Embed Size (px)

Citation preview

CF Industries Holdings, Inc.CF Industries Holdings, Inc.

2006 Goldman Sachs 2006 Goldman Sachs Agriculture Biotech ForumAgriculture Biotech Forum

CF Industries Holdings, Inc.CF Industries Holdings, Inc.NYSE: CFNYSE: CF February 14,February 14, 20062006

2

Safe Harbor Statement

Certain statements contained in this presentation may constitute “forward-looking statements” within the meaning of federal securities laws. All statements in this presentation, other than those relating to our historical information or current condition, are forward-looking statements. These forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond our control, which could cause our actual results to differ materially from such statements. These risks and uncertainties include the relatively expensive and volatile cost of North American natural gas; the cyclical nature of our business; the nature of our products as global commodities; intense global competition in the consolidating markets in which we operate; conditions in the U.S. agricultural industry; weather conditions; our inability to accurately predict seasonal demand for our products; the concentration of our sales to pre-IPO owners and other large customers; the impact of changing market conditions on our forward pricing program; the significant risks and hazards involved in fertilizer manufacturing; unanticipated consequences related to future expansion of our business; our inability to expand our business, including consequences due to the significant resources that could be required; potential liabilities and expenditures related to environmental and health and safety laws and regulations; our inability to obtain or maintain required permits and governmental approvals; acts of terrorism; difficulties in securing the raw materials we use; changes in global fertilizer supply and demand and the other risks and uncertainties included from time to time in our filings with the Securities and Exchange Commission. We undertake no obligation to update or revise any forward-looking statements.

3

CF Industries will report Q4 and ’05 results on February 23; Conference Call on February 24

‘We’re taking some extra time our first time around!’

We have not released our year-end results yet, so today’s presentation will take a longer-term, strategic look at CF Industries

Today’s Presentation

4

Leading manufacturer and distributor of nitrogen and phosphate fertilizer

Founded as a cooperative in 1946; new bottom line oriented business model in 2003

Market shares for fertilizer year 2004 were 22 percent nitrogen and 14 percent phosphate; Corn Belt 29 percent for nitrogen and 20 percent for phosphate

IPO in August 2005; 2005 high and low: $18.00 and $11.19

Reported strong sales and operating earnings through Q3 2005

Who We Are . . .

5

Fertilizer is a global worldwide commodity, and commodity prices don’t necessarily reflect cost of raw materials

Three major nutrients – N, P and K – essential for improved crop yield, growth and durability

No substitutes – and N, P and K not substitutable for each other

Key variable in nitrogen profitability is relationship between natural gas costs and fertilizer costs

U.S. net nitrogen and potash importer; net phosphate exporter

Growth has been consistent at approximately 2.7% annually

The Fertilizer Market

6

The assets, the financial strength, and the flexibility to adapt to changing market conditions and create long-term shareholder value

We donWe don’’t underestimate the neart underestimate the near--term challengesterm challenges…… but we but we believe CF Industries is well positioned believe CF Industries is well positioned –– strategically strategically –– to to adapt to and ultimately capitalize on changes in the globaadapt to and ultimately capitalize on changes in the global l fertilizer marketplace!fertilizer marketplace!

CF Industries’ Strategic Focus in a Volatile Industry...

7

Assets and Flexibility in Nitrogen Fertilizer

Two of three largest North American nitrogen fertilizer complexes– Donaldsonville, Louisiana– Medicine Hat, Alberta

Nitrogen

8

North America’s largest: four ammonia plants, four urea plants and two UAN plants

Operational, product and transport flexibility

TODAY: Flexibility, modularity and “make versus buy”capability to cope with high natural gas prices

FUTURE: Modern, productive facility with economies of scale for era of ‘normalized’ natural gas prices and/or alternative feedstock

CF Industries’ Donaldsonville Complex

9

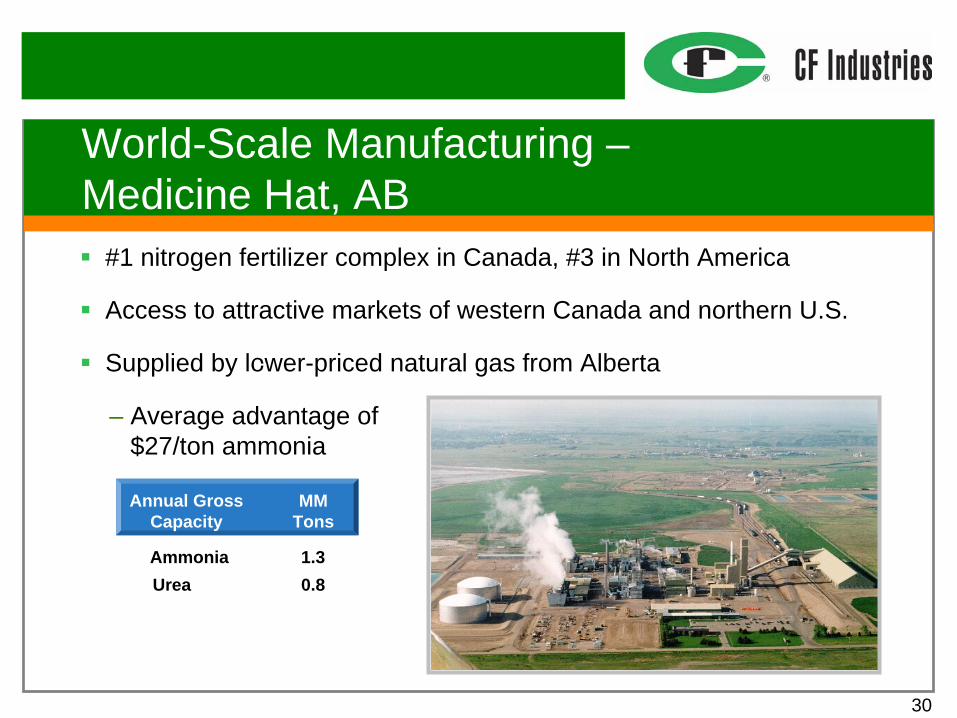

Joint venture is third largest nitrogen complex in North America: two ammonia plants and one urea plant

Access to lower-cost AECO natural gas, as well as to markets in northern-tier U.S. and western Canada

Average natural gas cost advantage $27 per ton of ammonia

TODAY: Competitive presence in a strong, growing marketFUTURE: Cost structure and location should remain

competitive advantages

CF Industries’ Medicine Hat Complex

10

Modern, competitive mining, processing and shipping facilities in Central Florida

Newest U.S. phosphate rock mine (Hardee County)

One of largest U.S. integrated DAP/MAP complexes (Plant City)

Ammonia terminal and warehouse/shipping complex at Port of Tampa

Assets and Flexibility in Phosphate

11

CF Industries’ Central Florida Phosphate Operations

Strong (26 years) rock reserve position

Produce DAP and MAP: fastest growing phosphate fertilizer products

Access to domestic and export markets

TODAY: Diversification from nitrogen market and access to export markets

FUTURE: Benefit from value of finite amount of Florida rock reserves; continued access to world markets

12

Assets and Flexibility in Distribution

49 nitrogen and phosphate distribution facilities, strategicallylocated primarily in midwestern grain-producing states

Most can access multiple modes of incoming transportation, including pipeline, barge, rail and truck

Access – thanks to Donaldsonville “make versus buy”capability – to domestic and imported product

13

Assets and Flexibility in Distribution

With 20 ammonia terminals, one of only three producers that can effectively provide ammonia (approximately one fourth of nitrogen fertilizer market) to Corn Belt

Locations are key advantage in regional markets

Good mix of new and old customers

TODAY:TODAY: Strong complement to manufacturing operations with access to fertilizer-intensive markets

FUTURE:FUTURE: A strategic asset providing unique market access

14

Assets and Flexibility to Compete

World-scale assets in nitrogen fertilizer, phosphate fertilizer and product distribution

Significant flexibility / capability to anticipate changing market conditions

Strong financial position

We have strategic options in a changing marketWe have strategic options in a changing market

15

Additional Strengths

Innovative program to manage margin riskItIt’’s much more than simply a forward pricing programs much more than simply a forward pricing program

Strong customer relationshipsMultiMulti--year contracts with previous owners, plus new year contracts with previous owners, plus new relationships with major agricultural suppliersrelationships with major agricultural suppliers

Leading market positionUnlike many Unlike many IPOsIPOs, we, we’’re established in the market!re established in the market!

16

The Natural Gas Issue

North America’s position as high-cost nitrogen fertilizer producer worsened post-Katrina

Large percentage of capacity (including much of CF Industries’ Donaldsonville complex) idled in Q4

Phosphate less sensitive to natural gas (approximately7 mmBTU versus 33 mmBTU for ammonia)

Significant downturn in North American natural gas prices since December 2005…

17

The Natural Gas Issue

Clearly a challenge today, although lower natural gas and current fertilizer prices permit resumed North American nitrogenproductionLong-term factors offer promise, including alternative feed stocks and increased exploration in U.S. LNG also an option, as increased availability could, as with oil, create world commodity market for natural gasLack of distribution capabilities – especially for ammonia and, to lesser extent, UAN – remains a challenge for offshore producers

In this environment, we view CF IndustriesIn this environment, we view CF Industries’’ assets and assets and flexibility as key strategic strengths, providing us the flexibility as key strategic strengths, providing us the opportunity to capitalize on a wide range of outcomes in opportunity to capitalize on a wide range of outcomes in world fertilizer marketsworld fertilizer markets

18

To capitalize on our assets and flexibilities …

Reduce dependence on North American natural gas– Proposed Trinidad joint venture– Alternative feedstock at Donaldsonville

Expand usage and duration of margin risk management programIdentify next generation of cost-reduction opportunitiesContinue to develop new, post-cooperative market opportunitiesRefine longer-term vision

CF Industries’ Strategic Priorities

19

CF Industries ‘Investable Idea’

A business model transformation that has effectively positioned CF Industries as a profit-driven company focused on building shareholder value

The assets, the financial strength, and the flexibility to adapt to changing market conditions and create long-term shareholder value

We donWe don’’t underestimate the neart underestimate the near--term challenges . . . but term challenges . . . but we believe CF Industries is well positioned we believe CF Industries is well positioned –– strategically strategically ––to adapt to and ultimately capitalize on changes in the to adapt to and ultimately capitalize on changes in the global fertilizer marketplace!global fertilizer marketplace!

20

21

Addendum

22

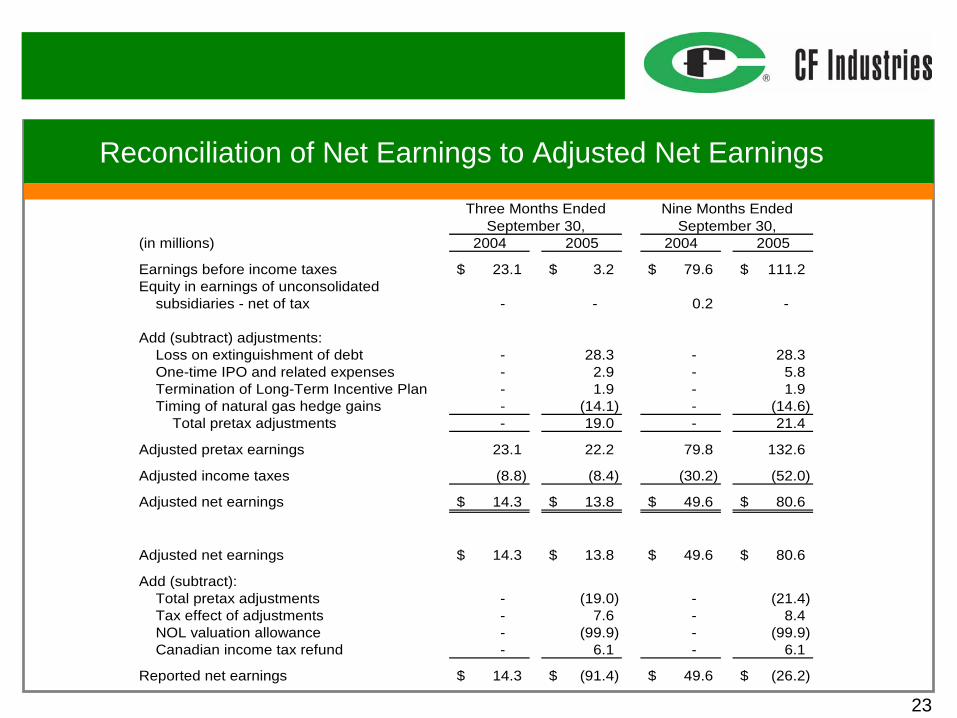

Third Quarter Performance

Net sales increased by 10 percent to $359.4 millionOperating earnings of $35.1 million more than offset by non-recurring IPO-related charges and other itemsNet loss of $91.4 millionAdjusted net earnings, totaled $13.8 million, or $0.25 per common share, on a pro forma basis, compared to $14.3 million, or $0.26 per share, on a pro forma basis, for 2004’s third quarter.At September 30, 2005: gross cash and short-term investments of $317.5 million, debt of $4.2 million, and current liability for customer advances of $183.4 million.

23

Reconciliation of Net Earnings to Adjusted Net Earnings

Three Months Ended September 30,

Nine Months Ended September 30,

(in millions) 2004 2005 2004 2005

Earnings before income taxes 23.1$ 3.2$ 79.6$ 111.2$ Equity in earnings of unconsolidated

subsidiaries - net of tax - - 0.2 -

Add (subtract) adjustments:Loss on extinguishment of debt - 28.3 - 28.3 One-time IPO and related expenses - 2.9 - 5.8 Termination of Long-Term Incentive Plan - 1.9 - 1.9 Timing of natural gas hedge gains - (14.1) - (14.6)

Total pretax adjustments - 19.0 - 21.4

Adjusted pretax earnings 23.1 22.2 79.8 132.6

Adjusted income taxes (8.8) (8.4) (30.2) (52.0)

Adjusted net earnings 14.3$ 13.8$ 49.6$ 80.6$

Adjusted net earnings 14.3$ 13.8$ 49.6$ 80.6$

Add (subtract):Total pretax adjustments - (19.0) - (21.4) Tax effect of adjustments - 7.6 - 8.4 NOL valuation allowance - (99.9) - (99.9) Canadian income tax refund - 6.1 - 6.1

Reported net earnings 14.3$ (91.4)$ 49.6$ (26.2)$

24

Reconciliation of Net Earnings to EBITDA and Adjusted EBITDA

Three Months Ended September 30,

Nine Months Ended September 30,

(in millions) 2004 2005 2004 2005

Net earnings (loss) 14.3$ (91.4)$ 49.6$ (26.2)$ Interest - net 4.0 (0.9) 13.8 1.9 Income tax provision 8.8 94.6 30.2 137.4 Depreciation, depletion and amortization 27.5 23.2 81.1 76.4 Less: Loan fee amortization (a) (0.3) (0.1) (0.8) (0.7)

EBITDA 54.3$ 25.4$ 173.9$ 188.8$

Add (subtract) adjustments:Loss on extinguishment of debt - 28.3 - 28.3 IPO and related expenses - 2.9 - 5.8 Termination of Long-Term Incentive Plan - 1.9 - 1.9 Timing of natural gas hedge gains - (14.1) - (14.6)

Total adjustments - 19.0 - 21.4

Adjusted EBITDA 54.3$ 44.4$ 173.9$ 210.2$

(a) To adjust for amount included in both interest and amortization.

25

Industry Overview

Three key nutrients:

– Nitrogen (N)

– Phosphate (P)

– Potash (K)

Global Fertilizer ConsumptionTotal Tons 2004: 162MM

Potash (K)

Phosphate (P)

Nitrogen (N)

17%

24%

59%

26

050

100150200250300

Corn Wheat Soybeans

…While World Meat Consumption Is Increasing…

MM Tonnes

Developed Developing

…Requiring More Corn to Feed More Livestock…

Pounds per Acre

World Population is Growing…

04080

120160

1970/1971 1980/1981 1990/1991 2000/2001 2009/2010E

MM Tons

CAGR 2.7%

Global Fertilizer Consumption (1)

NPK

NPK

Billions

Notes: (1) Excludes former Soviet Union countries

02468

10

2000 2015E 2030E0

100

200

300

400

2000 2015E 2030E

Long-Term Demand Drivers

1970/1971 1980/1981 1990/1991 2000/2001 2009/20010E

27

Competitive Strengths

World-Scale Manufacturing FacilitiesStrategically Located, Flexible Distribution SystemLong-Standing Customer RelationshipsLeading Market PositionsInnovative Risk ManagementStrong Financial PositionExperienced Management Team

28

Significant Scale Advantage

North American Nitrogen Fertilizer Facilities – By CapacityMM Tons

Donaldsonville

Medicine Hat

0.0

0.5

1.0

1.5

2.0

2.5

29

#1 nitrogen fertilizer complex in North America

Significant production flexibility

Access to low-cost transportation by barge, pipeline and rail

Deep-water dock

Annual GrossCapacity

AmmoniaUreaUAN

MMTons

2.31.72.7

2.31.72.7

World-Scale Manufacturing –Donaldsonville, LA

30

#1 nitrogen fertilizer complex in Canada, #3 in North America

Access to attractive markets of western Canada and northern U.S.

Supplied by lower-priced natural gas from Alberta-

– Average advantage of$27/ton ammonia

Annual GrossCapacity

AmmoniaUrea

MMTons

2.31.72.7

1.30.8

World-Scale Manufacturing –Medicine Hat, AB

31

Hardee Rock Mine – newest U.S. phosphate rock mine– 27 years of reserves Plant City Complex – one of the largest, integrated DAP/MAPcomplexes in U.S.

Port of Tampa – access to domestic and international markets

-

Annual GrossCapacity

Phosphate RockSulfuric Acid

MMTons

2.31.72.7

3.52.6

World-Scale Manufacturing –Central Florida

Phosphoric AcidPhosphoric Acid

1.02.0

32

Strategically Located, Flexible Distribution Network

Medicine Hat

Nitrogen Complex

Phosphate PlantPhosphate Rock Mine

Ammonia Terminal and UAN Terminal

Urea Warehouse

Ammonia Terminal

UAN Terminal

WI

IN

MN

IA

MO

NEOH

ND

IL

SD

Donaldsonville

Plant CityHardee

Low High

KS

MI

33

Forward Pricing Program

>50% of nitrogen fertilizer sold under FPP in 2004

ChallengeNatural gas and nitrogen fertilizer prices are highly volatile

SolutionCustomers purchase product forward

CF locks in margin by fixing natural gas costs

Substantial customer deposit

+ Margin certainty

+ Improved production scheduling

+ Reduced inventory risk

+ Enhanced liquidity

+ Integration with customers

Benefits

34

Leading Market Positions in North America

Market Share (2004)

(%)Nitrogen Phosphate

(%)

Key Driver: Strategically located network of terminals and warehouses

29%

22%

0

5

10

15

20

25

30

35

Total U.S. Ten Core States

20%

14%

0

5

10

15

20

25

Total U.S. Ten Core States

35

Experienced Management Team

Age PositionName

56 President, CEO and ChairmanSteve Wilson 15

51 SVP and CFOErnie Thomas 1

53 VP, Corporate PlanningSteve Chase 30

53 VP, Raw Materials ProcurementPhil Koch 2

54 VP, Supply and LogisticsFred Mugica 29

52 VP, SalesMonty Summa 8

54 VP, GM DonaldsonvilleLou Frey 30

Years In Industry

58 VP, GM Medicine HatRuss Holowachuk 36

54 VP, GM Phosphate OperationsHerschel Morris 30

51 SVP, OperationsDavid Pruett -