Embed Size (px)

Citation preview

CC&G

Your global Post Trade partner

“CC&G prides itself on the robustness of its clearing platform, enabling our clients to conduct their business safely, securely and with confidence in our full service offering.”P. Cittadini, CEO of CC&G

01 CC&G / Your global Post Trade partner

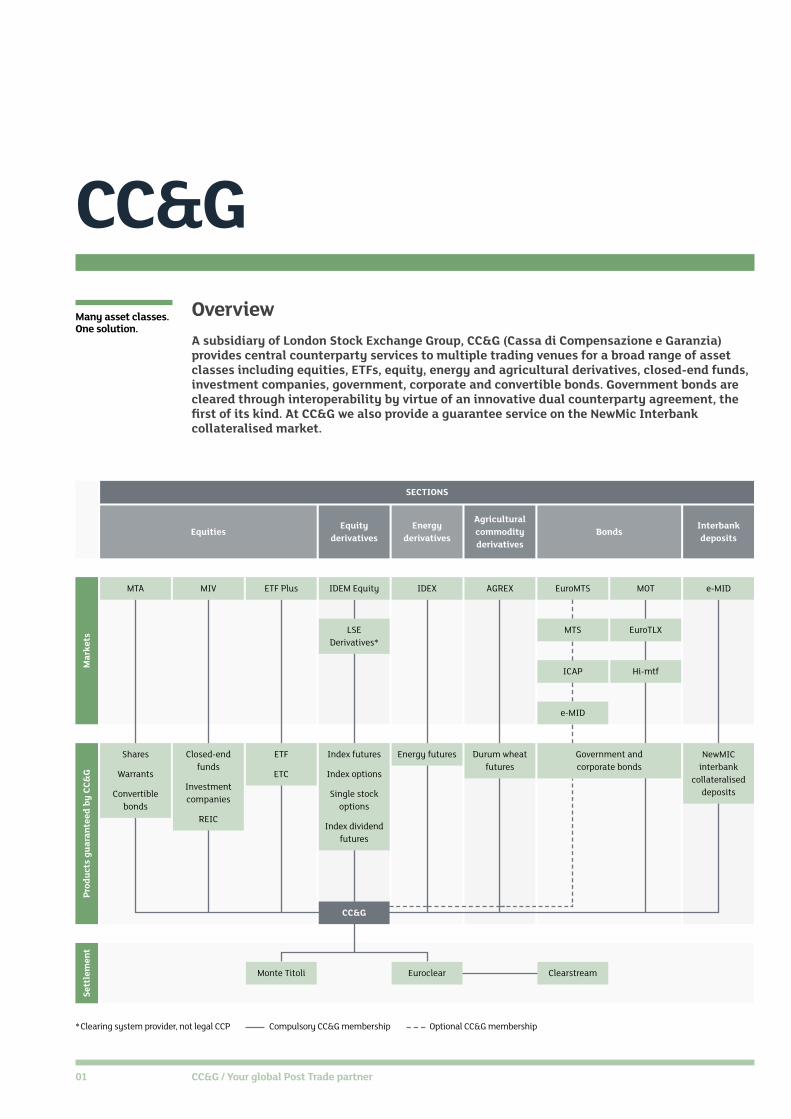

CC&GOverviewA subsidiary of London Stock Exchange Group, CC&G (Cassa di Compensazione e Garanzia) provides central counterparty services to multiple trading venues for a broad range of asset classes including equities, ETFs, equity, energy and agricultural derivatives, closed-end funds, investment companies, government, corporate and convertible bonds. Government bonds are cleared through interoperability by virtue of an innovative dual counterparty agreement, the first of its kind. At CC&G we also provide a guarantee service on the NewMic Interbank collateralised market.

Many asset classes. One solution.

Prod

ucts

gua

rant

eed

by C

C&G

Sett

lem

ent

MTA e-MIDMIV ETF Plus IDEM Equity IDEX EuroMTS MOT

EquitiesInterbank deposits

Equity derivatives

Energy derivatives

Bonds

LSE Derivatives*

MTS EuroTLX

ICAP

Mar

kets

SECTIONS

* Clearing system provider, not legal CCP Compulsory CC&G membership

AGREX

Agricultural commodity derivatives

Hi-mtf

e-MID

Shares

Warrants

Convertible bonds

Closed-end funds

Investment companies

REIC

ETF

ETC

Index futures

Index options

Single stock options

Index dividend futures

Energy futures Government and corporate bonds

NewMIC interbank

collateralised deposits

Durum wheat futures

CC&G

ClearstreamEuroclearMonte Titoli

Optional CC&G membership

An offering that keeps on growing

EMIRCC&G has remodeled its processes and risk management practices to provide its customers with an enhanced clearing service offering. On May 2014 CC&G has been deemed fully compliant to EMIR requirements to operate as CCP and to manage the interoperability link with LCH_CLearnet SA.

Renovated safeguarding frameworkCC&G has enforced the existing risk management practices to magnify the level of protection against counterparty risk. The new prudential framework accounts for a strengthened multi-level safeguarding system, including “skin in the game” resources, designed to better protect market integrity in case of a participant’s default. Cutting edge risk evaluation methodologies will further guarantee margin and default funds’ resilience under periods of stressed markets.

02–03 CC&G / Your global Post Trade partner

CC&G is an authorized Central Counterparty under the EMIR regulatory framework

Ahead of the regulatory evolution More functionalities

and safety

“CC&G clears the way to safety, in EMIR and beyond.”

Enhanced service offeringA brand new set of functionalities have been brought to life to broaden the range of clearing solutions for CC&G’s participants

— Multiple Account structure configuration: House account, Individual Segregated Account, Omnibus client Account and Additional Omnibus Account

— Segregation and Portability: segregation of positions into segregated accounts for accounting and guarantee purposes

— Extended list of eligible Sovereign Issuers of collateralizable securities: Austria, Belgium, France, Italy, Germany, Netherlands and Spain.

02–03 CC&G / Your global Post Trade partner

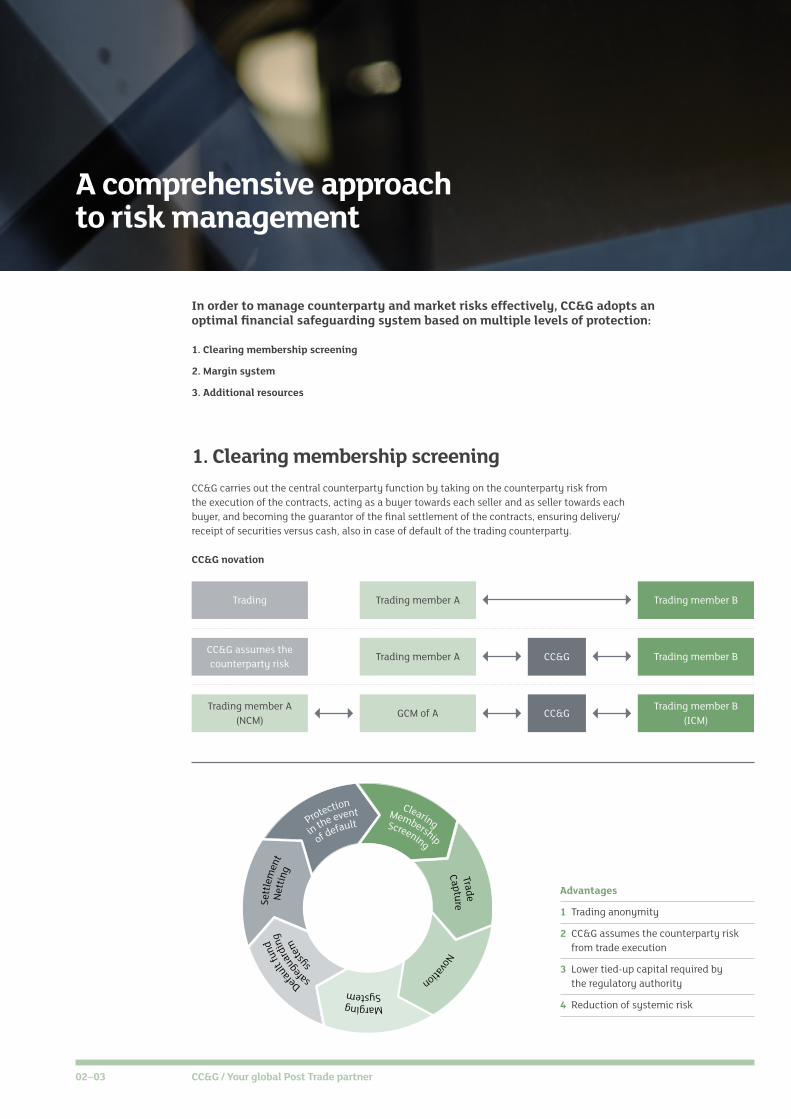

1. Clearing membership screeningCC&G carries out the central counterparty function by taking on the counterparty risk from the execution of the contracts, acting as a buyer towards each seller and as seller towards each buyer, and becoming the guarantor of the final settlement of the contracts, ensuring delivery/receipt of securities versus cash, also in case of default of the trading counterparty.

CC&G novation

Trading

In order to manage counterparty and market risks effectively, CC&G adopts an optimal financial safeguarding system based on multiple levels of protection:

1. Clearing membership screening

2. Margin system

3. Additional resources

Trading member A Trading member B

CC&G assumes the counterparty risk

Trading member A Trading member B

Trading member A (NCM)

GCM of ATrading member B

(ICM)CC&G

CC&G

A comprehensive approach to risk management

Novation

MargingSystem

safegua

rdin

g

Defaul

t fun

d

syste

m

Sett

lem

ent

Nett

ing

in the eventProtection

of defaultMembership

ClearingScreening

Trade

Capture

Advantages

1 Trading anonymity

2 CC&G assumes the counterparty risk from trade execution

3 Lower tied-up capital required by the regulatory authority

4 Reduction of systemic risk

04–05 CC&G / Your global Post Trade partner

i

3categories of membership

Clients may subscribe to CC&G as:

— General Clearing Member: GCMs become counterparties to CC&G for proprietary and client transactions; they can also clear contracts on behalf of their Non-Clearing Members.

— Individual Clearing Member: ICMs become counterparties of CC&G for proprietary and client transactions.

— Non-Clearing Member: NCMs are not counterparties to CC&G. They must be market members and must sign an agreement with a General Clearing Member for the provision of GCM services.

Who is eligible for membership?

— Banks and investment firms authorised to provide investment services in Italy

— Those authorised to provide such services subject to mutual recognition

— Other members of the markets guaranteed by CC&G who have signed the agreement with a GCM to become an NCM.

How to become a memberThe entire membership process for CC&G, Borsa Italiana and Monte Titoli is managed online via the BIt Club website, a simple, fast and efficient communication tool.

Multiple membership profiles

Membership requirements

Individual Clearing MemberGeneral Clearing Member

Supervisory capital (€) N. of Non-Clearing Members

25m Up to 1

30m From 2 to 5

35m From 6 to 10

40m Above 10

Only for Bond wholesale markets: supervisory capital at least equal to 400m.

CC&G accepts a guarantee for the difference between the supervisory capital requirement and the following minimum level of supervisory capital held: — €15m for sections other than the bond section— €200m for the bond wholesale markets.

Supervisory capital (€) Section

3m Equities

10m Derivatives

10m ICSD bond / Bond retail markets

10m X-COM

100m Bond wholesale markets

CC&G accepts a bank guarantee for the difference between the Supervisory Capital requirement and the following minimum level of Supervisory Capital held: — €3m for sections other than the Bond section— €50m for the Bond wholesale markets.

Banks or Investment Firms participating to X-COM Section may supply a bank guarantee also if their Net Capital is at least equal to € 5m

The participation to multiple Sections requires a Supervisory Capital at least equal to the greater of each individual Section’s requirement

“CC&G members must meet supervisory capital, organisational and technical requirements.”

Technical and organisational

— Organisational structure, technological and information technology systems— Two reference people for each section

— Hold a central cash account in Target 2

— Join the central depository system (CSD)

— Join the settlement services

Directly or through a settlement agent

NCM’s requisites

5proven systems for calculating margins

2. Margin systemThe margin system is CC&G’s fundamental risk management tool. Our risk management approach is fully compliant with international recommendations. On May 2014 CC&G obtained the authorization with unanimous opinion of the College of Regulators to operate as a CCP in full compliance of the EMIR requirements. Margins are calculated using sophisticated, proven systems for equity derivatives products; the Equity Risk Management (ERM) methodology for cash equity products; methodology for agricultural derivatives (MMeG) and the method for portfolio valuation (MVP) methodology for Italian government bonds.

Equity derivatives and cash equity margin calculationThe methodologies used for equities and equity derivatives are integrated and correlated, and are therefore capable of recognising the overall risk in a portfolio. This allows the offsetting of risk between closely correlated products, as well as cross-margining between derivatives and equity cash products in the portfolio. The overall risk exposure for

integrated portfolios with significant price correlation is determined by:

— Product Group: an integrated portfolio of underlying assets with statistically significant price trend correlation

— Class Group: an integrated portfolio of cash and derivatives instruments related to the same underlying stock.

Energy derivatives margin calculationDerivatives contracts traded on IDEX form an integrated portfolio considered as a whole for the purpose of Initial Margins calculation. The MMeL margining methodology has a structure of classes which groups all the contracts of the same type (futures or options) with the same underlying security (PUN) and the same characteristics (delivery period and type of supply: baseload, peakload or off-peak).

04–05 CC&G / Your global Post Trade partner

RomeAdvantages

1 Full flexibility in the choice of membership type per market cleared

2 International CC&G client base of more than 150 clearing members

3 Over 80 direct members, including major international players as GCMs

Members of both the cash equity and equity derivatives sections of CC&G benefit from a significant decrease in initial margin requirements thanks to our unique cross-margining function.

06–07 CC&G / Your global Post Trade partner

Bonds margin calculationMVP determines the overall risk exposure for integrated portfolios by grouping classes of bonds with statistically significant correlation in their sensitivity to interest rate variations, measured by duration. A single net position is calculated independently from the market origin of the contracts – MTS, EuroMTS, BrokerTec, MOT or EuroTLX – and risk management is accordingly performed on the net positions.

Agricultural derivatives margin calculationDerivative contracts traded on AGREX are aggregated in integrated portfolios, evaluated unitarily and consequently subjected to an aggregated calculation of initial margins. The MMeG margining methodology foresees a class structure capable of classifying the contracts which are actually traded on the market plus additional classes for managing delivery positions.

Initial marginInitial margin is called on a daily basis to cover the theoretical costs of liquidation, which CC&G would incur in the event of a member’s default, in order to close the open positions in the worst possible market scenario within a maximum price variation range called ‘Margin Interval’. The specific Margin Interval for each financial instrument is periodically reviewed on the basis of statistical analysis.

Advantages

1 Cross-margining between cash equity and equity derivatives significantly reduces margins, with optional separate calculation reporting to satisfy customers’ cost allocation needs

2 One collateral pool: guarantees in place cover the cash call on all asset classes

3 Members trading the same asset classes on multiple trading venues cleared by CC&G can take advantage of full netting for settlement and margining purposes

4 Customer can choose the number of accounts/ sub-accounts on derivatives and net/gross margining between main and sub-accounts.

Intraday marginIntraday margins are called by CC&G in case of sudden sharp price variations or an excessive increase in a member’s overall risk exposure. Intraday margin is calculated with the same methodologies as the initial margin.

CollateralInitial margin can be placed in cash (Euro) or in Euro denominated securities: Austrian, Belgian, Dutch, French, Italian, German and Spanish government bonds traded on MTS and EuroMTS. Up to 50% of the total Initial Margin requirement can be deposited through securities, with an overall 45% total IM limit on a single issuer.

Government bonds are marked to market on a daily basis. The bonds deposited as collateral are grouped in classes of haircut based on their duration. Intraday margins must be deposited in cash (Euro).

“Margins are evaluated according to cutting-edge risk management practices, in order to ensure the highest levels of protection with the minimum collateral requirement.”

Multiple levels of protection

1collateral pool for all asset classes

Maximun 45% of assets form a single issuer over total Initial Margin

Minimun 50% of cash over total Initial Margin

Austria

Belgium

Netherlands

France

Italy

Germany

Spain

Finland

Max 50%

Cash

Assets

Min 50%

Ireland

Unfunded default fund

CCP capital except regulatory plus threshold

Outstanding default fund

Skin in the game

Defaulter's contribution to the default fund

Guarantees deposited by the defaulter

Multi-level safeguarding system

Service closure-cash settlement with loss sharing (reduction

of payouts)

06–07 CC&G / Your global Post Trade partner

3. Lines of defenceCC&G manages four separate default funds: one for equity and equity derivatives, one for energy derivatives, one for fixed income and one for agricultural derivatives. These default funds fulfil an essential role as additional protection to cover any risks associated with sharp price/interest rate movements. Initial default fund contributions are calculated based on the results of periodic stress tests. Default fund contributions are re calculated on a monthly basis based on the previous month’s activity.

Multilevel financial safeguarding systemIn the event of default by a clearing member, CC&G protects market integrity by using a set of financial resources derived from the following:

a Margins and defaulting participant’s default fund contribution

b CC&G’s own resources as skin in the game measure

c Other participant’s default fund contributions

d Additional CC&G’s Capital resources

e Further loss sharing among participants according to their contribution to the default fund.

In case of default of a participant, market integrity is preserved by a multi tiered financial safeguard system.

Advantages

1 Optimal protection for members in times of stressed markets

2 In case of default by a clearing member, the maximum exposure of each clearing member is limited to his contribution to the relevant default fund

4separate default funds

“Default funds are established to ensure the stability of the system in the event of members’ simultaneous defaults under extreme but plausible conditions. Periodic stress test are performed to evaluate the Exposure of Participants in different historical and hypothetical scenario, in order to gauge the required amount of Default Funds.”

Multiple sources of finance to protect market integrity

Capped CM's loss sharing

CC&G own assets

Defaulter's assets

Discretional

08 CC&G / Your global Post Trade partner

Alltrades settled on a net basis

CC&G and settlementCC&G has a direct account in the Express II settlement system managed by Monte Titoli and in Euroclear to settle on net basis securities traded on several markets cleared. Net balances against CC&G can be split into partials in the net settlement cycles, and are subject to being parcelled into smaller lots prior to being submitted to the gross settlement cycle. Since October 2013, CC&G has extended its clearing services to Corporate and Government Bonds traded on EuroMOT, ExtraMOT, Hi-Mtf and EuroTLX markets, which are settled in Euroclear and Clearstream.

CC&G automatically manages buy-ins and sell-outs according to published rules. We have introduced additional reporting to highlight the separate margining of fails and partials, and to report the buy-in and sell-out process.

Advantages

1 Settlement of net balances against CC&G is prioritised over non-CCP guaranteed and ‘off-exchange’ trades

2 For settlement purposes, one single balance per security and account is created for Italian government bonds independently of the trading venue: MTS, EuroMTS, BrokerTec, MOT, EuroTLX and Hi-mtf.

Real-time post-trade management made easyFor accessing the clearing system, CC&G offers a range of flexible connectivity solutions to suit the needs of all clearing members.

1. Derivatives clearingBCS, the user interface, integrates all derivatives clearing functionalities – such as early exercise, international give-up combined with the splitting facility, position transfer and related enquires – into a single technical infrastructure. It also enables the download of clearing reports and data files used to support clearing on the derivatives market. BCS, fully integrated with the IDEM market infrastructure, is available in the following versions:

— BCS-WS: a stand-alone windows workstation

— BCS-API: an Application Program Interface to automate the end-to-end processing of transactions

— BCS PLUS, both WS and API, allows the automation of the international give-up.

International give-up business modelContracts executed on the IDEM market can be transferred on trade date at the execution price. This functionality, combined with the trade splitting facility, fully complies with the international uniform give-up agreement and allows STP into the middle and back office systems.

2. ReportingA wide range of reports and data files is available to allow for quick reconciliation of transactions, positions and margins. ICWS enables the download of clearing reports, fails reporting and data files to support clearing on all markets. FTP, FTPS and SFTP are available for all markets to download batch files, with different levels of security.

Advantages

1 General Clearing Members benefit from a complete Non-Clearing Member post-trading report for reconciliation purposes

2 BCS PLUS automates international give-up management

3 General Clearing Members can monitor the trading activity of their NCMs throughout the business day.

General Clearing Members benefit from a complete Non-Clearing member post-trading report for reconciliation purposes.

3versions of the user interface available

“Give-up functionality combined with trade splitting is available as a complete STP model.”

Contacts

CC&G – Cassa di Compensazione e GaranziaPiazza degli Affari, 6 20123 Milano – Italia

Via Tomacelli, 146 00186 Roma – Italia

Telephone+39 02 72426 504+39 02 33635 283

This publication contains text, data, graphics, photographs, illustrations, artwork, names, logos, trade marks, service marks and information (“Information”) connected with CC&G S.p.A. (“CC&G”) or “The Company”). CC&G attempts to ensure Information is accurate, however Information is provided “AS IS” and on an “AS AVAILABLE” basis and may not be accurate or up to date. Information in this publication may or may not have been prepared by CC&G but is made available without responsibility on the part of CC&G. The Company does not guarantee the accuracy, timeliness, completeness, performance or fitness for a particular purpose of the publication or any of the Information. No responsibility is accepted by or on behalf of CC&G for any errors, omissions, or inaccurate Information in this publication. No action should be taken or omitted to be taken in reliance upon Information in this publication. We accept no liability for the results of any action taken on the basis of the Information. The Company promotes and offers the post-trading services in an equitable, transparent and non-discriminatory manner and on the basis of criteria and procedure aimed at assuring interoperability, security and equal treatment among market infrastructures, to all subjects who so request and are qualified in accordance with national and community legislation, applicable rules and decisions of the competent Authorities.

© March 2015 CC&G S.p.A. – London Stock Exchange Group All rights reserved. CC&G S.p.A. Via Tomacelli, 146 – 00186 Roma (Italy) www.ccg.it