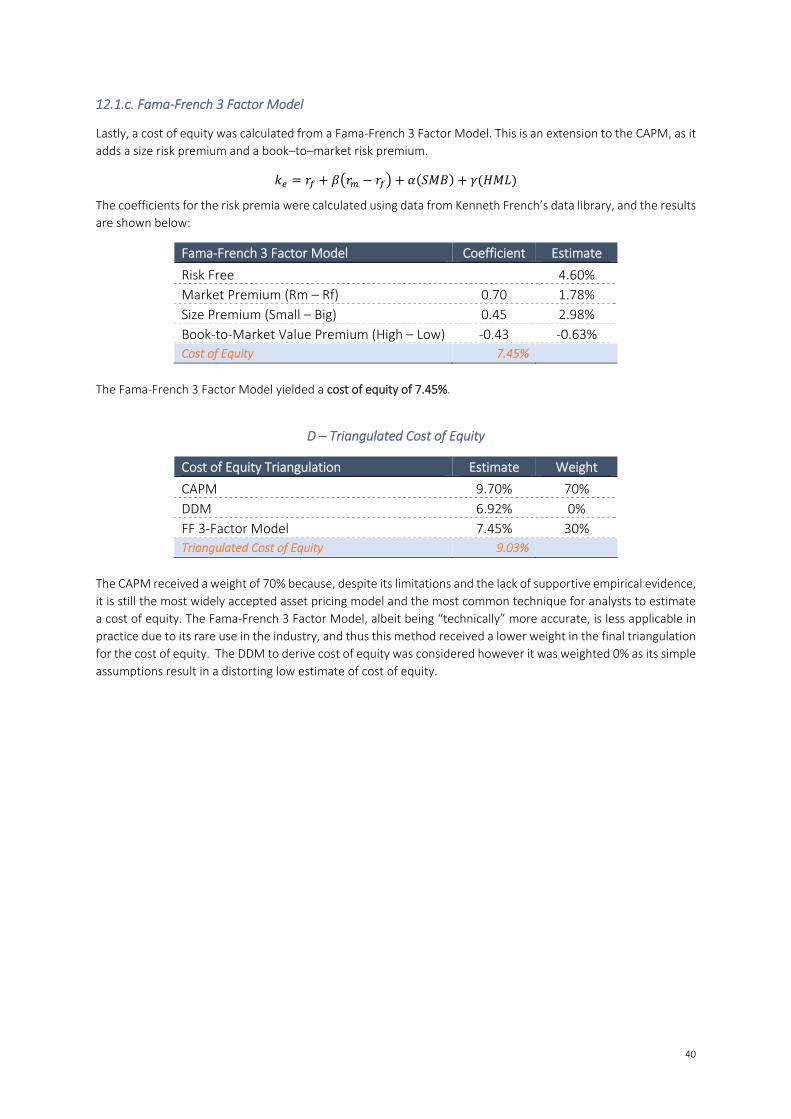

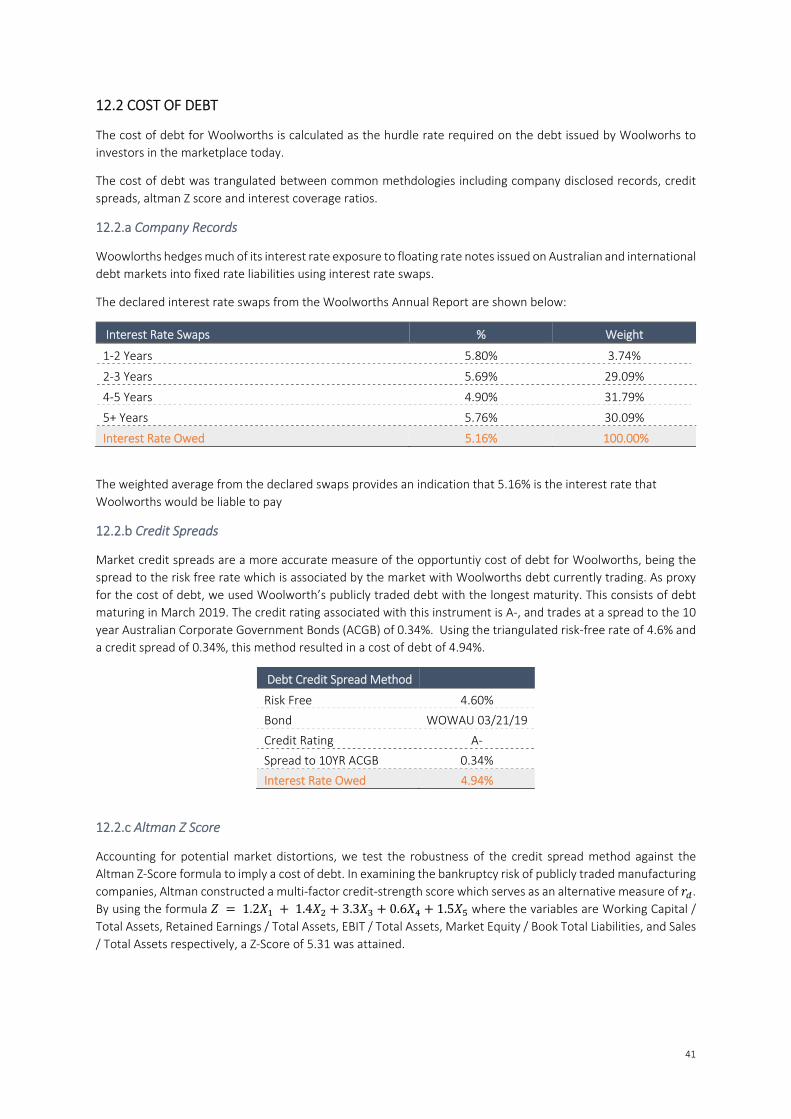

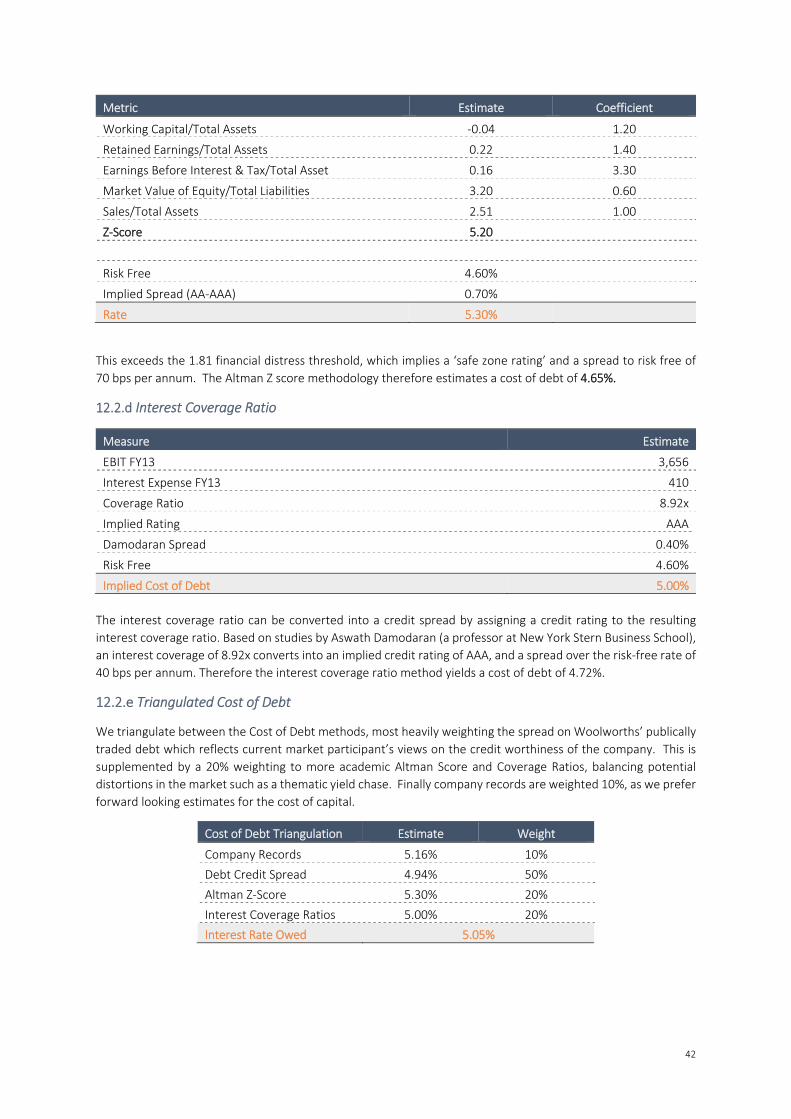

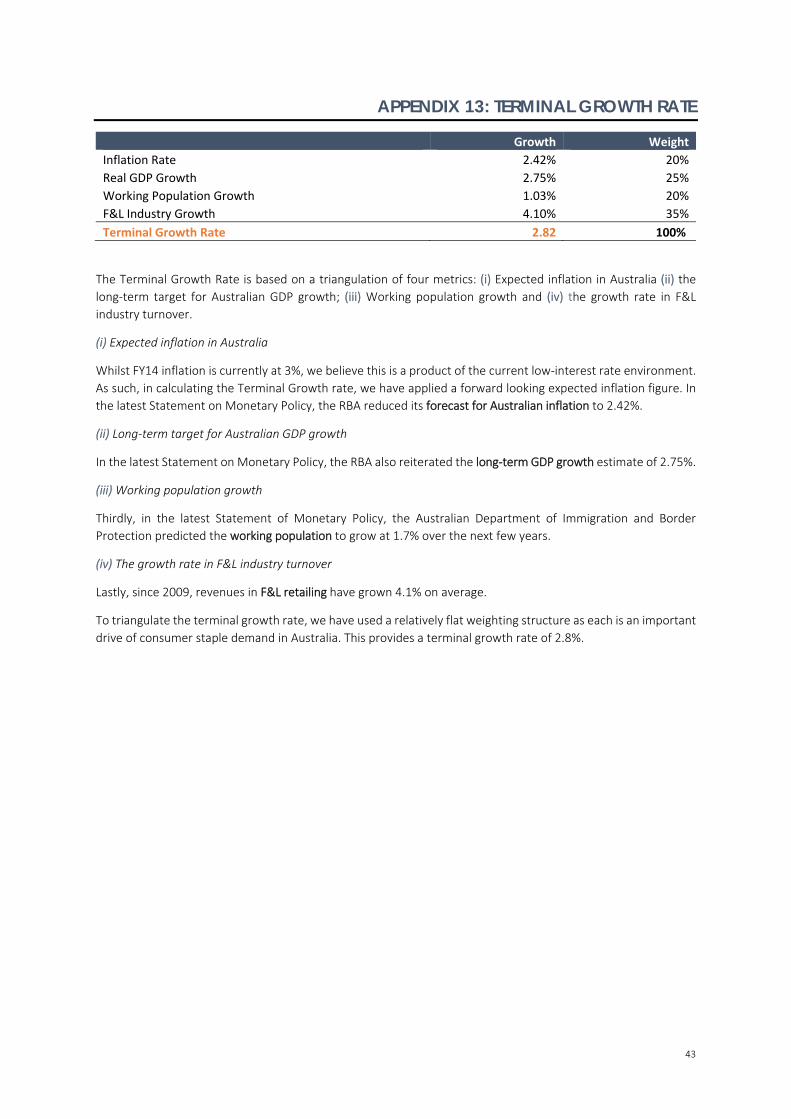

Embed Size (px)

Citation preview

CFA Institute Research Challenge

Hosted by:

CFA Society Sydney, Australia The University of Sydney

Woolworths Australia Limited (WOW.ASX) Food Fight: The New Reality for Australian Grocers We initiate coverage on Woolworths Australia Limited (WOW.ASX) with a SELL recommendation and price target of $29.27, representing a 16.5% downside from the current price of $35.07. The Australian grocery market is re‐fragmenting and the period of oligopolistic consolidation which historically fostered WOW’s growth is drawing to a close. As Management has failed to implement strategic growth opportunities in the wake of increased competition and a resurgence in discount grocers, we do not see support for the current price. SUPERMARKETS | CHANGING OF THE GUARD

‐ Industry re‐fragmentation represents a material threat to WOW’s core Food and Liquor (F&L) segment (76% of sales). Stagnant real wage growth and heighted consumer price awareness have acted as catalysts for the bifurcation of Australian grocery expenditure. Instead of weekly ‘one‐stop shops’, consumers are increasingly making bulk‐value purchases at discount grocers (ALDI) and periodically shopping at specialist retailers (Harris Farm Markets). We do not believe WOW’s ‘all‐in‐one’ model is sufficiently positioned to accommodate this shift in consumer demand.

‐ The Australian consumer’s appetite for discount supermarkets, once fulfilled by Franklins, is now being satiated by ALDI. Buoyed by a resurgence in private‐label products, the German grocer has gained ~10% market share since 2001 and outperforms all Australian competitors on ‘known value indicator’ metrics. As ALDI succesfully executes an aggressive expansion strategy, we expect material erosion to WOW’s 39.5% market share.

CAPITAL MANAGEMENT | DESTROYING SHAREHOLDER VALUE

‐ Management has failed to drive new sources of growth. Despite facilitative negative working capital from the scaled supermarket business, WOW has engaged in projects that distract from its core business: > Masters: WOW has fundamentally misunderstood the Australian Home Improvement

market. In misapplying Lowes’ American experience, the Master’s business has persistently failed to meet growth expectations; posting an FY14 loss of $169m. In the absence of renewed guidance from Management, and noting it took Bunnings decades to build a 17% share of the fragmented hardware market, we do not expect Master’s to materially contribute to profit until at least FY17.

> Premium Services: We do not see value in the roll out of in store services such as sushi and pizza bars, which serve to (1) increase Woolworths’ cost of doing business (up 20bp to 20.9% FY14) and (2) adversely impact price perception, on which Woolworths trails Coles and ALDI.

> Online Retail is undoubtedly an important market trend. However, as it only comprises 3% of F&L sales, Mercury Two disproportionately focuses on enabling “click and collect”.

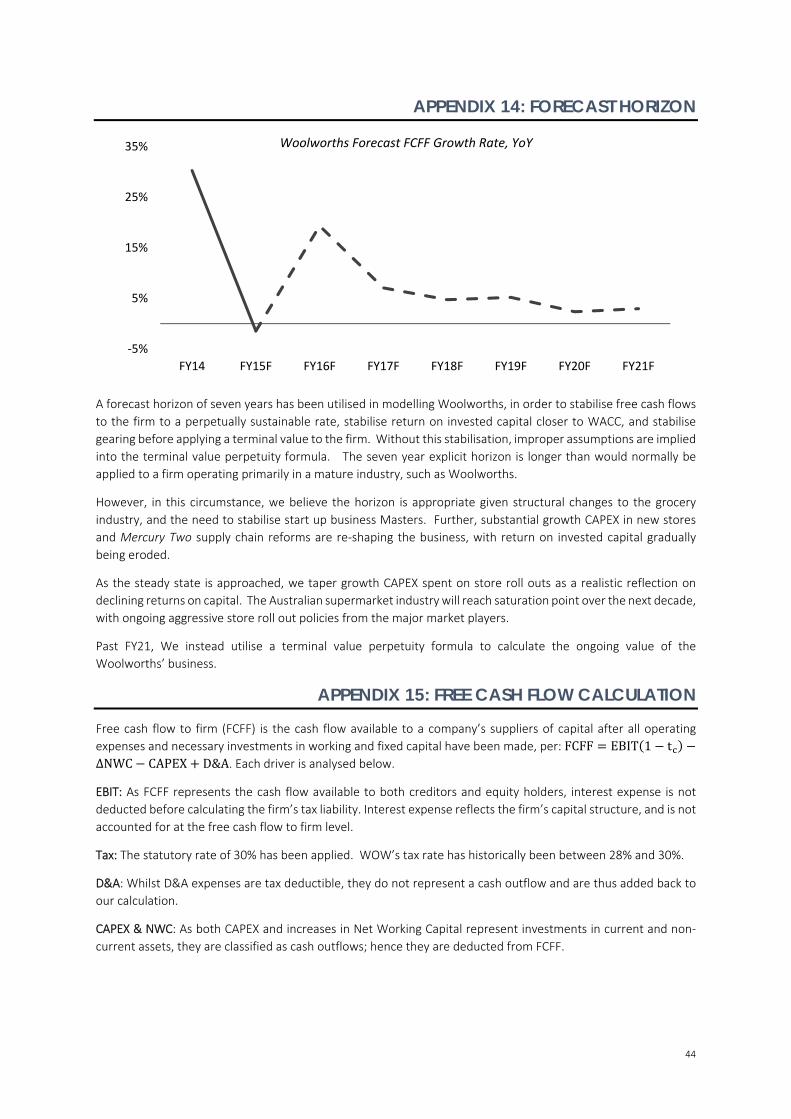

SUPPLY CHAIN DECAY | IS THE “VIRTUOUS DOUBLE LOOP” SLOWING? ‐ Supply chain reforms are a necessity. FY14 F&L Inventory DSO have risen to 34.1 (excl.

Masters), a level not seen since FY03. Improving inventory turnover is critical, as interest free gearing is created from the timing gap between customer and supplier payments. Slowing inventory turnover impacts stock freshness and limits WOW’s ability to achieve volume‐driven productivity gains. With project leader Julie Coates leaving 10 months in to the 5 year reform, we are concerned for effective execution of Mercury Two.

VALUATION | 16.5% DOWNSIDE $m AUD FY13 FY14 FY15 FY16 FY17

Revenue 58,516 60,773 63,786 65,780 67,891 Gross Profit 15,762 16,478 17,292 17,695 18,127 EBITDA 4,619 4,772 4,946 4,893 4,841 NPAT 2,359 2,459 2,545 2,441 2,363

Gross Margin 26.9% 27.1% 27.1% 26.9% 26.7% Net Margin 4.0% 4.0% 4.0% 3.7% 3.5%

LT Debt to Assets 19.2% 17.1% 15.9% 14.6% 13.3% Net Interest 12.3x 14.5x 15.3x 15.1x 15.1x

Return on Equity 25.3% 23.3% 22.0% 19.4% 17.4% EPS ($) 1.91 1.91 2.03 1.93 1.86

WOW.ASX SELL

GICS Industry: Food & Staples Retailing

GICS Sector: Consumer Staples

Target Price: 29.27

Last Price 19/09/2014 35.07

52 week high 38.92

52 week low 32.42

Market capitalisation ($bn) 44.06

Shares (m) 1,248

SYDNEY UNIVERSITY RESEARCH GROUP

Total Area and Return on Funds

Employed

Source: Company Reports

0.0

0.5

1.0

1.5

2.0

FY09 FY10 FY11 FY12 FY13 FY14

Price History Rebased

WOW ASX200

Source: Bloomberg

24%

25%

26%

27%

28%

29%

30%

31%

32%

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

FY10 FY11 FY12 FY13 FY14

Area sqm '000

Total Area (LHS)

ROFE (RHS)

2

6.61%

7.09%

7.44%7.74%

7.92%7.73%

FY10 FY11 FY12 FY13 FY14 FY15E

Group EBITDA Margin

BUSINESS DESCRIPTION

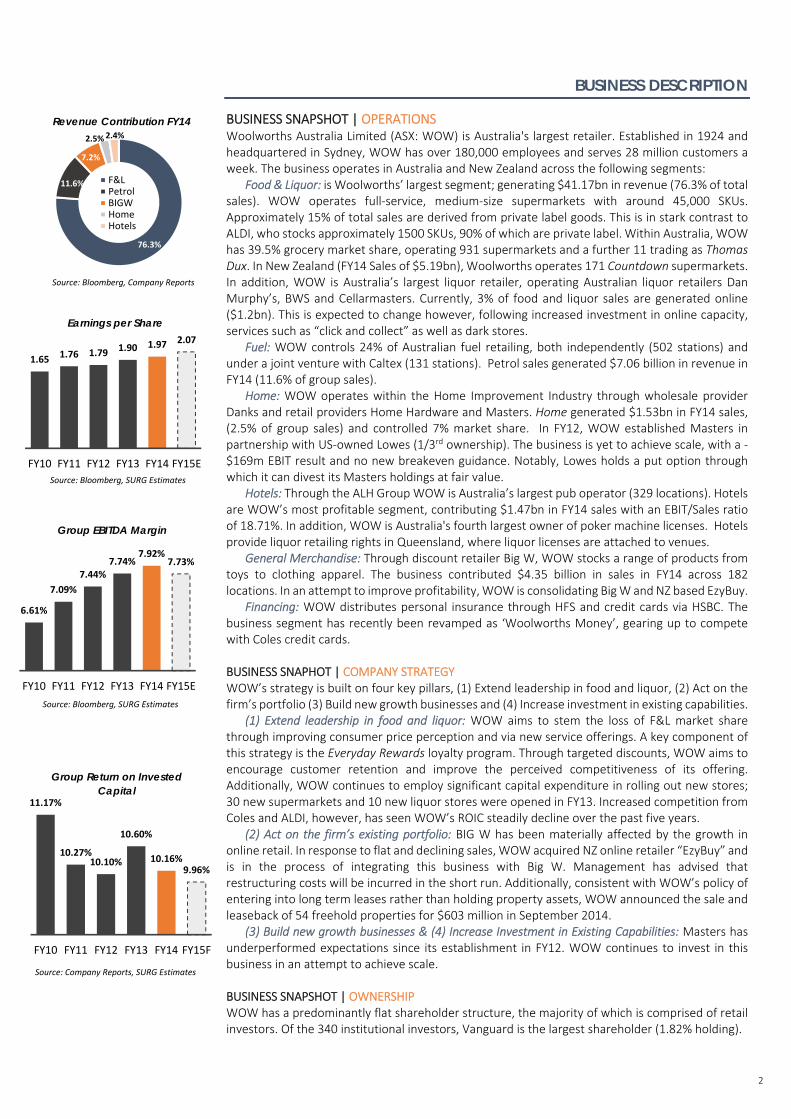

BUSINESS SNAPSHOT | OPERATIONS Woolworths Australia Limited (ASX: WOW) is Australia's largest retailer. Established in 1924 and headquartered in Sydney, WOW has over 180,000 employees and serves 28 million customers a week. The business operates in Australia and New Zealand across the following segments:

Food & Liquor: is Woolworths’ largest segment; generating $41.17bn in revenue (76.3% of total sales). WOW operates full‐service, medium‐size supermarkets with around 45,000 SKUs. Approximately 15% of total sales are derived from private label goods. This is in stark contrast to ALDI, who stocks approximately 1500 SKUs, 90% of which are private label. Within Australia, WOW has 39.5% grocery market share, operating 931 supermarkets and a further 11 trading as Thomas Dux. In New Zealand (FY14 Sales of $5.19bn), Woolworths operates 171 Countdown supermarkets. In addition, WOW is Australia’s largest liquor retailer, operating Australian liquor retailers Dan Murphy’s, BWS and Cellarmasters. Currently, 3% of food and liquor sales are generated online ($1.2bn). This is expected to change however, following increased investment in online capacity, services such as “click and collect” as well as dark stores.

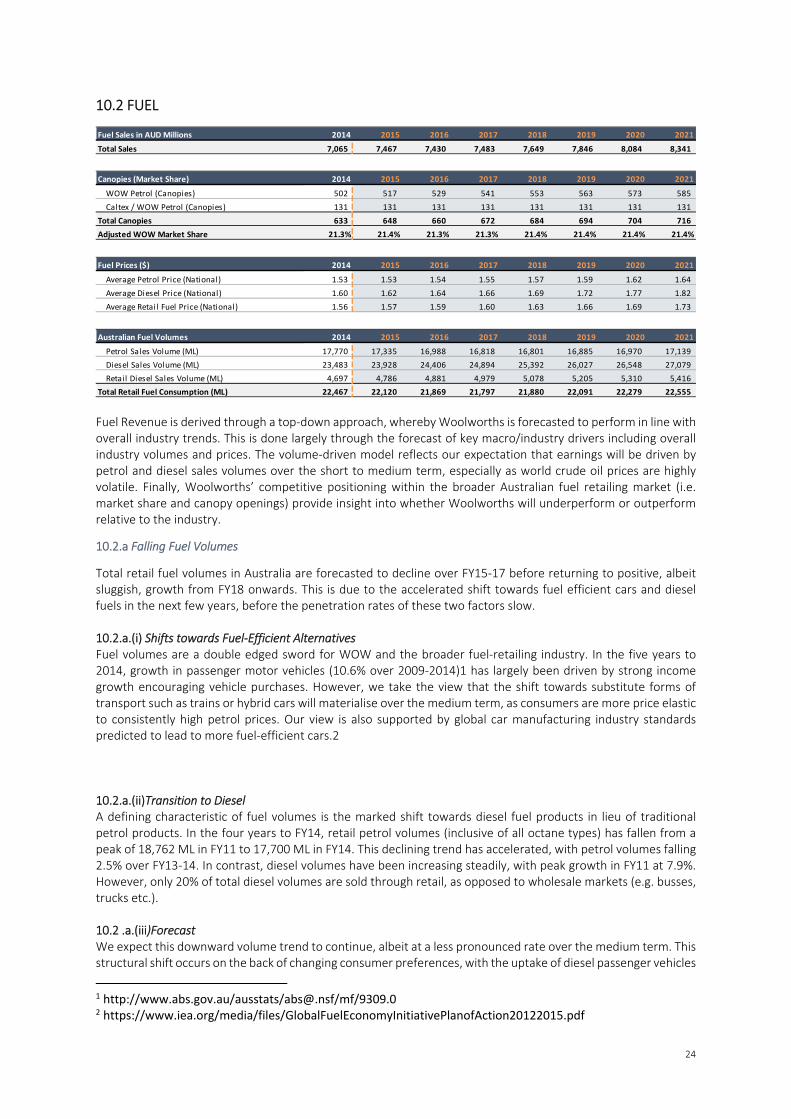

Fuel: WOW controls 24% of Australian fuel retailing, both independently (502 stations) and under a joint venture with Caltex (131 stations). Petrol sales generated $7.06 billion in revenue in FY14 (11.6% of group sales).

Home: WOW operates within the Home Improvement Industry through wholesale provider Danks and retail providers Home Hardware and Masters. Home generated $1.53bn in FY14 sales, (2.5% of group sales) and controlled 7% market share. In FY12, WOW established Masters in partnership with US‐owned Lowes (1/3rd ownership). The business is yet to achieve scale, with a ‐$169m EBIT result and no new breakeven guidance. Notably, Lowes holds a put option through which it can divest its Masters holdings at fair value.

Hotels: Through the ALH Group WOW is Australia’s largest pub operator (329 locations). Hotels are WOW’s most profitable segment, contributing $1.47bn in FY14 sales with an EBIT/Sales ratio of 18.71%. In addition, WOW is Australia's fourth largest owner of poker machine licenses. Hotels provide liquor retailing rights in Queensland, where liquor licenses are attached to venues.

General Merchandise: Through discount retailer Big W, WOW stocks a range of products from toys to clothing apparel. The business contributed $4.35 billion in sales in FY14 across 182 locations. In an attempt to improve profitability, WOW is consolidating Big W and NZ based EzyBuy.

Financing: WOW distributes personal insurance through HFS and credit cards via HSBC. The business segment has recently been revamped as ‘Woolworths Money’, gearing up to compete with Coles credit cards. BUSINESS SNAPHOT | COMPANY STRATEGY WOW’s strategy is built on four key pillars, (1) Extend leadership in food and liquor, (2) Act on the firm’s portfolio (3) Build new growth businesses and (4) Increase investment in existing capabilities.

(1) Extend leadership in food and liquor: WOW aims to stem the loss of F&L market share through improving consumer price perception and via new service offerings. A key component of this strategy is the Everyday Rewards loyalty program. Through targeted discounts, WOW aims to encourage customer retention and improve the perceived competitiveness of its offering. Additionally, WOW continues to employ significant capital expenditure in rolling out new stores; 30 new supermarkets and 10 new liquor stores were opened in FY13. Increased competition from Coles and ALDI, however, has seen WOW’s ROIC steadily decline over the past five years.

(2) Act on the firm’s existing portfolio: BIG W has been materially affected by the growth in online retail. In response to flat and declining sales, WOW acquired NZ online retailer “EzyBuy” and is in the process of integrating this business with Big W. Management has advised that restructuring costs will be incurred in the short run. Additionally, consistent with WOW’s policy of entering into long term leases rather than holding property assets, WOW announced the sale and leaseback of 54 freehold properties for $603 million in September 2014.

(3) Build new growth businesses & (4) Increase Investment in Existing Capabilities: Masters has underperformed expectations since its establishment in FY12. WOW continues to invest in this business in an attempt to achieve scale. BUSINESS SNAPSHOT | OWNERSHIP WOW has a predominantly flat shareholder structure, the majority of which is comprised of retail investors. Of the 340 institutional investors, Vanguard is the largest shareholder (1.82% holding).

Revenue Contribution FY14

76.3%

11.6%

7.2%

2.5%2.4%

F&LPetrolBIGWHomeHotels

Source: Company Reports, SURG Estimates

Group Return on Invested Capital

1.65 1.76 1.79 1.90 1.97 2.07

FY10 FY11 FY12 FY13 FY14 FY15E

Earnings per Share

11.17%

10.27%10.10%

10.60%

10.16%9.96%

FY10 FY11 FY12 FY13 FY14 FY15F

Source: Bloomberg, SURG Estimates

Source: Bloomberg, SURG Estimates

Source: Bloomberg, Company Reports

3

BUSINESS DETAIL | CORPORATE GOVERNANCE & SOCIAL RESPONSIBILITY WOW has sound corporate governance and sufficiently fulfils Australia’s prudential regulatory requirements. To ensure that WOW meets high levels compliance standards, a number of committees have been established, including the Nomination, Audit, Risk Management and Compliance Committees. In addition, WOW attempts to maintain strong community partnerships, investing 1% of pre‐tax profits in community projects and initiatives. In recognition of the firm’s commitment to responsible reporting, WOW is the only Australian retailer listed on the Carbon Disclosure Project Leadership Index. However, we identify the ALH Group as Australia’s 4th largest operator of poker machines. While the firm was awarded the “Socially Responsible Operator of 2012”, we recognise that gambling may be an issue for individuals pursuing Socially Responsible investment strategies.

INDUSTRY OVERVIEW & COMPETITIVE POSITIONING

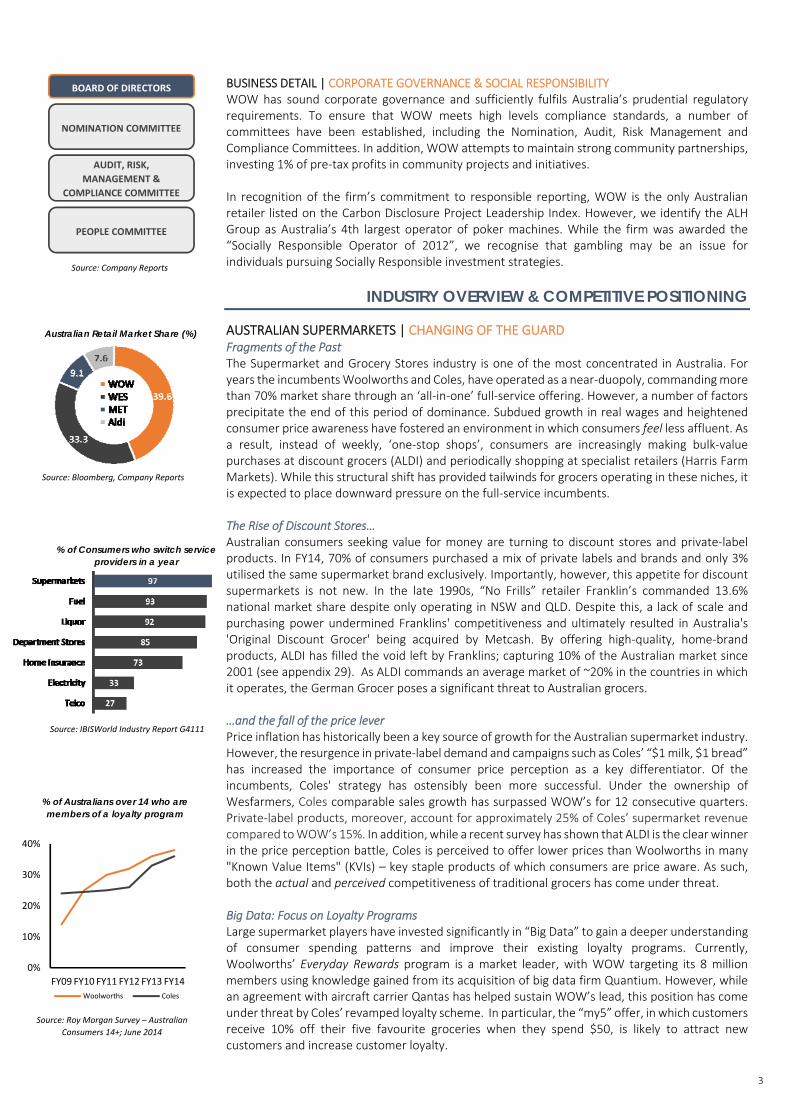

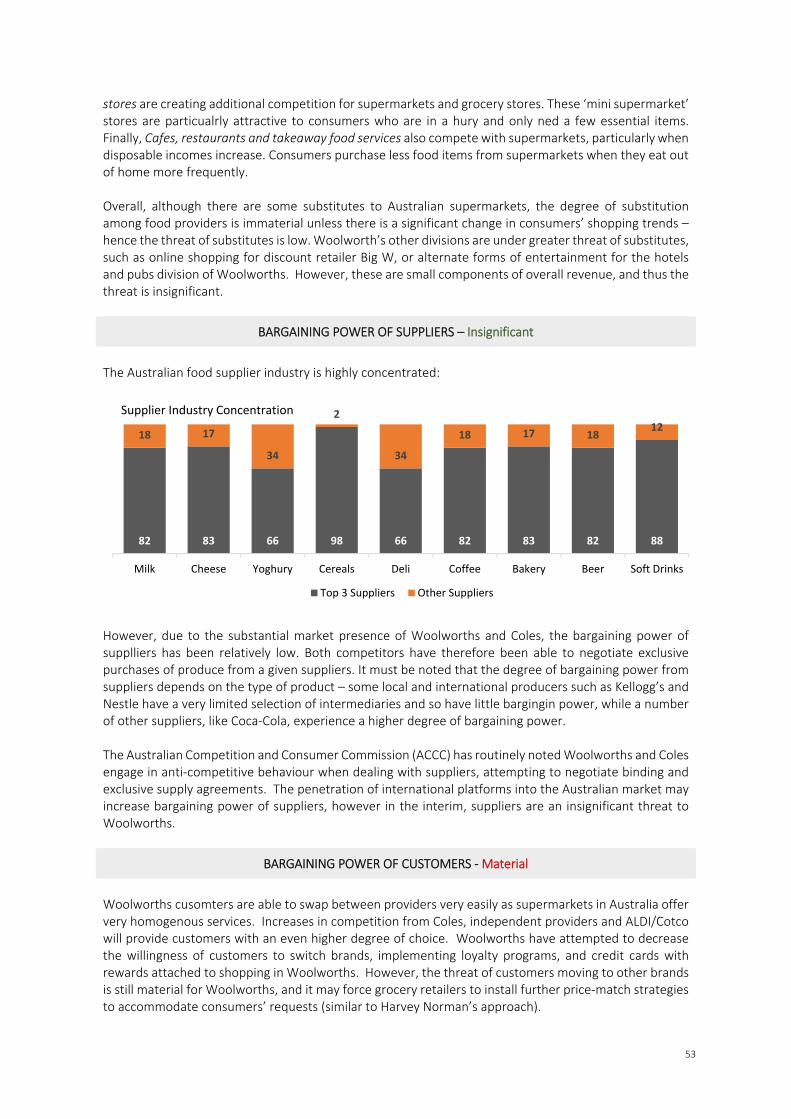

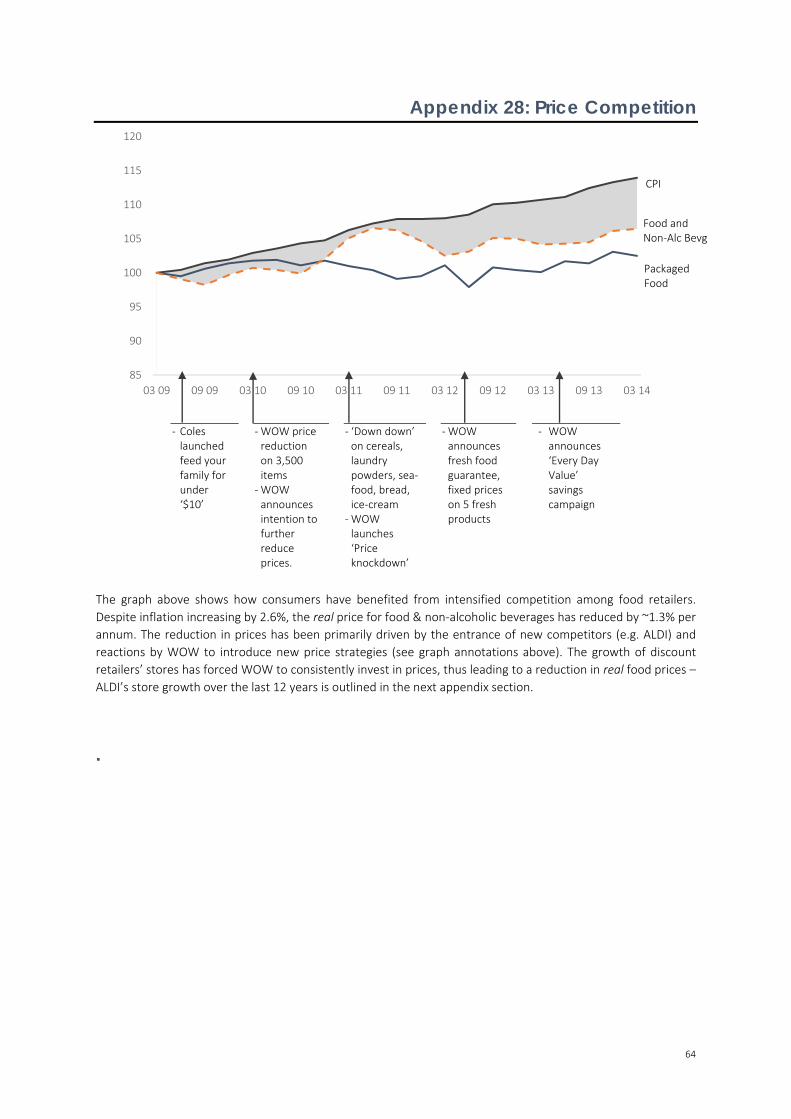

AUSTRALIAN SUPERMARKETS | CHANGING OF THE GUARD Fragments of the Past The Supermarket and Grocery Stores industry is one of the most concentrated in Australia. For years the incumbents Woolworths and Coles, have operated as a near‐duopoly, commanding more than 70% market share through an ‘all‐in‐one’ full‐service offering. However, a number of factors precipitate the end of this period of dominance. Subdued growth in real wages and heightened consumer price awareness have fostered an environment in which consumers feel less affluent. As a result, instead of weekly, ‘one‐stop shops’, consumers are increasingly making bulk‐value purchases at discount grocers (ALDI) and periodically shopping at specialist retailers (Harris Farm Markets). While this structural shift has provided tailwinds for grocers operating in these niches, it is expected to place downward pressure on the full‐service incumbents. The Rise of Discount Stores… Australian consumers seeking value for money are turning to discount stores and private‐label products. In FY14, 70% of consumers purchased a mix of private labels and brands and only 3% utilised the same supermarket brand exclusively. Importantly, however, this appetite for discount supermarkets is not new. In the late 1990s, “No Frills” retailer Franklin’s commanded 13.6% national market share despite only operating in NSW and QLD. Despite this, a lack of scale and purchasing power undermined Franklins' competitiveness and ultimately resulted in Australia's 'Original Discount Grocer' being acquired by Metcash. By offering high‐quality, home‐brand products, ALDI has filled the void left by Franklins; capturing 10% of the Australian market since 2001 (see appendix 29). As ALDI commands an average market of ~20% in the countries in which it operates, the German Grocer poses a significant threat to Australian grocers. …and the fall of the price lever Price inflation has historically been a key source of growth for the Australian supermarket industry. However, the resurgence in private‐label demand and campaigns such as Coles’ “$1 milk, $1 bread” has increased the importance of consumer price perception as a key differentiator. Of the incumbents, Coles' strategy has ostensibly been more successful. Under the ownership of Wesfarmers, Coles comparable sales growth has surpassed WOW’s for 12 consecutive quarters. Private‐label products, moreover, account for approximately 25% of Coles’ supermarket revenue compared to WOW’s 15%. In addition, while a recent survey has shown that ALDI is the clear winner in the price perception battle, Coles is perceived to offer lower prices than Woolworths in many "Known Value Items" (KVIs) – key staple products of which consumers are price aware. As such, both the actual and perceived competitiveness of traditional grocers has come under threat. Big Data: Focus on Loyalty Programs Large supermarket players have invested significantly in “Big Data” to gain a deeper understanding of consumer spending patterns and improve their existing loyalty programs. Currently, Woolworths’ Everyday Rewards program is a market leader, with WOW targeting its 8 million members using knowledge gained from its acquisition of big data firm Quantium. However, while an agreement with aircraft carrier Qantas has helped sustain WOW’s lead, this position has come under threat by Coles’ revamped loyalty scheme. In particular, the “my5” offer, in which customers receive 10% off their five favourite groceries when they spend $50, is likely to attract new customers and increase customer loyalty.

% of Australians over 14 who are members of a loyalty program

Australian Retail Market Share (%)

Source: Bloomberg, Company Reports

Source: Company Reports

% of Consumers who switch service providers in a year

Source: IBISWorld Industry Report G4111

BOARD OF DIRECTORS

NOMINATION COMMITTEE

AUDIT, RISK,

MANAGEMENT &

COMPLIANCE COMMITTEE

PEOPLE COMMITTEE

0%

10%

20%

30%

40%

FY09 FY10 FY11 FY12 FY13 FY14

Woolworths Coles

Source: Roy Morgan Survey – Australian

Consumers 14+; June 2014

4

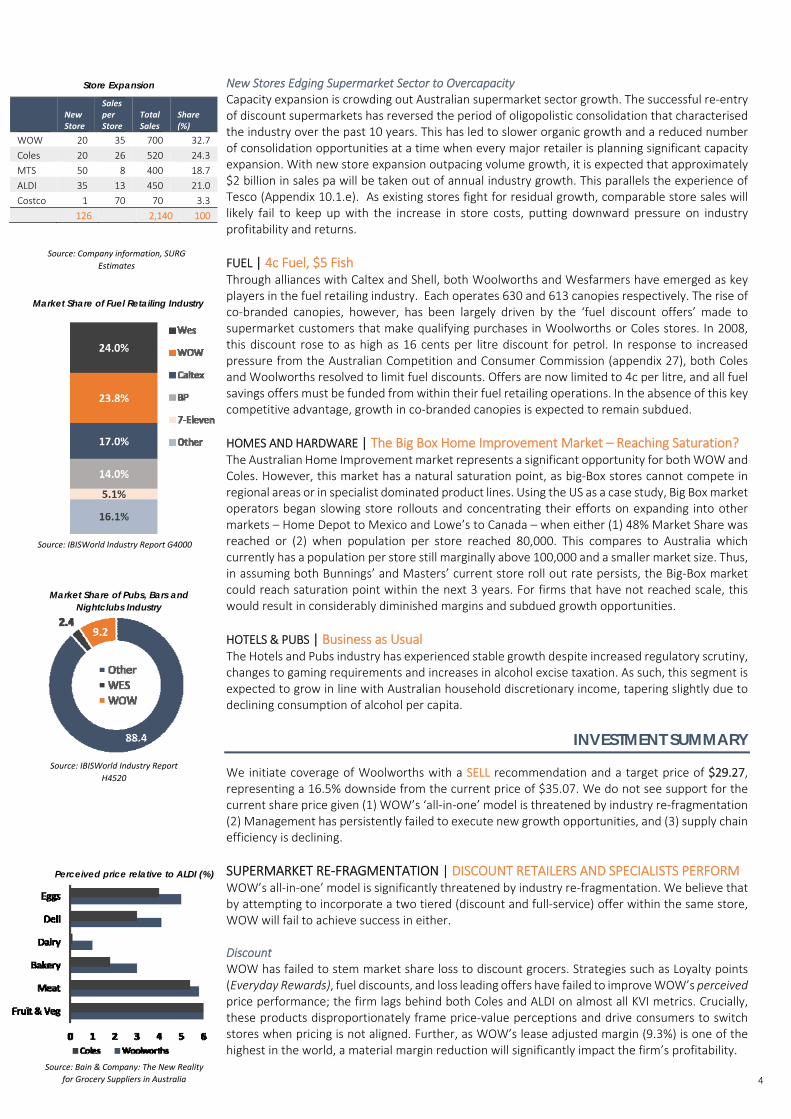

New Stores Edging Supermarket Sector to Overcapacity Capacity expansion is crowding out Australian supermarket sector growth. The successful re‐entry of discount supermarkets has reversed the period of oligopolistic consolidation that characterised the industry over the past 10 years. This has led to slower organic growth and a reduced number of consolidation opportunities at a time when every major retailer is planning significant capacity expansion. With new store expansion outpacing volume growth, it is expected that approximately $2 billion in sales pa will be taken out of annual industry growth. This parallels the experience of Tesco (Appendix 10.1.e). As existing stores fight for residual growth, comparable store sales will likely fail to keep up with the increase in store costs, putting downward pressure on industry profitability and returns.

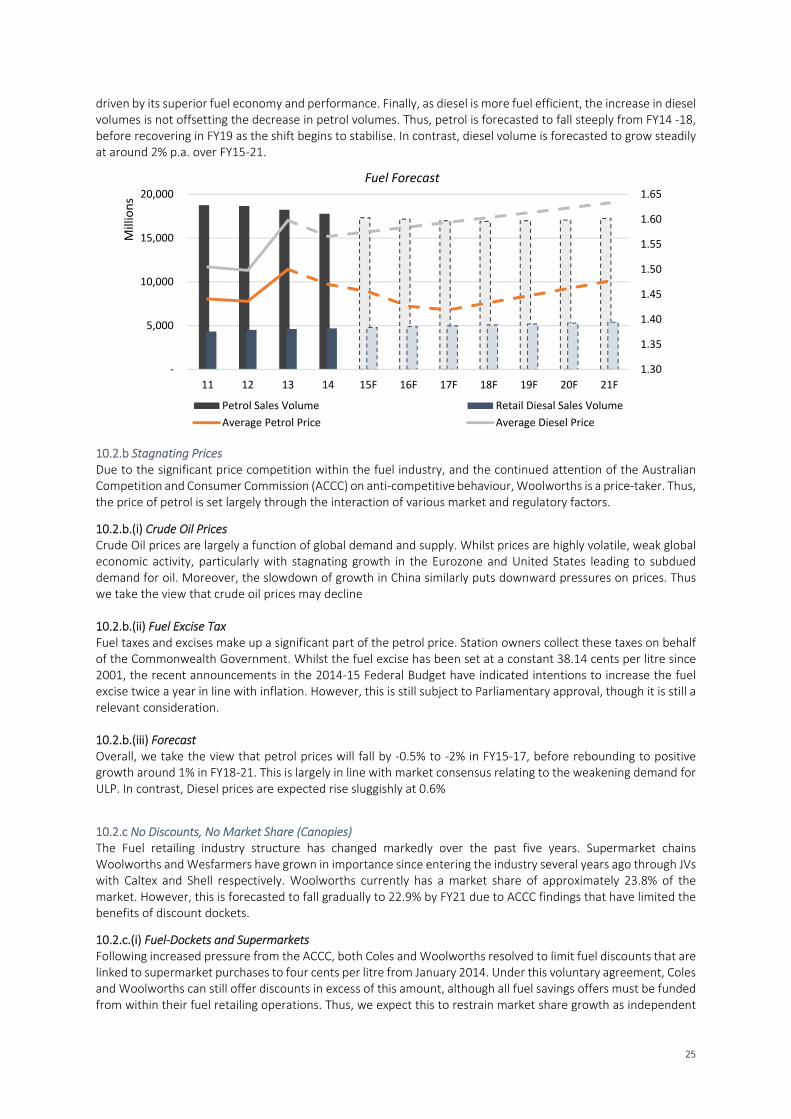

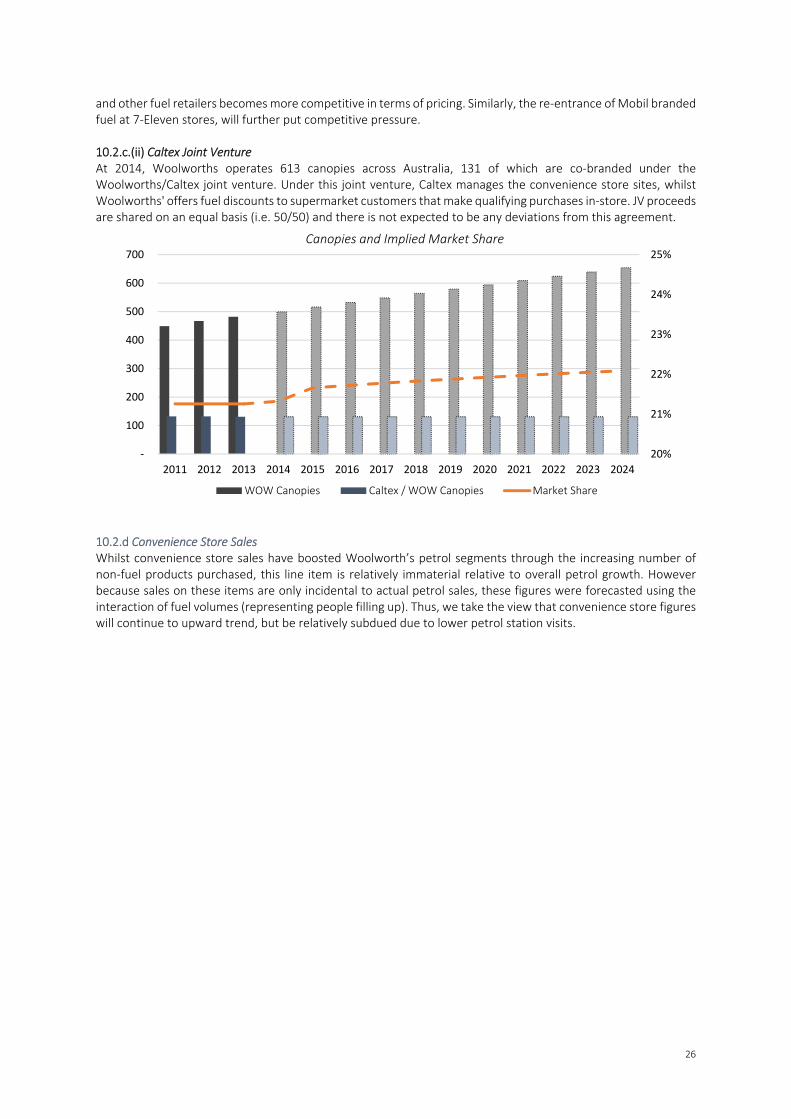

FUEL | 4c Fuel, $5 Fish Through alliances with Caltex and Shell, both Woolworths and Wesfarmers have emerged as key players in the fuel retailing industry. Each operates 630 and 613 canopies respectively. The rise of co‐branded canopies, however, has been largely driven by the ‘fuel discount offers’ made to supermarket customers that make qualifying purchases in Woolworths or Coles stores. In 2008, this discount rose to as high as 16 cents per litre discount for petrol. In response to increased pressure from the Australian Competition and Consumer Commission (appendix 27), both Coles and Woolworths resolved to limit fuel discounts. Offers are now limited to 4c per litre, and all fuel savings offers must be funded from within their fuel retailing operations. In the absence of this key competitive advantage, growth in co‐branded canopies is expected to remain subdued.

HOMES AND HARDWARE | The Big Box Home Improvement Market – Reaching Saturation? The Australian Home Improvement market represents a significant opportunity for both WOW and Coles. However, this market has a natural saturation point, as big‐Box stores cannot compete in regional areas or in specialist dominated product lines. Using the US as a case study, Big Box market operators began slowing store rollouts and concentrating their efforts on expanding into other markets – Home Depot to Mexico and Lowe’s to Canada – when either (1) 48% Market Share was reached or (2) when population per store reached 80,000. This compares to Australia which currently has a population per store still marginally above 100,000 and a smaller market size. Thus, in assuming both Bunnings’ and Masters’ current store roll out rate persists, the Big‐Box market could reach saturation point within the next 3 years. For firms that have not reached scale, this would result in considerably diminished margins and subdued growth opportunities.

HOTELS & PUBS | Business as Usual The Hotels and Pubs industry has experienced stable growth despite increased regulatory scrutiny, changes to gaming requirements and increases in alcohol excise taxation. As such, this segment is expected to grow in line with Australian household discretionary income, tapering slightly due to declining consumption of alcohol per capita.

INVESTMENT SUMMARY

We initiate coverage of Woolworths with a SELL recommendation and a target price of $29.27, representing a 16.5% downside from the current price of $35.07. We do not see support for the current share price given (1) WOW’s ‘all‐in‐one’ model is threatened by industry re‐fragmentation (2) Management has persistently failed to execute new growth opportunities, and (3) supply chain efficiency is declining.

SUPERMARKET RE‐FRAGMENTATION | DISCOUNT RETAILERS AND SPECIALISTS PERFORM WOW’s all‐in‐one’ model is significantly threatened by industry re‐fragmentation. We believe that by attempting to incorporate a two tiered (discount and full‐service) offer within the same store, WOW will fail to achieve success in either. Discount WOW has failed to stem market share loss to discount grocers. Strategies such as Loyalty points (Everyday Rewards), fuel discounts, and loss leading offers have failed to improve WOW’s perceived price performance; the firm lags behind both Coles and ALDI on almost all KVI metrics. Crucially, these products disproportionately frame price‐value perceptions and drive consumers to switch stores when pricing is not aligned. Further, as WOW’s lease adjusted margin (9.3%) is one of the highest in the world, a material margin reduction will significantly impact the firm’s profitability.

Source: Company information, SURG

Estimates

New Store

Sales per Store

Total Sales

Share (%)

WOW 20 35 700 32.7

Coles 20 26 520 24.3

MTS 50 8 400 18.7

ALDI 35 13 450 21.0

Costco 1 70 70 3.3

126 2,140 100

Store Expansion

Market Share of Fuel Retailing Industry

Source: IBISWorld Industry Report G4000

Perceived price relative to ALDI (%)

Source: Bain & Company: The New Reality

for Grocery Suppliers in Australia

Market Share of Pubs, Bars and Nightclubs Industry

Source: IBISWorld Industry Report

H4520

5

3,8604,240 4,470

4,7405,140

5,510

174 183 222 320654

993

FY09 FY10 FY11 FY12 FY13 FY14

Bunnings WOW

In addition to perceived price performance, WOW is unable to achieve actual price competitiveness with discount retailer ALDI. As WOW maintains a premium range of 45,000 SKUs compared to ALDI’s 1,250, the latter has a fundamentally lower cost base. Supermarket history indicates, moreover, that there is a significant appetite for discount supermarkets from the Australian consumer, as Franklins attained a 13.6% market share. As ALDI averages ~20% market share internationally, we expect the German grocer to take material market share from Woolworths. Specialists Here to Stay WOW’s focus on offering in‐store premium services is an identity crisis. Serving barista coffee, and freshly cooked food such as pizzas and bakeries increases WOW’s cost of doing business (+20bps FY14) and decreases WOW’s perceived price competitiveness. At the same time, a strategic focus on discount products reduces the perceived quality of WOW’s specialist products. As such, we do not believe WOW will capture sufficient market share from specialist providers, particularly well recognised brands such as Domino’s Pizza (13.4% market share). In addition, as Coles is pursuing a similar store enhancement policy, this strategic direction offers little competitive advantage. Thus, with 61% of consumers shopping with both specialists and supermarkets each week, we see no abatement to the success of specialists in Australia.

PRICE CATALYSTS: Despite ALDI’s rise, the market is overly complacent in forecasting WOW’s market power. Incremental market share data will reveal the extent of dual losses to discount and specialists, undermining valuation with downward revisions in revenue growth and cost control.

CAPITAL MANAGEMENT | NO MASTERS OF GROWTH Masters – A Low(e) Point In applying the experience of its American partner, WOW has fundamentally misunderstood the fragmented nature of Australian hardware. To quote then CEO, Melinda Smith, “We didn’t know a lot about this business when we set the budget”. Despite the fact it took Bunnings over a century to achieve 17% market share, Management continues to defend its overly optimistic growth forecasts. Moreover, a failure to grasp seasonality of Australian hardware has led to poor inventory turnover, with inventory days increasing to 38.3 days in FY14, up from 31.0 in FY10. Most crucially, Masters has a mediocre customer value proposition, with “bright lights” and “air conditioning” cited as key differentiators to Bunnings. These factors have failed to attract tradespeople, who continue to return to the “rougher” Bunnings. The result of this is that Masters has 49 loss making stores with no new break even guidance. We forecast Masters will incur further losses as Management invests in a save‐face operation, indicative of a failure to create new growth.

Online Sales ‐ Bricks vs. Clicks Few sequels are as good as the original, and Managements second Project Mercury is particularly uninspiring. While online retailing is a notable market trend, online sales comprise 2% of WOW’s F&L sales. We believe the headline focus of Mercury Two on “click and collect” functionality misses the core driver of Woolworths’ performance during the 2000s, which was inventory turnover.

PRICE CATALYSTS: The market has not priced the implications of a failure to create growth in a mature firm: when Masters missed guidance (12/08/14), WOW moved only ‐45bps. Further losses will emphasise Woolworths’ decline. Lowe’s put option may also materially affect WOW cash flow.

SUPPLY CHAIN DECAY | THE END OF THE VIRTUOUS LOOP? The benefits of Project Refresh have eroded, with inventory turning only 10 times in FY14, a level not seen since FY03. WOW’s historic success has been driven by a virtuous cycle of volume‐driven productivity gains. Under this business model, WOW achieves volume growth through driving down costs and investing savings in lower prices for customers. A key driver of this “double loop”, however, is the relationship between WOW’s sales and inventories. As inventory turns faster than payables, Management can draw upon interest free leverage to invest in cost efficiencies. Thus, declining inventory and an upward trend in cost of doing business since FY10 has limited the double loop, restricting scope for investment, price drops and volume growth. In addition, slower inventory turnover negatively impacts the freshness of WOW’s produce, further eroding market share. Thus, we forecast cost improvements to have peaked, with margins contracting, and supply chain inefficiencies to extend. PRICE CATALYSTS: We perceive market expectations of Mercury Two as replicating Project Refresh, however FY15 updates of stagnant inventory turns will reverse consensus on the reform.

WOW & ALDI Market Share: Eastern Australia

0%

3%

6%

9%

12%

15%

0%

10%

20%

30%

40%

50%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

Woolworths (LH) ALDI (RH)

WOW Online Sales $m AUD

Total Area and Return on Funds Employed

Source: ABS, Bloomberg, SURG Estimates

118.8188.9

307.9

600.4

1074.3

FY10 FY11 FY12 FY13 FY14

24%

25%

26%

27%

28%

29%

30%

31%

32%

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

FY10 FY11 FY12 FY13 FY14

Area sqm '000

Total Area (LHS)

ROFE (RHS)

Source: Company Reports

Source: Company Reports

Source: IBISWorld Industry Report G4231

Historical Hardware Revenue

6

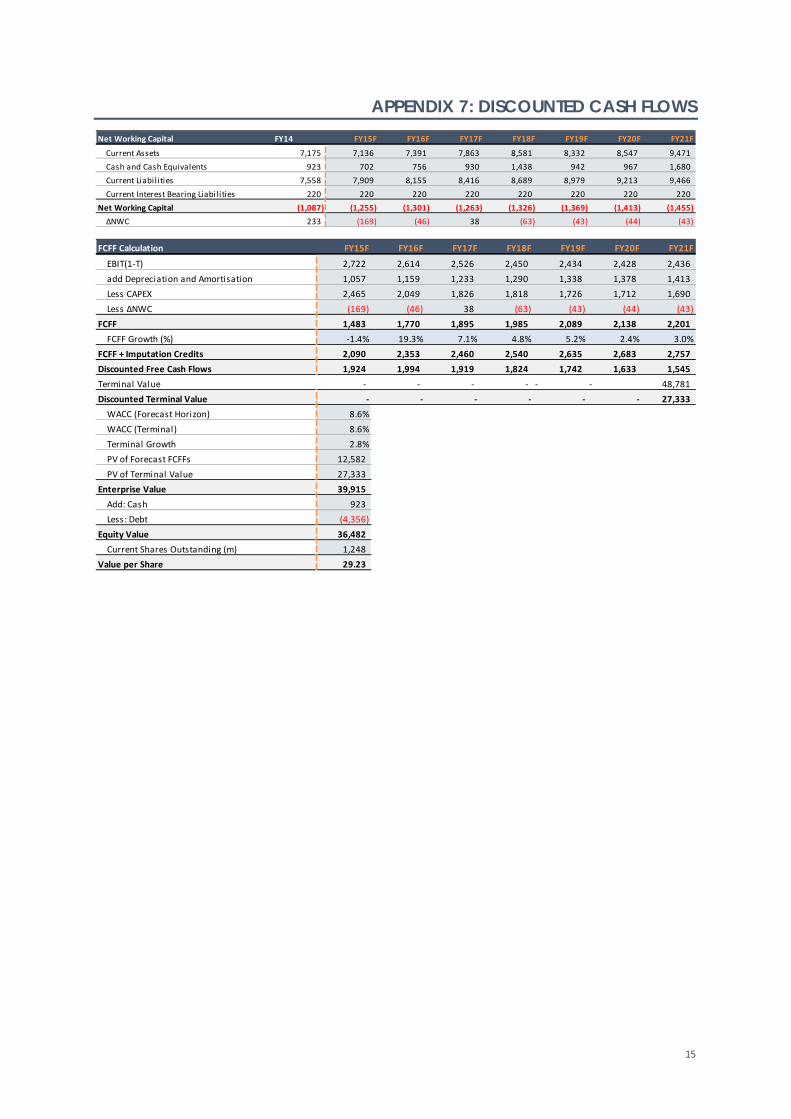

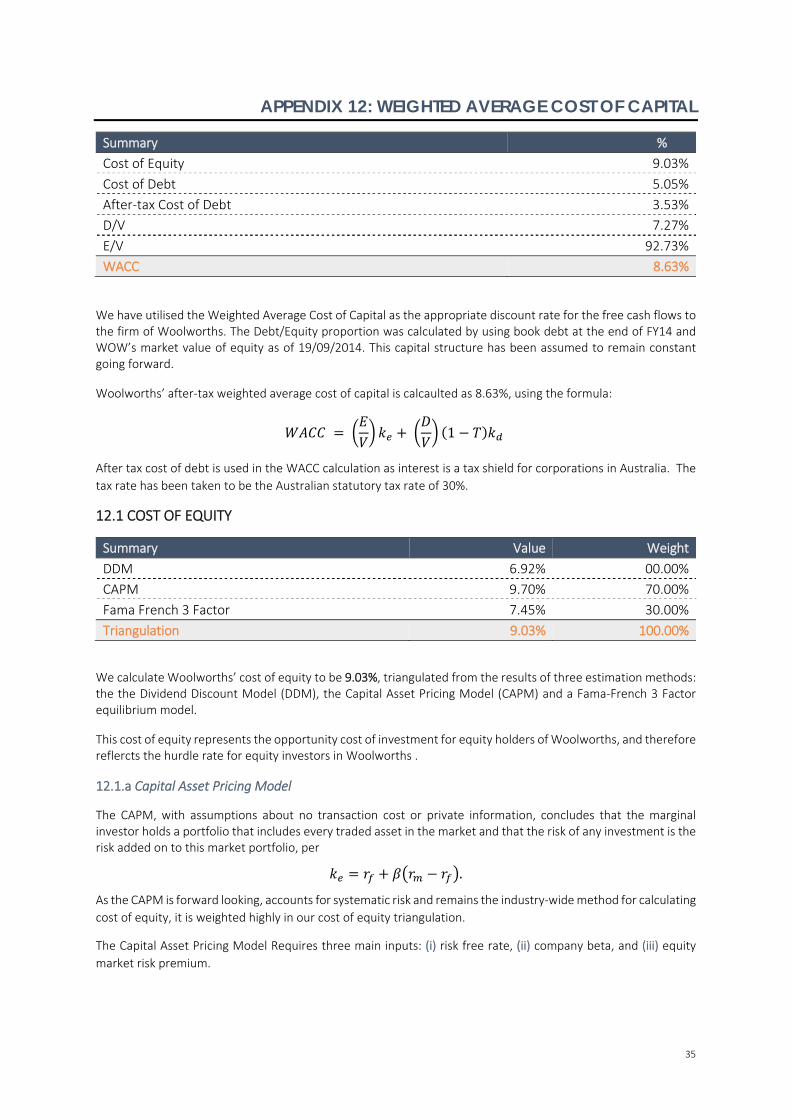

WACC Derivation

WACC (Explicit) 8.63%

WACC (Terminal) 8.63%

Terminal Growth 2.82%

PV Forecast FCFFs $ 12,582

PV Terminal Value $ 27,333

Enterprise Value $ 39,915

Add: Cash $ 923

Less: Debt ‐$ 4,356

Equity Value $ 36,482

Shares Outstanding (m) 1,248

Value per Share $ 29.23

Method Value Weight

DCF Price $29.23 80%

Multiples $29.45 20%

Triangulation $29.27

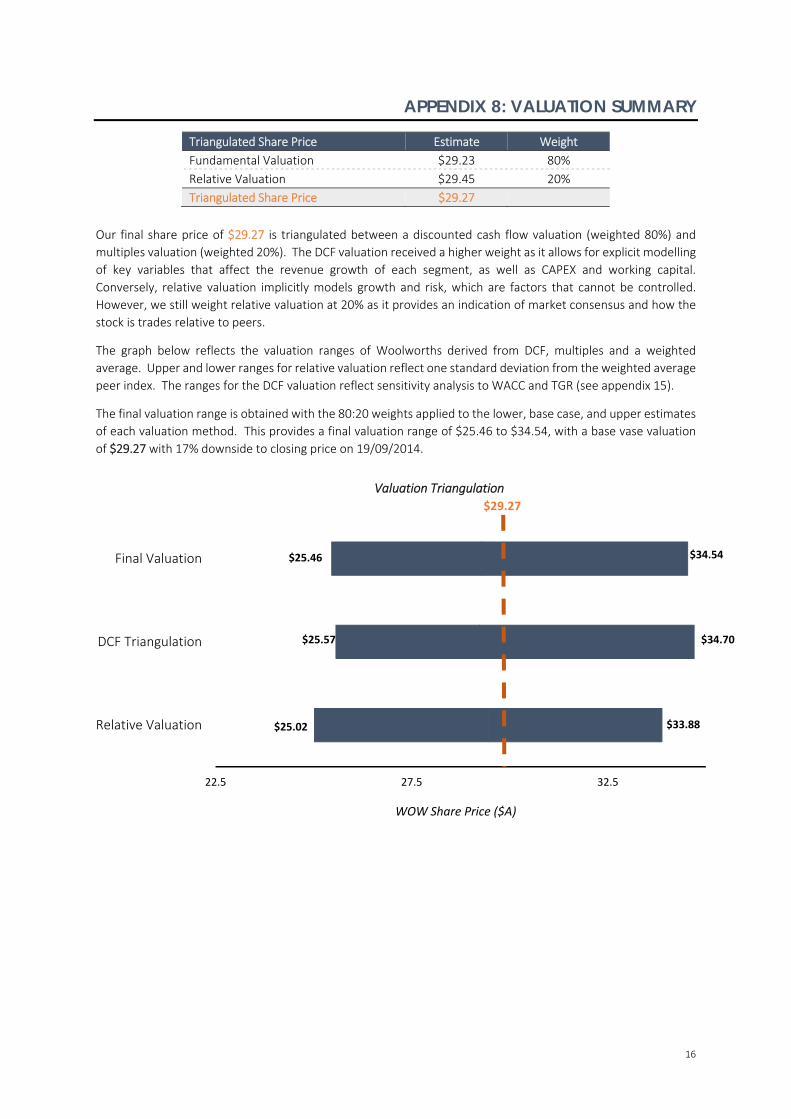

VALUATION

The target share price target of $29.27 has been derived by triangulating the results of two separate valuation methods; a discounted cash flow analysis (DCF) and multiples analysis. The methods were weighted at 80% and 20% respectively, which we justify as the DCF allows explicit modelling of segmental performance.

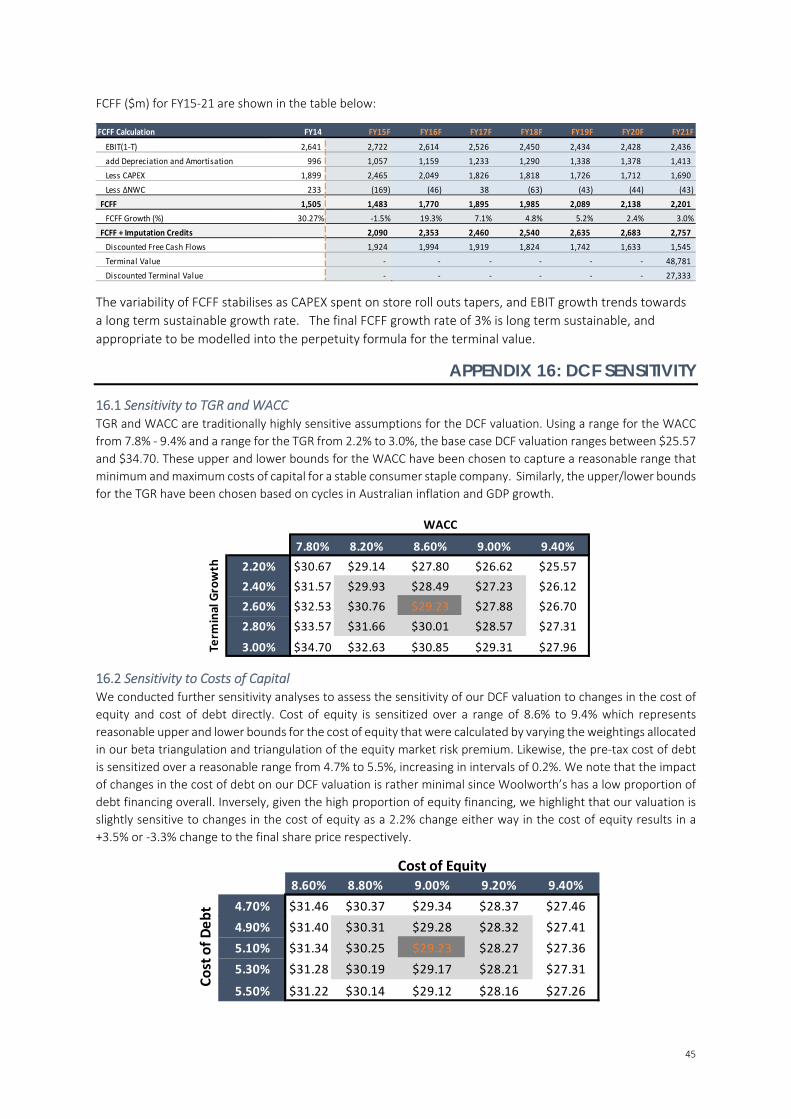

DISCOUNTED CASH FLOW | METHODOLOGY Our DCF analysis produced an intrinsic value per share of $29.23. In deriving this valuation, revenue has been modelled on a segmented basis. As detailed divisional financials are not provided by Management, a sum‐of‐the‐parts DCF has not been utilised. Instead, a two‐stage growth model has been applied in which performance is forecasted year‐on‐year up to 2021, after which we assume revenues will grow at a constant terminal rate. Despite operating in a mature industry, a relatively long explicit forecast horizon was applied, such that the effects of the Masters roll‐out and changes in industry structure could be adequately imputed into the model. After consolidating segment performance at the revenue line, remaining line items were modelled as a consolidated entity. Free cash flows to firm are then calculated, discounted at WACC, with outside equity holdings and debt liabilities netted out. Key assumptions are detailed below, and in Appendix 10.

Revenue Assumptions Food and Liquor revenue is derived as a function of store rollouts, average store size, and average sales per m2. Through FY10‐FY14, WOW rolled‐out an average of 30 supermarkets p.a. in Australia and New Zealand. Per Management’s guidance, we have modelled a reduced opening rate of 16‐17 stores p.a. With respect to store size, Management has indicated that supermarket floor space will increase to accommodate specialist offerings (sushi bars etc.). As such, we expect average store size to grow by 3% in FY15 (in line with Management guidance) before falling to 0.9% in FY21 as this strategy is implemented. Finally, growth in sales per m2, has been modelled per:1 1 . Population growth, as a proxy for market size, is expected to grow at 1.03% throughout FY14‐21. As we are of the view that prices will remain sluggish over the medium‐long term, food inflation is forecasted to range from ‐0.1% in FY15 to 1.9% in FY21, slightly below the RBA’s target CPI rate of 2‐3%. Finally, we take a negative view on WOW’s market share in light of the continued expansion of low‐cost competitors ALDI and Costco and the continued threat of its revitalised rival, Coles. However, we also believe that a lack of available space due to the reluctance of Local and State Governments to change zoning laws will limit ALDI’s ability to adopt its ‘small‐format store’ strategy. As such, market share is expected to fall gradually from 39.60% in FY14 to 35.50% in FY21. This generates total F&L revenue growth of 4.8% in FY14, declining to 2.6% in FY21. Fuel performance is derived through a top‐down approach, whereby WOW is forecasted to

perform in line with overall industry trends. Revenue is therefore modelled as a function of key

macro drivers (Australian retail fuel consumption, average national retail fuel prices) and

Woolworths’ competitive position within the Australian fuel retailing market (market share). From

FY12‐FY14, Australian petrol sales declined on average 1.8% p.a. We forecast stabilisation to 1%

p.a. growth by FY21, with diesel rising 2% p.a. due to increasing demand for fuel efficient vehicles.

Average national prices are forecast to long term trend, according to Australian Institute of

Petroleum figures. Woolworths’ fuel retailing share is assumed relatively constant, declining 0.9%

over the horizon due to ACCC protection of independent retailers. This supports a forecast of 4.4%

fuel revenue growth FY14, tapering to 2.2% FY21.

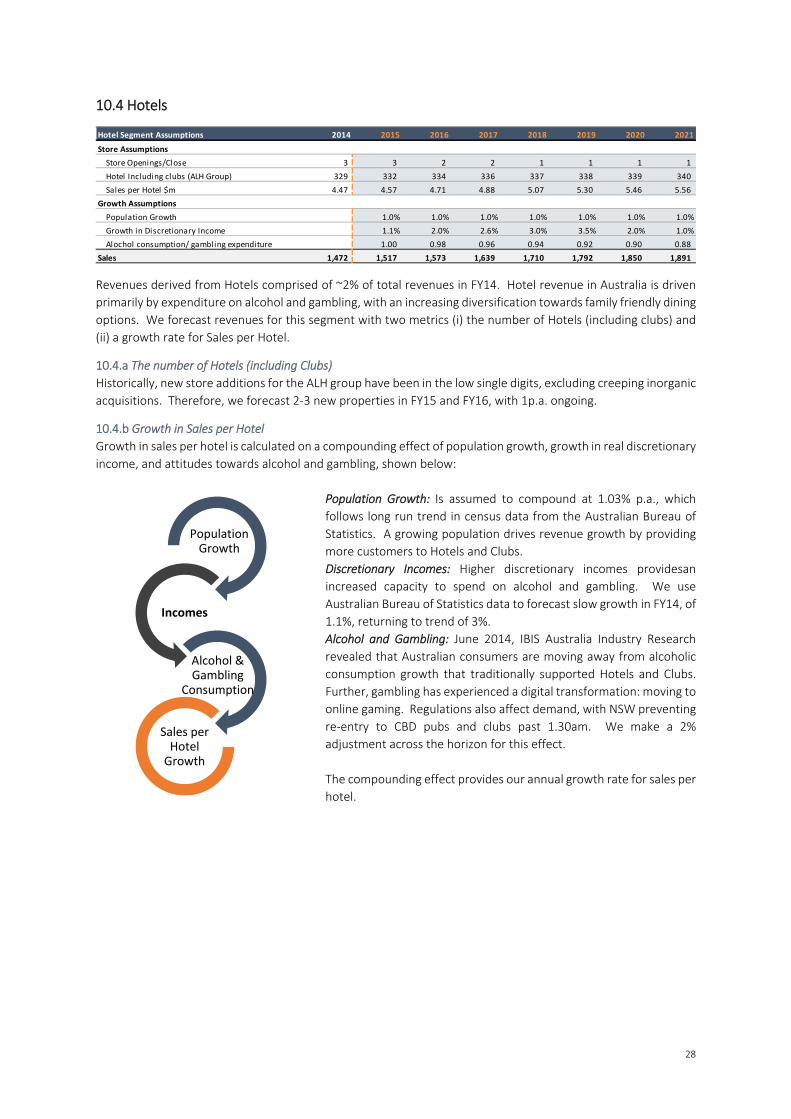

General Merchandise is modelled as a function of sales per m2. The general merchandise segment is forecasted to drop by 0.94% in FY16 as Big W continues to struggle generating meaningful growth. However, it is expected that growth in general merchandise will improve over FY17‐21 following the store transformation, with revenue growing between 1.04% and 1.83% p.a. Hotel revenues were estimated by forecasting two metrics; the number of Hotels (including clubs) and a growth rate for Sales per hotel. As new store additions for the ALH group have historically been in the low digits, we have assumed that hotels will increase by 3 and 2 new properties in FY15 and FY16 respectively, growing at 1 hotel p.a. thereafter. Growth in sales per hotel is indexed to population growth, growth in discretionary income, and social attitudes towards alcohol and gambling.

F&L Revenue Forecast

Source: Company Reports, SURG Estimates

*Source: Company Reports, SURG Estimates

38 40 41 44 45 47 50 53

4 5 5 5 5 5 5 6

10

20

30

40

50

60

FY12

FY13

FY14

FY15E

FY16E

FY17E

FY19E

FY21E

Millions

Aus Sales NZ Sales

Fuel Price and Volume Forecast

1.3

1.4

1.5

1.6

1.7

5

10

15

20

Thousands

Petrol Sales Volume (LHS)

Retail Diesel Sales Volume (LHS)

Petrol Price (RHS)

Diesel Price (RHS)

3,900

4,000

4,100

4,200

4,300

960

1,000

1,040

1,080

1,120

Thousands

Total Area (LHS)

Sales per sqm (RHS)

*Source: Company Reports, SURG Estimates

General Merchandise Forecast

7

Method Value

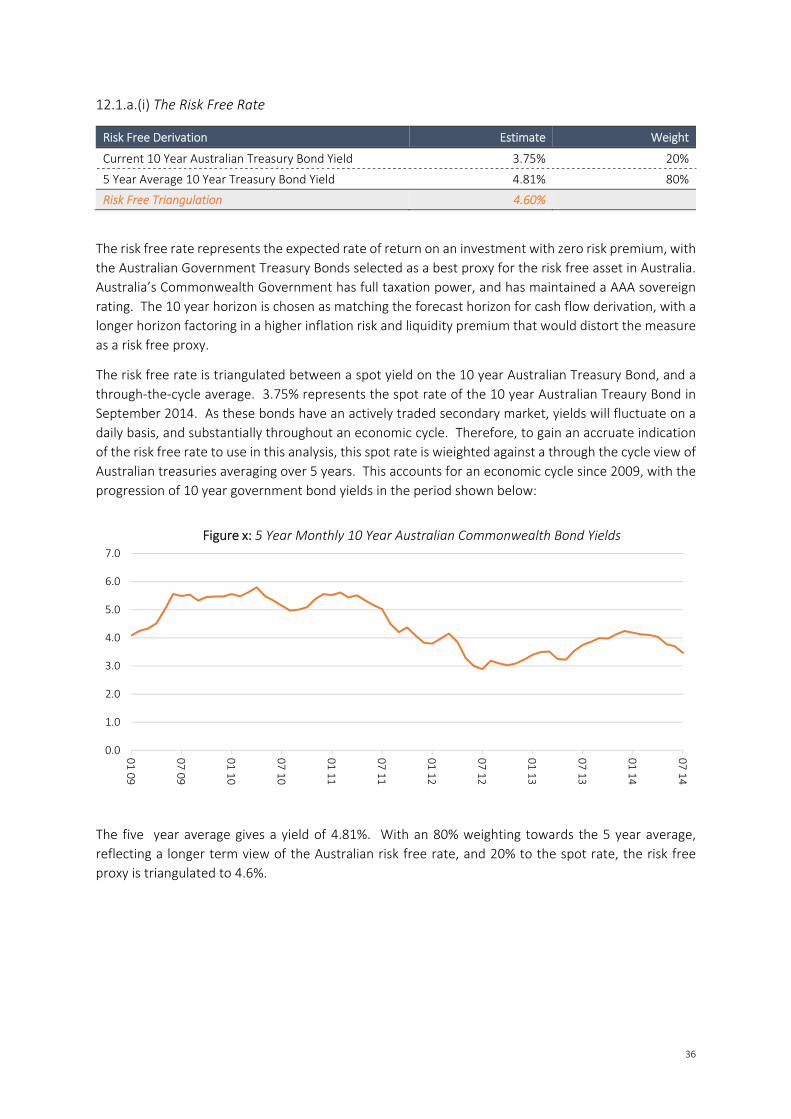

Spot Yield (10Y AU Gov Bond) 3.75%

5 Year Average 4.81%

Risk Free Rate 4.59%

Beta 0.80

Equity Risk Premium Australia 6.38%

CAPM Cost of Equity 9.7%

WOWAU 03/21/19 Spread 0.34%

Credit Rating A‐

Tax Rate 30%

After Tax Cost of Debt 3.53%

WACC 8.63%

Population Growth

Growth in Discretionary

Income

Alcohol & Gambling

Consumption

Sales per Hotel Growth

Method Avg. Value

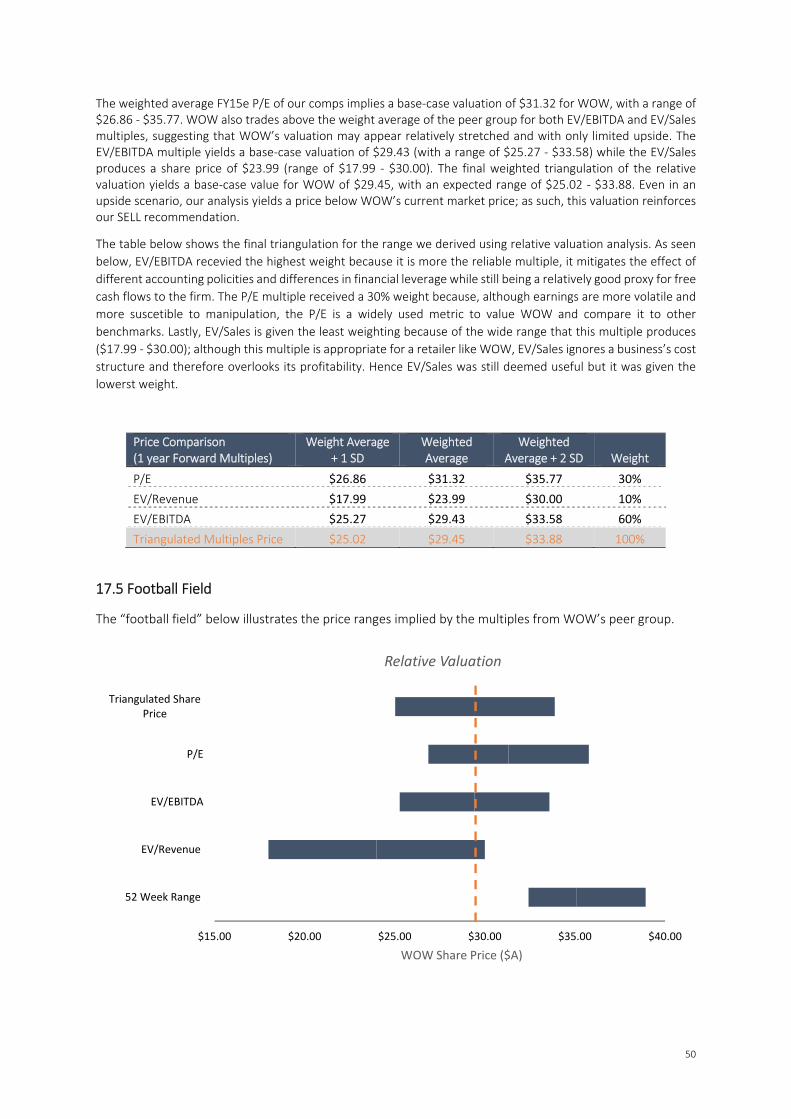

EV/EBITDA $23.99 60%

EV/Revenue $29.43 10%

P/E $31.32 30%

Price 29.45 100%

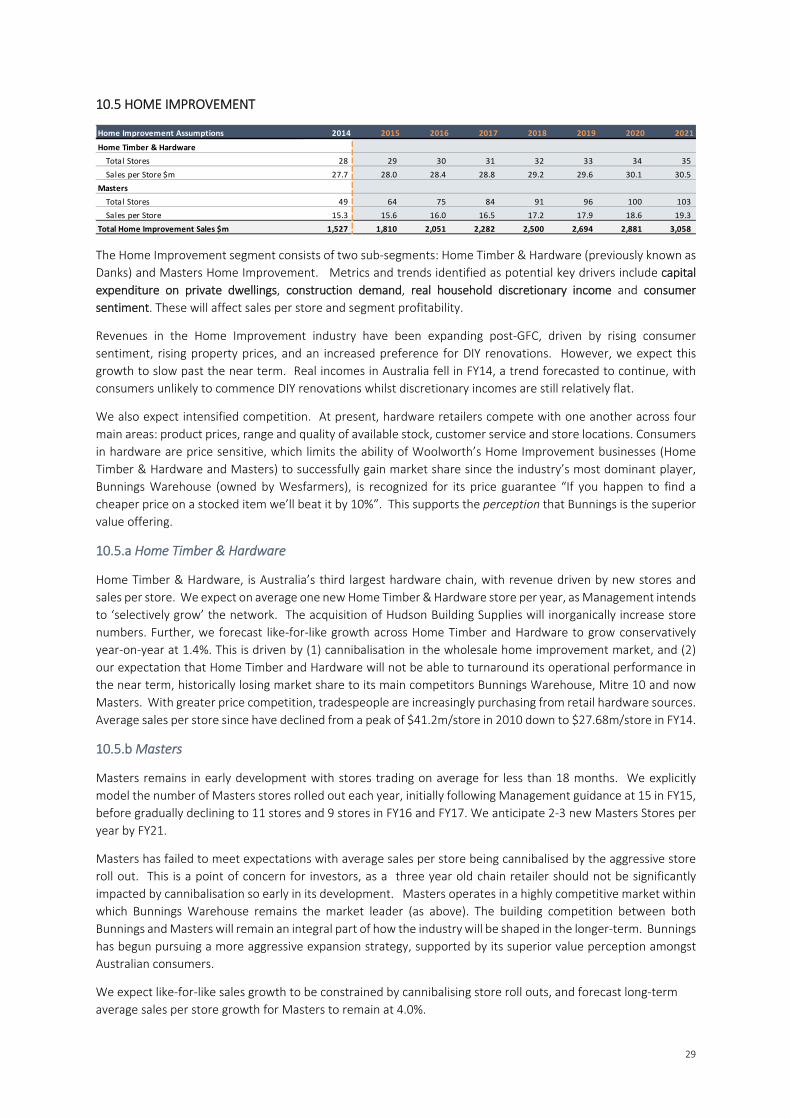

In light of declining alcohol per capita consumption and increasing regulatory restrictions on both alcohol and gambling, we expect consumer sentiment to decline over time. This decrease, however, is counteracted by growth in population growth and growth in disposable income. Accumulatively, we expect Revenue to grow at an average of 3.6% p.a. in FY15‐21. Home Improvement revenue is split between Home Timber & Hardware (formerly Danks) and Masters. Masters is assumed to roll out 15 stores in FY15, tapering to 3 by FY21. Our long term forecast for sales per store growth is 4%. While we do not expect Masters to be a material profit contributor, we accept Management’s assertion that the business will eventually break even. We forecast total home improvement revenue growth of 18.5% FY15, tapering to 6.1% FY21.

Pro Forma Assumptions

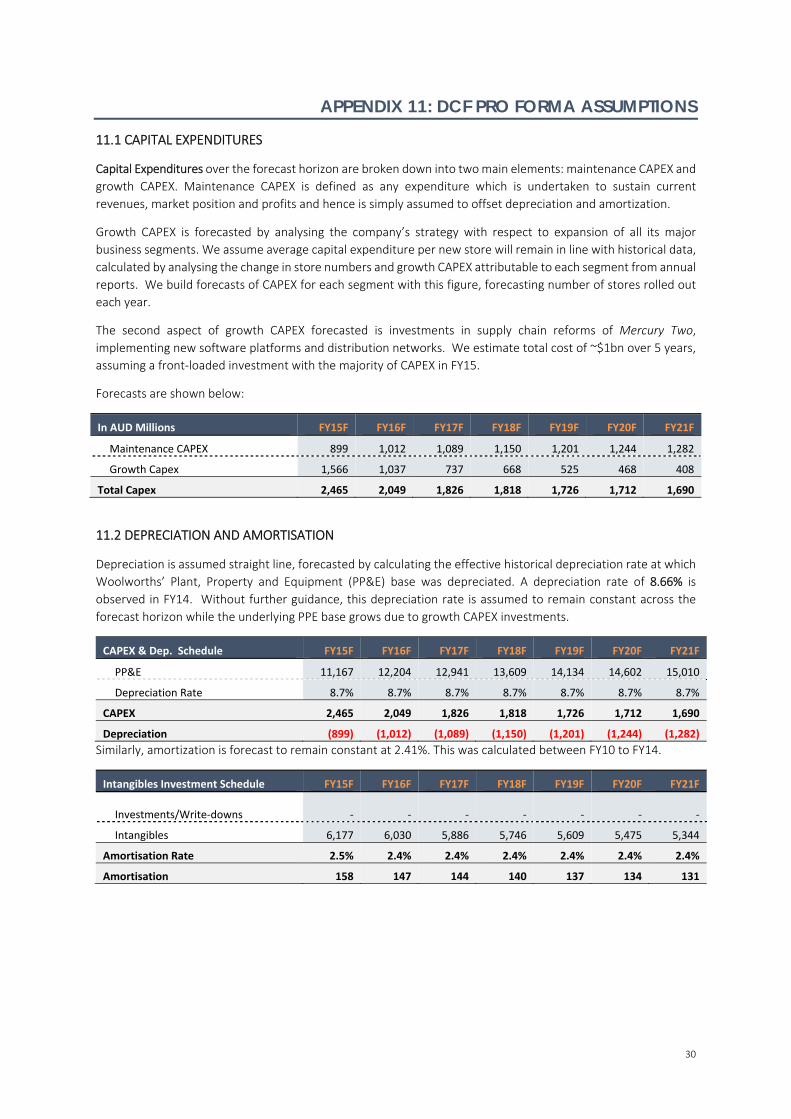

Group statements are forecast upon consolidation. EBITDA Margins plateau at 7.7% in FY15 before declining to 6.5% by FY21. This reflects an increased OPEX ratio from 72.9% in FY15 to 73.6% in FY21 as discussed in our financial analysis. Depreciation and amortisation rates were held constant at their historical rates of 8.9% and 2.4% respectively. Taxation was set at the Australian statutory rate of 30%. No significant corporate financing changes are forecast with the payout ratio remaining between 68%‐70%. Group CAPEX is modelled on segmental CAPEX forecasts, comprising maintenance CAPEX (set to depreciation) plus growth CAPEX to account for increased store openings and investments in supply chain reform. Average CAPEX per store opening is kept at historical levels of $14m. After integrating a front loaded investment attributable to Mercury Two supply chain reforms, which totals $1bn over 5 years, FY15 forecasts of CAPEX total $2,413m. Working Capital remains negative at ‐$1,255m, highlighting the generation of cash flow as inventory turns faster than payables as discussed in our financial analysis.

Free Cash Flows to Firm stabilise to a sustainable 3% growth at the end of the forecast horizon and are calculated by adjusting after‐tax EBIT for cash and non‐cash charges. After adding the value of imputation credits for Australian investors (worth on average $565m p.a.) FCFF is derived for FY15 to be $2,090m, increasing to $2,757m by FY21. WACC is used to discount FCFF’s as a whole firm measure of capital cost and is derived on the left (with further detail in appendix 12). As per our financial analysis, capital structure is held constant.

Undiscounted terminal value as at FY21 is estimated as $47,591m which represents an effective multiple of 17x FY21 FCFF. The terminal WACC is held at 8.6%, with Terminal Growth of 2.8% triangulated between (1) long‐term Australian GDP at 2.75%, (2) RBA inflation expectation 2.4% p.a., (3) population growth of 1.03% and (4) growth rate in F&L industry turnover of 4.1%. Net debt is subtracted from discounted cash flows to provide an equity value which is then divided by shares outstanding to provide an intrinsic valuation per share of $29.23. Sensitivity Analysis

To analyse the robustness of our analysis, we performed a series of sensitivity analyses on WACC

and terminal growth rate, as well as macroeconomic and industry factors (see Appendix 16).

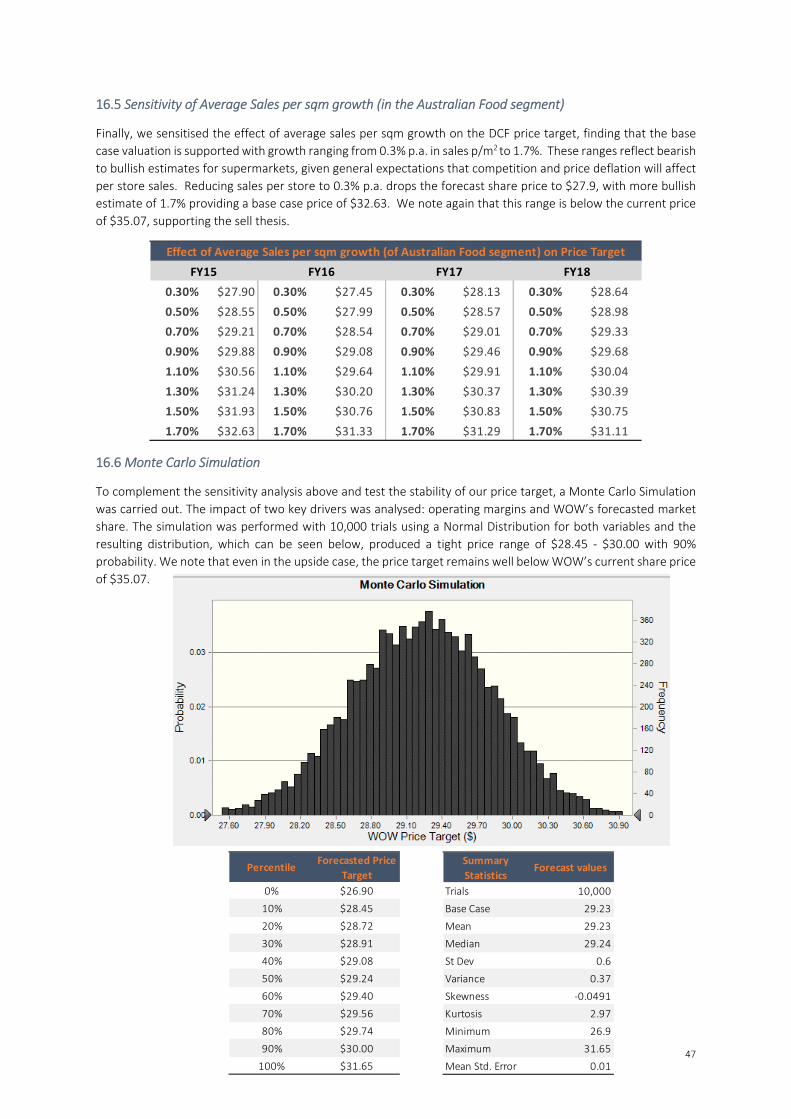

However, as sensitivity analyses are not probability weighted, we complemented this study with a

Monte Carlo simulation. In examining changes in Operating Margins and F&L Market share

assumptions within 10,000 trials, the resulting distribution provides a share price range of $28.45

‐ $30.00 with 90% confidence.

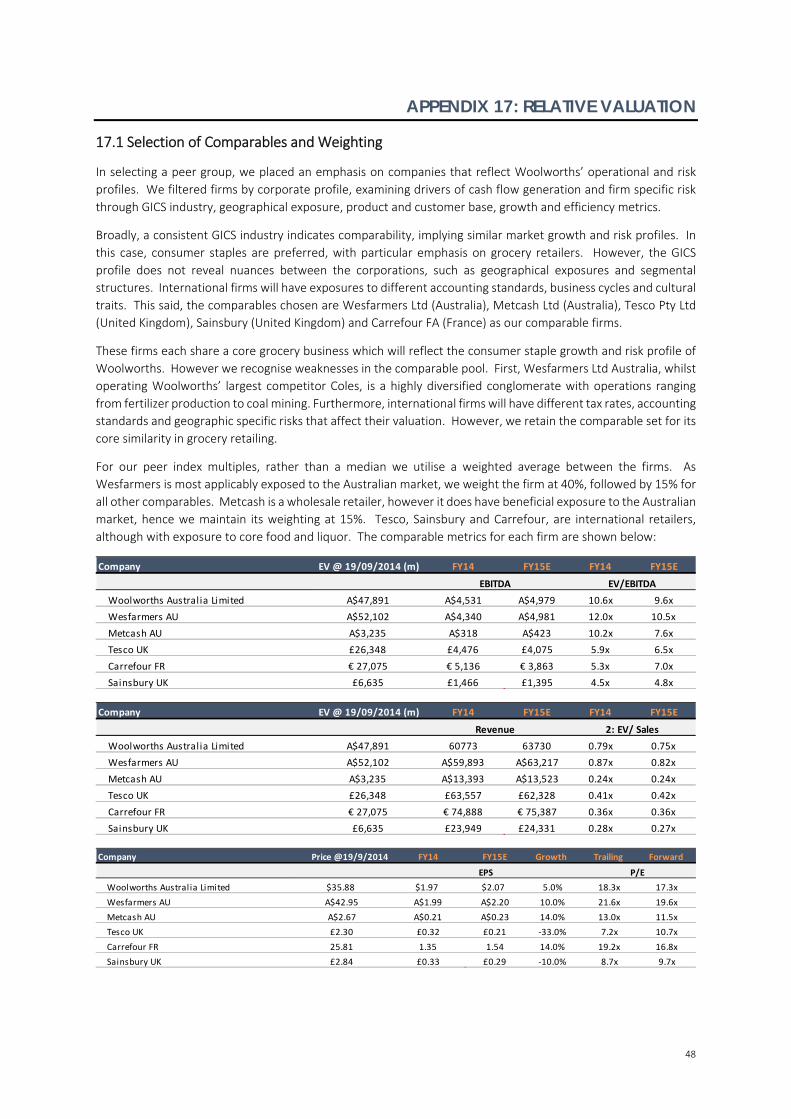

MULTIPLES ANALYSIS | METHODOLOGY In addition to our DCF valuation, we conducted a multiples analysis on the consolidated operations

of WOW. Specifically, we have utilised a weighted average peer index comprised of one‐year

forward estimates of P/E, EV/Sales and EV/EBITDA. Five companies have been utilised to infer the

market value of WOW; Wesfarmers, Metcash, Tesco, Sainsbury, and Carrefour. These firms were

selected as they exhibit similar financial and business profiles to WOW. As Wesfarmers is WOW’s

largest Australian competitor, we applied a weighting of 40%, with other comparables receiving

15%.

WACC Derivation

Hotels Growth Rate

‐5%

5%

15%

25%

35%

DCF: FCFF Growth

Monte Carlo Simulation *Source: Company Reports, SURG Estimates

*Source: Bloomberg

Multiples Analysis

8

The P/E multiple was chosen as it is a widely observed measure of equity in all markets. The weighted average FY15e P/E of our comparables implies a base‐case valuation of $31.32 for WOW. WOW currently trades at a one year forward P/E of 17.3x, a ~15% premium to the market P/E of 15x and a ~4% premium to the 16.6x peer group median. EV/EBITDA was selected as it is largely unaffected by changes in capital structure, while EV/Sales has the advantage of being the least susceptible to differences in accounting policies. As WOW trades above the weighted average of both EV/EBITDA ($29.4) and EV/Sales ($24.0) multiples, the firm appears to be overvalued on a relative basis. In weighting the multiples, outlined in appendix 17, we derive a base case price of $29.45, with higher weighting toward EV/EBITDA to account for cost structure.

FINANCIAL ANALYSIS

PROFITABILITY Stalling Food and Liquor Sales Productivity Woolworth’s sales productivity – measured as average sales per m2 ‐ increased from $11,811 p/m2 in 1999 to a peak of $16,172 p/m2 in 2011. This 37% increase in productivity was primarily driven by supply chain reforms achieved through Project Refresh. However, stagnation has occurred since FY11, with sales p/m2 falling to $16,021 in FY14 (‐5.75%).

We attribute this fall in productivity to (1) aggressive price competition and (2) store roll outs aimed at precipitating market saturation. First, price competition from ALDI and Coles has driven food prices into real deflation, with prices increasing by an average of 0.5% p.a. from FY09‐14. Our forecasts reflect this ongoing price pressure, incorporating an average 0.9% p.a. food inflation from FY15‐21. Second, aggressive supermarket roll outs of 30 per annum cannibalise sales, with 60% opened in postcodes with existing Woolworths’ stores. As Woolworths’ erodes competition by consciously saturating markets with stores, the firm’s normalised return on funds employed has been eroded from 31% in FY10 to 27% FY14.

Our forecast continues sluggish sales p/m2 growth, ranging between ‐0.1% to 0.9% p.a. FY15‐FY21.

Margins Under Pressure Woolworths’ gross profit margins increased from 25.7% in FY09 to 27.11% in FY14, with EBIT margins up to 6.21% in FY14. This improvement was drawn from leveraging market power over suppliers, and rolling out private label products, which reached 15% of total sales in FY14.

However, as revenue growth is slowing at a time of increasing costs, we forecast gross margins to tighten. Revenue growth is stunted by sluggish price inflation, and slowing inventory turns. Additionally, premium services (barista coffee, sushi bars) will increase COGS, requiring specialist staff and produce. As such, gross profit margins tighten in our forecast to 26.4% by FY21, and EBIT margins to 4.56% in FY21. EBIT margin contraction is amplified by rent expense. However, we do forecast some SG&A efficiencies with automation from Mercury Two declining from 16.1% in FY14 to 15.97% F21.

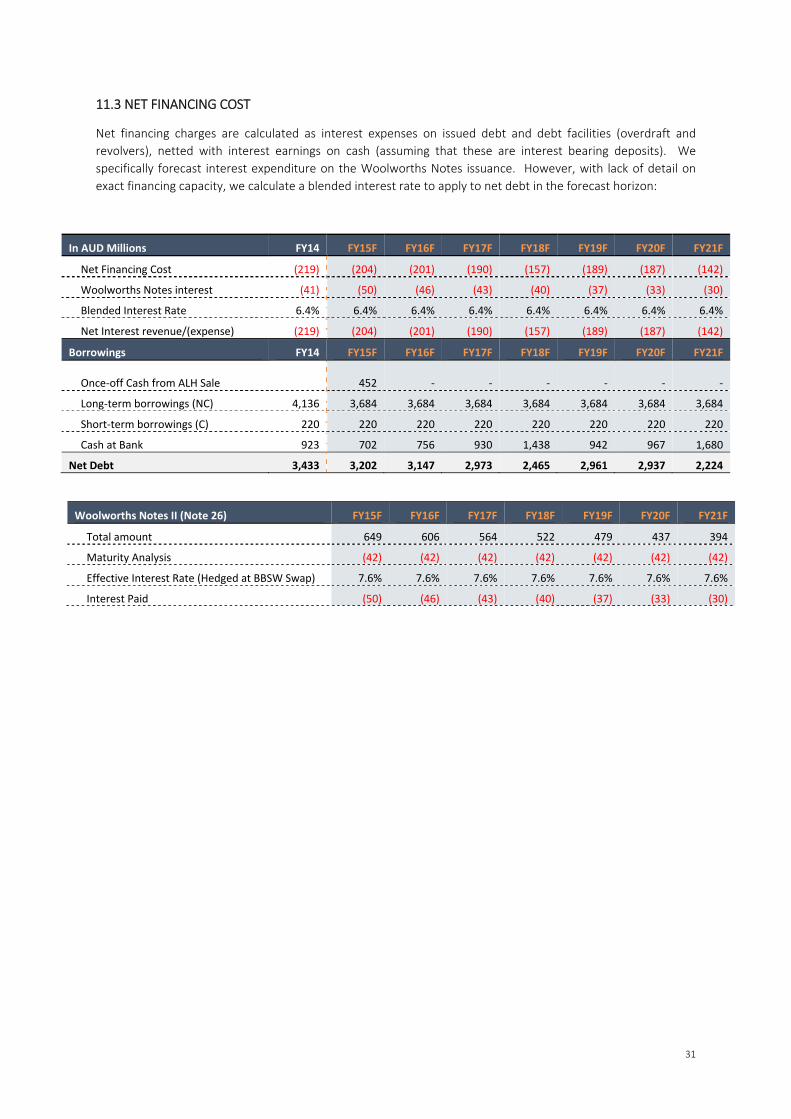

FINANCING Increasing Effective Gearing Woolworths’ interest expenses declined 12% in FY14, as proceeds from property sales were directed towards US bond redemptions in FY13. FY14 EBIT interest coverage is a strong 10.7x, however this metric is deceiving as effective gearing rises once Woolworths’ property policy is taken into account. By selling off property, and re‐deploying the capital into the firm, the firm is geared with long term rental liabilities. EBITDAR coverage of interest in FY14 was 25.6x, however only 3.1x accounting for all interest charges and rent.

In FY14, minimum rental payments were $1.9bn, 28.5% of EBITDAR. During FY14, Woolworths’ rental burden substantially increased with the sale of the ALH Hotels property portfolio, contributing a further forecasted $30.8m in rent in FY15. We forecast rental expense to increase with store roll outs, and growth in rental yields, up to 38.6% of EBITDAR in FY21. This results in EBITDAR Margins declining from 11% in FY15 to 10.4% in FY21. On a coverage basis, we forecast EBITDAR coverage of rent and interest charges to fall to 2.5x in F21, from 3.1x in FY14.

15.0

15.5

16.0

16.5

17.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY12

FY13

FY14

FY15E

FY16E

FY17E

FY19E

FY21E

Thousands

Millions

Total Area (sqm) (LHS)

Sales per sqm (RHS)

0%

3%

5%

8%

10%

‐

15

30

45

60

75

FY12

FY13

FY14

FY15E

FY16E

FY17E

FY19E

FY21E

Millions

Sales (LHS)

COGS, SG&A, Rent (LHS)

EBITDA MARGIN (RHS)

Cost Composition

Total Area & Sales per square metre

*Source: Bloomberg, SURG Estimates

*Source: Bloomberg, SURG Estimates

*Source: Bloomberg, SURG Estimates

EBITDA Margin

0.0

0.2

0.4

0.6

0.8

1.0

0

5

10

15

20

25

30

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Historic Multiples

EV/EBITDA (LHS) EV/EPS (LHS)

EV/Sales (RHS)

9

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Inventories A/C Payable

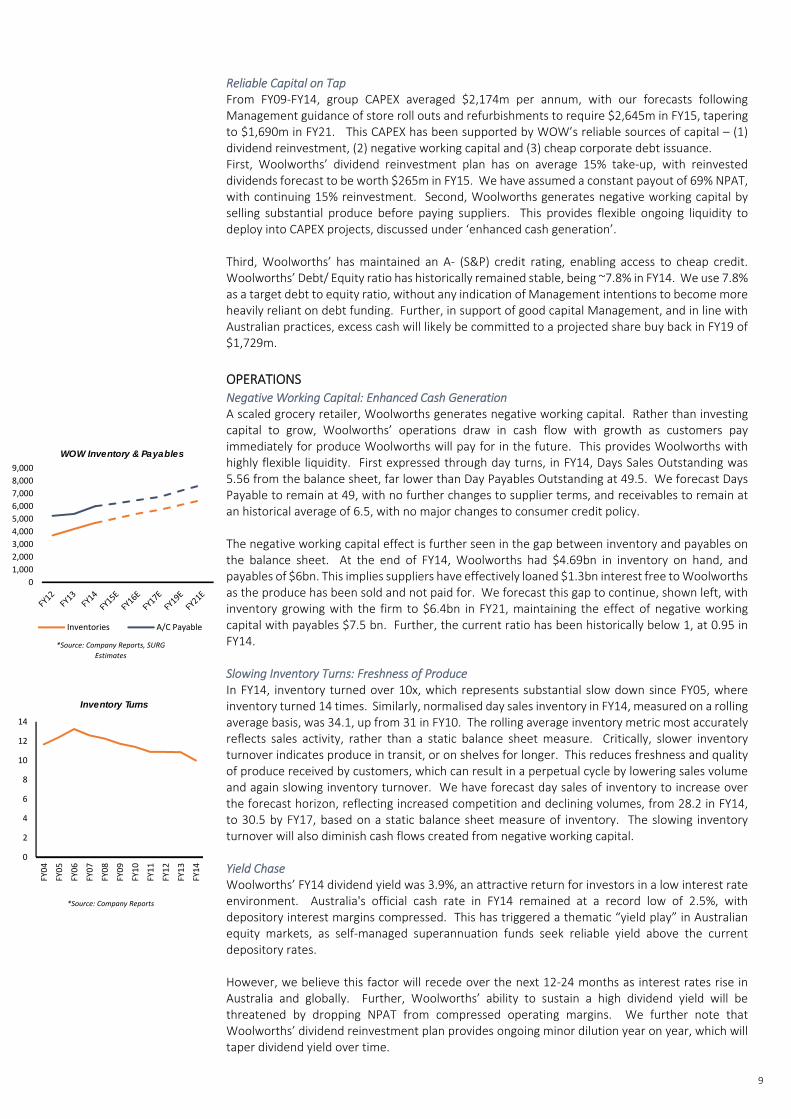

Reliable Capital on Tap From FY09‐FY14, group CAPEX averaged $2,174m per annum, with our forecasts following Management guidance of store roll outs and refurbishments to require $2,645m in FY15, tapering to $1,690m in FY21. This CAPEX has been supported by WOW’s reliable sources of capital – (1) dividend reinvestment, (2) negative working capital and (3) cheap corporate debt issuance. First, Woolworths’ dividend reinvestment plan has on average 15% take‐up, with reinvested dividends forecast to be worth $265m in FY15. We have assumed a constant payout of 69% NPAT, with continuing 15% reinvestment. Second, Woolworths generates negative working capital by selling substantial produce before paying suppliers. This provides flexible ongoing liquidity to deploy into CAPEX projects, discussed under ‘enhanced cash generation’. Third, Woolworths’ has maintained an A‐ (S&P) credit rating, enabling access to cheap credit. Woolworths’ Debt/ Equity ratio has historically remained stable, being ~7.8% in FY14. We use 7.8% as a target debt to equity ratio, without any indication of Management intentions to become more heavily reliant on debt funding. Further, in support of good capital Management, and in line with Australian practices, excess cash will likely be committed to a projected share buy back in FY19 of $1,729m.

OPERATIONS Negative Working Capital: Enhanced Cash Generation A scaled grocery retailer, Woolworths generates negative working capital. Rather than investing capital to grow, Woolworths’ operations draw in cash flow with growth as customers pay immediately for produce Woolworths will pay for in the future. This provides Woolworths with highly flexible liquidity. First expressed through day turns, in FY14, Days Sales Outstanding was 5.56 from the balance sheet, far lower than Day Payables Outstanding at 49.5. We forecast Days Payable to remain at 49, with no further changes to supplier terms, and receivables to remain at an historical average of 6.5, with no major changes to consumer credit policy.

The negative working capital effect is further seen in the gap between inventory and payables on the balance sheet. At the end of FY14, Woolworths had $4.69bn in inventory on hand, and payables of $6bn. This implies suppliers have effectively loaned $1.3bn interest free to Woolworths as the produce has been sold and not paid for. We forecast this gap to continue, shown left, with inventory growing with the firm to $6.4bn in FY21, maintaining the effect of negative working capital with payables $7.5 bn. Further, the current ratio has been historically below 1, at 0.95 in FY14. Slowing Inventory Turns: Freshness of Produce In FY14, inventory turned over 10x, which represents substantial slow down since FY05, where inventory turned 14 times. Similarly, normalised day sales inventory in FY14, measured on a rolling average basis, was 34.1, up from 31 in FY10. The rolling average inventory metric most accurately reflects sales activity, rather than a static balance sheet measure. Critically, slower inventory turnover indicates produce in transit, or on shelves for longer. This reduces freshness and quality of produce received by customers, which can result in a perpetual cycle by lowering sales volume and again slowing inventory turnover. We have forecast day sales of inventory to increase over the forecast horizon, reflecting increased competition and declining volumes, from 28.2 in FY14, to 30.5 by FY17, based on a static balance sheet measure of inventory. The slowing inventory turnover will also diminish cash flows created from negative working capital. Yield Chase Woolworths’ FY14 dividend yield was 3.9%, an attractive return for investors in a low interest rate environment. Australia's official cash rate in FY14 remained at a record low of 2.5%, with depository interest margins compressed. This has triggered a thematic “yield play” in Australian equity markets, as self‐managed superannuation funds seek reliable yield above the current depository rates. However, we believe this factor will recede over the next 12‐24 months as interest rates rise in Australia and globally. Further, Woolworths’ ability to sustain a high dividend yield will be threatened by dropping NPAT from compressed operating margins. We further note that Woolworths’ dividend reinvestment plan provides ongoing minor dilution year on year, which will taper dividend yield over time.

*Source: Company Reports, SURG

Estimates

WOW Inventory & Payables

0

2

4

6

8

10

12

14

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

Inventory Turns

*Source: Company Reports

10

INVESTMENT RISKS

DOWNSIDE RISKS

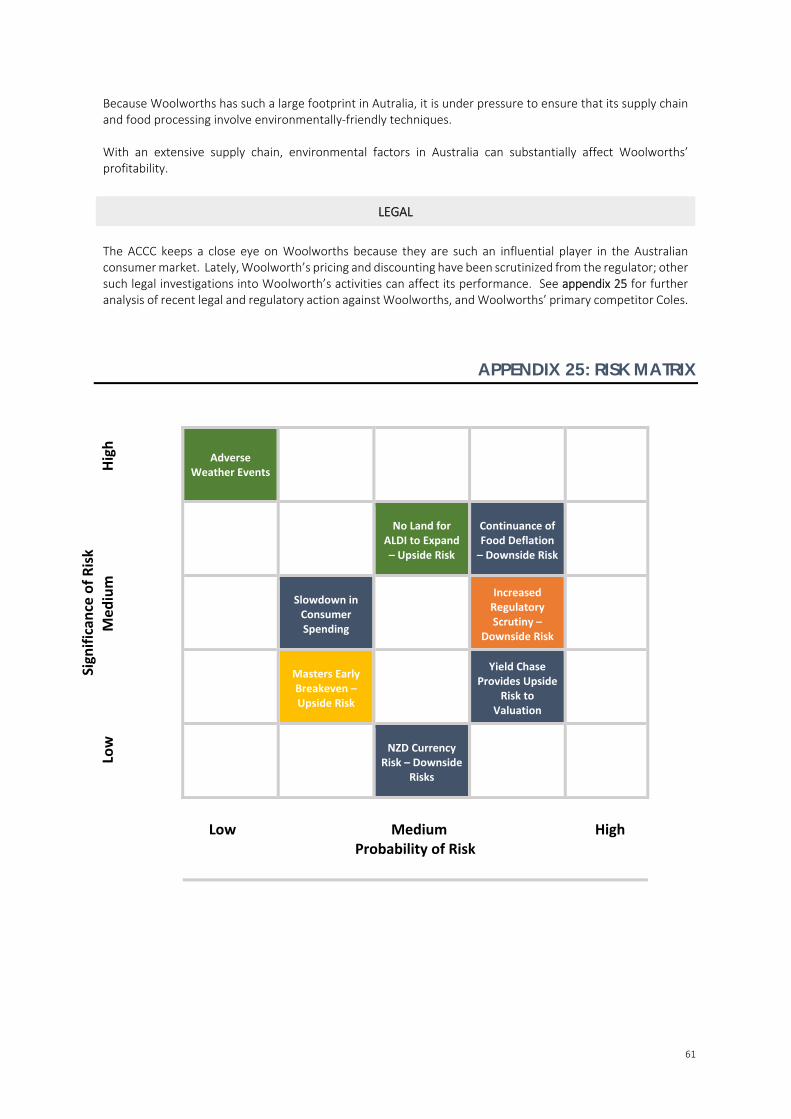

Economic | Further slowdown in the rate of consumer spending and consumption (E1)

Australian real wages fell 0.3% in FY14 and unemployment is at a 12 year high (6.1%). Australian

retailers are therefore competing for shrinking disposable incomes. Any economic slowdown or

decline in house prices will affect fragile consumer confidence, driving demand for discount and

private label products. Moreover, with car ownership in Australia at nearly 88%, consumers are

willing to travel to discount retailers. As Costco and ALDI both have lower cost bases, and superior

value perception, an economic slowdown will disproportionately favour these staple providers.

Economic | Food Deflation Continues (E2)

Real price deflation may accelerate in the event that ALDI adopts an aggressive store roll‐out strategy or if Coles implements further price reductions. Importantly, broad price reductions will disproportionately affect WOW’s high‐margin products. As WOW exhibits market leading gross profit margins, this poses a significant risk to both its profitability and valuation.

Economic Risk | NZD Currency Risk (E3) Strong movements in the AUD/NZD rate will affect the profitability of WOW’s New Zealand

operations. While WOW hedges NZD sourced revenue to reduce currency risk, an unforseen

appreciation of the AUD relative to NZD will decrease revenue attributable to equity holders.

However, the AUD/NZD rate is traditionally stable, trading within a range of $1.08‐$1.37 from

2010‐2013 with a standard deviation of 6 cents. We therefore do not believe this represents a

material risk.

Regulatory | Increased Regulatory Scrutiny (R1)

The Australian Supermarket and Grocery industry has been subject to increasing political and

regulatory scrutiny. In February 2014, the ACCC instituted Federal Court proceedings against WOW

for allegedly breaching fuel shopper docket undertakings. Additionally, in FY13‐14 the ACCC

continued investigation into misuse of market power by Coles and Woolworths. These

investigations provide a distraction for management, and can force changes to operations. In

contrast, the ACCC has welcomed ALDI’s competitive tension. Any adverse ACCC action will detract

from public perception of Woolworths. Similarly, changes to gaming machine legislation, such as

pre‐commitment, and taxation will materially impact ALH division profitability.

Industry | Adverse Weather Events (I1) Australia is the world’s 51st largest country by population and 6th largest by area. As WOW sources

90% of produce domestically, the business’ supply chain is exposed to adverse weather events.

Although the probability of events such as droughts and floods are low, these can significantly

impact WOW’s operations and inventory management as well as lead to product write downs.

UPSIDE RISKS

Industry | No Land to Grab (I2)

The lack of available space for store openings is a key restraint to the expansion of alternative low‐cost retailers. We view this factor as the single most significant constraint on ALDI’s ability to adopt its ‘small‐format store’ strategy. Similarly, Costco’s expansion is restricted by a lack of suitable sites for its warehouse store format. As such, if these issues persist, our forecasted decline in WOW’s market share may be significantly smaller than expected. Operational Risk | Masters Breakeven Before Expectation (O1) Masters achieving break‐even prior to market expectation can provide upside potential for Woolworths. A successful execution of Masters will restore market confidence in management’s ability to generate new growth for the firm. Further, capital will be freed for alternative growth ventures. Economic Risk | Chasing Yield (E4)

Lastly, investors have historically been attracted to WOW’s consistent dividend yield. As such we recognise that defensive investors may ignore WOW’s underlying risks in favour of a stable income stream. This may provide material support to the current share price.

Downside Risks

Significance of Risk

Low M

edium High

I(1) I)

R) I(2) E(2)

E1) E(1) R(1) (4)

O(1)

O(1) E(4)

I1) E(3)

Low Medium High Probability of Risk

11

APPENDIX 1: STATEMENT OF FINANCIAL POSITION

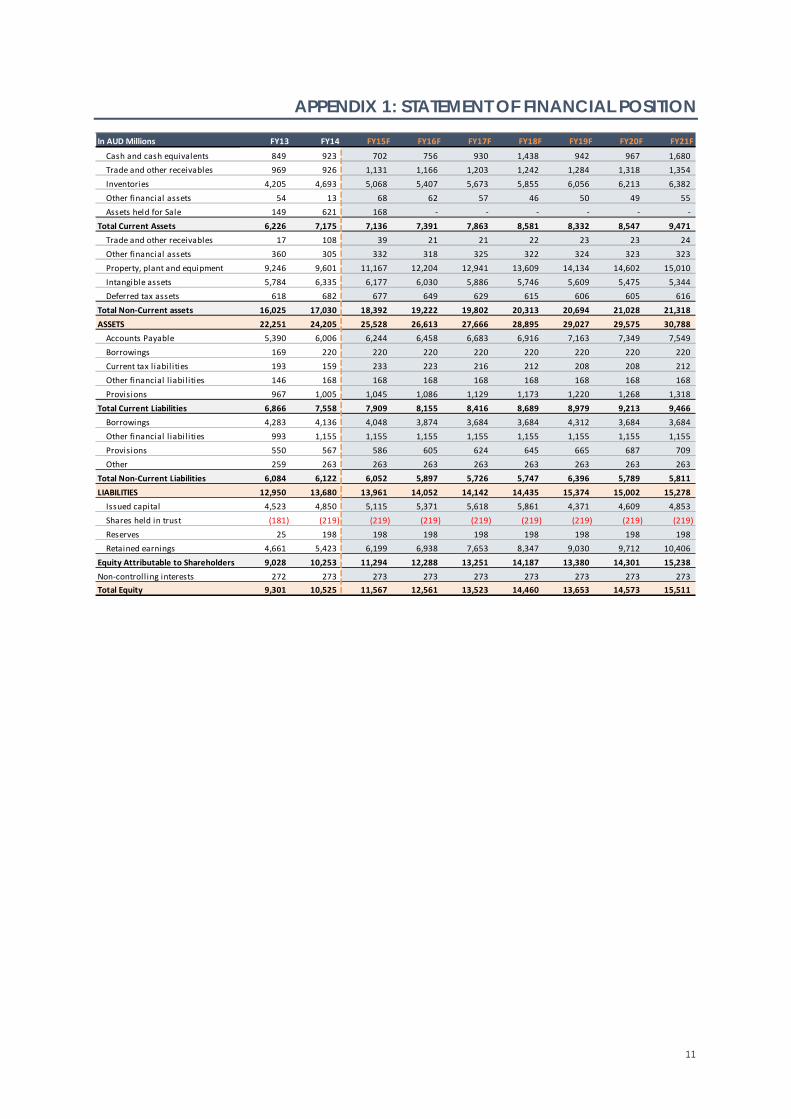

In AUD Millions FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Cash and cash equivalents 849 923 702 756 930 1,438 942 967 1,680

Trade and other receivables 969 926 1,131 1,166 1,203 1,242 1,284 1,318 1,354

Inventories 4,205 4,693 5,068 5,407 5,673 5,855 6,056 6,213 6,382

Other financial assets 54 13 68 62 57 46 50 49 55

Assets held for Sale 149 621 168 ‐ ‐ ‐ ‐ ‐ ‐

Total Current Assets 6,226 7,175 7,136 7,391 7,863 8,581 8,332 8,547 9,471

Trade and other receivables 17 108 39 21 21 22 23 23 24

Other financial assets 360 305 332 318 325 322 324 323 323

Property, plant and equipment 9,246 9,601 11,167 12,204 12,941 13,609 14,134 14,602 15,010

Intangible assets 5,784 6,335 6,177 6,030 5,886 5,746 5,609 5,475 5,344

Deferred tax assets 618 682 677 649 629 615 606 605 616

Total Non‐Current assets 16,025 17,030 18,392 19,222 19,802 20,313 20,694 21,028 21,318

ASSETS 22,251 24,205 25,528 26,613 27,666 28,895 29,027 29,575 30,788

Accounts Payable 5,390 6,006 6,244 6,458 6,683 6,916 7,163 7,349 7,549

Borrowings 169 220 220 220 220 220 220 220 220

Current tax l iabil ities 193 159 233 223 216 212 208 208 212

Other financial l iabil ities 146 168 168 168 168 168 168 168 168

Provisions 967 1,005 1,045 1,086 1,129 1,173 1,220 1,268 1,318

Total Current Liabilities 6,866 7,558 7,909 8,155 8,416 8,689 8,979 9,213 9,466

Borrowings 4,283 4,136 4,048 3,874 3,684 3,684 4,312 3,684 3,684

Other financial l iabil ities 993 1,155 1,155 1,155 1,155 1,155 1,155 1,155 1,155

Provisions 550 567 586 605 624 645 665 687 709

Other 259 263 263 263 263 263 263 263 263

Total Non‐Current Liabilities 6,084 6,122 6,052 5,897 5,726 5,747 6,396 5,789 5,811

LIABILITIES 12,950 13,680 13,961 14,052 14,142 14,435 15,374 15,002 15,278

Issued capital 4,523 4,850 5,115 5,371 5,618 5,861 4,371 4,609 4,853

Shares held in trust (181) (219) (219) (219) (219) (219) (219) (219) (219)

Reserves 25 198 198 198 198 198 198 198 198

Retained earnings 4,661 5,423 6,199 6,938 7,653 8,347 9,030 9,712 10,406

Equity Attributable to Shareholders 9,028 10,253 11,294 12,288 13,251 14,187 13,380 14,301 15,238

Non‐controlling interests 272 273 273 273 273 273 273 273 273

Total Equity 9,301 10,525 11,567 12,561 13,523 14,460 13,653 14,573 15,511

12

APPENDIX 2: STATEMENT OF COMPREHENSIVE INCOME

APPENDIX 3: STATEMENT OF CASH FLOWS

In AUD Millions FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Food and Liquor (Australia) 40,031 41,171 43,889 45,485 47,032 48,510 50,211 51,401 52,722

Food and Liquor (New Zealand) 4,600 5,186 4,711 4,892 5,059 5,244 5,407 5,544 5,685

Fuel 6,794 7,065 7,467 7,430 7,483 7,649 7,846 8,084 8,341

General Merchandise (Big W) 4,383 4,352 4,392 4,350 4,395 4,454 4,523 4,596 4,680

Hotels (ALH) 1,469 1,472 1,517 1,573 1,639 1,710 1,792 1,850 1,891

Home Improvement (Danks) 710 775 813 853 894 936 978 1,022 1,067

Home Improvement (Masters) 529 752 997 1,197 1,388 1,564 1,716 1,859 1,991

Sales 58,516 60,773 63,786 65,780 67,891 70,067 72,472 74,356 76,378

COGS (42,755) (44,295) (46,493) (48,085) (49,764) (51,499) (53,339) (54,726) (56,214)

Gross Profit 15,762 16,478 17,292 17,695 18,127 18,568 19,133 19,630 20,164

SG&A (9,379) (9,807) (10,269) (10,571) (10,897) (11,225) (11,596) (11,890) (12,198)

EBITDAR 6,383 6,670 7,023 7,124 7,230 7,343 7,537 7,740 7,966

Rent (1,764) (1,899) (2,076) (2,231) (2,389) (2,554) (2,722) (2,894) (3,074)

EBITDA 4,619 4,772 4,946 4,893 4,841 4,790 4,815 4,847 4,893

Depreciation (810) (816) (899) (1,012) (1,089) (1,150) (1,201) (1,244) (1,282)

Amortisation (155) (180) (158) (147) (144) (140) (137) (134) (131)

EBIT 3,653 3,776 3,889 3,734 3,609 3,500 3,477 3,469 3,480

Net Financing Cost (251) (219) (204) (201) (190) (157) (189) (187) (142)

Woolworths Notes interest (46) (41) (50) (46) (43) (40) (37) (33) (30)

Profit Before tax & significant items 3,356 3,515 3,636 3,487 3,376 3,303 3,252 3,248 3,308

Tax (997) (1,057) (1,091) (1,046) (1,013) (991) (975) (974) (992)

NPAT 2,359 2,459 2,545 2,441 2,363 2,312 2,276 2,274 2,316

Shares Outstanding at Period End (m) 1,237.4 1,248 1,256 1,263 1,270 1,277 1,234 1,241 1,248

Total Dividend/Share (Cents) 133.0 137 141 135 130 127 129 128 130

Total Dividend Paid (m) 1,645.7 1,710 1,769 1,702 1,648 1,618 1,593 1,592 1,621

Retained Earnings 713.4 749 776 739 715 694 683 682 695

Imputation credits (Fully Franked) 695.2 735 606 584 565 555 546 546 556

In AUD Millions FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

EBITDA 4,619 4,772 4,946 4,893 4,841 4,790 4,815 4,847 4,893

Financing Expense (298) (260) (254) (247) (233) (197) (225) (221) (172)

Tax Paid (997) (1,057) (1,091) (1,046) (1,013) (991) (975) (974) (992)

Change in Working Capital (601) 176 (355) (123) (81) 26 (3) (4) (12)

Net Cash Flows from Operating Activities 2,724 3,631 3,247 3,478 3,515 3,628 3,612 3,648 3,716

Total Capex (1,955) (1,899) (2,465) (2,049) (1,826) (1,818) (1,726) (1,712) (1,690)

Proceeds from Asset Sale ‐ ‐ 452 ‐ ‐ ‐ ‐ ‐ ‐

Net Cash Flows From Investing Activities (1,955) (1,899) (2,013) (2,049) (1,826) (1,818) (1,726) (1,712) (1,690)

Change in Existing Debt (295) (96) (495) (42) (42) (42) (42) (42) (42)

Financing Repayment/Addition 1,002 (180) 544 115 (72) 116 744 (516) 107

Distributions Paid (1,646) (1,710) (1,769) (1,702) (1,648) (1,618) (1,593) (1,592) (1,621)

Change in Equity 186 327 265 255 247 243 (1,490) 239 243

Net Cash Flows from Financing Activities (752) (1,659) (1,455) (1,374) (1,515) (1,302) (2,381) (1,911) (1,313)

Net increase in cash 16 73 (221) 55 174 508 (496) 24 713

Opening Cash 833 849 923 702 756 930 1,438 942 967

Net Change in Cash 16 73 (221) 55 174 508 (496) 24 713

Closing Cash 849 923 702 756 930 1,438 942 967 1,680

13

APPENDIX 4: COMMON-SIZE STATEMENT OF FINANCIAL POSITION

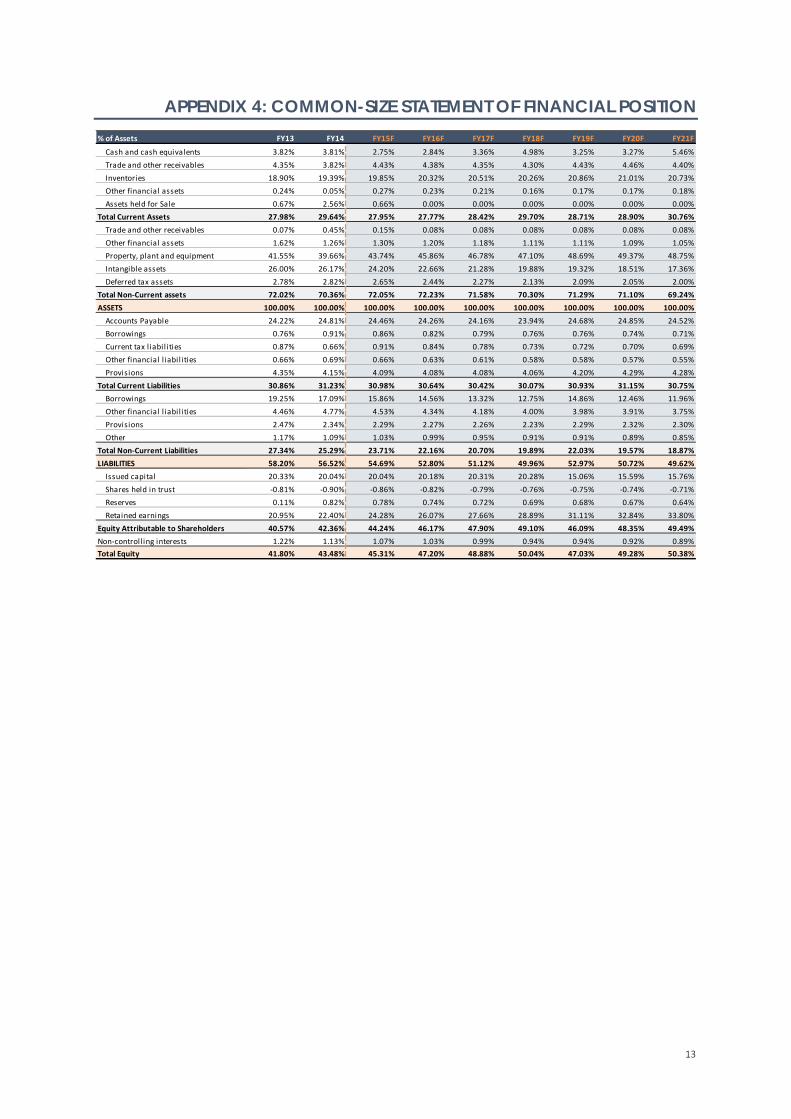

% of Assets FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Cash and cash equivalents 3.82% 3.81% 2.75% 2.84% 3.36% 4.98% 3.25% 3.27% 5.46%

Trade and other receivables 4.35% 3.82% 4.43% 4.38% 4.35% 4.30% 4.43% 4.46% 4.40%

Inventories 18.90% 19.39% 19.85% 20.32% 20.51% 20.26% 20.86% 21.01% 20.73%

Other financial assets 0.24% 0.05% 0.27% 0.23% 0.21% 0.16% 0.17% 0.17% 0.18%

Assets held for Sale 0.67% 2.56% 0.66% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Total Current Assets 27.98% 29.64% 27.95% 27.77% 28.42% 29.70% 28.71% 28.90% 30.76%

Trade and other receivables 0.07% 0.45% 0.15% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08%

Other financial assets 1.62% 1.26% 1.30% 1.20% 1.18% 1.11% 1.11% 1.09% 1.05%

Property, plant and equipment 41.55% 39.66% 43.74% 45.86% 46.78% 47.10% 48.69% 49.37% 48.75%

Intangible assets 26.00% 26.17% 24.20% 22.66% 21.28% 19.88% 19.32% 18.51% 17.36%

Deferred tax assets 2.78% 2.82% 2.65% 2.44% 2.27% 2.13% 2.09% 2.05% 2.00%

Total Non‐Current assets 72.02% 70.36% 72.05% 72.23% 71.58% 70.30% 71.29% 71.10% 69.24%

ASSETS 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Accounts Payable 24.22% 24.81% 24.46% 24.26% 24.16% 23.94% 24.68% 24.85% 24.52%

Borrowings 0.76% 0.91% 0.86% 0.82% 0.79% 0.76% 0.76% 0.74% 0.71%

Current tax l iabilities 0.87% 0.66% 0.91% 0.84% 0.78% 0.73% 0.72% 0.70% 0.69%

Other financial l iabilities 0.66% 0.69% 0.66% 0.63% 0.61% 0.58% 0.58% 0.57% 0.55%

Provisions 4.35% 4.15% 4.09% 4.08% 4.08% 4.06% 4.20% 4.29% 4.28%

Total Current Liabilities 30.86% 31.23% 30.98% 30.64% 30.42% 30.07% 30.93% 31.15% 30.75%

Borrowings 19.25% 17.09% 15.86% 14.56% 13.32% 12.75% 14.86% 12.46% 11.96%

Other financial l iabilities 4.46% 4.77% 4.53% 4.34% 4.18% 4.00% 3.98% 3.91% 3.75%

Provisions 2.47% 2.34% 2.29% 2.27% 2.26% 2.23% 2.29% 2.32% 2.30%

Other 1.17% 1.09% 1.03% 0.99% 0.95% 0.91% 0.91% 0.89% 0.85%

Total Non‐Current Liabilities 27.34% 25.29% 23.71% 22.16% 20.70% 19.89% 22.03% 19.57% 18.87%

LIABILITIES 58.20% 56.52% 54.69% 52.80% 51.12% 49.96% 52.97% 50.72% 49.62%

Issued capital 20.33% 20.04% 20.04% 20.18% 20.31% 20.28% 15.06% 15.59% 15.76%

Shares held in trust ‐0.81% ‐0.90% ‐0.86% ‐0.82% ‐0.79% ‐0.76% ‐0.75% ‐0.74% ‐0.71%

Reserves 0.11% 0.82% 0.78% 0.74% 0.72% 0.69% 0.68% 0.67% 0.64%

Retained earnings 20.95% 22.40% 24.28% 26.07% 27.66% 28.89% 31.11% 32.84% 33.80%

Equity Attributable to Shareholders 40.57% 42.36% 44.24% 46.17% 47.90% 49.10% 46.09% 48.35% 49.49%

Non‐controlling interests 1.22% 1.13% 1.07% 1.03% 0.99% 0.94% 0.94% 0.92% 0.89%

Total Equity 41.80% 43.48% 45.31% 47.20% 48.88% 50.04% 47.03% 49.28% 50.38%

14

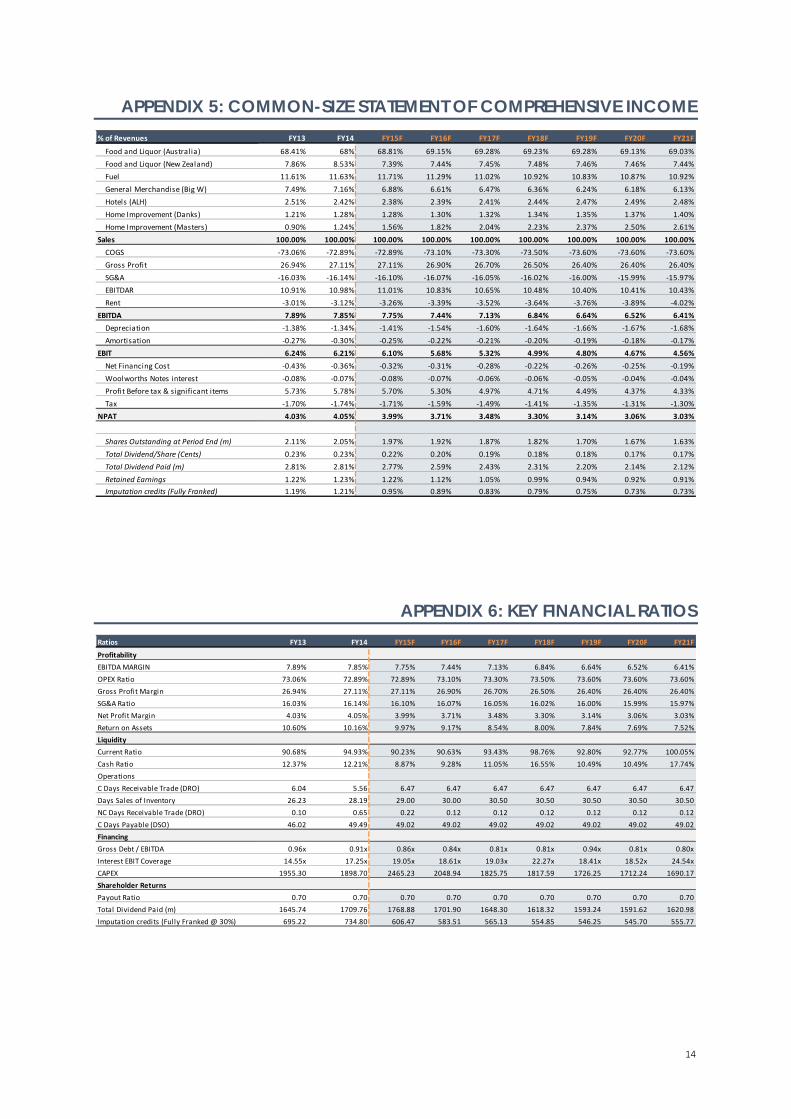

APPENDIX 5: COMMON-SIZE STATEMENT OF COMPREHENSIVE INCOME

APPENDIX 6: KEY FINANCIAL RATIOS

% of Revenues FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Food and Liquor (Australia) 68.41% 68% 68.81% 69.15% 69.28% 69.23% 69.28% 69.13% 69.03%

Food and Liquor (New Zealand) 7.86% 8.53% 7.39% 7.44% 7.45% 7.48% 7.46% 7.46% 7.44%

Fuel 11.61% 11.63% 11.71% 11.29% 11.02% 10.92% 10.83% 10.87% 10.92%

General Merchandise (Big W) 7.49% 7.16% 6.88% 6.61% 6.47% 6.36% 6.24% 6.18% 6.13%

Hotels (ALH) 2.51% 2.42% 2.38% 2.39% 2.41% 2.44% 2.47% 2.49% 2.48%

Home Improvement (Danks) 1.21% 1.28% 1.28% 1.30% 1.32% 1.34% 1.35% 1.37% 1.40%

Home Improvement (Masters) 0.90% 1.24% 1.56% 1.82% 2.04% 2.23% 2.37% 2.50% 2.61%

Sales 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

COGS ‐73.06% ‐72.89% ‐72.89% ‐73.10% ‐73.30% ‐73.50% ‐73.60% ‐73.60% ‐73.60%

Gross Profit 26.94% 27.11% 27.11% 26.90% 26.70% 26.50% 26.40% 26.40% 26.40%

SG&A ‐16.03% ‐16.14% ‐16.10% ‐16.07% ‐16.05% ‐16.02% ‐16.00% ‐15.99% ‐15.97%

EBITDAR 10.91% 10.98% 11.01% 10.83% 10.65% 10.48% 10.40% 10.41% 10.43%

Rent ‐3.01% ‐3.12% ‐3.26% ‐3.39% ‐3.52% ‐3.64% ‐3.76% ‐3.89% ‐4.02%

EBITDA 7.89% 7.85% 7.75% 7.44% 7.13% 6.84% 6.64% 6.52% 6.41%

Depreciation ‐1.38% ‐1.34% ‐1.41% ‐1.54% ‐1.60% ‐1.64% ‐1.66% ‐1.67% ‐1.68%

Amortisation ‐0.27% ‐0.30% ‐0.25% ‐0.22% ‐0.21% ‐0.20% ‐0.19% ‐0.18% ‐0.17%

EBIT 6.24% 6.21% 6.10% 5.68% 5.32% 4.99% 4.80% 4.67% 4.56%

Net Financing Cost ‐0.43% ‐0.36% ‐0.32% ‐0.31% ‐0.28% ‐0.22% ‐0.26% ‐0.25% ‐0.19%

Woolworths Notes interest ‐0.08% ‐0.07% ‐0.08% ‐0.07% ‐0.06% ‐0.06% ‐0.05% ‐0.04% ‐0.04%

Profit Before tax & significant items 5.73% 5.78% 5.70% 5.30% 4.97% 4.71% 4.49% 4.37% 4.33%

Tax ‐1.70% ‐1.74% ‐1.71% ‐1.59% ‐1.49% ‐1.41% ‐1.35% ‐1.31% ‐1.30%

NPAT 4.03% 4.05% 3.99% 3.71% 3.48% 3.30% 3.14% 3.06% 3.03%

Shares Outstanding at Period End (m) 2.11% 2.05% 1.97% 1.92% 1.87% 1.82% 1.70% 1.67% 1.63%

Total Dividend/Share (Cents) 0.23% 0.23% 0.22% 0.20% 0.19% 0.18% 0.18% 0.17% 0.17%

Total Dividend Paid (m) 2.81% 2.81% 2.77% 2.59% 2.43% 2.31% 2.20% 2.14% 2.12%

Retained Earnings 1.22% 1.23% 1.22% 1.12% 1.05% 0.99% 0.94% 0.92% 0.91%

Imputation credits (Fully Franked) 1.19% 1.21% 0.95% 0.89% 0.83% 0.79% 0.75% 0.73% 0.73%

Ratios FY13 FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Profitability

EBITDA MARGIN 7.89% 7.85% 7.75% 7.44% 7.13% 6.84% 6.64% 6.52% 6.41%

OPEX Ratio 73.06% 72.89% 72.89% 73.10% 73.30% 73.50% 73.60% 73.60% 73.60%

Gross Profit Margin 26.94% 27.11% 27.11% 26.90% 26.70% 26.50% 26.40% 26.40% 26.40%

SG&A Ratio 16.03% 16.14% 16.10% 16.07% 16.05% 16.02% 16.00% 15.99% 15.97%

Net Profit Margin 4.03% 4.05% 3.99% 3.71% 3.48% 3.30% 3.14% 3.06% 3.03%

Return on Assets 10.60% 10.16% 9.97% 9.17% 8.54% 8.00% 7.84% 7.69% 7.52%

Liquidity

Current Ratio 90.68% 94.93% 90.23% 90.63% 93.43% 98.76% 92.80% 92.77% 100.05%

Cash Ratio 12.37% 12.21% 8.87% 9.28% 11.05% 16.55% 10.49% 10.49% 17.74%

Operations

C Days Receivable Trade (DRO) 6.04 5.56 6.47 6.47 6.47 6.47 6.47 6.47 6.47

Days Sales of Inventory 26.23 28.19 29.00 30.00 30.50 30.50 30.50 30.50 30.50

NC Days Receivable Trade (DRO) 0.10 0.65 0.22 0.12 0.12 0.12 0.12 0.12 0.12

C Days Payable (DSO) 46.02 49.49 49.02 49.02 49.02 49.02 49.02 49.02 49.02

Financing

Gross Debt / EBITDA 0.96x 0.91x 0.86x 0.84x 0.81x 0.81x 0.94x 0.81x 0.80x

Interest EBIT Coverage 14.55x 17.25x 19.05x 18.61x 19.03x 22.27x 18.41x 18.52x 24.54x

CAPEX 1955.30 1898.70 2465.23 2048.94 1825.75 1817.59 1726.25 1712.24 1690.17

Shareholder Returns

Payout Ratio 0.70 0.70 0.70 0.70 0.70 0.70 0.70 0.70 0.70

Total Dividend Paid (m) 1645.74 1709.76 1768.88 1701.90 1648.30 1618.32 1593.24 1591.62 1620.98

Imputation credits (Fully Franked @ 30%) 695.22 734.80 606.47 583.51 565.13 554.85 546.25 545.70 555.77

15

APPENDIX 7: DISCOUNTED CASH FLOWS

Net Working Capital FY14 FY15F FY16F FY17F FY18F FY19F FY20F FY21F

Current Assets 7,175 7,136 7,391 7,863 8,581 8,332 8,547 9,471

Cash and Cash Equivalents 923 702 756 930 1,438 942 967 1,680

Current Liabilities 7,558 7,909 8,155 8,416 8,689 8,979 9,213 9,466

Current Interest Bearing Liabilities 220 220 220 220 220 220 220 220

Net Working Capital (1,087) (1,255) (1,301) (1,263) (1,326) (1,369) (1,413) (1,455)

ΔNWC 233 (169) (46) 38 (63) (43) (44) (43)

FCFF Calculation FY15F FY16F FY17F FY18F FY19F FY20F FY21F

EBIT(1‐T) 2,722 2,614 2,526 2,450 2,434 2,428 2,436

add Depreciation and Amortisation 1,057 1,159 1,233 1,290 1,338 1,378 1,413

Less CAPEX 2,465 2,049 1,826 1,818 1,726 1,712 1,690

Less ΔNWC (169) (46) 38 (63) (43) (44) (43)

FCFF 1,483 1,770 1,895 1,985 2,089 2,138 2,201

FCFF Growth (%) ‐1.4% 19.3% 7.1% 4.8% 5.2% 2.4% 3.0%

FCFF + Imputation Credits 2,090 2,353 2,460 2,540 2,635 2,683 2,757

Discounted Free Cash Flows 1,924 1,994 1,919 1,824 1,742 1,633 1,545

Terminal Value ‐ ‐ ‐ ‐ ‐ ‐ 48,781

Discounted Terminal Value ‐ ‐ ‐ ‐ ‐ ‐ 27,333

WACC (Forecast Horizon) 8.6%

WACC (Terminal) 8.6%

Terminal Growth 2.8%

PV of Forecast FCFFs 12,582

PV of Terminal Value 27,333

Enterprise Value 39,915

Add: Cash 923

Less: Debt (4,356)

Equity Value 36,482

Current Shares Outstanding (m) 1,248

Value per Share 29.23

16

$25.02

$25.57

$25.46

$33.88

$34.70

$34.54

22.5 27.5 32.5

Relative Valuation

DCF Triangulation

Final Valuation

WOW Share Price ($A)

Valuation Triangulation

$29.27

APPENDIX 8: VALUATION SUMMARY

Triangulated Share Price Estimate Weight

Fundamental Valuation $29.23 80%

Relative Valuation $29.45 20%

Triangulated Share Price $29.27

Our final share price of $29.27 is triangulated between a discounted cash flow valuation (weighted 80%) and

multiples valuation (weighted 20%). The DCF valuation received a higher weight as it allows for explicit modelling

of key variables that affect the revenue growth of each segment, as well as CAPEX and working capital.

Conversely, relative valuation implicitly models growth and risk, which are factors that cannot be controlled.

However, we still weight relative valuation at 20% as it provides an indication of market consensus and how the

stock is trades relative to peers.

The graph below reflects the valuation ranges of Woolworths derived from DCF, multiples and a weighted

average. Upper and lower ranges for relative valuation reflect one standard deviation from the weighted average

peer index. The ranges for the DCF valuation reflect sensitivity analysis to WACC and TGR (see appendix 15).

The final valuation range is obtained with the 80:20 weights applied to the lower, base case, and upper estimates

of each valuation method. This provides a final valuation range of $25.46 to $34.54, with a base vase valuation

of $29.27 with 17% downside to closing price on 19/09/2014.

17

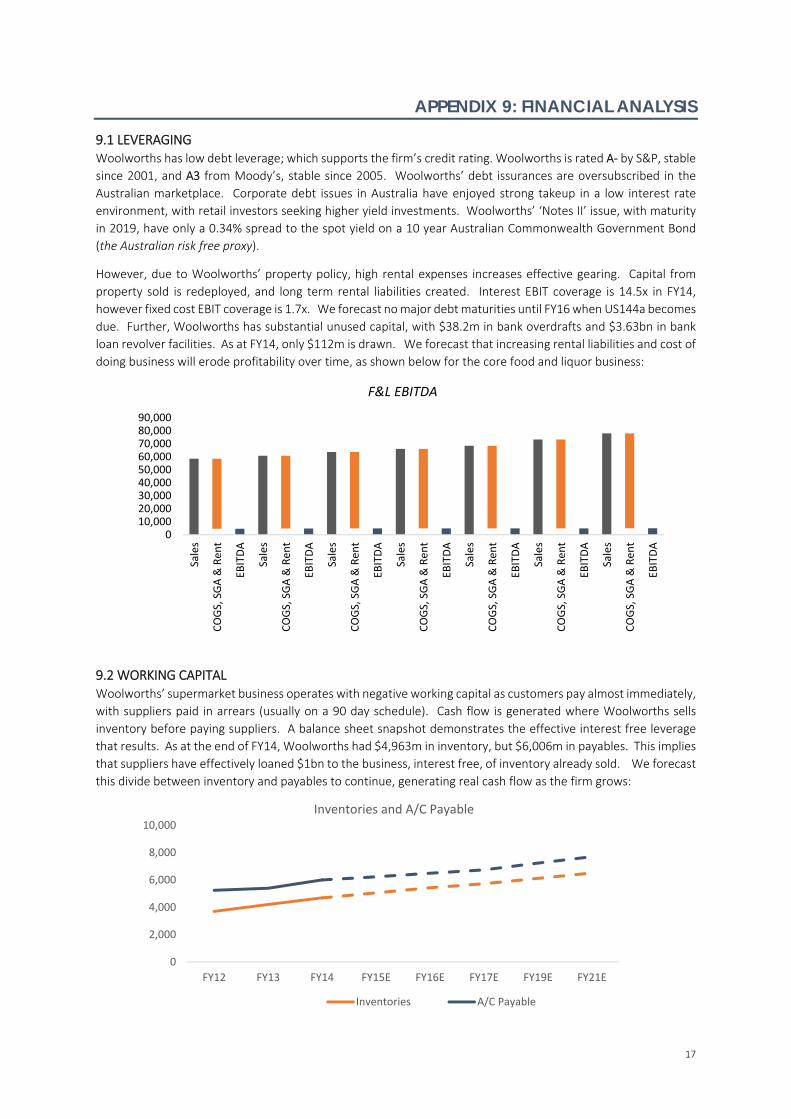

APPENDIX 9: FINANCIAL ANALYSIS

9.1 LEVERAGING Woolworths has low debt leverage; which supports the firm’s credit rating. Woolworths is rated A‐ by S&P, stable

since 2001, and A3 from Moody’s, stable since 2005. Woolworths’ debt issurances are oversubscribed in the

Australian marketplace. Corporate debt issues in Australia have enjoyed strong takeup in a low interest rate

environment, with retail investors seeking higher yield investments. Woolworths’ ‘Notes II’ issue, with maturity

in 2019, have only a 0.34% spread to the spot yield on a 10 year Australian Commonwealth Government Bond

(the Australian risk free proxy).

However, due to Woolworths’ property policy, high rental expenses increases effective gearing. Capital from

property sold is redeployed, and long term rental liabilities created. Interest EBIT coverage is 14.5x in FY14,

however fixed cost EBIT coverage is 1.7x. We forecast no major debt maturities until FY16 when US144a becomes

due. Further, Woolworths has substantial unused capital, with $38.2m in bank overdrafts and $3.63bn in bank

loan revolver facilities. As at FY14, only $112m is drawn. We forecast that increasing rental liabilities and cost of

doing business will erode profitability over time, as shown below for the core food and liquor business:

9.2 WORKING CAPITAL Woolworths’ supermarket business operates with negative working capital as customers pay almost immediately,

with suppliers paid in arrears (usually on a 90 day schedule). Cash flow is generated where Woolworths sells

inventory before paying suppliers. A balance sheet snapshot demonstrates the effective interest free leverage

that results. As at the end of FY14, Woolworths had $4,963m in inventory, but $6,006m in payables. This implies

that suppliers have effectively loaned $1bn to the business, interest free, of inventory already sold. We forecast

this divide between inventory and payables to continue, generating real cash flow as the firm grows:

0

2,000

4,000

6,000

8,000

10,000

FY12 FY13 FY14 FY15E FY16E FY17E FY19E FY21E

Inventories and A/C Payable

Inventories A/C Payable

010,00020,00030,00040,00050,00060,00070,00080,00090,000

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

Sales

COGS, SGA & Rent

EBITDA

F&L EBITDA

18

$10

$11

$12

$13

$14

$15

$16

$17

$18

10

510

1010

1510

2010

2510

3010

3510

07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

Sales p/sqm $000

Area sqm '000

Area & Sales p/sqm

Total Area Sales per SQM

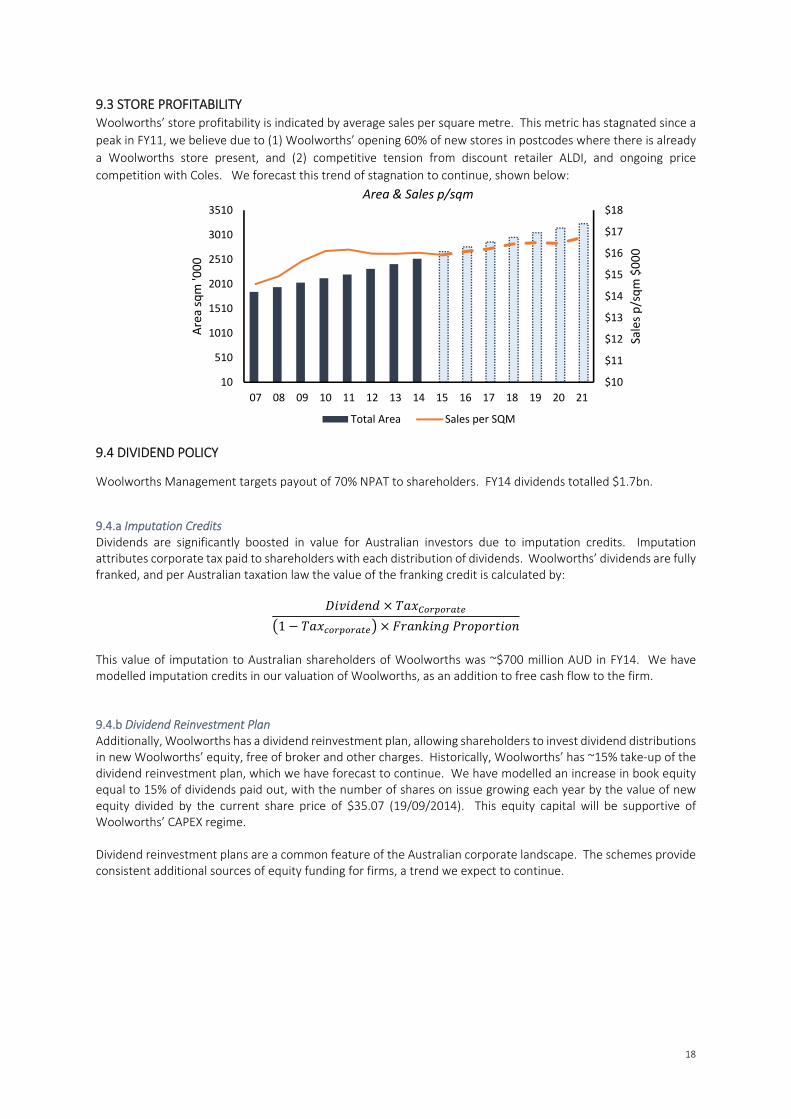

9.3 STORE PROFITABILITY Woolworths’ store profitability is indicated by average sales per square metre. This metric has stagnated since a

peak in FY11, we believe due to (1) Woolworths’ opening 60% of new stores in postcodes where there is already

a Woolworths store present, and (2) competitive tension from discount retailer ALDI, and ongoing price

competition with Coles. We forecast this trend of stagnation to continue, shown below:

9.4 DIVIDEND POLICY

Woolworths Management targets payout of 70% NPAT to shareholders. FY14 dividends totalled $1.7bn.

9.4.a Imputation Credits Dividends are significantly boosted in value for Australian investors due to imputation credits. Imputation attributes corporate tax paid to shareholders with each distribution of dividends. Woolworths’ dividends are fully franked, and per Australian taxation law the value of the franking credit is calculated by:

1

This value of imputation to Australian shareholders of Woolworths was ~$700 million AUD in FY14. We have modelled imputation credits in our valuation of Woolworths, as an addition to free cash flow to the firm. 9.4.b Dividend Reinvestment Plan Additionally, Woolworths has a dividend reinvestment plan, allowing shareholders to invest dividend distributions in new Woolworths’ equity, free of broker and other charges. Historically, Woolworths’ has ~15% take‐up of the dividend reinvestment plan, which we have forecast to continue. We have modelled an increase in book equity equal to 15% of dividends paid out, with the number of shares on issue growing each year by the value of new equity divided by the current share price of $35.07 (19/09/2014). This equity capital will be supportive of Woolworths’ CAPEX regime. Dividend reinvestment plans are a common feature of the Australian corporate landscape. The schemes provide consistent additional sources of equity funding for firms, a trend we expect to continue.

19

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

‐

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

12 13 14 15F 16F 17F 19F 21F

EBITDA Margin

Sales COGS, SGA & Rent EBITDA Margin

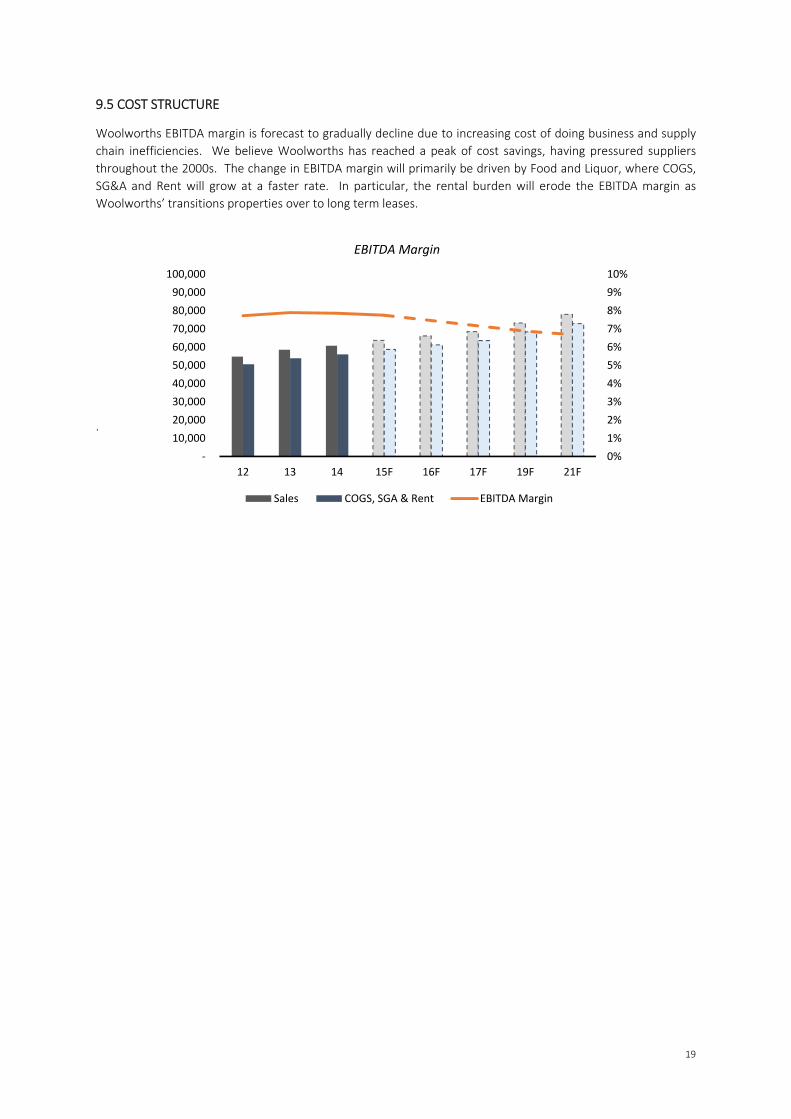

9.5 COST STRUCTURE

Woolworths EBITDA margin is forecast to gradually decline due to increasing cost of doing business and supply

chain inefficiencies. We believe Woolworths has reached a peak of cost savings, having pressured suppliers

throughout the 2000s. The change in EBITDA margin will primarily be driven by Food and Liquor, where COGS,

SG&A and Rent will grow at a faster rate. In particular, the rental burden will erode the EBITDA margin as

Woolworths’ transitions properties over to long term leases.

.

20

APPENDIX 10: DCF REVENUE ASSUMPTIONS

10.1 Food & Liquor

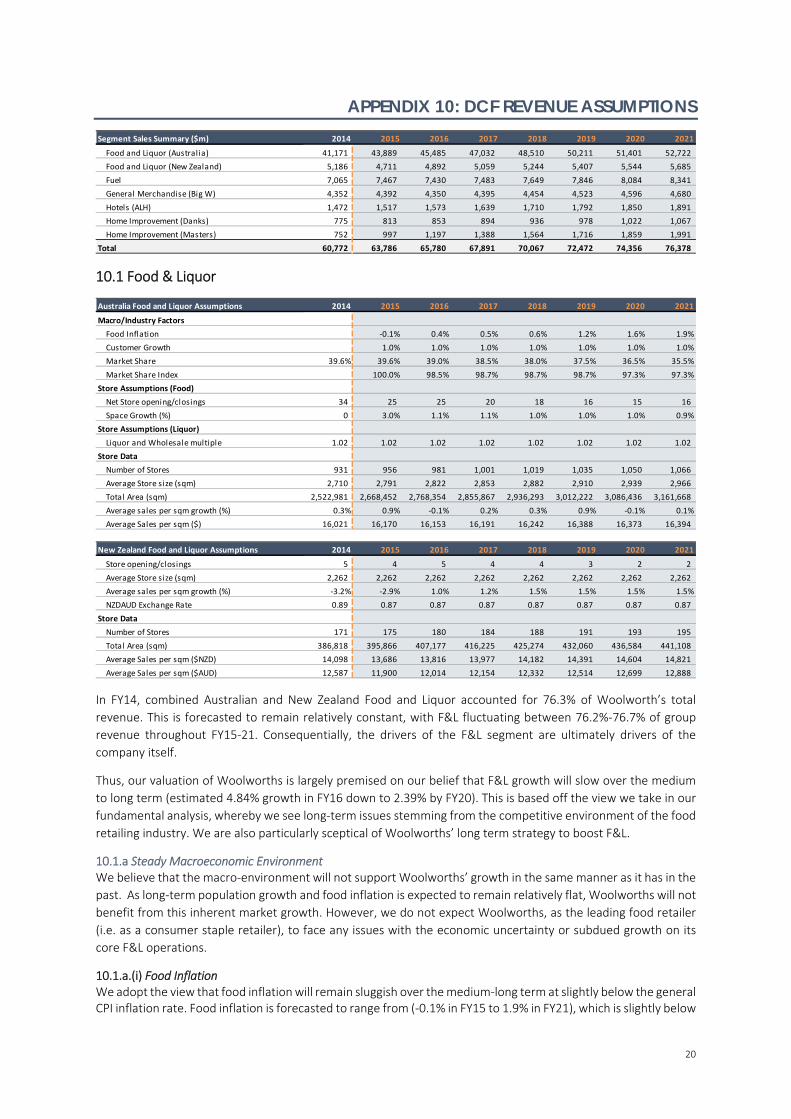

In FY14, combined Australian and New Zealand Food and Liquor accounted for 76.3% of Woolworth’s total

revenue. This is forecasted to remain relatively constant, with F&L fluctuating between 76.2%‐76.7% of group

revenue throughout FY15‐21. Consequentially, the drivers of the F&L segment are ultimately drivers of the

company itself.

Thus, our valuation of Woolworths is largely premised on our belief that F&L growth will slow over the medium

to long term (estimated 4.84% growth in FY16 down to 2.39% by FY20). This is based off the view we take in our

fundamental analysis, whereby we see long‐term issues stemming from the competitive environment of the food

retailing industry. We are also particularly sceptical of Woolworths’ long term strategy to boost F&L.

10.1.a Steady Macroeconomic Environment We believe that the macro‐environment will not support Woolworths’ growth in the same manner as it has in the

past. As long‐term population growth and food inflation is expected to remain relatively flat, Woolworths will not

benefit from this inherent market growth. However, we do not expect Woolworths, as the leading food retailer

(i.e. as a consumer staple retailer), to face any issues with the economic uncertainty or subdued growth on its

core F&L operations.

10.1.a.(i) Food Inflation We adopt the view that food inflation will remain sluggish over the medium‐long term at slightly below the general CPI inflation rate. Food inflation is forecasted to range from (‐0.1% in FY15 to 1.9% in FY21), which is slightly below

Segment Sales Summary ($m) 2014 2015 2016 2017 2018 2019 2020 2021

Food and Liquor (Australia) 41,171 43,889 45,485 47,032 48,510 50,211 51,401 52,722

Food and Liquor (New Zealand) 5,186 4,711 4,892 5,059 5,244 5,407 5,544 5,685

Fuel 7,065 7,467 7,430 7,483 7,649 7,846 8,084 8,341

General Merchandise (Big W) 4,352 4,392 4,350 4,395 4,454 4,523 4,596 4,680

Hotels (ALH) 1,472 1,517 1,573 1,639 1,710 1,792 1,850 1,891

Home Improvement (Danks) 775 813 853 894 936 978 1,022 1,067

Home Improvement (Masters) 752 997 1,197 1,388 1,564 1,716 1,859 1,991

Total 60,772 63,786 65,780 67,891 70,067 72,472 74,356 76,378

Australia Food and Liquor Assumptions 2014 2015 2016 2017 2018 2019 2020 2021

Macro/Industry Factors

Food Inflation ‐0.1% 0.4% 0.5% 0.6% 1.2% 1.6% 1.9%

Customer Growth 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Market Share 39.6% 39.6% 39.0% 38.5% 38.0% 37.5% 36.5% 35.5%

Market Share Index 100.0% 98.5% 98.7% 98.7% 98.7% 97.3% 97.3%

Store Assumptions (Food)

Net Store opening/closings 34 25 25 20 18 16 15 16

Space Growth (%) 0 3.0% 1.1% 1.1% 1.0% 1.0% 1.0% 0.9%

Store Assumptions (Liquor)

Liquor and Wholesale multiple 1.02 1.02 1.02 1.02 1.02 1.02 1.02 1.02

Store Data

Number of Stores 931 956 981 1,001 1,019 1,035 1,050 1,066

Average Store size (sqm) 2,710 2,791 2,822 2,853 2,882 2,910 2,939 2,966

Total Area (sqm) 2,522,981 2,668,452 2,768,354 2,855,867 2,936,293 3,012,222 3,086,436 3,161,668

Average sales per sqm growth (%) 0.3% 0.9% ‐0.1% 0.2% 0.3% 0.9% ‐0.1% 0.1%

Average Sales per sqm ($) 16,021 16,170 16,153 16,191 16,242 16,388 16,373 16,394

New Zealand Food and Liquor Assumptions 2014 2015 2016 2017 2018 2019 2020 2021

Store opening/closings 5 4 5 4 4 3 2 2

Average Store size (sqm) 2,262 2,262 2,262 2,262 2,262 2,262 2,262 2,262

Average sales per sqm growth (%) ‐3.2% ‐2.9% 1.0% 1.2% 1.5% 1.5% 1.5% 1.5%

NZDAUD Exchange Rate 0.89 0.87 0.87 0.87 0.87 0.87 0.87 0.87

Store Data

Number of Stores 171 175 180 184 188 191 193 195

Total Area (sqm) 386,818 395,866 407,177 416,225 425,274 432,060 436,584 441,108

Average Sales per sqm ($NZD) 14,098 13,686 13,816 13,977 14,182 14,391 14,604 14,821

Average Sales per sqm ($AUD) 12,587 11,900 12,014 12,154 12,332 12,514 12,699 12,888

21

Source: ABS Data Series 6401 Consumer Price Index

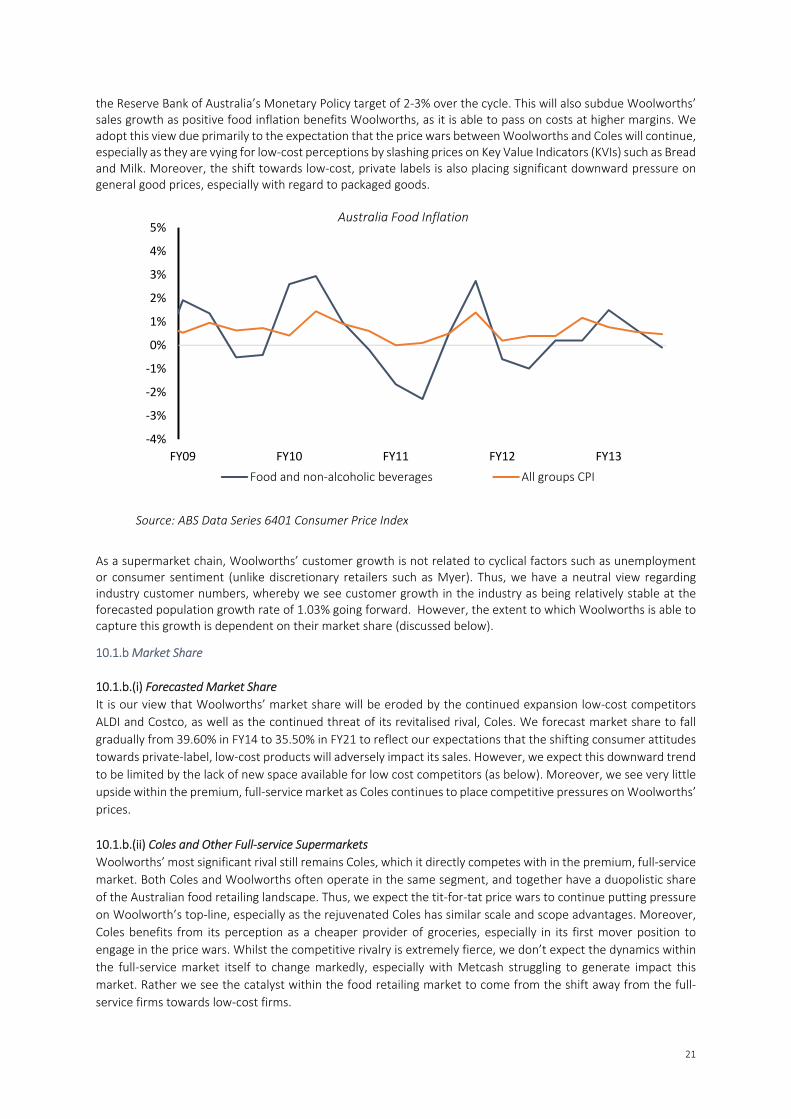

the Reserve Bank of Australia’s Monetary Policy target of 2‐3% over the cycle. This will also subdue Woolworths’ sales growth as positive food inflation benefits Woolworths, as it is able to pass on costs at higher margins. We adopt this view due primarily to the expectation that the price wars between Woolworths and Coles will continue, especially as they are vying for low‐cost perceptions by slashing prices on Key Value Indicators (KVIs) such as Bread and Milk. Moreover, the shift towards low‐cost, private labels is also placing significant downward pressure on general good prices, especially with regard to packaged goods.

As a supermarket chain, Woolworths’ customer growth is not related to cyclical factors such as unemployment or consumer sentiment (unlike discretionary retailers such as Myer). Thus, we have a neutral view regarding industry customer numbers, whereby we see customer growth in the industry as being relatively stable at the forecasted population growth rate of 1.03% going forward. However, the extent to which Woolworths is able to capture this growth is dependent on their market share (discussed below).

10.1.b Market Share

10.1.b.(i) Forecasted Market Share

It is our view that Woolworths’ market share will be eroded by the continued expansion low‐cost competitors