Embed Size (px)

Citation preview

CERAWEEK®2007

Technology Needs for a

Carbon-Constrained World

Jeff SterbaChairman, President, CEO

PNM Resources, Inc.

February 15, 2007

2

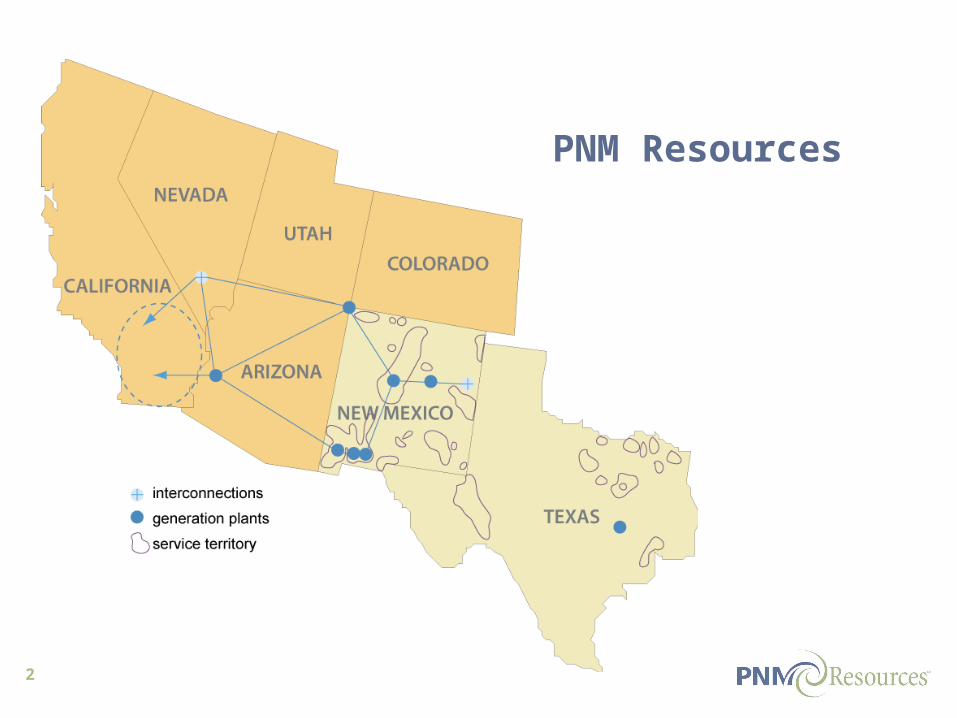

PNM Resources

3

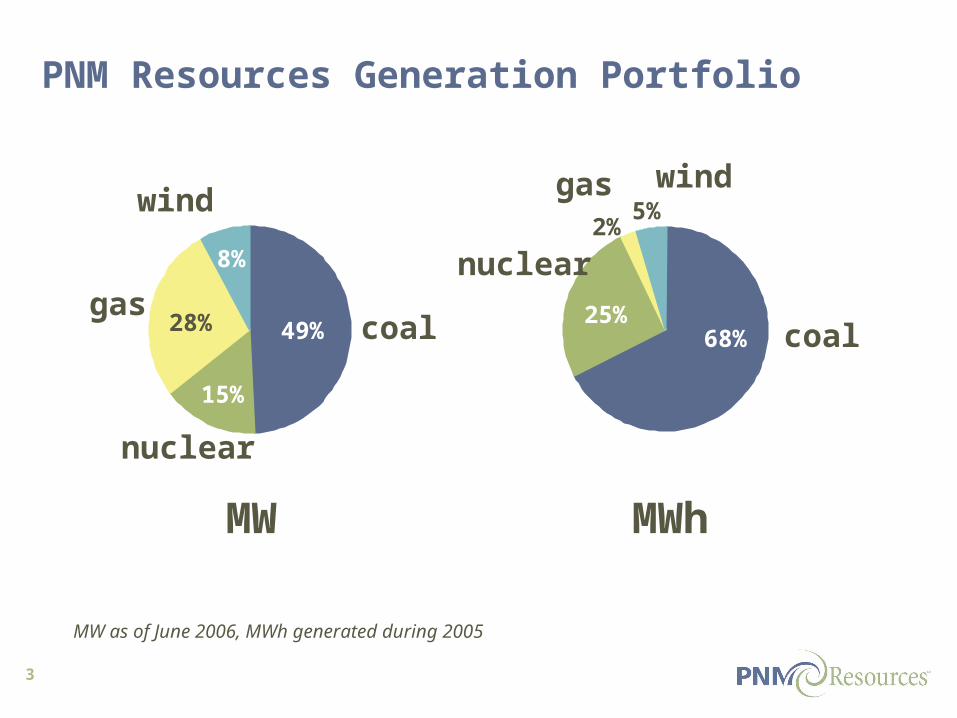

PNM Resources Generation Portfolio

MW

coal

nuclear

gas

wind

coal

nuclear

gas wind

49%

15%

28%

8%

68%25%

2%5%

MW as of June 2006, MWh generated during 2005

MWh

4

Electricity Technology in a Carbon-Constrained Future

…But what is technically feasible???

• Growing scientific and public opinion that GHG emissions are contributing to climate change…

• Priority of 110th Congress …

• U.S. responsible for 1/4 of worldwide CO2 emissions…

• Electric utilities responsible for 1/3 of U.S. CO2 emissions…

• Agreement that technology solutions are needed…

5

Comparative Costs 2010 to 2015

Source: EPRI 2007

6

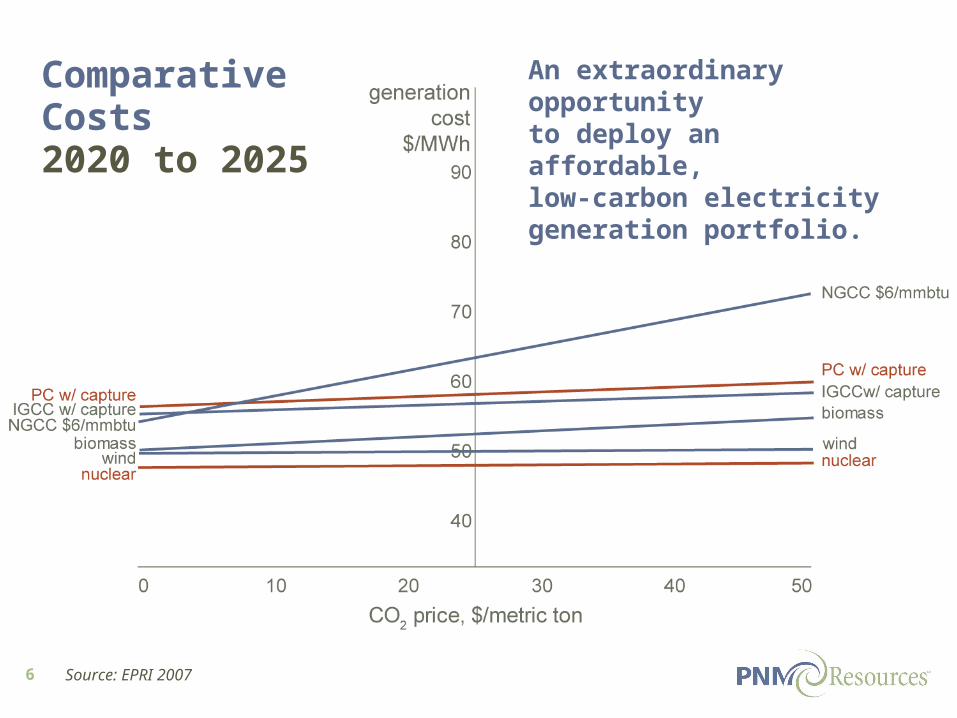

Comparative Costs 2020 to 2025

An extraordinary opportunity to deploy an affordable, low-carbon electricity generation portfolio.

Source: EPRI 2007

7

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2

Em

issi

on

s (m

illio

n m

etri

c to

ns)

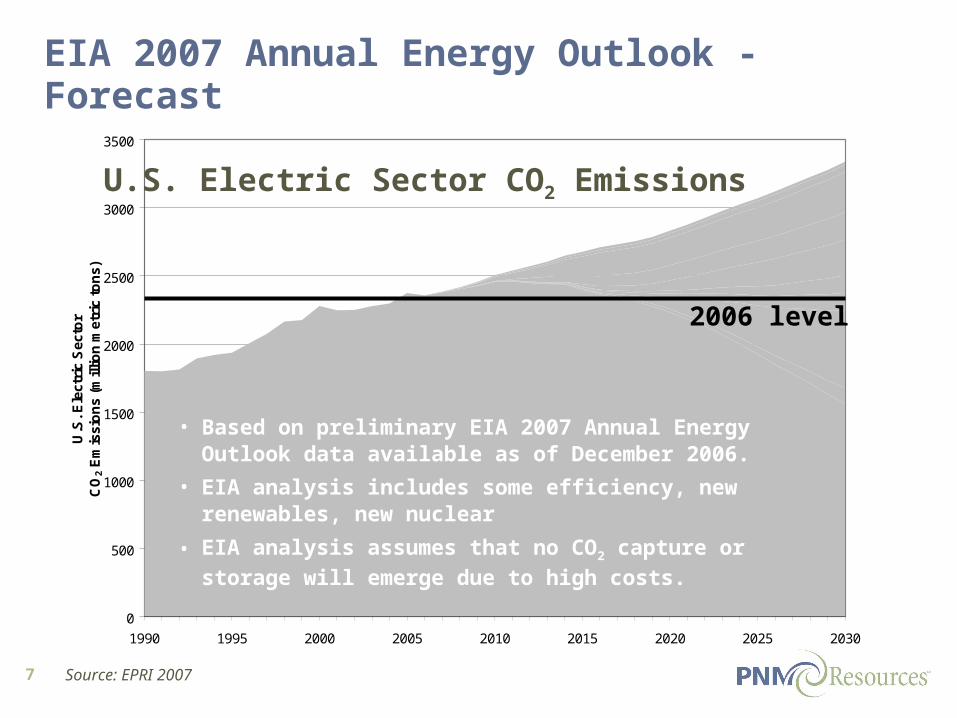

EIA 2007 Annual Energy Outlook - Forecast

U.S. Electric Sector CO2 Emissions

• Based on preliminary EIA 2007 Annual Energy Outlook data available as of December 2006.

• EIA analysis includes some efficiency, new renewables, new nuclear

• EIA analysis assumes that no CO2 capture or storage will

emerge due to high costs.

2006 level

Source: EPRI 2007

8

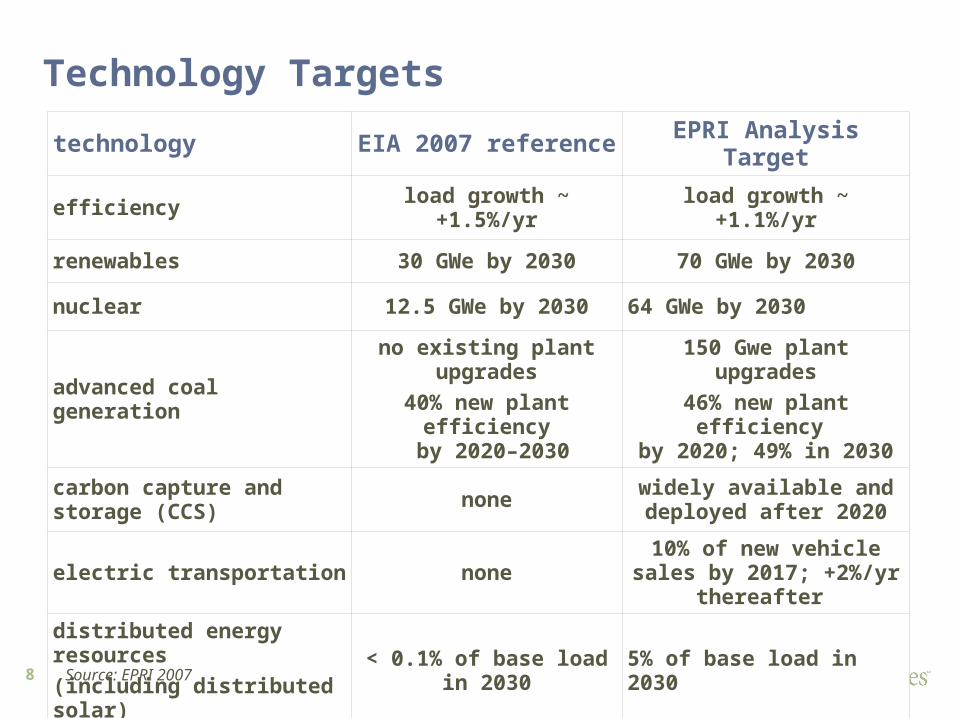

technology EIA 2007 reference EPRI Analysis Target

efficiency load growth ~ +1.5%/yr load growth ~ +1.1%/yr

renewables 30 GWe by 2030 70 GWe by 2030

nuclear 12.5 GWe by 2030 64 GWe by 2030

advanced coal generation

no existing plant upgrades

40% new plant efficiency by 2020–2030

150 Gwe plant upgrades

46% new plant efficiency by 2020; 49% in 2030

carbon capture and storage (CCS)

nonewidely available and deployed after 2020

electric transportation none10% of new vehicle sales

by 2017; +2%/yr thereafter

distributed energy resources

(including distributed solar)< 0.1% of base load in

20305% of base load in 2030

Source: EPRI 2007

Technology Targets

9

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

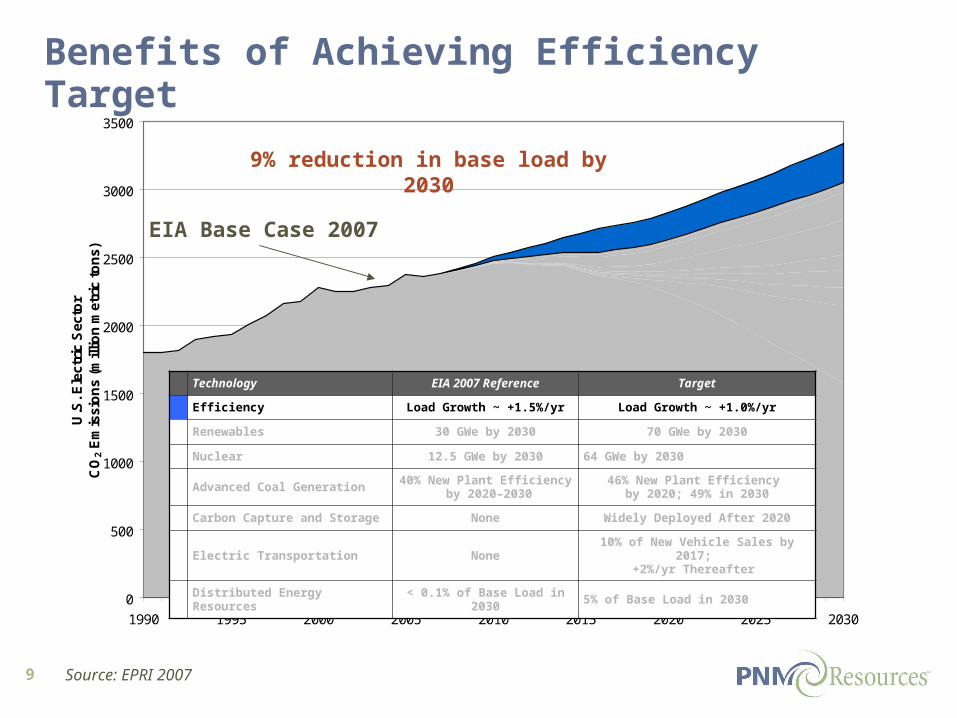

EIA Base Case 2007

9% reduction in base load by 2030

Benefits of Achieving Efficiency Target

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

10

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. E

lec

tric

Se

cto

rC

O2

Em

iss

ion

s (

mil

lio

n m

etr

ic t

on

s) EIA Base Case 2007

Benefits of Achieving Renewables Target

50 GWe new renewables by 2020; +2 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

11

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

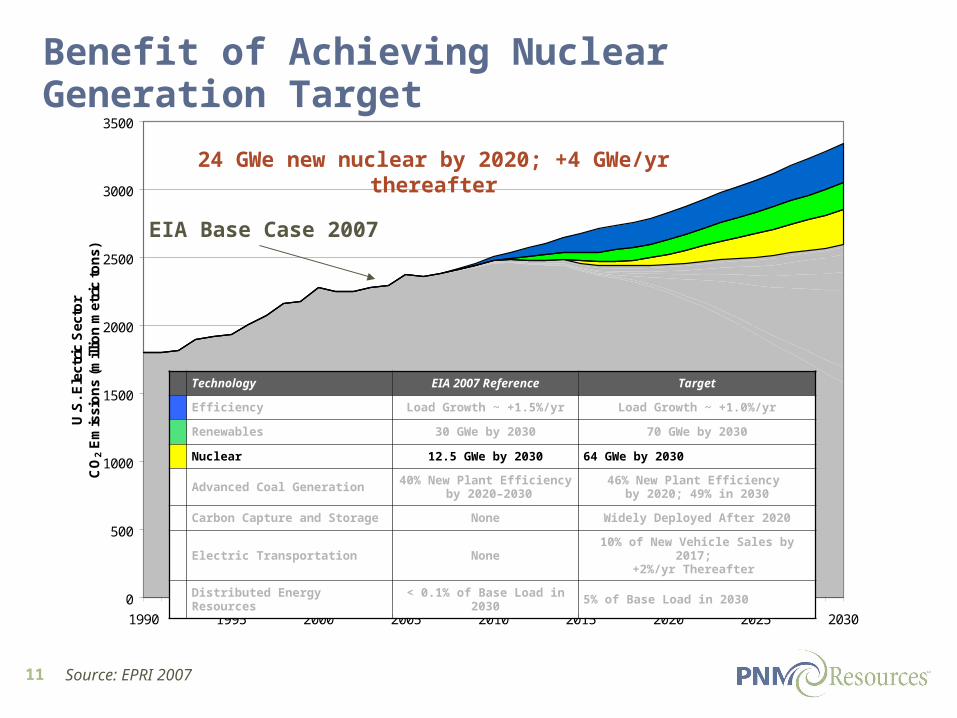

EIA Base Case 2007

Benefit of Achieving Nuclear Generation Target

24 GWe new nuclear by 2020; +4 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

12

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

Benefit of Achieving Advanced Coal Target

46% efficiency by 2020, 49% efficiency by 2030

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

13

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

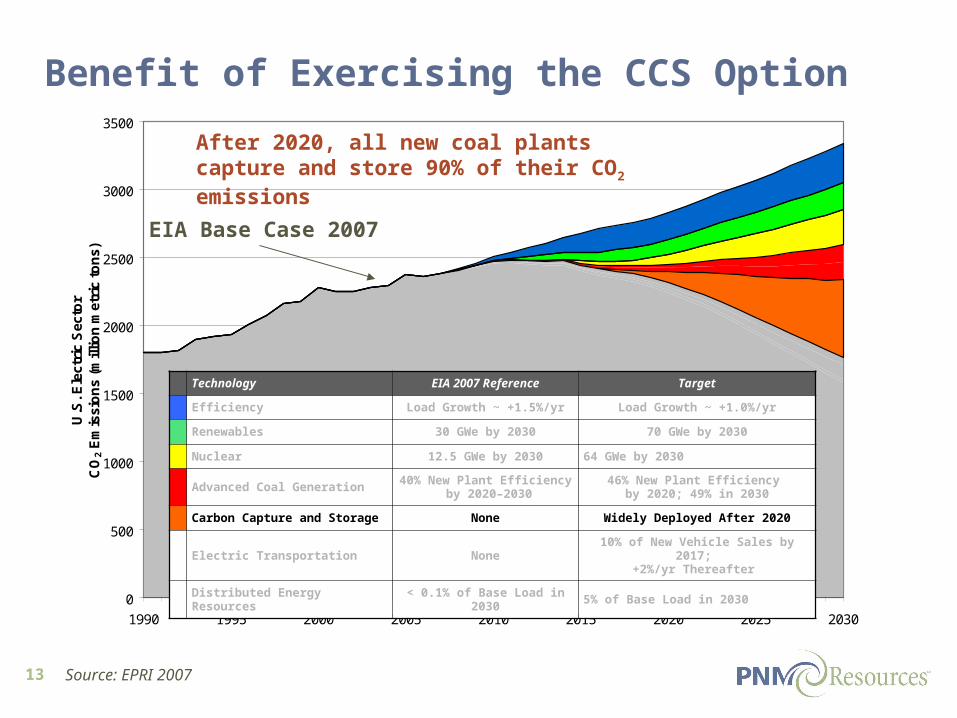

Benefit of Exercising the CCS Option

After 2020, all new coal plants capture and store 90% of their CO2 emissions

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

14

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

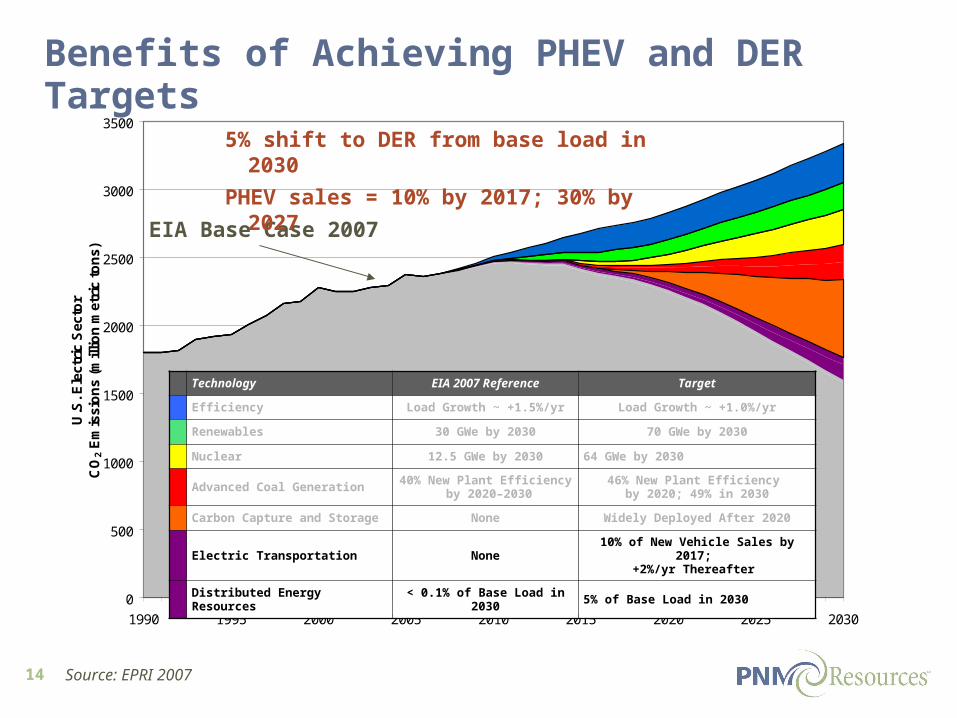

Benefits of Achieving PHEV and DER Targets

5% shift to DER from base load in 2030

PHEV sales = 10% by 2017; 30% by 2027

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

Source: EPRI 2007

15

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)CO2 Reductions…What’s Technically Feasible

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.0%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation40% New Plant Efficiency

by 2020–203046% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage None Widely Deployed After 2020

Electric Transportation None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

Distributed Energy Resources < 0.1% of Base Load in 2030 5% of Base Load in 2030

2006 level

Source: EPRI 2007

EIA Base Case 2007

16 Source: EPRI 2007

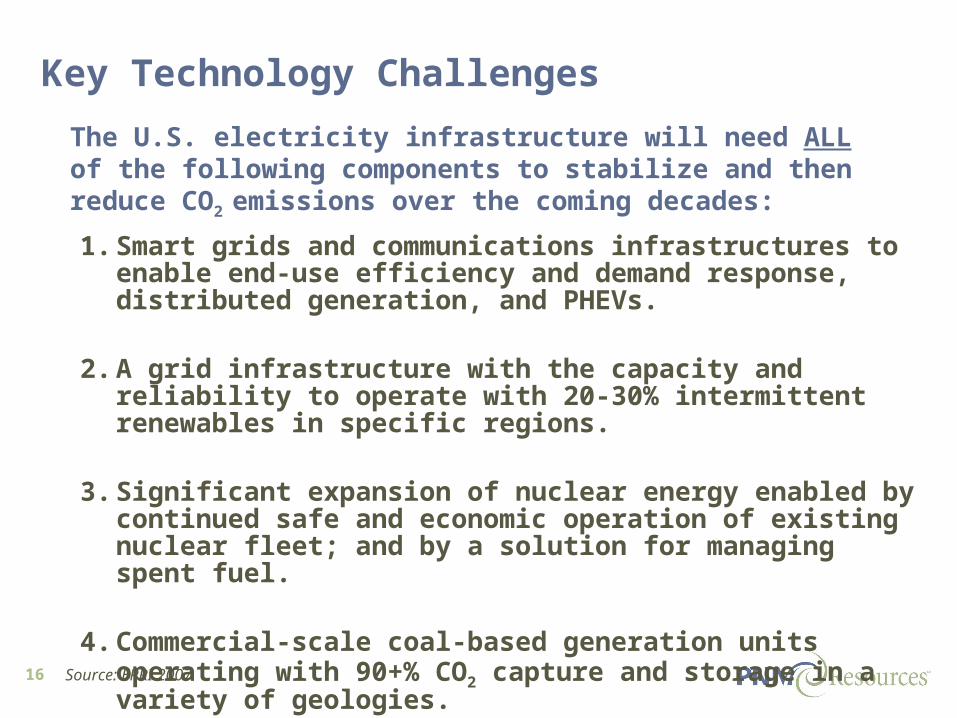

The U.S. electricity infrastructure will need ALL of the following components to stabilize and then reduce CO2 emissions over the coming decades:

1. Smart grids and communications infrastructures to enable end-use efficiency and demand response, distributed generation, and PHEVs.

2. A grid infrastructure with the capacity and reliability to operate with 20-30% intermittent renewables in specific regions.

3. Significant expansion of nuclear energy enabled by continued safe and economic operation of existing nuclear fleet; and by a solution for managing spent fuel.

4. Commercial-scale coal-based generation units operating with 90+% CO2 capture and storage in a variety of geologies.

Key Technology Challenges

17

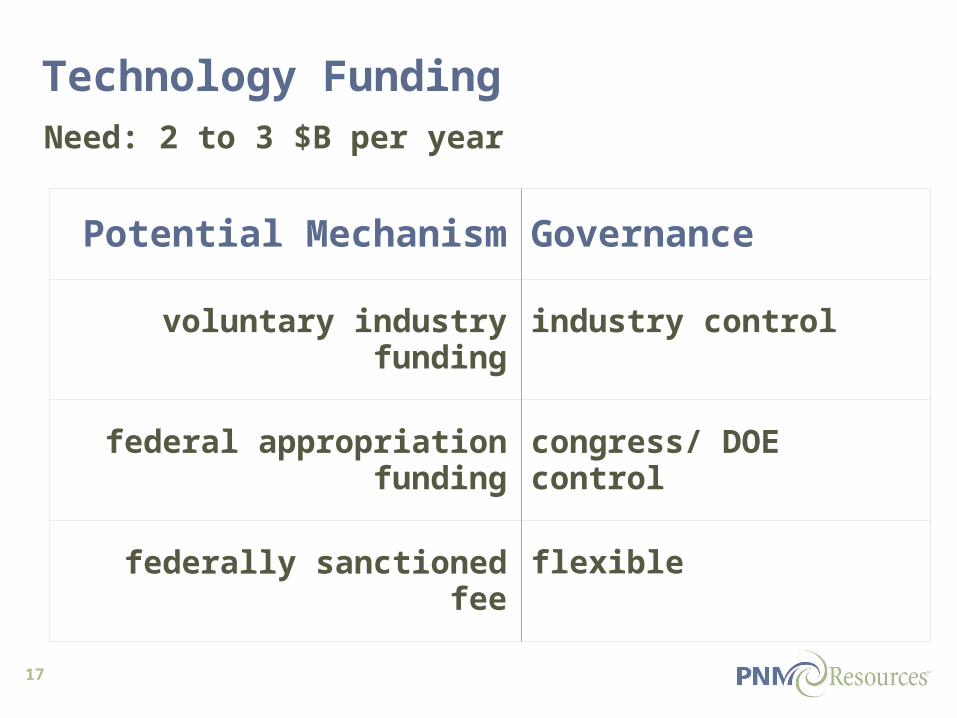

Technology Funding

Potential Mechanism Governance

voluntary industry funding industry control

federal appropriation funding congress/ DOE control

federally sanctioned fee flexible

Need: 2 to 3 $B per year