Embed Size (px)

Citation preview

Bachelor thesis

CEO duality at S&P 500 and FTSE 100 companies

December 1st 2004

Sjoerd Arlman, 9900578

Accompanying professor: dr. C.M. van Praag

Faculteit der Economische Wetenschappen en Econometrie

Universiteit van Amsterdam

1

1. Introduction

Since the Cadbury commission published its report on corporate governance in 1992,

governance has been a widely published and hotly debated topic. The interaction between a

company and its share- and stakeholders, the way the board is run, the number of

independent directors and the salary of the CEO are all issues related to corporate

governance that have received quite some attention. In most countries the discussions

regarding corporate governance were given an extra push by the emergence of corporate

scandals at (formerly) well-respected firms like Enron, Tyco, Ahold and Parmalat.

A difficulty in corporate governance is that almost every country in the world has its own

way of doing and regulating business and therefore its own corporate governance system,

leading to considerable differences in corporate governance between countries.

One of the factors in corporate governance that is different all around the world concerns

the issue of CEO duality, which is the situation when the same person holds both the job of

Chief Executive Officer (CEO) and Chairman of the board of a firm. In some countries

especially countries that have a two-tier board CEO duality is non-existing. In other

countries it is almost taken for granted. For example, in 1987 Dalton and Kesner found that

for a small sample of US and UK firms, some 30% of the UK companies had the same

person as chairman and chief executive while the figure was 82% for the USA.1

For my own research I have compared the duality in US firms in the S&P 500 index with

UK firms in the FTSE 100 index. This research shows that only 4% of FTSE 100 companies

have the same chairman as CEO, while the figure for the S&P 500 companies is 76%.

Apparently in the 17 years since the research by Dalton and Kesner, more UK firms have

decided to split the top two management positions. In the USA the number of firms with

two different individuals as Chairman and CEO has also increased, but is still much lower

than in the UK. Therefore while both the UK and the USA are classified as having similar

1 Dalton, D.R., Kesner, I.F., p 39.

2

Anglo Saxon corporate governance and business structures, they are at least concerning

this duality issue quite different.

In this paper I will present the results of my research regarding CEO duality in the UK and

the USA in more detail. As the USA has a much lower degree of separation, I will look in to

the possible explanations for this trans-Atlantic difference.

Also I will look into two related topics.

The first concerns CEO remuneration. Entrenchment theory claims that entrenched CEO s

often earn more money than their peers, as they are able to influence or dictate board

remuneration decisions. It is often claimed that CEO duality has an increased chance of

leading to CEO entrenchment.2 I will research if CEO s who also occupy the chairman s seat

have a higher remuneration than their peers who are just CEO.

The second issue regards CEO tenure. According to a common succession theory an

outgoing CEO/Chairman will often stay on as chairman a number of years after having

retired as CEO. Furthermore, if after a period of time the incoming CEO has proven

himself capable, the former CEO who still holds the chairmanship will step down as

chairman, enabling the incumbent CEO to also become chairman.3 I will test this succession

theory by comparing the tenure of CEO s who also hold the chairmanship with CEO s who

have a predecessor running the board. My hypothesis is that the latter group has shorter

tenures than the former.

In the next section I will go into the theoretical issues of corporate governance, board

structure and CEO duality in more detail. The third section contains information about my

research and my research results. In the fourth section I will analyze the results of my

research and give possible explanations for the results. Also I will give an outlook into the

future regarding CEO duality. The fifth and final section contains a summary and conclusion

of my findings.

2 Among others by Morck, Schleifer and Vishny (1988) and Finkelstein and D Aveni (1994). 3 See for example Harrison, Torres and Kukalis (1988) and Vancil (1987).

3

2. Corporate governance and board structure

According to the definition given by the OECD, corporate governance is the set of

relationships between company management, board, shareholders and other stakeholders.

Important other elements are the structuring of objectives, the means of attaining those

objectives and the manner in which the company is monitored.4 Other definitions describe

corporate governance in terms of protection of (mainly minority) shareholders or prevention

of fraud and corporate scandals.

As business practices and differ between the various countries and regions, there are also

large differences in corporate governance practices. Customs that are completely normal in

one country may be unheard of in another. For example, the Netherlands uses a much

frowned upon cooptation system for the election of supervisory board members, which in

essence means that current board members select their peers.

Starting in the UK with the Cadbury Commission in 1992, there have been numerous

attempts in most developed (and some developing) countries to codify these governance

issues and set a (national) standard.5 Paradoxically while the USA is claimed by many to have

the most advanced corporate governance systems in the world, it is one of the few

developed countries which does not have a national code of corporate governance. Instead

the USA has restricted itself to occasional changes in listing requirements of the exchanges

and various discussion papers by different groups, ranging from investment funds like

CalPERS or IIS to business associations such as the Conference Board or the Business

Roundtable. Only in the past few years has the US resorted to stricter measures, including

legislation on a federal level such as the quite recent Sarbanes-Oxley act.

As mentioned there are large differences in business practices and corporate governance

around the world. One major international difference is in the structure of the board of

directors. Some countries have a so-called two-tier board system, with one executive board

that is responsible for the day-to-day management and one supervisory board that monitors

the executive board. Other countries have a one-tier system with just one board containing

4 OECD, p 2. 5 For a list of corporate governance codes in different countries, see http://ecgi.org/codes/

4

executives as well as non-executives. Most European companies operate a two-tier system,

while most Anglo-Saxon companies use the one-tier system. There are however exceptions,

for example the French mostly have one-tier boards.

In regard to that issue of board structure there is one quite sensitive difference, namely the

separation or not of the functions of chief executive and chairman. In two-tier board

systems, the separation between the two top jobs is almost implied. In the one-tier system

the results are more mixed, with some countries and companies opting for a unitary

leadership structure with the same person as CEO and chairman, and other companies

opting for a dual leadership structure which separates the two top jobs.

Before discussing the trade-offs between a unitary leadership structure (with one person as

CEO and chairman) as opposed to a dual leadership structure (with a separation between the

two most senior jobs), it is relevant to first go into the different roles of the board, the

chairman and the CEO.6 Although even these roles are the subject of academic debate, there

are a number of points that stand out.

Roles of the board, chairman and CEO

The most important roles of the board are to monitor management, review the strategy, and

pick executive directors. In doing this the board must be careful not to take over the

executive tasks from the CEO and his colleagues. However the board must also be careful

that it does not rubber-stamp everything the chief executive says and does. There is still

quite some discussion whether the board is the representative of the shareholders7 or the

firm in general.8

The chairman is responsible for the functioning of the board. This means that he runs the

board, sets the agenda and ensures that the other board members obtain information timely,

6 A fourth important group could be added to this list: shareholders. However, I will not go into the roles of shareholders in this paper. 7 Advocated by among others the Conference Board and in the papers of Condit and Hess (2003) and Vance (1983, in Finckelstein and d Aveni (1994)). 8 Advocated by among others the Combined Code on Corporate Governance in the UK (2003) and by some CEO s in the review by Spencer Stuart (2003).

5

clearly and accurately. The chairman should stimulate the other board members to take part

actively in discussion and assure that his peers are sufficiently skilled to perform their duties

as board member. While not the main person to communicate with shareholders, the

chairman should ensure that the views of shareholders are known to the board.9

As the name clearly indicated the CEO is the first and foremost executive responsible for

the day-to-day operations of the company. The chief executive is the main representative of

the company to all share- and stakeholders.

Duality or separation

The debate around the separation or integration of the jobs of CEO and Chairman is a

frequently debated topic in corporate governance. It is not difficult to see the potential

conflict of interest when the two functions are combined. As the chief executive is

monitored by the board of directors it is therefore in the CEO s interest to present

information to the board that makes his results look good. Therefore, having a CEO who is

also chairman of the board gives a situation where the CEO is basically marking his own

exam papers. 10 Mallette and Fowler (1992) argue that in combined roles the chairman of the

board must make decisions as chairman that influence his personal well-being as CEO,

potentially leading to a conflict of interest. The authors argue that as chairman the CEO can

set (and therefore influence) the board s agenda and the CEO can influence (if not control)

the nomination of directors for the board. Their research into the adoption of poison pills11

by companies shows that firms with dual leadership adopt less poison pills. Mallette and

Fowler therefore conclude in their paper that CEO duality can challenge a board s ability to

monitor executives.12

A CEO who can influence or even decide on the appointment of board members changes

the incentives for (independent) directors. Because of the power of the CEO, a reputation

for asking difficult (but necessary questions) may not be in a director s best interest, while a

9 Combined code, p 5. 10 Dedman (2002), p 345. 11 This is a strategy to avoid a hostile takeover bid, often by taking on large debts or otherwise diluting the value of the company s stock. 12 Mallette and Fowler (2002), p 1028.

6

reputation as yes man will most probably serve the director well.13 Kenneth Lay, former

CEO of Enron is supposed to have said that filling the board of directors was up to what

the CEO saw fit for the company at that moment.14 Jensen and Fuller (2002) argue that the

management rights must be separated from the control rights at all levels of the

organization, especially at the board level.15

Related research by Shivdasani and Yermack (1999) points out that when the CEO is

involved in the nomination process of directors firms are less likely to appoint aggressive

monitors or independent outsiders and are more likely to appoint gray directors with a

conflict of interest.16 Going even further, Mace (1986) has shown that in many cases

directors remain loyal to misguided CEO s.17

In a recent survey done by Spencer Stuart (2003) all of the CEO s interviewed indicated that

a good relationship between the chief executive and chairman was essential for the well

functioning of the board. Therefore simply appointing an outside (and unknown) director as

chairman is not as straightforward a solution as it seems. Besides the fact that CEO and

outside Chairman have to get along, an outsider will

ceteris paribus have less knowledge

about the firm and the business the firm is in. Besides, having a separate person as CEO and

chairman adds an extra layer in the firm s organization.

Therefore, the main tradeoff in the discussion of splitting roles of CEO and Chairman is

basically between efficiency because of unitary leadership or accountability with a dual

leadership structure.18 On the one hand, proponents of the agency cost theory argue that the

combination of the two functions leads to high chance of entrenchment of the chief

executive and dilutes the monitoring role of the board. They argue that the combination of

decision management and decision control is a fundamental flaw. Again, by also being

chairman of the board, a CEO is in essence monitoring his own performance.

13 Morck (2004), p 20. 14 However, according to Sonnenfeld (2004), the director attendance at Enron meeting is supposed to have been nearly perfect. 15 Jensen and Fuller (2002), p 9. 16 Shivdasani and Yermack (1999), p 1852. 17 Mace (1986) in Morck (2004), p 10. 18 Koningsberg (2004), p 35.

7

Furthermore Collier and Gregory (1999) provide evidence that a CEO who also fills the

function of chairman is negatively associated with the activity of the audit committee, one

possible proof for the dilution of board monitoring in the case of duality. As the recent

corporate governance scandals at companies such as Ahold, Parmalat and Enron have

shown, the auditing of a company is quite important.

The other side of the argument prefers unity of command at the top of the firm and a single

person who is accountable for firm outcomes vis-à-vis the different stakeholders.19

Proponents for these arguments assert that there are a number of costs associated with the

separation of the functions of the CEO and chairman. First of all there is the issue that is it

much more difficult for a non-CEO chairman to know the business sufficiently well.

According to Campbell (1995) this problem can even be made worse when the influence of

independent directors is increased due to the influence of the non-CEO chairman, thereby

increasing the voice of the non-experts . An easy solution for this issue is used by many

firms, namely to have the (former) CEO in the chairman s seat.

The second group of costs are agency costs. While an independent chairman reduces the

agency costs related to monitoring the CEO s behavior, it introduces the additional costs of

checking the chairman s conduct. Included in these costs are the abovementioned costs of

introducing another layer of organization in the firm.20

A third reason for firms not to split the two top jobs is the loss of clear responsibilities. In a

unitary leadership structure it is quite clear which person is responsible for all firm outcomes.

However as mentioned above, in a dual leadership structure there are costs associated with

the fact that there is not one person solely accountable for performance.21

As mentioned above, a major reason for firms to place a former CEO in the chairman s seat

is for orderly transition of the company management. Many firms maintain a succession

method wherein the outgoing CEO remains chairman until the new CEO is accustomed to

the job and can also take over the chairman s seat. In this theory, the prospect of becoming

19 Coles and Hesterley (2000), p 198. 20 Campbell (1995), p 107. 21 Brickley, Coles and Jarrell (1997), p 195.

8

chairman is another incentive for the CEO to do well. According to proponents, this

succession formula also leads to better use of the outgoing CEO s information.22

22 Arguments in this direction have been made in the articles by Coles and Hesterley (2000), Finkelstein and d Aveni (1994) and Brickley, Coles and Jarrell (1997).

9

3. Research into CEO duality in S&P 500 and FTSE 100

companies

In this section I will show the results of my empirical research into the practice of CEO

duality in S&P 500 and FTSE 100 firms. For both groups of firms the data was collected in

August of 2004.23 The composition and data for the S&P firms was accessed from The

Corporate Library (including Board Analyst) and individual company websites. Information

for the FTSE firms was acquired from FTSE, Hemscott and also from individual company

websites.

For the FTSE 100 firms the dataset only included the name of the firm and the names of the

CEO and chairman. The dataset for the S&P 500 firms included not only the names but also

among others the tenure of the current CEO, his or her annual salary, the number of shares

held and the position of the chairman.24

The data were checked for consistency, which resulted in the discarding of a number of

results from the list of S&P 500 companies, leaving 486 in the data set.25 No inconsistencies

were found in the FTSE 100 list. Only one firm is in both the S&P 500 as well as the FTSE

100, namely Carnival.

In my sample of 486 S&P 500 companies, I found that 24% (119 companies) had a different

chairman than CEO. For the FTSE 100 companies 96% had a split between the function of

CEO and chairman. In comparison with the results of Dalton and Kestner (1987), it seems

that the amount of firms with a separate chairman from CEO has grown in the past years.

However, while today the UK has almost complete separation between the office of

chairman and CEO, the Americans still prefer to combine the two jobs in more than three

out of four companies.

23 The author would have preferred comparing the duality data for 2004 with data for earlier years. However the data prior to 2003 was only attainable at great financial cost, which regrettably was outside the scope of this paper and the author s financial situation at this time. 24 Current CEO, former CEO, other executive director, outside director etc. 25 The main reasons to exclude certain entries were unavailability of information and changes due to takeovers or mergers.

10

CEO duality and CEO tenure

Of the 119 companies of the S&P 500 that had a different person occupying the position of

CEO and chairman, 69 firms had a former CEO as chairman. If we consider the succession

theory, meaning that former CEOs stay on as chairman until the incumbent is proficient

enough, we would suspect that the current tenure for CEO s in these companies to be

relatively short. The data supports this hypothesis. In my dataset of 486 firms, the average of

the CEO s tenure in all firms is 6.3 years. However, the average tenure for CEO s who are

not chairman is 3.4 years and even less at 2.7 years for companies with a former CEO as

chairman. In companies with the current CEO doubling as chairman, the average tenure is

7.2 years. These last results could also point out that a combined CEO/Chairman has

enough power to remain in the job for quite some time, giving some strength to the

entrenchment objections of the opponents of unitary leadership structure. Also the results

could point out that the succession theory is valid, as the CEO tenure of companies with a

former CEO in the chairman s seat is significantly lower than other companies. At a 95%

confidence level all differences in tenure are statistically significant.26

One of the factors that I did not take into account in my research was the fact that in a

number of firms with a former CEO as chairman that particular person is one of the

founding fathers of the company. Being founding father this person will more often than

not remain chairman, not stepping down for the incumbent CEO even if the latter performs

well. Examples of these kinds firms are Intel, Microsoft, Analog Devices and E-Bay. The

data shows that the tenure for the current CEO in these firms is decidedly higher than in

other firms with a former CEO as chairman. Discarding these firms from the dataset would

probably lead to an even shorter tenure for CEO s with a predecessor in the chairman s seat

and therefore give even more strength to the succession theory. The same argument could

also be made for firms with a (grand)child of the founder as chairman, such as Ford or (until

a few years ago) Philips.

CEO duality and CEO remuneration

26 For the statistical results, please refer to appendix 2.

11

Another factor I looked at was total CEO compensation for S&P 500 executives in 2003.

The average total annual compensation for CEO s in the S&P 500 was $ 2.71 million. The

average for firms with a single person as CEO and chairman is a bit higher, at $ 2.80 million

annually. This figure is lower in firms where a former chief executive is chairman ($ 2.63

million) and is even lower in firms where the chairman is neither current nor former chief

executive ($ 2.15 million). CEO s who also hold the chairmanship earn on average 30%

more than their peers who are not in the chairman s seat themselves or have a predecessor in

that position. At a 95% confidence level, only this last difference is significant. However,

considering the fact that a combined CEO/chairman is in fact doing both jobs, and the

American tendency to overcompensate executives, I do not find the difference in

compensation stunningly large.27

27 For the statistical results, please refer to appendix 2.

12

4. Interpretation of results and discussion

As mentioned before, in 1988 only 70% of UK companies had a split between the jobs of

CEO and chairman compared to the 96% of today.28 The movement to almost complete

separation between chief executive and chairman gained an impulse with the Cadbury

commission on corporate governance in 1992. The commission recognized that the

combination of the two functions was a considerable concentration of power. It therefore

suggested that the role of the chairman should in principle be separate from that of the chief

executive.29 A decade later the combined corporate governance code plainly stated that the

roles of chairman and chief executive should not be exercised by the same individual. 30 Note

however that the UK has a so called principles system , which means that the provisions of

the code are not binding in its entirety. A firm may deviate from the code, as long as it

explains its reasons to do so.31

The United States operates a different corporate governance system. The US system is not

principles based like in the UK but rather more rules based , built on the strict application of

rules and regulations. Although the unitary leadership structure is not obligatory in the USA

it is frequently used, probably due to sociological reasons. Historically, independent

chairmen have only been acceptable in the US during transitional periods or when the CEO

is weak or new to the job. A combination of the two jobs is seen as powerful in the US,

probably also reflecting the American idea of the CEO as Superman.32 There is a saying in

the US that every American wants to become president. If the presidency of the USA is not

achievable, a company presidency (combined with the chairmanship and job as CEO) is the

next best thing.

28 Unfortunately the dataset for the 1998 data is a different one than the one used in this paper, hampering a completely sound comparison between the two figures. However the degree of firms with a dual leadership structure has probably increased in the past decades. 29 Cadbury et al (1992), p 20. 30 Financial Reporting Council (2003), p 6. 31 This system, which is gaining in popularity both inside as well as outside of the UK, is commonly known as a comply or explain

or even an apply or explain or blame and shame system. 32 Koningsberg (2004), p 35.

13

As shown in my research above, the succession theory is one of the reasons given to split the

jobs, even if only temporary.

Another situation in which firms choose to split the two top jobs is in the case of a merger

or major acquisition. Often the two CEOs will agree that one becomes CEO of the merged

company, while the other takes the chairmanship of the board. For example, in the recent

Bank of America and Fleet Boston merger, the Bank of America CEO and chairman

Kenneth Lewis became CEO of the merged firm, while Charles Gifford CEO and chairman

of Fleet Boston became chairman.

One of the main drawbacks put forward by the opponents of CEO duality is (the risk of)

CEO entrenchment. As my research shows, CEO s that also hold the job of chairman have

been in office for more than seven years, ceteris paribus increasing the chance of

entrenchment. Research in this field, most notably by Morck, Shleifer and Vishny (1988)

shows that firms with CEO duality are less likely to fire the CEO after bad performance,

strengthening the fear for entrenchment. Also Brickley and James (1987) have shown that

firms that combine the function of chairman and CEO tend to be larger with older CEO s,

longer tenures and larger CEO share ownership. The risk of entrenchment is quite high in

these cases.

My research has shown that CEO s who also hold the job of chairman have a relatively long

tenure in comparison with their peers. Note that I recognized three categories, namely firms

where CEO and chairman are the same person, firms with a former CEO as chairman and

firms with someone other than the current or former CEO as chairman. The average tenure

is therefore not an interesting number. More interesting is the fact that the difference in

CEO tenure between firms with unitary leadership structure is significantly higher than in

firms with a dual leadership structure. Maybe the CEO s who are chairman are doing a better

job, but maybe they are in a better position to entrench themselves in the company.

Duality and firm performance

This last issue also raises the question of the relationship between CEO duality and firm

performance. Over the past years many researchers have tried to link board structure and

14

CEO duality to firm performance, unfortunately with almost as many different conclusions

as there are papers written on the topic.

Brickley, Coles and Jarrell (1997) point out that firms with a separate chairman and CEO do

not have an increased (accounting) profit. According to these authors the stock value of

firms switching from a unitary to a dual leadership structure actually decreased.

In contrast to the above conclusion, Palmon and Ward (2001) have shown that a change

from a unitary to dual leadership structure leads to positive abnormal returns for large firms,

but for negative abnormal returns for small firms. Other authors however have again

reached other conclusions. Rechner and Dalton (1991) found that firms with a dual

leadership situation consistently outperformed firms with unitary leadership in the period

1978 to 1983.

The recent research by Fosberg and Nelson (1999) supports both sides. In firms with

significant agency problems the authors show that there is a significant increase in

performance following a change in leadership structure. However, for firms shifting to dual

leadership as part of their succession process show no evidence of changed performance

following the change in structure.

There are also a number of researches that do not show any result of performance due to

CEO duality.33 Most interesting in this field is the paper by Coles and Hesterley (2000) who

write that the inability to show returns one way or the other for either unitary or dual firms

may result from the fact that the separation is used by many researchers as a proxy for

independence. However the authors argue that a dual leadership structure is not a guarantee

for independence.

This last point raises an interesting issue. The general idea behind the split between CEO

and chairman is the fact that it stimulates the board to perform better and more

independently of management. If one is a strong believer in agency theory, it would indeed

seem wise to make an independent (or outside) director chairman of the firm. However, the

33 Finckelstein and d Aveni (2000), p4, have quite an extensive overview on the research regarding this topic.

15

fact that there are two different people performing the job of CEO and chairman does not

per se lead to better governance. An independent chairman (or board) would not guarantee

better monitoring and/or performance. Directors simply need to be honest and decent in

their jobs. The firm itself requires a good strategy. A well functioning corporate governance

system is of course important, as it reduces the chances firms can hide bad results.

Up to this point I have discussed the various reasons firms have for choosing a particular

governance model and I have shown what the past and current trends are. In the following

section I would like to go into future developments regarding CEO duality.

Future developments

In my opinion an increasing number of firms will decide to split the functions of CEO and

chairman in the future. I recognize a number of trends and recent events that support this

theory.

First of all there are increasing numbers of corporate governance codes and exchange listring

requirements recommending or even mandating a split in the two jobs. As mentioned the

different codes in the UK strongly urge companies to separate the functions. On the other

side of the Atlantic the results are mixed. The New York Stock Exchange (NYSE) does not

say anything about CEO duality in its listing requirements. However the NYSE itself has

split the function of chairman and chief executive in its own organization.34 Given the old

aphorism you lead by example , the NYSE might well be setting a standard.

Business groups, such as the Business Roundtable or the Conference Board, have conflicting

ideas. The Conference Board urges companies to at least install an independent lead director

if not an independent chairman.35 The Business Roundtable however is very positive about

the American governance model stating that most American corporations are well served

by a structure in which the CEO also serves as chairman of the board. However the

34 The listing requirements were made under the leadership of CEO and chairman Richard Grasso. Some claim that the recent split of these top jobs at the NYSE are due to the situation left by Grasso. 35 The Conference Board (2003), p 19.

16

Business Roundtable also writes that every company should make its own judgments

regarding the separation of CEO and chairman.36

Another recent factor which might shift the balance towards more separation of top jobs is

the growing amount of work needed from the top executives at firms to comply with

increasing government laws and regulations. The workload for CEO s and chairmen will

probably increase greatly as an effect of the Sarbanes Oxley Act in the USA and the

Financial Services Action Plan in the EU. It will therefore be increasingly difficult and time

consuming for one person to perform all that work.

The most important group however to mandate a separation, are of course the owners of the

company. Recently there has been an increasing number of investors who demand

separation between the top jobs for them to invest in the firm. While not going as far as

mandating or recommending a split, the California Public Employees Retirement System

(CalPERS) has stated in their 1998 governance principles that the traditional combination of

the jobs should be re-evaluated.37 Other investors go further and do demand a separation. In

a speech made in June 2004, Jan Willem Baud, the CEO of NPM capital, stated that NPM in

the future would only consider investing in companies which adhered to certain corporate

governance practices, one of which was a split in functions between the chairman and the

chief executive.

There has also been an great increase in shareholder proposals urging the adoption of a dual

leadership structure. In the USA in 2002 there were only four such proposals handed in,

while in 2003 there were more than 25 proposals urging the separation between the top jobs.

Most proposals were handed in by labor organizations such as the AFL-CIO, but there are

an increasing number of proposals being handed in by individuals.38

36 Business Roundtable (2002), p 11. 37 Corporate Governance Core Principles & Guidelines (1998), p 10. 38 Taub (2003) http://www.cfo.com/article.cfm/3008374

17

Furthermore, in a research by McKinsey (2000) over 80% of investors say they would be

prepared to pay more for the shares of well-governed companies than those of poorly

governed companies. 39

Other McKinsey surveys show that 72% of directors and 69% of investors support a

separation of CEO and chairman. The main opponent in the eyes of the directors to

splitting the jobs is the CEO.40

There is one other important factor that might shift the balance in favor of separation of

CEO and chairman. In the past corporate governance has been seen as a soft topic, with

little direct impact on company performance or cost of doing business. Recently however,

Fitch Ratings, Standard & Poor s and Moody s, all three credit rating agencies, have stated

that they will use corporate governance measurements in determining credit ratings,

including measurements on (non)independent chairmen.

In 2002 another McKinsey survey found that shareholders were prepared to pay a premium

of 14% on stocks of well-governed companies.

Therefore, in the future, good corporate governance or lack of it will have a direct effect

on the cost of capital for the company and the decisions investors make whether to invest in

the company or not. I assume that when more and more institutions base their investment

and rating activities on certain issues regarded as best practices, that the firms eventually will

not be able to resist the pressure to adapt to these best practices. Eventually due to these

factors, the combination of chairmanship and CEO may not be an option.

Up until now I have discussed reasons why the Americans might adopt more dual leadership

structures in their firms. However it might well be that Europeans increasingly adopt the

unitary leadership system. In contrast to the corporate governance codes in place, an

increasing number of European firms are appointing former CEO s as chairmen. The

Financial Times reported that a small majority (16) of Germany s top 30 firms have a former

39 McKinsey & Co (2000) 40 Mckinsey (2003) US Directors Survey And (2004) US Institutional Investors Survey.

18

CEO as chairman, with more firms planning to do so soon. The next step the Germans (and

other Europeans) could take is directly appointing their incumbent CEO s as chairman.

19

5. Summary and conclusion

In this paper I have researched the degree of CEO duality at S&P 500 and FTSE 100

companies. In 1987 Dalton and Kesner found that 30% of UK companies but 82% of US

companies have the same person as chairman and chief executive. My own research results

from 2004 show that 76% S&P 500 companies have the same chairman as chief executive,

while for FTSE 100 companies, it is only 4%.

Many reasons are given for the absence of a separation in the United States. One of the main

reasons quoted for the difference is the CEO succession method in the USA. I tested this

succession theory by comparing the average tenure for CEO s in different situations. The

average tenure for all companies in the S&P 500 was 6.3 years. In companies with a dual

CEO and chairman, the tenure was higher at 7.2 years. For companies with a different

person as CEO the average was 3.4 years, and even lower for companies with a former CEO

as chairman at 2.7 years. My research shows that in firms with a former CEO as chairman

the incumbent CEO is usually quite new to the job, possibly supporting the succession

theory. The differences in tenure are statistically significant at the 95% confidence level.

But this difference in tenure can also support the entrenchment theory. The above results

show that CEO tenure in firms with a dual CEO and chairman is on average more than

twice as long as in firms where a different person is chairman. Based on these figures, it is

not difficult to support the thesis that duality leads to entrenchment.

Another factor I researched that can point to CEO entrenchment is CEO compensation.

According to my research, firms with a single CEO/Chairman pay that person on average $

2.8 million. For split firms the average is $ 2.63 million with a former CEO as chairman and

even less at $ 2.15 million when the chairman is neither current nor former CEO. Only the

difference in pay between this last group and the group of combined CEO/Chairman is

statistically significant. However, as a single person as both Chairman and CEO is in fact

doing both jobs, I do not find the difference in pay scales between the groups large enough to

support the entrenchment theory on this point.

20

Finally I have looked at trends and movements regarding corporate governance on the point

of CEO duality. In general most trends point to an increase of separation between the jobs

of chairman and chief executive.

First of all, an increasing number of corporate governance codes is recommending a

separation between chairman and chief executive, partially due to the increased workload

following legislation like Sarbanes Oxley in the USA and the Financial Services Action Plan

in the EU.

Secondly, an increasing number of shareholders are urging the adoption of a dual leadership

structure. An increasing number of proposals are being handed in at shareholder meetings

urging the separation, and institutional investors are increasingly demanding that companies

adhere to certain corporate governance best practices including separation of CEO and

chairman before they invest in a company.

Thirdly there is the fact that corporate governance is starting to affect the cost of doing

business for companies. Credit rating agencies are increasingly using certain governance

measurements in determining the credit rating for companies. Surveys have also found that

investors are prepared to pay a premium for well governed companies. Both groups

appreciate separating the two top jobs.

However, while it is useful, the separation of chairman and chief executive per se does not

lead to better governance. Investors are wise to keep that in mind.

21

Appendix 1: Literature list

Baliga, B.R., Moyer, R.C., Rao, R.S., 1996, CEO duality and Firm Performance: What s the Fuss? . Strategic Management Journal, Vol. 17, No. 1, 41-53.

Brickley, J.A., Coles, J.L., Jarrell, G., 1997, Leadership Structure: Separating the CEO and Chairman of the Board . Journal of Corporate Finance 3, 189-220.

Brickley, J.A., James, C.M., The Takeover Market, Corporate Board Composition, and Ownership Structure: The Case of Banking . Journal of Law & Economics, Vol 30, No 1, 161-180.

Business Roundtable, 2002, Principles of Corporate Governance . White Paper.

Cadbury, A. et al, 1992, Report of the Committee on the Financial Aspects of Corporate Governance .

California Public Employees Retirement System, 1998, Corporate Governance Core Principles & Guidelines .

Campbell, A., 1995, The Cost of Independent Chairmen . Long Range Planning, Vol. 28, No. 6, 107-108.

Carapeto, M., Lasfer, M., Machera, K., 2004, Does the splitting of the roles of CEO and Chairman create value? . Paper for Second European Academic Conference on Internal Audit and Corporate Governance, Cass Business School, 22-23 April 2004.

Coles, J.W., Hesterly, W.S., 2000, Independence of the Chairman and Board Composition: Firm Choices and Shareholder Value . Journal of Management, Vol. 26, No. 2, 195 214.

Collier, P., Gregory, A., 1999, Audit Committee Activity and Agency Costs . Journal of Accounting and Public Policy 18, 311-332.

Condit, M.B., Hess, E.D., 2003, Is it Time for the Non-Executive Chairman? . The Corporate Board, Jan/Feb 2003, 1-4.

Conference Board, 2003, Commission on Public Trust and Private Enterprise . Findings and Recommendations. http://www.conference-board.org/

Dalton, D.R., Kesner, I.F., 1987, Composition and CEO Duality in Boards of Directors: An International Perspective . Journal of International Business Studies, Vol 18, No 3, 33-42.

Davis Global Advisors, 2002, Leading Corporate Governance Indicators 2002 . http://www.davisglobal.com/

22

Dedman, E., 2002, The Cadbury Committee Recommendation on Corporate Governance

A Review of Compliance and Performance Impacts . International Journal of

Management Reviews. Volume 4, Issue 4, 335-352.

Donaldson, L., Davis, J.H., 1991, Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns . Australian Journal of Management, Vol 16, No 1, 49-65.

Fama, E.F., Jensen, M.C., 1983, Separation of Ownership and Control . Journal of Law and Economics, Vol. 26.

Financial Reporting Council, 2003, Combined Code on Corporate Governance . http://www.asb.org.uk/

Finkelstein, S., D Aveni, R.A., 1994, CEO Duality as a Double-Edged Sword: How Boards of Directors Balance Entrenchment Avoidance and Unity of Command . The Academy of Management Journal, Vol 37, No 5, 1079-1108.

Fosberg, R.H., Nelson, M.R., 1999, Leadership Structure and Firm Performance . International Review of Financial Analysis, Vol 8, 83-96.

Harrison, J.R., Torres, D.L., Kukalis, S., 1988, The Changing of the Guard: Turnover and Structural Change in the Top-Management Positions . Administrative Science Quarterly, Vol 33, No 2, 211-232.

Jensen, M.C., Fuller, J., 2002, What's a Director to do? . Harvard NOM Research Paper No 02-38.

Jensen, M.C., Meckling, W.H., 1976, Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure . Journal of Financial Economics, Vol 3, No 4, 305-360.

Keenan, J., 2004, Corporate Governance in UK/ USA Boardrooms . Corporate Governance, Vol 12, No 2, 172-176.

Koningsburg, D., 2003, Corporate Governance, UK v US: Who s in the Lead? . Treasury Management International. 34-36.

Lucier, C., Schuyt, R., Handa, J., 2003, CEO Succession 2003: The Perils of Good Governance , Booz Allen Hamilton.

Malette, P., Fowler, K.L., 1992, Effects of Board Composition and Stock Ownership on the Adaption of Poison Pills . The Academy of Management Journal, Vol 35, No 5, 1010-1035.

Morck, R., Schleifer, A., Vishny, R.W., 1988, Alternative Mechanisms for Corporate Control . The American Economic Review, Vol 79, No 4, 842-852.

23

Morck, R., 2004, Behavioral Finance in Corporate Governance Independent Directors and Non-Executive Chairs . Harvard Institute of Economic Research Discussion Paper Number 2037.

New York Stock Exchange, 2004, New Governance Architecture . http:/ / www.nyse.com/

Organisation for Economic Co-operation and Development, 1999, OECD Principles of Corporate Governance . http:/ / www.oecd.org/

Palmon, O., Wald, J.K., 2002, Are Two Heads Better Than One? The Impact of Changes in Management Structure on Performance by Firm Size . Journal of Corporate Finance 8, 213226.

Peters, J.F.M. et al, 1997, Corporate Governance in Nederland. De Veertig Aanbevelingen .

Pillsbury Winthrop, 2003, Another Growing Trend in Corporate Governance Best Practices: Separation of the Positions of Chairman and Chief Executive Officer . http://www.pillsburywinthrop.com/

Rechner, P.L., Dalton, D.R., 1991, CEO Duality and Organizational Performance: A Longitudinal Analysis . Strategic Management Journal, Vol 12, No 2, 155-160.

Shivdasani, A., Yermack, D., 1999, CEO Involvement in the Selection of New Board Members: An Empirical Analysis . The Journal of Finance, Vol 54, No 5, 1829-1853.

Sonnenfeld, J., 2004, Good Governance and the Misleading Myths of Bad Metrics . Academy of Management Executive, Vol 18, No 1, 108-113.

Spencer Stuart, 2003, Managing Boards in Challenging Times: Perspectives from 12 FTSE-100 CEO s . http://www.spencerstuart.com/

Taub, S., 2003, Coming: Surge in Proxy Battles . http://www.cfo.com/article.cfm/3008374

Vancil, R.F., 1987, A Look at CEO Succession . Harvard Business Review, Vol 65, No 2, 107-117.

24

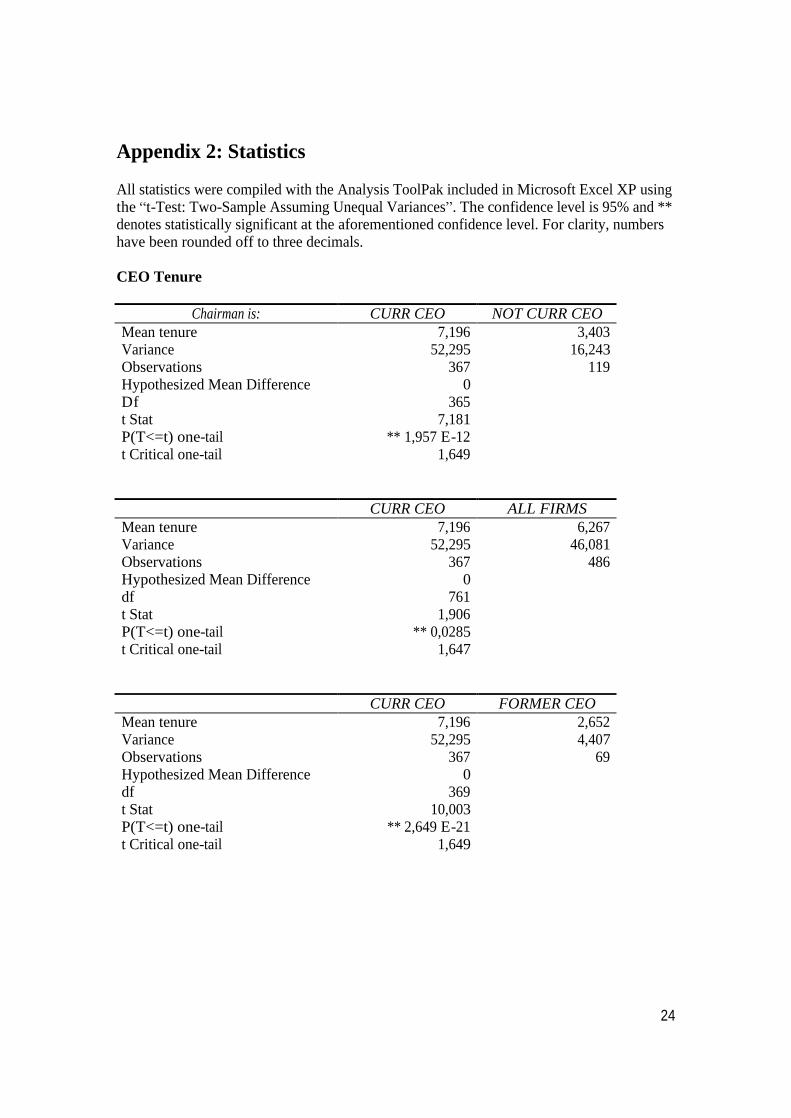

Appendix 2: Statistics

All statistics were compiled with the Analysis ToolPak included in Microsoft Excel XP using the t-Test: Two-Sample Assuming Unequal Variances . The confidence level is 95% and ** denotes statistically significant at the aforementioned confidence level. For clarity, numbers have been rounded off to three decimals.

CEO Tenure

Chairman is: CURR CEO NOT CURR CEO Mean tenure 7,196

3,403

Variance 52,295

16,243

Observations 367

119

Hypothesized Mean Difference 0

Df 365

t Stat 7,181

P(T<=t) one-tail ** 1,957 E-12

t Critical one-tail 1,649

CURR CEO ALL FIRMS Mean tenure 7,196

6,267

Variance 52,295

46,081

Observations 367

486

Hypothesized Mean Difference 0

df 761

t Stat 1,906

P(T<=t) one-tail ** 0,0285

t Critical one-tail 1,647

CURR CEO FORMER CEO Mean tenure 7,196

2,652

Variance 52,295

4,407

Observations 367

69

Hypothesized Mean Difference 0

df 369

t Stat 10,003

P(T<=t) one-tail ** 2,649 E-21

t Critical one-tail 1,649

25

NOT CEO FORMER CEO Mean tenure 3,403

2,652

Variance 16,243

4,407

Observations 119

69

Hypothesized Mean Difference 0

df 184

t Stat 1,678

P(T<=t) one-tail ** 0,0475

t Critical one-tail 1,653

CURR CEO NOT CUR/FMR CEO

Mean tenure 7,196

4,440

Variance 52,295

31,109

Observations 367

50

Hypothesized Mean Difference 0

df 73

t Stat 3,152

P(T<=t) one-tail ** 0,001

t Critical one-tail 1,666

CURR/FMR CEO NOT CUR/FMR CEO

Mean 6,477

4,440

Variance 47,445

31,109

Observations 436

50

Hypothesized Mean Difference 0

df 67

t Stat 2,383

P(T<=t) one-tail ** 0,010

t Critical one-tail 1,668

26

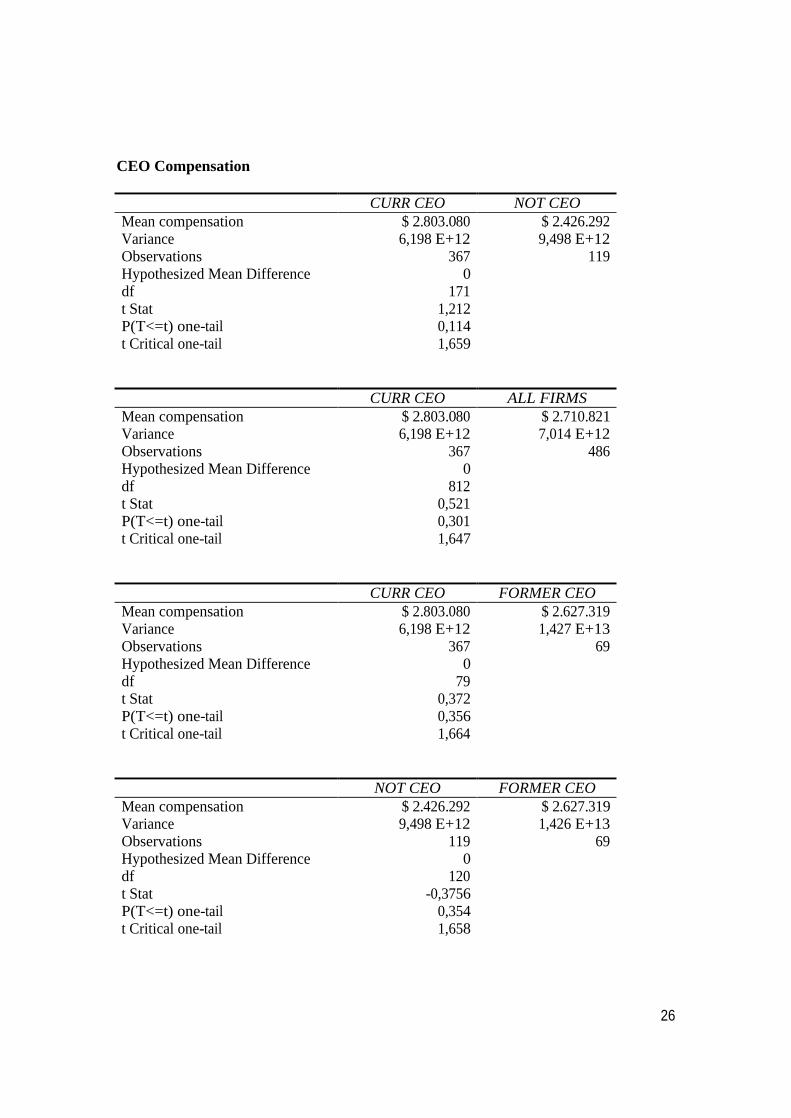

CEO Compensation

CURR CEO NOT CEO

Mean compensation $ 2.803.080

$ 2.426.292

Variance 6,198 E+12

9,498 E+12

Observations 367

119

Hypothesized Mean Difference 0

df 171

t Stat 1,212

P(T<=t) one-tail 0,114

t Critical one-tail 1,659

CURR CEO ALL FIRMS Mean compensation $ 2.803.080

$ 2.710.821

Variance 6,198 E+12

7,014 E+12

Observations 367

486

Hypothesized Mean Difference 0

df 812

t Stat 0,521

P(T<=t) one-tail 0,301

t Critical one-tail 1,647

CURR CEO FORMER CEO Mean compensation $ 2.803.080

$ 2.627.319

Variance 6,198 E+12

1,427 E+13

Observations 367

69

Hypothesized Mean Difference 0

df 79

t Stat 0,372

P(T<=t) one-tail 0,356

t Critical one-tail 1,664

NOT CEO FORMER CEO Mean compensation $ 2.426.292

$ 2.627.319

Variance 9,498 E+12

1,426 E+13

Observations 119

69

Hypothesized Mean Difference 0

df 120

t Stat -0,3756

P(T<=t) one-tail 0,354

t Critical one-tail 1,658

27

CURR CEO NOT CUR/FRM CEO

Mean compensation $ 2.803.080

$ 2.148.875

Variance 6,198 E+12

2,944 E+12

Observations 367

50

Hypothesized Mean Difference 0

df 80

t Stat 2,377

P(T<=t) one-tail ** 0,010

t Critical one-tail 1,664

CURR/FMR CEO NOT CUR/FRM CEO

Mean $ 2.775.264

$ 2.148.875

Variance 7,449 E+12

2,944 E+12

Observations 436

50

Hypothesized Mean Difference 0

df 81

t Stat 2,273

P(T<=t) one-tail ** 0,013

t Critical one-tail 1,664