on page 39 of this Circular and summarized below.

If you are a Shareholder and wish to buy more Claw‐back Rights Offer Shares, over and above your entitlement on the Record Date, you

should contact your stockbroker to purchase tradable rights or Letters of Allocation (LAs) listed on the LuSE during the period from 16

November 2012 to 05 December 2012, at the then prevailing market price, and thereafter proceed to purchase the Claw‐back Rights Offer

Shares associated with the purchased LAs, at the Claw‐back Rights Offer Price of ZMK 1.40 (one Kwacha and four ngwee) per Claw‐back

Rights Offer Share.

Pursuant to this Claw‐back Rights Offer by Cavmont Capital Holdings Zambia Plc, shareholders may elect one of four courses of action to

follow. The four options are summarised below. Should you have any questions about the appropriate action to take, please consult your

financial advisor or your stockbroker, or the Sponsoring Broker to the transaction, Stockbrokers Zambia Limited.

1. SUBSCRIBE for Claw‐back Rights Offer Shares offered (acceptance)

Complete Section A of the Renounceable Letter of Allocation/ Acceptance Form (at the end of this Circular) and see your broker to effect

payment for the Claw Back shares being subscribed for. Alternatively you can deposit or transfer your payment to the following bank account:

BANK : CAVMONT BANK LIMITED

ACCOUNT NAME : CCHZ CLAW‐BACK RIGHTS OFFER

ACCOUNT NUMBER : 0800000104572

BRANCH SORT CODE : 13‐00‐17

And send the completed Acceptance Form, together with your certified Deposit Slip as proof of payment, or a Cheque or Bank Draft, in favour

of “CCHZ CLAW‐BACK RIGHTS OFFER”, crossed “not negotiable” and “not transferable” by no later than 16h00 on Friday, 07 December 2012 to

the Sponsoring Broker whose details are given on page 3.

2. SELL your rights through the LuSE (renunciation)

Complete Section B of the Renounceable Letter of Allocation (at the end of this Circular) and send it to your stockbroker, or to the Sponsoring

Broker with the instructions to “sell the rights”. Participants will be permitted to sell their rights over the LuSE during the Offer Period.

3. SUBSCRIBE in part for Claw‐back Rights Offer Shares AND SELL the remaining rights through the LuSE

Complete Section B of the Renounceable Letter of Allocation (at the end of this Circular) and deposit or transfer your payment to the following

bank account:

BANK : CAVMONT BANK LIMITED

ACCOUNT NAME : CCHZ CLAW‐BACK RIGHTS OFFER

ACCOUNT NUMBER : 0800000104572

BRANCH SORT CODE : 13‐00‐17

Send the completed form to your stockbroker, or to the Sponsoring Broker with the instructions to “subscribe for a number of Rights Offer

Shares and sell the balance”, together with your certified Deposit Slip as proof of payment, or a Cheque or Bank Draft, in favour of “CCHZ

CLAW‐BACK RIGHTS OFFER”, crossed “not negotiable” and “not transferable” by no later than 13h00 on Wednesday, 05 December 2012 to the

Sponsoring Broker whose details are given in page 3.

Participants will be permitted to sell their rights over the LuSE between Friday, 16 November 2012 and Wednesday, 05 December 2012.

4. Non Action

Shareholders not selecting any of the foregoing options by Friday, 07 December 2012, the closing of the Offer Period, will be deemed to have

selected the option to sell all of their rights at the then prevailing price and, provided there are buyers for the rights, they will be sold by their

stockbroker or in the event that shareholders do not have a broker, by the Sponsoring Broker. This period for the sale of rights where the

shareholder “does nothing” will also close on Friday, 07 December 2012.

Page 6 of 84

IMPORTANT INFORMATION

The definitions as set out in the “Definitions” section of this Circular apply to this section regarding important information.

No person has been authorised by CCHZ to give any information or to make any representation not contained in or not consistent with this

Circular or any other information supplied in connection with the Claw‐back Rights Offer. If given or made, such information or representation

must not be relied upon as having been authorised by CCHZ, the Joint Lead Advisers or the Legal Advisers. Neither the delivery of this Circular

nor any subscription made in connection herewith shall, under any circumstances, create any implication that there has been no change in the

affairs of CCHZ since the date of the publication of this Circular, or that any other financial statement or other information supplied in

connection with the Circular is correct at any time subsequent to the date indicated in the document containing the same.

This Circular does not constitute an offer to sell or the solicitation of an offer to buy or subscribe for any Claw‐back Rights Offer Shares, in any

jurisdiction, to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. Neither CCHZ nor the Joint Lead Advisers

or Legal Adviser represent that this Circular may be lawfully distributed, or that any Claw‐back Rights Offer Shares may be lawfully offered, in

compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available there under,

or assumes any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by CCHZ, the Joint Lead

Advisers or the Legal Adviser that would permit a public offering of any Claw‐back Rights Offer Shares or distribution of this Circular in any

jurisdiction where action for that purpose is required. Accordingly, no Claw‐back Rights Offer Shares may be offered or subscribed for, directly

or indirectly, and neither this Circular nor any advertisement or other offering material may be distributed or published in any jurisdiction,

except in compliance with any applicable laws and regulations, and the Joint Lead Advisers have represented that all offers and sales or

subscriptions will be made in compliance with this prohibition. To the extent that this Circular may be sent to any jurisdiction in which the

dissemination of this Circular is illegal or fails to conform to the laws of such jurisdiction, it is provided for information purposes only.

The distribution of this Circular and the offer or sale of or subscriptions for Claw‐back Rights Offer Shares may be restricted by law in certain

jurisdictions. Persons into whose possession this Circular or any Claw‐back Rights Offer Shares come, must inform themselves about, and

observe any such restrictions. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such

jurisdiction.

The Claw‐back Rights Offer Shares have not been and will not be registered under the US Securities Act or with any securities regulator of any

state or jurisdiction of the United States. Claw‐back Rights Offer Shares may not be offered, sold, subscribed for or delivered within the United

States or to US persons except in accordance with Regulations under the US Securities Act.

Market and industry data

Market and other statistical information used throughout this Circular are based on independent industry publications, government

publications or other published independent sources. Although CCHZ believes these sources are reliable, the Company has not verified the

information independently and cannot guarantee its accuracy and completeness.

Forward looking statements

This Circular includes “forward‐looking statements” which include all statements other than statements of historical facts, including, without

limitation, those regarding CCHZ’s financial position, profit and revenue forecasts, business strategy, plans and objectives of management for

future operations (including development plans and objectives relating to CCHZ’s subsidiary’s products and services) and any statement

preceded by, followed by or that includes the word “projects”, “prospects”, “estimates”, “targets”, “believes”, “expects”, “aims”, “intends”,

“will”, “may”, “anticipates”, “would”, “could” or “seeks” or any similar expression or the negative thereof.

Such forward‐looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other

important factors beyond the Company’s control that could cause the actual results, performance and/or achievements of CCHZ to be

materially different from future results, performance and/or achievements expressed or implied by such forward‐looking statements. Such

forward‐looking statements are based on numerous assumptions regarding the Group’s present and future business performance and/or

strategies and the environment in which CCHZ will operate in the future.

These forward‐looking statements speak only as of the date of this document. CCHZ and its directors expressly disclaim any obligation or

undertaking to disseminate revisions to any forward‐looking statements contained in this Circular to reflect any change in CCHZ’s expectations

with regard to such statements or any change in events, conditions or circumstances on which any such statements are based, unless required

to do so by applicable law.

Page 7 of 84

SALIENT DATES AND TIMES

Last day to trade in CCHZ shares in order to settle by the Record Date and to qualify to participate

in the Claw‐back Rights Offer (cum entitlement)

Tuesday, 30 October 2012

Record Date for participation in the Claw‐back Rights Offer Friday, 02 November 2012

Listing of Letters of Allocation (Las) on the LuSE Friday, 16 November 2012

Claw‐back Offer Circular posted to CCHZ shareholders by Friday, 16 November 2012

Claw‐back Offer opens Friday, 16 November 2012

Last day to trade in Letters of Allocation on the LuSE Wednesday, 05 December 2012

Claw‐back Rights Offer closes Friday, 07 December 2012

Dematerialised CCHZ shareholders’ accounts updated with Claw‐back Rights Offer Shares to the

extent accepted

Friday , 14 December 2012

Results of Claw‐back Offer announcement published on or about Friday ,14 December 2012

Claw Back Shares commence trading ex‐claw‐back rights on the LuSE Monday , 17 December 2012

Page 8 of 84

DEFINITIONS

Throughout this Private Placing Offer Document and the appendices hereto, unless otherwise indicated, the words in the first column have the

meanings stated opposite them in the second column, words in the singular include the plural and vice versa, words importing one gender

include the other gender and references to a person include references to a body corporate and vice versa:

“Acceptance Form(s)” the forms of acceptance attached to the back of this Circular, to be used by

Applicants in connection with the Offer;

“Act” means the Securities Act Chapter 354 of the Laws of Zambia;

“Allocation” means the allocation of Claw‐back Rights Offer Shares to Applicants under the

Claw‐back Rights Offer;

“Applicable Laws” the Laws of the Republic of Zambia in force from time to time, to which this

Circular is subject;

“Applicant(s)” a person, including juristic persons, applying for Claw‐back Rights Offer Shares in

terms of the Claw‐back Rights Offer set out in this Circular;

“Articles” the Articles of Association of CCHZ as amended from time to time;

“ATS” Automated Trading System of the LuSE;

“Bank of Zambia” or “BOZ” the Central Bank of the Republic of Zambia;

“Bank of Zambia Policy Rate” or “BOZ Policy Rate” the policy rate as set by BoZ from time to time;

“Banking and Financial Services Act” the Banking and Financial Services Act, Chapter 387 of the laws of Zambia;

“Board” or “Board of Directors” the Board of Directors of CCHZ;

“Business Day” any day other than a Saturday, Sunday or official public holiday in the Republic of

Zambia;

“Cavmont Bank” or “CBL” Cavmont Bank Limited (registration number 26788), a wholly owned subsidiary of

CCHZ, a private company duly registered and incorporated in terms of the laws of

the Republic of Zambia and whose licensed activity is the provision of banking and

financial services in Zambia;

“CEE Act” the Citizenship Economic Empowerment Act, No 9 of 2006;

“Central Share Depository” or “CSD” the LuSE Central Shares Depository Limited, a company incorporated in Zambia

with registration number 36617, whose functions are to serve as custodian of the

LuSE tradable securities and to hold such securities in electronic form in its central

depository on behalf of the beneficial owners; and to provide clearing and

settlement services to the LuSE;

“Central Statistics Office” or “CSO” the Central Statistics Office of the Government of the Republic of Zambia;

“CIH” Capricorn Investment Holdings Limited, a company registered in Namibia under

registration number 82/031 and whose registered office is 6th Floor, CIH House,

Kasino Street, P. O. Box 15, Windhoek, Namibia

“Circular” this circular to CCHZ shareholders dated DD, 16 November 2012, including any

annexure and document incorporated by reference and the Acceptance Form;

“Claw‐back Rights Offer” the renounceable claw‐back offer by CCHZ of 64,285,714,286ordinary shares at a

subscription price of ZMK 1.40 per share in the ratio of 90 new ordinary shares for

every 7 ordinary shares held at the close of business on Friday, 02 November 2012;

“Claw‐back Rights Offer Price” ZMK1.40 per Claw‐back Rights Offer Share;

Page 9 of 84

“Claw‐back Rights Offer Shares” the 64,285,714,286 new ordinary shares which are the subject of the Claw‐back

Rights Offer;

“Closing Date” being the last date and time for submission of Acceptance Forms which falls on

Friday, 07 December 2012;

“Company” or “CCHZ” Cavmont Capital Holdings Zambia Plc (registration number 41902), a public limited

liability company duly registered and incorporated in terms of the laws of the

Republic of Zambia and whose registered office is located at PwC Place, Plot 2374,

Thabo Mbeki Road, Lusaka, Zambia;

“Companies Act” the Companies Act, Chapter 388 of the laws of Zambia;

“Directors” the executive and non‐executive directors of the Company whose details are set

out in Section E of this Circular;

“DPS” dividend per share;

“Employees” individuals that are pensionable employees, contractual employees, executives or

Directors of the Company;

“EPS” earnings per share;

“FSDP” the Financial Sector Development Plan. A comprehensive strategy that has been

formulated by the Government of the Republic of Zambia (GRZ) to address the

current weaknesses in the Zambian financial system as well as guide efforts aimed

at realising the vision of a financial system that is stable, sound and market‐based

and that would support efficient resource mobilisation necessary for economic

diversification and sustainable growth;

“Global Share Certificate” the single certificate, registered in the name of the LuSE CSD or its nominee, and

representing dematerialised shares;

“GDP” Gross Domestic Product;

“Imara” Imara Botswana Limited (Registration number 2002/2770), a company registered

in Botswana;

“Joint Lead Advisers” Stockbrokers Zambia Limited (Registration number 52224), a company registered

in Zambia and Imara Botswana Limited (Registration number 2002/2770), a

company registered in Botswana;

“Kwacha” or “K” or “ZMK” or “ZK” the legal tender of Zambia in which all monetary amounts in this Private Placing

Offer Document are expressed unless otherwise indicated;

“Legal Adviser” Lewis Nathan Advocates;

“Letter of Allocation” or “LA” the renounceable Letter of Allocation, for each shareholder of CCHZ as at Record

Date, in respect to the Claw‐back Rights Offer, which is attached hereto as

Appendix 7, that will be posted to each shareholder of CCHZ after the Record Date,

and which sets out the entitlement of the person/ shareholder to whom this

Circular is addressed with respect to the Claw‐back Rights Offer;

“Lewis Nathan Advocates” a law firm incorporated in Zambia and regulated by the Law Association of Zambia.

“the LuSE” the Lusaka Stock Exchange Limited a company incorporated in Zambia with

registration number 30495, whose functions are to operate a market for the

trading (i.e. buying and/ or selling) of securities. The LuSE is licensed and regulated

by the Securities and Exchange Commission of Zambia (“SEC”) under the Securities

Act Chapter 354 of the Laws of Zambia;

Page 10 of 84

“Mukumbi” Mukumbi Investments Limited (registration number 105785), a wholly owned

subsidiary of CIH, a private company duly registered and incorporated in terms of

the laws of the Republic of Zambia and created to facilitate the participation of

Zambians or Zambian entities in the ownership of Cavmont Bank;

“Net Asset Value” or “NAV” the result of subtracting a company’s long term and current liabilities from the

sum of its fixed and current assets;

“Ordinary Shares” Ordinary Shares with a par value of K 1.00 each in the share capital of CCHZ;

“PACRA” the Patents and Company Registration Agency of Zambia;

“PAT” profit after tax;

“PBT” profit before tax;

“PBV ratio” price to book value ratio;

“PE ratio” price to earnings ratio;

“the Receiving Agents” the receiving agents to the Offer;

“the Registrar of Companies” the Zambian Registrar of Companies, established pursuant to section 366 of the

Company’s Act;

“Return on Assets” or “ROA” the result of dividing a company’s PAT by the average total assets;

“Return on Equity” or “ROE” the result of dividing a company’s PAT by the average shareholder’s equity;

“RTGS” Real Time Gross Settlement;

“SADC” Southern African Development Community;

“the Securities Act” the Securities Act, Chapter 354 of the laws of Zambia;

“the SEC” the Securities and Exchange Commission Zambia, a statutory body established

under the Securities Act Cap 354 of the laws of Zambia;

“Sponsoring Broker” Stockbrokers Zambia Limited;

“Stockbrokers Zambia Limited” Stockbrokers Zambia Limited (Registration number 52224), a company registered

in Zambia and a member of the LuSE and licensed by the SEC as a dealer;

“Underwriter(s)” CIH and Mukumbi;

“Underwriting Agreement” The underwriting agreement entered into between CCHZ as issuer and the

Underwriters whereby on 28 September 2012 CIH , subscribed for 17,009,814,181

shares and Mukumbi for 13,619,471,534 shares, in CCHZ, on a claw back basis at

the Claw Back Rights Offer Price;

“USD” or “US$” United States Dollars;

“US Securities Act” US Securities Act of 1933, as amended;

Page 11 of 84

SALIENT FEATURES OF THE CLAW‐BACK RIGHTS OFFER

This summary section highlights certain information contained in this Circular, which should be read in its entirety for a full appreciation of the subject matter contained herein. If you are in any doubt as to its meaning, or what action to take, please consult, a licensed broker, investment adviser, accountant, lawyer or other professional adviser.

This section does not purport to be complete and is taken from, and is qualified by, the remainder of this Circular. Terms not otherwise defined in this section have the same meaning as used in the “Definitions” section of the Circular.

1. THE CLAW‐BACK RIGHTS OFFER

1.1 Introduction and terms of the Claw‐back Rights Offer

At the 13th Annual General Meeting of the Company held on 05 July 2012, shareholders authorised the Board of Directors to proceed with the

recapitalisation of Cavmont Bank Limited, the wholly owned subsidiary of Cavmont Capital Holdings Zambia PLC, to comply with the new BoZ

capital adequacy framework announced on 30 January 2012, by raising up to a maximum of Zambian Kwacha 90,000,000,000 (ZMK 90 billion).

On 28 September 2012, CCHZ issued 17,009,814,181 ordinary shares to CIH and 13,619,471,534 ordinary shares to Mukumbi at a price of ZMK

1.40 per share as the first step towards recapitalisation of Cavmont Bank Limited on the basis of Claw‐back Rights Offer by CCHZ.

Shareholders were subsequently notified by way of the First and Second Announcements published in the press on 19 October 2012 and 29

October 2012 respectively, that in order to provide equal opportunity to all shareholders to participate in the recapitalisation of Cavmont Bank

Limited, CCHZ was undertaking a Renounceable Claw‐back Rights Offer.

The second step and final stage of the Claw‐back Rights Offer is now to offer the Claw Back Rights Shares to all shareholders of CCHZ other

than CIH and Mukumbi.

Accordingly, CCHZ shareholders are now offered the right to claw back their shareholding in CCHZ by participating in this Claw‐back Rights

Offer to acquire the Claw Back Rights Shares as ordinary shares in CCHZ on the basis of 90 Claw‐back Rights Offer Shares for every 7 CCHZ

ordinary shares held on the Record Date at a price of ZMK 1.40 per Claw‐back Rights Offer Share.

All shareholders who are owed dividends which were declared but not paid by the Company, may use those unpaid dividends to take up Claw

Back Rights Shares at a price of ZMK 1.40 per Claw‐back Rights Offer Share as part of this Claw‐back Rights Offer process.

1.2 Purpose of the Claw‐back Rights Offer

The proceeds of the Claw‐back Rights Offer will be used to recapitalise Cavmont Bank Limited, the 100 % wholly owned subsidiary of Cavmont

Capital Holdings Zambia Plc, in an effort to comply with the new Bank of Zambia capital adequacy framework announced on 30 January 2012.

1.3 Underwriting Agreement

In terms of the Underwriting Agreement (incorporated herein by reference), CIH and Mukumbi agreed to subscribe for a combined total of

30,629,285,715 Claw‐back Rights Offer Shares at an issue price of ZMK 1.40 per Claw‐back Rights Offer Share as partial underwriting of the

ZMK 90 billion capital raise by CCHZ. In addition it is envisaged that some Zambian institutional investors may commit to participate as co‐

underwriters. An underwriting flat fee of 1.5% of the value of the underwriting commitment is payable to each of the Underwriters and any co‐

underwriters who subsequently sign up for this role.

2. FINANCIAL EFFECTS OF THE CLAW‐BACK OFFER

At ANNEXURE IV is provided the Reporting Accountants Report on the forecast statement of comprehensive income and statement of financial

position to 31 December 2012.

3. DIRECTORS’ OPINION, RECOMMENDATION AND UNDERTAKING

The directors, whose names are given in the “Information relating to the directors” in section F of this circular, have considered the terms of

the Claw‐back Rights Offer and are of the opinion that the terms thereof are fair and reasonable to CCHZ shareholders and, accordingly,

recommend that the shareholders follow their Claw‐back Rights in terms of the Claw‐back Rights Offer as set out in this Circular.

4. PRE‐LISTING STATEMENT

In compliance with paragraph 6.18(g) of the LuSE Listing Requirements, this Circular contains information required in a Pre‐Listing Statement.

COPIES OF THIS CIRCULAR

Copies of this Circular, in English, may be obtained during normal business hours between Friday, 16 November 2012 and Friday, 07 December

2012 from the registered office of the Company and the offices of the Sponsoring Broker, at the addresses set out in the “Corporate

information” section of this Circular.

Page 12 of 84

CAVMONT CAPITAL HOLDINGS ZAMBIA PLC

(Incorporated in the Republic of Zambia, Company Registration Number: 41902) Share Code: CCHZ

ISIN: ZM0000000227 (“Cavmont” or “the Company”)

________________________________ Directors

Guy D. Z Phiri (Independent Chairman), Joseph Ngosa (Non‐Executive Director), Johan Swanepoel (Non‐Executive Director)

Johan Minnaar (Managing Director).

Address: PwC Place, Plot 2374, Thabo Mbeki Road, Stand no. 2374 P O Box 38474, Lusaka, Zambia.

CIRCULAR TO SHAREHOLDERS

A. PURPOSE OF THIS CIRCULAR

Background

In 2011 the Board of Cavmont Bank Limited approached CIH to obtain long term funds to recapitalise the bank. Subsequently CIH provided K20

billion as Tier II capital which the Bank of Zambia approved in December 2011 and was ratified by the shareholders of CCHZ at the 13th

AGM held on 05 July 2012.

At the AGM held on 05 July 2012, shareholders of CCHZ also authorised the Board of Directors to proceed with a recapitalisation plan to

ensure Cavmont Bank Limited, the wholly owned subsidiary of Cavmont Capital Holdings Zambia PLC, complies with the new Bank of Zambia

capital adequacy framework announced on 30 January 2012 for locally owned banks, by raising up to a maximum of Zambian Kwacha

90,000,000,000 (K90 billion).

At the AGM held on 05 July 2012, the shareholders approved the following resolution:

“ To AUTHORISE the Board of Directors to proceed with the capital raise to ensure Cavmont Bank Limited, the wholly owned subsidiary of

Cavmont Capital Holdings Zambia PLC, complies with the new Bank of Zambia capital adequacy framework announced on 30 January 2012, by

raising up to a maximum of Zambian Kwacha 90,000,000,000 (K90 billion) at a share issue price not less than the minimum allowed in terms of

the prevailing Lusaka Stock Exchange Listings Rules and Requirements as they pertain to a capital raise, provided that such capital raise shall be

in compliance with and in a form acceptable to both the Lusaka Stock Exchange and the Bank of Zambia requirements for such capital raise.

The capital raise will be in the form of an underwritten rights offer (the “Rights Offer”) or an underwritten public offer (the “Public Offer”)

where the existing shareholders shall have a pre‐emptive right to acquire shares.”

On 28 September 2012, CCHZ issued 17,009,814,181 ordinary shares to CIH and 13,619,471,534 ordinary shares to Mukumbi at a price of ZMK

1.40 per share to raise a total of ZMK 42,881,000,000 as the first step of the Claw‐back Rights Offer to raise the required sum of ZMK 90 billion

for recapitalisation of Cavmont Bank Limited. Part of the proceeds from this claw back capital raise will be used to acquire and convert into

ordinary shares the Tier II capital that was provided by CIH to Cavmont Bank in 2011.

Shareholders were subsequently notified by way of the First and Second Announcements dated 19 October 2012 and 29 October 2012 that in

order to provide equal opportunity to all shareholders to participate in the recapitalisation of Cavmont Bank Limited, CCHZ was undertaking a

Renounceable Claw‐back Rights Offer.

The second step and final stage of the Claw‐back Rights Offer is to now offer the Claw Back Rights shares to all shareholders of CCHZ, other

than CIH and Mukumbi, as per this Circular document.

Page 13 of 84

Accordingly, CCHZ shareholders are now offered the right to claw back their shareholding in CCHZ by participating in this Claw‐back Rights

Offer by acquiring shares in CCHZ on the basis of 90 Claw‐back Rights Offer Shares for every 7 CCHZ ordinary shares held on the Record Date at

a price of ZMK 1.40 per Claw‐back Rights Offer Share.

The purpose of this Circular is to provide CCHZ shareholders with all the relevant information relating to the Claw‐back Rights Offer and the

implications thereof in accordance with the LuSE Listing Requirements and the Securities Act.

This Circular contains information required for a Pre‐Listing Statement, which information is required in terms of paragraph 6.18(g) of the LuSE

Listing Requirements as a result of the Company issuing shares in terms of the Claw‐back Rights Offer in excess of 30% of its current shares in

issue.

B. THE CLAW‐BACK OFFER

1. INTRODUCTION

1.1 At the 13th Annual General Meeting of the Company held on 05 July 2012, shareholders authorised the Board of Directors to proceed

with the recapitalisation of Cavmont Bank Limited, the wholly owned subsidiary of Cavmont Capital Holdings Zambia Plc, to comply with

the new Bank of Zambia capital adequacy framework for local banks announced on 30 January 2012, by raising up to a maximum of

Zambian Kwacha 90,000,000,000 (ZMK 90 billion). Holders of CCHZ ordinary shares registered as such at the close of business on Friday

02 November 2012 (the Record Date) will be entitled to receive rights or Letters of Allocation, reflecting the number of Claw‐back Rights

Offer Shares they are entitled to in terms of the Claw‐back Offer.

1.2 The LuSE has approved the listing of the Letters of Allocation (LAs) in respect of the Claw‐back Rights Offer Shares and from the

commencement of trade on Friday, 16 November 2012 until the close of trade on Wednesday, 05 December 2012.

1.3 In terms of the Claw‐back Offer, CCHZ shareholders recorded in the register at the close of business on Friday, 02 November 2012, being

the Record Date, will receive rights to subscribe for Claw‐back Rights Offer Shares in term of the Claw‐back Rights Offer on the basis of

90 Claw‐back Rights Offer Shares for every 7 CCHZ ordinary shares held on the Record Date, at a Claw‐back Rights Offer Price of ZMK

1.40 per Claw‐back Offer Share

1.4 The Claw‐back Rights Offer Shares, upon their issue, will rank pari passu in all respects, with the ordinary shares currently in issue.

2. PURPOSE OF THE CLAW‐BACK RIGHTS OFFER

On 30 January 2012, the Bank of Zambia issued a circular, (referenced as CB Circular No.: 02/2012), revising the capital requirements of

commercial banks in Zambia. Prior to 30 January 2012 the minimum capital requirement for commercial banks operating in Zambia was ZMK

12 billion. In the revised BOZ regulations, the new capitalisation requirements for commercial banks are linked to the shareholding structure of

the banks as follows:‐

i) For foreign owned banks, the minimum capital requirement is now ZMK 520 billion; and

ii) For locally owned banks a lower capital requirement threshold of ZMK 104 billion has been set.

A locally owned bank refers to a bank licenced by the BOZ where at least 51% of its equity is owned by Zambian citizens and or entities

incorporated in Zambia that have at least 51 % equity owned by Zambian citizens .

A foreign owned bank refers to a bank licensed by the BOZ where more than 49% of its equity is owned by foreign entities.

Cavmont Bank Limited is a wholly owned subsidiary of CCHZ. CCHZ is listed on the Lusaka Stock Exchange.

Following the announcement by BOZ on 30 January 2012 regarding the revised capital requirements of commercial banks in Zambia, CCHZ

initiated a shareholding restructuring and recapitalisation plan for the Company. The proposed plan essentially involves the following two key

and critical actions on a simultaneous basis:

i) The restructuring of the shareholding in CCHZ such that Cavmont Bank qualifies as a locally owned bank in terms of the revised BOZ

regulations; and

ii) The recapitalisation of Cavmont Bank via a capital raise by CCHZ.

The primary reason for the Claw‐back Rights Offer is therefore to restructure the shareholding of CCHZ and simultaneously recapitalise CBL,

the wholly owned subsidiary of CCHZ.

Page 14 of 84

3. TERMS OF THE CLAW‐BACK RIGHTS OFFER

3.1 Particulars of the Claw‐back Rights Offer

CCHZ shareholders and/ or their renounces are hereby offered for subscription, by way of a Renounceable Claw‐back Rights Offer, a total of

64,285,714,286 CCHZ ordinary shares at a Claw‐back Rights Offer Price of ZMK 1.40 per Claw‐back Rights Offer Share on the basis of 90 Claw‐

back Rights Offer Shares for every 7 CCHZ ordinary shares held as at the Record date, being Friday, 02 November 2012.

The Claw‐back Offer Price is payable in Zambian Kwacha in full upon acceptance of the Claw‐back Offer.

The Claw‐back Offer Price represents a discount of 69% to the 90 day volume weighted average price (VWAP) of ZMK 4.50 of CCHZ shares on

28 September 2012, the date of the Underwriting Agreement.

CCHZ shareholders recorded in the register on the Record Date, being Friday, 02 November 2012, or renounces in terms of the Claw‐back Offer

will be entitled to participate in the Claw‐back Offer.

The Letters of Allocation may be traded on the LuSE during the period from Friday, 16 November 2012 to Wednesday, 05 December 2012.

3.2 Opening and closing dates of the Claw‐back Offer

The Claw‐back Offer will open at the commencement of trade on Friday, 16 November 2012 and will close at 14h00 on Friday, 07 December

2012.

3.3 Entitlement

CCHZ shareholders are entitled to subscribe for 90 Claw‐back Rights Offer Shares for every 7 CCHZ ordinary share held as at Record Date and

are referred to the Table of Entitlements set out in Annexure 2 to this Circular. The allocation of Claw‐back Shares will be such that only whole

numbers of Claw‐back Rights Offer Shares will be issued and shareholders will be entitled to rounded numbers of Claw‐back Rights Offer

Shares. Fractional entitlements of 0.5 or greater will be rounded up and those less than 0.5 will be rounded down.

3.4 Excess applications

Holders of Letters of Allocation may apply for a greater number of Claw‐back Rights Offer Shares than those allocated in terms of the Claw‐

back Offer and set out in such Letter of Allocation.

Applications for excess Claw‐back Rights Offer Shares must be made by completing the Acceptance Form in accordance with instructions

contained therein.

All applications for excess Claw‐back Rights Offer Shares must be accompanied by sufficient funds to cover such applications in accordance

with 5.3 below.

Cheques and/ or the refunding of monies in respect of unsuccessful applicants for additional Claw‐back Rights Offer Shares will be posted to

the relevant applicant, at their risk, on or about 17 December 2012. No interest will be paid on any monies received in respect of unsuccessful

applications.

3.5 Listing of Letters of Allocation and Claw Back Rights Offer Shares on the LuSE

The LuSE has granted the listings for the Claw‐back Rights Offer Shares and Letters of Allocation as follows:

i) Letters of Allocation in respect of 64,285,714,286 Claw‐back Rights Offer Shares will be listed from the commencement of trade on Friday,

16 November 2012 until the close of trade on Wednesday, 05 December 2012, both days inclusive;

ii) 64,285,714,286 Claw‐back Rights Offer Shares will be listed with effect from the commencement of trade on Monday, 17 December 2012.

3.6 Takeover and Mergers Rules

At the 13th Annual General Meeting of the Company held on 05 July 2012, shareholders resolved that a mandatory offer in terms of Clause 56

of the Securities (Takeover and Mergers) Rules, Statutory Instrument No 170 of 1993 of the Securities Act, would be waived in the event that a

person or entity or related parties acquired 35% or more voting rights in CCHZ arising from the participation in the Claw‐back Rights Offer

described in this Circular.

3.7 Limits on voting rights under Zambian banking regulations

Under the BFSA, no person or entity can hold directly or indirectly more than 25% voting rights in a bank in Zambia unless that person or entity

is listed on a recognised stock exchange. Accordingly, it will be necessary to seek and obtain BOZ approval for any shareholding exceeding 25%

voting power in CCHZ as a result of the Claw Back Rights Offer described in this document.

Page 15 of 84

4. APPLICATION OF NEW CAPITAL

The new capital shall be applied as follows:‐

Figures (ZMK’ Millions) 2012 2013 2014 Total

Support Lending Capacity 37,500 37,500 75,000

Branch Refurbishments 1,000 2,400 3,000 6,400

Branch Relocations 1,000 800 1,800

Fixed Assets 1,000 1,500 1,000 3,500

Technology 1,300 2,000 3,300

Total 90,000

Loans and advances – The capital shall be used to support the lending capacity;

Branch improvements & renovation of Archives Building;

Branch Relocations;

Fixed Assets for improvements to security (CCTV), office equipment and teller cubicles; and

Technology includes Mobile banking and ATMs.

5. PROCEDURE FOR ACCEPTANCE, RENUNCIATION AND SALE OF CLAW‐BACK RIGHTS

The enclosed Letter of Allocation reflects the number of Claw‐back Rights Offer Shares for which a shareholder is entitled to subscribe. Any

instruction to accept, sell or renounce all or part of the Claw‐back Rights Offer Shares allocated to them may be made by means of the

Acceptance Form.

5.1 Acceptance

Full details of the procedure for acceptance of the Claw‐back Rights Offer are contained in the Acceptance Form enclosed with this Circular. It

should be noted that:

5.1.1 acceptances are irrevocable and may not be withdrawn;

5.1.2 acceptances may be made only by means of the Acceptance Form;

5.1.3 any instruction to sell or renounce all or part of the Claw‐back Rights Shares may only be made by means of the Acceptance Form;

5.1.4 the properly completed Acceptance Form and together with your certified Deposit Slip as proof of payment, or a Cheque or Bank

Draft, in favour of “CCHZ CLAW‐BACK RIGHTS OFFER”, crossed “not negotiable” and “not transferable”, for the relevant Claw‐back

Rights Offer Shares must be received by the Sponsoring Broker at the addresses set out in the “Corporate information” section of this

Circular by no later than 14h00 on Friday, 07 December 2012;

5.1.5 the Acceptance Form to take up the Claw‐back Offer Rights will be regarded as complete only when monies have been cleared for

payment;

5.1.6 such payment will constitute an irrevocable acceptance of the Claw‐back Offer upon the terms and conditions set out in this circular

and in the Acceptance Form once monies have been cleared for payment;

5.1.7 if any Acceptance Form is not received as set out above, the Claw‐back Rights Offer will be deemed to have been declined and the

Claw‐back Rights to purchase the Claw‐back Rights Offer Shares in terms of the Letter of Allocation will lapse regardless of who holds

it;

5.1.8 no acknowledgement of receipt will be given for monies received in respect of the Claw‐back Rights Offer.

Page 16 of 84

5.2 Renunciation or sale of Claw‐back Rights

5.2.1 CCHZ has issued the Letters of Allocation in dematerialised form.

5.2.2 The Letters of Allocation to which the Acceptance Form relates are negotiable and can be traded on the LuSE.

5.2.3 Shareholders who do not wish to purchase all, or some of the Claw‐back Rights Offer Shares allocated to them as reflected in the

Letter of Allocation, may sell or renounce or lapse their Claw‐back Rights.

5.2.4 In addition, shareholders who wish to sell the Claw‐back Rights allocated to them as reflected in the Letter of Allocation must

complete the relevant section of the Acceptance Form and return it to the Sponsoring Brokers in accordance with the instructions

contained therein, to be received no later than 14h00 on Friday, 07 December 2012.

5.2.5 The Sponsoring Broker will endeavour to procure the sale of the Claw‐back Rights on the LuSE on behalf of such shareholders and will

remit the proceeds in accordance with the payment instruction reflected in the Acceptance Form, net of brokerage charges and

associated expenses. Neither the Sponsoring Broker nor the Company nor any broker appointed by either of them will have any

obligation or responsibility for any loss or damage whatsoever in relation to or arising out of the timing of such sales, the price

obtained or any failure to sell such Claw‐back Rights. References in this paragraph to shareholders include references to the person

or persons executing the Acceptance Form and any person or persons on whose behalf such person or persons executing the

Acceptance Form is/ are acting and in the event of more than one person executing the Acceptance Form, the provisions of this

paragraph shall apply to them, jointly and severally.

5.2.6 Shareholders who do not wish to sell the Claw‐back Rights allocated to them as reflected in the Letter of Allocation, and who do not

wish to purchase the Claw‐back Rights Offer Shares offered in terms of the Acceptance Form but who wish to renounce their Claw‐

back Rights, should complete the relevant section of the Acceptance Form and return it to the Sponsoring Broker in accordance with

the instructions contained therein, to be received by no later than 14h00 on Friday, 07 December 2012.

5.2.7 Shareholders who wish to purchase only a portion of the Claw‐back Rights Offer Shares allocated to them must indicate on the

Acceptance Form, the number of Claw‐back Rights Offer Shares which they wish to purchase.

5.3 Payment

5.3.1 Currency

The amount due on acceptance of the Claw‐back Offer is payable in Zambian Kwacha.

5.3.2 Payment terms

The amount due on acceptance is payable in Zambia Kwacha by deposit or transfer to the following bank account:

BANK : CAVMONT BANK LIMITED

ACCOUNT NAME : CCHZ CLAW‐BACK RIGHTS OFFER

ACCOUNT NUMBER : 0800000104572

BRANCH SORT CODE : 13‐00‐17

Payment may also be in the form of manager’s cheques or bankers’ drafts (crossed “not negotiable”) in respect of subscriptions and should be

made payable to “CCHZ CLAW‐BACK OFFER”. Cheques and bankers’ drafts and completed Letters of Allocation should be lodged, with

payment, with the Sponsoring Brokers Broker at the addresses set out in the “Corporate information” section of this Circular by no later than

14h00 on Friday, 07 December 2012.

All cheques or drafts received by the Sponsoring Broker will be deposited immediately. In the event that any cheque or bank’s draft is

dishonoured, CCHZ, in its sole discretion, may treat the relevant acceptance as void or may tender delivery of the relevant Claw‐back Rights

Offer Shares to which it relates against payment in cash of the Claw‐back Offer Price for such Claw‐back Rights Offer Shares. Payments

received in respect of an Application which is rejected or otherwise treated as void by CCHZ, or which is otherwise not validly received in

accordance with the terms stipulated in this paragraph, will be posted by registered mail (without interest) by way of a cheque drawn in

Zambian Kwacha to the Applicant concerned, at the Applicant’s risk on or about 17 December 2012. If the Applicant concerned is not a CCHZ

shareholder and gives no address in the Acceptance Form, then the relevant refund will be held by CCHZ with no interest payable to the

Applicant until collected by the Applicant.

Page 17 of 84

5.3.3 Share certificates

Where applicable, share certificates in respect of Claw‐back Rights Offer Shares will be posted, by registered mail, by the Transfer Secretaries,

at the risk of the certificated shareholders concerned, on or about Monday, 17 December 2012.

Certificated shareholders receiving Claw‐back Rights Offer Shares in certificated form must note that such shares cannot trade on the LuSE

until they have been dematerialised.

Dematerialised shareholder’s LuSE CSD accounts will be credited with the Claw‐back Rights Offer Shares subscribed for in terms of the Claw‐

back Offer on Monday, 17 December 2012.

6. UNDERWRITING AGREEMENT

CCHZ has entered into the Underwriting Agreement with CIH and Mukumbi in terms of which CIH and Mukumbi subscribed for and were

issued 17,009,814,181 and 13,619,471,534 Claw‐back Rights Offer Shares each respectively at an issue price of ZMK 1.40 per Claw‐back Offer

Share, which raised a total of ZMK 42.9 billion or 47.66% of the Claw Back Rights Offer, and subject to claw‐back in terms of the Renounceable

Claw‐back Offer to CCHZ shareholders.

An underwriting fee of 1.50 % of the value of the subscription commitment is payable to each Underwriter.

Information relating to the Underwriters is set out in ANNEXURE III to this Circular.

Minimum subscription

The minimum subscription is ZMK 45 billion or 50 % of the total Claw back Rights Offer Shares on offer. Of this ZMK 45 billion, a total of ZMK

42.9 billion or 47.66 % has already been raised from the Underwriters

7. TAX CONSEQUENCES

CCHZ shareholders are advised to consult their professional advisers regarding the tax consequences of the Claw‐back Offer.

8. JURISDICTION

The distribution of this Circular and the offer of Claw‐back Rights Offer Shares may be restricted by law in certain jurisdictions. Persons who

are in possession of this Circular are cautioned to familiarise themselves, and to observe any such restrictions. The Claw‐back Rights Offer

Shares have not been and will not be registered in any jurisdiction outside of Zambia. Any investor(s) from any jurisdiction outside of Zambia,

is (are) required to comply with the laws of that jurisdiction in participating in this Rights Offer.

C. INFORMATION RELATING TO CAVMONT CAPITAL HOLDINGS ZAMBIA PLC

1. INCORPORATION AND HISTORY

The Company was originally incorporated in Zambia on 6 January 1999 as Cavmont Capital Leasing Company Limited. Its name was

subsequently changed to Cavmont Capital Holdings Zambia Limited and to Cavmont Capital Holdings Zambia PLC following its conversion to a

public company on 25 September 2003. Its ordinary shares were first quoted on the LuSE in October 2005 and it became fully listed on the

LuSE in September 2006.

Cavmont Bank Limited is 100 % owned by CCHZ and was originally incorporated as Cavmont Merchant Bank Limited on 29 October 1992 and is

registered as a bank under the Banking and Financial Services Act. It changed its name to Cavmont Capital Bank Limited following its merger

with its affiliate New Capital Bank Limited, a Zambian retail bank incorporated in March 1992.

In 2007, CIH, a banking and financial services group from Namibia acquired a 25% stake in CCHZ. CIH subsequently provided partial

underwriting to the renounceable rights offer undertaken by CCHZ in November 2007 and consequently increased its equity stake in CCHZ

beyond 25% by holding non‐voting shares. CIH has supported CBL with technical support services in the past when required. In 2010 CCHZ

conducted a rebranding exercise and changed the name of the bank to Cavmont Bank Limited.

Page 18 of 84

Current Holding Structure

2. NATURE OF BUSINESS AND PROSPECTS

2.1 Nature of business

Cavmont Bank Limited distributes its products via a branch network of 15 branches and 1 agency. Six are community branches through which

the Bank distributes banking services to local communities. Started as a project in 2003 with seed funding from the United Kingdom’s

Department for International Development (DFID) under its Financial Deepening Challenge Fund (FDCF), the Bank has now invested more than

ZMK 4.1 billion in its Community Banking Division, which enables the Bank to provide banking services to community enterprises and small

businesses that otherwise would not be able to access banking services.

i) The Bank presently provides corporate, retail, treasury and community banking facilities to over 52,000 customers. The number of

customers is on a strong growth path as its points of representation increase for the retail, community and rural branches.

ii) Historically, CBL traditionally deployed its deposits in the GRZ treasury‐bill and bond market. With the repositioning and rebranding of the

bank in 2010, CBL now operates as a full scope commercial bank with a full suite of lending, deposit and other banking service and

product offerings.

iii) The vision of CBL is “to be a world class bank rated amongst the best in Zambia with a focus on partnering with all (its) stakeholders”. To

this end, the bank seeks to provide tailored, convenient banking products and services coupled with a focus on customer service.

iv) As at 30th June 2012, compared to other Zambian banks, CBL ranked 7

th in terms of number of branches, 10

th in terms of loans and

advances to customers, 14th in terms of total assets, and 11

th in terms of customer deposits.

Regulatory Framework

The Bank operates under the following legal framework;

Banking and Financial Services Act, 1994, as amended – this prescribes the operating and reporting framework for financial institutions.

The monitoring and compliance aspect is handled by the Bank of Zambia (BOZ) who is the regulator of the industry. From time to time

BOZ issues circulars prescribing changes in certain legislation

Companies’ Act, 1994, as amended – the Act prescribes the operating and reporting framework for all types of companies and gives

guidance on various matters including share capital, dividends, directors, meetings of directors and winding up of companies.

Securities Act – this prescribe the continuing obligations of companies listed and quoted on the Lusaka Stock Exchange (LuSE).

Income Tax Act – this prescribes the income tax framework for Banks.

Lusaka Stock Exchange (LuSE) – its listing rules and guidelines.

Anti‐money laundering guidelines – the act provides guidance on how to deal and report money laundering activities in the conduct of

banking activities.

Non-Voting 19.2% Voting 25.0% Total 44.2%

CCHZ

CAVMONT BANK

LIMITED

100%

Capricorn Investment Other Shareholders

Non-Voting 0%

Voting 75% Total 55.8%

Page 19 of 84

The principal activity of CCHZ is that of a holding company. Its major activity comprises commercial banking through Cavmont Bank Limited, a

100% wholly owned subsidiary.

2.2 Prospects

The Zambian banking industry has experienced dramatic growth over the last 10 years, with more growth expected as the economy expands.

Over the last two years CBL’s balance sheet has grown substantially, a new system has been implemented, the bank has been rebranded and

additional services have been rolled out (Visa Cards, Electronic Internet banking etc.). CBL is well positioned in the local market and the

recapitalisation presents an opportunity for the bank to leverage off its current infrastructure and expand the business. With support from

shareholders, local institutions and the strategic investor, and with the increased capital at its disposal, the management team of CBL is

confident that the bank will return to profitability. The recapitalisation of the banking sector in Zambia will have a significant effect on the

industry. CBL is recognised as a leading local bank and believes that this presents an opportunity to strengthen its position in the market.

3. CAPITAL STRUCTURE

3.1 Summary of alterations to the share capital and issued shares in the past three years

At the 13th Annual General Meeting of shareholders of CCHZ, resolutions were passed to approve the increase in authorised share capital from

7,255,000,000 ordinary shares of ZMK 1.00 par value each to 57,255,000,000 ordinary shares of ZMK 1.00 par value each. The share capital of

the Company has not been changed in any other way over the past three years.

Date Number of shares Nominal Value per share

(ZMK)

Total Nominal Value

(ZMK)

Authorised share capital (ZMK)

31 December 2011 5,500,000,000 ordinary shares 1.00 5,500,000,000

31 December 2011 1,750,000,000 non‐convertible 1.00 1,750,000,000

31 December 2011 5,000 preference shares 1,000 5,000,000

Increase in Authorised share capital 28 September 2012 50,000,000,000 ordinary shares 1.00 50,000,000,000

31 October 2012 42,745,000,000 ordinary shares 1.00 42,745,000,000

Total Authorised share capital 31 October 2012 100,000,000,000 1.00 100,000,000,000

Issued share capital (ZMK) 31 December 2011 5,000,000,000 1.00 5,000,000,000

Increase in Issued share capital 28 September 2012 30,629,285,715 1.00 30,629,285,715

31 October 2012 28,656,428,570 1.00 28,656,428,570

Total Issued shares after Rights Offer 69,285,714,286 1.00 69,285,714,286

Note* on 28th September 2012, 30,629,285,715 shares were issued at a price of ZMK1.40 per share and a total amount of capital of ZMK42,881,000,000.00 was

underwritten by CIH and Mukumbi to facilitate the underwritten claw back rights offer.

3.2 Unissued shares

The Company’s unissued ordinary shares are under the control of the Directors as directed and authorised by the shareholders subject to the

provisions of the Companies Act.

3.3 Information relating to the share capital and shares

3.3.1 Ordinary share capital

The entire issued ordinary share capital of CCHZ is listed on the LuSE and the LuSE has confirmed its continued listing subsequent to the Claw‐

back Offer.

3.4 Variation of rights attaching to shares

In accordance with the Company’s Articles of Association any variation of rights attaching to shares will require the consent of shareholders in

general meeting.

3.5 Voting rights

In accordance with the Articles of Association of CCHZ, at any general meeting, every shareholder present in person or by authorised

representative shall have one vote on a show of hands and on a poll every shareholder present in person, by authorised representative or by

Page 20 of 84

proxy shall have that proportion of the total votes in the Company which the aggregate amount of the par value of the shares held by that

shareholder bears to the aggregate of the par value of all the shares issued by the Company to which voting rights attach.

3.6 Authorisations relating to shares

At the 13th Annual General Meeting of CCHZ held on 05 July 2012 at Taj Pamodzi Hotel in Lusaka, shareholders authorised an increase in the

authorized share capital of CCHZ from 7,255,000,000 to 57,255,000,000 ordinary shares of ZMK 1.00 for the purposes of raising ZMK 90 billion

via an underwritten rights offer or an underwritten public offer.

Subsequently, a filing was made into PACRA increasing the authorised share capital from 57,225,000,000 ordinary shares to 100,000,000,000

ordinary shares in order to facilitate the issuance of 64,285,714,286 ordinary shares at ZMK 1.40 per share required to raise the required ZMK

90 billion. This addendum is to be ratified at the next extra ordinary general meeting of shareholders tentatively scheduled to be held on or

about 07 December 2012.

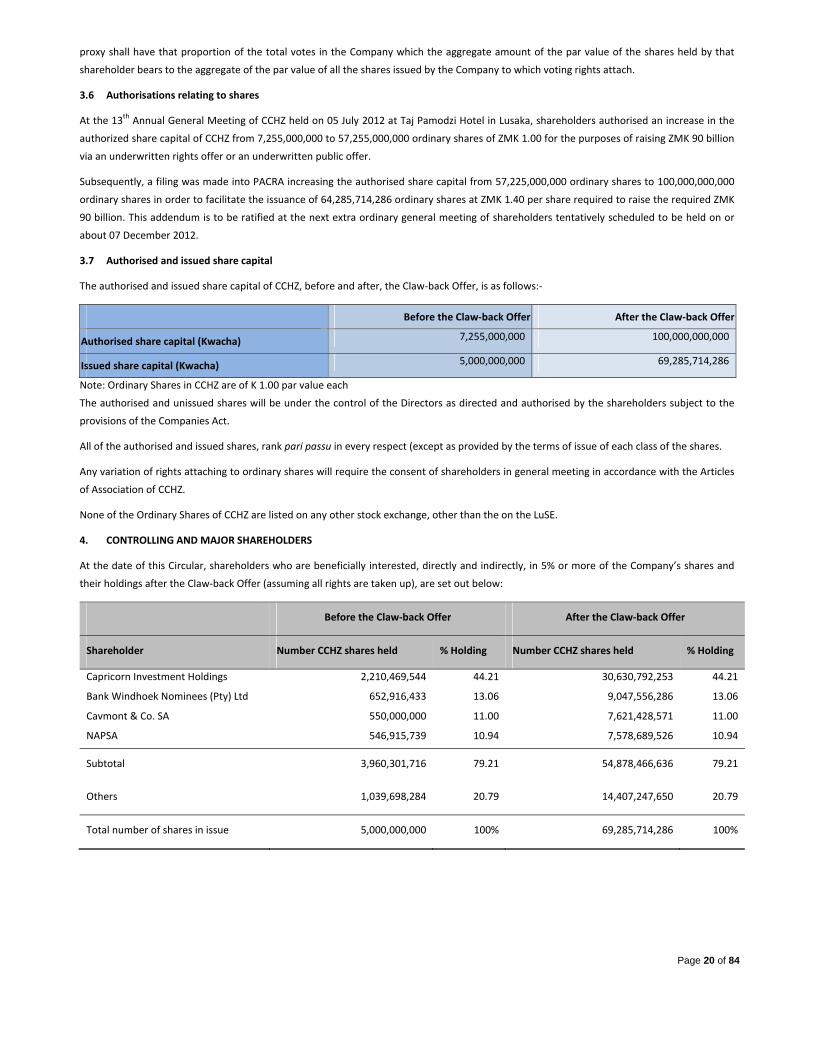

3.7 Authorised and issued share capital

The authorised and issued share capital of CCHZ, before and after, the Claw‐back Offer, is as follows:‐

Before the Claw‐back Offer After the Claw‐back Offer

Authorised share capital (Kwacha) 7,255,000,000 100,000,000,000

Issued share capital (Kwacha) 5,000,000,000 69,285,714,286

Note: Ordinary Shares in CCHZ are of K 1.00 par value each

The authorised and unissued shares will be under the control of the Directors as directed and authorised by the shareholders subject to the

provisions of the Companies Act.

All of the authorised and issued shares, rank pari passu in every respect (except as provided by the terms of issue of each class of the shares.

Any variation of rights attaching to ordinary shares will require the consent of shareholders in general meeting in accordance with the Articles

of Association of CCHZ.

None of the Ordinary Shares of CCHZ are listed on any other stock exchange, other than the on the LuSE.

4. CONTROLLING AND MAJOR SHAREHOLDERS

At the date of this Circular, shareholders who are beneficially interested, directly and indirectly, in 5% or more of the Company’s shares and

their holdings after the Claw‐back Offer (assuming all rights are taken up), are set out below:

Before the Claw‐back Offer After the Claw‐back Offer

Shareholder Number CCHZ shares held % Holding Number CCHZ shares held % Holding

Capricorn Investment Holdings 2,210,469,544 44.21 30,630,792,253 44.21

Bank Windhoek Nominees (Pty) Ltd 652,916,433 13.06 9,047,556,286 13.06

Cavmont & Co. SA 550,000,000 11.00 7,621,428,571 11.00

NAPSA 546,915,739 10.94 7,578,689,526 10.94

Subtotal 3,960,301,716 79.21 54,878,466,636 79.21

Others 1,039,698,284 20.79 14,407,247,650 20.79

Total number of shares in issue 5,000,000,000 100% 69,285,714,286 100%

Page 21 of 84

5. MATERIAL CONTRACTS, PROMOTERS, SERVICE AND OTHER AGREEMENTS

CIH and CBL have entered into an agreement for professional and technical services relating to various support to CBL.

6. LITIGATION

Subject to review by the Legal Adviser , the Directors of CCHZ believe the current ongoing litigation cases do not affect the operations of CCHZ

or CBL, and therefore not material.

7. SUBSIDIARY COMPANIES

Cavmont Bank Limited is a wholly owned subsidiary of CCHZ, a private company duly registered and incorporated in terms of the laws of the

Republic of Zambia and whose licensed activity is the provision of banking and financial services in Zambia.

8. SHARE PRICE HISTORY AND RIGHTS OFFER VALUATION

The graph below depicts the trend in the share price of CCHZ on the LuSE over the past eight years since 2005.

0

2

4

6

8

1 0

1 2

1 4

1 6

1 8

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Share Price -Zmk

Y E A R

C C H Z Sh a re Pr ice tre nd :J a nua ry 2005 - Septem ber 2012

CCH Z

Rights Offer Pricing

CCHZ last traded on the LuSE at a share price of ZMK 4.50 on 15 October 2012. To take into account the low liquidity in the share price on the

LuSE a valuation exercise was undertaken to determine the appropriate offer price for the Claw Back Rights Offer Accordingly the Claw Back

Rights Offer price has been set at ZMK 1.40 which represents a discount of 69 % to the last traded price. The Offer price of ZMK 1.40 can be

contrasted to the Net Asset Value of ZMK 1.33 per share (as shown in the table below) and this gives a Price to Book Value (PBV) ratio of 1.05.

It is envisaged that that the high discount of 69 % and the low PBV ratio will encourage Zambian shareholders to follow their rights in the Claw

Back Rights Offer.

Date/reference Share Price Net Asset Value per share (NAV) Price to Book Value (PBV)

31 Dec 2011 ZMK 5.00 ZMK 2.37 2.10

29 June 2012 ZMK 4.00 ZMK1.33 3.00

November 2012 ‐ Rights Offer ZMK 1.40 ZMK 1.33 1.05

Page 22 of 84

9. CONSOLIDATION OF SHARE CAPITAL

On 09 November 2012 the company issued a notice to shareholders of an extraordinary shareholders meeting to consider and approve a

consolidation of the shares of the company to accommodate the Kwacha rebasing scheduled for 1 January 2013. The number of issued shares,

should all rights be taken up, will therefore reduce from 69,285,714,286 of ZMK 1 each to 69,285 714 of ZMK 1000 each.

It is proposed that, subject to the passing of the requisite special and ordinary resolutions at the EGM on 07 December 2012 and the filing of

the Resolutions at PACRA, CCHZ will implement a Consolidation of the authorised and issued share capital of the Company on the basis of 1

new CCHZ Consolidated Share for every 1,000 CCHZ ordinary shares of ZMK 1.00 par value each held as at the Record Date of 14 December

2012 by the consolidation of every 1,000 ordinary shares of par value of ZMK 1.00 each into 1 new CCHZ ordinary share with a par value of

ZMK 1,000.00 each.

The Consolidation is being proposed primarily to prepare CCHZ for the proposed currency rebasing exercise in Zambia.

The Bank of Zambia will rebase the Zambian currency by a factor of 1,000 commencing 01 January 2013. Therefore, share prices reported on

the LuSE will be divided by a factor of 1,000 across the board. Accordingly, the Consolidation is also intended to adjust the share price of CCHZ

ahead of the currency rebasing (but with no change in market value), and give a realistic resultant working figure when currency rebasing is

effected, commencing 01 January 2013.

Page 23 of 84

D. FINANCIAL INFORMATION

1. HISTORICAL FINANCIAL INFORMATION

The following tables set out selected historical financial information for the three years ended 31 December 2009, 2010 and 2011 and the six

months period ended 30 June 2012 from the Report of the Independent Reporting Accountant in ANNEXURE Vof this Circular. The Report of

the Independent Reporting Accountant on CCHZ has been prepared with reference to the financial statements audited by PWC. The financial

statements have been prepared in accordance with IFRS.

Report of the Independent Reporting Accountant

The Report of the Independent Reporting Accountant on CCHZ is contained in ANNEXURE V of this Circular.

Consolidated statement of comprehensive income for the preceding three years

The following table should be read in conjunction with the Report of the independent Reporting Accountant.

Kwacha millions

2011 2010 2009

Interest income 26,310 20,049 17,996

Interest expense (9,937) (4,213) (2,195)

NET INTEREST INCOME 16,373 15,836 15,801

Impairment losses on loans & advances (754) (1,194) (1,608)

Net interest income after loan impairment 15,619 14,642 14,193

Fees and commission income 15,471 11,321 9,480

Fees and commission expense (603) ‐ ‐

NET FEE AND COMMISSION INCOME 14,868 11,321 9,480

Foreign exchange income 4,339 3,658 4,778

Other income 111 79 680

Depreciation expense (1,809) (1,888) (1,469)

Operating expenses (50,151) (35,562) (29,747)

Loss before income tax (17,023) (7,749) (2,085)

Income tax credit (expense) 4,186 3,724 639

Loss for the year (12,837) (4,025) (1,446)

Earnings per share (2.57) (0.81) (0.28)

Dividend per share ‐ ‐ (0.40)

Years ended 31 December

Page 24 of 84

Consolidated statement of financial position as at 31 December for the last 3 years

Kwacha millions 2011 2010 2009

Assets

Cash and Balances with Bank of Zambia 35,645 31,966 32,660

Placements with other banks 28,008 31,877 14,115

Loans and advances 134,257 64,553 33,176

Investment securities 66,688 50,245 58,039

Current income tax 3,208 2,236 768

Property and equipment 19,907 17,964 8,409

Intangible assets 12,913 14,137 12,971

Deferred income tax 8,415 3,983 2,611

Receivables and prepayments 10,540 5,553 5,699

TOTAL ASSETS 319,581 222,514 168,448

Liabilities

Convertible redeemable preference shares 10,000 ‐ ‐

Customer Deposits 290,329 187,399 122,530

Other liabilities 7,371 10,643 15,317

Obligation under finance lease ‐ ‐ 79

Retirement benefit obligations ‐ ‐ 4,599

Total liabilities 307,700 198,042 142,525

Shareholders' equity

Share capital 5,000 5,000 5,000

Share premium 16,992 16,992 16,992

Revaluation reserve 3,200 2,954 380

Non distributable reserve 3,327 3,327 3,327

(Accumulated losses) Retained earnings (16,638) (3,801) 224

Total shareholders' equity 11,881 24,472 25,923

TOTAL EQUITY AND LIABILITIES 319,581 222,514 168,448

Net assets per share 2.37 4.89 5.18

Net (liabilities) assets per share (0.21) 2.07 2.59

2. PROFIT FORECAST

The Report of the Independent Reporting Accountant on the forecast Statement of comprehensive Income and Statement of financial position

for the year ended 31st December 2012 are contained in ANNEXURE IV of this Circular.

3. DIVIDENDS

The company has not paid a dividend in the last 3 years.

The company had unpaid dividends to a class of shareholders as at 31 December 2009 amounting to ZMK 1.3 billion and it is the intention of

the directors to issue shares or pay cash to eliminate the liability.

Page 25 of 84

E. INFORMATION RELATING TO THE DIRECTORS

1. DETAILS

The full names, qualifications, nationalities, addresses and occupations of the directors of CCHZ are set out below:

The Business Address of all Directors is PwC Place, Plot 2374, Thabo Mbeki Road, P O Box 32322, Lusaka, Zambia.

Brief profiles of the members of the CCHZ Board of Directors and the Company Secretary are set out in the table below.

Name of Director Summary profile

Guy Phiri

(Zambian)

(Independent)

Mr. Phiri was appointed as a Independent Director of CCHZ and CBL in November 2011. He was

subsequently elected chairman of the Board of CCHZ. Mr. Phiri is currently serving as the Managing Director

of Engen Petroleum Zambia Limited, overseeing all operations of Engen in Zambia. Mr Phiri is also chairman

of Engen Malawi, a director of the Zambian Federation of Employers, a member of the Institute of Directors,

a former director of Engen Botswana PLC and he holds a post graduate degree in Chemical Engineering.

Joseph Ngosa

(Zambian)

(Non‐Executive)

Mr. Joseph Ngosa was appointed as a Non-Executive Director for Cavmont Bank in August 2008. Mr. Ngosa

serves as a Director for the National Pension Scheme Authority (NAPSA) in charge of Investments. Prior to

his engagement with NAPSA, Mr. Ngosa served as Financial Services Manager, Financial Analyst and

Internal Auditor for Cavmont Bank Limited.

Johan Swanepoel

(Namibian)

(Non‐Executive)

Mr. Swanepoel was appointed as Managing Director of Bank Windhoek Limited on 1 July 1999. In 2005 he

took up the position of Group Managing Director of the Capricorn Investment Holdings Group. After joining

Coopers & Lybrand (now PricewaterhouseCoopers) in 1980, he qualified as a Chartered Accountant in 1982.

He was appointed Managing Partner of Coopers & Lybrand in Namibia in 1989

Johan Minnaar

(Namibian)

(Managing Director)

Mr. Johan Minnaar was appointed Managing Director for Cavmont Bank Limited in January 2010. He joined

Cavmont Capital Holdings Zambia PLC (CCHZ) in February 2008 as Executive Director on secondment from

Capricorn Investment Holdings Limited (CIH). He served as director for the repositioning project named

Project Makumbi. Mr. Minnaar started his banking career in 1973, and brings a considerable amount of

banking experience gained over three decades at Bank Windhoek in Namibia and Absa in South Africa,

amongst others.

Louis Kabula

(Zambian)

(Company Secretary)

Mr Kabula was appointed Chief Financial Officer for Cavmont Bank Limited in October 2009. In his role he is

responsible for Strategic Financial Guidance and Governance. Prior to joining Cavmont Bank Limited he held

a number of senior management positions in the Finance Portfolio at Flora Clothing, Standard Chartered

Bank Zambia Limited and Stanbic Bank Zambia Limited.

2. INTEREST IN THE COMPANY’S SHARES

Interests of Directors

The beneficial, direct and indirect interests of the directors and their associates in the Company’s shares before and after the Claw‐back Offer

(assuming all Claw‐back Rights Offer Shares are subscribed for) are set out below:

Name of Director Before Claw‐back Offer After Claw‐back Offer

Direct Indirect % Direct Indirect %

Guy D. Z. Phiri 1,182,216 ‐ 0.02 16,382,136 ‐ 0.02

Johan Swanepoel ‐ ‐ ‐ ‐ 2.00

There was no change in the directors’ interest, before the Claw‐back Offer, between the date of the Company’s most recent year‐end (31

December 2011) and the date of this Circular.

CIH and Mukumbi have entered into an underwriting agreement with CCHZ and it is noted that Johan Swanepoel is a director of both CIH and

CCHZ.

Page 26 of 84

Interests of Experts

The number of shares in which each expert holds relevant interest on the date of this Circular and on completion of this Claw back Rights Offer

are and will be approximately as follows :

Expert No of Share held prior to Rights Offer

Entitlement to new shares

on 90 for 7 basis

Total shares held after the Rights Offer

(assuming rights fully taken)

Charles Mate 668,469 8,594,601 9,263,070

3. INTERESTS IN TRANSACTIONS

Save as disclosed above neither the Directors of CCHZ nor any person acting in concert with the Directors, controls or is interested, beneficially

or otherwise, in any CCHZ Shares or in any securities convertible to rights to subscribe for CCHZ Shares.

4. AUTHORITY AND REMUNERATION OF DIRECTORS

The relevant provisions of the Articles of Association which authorise a rights offer are set out in ANNEXURE I to this Circular.

4.1 The remuneration paid to directors of CCHZ in the financial year ended 31 December 2011 was ZMK 370 million (2010: ZMK 367 million).

5. MATERIAL CHANGES

The Directors report that to their knowledge there have been no material changes in the financial or trading position of the Company since 31

December 2011, the date of the last audited financial statements of the same and set out in the Independent Reporting Accountants’ Report

on the Historical Financial Information of the Company as set out in Annexure V.

6. DIRECTORS’ RESPONSIBILITY STATEMENT

The directors, whose names are given in this section of the Circular, collectively and individually accept full responsibility for the accuracy of

the information given and certify that to the best of their knowledge and belief there are no other facts the omission of which would make any

statement false or misleading, that they have made all reasonable enquiries to ascertain such facts and that the Circular contains all

information required by law

Page 27 of 84

F. GENERAL INFORMATION

1. ADEQUACY OF CAPITAL

The Directors are of the opinion that after the issue of the 64,285,714,286 new Claw Back Rights shares:

The Company’s authorized share capital is adequate for the purposes of the business of the Company for the foreseeable future; and

The Company’s working capital resources will be adequate to cover for its current and foreseeable requirements.

2. PRELIMINARY EXPENSES