Embed Size (px)

Citation preview

Semi-AnnualPublication

Fall 2002

Volume XX

FIGHT WITH FEEDBACK

CONSTRUCTION CONTROLSPRESIDENT'S MESSAGE

2002 FALL CONFERENCE

INSIDE THIS ISSUECCIA OFFICERS

2002-2003

PresidentMr. Richard Pagel, CIACoast CCD(714) [email protected]

First Vice PresidentMr. John HowardVictor Valley CCD(760) 245-4271 (Ext. 2284)[email protected]

Second Vice PresidentMr. Reuben JamesCompton CCD(310)900-1600 (Ext. 2110)[email protected]

SecretaryMs. Jane Chawinga, CPAYosemite CCD(209) [email protected]

TreasurerMr. Cory Wathen, CPALos Rios CCD(916) [email protected]

PublicationsMr. John Thompson, CPARancho Santiago CCD(714) [email protected]

Past PresidentMs. Judith Vroman, CPA,CIA, CFEContra Costa CCD(925) 229-1000 (Ext. 1228)[email protected]

AdvisorMr. John Shaffer, CIA,CFEPeralta CCD(510) [email protected]

A Publication of the Community College Internal Auditors (CCIA)

Business Advisor

CCIA WEBSITE GIVE UP SOME CONTROL

Community College Internal AuditorsFall Conference

October 3-4, 2002Chancellor's Office - Sacramento, CA

Legal Aspects of Bond Funds - John Hartenstein, Attorney at Law, Orrick, Herringtonand Sutcliffe, a bond counsel firm will cover post issuance legal issues. Some of thetopics to be addressed include: federal tax arbitrage, rebate compliance, investment offunds, use of bond proceeds and interest earnings, and continuing disclosure - i.e. postissuance securities law compliance.

Construction Management - Timothy Murchison J.D., Senior Vice President, 3DInternational, will provide a general overview of Construction Management topics. Some ofthe topics will include: the construction process (responsibilities, critical path, timedelays, change orders); prebid strategies for minimizing construction problems and costs;and guidance to avoid problems on construction projects.

Construction Audits - Scott Jones, General Manager, PinnacleOne, a constructionconsulting and management firm, will address the internal auditor as a positive player inthe construction process. All too often, auditors are viewed as "the ones who come inafter the war is lost and bayonet the wounded." Mr. Jones will discuss how internalauditors can be proactive in the process of construction and assist in the overall costcontrol and success of a project, from budgeting, through change order negotiation, andproject close-out.

State Capital Outlay and Local Assistance Programs - Paul Barth and Cheryl Larry,Program Managers, California Community Colleges Chancellor's Office, will give anoverview of the project selection process and reimbursement guidelines for capital outlayand local assistance (i.e. Scheduled maintenance and Hazardous Substance) programs.

Bookstore Operations: Mark Freed, CSP Orange Coast College Bookstore, and JimLadd, Foothill & DeAnza Bookstores, will present on Bookstore Operational issues. Theseseasoned professionals will cover areas such as inventory control methods, contracted vs.district operated bookstores, working with book wholesalers and buyback contracts, andother operational issues facing today's bookstores.

Vending Commission and Auxiliary Audits – Jane Chawinga, CPA, Yosemite CCD,Judy Vroman, CPA, CIA, CFE, Contra Costa CCD, and Richard Pagel, CIA, CoastCCD, will present an overview of their procedures and findings on vending commission andauxiliary operations audits. Audit recommendations resulted in $17,000 in back duevending commission revenue as well as corrected commission rates and improved cash/inventory controls and information security for auxiliaries.

1

*Name Change*Judy Osgood is now

Judy Vroman due to herrecent wedding.

Congratulations Judy!

NEWCCIA Website

The Mission of CCIA is to:

1. Encourage cooperativerelationships among com-munity college internal au-ditors;

2. Promote and encouragethe establishment of internalauditing functions withincommunity colleges, andencourage the adoption ofthe Standards for the Pro-fessional Practice of Inter-nal Audit;

3. Provide members withquality training and continu-ing professional education;and

4. Keep members informedon current issues.

Community College

Internal Auditor

President's Message

As the 2001/2002 financial year comes to a close, we look backon a year of experiences that truly build character and community. Overthe past twelve months our community has grown stronger as our free-doms have been challenged and corporate ethics questioned. As Accoun-tants, Auditors, Controllers, and CFO's we realize that our ethical busi-ness conduct is essential to keeping the trust of our communities andsetting the example for our students. Trust is important as many of ourDistricts look to our local communities to support future bond issues.

For the Fall 2002 Conference, the CCIA board has gathered agroup of professionals to speak about bonds, construction, and auxiliaryoperations. The topics on the agenda will impart valuable knowledge toall of us as we reinforce our community college infrastructures and lookto the challenges of our next fiscal year. To contribute to our mutualmission and provide increased resources to our members, the CCIAboard has moved to develop a website. A primary objective of thewebsite is to improve communication throughout our community collegesand provide a point of reference for the CCIA. I would encourage all ofyou to utilize both the conference training and website to assist in thecultivation of our community colleges. I look forward to seeing you allin Sacramento at the Chancellors Office for the 2002 Fall Conference.

Richard Pagel, CIA

2002 FALL CONFERENCE

CHANCELLOR'S OFFICESACRAMENTO, CA

OCTOBER 3-4, 2002

The CCIA board isexcited to announce

the new CCIAWebsite.

www.theccia.orgWe encourage all of

our colleagues tobookmark the websiteand check in for con-

ference highlights,resource links, and

contact information.Website hosted by Contra Costa

Community College District

2

Give Up SomeControl

Fighting MisconductWith Feedback

An estimated $600 billion will be lost in 2002 as a result of

occupational fraud and abuse.

This alarming figure comes from the Association of Certified Fraud Examiners’(ACFE) 2002 Report to the Nation. With these projections, the report confirmsthe prevalence of unethical and illegal workplace activity and indicates that it is stilllargely underreported.

By not taking a proactive approach to reporting this activity, some of America’slargest companies have left themselves open to catastrophic, high-profile lawsuits,bottom line losses and permanent damage to their reputations. That’s why it’s criticalto implement strategies that focus on detection and prevention.

Reducing your organization’s exposure is an attainable goal, and the first step ismaintaining awareness of workplace activity. This approach gives you the informa-tion you need to identify theft, fraud and other misconduct and take action before itcauses further damage.

The question is how to obtain such information. According to the Report to the Nation, the majority of it comes fromtips or feedback from an organization’s own employees. One solution for gathering that feedback is implementing a systemsuch as a hotline for employees to confidentially report incidents or concerns.

The Hotline AdvantageWhen your employees have a way to report problems such as theft and fraud, they become active participants in

prevention and detection efforts, so your organization takes a proactive, rather than reactive posture to misconduct.Because a hotline makes misconduct much easier to report, employees are less likely to violate laws and organizationalpolicies. With such a system in place, your organization is better equipped to detect problems, react quickly, investigateincidents and take corrective steps to reduce loss. In fact, the Report to the Nation shows organizations that have fraudhotlines actually reduce their losses by about 50% per scheme.

The case of PPG Industries in Pittsburgh is just one example of a hotline’s effectiveness. An anonymous tip called in totheir ethics hotline in 2001 launched an investigation that uncovered evidence of an employee who had been embezzlingfrom the company for an extended period of time. The accused employee was convicted, and the company received$240,000 in restitution.

By not taking a proactive approach some of Americaís largest companies haveleft themselves open to permanent damage to their reputations.

When correcting employ-ees' mistakes, offerchoices. Instead of tellingthem what to do, give twoalternatives, either one ofwhich will meet your needsand the organization'sgoals. They'll feel more incontrol if they make achoice.

Example: "Wouldyou rather run your reportsthrough spell-check to catchthose errors or have Jimproofread behind you?"

copyright 2002Manager’s Edge

reprinted with permissionwww.briefings.com

See FEEDBACK on page 4

3

According to theConstruction Indus-try Institute's "As-sessment of OwnerProject Manage-

ment Practices andPerformance" sur-vey, about one out

of every three

Education & AwarenessBut a hotline alone will not solve all of your

organization’s woes. The Report to the Na-tion concludes that any serious effort at con-trolling fraud and other misconduct dependson an organization’s employees. It furtherstates that employees who receive regular andrecurring training about the detrimental aspectsof fraud are more likely to aid in controlling it.

To that end, ongoing employee educationis another important tool in preventing unethi-cal or illegal activity. Materials such as post-ers, signage, brochures and other ongoingforms of communication are necessary to pro-mote the hotline and educate employees onorganizational standards and expectations.

Gathering employee feedback doesn’t justmake good business sense, it’s an essentialstep any organization can take in the fightagainst unethical or illegal activity. Implement-ing an anonymous reporting system like ahotline can significantly improve their abilityto limit losses and get their employees involvedin meeting their goals for preventing miscon-duct and establishing a more ethical and prof-itable workplace.

Because more organizations are realizingthe benefits of hotlines, this reporting methodis quickly becoming a standard tool of busi-ness. But if a hotline is operated internally, em-ployees are less likely to use it for fear of ret-ribution. As a result, many organizations arechoosing to outsource their hotlines to third-party professionals like The Network.

The Network combines 24-hour, 365-dayissue-specific employee hotlines with pro-grams for employee education and awareness.They focus on helping organizations gather in-formation on problems such as theft and fraudand educating employees on the right behav-iors and preventive techniques to prevent mis-conduct.

Mary L. HughesProgram Manager,

Business DevelopmentThe Network, Inc.

(800) 253-0453 ext. 6648

FEEDBACK continued from page 3

See CONSTRUCTION on page 5

Building Controls IntoCapital

ConstructionConstruction projects offer fertile groundfor internal auditors to provide increasedservice while meeting the new profes-sional requirements of risk mitigation andcontrol assurance.

Capital construction projects can create significant exposure fororganizations that are unaware of the risks associated with excessivecost, project delay, and quality issues. According to a constructioncontract audit survey reported in the February 1999 issues of Internal

Auditor, less that half of the internalauditors whose companies regularlyenter into construction contracts ac-tually examine compliance issues andthe propriety of construction costs.Yet, the future of many companies of-ten rides on completing a capital ex-pansion on time, with sufficient qual-ity, and within budget. With so muchat stake on multimillion and sometimesbillion dollar-plus constructionprojects, management needs the in-

ternal control design and independent project appraisals that internalauditors can provide.

Monitoring Project ProgressArchitects, engineers, and contractors are typically rewarded for

surfacing cost, quality, and other issues that are important to the projectowner. Independent project controls are needed to ensure the owner'sinterests are protected. Even if a project management firm is retainedto oversee or monitor construction, project controls are necessary toensure that the underlying cost and schedule data are sufficient andreliable; the on-site construction status is observed and documented;and the architects, engineers, and contractors address technical issues.

4

If a project lacks these controls, it could easily accu-mulate a mountain of change orders because no one in thecompany knows enough about the project to resolve them.Additionally, costs charged to the job may exceed avail-able funding -- a huge embarrassment. Worst of all, theproject may not fulfill the organization's needs, and thecompany's facilities and maintenance departments may needto take remedial action at additional cost to the organiza-tion. Protracted and costly litigation may ensue, as thecompany seeks to recover damages from the architects,engineers, and contractors. Unfortunately, the company'scase will likely be weak because its attorneys lack inde-pendent data about the project from the owner's perspec-tive.

But this scenario could be avoided if the organization'sinternal auditors are fully engaged in examining issues ofcost, compliance, and management controls from projectinception. In the construction contract auditing survey, 90percent of the internal auditors performing construction costaudits found significant overcharges. Additionally, accord-ing to the Construction Industry Institute's "Assessment ofOwner Project Management Practices and Performance"survey, about one out of every three projects is over bud-get or behind schedule.

CONSTRUCTION continued from page 4

See CONSTRUCTION on page 6

In assessing projectcontrols, internal

auditors should deter-mine whether projectmanagement, costengineering, and

finance personnel areexperienced and well-

trained.

OvOvOvOvOverererererall Prall Prall Prall Prall ProjectojectojectojectojectContrContrContrContrControlsolsolsolsols

This check list will help auditors ensure that overall con-struction management controls are in place to protect theowner's interests.

√ Cost and schedule processes, procedures, and manage-ment systems are defined and documented.

√ Appropriate contractor selection methods are in placeand have been correctly applied, taking advantage ofcompetitive bidding opportunities where possible.

√ Where appropriate, there has been an independentassessment of project design and related costs.

√ Management has approved a contract scope thatmatches the project design and functional requirements.

√ Value engineering has been performed to ensure that theproject design comports with functional, operational, andmaintenance requirements.

√ A master project schedule has been developed withmilestones that are consistent with project requirements.

√ A project work-breakdown structure has been developed,assigning budgetary and schedule authority, and is used asthe basis for the master project schedule in appropriatedetail.

√ A project budgeting process has been implemented atthe same level of detail as the project cost accounting toensure relevant and reliable management reporting duringconstruction.

√ Processes are in place to verify or assess for reason-ableness supporting documentation backing contractorbillings.

√ Document control processes have been established forarchitectural and engineering programs, developmentalstudies, and project designs and to track contractorchanges in the as-built documents.

√ A procedure is in place to independently assess anddocument, in sufficient detail, the status of site conditionson a periodic basis.

Project completion delayed 12 months, causing $150 million of new revenue to be foregone.Excessive change order charges costing $4.5 million on an $8 million contract.Direct labor overcharges of $2.3 million.Inappropriate worker' compensation insurance costing $12 million.Duplicate payments of $4 millionRemedial work of $3 million following termination of the prime contractor, and legal fees of $1 million defendingthe termination.

A few examples of the kinds of "surprises" the authorshave observed firsthand over many years in the businessinclude:

5

CONSTRUCTION continued from page 5

Most of these problems could be avoided if the ownerbetter understood project risk and applied appropriateconstruction project controls.

Addressing Project RiskThere are a variety of risk and control issues that can

adversely affect a capital construction project.Unclear or multiple channels of direction from the

owner and management can produce excessive require-ments and scope creep.

Owner-caused design errors or project delays canresult in excessive change-order costs, claims, disputes,and budget management issues.

Design and construction quality defects can causeunmet occupant requirements and excessive lifetime main-tenance costs.

Insufficient project staffing may impede the deliveryof projects on time and within budget.

Ineffective project management systems can hamperproject monitoring and construction oversight.

Inaccurate financial records and reports, as well asloose monitoring of contractor financial controls, can resultin costly practices and overcharges.

Insufficient insurance may lead to gaps in property andcasualty loss coverage. Alternatively, insurance premiumsmay be excessive given the actual project risk.

Addressing construction project exposures need notbe a daunting task. Exposure in any business environmentis the amount of risk that remains given the nature and ex-tent of the controls in place. With the right controls, projectexposure declines to the point at which the cost of the con-trols is less than or equal to the benefits expected to bederived - an internal audit concept known as reasonableassurance.

Companies entering into capital construction contractsshould implement controls that provide reasonable assur-ance of mitigating cost, schedule, and technical risk to animmaterial level. A minimal variance of no more than 5percent from the intended objective in each of these threeperformance categories is typical.

Generally, the functions or processes that require thegreatest project control given the risk involved are:

Construction contracting methodChange order managementSafety, risk, and insuranceFinance, budget management, and reportingMaterials, labor, and overhead cost accountingsystems, including rental equipmentProject close-out and acceptance proceduresOverall internal project control structure

See CONSTRUCTION on page 7

KKKKKeeeeey Changy Changy Changy Changy Change Ore Ore Ore Ore Order Prder Prder Prder Prder Process Controcess Controcess Controcess Controcess ControlsolsolsolsolsThis check list will help ensure that only valid and necessary change orders are authorized and that change order pricingis appropriate.

Contract specifications, knowledge of site conditions, required owner-contractor communications, and subcontractor scheduling and coordination are suitable to prevent or minimize contract change orders.

The contractor is required to submit full explanations and documented cost, schedule, and technical support forcontract change proposals.

The change-order process provides for appropriate owner-management reviews of contractor change proposalsbased on an independent assessment of technical specifications, design documents, and related costs.

Owner and management representatives regularly monitor the construction site and document their observationsof project status to clarify and support the owner's position in contract disputes as construction progresses.

The owner has retained qualified staff capable of isolating and evaluating the cost of contractor change proposalsin light of the original project scope and contract specifications.

Approved contract change orders are documented in contract amendments, including appropriate revisions to thecontract value, and all parties have executed them.

6

Assessing Project ControlsInternal Auditors should review management's plans

for a project control structure before construction begins(see "Overall Project Controls Checklist"). The Commit-tee of Sponsoring Organizations of the TreadwayCommission's (COSO) control environment factors aregood criteria for auditors to use in this assessment.

In assessing project controls, internal auditors shoulddetermine whether project management, cost engineering,and finance personnel are experienced and well-trained.The ability to transition the project from the contractor tothe owner and management is crucial. The owner and con-tractor should predetermine, in writing, how this will beaccomplished.

Flexibility is required to match construction require-ments with the cost efficiencies needed to achieve budgetgoals. Contingency planning is therefore essential, and fund-ing should be reserved and controls established for thispurpose. Outside technical specialists, such as construc-tion management advisors, construction consultants, andindependent engineers, also should be considered to bol-ster project management staff and to provide technical ex-pertise if litigation ensues. Additionally, internal auditorsshould review contractual provisions covering liquidateddamages due to contractor nonperformance.

Given the litigious nature of the construction industry,the safety program, bonding, and insurance plan must bewell thought out and documented. Internal auditors shouldevaluate the plan for cost versus risk trade-offs, the ad-equacy of insurance coverage based on the exposure pre-sented, and the efficacy of the management controls in placeto mitigate risk.

At a minimum, bonding and insurance levels need tobe assessed in terms of the organization's appetite for risk.Internal auditors also need to confirm that the plan has beenreviewed with senior management and that appropriateauthorizations have been obtained.

CONSTRUCTION continued from page 6

We Want to Hear fromYOU!

We are eager to hear from you!Please send us any news that wouldbe of interest to your colleagues.

Have you read anything of interestsuch as audit findings, fraud findings,interesting books or articles? Isthere a particular experience thatwas successful or not so successfulthat you wish to share?

Send articles to: Rancho SantiagoCommunity College District, 2323North Broadway, Santa Ana, CA92706-1640.Attention:John Thompson, Internal Auditor

On large construction projects, an owner-controlledinsurance program often replaces traditional contractor-supplied insurance - a form of self-insurance. Organiza-tions often choose this type of program to gain better cov-erage of the assessed construction risk or to realize theperceived cost savings of lower insurance premiums. Al-though the potential benefits are attractive, the risks tendto increase proportionately as project management leanstoward sacrificing coverage--perhaps inadvertently--forcost reduction. It is an approach that warrants heavy scru-tiny by the internal auditor.Dennis Applegate, CIA, CPA, CMA, CFM,The

Boeing Co.Curtis Matthews, CPA, CISA, CCEA,

Pricewaterhouse Coopers LLPThis article was reprinted with

permission from the June 2002 issue ofInternal Auditor, published by

The Institute of Internal Auditors, Inc- www.theiia.org

7

2002 FALL ConferenceState Chancellor's Office - 1102 Q Street, Sacramento

October 3rd and 4th, 2002

From the Bay Area:

I-80 East to Hwy 50/Bus 80Exit I-5 north to ReddingExit Q Street

Directions and Parking

From the Airport:

I-5 SouthExit Q StreetEast on Q Street

2 Parking Garages At:

10th & P (between O & P) $12.00/day

11th & 12th (between O & P)$12.00/day

Hotel AccommodationsVagabond Inn909 Third StreetSacramento, CAOne Person - $79.00Additional Person - $10/dayAsk for CCIA RatePhone (916) 498-1101

Conference participants are encouraged to book room reservations early in order to insure a room

2002 Fall CCIA Conference - Confirmation NoticeFees and Deadlines:

$85.00 - Single Attendee paid by Sept. 20, 2002$75.00 - Multiple Attendees from a District paid by Sept. 20, 2002$95.00 - Any attendee paid after Sept. 20, 2002$30.00 - Materials Only

Refunds: Must be requested in writing 7 days prior to conference.

To Register: 1) Contact Cory Wathen at (916) 568-3083 or [email protected]) Make Checks payable to: Community College Internal Auditors3) Return this confirmation notice and registration fee to:

Cory Wathen, Los Rios Community College District1919 Spanos Ct., Sacramento, CA 95825

Yes, I am planning to attend. Enclosed is a check for $ _________________

Name

District Name

Phone Number

Name

District Name

Phone Number

Name

District Name

Phone Number

In order to have an accurate count for our caterer, please indicate the number of registrants attending lunch.October 3, 2002 Thursday How many will attend lunch? _______October 4, 2002 Friday How many will attend lunch? _______

Holiday Inn300 "J" StreetSacramento, CAOne Person - $119.00Additional person - $10Reserve by Sept. 11, 2002Ask for CCIA RatePhone (916) 446-0100

8

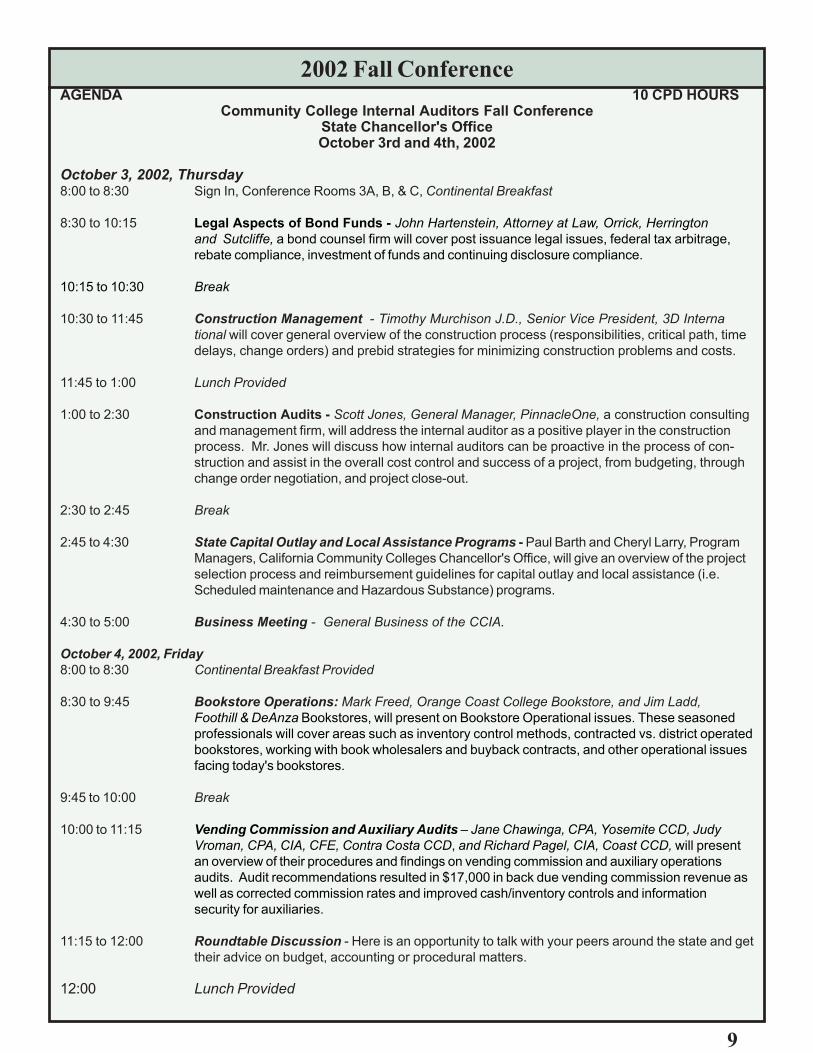

2002 Fall ConferenceAGENDA 10 CPD HOURS

Community College Internal Auditors Fall ConferenceState Chancellor's OfficeOctober 3rd and 4th, 2002

October 3, 2002, Thursday8:00 to 8:30 Sign In, Conference Rooms 3A, B, & C, Continental Breakfast

8:30 to 10:15 Legal Aspects of Bond Funds - John Hartenstein, Attorney at Law, Orrick, Herringtonand Sutcliffe, a bond counsel firm will cover post issuance legal issues, federal tax arbitrage,rebate compliance, investment of funds and continuing disclosure compliance.

10:15 to 10:30 Break

10:30 to 11:45 Construction Management - Timothy Murchison J.D., Senior Vice President, 3D International will cover general overview of the construction process (responsibilities, critical path, timedelays, change orders) and prebid strategies for minimizing construction problems and costs.

11:45 to 1:00 Lunch Provided

1:00 to 2:30 Construction Audits - Scott Jones, General Manager, PinnacleOne, a construction consultingand management firm, will address the internal auditor as a positive player in the constructionprocess. Mr. Jones will discuss how internal auditors can be proactive in the process of con-struction and assist in the overall cost control and success of a project, from budgeting, throughchange order negotiation, and project close-out.

2:30 to 2:45 Break

2:45 to 4:30 State Capital Outlay and Local Assistance Programs - Paul Barth and Cheryl Larry, ProgramManagers, California Community Colleges Chancellor's Office, will give an overview of the projectselection process and reimbursement guidelines for capital outlay and local assistance (i.e.Scheduled maintenance and Hazardous Substance) programs.

4:30 to 5:00 Business Meeting - General Business of the CCIA.

October 4, 2002, Friday8:00 to 8:30 Continental Breakfast Provided

8:30 to 9:45 Bookstore Operations: Mark Freed, Orange Coast College Bookstore, and Jim Ladd,Foothill & DeAnza Bookstores, will present on Bookstore Operational issues. These seasonedprofessionals will cover areas such as inventory control methods, contracted vs. district operatedbookstores, working with book wholesalers and buyback contracts, and other operational issuesfacing today's bookstores.

9:45 to 10:00 Break

10:00 to 11:15 Vending Commission and Auxiliary Audits – Jane Chawinga, CPA, Yosemite CCD, JudyVroman, CPA, CIA, CFE, Contra Costa CCD, and Richard Pagel, CIA, Coast CCD, will presentan overview of their procedures and findings on vending commission and auxiliary operationsaudits. Audit recommendations resulted in $17,000 in back due vending commission revenue aswell as corrected commission rates and improved cash/inventory controls and informationsecurity for auxiliaries.

11:15 to 12:00 Roundtable Discussion - Here is an opportunity to talk with your peers around the state and gettheir advice on budget, accounting or procedural matters.

12:00 Lunch Provided

9