Embed Size (px)

Citation preview

CFA Society of IndianapolisFinancial Planning Association of Greater Indiana

State of the Credit Cycle: Past vs. PrologueSeptember 18, 2015

Glenn Reynolds, CFA

Nathan Wenger, CFA

2

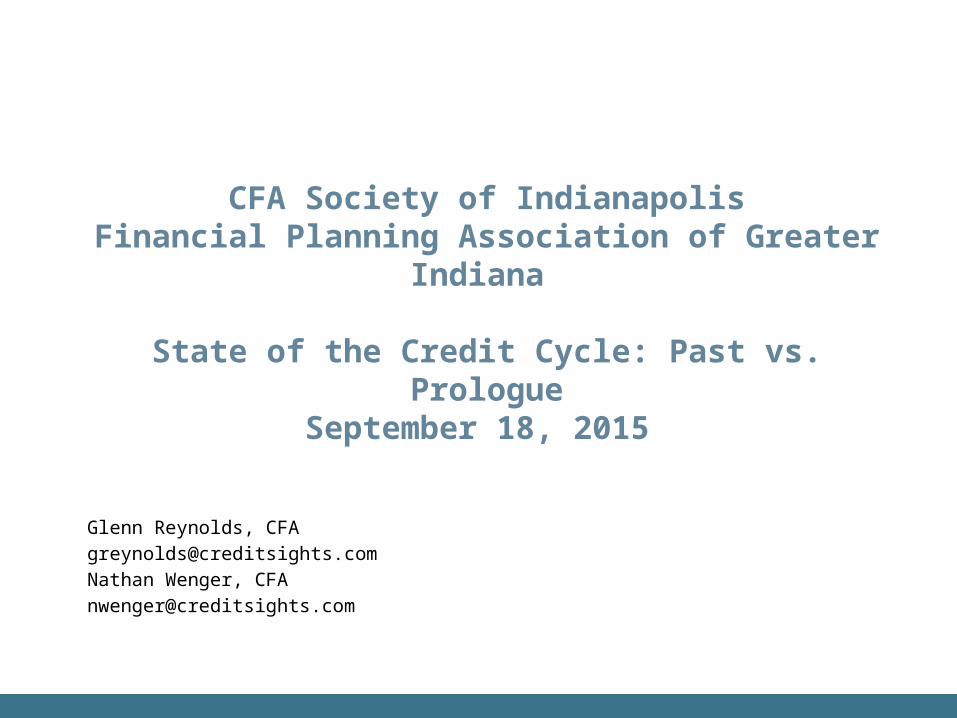

Annual Relative Total Return Ranking - USD Multi-Asset Class

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTDS&P 500

33.3%

CCMP 40.2%

CCMP 86.1%

Mid Cap

17.5%

High Grade 10.7%

EM Sov

13.7%

EM Equity 55.8%

EM Equity 26.0%

EM Equity 34.3%

EM Equity 32.5%

EM Equity 39.7%

US Gov't 14.0%

EM Equity 78.9%

Russell 2000 26.8%

Munis 11.2%

EM Equity 18.6%

CCMP 40.2%

P refs 15.4%

P refs 3.9%

Mid Cap

32.2%

S&P 500

28.5%

EM Equity 66.5%

Munis 17.1%

P refs 9.8%

US Gov't 11.6%

CCMP 50.8%

Russell 2000 18.3%

Mid Cap

12.6%

Russell 2000 18.3%

CCMP 10.7%

Mtges 8.3%

High Yield 57.5%

Mid Cap

26.6%

US Gov't 9.8%

EM Sov

18.3%

Russell 2000 38.8%

CCMP 14.8%

Loans 2.7%

Russell 2000 22.2%

Mid Cap 19.1%

Conv 36.0%

P refs 16.2%

Mtges 8.1%

Munis 10.7%

Russell 2000 47.3%

Mid Cap

16.5%

EM Sov

12.0%

S&P 500

15.8%

US Gov't 9.1%

Munis -4.0%

Loans 52.5%

EM Equity 19.3%

EM Sov 8.2%

Mid Cap

17.8%

Mid Cap

33.5%

S&P 500

13.7%

EM Corp 2.0%

CCMP 22.2%

Conv 12.2%

EM Sov

23.6%

EM Sov

14.7%

EM Corp 7.0%

High Grade 10.2%

Mid Cap

35.6%

EM Sov 11.8%

EM Corp 5.7%

Conv 12.0%

Mid Cap 8.0%

High Grade -6.8%

Conv 45.6%

CCMP 18.1%

High Grade 7.5%

CCMP 17.7%

S&P 500

32.4%

Conv 10.0%

CCMP 1.7%

Conv 15.5%

US Gov't 10.0%

Russell 2000 21.3%

US Gov't 13.4%

US Gov't 6.7%

EM Corp 9.4%

S&P 500

28.7%

S&P 500

10.9%

Loans 5.3%

High Yield 11.8%

Mtges 7.0%

EM Sov

-10.2%

CCMP 45.3%

Conv 15.7%

Mtges 6.1%

Russell 2000 16.4%

Conv 26.6%

Munis 9.8%

Munis 1.1%

EM Sov 15.1%

High Grade 8.7%

S&P 500

21.0%

Mtges 11.3%

EM Sov 4.8%

Mtges 9.4%

High Yield 28.1%

High Yield 10.9%

S&P 500 4.9%

CCMP 10.9%

EM Sov 6.4%

EM Corp -17.5%

EM Corp 38.3%

High Yield 15.2%

High Yield 4.4%

S&P 500

16.0%

High Yield 7.4%

Mid Cap 9.7%

Mtges 0.9%

High Yield 13.3%

Mtges 7.2%

Mid Cap

14.7%

EM Corp 9.8%

High Yield 4.5%

P refs 7.7%

EM Sov

27.6%

CCMP 10.3%

Russell 2000 4.5%

EM Sov

10.6%

S&P 500 5.6%

P refs -25.2%

Mid Cap

37.3%

S&P 500

15.1%

EM Corp 4.2%

High Yield 15.6%

Loans 5.4%

High Grade 7.5%

US Gov't 0.9%

Munis 10.9%

Munis 7.1%

EM Corp 14.5%

High Grade 9.1%

Munis 4.5%

Loans 2.6%

Conv 23.0%

EM Corp 8.9%

Munis 3.9%

Mid Cap

10.3%

High Grade 4.6%

High Yield

-26.4%

EM Sov

27.2%

P refs 13.7%

P refs 4.1%

EM Corp 15.5%

EM Corp -1.3%

EM Sov 7.3%

EM Sov 0.8%

High Grade 10.4%

P refs 6.7%

Loans 4.1%

Loans 5.1%

Loans 3.3%

High Yield -1.9%

EM Corp 14.5%

Conv 8.3%

US Gov't 2.8%

P refs 8.1%

EM Corp 4.4%

Loans -29.3%

Russell 2000 27.1%

EM Corp 12.8%

S&P 500 2.1%

Conv 13.6%

Mtges -1.4%

Mtges 6.1%

Conv 0.3%

P refs 10.0%

Loans 5.6%

High Yield 2.5%

Russell 2000 -3.0%

Russell 2000 2.5%

Conv -3.1%

Loans 9.8%

Munis 5.5%

High Yield 2.7%

Loans 6.9%

Conv 3.9%

Conv -29.4%

S&P 500

26.4%

EM Sov

12.5%

Loans 1.5%

P refs 13.6%

High Grade -1.5%

US Gov't 6.0%

High Yield 0.1%

US Gov't 9.6%

High Yield 3.0%

Mtges 1.6%

High Yield -5.1%

Mid Cap

-0.6%

EM Equity -5.9%

P refs 9.4%

High Grade 5.4%

Mtges 2.6%

EM Corp 6.6%

Munis 3.3%

Russell 2000

-33.8%

P refs 20.1%

Loans 10.4%

CCMP -0.8%

High Grade 10.4%

EM Equity -2.3%

Russell 2000 4.9%

High Grade -0.6%

Mtges 9.3%

Russell 2000 -2.1%

High Grade -1.9%

Conv -7.5%

EM Equity -2.4%

Mid Cap

-14.5%

High Grade 8.3%

Loans 5.3%

CCMP 2.1%

Mtges 5.3%

High Yield 2.2%

Mid Cap

-36.2%

High Grade 19.8%

High Grade 9.5%

Mid Cap -1.7%

Loans 9.8%

Munis -2.9%

EM Corp 3.7%

Mid Cap -1.5%

Loans 7.5%

EM Sov

-15.3%

US Gov't -2.4%

S&P 500

-9.1%

Conv -2.9%

Russell 2000

-20.5%

Munis 6.2%

P refs 5.1%

High Grade 2.0%

Munis 5.0%

Loans 2.0%

S&P 500

-37.0%

Munis 14.5%

US Gov't 5.9%

Conv -3.8%

Munis 7.3%

US Gov't -3.3%

High Yield 2.5%

S&P 500

-2.9%

EM Equity -12.3%

EM Equity -26.0%

P refs -4.4%

EM Equity -30.7%

S&P 500

-11.9%

S&P 500

-22.1%

Mtges 3.3%

Mtges 4.7%

P refs 1.0%

High Grade 4.4%

Russell 2000 -1.6%

CCMP -40.0%

Mtges 5.8%

Mtges 5.7%

Russell 2000 -4.2%

Mtges 2.6%

P refs -3.7%

Loans 1.8%

Russell 2000 -3.0%

EM Corp

na

EM Corp

na

Munis -6.3%

CCMP -39.2%

CCMP -20.8%

CCMP -31.2%

US Gov't 2.3%

US Gov't 3.5%

Conv -0.2%

US Gov't 3.1%

P refs -11.3%

EM Equity -53.2%

US Gov't -3.7%

Munis 2.3%

EM Equity -18.2%

US Gov't 2.2%

EM Sov

-5.8%

EM Equity -2.0%

EM Equity -12.7%

Source: CreditSights, BofA/ML, S&P /LSTA, Bloomberg. EM Equity is USD MSCI Emerging Market Index, M id Cap is S&P Mid Cap 400 Index

CCMP =NASDAQ EM Sov is USD EM Sovereign BBB & lower index, EM Corp is USD EM Corporate P lus IndexYTD calculated as of Aug 31, 2015

3

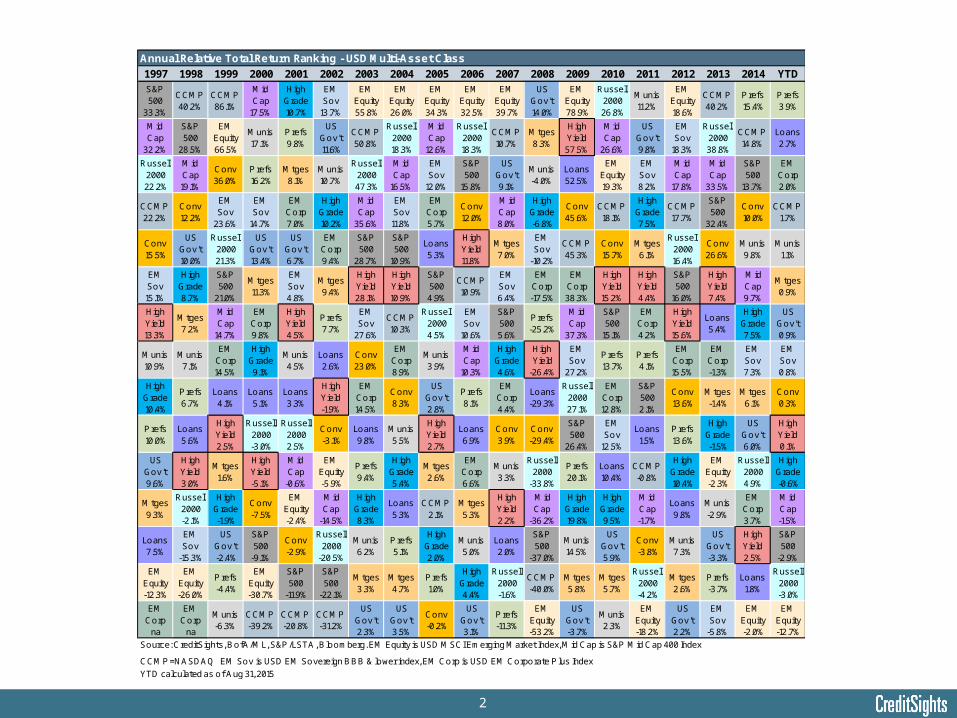

US Asset Class Correlation Matrix

UST EM Sov <=BB Mtge ABS SPX HG Loans HY

HG Bonds Jan '97 - Current 0.62 0.43 0.65 0.32 0.19 - 0.39 0.54

HG Bonds Jan '97- Jun '07 0.88 0.25 0.81 0.38 0.01 - 0.08 0.37

HG Bonds Sep '08 - Dec '09 0.16 0.80 0.37 0.30 0.63 - 0.61 0.74

HG Bonds Jan '08 - Dec '10 0.26 0.77 0.42 0.32 0.50 - 0.56 0.70

HY Bonds Jan '97 - Current -0.17 0.57 0.07 0.35 0.61 0.54 0.79 -

HY Bonds Jan '97-Jun '07 -0.01 0.49 0.09 0.02 0.49 0.37 0.56 -

HY Bonds Sep '08 - Dec '09 -0.37 0.77 0.07 0.58 0.77 0.74 0.92 -

HY Bonds Jan '08 - Dec '10 -0.35 0.77 0.04 0.53 0.75 0.70 0.89 -

Loans Jan '99 - Current -0.33 0.44 -0.09 0.51 0.45 0.39 - 0.79

Loans Jan '99 - Jun '07 -0.19 0.22 -0.17 0.27 0.17 0.08 - 0.56

Loans Sep '08 - Dec '09 -0.56 0.65 -0.09 0.70 0.66 0.61 - 0.92

Loans Jan '08 - Dec '10 -0.50 0.63 -0.08 0.61 0.61 0.56 - 0.89

EM Sovereign <=BB Jan '97- Current 0.05 - 0.23 0.14 0.51 0.43 0.44 0.57

EM Sovereign <=BB Jan '97 - Jun '07 0.05 - 0.19 0.02 0.46 0.25 0.22 0.49

EM Sovereign <=BB Sep '08 - Dec '09 0.09 - 0.42 0.31 0.77 0.80 0.65 0.77

EM Sovereign <=BB Jan '08 - Dec '10 0.08 - 0.31 0.29 0.72 0.77 0.63 0.77Source: CreditSights, BoA/ ML Indices, J P Morgan, S&P /LSTA, Bloomberg Loan data starts J anuary 1999Current data through 08/28/2015

4

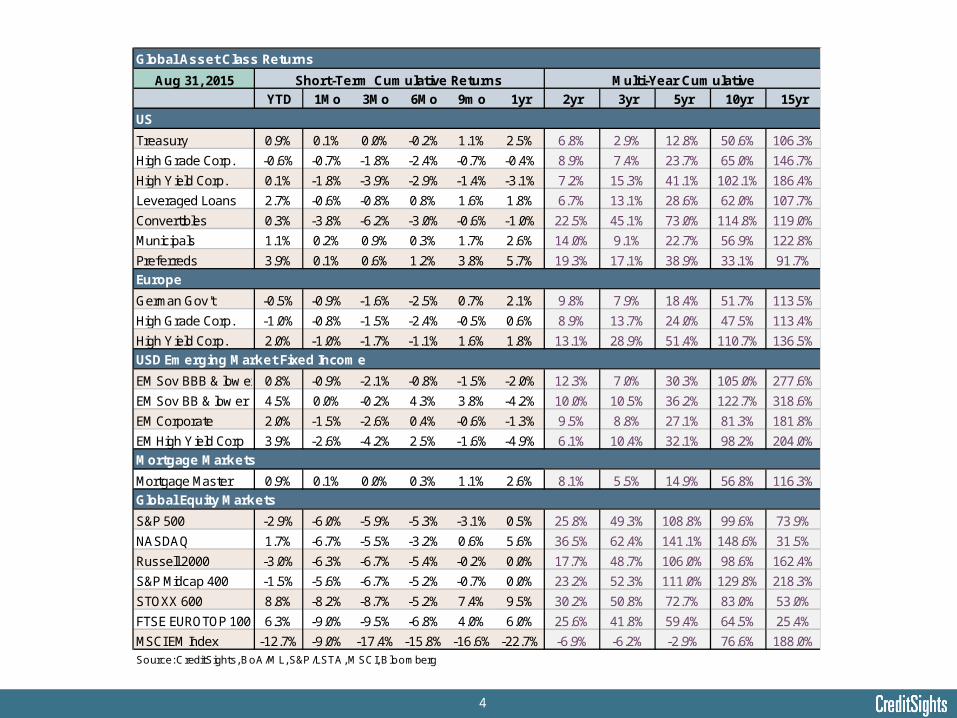

Global Asset Class Returns

Aug 31, 2015

YTD 1Mo 3Mo 6Mo 9mo 1yr 2yr 3yr 5yr 10yr 15yr

US

Treasury 0.9% 0.1% 0.0% -0.2% 1.1% 2.5% 6.8% 2.9% 12.8% 50.6% 106.3%

High Grade Corp. -0.6% -0.7% -1.8% -2.4% -0.7% -0.4% 8.9% 7.4% 23.7% 65.0% 146.7%

High Yield Corp. 0.1% -1.8% -3.9% -2.9% -1.4% -3.1% 7.2% 15.3% 41.1% 102.1% 186.4%

Leveraged Loans 2.7% -0.6% -0.8% 0.8% 1.6% 1.8% 6.7% 13.1% 28.6% 62.0% 107.7%

Convertibles 0.3% -3.8% -6.2% -3.0% -0.6% -1.0% 22.5% 45.1% 73.0% 114.8% 119.0%

Municipals 1.1% 0.2% 0.9% 0.3% 1.7% 2.6% 14.0% 9.1% 22.7% 56.9% 122.8%

Preferreds 3.9% 0.1% 0.6% 1.2% 3.8% 5.7% 19.3% 17.1% 38.9% 33.1% 91.7%

Europe

German Gov't -0.5% -0.9% -1.6% -2.5% 0.7% 2.1% 9.8% 7.9% 18.4% 51.7% 113.5%

High Grade Corp. -1.0% -0.8% -1.5% -2.4% -0.5% 0.6% 8.9% 13.7% 24.0% 47.5% 113.4%

High Yield Corp. 2.0% -1.0% -1.7% -1.1% 1.6% 1.8% 13.1% 28.9% 51.4% 110.7% 136.5%

USD Emerging Market Fixed Income

EM Sov BBB & low er 0.8% -0.9% -2.1% -0.8% -1.5% -2.0% 12.3% 7.0% 30.3% 105.0% 277.6%

EM Sov BB & low er 4.5% 0.0% -0.2% 4.3% 3.8% -4.2% 10.0% 10.5% 36.2% 122.7% 318.6%

EM Corporate 2.0% -1.5% -2.6% 0.4% -0.6% -1.3% 9.5% 8.8% 27.1% 81.3% 181.8%

EM High Yield Corp 3.9% -2.6% -4.2% 2.5% -1.6% -4.9% 6.1% 10.4% 32.1% 98.2% 204.0%

Mortgage Markets

Mortgage Master 0.9% 0.1% 0.0% 0.3% 1.1% 2.6% 8.1% 5.5% 14.9% 56.8% 116.3%

Global Equity Markets

S&P 500 -2.9% -6.0% -5.9% -5.3% -3.1% 0.5% 25.8% 49.3% 108.8% 99.6% 73.9%

NASDAQ 1.7% -6.7% -5.5% -3.2% 0.6% 5.6% 36.5% 62.4% 141.1% 148.6% 31.5%

Russell 2000 -3.0% -6.3% -6.7% -5.4% -0.2% 0.0% 17.7% 48.7% 106.0% 98.6% 162.4%

S&P Midcap 400 -1.5% -5.6% -6.7% -5.2% -0.7% 0.0% 23.2% 52.3% 111.0% 129.8% 218.3%

STOXX 600 8.8% -8.2% -8.7% -5.2% 7.4% 9.5% 30.2% 50.8% 72.7% 83.0% 53.0%

FTSE EUROTOP 100 6.3% -9.0% -9.5% -6.8% 4.0% 6.0% 25.6% 41.8% 59.4% 64.5% 25.4%

MSCI EM Index -12.7% -9.0% -17.4% -15.8% -16.6% -22.7% -6.9% -6.2% -2.9% 76.6% 188.0%Source: CreditSights, BoA/ML, S&P /LSTA, MSCI, Bloomberg

Multi-Year CumulativeShort-Term Cumulative Returns

5

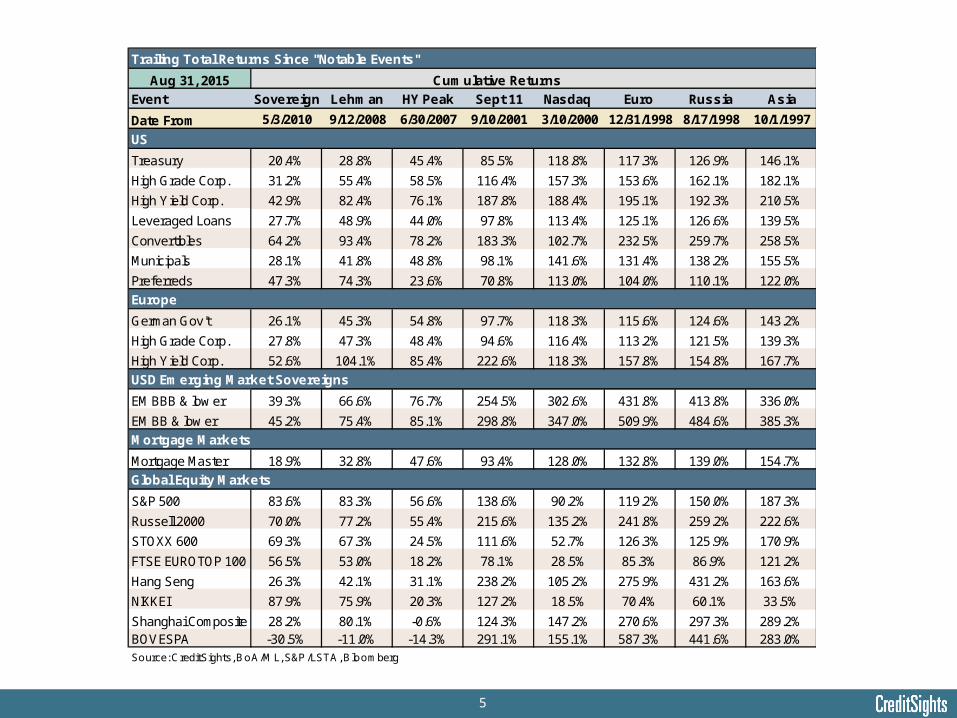

Trailing Total Returns Since "Notable Events"

Aug 31, 2015

Event Sovereign Lehman HY Peak Sept 11 Nasdaq Euro Russia Asia

Date From 5/3/2010 9/12/2008 6/30/2007 9/10/2001 3/10/2000 12/31/1998 8/17/1998 10/1/1997

US

Treasury 20.4% 28.8% 45.4% 85.5% 118.8% 117.3% 126.9% 146.1%

High Grade Corp. 31.2% 55.4% 58.5% 116.4% 157.3% 153.6% 162.1% 182.1%

High Yield Corp. 42.9% 82.4% 76.1% 187.8% 188.4% 195.1% 192.3% 210.5%

Leveraged Loans 27.7% 48.9% 44.0% 97.8% 113.4% 125.1% 126.6% 139.5%

Convertibles 64.2% 93.4% 78.2% 183.3% 102.7% 232.5% 259.7% 258.5%

Municipals 28.1% 41.8% 48.8% 98.1% 141.6% 131.4% 138.2% 155.5%

Preferreds 47.3% 74.3% 23.6% 70.8% 113.0% 104.0% 110.1% 122.0%

Europe

German Gov't 26.1% 45.3% 54.8% 97.7% 118.3% 115.6% 124.6% 143.2%

High Grade Corp. 27.8% 47.3% 48.4% 94.6% 116.4% 113.2% 121.5% 139.3%

High Yield Corp. 52.6% 104.1% 85.4% 222.6% 118.3% 157.8% 154.8% 167.7%

USD Emerging Market Sovereigns

EM BBB & low er 39.3% 66.6% 76.7% 254.5% 302.6% 431.8% 413.8% 336.0%

EM BB & low er 45.2% 75.4% 85.1% 298.8% 347.0% 509.9% 484.6% 385.3%

Mortgage Markets

Mortgage Master 18.9% 32.8% 47.6% 93.4% 128.0% 132.8% 139.0% 154.7%

Global Equity Markets

S&P 500 83.6% 83.3% 56.6% 138.6% 90.2% 119.2% 150.0% 187.3%

Russell 2000 70.0% 77.2% 55.4% 215.6% 135.2% 241.8% 259.2% 222.6%

STOXX 600 69.3% 67.3% 24.5% 111.6% 52.7% 126.3% 125.9% 170.9%

FTSE EUROTOP 100 56.5% 53.0% 18.2% 78.1% 28.5% 85.3% 86.9% 121.2%

Hang Seng 26.3% 42.1% 31.1% 238.2% 105.2% 275.9% 431.2% 163.6%

NIKKEI 87.9% 75.9% 20.3% 127.2% 18.5% 70.4% 60.1% 33.5%

Shanghai Composite 28.2% 80.1% -0.6% 124.3% 147.2% 270.6% 297.3% 289.2%BOVESPA -30.5% -11.0% -14.3% 291.1% 155.1% 587.3% 441.6% 283.0%Source: CreditSights, BoA/ML, S&P /LSTA, Bloomberg

Cumulative Returns

6

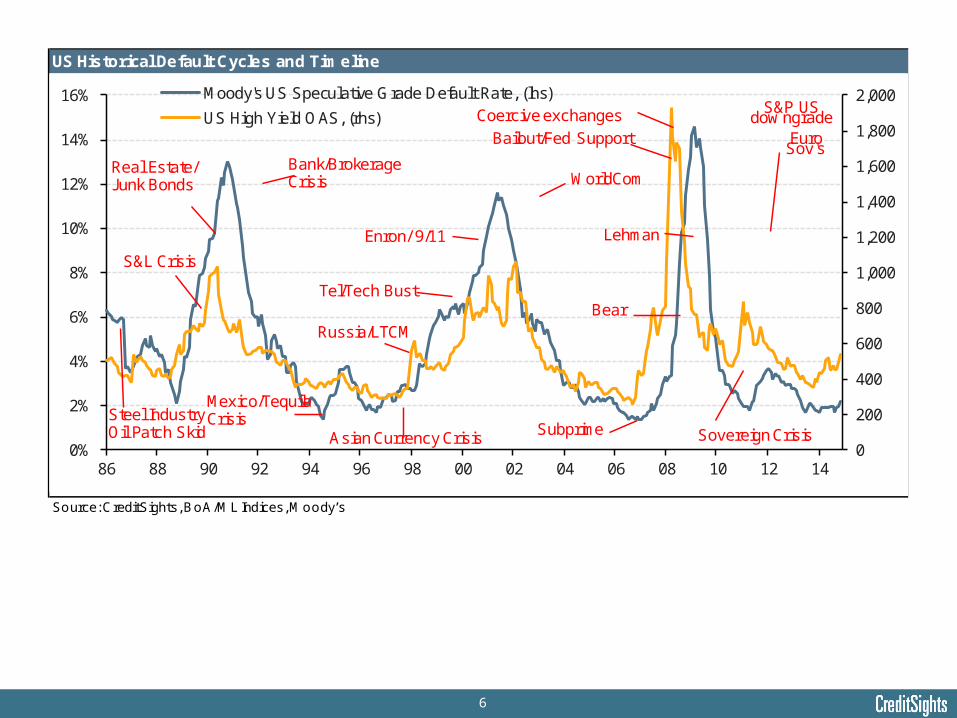

US Historical Default Cycles and Timeline

Source: CreditSights, BoA/ML Indices, Moody’s

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0%

2%

4%

6%

8%

10%

12%

14%

16%

86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

Moody's US Speculative Grade Default Rate, (lhs)

US High Yield OAS, (rhs)

Steel IndustryOil Patch Skid

Real Estate/Junk Bonds

S&L Crisis

Bank/Brokerage Crisis

Russia/LTCM

Enron/ 9/11

Asian Currency Crisis

Tel/Tech Bust

Subprime

Bear

Bailout/Fed Support

S&P US dow ngrade

Euro Sov's

Lehman

WorldCom

Sovereign Crisis

Mexico/Tequila Crisis

Coercive exchanges

7

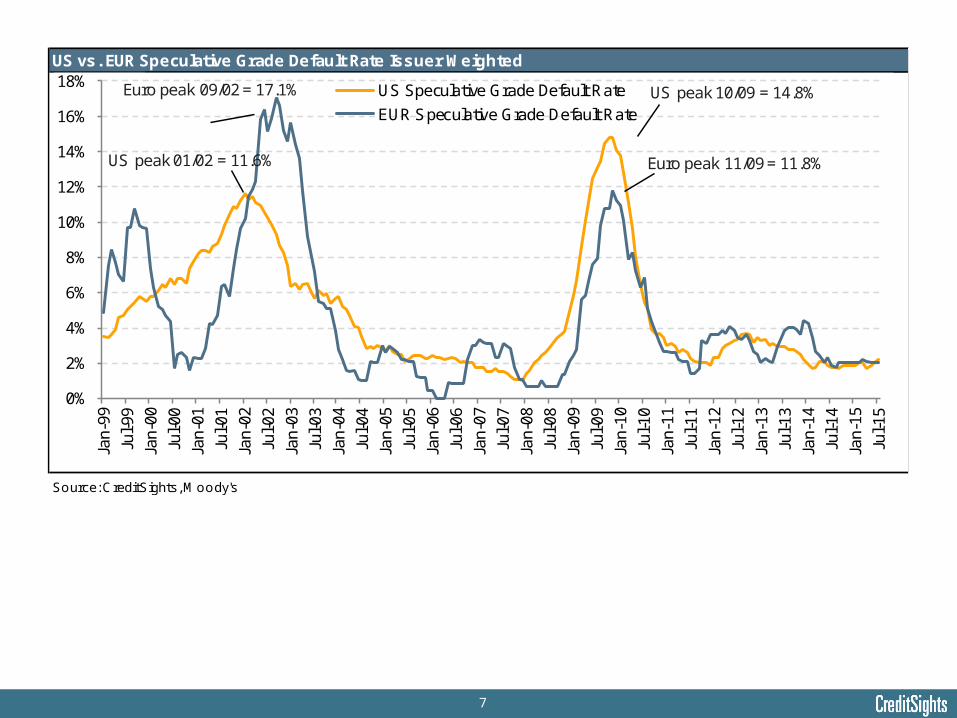

US vs. EUR Speculative Grade Default Rate Issuer Weighted

Source: CreditSights, Moody's

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%Ja

n-99

Jul-9

9

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

US Speculative Grade Default Rate

EUR Speculative Grade Default RateUS peak 10/09 = 14.8%Euro peak 09/02 = 17.1%

US peak 01/02 = 11.6% Euro peak 11/09 = 11.8%

8

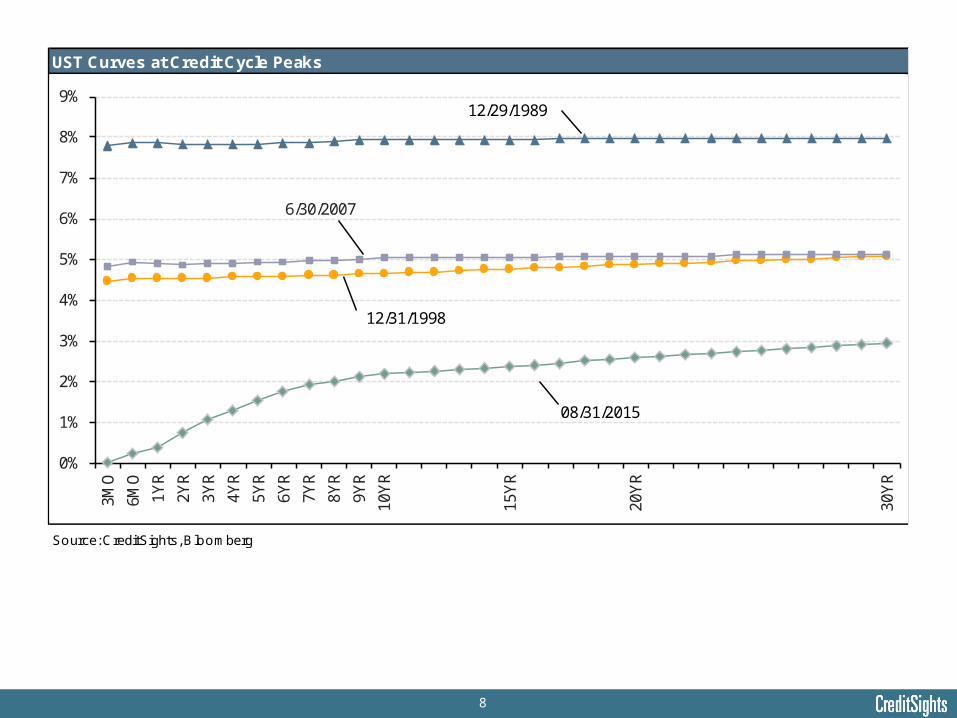

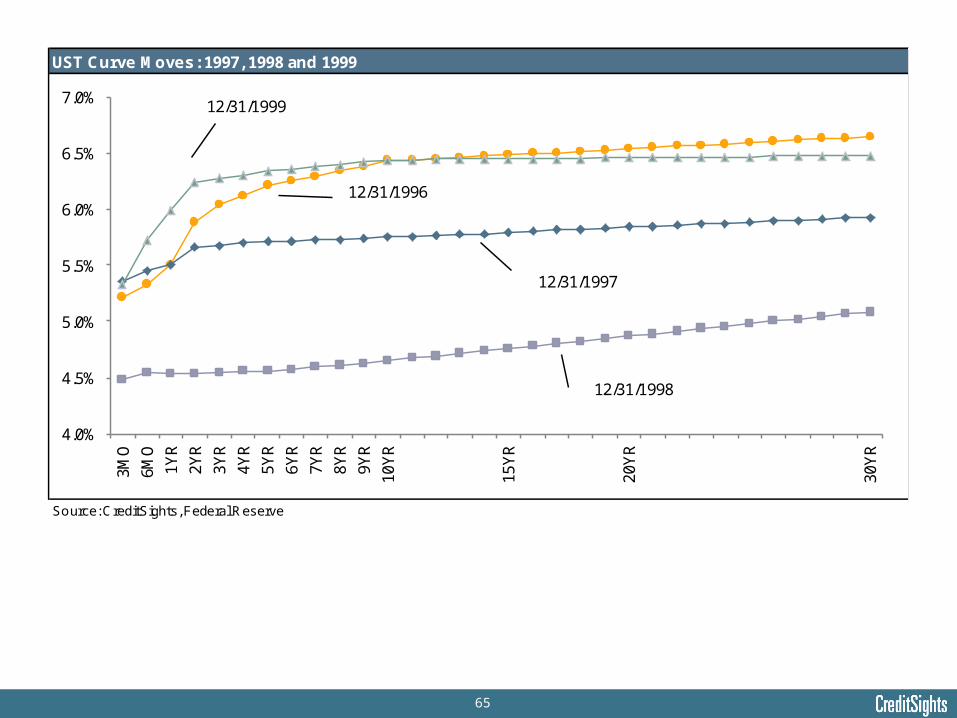

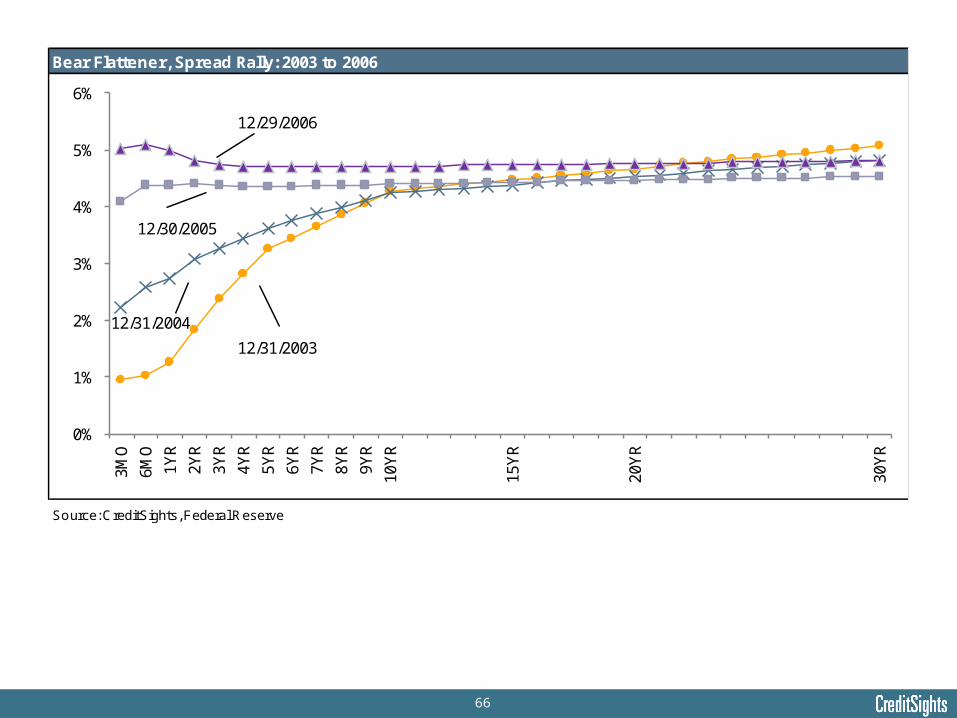

UST Curves at Credit Cycle Peaks

Source: CreditSights, Bloomberg

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%3M

O

6MO

1YR

2YR

3YR

4YR

5YR

6YR

7YR

8YR

9YR

10Y

R

15Y

R

20Y

R

30Y

R

12/29/1989

08/31/2015

12/31/1998

6/30/2007

9

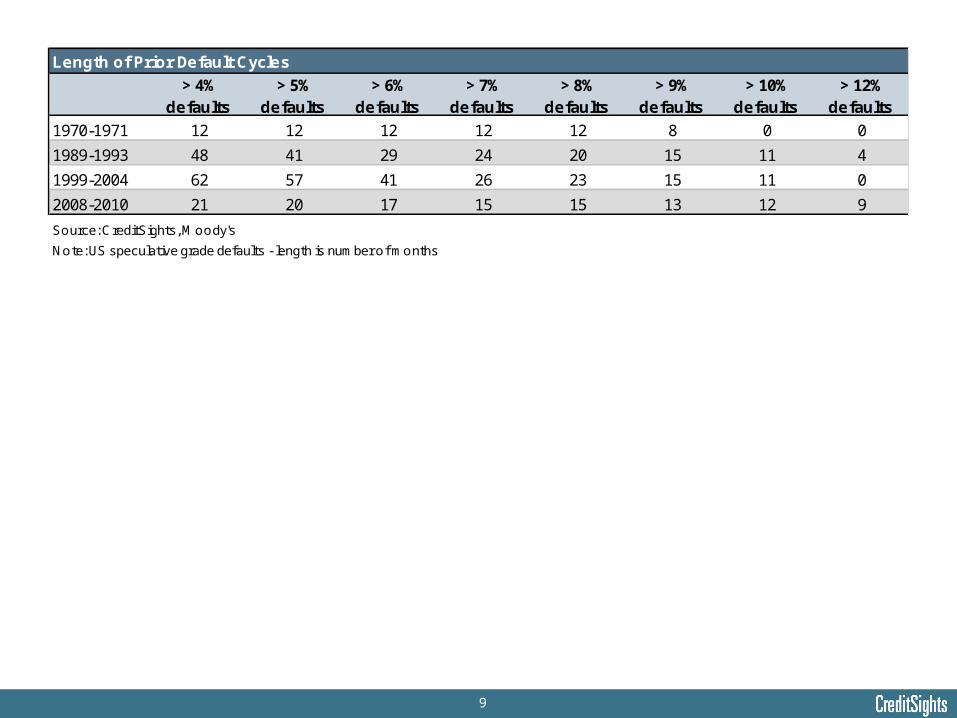

Length of Prior Default Cycles

> 4% defaults

> 5% defaults

> 6% defaults

> 7% defaults

> 8% defaults

> 9% defaults

> 10% defaults

> 12% defaults

1970-1971 12 12 12 12 12 8 0 0

1989-1993 48 41 29 24 20 15 11 4

1999-2004 62 57 41 26 23 15 11 0

2008-2010 21 20 17 15 15 13 12 9

Source: CreditSights, Moody's

Note: US speculative grade defaults - length is number of months

10

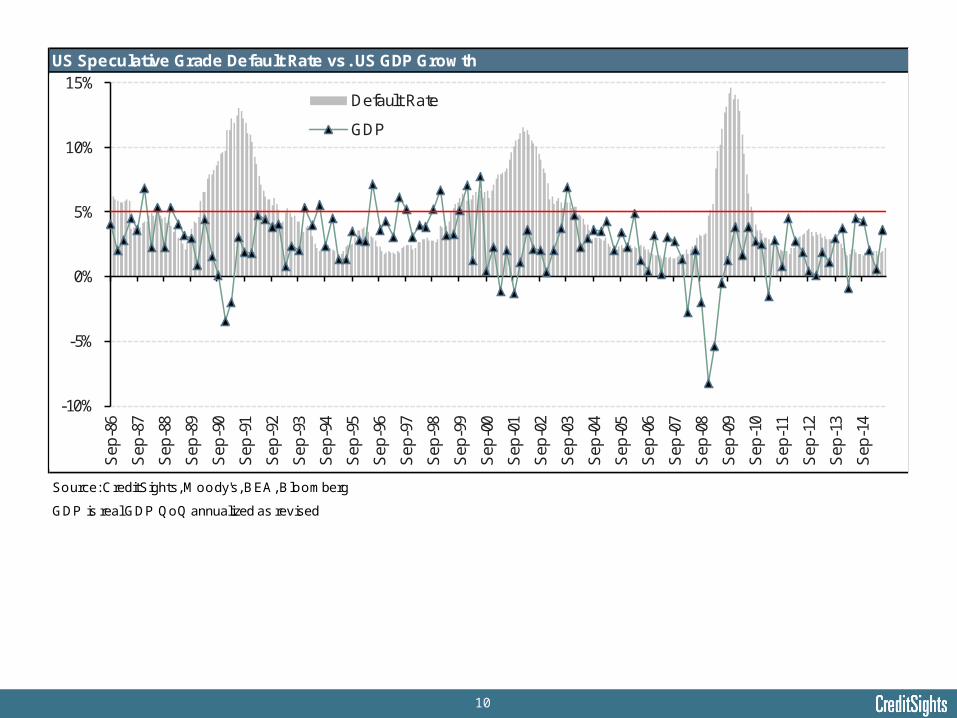

US Speculative Grade Default Rate vs. US GDP Growth

Source: CreditSights, Moody's, BEA, Bloomberg

GDP is real GDP QoQ annualized as revised

-10%

-5%

0%

5%

10%

15%

Sep

-86

Sep

-87

Sep

-88

Sep

-89

Sep

-90

Sep

-91

Sep

-92

Sep

-93

Sep

-94

Sep

-95

Sep

-96

Sep

-97

Sep

-98

Sep

-99

Sep

-00

Sep

-01

Sep

-02

Sep

-03

Sep

-04

Sep

-05

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

Sep

-11

Sep

-12

Sep

-13

Sep

-14

Default Rate

GDP

11

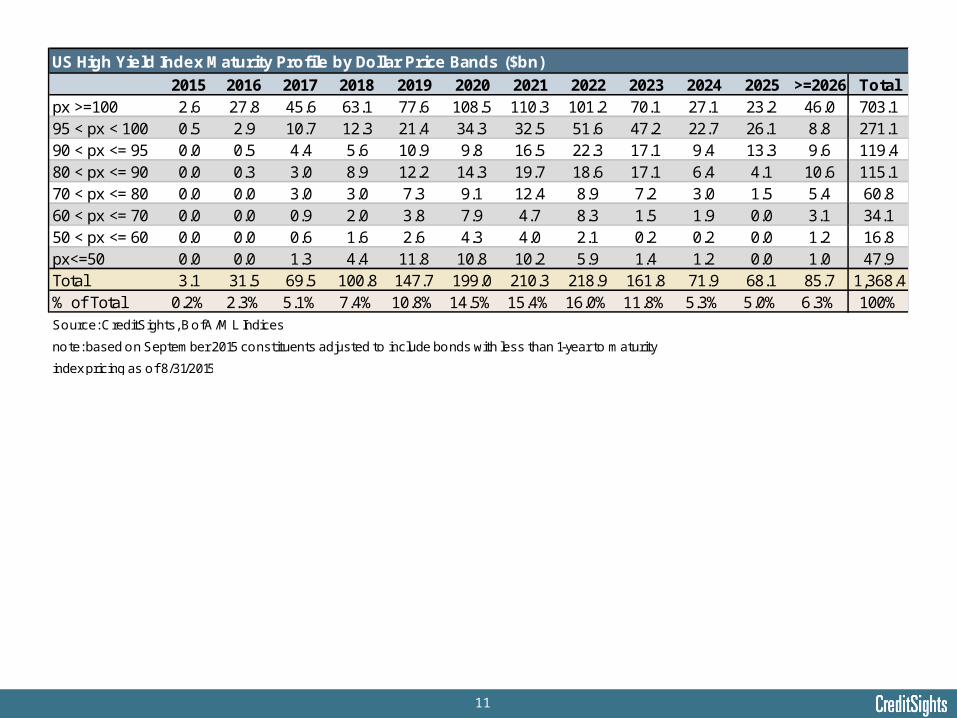

US High Yield Index Maturity Profile by Dollar Price Bands ($bn)

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 >=2026 Totalpx >=100 2.6 27.8 45.6 63.1 77.6 108.5 110.3 101.2 70.1 27.1 23.2 46.0 703.195 < px < 100 0.5 2.9 10.7 12.3 21.4 34.3 32.5 51.6 47.2 22.7 26.1 8.8 271.190 < px <= 95 0.0 0.5 4.4 5.6 10.9 9.8 16.5 22.3 17.1 9.4 13.3 9.6 119.480 < px <= 90 0.0 0.3 3.0 8.9 12.2 14.3 19.7 18.6 17.1 6.4 4.1 10.6 115.170 < px <= 80 0.0 0.0 3.0 3.0 7.3 9.1 12.4 8.9 7.2 3.0 1.5 5.4 60.860 < px <= 70 0.0 0.0 0.9 2.0 3.8 7.9 4.7 8.3 1.5 1.9 0.0 3.1 34.150 < px <= 60 0.0 0.0 0.6 1.6 2.6 4.3 4.0 2.1 0.2 0.2 0.0 1.2 16.8px<=50 0.0 0.0 1.3 4.4 11.8 10.8 10.2 5.9 1.4 1.2 0.0 1.0 47.9Total 3.1 31.5 69.5 100.8 147.7 199.0 210.3 218.9 161.8 71.9 68.1 85.7 1,368.4% of Total 0.2% 2.3% 5.1% 7.4% 10.8% 14.5% 15.4% 16.0% 11.8% 5.3% 5.0% 6.3% 100%

Source: CreditSights, BofA/ML Indices

note: based on September 2015 constituents adjusted to include bonds with less than 1-year to maturity

index pricing as of 8/31/2015

12

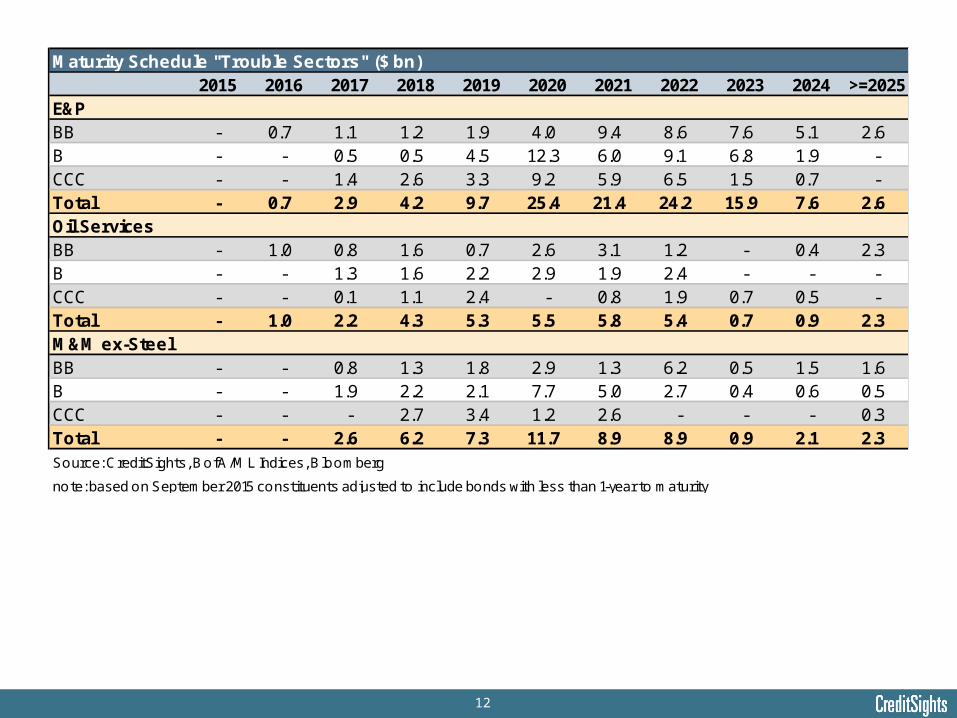

Maturity Schedule "Trouble Sectors" ($ bn)2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 >=2025

E&PBB - 0.7 1.1 1.2 1.9 4.0 9.4 8.6 7.6 5.1 2.6B - - 0.5 0.5 4.5 12.3 6.0 9.1 6.8 1.9 -CCC - - 1.4 2.6 3.3 9.2 5.9 6.5 1.5 0.7 -Total - 0.7 2.9 4.2 9.7 25.4 21.4 24.2 15.9 7.6 2.6Oil ServicesBB - 1.0 0.8 1.6 0.7 2.6 3.1 1.2 - 0.4 2.3B - - 1.3 1.6 2.2 2.9 1.9 2.4 - - -CCC - - 0.1 1.1 2.4 - 0.8 1.9 0.7 0.5 -Total - 1.0 2.2 4.3 5.3 5.5 5.8 5.4 0.7 0.9 2.3M&M ex-SteelBB - - 0.8 1.3 1.8 2.9 1.3 6.2 0.5 1.5 1.6B - - 1.9 2.2 2.1 7.7 5.0 2.7 0.4 0.6 0.5CCC - - - 2.7 3.4 1.2 2.6 - - - 0.3Total - - 2.6 6.2 7.3 11.7 8.9 8.9 0.9 2.1 2.3

Source: CreditSights, BofA/ML Indices, Bloomberg

note: based on September 2015 constituents adjusted to include bonds with less than 1-year to maturity

13

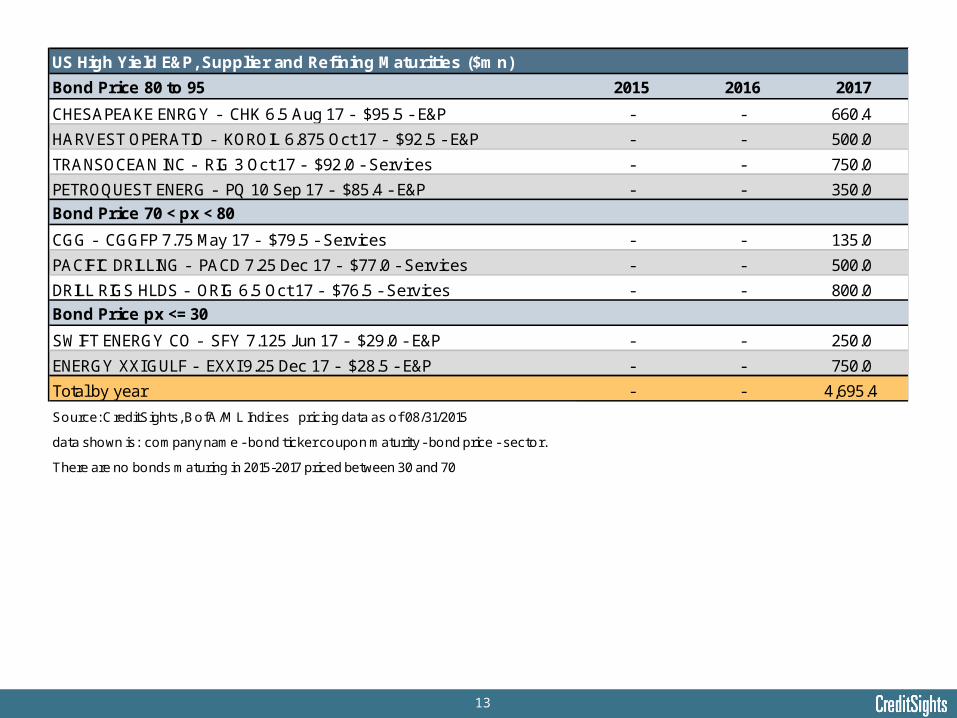

US High Yield E&P, Supplier and Refining Maturities ($mn)

Bond Price 80 to 95 2015 2016 2017

CHESAPEAKE ENRGY - CHK 6.5 Aug 17 - $95.5 - E&P - - 660.4

HARVEST OPERATIO - KOROIL 6.875 Oct 17 - $92.5 - E&P - - 500.0

TRANSOCEAN INC - RIG 3 Oct 17 - $92.0 - Services - - 750.0

PETROQUEST ENERG - PQ 10 Sep 17 - $85.4 - E&P - - 350.0

Bond Price 70 < px < 80

CGG - CGGFP 7.75 May 17 - $79.5 - Services - - 135.0

PACIFIC DRILLING - PACD 7.25 Dec 17 - $77.0 - Services - - 500.0

DRILL RIGS HLDS - ORIG 6.5 Oct 17 - $76.5 - Services - - 800.0

Bond Price px <= 30

SWIFT ENERGY CO - SFY 7.125 Jun 17 - $29.0 - E&P - - 250.0

ENERGY XXI GULF - EXXI 9.25 Dec 17 - $28.5 - E&P - - 750.0

Total by year - - 4,695.4

Source: CreditSights, BofA/ML Indices pricing data as of 08/31/2015

data shown is: company name - bond ticker coupon maturity - bond price - sector.

There are no bonds maturing in 2015-2017 priced between 30 and 70

14

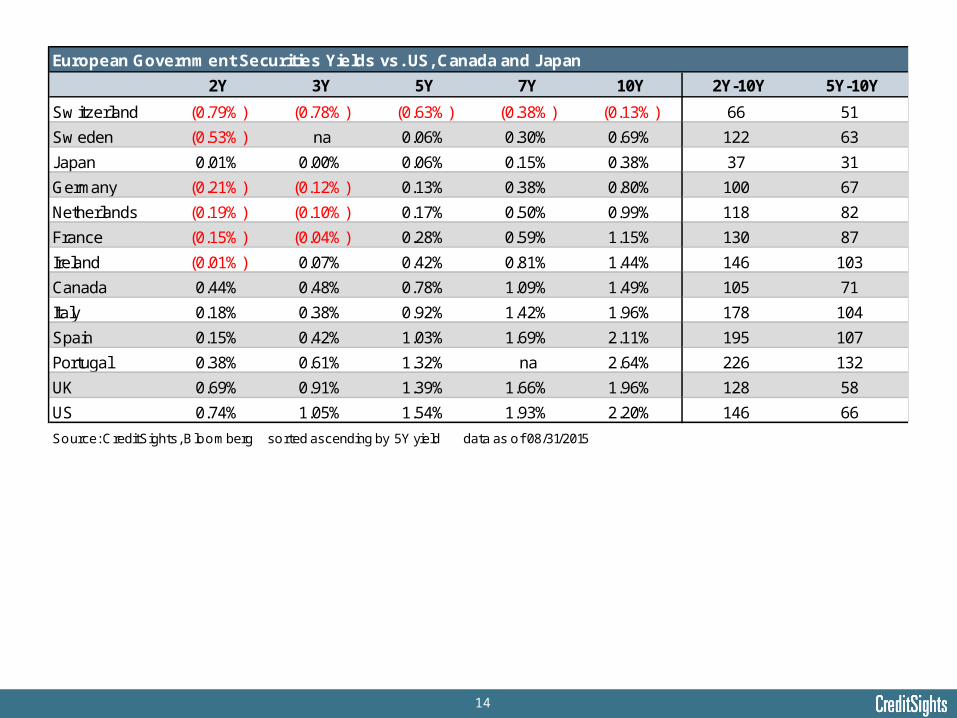

European Government Securities Yields vs. US, Canada and Japan

2Y 3Y 5Y 7Y 10Y 2Y-10Y 5Y-10Y

Sw itzerland (0.79%) (0.78%) (0.63%) (0.38%) (0.13%) 66 51

Sw eden (0.53%) na 0.06% 0.30% 0.69% 122 63

Japan 0.01% 0.00% 0.06% 0.15% 0.38% 37 31

Germany (0.21%) (0.12%) 0.13% 0.38% 0.80% 100 67

Netherlands (0.19%) (0.10%) 0.17% 0.50% 0.99% 118 82

France (0.15%) (0.04%) 0.28% 0.59% 1.15% 130 87

Ireland (0.01%) 0.07% 0.42% 0.81% 1.44% 146 103

Canada 0.44% 0.48% 0.78% 1.09% 1.49% 105 71

Italy 0.18% 0.38% 0.92% 1.42% 1.96% 178 104

Spain 0.15% 0.42% 1.03% 1.69% 2.11% 195 107

Portugal 0.38% 0.61% 1.32% na 2.64% 226 132

UK 0.69% 0.91% 1.39% 1.66% 1.96% 128 58

US 0.74% 1.05% 1.54% 1.93% 2.20% 146 66

Source: CreditSights, Bloomberg sorted ascending by 5Y yield data as of 08/31/2015

15

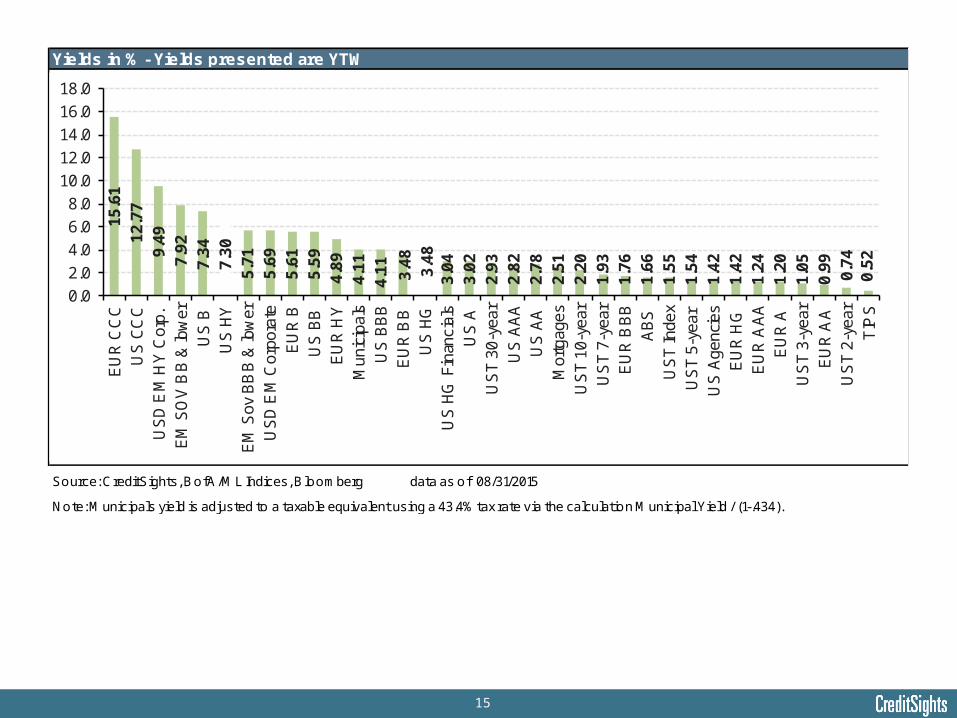

Yields in % - Yields presented are YTW

Source: CreditSights, BofA/ML Indices, Bloomberg data as of 08/31/2015

Note: Municipals yield is adjusted to a taxable equivalent using a 43.4% tax rate via the calculation Municipal Yield / (1-.434).

15.6

112

.77

9.49

7.92

7.34

7.30

5.71

5.69

5.61

5.59

4.89

4.11

4.11 3.48

3.48

3.04

3.02

2.93

2.82

2.78

2.51

2.20

1.93

1.76

1.66

1.55

1.54

1.42

1.42

1.24

1.20

1.05

0.99

0.74

0.52

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

EU

R C

CC

US

CC

CU

SD

EM

HY

Cor

p.E

M S

OV

BB

& lo

wer

US

BU

S H

YE

M S

ov B

BB

& lo

wer

US

D E

M C

orpo

rate

EU

R B

US

BB

EU

R H

YM

unic

ipal

sU

S B

BB

EU

R B

BU

S H

GU

S H

G F

inan

cial

sU

S A

US

T 30

-yea

rU

S A

AA

US

AA

Mor

tgag

esU

ST

10-y

ear

US

T 7-

year

EU

R B

BB

AB

SU

ST

Inde

xU

ST

5-ye

arU

S A

genc

ies

EU

R H

GE

UR

AA

AE

UR

AU

ST

3-ye

arE

UR

AA

US

T 2-

year

TIP

S

16

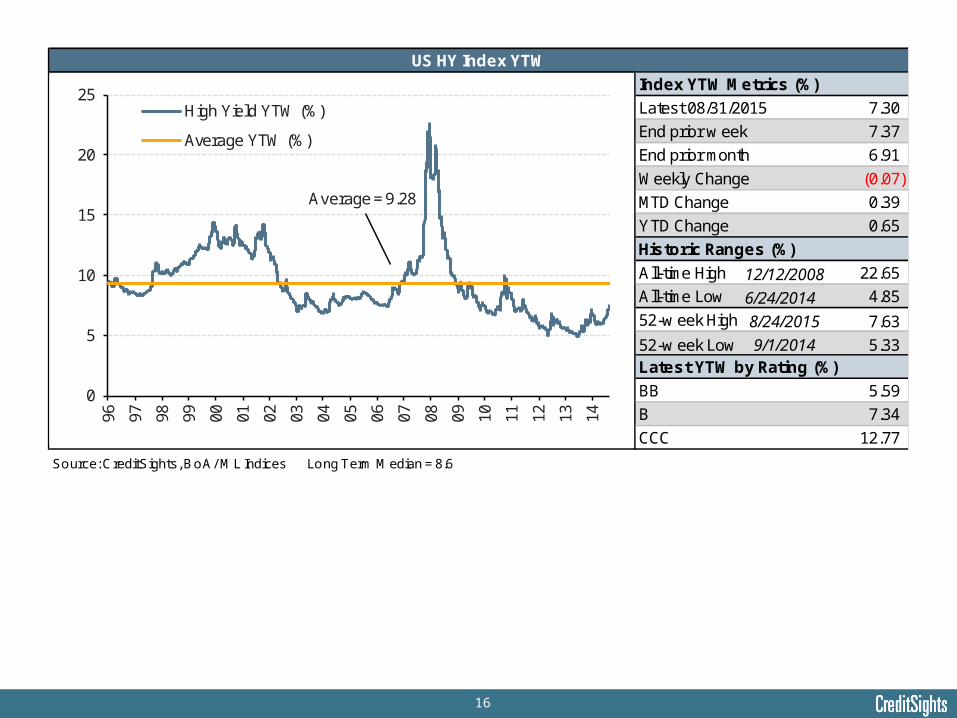

Index YTW Metrics (%)

Latest 08/31/2015 7.30

End prior w eek 7.37

End prior month 6.91

Weekly Change (0.07)

MTD Change 0.39

YTD Change 0.65

Historic Ranges (%)

All-time High 12/12/2008 22.65

All-time Low 6/24/2014 4.85

52-w eek High 8/24/2015 7.63

52-w eek Low 9/1/2014 5.33Latest YTW by Rating (%)

BB 5.59

B 7.34

CCC 12.77

Source: CreditSights, BoA/ ML Indices Long Term Median = 8.6

US HY Index YTW

0

5

10

15

20

2596 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

High Yield YTW (%)

Average YTW (%)

Average = 9.28

17

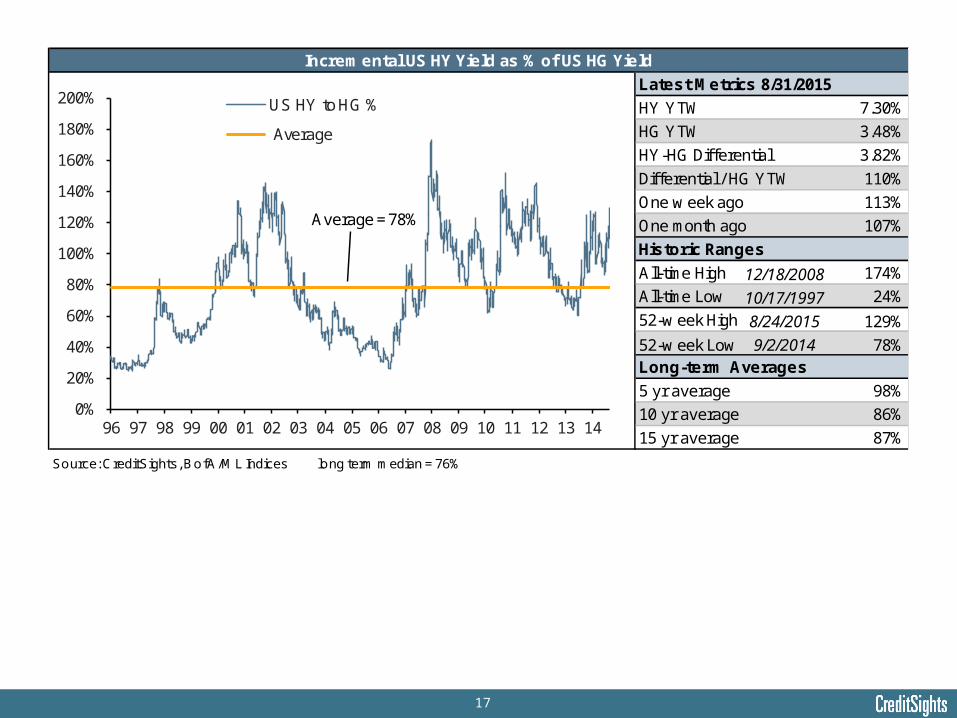

Latest Metrics 8/31/2015

HY YTW 7.30%

HG YTW 3.48%

HY-HG Differential 3.82%

Differential / HG YTW 110%

One w eek ago 113%

One month ago 107%

Historic Ranges

All-time High 12/18/2008 174%

All-time Low 10/17/1997 24%

52-w eek High 8/24/2015 129%

52-w eek Low 9/2/2014 78%Long-term Averages

5 yr average 98%

10 yr average 86%

15 yr average 87%

Source: CreditSights, BofA/ML Indices long term median = 76%

Incremental US HY Yield as % of US HG Yield

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

US HY to HG %

Average

Average = 78%

18

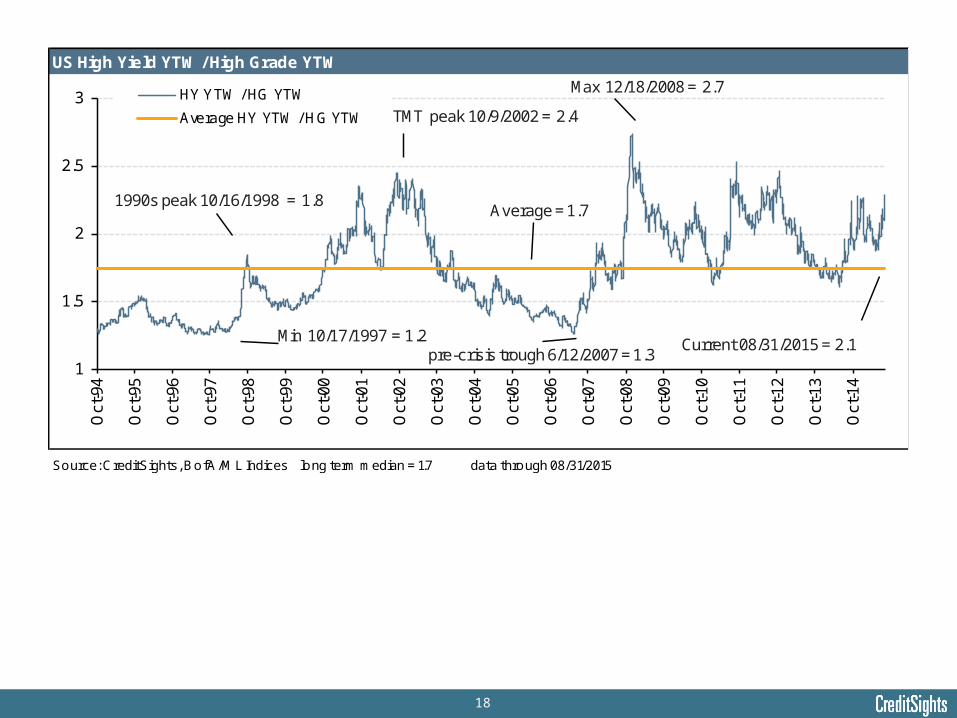

US High Yield YTW / High Grade YTW

Source: CreditSights, BofA/ML Indices long term median = 1.7 data through 08/31/2015

1

1.5

2

2.5

3O

ct-9

4

Oct

-95

Oct

-96

Oct

-97

Oct

-98

Oct

-99

Oct

-00

Oct

-01

Oct

-02

Oct

-03

Oct

-04

Oct

-05

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

HY YTW / HG YTW

Average HY YTW / HG YTW

Max 12/18/2008 = 2.7

Min 10/17/1997 = 1.2

Average = 1.7

Current 08/31/2015 = 2.1

1990s peak 10/16/1998 = 1.8

TMT peak 10/9/2002 = 2.4

pre-crisis trough 6/12/2007 = 1.3

19

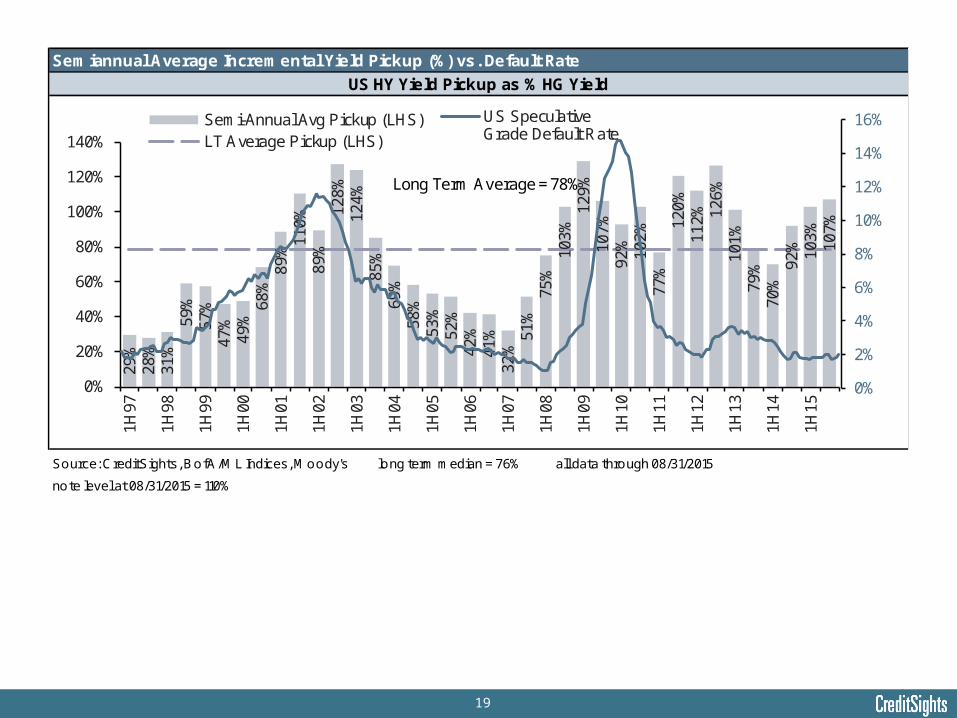

Source: CreditSights, BofA/ML Indices, Moody's long term median = 76% all data through 08/31/2015

note level at 08/31/2015 = 110%

Semiannual Average Incremental Yield Pickup (%) vs. Default Rate

US HY Yield Pickup as % HG Yield

29%

28%

31%

59%

57%

47%

49%

68%

89%

110%

89%

128%

124%

85%

69%

58%

53%

52%

42%

41%

32%

51%

75%

103%

129%

107%

92% 102%

77%

120%

112% 12

6%10

1%79

%70

%92

% 103%

107%

0%

20%

40%

60%

80%

100%

120%

140%1H

97

1H98

1H99

1H00

1H01

1H02

1H03

1H04

1H05

1H06

1H07

1H08

1H09

1H10

1H11

1H12

1H13

1H14

1H15

Semi-Annual Avg Pickup (LHS)LT Average Pickup (LHS)

0%

2%

4%

6%

8%

10%

12%

14%

16%US SpeculativeGrade Default Rate

Long Term Average = 78%

20

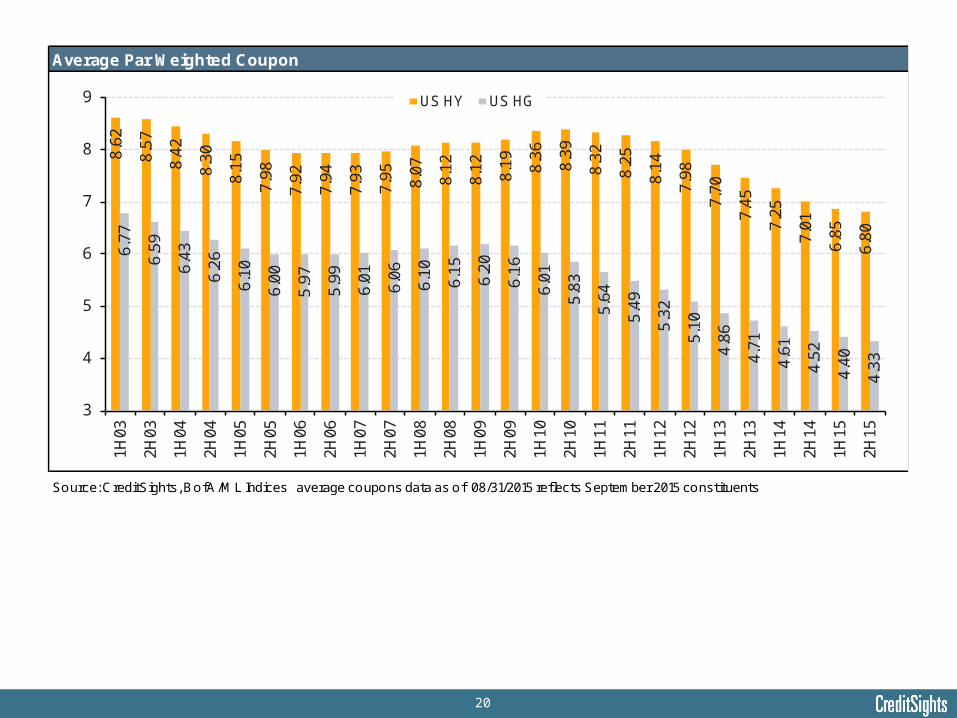

Average Par Weighted Coupon

Source: CreditSights, BofA/ML Indices average coupons data as of 08/31/2015 reflects September 2015 constituents

8.62

8.57

8.42

8.30

8.15

7.98

7.92

7.94

7.93

7.95 8.07

8.12

8.12

8.19 8.36

8.39

8.32

8.25

8.14

7.98

7.70

7.45

7.25

7.01

6.85

6.80

6.77

6.59

6.43

6.26

6.10

6.00

5.97

5.99

6.01

6.06

6.10

6.15

6.20

6.16

6.01

5.83

5.64

5.49

5.32

5.10

4.86

4.71

4.61

4.52

4.40

4.33

3

4

5

6

7

8

9

1H03

2H03

1H04

2H04

1H05

2H05

1H06

2H06

1H07

2H07

1H08

2H08

1H09

2H09

1H10

2H10

1H11

2H11

1H12

2H12

1H13

2H13

1H14

2H14

1H15

2H15

US HY US HG

21

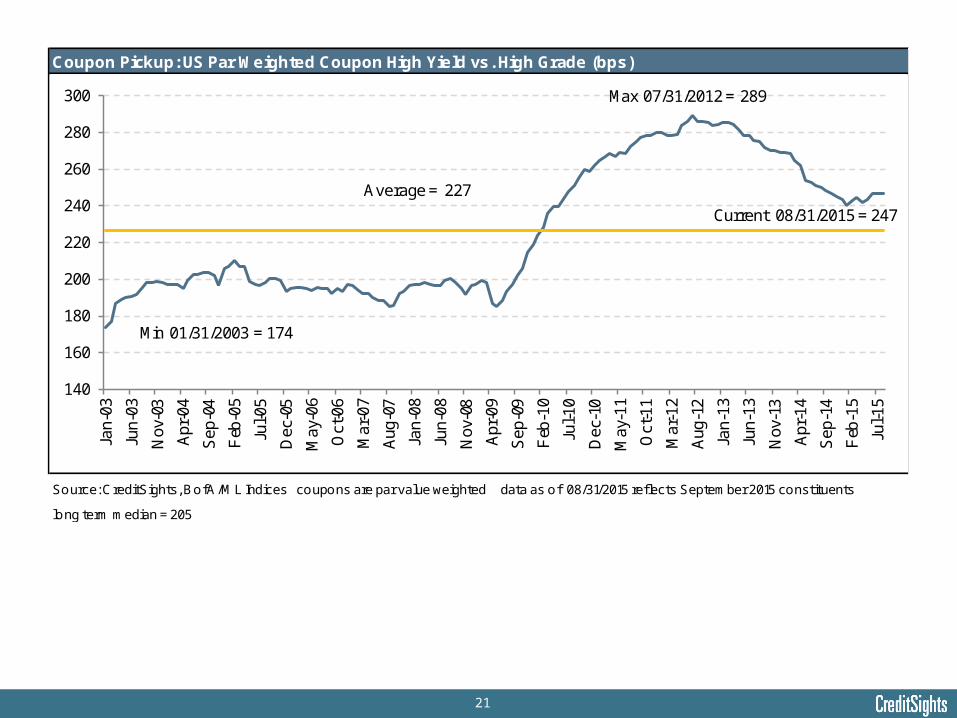

Coupon Pickup: US Par Weighted Coupon High Yield vs. High Grade (bps)

Source: CreditSights, BofA/ML Indices coupons are par value weighted data as of 08/31/2015 reflects September 2015 constituents

long term median = 205

140

160

180

200

220

240

260

280

300Ja

n-03

Jun-

03

Nov

-03

Apr

-04

Sep

-04

Feb

-05

Jul-0

5

Dec

-05

May

-06

Oct

-06

Mar

-07

Aug

-07

Jan-

08

Jun-

08

Nov

-08

Apr

-09

Sep

-09

Feb

-10

Jul-1

0

Dec

-10

May

-11

Oct

-11

Mar

-12

Aug

-12

Jan-

13

Jun-

13

Nov

-13

Apr

-14

Sep

-14

Feb

-15

Jul-1

5

Current 08/31/2015 = 247

Max 07/31/2012 = 289

Min 01/31/2003 = 174

Average = 227

22

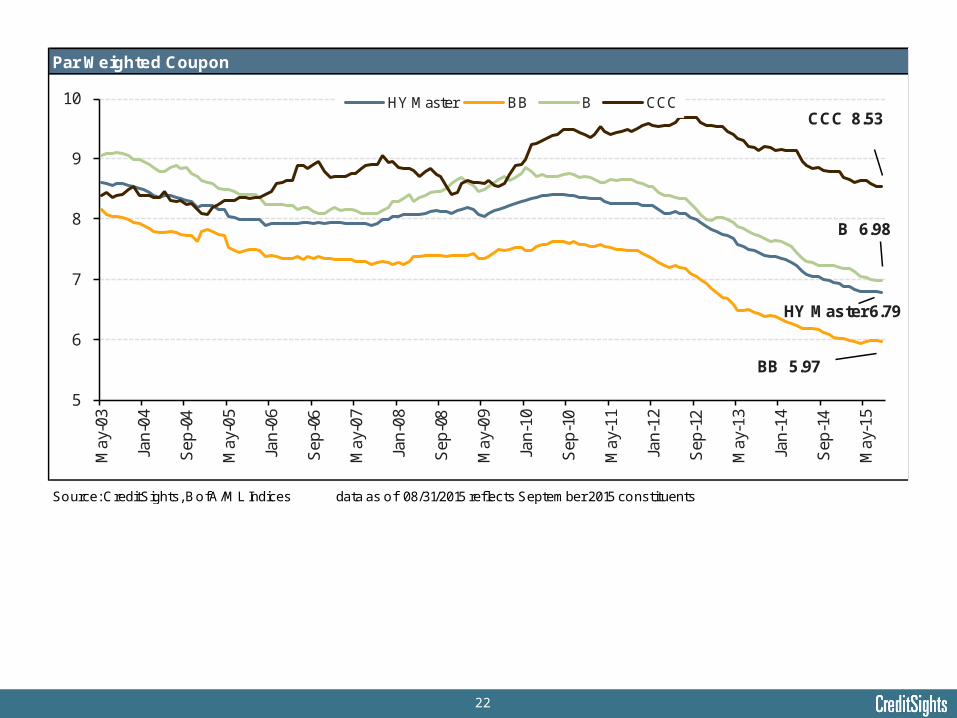

Par Weighted Coupon

Source: CreditSights, BofA/ML Indices data as of 08/31/2015 reflects September 2015 constituents

5

6

7

8

9

10M

ay-0

3

Jan-

04

Sep

-04

May

-05

Jan-

06

Sep

-06

May

-07

Jan-

08

Sep

-08

May

-09

Jan-

10

Sep

-10

May

-11

Jan-

12

Sep

-12

May

-13

Jan-

14

Sep

-14

May

-15

HY Master BB B CCC

HY Master 6.79

BB 5.97

B 6.98

CCC 8.53

23

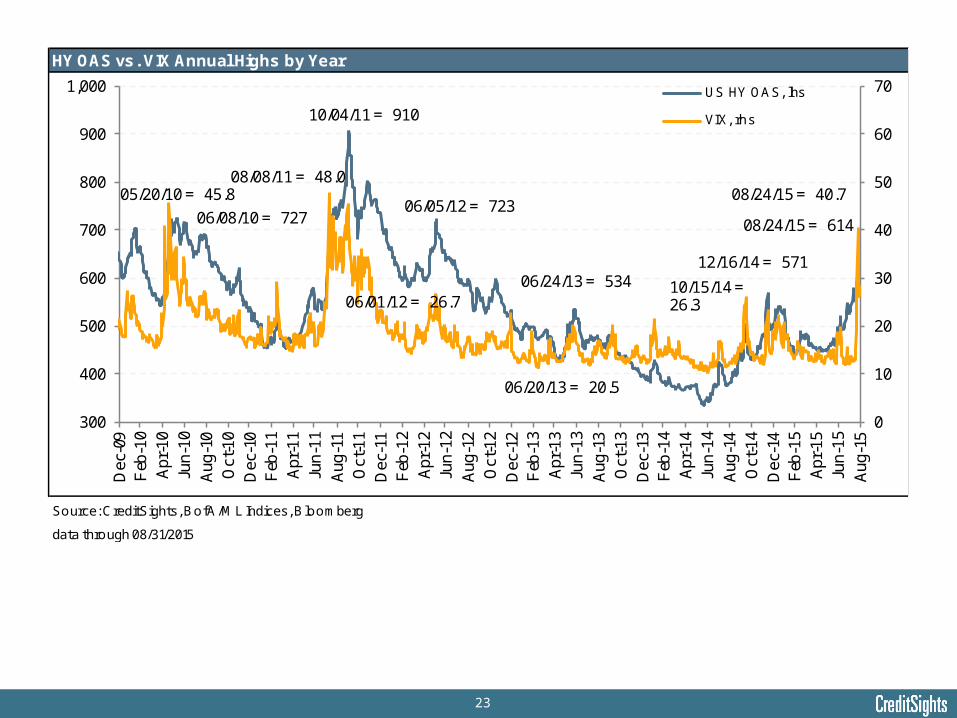

HY OAS vs. VIX Annual Highs by Year

Source: CreditSights, BofA/ML Indices, Bloomberg

data through 08/31/2015

0

10

20

30

40

50

60

70

300

400

500

600

700

800

900

1,000

Dec

-09

Feb

-10

Apr

-10

Jun-

10A

ug-1

0O

ct-1

0D

ec-1

0F

eb-1

1A

pr-1

1Ju

n-11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Apr

-12

Jun-

12A

ug-1

2O

ct-1

2D

ec-1

2F

eb-1

3A

pr-1

3Ju

n-13

Aug

-13

Oct

-13

Dec

-13

Feb

-14

Apr

-14

Jun-

14A

ug-1

4O

ct-1

4D

ec-1

4F

eb-1

5A

pr-1

5Ju

n-15

Aug

-15

US HY OAS, lhs

VIX, rhs

05/20/10 = 45.808/08/11 = 48.0

06/01/12 = 26.7

06/20/13 = 20.5

10/15/14 = 26.3

06/08/10 = 727

10/04/11 = 910

06/05/12 = 723

06/24/13 = 53412/16/14 = 571

08/24/15 = 614

08/24/15 = 40.7

24

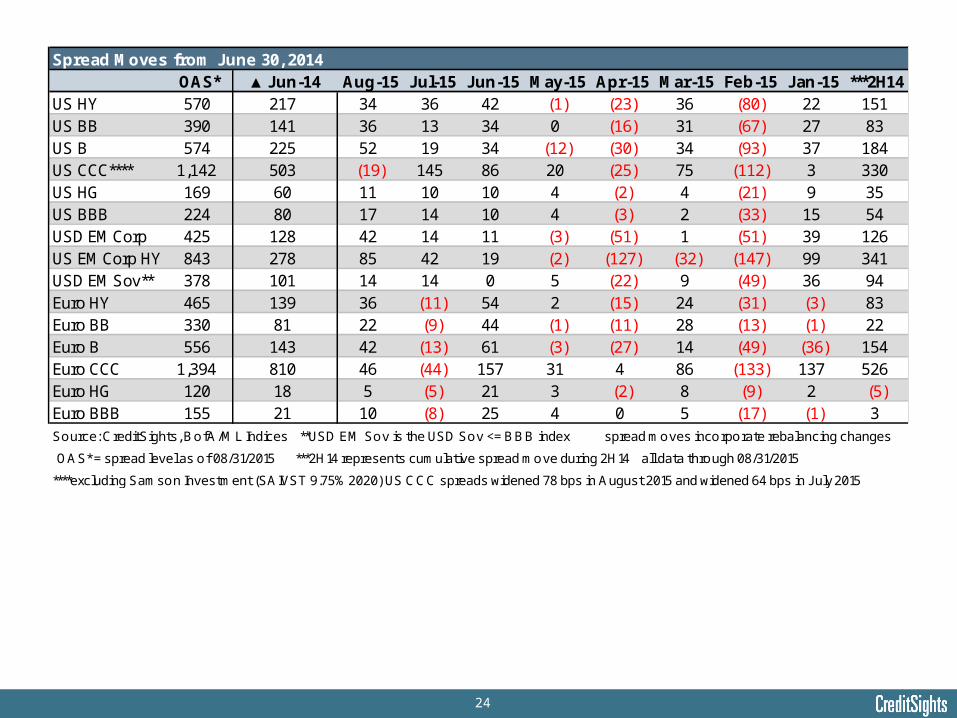

Spread Moves from June 30, 2014OAS* ▲Jun-14 Aug-15 Jul-15 Jun-15 May-15 Apr-15 Mar-15 Feb-15 Jan-15 ***2H14

US HY 570 217 34 36 42 (1) (23) 36 (80) 22 151US BB 390 141 36 13 34 0 (16) 31 (67) 27 83US B 574 225 52 19 34 (12) (30) 34 (93) 37 184US CCC**** 1,142 503 (19) 145 86 20 (25) 75 (112) 3 330US HG 169 60 11 10 10 4 (2) 4 (21) 9 35US BBB 224 80 17 14 10 4 (3) 2 (33) 15 54USD EM Corp 425 128 42 14 11 (3) (51) 1 (51) 39 126US EM Corp HY 843 278 85 42 19 (2) (127) (32) (147) 99 341USD EM Sov** 378 101 14 14 0 5 (22) 9 (49) 36 94Euro HY 465 139 36 (11) 54 2 (15) 24 (31) (3) 83Euro BB 330 81 22 (9) 44 (1) (11) 28 (13) (1) 22Euro B 556 143 42 (13) 61 (3) (27) 14 (49) (36) 154Euro CCC 1,394 810 46 (44) 157 31 4 86 (133) 137 526Euro HG 120 18 5 (5) 21 3 (2) 8 (9) 2 (5)Euro BBB 155 21 10 (8) 25 4 0 5 (17) (1) 3

Source: CreditSights, BofA/ML Indices **USD EM Sov is the USD Sov <= BBB index spread moves incorporate rebalancing changes

OAS* = spread level as of 08/31/2015 ***2H14 represents cumulative spread move during 2H14 all data through 08/31/2015

****excluding Samson Investment (SAIVST 9.75% 2020) US CCC spreads widened 78 bps in August 2015 and widened 64 bps in J uly 2015

25

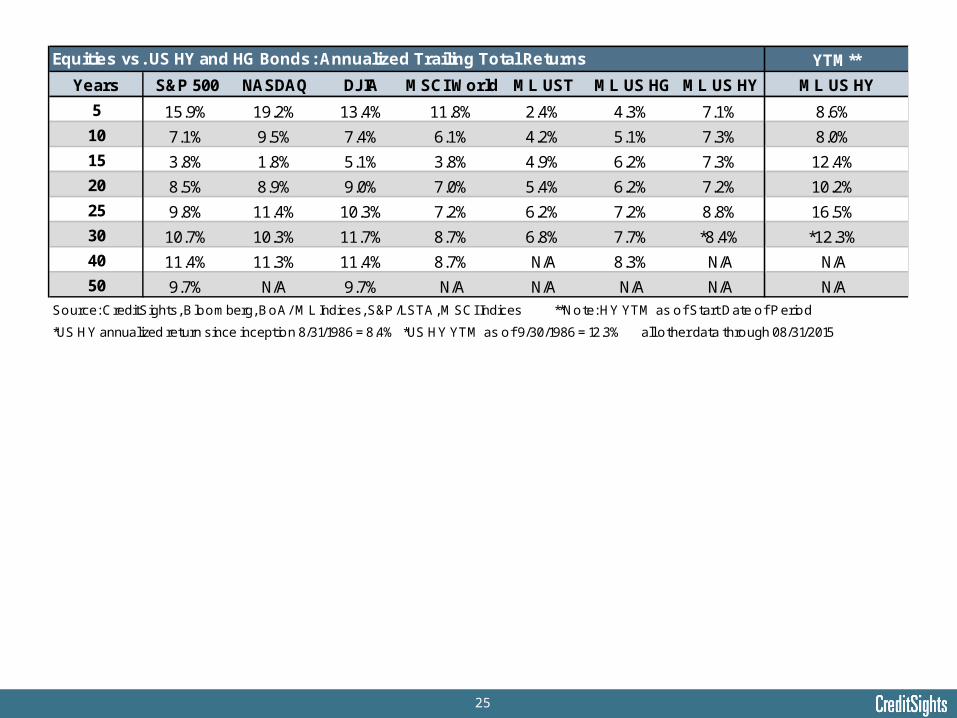

YTM**

Years S&P 500 NASDAQ DJIA MSCI World ML UST ML US HG ML US HY ML US HY

5 15.9% 19.2% 13.4% 11.8% 2.4% 4.3% 7.1% 8.6%

10 7.1% 9.5% 7.4% 6.1% 4.2% 5.1% 7.3% 8.0%

15 3.8% 1.8% 5.1% 3.8% 4.9% 6.2% 7.3% 12.4%

20 8.5% 8.9% 9.0% 7.0% 5.4% 6.2% 7.2% 10.2%

25 9.8% 11.4% 10.3% 7.2% 6.2% 7.2% 8.8% 16.5%

30 10.7% 10.3% 11.7% 8.7% 6.8% 7.7% *8.4% *12.3%

40 11.4% 11.3% 11.4% 8.7% N/A 8.3% N/A N/A

50 9.7% N/A 9.7% N/A N/A N/A N/A N/A

Source: CreditSights, Bloomberg, BoA/ ML Indices, S&P /LSTA, MSCI Indices **Note: HY YTM as of Start Date of P eriod

*US HY annualized return since inception 8/31/1986 = 8.4% *US HY YTM as of 9/30/1986 = 12.3% all other data through 08/31/2015

Equities vs. US HY and HG Bonds: Annualized Trailing Total Returns

26

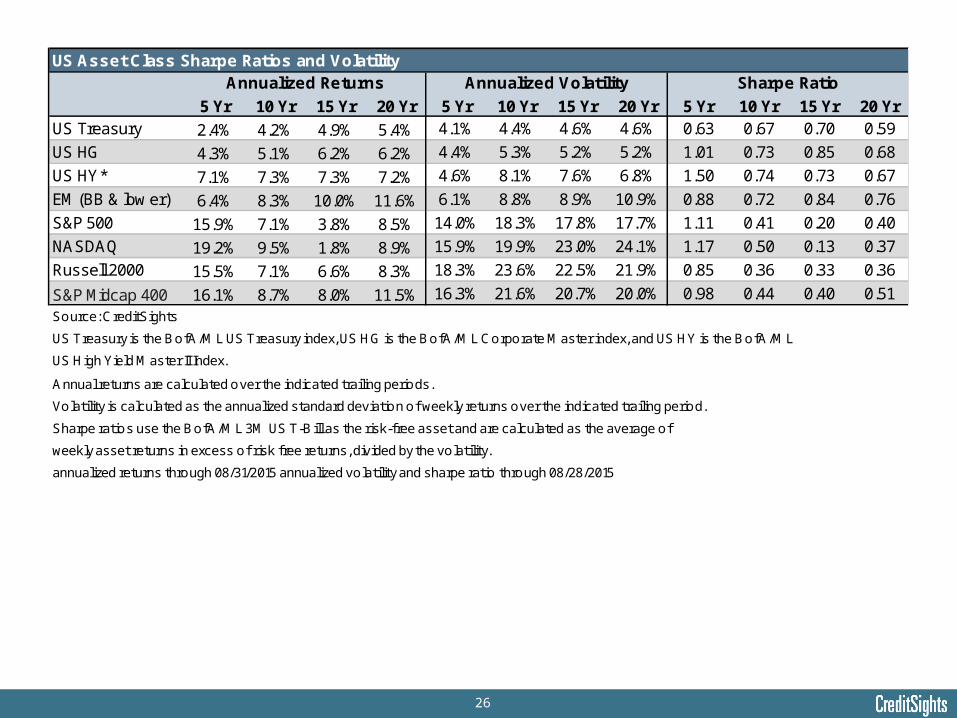

US Asset Class Sharpe Ratios and Volatility

5 Yr 10 Yr 15 Yr 20 Yr 5 Yr 10 Yr 15 Yr 20 Yr 5 Yr 10 Yr 15 Yr 20 YrUS Treasury 2.4% 4.2% 4.9% 5.4% 4.1% 4.4% 4.6% 4.6% 0.63 0.67 0.70 0.59

US HG 4.3% 5.1% 6.2% 6.2% 4.4% 5.3% 5.2% 5.2% 1.01 0.73 0.85 0.68

US HY* 7.1% 7.3% 7.3% 7.2% 4.6% 8.1% 7.6% 6.8% 1.50 0.74 0.73 0.67

EM (BB & low er) 6.4% 8.3% 10.0% 11.6% 6.1% 8.8% 8.9% 10.9% 0.88 0.72 0.84 0.76

S&P 500 15.9% 7.1% 3.8% 8.5% 14.0% 18.3% 17.8% 17.7% 1.11 0.41 0.20 0.40

NASDAQ 19.2% 9.5% 1.8% 8.9% 15.9% 19.9% 23.0% 24.1% 1.17 0.50 0.13 0.37

Russell 2000 15.5% 7.1% 6.6% 8.3% 18.3% 23.6% 22.5% 21.9% 0.85 0.36 0.33 0.36

S&P Midcap 400 16.1% 8.7% 8.0% 11.5% 16.3% 21.6% 20.7% 20.0% 0.98 0.44 0.40 0.51

Source: CreditSights

US Treasury is the BofA/ML US Treasury index, US HG is the BofA/ML Corporate Master index, and US HY is the BofA/ML

US High Yield Master II Index.

Annual returns are calculated over the indicated trailing periods.

Volatility is calculated as the annualized standard deviation of weekly returns over the indicated trailing period.

Sharpe ratios use the BofA/ML 3M US T-Bill as the risk-free asset and are calculated as the average of

weekly asset returns in excess of risk free returns, divided by the volatility.

annualized returns through 08/31/2015 annualized volatility and sharpe ratio through 08/28/2015

Annualized Returns Annualized Volatility Sharpe Ratio

27

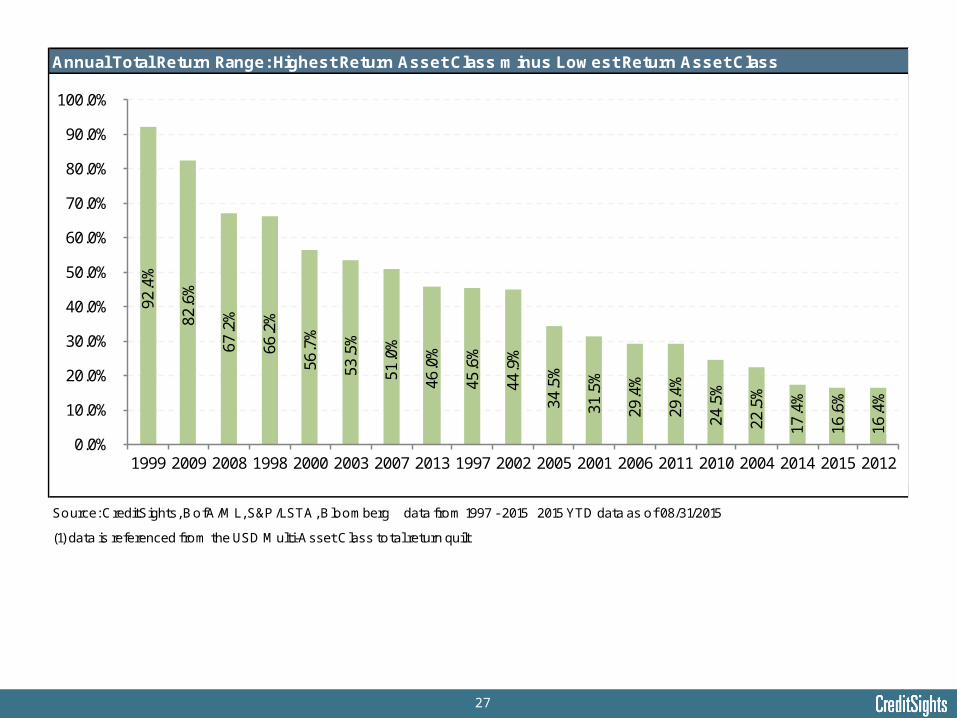

Annual Total Return Range: Highest Return Asset Class minus Lowest Return Asset Class

Source: CreditSights, BofA/ML, S&P /LSTA, Bloomberg data from 1997 - 2015 2015 YTD data as of 08/31/2015

(1) data is referenced from the USD Multi-Asset Class total return quilt

92.4

%

82.6

%

67.2

%

66.2

%

56.7

%

53.5

%

51.0

%

46.0

%

45.6

%

44.9

%

34.5

%

31.5

%

29.4

%

29.4

%

24.5

%

22.5

%

17.4

%

16.6

%

16.4

%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1999 2009 2008 1998 2000 2003 2007 2013 1997 2002 2005 2001 2006 2011 2010 2004 2014 2015 2012

28

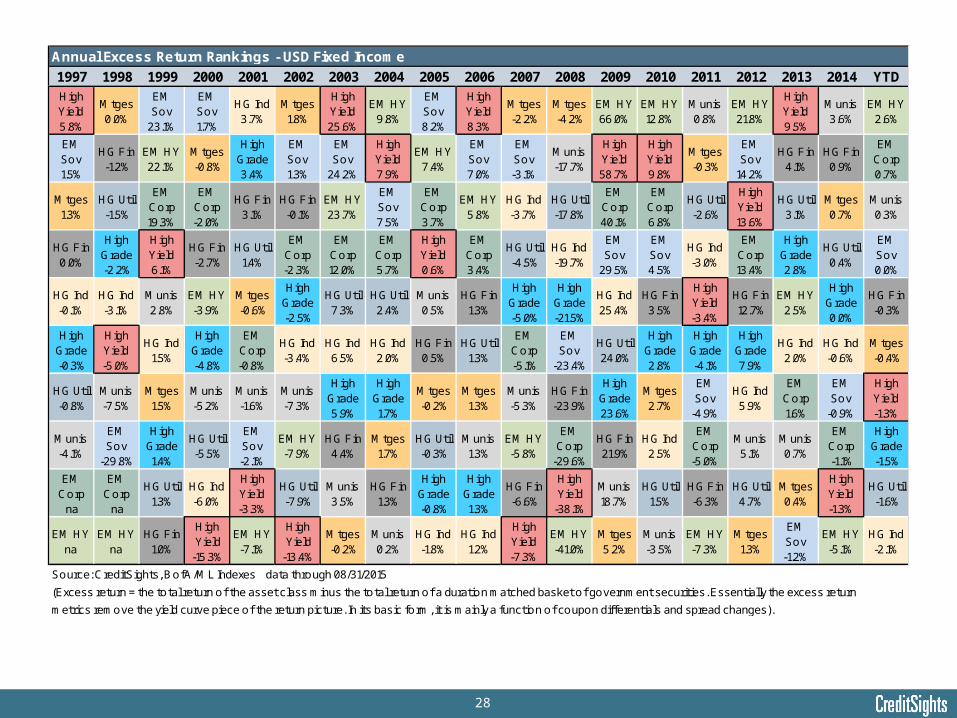

Annual Excess Return Rankings - USD Fixed Income

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

High Yield 5.8%

Mtges 0.0%

EM Sov

23.1%

EM Sov 1.7%

HG Ind 3.7%

Mtges 1.8%

High Yield 25.6%

EM HY 9.8%

EM Sov 8.2%

High Yield 8.3%

Mtges -2.2%

Mtges -4.2%

EM HY 66.0%

EM HY 12.8%

Munis 0.8%

EM HY 21.8%

High Yield 9.5%

Munis 3.6%

EM HY 2.6%

EM Sov 1.5%

HG Fin -1.2%

EM HY 22.1%

Mtges -0.8%

High Grade 3.4%

EM Sov 1.3%

EM Sov

24.2%

High Yield 7.9%

EM HY 7.4%

EM Sov 7.0%

EM Sov -3.1%

Munis -17.7%

High Yield 58.7%

High Yield 9.8%

Mtges -0.3%

EM Sov

14.2%

HG Fin 4.1%

HG Fin 0.9%

EM Corp 0.7%

Mtges 1.3%

HG Util -1.5%

EM Corp 19.3%

EM Corp -2.0%

HG Fin 3.1%

HG Fin -0.1%

EM HY 23.7%

EM Sov 7.5%

EM Corp 3.7%

EM HY 5.8%

HG Ind -3.7%

HG Util -17.8%

EM Corp 40.1%

EM Corp 6.8%

HG Util -2.6%

High Yield 13.6%

HG Util 3.1%

Mtges 0.7%

Munis 0.3%

HG Fin 0.0%

High Grade -2.2%

High Yield 6.1%

HG Fin -2.7%

HG Util 1.4%

EM Corp -2.3%

EM Corp 12.0%

EM Corp 5.7%

High Yield 0.6%

EM Corp 3.4%

HG Util -4.5%

HG Ind -19.7%

EM Sov

29.5%

EM Sov 4.5%

HG Ind -3.0%

EM Corp 13.4%

High Grade 2.8%

HG Util 0.4%

EM Sov 0.0%

HG Ind -0.1%

HG Ind -3.1%

Munis 2.8%

EM HY -3.9%

Mtges -0.6%

High Grade -2.5%

HG Util 7.3%

HG Util 2.4%

Munis 0.5%

HG Fin 1.3%

High Grade -5.0%

High Grade -21.5%

HG Ind 25.4%

HG Fin 3.5%

High Yield -3.4%

HG Fin 12.7%

EM HY 2.5%

High Grade 0.0%

HG Fin -0.3%

High Grade -0.3%

High Yield -5.0%

HG Ind 1.5%

High Grade -4.8%

EM Corp -0.8%

HG Ind -3.4%

HG Ind 6.5%

HG Ind 2.0%

HG Fin 0.5%

HG Util 1.3%

EM Corp -5.1%

EM Sov

-23.4%

HG Util 24.0%

High Grade 2.8%

High Grade -4.1%

High Grade 7.9%

HG Ind 2.0%

HG Ind -0.6%

Mtges -0.4%

HG Util -0.8%

Munis -7.5%

Mtges 1.5%

Munis -5.2%

Munis -1.6%

Munis -7.3%

High Grade 5.9%

High Grade 1.7%

Mtges -0.2%

Mtges 1.3%

Munis -5.3%

HG Fin -23.9%

High Grade 23.6%

Mtges 2.7%

EM Sov

-4.9%

HG Ind 5.9%

EM Corp 1.6%

EM Sov

-0.9%

High Yield -1.3%

Munis -4.1%

EM Sov

-29.8%

High Grade 1.4%

HG Util -5.5%

EM Sov -2.1%

EM HY -7.9%

HG Fin 4.4%

Mtges 1.7%

HG Util -0.3%

Munis 1.3%

EM HY -5.8%

EM Corp

-29.6%

HG Fin 21.9%

HG Ind 2.5%

EM Corp -5.0%

Munis 5.1%

Munis 0.7%

EM Corp -1.1%

High Grade -1.5%

EM Corp

na

EM Corp

na

HG Util 1.3%

HG Ind -6.0%

High Yield -3.3%

HG Util -7.9%

Munis 3.5%

HG Fin 1.3%

High Grade -0.8%

High Grade 1.3%

HG Fin -6.6%

High Yield

-38.1%

Munis 18.7%

HG Util 1.5%

HG Fin -6.3%

HG Util 4.7%

Mtges 0.4%

High Yield -1.3%

HG Util -1.6%

EM HY na

EM HY na

HG Fin 1.0%

High Yield

-15.3%

EM HY -7.1%

High Yield

-13.4%

Mtges -0.2%

Munis 0.2%

HG Ind -1.8%

HG Ind 1.2%

High Yield -7.3%

EM HY -41.0%

Mtges 5.2%

Munis -3.5%

EM HY -7.3%

Mtges 1.3%

EM Sov -1.2%

EM HY -5.1%

HG Ind -2.1%

Source: CreditSights, BofA/ML Indexes data through 08/31/2015

(Excess return = the total return of the asset class minus the total return of a duration matched basket of government securities. Essentially the excess return

metrics remove the yield curve piece of the return picture. In its basic form, it is mainly a function of coupon differentials and spread changes).

29

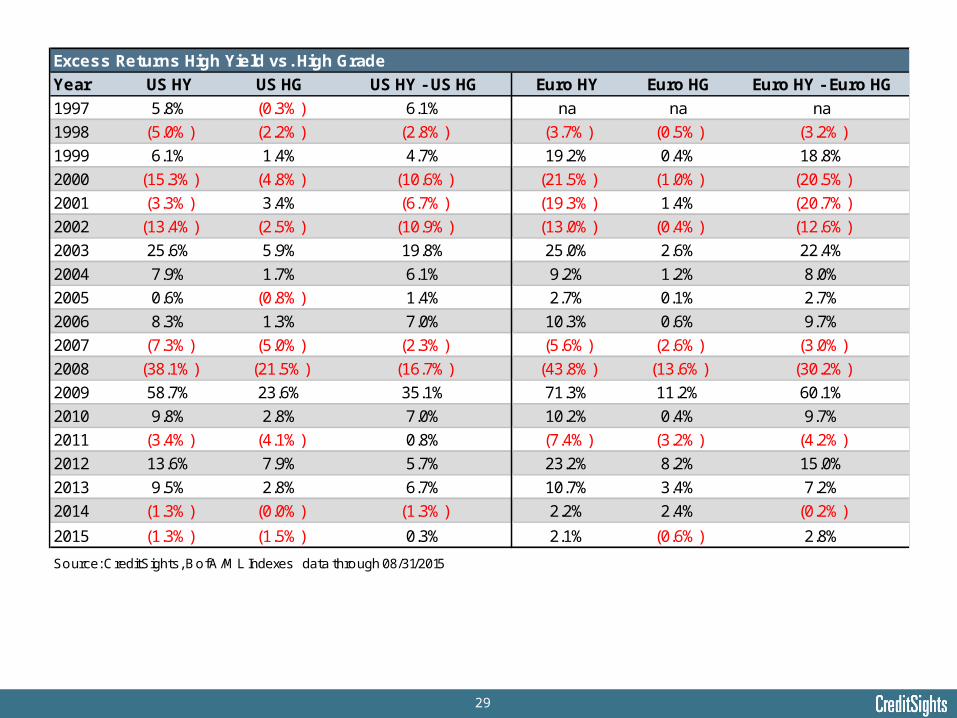

Excess Returns High Yield vs. High Grade

Year US HY US HG US HY - US HG Euro HY Euro HG Euro HY - Euro HG

1997 5.8% (0.3%) 6.1% na na na

1998 (5.0%) (2.2%) (2.8%) (3.7%) (0.5%) (3.2%)

1999 6.1% 1.4% 4.7% 19.2% 0.4% 18.8%

2000 (15.3%) (4.8%) (10.6%) (21.5%) (1.0%) (20.5%)

2001 (3.3%) 3.4% (6.7%) (19.3%) 1.4% (20.7%)

2002 (13.4%) (2.5%) (10.9%) (13.0%) (0.4%) (12.6%)

2003 25.6% 5.9% 19.8% 25.0% 2.6% 22.4%

2004 7.9% 1.7% 6.1% 9.2% 1.2% 8.0%

2005 0.6% (0.8%) 1.4% 2.7% 0.1% 2.7%

2006 8.3% 1.3% 7.0% 10.3% 0.6% 9.7%

2007 (7.3%) (5.0%) (2.3%) (5.6%) (2.6%) (3.0%)

2008 (38.1%) (21.5%) (16.7%) (43.8%) (13.6%) (30.2%)

2009 58.7% 23.6% 35.1% 71.3% 11.2% 60.1%

2010 9.8% 2.8% 7.0% 10.2% 0.4% 9.7%

2011 (3.4%) (4.1%) 0.8% (7.4%) (3.2%) (4.2%)

2012 13.6% 7.9% 5.7% 23.2% 8.2% 15.0%

2013 9.5% 2.8% 6.7% 10.7% 3.4% 7.2%

2014 (1.3%) (0.0%) (1.3%) 2.2% 2.4% (0.2%)

2015 (1.3%) (1.5%) 0.3% 2.1% (0.6%) 2.8%

Source: CreditSights, BofA/ML Indexes data through 08/31/2015

30

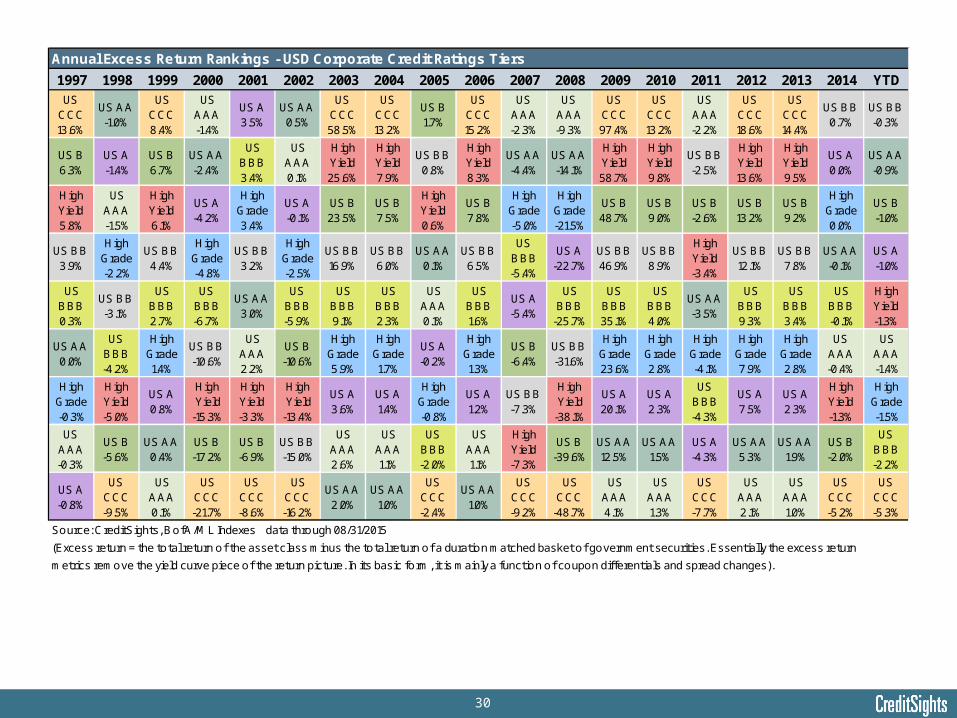

Annual Excess Return Rankings - USD Corporate Credit Ratings Tiers

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

US CCC 13.6%

US AA -1.0%

US CCC 8.4%

US AAA -1.4%

US A 3.5%

US AA 0.5%

US CCC 58.5%

US CCC 13.2%

US B 1.7%

US CCC 15.2%

US AAA -2.3%

US AAA -9.3%

US CCC 97.4%

US CCC 13.2%

US AAA -2.2%

US CCC 18.6%

US CCC 14.4%

US BB 0.7%

US BB -0.3%

US B 6.3%

US A -1.4%

US B 6.7%

US AA -2.4%

US BBB 3.4%

US AAA 0.1%

High Yield 25.6%

High Yield 7.9%

US BB 0.8%

High Yield 8.3%

US AA -4.4%

US AA -14.1%

High Yield 58.7%

High Yield 9.8%

US BB -2.5%

High Yield 13.6%

High Yield 9.5%

US A 0.0%

US AA -0.9%

High Yield 5.8%

US AAA -1.5%

High Yield 6.1%

US A -4.2%

High Grade 3.4%

US A -0.1%

US B 23.5%

US B 7.5%

High Yield 0.6%

US B 7.8%

High Grade -5.0%

High Grade -21.5%

US B 48.7%

US B 9.0%

US B -2.6%

US B 13.2%

US B 9.2%

High Grade 0.0%

US B -1.0%

US BB 3.9%

High Grade -2.2%

US BB 4.4%

High Grade -4.8%

US BB 3.2%

High Grade -2.5%

US BB 16.9%

US BB 6.0%

US AA 0.1%

US BB 6.5%

US BBB -5.4%

US A -22.7%

US BB 46.9%

US BB 8.9%

High Yield -3.4%

US BB 12.1%

US BB 7.8%

US AA -0.1%

US A -1.0%

US BBB 0.3%

US BB -3.1%

US BBB 2.7%

US BBB -6.7%

US AA 3.0%

US BBB -5.9%

US BBB 9.1%

US BBB 2.3%

US AAA 0.1%

US BBB 1.6%

US A -5.4%

US BBB

-25.7%

US BBB 35.1%

US BBB 4.0%

US AA -3.5%

US BBB 9.3%

US BBB 3.4%

US BBB -0.1%

High Yield -1.3%

US AA 0.0%

US BBB -4.2%

High Grade 1.4%

US BB -10.6%

US AAA 2.2%

US B -10.6%

High Grade 5.9%

High Grade 1.7%

US A -0.2%

High Grade 1.3%

US B -6.4%

US BB -31.6%

High Grade 23.6%

High Grade 2.8%

High Grade -4.1%

High Grade 7.9%

High Grade 2.8%

US AAA -0.4%

US AAA -1.4%

High Grade -0.3%

High Yield -5.0%

US A 0.8%

High Yield

-15.3%

High Yield -3.3%

High Yield

-13.4%

US A 3.6%

US A 1.4%

High Grade -0.8%

US A 1.2%

US BB -7.3%

High Yield

-38.1%

US A 20.1%

US A 2.3%

US BBB -4.3%

US A 7.5%

US A 2.3%

High Yield -1.3%

High Grade -1.5%

US AAA -0.3%

US B -5.6%

US AA 0.4%

US B -17.2%

US B -6.9%

US BB -15.0%

US AAA 2.6%

US AAA 1.1%

US BBB -2.0%

US AAA 1.1%

High Yield -7.3%

US B -39.6%

US AA 12.5%

US AA 1.5%

US A -4.3%

US AA 5.3%

US AA 1.9%

US B -2.0%

US BBB -2.2%

US A -0.8%

US CCC -9.5%

US AAA 0.1%

US CCC -21.7%

US CCC -8.6%

US CCC -16.2%

US AA 2.0%

US AA 1.0%

US CCC -2.4%

US AA 1.0%

US CCC -9.2%

US CCC

-48.7%

US AAA 4.1%

US AAA 1.3%

US CCC -7.7%

US AAA 2.1%

US AAA 1.0%

US CCC -5.2%

US CCC -5.3%

Source: CreditSights, BofA/ML Indexes data through 08/31/2015

(Excess return = the total return of the asset class minus the total return of a duration matched basket of government securities. Essentially the excess return

metrics remove the yield curve piece of the return picture. In its basic form, it is mainly a function of coupon differentials and spread changes).

31

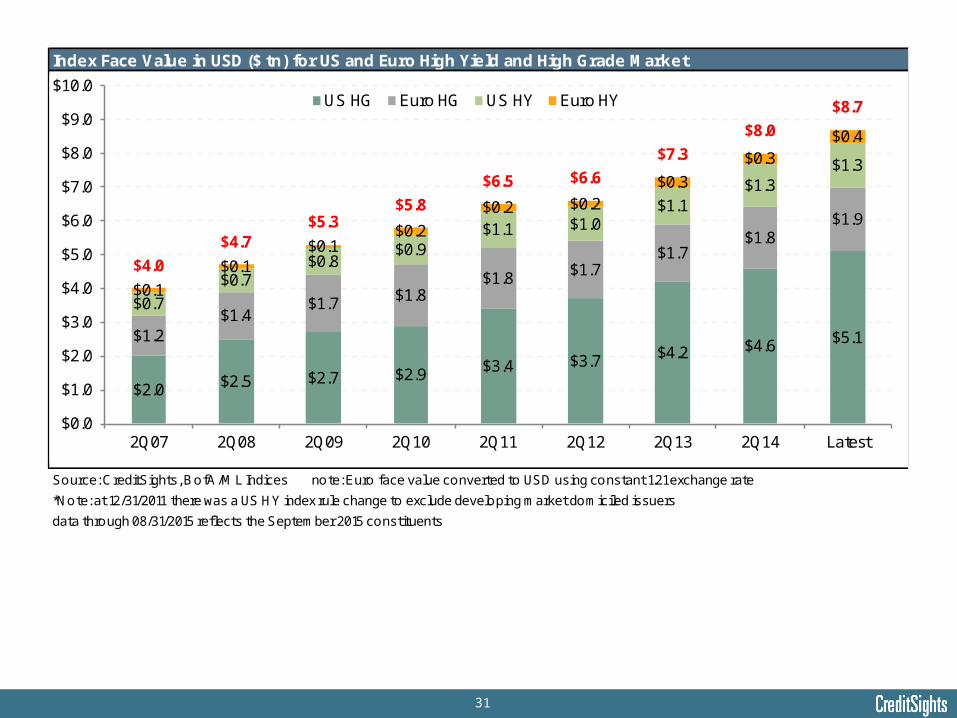

Index Face Value in USD ($ tn) for US and Euro High Yield and High Grade Market

Source: CreditSights, BofA/ML Indices note: Euro face value converted to USD using constant 1.21 exchange rate

*Note: at 12/31/2011 there was a US HY index rule change to exclude developing market domiciled issuers

data through 08/31/2015 reflects the September 2015 constituents

$2.0 $2.5 $2.7 $2.9 $3.4 $3.7 $4.2 $4.6 $5.1$1.2$1.4

$1.7 $1.8$1.8 $1.7

$1.7$1.8

$1.9

$0.7

$0.7$0.8

$0.9$1.1 $1.0

$1.1$1.3

$1.3

$0.1

$0.1$0.1

$0.2

$0.2 $0.2$0.3

$0.3$0.4

$4.0

$4.7$5.3

$5.8

$6.5 $6.6

$7.3

$8.0

$8.7

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

2Q07 2Q08 2Q09 2Q10 2Q11 2Q12 2Q13 2Q14 Latest

US HG Euro HG US HY Euro HY

32

US HG Growth by Credit Tier ($ bn)

Source: CreditSights, BofA/ML Indices note: based on Face Value data through 08/31/2015 reflects September 2015 constituents

$0.72 $0.84 $1.02 $1.14 $1.30$1.60 $1.85 $2.05 $2.33$0.79

$1.04$1.19

$1.26$1.44

$1.66$1.81

$1.92

$2.13

$0.44

$0.53$0.43

$0.51

$0.62

$0.43

$0.49$0.55

$0.58

$0.10

$0.12$0.02

$0.03

$0.06$0.05

$0.03

$0.04

$0.06

$2.05

$2.53 $2.66$2.95

$3.41$3.74

$4.18

$4.57

$5.11

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

2Q07 2Q08 2Q09 2Q10 2Q11 2Q12 2Q13 2Q14 latest

BBB A AA AAA

33

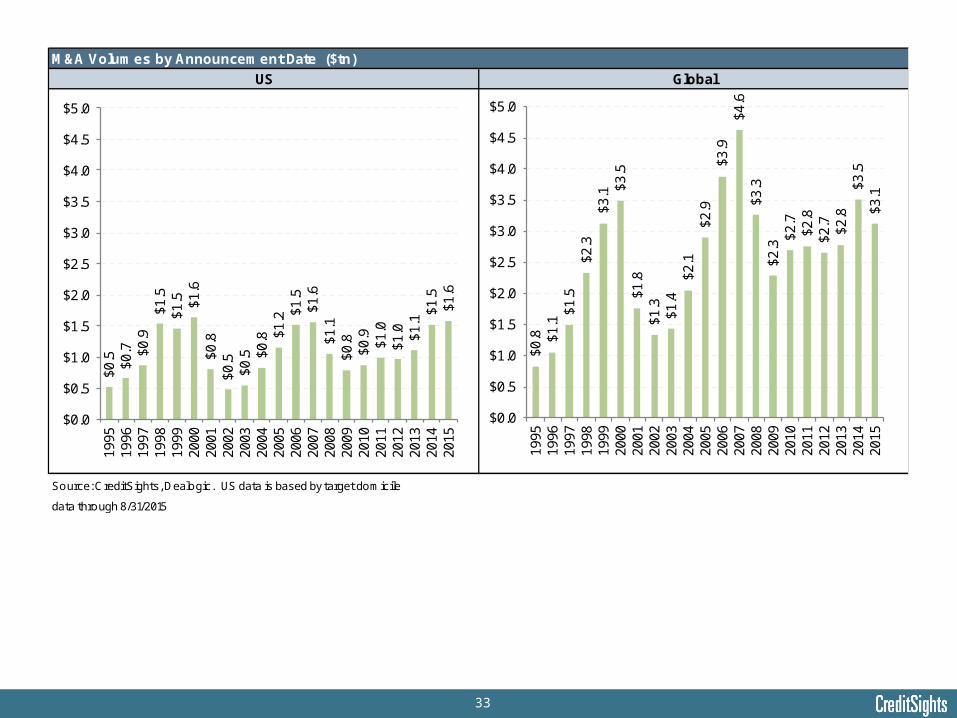

M&A Volumes by Announcement Date ($tn)

Source: CreditSights, Dealogic. US data is based by target domicile

data through 8/31/2015

US Global

$0.5 $0

.7 $0.9

$1.5

$1.5 $1

.6$0

.8$0

.5$0

.5 $0.8 $1

.2 $1.5

$1.6

$1.1

$0.8

$0.9

$1.0

$1.0 $1

.1$1

.5$1

.6

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.019

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

15

$0.8 $1

.1$1

.5$2

.3$3

.1 $3.5

$1.8

$1.3

$1.4

$2.1

$2.9

$3.9

$4.6

$3.3

$2.3

$2.7

$2.8

$2.7 $2

.8$3

.5$3

.1

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

34

US HY Growth by Credit Tier ($ bn)

Source: CreditSights, BofA/ML Indices note: based on Face Value data through 08/31/2015 reflects September 2015 constituents

$0.13 $0.14$0.24 $0.19 $0.18 $0.18 $0.21 $0.23 $0.22

$0.28 $0.31$0.23 $0.36 $0.41 $0.40

$0.46 $0.49 $0.52$0.27

$0.28 $0.33$0.36

$0.48 $0.42

$0.48$0.57

$0.59

$0.68$0.74

$0.79

$0.90

$1.06$1.00

$1.15

$1.29$1.34

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2Q07 2Q08 2Q09 2Q10 2Q11 2Q12 2Q13 2Q14 latest

CCC B BB

35

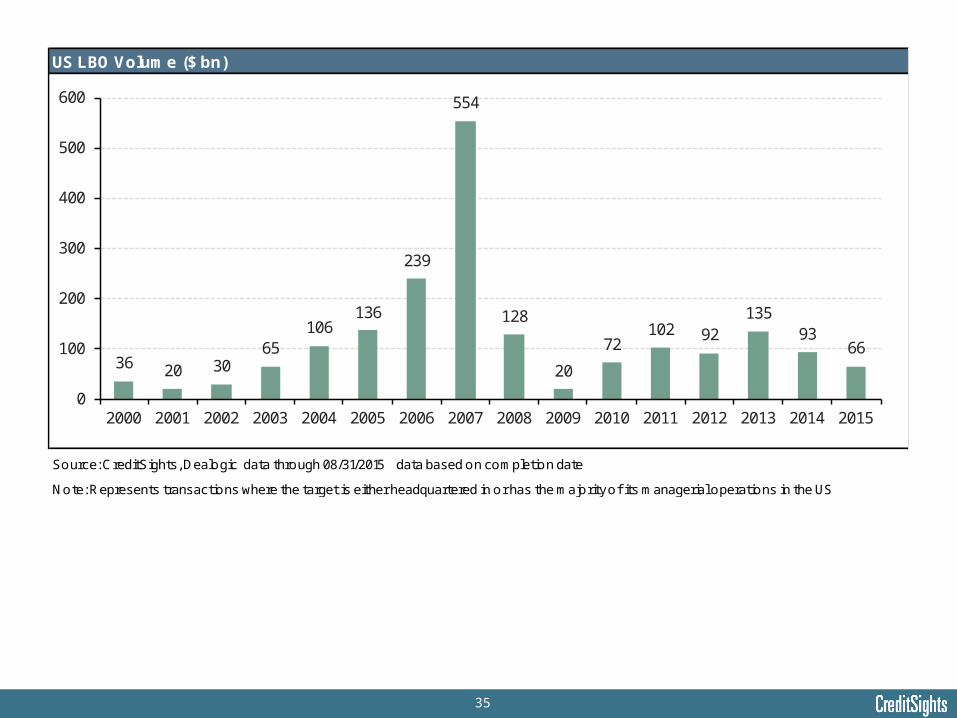

US LBO Volume ($ bn)

Source: CreditSights, Dealogic data through 08/31/2015 data based on completion date

Note: Represents transactions where the target is either headquartered in or has the majority of its managerial operations in the US

36 20 3065

106136

239

554

128

20

72102 92

13593

66

0

100

200

300

400

500

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

36

HY Net Debt to LTM EBITDA Trends

Source: CreditSights, CreditSights Ratings, FactSet

Note: average excludes the top and bottom 5% to mitigate outliers

1.3x 1.2x1.5x 1.4x 1.5x 1.5x 1.6x

2.8x 2.9x3.4x 3.5x

3.6x 3.8x 4.0x

4.9x 5.0x

5.8x 5.9x

6.8x 7.0x7.4x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

2010 2011 2012 2013 2014 1Q15 2Q15

Median of Low Quartile Median Median of High Quartile

37

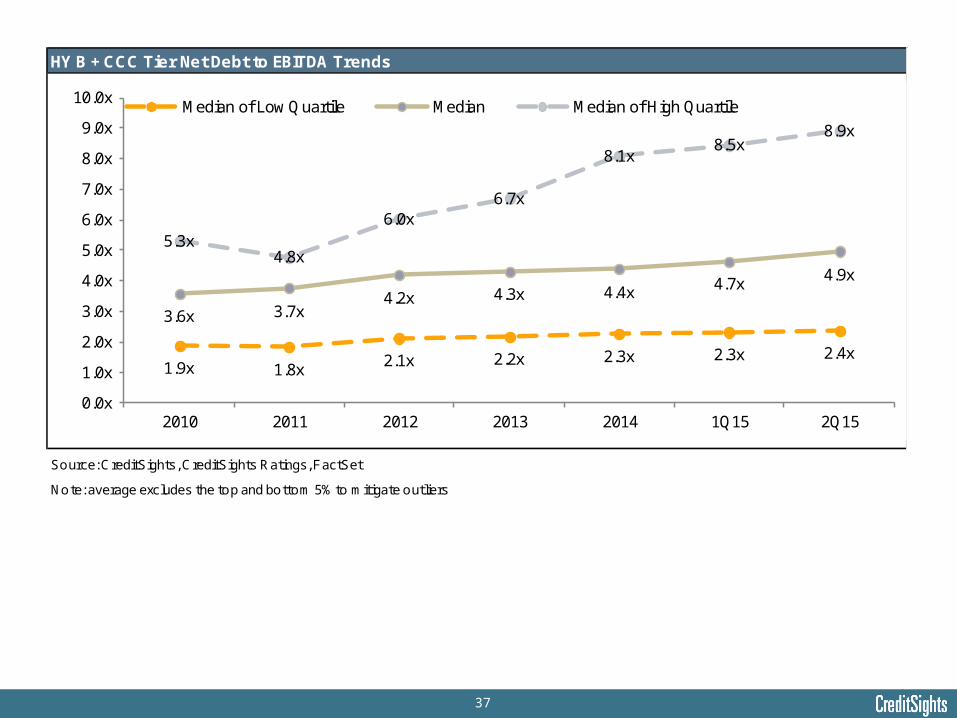

HY B + CCC Tier Net Debt to EBITDA Trends

Source: CreditSights, CreditSights Ratings, FactSet

Note: average excludes the top and bottom 5% to mitigate outliers

1.9x 1.8x2.1x 2.2x 2.3x 2.3x 2.4x

3.6x 3.7x4.2x 4.3x 4.4x 4.7x 4.9x

5.3x4.8x

6.0x6.7x

8.1x8.5x

8.9x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

2010 2011 2012 2013 2014 1Q15 2Q15

Median of Low Quartile Median Median of High Quartile

38

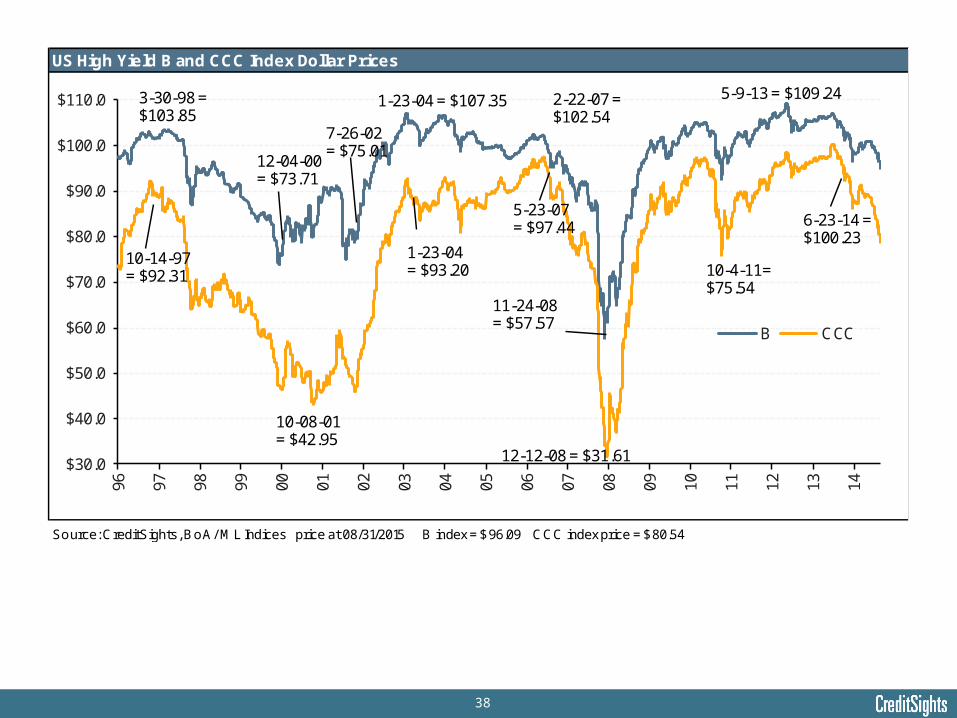

US High Yield B and CCC Index Dollar Prices

Source: CreditSights, BoA/ ML Indices price at 08/31/2015 B index = $96.09 CCC index price = $80.54

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

$100.0

$110.096 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

B CCC

5-9-13 = $109.24

11-24-08 = $57.57

6-23-14 = $100.23

12-12-08 = $31.61

10-08-01= $42.95

12-04-00 = $73.71

1-23-04 = $107.35

5-23-07 = $97.44

1-23-04 = $93.20

7-26-02 = $75.01

3-30-98 = $103.85

10-14-97 = $92.31

2-22-07 = $102.54

10-4-11= $75.54

39

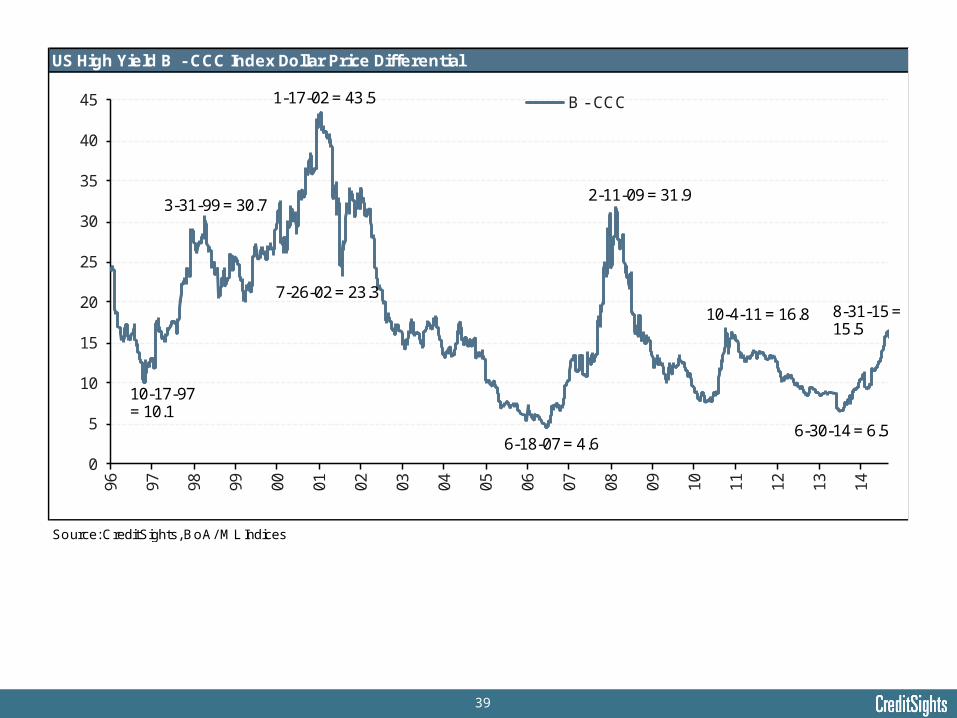

US High Yield B - CCC Index Dollar Price Differential

Source: CreditSights, BoA/ ML Indices

0

5

10

15

20

25

30

35

40

4596 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

B - CCC

10-17-97 = 10.1

3-31-99 = 30.7

1-17-02 = 43.5

2-11-09 = 31.9

6-18-07 = 4.6

8-31-15 = 15.5

7-26-02 = 23.310-4-11 = 16.8

6-30-14 = 6.5

40

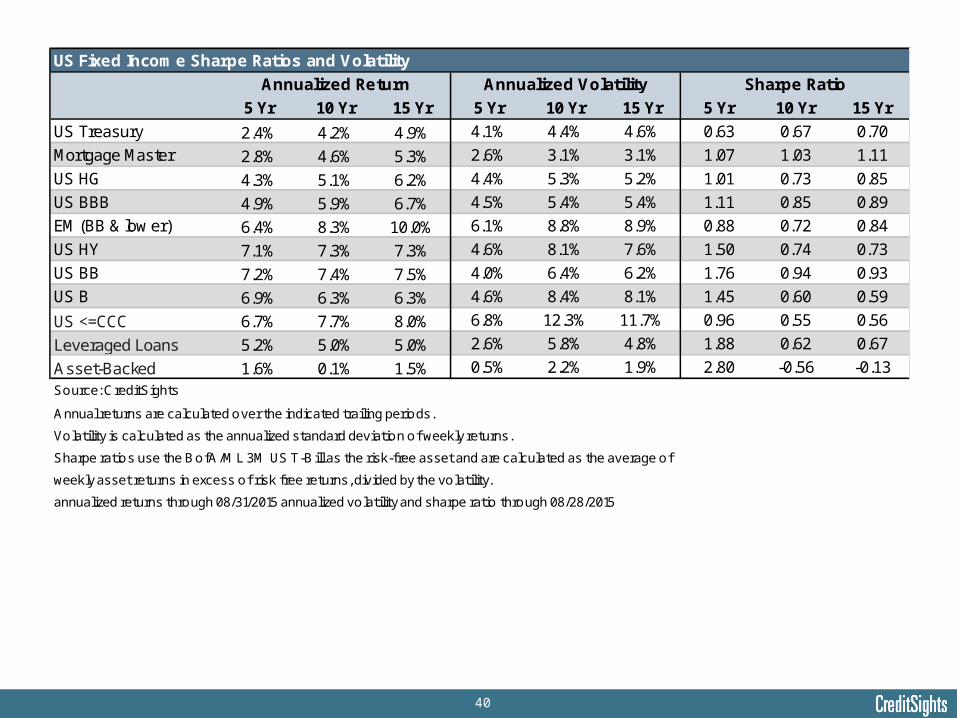

US Fixed Income Sharpe Ratios and Volatility

5 Yr 10 Yr 15 Yr 5 Yr 10 Yr 15 Yr 5 Yr 10 Yr 15 Yr

US Treasury 2.4% 4.2% 4.9% 4.1% 4.4% 4.6% 0.63 0.67 0.70

Mortgage Master 2.8% 4.6% 5.3% 2.6% 3.1% 3.1% 1.07 1.03 1.11

US HG 4.3% 5.1% 6.2% 4.4% 5.3% 5.2% 1.01 0.73 0.85

US BBB 4.9% 5.9% 6.7% 4.5% 5.4% 5.4% 1.11 0.85 0.89

EM (BB & low er) 6.4% 8.3% 10.0% 6.1% 8.8% 8.9% 0.88 0.72 0.84

US HY 7.1% 7.3% 7.3% 4.6% 8.1% 7.6% 1.50 0.74 0.73

US BB 7.2% 7.4% 7.5% 4.0% 6.4% 6.2% 1.76 0.94 0.93

US B 6.9% 6.3% 6.3% 4.6% 8.4% 8.1% 1.45 0.60 0.59

US <=CCC 6.7% 7.7% 8.0% 6.8% 12.3% 11.7% 0.96 0.55 0.56

Leveraged Loans 5.2% 5.0% 5.0% 2.6% 5.8% 4.8% 1.88 0.62 0.67

Asset-Backed 1.6% 0.1% 1.5% 0.5% 2.2% 1.9% 2.80 -0.56 -0.13

Source: CreditSights

Annual returns are calculated over the indicated trailing periods.

Volatility is calculated as the annualized standard deviation of weekly returns.

Sharpe ratios use the BofA/ML 3M US T-Bill as the risk-free asset and are calculated as the average of

weekly asset returns in excess of risk free returns, divided by the volatility.

annualized returns through 08/31/2015 annualized volatility and sharpe ratio through 08/28/2015

Annualized Return Annualized Volatility Sharpe Ratio

41

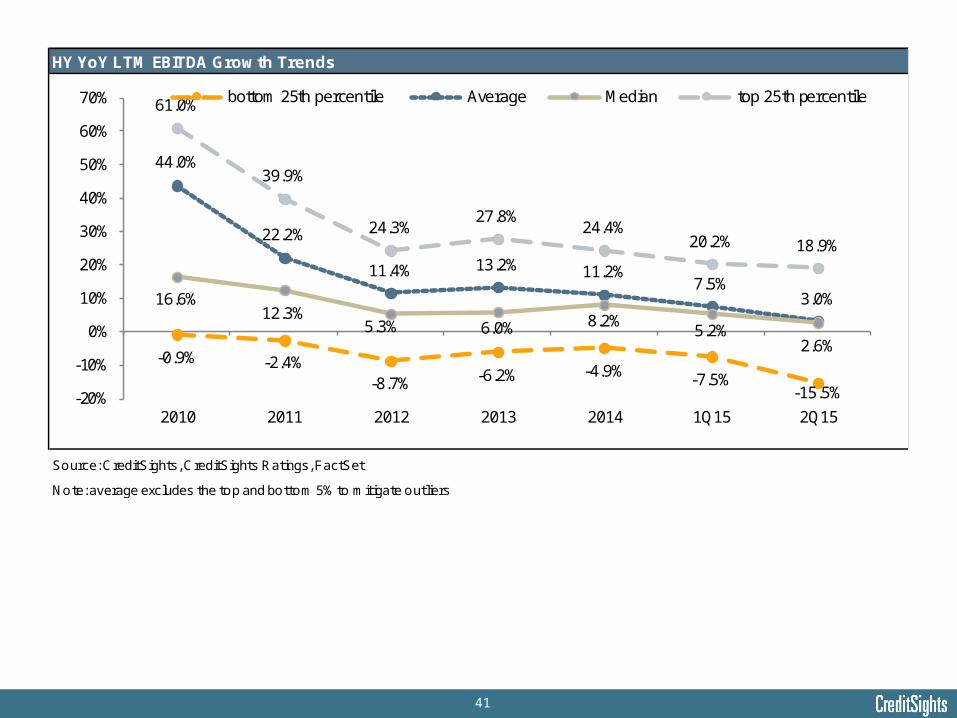

HY YoY LTM EBITDA Growth Trends

Source: CreditSights, CreditSights Ratings, FactSet

Note: average excludes the top and bottom 5% to mitigate outliers

-0.9% -2.4%-8.7% -6.2% -4.9% -7.5%

-15.5%

44.0%

22.2%

11.4% 13.2% 11.2%7.5%

3.0%16.6%12.3%

5.3% 6.0% 8.2%5.2%

2.6%

61.0%

39.9%

24.3%27.8%

24.4%20.2% 18.9%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014 1Q15 2Q15

bottom 25th percentile Average Median top 25th percentile

42

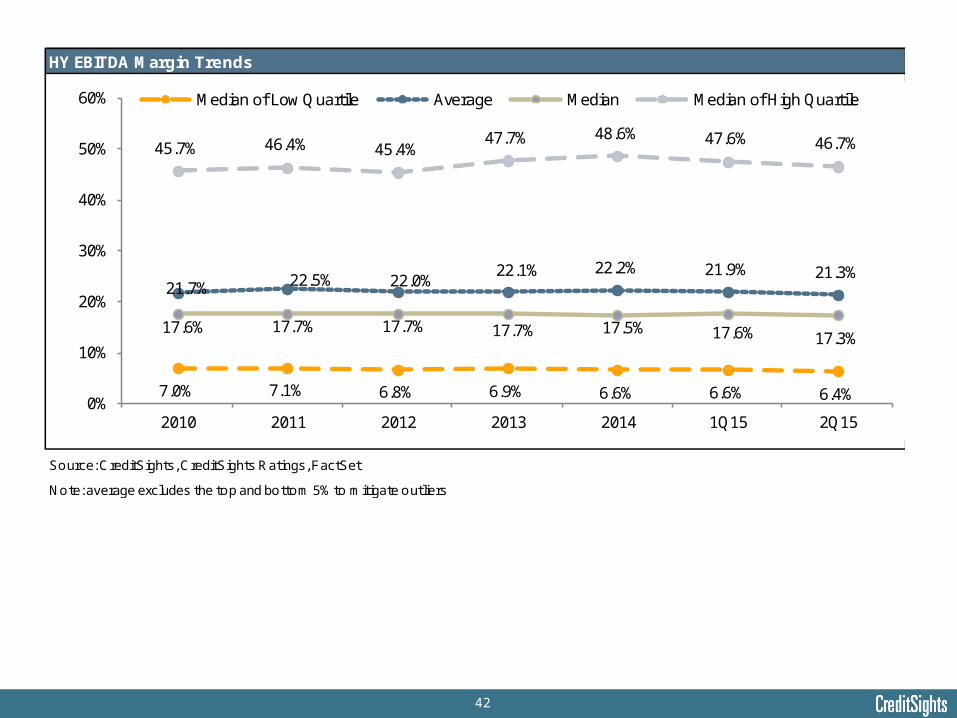

HY EBITDA Margin Trends

Source: CreditSights, CreditSights Ratings, FactSet

Note: average excludes the top and bottom 5% to mitigate outliers

7.0% 7.1% 6.8% 6.9% 6.6% 6.6% 6.4%

21.7% 22.5% 22.0% 22.1% 22.2% 21.9% 21.3%

17.6% 17.7% 17.7% 17.7% 17.5% 17.6% 17.3%

45.7% 46.4% 45.4% 47.7% 48.6% 47.6% 46.7%

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 1Q15 2Q15

Median of Low Quartile Average Median Median of High Quartile

43

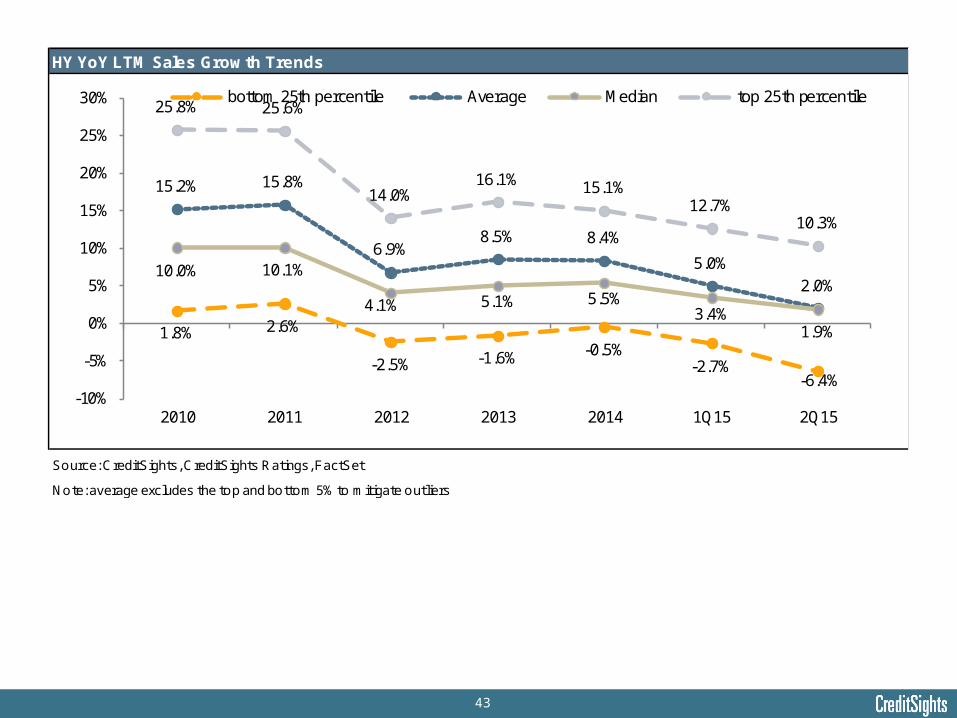

HY YoY LTM Sales Growth Trends

Source: CreditSights, CreditSights Ratings, FactSet

Note: average excludes the top and bottom 5% to mitigate outliers

1.8% 2.6%

-2.5% -1.6% -0.5%-2.7%

-6.4%

15.2% 15.8%

6.9%8.5% 8.4%

5.0%2.0%

10.0% 10.1%

4.1% 5.1% 5.5%3.4%

1.9%

25.8% 25.6%

14.0%16.1% 15.1%

12.7%10.3%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 1Q15 2Q15

bottom 25th percentile Average Median top 25th percentile

44

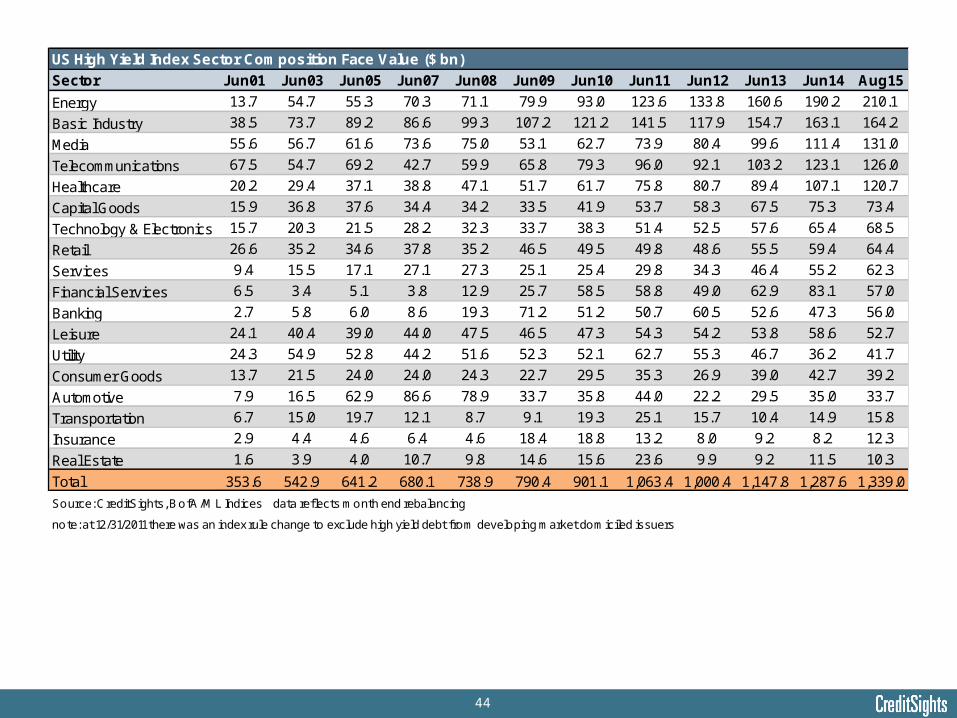

US High Yield Index Sector Composition Face Value ($ bn)

Sector Jun01 Jun03 Jun05 Jun07 Jun08 Jun09 Jun10 Jun11 Jun12 Jun13 Jun14 Aug15

Energy 13.7 54.7 55.3 70.3 71.1 79.9 93.0 123.6 133.8 160.6 190.2 210.1

Basic Industry 38.5 73.7 89.2 86.6 99.3 107.2 121.2 141.5 117.9 154.7 163.1 164.2

Media 55.6 56.7 61.6 73.6 75.0 53.1 62.7 73.9 80.4 99.6 111.4 131.0

Telecommunications 67.5 54.7 69.2 42.7 59.9 65.8 79.3 96.0 92.1 103.2 123.1 126.0

Healthcare 20.2 29.4 37.1 38.8 47.1 51.7 61.7 75.8 80.7 89.4 107.1 120.7

Capital Goods 15.9 36.8 37.6 34.4 34.2 33.5 41.9 53.7 58.3 67.5 75.3 73.4

Technology & Electronics 15.7 20.3 21.5 28.2 32.3 33.7 38.3 51.4 52.5 57.6 65.4 68.5

Retail 26.6 35.2 34.6 37.8 35.2 46.5 49.5 49.8 48.6 55.5 59.4 64.4

Services 9.4 15.5 17.1 27.1 27.3 25.1 25.4 29.8 34.3 46.4 55.2 62.3

Financial Services 6.5 3.4 5.1 3.8 12.9 25.7 58.5 58.8 49.0 62.9 83.1 57.0

Banking 2.7 5.8 6.0 8.6 19.3 71.2 51.2 50.7 60.5 52.6 47.3 56.0

Leisure 24.1 40.4 39.0 44.0 47.5 46.5 47.3 54.3 54.2 53.8 58.6 52.7

Utility 24.3 54.9 52.8 44.2 51.6 52.3 52.1 62.7 55.3 46.7 36.2 41.7

Consumer Goods 13.7 21.5 24.0 24.0 24.3 22.7 29.5 35.3 26.9 39.0 42.7 39.2

Automotive 7.9 16.5 62.9 86.6 78.9 33.7 35.8 44.0 22.2 29.5 35.0 33.7

Transportation 6.7 15.0 19.7 12.1 8.7 9.1 19.3 25.1 15.7 10.4 14.9 15.8

Insurance 2.9 4.4 4.6 6.4 4.6 18.4 18.8 13.2 8.0 9.2 8.2 12.3

Real Estate 1.6 3.9 4.0 10.7 9.8 14.6 15.6 23.6 9.9 9.2 11.5 10.3

Total 353.6 542.9 641.2 680.1 738.9 790.4 901.1 1,063.4 1,000.4 1,147.8 1,287.6 1,339.0

Source: CreditSights, BofA/ML Indices data reflects month end rebalancing

note: at 12/31/2011 there was an index rule change to exclude high yield debt from developing market domiciled issuers

45

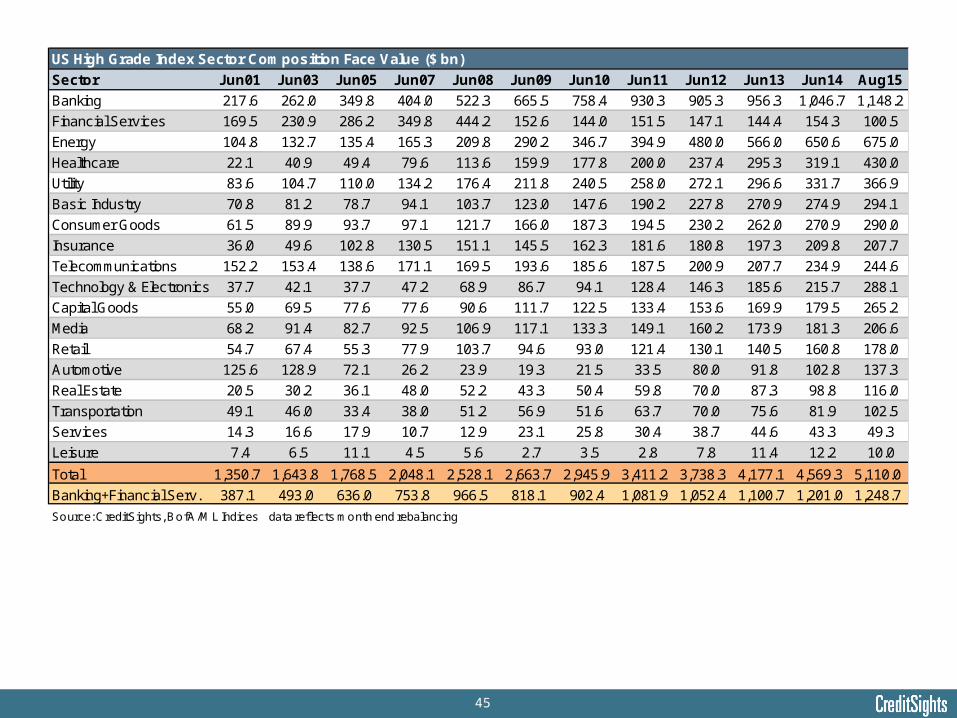

US High Grade Index Sector Composition Face Value ($ bn)

Sector Jun01 Jun03 Jun05 Jun07 Jun08 Jun09 Jun10 Jun11 Jun12 Jun13 Jun14 Aug15

Banking 217.6 262.0 349.8 404.0 522.3 665.5 758.4 930.3 905.3 956.3 1,046.7 1,148.2

Financial Services 169.5 230.9 286.2 349.8 444.2 152.6 144.0 151.5 147.1 144.4 154.3 100.5

Energy 104.8 132.7 135.4 165.3 209.8 290.2 346.7 394.9 480.0 566.0 650.6 675.0

Healthcare 22.1 40.9 49.4 79.6 113.6 159.9 177.8 200.0 237.4 295.3 319.1 430.0

Utility 83.6 104.7 110.0 134.2 176.4 211.8 240.5 258.0 272.1 296.6 331.7 366.9

Basic Industry 70.8 81.2 78.7 94.1 103.7 123.0 147.6 190.2 227.8 270.9 274.9 294.1

Consumer Goods 61.5 89.9 93.7 97.1 121.7 166.0 187.3 194.5 230.2 262.0 270.9 290.0

Insurance 36.0 49.6 102.8 130.5 151.1 145.5 162.3 181.6 180.8 197.3 209.8 207.7

Telecommunications 152.2 153.4 138.6 171.1 169.5 193.6 185.6 187.5 200.9 207.7 234.9 244.6

Technology & Electronics 37.7 42.1 37.7 47.2 68.9 86.7 94.1 128.4 146.3 185.6 215.7 288.1

Capital Goods 55.0 69.5 77.6 77.6 90.6 111.7 122.5 133.4 153.6 169.9 179.5 265.2

Media 68.2 91.4 82.7 92.5 106.9 117.1 133.3 149.1 160.2 173.9 181.3 206.6

Retail 54.7 67.4 55.3 77.9 103.7 94.6 93.0 121.4 130.1 140.5 160.8 178.0

Automotive 125.6 128.9 72.1 26.2 23.9 19.3 21.5 33.5 80.0 91.8 102.8 137.3

Real Estate 20.5 30.2 36.1 48.0 52.2 43.3 50.4 59.8 70.0 87.3 98.8 116.0

Transportation 49.1 46.0 33.4 38.0 51.2 56.9 51.6 63.7 70.0 75.6 81.9 102.5

Services 14.3 16.6 17.9 10.7 12.9 23.1 25.8 30.4 38.7 44.6 43.3 49.3

Leisure 7.4 6.5 11.1 4.5 5.6 2.7 3.5 2.8 7.8 11.4 12.2 10.0

Total 1,350.7 1,643.8 1,768.5 2,048.1 2,528.1 2,663.7 2,945.9 3,411.2 3,738.3 4,177.1 4,569.3 5,110.0

Banking+Financial Serv. 387.1 493.0 636.0 753.8 966.5 818.1 902.4 1,081.9 1,052.4 1,100.7 1,201.0 1,248.7

Source: CreditSights, BofA/ML Indices data reflects month end rebalancing

46

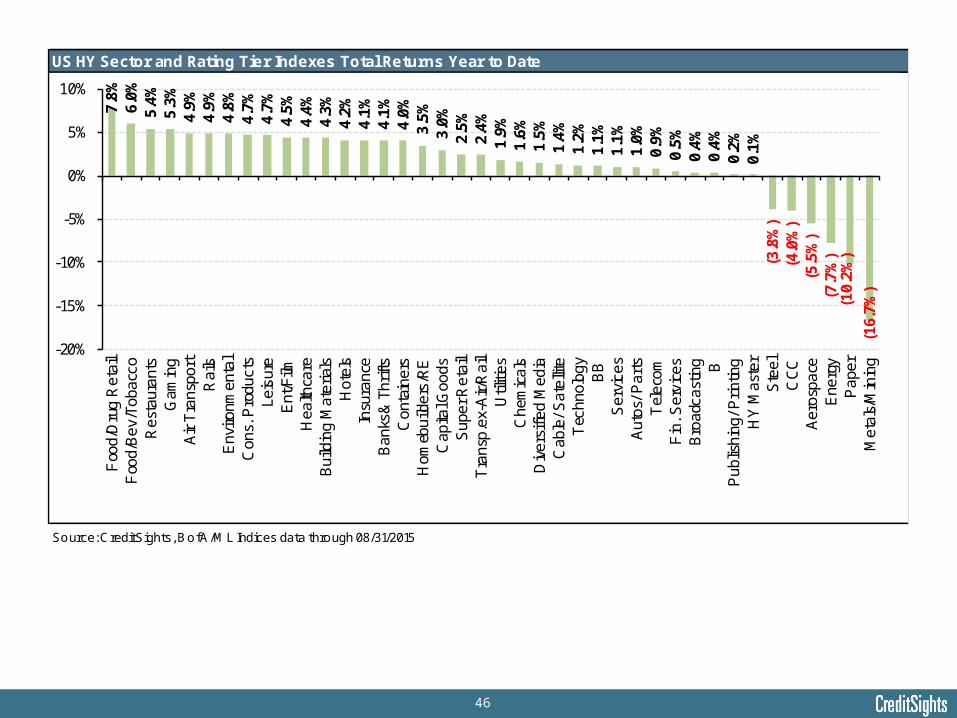

US HY Sector and Rating Tier Indexes Total Returns Year to Date

Source: CreditSights, BofA/ML Indices data through 08/31/2015

7.8%

6.0%

5.4%

5.3%

4.9%

4.9%

4.8%

4.7%

4.7%

4.5%

4.4%

4.3%

4.2%

4.1%

4.1%

4.0%

3.5%

3.0%

2.5%

2.4%

1.9%

1.6%

1.5%

1.4%

1.2%

1.1%

1.1%

1.0%

0.9%

0.5%

0.4%

0.4%

0.2%

0.1%

(3.8

%)

(4.0

%)

(5.5

%)

(7.7

%)

(10.

2%)

(16.

7%)

-20%

-15%

-10%

-5%

0%

5%

10%

Foo

d/D

rug

Ret

ail

Foo

d/B

ev/T

obac

coR

esta

uran

tsG

amin

gA

ir T

rans

port

Rai

lsE

nviro

nmen

tal

Con

s. P

rodu

cts

Leis

ure

Ent

/Film

Hea

lthca

reB

uild

ing

Mat

eria

lsH

otel

sIn

sura

nce

Ban

ks&

Thr

ifts

Con

tain

ers

Hom

ebui

lder

s/R

EC

apita

l Goo

dsS

uper

Ret

ail

Tra

nsp.

ex-A

ir/R

ail

Util

ities

Che

mic

als

Div

ersi

fied

Med

iaC

able

/ Sat

ellit

eT

echn

olog

yB

BS

ervi

ces

Aut

os/ P

arts

Tel

ecom

Fin

. Ser

vice

sB

road

cast

ing B

Pub

lishi

ng/ P

rintin

gH

Y M

aste

rS

teel

CC

CA

eros

pace

Ene

rgy

Pap

erM

etal

s/M

inin

g

47

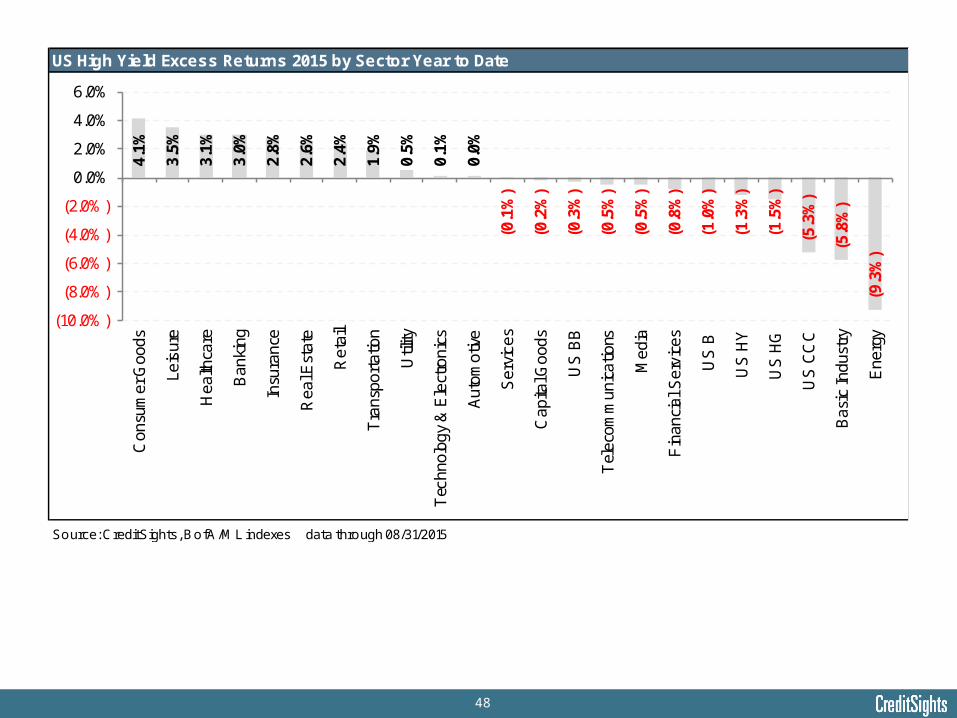

US High Yield Excess Returns 2015 by Sector Year to Date

Source: CreditSights, BofA/ML indexes data through 08/31/2015

4.1%

3.5%

3.1%

3.0%

2.8%

2.6%

2.4%

1.9%

0.5%

0.1%

0.0%

(0.1

%)

(0.2

%)

(0.3

%)

(0.5

%)

(0.5

%)

(0.8

%)

(1.0

%)

(1.3

%)

(1.5

%)

(5.3

%)

(5.8

%)

(9.3

%)

(10.0%)

(8.0%)

(6.0%)

(4.0%)

(2.0%)

0.0%

2.0%

4.0%

6.0%

Con

sum

er G

oods

Leis

ure

Hea

lthca

re

Ban

king

Insu

ranc

e

Rea

l Est

ate

Ret

ail

Tra

nspo

rtat

ion

Util

ity

Tec

hnol

ogy

& E

lect

roni

cs

Aut

omot

ive

Ser

vice

s

Cap

ital G

oods

US

BB

Tel

ecom

mun

icat

ions

Med

ia

Fin

anci

al S

ervi

ces

US

B

US

HY

US

HG

US

CC

C

Bas

ic In

dust

ry

Ene

rgy

48

US High Yield Excess Returns 2015 by Sector Year to Date

Source: CreditSights, BofA/ML indexes data through 08/31/2015

4.1%

3.5%

3.1%

3.0%

2.8%

2.6%

2.4%

1.9%

0.5%

0.1%

0.0%

(0.1

%)

(0.2

%)

(0.3

%)

(0.5

%)

(0.5

%)

(0.8

%)

(1.0

%)

(1.3

%)

(1.5

%)

(5.3

%)

(5.8

%)

(9.3

%)

(10.0%)

(8.0%)

(6.0%)

(4.0%)

(2.0%)

0.0%

2.0%

4.0%

6.0%

Con

sum

er G

oods

Leis

ure

Hea

lthca

re

Ban

king

Insu

ranc

e

Rea

l Est

ate

Ret

ail

Tra

nspo

rtat

ion

Util

ity

Tec

hnol

ogy

& E

lect

roni

cs

Aut

omot

ive

Ser

vice

s

Cap

ital G

oods

US

BB

Tel

ecom

mun

icat

ions

Med

ia

Fin

anci

al S

ervi

ces

US

B

US

HY

US

HG

US

CC

C

Bas

ic In

dust

ry

Ene

rgy

49

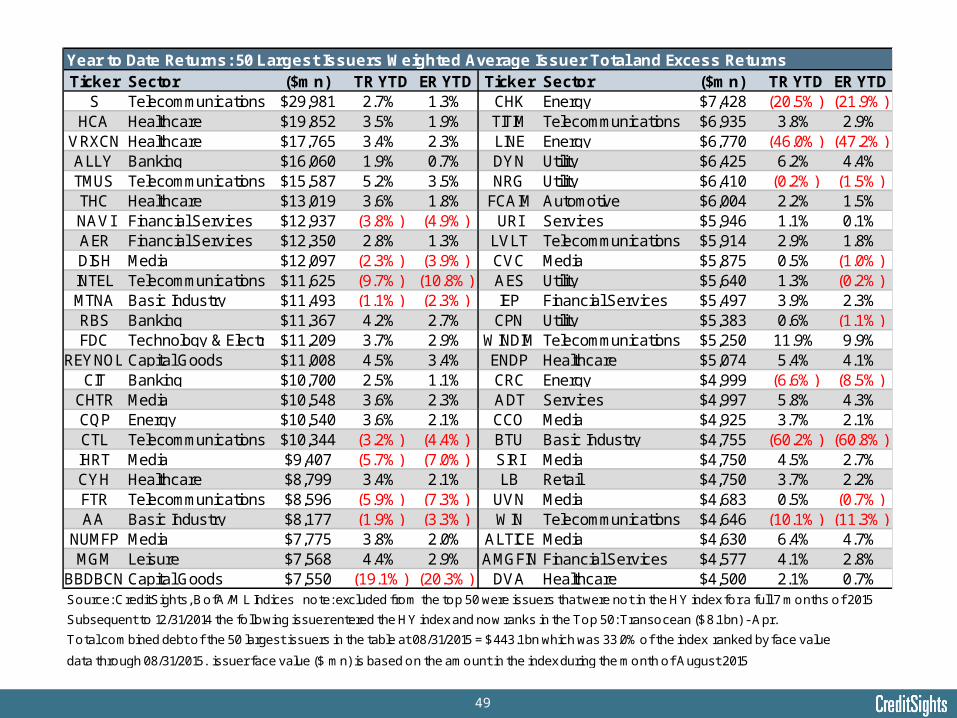

Year to Date Returns: 50 Largest Issuers Weighted Average Issuer Total and Excess Returns Ticker Sector ($mn) TR YTD ER YTD Ticker Sector ($mn) TR YTD ER YTD

S Telecommunications $29,981 2.7% 1.3% CHK Energy $7,428 (20.5%) (21.9%)HCA Healthcare $19,852 3.5% 1.9% TITIM Telecommunications $6,935 3.8% 2.9%

VRXCN Healthcare $17,765 3.4% 2.3% LINE Energy $6,770 (46.0%) (47.2%)ALLY Banking $16,060 1.9% 0.7% DYN Utility $6,425 6.2% 4.4%TMUS Telecommunications $15,587 5.2% 3.5% NRG Utility $6,410 (0.2%) (1.5%)THC Healthcare $13,019 3.6% 1.8% FCAIM Automotive $6,004 2.2% 1.5%NAVI Financial Services $12,937 (3.8%) (4.9%) URI Services $5,946 1.1% 0.1%AER Financial Services $12,350 2.8% 1.3% LVLT Telecommunications $5,914 2.9% 1.8%DISH Media $12,097 (2.3%) (3.9%) CVC Media $5,875 0.5% (1.0%)INTEL Telecommunications $11,625 (9.7%) (10.8%) AES Utility $5,640 1.3% (0.2%)MTNA Basic Industry $11,493 (1.1%) (2.3%) IEP Financial Services $5,497 3.9% 2.3%RBS Banking $11,367 4.2% 2.7% CPN Utility $5,383 0.6% (1.1%)FDC Technology & Electronics$11,209 3.7% 2.9% WINDIM Telecommunications $5,250 11.9% 9.9%

REYNOL Capital Goods $11,008 4.5% 3.4% ENDP Healthcare $5,074 5.4% 4.1%CIT Banking $10,700 2.5% 1.1% CRC Energy $4,999 (6.6%) (8.5%)

CHTR Media $10,548 3.6% 2.3% ADT Services $4,997 5.8% 4.3%CQP Energy $10,540 3.6% 2.1% CCO Media $4,925 3.7% 2.1%CTL Telecommunications $10,344 (3.2%) (4.4%) BTU Basic Industry $4,755 (60.2%) (60.8%)IHRT Media $9,407 (5.7%) (7.0%) SIRI Media $4,750 4.5% 2.7%CYH Healthcare $8,799 3.4% 2.1% LB Retail $4,750 3.7% 2.2%FTR Telecommunications $8,596 (5.9%) (7.3%) UVN Media $4,683 0.5% (0.7%)AA Basic Industry $8,177 (1.9%) (3.3%) WIN Telecommunications $4,646 (10.1%) (11.3%)

NUMFP Media $7,775 3.8% 2.0% ALTICE Media $4,630 6.4% 4.7%MGM Leisure $7,568 4.4% 2.9% AMGFIN Financial Services $4,577 4.1% 2.8%

BBDBCN Capital Goods $7,550 (19.1%) (20.3%) DVA Healthcare $4,500 2.1% 0.7%Source: CreditSights, BofA/ML Indices note: excluded from the top 50 were issuers that were not in the HY index for a full 7 months of 2015

Subsequent to 12/31/2014 the following issuer entered the HY index and now ranks in the Top 50: Transocean ($8.1 bn) - Apr.

Total combined debt of the 50 largest issuers in the table at 08/31/2015 = $443.1 bn which was 33.0% of the index ranked by face value

data through 08/31/2015. issuer face value ($ mn) is based on the amount in the index during the month of August 2015

50

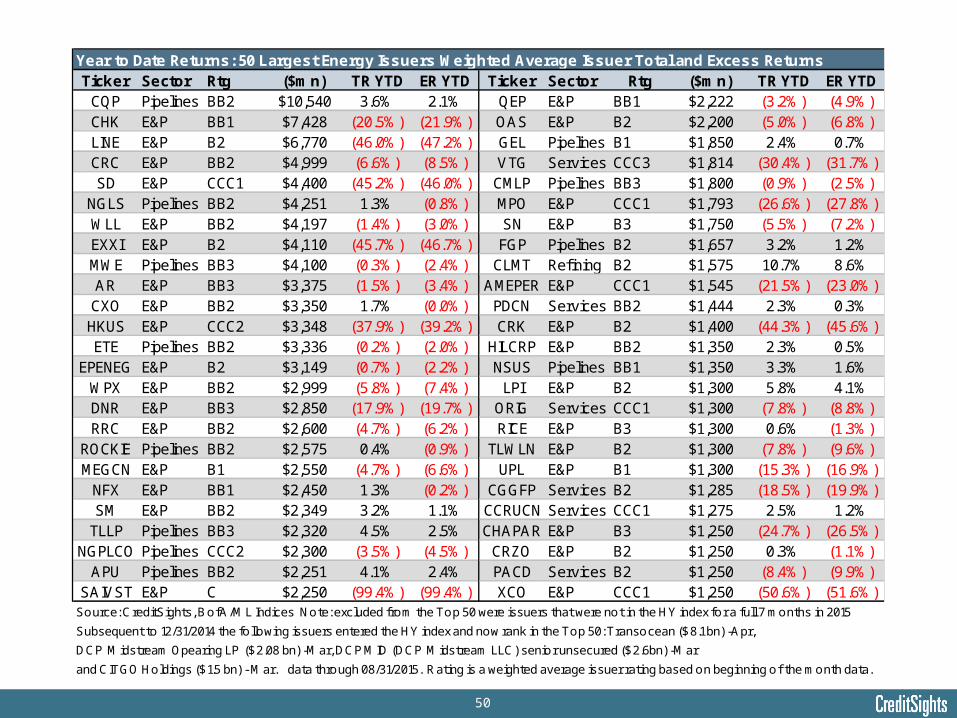

Year to Date Returns: 50 Largest Energy Issuers Weighted Average Issuer Total and Excess Returns Ticker Sector Rtg ($mn) TR YTD ER YTD Ticker Sector Rtg ($mn) TR YTD ER YTD

CQP Pipelines BB2 $10,540 3.6% 2.1% QEP E&P BB1 $2,222 (3.2%) (4.9%)CHK E&P BB1 $7,428 (20.5%) (21.9%) OAS E&P B2 $2,200 (5.0%) (6.8%)LINE E&P B2 $6,770 (46.0%) (47.2%) GEL Pipelines B1 $1,850 2.4% 0.7%CRC E&P BB2 $4,999 (6.6%) (8.5%) VTG Services CCC3 $1,814 (30.4%) (31.7%)SD E&P CCC1 $4,400 (45.2%) (46.0%) CMLP Pipelines BB3 $1,800 (0.9%) (2.5%)

NGLS Pipelines BB2 $4,251 1.3% (0.8%) MPO E&P CCC1 $1,793 (26.6%) (27.8%)WLL E&P BB2 $4,197 (1.4%) (3.0%) SN E&P B3 $1,750 (5.5%) (7.2%)EXXI E&P B2 $4,110 (45.7%) (46.7%) FGP Pipelines B2 $1,657 3.2% 1.2%MWE Pipelines BB3 $4,100 (0.3%) (2.4%) CLMT Refining B2 $1,575 10.7% 8.6%AR E&P BB3 $3,375 (1.5%) (3.4%) AMEPER E&P CCC1 $1,545 (21.5%) (23.0%)CXO E&P BB2 $3,350 1.7% (0.0%) PDCN Services BB2 $1,444 2.3% 0.3%HKUS E&P CCC2 $3,348 (37.9%) (39.2%) CRK E&P B2 $1,400 (44.3%) (45.6%)ETE Pipelines BB2 $3,336 (0.2%) (2.0%) HILCRP E&P BB2 $1,350 2.3% 0.5%

EPENEG E&P B2 $3,149 (0.7%) (2.2%) NSUS Pipelines BB1 $1,350 3.3% 1.6%WPX E&P BB2 $2,999 (5.8%) (7.4%) LPI E&P B2 $1,300 5.8% 4.1%DNR E&P BB3 $2,850 (17.9%) (19.7%) ORIG Services CCC1 $1,300 (7.8%) (8.8%)RRC E&P BB2 $2,600 (4.7%) (6.2%) RICE E&P B3 $1,300 0.6% (1.3%)

ROCKIE Pipelines BB2 $2,575 0.4% (0.9%) TLWLN E&P B2 $1,300 (7.8%) (9.6%)MEGCN E&P B1 $2,550 (4.7%) (6.6%) UPL E&P B1 $1,300 (15.3%) (16.9%)

NFX E&P BB1 $2,450 1.3% (0.2%) CGGFP Services B2 $1,285 (18.5%) (19.9%)SM E&P BB2 $2,349 3.2% 1.1% CCRUCN Services CCC1 $1,275 2.5% 1.2%

TLLP Pipelines BB3 $2,320 4.5% 2.5% CHAPAR E&P B3 $1,250 (24.7%) (26.5%)NGPLCO Pipelines CCC2 $2,300 (3.5%) (4.5%) CRZO E&P B2 $1,250 0.3% (1.1%)

APU Pipelines BB2 $2,251 4.1% 2.4% PACD Services B2 $1,250 (8.4%) (9.9%)SAIVST E&P C $2,250 (99.4%) (99.4%) XCO E&P CCC1 $1,250 (50.6%) (51.6%)

Source: CreditSights, BofA/ML Indices Note: excluded from the Top 50 were issuers that were not in the HY index for a full 7 months in 2015

Subsequent to 12/31/2014 the following issuers entered the HY index and now rank in the Top 50: Transocean ($8.1 bn) -Apr,

DCP M idstream Opearing LP ($2.08 bn) -Mar, DCP MID (DCP M idstream LLC) senior unsecured ($2.6bn) -Mar

and CITGO Holdings ($1.5 bn) - Mar. data through 08/31/2015. Rating is a weighted average issuer rating based on beginning of the month data.

51

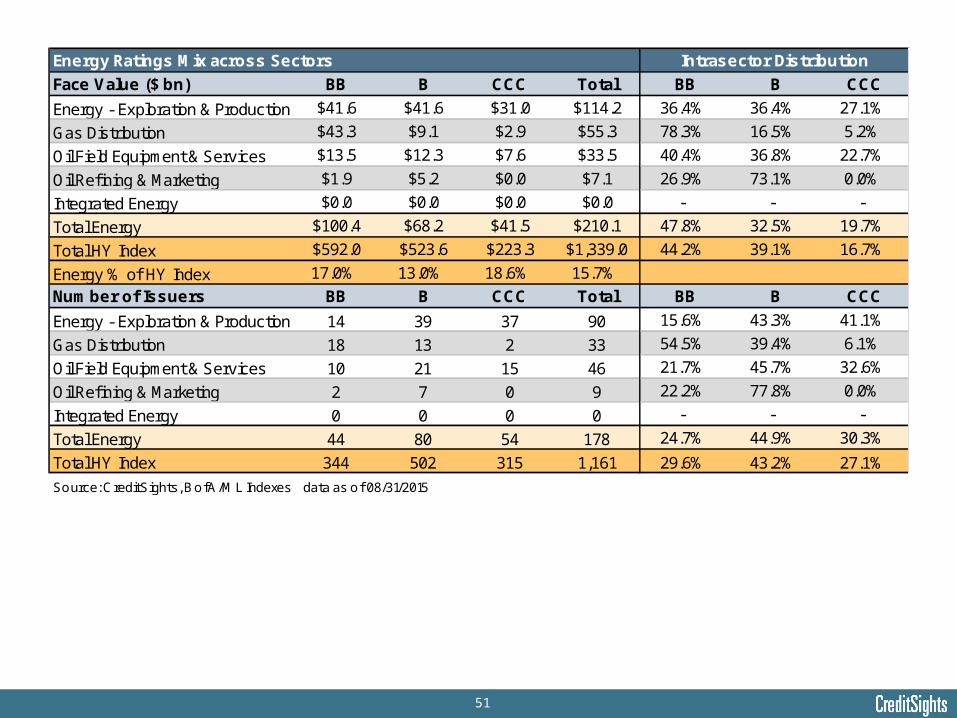

Energy Ratings Mix across Sectors

Face Value ($ bn) BB B CCC Total BB B CCC

Energy - Exploration & Production $41.6 $41.6 $31.0 $114.2 36.4% 36.4% 27.1%

Gas Distribution $43.3 $9.1 $2.9 $55.3 78.3% 16.5% 5.2%

Oil Field Equipment & Services $13.5 $12.3 $7.6 $33.5 40.4% 36.8% 22.7%

Oil Refining & Marketing $1.9 $5.2 $0.0 $7.1 26.9% 73.1% 0.0%

Integrated Energy $0.0 $0.0 $0.0 $0.0 - - -

Total Energy $100.4 $68.2 $41.5 $210.1 47.8% 32.5% 19.7%

Total HY Index $592.0 $523.6 $223.3 $1,339.0 44.2% 39.1% 16.7%

Energy % of HY Index 17.0% 13.0% 18.6% 15.7%

Number of Issuers BB B CCC Total BB B CCC

Energy - Exploration & Production 14 39 37 90 15.6% 43.3% 41.1%

Gas Distribution 18 13 2 33 54.5% 39.4% 6.1%

Oil Field Equipment & Services 10 21 15 46 21.7% 45.7% 32.6%

Oil Refining & Marketing 2 7 0 9 22.2% 77.8% 0.0%

Integrated Energy 0 0 0 0 - - -

Total Energy 44 80 54 178 24.7% 44.9% 30.3%

Total HY Index 344 502 315 1,161 29.6% 43.2% 27.1%

Source: CreditSights, BofA/ML Indexes data as of 08/31/2015

Intrasector Distribution

52

US High Yield E&P + Suppliers/Services

Source: CreditSights, BofA/ML indexes

3.1% 3.7% 3.5%

4.9% 5.7%

6.1% 6.5%

7.5%

9.2% 9.6%

9.9%

11.0%

10.920.3 22.7

33.742.1

48.058.7

79.3

91.8

110.1

127.9

147.7

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

Jun01 Jun03 Jun05 Jun07 Jun08 Jun09 Jun10 Jun11 Jun12 Jun13 Jun14 Aug15

Face Value % of Index,( rhs)

Face Value ($ mn), (lhs)

53

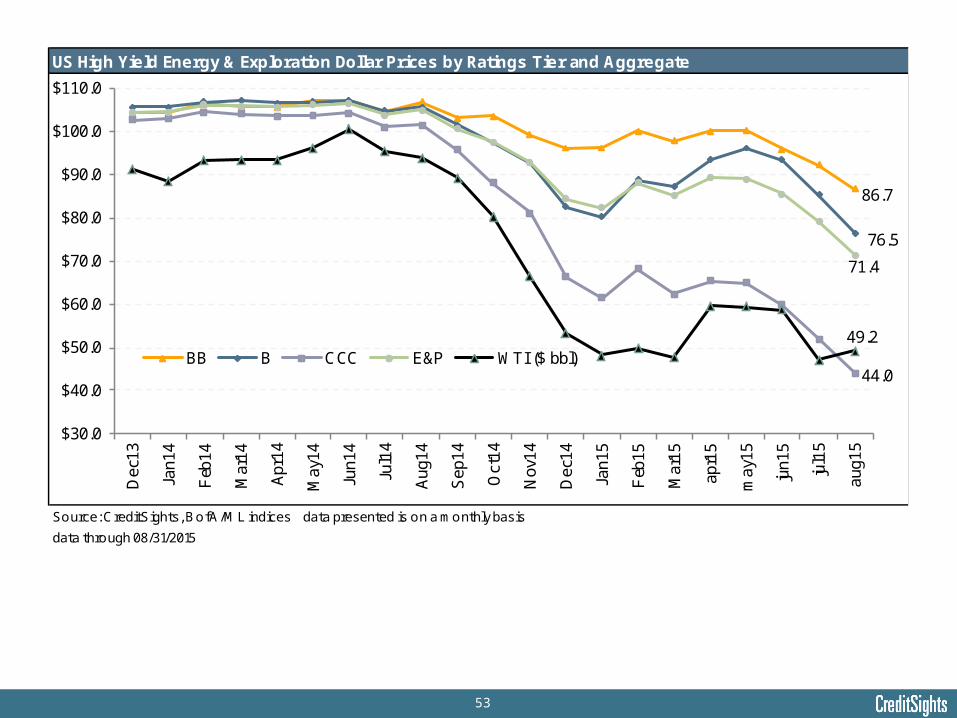

US High Yield Energy & Exploration Dollar Prices by Ratings Tier and Aggregate

Source: CreditSights, BofA/ML indices data presented is on a monthly basis

data through 08/31/2015

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

$100.0

$110.0

Dec

13

Jan1

4

Feb

14

Mar

14

Apr

14

May

14

Jun1

4

Jul1

4

Aug

14

Sep

14

Oct

14

Nov

14

Dec

14

Jan1

5

Feb

15

Mar

15

apr1

5

may

15

jun1

5

jul1

5

aug1

5

BB B CCC E&P WTI ($ bbl)

86.7

76.5

44.0

49.2

71.4

54

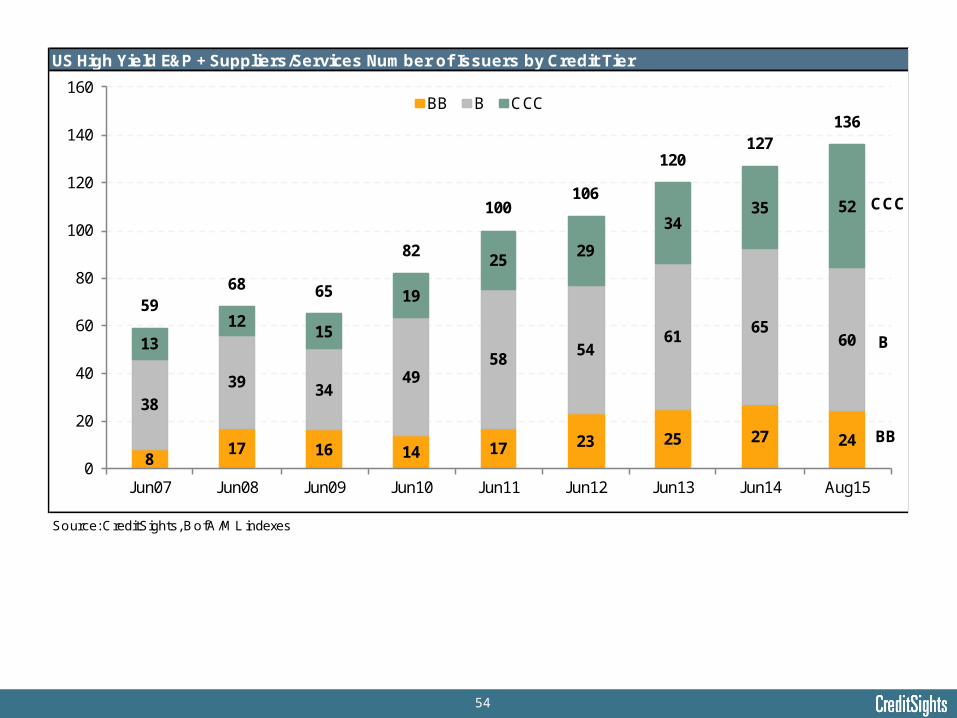

US High Yield E&P + Suppliers/Services Number of Issuers by Credit Tier

Source: CreditSights, BofA/ML indexes

817 16 14 17 23 25 27 24

38

39 3449

5854

6165

601312

15

19

2529

3435 52

5968 65

82

100106

120127

136

0

20

40

60

80

100

120

140

160

Jun07 Jun08 Jun09 Jun10 Jun11 Jun12 Jun13 Jun14 Aug15

BB B CCC

BB

B

CCC

55

Appendix

56

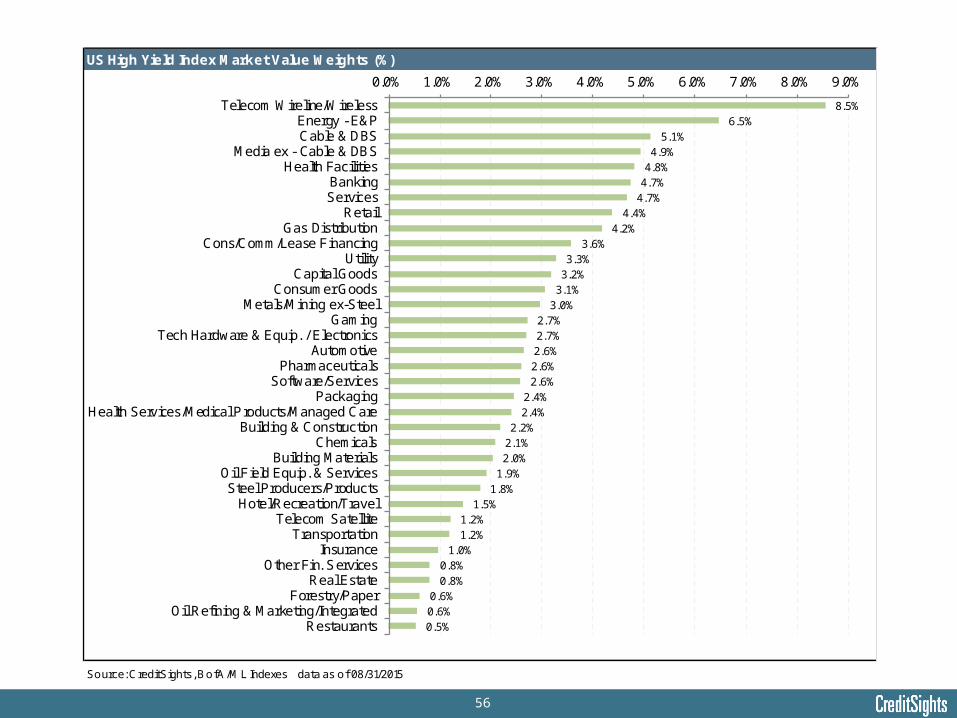

US High Yield Index Market Value Weights (%)

Source: CreditSights, BofA/ML Indexes data as of 08/31/2015

8.5% 6.5%

5.1% 4.9%

4.8% 4.7%

4.7% 4.4%

4.2% 3.6%

3.3% 3.2%

3.1% 3.0%

2.7% 2.7% 2.6% 2.6% 2.6%

2.4% 2.4%

2.2% 2.1% 2.0%

1.9% 1.8%

1.5% 1.2% 1.2%

1.0% 0.8% 0.8%

0.6% 0.6% 0.5%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0%

Telecom Wireline/WirelessEnergy - E&PCable & DBS

Media ex - Cable & DBSHealth Facilities

BankingServices

RetailGas Distribution

Cons/Comm/Lease FinancingUtility

Capital GoodsConsumer Goods

Metals/Mining ex-SteelGaming

Tech Hardware & Equip. / ElectronicsAutomotive

PharmaceuticalsSoftware/Services

PackagingHealth Services/Medical Products/Managed Care

Building & ConstructionChemicals

Building MaterialsOil Field Equip. & ServicesSteel Producers/Products

Hotel/Recreation/TravelTelecom Satellite

TransportationInsurance

Other Fin. ServicesReal Estate

Forestry/PaperOil Refining & Marketing/Integrated

Restaurants

57

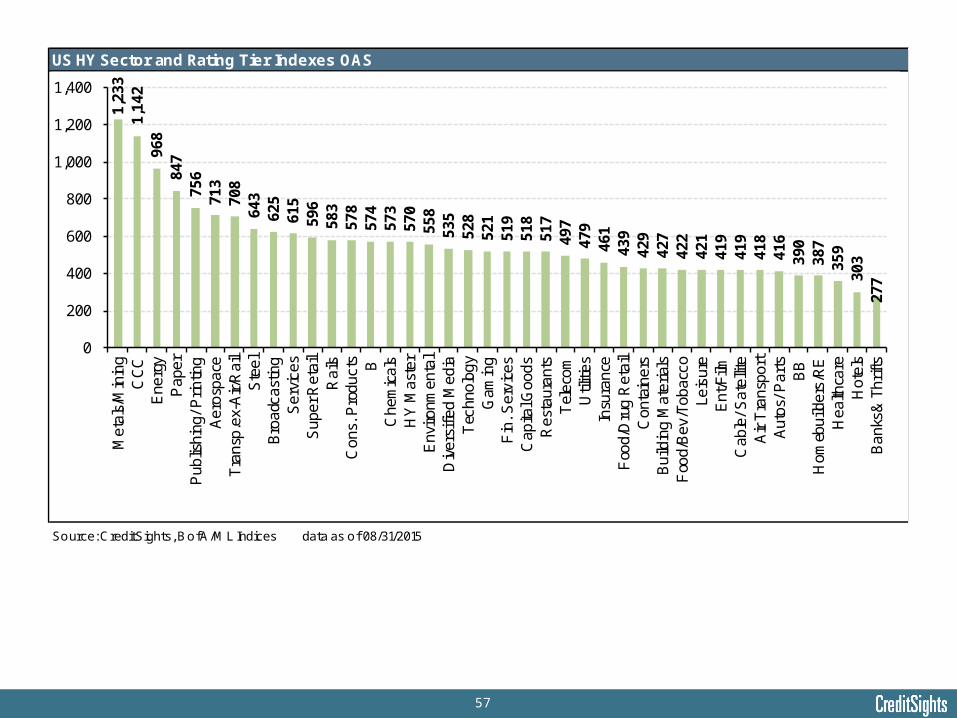

US HY Sector and Rating Tier Indexes OAS

Source: CreditSights, BofA/ML Indices data as of 08/31/2015

1,23

3 1,

142

968

847

756

713

708

643

625

615

596

583

578

574

573

570

558

535

528

521

519

518

517

497

479

461

439

429

427

422

421

419

419

418

416

390

387

359

303

277

0

200

400

600

800

1,000

1,200

1,400

Met

als/

Min

ing

CC

CE

nerg

yP

aper

Pub

lishi

ng/ P

rintin

gA

eros

pace

Tra

nsp.

ex-A

ir/R

ail

Ste

elB

road

cast

ing

Ser

vice

sS

uper

Ret

ail

Rai

lsC

ons.

Pro

duct

s BC

hem

ical

sH

Y M

aste

rE

nviro

nmen

tal

Div

ersi

fied

Med

iaT

echn

olog

yG

amin

gF

in. S

ervi

ces

Cap

ital G

oods

Res

taur

ants

Tel

ecom

Util

ities

Insu

ranc

eF

ood/

Dru

g R

etai

lC

onta

iner

sB

uild

ing

Mat

eria

lsF

ood/

Bev

/Tob

acco

Leis

ure

Ent

/Film

Cab

le/ S

atel

lite

Air

Tra

nspo

rtA

utos

/ Par

tsB

BH

omeb

uild

ers/

RE

Hea

lthca

reH

otel

sB

anks

& T

hrift

s

58

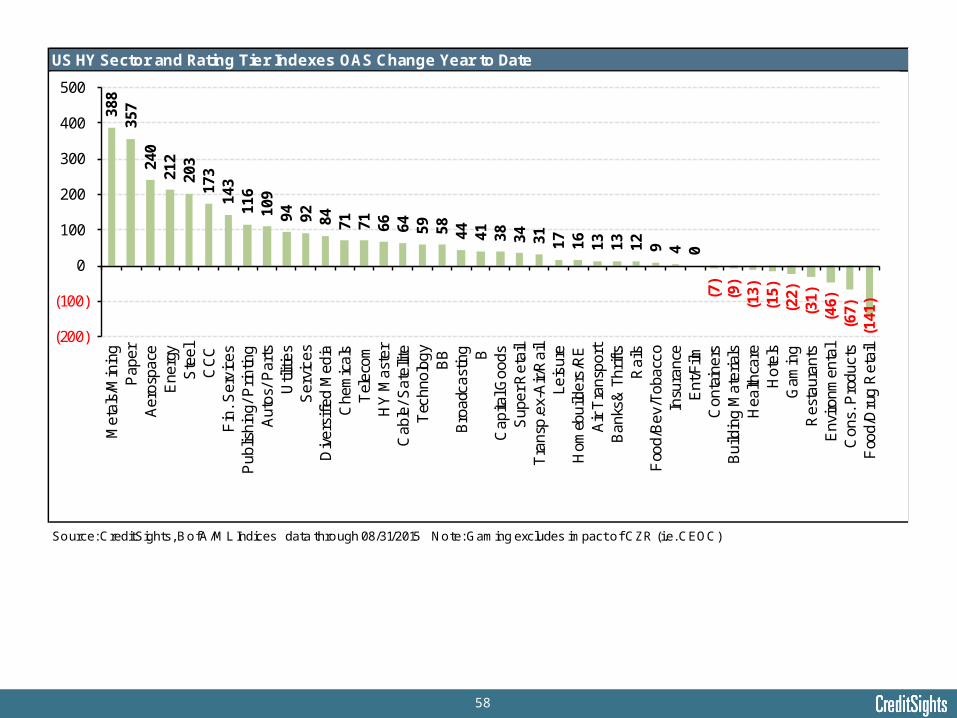

US HY Sector and Rating Tier Indexes OAS Change Year to Date

Source: CreditSights, BofA/ML Indices data through 08/31/2015 Note: Gaming excludes impact of CZR (i.e. CEOC)

388

357

240

212

203

173

143

116

109

94

92

84

71

71

66

64

59

58

44

41

38

34

31

17

16

13

13

12

9 4 0 (7

)(9

)(1

3)(1

5)(2

2)(3

1)(4

6)(6

7)(1

41)

(200)

(100)

0

100

200

300

400

500

Met

als/

Min

ing

Pap

erA

eros

pace

Ene

rgy

Ste

elC

CC

Fin

. Ser

vice

sP

ublis

hing

/ Prin

ting

Aut

os/ P

arts

Util

ities

Ser

vice

sD

iver

sifie

d M

edia

Che

mic

als

Tel

ecom

HY

Mas

ter

Cab

le/ S

atel

lite

Tec

hnol

ogy

BB

Bro

adca

stin

g BC

apita

l Goo

dsS

uper

Ret

ail

Tra

nsp.

ex-A

ir/R

ail

Leis

ure

Hom

ebui

lder

s/R

EA

ir T

rans

port

Ban

ks&

Thr

ifts

Rai

lsF

ood/

Bev

/Tob

acco

Insu

ranc

eE

nt/F

ilmC

onta

iner

sB

uild

ing

Mat

eria

lsH

ealth

care

Hot

els

Gam

ing

Res

taur

ants

Env

ironm

enta

lC

ons.

Pro

duct

sF

ood/

Dru

g R

etai

l

59

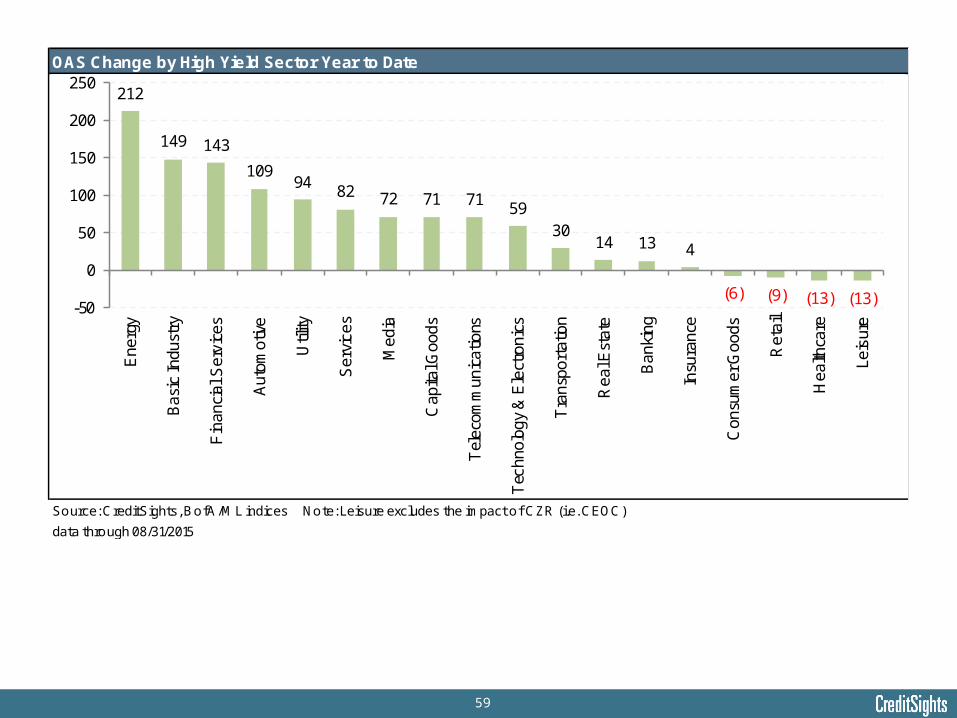

OAS Change by High Yield Sector Year to Date

Source: CreditSights, BofA/ML indices Note: Leisure excludes the impact of CZR (i.e. CEOC)

data through 08/31/2015

212

149 143

109 94

82 72 71 71 59 30

14 13 4

(6) (9) (13) (13)-50

0

50

100

150

200

250

Ene

rgy

Bas

ic In

dust

ry

Fin

anci

al S

ervi

ces

Aut

omot

ive

Util

ity

Ser

vice

s

Med

ia

Cap

ital G

oods

Tel

ecom

mun

icat

ions

Tec

hnol

ogy

& E

lect

roni

cs

Tra

nspo

rtat

ion

Rea

l Est

ate

Ban

king

Insu

ranc

e

Con

sum

er G

oods

Ret

ail

Hea

lthca

re

Leis

ure

60

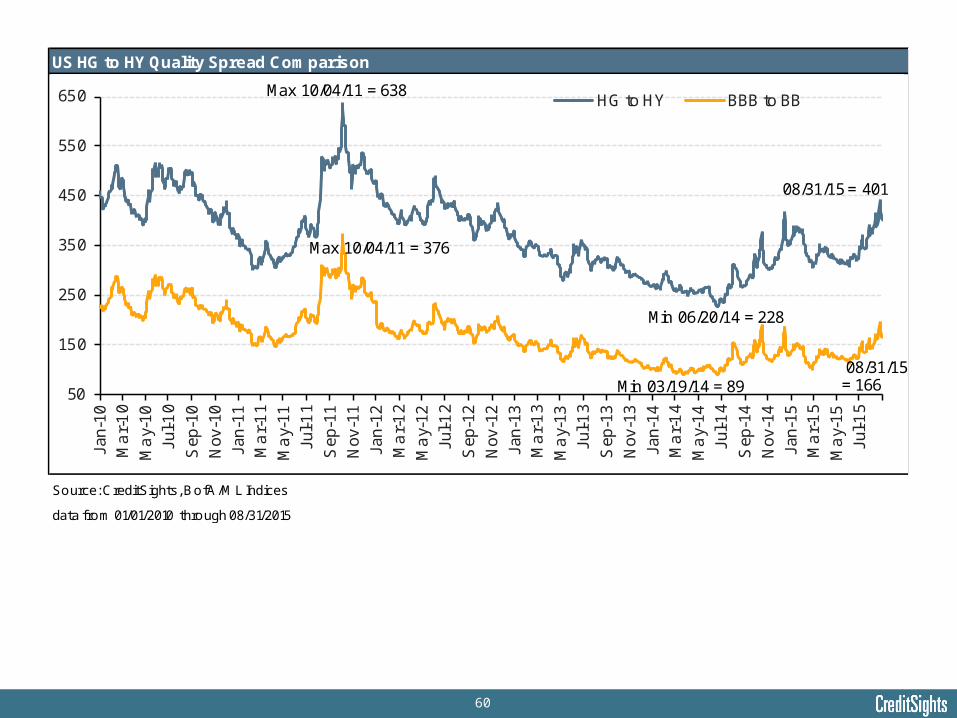

US HG to HY Quality Spread Comparison

Source: CreditSights, BofA/ML Indices

data from 01/01/2010 through 08/31/2015

50

150

250

350

450

550

650Ja

n-10

Ma

r-1

0

Ma

y-10

Jul-1

0

Sep

-10

Nov

-10

Jan-

11M

ar-

11

Ma

y-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Ma

r-1

2

Ma

y-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13M

ar-

13

Ma

y-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14M

ar-

14

Ma

y-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15M

ar-

15

Ma

y-15

Jul-1

5

HG to HY BBB to BBMax 10/04/11 = 638

08/31/15 = 401

Min 06/20/14 = 228

Max 10/04/11 = 376

08/31/15 = 166Min 03/19/14 = 89

61

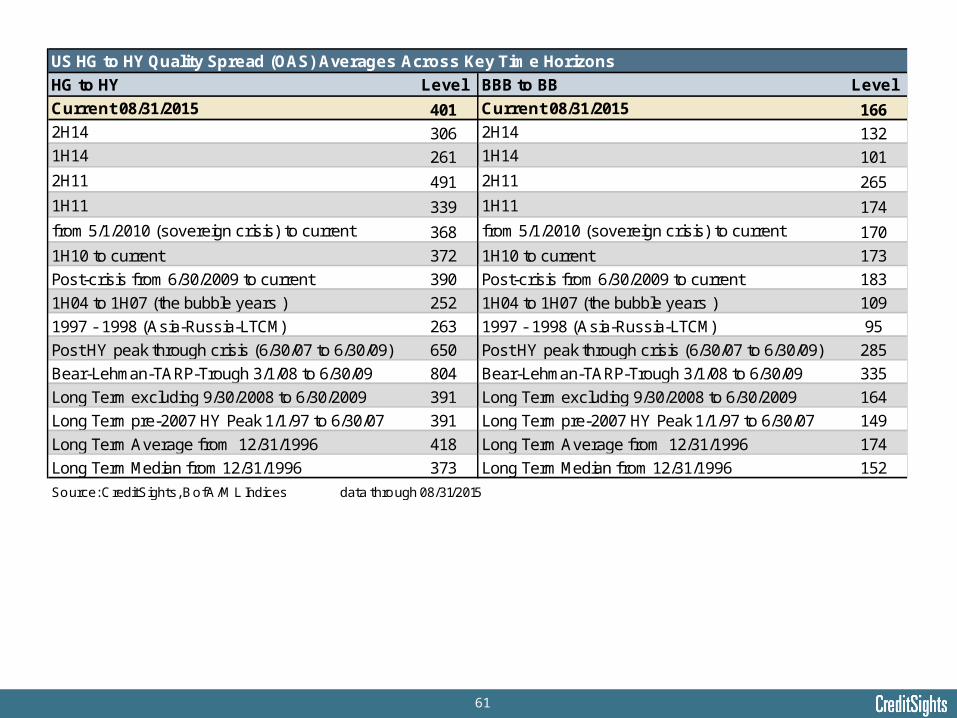

US HG to HY Quality Spread (OAS) Averages Across Key Time Horizons

HG to HY Level BBB to BB Level

Current 08/31/2015 401 Current 08/31/2015 1662H14 306 2H14 1321H14 261 1H14 101

2H11 491 2H11 265

1H11 339 1H11 174

from 5/1/2010 (sovereign crisis) to current 368 from 5/1/2010 (sovereign crisis) to current 170

1H10 to current 372 1H10 to current 173

Post-crisis from 6/30/2009 to current 390 Post-crisis from 6/30/2009 to current 183

1H04 to 1H07 (the bubble years ) 252 1H04 to 1H07 (the bubble years ) 109

1997 - 1998 (Asia-Russia-LTCM) 263 1997 - 1998 (Asia-Russia-LTCM) 95

Post HY peak through crisis (6/30/07 to 6/30/09) 650 Post HY peak through crisis (6/30/07 to 6/30/09) 285

Bear-Lehman-TARP-Trough 3/1/08 to 6/30/09 804 Bear-Lehman-TARP-Trough 3/1/08 to 6/30/09 335

Long Term excluding 9/30/2008 to 6/30/2009 391 Long Term excluding 9/30/2008 to 6/30/2009 164

Long Term pre-2007 HY Peak 1/1/97 to 6/30/07 391 Long Term pre-2007 HY Peak 1/1/97 to 6/30/07 149

Long Term Average from 12/31/1996 418 Long Term Average from 12/31/1996 174

Long Term Median from 12/31/1996 373 Long Term Median from 12/31/1996 152

Source: CreditSights, BofA/ML Indices data through 08/31/2015

62

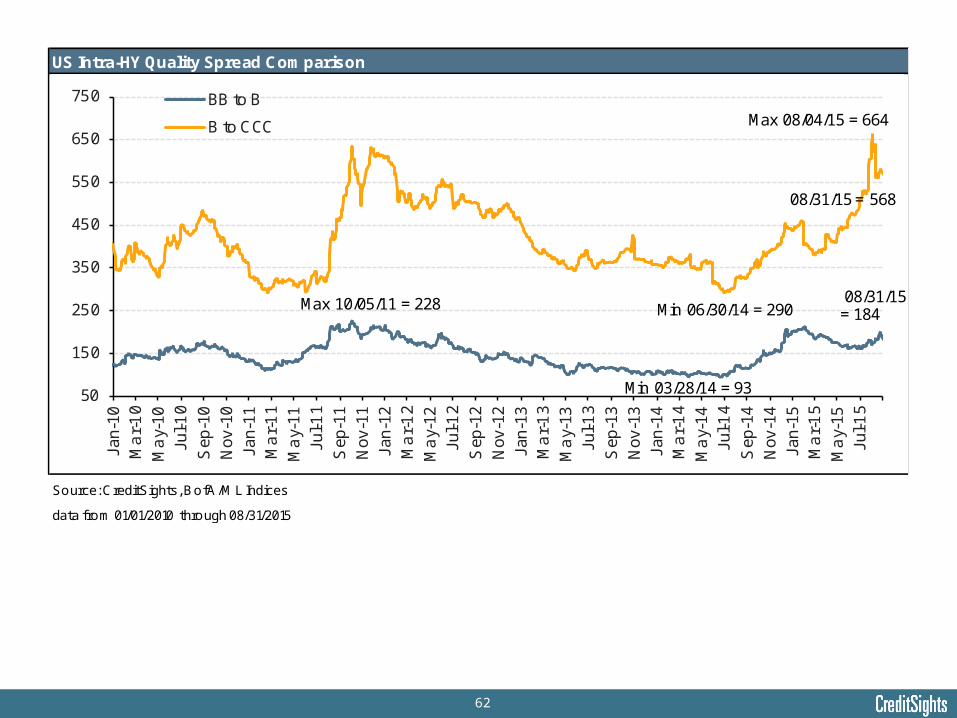

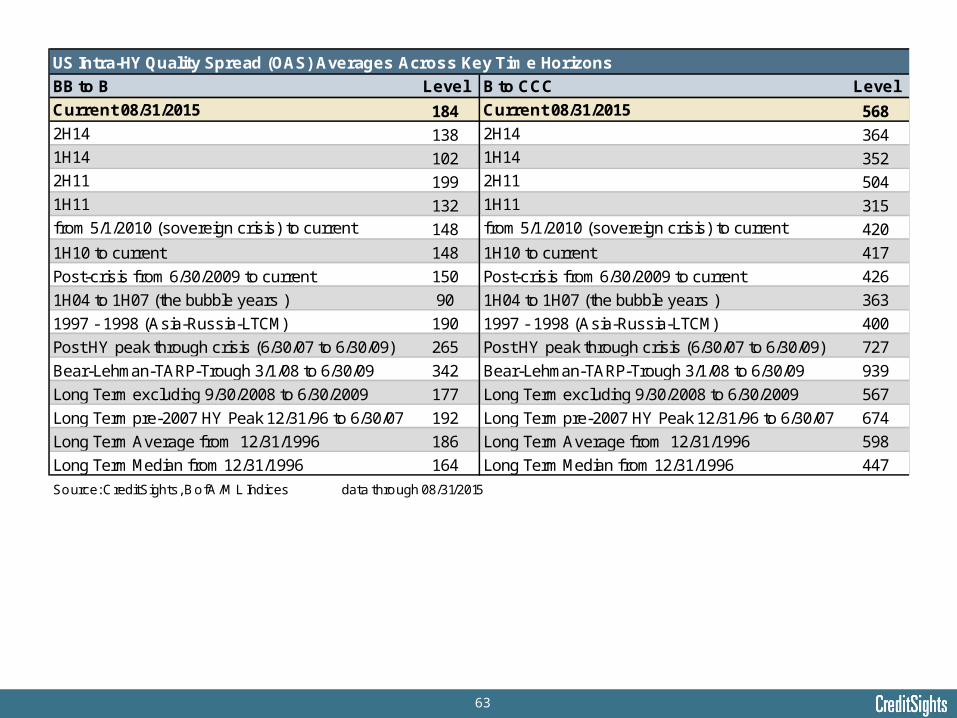

US Intra-HY Quality Spread Comparison

Source: CreditSights, BofA/ML Indices

data from 01/01/2010 through 08/31/2015

50

150

250

350

450

550

650

750Ja

n-10

Ma

r-1

0

Ma

y-10

Jul-1

0

Sep

-10

Nov

-10

Jan-

11M

ar-

11

Ma

y-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12M

ar-

12

Ma

y-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13M

ar-

13

Ma

y-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14M

ar-

14

Ma

y-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15M

ar-

15

Ma