Embed Size (px)

Citation preview

CENTURY 21 ACCOUNTING © Thomson/South-Western

LESSON 15-1LESSON 15-1

Cost Characteristics That Influence Decisions

CENTURY 21 ACCOUNTING © Thomson/South-Western

2

LESSON 15-1

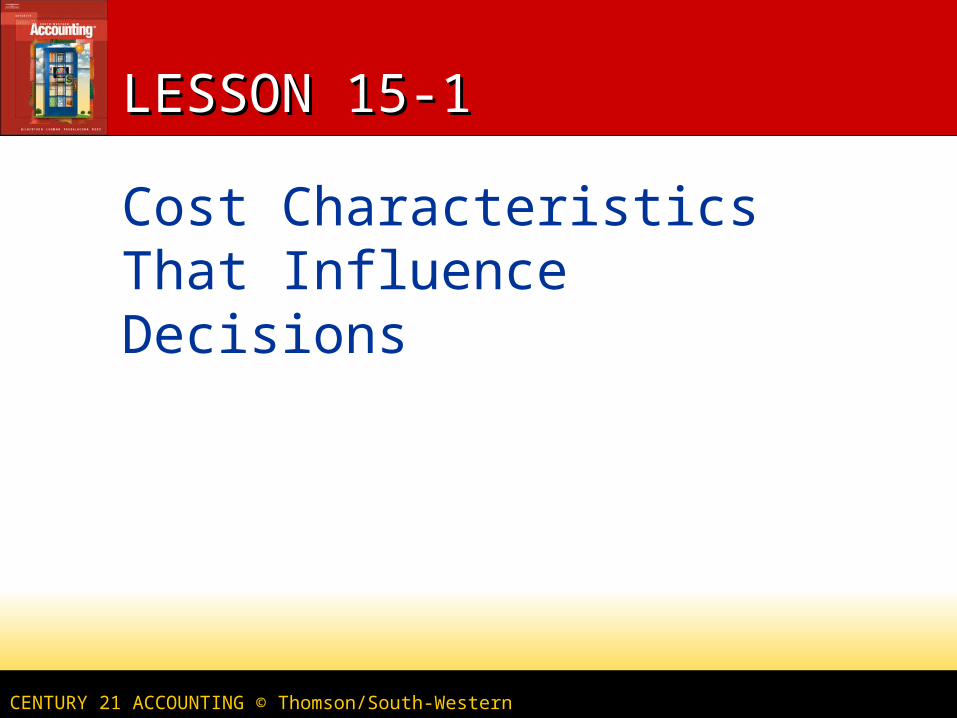

ABBREVIATED INCOME STATEMENTABBREVIATED INCOME STATEMENT page 445

All costs for a specific period of time are called total costs The above income statement shows the total cost of

merchandise sold was $118,800 and total selling expenses were $31,930

These totals show how much money was spent for these activities during a specific period of time

CENTURY 21 ACCOUNTING © Thomson/South-Western

3

LESSON 15-1

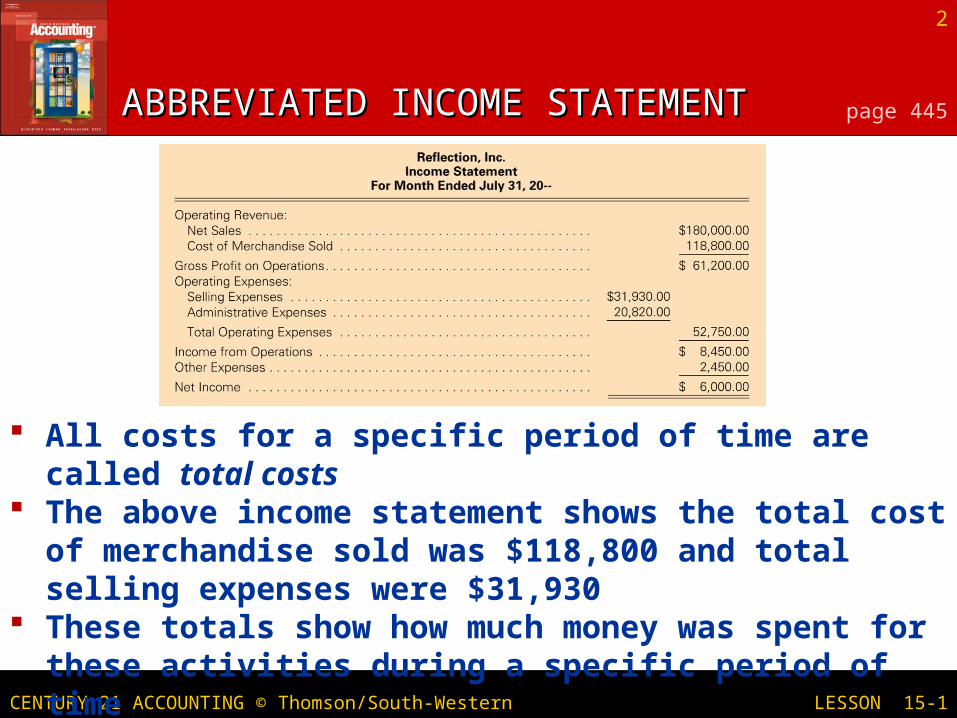

Cost of Merchandise Sold

Total Cost÷ Units Sold =

Cost of Merchandise Sold

Total Cost

$118,800.00 ÷ 36,000 = $3.30

CALCULATING COST OF CALCULATING COST OF MERCHANDISE SOLD UNIT COSTMERCHANDISE SOLD UNIT COST page 445

An amount spent for one unit of a specific product or service is called a unit cost

Units may be expressed in many different terms. Units should be expressed in terms that are

meaningful to the people who are responsible for the costs

CENTURY 21 ACCOUNTING © Thomson/South-Western

4

LESSON 15-1

VARIABLE COST CHARACTERISTICSVARIABLE COST CHARACTERISTICS page 446

Total costs can be separated into two parts: variable & fixed

Total costs that change in direct proportion to a change in the number of units are called variable costs

The total variable cost varies with a change in the number of units

Specifically, it increases The unit variable cost remains the

same regardless of the number of units

CENTURY 21 ACCOUNTING © Thomson/South-Western

5

LESSON 15-1

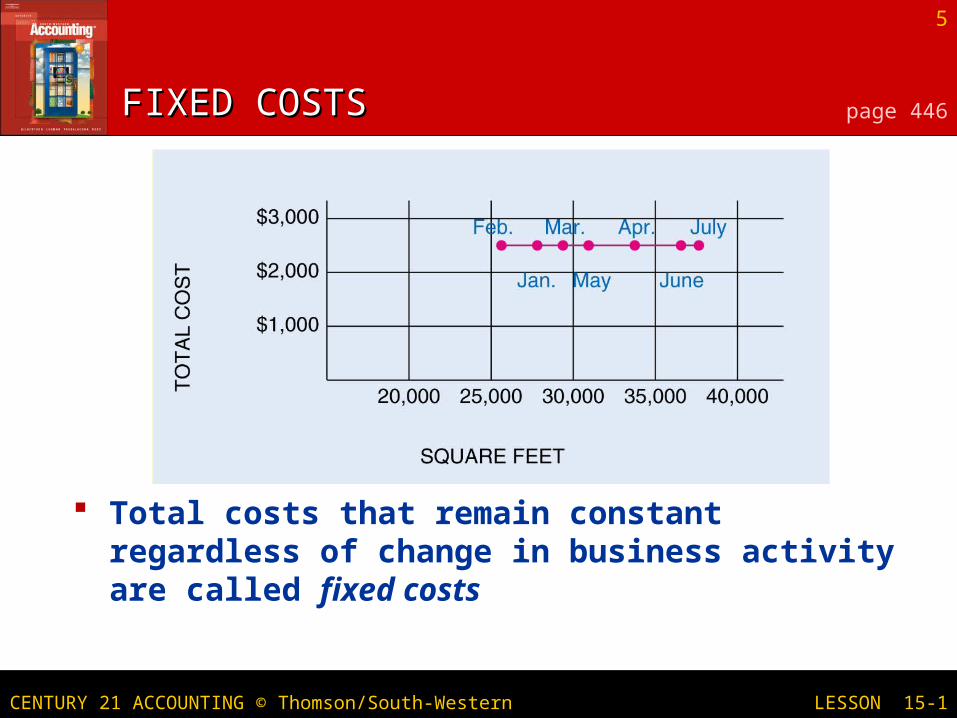

FIXED COSTSFIXED COSTS page 446

Total costs that remain constant regardless of change in business activity are called fixed costs

CENTURY 21 ACCOUNTING © Thomson/South-Western

6

LESSON 15-1

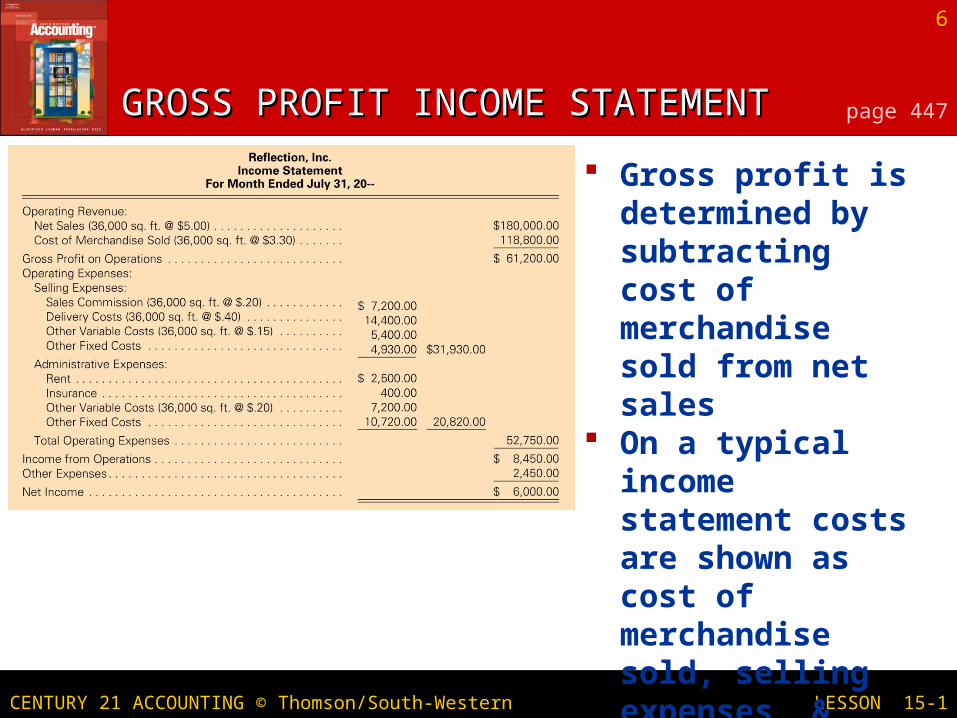

GROSS PROFIT INCOME STATEMENTGROSS PROFIT INCOME STATEMENT page 447

Gross profit is determined by subtracting cost of merchandise sold from net sales

On a typical income statement costs are shown as cost of merchandise sold, selling expenses, & administrative expenses

CENTURY 21 ACCOUNTING © Thomson/South-Western

7

LESSON 15-1

CONTRIBUTION MARGIN CONTRIBUTION MARGIN INCOME STATEMENTINCOME STATEMENT page 447

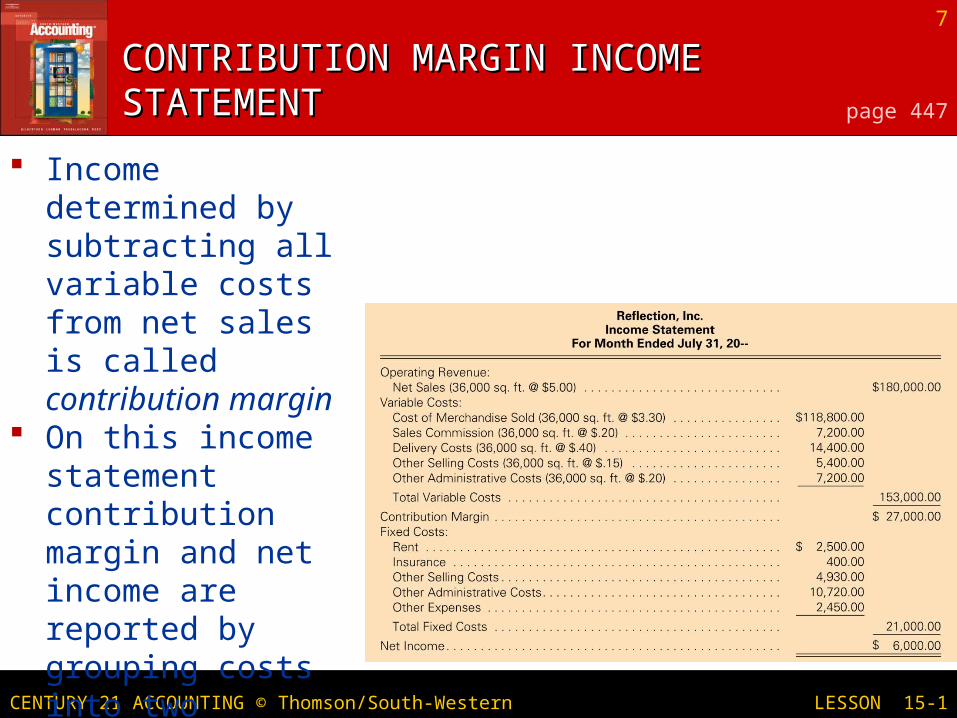

Income determined by subtracting all variable costs from net sales is called contribution margin

On this income statement contribution margin and net income are reported by grouping costs into two categories: variable and fixed

CENTURY 21 ACCOUNTING © Thomson/South-Western

8

LESSON 15-1

CONTRIBUTION MARGIN PER UNITCONTRIBUTION MARGIN PER UNIT page 448

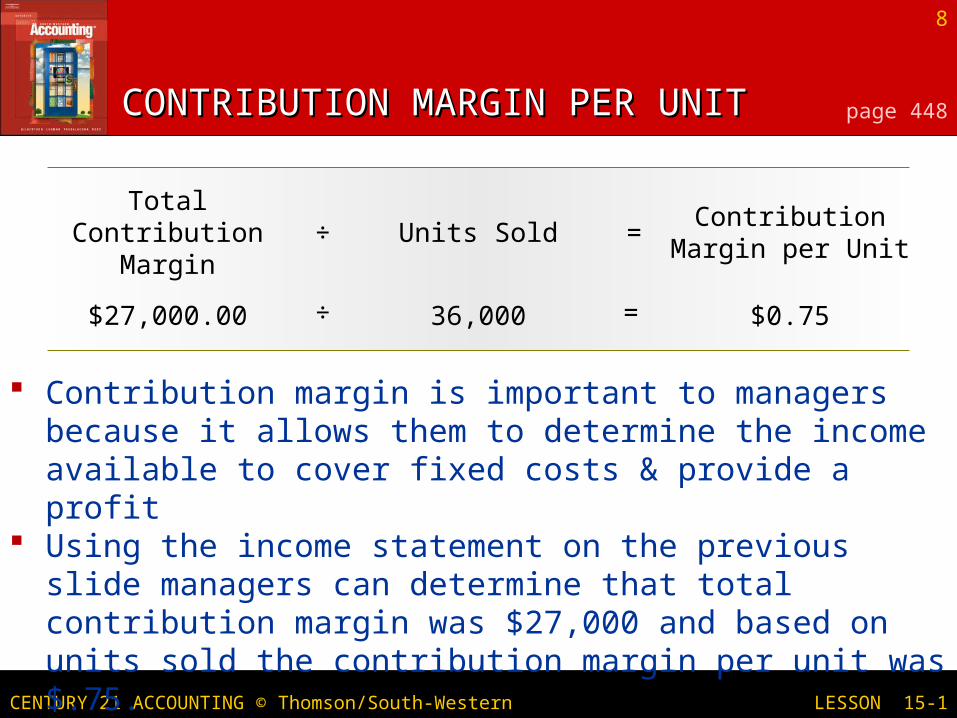

Total Contribution Margin

÷ Units Sold =Contribution Margin

per Unit

$27,000.00 ÷ 36,000 = $0.75

Contribution margin is important to managers because it allows them to determine the income available to cover fixed costs & provide a profit

Using the income statement on the previous slide managers can determine that total contribution margin was $27,000 and based on units sold the contribution margin per unit was $.75.

CENTURY 21 ACCOUNTING © Thomson/South-Western

9

LESSON 15-1

TERMS REVIEWTERMS REVIEW

total costs unit cost variable costs fixed costs contribution margin

page 450