Embed Size (px)

Citation preview

CENTURY 21 ACCOUNTING © Thomson/South-Western

LESSON 9-3LESSON 9-3

Accrued Expenses

CENTURY 21 ACCOUNTING © Thomson/South-Western

JOURNALIZING ACCRUED EXPENSESJOURNALIZING ACCRUED EXPENSES

Expenses incurred in one fiscal period but not paid until a later fiscal period are called accrued expenses

Four types of accrued expenses: Accrued interest expense Accrued salary expense Accrued employer payroll taxes expense Accrued federal income tax expense

2

LESSON 9-3

CENTURY 21 ACCOUNTING © Thomson/South-Western

3

LESSON 9-3

PrincipalInterest Rate

Time as Fraction of Year

Interest for 15 Days

=

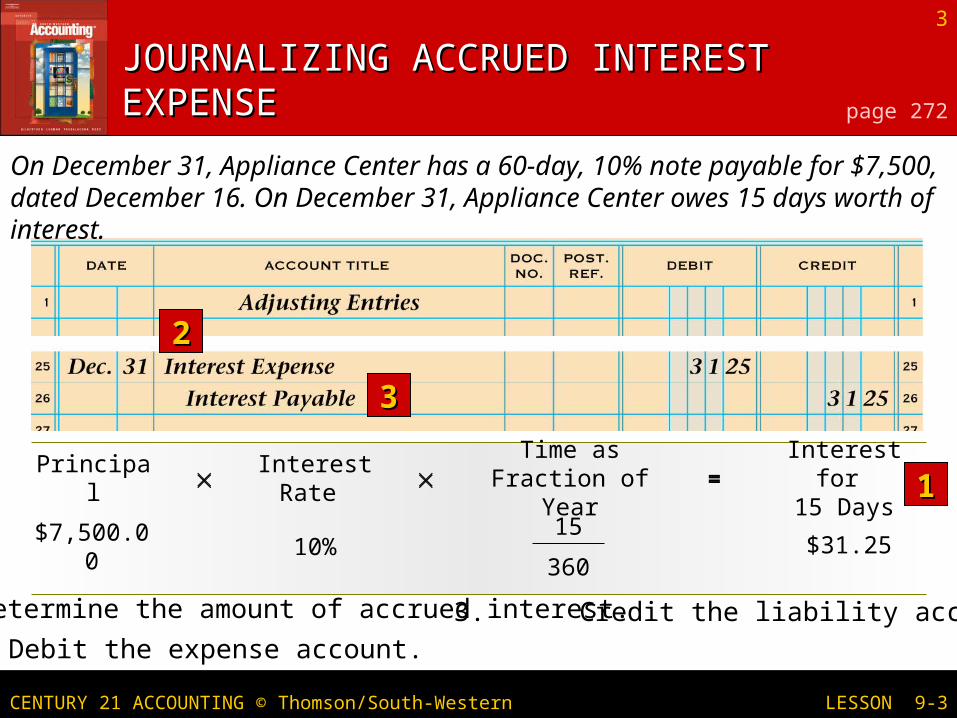

1. Determine the amount of accrued interest.

2. Debit the expense account.

3. Credit the liability account.

JOURNALIZING ACCRUED JOURNALIZING ACCRUED INTEREST EXPENSEINTEREST EXPENSE page 272

11

22

33

$7,500.00

10%

=

$31.2515

360

On December 31, Appliance Center has a 60-day, 10% note payable for $7,500, dated December 16. On December 31, Appliance Center owes 15 days worth of interest.

CENTURY 21 ACCOUNTING © Thomson/South-Western

4

LESSON 9-3

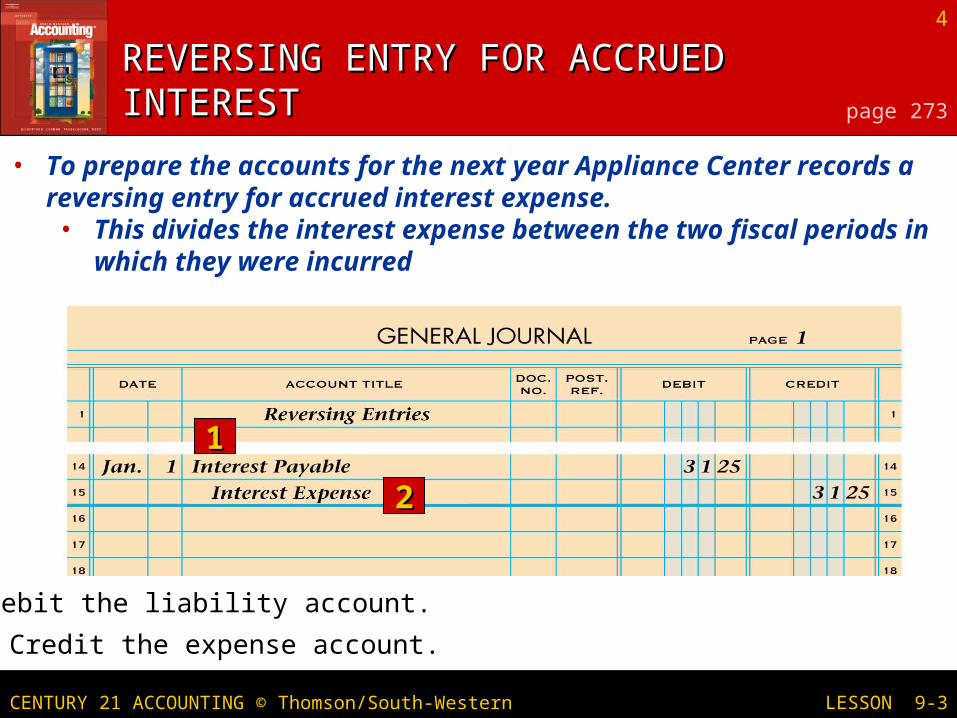

1. Debit the liability account.

2. Credit the expense account.

REVERSING ENTRY FOR REVERSING ENTRY FOR ACCRUED INTERESTACCRUED INTEREST page 273

11

22

• To prepare the accounts for the next year Appliance Center records a reversing entry for accrued interest expense.• This divides the interest expense between the two fiscal periods in which

they were incurred

CENTURY 21 ACCOUNTING © Thomson/South-Western

5

LESSON 9-3

Notes Payable

2/13 7,500.00 1/1 Bal. 7,500.00

Interest Expense

2/13 125.00 1/1 Bal. 31.25

PrincipalInterest Rate

Time as Fraction of Year

Total Interest Due

=

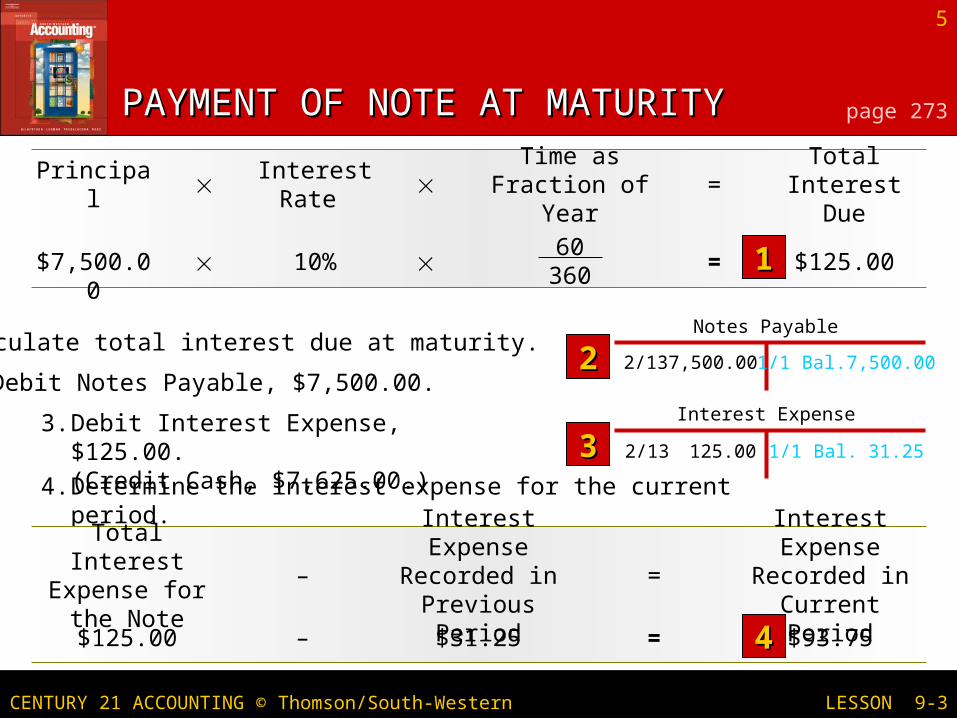

1. Calculate total interest due at maturity.

2. Debit Notes Payable, $7,500.00.

3. Debit Interest Expense, $125.00. (Credit Cash, $7,625.00.)

4. Determine the interest expense for the current period.

PAYMENT OF NOTE AT MATURITYPAYMENT OF NOTE AT MATURITY page 273

11

22

33

$7,500.00 10% = $125.0060360

Interest Expense Recorded in

Previous Period

Total Interest Expense for the

Note

Interest Expense Recorded in

Current Period– =

$125.00 – = $93.75$31.25 44

CENTURY 21 ACCOUNTING © Thomson/South-Western

6

LESSON 9-3

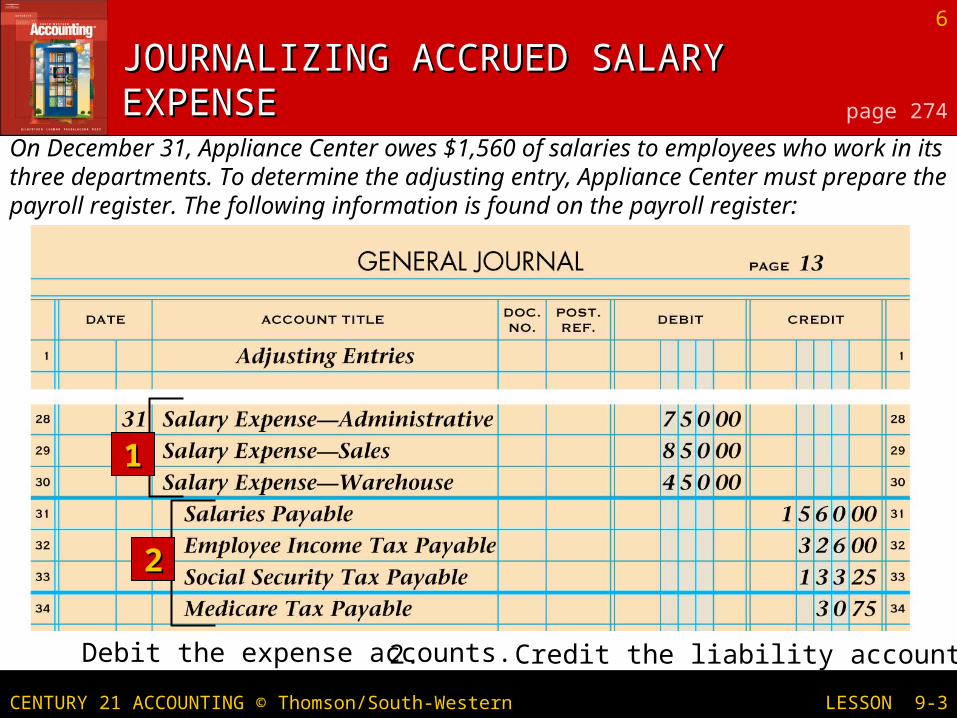

1. Debit the expense accounts. 2. Credit the liability accounts.

JOURNALIZING ACCRUED JOURNALIZING ACCRUED SALARY EXPENSESALARY EXPENSE page 274

11

22

On December 31, Appliance Center owes $1,560 of salaries to employees who work in its three departments. To determine the adjusting entry, Appliance Center must prepare the payroll register. The following information is found on the payroll register:

CENTURY 21 ACCOUNTING © Thomson/South-Western

7

LESSON 9-3

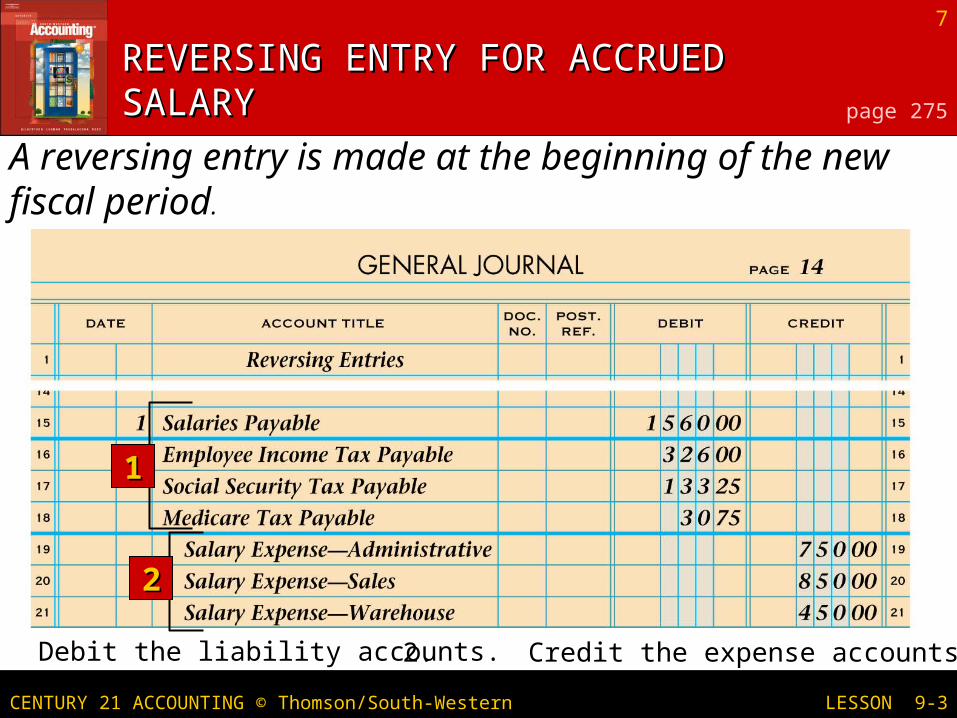

1. Debit the liability accounts. 2. Credit the expense accounts.

REVERSING ENTRY FOR REVERSING ENTRY FOR ACCRUED SALARYACCRUED SALARY page 275

11

22

A reversing entry is made at the beginning of the new fiscal period.

CENTURY 21 ACCOUNTING © Thomson/South-Western

8

LESSON 9-3

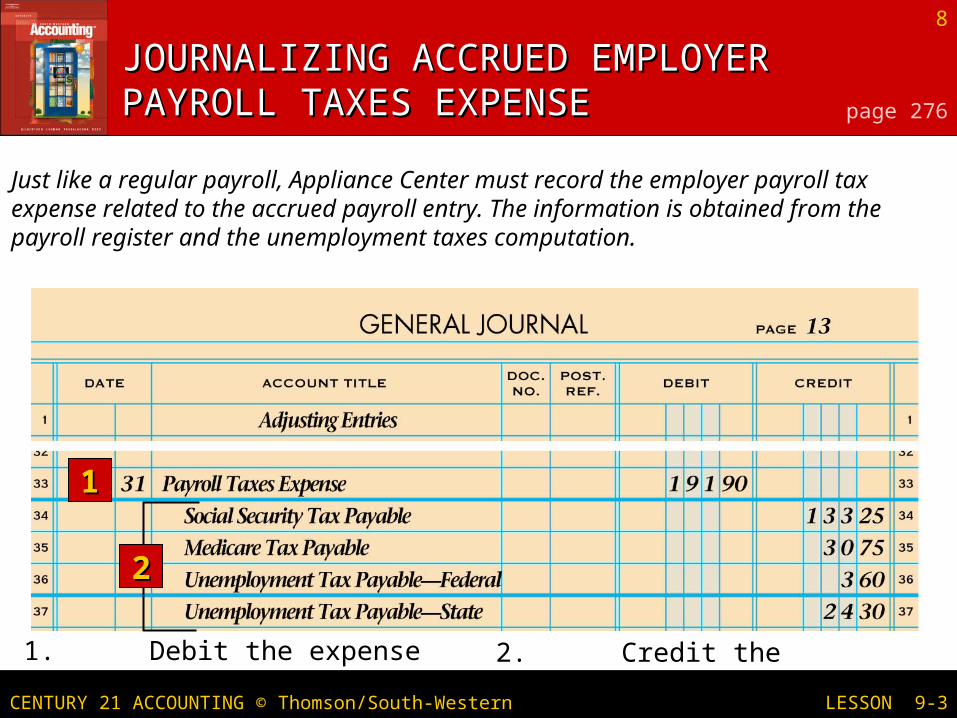

1. Debit the expense account. 2. Credit the liability accounts.

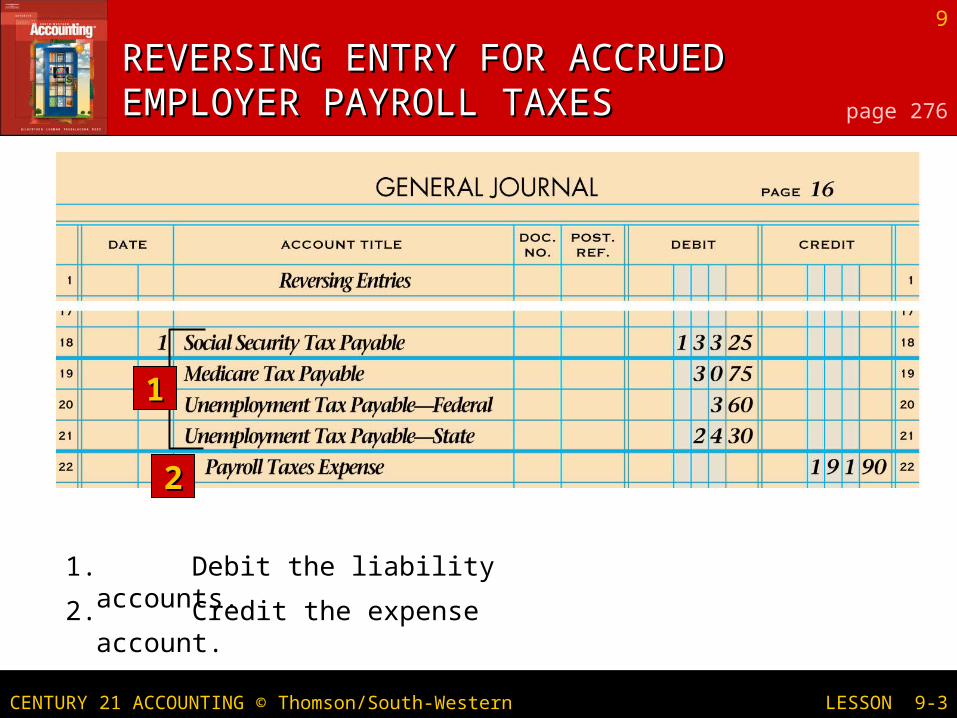

JOURNALIZING ACCRUED EMPLOYER JOURNALIZING ACCRUED EMPLOYER PAYROLL TAXES EXPENSEPAYROLL TAXES EXPENSE page 276

11

22

Just like a regular payroll, Appliance Center must record the employer payroll tax expense related to the accrued payroll entry. The information is obtained from the payroll register and the unemployment taxes computation.

CENTURY 21 ACCOUNTING © Thomson/South-Western

9

LESSON 9-3

1. Debit the liability accounts.

2. Credit the expense account.

REVERSING ENTRY FOR ACCRUED REVERSING ENTRY FOR ACCRUED EMPLOYER PAYROLL TAXESEMPLOYER PAYROLL TAXES page 276

11

22

CENTURY 21 ACCOUNTING © Thomson/South-Western

10

LESSON 9-3

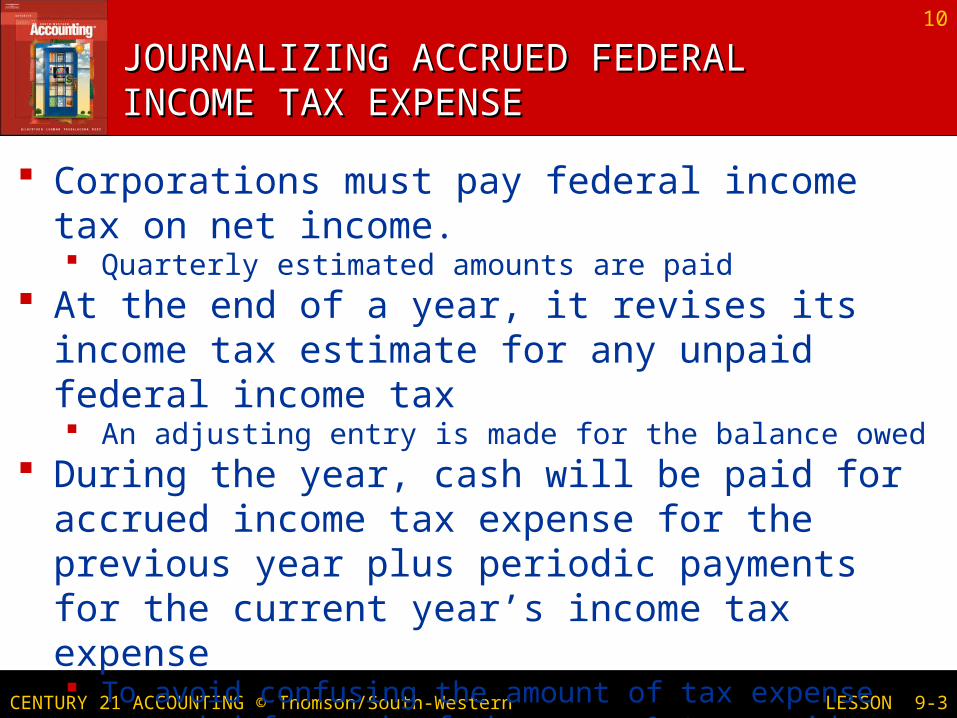

JOURNALIZING ACCRUED FEDERAL JOURNALIZING ACCRUED FEDERAL INCOME TAX EXPENSEINCOME TAX EXPENSE

Corporations must pay federal income tax on net income. Quarterly estimated amounts are paid

At the end of a year, it revises its income tax estimate for any unpaid federal income tax An adjusting entry is made for the balance owed

During the year, cash will be paid for accrued income tax expense for the previous year plus periodic payments for the current year’s income tax expense To avoid confusing the amount of tax expense recorded for each

of the years & to provide year-to-date income tax expense information, companies do not reverse this adjusting entry

CENTURY 21 ACCOUNTING © Thomson/South-Western

11

LESSON 9-3

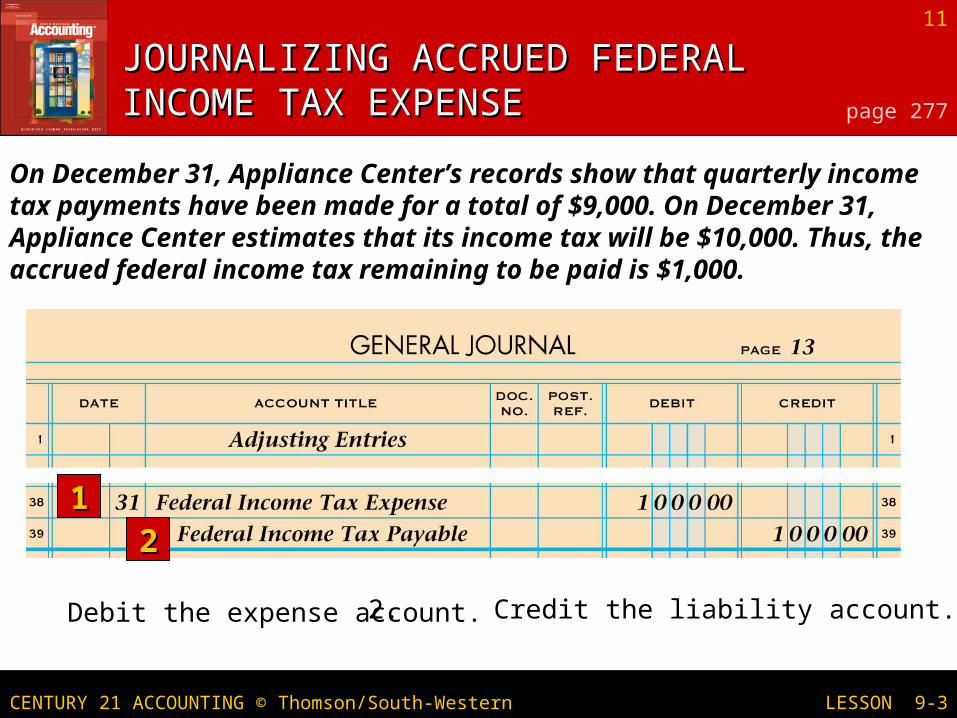

1. Debit the expense account. 2. Credit the liability account.

JOURNALIZING ACCRUED FEDERAL JOURNALIZING ACCRUED FEDERAL INCOME TAX EXPENSEINCOME TAX EXPENSE page 277

1122

On December 31, Appliance Center’s records show that quarterly income tax payments have been made for a total of $9,000. On December 31, Appliance Center estimates that its income tax will be $10,000. Thus, the accrued federal income tax remaining to be paid is $1,000.

CENTURY 21 ACCOUNTING © Thomson/South-Western

12

LESSON 9-3

TERM REVIEWTERM REVIEW

accrued expenses

page 279