Embed Size (px)

DESCRIPTION

CFA 1 Crash Course Corporate Finance

Citation preview

www.edupristine.com

Crash Course for

Corporate Finance

CFA Level-I Exam

www.edupristine.com © Neev Knowledge Management – Pristine

• Corporate Finance

www.edupristine.com © Neev Knowledge Management – Pristine

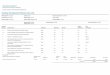

10 yrs AAA rated bond 8.5% Expected market return 20%

Beta of market 1.0 Debt/equity ratio 0.8

1 yr market returns 12% Credit spread (BB bond) 2.17%

Credit rating of XYZ BB 10 yrs Govt. Bond 7.33%

Beta of a stock XYZ 1.2 Tax rate 40%

Expected dividend $ 5 Dividends growth 10%

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

WACC=(wd)*kd*(1-t)

+ wpskps+ weke

Cost of Equity using

CAPM:

ke=Rf+ β*(Rmkt- Rf)

Q. Tax rate 35%, before

tax cost of debt:6.5%,

Capital Structure is 50:50

Cost of equity: 10.55%

Ans.WACC=(0.5)*6.5%*(

1-0.35) + 0.5*10.55

WACC = 7.4%

Working

Capital

Mgmt

Q. Calculate the weighted average cost of capital using above information?

a) 15% b) 17.5% c) 20%

Ans. 15%

Q. Which of the following will be a fair market price of stock according to

Gordon’s formula?

a) $ 25 b) $ 40 c) $ 30

Ans. $40

Q. Which of the following is most likely to be true, if there

are no outstanding convertible securities?

• EPS <= Diluted EPS

• EPS => Diluted EPS

• EPS=Diluted EPS

Ans. EPS=Diluted EPS

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

kP=DPS/P

Q. Preference dividend = $2,

Price of preference share = $20

Ans. Kp= 2/20 = 10%

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

Ke= (D1/P0) + g or

Ke= Rf + β*(Rmkt - Rf + CRP)

Country risk premium (CRP) =

sovereign yield spread *

(σ of developing country equity

index / σ of developed country

sovereign bond)

βlevered= βunlevered*(1+debt/equity)

Q. Stock is quoting at $ 20, expected

dividend is $ 2, Growth rate = 5%

Ans. cost of equity= 2/20+5%=15%

Q. A company has been paying a dividend of $ 15 for each stock held.

What shall be the stock price of the company if this dividend is expected to

be received till infinity and expected rate of return by the investor is 10%?

a) $ 15 b) $ 150 c) $ 100

Ans. P0 = 15 / 10% = $150

Q. If the difference between the

yields of Govt. of India bonds

denominated in Rupee and the

treasury bonds of USA having

same maturity, increases. What

will be the effect on the cost of

equity of a firm in India?

Ans. Increases

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

NPV & IRR Profitability index

NPV =CF0+ [CF1/

(1+k)]+[CF2/(1+k)2]+

….+[CFn/ /(1+k)n]

IRR: discount rate

that makes NPV

equal to 0.

PI = 1 + NPV/CF0

If PI > 0, accept project

If PI < 0, reject project

Avg accounting rate of

return (AAR)

AAR= avg NI / avg BV

Payback period

Payback period is no. of

years it takes to recover

initial project cost

Discount payback uses

present values of cash

flows

Treatment of Floatation Costs:

• Increase in Initial Cost of Project

(Preferred)

• Incorporate Floatation Costs in

discount rate (not preferred)

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

Receivables

Turnover =

Credit Sales /

Average

Receivables

Inventory

Turnover =

COGS /

Average

Inventory

Payables

Turnover =

Purchases /

Average Trade

Payables

Cash Management

Bond Equivalent Yield

= [(face value –

price)/ price] *

(365/days to maturity)

Money Market Yield

= [(face value –

price)/ price] *

(360/day to maturity)

% Discount =

(face value –

price) / face

value

Q. Which of the following ratios

cannot be directly observed in the

common size statements?

• Inventory turnover

• Profit Margin

• Debt /Asset Ratio

Ans. Inventory turnover ratio Q. Which of the following is least likely

to be bond with modifying maturity?

• Callable bonds

• Putable bonds

• Treasury bonds

Ans. Treasury bonds

Q. A bond matures in one year and pays interest at

maturity. If the face value of the bond and coupon rate is

$500,000 & 9% respectively, and the required rate of

return is 8%, what should be the present value?

• >$500,000

• <$500,000

• $500,000

Ans. >$500,000

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

2010 2011 2012

Operating Margin 78% 78% 78%

Effects of nonoperating

items

0.80 0.77 0.72

Tax Effect 0.65 0.65 0.65

Total asset turnover ratio 0.20 0.19 0.18

Financial leverage 2.50 2.86 3.37

ROE 20% 21% 22%

ROE= [O/P Income/Revenue] * [PBT/ (O/p Income)] *

[PAT/PBT] * [Revenue / avg. total assets] * [avg. total assets/ avg. equity]

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

1. Estimate the relations b/w changes in sales and changes in

income statement & balance sheet items

2. Estimate future tax rate, interest rates on debt, lease payments

etc.

3. Forecast sales

4. Estimate fixed operating and financial costs

5. Integrate these estimates into pro forma financial statements

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

Favor Shareholder

Interests

Harm Shareholder

Interests

• Independent board.

• Strong code of ethics

• Confidential voting

• Management-

aligned board

• Voting restrictions

• Takeover defenses

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

Leverage is present

because of:

• Fixed Operating Costs

• Use of Debt in capital

structure z

Degree of Operating Leverage

Degree of Financial Leverage

Degree of Total Leverage = DOL

*DFL

FVPQ

VPQDOL

)(

)(

CFVPQ

FVPQDFL

)(

)(

Breakeven: When Profit = 0 and

Revenue = Costs

Breakeven Points

Operating Break Even:

VP

CFQBE

VP

FQOBE

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com © Neev Knowledge Management – Pristine

Regular Cash

Dividends

Dividend

Reinvestment Plan

(DRP)

No floatation costs

Special Dividends

Used especially by

cyclical companies

in periods of strong

earnings

Liquidating

Dividends

Company goes

out of business

Stock

Splits

Reverse

Stock

Splits

Share

Repurchases

• Earning yield > Cost of debt

then EPS increases

• Earning yield < Cost of Debt

then EPS is reduced

• If market price > BVPS then

book value per share reduces

after repurchase

• If market price < BVPS then

book value per share

increases after repurchase

For equal taxation and

information content

cash dividends = share

repurchases

• EPS and other per market

data decline by half

• P/E, Dividend Yield are

same

• Wealth remains same

Corporate Finance

Weighted

Average Cost

of Capital

Cost of

Equity

Capital

Extended

DuPont

Expression

Corporate

Governance

Cost of

Preference

Stock

Capital

Budgeting

Pro Forma

Financial

Statements

Working

Capital

Mgmt

Measure of

Leverage

Dividend

and Share

Repurchases

www.edupristine.com

Question 1

Sigma Corporation is planning to launch a new product in the market for which it has

paid Xylus Consultants a fee of $4000 to do a market survey to gauge the demand for

the product. The new product is expected to cause a 5% decline in the market share of

its existing brands. Also the facilities for the manufacturing of the project could earn a

lease rent of $1500 per month, if the project were not to be undertaken. Which of the

following regarding the project cash flow is least likely true?

A. The cash flows should not take into account the consultants fee

B. The loss in lease rent is relevant to the decision making

C. The loss of sale of existing product is irrelevant to the decision making

www.edupristine.com

Answer 1

C.

The cost of cannibalisation should be considered in the incremental cash flows

www.edupristine.com

Question 2

Company A's stock is selling for $120 and the expected return on equity is 10%.

Dividend planned for next year is $6 and the company plans to pay out 30% of its

earnings. What is the cost of retained earnings for Company A using the discounted

cash flow approach?

A. 12.5%

B. 15%

C. 10%

www.edupristine.com

Answer 2

A.

Kre = D1/P0 + g where g = (1-payout ratio) x ROE, P0 = Current price and D1 =

Dividend expected. Hence, Kre = 6/120 + (1-0.3) x 0.1 = 0.125 i.e. 12.5%

www.edupristine.com

Question 3

A company is considering a project with future cash flows:

Year Cash flow

0 -1500

1 450

2 400

3 513

4 580

The firm plans to invest in another project after its maximum payback period of 3 years.

The WACC of the firm is 10%. Which of the following is least likely the company’s

decision regarding the two projects?

A. The first project is least likely to be profitable within the maximum payback period

B. The first project should not have been accepted by the company in the first place

C. The firm’s major concern is profitability and not liquidity as evident from the capital

budgeting methods followed by it

www.edupristine.com

Answer 3

C.

The maximum payback period method followed reflects that the firm is more concerned

about the liquidity from the project as the payback period method is not appropriate to

calculate the profitability of the project.

www.edupristine.com

Question 4

Rio Inc has invested $650 million in a real estate project. The present value of the after

tax future cash flows from the project is $900 million, as estimated by the company. If

Rio at present has 100 million shares outstanding trading at $50 per share, what

should an analyst analysing Rio recommend to his clients about this company after

receiving and analysing this information?

A. Buy as the stock price is expected to rise to $52.5

B. Cannot be said with certainty

C. Buy as the stock price is expected to rise to $59

www.edupristine.com

Answer 4

B.

The analyst may expect a lower level of profitability than that estimated by the

company

www.edupristine.com

Question 5

A firm has a target equity share capital of $400 million and debt of $100 million. It

raises another $120 million from the market through a rights issue. If the cost of equity

is 13% and the after tax cost of debt is 8%, what is most likely the WACC of the firm

after the additional fund raised?

A. 12%

B. 12.19%

C. 11.27%

www.edupristine.com

Answer 5

A.

The WACC is calculated based on the target capital structure of the firm which is

80:20. Hence, WACC is 0.8*0.13+0.2*0.08= 0.12

www.edupristine.com

Question 6

Plasma Inc is considering the purchase of an automatic capping machine to reduce

labor costs. The machine is projected to save Plasma $5,000 per year. The machine

costs $40,000 and is expected to last for 15 years. Plasma has estimated that their

cost of capital for such an investment is 10%. For an extra $750 per year, Plasma can

get a “Good As New” service contract. The contract keeps the machine in new

condition forever. Net of the cost of the service contract, the machine would produce

cash flows of $4250 per year in perpetuity. Which of the following decisions is the most

appropriate?

A. Plasma should not avail of the service contract

B. Plasma’s profitability would increase if it accepts the service contract

C. Plasma should not accept the entire project in the first place

www.edupristine.com

Answer 6

B.

The NPV for purchase of machine only is negative (-$1970), however with the service

contract the NPV is positive $2500 and the IRR is more than the WACC of the firm

(10.81%).

www.edupristine.com

Question 7

What is a firm's weighted-average cost of capital if the stock has a beta of 1.45,

Treasury bills yield 5%, and the market portfolio offers an expected return of 14%? In

addition to equity, the firm finances 30% of its assets with debt that has a yield to

maturity of 9%. The firm is in the 35% marginal tax bracket.

A. 14.39%

B. 12.66%

C. 15.21%

www.edupristine.com

Answer 7

A.

Cost of equity = 5+1.45(14-5) = 18.05%

After tax Cost of debt = 9(1-0.35)=5.85%

WACC = 0.3*0.0585+0.7*0.18= 14.39%

www.edupristine.com

Question 8

The opportunity cost of capital is 8%. Your firm is evaluating two mutually exclusive

projects with scale differences. Each project requires an initial investment at time zero

and produces one cash inflow at the end of the tenth year. Project A (the smaller

project, requiring an initial investment of $10,000) has an internal rate of return of 9%.

Project B (the larger project, requiring an initial investment of $12,000) has an internal

rate of return of 10%. Which of the two projects has the higher NPV?

A. Project A has the higher NPV.

B. Project B has the higher NPV

C. Both projects have the same NPV.

www.edupristine.com

Answer 8

B.

Since the IRR of project B is higher than project A , the NPV of project B will also be

higher.

www.edupristine.com

Question 9

Chempro has planned to purchase a machine to add to the current production

capacities to meet the growing demand of its products in the market. The following

are the additional information provided in addition to the table below:

All sales are on cash basis

Interest on capital is 10%

Corporate income tax is 40%

Machine life is 2 years

What is the net cash flow from the project?

A. $123000

B. $24000

C. $88000

Sr No Description Amount ($)

1 Initial Investment 150,000

2 Estimated Sales 250,000

3 Cost of goods sold 75,000

4 Administration, selling and Distribution expenses

20,000

www.edupristine.com

Answer 9

A.

Initial investment 150000

Estimated sales (Annual) 250000

Cost of goods sold 75000

Admin, Selling and Distribution expenses 20000

Depreciation (2 years life) 75000

Interest on capital (10% of investment) 15000

PBT 65000

Less : Tax at 40% PBT 16000

Profit After Tax 39000

Add: Depreciation 75000

Net Cash Flow 114000

www.edupristine.com

Question 10

In a mutually exclusive project, the IRR of project A is 20% while NPV at 10% cost of

capital is $4000. The IRR of project B is 18% while NPV at 10% cost of capital is

$6000, the preferred capital budgeting method to be chosen is

A. IRR

B. NPV

C. Discounted Payback

www.edupristine.com

Answer 10

B.

NPV is the preferred method in capital budgeting . Only if NPV is the same then IRR is

compared.

www.edupristine.com

Question 11

In Drag on liquidity pressures from credit management deteriorates because:

A. Payments are made before due dates to vendors, employees and contractors.

B. Banks which trades with the company reduces the line of credit.

C. Uncollected receivables are longer and many may not be collected along with

increasing bad debt expenses.

www.edupristine.com

Answer 11

C.

Drag on liquidity is delay or reduction in cash inflow.

Hence only option “Uncollected receivables are longer and many may not be collected

along with increasing bad debt expenses” causes drag on liquidity.

www.edupristine.com

Question 12

Silverton Inc is considering a project in the garment manufacturing industry. It has a

D/E ratio of 1.2 and its debt currently has a after tax return of 6%.Ashley Inc is a

publicly traded company which is only in the garment manufacturing business with a

D/E ratio of 2 and equity beta of 1.1. If the risk free rate is 5% and return on market is

10%, find the appropriate WACC to be used to evaluate Silverton’s project. Assume tax

rate of 40%

A. 8.6%

B. 7.5%

C. 10.3%

www.edupristine.com

Answer 12

B.

Ashley’s unlevered/asset beta = 1.1*[1/{1+(1-0.4)*2}] = 0.5. Silverton’s project beta =

0.5*[1+(1-0.40)*1.2]= 0.86

Silverton’s cost of equity using CAPM = 0.05+0.86(0.1-0.05) =9.3%

WACC = (1.2/2.2)*0.06+(1/2.2)*0.093 = 0.075

www.edupristine.com

Question 13

Zeta Technologies is planning to expand into China. The following information is

available:

Chinese US dollar denominated 10 year Govt bond yield= 8.9%

10 Year US treasury bond yield = 4.8%

Annualised standard deviation of Chinese stock Index= 23%

Annualised std dev of Chinese US dollar denominated 10 year govt bond = 14%

Find the country risk premium of China.

A. 8.93%

B. 5.54%

C. 6.73%

www.edupristine.com

Answer 13

C.

Country risk premium= (8.9-4.8)*(23/14) =6.73%

www.edupristine.com

Question 14

What happens to a company’s weighted average cost of capital if the firm’s corporate

tax rate increases and if the risk free interest rate decreases, considering the two

events separately?

Tax rate increase / Decrease in risk free rate

A) Decrease / Decrease

B) Increase / Decrease

C) Decrease / Increase

www.edupristine.com

Answer 14

A.

Increase in the tax rate will reduce the cost of debt and decrease in the risk free rate

will decrease the cost of equity

www.edupristine.com

Question 15

Under which of the following circumstances would a company be most likely to avail of

a trade discount?

A. Company with a high payable turnover

B. Availability of low cost funds to finance the working capital requirements

C. Company with a low payable turnover

www.edupristine.com

Answer 15

B.

In such a situation the company would prefer to pay off the payables and use the low

cost funds available to finance its working capital requirements.

www.edupristine.com

Question 16

Which of the following would most likely to be a sign of independence, prudence of the

auditing committee?

A. 2/3 of the audit committee comprises of independent members and committee is

chaired by managing director

B. Same external auditor is advising company management in M&A activities

C. Committee members are financial experts

www.edupristine.com

Answer 16

C.

Auditing committee headed by management director is more likely to create a principal

agent problem and would not be effective in protecting shareholders’ interest

www.edupristine.com

Question 17

The difference between primary and secondary sources of liquidity is

A. Primary source is easily accessible from the market than secondary source of

liquidity.

B. Primary source is likely to affect the normal operations of the company whereas

using the secondary source will not result in company’s financial and operating

position.

C. The normal operations are not affected while using primary source but secondary

source will result in changing the company’s financial and operating position.

www.edupristine.com

Answer 17

C.

Primary source of liquidity are the sources of cash it uses in its normal day to day

operations.

Secondary source of liquidity include liquidating short term or long lived assets etc.

www.edupristine.com

Question 18

American Outlook Inc. is issuing bonds to obtain the funding necessary to acquire a

major competitor. Review of the balance sheets indicates that American Outlook has

also issued preferred and common stock in the past. Which component cost(s) should

American Outlook use in evaluating the financial cost of acquiring the new firm?

A. The weighted average component cost of common stock, preferred stock and debt

B. The price the firm paid for its assets divided by their market value

C. The cost of the new debt issue alone

www.edupristine.com

Answer 18

A.

How a company raises capital and how it invests it are considered independently. In

the short run, a company may highlight the latest capital issued. But in the long run the

firm would look at a targeted capital structure and hence the investment decision

should be made assuming a weighted average cost of capital including each source of

capital.

www.edupristine.com

Question 19

Which of the following is a case where there is a problem in using the IRR?

A. Mutually exclusive projects

B. Cost of capital not available

C. Cut-off rate is high

www.edupristine.com

Answer 19

A.

While NPV and IRR are useful metrics for analyzing mutually exclusive projects - that

is, when the decision must be one project or another - these metrics do not always

point you in the same direction. This is a result of the timing of cash flows for each

project. In addition, conflicting results may simply occur because of the project sizes.

www.edupristine.com

Question 20

Accounting beta is calculated by running a regression using

A. Company's turnover against the operating turnover for market benchmark

B. Company's operating margin against the operating margin for market benchmark

C. Company's return on assets against the return on assets for market benchmark

www.edupristine.com

Answer 20

C.

www.edupristine.com

Question 21

A company XYZ Ltd sells 10,000 units of water bottles at a price of $4 per unit. ABC’s

fixed costs are $10,000 and it pays an annual interest of $ 3,000.The variable cost of

production is $ 2 per unit and the operating profit (EBIT) is $ 14,000. Which of the

following statements is true?

A. Degree of Operating leverage = 2.00 , Degree of Financial leverage = 1.27

B. Degree of Operating leverage = 1.27 , Degree of Financial leverage = 2.00

C. Degree of Operating leverage = 1.27 , Degree of Financial leverage = 1.50

www.edupristine.com

Answer 21

A.

Degree of operating leverage = Q*(P-V)/ (Q*(P-V)-F)

Where Q = number of units sold = 10,000

P = Cost price per unit =$4

V = Variable cost per unit = $2

F = Fixed cost = $10,000

Hence DOL = 10,000*($4-$2)/ (10,000*($4-$2) -$10,000) = 2.00

Degree of Financial leverage = EBIT/ (EBIT – Interest) = $14,000/ ($14,000-$3,000)

= 1.27

www.edupristine.com

Question 22

25% increase in sales of Irrelevant Corporation causes 50% growth in EPS If operating

earnings of the company is $ 12,000 and financial leverage is 1.5. Calculate operating

earnings of the company if sales increase by 10% next year

A. 15000

B. 14000

C. 13000

www.edupristine.com

Answer 22

B.

Total leverage = EPS growth/sales growth

Operating leverage (OL) = total leverage/financial leverage

New operating income = old income *(1+ OL * sales growth)