Embed Size (px)

Citation preview

company confidential

Certainty & Sustainability: The keys to

incentivising long term broadband

infrastructure investments in Asia

CTO Broadband Asia Forum 2016

Dominic P Arena

Group Chief Strategy & Marketing Officer

22 September 2016

2company confidential

3company confidential

PAKISTAN (2005)

12,000 km fiber

CAMBODIA (1998)

7.6m subs

First to launch 4G LTE

Smart-Hello merger (2012)

MALAYSIA (1998*)

12.3m subs

Leading mobile broadband provider

BANGLADESH (1995)

28.3m subs

Pending acquisition /

merger with Airtel

INDIA (2008)

181.9m subs*

Integrated pan-India

operator 2G/3G

NEPAL(2015/16)

13mil subs

Leading mobile provider

~2,100 towers

SRI LANKA (1995)

10.9m subs

First to launch 3G in S.Asia

Dialog-Suntel merger (2011)

Dialog TV- SkyTV merger (2013)

SINGAPORE (2005)

1.9m subs**

First to offer 4G LTE in ASEAN

INDONESIA (2005)

42m subs

XL-Axis merger (2012)

MYANMARAcquisition via edotco Group completed 4th Dec 2015 (75% stake)~1250 towers

edotco Group (2012)

Managing over 17,000 towers in 6 countries;

World’s 12th largest independent TowerCo

12th

GloballyAxiata Digital Services (2014)

Portfolio of 28 Digital businesses

21M MAUs; $200M in investment

At Q3 2016 Axiata is the second largest telecom operator in South Asia &

ASEAN, with over 310 million* customers & 25,000 staff in 10 countries+

*Comprises 290 million mobile and fixed network subscribers in 10 countries plus over 20 million MAUs of Digital Applications & Services (OTTs) in which Axiata holds direct equity investments

4company confidential

PEER GROUP (ASEAN & South Asia) – TOP 10 CUSTOMER REACH/BASE [Mn. Sims]

31.12.2015

193.6

82.6

99.0

110.0

154.9

171.9

194.0

255.5

274.0

507.8

MAXIS (incl. Aircel)

IDEA

TELKOMSEL

BHARTI AIRTEL

BSNL

RELIANCE

VODAFONE

TELENOR

SINGTEL

AXIATA

Regional Players Single Market Player

Source: Axiata Group Strategy, Informa WCIS Note: Vimpelcom 2010 incl. pro forma PMCL which was only consumated during H1-2011, Vodafone adjusted for India operations only

ASIA PACIFIC, excl. holdings below 19,9%

#7 #2+234 Mn Subs

41.0

24.1

30.0

36.8

39.8

39.9

47.9

53.3

55.2

164.5

TELKOMSEL

TELENOR

RELIANCE

BHARTI AIRTEL

VODAFONE

SINGTEL

AXIATA

PLDT

BSNL

AIS

31.12.2007

In terms of customer reach we have grown to become #2 in

the Region (ASEAN & South Asia)+

among regional

& major single

market players

Notes :

‒ Regional market is defined as ASEAN and South Asia

7th

2nd (now 310m)

5company confidential

Invested Capital +

Expenditure more than

44.5 BillionUSD

SELECTED ACHIEVEMENTS ACROSS THE GROUP

Creating more than

1.3 million Job

Opportunities

across Asia

BangladeshInvestment (2008-2015):

USD 3.3 bil~368,000 jobs created

~0.4% of GDP

Sri Lanka Investment (2008-2015):

USD 2.6 bil~112,000 jobs created

~1.3% of GDP

No. 1 FDI

CambodiaInvestment (2008-2015):

USD 0.5 bil~66,000 jobs created

~1.5% of GDP

Highest Tax-Payer

MalaysiaInvestment (2008-2015):

USD 10.1 bil~126,000 jobs created

~0.9% of GDP

IndonesiaInvestment (2008-2015):

USD 9.8 bil~195,000 jobs created

~0.2% of GDP

1995 1995

1998

1988* 2005

Year of Investment

Note : Investment in the forms of capital expenditure and operating expenditure

Source : KPMG Independent Analysis

* Incorporate in 1988 under TM, then sold to Axiata during TMI demerger in 2008; ** Purchase Enterprise Value representing 1.5x Book Value of Invested Capital

Axiata is recognised as a long-term investor & contributor to

national development in our markets (~1.0% of GDP)+

NepalInvestment (2004-2015)**:

USD 1.4 bil~2.4% of GDP

No. 1 FDI

Highest Tax-Payer

2016

6company confidential

Digital communications and connectivity (B2C and B2B Convergence – Fixed and Mobile)

Enabling infrastructure and platforms(Passive Infra., Active Networks, OTT/IoT & Analytics)

Digital applications and services(FinTech, Advertising, eCommerce, EduHealth, IoT)

We are focused on our Core Business which is defined as 3

Core Pillars addressing all aspects of the Digital Economy+

1

2

3

7company confidential

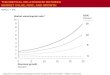

0.03

58

1.64

0.10

1.00

10.00

100.00

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Cost/GB Index (LHS) DL BW Index Data ARPU Index

Notes: Applies Nielsen’s Bandwidth Law driven by AR/VR, UHD, 5G and IoT; Data Pricing and ARPU analysed using Malaysia operator data 2012-15

Data Unit Price

& Cost Index

35x

Status Quo Connectivity Focus will Constrain Data ARPU Growth

30x

1 Gbps

per User1 Gbps

per Node

OTTs

Smart-phone

… Data/BW Driver

5-10 Mbps

per User

FMC HetNet

Video 4k UHD

Mobile 1st

IOTAR/ VR360

5GVideo 8k UHD

Our industry is now facing a ‘scissor curve’ challenging traditional

business models and network investment economics+

Social B-cast

0.7GB 8.5GB

Avg. Monthly

Usage Per Axiata

Data User

59GB /

500GB (FMC)

8company confidential

WACC Range

The new data-led reality is that network & industry economics more strongly

favour economies of scale, with implications for financing & shareholder return

Source: ATKearney – based on a global survey of 54 operators over past 3 years using Bloomberg, GSMA and operator data and Axiata Group Strategy Analysis

~17%

No. 1 No. 2

(Strong)

No. 3-4 No. 5

~12%

~5%

~ -4%

Long Term Investment Returns for Infrastructure Based Mobile Operators (%ROIC)

Economic Value Add

Economic Value Destruction

ROIC-WACC

has a 0.99

correlation to

share price (JP Morgan)

~7.5%

No. 2

(Weak)

Dilutive effect of

#2-3 fighting for

market share

(<10pp gap)

9company confidential

-4.00%

0.00%

4.00%

8.00%

12.00%

10 5 3 1

US Europe Asia Globally

-4.00%

0.00%

4.00%

8.00%

12.00%

10 5 3 1

Revenue CAGR

US Europe Asia Globally

+this is supported by the trend of Telecom revenue and profit growth slowing

(in Asia and Globally) over the past 10 years+

Revenue CAGR [1] Profit CAGR [2]

[1]: Revenue Growth Rates are extracted from GSMA and consist of 242 samples

[2]: Profit Growth Rate is calculated based company filings of 7 of the largest Telco Groups, All Data points are taken as of Q1 for years 2016, 2015, 2013, 2011, and 2006

10company confidential

Therefore, Certainty and Sustainability are the two key drivers

of long term Broadband infrastructure investment+

� Regulatory Frameworks

• Rational License Pricing (capital intensity, profitability) and Industry Specific Taxation (consumer purchasing

power)

• Convergence Regulation approach (eg. Fixed & Mobile RMS, TV, Digital Services/OTT/SSSR, Spectrum Neutrality,

Carriage vs Content)

� Return on Investment

• Sustainable market structures and supportive Regulation such as Spectrum Pooling / Trading, Active NetCo,

Mergers/Consolidation Rules

� Access to Capital

• Liquidity and depth of Local Capital Markets (access to debt and equity)

• Currency (monetary policy) stability and hedging instruments (risk management)

� Ability to Launch New Services

• Certainty of Spectrum Availability and Allocation (450/700/800MHz and 1500/2300/2600/3600/5000MHz,

800-900MHz and 2400MHz ISM for IoT / LTE-U) for LTE, IoT and 5G

• FinTech related licensing for telecom operators (payments, deposits, remittances, insurance)

• Spectrum Re-farming / Neutrality for upgrading to more efficient (lower cost, higher performance) technologies