Embed Size (px)

Citation preview

IC10-31 January 27, 2010

CBSX Trader News Update CBSX to Add New Stocks for Trading

TO: Members SUBJECT: Bank of America Corporation Index Linked Notes Compliance and supervisory personnel should note that, among other things, this Information Bulletin discusses the need to deliver a prospectus to customers purchasing shares (“Shares”) of the seventeen (17) exchange-traded funds (“Funds”) listed below issued by Bank of America. Please forward this Information Bulletin to other interested persons within your organization. The following securities have been approved for trading on CBSX:

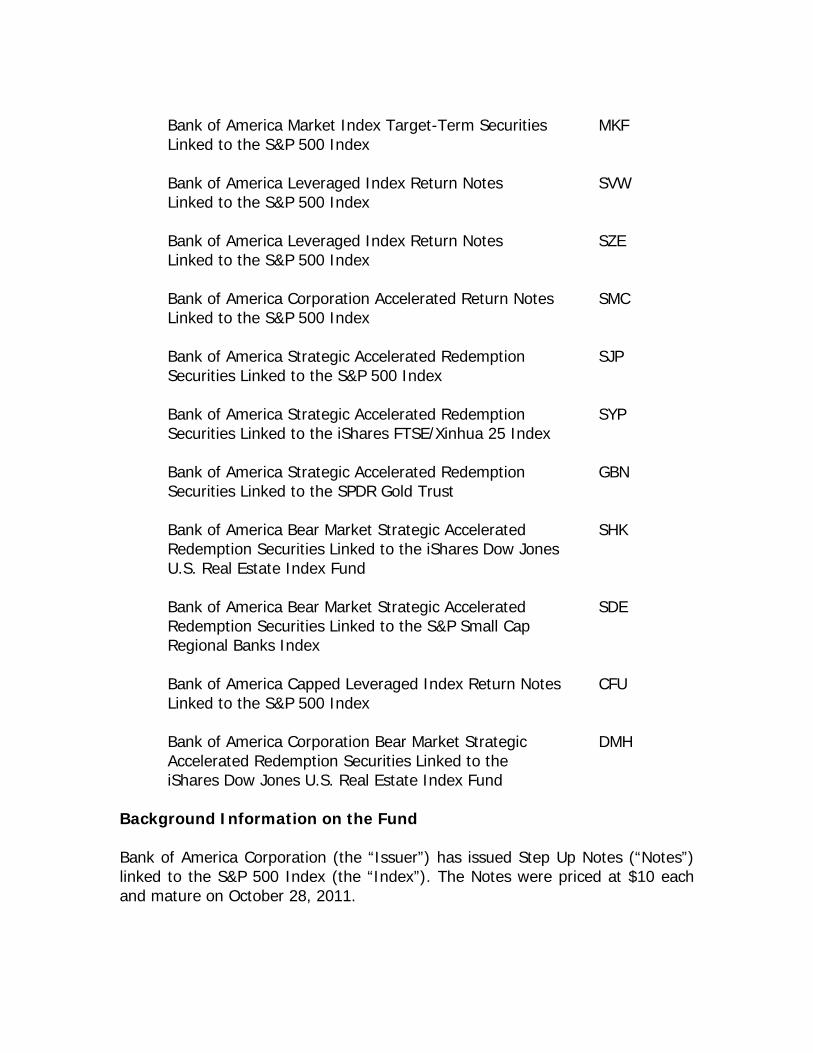

Exchange-Traded Funds Symbol Bank of America Corporation Step Up Notes SKN Linked to the S&P 500 Index Bank of America Corporation Step Up Notes RIH Linked to the Russell 2000 Index Bank of America Market Index Target-Term Securities MLA Linked to the S&P 500 Index Bank of America Corporation Step Up Notes SKL Linked to the S&P 500 Index Bank of America Corporation Accelerated Return Notes SPC Linked to the S&P 500 Index Bank of America Leveraged Index Return Notes SBA Linked to the S&P 500 Index

Bank of America Market Index Target-Term Securities MKF Linked to the S&P 500 Index Bank of America Leveraged Index Return Notes SVW Linked to the S&P 500 Index Bank of America Leveraged Index Return Notes SZE Linked to the S&P 500 Index Bank of America Corporation Accelerated Return Notes SMC Linked to the S&P 500 Index Bank of America Strategic Accelerated Redemption SJP Securities Linked to the S&P 500 Index Bank of America Strategic Accelerated Redemption SYP Securities Linked to the iShares FTSE/Xinhua 25 Index Bank of America Strategic Accelerated Redemption GBN Securities Linked to the SPDR Gold Trust Bank of America Bear Market Strategic Accelerated SHK Redemption Securities Linked to the iShares Dow Jones U.S. Real Estate Index Fund Bank of America Bear Market Strategic Accelerated SDE Redemption Securities Linked to the S&P Small Cap Regional Banks Index Bank of America Capped Leveraged Index Return Notes CFU Linked to the S&P 500 Index Bank of America Corporation Bear Market Strategic DMH Accelerated Redemption Securities Linked to the iShares Dow Jones U.S. Real Estate Index Fund

Background Information on the Fund Bank of America Corporation (the “Issuer”) has issued Step Up Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on October 28, 2011.

The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide investors with the Step Up Payment if the level of the Index is unchanged or increases from the Starting Value to the Ending Value, determined on the calculation day, but does not increase above the Step Up Value. If the level of the Index increases from the Starting Value to an Ending Value that is above the Step Up Value, investors will participate on a 1-for-1 basis in the increase above the Starting Value. Investors should be of the view that the level of the Index will increase over the term of the Notes. Investors must be willing to forgo interest payments on the notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price if the Ending Value is less than the Starting Value. At maturity, investors will receive:

• If the Ending Value is less than the Starting Value:

o $10 - [$10 x ((Threshold Value – Ending Value)/Starting Value)]

• If the Ending Value is greater than the Step Up Value:

o $10 + [$10 x ((Ending Value – Starting Value)/Starting Value)]

• If the Ending Value is greater than or equal to the Starting Value, but less than the Step Up Value:

o $10 + Step Up Value

The Step Up Value is $2.26 per Note (a return of 22.6% over the original offering price). The Starting Value is 1,042.63. The Threshold Value is 1,042.63. The Ending Value will be the closing level of the Index on a calculation day shortly before the maturity date of the notes, as described in the pricing supplement for the Notes. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index.

Bank of America Corporation (the “Issuer”) has issued Step Up Notes (“Notes”) linked to the Russell 2000 Index (the “Index”). The Notes were priced at $10 each and mature on October 28, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide investors with the Step Up Payment if the level of the Index is unchanged or increases from the Starting Value to the Ending Value, determined on the calculation day, but does not increase above the Step Up Value. If the level of the Index increases from the Starting Value to an Ending Value that is above the Step Up Value, investors will participate on a 1-for-1 basis in the increase above the Starting Value. Investors should be of the view that the level of the Index will increase over the term of the Notes. Investors must be willing to forgo interest payments on the notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price if the Ending Value is less than the Starting Value. At maturity, investors will receive:

• If the Ending Value is less than the Starting Value:

o $10 - [$10 x ((Threshold Value – Ending Value)/Starting Value)]

• If the Ending Value is greater than the Step Up Value:

o $10 + [$10 x ((Ending Value – Starting Value)/Starting Value)]

• If the Ending Value is greater than or equal to the Starting Value, but less than the Step Up Value:

o $10 + Step Up Value

The Step Up Value is $2.70 per Note (a return of 27% over the original offering price). The Starting Value is 566.36. The Threshold Value is 719.28. The Ending Value will be the closing level of the Index on a calculation day shortly before the maturity date of the notes, as described in the pricing supplement for the Notes.

Bank of America (the “Issuer”) has issued Market Index Target-Term Securities (“MITTS”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on September 27, 2013. The MITTS are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The MITTS will rank equally with all other unsecured and unsubordinated debt, and any payments due on the MITTS, including any repayment of principal, will be subject to the credit risk of the Issuer. The MITTS provide investors with a 100% participation rate in increases in the level of the Index from the Starting Value of the Index, determined on the pricing date, to the Ending Value of the Index, determined during the Maturity Valuation Period shortly before the maturity date, subject to a maximum return of 46.4% over the Original Offering Price. Investors must be willing to forgo interest payments on the MITTS and be willing to accept a return that is capped. At maturity, investors will receive:

• If the Ending Value of the Index is greater than the Starting Value of the Index:

o $10 + [$10 X ((Ending Value – Starting Value)/Starting Value)]

• Payment will not exceed the Capped Value of $14.64 per MITTS.

• If the Ending Value of the Index is less than the Starting Value of the

Index:

o $10 The Starting Value of the Index is 1060.87. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. Bank of America Corporation (the “Issuer”) has issued Step Up Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on October 4, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and

unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for investors who anticipate that the level of the Index will increase over the term of the notes from the Starting Value to the Ending Value. Investors must be willing to forgo interest payments on the notes and bear the risk of loss of all or substantially all of their investment. At maturity, investors will receive:

• If the Ending Value is less than the Starting Value:

o $10 + [$10 x ((Ending Value – Starting Value)/Starting Value)]

• If the Ending Value is greater than or equal to the Starting Value:

o $10 + [$10 x ((Ending Value – Starting Value)/Starting Value)]

• And

o $10 + Redemption Premium The Redemption Premium is $2.485 per unit of the notes (representing a return of 24.85% above the original offering price). The Starting Value is 1,060.87, determined on September 23, 2009 (the “pricing date”). The Ending Value will be the closing level of the Index on a calculation day shortly before the maturity date of the notes, as described in the pricing supplement for the Notes. Bank of America Corporation (the “Issuer”) has issued Accelerated Return Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on October 29, 2010. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer.

The Notes provide full exposure to any downside movement in the Index and triple exposure to any upside movement in the Index, subject to a capped maximum payment at maturity of $12.472. At maturity, investors will receive:

• If the Ending Value is less than or equal to the Starting Value:

o $10 x (Ending Value/Starting Value)

• If the Ending Value is greater than the Starting Value:

o $10 + [$30 x ((Ending Value – Starting Value)/Starting Value)] Subject to a maximum total payment at maturity of $12.472. The Starting Value for the Index is 1028.12 The Ending Value will be determined near the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on August 2, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount

investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date. If the Notes are called, investors will receive:

• $11.2410 if called on August 2, 2010; • $11.8615 if called on January 25, 2011; or • $12.4820 if called on July 26, 2011.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is less than the Threshold Value of the Index:

o $10 + [$10 X ((Ending Value – Threshold Value)/Starting Value)]

• If the Ending Value of the Index is equal to or greater than the Threshold

Value of the Index:

o $10 The Starting Value of the Index is 975.15. The Threshold Value is 877.64. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Market Index Target-Term Securities (“MITTS”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature in July 2013.

The MITTS are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The MITTS will rank equally with all other unsecured and unsubordinated debt, and any payments due on the MITTS, including any repayment of principal, will be subject to the credit risk of the Issuer. The MITTS provide investors with a 100% participation rate in increases in the level of the Index from the Starting Value of the Index, determined on the pricing date, to the Ending Value of the Index, determined during the Maturity Valuation Period shortly before the maturity date, subject to a maximum return (to be determined on the pricing date) over the Original Offering Price. Investors must be willing to forgo interest payments on the MITTS and be willing to accept a return that is capped. At maturity, investors will receive:

• If the Ending Value of the Index is greater than the Starting Value of the Index:

o $10 + [$10 X ((Ending Value – Starting Value)/Starting Value)]

• Payment will not exceed the Capped Value, which will be determined on

the pricing date.

• If the Ending Value of the Index is less than the Starting Value of the Index:

o $10

The Starting Value of the Index will be determined on the pricing date. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Leveraged Index Return Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on June 29, 2012.

The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide a leveraged return for investors if the level of the Index (the “Index”) increases from the Starting Value of the Index, determined on the pricing date, to the Ending Value of the Index, determined during the Maturity Valuation Period. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that is less, and potentially significantly less, than the original offering price of the Notes. At maturity, investors will receive:

• If the Ending Value of the Index is greater than the Starting Value of the Index:

o $10 + [$10 X 134.2% X ((Ending Value – Starting Value)/Starting

Value)]

• If the Ending Value of the Index is less than the Starting Value of the Index, but greater than the Threshold Value (810.85):

o $10

• If the Ending Value of the Index is less than the Threshold Value:

o $10 - [$10 X 100% X ((Threshold Value – Ending Value)/Starting

Value)] The Starting Value of the Index is 900.94. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer.

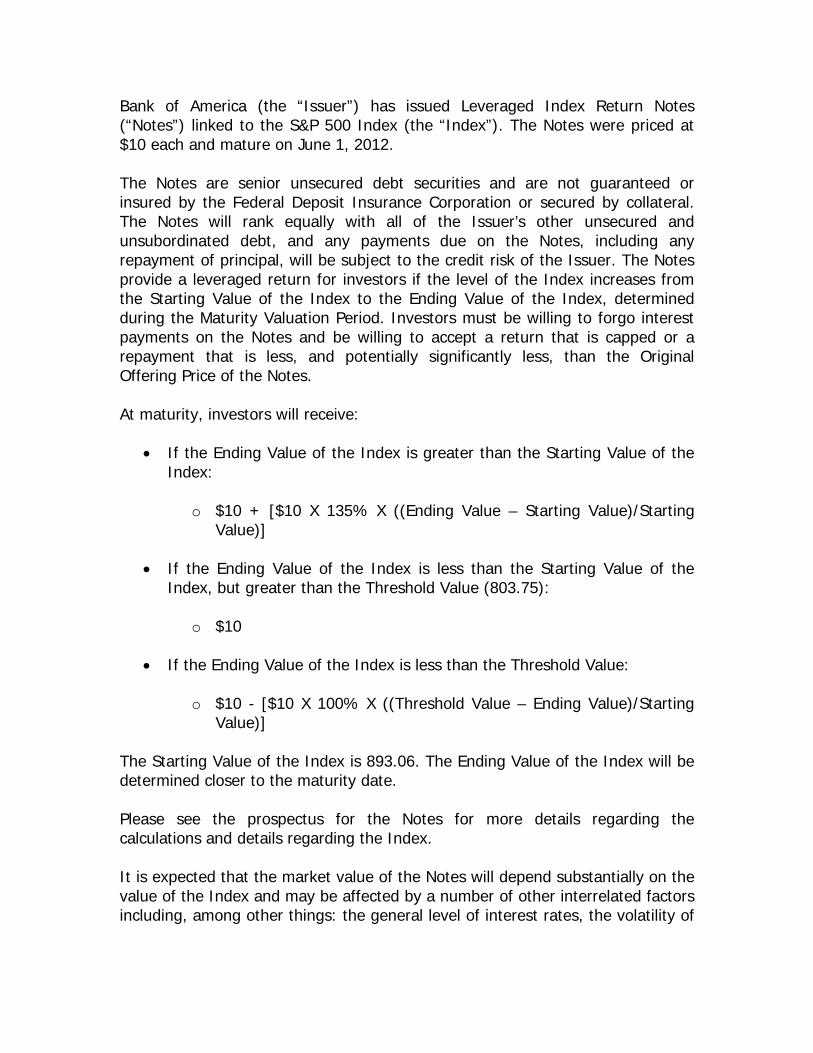

Bank of America (the “Issuer”) has issued Leveraged Index Return Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on June 1, 2012. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide a leveraged return for investors if the level of the Index increases from the Starting Value of the Index to the Ending Value of the Index, determined during the Maturity Valuation Period. Investors must be willing to forgo interest payments on the Notes and be willing to accept a return that is capped or a repayment that is less, and potentially significantly less, than the Original Offering Price of the Notes. At maturity, investors will receive:

• If the Ending Value of the Index is greater than the Starting Value of the Index:

o $10 + [$10 X 135% X ((Ending Value – Starting Value)/Starting

Value)]

• If the Ending Value of the Index is less than the Starting Value of the Index, but greater than the Threshold Value (803.75):

o $10

• If the Ending Value of the Index is less than the Threshold Value:

o $10 - [$10 X 100% X ((Threshold Value – Ending Value)/Starting

Value)] The Starting Value of the Index is 893.06. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of

the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America Corporation (the “Issuer”) has issued Accelerated Return Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on July 30, 2010. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide full exposure to any downside movement in the Index and triple exposure to any upside movement in the Index, subject to a capped maximum payment at maturity of $11.74. At maturity, investors will receive:

• If the Ending Value is less than or equal to the Starting Value:

o $10 x (Ending Value/Starting Value)

• If the Ending Value is greater than the Starting Value:

o $10 + [$30 x ((Ending Value – Starting Value)/Starting Value)]

• Subject to a maximum total payment at maturity of $11.74. The Starting Value for the Index will be the lesser of (a) 893.06, the closing level of the Index on the pricing date, and (b) the lowest closing level of the Index on any Market Measure Business Day during the Starting Value Determination Period (as defined below) on which a Market Disruption Event has not occurred. The actual Starting Value will be determined after the expiration of the Starting Value Determination Period and will be provided or otherwise made available to the investors in the Notes after the Starting Value has been determined. The Starting Value Determination Period is the period from and including May 28, 2009 to and including June 26, 2009 (or if that day is not a Market Measure Business Day, the following Market Measure Business Day). The Ending Value will be determined near the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index.

It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on June 1, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date. If the Notes are called, investors will receive:

• $11.40 if called on June 1, 2010; • $12.10 if called on November 23, 2010; or • $12.80 if called on May 24, 2011.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is less than the Threshold Value of the Index:

o $10 + [$10 X ((Ending Value – Threshold Value)/Starting Value)]

• If the Ending Value of the Index is equal to or greater than the Threshold

Value of the Index:

o $10 The Starting Value of the Index is 893.06. The Threshold Value is 803.75. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the iShares FTSE/Xinhua 25 Index (the “Index”). The Notes were priced at $10 each and mature on June 1, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date.

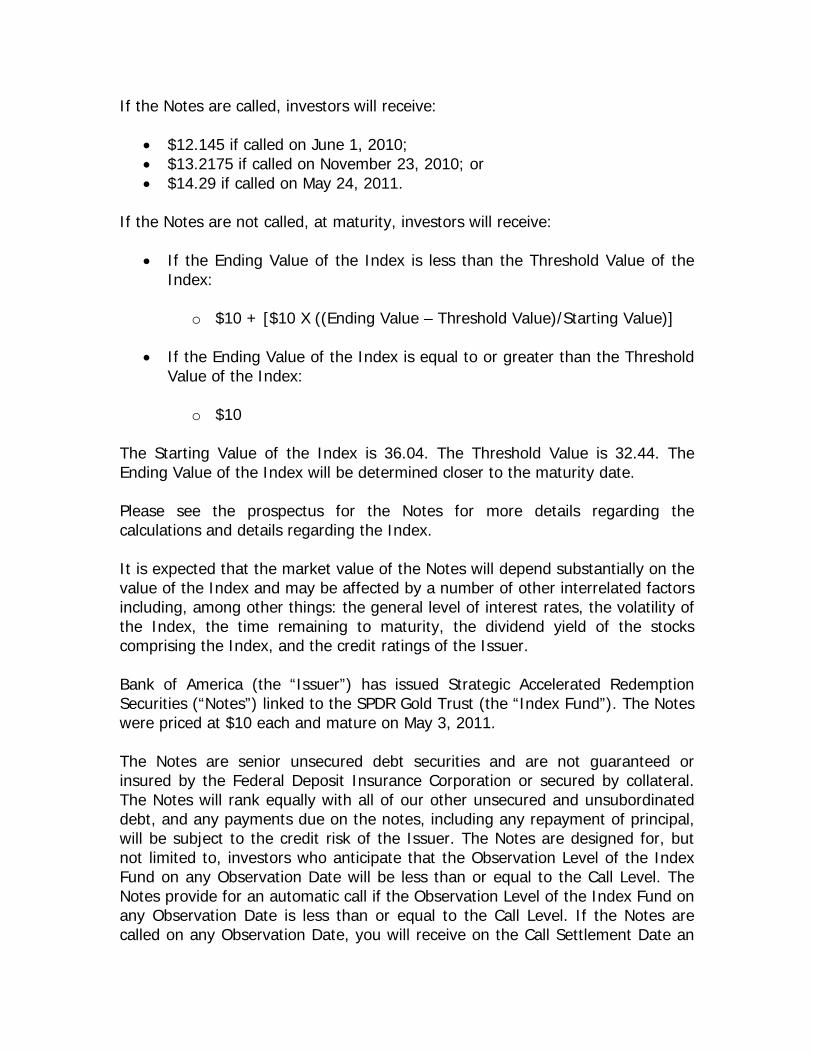

If the Notes are called, investors will receive:

• $12.145 if called on June 1, 2010; • $13.2175 if called on November 23, 2010; or • $14.29 if called on May 24, 2011.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is less than the Threshold Value of the Index:

o $10 + [$10 X ((Ending Value – Threshold Value)/Starting Value)]

• If the Ending Value of the Index is equal to or greater than the Threshold

Value of the Index:

o $10 The Starting Value of the Index is 36.04. The Threshold Value is 32.44. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the SPDR Gold Trust (the “Index Fund”). The Notes were priced at $10 each and mature on May 3, 2011. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index Fund on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index Fund on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an

amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index Fund from the Starting Value, as determined on the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date. If the Notes are called, investors will receive:

• $11.421 if called on April 26, 2010; • $12.1315 if called on October 26, 2010; or • $12.842 if called on April 26, 2011.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is less than the Threshold Value of the Index:

o $10 + [$10 X ((Ending Value – Threshold Value)/Starting Value)]

• If the Ending Value of the Index is equal to or greater than the Threshold

Value of the Index:

o $10 The Starting Value of the Index is 88.80. The Threshold Value is 79.92. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index Fund and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index Fund, the time remaining to maturity, the dividend yield of the stocks comprising the Index Fund, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the iShares Dow Jones U.S. Real Estate Index Fund

(the “Index”). The Notes were priced at $10 each and mature on September 30, 2010. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on March 26, 2009, the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date. If the Notes are called, investors will receive:

• $10.805 if called on September 23, 2009; • $11.610 if called on March 31, 2010; or • $12.415 if called on September 23, 2010.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is greater than the Threshold Value of the Index:

o $10 + [$10 X ((Threshold Value – Ending Value)/Starting Value)]

• If the Ending Value of the Index is less than the Threshold Value of the

Index:

o $10

The Starting Value of the Index is 25.93. The Threshold Value is 28.52. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Strategic Accelerated Redemption Securities (“Notes”) linked to the S&P Small Cap Regional Banks Index (the “Index”). The Notes were priced at $10 each and mature on August 31, 2010. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes are designed for, but not limited to, investors who anticipate that the Observation Level of the Index on any Observation Date will be less than or equal to the Call Level. The Notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the Notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the Notes are not called, the amount investors will receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on February 26, 2009, the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the Notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the Notes. Investors also must be prepared to have their Notes called by the Issuer on any Observation Date. If the Notes are called, investors will receive:

• $10.85 if called on August 25, 2009; • $11.70 if called on March 1, 2010; or • $12.55 if called on August 24, 2010.

If the Notes are not called, at maturity, investors will receive:

• If the Ending Value of the Index is greater than the Threshold Value of the Index:

o $10 + [$10 X ((Threshold Value – Ending Value)/Starting Value)]

• If the Ending Value of the Index is less than the Threshold Value of the

Index:

o $10 The Starting Value of the Index is 47.06. The Threshold Value is 51.77. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America (the “Issuer”) has issued Capped Leveraged Index Return Notes (“Notes”) linked to the S&P 500 Index (the “Index”). The Notes were priced at $10 each and mature on August 27, 2010. The Notes are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the Notes, including any repayment of principal, will be subject to the credit risk of the Issuer. The Notes provide a leveraged return for investors, subject to a cap, if the level of the Index increases moderately from the Starting Value of the Index, determined on February 26, 2009, the pricing date, to the Ending Value of the Index, determined during the Maturity Valuation Period. Investors must be willing to forgo interest payments on the Notes and be willing to accept a return that is capped or a repayment that is less, and potentially significantly less, than the Original Offering Price of the Notes. At maturity, investors will receive:

• If the Ending Value of the Index is greater than the Starting Value of the Index:

o $10 + [$10 X 200% X ((Ending Value – Starting Value)/Starting

Value)] Payment will not exceed the Capped Value of $13.312.

• If the Ending Value of the Index is less than the Starting Value of the Index, but greater than the Threshold Value (677.55):

o $10

• If the Ending Value of the Index is less than the Threshold Value:

o $10 - [$10 X 100% X ((Threshold Value – Ending Value)/Starting

Value)] The Starting Value of the Index is 752.83. The Ending Value of the Index will be determined closer to the maturity date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer. Bank of America Corporation (the “Issuer”) has issued Bear Market Strategic Accelerated Redemption Securities (“STARS”) linked to the iShares Dow Jones U.S. Real Estate Index Fund (the “Index”). The Notes were priced at $10 each and mature on August 30, 2010. The STARS are senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation (“FDIC”) or secured by collateral. The STARS will rank equally with all of the Issuer’s other unsecured and unsubordinated debt, and any payments due on the STARS, including any repayment of principal, will be subject to the credit risk of the Issuer. The STARS provide for an automatic call if the Observation Level of the Index on any Observation Date is equal to or less than the Call Level. If the STARS are called on any Observation Date, investors will receive on the Call Settlement

Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If the STARS are not called, the amount investors receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage change in the value of the Index from the Starting Value, as determined on January 29, 2009, the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the STARS and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the notes. Investors also must be prepared to have the STARS called by the Issuer on any Observation Date. The call amounts and Observation Dates: 1) $10.945 if called on July 27, 2009; 2) $11.890 if called on February 1, 2010; or 3) $12.835 if called on July 27, 2010. If held to maturity, investors will receive:

• If the Ending Value of the Index is equal to or less than the Threshold Value:

o $10

• If the Ending Value of the Index is greater than the Threshold Value:

o $10 + [$10 x ((Ending Value – Threshold Value)/Starting Value)]

The Starting Value for the Index is 33.40. The Threshold Value is 36.74. The Ending Value will be determined on the final Observation Date. Please see the prospectus for the Notes for more details regarding the calculations and details regarding the Index. It is expected that the market value of the Notes will depend substantially on the value of the Index and may be affected by a number of other interrelated factors including, among other things: the general level of interest rates, the volatility of the Index, the time remaining to maturity, the dividend yield of the stocks comprising the Index, and the credit ratings of the Issuer.

Dissemination of Fund Data The Consolidated Tape Association will disseminate real time trade and quote information for the Funds to Tape B. Exchange Rules Applicable to Trading the Shares The Shares are considered equity securities, thus rendering trading in the Shares subject to the Exchange’s existing rules governing the trading of equity securities. Trading Hours The values of any security underlying the Shares are disseminated to data vendors every 15 seconds. The Shares will trade on the CBSX from 8:00 a.m. CT until 3:00 p.m. CT. The trading increment for the Fund’s Shares will be $0.01. Extended Hours Trading Members are reminded that trading in the Fund’s Shares prior to 8:30 a.m. may result in additional trading risks which include: (1) that the current underlying index value may not be updated, (2) the intraday indicative value may not be updated, (3) lower liquidity may impact pricing, (4) higher volatility may impact pricing, (5) wider spreads may occur, and (6), since the intraday indicative value is not calculated or widely disseminated, an investor who is unable calculate an implied value for an ETF in those sessions may be at a disadvantage to market professionals. Trading Halts The Exchange will halt trading in the Shares based on Rule 52.3 and/or because dissemination of the intraday indicative value of the Shares and/or the underlying value of the index has ceased. Suitability Members are reminded of their obligation under Rule 53.6 whereby the Member shall use due diligence to learn the essential facts relative to every customer prior to trading the Shares or recommending a transaction in the Shares that an investment I the Shares is suitable for the customer. Members should adopt appropriate procedures for the opening and maintaining of accounts, including the maintaining of records prescribed by any applicable regulatory organization and by the rules and regulations of the Commission.

Delivery of a Prospectus Consistent with the requirements of the Securities Act and the rules thereunder, investors purchasing Shares in the initial public offering and anyone purchasing Shares directly from a Fund (by delivery of the designated securities) must receive a Prospectus. In addition, Members are required to deliver a Prospectus to all purchasers of newly-issued Shares (i.e. during the initial public offering). Members purchasing shares from a Fund for resale to investors will deliver a Prospectus to such investors. Prospectuses may be obtained through the Fund’s website. The Prospectus does not contain all of the information set forth in the Registration Statement (including the exhibits to the Registration Statement), parts of which have been omitted in accordance with the rules and regulations of the Commission. For further information about a Fund, please refer to the Registration Statement. In the event that a Fund relies upon an order by the Commission exempting the Shares from certain Prospectus delivery requirements under Section 24(d) of the 1940 Act and makes available a written product description, the Exchange requires that Members provide to all purchasers of Shares a written description of the terms and characteristics of such securities, in a form prepared by the Trust, no later than the time a confirmation of the first transaction in the Shares, is delivered to such purchaser. In addition, ETP Holders shall include such a written description with any sales material relating to the Shares that is provided to customers or the public. Any other written materials provided by a Member to customers or the public making specific reference to the Shares as an investment vehicle must include a statement in substantially the following form: “A circular describing the terms and characteristics of Shares of the Fund has been prepared by the Trust and is available from your broker. It is recommended that you obtain and review such circular before purchasing Shares of the Fund. In addition, upon request you may obtain from your broker a prospectus for Shares of the Fund.” An Member carrying an omnibus account for a non-Member is required to inform such non-Member that execution of an order to purchase Shares for such omnibus account will be deemed to constitute agreement by the non-Member to make such written description available to its customers on the same terms as are directly applicable to Members under this rule. Upon request of a customer, Members shall also provide a copy of the Prospectus.

This Information Bulletin is not a statutory Prospectus. Members should consult the Trust’s Registration Statement, SAI, Prospectus and the Fund’s website for relevant information. Inquiries regarding this Information Bulletin should be directed to David Reed, 866.458.2279. CBOE Stock Exchange® and CBSX® are registered trademarks of CBOE Stock Exchange, LLC. CBOE® and Chicago Board Options Exchange® are registered trademarks of Chicago Board Options Exchange, Incorporated.