Embed Size (px)

Citation preview

Bank of Canada staff discussion papers are completed staff research studies on a wide variety of subjects relevant to central bank policy, produced independently from the Bank’s Governing Council. This research may support or challenge prevailing policy orthodoxy. Therefore, the views expressed in this paper are solely those of the authors and may differ from official Bank of Canada views. No responsibility for them should be attributed to the Bank.

www.bank-banque-canada.ca

Staff Discussion Paper/Document d’analyse du personnel 2016-22

Central Bank Digital Currencies: A Framework for Assessing Why and How

by Ben S. C. Fung and Hanna Halaburda

2

Bank of Canada Staff Discussion Paper 2016-22

November 2016

Central Bank Digital Currencies: A Framework for Assessing Why and How

by

Ben S. C. Fung and Hanna Halaburda

Currency Department Bank of Canada

Ottawa, Ontario, Canada K1A 0G9 [email protected]

ISSN 1914-0568 © 2016 Bank of Canada

i

Acknowledgements

We thank Walter Engert, Theodoros Garanzotis, Grahame Johnson, Anneke Kosse, Scott Hendry, Tim Lane, Lukasz Pomorski, Francisco Rivadeneyra, Gerald Stuber, Maarten van Oordt, Warren Weber, Carolyn Wilkins and seminar participants at the Bank of Canada for helpful comments and suggestions. All remaining errors are our own.

ii

Abstract

Digital currencies have attracted strong interest in recent years and have the potential to become widely adopted for use in making payments. Public authorities and central banks around the world are closely monitoring developments in digital currencies and studying their implications for the economy, the financial system and central banks. One key policy question for public authorities such as a central bank is whether or not to issue its own digital currency that can be used by the general public to make payments. There are several public policy arguments for a central-bank-issued digital currency. This paper proposes a framework for assessing why a central bank should consider issuing a digital currency and how to implement it to improve the efficiency of the retail payment system.

Bank topics: E-money; Financial Services; Payment clearing and settlement systems JEL codes: E41, E42

Résumé

Les monnaies numériques suscitent un vif intérêt depuis quelques années et sont susceptibles d’être adoptées à grande échelle comme moyens de paiement. Les autorités publiques et les banques centrales de partout dans le monde surveillent de près l’évolution de ces monnaies et étudient leurs implications pour l’économie, le système financier et les banques centrales. L’une des questions de politique importantes qui se posent aux autorités publiques, notamment les banques centrales, est de savoir si elles devraient ou non émettre leur propre monnaie numérique, que le grand public pourrait utiliser pour effectuer des paiements. Plusieurs arguments de politique publique plaident en faveur d’une monnaie numérique émise par une banque centrale. Le présent article propose un cadre visant à déterminer pourquoi une banque centrale devrait envisager l’émission d’une monnaie numérique et comment celle-ci pourrait être mise en place pour améliorer l’efficacité du système de paiement de détail.

Sujets : Monnaie électronique; Services financiers; Systèmes de compensation et de règlement des paiements Codes JEL : E41, E42

1

1 Introduction

Rapid technological progress and new business models in recent years have resulted in many innovative products in retail payments. These innovations are increasing the potential for major changes in the retail payment environment, including the decreased use of cash.1 To effectively carry out their own main functions in a changing environment, central banks need to monitor new developments and study the implications closely. One of the most significant developments in recent years is the renewed interest in e-money.2 E-money developments and their implications were studied extensively in the early 1990s.3 Since then, the adoption of e-money products has been slower than expected both globally and in Canada. However, since 2009, innovations related to Bitcoin and its underlying blockchain technology have attracted strong interest in cryptocurrencies. These new generations of e-money, which are also often called digital or virtual currencies, are raising important questions for central banks, the financial system and the economy.4 For example, private digital currencies, if widely adopted for making payments, could substantially reduce the demand for bank notes and even chequing account deposits in banks. Therefore, it is important for central banks to understand the impact of these developments on their seigniorage revenue and monetary policy operations, on the safety and efficiency of payments systems, and on the policy for financial stability. Moreover, central banks should examine their own role in light of these developments, including whether to regulate digital currency or to develop their own digital currency. Central banks have a keen interest in monitoring developments in e-money, understanding their implications and establishing a view on the potential role of public institutions.5 A key policy question for central banks is whether or not to issue its own digital currency that can be used by the general public to make payments.6 In fact, there are two closely related questions:

(i) Why might a central bank choose to issue its own digital currency?

1 For a discussion of innovations in retail payments and their implications in a number of countries, see Committee

on Payment and Settlement Systems (2012). 2 E-money is broadly defined as monetary value stored in an electronic device that can be used to make payments.

For a more detailed discussion about recent developments and issues about e-money, see Fung, Molico and Stuber (2014). While there are some differences among the terms e-money, digital currency and virtual currency, for the sake of simplicity, we use them interchangeably in this paper.

3 For example, see Bank for International Settlements (1996), Freedman (2000) and Stuber (1996). 4 See, for example, Ali et al. (2014), Committee on Payments and Market Infrastructures (2015) and Wilkins

(2014). 5 For example, the Bank of Canada started its e-money research program in 2013 and has published a number of

research papers on its website. The main objectives of the research program are to (i) deepen the understanding of digital alternatives to cash and their likely evolution and pace of adoption; (ii) analyze the implications for the Bank of an increased reliance on these alternatives; and (iii) establish a view on the potential role of public institutions as e-money issuers, and the need for regulation of e-money schemes. For research published by Bank of Canada staff under this e-money research program, see http://www.bankofcanada.ca/e-money.

6 A central bank digital currency can be defined as monetary value stored electronically that is a liability of the central bank and can be used to make payments.

2

(ii) If a central bank were to issue its own digital currency, what should it look like? To answer the first question, a central bank would need to explore the public policy arguments for issuing its own digital currency and assess the effects on the economy, the financial system and the banks. For the second, a central bank would need to determine the design and characteristics of its digital currency, and the steps required to promote broad adoption. These two questions need not be answered in sequential order. For example, a digital currency’s design could affect its demand and its likelihood of being substituted for bank notes and bank deposits. Digital currency is an area that will continue to evolve in ways that cannot be fully anticipated today. For example, while Bitcoin has attracted much attention in recent years, the focus now is on the underlying blockchain technology. As such, the purpose of this paper is not to answer the two questions posed above but to propose a general framework to guide further thinking to address these questions. The framework should be general enough to be effective with today’s technology and with further technological advances. This paper is a first step in the research agenda on studying central bank digital currency. The rest of the paper is organized as follows. In the next section, we discuss three broad public policy arguments for a central bank to consider issuing a digital currency. Section 3 focuses on one particular policy argument—whether a central bank should issue a digital currency to improve the efficiency of retail payments. In Section 4, we discuss some of the main characteristics of such a central bank digital currency. The final section concludes. To simplify terminology, we refer to central bank digital currency as CBDC.

2 Why Should a Central Bank Consider Issuing a Digital Currency?

In this section, we consider three public policy arguments for why a central bank might consider issuing its own digital currency. First, a central bank may explore whether issuing a CBDC would improve the efficiency of its currency function. For example, as the sole issuer of bank notes in Canada, the Bank of Canada supplies bank notes that Canadians can use with confidence. In carrying out this function, the Bank is responsible for the design, production, distribution and destruction of bank notes. As such, the Bank is constantly exploring ways to improve the efficiency of currency operation and reduce the cost of cash handling. The evolution from paper bank notes to polymer bank notes—both in Canada and elsewhere—has improved the efficiency of the currency function and enhanced bank note security and durability. Going forward, it is important for a central bank to examine if it would further improve efficiency and security by issuing future generations of bank notes in digital form, taking advantage of the latest technological advances.

3

Second, a CBDC could improve the efficiency and safety of both retail and large-value payment systems. On the retail side, the focus is on how a digital currency can improve the efficiency of making payments—for example, at the point of sale (POS), online and peer-to-peer (P2P). There could also be benefits of having a CBDC for wholesale and interbank payments; for example, it could facilitate faster settlement and extended settlement hours.7 Third, a CBDC could be an appropriate policy response to payment innovations such as privately issued e-money and digital currency that might impair the central bank’s ability to achieve its monetary policy goals and to implement policies promoting financial stability.8 For instance, widely adopted private cryptocurrencies could severely weaken the transmission of monetary policy and also restrict the ability of the central bank to act as the lender of last resort. Moreover, it has been suggested that replacing physical bank notes with a CBDC would remove the effective lower bound on policy interest rates, permitting the central bank to implement negative policy interest rates if that were warranted by economic circumstances.9 The objective of this paper is to develop a framework for studying whether a central bank should consider issuing CBDC to improve the safety and efficiency of the retail payment system. Typically, a central bank provides bank notes for the general public and deposits at the central bank (reserves or settlement balances) for certain financial institutions.10 If a central bank were to issue a digital currency that could be used by the general public to make payments, the digital currency would compete with bank notes and other electronic payment methods, which would have important implications for the safety and efficiency of retail payments.11 Moreover, businesses and financial institutions could use a CBDC to make payments among themselves. Eventually, a CBDC would also have implications for large-value payments. Thus it seems reasonable to begin the study on CBDC with a focus on the payment systems.

7 See, for example, Ali et al. (2014) and Barrdear and Kumhof (2016). 8 See, for example, Committee on Payments and Market Infrastructures (2015). 9 See, for example, Rogoff (2015). For a discussion of the zero lower bound in Canada, see Witmer and Yang

(2016). 10 For example, in Canada, there are 17 financial institutions that are direct participants in the interbank settlement

system known as the Large Value Transfer System (LVTS). Each direct participant has a settlement account at the Bank of Canada and thus has access to deposits at the central bank. For a discussion of the LVTS and the settlement balance, see Arjani and McVanel (2006).

11 If a central bank were to issue a CBDC, it might consider allowing the general public to have access to its deposits or issuing a new digital currency that is completely different from bank notes and deposits by banks. We discuss this consideration in Section 4.

4

Central banks often play three roles in promoting the safety and efficiency of payment systems: facilitator or catalyst, overseer, and operator or direct provider.12 The level and type of intervention vary across central banks, reflecting different histories, institutional structures and legislative authorities. Currently, many central banks are closely monitoring developments in private digital currencies and their implications for payment systems. Also, a number of central banks—including the Bank of Canada—have been actively conducting research and engaging in dialogue with the private sector and academics about issues and benefits related to digital currencies as well as the challenges raised. Some central banks and public authorities are also exploring if there is a role for them in helping promote common standards among issuers as well as collaboration among stakeholders. If private digital currencies become broadly adopted, one of the main concerns is related to the safety of these systems. If privately issued digital currencies are used mainly for making retail payments, they do not necessarily pose any systemic risk to the financial system. Nevertheless, the failure of a major private digital currency scheme could potentially result in significant financial losses to users, a loss of confidence in these schemes, a disruption of retail payments and even considerable adverse economic effects. In addition, there could be a reputational risk for the regulators—including the central bank—who are seen as being responsible for oversight of the payment systems to ensure their safety. In that case, central banks and other public authorities would need to assess whether the existing oversight framework is adequate to address these concerns, and to improve the framework as required. Looking forward, if the risks related to digital currencies were to increase in a scenario where these digital currencies have become widely adopted and therefore the risks to the system have become more significant, the best course of action for central banks and public authorities would be to consider subjecting digital currencies to oversight. In this case, it is not necessary for a central bank to consider issuing its own digital currency. Therefore, as far as the retail payment system is concerned, one possible reason for public authorities such as a central bank to issue a digital currency would be to promote efficiency. The next section discusses a framework for analyzing such a scenario.

12 For a discussion of the role of the central bank regarding e-money, see Fung, Molico and Stuber (2014).

5

3 Should a Central Bank Issue a Digital Currency in the Interest of Retail Payment System Efficiency?

A new payment system would be more efficient than existing alternatives if the social benefits from its introduction outweighed the social costs. Besides technological and economic factors affecting the costs and benefits, improvements—such as increasing protection of private data and providing easy access to new payment methods—would also enhance the benefits of these systems for customers and therefore the efficiency of the payment system overall. As discussed above, it is in the context of efficiency that we discuss whether a central bank should issue its own digital currency. We propose a general framework to study this complex question. 1. Would a digital currency improve efficiency?

The first key question is whether a digital currency could improve the efficiency of payment systems in the first place. If not, there is really no need for a central bank to consider issuing a digital currency. 2. Would privately issued digital currencies provide such efficiency improvements without

government intervention?

Even if a digital currency could improve efficiency, another key question that a central bank needs to answer is whether the provision of such a currency could be left to the market. In other words, it is necessary to assess whether the private sector is likely to arrive at an efficient outcome without government intervention. Clearly, there are already a number of privately provided digital currencies today, such as Bitcoin and other cryptocurrencies. The real question is whether these digital currencies improve social efficiency to the full extent of what is technologically possible, and whether these digital currencies are broadly adopted by users. If both questions are answered with “yes,” then there is no need for a CBDC in the context of improving efficiency of the retail payment system. Nevertheless, there may still be a potential role for the central bank or government to establish rules and regulations and to monitor compliance. Rules and regulations would protect the safety of these systems. However, there would be no need for the central bank to issue digital currency directly. The question of whether the market could provide a digital currency that is at least as efficient as that of the central bank is not entirely a new one. This type of question has long been discussed in the economics literature in the context of other technologies (e.g., cellular phones). Importantly, this literature reflects concerns about anti-competitive forces such as barriers to

6

entry and market power that can arise because of network effects. Previous research has shown that there are strong network effects in the payments space as well.13 3. Would issuing a digital currency be the role that central banks should play in improving

efficiency?

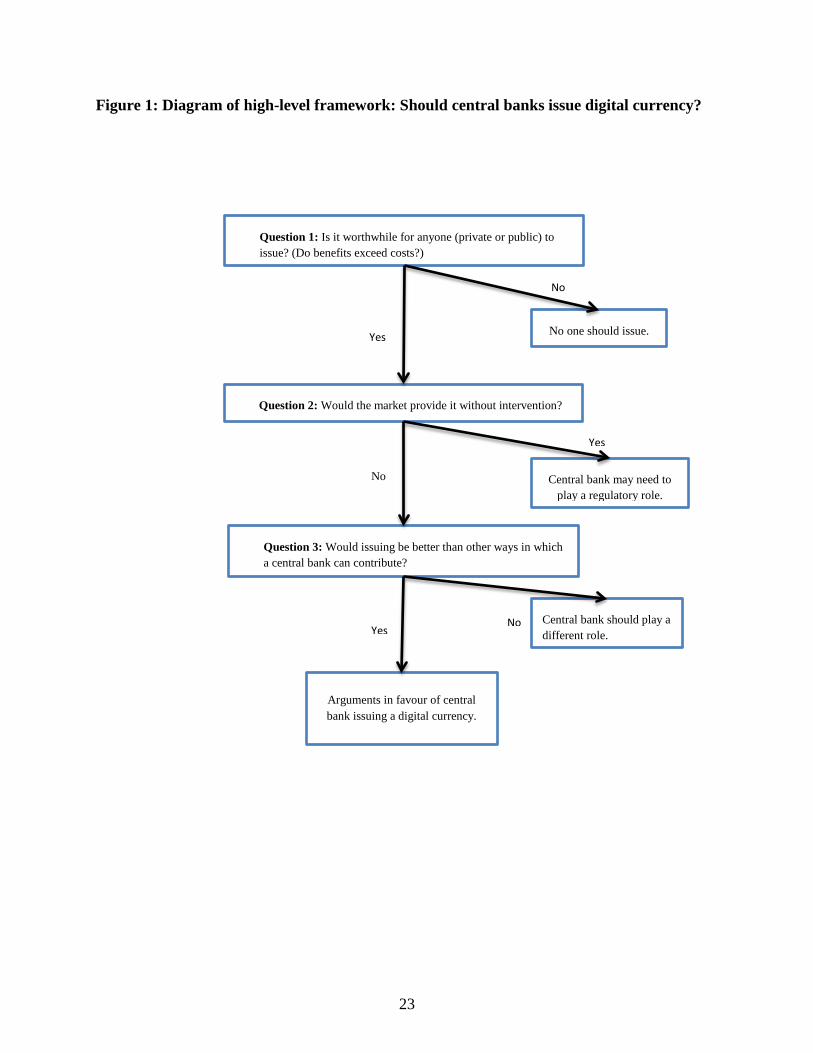

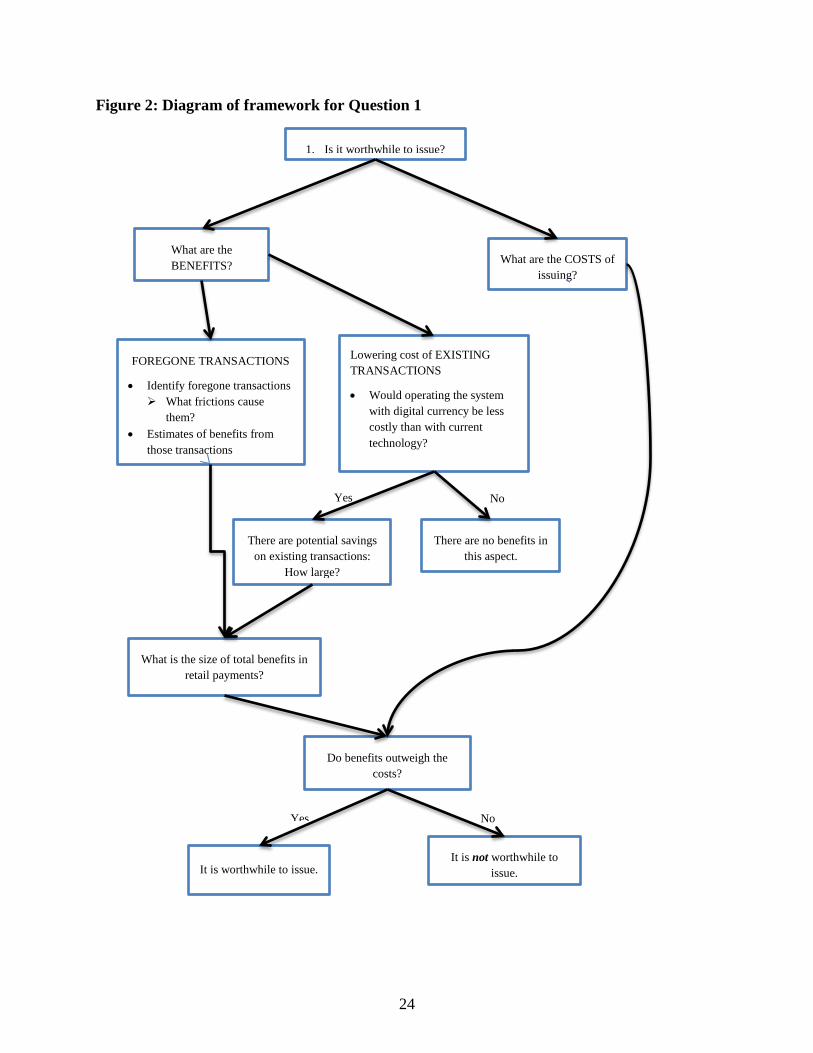

Finally, if a digital currency could improve efficiency but the privately provided solutions did not provide the efficiency improvement, then the next question is whether there is anything that a central bank could do to help bring an efficient digital currency to the market, such as examining if there is a barrier to entry and clarifying regulatory requirements. It is also important to ask whether issuing its own digital currency would be more desirable than other potential roles that the central bank could play, for example, facilitating or regulation. Figure 1 provides a recap of this high-level framework. As we analyze each of these questions in more detail below, it will quickly become clear that the discussion also depends on what type of digital currency a central bank is considering. There is currently a wide range of digital currencies with different properties and characteristics, and an even broader spectrum of potential digital currencies that could be designed. Thus, the analysis will need to be conducted in parallel to the question of what characteristics of a digital currency would be desirable to increase the efficiency of retail payment system. Figure 2 and Figure 3 illustrate the detailed analytical framework for individual questions, and we discuss these questions in the next three subsections.

3.1 Would a digital currency improve retail payment system efficiency?

The first issue is whether and how a digital currency could improve efficiency of the retail payment system. There are costs and benefits to every innovation. Efficiency is improved when the benefits to society are greater than the costs. It is possible to identify the following potential benefits of a digital currency:

• enabling transactions that are foregone at present because existing payment instruments do not allow users to overcome frictions in the marketplace

• reducing the cost of transactions currently conducted using existing payment methods; i.e., the digital currency could become a more cost-effective way to conduct such transactions than other instruments that already exist in the marketplace

13 See Katz and Shapiro (1985) and subsequent research about entry into the market with strong network effects

(e.g., Halaburda, Piskorski and Yildirim 2015). Literature on optimal pricing in two-sided markets (e.g., Rochet and Tirole 2003) tells us about strategies the credit card companies adopt, i.e., subsidizing consumers and charging high merchant fees. Halaburda, Jullien and Yehezkel (2014) give insight into dynamics of the market with network effects.

7

3.1.1 Potential benefits of issuing a digital currency

Enabling transactions that are foregone at present

Foregone transactions are those that are economically beneficial (i.e., improving the welfare of the transacting parties) but do not occur because of various frictions.14 If such transactions occurred, they would improve the well-being of the transacting parties and contribute to an increase in the overall output of the economy. This means that a new payment technology that allows more transactions to occur will improve efficiency. There are a number of frictions that could preclude some economically beneficial transactions; for example, concerns about security, and monetary and non-monetary transaction costs. Specific instances of frictions that may hinder economic exchange will vary for different types of transactions. Table 1 summarizes the main transaction types—online, POS, P2P and remittances (which can be thought of as international P2P transactions)—and for each type gives examples of frictions affecting that particular type of transaction. For example, online transactions may be foregone because of the following frictions:15

• Security and privacy concerns: Users may worry about how their payment information is stored and transferred. However, there are some market solutions that address these concerns. For example, for those who worry about dishonest merchants misusing their credit card information, there are services such as PayPal that do not allow merchants to have access to credit card information.16 However, some people may still worry about the safety of their PayPal account. If hackers gain access to a person’s PayPal account, they could also access both the credit card and bank account information. In this case, a security breach to the PayPal account could be even more damaging than having only the credit card information directly compromised.

• Non-monetary costs: There are also non-monetary costs of time and effort when making payments online. The user incurs a cost of entering the credit/debit card information (especially when the process is interrupted and the customer needs to enter it again), and also when setting up a PayPal account.

14 It is also necessary to consider social desirability of transactions, e.g., increasing the efficiency of illegal

transactions may not be desirable from the social point of view. 15 According to a Statistics Canada (2014), e-commerce accounted for 1.5 per cent of total retail sales in Canada in

2012, amounting to $7.7 billion. By comparison, retail e-commerce sales in the United States accounted for 5.2 per cent of its total retail sales in 2012. Technology Strategies International (2016) forecast that online spending will continue to grow strongly and will account for almost 8 per cent of total retail sales ($49 billion) in Canada in 2020.

16 Credit card networks are working on other solutions to deal with this concern, for example, “Verified by Visa” and “Buy with MasterPass” by MasterCard. The networks are also introducing tokenization (e.g., MasterCard SecureCode) so that online merchants do not store any credit card information such as a cardholder’s name and card number. There are also other online payment schemes such as Interact Online.

8

• Fees: Online transactions are often associated with fees, which can be quite high, especially for small-value transactions. Therefore, some merchants may choose not to offer their products online, particularly in the case of very small-ticket (low-price) items such as a single news story, even though consumers may be willing to pay a small fee to access such items. Those transactions would therefore be foregone.

Further, transactions at POS may be foregone because of the following:

• Security concerns: Users may be reluctant to use their credit cards at small unknown temporary street vendors. Sometimes, even at larger and more established stores, it is also possible that people are concerned that a dishonest employee may steal their credit card information. In addition, people worry about their credit card information stored in the data repository of large merchants, as such information has been stolen in the past (e.g., Target and Home Depot).

• Non-monetary costs: In the case of merchants that accept only cash, it may happen that a customer does not have enough cash on hand. There is a non-monetary cost of going to an ATM to retrieve cash, and the customer may not wish to incur this cost, thus preferring not to make the transaction.

In addition, some P2P transactions may be foregone because of the following:

• Non-monetary costs: Cash is the most common means of conducting P2P transactions.17 The cost of finding an ATM and going there may hinder some transactions. Among younger users, this problem has been solved by smartphone apps (e.g., Venmo in the United States), which are used to settle some P2P transactions, and by online banking functions such as Interac Online. However, for certain demographic groups, the cost of downloading and learning to use the new app may hinder adoption of this approach. Moreover, individuals who do not yet have access to a smartphone that can download such apps and those who do not use online banking will not be able to use these alternative payment methods.

• Fees: The apps and other electronic P2P money transfer methods usually carry fees.18 As a result, transactions, especially of small value, may not be carried out.

In the case of remittances—one of the most common and important type of P2P transactions—high fixed fees may force senders to send funds less frequently than is optimal, as the senders may want to accumulate a larger sum of money before sending it in order to minimize costs.19 As

17 Fung, Huynh and Stuber (2015) report that cash accounts for 55, 69 and 67 per cent of P2P transactions in

Australia, Canada and the United States, respectively. 18 For example, in Canada, Internet e-transfer allows users to send funds to another party through email. Canadian

banks typically charge a fee of $1 to $1.50 for such transfers. Recently, some banks began to offer free Interac e-transfers to their customers.

19 For example, it costs $10 to send $100 from Canada to India using MoneyGram, at a rate of 10 per cent. However, it also costs $10 to send $500, and the rate now drops to only 2 per cent.

9

a result, this may create additional risks and costs. In the case of cash, there is a risk that some of the money will never be sent; for example, it may be lost or stolen. Moreover, utility is lost if remittances cannot be sent at optimal intervals, even if the money eventually reaches its destination because, for example, the receiver needs to borrow against future income or delay consumption. Different transaction frictions may result in remittances being sent less frequently, or not at all.

• Security concerns: Mailing cash or sending it with other travellers going in the same direction is unsafe and unreliable.

• Fees: Other options for electronic transfer of remittances (e.g., Western Union or PayPal) also carry high fees, which may hinder transfers and make cross-border payments less than optimal.20

There are at least two possible reasons why the market is not providing payment solutions that can facilitate those transactions. First, the costs to potential providers may be higher than the benefits (to the providers) resulting from those trades. The examples in Table 1 suggest that the value of the currently foregone transactions is likely to be quite small relative to the total value of existing retail transactions. There is also the issue of whether users are willing to adopt these new payment solutions. In future research, it would be necessary to estimate the cost of providing those transactions. The second reason is related to market inefficiencies resulting from the underlying market structure. That is, some transactions may potentially bring large benefits to providers that more than offset their costs of conducting the transaction; however, these do not occur because of barriers to entry or market power. In such a case, there may be a need for some form of government intervention. We will look at this issue more carefully in Section 3.2. Notice also that the variety of categories for transaction frictions and payment methods discussed above indicates that a digital currency with different attributes may appeal to different segments of the market (that is, it would help to alleviate some frictions, but not necessarily all). Therefore, it is not possible to evaluate efficiency gains of a digital currency in isolation without knowing the characteristics of the digital currency. While we discuss the potential characteristics of CBDC separately in Section 5 for convenience of exposition, the analyses in both sections should be considered in parallel.

20 Two Canadian banks are now offering a no-fee international transfer that promises to have the funds delivered

within one to three business days. The sender is charged about 2.5 to 3 per cent exchange rate spread, which is similar to a credit card transaction. However, both the sender and receiver must have access to a bank account. This is not a problem in Canada but can be a serious impediment for receivers who live in a country where access to banking is limited.

10

Decreasing the costs of transactions that are already occurring

The efficiency of the payment system could also be improved if a digital currency decreases the cost of processing existing transactions. Thus, there is a need to estimate the possible cost savings from operating a payment system based on digital currency. However, even if some digital currencies indeed allow for some transactions to be carried out at a lower cost than with current technologies, there is still the concern about whether such digital currencies would be brought to the market by private providers because of the barriers to entry arising from network effects. The literature on network economics and the recent experience of the payments market highlight that the entry of new players to markets with strong network effects is often very difficult. We discuss this issue in the next subsection.

3.1.2 Costs of introducing a digital currency to the market

To fully analyze the efficiency of introducing a digital currency, the benefits should be compared with the costs of designing and providing a digital currency. Again, the costs cannot be evaluated without taking into consideration the specific characteristics that the digital currency would possess (investigated in Section 5). In this paper, these costs are recognized but not yet fully analyzed. Thus it remains a topic of future study.

3.2 Would privately provided digital currencies deliver efficiency improvement by themselves?

If the benefits of digital currency indeed outweigh the costs of introducing it to the market and operating it after introduction, the question then becomes whether the market would be able to deliver such an efficiency-improving digital currency. As discussed above, in a market that displays strong network effects (such as the payment market), it is inherently difficult to enter; these network effects create a substantial barrier to entry and, at the same time, give incumbents large market power. In general, a product or service exhibits positive network effects when its value increases as more people purchase or use it. A classic example is the telephone. There are very few benefits if only one person owns a telephone; the more people who own a phone, the larger the overall value of that technology. This is applicable to many examples of recent telecommunications technologies. It is easy to see that money and payments also exhibit strong network effects. For example, a means of payment is more useful to everyone when more people are using and accepting it. It has been well documented in the economics literature that, in environments with network effects, a new entrant may not succeed in the market even if a firm has superior technology or offers lower prices.

11

Despite the presence of network effects, it does not necessarily mean that the government should be providing services in all these cases. The issue relevant to this paper is whether efficiency would be improved if public authorities such as a central bank were to issue a digital currency when the market fails to provide it. In the context of payment systems, many innovative payment methods that have been brought to the market failed to achieve wide adoption.21 Even large, established players find it hard to enter the market and compete with incumbents despite offering increased convenience or charging lower costs. For example, Google Wallet has changed its focus from POS payments to P2P payments.22 Apple Pay, despite some early reported success, has not yet been able to gain much traction.23 Another new entrant, Bitcoin, has attracted much attention but is still struggling with widespread adoption. It is possible that, despite all the high-tech innovation, the payments market is not necessarily structured in a way that favours the most efficient solution. Thus it is possible that, although digital currency could be a socially beneficial technology, private provision would not be successful without some form of government intervention.

3.3 Would issuing its own digital currency be the most desirable role for a central bank?

In the previous subsection, we considered several possible scenarios where the market may not be able to provide an efficiency-improving technology by itself. In such cases, the market may benefit from some form of government intervention, ranging from facilitating and catalyzing private provision to regulation. Unfortunately, in cases where the underprovision is caused by network effects, regulation may help very little in mitigating this barrier to entry.24 The natural question is then whether direct provision by the central bank is a more desirable option.

21 In Canada, credit cards (introduced in the 1970s) and debit cards (introduced in the 1990s) remain the most

popular electronic payment methods (Fung, Huynh and Stuber 2015). Many other innovative payment methods have been introduced to the Canadian market without much success.

22 Dating back to 2011, Google Wallet is a mobile wallet that allows users to make purchases and P2P transfers. It has not been able to gain much traction. In 2015, Google Wallet dropped its near-field communication capability and is now focusing on P2P payments.

23 That is the case in the United States. See, for example, http://www.pymnts.com/apple-pay-adoption/. It is important to note that there are other reasons why consumers are not switching to these new payment methods; for example, they may not find sufficient benefits from switching or they may find the switching costs too high.

24 There are examples of barriers to entry arising from other causes that were alleviated by government regulation. For example, in the case of railways or cellphone networks, there is a very large cost of setting up the infrastructure (tracks or cellphone towers). Duplicating the cost in the case of duplicating the infrastructure by competitors may make entry socially inefficient, while the market can benefit from competition when the infrastructure cost is paid only once. In such a situation, regulation mandating the incumbent to share the infrastructure at a reasonable fee with entrants helps to alleviate this barrier to entry.

12

In considering whether issuing CBDC is the most desirable role for a central bank, a related question is: What are the advantages and disadvantages of the central bank issuing a digital currency compared with a private issuer? There are a number of advantages. First, only the central bank could credibly commit to exchanging its digital currency with legal tender (bank notes and central bank deposits) at par and thus maintain the fixed exchange rate between its digital currency and the legal tender. Other privately issued digital currency cannot guarantee that it will always trade at par with legal tender. A case in point is Bitcoin, which has exhibited high volatility in its exchange rate with a sovereign currency.25 In other words, only the central bank could commit to a monetary policy framework that would maintain the stability of the value of its digital currency. Second, one of the major innovations with cryptocurrencies such as Bitcoin, besides its technology, is that it has its own unit of account. It is denominated in bitcoin but not in any sovereign currency. One obvious advantage is that it can easily flow through borders without the need to exchange for different currencies. However, this advantage would be realized only when most people around the world use bitcoin for their transactions. If people in different countries still mainly use their own national currencies, then they will always have to exchange bitcoins for the national currency and thus potentially suffer from the high volatility of its exchange rate (as is currently the case). So far, the exchange rate for Bitcoin against major currencies such as the US dollar has been very volatile. In this case, Bitcoin and other cryptocurrencies may best be used or viewed as a payment system that people use to make payments electronically at a relatively high speed and low cost. But they will convert to bitcoins only when they are about to make the payment and convert back to their local currency as soon as they receive the bitcoins. There are, however, a number of disadvantages for a central bank to issue CBDC. First, it is questionable whether the central bank would have a comparative advantage in issuing a digital currency, given its lack of market and technical expertise. Also, competing with the private sector to acquire such expertise would be difficult. Second, CBDC might stifle future innovation in this area, as it reduces the incentive for private investment. Third, any security breaches of its digital currency could potentially negatively affect the central bank’s reputation when it carries out its other functions such as conducting monetary policy and financial stability policy. When considering a CBDC, there are also other questions to be answered. If a central bank were to issue CBDC, should it be the sole issuer of digital currency?26 Would the central bank need to be a legal monopoly for the CBDC to be viable? On the one hand, having a variety of digital

25 Bolt and van Oordt (2016) argue that the initial volatility of the Bitcoin exchange rate is typical for a new

currency and the exchange rate will stabilize over time. 26 Weber (2015) argues that, while the Federal Reserve banks were given a monopoly on bank note issuance, it

does not necessarily mean that central banks should be given a monopoly on e-money issuance.

13

currencies could create confusion among customers, which could hinder adoption of any digital currency. On the other hand, one of the lessons learned from the history of bank notes is that private bank notes and government-issued notes could coexist and function smoothly.27 In any case, the crucial question of whether a central bank should issue its own digital currency (the “why” question), as well as many other questions along the way, cannot be answered without considering what a digital currency issued by the central bank would look like (the “how” question). Several related questions can be raised, including: What characteristics would it have, and how would it be introduced to the market? In other words, the questions of “why” and “how” should not be analyzed separately.

4 How to Evaluate the Desirability of Potential Attributes of a CBDC

When a central bank considers issuing a CBDC, it would be necessary to ask what characteristics the CBDC should have, as well as how a central bank could get it into circulation and promote adoption by the public. It would make sense to introduce a CBDC only if it would be broadly adopted and circulated. In this section, we provide a framework for how to study the characteristics of a CBDC. In general, there are two sets of characteristics. The first set contains predetermined characteristics that do not depend on the reasons why a central bank is issuing a CBDC. The second set contains characteristics to be determined, which are related to the central bank’s motivation for issuing a CBDC and depend on the technology employed.

4.1 Predetermined characteristics

First, the unit of account would be the national currency, the same as the other liabilities on the central bank’s balance sheet. Second, the central bank would continue to issue bank notes and provide settlement balance or reserve accounts to banks.28 In addition, it would stand ready to exchange CBDC with bank notes and central bank deposits at par. Third, the supply of CBDC

27 Weber (2015) studies the period from 1914 to 1935, when Federal Reserve notes issued by the Federal Reserve

banks circulated alongside national bank notes in the United States. He concludes that private- and government-issued notes can circulate simultaneously. Fung, Hendry and Weber (forthcoming) find that both private bank notes and Dominion notes issued by the government circulated and worked smoothly in Canada from 1871 to 1935. These two papers also discuss whether a CBDC would drive out private digital currencies and whether the government should be the monopoly issuer of digital currencies.

28 At some point in the future, the demand for bank notes and central bank deposits might decline to such a low level that the central bank would need to consider terminating their supply.

14

would be determined by the central bank in a way that is consistent with its monetary policy framework (unlike most cryptocurrencies today).29 While such predetermined characteristics may be straightforward to state, there are challenges in ensuring these attributes.30 For example, to have the national currency as the unit of account for the CBDC, the central bank would need to ensure at-par convertibility among its other liabilities and CBDC. What mechanism would ensure at-par exchange among these liabilities? Would it be guaranteed if the central bank committed to exchanging bank notes and central bank deposits for CBDC at par with financial institutions? Would that provide sufficient incentive for merchants and other users to accept both bank notes and CBDC at par?

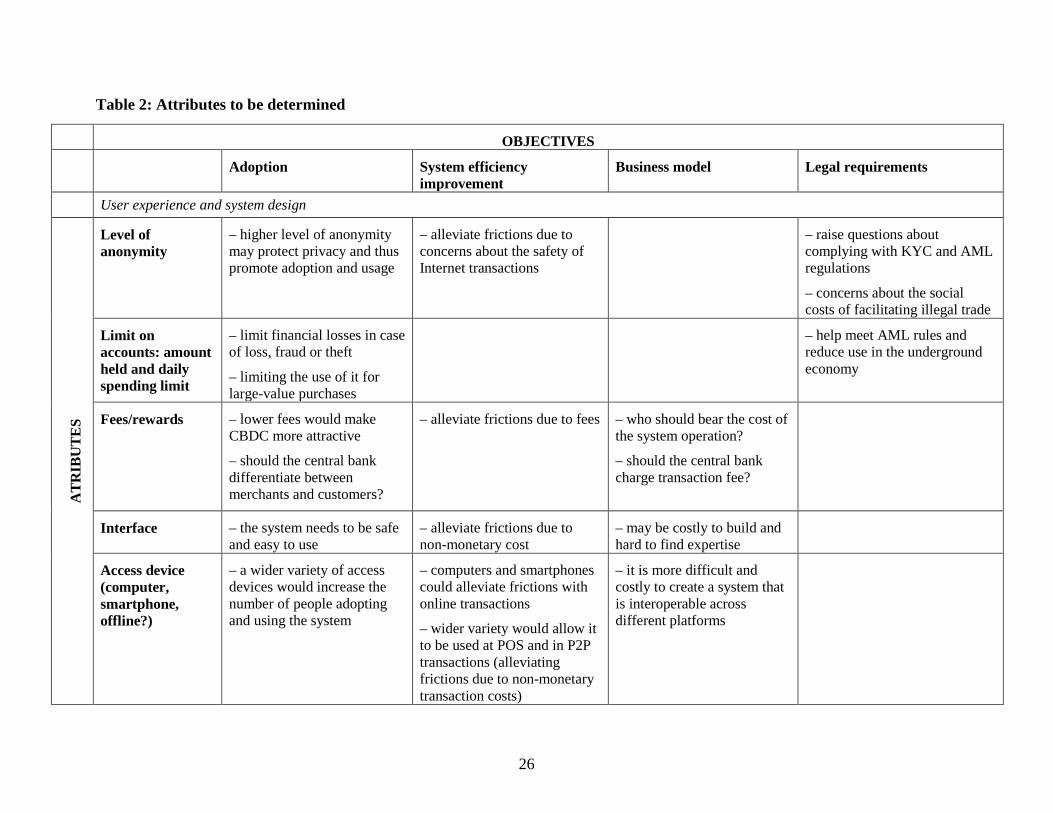

4.2 Attributes to be determined

Besides predetermined characteristics, the design of any potential digital currency should allow the central bank to address any economic needs and frictions currently present in the marketplace, such as those outlined above and summarized in Table 1. To decide on the desirability of individual attributes, a framework would be needed to analyze these attributes.31 Such a framework recognizes the following objectives when considering possible characteristics:

(i) provision of a more-efficient payment system—whether by alleviating frictions and thus reducing the number of foregone transactions, or by providing a less expensive method of conducting existing transactions, as discussed in Section 4;

(ii) wide adoption of a CBDC—a necessary condition for the effectiveness of the system;32 (iii) efficient allocation of resources to deliver this service—meaning a good business model

for the central bank. In addition, it should also be important to keep in mind legal requirements such as compliance with anti-money laundering (AML) and counterterrorist funding (CTF) requirements. In balancing multiple objectives, it is important to be aware that, in some cases, some characteristics may work in favour of one objective but against another. Thus, when considering

29 Currently, central banks typically manage the supply of bank notes to meet the public’s demand and thus the

supply of CBDC could follow the same policy. 30 In the context of the launching of a new fiat currency, Selgin (1994) studies the requirements for the successful

introduction of a new fiat currency by reviewing the writings of several early 20th-century authors. Lotz and Rocheteau (2000) use a dual-currency search-theoretic model to study the effectiveness of three types of policies (e.g., legal tender laws) to guarantee the acceptability of a new currency.

31 Chiu and Wong (2015) use a mechanism design approach to examine some essential features of an e-money system.

32 Another important factor that will affect adoption is the safety of the system, e.g., resistance to cyber attacks or hacking of the system. We assume that the central bank would put its best efforts toward ensuring the safety of every attribute, although we do not discuss this property separately.

15

potential characteristics of a CBDC, it is important to take into account such trade-offs. Below we discuss the most important potential characteristics in the context of the objectives outlined above. And we organize our discussion of these characteristics along the dimensions of user experience and system design, as well as technological issues. Table 2 summarizes this discussion and the trade-offs involved. We start with user experience and system design. Consider, for example, the level of anonymity as an attribute of a CBDC. Allowing for anonymous electronic transactions with a CBDC would alleviate frictions related to people’s concerns about the safety of Internet transactions by making it similar to cash. This would decrease the number of foregone electronic transactions (e.g., online) and thus improve the system’s efficiency and increase adoption. Similarly, it would facilitate additional transactions at POS and P2P, even when the other party is not trusted (as discussed in Section 4). At the same time, such anonymity would make it easier to avoid AML regulations, especially as a large amount of CBDC can be sent across geographical locations over a short period of time between private parties. If this led to an increase in illegal transactions or tax evasion, it could also bring additional social costs. Such an association may also discourage some people from using a CBDC, as in the case of Bitcoin. It is possible that putting limits on accounts in terms of the amount of funds held and the daily spending limit could alleviate some of the concerns discussed above. In fact, many existing e-money schemes around the world already have such limits. At the same time, it could be beneficial for some users as there would be a limit in case they lose their CBDC by accident, theft or fraud, or it could be used as a way of budgeting.33,34 On the other hand, some users could find it inconvenient and restrictive in what purchases they can make with a CBDC. Should the central bank charge transaction fees or offer rewards? Charging fees lower than credit and debit cards or eliminating fees altogether would alleviate another source of friction (identified earlier as “fees”) and decrease the number of foregone transactions. This would improve the system’s efficiency and make CBDC more attractive to users (as discussed in Section 4.1.1), which in turn would promote adoption. While low or no fees are good for users, it would pose issues for the central bank’s business model if it were to bear the cost of operating the system.35 If the central bank were to charge fees, should the fees be uniform for all parties, or should the system differentiate between different types of users, for example, between merchants and customers?

33 It would also be important to consider whether the system should give the central bank authority to intervene,

e.g., to reverse transactions because of fraud or other illegal activities. 34 For the use of cash for budgeting, see von Kalckreuth, Schmidt and Stix (2014). 35 Central banks will earn seigniorage revenue from issuing a CBDC, but they should also consider whether to

issue a CBDC on a cost-recovery basis.

16

An easy-to-use interface would play a role in lowering non-monetary cost, which is another source of friction. Again, alleviating the friction would improve the system’s efficiency and increase adoption. At the same time, designing a safe and easy-to-use system requires expertise that is hard to find and highly sought after in the market. It would be very difficult and costly for a central bank to compete with technology companies for the expertise needed.36 Another issue to consider is the range of access devices for a CBDC system; that is, on what devices users would be able to make CBDC transactions. The possible range includes computers, smartphones and some potential offline schemes.37 Allowing a CBDC to be used on computers could alleviate frictions related to online transactions. Using smartphones, users can make online, POS and P2P payments with a CBDC. Offline schemes would probably be limited to POS and P2P transactions but would allow a CBDC to be transferred even when access to technology is limited. In general, a wider variety of devices through which the CBDC system could be accessed would increase the number of people attracted to the system and would improve adoption. At the same time, it would be more challenging to create a stable, easy-to-use system that functions seamlessly on many types of devices. Again, it would also be a challenge for the central bank to attract technology professionals with the expertise to develop such a system. Another point for consideration is how users would acquire the CBDC. What distribution channels should be used? Would the CBDC be distributed through commercial banks or acquired directly from the central bank? Easy access and multiple sources would promote adoption and use. But what mechanism could be used to make CBDC easy to acquire? Should a central bank provide incentives for buyers or sellers to adopt the technology first, or should the central bank simply allow it to grow organically? As a CBDC is acquired by users, what safeguards could be put in place to ensure compliance with know-your-customer (KYC) and AML regulations? The characteristics considered so far are concerned with the related issues of user experience and system design. Technological issues that are not necessarily related to the user’s experience are also important. One such technological characteristic that would need to be determined is the type of verification system to be used. Transactions would need to be verified whether in a centralized or decentralized system. Most of the existing systems (and all traditional electronic systems) are centralized and typically the network operator verifies and validates all transactions, for example, in the case of credit cards or debit cards. However, with the introduction and increased popularity of cryptocurrencies and blockchain technology, a decentralized system for digital

36 Central banks should also consider the possibility of outsourcing and working in partnership with relevant

technology companies. 37 Mondex and the Octopus Card are examples of electronic offline schemes. Bitcoin users can also keep their

private keys offline by writing them down on paper.

17

currencies also becomes possible. While centralized systems have been around for a long time and been widely used, they have not been successful in addressing the frictions as discussed in Section 4, thus resulting in foregone transactions. In the case of Canada, for example, the Bank of Canada provides settlement accounts to direct participants in the Large Value Transfer System (LVTS) so that they can make payments to each other using central bank deposits. This system can be viewed as a centralized e-money or digital currency system. Extending such a system to allow everyone to have an account with the central bank—using deposits at the account to make a payment—would be akin to providing banking and payment services for the general public. The question would then be what retail payment problems such a CBDC could solve that deposit accounts in commercial banks cannot. As such, decentralized systems should be considered as a possible alternative in improving the system’s efficiency if the central bank were to issue its own digital currency.38 At the same time, it is not clear how costly a decentralized verification system would be; the issue has not yet been thoroughly investigated, although it is often claimed that a decentralized system is cheaper than a centralized one. In addition, when deciding on the details of a decentralized system, central banks would need to decide whether to use blockchain technology and, if so, whether it should be open or closed (permissioned or permissionless); what consensus mechanism should be used; what incentives the system should provide for the nodes to participate in the verification process, etc.39 Another technological issue is the speed of settlement. Quick settlement would make it more attractive to users and thus encourage adoption. But quick settlement using blockchain technology could be a challenge to the stability of the system.40 A CBDC system, like other payment systems, would need a well-developed ecosystem to be fully functional and facilitate adoption. As the designer of the CBDC system, the central bank should also consider what aspects of the ecosystem it should be managing and what parts can be left to the market. For example, one lesson learned from the Bitcoin experience is that the most vulnerable points in the decentralized Bitcoin ecosystem have been the wallets and exchanges. Thus the central bank would need to decide whether to provide proprietary wallets and exchanges. The central bank would also have to consider setting safety standards and

38 Proponents of decentralized systems may be motivated by other considerations such as the desire of not relying

on a trusted third party to run the system. 39 There are a number of important issues related to a decentralized system that would need to be considered, e.g.,

verification, risk control and the mitigation mechanism. But the most important is verification of transactions. See, for example, Wilkins (2016).

40 This is a known issue with blockchain technologies. Transactions are settled more quickly when blocks of transactions are added to the blockchain more quickly. This, however, increases the risks of so-called “forking” and the length of the fork before the fork is resolved. When a fork occurs, some transactions need to be retrospectively rejected, thus creating a threat to the stability of the system.

18

requirements to ensure the safety of the ecosystem and to allow for the private provision of wallets and exchanges as long as they satisfy the set of requirements.

5 Conclusions

Central banks are typically responsible for issuing bank notes and promoting safety and efficiency of payment systems. Many recent developments, particularly rapid technological innovations, have changed the payment landscape around the world. In this paper, we provide a framework to study whether a central bank should consider issuing its own digital currency to promote the efficiency of retail payments. Equally important for this discussion is a framework to study the attributes that such a digital currency should possess to improve the efficiency of the system and promote adoption and usage. Technological advances will likely continue to result in innovative payment products that can fill existing payment gaps in ways that we cannot currently anticipate. As such, the framework needs to be general enough to address these issues. Addressing those questions will inform the discussion about whether it is in the best interests of society for a central bank to issue its own digital currency and, if so, what considerations should be given to its design. It is important to keep in mind that there are other aspects besides retail payment system efficiency that are important in the discussion of a central bank digital currency. Those considerations are left for future research.

19

References

Ali, R., J. Barrdear, R. Clews and J. Southgate. 2014. “Innovations in Payment Technologies and the Emergence of Digital Currencies.” Bank of England Quarterly Bulletin Q3: 262–75.

Arjani, N. and D. McVanel. 2006. “A Primer on Canada’s Large Value Transfer System.” www.bankofcanada.ca/en/financial/lvts_neville.pdf.

Bank for International Settlements. 1996. Implications for Central Banks of the Development of Electronic Money. Basel: Bank for International Settlements.

Barrdear, J. and M. Kumhof. 2016. “The Macroeconomics of Central Bank Issued Digital Currencies.” Bank of England Staff Working Paper No. 605.

Bolt, W. and M. R. C. van Oordt. 2016. “On the Value of Virtual Currencies.” Bank of Canada Staff Working Paper No. 2016-42.

Chiu, J. and T.-N. Wong. 2015. “On the Essentiality of E-Money.” Bank of Canada Staff Working Paper No. 2015-4.

Committee on Payment and Settlement Systems. 2012. “Innovations in Retail Payments.” Bank for International Settlements (May).

———. 2015. “Digital Currencies.” Bank for International Settlements (November).

Freedman, C. 2000. “Monetary Policy Implementation: Past, Present and Future – Will Electronic Money Lead to the Eventual Demise of Central Banking?” International Finance 3 (2): 221–27.

Fung, B., S. Hendry and W. Weber. “Canadian Bank Notes and Dominion Notes: Lessons for E-Moneys.” Bank of Canada Staff Working Paper (forthcoming).

Fung, B., K. P. Huynh and G. Stuber. 2015. “The Use of Cash in Canada.” Bank of Canada Review (Spring): 45–56.

Fung, B., M. Molico and G. Stuber. 2014. “Electronic Money and Payments: Recent Developments and Issues.” Bank of Canada Discussion Paper No. 2014-2.

Halaburda, H., B. Jullien and Y. Yehezkel. 2014. “Dynamic Platform Competition.” September. NET Institute Working Paper.

Halaburda, H. and M. J. Piskorski. 2010. “When Should a Platform Give People Fewer Choices and Charge More for Them?” The CPI Antitrust Journal 6 (2): 2010–11.

Halaburda, H., M. J. Piskorski and P. Yildirim. 2015. "Competing by Restricting Choice: The Case of Search Platforms." Harvard Business School Strategy Unit Working Paper.

Katz, M. and C. Shapiro. 1985. “Network Externalities, Competition, and Compatibility.” American Economic Review 75 (3): 424–40.

Lotz, S. and G. Rocheteau. 2000. “Launching of a New Currency in a Simple Random Matching Model.” Mimeo.

Rochet, J.-C. and J. Tirole. 2003. “Platform Competition in Two-Sided Markets.” Journal of the European Economic Association 1 (4): 990–1029.

20

Rogoff, K. 2015. “Costs and Benefits to Phasing out Paper Currency.” NBER Macroeconomics Annual 2014 29: 445–56.

Selgin, G. 1994. “On Ensuring the Acceptability of a New Fiat Money.” Journal of Money, Credit and Banking 26 (4): 808–26.

Statistics Canada. 2014. “Retail at a Glance: E-Commerce Sales, 2012.” The Daily, 8 July 2014.

Stuber, G. 1996. “Electronic Purse – An Overview of Recent Developments and Policy Issues.” Bank of Canada Technical Report No. 74.

Technology Strategies International (TSI). 2016. “Canadian Payments Forecast 2016.” http://tsiglobalnet.com/cpf2016.html.

von Kalckreuth, U., T. Schmidt and H. Stix. 2014. “Using Cash to Monitor Liquidity: Implications for Payments, Currency Demand, and Withdrawal Behavior.” Journal of Money, Credit and Banking 46 (8): 1753–86.

Weber, W. E. 2015. “Government and Private E-Money-Like Systems: Federal Reserve Notes and National Bank Notes.” Bank of Canada Staff Working Paper No. 2015-18.

Wilkins, C. 2014. “Money in a Digital World.” Remarks to Wilfrid Laurier University, Waterloo, Ontario, 13 November.

———. 2016. “Fintech and the Financial Ecosystem: Evolution or Revolution?” Remarks to Payments Canada, Calgary, Alberta, 17 June.

Witmer, J. and J. Yang. 2016. “Estimating Canada’s Effective Lower Bound.” Bank of Canada Review (Spring): 3–14.

21

Appendix

Summary of Future Research Questions

1. Would a digital currency improve the efficiency of the payment system? o What would be the cost of providing digital currency (for a central bank and for a

private party)? o What would be the cost of operating a digital currency system? o Could digital currency serve existing payment needs at a lower cost? o Are transactions currently foregone because the cost of providing those

transactions exceeds the benefit, or because of the market structure? o What is the estimated number and value of foregone transactions?

2. Would the private sector be able to provide a digital currency without government intervention?

o What is the market structure in payments? Is it competitive? Are there barriers to entry that are hindering introduction of more efficient technology?

3. Would issuing a digital currency be a more desirable role than other ways in which a central bank could engage?

o What could a central bank do to facilitate the private provision of digital currency if network effects constitute substantial barriers to entry?

4. What are the desired characteristics of a CBDC and the strategy of bringing it to the market?

o What would be the desired characteristics of a CBDC? o What would be the optimal strategy for bringing a CBDC to the market? o What would be the effects on the financial system (including private banks) if the

central bank were to issue a CBDC?

22

Table 1: Categorization of foregone transactions

Security/privacy Non-monetary cost Fees

Online • Worries about the safety of Internet transactions

• Worries about information storage and transfer

• Cost of setting up online account such as PayPal

• Cost of entering credit/debit card information

• Credit card fees (especially for small-value purchases and micropayments)

POS • Lack of trust in certain merchants

• Cash-only merchant • Cost of going to ATM

P2P • Cost of going to ATM • Cost of downloading

and learning new app

• Price of new apps • Fees for using

electronic P2P payment methods

Remittances • Mailing cash or passing it though travellers is unsafe and unreliable

• Western Union or PayPal fees

23

Figure 1: Diagram of high-level framework: Should central banks issue digital currency?

No Yes

Yes

No

Yes

No

Question 1: Is it worthwhile for anyone (private or public) to issue? (Do benefits exceed costs?)

Question 2: Would the market provide it without intervention?

Question 3: Would issuing be better than other ways in which a central bank can contribute?

Arguments in favour of central bank issuing a digital currency.

Central bank should play a different role.

No one should issue.

Central bank may need to play a regulatory role.

24

Figure 2: Diagram of framework for Question 1

No Yes

No Yes

1. Is it worthwhile to issue?

What are the BENEFITS? What are the COSTS of

issuing?

FOREGONE TRANSACTIONS

• Identify foregone transactions What frictions cause

them? • Estimates of benefits from

those transactions

Lowering cost of EXISTING TRANSACTIONS

• Would operating the system with digital currency be less costly than with current technology?

There are potential savings on existing transactions:

How large?

There are no benefits in this aspect.

What is the size of total benefits in retail payments?

Do benefits outweigh the costs?

It is worthwhile to issue. It is not worthwhile to

issue.

25

Figure 3: Framework for Question 2 and Question 3

Question 2: Would the market provide digital currency without government/central bank’s intervention?

• What may prevent the industry from efficient provision of the new technology? • Literature suggests that, because of network effects, this industry is not necessarily

competitive. In-depth analysis of potential competitive distortions in the context of

introducing new technology Lessons from introductions of other technologies (e.g., chip and PIN payment

cards; look for examples of unsuccessful introductions and neglected technologies)

Question 3: Would issuing be a more desirable role for the central bank to play?

• What are the other roles for a central bank? • For each, in-depth analysis of whether it would fix the problems identified in the

earlier part of the analysis (Also: Is the intervention needed at all, even with inefficiency of market provision?)

26

Table 2: Attributes to be determined

OBJECTIVES

Adoption System efficiency improvement

Business model Legal requirements

User experience and system design

AT

RIB

UT

ES

Level of anonymity

– higher level of anonymity may protect privacy and thus promote adoption and usage

– alleviate frictions due to concerns about the safety of Internet transactions

– raise questions about complying with KYC and AML regulations

– concerns about the social costs of facilitating illegal trade

Limit on accounts: amount held and daily spending limit

– limit financial losses in case of loss, fraud or theft

– limiting the use of it for large-value purchases

– help meet AML rules and reduce use in the underground economy

Fees/rewards – lower fees would make CBDC more attractive

– should the central bank differentiate between merchants and customers?

– alleviate frictions due to fees – who should bear the cost of the system operation?

– should the central bank charge transaction fee?

Interface – the system needs to be safe and easy to use

– alleviate frictions due to non-monetary cost

– may be costly to build and hard to find expertise

Access device (computer, smartphone, offline?)

– a wider variety of access devices would increase the number of people adopting and using the system

– computers and smartphones could alleviate frictions with online transactions

– wider variety would allow it to be used at POS and in P2P transactions (alleviating frictions due to non-monetary transaction costs)

– it is more difficult and costly to create a system that is interoperable across different platforms

27

Distribution channels (commercial bank, and/or directly from central bank?)

– should a central bank provide incentives for buyers or for sellers to adopt the technology first?

– easy access will promote adoption and use

– how to ensure compliance with AML and KYC regulations?

Technological issues

AT

RIB

UT

ES

Verification system

– centralized system would not alleviate the frictions that have been identified

– decentralized system (blockchain) would need to be assessed based on cost

– which consensus mechanism?

– open or closed blockchain?

– what incentives for verification of transactions?

Speed of settlement and reversibility (e.g., charge back)

– quick settlement will encourage adoption

– quicker settlement in blockchain technology could be a challenge to the stability of the system

Ecosystem management

– need to understand known risks of a decentralized system and learn from them, e.g., the Bitcoin experience

![Centrally Banked Cryptocurrencies - Cryptology … the European Central Bank anticipates their “impact on monetary policy and price stability” [8]; the US Federal Reserve their](https://img.pdfslide.net/doc/110x75/5ad110f47f8b9a72118b9fd0/centrally-banked-cryptocurrencies-cryptology-the-european-central-bank-anticipates.jpg)