Embed Size (px)

Citation preview

0

CFO Handbook

Publication Date: October 2019

1

CFO Handbook

Copyright © 2019 by

DELTACPE LLC

All rights reserved. No part of this course may be reproduced in any form or by any means, without permission

in writing from the publisher.

The author is not engaged by this text or any accompanying lecture or electronic media in the rendering of legal,

tax, accounting, or similar professional services. While the legal, tax, and accounting issues discussed in this ma-

terial have been reviewed with sources believed to be reliable, concepts discussed can be affected by changes in

the law or in the interpretation of such laws since this text was printed. For that reason, the accuracy and com-

pleteness of this information and the author's opinions based thereon cannot be guaranteed. In addition, state

or local tax laws and procedural rules may have a material impact on the general discussion. As a result, the

strategies suggested may not be suitable for every individual. Before taking any action, all references and cita-

tions should be checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the subject matter

covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or

other professional service. If legal advice or other expert advice is required, the services of a competent profes-

sional person should be sought.

—-From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a Com-

mittee of Publishers and Associations.

2

Course Description

The world of the CFO is in constant flux; today’s CFO is tomorrow’s CEO or chairman. The contemporary CFO

should be at the elbow of the CEO, a strategic partner and advisor to the CEO. To fulfill the expectations and ef-

fectively operate as a key member of the leadership team, CFOs need a broad perspective and a wide set of ca-

pabilities and skills. This course is designed to help CFOs and future aspiring CFOs in enhancing competence

through learning the tools and techniques that support sustainable business success. It also shares good practic-

es and ideas that apply in performing a CFO role. In particular, it contains the following topics:

• The changing and expanding role of the CFO and skills needed in the future

• Key topics in financial reporting such as revenue, leases, fixed assets, and inventory

• Accounting changes and error corrections and proper treatments of them

• Securities and Exchange Commission (SEC) filing requirements and its disclosure review process

• Cybersecurity disclosure requirements for public companies

• Sarbanes-Oxley Act key provisions and recommended compliance structure

• Asset and liability management (e.g., cash, accounts receivable, inventory)

• Financial planning processes including strategic planning and budgeting

• Analysis of cost behavior and cost prediction

• Forecasting techniques such as break-even analysis, contribution margin analysis, and margin of sale

• Capital investment analysis techniques (e.g., payback period, discount rate, internal rate of return)

• Analysis of financial statements including comparative financial statements and ratio analysis

• Risk management principles focused on enterprise risk management and the lines of defense model

• The basics of accounting for derivatives and hedge accounting

• The concept of risk and return of an investment and types of investments

• The Capital Asset Pricing Model

• Financial management strategies for multinational companies

• Features of modern accounting information systems (e.g. procure-to-pay, inventory optimization)

• Benefits of emerging technologies including Big Data, blockchain, robotic process automation, and cloud

• Performance management structure; balanced scorecard and key performance indicators

• Characteristics of a world-class finance organization

• Internal control principles including components, limitations, and types of controls

Field of Study Accounting

Level of Knowledge Basic to Intermediate

Prerequisite None

Advanced Preparation None

3

Table of Contents

INTRODUCTION .................................................................................................................................................................... i

PART I: PROFILING THE MODERN CFO................................................................................................................................ 1

Chapter 1: The CFO as a Strategic Partner ......................................................................................................................... 2

Learning Objectives: ................................................................................................................................................................ 2

The Roles and Expectations of the Modern CFO ...................................................................................................................... 3

The Changing Role of the CFO ............................................................................................................................................. 3

The Duties of a Modern CFO ............................................................................................................................................... 6

CFO vs. Controller ............................................................................................................................................................... 9

The Next-Generation CFO ...................................................................................................................................................... 11

Talent and Capability ........................................................................................................................................................ 11

Transformation in the Digital Age ..................................................................................................................................... 13

Chapter 1 Review Questions .................................................................................................................................................. 17

PART II: REPORTING VALUE .............................................................................................................................................. 18

Chapter 2: The Financial Statements ............................................................................................................................... 19

Learning Objectives ............................................................................................................................................................... 19

The Role of the CFO ............................................................................................................................................................... 19

Objectives of Financial Reporting .......................................................................................................................................... 20

The Common Financial Statements ....................................................................................................................................... 21

The Income Statement .......................................................................................................................................................... 23

Key Elements ..................................................................................................................................................................... 23

Income Statement Formats .............................................................................................................................................. 25

The Balance Sheet ................................................................................................................................................................. 27

Key Elements ..................................................................................................................................................................... 27

Balance Sheet Limitations ................................................................................................................................................. 30

Chapter 2 - Section 1 Review Questions ................................................................................................................................ 31

Statement of Cash Flows ....................................................................................................................................................... 32

Cash and Cash Equivalents ................................................................................................................................................ 32

Classification of Cash Flows .............................................................................................................................................. 33

Accrual Basis of Accounting .............................................................................................................................................. 38

Preparation of the Statement of Cash Flows .................................................................................................................... 39

Gross vs. Net Cash Flows ................................................................................................................................................... 43

IFRS Differences Affecting the Statement of Cash Flows ....................................................................................................... 45

4

Notes to Financial Statements ............................................................................................................................................... 45

Chapter 2 - Section 2 Review Questions ................................................................................................................................ 46

Chapter 3: Principles of Financial Reporting .................................................................................................................... 47

Learning Objectives: .............................................................................................................................................................. 47

The Role of the CFO ............................................................................................................................................................... 47

Financial Accounting vs. Management Accounting .............................................................................................................. 48

Key Financial Accounting Areas ............................................................................................................................................. 49

Revenue Recognition ........................................................................................................................................................ 49

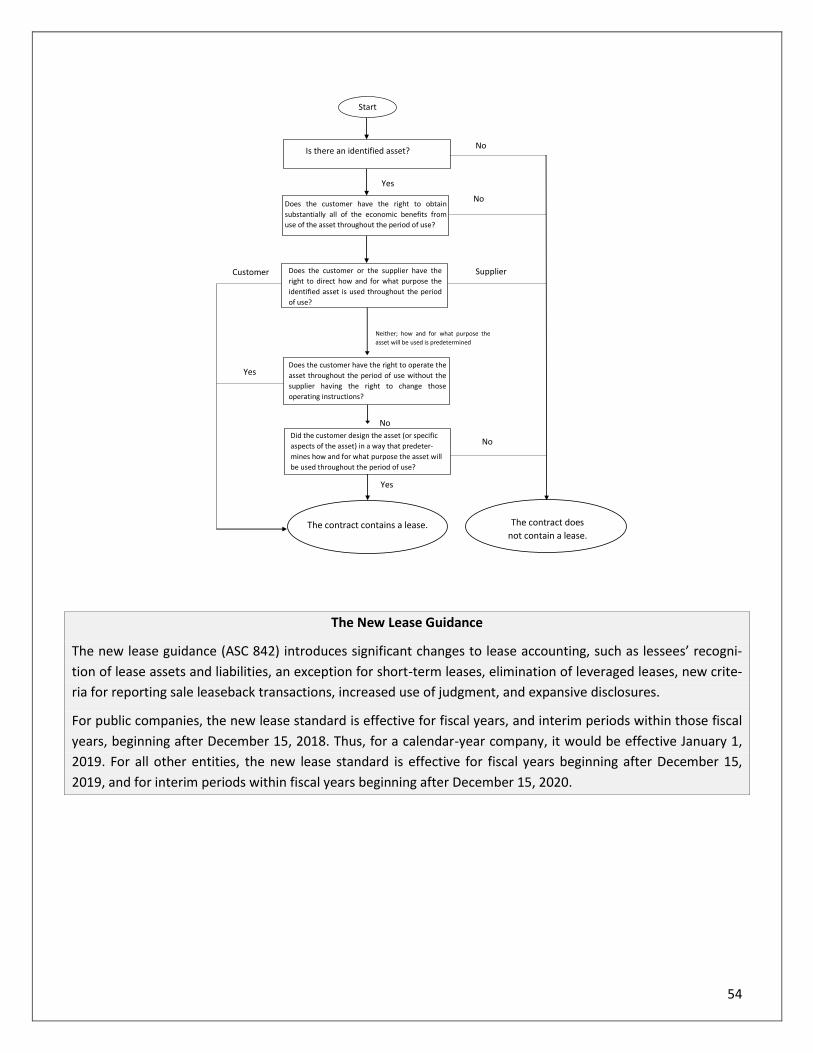

Leases ................................................................................................................................................................................ 53

Consolidation .................................................................................................................................................................... 58

Chapter 3 Section 1 Review Questions ................................................................................................................................. 63

Key Financial Accounting Areas ............................................................................................................................................. 64

Fixed Assets ....................................................................................................................................................................... 64

Inventory ........................................................................................................................................................................... 68

Earnings per Share ............................................................................................................................................................ 71

Accounting Changes and Error Corrections ........................................................................................................................... 75

Definition of Accounting Changes ..................................................................................................................................... 75

Change in Accounting Principle ......................................................................................................................................... 76

Change in Accounting Estimate ........................................................................................................................................ 81

Change in Reporting Entity ............................................................................................................................................... 82

Correction of an Error ....................................................................................................................................................... 83

Chapter 3 - Section 2 Review Questions ................................................................................................................................ 86

PART III: ENSURING REGULATORY COMPLIANCE .............................................................................................................. 87

Chapter 4: Securities and Exchange Commission Filings ................................................................................................. 88

Learning Objectives: .............................................................................................................................................................. 88

The Role of the CFO ............................................................................................................................................................... 88

Periodic Reporting Requirements .......................................................................................................................................... 89

Accelerated Filer vs. Non-Accelerated Filer Status ........................................................................................................... 89

Major Corporate Forms .................................................................................................................................................... 89

Segmental Reporting ......................................................................................................................................................... 93

The Failure of (or Late) Filing ............................................................................................................................................ 95

Cybersecurity Disclosure Requirements ................................................................................................................................. 96

Risk Factors ....................................................................................................................................................................... 96

MD&A................................................................................................................................................................................ 97

Financial Statement Disclosures ....................................................................................................................................... 98

The SEC Disclosure Review Process ........................................................................................................................................ 99

The Scope of Review ......................................................................................................................................................... 99

5

The Review Process ......................................................................................................................................................... 101

Chapter 4 Review Questions ................................................................................................................................................ 105

Chapter 5: The Sarbanes-Oxley Act ............................................................................................................................... 106

Learning Objectives: ............................................................................................................................................................ 106

The Role of the CFO ............................................................................................................................................................. 106

SOX Section 404 − Management Assessment of Internal Controls ..................................................................................... 107

Evaluation of Control Deficiency ..................................................................................................................................... 107

Examples of Significant Deficiencies and Material Weaknesses ..................................................................................... 109

Management Internal Control Report ............................................................................................................................ 111

Assessment of Process Maturity for Internal Control over Financial Reporting ............................................................. 113

SOX Section 302 − Corporate Responsibility for Financial Reports ...................................................................................... 116

SOX Section 906 − Corporate Responsibility for Financial Reports ...................................................................................... 117

Alternative Sarbanes-Oxley Compliance Structures ............................................................................................................ 118

Chapter 5 Review Questions ................................................................................................................................................ 121

PART IV: ASSET AND LIABILITY MANAGEMENT .............................................................................................................. 122

Chapter 6: Working Capital and Cash Management ...................................................................................................... 123

Learning Objectives ............................................................................................................................................................. 123

The Role of the CFO ............................................................................................................................................................. 123

The Concept of Working Capital .......................................................................................................................................... 124

Cash Management .............................................................................................................................................................. 125

The Significance of Cash Management ........................................................................................................................... 125

Techniques for Optimizing Cash...................................................................................................................................... 126

Opportunity Cost of Foregoing a Cash Discount ............................................................................................................. 131

Accounts Receivable Management ..................................................................................................................................... 132

Inventory Management ....................................................................................................................................................... 134

Accounts Payable Management .......................................................................................................................................... 135

Chapter 6 Review Questions ................................................................................................................................................ 137

PART V: PROVIDING STRATEGIC FINANCE SUPPORT AND ANALYSIS .............................................................................. 138

Chapter 7: The Financial Planning Process .................................................................................................................... 139

Learning Objectives ............................................................................................................................................................. 139

The Role of the CFO ............................................................................................................................................................. 139

Strategic Planning ............................................................................................................................................................... 140

The Concept of Strategic Planning .................................................................................................................................. 140

6

Short-Term Plans ............................................................................................................................................................. 141

Long-Term Plans .............................................................................................................................................................. 141

Budgeting for Planning and Control .................................................................................................................................... 142

The Concept of Budgeting ............................................................................................................................................... 142

Budgetary Process ........................................................................................................................................................... 143

Types of Budgets ............................................................................................................................................................. 144

Types of Budget Reports ................................................................................................................................................. 150

Other Considerations ...................................................................................................................................................... 152

Chapter 7 Review Questions ................................................................................................................................................ 156

Chapter 8: Financial Forecasting Techniques ................................................................................................................. 157

Learning Objectives: ............................................................................................................................................................ 157

The Role of the CFO ............................................................................................................................................................. 157

Analysis of Cost Behavior and Cost Prediction..................................................................................................................... 158

Costs by Behavior ............................................................................................................................................................ 158

Methods for Estimating Costs ......................................................................................................................................... 160

Break-Even and Contribution Margin Analysis .................................................................................................................... 163

The Concept of Cost-Volume-Profit Analysis .................................................................................................................. 163

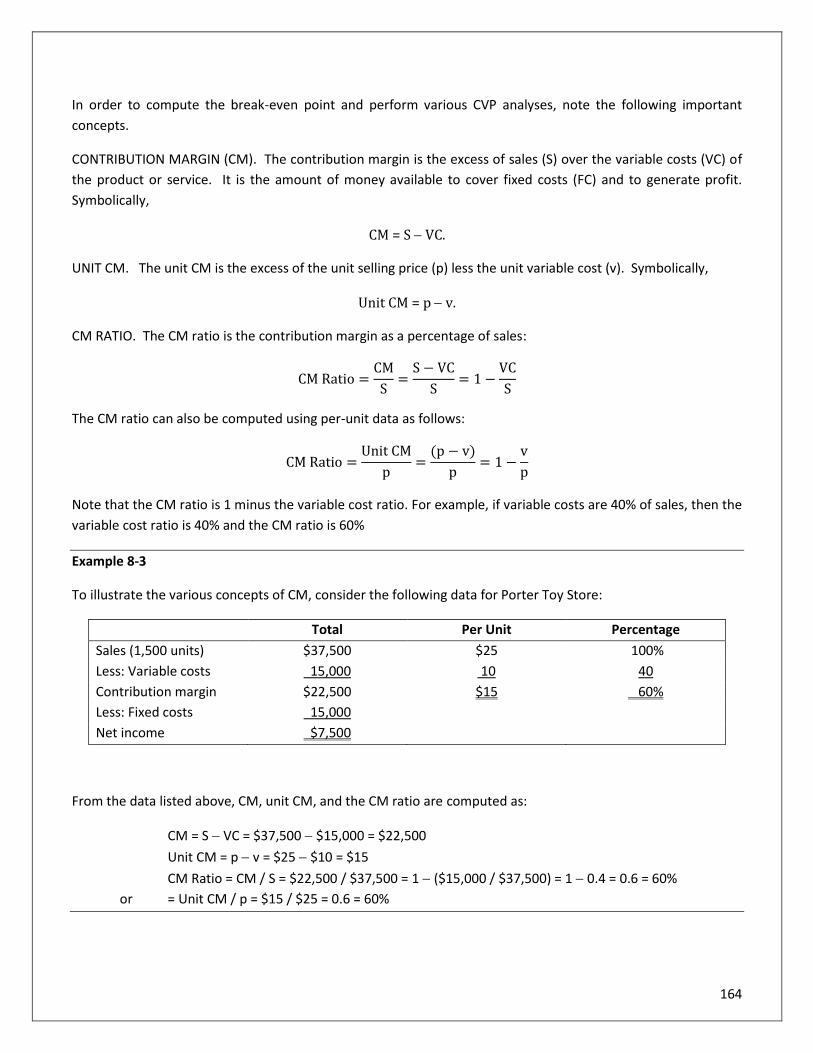

Contribution Margin (CM) ............................................................................................................................................... 163

Break-Even Analysis ........................................................................................................................................................ 165

Margin of Safety .............................................................................................................................................................. 167

Sales Mix Analysis ........................................................................................................................................................... 168

Chapter 8 Review Questions ................................................................................................................................................ 170

Chapter 9: Capital Investment Analysis ......................................................................................................................... 171

Learning Objectives ............................................................................................................................................................. 171

The Role of the CFO ............................................................................................................................................................. 171

The Concept of Capital Budgeting ....................................................................................................................................... 172

The Definition of Capital Budgeting ................................................................................................................................ 172

Types of Long-Term Investment Decisions ..................................................................................................................... 172

Features of Investment Projects ..................................................................................................................................... 173

The Uses of Capital Budgeting ........................................................................................................................................ 173

Techniques for Evaluating Investment Proposals ................................................................................................................ 174

Discount Rate .................................................................................................................................................................. 174

Payback Period ................................................................................................................................................................ 177

Discounted Payback Period ............................................................................................................................................. 178

Accounting Rate of Return .............................................................................................................................................. 179

Net Present Value ........................................................................................................................................................... 180

Internal Rate of Return ................................................................................................................................................... 181

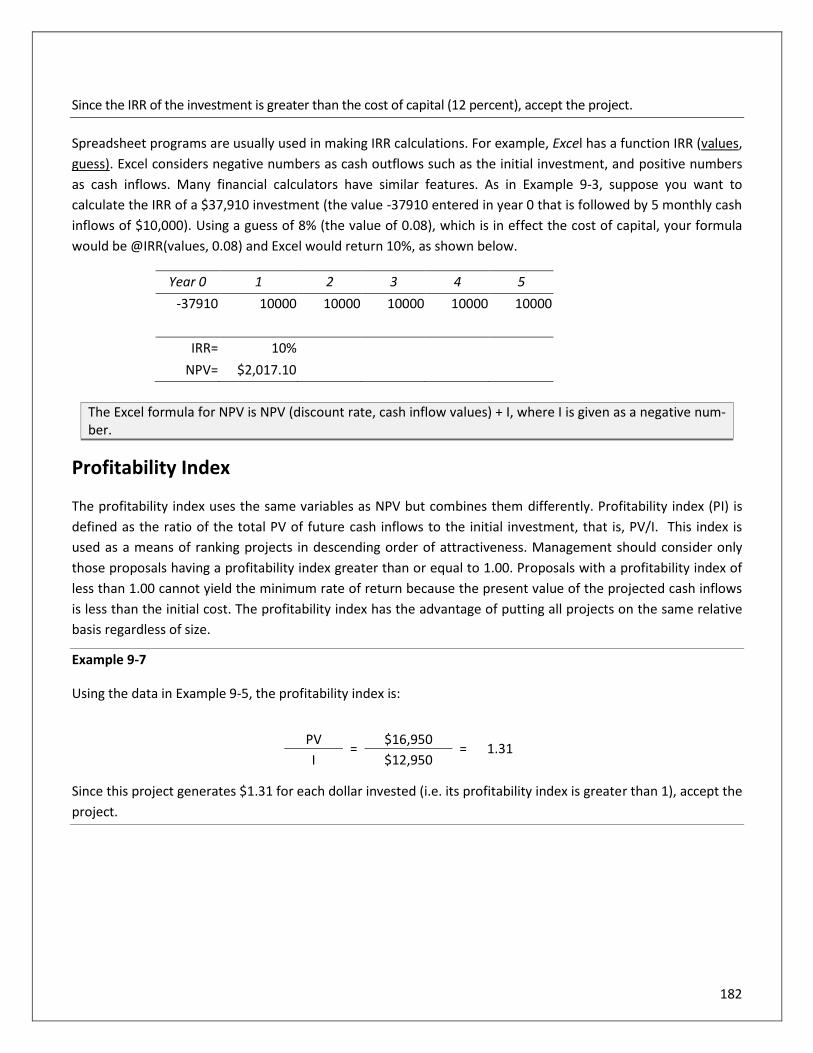

Profitability Index ............................................................................................................................................................ 182

Capital Rationing ................................................................................................................................................................. 183

7

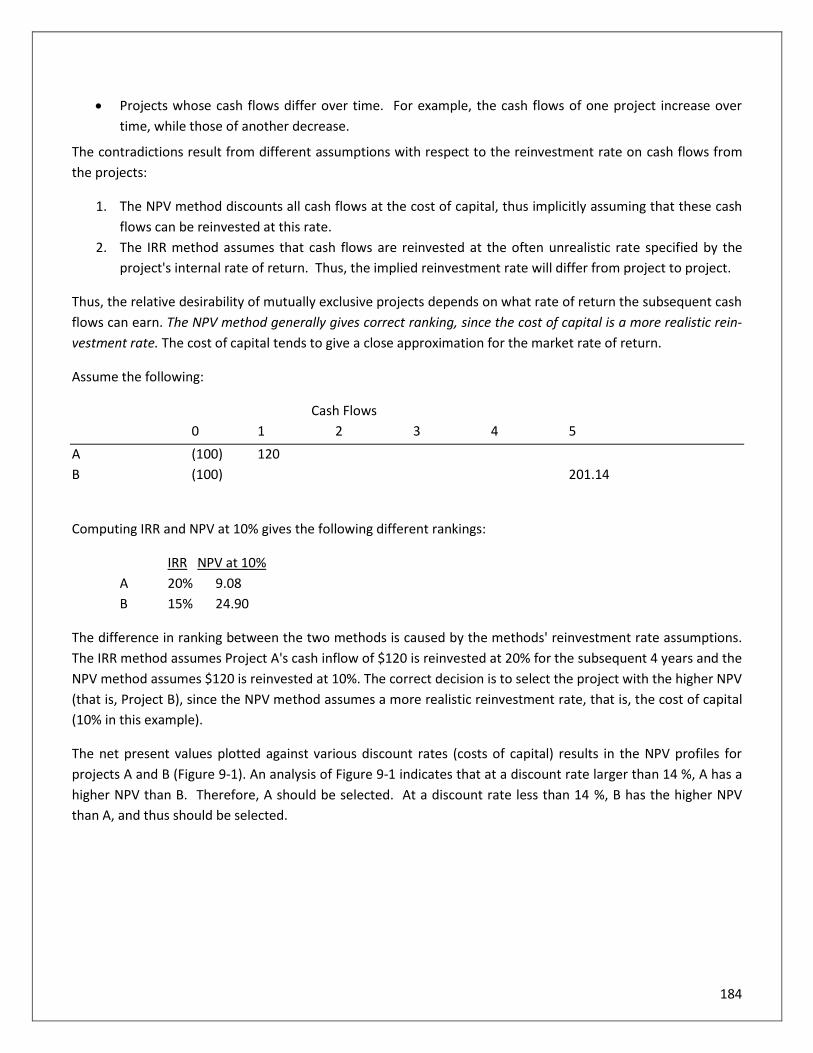

Selecting the Best Mix of Projects with a Limited Budget .............................................................................................. 183

Handling Mutually Exclusive Investments....................................................................................................................... 183

Income Taxes and Investment Decisions ............................................................................................................................. 185

Chapter 9 Review Questions ................................................................................................................................................ 187

Chapter 10: Financial Statement Analysis ..................................................................................................................... 188

Learning Objectives: ............................................................................................................................................................ 188

The Role of the CFO ............................................................................................................................................................. 188

Techniques of Financial Analysis ......................................................................................................................................... 189

Comparative Financial Statements ................................................................................................................................. 189

Ratio Analysis .................................................................................................................................................................. 195

The Operating Cycle of a Business ....................................................................................................................................... 198

Chapter 10 - Section 1 Review Questions ............................................................................................................................ 200

Evaluation of Financial Outcomes ....................................................................................................................................... 201

Liquidity Ratios: Analyzing Short-Term Cash Needs ....................................................................................................... 201

Activity Ratios: Analyzing the Efficient Use of Assets ..................................................................................................... 202

Leverage Ratios: Measuring the Ability to Pay Long-Term Debt .................................................................................... 205

Profitability Ratios: Analyzing Operating Activities ......................................................................................................... 206

Market Ratios: Analyzing Financial Returns to Investors ................................................................................................ 215

Cash Flow Coverage (Adequacy) Ratios .......................................................................................................................... 218

Chapter 10 - Section 2 Review Questions ............................................................................................................................ 221

PART VI: OPTIMIZING PROFITABILITY AND MITIGATING RISKS ...................................................................................... 222

Chapter 11: Risk Management Strategy ........................................................................................................................ 223

Learning Objectives: ............................................................................................................................................................ 223

The Role of the CFO ............................................................................................................................................................. 223

Enterprise Risk Management Principles .............................................................................................................................. 224

Key Concepts of Risk Management ................................................................................................................................. 225

Enterprise Risk Management vs. Traditional Risk Management Approaches ................................................................ 228

Components of Enterprise Risk Management ................................................................................................................ 232

The Risk Assessment Process .......................................................................................................................................... 233

Other Considerations ...................................................................................................................................................... 240

The Three Lines of Defense Model ....................................................................................................................................... 242

The First Line of Defense ................................................................................................................................................. 244

The Second Line of Defense ............................................................................................................................................ 244

The Third Line of Defense ............................................................................................................................................... 244

Other Considerations ...................................................................................................................................................... 246

Fraud Risk Assessment ........................................................................................................................................................ 246

Chapter 11 Review Questions .............................................................................................................................................. 248

8

Chapter 12: Derivative Instruments and Hedge Accounting ......................................................................................... 249

Learning Objectives: ............................................................................................................................................................ 249

The Role of the CFO ............................................................................................................................................................. 249

Derivatives and Hedge ......................................................................................................................................................... 250

The Characteristics of Derivative Instruments ................................................................................................................ 250

Concepts of Hedge Accounting ....................................................................................................................................... 252

Principles of Hedge Accounting ........................................................................................................................................... 253

Hedge Criteria ................................................................................................................................................................. 253

Types of Hedges .............................................................................................................................................................. 254

Chapter 12 Review Questions .............................................................................................................................................. 259

Chapter 13: Corporate Investments .............................................................................................................................. 260

Learning Objectives: ............................................................................................................................................................ 260

The Role of the CFO ............................................................................................................................................................. 260

Risk vs. Return ..................................................................................................................................................................... 261

Types of Investments ........................................................................................................................................................... 264

The Capital Asset Pricing Model (CAPM) ............................................................................................................................. 269

Chapter 13 Review Questions .............................................................................................................................................. 272

Chapter 14: International Finance ................................................................................................................................. 273

Learning Objectives: ............................................................................................................................................................ 273

The Role of the CFO ............................................................................................................................................................. 273

Essentials for Multinational Corporations ........................................................................................................................... 274

The Features of MNCs ..................................................................................................................................................... 274

The Types of Foreign Operations .................................................................................................................................... 274

Types of International Risks ................................................................................................................................................. 275

Currency Risk ................................................................................................................................................................... 275

Political and Credit Risk ................................................................................................................................................... 277

Foreign Exchange Rate Determination ................................................................................................................................ 278

Direct vs. Indirect Quotation ........................................................................................................................................... 278

Spot vs. Forward Exchange Rates ................................................................................................................................... 278

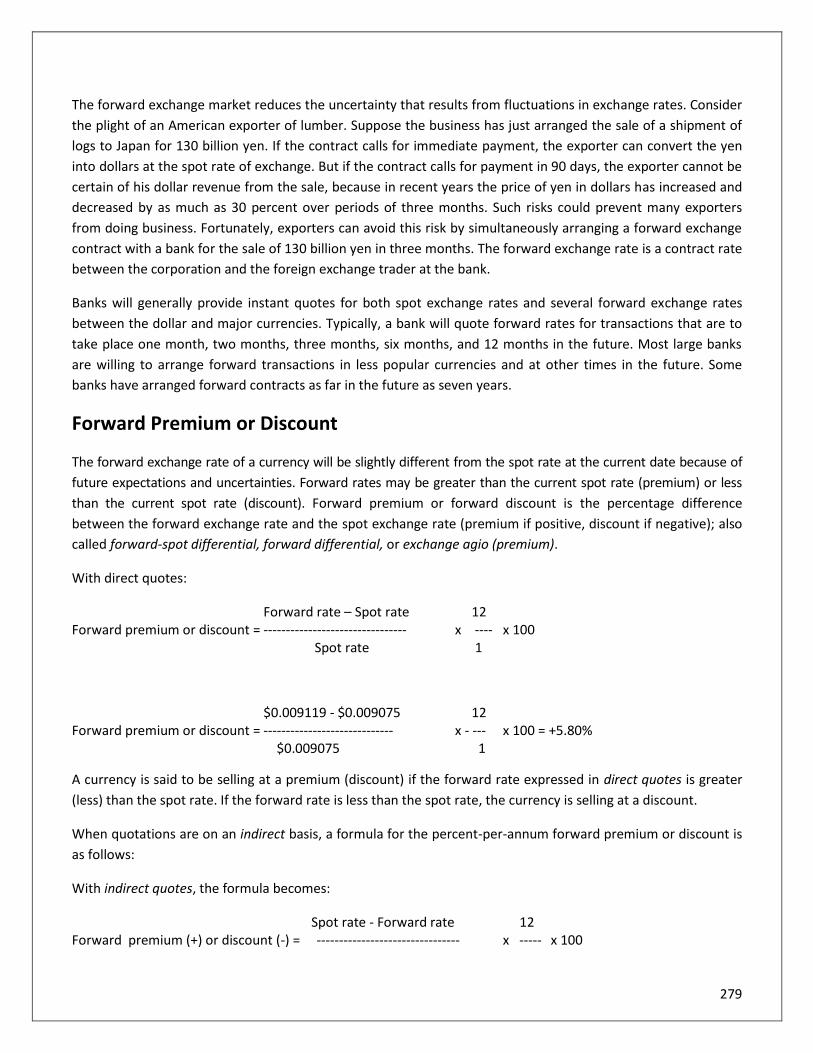

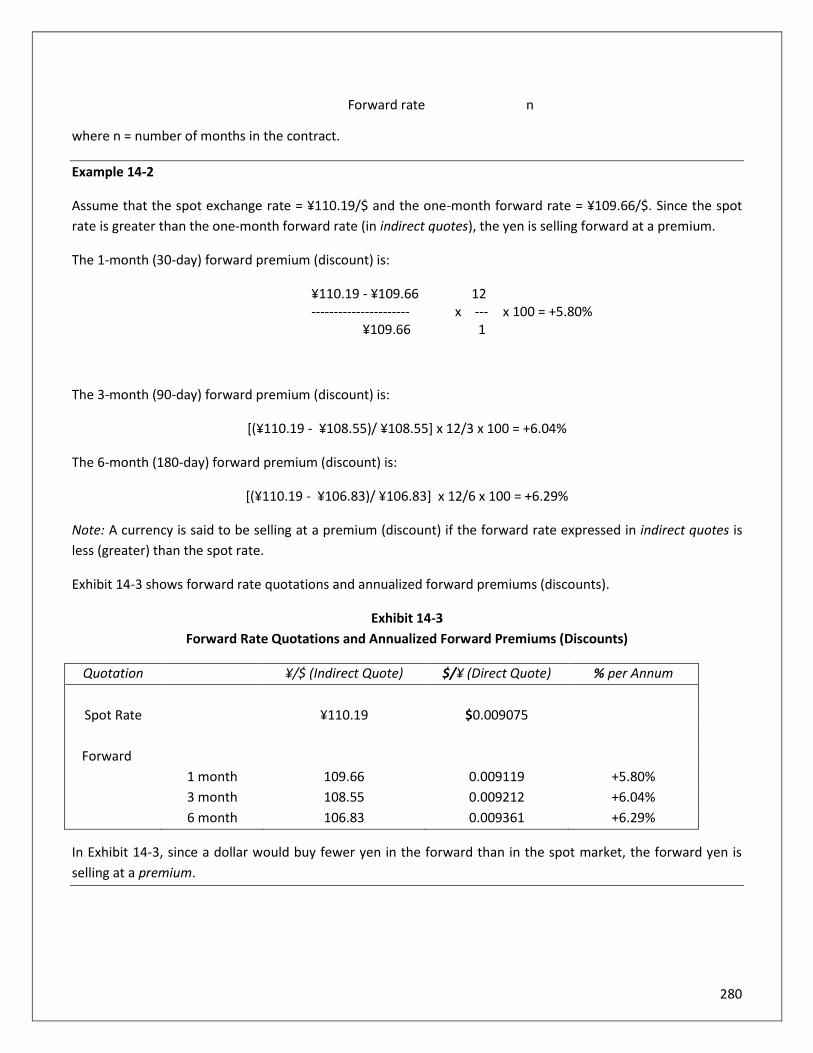

Forward Premium or Discount ........................................................................................................................................ 279

Cross Rates ...................................................................................................................................................................... 281

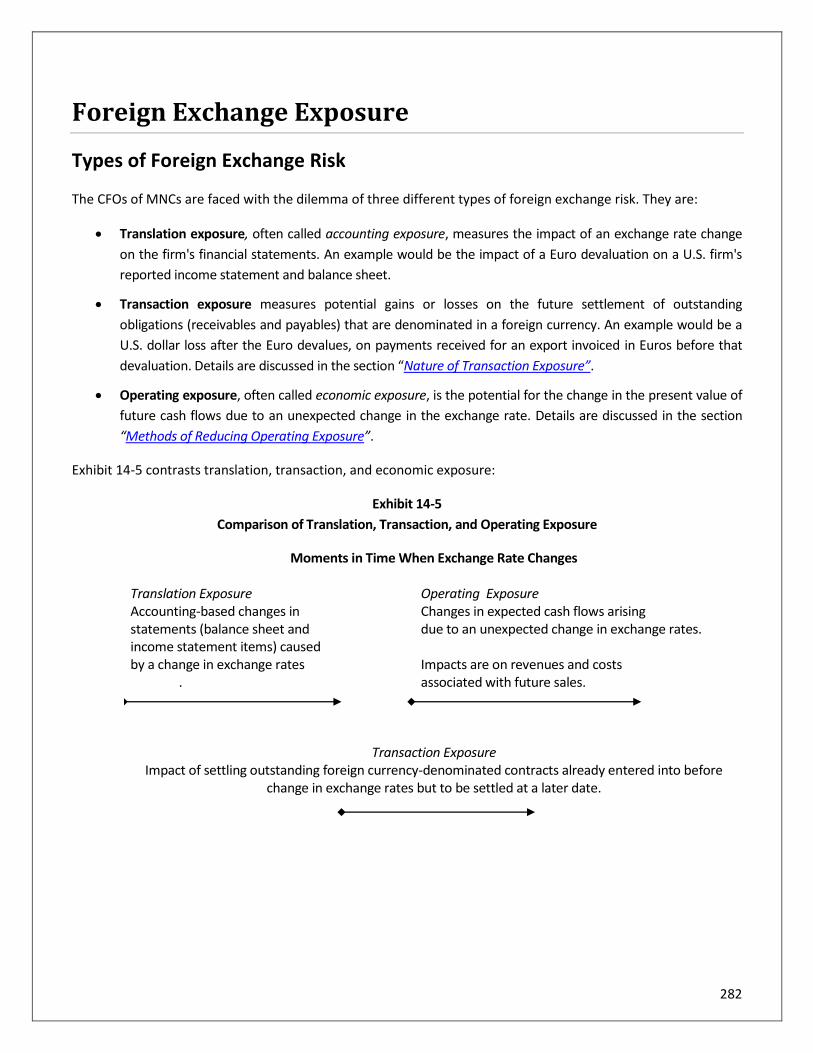

Foreign Exchange Exposure ................................................................................................................................................. 282

Types of Foreign Exchange Risk ...................................................................................................................................... 282

Ways to Neutralize Foreign Exchange Risk ..................................................................................................................... 283

Nature of Transaction Exposure .......................................................................................................................................... 285

Transferring Exposure ..................................................................................................................................................... 285

9

Net Transaction Exposure ............................................................................................................................................... 285

Methods of Reducing Operating Exposure .......................................................................................................................... 286

Matching Cash Flows ...................................................................................................................................................... 286

Global Diversification ...................................................................................................................................................... 286

Financing Strategies ........................................................................................................................................................ 287

Chapter 14 Review Questions .............................................................................................................................................. 288

PART VII: ACHIEVING OPERATIONAL EXCELLENCE ........................................................................................................... 289

Chapter 15: Information Technology ............................................................................................................................. 290

Learning Objectives ............................................................................................................................................................. 290

The Role of the CFO ............................................................................................................................................................. 290

Accounting Information Systems ......................................................................................................................................... 291

Credit and Collection Management ................................................................................................................................ 291

Procure-to-Pay ................................................................................................................................................................ 292

Fixed Asset System .......................................................................................................................................................... 294

Inventory Optimization Software .................................................................................................................................... 296

Modern Close Software .................................................................................................................................................. 297

E-Budgeting ..................................................................................................................................................................... 299

Leveraging Technology ........................................................................................................................................................ 300

Advanced Data Analytics ................................................................................................................................................. 300

Blockchain Technology .................................................................................................................................................... 301

Robotic Process Automation ........................................................................................................................................... 302

Cloud Computing ............................................................................................................................................................ 304

Chapter 15 Review Questions .............................................................................................................................................. 308

Chapter 16: Performance Management ........................................................................................................................ 309

Learning Objectives ............................................................................................................................................................. 309

The Role of the CFO ............................................................................................................................................................. 309

Balanced Scorecard ............................................................................................................................................................. 309

The Concept of Balanced Scorecard ............................................................................................................................... 309

The Four Dimensions of Performance ............................................................................................................................ 311

Key Performance Indicators ................................................................................................................................................. 314

The Development of Performance Measures ................................................................................................................. 314

Performance Measures that Every CFO Should Know .................................................................................................... 315

Benchmarking ...................................................................................................................................................................... 317

Chapter 16 Review Questions .............................................................................................................................................. 319

Chapter 17: Modern Finance Organizations .................................................................................................................. 320

Learning Objectives ............................................................................................................................................................. 320

10

The Role of the CFO ............................................................................................................................................................. 320

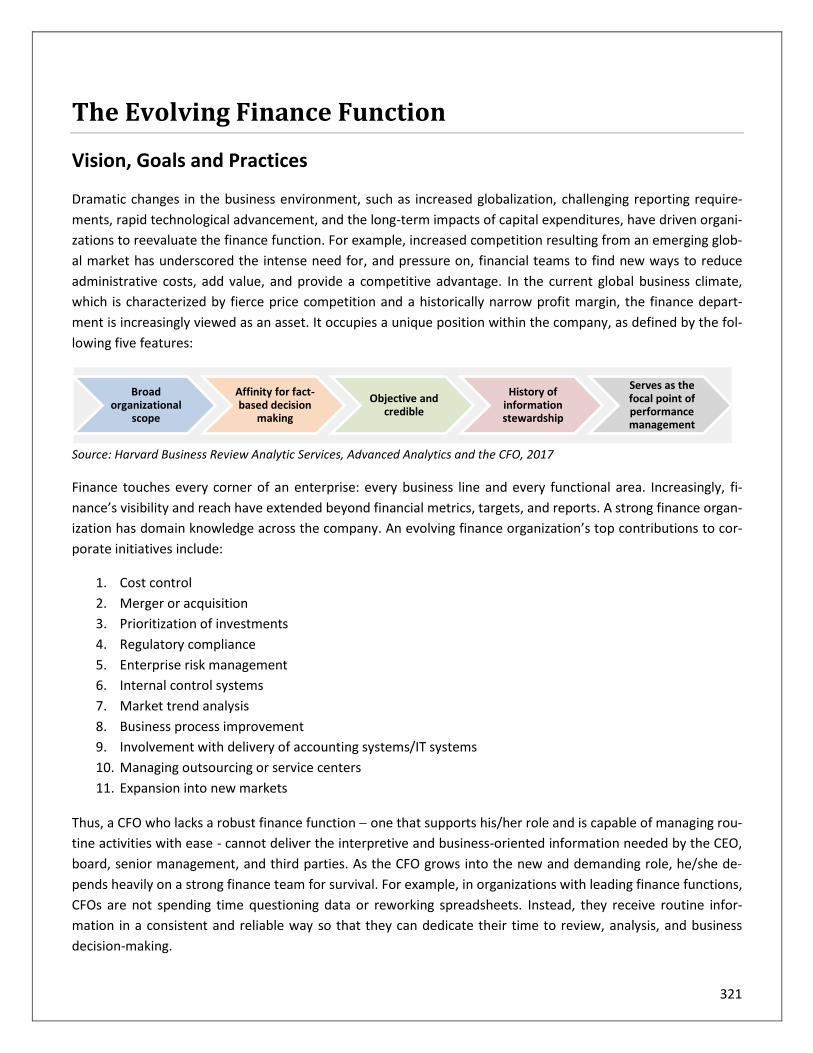

The Evolving Finance Function ............................................................................................................................................ 321

Vision, Goals and Practices ............................................................................................................................................. 321

Characteristics of a World-Class Finance Organization ................................................................................................... 323

Building Effective Internal Control Systems ......................................................................................................................... 324

Elements of Internal Control Systems ............................................................................................................................. 324

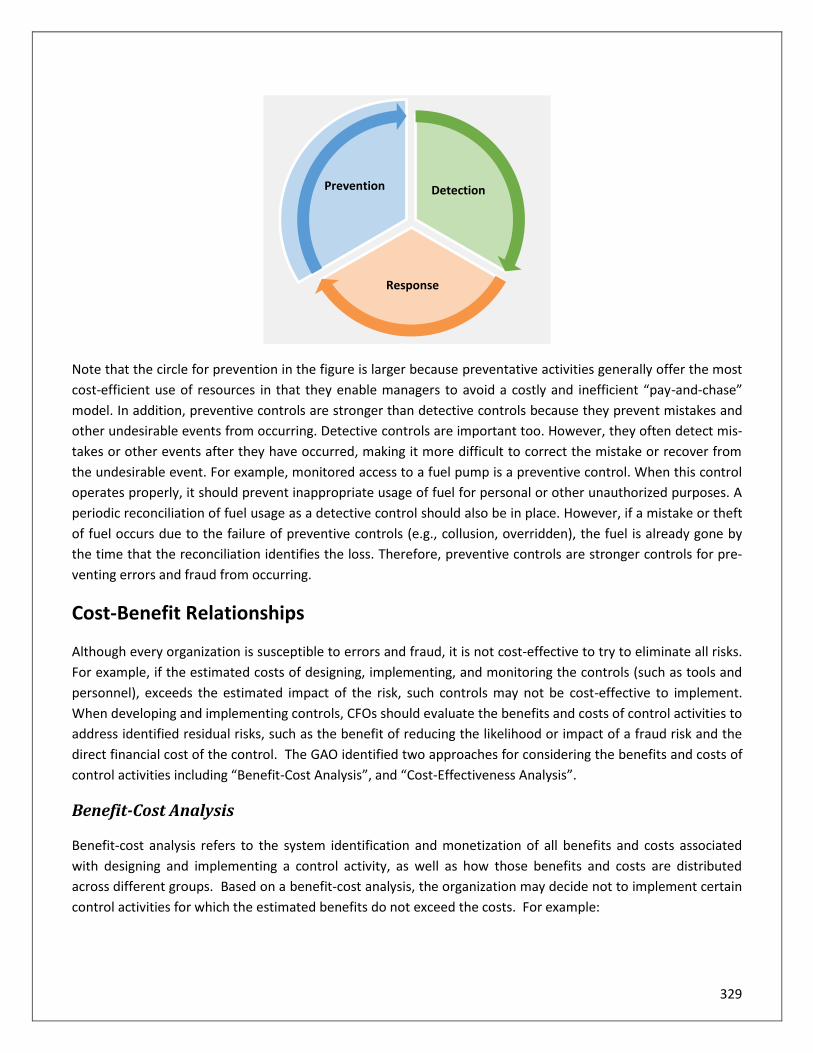

Limitations of Internal Controls ...................................................................................................................................... 327

Types of Internal Controls ............................................................................................................................................... 327

Cost-Benefit Relationships .............................................................................................................................................. 329

Chapter 17 Review Questions .............................................................................................................................................. 331

Appendix A: Best Practices of Disclosing Material Cybersecurity Breach ........................................................................ 332

Appendix B: Financial Statement Disclosure − Data Breach ............................................................................................. 333

Appendix C: Examples of Circumstances that May be Deficiencies, Significant Deficiencies, or Material Weaknesses .... 335

Deficiencies in the Design of Controls .................................................................................................................................. 335

Failures in the Operation of Internal Control ....................................................................................................................... 336

Appendix D: A List of Questions Management Needs to Answer for Sarbanes-Oxley Compliance ................................... 337

Appendix E: Example of a Statement of Risk Management Vision, Mission, Goals and Objectives .................................. 338

Appendix F: Three Lines of Defense - Recommended Practices by COSO ......................................................................... 339

Appendix G: Financial Statement Disclosure - Derivative Financial Instruments and Hedging Activities .......................... 341

Appendix H: International Business Planning Checklist.................................................................................................... 345

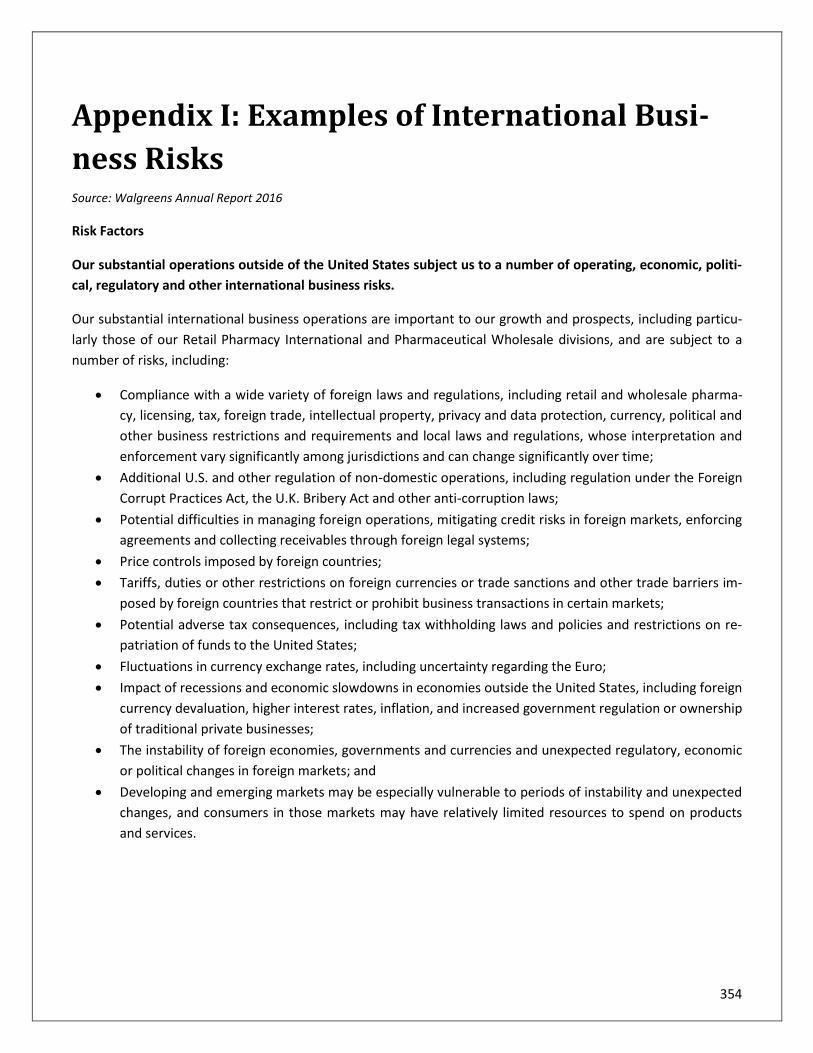

Appendix I: Examples of International Business Risks ...................................................................................................... 354

Appendix J: Developing an Automation Strategy ............................................................................................................ 355

Solutions to Review Questions ........................................................................................................................................ 356

Chapter 1 Review Questions ................................................................................................................................................ 356

Chapter 2 Section 1 Review Questions ................................................................................................................................ 357

Chapter 2 Section 2 Review Questions ................................................................................................................................ 358

Chapter 3 Section 1 Review Questions ................................................................................................................................ 359

Chapter 3 Section 2 Review Questions ................................................................................................................................ 361

Chapter 4 Review Questions ................................................................................................................................................ 362

Chapter 5 Review Questions ................................................................................................................................................ 364

Chapter 6 Review Questions ................................................................................................................................................ 365

11

Chapter 7 Review Questions ................................................................................................................................................ 367

Chapter 8 Review Questions ................................................................................................................................................ 368

Chapter 9 Review Questions ................................................................................................................................................ 369

Chapter 10 Section 1 Review Questions .............................................................................................................................. 370

Chapter 10 Section 2 Review Questions .............................................................................................................................. 372

Chapter 11 Review Questions .............................................................................................................................................. 374

Chapter 12 Review Questions .............................................................................................................................................. 375

Chapter 13 Review Questions .............................................................................................................................................. 376

Chapter 14 Review Questions .............................................................................................................................................. 377

Chapter 15 Review Questions .............................................................................................................................................. 379

Chapter 16 Review Questions .............................................................................................................................................. 380

Chapter 17 Review Questions .............................................................................................................................................. 381

Glossary ........................................................................................................................................................................... 383

Index ............................................................................................................................................................................... 388

i

INTRODUCTION In the changing business landscape where volatility, uncertainty, risk, and disruption are becoming more preva-

lent, the role of the CFO has undergone an evolution. CFOs continue to be stretched and scrutinized. In addition

to financial reporting, planning and analysis, CEOs and boards expect the CFO to contribute to the major deci-

sions, such as growth strategy, risk management strategy, and investment strategy. Key issues and emerging

priorities affecting the future role of the CFO include:

• A spotlight on talent, capability and behaviors in the top finance role (Part I)

• An enhanced financial reporting to promote transparency, accuracy, and compliance (Part II)

• An increasing personal stake in, and accountability for, regulatory adherence and compliance (Part III)

• The appropriate policies of capital investment, cash availability and shareholder return (Part IV and Part V )

• The necessity of controlling cost, managing risk and maintaining liquidity (Part IV and Part VI)

• An ability to support, monitor, and provide assistance in the execution of budgets and forecasts (Part V)

• Higher expectations from other stakeholders on the adequacy of financial plans (Part V)

• A greater scrutiny of the effectiveness of risk management approaches (Part VI)

• The ability to calibrate business risks and to advise on appropriate actions (Part VI)

• Effective hedges against market risks (e.g., interest rate risk, foreign exchange risk) using derivatives (Part

VI)

• A need to develop a finance department that works effectively on the global stage (Part VI)

• The incorporation of new technologies to improve finance processes and drive business insight (Part VII)

• A growing pressure to transform the finance functions to drive better customer service (Part VII)

• The need to implement and monitor effective internal control systems (Part VII)

This course is designed to help CFOs navigate these issues. It is divided into seven parts, which provide guidance

to the issues faced by the CFO and the finance and accounting functions.

Part I: Profiling the Modern CFO (Chapter 1) details principles guiding the role and expectations of a CFO. It cap-

tures the key requirements including the key competencies required by CFOs today and for tomorrow. It also

describes the ever-expanding role of the CFO, and how CFOs are transforming their departments and revamping

their teams to deal with the growing complexity.

Part II: Reporting Value (Chapters 2-3) covers the objectives and uses of financial statements. It also discusses

the key financial accounting requirements including revenue recognition, leases, consolidation, fixed assets, in-

ventory, and earnings per share. The different types of accounting changes and errors are also noted.

Part III: Ensuring Regulatory Compliance (Chapters 4-5) addresses one of the most fundamental roles of CFOs -

ensuring compliance with financial controls and financial reporting requirements. It focuses on the Securities

and Exchange Commission (SEC) filing requirements and key provisions of the Sarbanes-Oxley Act. It covers the

SEC disclosure review process to help CFOs respond to any potential SEC queries, including areas where the SEC

staff may challenge the accounting treatment or request enhanced disclosure.

ii

Part IV: Asset and Liability Management (Chapter 6) shares insights into managing cash, receivables, inventory

and accounts payable to order to support the CFO in maximizing return and minimizing the liquidity and busi-

ness risk.

Part V: Providing Strategic Finance Support and Analysis (Chapters 7-10) focuses on the planning required so

that CFOs can provide assistance in the budgetary and forecasting process. It highlights forecasting techniques,

including break-even analysis, contribution margin analysis, margin of sale, and sales mix analysis, in order to

support CFOs in strategy formulation. It also introduces the general concepts behind capital budgeting, along

with six methods for selecting the best alternatives among capital projects. Finally, it discusses the most com-

mon financial ratios (e.g., profit margin, inventory ratio, debt ratio) that allow the CFO to evaluate various as-

pects of a company’s operating and financial performance.

Part VI: Optimizing Profitability and Mitigating Risks (Chapters 11-14) deals with how to establish robust risk

management practices. It addresses what CFOs should know about the principles of enterprise risk manage-

ment, the concept of the ‘lines of defense’ model, and the importance of fraud risk assessment. Moreover, it

covers the basics of hedge accounting, a useful tool for organizations that experience financial statement volatil-

ity. It also recognizes the risks associated with derivatives. The types of risks applied to designing a portfolio are

identified. A sophisticated value-based analytics (the Capital Asset Pricing Model), is introduced as well. The fi-

nancial management of overseas operations for multinational companies is explained. Finally, strategies for

managing foreign exchange exposure are highlighted.

Part VII: Achieving Operational Excellence (Chapters 15-17) discusses how modern CFOs should embrace new

technologies to reduce costs, improve operational efficiency and strengthen processes. It also explores the

anatomy of a Balanced Scorecard strategy to support CFOs in creating an action plan to move them from an or-

ganization that just reports to an organization that drives business performance with key performance indica-

tors. It discusses some common performance measures used by accounting professionals as well. Finally, it fo-

cuses on the practices that today’s best-in-class CFOs follow and insights into building an effective internal con-

trol framework.

1

PART I:

PROFILING

THE MODERN CFO

2

Chapter 1: The CFO as a Strategic Partner

Learning Objectives:

After completing this section, you will be able to:

• Identify the key responsibilities of the CFO position

• Recognize the changing role and expectations of today’s CFO

• Differentiate between the role of a CFO and controller

Prior to the 1990s, the CFO’s role was typically the gatekeeper of the financial health of an organization, over-

seeing the financial controls and infrastructure. Since then, the range of responsibilities has expanded due to an

increased competitive marketplace. CFO’s must respond to rapid changes, such as new national and interna-

tional financial regulations and procedures, the updates to industry practices, and the effects of the global

economy. As a result, CFOs are under pressure to deliver fast and reliable reporting to management and stake-

holders.

CFOs know that they can no longer just assume their traditional role. Instead, for CFOs to deliver value as their

duties evolve, they must build skills in other areas of the business; playing a more active leadership role, rethink-

ing their usual approaches to overcoming external pressures, and finding new investment opportunities. Faced

with increasing demands and limited resources, CFOs must find ways to increase the efficiency and effectiveness

of the finance department.

This chapter explains who CFOs are, what they do, and why it matters. You will find the answers to questions

that are of interest to the CFO, such as:

• How is the CFO role evolving?

• What is the most critical expertise, knowledge, and experience to assuming the role of CFO?

• What are key development areas for aspiring finance leaders?

• How does emerging technology transform the role of CFO?

3

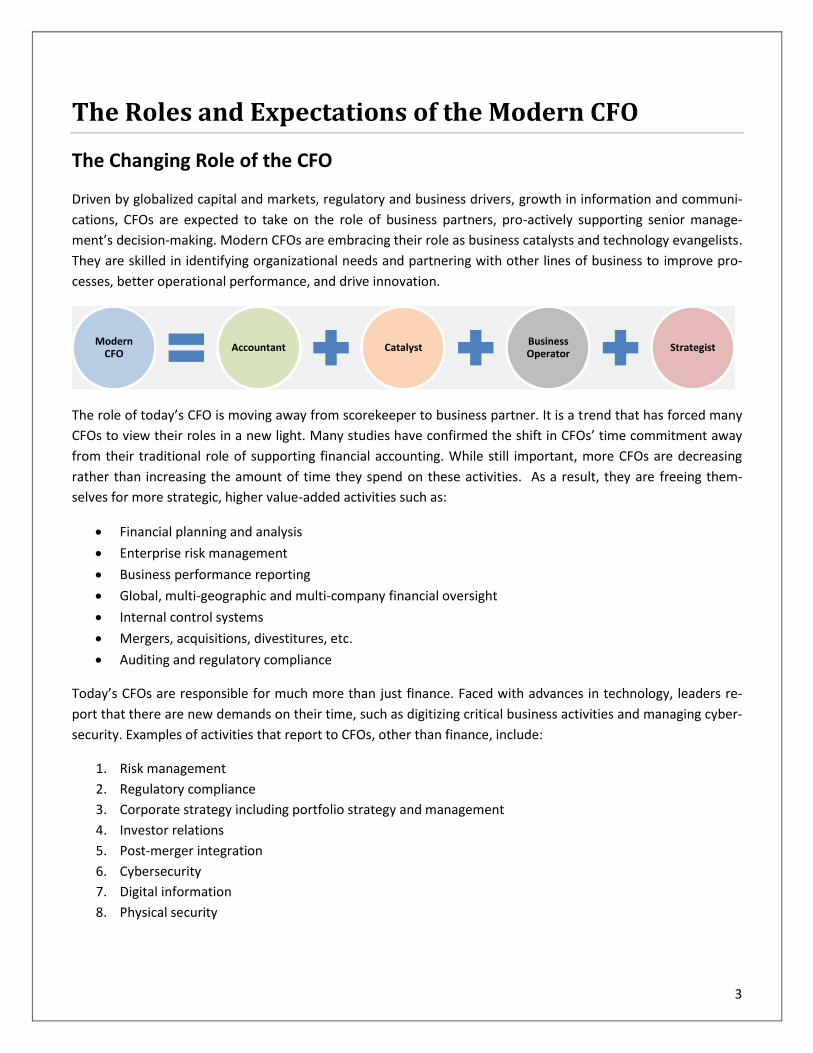

The Roles and Expectations of the Modern CFO

The Changing Role of the CFO

Driven by globalized capital and markets, regulatory and business drivers, growth in information and communi-

cations, CFOs are expected to take on the role of business partners, pro-actively supporting senior manage-

ment’s decision-making. Modern CFOs are embracing their role as business catalysts and technology evangelists.

They are skilled in identifying organizational needs and partnering with other lines of business to improve pro-

cesses, better operational performance, and drive innovation.

The role of today’s CFO is moving away from scorekeeper to business partner. It is a trend that has forced many

CFOs to view their roles in a new light. Many studies have confirmed the shift in CFOs’ time commitment away

from their traditional role of supporting financial accounting. While still important, more CFOs are decreasing

rather than increasing the amount of time they spend on these activities. As a result, they are freeing them-

selves for more strategic, higher value-added activities such as:

• Financial planning and analysis

• Enterprise risk management

• Business performance reporting

• Global, multi-geographic and multi-company financial oversight

• Internal control systems

• Mergers, acquisitions, divestitures, etc.

• Auditing and regulatory compliance

Today’s CFOs are responsible for much more than just finance. Faced with advances in technology, leaders re-

port that there are new demands on their time, such as digitizing critical business activities and managing cyber-

security. Examples of activities that report to CFOs, other than finance, include:

1. Risk management

2. Regulatory compliance

3. Corporate strategy including portfolio strategy and management

4. Investor relations

5. Post-merger integration

6. Cybersecurity

7. Digital information

8. Physical security

StrategistBusiness Operator

CatalystAccountantModern

CFO

4

CFOs have been striving to transform the finance function from an inward-looking organization focused primari-

ly on financial reporting, to one that spends more time focused on strategic decision-making and value creation.

The CFO is now recognized as a partner to the CEO, requiring a broader set of skills and responsibilities. CEOs

and boards are expecting the CFO to contribute to almost all major decisions including growth and acquisition

strategy, as well as the evaluation of investments. Thus, the top requirements of the board from a CFO are:

Today’s CFOs often need to spend one-third of their time communicating with their finance team and stake-

holders, it is not enough for them to just produce and report the financial results. It is increasingly important for

CFOs to understand how the organization arrived at those results and to provide insights from those results. An

evolving CFO increasingly understands the business across all lines, not just the financial aspects. He/she needs

to know, for instance, what revenue increase expectation Marketing has in launching a discounted price cam-

paign, or why Production has decided to change electrical cables requiring another sizeable investment.

Ernst & Young highlighted six principal activities that represent the contribution of today’s top CFOs, including:

1. Ensuring business decisions are grounded in solid financial criteria.

2. Providing insight and analysis to support the CEO and other senior managers.

3. Leading key initiatives in finance that support overall strategic goals.

4. Funding, enabling and executing the strategy set by the CEO.

5. Developing and defining the overall strategy for the organization.

6. Communicating the organization’s progress on strategic goals to external stakeholders.

The following table summarizes the key skills of evolving CFOs and suggestions about how to improve these

skills:

Strategic Thinking

• Keep abreast of the latest business developments, thinking and practices.

• Embrace and leverage information technology and deploy data analytics to spot

trends and changes in the business environment.

• Partner with other C-suite executives to develop operation plans and strategies.

• Plan scenarios and evaluate different options for application.

Communication

• Learn to handle and leverage to new forms of media (e.g. social media).

• Review internal information capture, retrieval and reporting processes to ensure

timely, accurate and transparent responses.

• Communicate changes in strategy and direction to internal stakeholders in a

timely and detailed manner.

Risk Management

• Keep abreast of the latest risk management developments, practices and ERM

models.

• Develop full understanding of changes in business profile and models.

Strategic partnerAnnual budgeting

and outlook forecasting

Risk managementCommunication and

influencing skills

5

• Revalidate existing risks, identify new risks, and measure changes in risk profile

and impact of the risks in the risk register.

• Review the ERM framework to ensure appropriate processes and procedures are

in place to either mitigate or minimize the risks.

Analysis and

Advisory

• Build knowledge of data analytics and analytical tools and their use.

• Apply analytics on the organization’s financial and operational data to reduce

the cost per transaction, monitor gross margins across product or service lines,

and identify anomalies or unusual transactions.

• Leverage analysis and provide feedback to operations and other departments for

improvements to policies and processes.

People

Management

• Support continuing education of finance staff including developing and enhanc-

ing technical competency and analysis skills.

• Help the finance team build the necessary platform to partner other functions to

improve operational performance.

Source: EY, Ready for the future economy? 2016

To ensure a well-governed organization, it is critical to have professional accountants in key finance leadership

roles. In particular, the CFO should be a vital part of a chain of actors, including the governing body (e.g. board of

directors), CEO, audit committee, and auditor. They all have their respective responsibilities to ensure that busi-

ness reporting provides relevant, accurate, and comparable information on the financial position and perfor-

mance of an organization. In addition, the transparency, financial stability, and performance of governments and

public sector organizations are closely linked with the quality and professionalism of the CFO and the finance

function.

How can the CFO help to ensure that the board makes good use of its limited time?

1. Plan carefully, even aggressively, in securing the time required to focus on the most important issues, for ex-

ample, by giving priority and quality time to strategic discussions and fitting the routine issues around them ra-

ther than the other way around.

2. Manage expectations, for example, it may not be possible or wise to complete a major strategic discussion in

one day. It may need to be supported by site visits, specialized briefings and/or in-depth work on historic and

future performance before all these strands can be brought together to make strategic decisions.

3. Use opportunities for free-flowing conversation, for example, at dinners the night before the Board meeting.

These can also be valuable for leveraging the diverse talents of the non-executive directors by getting them to

talk about their skills and experience.

4. Think carefully about what the board needs to hear and don’t assume that the 40-slide presentation is al-

ways the best approach. Instead, make strategic use of pre-reads and concentrate on facilitating a meaningful

discussion.

Source: Chartered Institute of Management Accountants, The Role of the CFO on the Modern Board, 2017

6

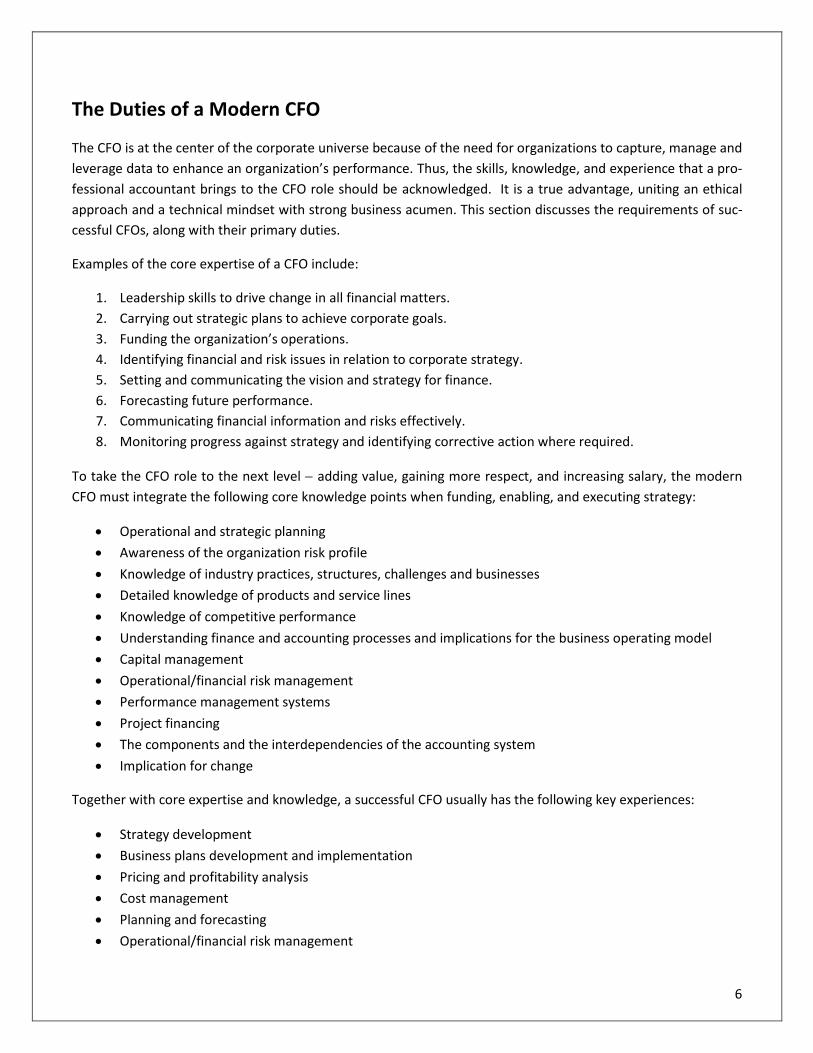

The Duties of a Modern CFO

The CFO is at the center of the corporate universe because of the need for organizations to capture, manage and

leverage data to enhance an organization’s performance. Thus, the skills, knowledge, and experience that a pro-

fessional accountant brings to the CFO role should be acknowledged. It is a true advantage, uniting an ethical

approach and a technical mindset with strong business acumen. This section discusses the requirements of suc-

cessful CFOs, along with their primary duties.

Examples of the core expertise of a CFO include:

1. Leadership skills to drive change in all financial matters.

2. Carrying out strategic plans to achieve corporate goals.

3. Funding the organization’s operations.

4. Identifying financial and risk issues in relation to corporate strategy.

5. Setting and communicating the vision and strategy for finance.

6. Forecasting future performance.

7. Communicating financial information and risks effectively.

8. Monitoring progress against strategy and identifying corrective action where required.

To take the CFO role to the next level − adding value, gaining more respect, and increasing salary, the modern

CFO must integrate the following core knowledge points when funding, enabling, and executing strategy:

• Operational and strategic planning

• Awareness of the organization risk profile

• Knowledge of industry practices, structures, challenges and businesses

• Detailed knowledge of products and service lines

• Knowledge of competitive performance

• Understanding finance and accounting processes and implications for the business operating model

• Capital management

• Operational/financial risk management

• Performance management systems

• Project financing

• The components and the interdependencies of the accounting system

• Implication for change

Together with core expertise and knowledge, a successful CFO usually has the following key experiences:

• Strategy development

• Business plans development and implementation

• Pricing and profitability analysis

• Cost management

• Planning and forecasting

• Operational/financial risk management

7

• Financial planning and reporting

• Financial process improvement and transformation

• International exposure (e.g., managing diverse teams, understanding global markets)

• Dealing with mergers or acquisitions

• Managing relationships with external parties (e.g., regulators, auditors, investors)

CFOs’ expertise, knowledge, and experience are essential elements in an effective leadership team as well as for

ensuring strong management practices and information systems, supported by an appropriate infrastructure

and ethical culture. Robert Half identifies the following typical job duties for the CFO:

1. Directing accounting policies, procedures and internal controls.

2. Providing strategic management of the accounting and finance functions.

3. Recommending improvements to ensure the integrity of a company’s financial information.

4. Managing or overseeing the relationship with independent auditors.

5. Collaborating with CIOs on technology decisions.

6. Overseeing financial systems implementations and upgrades.

7. Managing relationships with investors and investment institutions.

8. Identifying and managing business risks and insurance requirements.

As businesses grow in complexity and size, so do the expectations of a CFO. In addition to being the financial

gatekeeper, the CFO is also expected to participate in driving the organization toward achieving its objectives.

For example, CFOs are called upon more often to apply their analytical and business skills to more strategically

oriented organizational issues, increasing the value that they provide to their organization. A highly influential

CFO usually spends the most time on the following tasks:

• Strategic business planning

• Working capital and cash flow management

• Risk management

• Financial policy making and planning

• Corporate governance

• Financial reporting

• Investment strategy and management

• Regulatory compliance

• Investor relations and stakeholder management

8

The following represents a snapshot of the average CFO compensation and background for public and private

sectors.

Portrait of a CFO

Public Private Median base salary $300,00 $200,000 Median annual bonus $99,000 $ 42,000 Median total compensation, including salary, bonus, long- term compensation and value of all benefits

$513,000 $285,000

Eligible to receive cash-based long-term incentives 22% 23% Eligible stock-based long-term incentives 89% 46% Employment contracts prevalence 88% 47% Most popular CFO contract provision is change-in-control severance, based on number of months

46% 41%

Eligible to participate in a defined benefit plan 30% 14% Has a master’s degree 48% 53% Years in current position 6 7 Female 22% 19% Male 78% 81%

Source: Grant Thornton, Financial Executive Compensation Report 2017

In summary, modern CFOs are expected to be both a strategist and a controller, focusing on growth and cost

management. They must combine traditional qualities with new responsibilities. The duties of operational effi-

ciency, compliance with corporate and regulatory standards, and safeguarding the integrity of company and

stakeholder data are still firmly on the CFO’s agenda. Moreover, CFOs continue to be responsible for financial

management, accounting and control, as well as areas such as IT, HR and risk management in smaller and pri-

vately-owned firms. They unite in-depth financial expertise with additional capabilities in IT, legal, HR and pro-

curement, and the ability to drive change. These attributes and many more seem very much in the CFO skill set,

as the role becomes increasingly strategic.

Professional Accountants in Business

Professional accountants working in business can typically be found in four types of roles: as value creators, en-

ablers, preservers, and reporters. The CFO principles relate to these roles and need to ensure success in each by: