Embed Size (px)

Citation preview

CCERTIFIED

FFINANCIAL

CCOUNSELOR

Georgia Chapter

FFFIIISSSCCCAAALLLLLLYYY FFFIIITTT

Training and Reference Manual 2011-2012

CPAR / CFC 2011-2012 Committee

“FISCALLY FIT”

FACILITATOR Carmen Sessoms, FHFMA

Firstsource

BOARD MEMBER Gail Scarboro-Hritz, CHFP

Navigant Consulting - Healthcare Practice

CPAR/CFC CHAIRPERSON Ricky Wainscott

Gwinnett Hospital System

CPAR/CFC CO-CHAIR Linda Johnson

RelayHealth

CPAR/CFC COMMITTEE James Barwick

Gwinnett Hospital System

Bonnie Breland Phoebe Putney Memorial Hospital

Amon Buchanan Gwinnett Hospital System

Maria Cancela Chamberlin Edmonds

Cathy Dougherty, FHFMA

Gwinnett Hospital System

Janet Jester

The Medical Center of Central Georgia

Elizabeth Richards, FHFMA

Clinton A. Harkins, P.C. Attorney At Law

Brenda Stodghill, FHFMA

Tift Regional

Debbie Young

FirstSource

As this was the first year to

merge the CPAR and CFC

Committees, this dedicated

team of individuals have

exceeded all expectations to

provide you with the utmost

quality and level of expertise

in the pages of this manual.

A special thank you is

extended to Amon

Buchanan for her energy

and commitment as she so

graciously accepted the

technical challenge to

reformat the CPAR manual

and incorporate those items

identified as updates to the

content of both the

CPAR/CFC manuals.

ACKNOWLEDGEMENTS

The Georgia Chapter of HFMA & the CPAR/CFC Committee would like to extend its sincere

appreciation to the following individuals and organizations that volunteered in the production of

the 2011-2012 CPAR/CFC Training and Reference Manuals:

Chamberlin Edmonds

Linda Benefield

Firstsource

Mary Acosta

Gwinnett Hospital System

Carol Fowler

Susie Kelso

Jamie Lloyd

Carolyn Regen

Melissa Smith

RelayHealth

RoxAnne Anderson

Nicole Harris

Nicole Smith

Tift Regional

Sherry Robinson

Carole Walker

CERTIFIED FINANCIAL COUNSELOR

TABLE OF CONTENTS

INTRODUCTION Chapter 1 - ACCESSING A HOSPITAL Chapter 2 – COLLECTING FROM THE PATIENT OR GUARANTOR Chapter 3 – UNDERSTANDING COLLECTION LAW

The Fair Debt Collection Practices Act The Fair Credit Reporting Act

Chapter 4 – HOW TO COLLECT Chapter 5 – FINANCIAL ASSISTANCE PROGRAMS Chapter 6 – PAYMENT PLANS Chapter 7 – DISCOUNTS Chapter 8 – INSURANCE VERIFICATION & PRE-CERTIFICATION Chapter 9 – INSURANCE DENIALS AND APPEALS

Denial Types

Technical vs. Clinical Denials

Other Substantive Denials

Medical Necessity Denials

Hard vs. Soft Denials

Partial Denials The Appeals Process

Initial Steps

Know Your Contacts

Follow-Up

Exhaust All Available Options

CERTIFIED FINANCIAL COUNSELOR

TABLE OF CONTENTS, continued

Chapter 10 – MEDICAID, MEDICARE & WORKERS COMPENSATION Chapter 11 – ALTERNATIVE PAYER SOURCES

Third Party Liability

Cancer State Aid

Vocational Rehabilitation Program

Children’s Medical Services

Veterans Health Administration

Estates

Crime Victims Chapter 12 – LEGAL REMEDIES

Judgment Liens

Garnishments

Hospital Liens

Bankruptcy Chapter 13 – GEORGIA PROMPT PAY LAWS Chapter 14 – HEALTH SAVINGS ACCOUNTS (HSA’s) Chapter 15 - PROHIBITED PRACTICES (Senate Bill 476 Enacted) Sources

INTRODUCTION

The Certified Financial Counselor (CFC) program, organized by the Georgia Healthcare Financial Management Association in 2005, equips healthcare financial professionals with the tools and skills necessary to locate funding, secure payment and funding sources, and determine the best financial solution available for patients with a focus on the underinsured and uninsured. By providing training and access to financial solutions, Certified Financial Counselors promote the utilization of critical thinking skills, a friendly and helpful personality, social worker approach, and the treatment of all patients with dignity and respect.

Certification in Financial Counseling offers benefits such as increased self-esteem, educational advancement and improved job performance.

Congratulations on your commitment to becoming a Certified Financial Counselor.

Chapter 1 - ACCESSING A HOSPITAL

Pre-Registration Patients have their first interaction with hospitals for medical care in many ways:

Scheduling tests or procedures

The Emergency Room for an emergent condition

Their physician‘s office where hospital materials may be provided

Telephone contact from a hospital employee for pre-registration

Materials mailed to a patient for a future visit One of the most valuable access processes is the ―pre-registration program.‖ The objective of a pre-registration program should be to complete all possible processes prior to access (admission) or date of service, preferably by telephone. Mail will work, as well, if the patient is scheduled well in advance. There are a multitude of benefits to pre-registration, both for the patient and the hospital. For Example: 1) Going through the registration steps prior to admitting the patient familiarizes them with the entire access process, hospital regulations and procedures. 2) Pre-registration reduces processing time on the date of access by allowing patients to complete many requirements in advance. For the patient this means less waiting and faster throughput to care. 3) Pre-registration also educates the patient, giving them time to understand insurance/employer requirements and expected benefit levels. 4) Pre-registration allows time for complete and sound financial arrangements to be made, avoiding account issues after the fact. 5) Pre-registration facilitates the flow of information between the physician and the hospital. This timely data exchange can prevent unnecessary work duplication, improve the quality of patient information, and foster a more cooperative relationship between the hospital and the physician. 6) The pre-registration process allows the hospital to proactively plan for the patient visit. Scheduling of procedures and/or tests can also be incorporated at this time. 7) Pre-registration allows/sets the stage for pre-notification – the act of informing the patient of co-payment and deductible responsibility, of where to park, of where to go once in the hospital, of what other issues they may expect on the date of service.

Chapter 1 - ACCESSING A HOSPITAL, continued Pre-Registration, continued All hospitals should create some type of pre-registration form designed to capture all data necessary to assess the patient‘s ability to pay and meet the hospital‘s financial requirements. Financially securing accounts prior to rendering medical services is a proven best practice. For this reason, Financial Counselors should be involved in the pre-registration process as soon as possible. The following information should be the minimum data set of information obtained from the patient: Patient:

Name, address, telephone number and email address

Date of birth

Social security number

Next of kin and personal representative information

Employer information

Guarantor information (if not the patient)

Advance Directive information Guarantor (if different than the patient):

Name, address, telephone number and email address

Date of birth

Social security number

Employer information Insurance:

Name, address and telephone number of insurance company

Name of insured

Relationship of insured to patient (if different than patient)

Policy or contract number

Group number and group name

Retirement date (if applicable)

Claim mailing address

Pre-certification information

Accident type, date and place (if applicable)

Medicare Secondary Payer (MSP) questions (for all Medicare beneficiaries)

Chapter 1 - ACCESSING A HOSPITAL, continued Insurance, continued: Accessing a hospital through the Emergency Department presents many challenges for gathering accurate patient data and financially securing the account. Best practice has shown that a Financial Counseling function in Emergency Departments will produce increased point-of-service collections. Patient Access personnel may be made responsible for collecting money from patients during the discharge process (remember EMTALA prevents asking questions regarding ability to pay until the patients condition has been assessed). A better plan may be for a dedicated Financial Counselor who has more time to review a patient‘s history with the facility, to review online insurance eligibility, and review the charges being incurred to allow a realistic conversation with the patient/guarantor about payment options. The Financial Counselor may also provide a better customer service approach to collecting. Regardless of where the responsibility lies for collection of Emergency Department charges, it is recommended that a program for collection in Emergency settings be established. Once established, it is imperative that the Patient Access management work closely with nursing staff to assure that all (or most) patients are routed by the Financial Counselor or designated collector before leaving the Emergency Department. Finally, be certain to fairly apply any applicable prompt payment or other policy-approved discounts to your self-pay accounts. Pre-Notification

The benefits of pre-notification are only as good as the pre-registration process. The purpose of pre-notification is to alert scheduled patients to a variety of issues they need to be aware of prior to access. For example: 1) The patient‘s insurance may not cover the procedure they are scheduled to undergo. If the benefits are exhausted or the service is not covered, the patient must be made aware of the lack of coverage and that the responsibility for payment is theirs, so they can plan accordingly. 2) Where required, a pre-certification or pre-authorization from the person‘s insurance carrier must be obtained before the date of service. The patient must be made aware of the requirement and their potential liability if not completed. Patients may also be helpful in communicating with their insurance carrier and the ordering physician. 3) The out of pocket portion of the future hospital visit should be communicated to the patient. The patient should be instructed in a very polite tone to be prepared on the date of service/or pre-op date, to pay the out of pocket expenses. If the patient cannot pay all of what is owed, payment arrangements or financial assistance should be offered based on hospital policy. 4) Outstanding balances from prior visits should be resolved with the patient/guarantor. Chapter 1 - ACCESSING A HOSPITAL, continued

Pre-Notification, continued

5) Pre-notification should include instructions to the patient regarding when to arrive, where to go, directions, and personal items which should or should not be brought. If parking is problematic, it is a great time to advise on where to park, and if there is a charge for parking, the patient should be made aware at this time. As you can see, without a thorough pre-registration process, these important issues might not be spotted. It is critical that personnel in pre-registration/pre-notification work to resolve the problems prior to the date of service. Obviously any of the above-mentioned scenarios could negatively impact reimbursement. Using dedicated Financial Counselors in the pre-notification process has proven to be a best practice.

Chapter 2 - COLLECTING FROM THE PATIENT OR GUARANTOR

Point of Service Collections

The best time to collect healthcare self-pay portions from the patient is prior to the patient receiving service, except where EMTALA laws apply. The provider has a psychological advantage when collections are attempted prior to the patient‘s arrival at the medical facility or at point of service. The hospital (or other medical provider) should have methods in place to calculate patient portions of an estimated bill prior to the time of service. For example:

An out of pocket expense amount may be obtained by utilization of one of several automated programs designed to provide benefits verification within seconds – during the registration process

An out of pocket amount may be derived by verifying coverage limits and co-pay requirements telephonically. The telephone, though sometimes slow and tedious, is often the most reliable way to determine the patients out of pocket amount

An estimate of the out of pocket amount may be accomplished by taking an average out of pocket for a particular payer, type of service, etc. If this method is utilized, collect slightly lower than the average, which should help avoid over collecting which necessitates refunds

One may also just choose to come up with a reasonable deposit. The deposit should be more than simply a wild guess; it should be based on current verified data for the procedure.

Note: In each of the estimate, deposit, and even verified scenarios listed above, there should be disclaimers to state, ―This is only an estimate‖. When presenting the estimate to the patient, the Financial Counselor or other staff should offer detailed explanations. The best advice is to:

Reveal the range from which estimates were derived

Clarify that charges could be more or less than the estimated amount

Explain how charges are applied

Explain that final charges are based on actual services provided

Provide a written copy of the estimate, including a disclaimer statement

Be prepared to discuss payment options and means of payment (cash, check, charge

cards, debit cards, automated bank drafts)

Notify the patient regarding any applicable discounts which policy allows

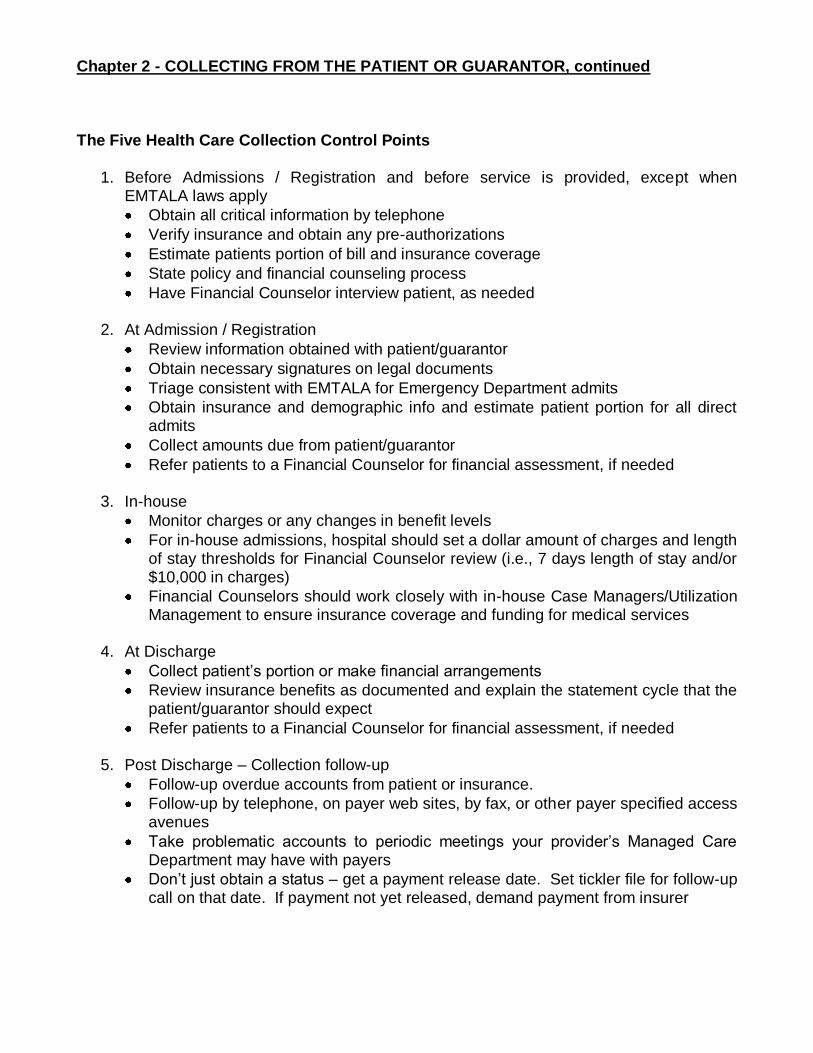

Chapter 2 - COLLECTING FROM THE PATIENT OR GUARANTOR, continued

The Five Health Care Collection Control Points

1. Before Admissions / Registration and before service is provided, except when EMTALA laws apply

Obtain all critical information by telephone

Verify insurance and obtain any pre-authorizations

Estimate patients portion of bill and insurance coverage

State policy and financial counseling process

Have Financial Counselor interview patient, as needed

2. At Admission / Registration

Review information obtained with patient/guarantor

Obtain necessary signatures on legal documents

Triage consistent with EMTALA for Emergency Department admits

Obtain insurance and demographic info and estimate patient portion for all direct admits

Collect amounts due from patient/guarantor

Refer patients to a Financial Counselor for financial assessment, if needed

3. In-house

Monitor charges or any changes in benefit levels

For in-house admissions, hospital should set a dollar amount of charges and length of stay thresholds for Financial Counselor review (i.e., 7 days length of stay and/or $10,000 in charges)

Financial Counselors should work closely with in-house Case Managers/Utilization Management to ensure insurance coverage and funding for medical services

4. At Discharge

Collect patient‘s portion or make financial arrangements

Review insurance benefits as documented and explain the statement cycle that the patient/guarantor should expect

Refer patients to a Financial Counselor for financial assessment, if needed

5. Post Discharge – Collection follow-up

Follow-up overdue accounts from patient or insurance.

Follow-up by telephone, on payer web sites, by fax, or other payer specified access avenues

Take problematic accounts to periodic meetings your provider‘s Managed Care Department may have with payers

Don‘t just obtain a status – get a payment release date. Set tickler file for follow-up call on that date. If payment not yet released, demand payment from insurer

Chapter 3 – UNDERSTANDING COLLECTION LAW

The Fair Debt Collection Practices Act (FDCPA)

The Fair Debt Collection Practices Act (aka FDCPA) is a United States statute added in 1978 as Title VIII of the Consumer Credit Protection Act. Its purposes are to eliminate abusive practices in the collection of consumer debts, to promote fair debt collection and to provide consumers with an avenue for disputing and obtaining validation of debt information in order to ensure the information's accuracy. The Act creates guidelines under which debt collectors may conduct business, defines rights of consumers involved with debt collectors, and prescribes penalties and remedies for violations of the Act. It is sometimes used in conjunction with the Fair Credit Reporting Act, which will be discussed in more detail in this chapter.

The FDCPA broadly defines a debt collector as "any person who uses any instrumentality of interstate commerce or the mails in any business the principal purpose of which is the collection of any debts, or who regularly collects or attempts to collect, directly or indirectly, debts owed or due or asserted to be owed or due another." While the FDCPA generally only applies to third party debt collectors--not internal collectors for an "original creditor" e.g. the hospital -- some states, have similar state consumer protection laws which mirror the FDCPA, and regulate original creditors. In addition, courts have generally found debt buyers to be covered by the FDCPA even though they are collecting their own debts. The definitions and coverage have changed over time. The FDCPA itself contains numerous exceptions to the definition of a "debt collector," particularly after the October 13, 2006, passage of the Financial Services Regulatory Relief Act of 2006 (for an overview, see http://banking.senate.gov/public/_files/RegRel_summary.pdf). Attorneys, originally explicitly excepted from the definition of a debt collector, have been included (to the extent that they otherwise meet the definition) since 1986.

The FDCPA's definitions of ―consumers‖ and ―debt‖ specifically restrict the coverage of the act to personal, family or household transactions. These laws are for the protection of the debtor and debt collectors. Our society has become highly litigious. With information like the FDCPA so accessible, the person on the other end of the phone may very well be as equally knowledgeable of their rights under this act as the collector. How does this relate to Healthcare, you may ask? It is simple, each healthcare professional should be: Informed and thoroughly compliant with all aspects of this act, and; Have every applicable member of our organizations equally aware and in compliance

with the requirements. Although a full copy of the FDCPA is not included in this manual, a basic outline has been provided to guide collections in the most critical aspects of the Act as they relate to your job.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued The complete FDCPA is available on the FTC website @ www.ftc.gov/os/statutes/fdcpa/fdcpact.htm. This summary is not intended to provide all necessary information regarding the FDCPA. Here are the essentials: 1) Correspondence with the consumer:

Notify the consumer with a validation notice that the account is with a debt collection agency.

The consumer has 30 days from the date of their validation notice to dispute their debt in writing.

When the consumer disputes their debt in writing within the 30 days, the debt collector must either mail the consumer the requested validation information or cease collection efforts altogether or file suit.

2) Speaking with the consumer on the telephone:

Debt collector must identify themselves and notify the consumer that the communication is from a debt collector with the intent to collect a debt.

Calls must be placed between 8:00am and 9:00pm local time of the consumer.

If the consumer has made you aware that certain times or places are inconvenient, calls during such times or to such places must cease.

Calls to the consumer‘s place of employment are prohibited a) if you know or have reason to know that the employer forbids this type of communication and b) when the consumer has requested in writing that this contact is not acceptable.

Causing a telephone to ring or engaging a person in conversation repeatedly or continuously with the intent to annoy, abuse or harass is prohibited.

When a consumer requests in writing that all contact stop and that they refuse to pay the debt, you may not engage in telephone communications; however you can provide written notice that either a) collection efforts are being terminated or b) that you intend to file a lawsuit or pursue other remedies when permitted.

The debt collector may not contact the consumer after receipt of their dispute of a debt during their 30 days from the date of receipt of their validation notice of their debt.

3) Third-party involvement on the consumer‘s behalf:

If the consumer has acquired legal representation, as a collector, you are barred from legally speaking to anyone concerning the consumer‘s debt(s) other than the above-mentioned attorney.

If there is no attorney involved, you may contact people whom the debtor in question knows, but only to determine where the consumer lives and works. Take precaution that you not speak with this type of third party more than once, instead get the information you need while you are talking to them. You may at no time disclose – unless you are speaking with an attorney – that the consumer owes money

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

4) Certain types of behavior that are prohibited: Harassment:

Threats of violence against the person, their property, or their reputation

Publishing a list of consumers who refuse to pay their debts (except to a credit bureau)

Use of obscene or profane language

Repeatedly calling the consumer with the intent to unnerve or annoy False or Misleading Information:

Failing to identify yourself when calling the consumer

Falsely imply that you are an attorney or government representative

Falsely imply that the consumer has committed a crime

Falsely imply that you work for or represent a credit bureau

Failing to accurately communicate that actual dollar amount of the debt(s)

Claiming information being mailed is a legal document when it is not, or, that information being mailed is not a legal document when it is

Telling the consumer that he/she will be arrested for failure to pay the debt(s)

Threatening the consumer with seizure or garnishment

The use of any false representation or deceptive means to collect or attempt to collect any debt or obtain information concerning a consumer

Unfair Practices:

The collection of any amount (including any interest, fee, charge, or expense incidental to the principal obligation) unless such amount is expressly authorized by the agreement creating the debt

The acceptance by a debt collector from any person of a check or other payment instrument postdated by more than five days unless such person is notified in writing of the debt collector‘s intent to deposit such check or instrument not more than ten or less than three business days prior to such deposit

The solicitation by a debt collector of any postdated check or other postdated payment instrument for the purpose of threatening or instituting criminal prosecution

Depositing or threatening to deposit any postdated check or other postdated payment instrument prior to the date on such check or instrument.

Communicating with a consumer regarding a debt by post card. Violations of these ―practices‖ can be $1000.00 per offense.

The Fair Credit Reporting Act (FCRA) - The Fair Credit Reporting Act (FCRA) is United States federal law that regulates the collection, dissemination, and use of consumer credit information. As with the FDCPA, only a summary of the FCRA is included here. To read the Act in its entirety, it is available on www.ftc.gov/os/statutes/fcra.htm.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

The Fair Credit Reporting Act (FCRA) is designed to promote accuracy, fairness, and privacy of information in the files of every "consumer-reporting agency" (CRA). Most CRAs are credit bureaus that gather and sell information about you to creditors, employers, and other businesses. This information includes:

where you work and live

if you pay your bills on time

whether you've been sued, arrested, or filed for bankruptcy

the types of debts you have, i.e. credit cards, homes, auto‘s etc.

The FCRA gives individuals specific rights in dealing with CRAs which requires them to provide consumers with a summary of these rights as listed below. The complete text of the FCRA, 15 U.S.C., 1681 et seq. at the Federal Trade Commission‘s web site (http://www.ftc.gov).

Individuals must be told if information in their file has been used against them. Anyone who uses information from a CRA to take action against an individual (such as denying an application for credit, insurance, or employment) must provide the name, address, and phone number of the CRA that provided the report.

Consumers are able to find out what is in their file. A CRA must provide all the information in one‘s file, and a list of everyone who has requested it recently. However, individuals are not entitled to a "risk score" or a "credit score" that is based on information in their file. There is no charge for the report if a person‘s application was denied because of information supplied by the CRA, although the request for the report must occur within 60 days of receiving the denial notice.

Individuals are also entitled to one free report a year if it is certified that (1) they are unemployed and plan to seek employment within 60 days, (2) they are on welfare, or (3) their report is inaccurate due to fraud. Otherwise, a CRA may charge you a fee of up to eight dollars. Currently, one free credit report per year (from each of the big three consumer reporting agencies - Equifax, Experian & Trans Union) has been made available courtesy of AnnualCreditReport.com.

Consumers can dispute inaccurate information with the CRA. If an individual tells a CRA that their file contains inaccurate information, the CRA must reinvestigate the items (usually within 30 days) unless the dispute is frivolous. The CRA must pass along to its source all relevant information the individual provides. The CRA also must supply written results of the investigation and a copy of the report, if it has changed. If an item is altered or deleted because it is disputed, the CRA cannot place it back in the file unless the source of the information verifies its accuracy and completeness, and the CRA provides a written notice that includes the name, address and phone number of the source.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

Inaccurate information must be deleted. A CRA must remove inaccurate information from its files, usually within 30 days after disputing its accuracy. The largest credit bureaus must notify other national CRAs if items are altered or deleted. However, the CRA is not required to remove data from a file that is accurate unless it is outdated or cannot be verified.

It is possible to dispute inaccurate items with the source of the information. If mentioned (such as to a creditor who reports to a CRA) that an item is disputed, they may not then report the information to a CRA without including a notice of the dispute. In addition, once the source is notified of the error in writing, they may not continue to report it if it is in fact an error. Outdated information may not be reported. In most cases, a CRA may not report negative information that is more than seven years old; ten years for bankruptcies.

Access to an individual‘s file is limited. A CRA may provide information about a person only to those who have a need recognized by the FCRA (usually to consider an application you have submitted to a creditor, insurer, employer, landlord, or other business). One‘s consent is required for reports that are provided to employers or that contain medical information. A CRA may not report to an individual‘s employer, or prospective employer, about or without that person‘s written consent. A CRA may not divulge one‘s medical information without their permission.

It is possible to stop a CRA from including one‘s name on lists for unsolicited credit and insurance offers. Creditors and insurers may use file information as the basis for sending unsolicited offers of credit or insurance. Such offers must include a toll-free number to call if an individual wants their name and address excluded from future lists or offers. When notifying the CRA through the toll-free number, they must keep the requestor off the lists for two years. However, individuals may request and complete the CRA form provided for this purpose, thereby having their name and address removed indefinitely.

Individuals may seek damages from violators. Additionally, it is possible to sue a CRA or other party in state or federal court for violations of the FCRA. If such a suit is won, the defendant may have to pay damages and reimbursement of attorney fees. If the individual loses and the court specifically finds the suit to be in bad faith, the individual or their attorney may have to pay the defendant's fees.

Legal Implications of Credit Reporting:

Reporting medical debt to credit agencies is often a must in our industry, especially when a patient/guarantor continuously fails to make an agreed upon payment to satisfy their financial obligation. However, being informed about the process of credit reporting - especially its legal implications - will save everyone involved the potential difficulty of improperly reporting the debt.

First of all, most credit reporting agencies require membership before they will accept information from a creditor. Membership is generally fairly inexpensive, and usually entitles the member to receive credit reports that are not available to the general public. Typically, a nominal fee is charged for each credit report accessed.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

Secondly, a creditor can only report truthful information to a CRA, such as a debtor who did not pay a bill on time. The focus should be appropriately placed on collecting the debt - that is the first priority. Reporting is a viable recourse when that debt is uncollectible.

For that very reason, it is a good idea to notify a debtor of the intent to report their debt to a credit-reporting agency. Here are several reasons:

1) It is a good public relations move on the part of the institution. There is not a single hospital in America that wants to be known as the one that ruined someone‘s credit over a $75.00 bill. Besides, repeat customers are good business for hospitals.

2) It gives the debtor one last opportunity to satisfy the debt, and perhaps that is the very opportunity they need. Being able to speak to the debtor, about the seriousness of the debt reinforcing the obligation to pay, is sometimes all it takes to get that commitment.

3) Although there will certainly be exceptions, many debtors may simply need to know that the possibility exists of being reported to a credit-reporting agency. Often this will be all the incentive needed to clear up the debt. Remember, that the goal is to collect the money, and as long as that is accomplished legally, ethically and honestly, it is a job well done.

Credit Report:

A credit report can be intimidating and confusing when one does not know what the abbreviations and alphanumeric codes indicate. This section on credit reports is a generalized explanation with a few keys provided on the most common credit reporting codes.

There are three different reporting agencies, Experian, Trans Union, and Equifax. All three agencies may have different information on a consumer because companies may or may not subscribe to all of them. Generally, a report is organized into five different sections: 1. identifying information 2. credit/account history (also known as trade lines) 3. collection agencies 4. public records 5. inquiries Depending on the reporting agency, other sections may be provided such as credit summary, special messages, and consumer statements.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

All five sections are fairly easy to read and understand with the exception of one: the credit/account history section. The credit bureaus use industry standard codes to report the type of account, the manner of payment, and the account designator(s) which makes this section difficult. The sections are described below.

Credit/Account History: This section reveals information about account history and lines of credit. Also, it will provide insight into a consumer‘s buying and payment activities. The creditor name and account number will be displayed. Other items provided on the report include:

When the account was opened The type of account (installment, such as a mortgage or car loan, or revolving, such as

a department store credit card) Account Designator(s): whether the account is in the consumer‘s name alone or with

another person Total amount of the loan, high credit limit or highest balance on the card How much remains as balance due Fixed monthly payments or minimum monthly amount Status of the account (open, inactive, closed, paid, etc.) Manner of payment: how well the account has been paid

During the collection process, it is important for a financial counselor to be informed of available lines of credit. Therefore, being able to determine lines of credit on cards (subtract balance due from the credit limit) is key to successful collection negotiations.

Type of Account –

O - Open Account – provides the entire balance due each month R – Revolving or Option – amount due can change each month I – Installment – fixed amount due each month

Account Designator(s) – These codes may vary slightly depending on the reporting agency.

I Individual account. The subject of the report, and no one else, is responsible for payment on the account.

J Joint account. The subject and another person or persons are jointly

responsible for payment on the account. A Authorized Use. This is a shared account, but one person has responsibility for

payment, while the other person does not. U Undesignated. This code is an indication that the credit grantor does not have

enough information to give the account a more specific designator code.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

T Terminated. The subject relationship to the account has ended, although other parties who once shared the account with the subject may continue to maintain the account. This code is used often after a divorce, when one party continues to maintain an account, while the other party is disassociated from it.

M Maker. The subject is responsible for payment of an installment loan, but a co-

maker is involved as assurance that the loan will be repaid. C Co-maker or Co-signor. The subject has co-signed for an installment loan, and

will be responsible for payment if the borrower should default – ―guarantor‖. B On behalf of another person. The subject has financial responsibility for an

account which is used exclusively by another person, as when a father opens a charge account for his daughter‘s use at college.

S Shared, but otherwise undesignated. This codes is an indication that the credit

grantor knows that the subject and at least one other person share the account, but not enough information is available to designate the account as either J (joint) or A (authorized use).

Manner of Payment – Manner of payment codes are standardized codes/numbers and are used to report a consumer‘s payment history.

The standard codes are: 0 – Approved, but account is too new to rate or not yet used 1 – Paid as agreed 2 – 30 or more days past due 3 – 60 or more days past due 4 – 90 or more days past due 5 – 120 or more days past due or is a collection account 7– Making regular payments under a wage earner plan or other repayment arrangement 8 – Repossession 9 – Charged off account (Bad Debt)

Some agencies report manner of payments in clear statements such paid as agreed. Where others may use payment codes ranging from 1 to 9; or a combination of ‗type of account‘ with the ‗manner of payment‘, such as an R1 or I1 on a report is an indication of a good payment history on a revolving or installment account.

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

As an example of variation, Trans Union uses the following codes in addition to the standard codes/numbers as their manner of payments: 8A – Voluntary repossession 8D – Legal repossession 8P – Paying or paid account with manner of payment 08 9B – Collection account 9P – Paying or paid account with manner of payment 09 or 9B UC – Unclassified UR – Unrated Often the ‗manner of payment‘ is used to determine if a consumer/patient will pay his/her hospital balance. The higher the ‗manner of payment‘ number, the less likely the consumer/patient will pay timely or at all which will add cost to collecting balances due over the long term. Manner of payments are used often to justify write-off adjustments to uncollectible or charity. Identifying information: This section is used to confirm the identity of the individual. It is not unusual for different variations of the consumer name to be displayed. This depends on how companies have reported the information to credit bureaus. Other information displayed may include current and previous addresses, date of birth, telephone numbers, driver‘s license numbers, employer information, and spouse‘s name. Collection Agencies: This section reports accounts that have been transferred to a collection agency. The section is easy to read as it provides the collection agency name, amount due, and the date the account was transferred to bad debt. Public Records: Information applied to a consumer‘s public record is provided by county, state, and federal courts. Items reported on a public record include tax liens, civil judgments, and bankruptcies. The items remain on a credit report will vary depending on the type of record. Civil judgments = seven years Unpaid tax liens = indefinite Paid tax liens = seven years from date paid Chapter 7, 11, or 12 bankruptcies = 10 years Chapter 13 bankruptcy filings = 10 years Chapter 13 bankruptcy dismissal or discharges = seven years Bankruptcies voluntarily dismissed = seven years

Chapter 3 – UNDERSTANDING COLLECTION LAW, continued

Inquiries: The inquiring section of a credit report provides a listing of all the companies that have requested and obtained a credit report. A ―hard‖ inquiry is defined as the consumer/patient completed a credit application, and the creditor requested his/her credit report.

A ―soft‖ inquiry is defined as a company requesting information for promotional/marketing opportunities. Not all information is released or provided for ‗soft‘ inquiries.

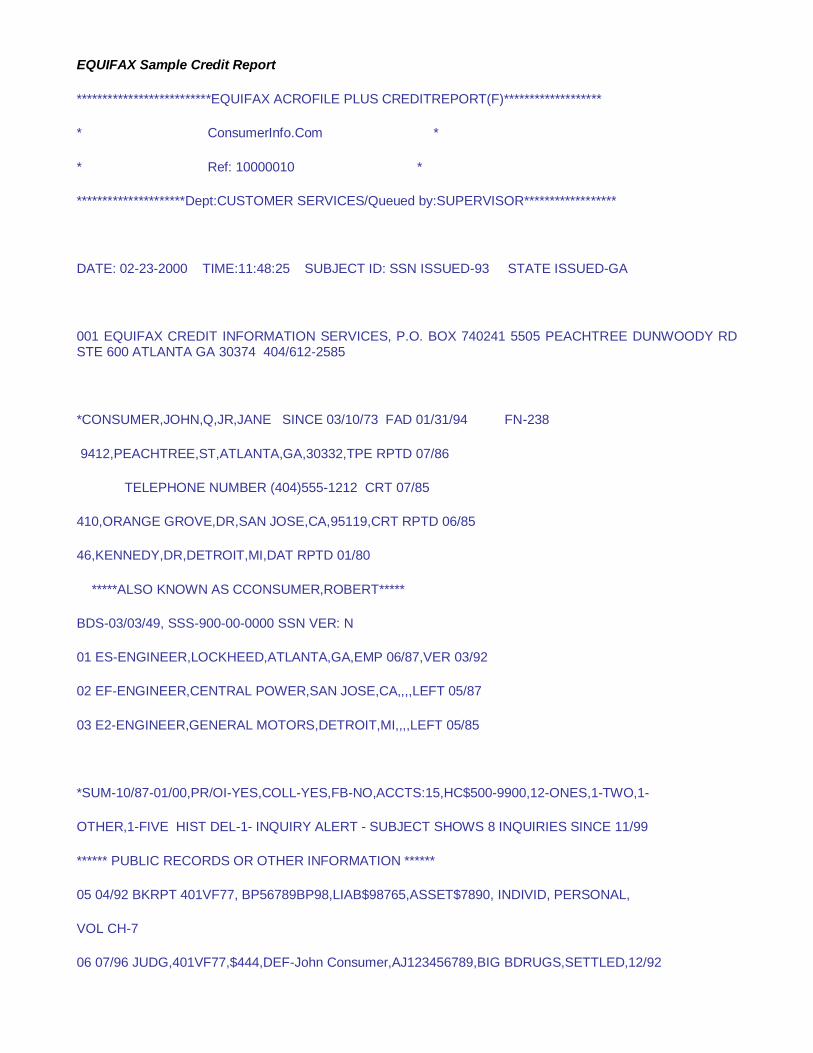

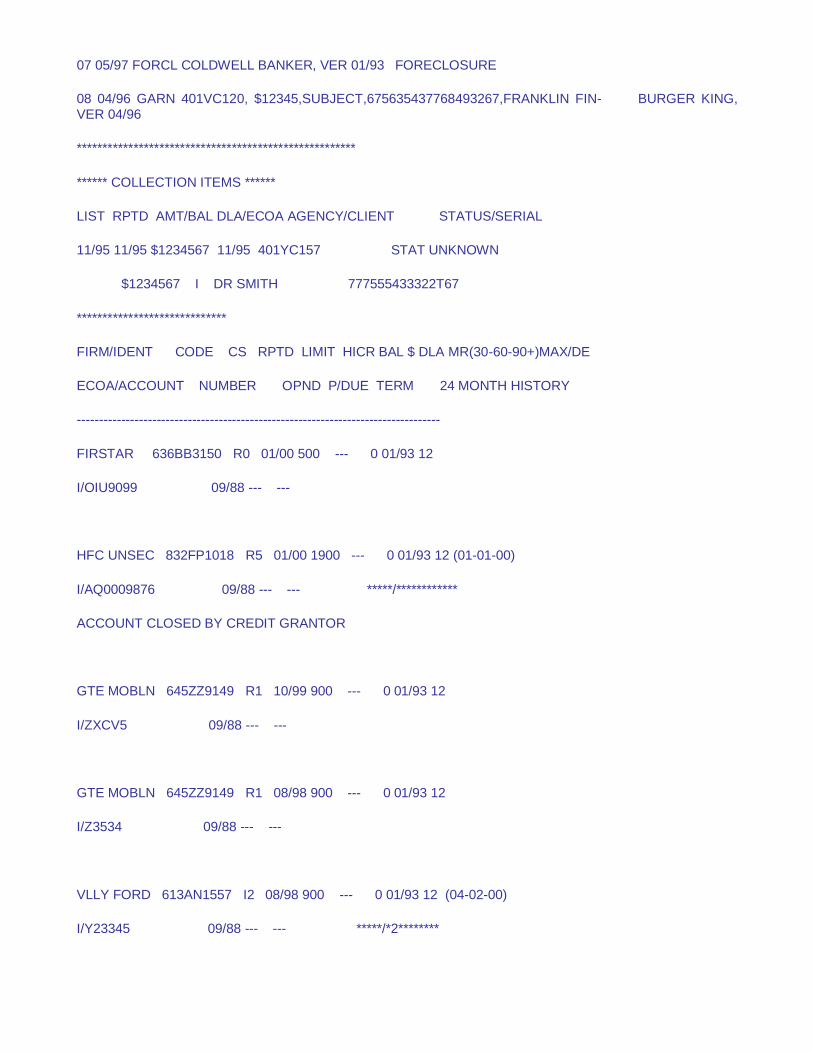

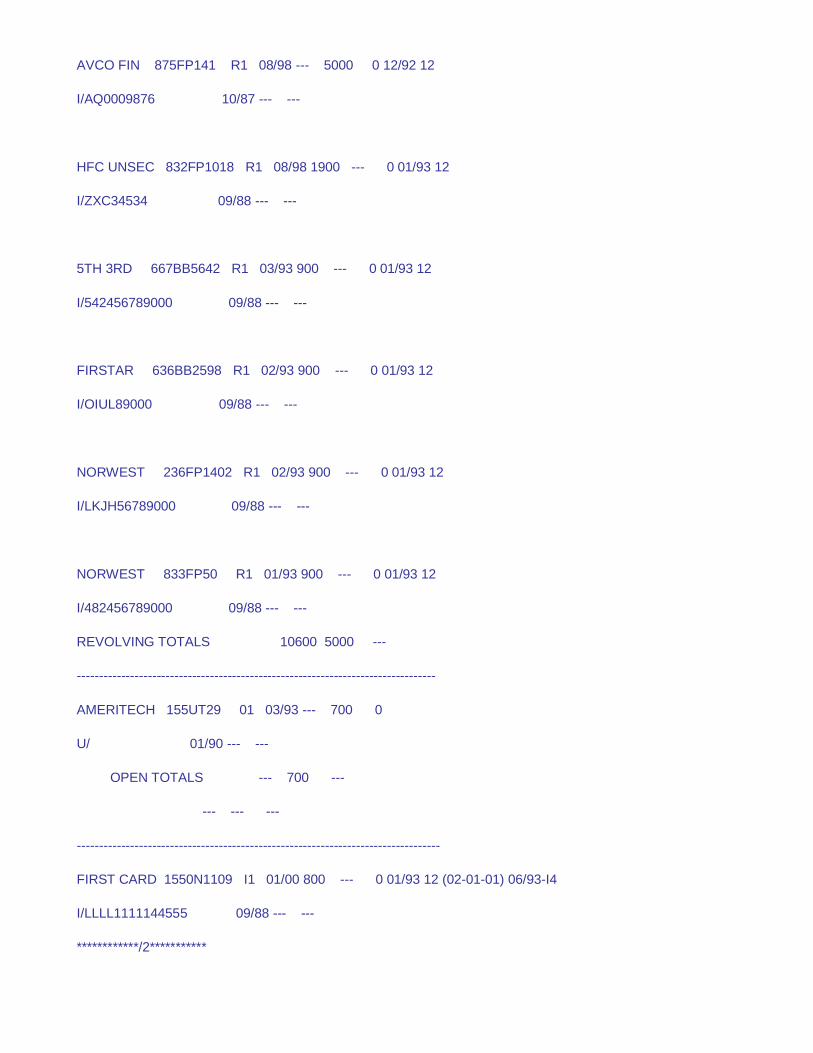

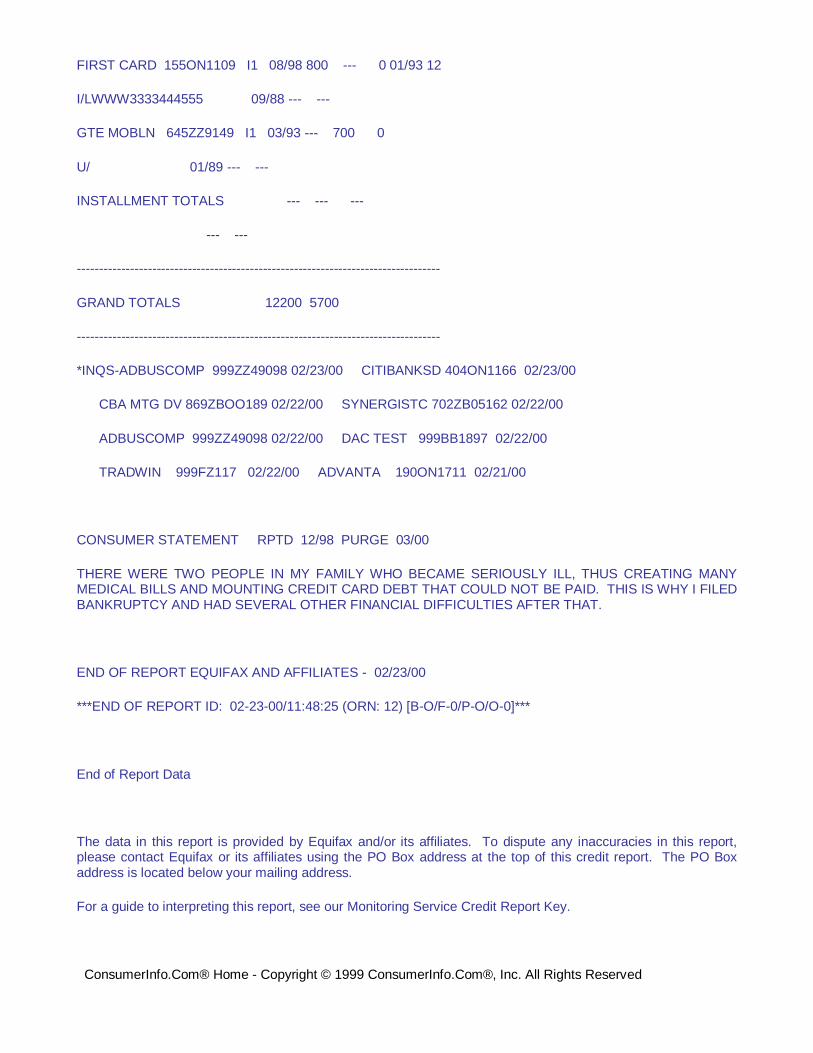

Following are examples of a Credit Report from Equifax and Experian.

EQUIFAX Sample Credit Report

**************************EQUIFAX ACROFILE PLUS CREDITREPORT(F)*******************

* ConsumerInfo.Com *

* Ref: 10000010 *

*********************Dept:CUSTOMER SERVICES/Queued by:SUPERVISOR******************

DATE: 02-23-2000 TIME:11:48:25 SUBJECT ID: SSN ISSUED-93 STATE ISSUED-GA

001 EQUIFAX CREDIT INFORMATION SERVICES, P.O. BOX 740241 5505 PEACHTREE DUNWOODY RD STE 600 ATLANTA GA 30374 404/612-2585

*CONSUMER,JOHN,Q,JR,JANE SINCE 03/10/73 FAD 01/31/94 FN-238

9412,PEACHTREE,ST,ATLANTA,GA,30332,TPE RPTD 07/86

TELEPHONE NUMBER (404)555-1212 CRT 07/85

410,ORANGE GROVE,DR,SAN JOSE,CA,95119,CRT RPTD 06/85

46,KENNEDY,DR,DETROIT,MI,DAT RPTD 01/80

*****ALSO KNOWN AS CCONSUMER,ROBERT*****

BDS-03/03/49, SSS-900-00-0000 SSN VER: N

01 ES-ENGINEER,LOCKHEED,ATLANTA,GA,EMP 06/87,VER 03/92

02 EF-ENGINEER,CENTRAL POWER,SAN JOSE,CA,,,,LEFT 05/87

03 E2-ENGINEER,GENERAL MOTORS,DETROIT,MI,,,,LEFT 05/85

*SUM-10/87-01/00,PR/OI-YES,COLL-YES,FB-NO,ACCTS:15,HC$500-9900,12-ONES,1-TWO,1-

OTHER,1-FIVE HIST DEL-1- INQUIRY ALERT - SUBJECT SHOWS 8 INQUIRIES SINCE 11/99

****** PUBLIC RECORDS OR OTHER INFORMATION ******

05 04/92 BKRPT 401VF77, BP56789BP98,LIAB$98765,ASSET$7890, INDIVID, PERSONAL,

VOL CH-7

06 07/96 JUDG,401VF77,$444,DEF-John Consumer,AJ123456789,BIG BDRUGS,SETTLED,12/92

07 05/97 FORCL COLDWELL BANKER, VER 01/93 FORECLOSURE

08 04/96 GARN 401VC120, $12345,SUBJECT,675635437768493267,FRANKLIN FIN- BURGER KING, VER 04/96

******************************************************

****** COLLECTION ITEMS ******

LIST RPTD AMT/BAL DLA/ECOA AGENCY/CLIENT STATUS/SERIAL

11/95 11/95 $1234567 11/95 401YC157 STAT UNKNOWN

$1234567 I DR SMITH 777555433322T67

*****************************

FIRM/IDENT CODE CS RPTD LIMIT HICR BAL $ DLA MR(30-60-90+)MAX/DE

ECOA/ACCOUNT NUMBER OPND P/DUE TERM 24 MONTH HISTORY

----------------------------------------------------------------------------------

FIRSTAR 636BB3150 R0 01/00 500 --- 0 01/93 12

I/OIU9099 09/88 --- ---

HFC UNSEC 832FP1018 R5 01/00 1900 --- 0 01/93 12 (01-01-00)

I/AQ0009876 09/88 --- --- *****/************

ACCOUNT CLOSED BY CREDIT GRANTOR

GTE MOBLN 645ZZ9149 R1 10/99 900 --- 0 01/93 12

I/ZXCV5 09/88 --- ---

GTE MOBLN 645ZZ9149 R1 08/98 900 --- 0 01/93 12

I/Z3534 09/88 --- ---

VLLY FORD 613AN1557 I2 08/98 900 --- 0 01/93 12 (04-02-00)

I/Y23345 09/88 --- --- *****/*2********

AVCO FIN 875FP141 R1 08/98 --- 5000 0 12/92 12

I/AQ0009876 10/87 --- ---

HFC UNSEC 832FP1018 R1 08/98 1900 --- 0 01/93 12

I/ZXC34534 09/88 --- ---

5TH 3RD 667BB5642 R1 03/93 900 --- 0 01/93 12

I/542456789000 09/88 --- ---

FIRSTAR 636BB2598 R1 02/93 900 --- 0 01/93 12

I/OIUL89000 09/88 --- ---

NORWEST 236FP1402 R1 02/93 900 --- 0 01/93 12

I/LKJH56789000 09/88 --- ---

NORWEST 833FP50 R1 01/93 900 --- 0 01/93 12

I/482456789000 09/88 --- ---

REVOLVING TOTALS 10600 5000 ---

---------------------------------------------------------------------------------

AMERITECH 155UT29 01 03/93 --- 700 0

U/ 01/90 --- ---

OPEN TOTALS --- 700 ---

--- --- ---

----------------------------------------------------------------------------------

FIRST CARD 1550N1109 I1 01/00 800 --- 0 01/93 12 (02-01-01) 06/93-I4

I/LLLL1111144555 09/88 --- ---

************/2***********

FIRST CARD 155ON1109 I1 08/98 800 --- 0 01/93 12

I/LWWW3333444555 09/88 --- ---

GTE MOBLN 645ZZ9149 I1 03/93 --- 700 0

U/ 01/89 --- ---

INSTALLMENT TOTALS --- --- ---

--- ---

----------------------------------------------------------------------------------

GRAND TOTALS 12200 5700

----------------------------------------------------------------------------------

*INQS-ADBUSCOMP 999ZZ49098 02/23/00 CITIBANKSD 404ON1166 02/23/00

CBA MTG DV 869ZBOO189 02/22/00 SYNERGISTC 702ZB05162 02/22/00

ADBUSCOMP 999ZZ49098 02/22/00 DAC TEST 999BB1897 02/22/00

TRADWIN 999FZ117 02/22/00 ADVANTA 190ON1711 02/21/00

CONSUMER STATEMENT RPTD 12/98 PURGE 03/00

THERE WERE TWO PEOPLE IN MY FAMILY WHO BECAME SERIOUSLY ILL, THUS CREATING MANY MEDICAL BILLS AND MOUNTING CREDIT CARD DEBT THAT COULD NOT BE PAID. THIS IS WHY I FILED BANKRUPTCY AND HAD SEVERAL OTHER FINANCIAL DIFFICULTIES AFTER THAT.

END OF REPORT EQUIFAX AND AFFILIATES - 02/23/00

***END OF REPORT ID: 02-23-00/11:48:25 (ORN: 12) [B-O/F-0/P-O/O-0]***

End of Report Data

The data in this report is provided by Equifax and/or its affiliates. To dispute any inaccuracies in this report, please contact Equifax or its affiliates using the PO Box address at the top of this credit report. The PO Box address is located below your mailing address.

For a guide to interpreting this report, see our Monitoring Service Credit Report Key.

ConsumerInfo.Com® Home - Copyright © 1999 ConsumerInfo.Com®, Inc. All Rights Reserved

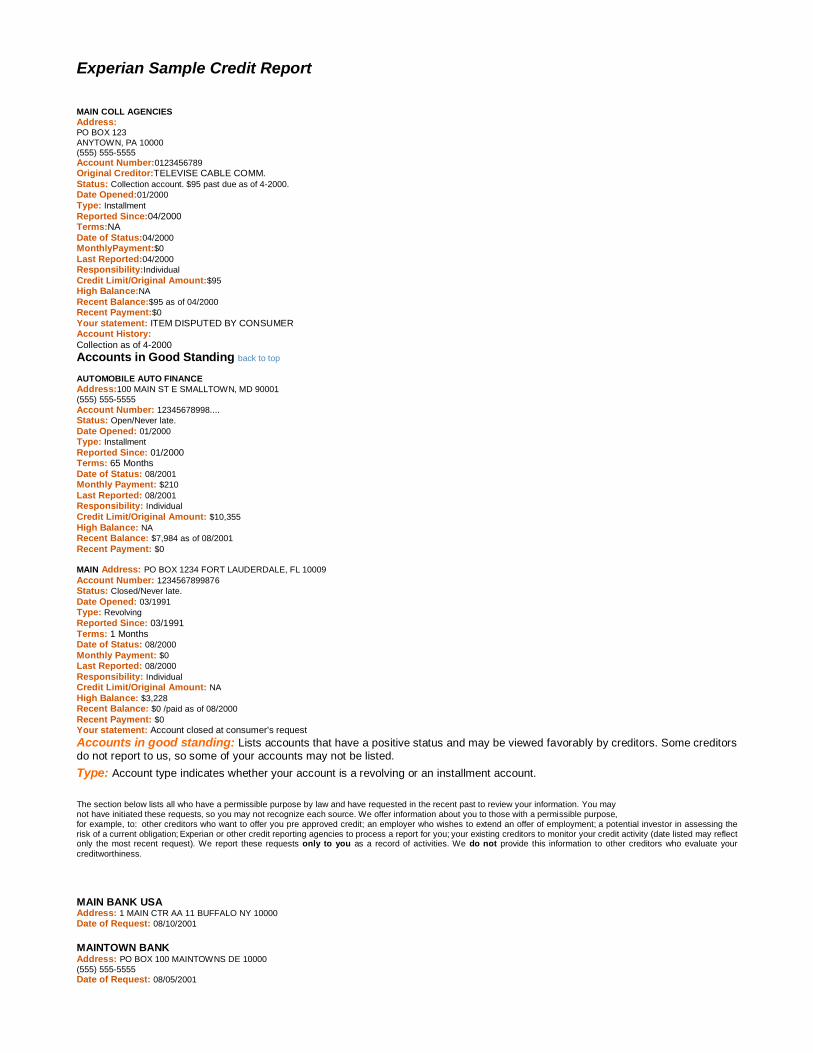

Experian Sample Credit Report

MAIN COLL AGENCIES

Address: PO BOX 123

ANYTOWN, PA 10000 (555) 555-5555

Account Number:0123456789

Original Creditor:TELEVISE CABLE COMM. Status: Collection account. $95 past due as of 4-2000.

Date Opened:01/2000

Type: Installment

Reported Since:04/2000 Terms:NA Date of Status:04/2000

MonthlyPayment:$0

Last Reported:04/2000

Responsibility:Individual

Credit Limit/Original Amount:$95

High Balance:NA

Recent Balance:$95 as of 04/2000

Recent Payment:$0

Your statement: ITEM DISPUTED BY CONSUMER Account History:

Collection as of 4-2000

Accounts in Good Standing back to top

AUTOMOBILE AUTO FINANCE

Address:100 MAIN ST E SMALLTOWN, MD 90001

(555) 555-5555

Account Number: 12345678998....

Status: Open/Never late.

Date Opened: 01/2000

Type: Installment

Reported Since: 01/2000 Terms: 65 Months Date of Status: 08/2001

Monthly Payment: $210

Last Reported: 08/2001

Responsibility: Individual

Credit Limit/Original Amount: $10,355

High Balance: NA

Recent Balance: $7,984 as of 08/2001

Recent Payment: $0

MAIN Address: PO BOX 1234 FORT LAUDERDALE, FL 10009

Account Number: 1234567899876

Status: Closed/Never late.

Date Opened: 03/1991

Type: Revolving

Reported Since: 03/1991 Terms: 1 Months Date of Status: 08/2000

Monthly Payment: $0

Last Reported: 08/2000

Responsibility: Individual

Credit Limit/Original Amount: NA

High Balance: $3,228

Recent Balance: $0 /paid as of 08/2000

Recent Payment: $0

Your statement: Account closed at consumer's request

Accounts in good standing: Lists accounts that have a positive status and may be viewed favorably by creditors. Some creditors do not report to us, so some of your accounts may not be listed.

Type: Account type indicates whether your account is a revolving or an installment account. 6 5 The section below lists all who have a permissible purpose by law and have requested in the recent past to review your information. You may not have initiated these requests, so you may not recognize each source. We offer information about you to those with a permissible purpose, for example, to: other creditors who want to offer you pre approved credit; an employer who wishes to extend an offer of employment; a potential investor in assessing the risk of a current obligation; Experian or other credit reporting agencies to process a report for you; your existing creditors to monitor your credit activity (date listed may reflect only the most recent request). We report these requests only to you as a record of activities. We do not provide this information to other creditors who evaluate your

creditworthiness.

MAIN BANK USA Address: 1 MAIN CTR AA 11 BUFFALO NY 10000

Date of Request: 08/10/2001

MAINTOWN BANK Address: PO BOX 100 MAINTOWNS DE 10000

(555) 555-5555

Date of Request: 08/05/2001

ANYTOWN DATA CORPS Address: 2000 S MAINTOWN BLVD STE

INTOWN CO 11111 (555) 555-5555

Date of Request: 07/16/2001

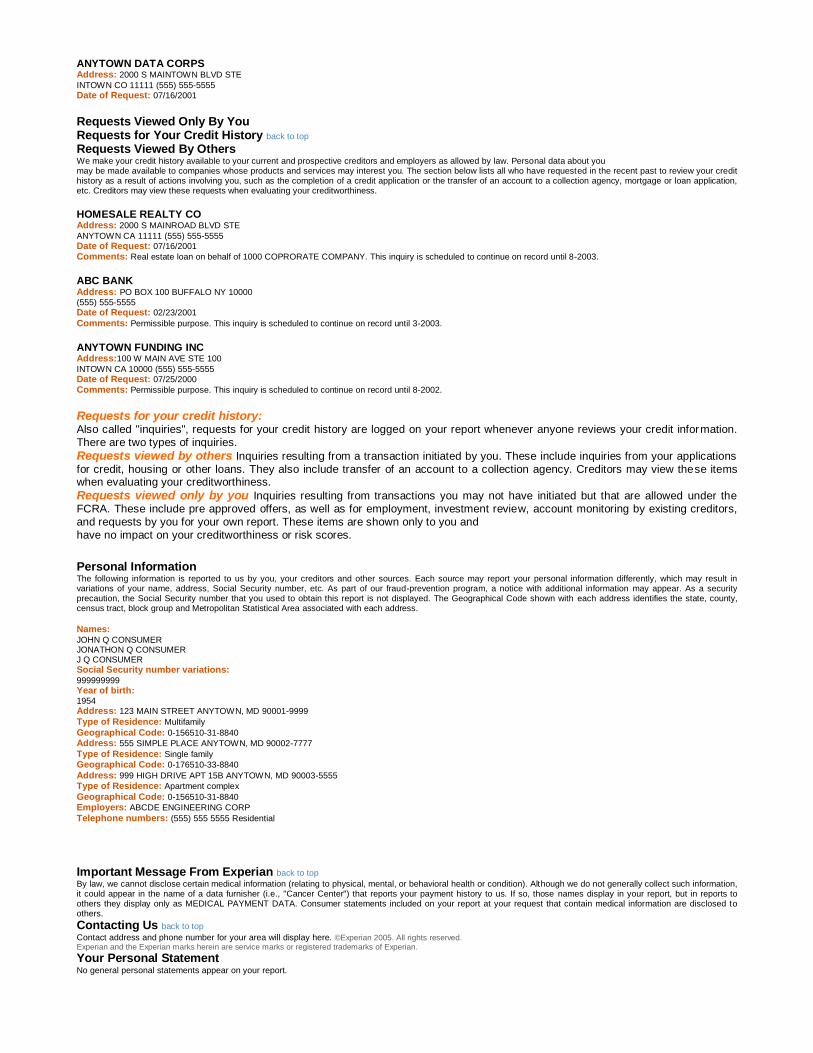

Requests Viewed Only By You Requests for Your Credit History back to top

Requests Viewed By Others We make your credit history available to your current and prospective creditors and employers as allowed by law. Personal data about you may be made available to companies whose products and services may interest you. The section below lists all who have requested in the recent past to review your credit history as a result of actions involving you, such as the completion of a credit application or the transfer of an account to a collection agency, mortgage or loan application, etc. Creditors may view these requests when evaluating your creditworthiness.

HOMESALE REALTY CO Address: 2000 S MAINROAD BLVD STE

ANYTOWN CA 11111 (555) 555-5555

Date of Request: 07/16/2001

Comments: Real estate loan on behalf of 1000 COPRORATE COMPANY. This inquiry is scheduled to continue on record until 8-2003.

ABC BANK Address: PO BOX 100 BUFFALO NY 10000

(555) 555-5555

Date of Request: 02/23/2001

Comments: Permissible purpose. This inquiry is scheduled to continue on record until 3-2003.

ANYTOWN FUNDING INC Address:100 W MAIN AVE STE 100

INTOWN CA 10000 (555) 555-5555

Date of Request: 07/25/2000

Comments: Permissible purpose. This inquiry is scheduled to continue on record until 8-2002.

Requests for your credit history: Also called "inquiries", requests for your credit history are logged on your report whenever anyone reviews your credit information. There are two types of inquiries.

Requests viewed by others Inquiries resulting from a transaction initiated by you. These include inquiries from your applications

for credit, housing or other loans. They also include transfer of an account to a collection agency. Creditors may view these items when evaluating your creditworthiness.

Requests viewed only by you Inquiries resulting from transactions you may not have initiated but that are allowed under the FCRA. These include pre approved offers, as well as for employment, investment review, account monitoring by existing creditors, and requests by you for your own report. These items are shown only to you and have no impact on your creditworthiness or risk scores.

7

Personal Information The following information is reported to us by you, your creditors and other sources. Each source may report your personal information differently, which may result in variations of your name, address, Social Security number, etc. As part of our fraud-prevention program, a notice with additional information may appear. As a security precaution, the Social Security number that you used to obtain this report is not displayed. The Geographical Code shown with each address identifies the state, county, census tract, block group and Metropolitan Statistical Area associated with each address.

Names: JOHN Q CONSUMER JONATHON Q CONSUMER J Q CONSUMER

Social Security number variations: 999999999

Year of birth: 1954

Address: 123 MAIN STREET ANYTOWN, MD 90001-9999

Type of Residence: Multifamily

Geographical Code: 0-156510-31-8840

Address: 555 SIMPLE PLACE ANYTOWN, MD 90002-7777

Type of Residence: Single family

Geographical Code: 0-176510-33-8840

Address: 999 HIGH DRIVE APT 15B ANYTOWN, MD 90003-5555

Type of Residence: Apartment complex

Geographical Code: 0-156510-31-8840

Employers: ABCDE ENGINEERING CORP

Telephone numbers: (555) 555 5555 Residential

Important Message From Experian back to top

By law, we cannot disclose certain medical information (relating to physical, mental, or behavioral health or condition). Although we do not generally collect such information, it could appear in the name of a data furnisher (i.e., "Cancer Center") that reports your payment history to us. If so, those names display in your report, but in reports to others they display only as MEDICAL PAYMENT DATA. Consumer statements included on your report at your request that contain medical information are disclosed to others.

Contacting Us back to top

Contact address and phone number for your area will display here. ©Experian 2005. All rights reserved. Experian and the Experian marks herein are service marks or registered trademarks of Experian.

Your Personal Statement No general personal statements appear on your report.

10 Personal information: Personal information associated with your history that has been reported to Experian by you, your

creditors and other sources. May include name and Social Security number variations, employers, telephone numbers, etc. Experian lists all variations so you know what is being reported to us as belonging to you.

Address information: Your current address and previous address(es)

Personal statement: Any personal statement that you added to your report appears here.

Note - statements remain as part of the report for 2 years and display to anyone who has permission to review your report.

8

Chapter 4 – HOW TO COLLECT

The Value of Role Playing

Although role-playing is used in many industries, very few people really enjoy role-playing. It makes one nervous, one may feel put on the spot, and often times find the entire process to be embarrassing. Let‘s take a look at role playing from a different perspective and see what benefits one can receive.

A simple definition of role playing is: Pretending to be someone you are not so as to be prepared to handle certain people and situations when they arise. Role-playing is common in a variety of industries. Police officers conduct role-playing exercises to learn how to handle any number of dangerous situations while removed from the actual threat of danger. If, as an officer, you have never experienced handcuffing someone until making your first arrest, you might find yourself wishing you could have practiced a few times in a controlled environment. Police role-playing is an example of the physical aspect of role-playing. However, there is a visual element to role-playing as well. Professional athletes make use of the visual element on a daily basis. Golfers visualize bringing the proper swing club back, the follow through, the ball falling where it is supposed to…and ultimately seeing the ball drop into the hole with one putt. Similarly, football players visualize catching a pass, or tackling the receiver. The accepted theory is, when the time comes and the pressure is on, the athlete will be able to rely on his or her mental preparedness to make the shot, score the touchdown, or whatever the case may be, simply because they were ready for the situation. The concept is ―been there – done that‖, so in the reality of the moment one finds oneself prepared.

Healthcare financial counselors, collectors, registrars, cashiers, and customer service personnel must prepare in the same way. There are practical benefits to role playing for anyone who spends time on the phone or in-person negotiating payments.

For the Collector

One could write a book simply based on the excuses heard from patients, where the patient attempts to explain why they did not follow through with promises to make a payment. Examples of excuses may be: (be careful not to judge too quickly)

―I am only 17, the head of my household because both of my parents were recently killed in an car accident‖

―I would have paid but I had a serious illness and had to pay all my money to the doctor‖

―My wallet was lost‖

―I am not responsible for this bill. I am divorced and my spouse is responsible‖

There often are excuses; however, the excuses are at times, correct and true. In fact, those excuses listed above are all true events the writer has heard. Many other excuses are far-fetched and easy to dismiss; others actually seem legitimate and might even pull at your heartstrings. Knowing how to respond to both false and real/legitimate excuses is critical to

Chapter 4 – HOW TO COLLECT, continued

For the Collector, continued

providing excellent customer service, as well as successfully collecting the debt. Role-playingcan significantly improve the way in which you interact with the person on the other end of the phone, as well as make you more comfortable with the entire process.

When collecting self-pay debt it is critical that, from the moment one picks up the phone, or interacts face-to-face with a debtor, one is prepared and in control. Most likely the patient is in a difficult financial situation, and one will need to know how to navigate through the obstacles he or she throws up as a reason to avoid paying this debt. Role-playing helps make navigation possible. There are several critical skills that one must have mastered before contacting the patient/guarantor, each of which consistently improves the hospital‘s chances of collecting the debt.

Critical Skills to Practice by Role Playing

1) Get comfortable introducing yourself and state from where you are calling. This may sound simple, but doing it properly can be the first thing you forget when the debtor picks up the phone. Scripting may be effective in knowing what to say. For instance – Something like:

- ―This is ___________ calling from XYZ Hospital, may I speak to Mr. Robert Jones?‖

It is important to get familiar with identifying the debtor by his or her first and last name, then simply by the appropriate title followed by their last name. In the example above, ―Mr. Jones‖ should be the way you address him during the remainder of the conversation.

2) Imagine what the patient has recently experienced health wise. Remember, the person you‘re speaking to has most likely recently been a hospital patient; if not, he/she is the guarantor for a patient, for example, a child. The possibility exists that this person might have gone through traumatic circumstances that led to their experience with the hospital. Unless one has been able to view medical records associated with the outstanding debt, one cannot be sure what event made it necessary for this person to seek treatment in your facility. It is quite possible that the person you will be speaking to has more on their mind at the moment than fulfilling their financial obligation to your institution. These facts do not make the debt any less real or important, but should serve as a reminder to the caller that rarely do patients fall into a consistent mold, and one should be prepared to address whatever issues arise.

3) Remember your primary responsibility. While circumstances may be difficult for the debtor you‘re speaking with, be mindful of your objective: collecting the money. Some people will talk to you for an hour if you let them. They will give you their entire life story twice, as well as the life stories of each of their family members. You should be on and off the phone in between three and five minutes, therefore you have to be in control of the conversation. Role-playing can make you more comfortable with saying things like, ―I understand this has been difficult Mr. Jones, but the issue we‘re dealing with today is your financial obligation to the hospital.‖ Stay on issue, and don‘t let up.

Chapter 4 – HOW TO COLLECT, continued

Critical Skills to Practice by Role Playing, continued

4) Control your emotions. As a collector, it is your job to be calmly assertive. The person on the other end of the phone or across the desk might break your heart with their sad stories or curse you for even having the nerve to talk about money at a time like this. Regardless, you must remain composed and unaffected by their response. While one certainly retains the right to end a phone conversation if the debtor becomes irrational, through it all one must handle his or herself with integrity. Role playing not only helps you get accustomed to one of the more difficult parts of collecting, it will also provide you with opportunities to work on overcoming even the most wild objections.

5) Don‘t take ―no‖ for an answer. As we mentioned earlier, debtors will come up with every possible excuse for not making a payment. It is your responsibility to know how to effectively overcome each of their objections, therefore, you must be in the habit of not taking ―no‖ for answer. Use role-playing to learn how to respond in a variety of scenarios, especially when a debtor is trying to stall on making a payment.

Negotiating Skills

To assume that every collection call you make, or every patient/guarantor you deal with, will be identical experiences would be a mistake. Although there are certainly common themes when dealing with debtors, there unfortunately isn‘t a guarantee, ―this works every time‖ plan that you can follow. You have to be prepared to negotiate, and in this case, there are three distinct steps in every negotiation:

1) Clarify the objections. Find out what the debtor wants and know what you want to accomplish. Negotiate with a strong sense of purpose. If your goal is payment in full, negotiate for it. Keep ―payment in full‖ on your mind during the conversation. Don‘t enter the discussion with a ―wishy-washy‖ attitude that says you‘ll take whatever you can get.

2) Gather information about the debtor. Some of the information may not have anything to do with the demands or needs of that person, but it will help you decide what strategy or method you will use. You cannot successfully negotiate with incomplete information, especially as it relates to sources of income and other assets. Review past hospital accounts to gather information about the payment personality of this person before talking with them.

3) Last resort - Reach an agreement or compromise. This is the stage every collector wants to get to, and sometimes too quickly. Stages one and two lay the groundwork for improving the chances of this final step being successful. Be patient as you begin negotiating with the debtor, even if they appear to be rushing you towards the agreement. You want to remain in control, and you will benefit greatly from gathering the necessary information before reaching your ultimate goal.

Chapter 4 – HOW TO COLLECT, continued

Negotiating Skills, continued

In an earlier section you read about the importance role-playing has on handling objections. Now it‘s time to learn how to actually handle them, specifically in the context of negotiation. When collecting, you hear many of the same excuses for not paying - from patients and insurance companies alike. Becoming an expert at handling these objections will lead to improved collection totals, as well as reduce some of the inherent stress of negotiating payments. The following six insights are the basic offenses that should be used when handling objections: Remember ―The best defense is a good offense‖.

1) Don’t argue. You might easily win an argument with a patient/guarantor, but would you get paid in full, probably not? Would you generate a complaint in the process, maybe? The goal is not to win an argument and make a patient feel angry, or helpless, but rather to collect payment in full, all the while maintaining and protecting patient relations.

2) Use intelligence - not emotion. Patients may become emotional when they are talking to you (and as we discussed above, that could mean tears or shouting). You need to express sympathy, but remain calm and logical. Avoid getting emotionally involved in the conversation.

3) Use a professional and businesslike manner. Treat manners seriously. State your facts with authority and assurance. Be friendly, but not too familiar. Stick to business-related matters without alienating patients.

4) Be courteous. Always consider the other person‘s feelings by being polite and practicing good manners. Treat the patient as you would want to be treated or as you would want your family member treated.

5) Be flexible. There is not a set-in-stone method for each collection encounter; therefore your collection approach should change if the situation warrants it. Remember, every patient will respond differently to your requests for payment. You will need to use a variety of motivators.

6) Be natural. Use simple, uncomplicated words and phrases. Avoid technical jargon and acronyms, which will confuse others. If people feel you are talking above them, they will have a difficult time trusting what you are telling them. Your delivery should be unhurried and deliberate.

Remember that good collectors are always in control of the conversation tone and their emotions when negotiating with a debtor or handling their objections. Quality collectors consistently provide patients and insurance companies with logical reasons why payment in full is necessary.

Chapter 4 – HOW TO COLLECT, continued

Collection Tactics

At its very core, quality collection is rooted in motivation. People might very well make a one-time payment just to ―get you off their back‖, or occasional payments in varying amounts simply as a means of keeping you off their back, and do so without any motivation whatsoever. However, to either obtain payment in full or to work a debtor into a consistent payment plan, you must motivate them.

Below are some of the motivators behind people paying their bills:

1) Having a good credit rating

2) Doing the right or fair thing

3) Not having to worry about the bill

4) Feeling good about paying their bills

5) Saving additional collection costs (interest, late charges, etc.)

6) Avoiding further collection action

Additionally, there are many more reasons why people pay their bills. For the most part, these reasons fall into one of three categories of motivators:

1) Pride Motivators

2) Honesty Motivators

3) Fear Motivators

If you understand that most people pay because of pride, honesty, or fear, these become your motivational building blocks - the ultimate tactics in collection. Your motivational phrases, designed to give patients a reason to pay, should be built around pride, honesty and fear.

Pride Motivators deal with the self-respect or reputation of the other person. People are usually proud that they can earn a good living for themselves or their family and pay their bills on time. A good credit rating and payment reputation are also things to be proud of. Examples of patient pride motivators include the following:

- ―It took many years to build such a good credit rating. You don‘t want to jeopardize it on this bill, do you?‖

- ―You‘ve always had an excellent payment reputation here at our hospital. Don‘t you want to clear this up today?‖

Chapter 4 – HOW TO COLLECT, continued

Collection Tactics, continued

Note: If your hospital does not utilize a credit-reporting agency (CRA), AKA credit bureau, you cannot utilize the argument regarding ―protecting ones credit rating.‖ If your hospital does utilize a CRA, do not threaten placement of the account with the agency unless that is your full intention. Such an accusation without the intent to follow through may be viewed as harassment and may subject the hospital to unwanted litigation and bad press. Read and understand the Fair Debt Collection Practices Act (FDCPA) to fully understand the implications of your hospital‘s policies if they support the type of collection tactics mentioned above. Examples of using pride motivators with insurance companies include:

- ―Your company has a great payment record with us. I‘m surprised to have this bill outstanding.‖

- ―Isn‘t your reputation as a good payer important to you?‖

Honesty motivators consider people‘s natural reaction to do what‘s right. Most people want to be known as someone who pays bills on time and is fair with others. Patients who received good care from your facility generally know it is only right to pay you in full. Honesty motivators are built around this sense of fair play. Examples of patient honesty motivators include the following:

- ―Do you believe it‘s fair to shortchange the hospital after we gave you our best care?‖

- ―Won‘t you feel better once this bill is off your conscience?‖

Examples of using honesty motivators with insurance companies include:

- ―The patient pays your premium on time. Isn‘t it fair to pay this bill on time too?‖

- ―We‘ve provided you with all the necessary information in a timely fashion. Don‘t you think it‘s only right to pay us now?‖

Fear motivators can be designed around anything that threatens the other person‘s well being. This could be the fear of loss of reputation, loss of future services at your facility, or loss of respect. Many patients fear further collection activity or loss of their good credit rating. Examples of patient fear motivators include the following:

- ―Legal action is expensive, but may be necessary if your promise is not kept. You don‘t want that, do you?‖

- ―Credit is a valuable asset. You don‘t want to risk it on an unpaid bill, do you?‖

Note: See note above in reference to FDCPA.

Chapter 4 – HOW TO COLLECT, continued

Collection Tactics, continued

Examples of using fear motivators with insurance companies include:

- ―If we don‘t get payment from you soon, I have no choice but to contact your subscriber for payment.‖

- ―The insurance commissioner requires payment of a clean claim in 30 days. If you can clear payment today, we won‘t notify them of your delinquency.‖

Sometimes collectors make the mistake of using only fear motivators in their collection strategy. This can lead to many complaints and possibly lost customers. Your collection approach should always start with pride and honesty motivators, because these are positive reasons for paying. Starting with these motivators sets a positive theme early in the call.

If pride and honesty motivators do not work, and one has to use fear motivators, patients will be in a better frame of mind if they‘ve already heard the positives. When one begins with fear motivators, one may create a defensive attitude, and the patient will resist even if you later present the positive pride and honesty motivations for paying.

But wait…what’s in it for me?

As a culture, we like to know what we‘re getting for our cooperation, simply put, ―what‘s in it for me (WIFM)?‖ We‘re all like this in certain ways and it is crucial that you remember this key element of people‘s psyche. Here is how it could work:

Patient objection: ―I‘ve always waited until my insurance pays. Why do you need me to pay my part now?‖

Collection approach without “what’s in it for me” concept: ―It is our policy to collect the patient liability at the time of service. We need you to pay now.‖

Collection approach with WIFM: ―You‘re right; you‘ve always had an excellent payment record with us. But many of our patients have asked us what their responsibility is up front, so they can take care of it right away, and not have to worry about it. We‘ve started this program as a courtesy to our patients.‖

Which approach will get a better response? Without WIFM, the collector uses words like ―our policy‖ and ―we need.‖ These types of words generally make people angry; basically, your patients don‘t care what you need.

Chapter 4 – HOW TO COLLECT, continued

But wait…what’s in it for me?, continued

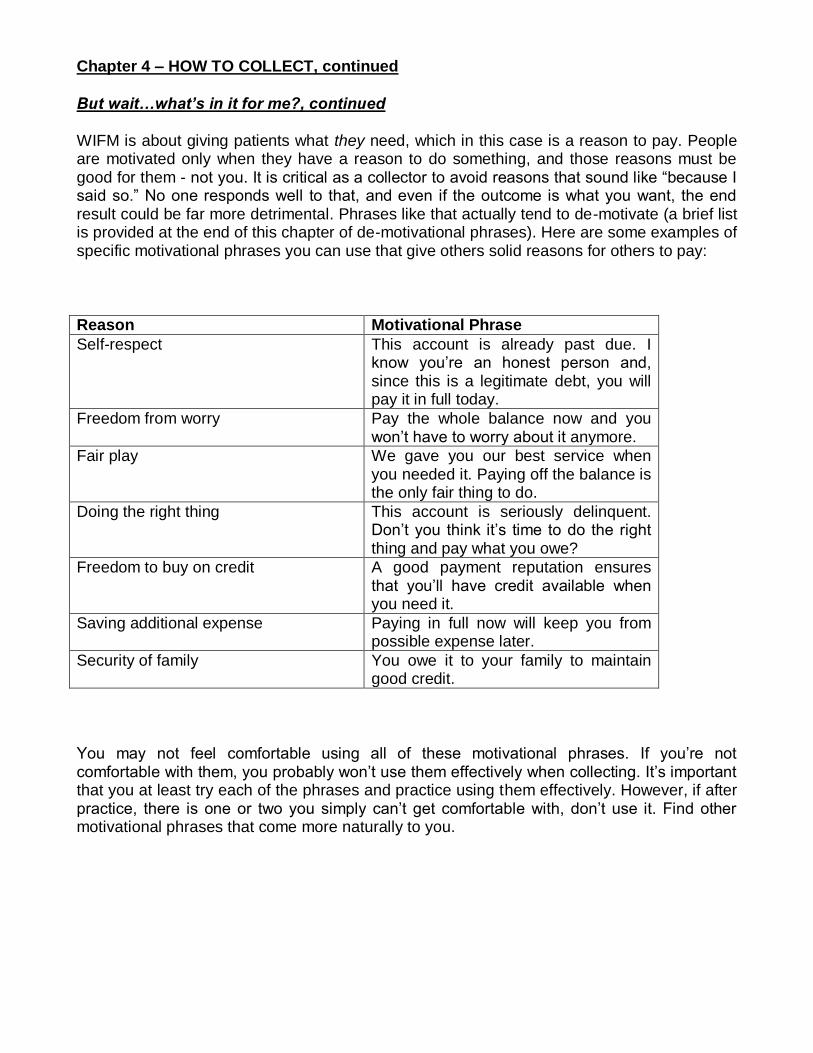

WIFM is about giving patients what they need, which in this case is a reason to pay. People are motivated only when they have a reason to do something, and those reasons must be good for them - not you. It is critical as a collector to avoid reasons that sound like ―because I said so.‖ No one responds well to that, and even if the outcome is what you want, the end result could be far more detrimental. Phrases like that actually tend to de-motivate (a brief list is provided at the end of this chapter of de-motivational phrases). Here are some examples of specific motivational phrases you can use that give others solid reasons for others to pay:

Reason Motivational Phrase

Self-respect This account is already past due. I know you‘re an honest person and, since this is a legitimate debt, you will pay it in full today.

Freedom from worry Pay the whole balance now and you won‘t have to worry about it anymore.

Fair play We gave you our best service when you needed it. Paying off the balance is the only fair thing to do.

Doing the right thing This account is seriously delinquent. Don‘t you think it‘s time to do the right thing and pay what you owe?

Freedom to buy on credit A good payment reputation ensures that you‘ll have credit available when you need it.

Saving additional expense Paying in full now will keep you from possible expense later.

Security of family You owe it to your family to maintain good credit.

You may not feel comfortable using all of these motivational phrases. If you‘re not comfortable with them, you probably won‘t use them effectively when collecting. It‘s important that you at least try each of the phrases and practice using them effectively. However, if after practice, there is one or two you simply can‘t get comfortable with, don‘t use it. Find other motivational phrases that come more naturally to you.

Chapter 4 – HOW TO COLLECT, continued

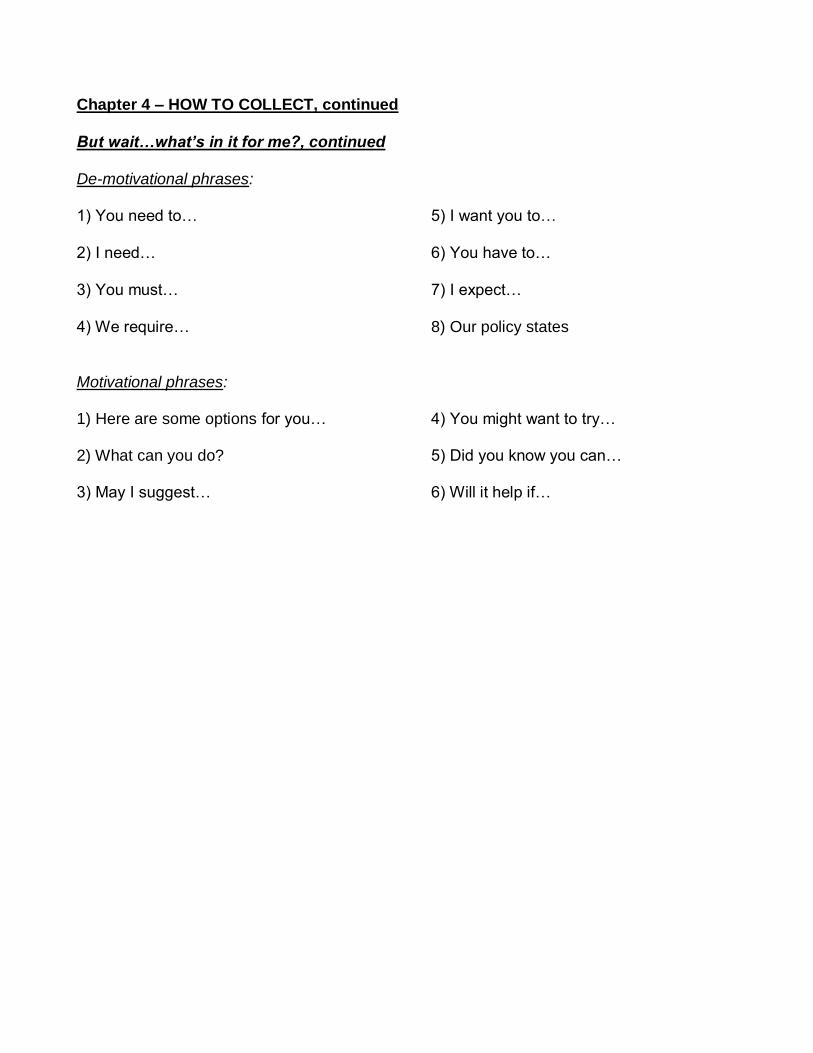

But wait…what’s in it for me?, continued

De-motivational phrases:

1) You need to…

2) I need…

3) You must…

4) We require…

5) I want you to…

6) You have to…

7) I expect…

8) Our policy states

Motivational phrases: 1) Here are some options for you… 2) What can you do? 3) May I suggest…

4) You might want to try… 5) Did you know you can… 6) Will it help if…

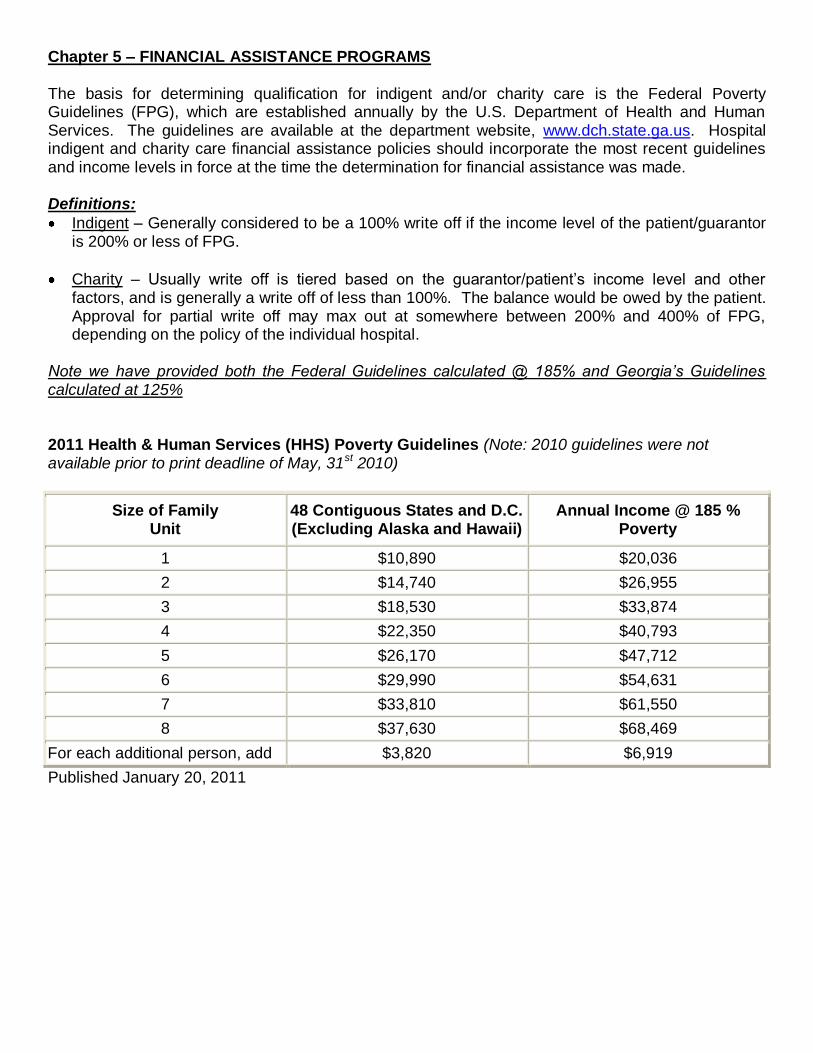

Chapter 5 – FINANCIAL ASSISTANCE PROGRAMS

The basis for determining qualification for indigent and/or charity care is the Federal Poverty Guidelines (FPG), which are established annually by the U.S. Department of Health and Human Services. The guidelines are available at the department website, www.dch.state.ga.us. Hospital indigent and charity care financial assistance policies should incorporate the most recent guidelines and income levels in force at the time the determination for financial assistance was made. Definitions:

Indigent – Generally considered to be a 100% write off if the income level of the patient/guarantor is 200% or less of FPG.

Charity – Usually write off is tiered based on the guarantor/patient‘s income level and other factors, and is generally a write off of less than 100%. The balance would be owed by the patient. Approval for partial write off may max out at somewhere between 200% and 400% of FPG, depending on the policy of the individual hospital.

Note we have provided both the Federal Guidelines calculated @ 185% and Georgia’s Guidelines calculated at 125%

2011 Health & Human Services (HHS) Poverty Guidelines (Note: 2010 guidelines were not available prior to print deadline of May, 31st 2010)

Size of Family Unit

48 Contiguous States and D.C. (Excluding Alaska and Hawaii)

Annual Income @ 185 % Poverty

1 $10,890 $20,036

2 $14,740 $26,955

3 $18,530 $33,874

4 $22,350 $40,793

5 $26,170 $47,712

6 $29,990 $54,631

7 $33,810 $61,550

8 $37,630 $68,469

For each additional person, add $3,820 $6,919

Published January 20, 2011

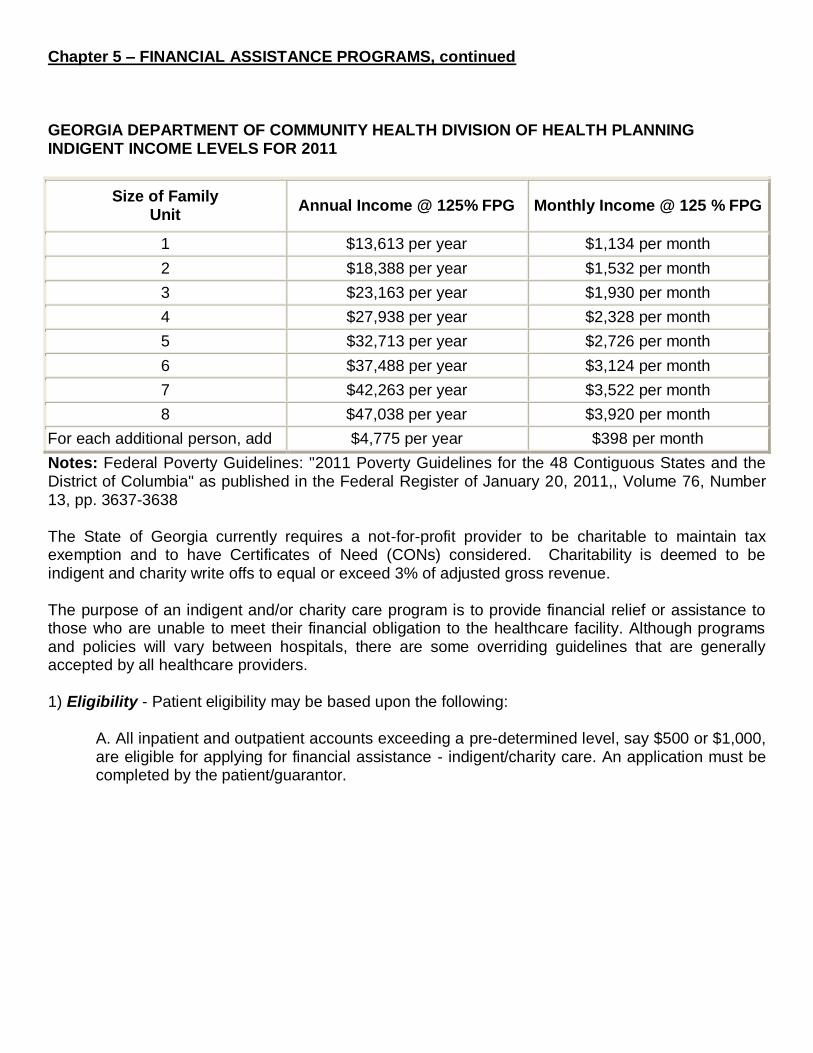

Chapter 5 – FINANCIAL ASSISTANCE PROGRAMS, continued

GEORGIA DEPARTMENT OF COMMUNITY HEALTH DIVISION OF HEALTH PLANNING INDIGENT INCOME LEVELS FOR 2011

Size of Family Unit

Annual Income @ 125% FPG Monthly Income @ 125 % FPG

1 $13,613 per year $1,134 per month

2 $18,388 per year $1,532 per month

3 $23,163 per year $1,930 per month

4 $27,938 per year $2,328 per month

5 $32,713 per year $2,726 per month

6 $37,488 per year $3,124 per month

7 $42,263 per year $3,522 per month

8 $47,038 per year $3,920 per month

For each additional person, add $4,775 per year $398 per month

Notes: Federal Poverty Guidelines: "2011 Poverty Guidelines for the 48 Contiguous States and the District of Columbia" as published in the Federal Register of January 20, 2011,, Volume 76, Number 13, pp. 3637-3638 The State of Georgia currently requires a not-for-profit provider to be charitable to maintain tax exemption and to have Certificates of Need (CONs) considered. Charitability is deemed to be indigent and charity write offs to equal or exceed 3% of adjusted gross revenue. The purpose of an indigent and/or charity care program is to provide financial relief or assistance to those who are unable to meet their financial obligation to the healthcare facility. Although programs and policies will vary between hospitals, there are some overriding guidelines that are generally accepted by all healthcare providers. 1) Eligibility - Patient eligibility may be based upon the following:

A. All inpatient and outpatient accounts exceeding a pre-determined level, say $500 or $1,000, are eligible for applying for financial assistance - indigent/charity care. An application must be completed by the patient/guarantor.

Chapter 5 – FINANCIAL ASSISTANCE PROGRAMS, continued

B. The application should include:

Income from all sources, listing, at a minimum, gross income for the most recent three-month period. Some providers may require additional documentation such as W2 for prior year.

Resources from savings and checking accounts, certificates of deposit, stocks, bonds, real estate, etc

Assets including homes, cars, boats, and any other vehicles, or assets

Monthly expenses

Number of dependents

A copy of the most recent federal income tax forms C. All third-party resources and non-hospital financial aid programs, including public assistance available through Medicaid, must be exhausted before financial assistance can be approved. D. Deductible and coinsurance amounts may be eligible for assistance if financial circumstances warrant. E. Some hospitals do not allow financial assistance applications after an account has been sent to legal counsel for collection.

2) Program Administration - The financial assistance (indigent/charity) program should be administered according to the following guidelines:

A. The application information, along with the federal income tax forms, should be reviewed and verified by a Financial Counselor or authorized person B. After reviewing income and expenses, the Financial Counselor or authorized person should determine if the patient/guarantor qualifies for financial assistance based on an Income and Assets Guideline Worksheet. A specific worksheet for use by Financial Counselors will ensure that all patients are assessed using the same criteria and represents a best practice

If the patient/guarantor qualifies for 100 percent write-off, he or she should be notified and the balance of the account should be written off per the facility‘s procedures