Embed Size (px)

Citation preview

CFS021002HK-ZWE391-ql

Predicting Stock Market Returns with Aggregate Discretionary Accruals

Qiang Kang, University of Miami Qiao Liu, University of Hong Kong Rong Qi, St. John’s University

2006 NTUICF December 2006

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Account for Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

Motivations

Managerial Market Timing

The Discounted-Cash-Flow Model Aggregate corporate decision

variables such as aggregate investment plans (Lamont 2000); IPOs (Baker and Wurgler 2000); insider trading (Lakonishok and Lee 2001) are able to predict stock market returns.

Earnings management, measured by (discretionary) accruals, is routine decision subject to a great deal of discretion. Then, do aggregate earnings management decisions predict stock market returns?

Modern markets show micro-efficiency but considerable macro-inefficiency (Shiller 2001; Lamont and Stein 2006).

Aggregate earnings have little predicative power (Kothari, Lewellen, and Warner 2005). Not sure whether another component of cash flow – accruals – has predicative power.

Especially, it has been suggested that accruals/discretionary accruals are able to predict stock returns at firm- and portfolio- levels (Sloan 1996; Xie 2001).

Some preliminary evidence shows that total accruals do predict market returns (Hirshleifer, Hou, and Teoh, 2005). But reasons remain unclear.

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Drives Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

This Paper Mainly Attacks Three Questions

Do aggregate accruals predict stock market returns?

What drives aggregate accruals’ return predictability --- normal accruals vs. discretionary accruals?

What accounts for aggregate accruals’ return predictability --- testing equity market timing hypothesis

The Focus of Our Empirical

Analysis!

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Account for Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

Variables

Accruals measures

Other variables We apply the balance sheet method

(Sloan 1996)

Normal vs. Discretionary Accruals

The predicted value is normal accrual, while the residual is defined as discretionary accrual

We use both equal-weighting method and value-weighting method to aggregate accruals and normal or discretionary accruals

Market returns – annual returns on both equal weighted and value weighted NYSE/AMEX indexes in excess of the one-month Treasure bill rate from 1965 to 2004.

The commonly used return predictors include:Dividend yield (DP); Term premium (TERM); Default premium; Short rate (TB1M); stochastically-detrended short rate (SHORT); The consumption-wealth ratio (CAY); equal-weighted and value weighted book-to market ratio; equity shares in new issues (S); investor sentiment index (SF2RAW); aggregate corporate investment plans (GHAT)

The Dynamics of Aggregate Accruals Measures across Time

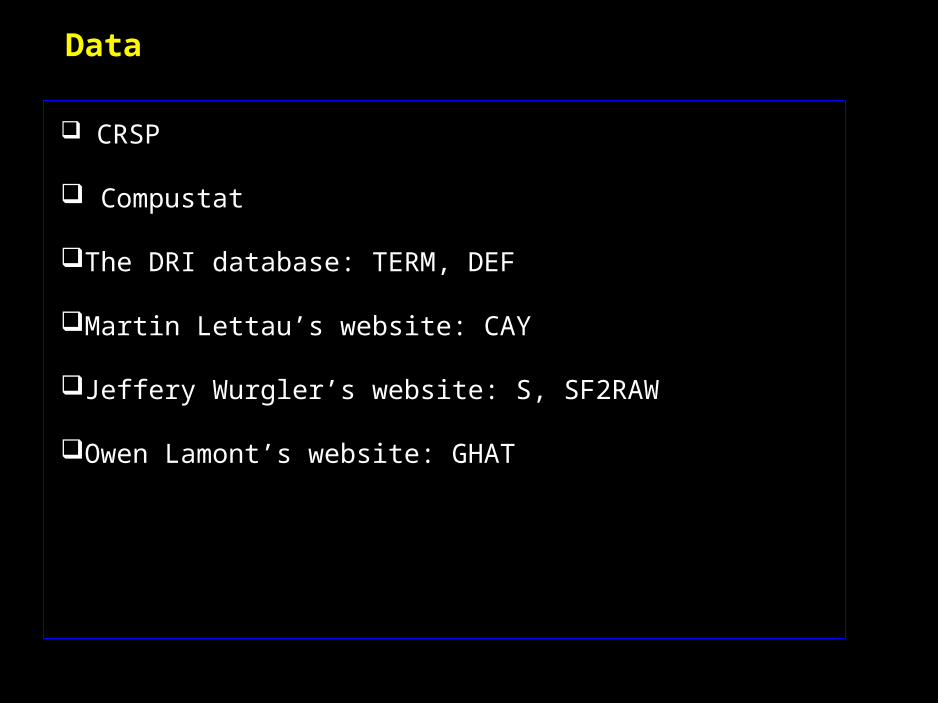

Data

CRSP

Compustat

The DRI database: TERM, DEF

Martin Lettau’s website: CAY

Jeffery Wurgler’s website: S, SF2RAW

Owen Lamont’s website: GHAT

Summary Statistics – Panel A of Table 1

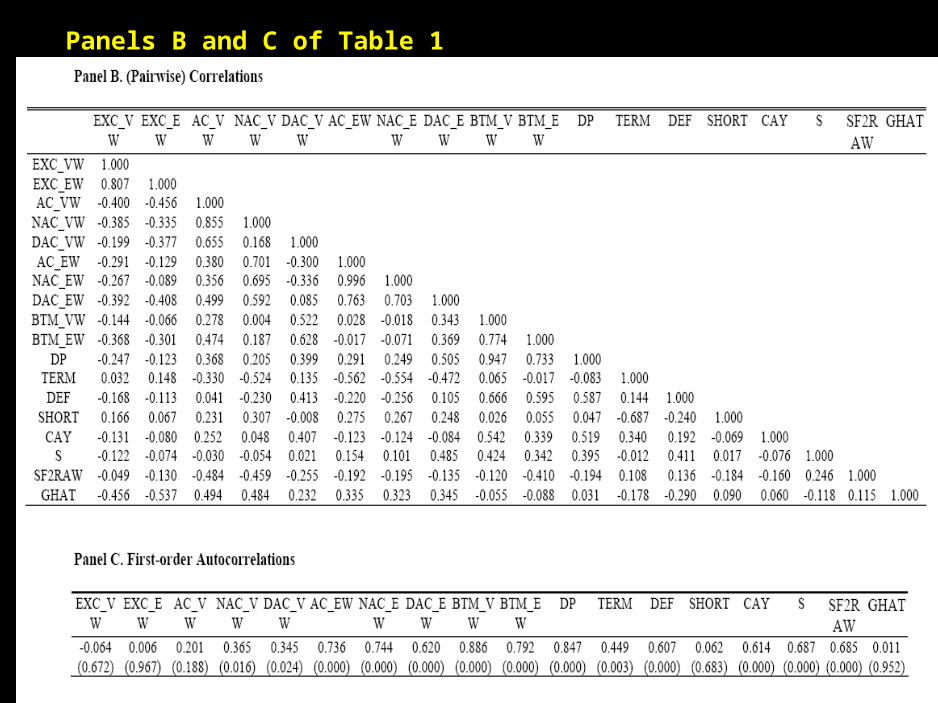

Panels B and C of Table 1

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Account for Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

First of all, we need to establish that small-sample bias is not a big concern

We test the null hypothesis of no stock return predictability by creating 50,000 serioes of value-weighted market return based on the following system and then do OLS

Value-Weighted Aggregate Accruals are a predictor of Stock Market Return – Panel A of Table 2

Value-weighed aggregate accrual is one robust predictor!

And, Aggregate Accruals' return predictability is solely driven by aggregate discretionary accruals, not normal accruals – Univariate Analysis

Value-weighted aggregate discretionary accruals explain excess stock market returns!

And, Aggregate Accruals' return predictability is solely driven by aggregate discretionary accruals, not normal accruals – Multivariate Analysis

Value-weighted aggregate discretionary accruals’ return

predictability is robust to inclusion of other know

predictors.

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Account for Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

Market Efficiency Argument I: Testing Omitted Factor Hypothesis

There is only one-directional Granger causality form the value-weighted (discretionary) accruals to the aggregate stock market returns. The omitted factor hypothesis, which implies a bi-directional Granger causality between the two, lacks the empirical support!

Market Efficiency Argument II: Aggregate accruals as Proxies for Business Conditions

Aggregate normal accruals are a predictor of GDP growth. But value-weighted aggregate discretionary accruals are not!!!

Using Value-Weighted Discretionary Accruals to Predict Market Excess Return

Using Value-Weighted Discretionary Accruals to Predict Market Excess Return

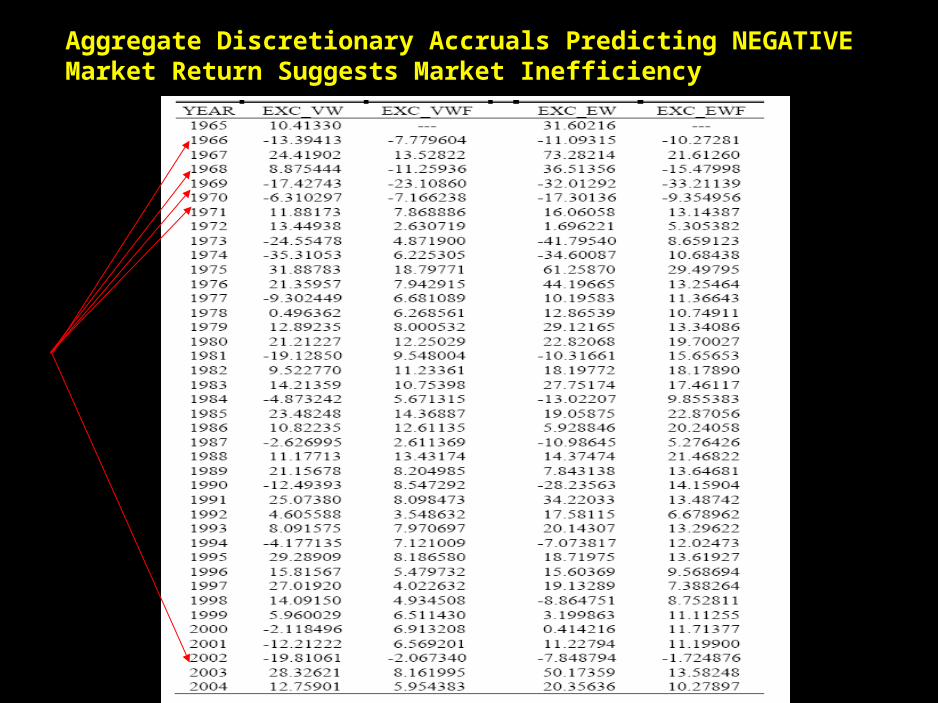

Aggregate Discretionary Accruals Predicting NEGATIVE Market Return Suggests Market Inefficiency

We Apply the GMM Estimation To Explore the Contemporaneous Relations between Aggregate Accruals and Aggregate Market Returns

We Apply the GMM Estimation To Explore the Contemporaneous Relations between Aggregate Accruals and GDP Growth Rate

The Aggregate Discretionary Accruals’ Return Predictability is Mainly Driven by Large Firms

Thanks

• Motivations

• Research Questions

• Data and Variables

• Do Aggregate Discretionary Accruals Predict Stock Market Returns?

• What Drives Aggregate Discretionary Accruals’ Return Predictability?

• Conclusion and Future Research

Presentation Outline

Our Main Thesis

Total Aggregate accrualsValue-weighted Discretionary accruals

• The value-weighted aggregate accruals are able to predict one-year ahead excess market returns

• The aggregate accruals’ return predictability is driven by value-weighted discretionary accruals --- which can be used to measure the overall level of earnings management

• Aggregate normal accruals, while highly correlated with macroeconomic variables, have no predictive power

• Value weighted discretionary accruals predict negative returns suggest market inefficiency

• Various evidence favors managerial equity market timing hypothesis

• The value-weighted discretionary accruals are robust with the inclusion of other proxies for market timing abilities

Market inefficiency – equity market timing Hypothesis

Future Research

Why equal-weighted discretionary accruals do not have any predicative power?

Further understanding of the properties of value-weighted discretionary accruals

Cross-country Comparison?

Others…

Thanks