Embed Size (px)

Citation preview

Ch 15Home Purchase Decisions

Outline

1. Rent vs. Buy Decisions2. How Much Can You Afford?3. Choosing the property:

a) Choosing the Areab) Evaluating the Homec) Making the Deal

1. Rent vs. Buy Decisions Consider:

- Emotional factors - Financial Analysis: Monthly payments & value appreciation

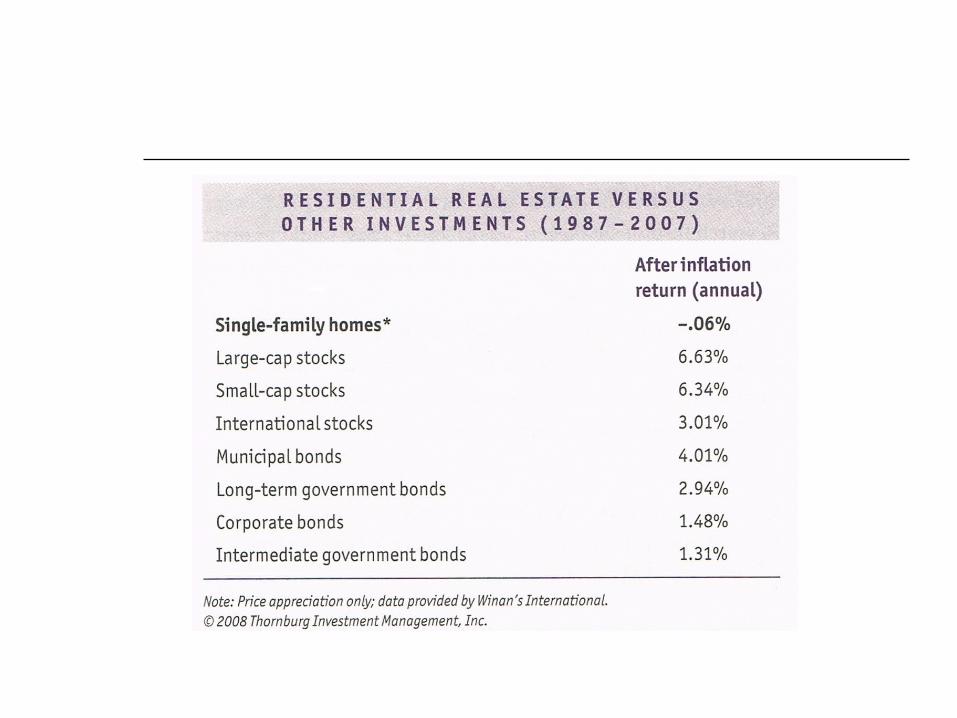

Variables to consider:- Tax consequences- Alternative investments- Inflation and home prices*- Impact of mortgage interest rates - Period of ownership

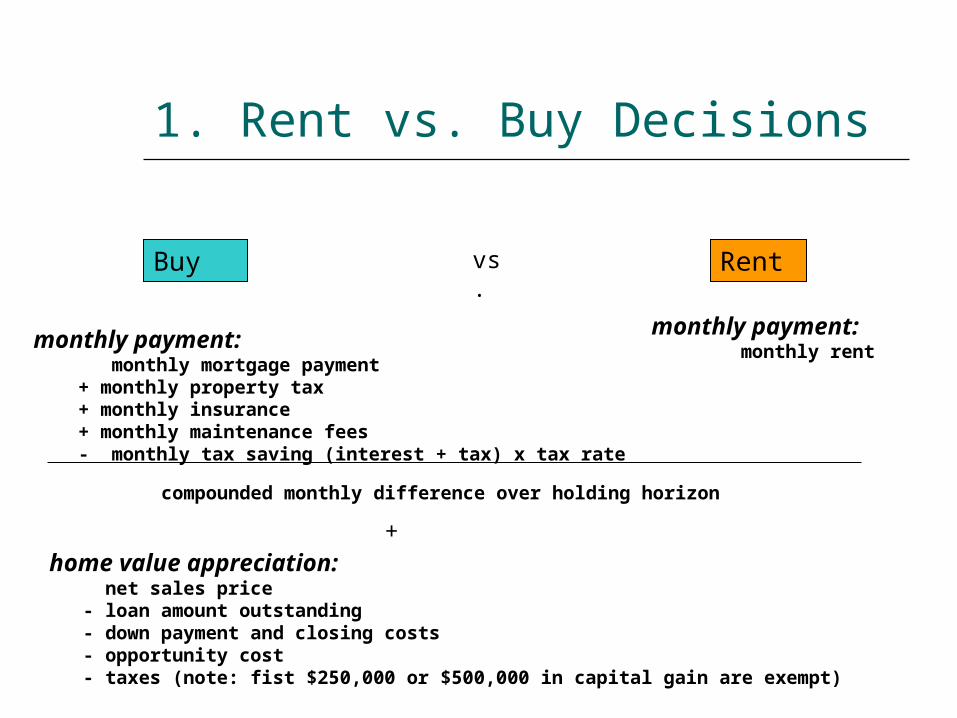

1. Rent vs. Buy Decisions

RentBuy vs.

monthly payment: monthly mortgage payment + monthly property tax + monthly insurance + monthly maintenance fees - monthly tax saving (interest + tax) x tax rate

monthly payment: monthly rent

+home value appreciation: net sales price - loan amount outstanding - down payment and closing costs - opportunity cost - taxes (note: fist $250,000 or $500,000 in capital gain are exempt)

compounded monthly difference over holding horizon

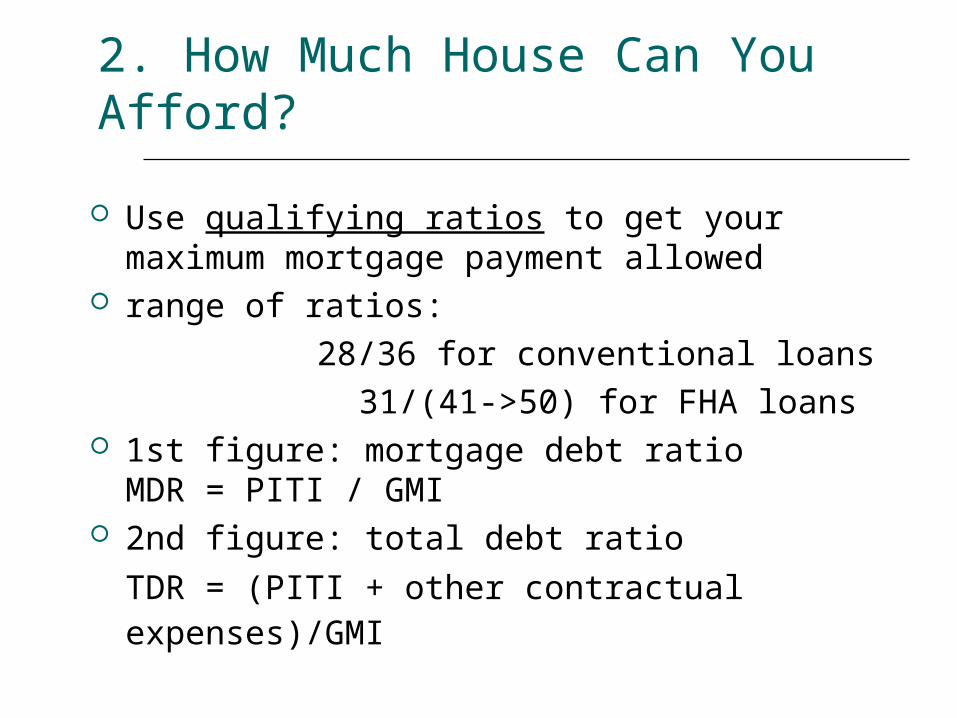

2. How Much House Can You Afford?

Use qualifying ratios to get your maximum mortgage payment allowed

range of ratios: 28/36 for conventional loans

31/(41->50) for FHA loans 1st figure: mortgage debt ratio

MDR = PITI / GMI 2nd figure: total debt ratio

TDR = (PITI + other contractual expenses)/GMI

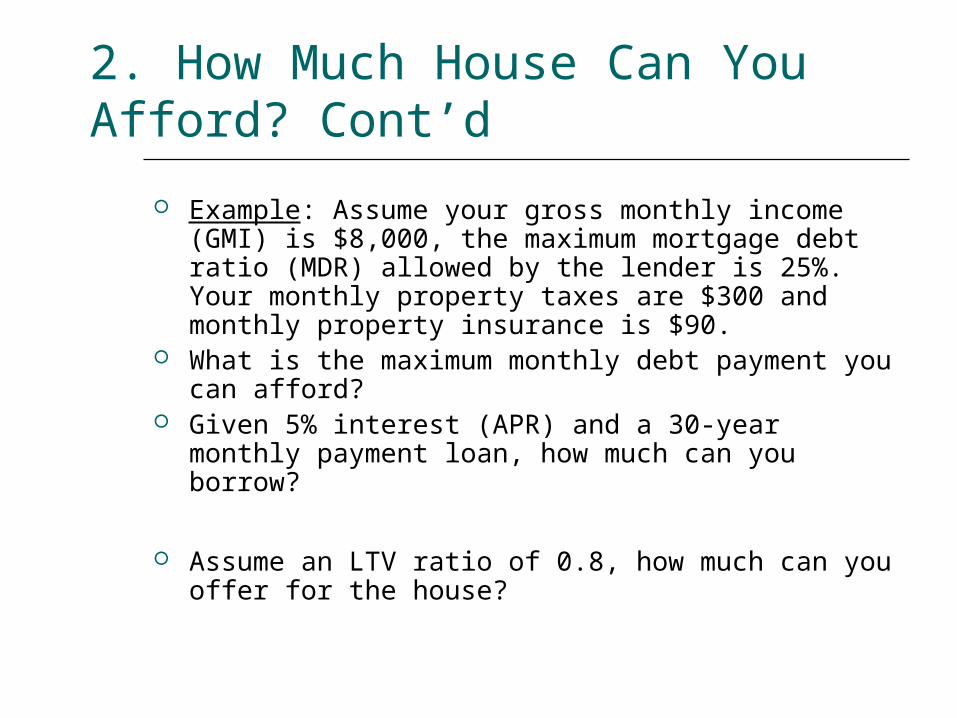

2. How Much House Can You Afford? Cont’d

Example: Assume your gross monthly income (GMI) is $8,000, the maximum mortgage debt ratio (MDR) allowed by the lender is 25%. Your monthly property taxes are $300 and monthly property insurance is $90.

What is the maximum monthly debt payment you can afford?

Given 5% interest (APR) and a 30-year monthly payment loan, how much can you borrow?

Assume an LTV ratio of 0.8, how much can you offer for the house?

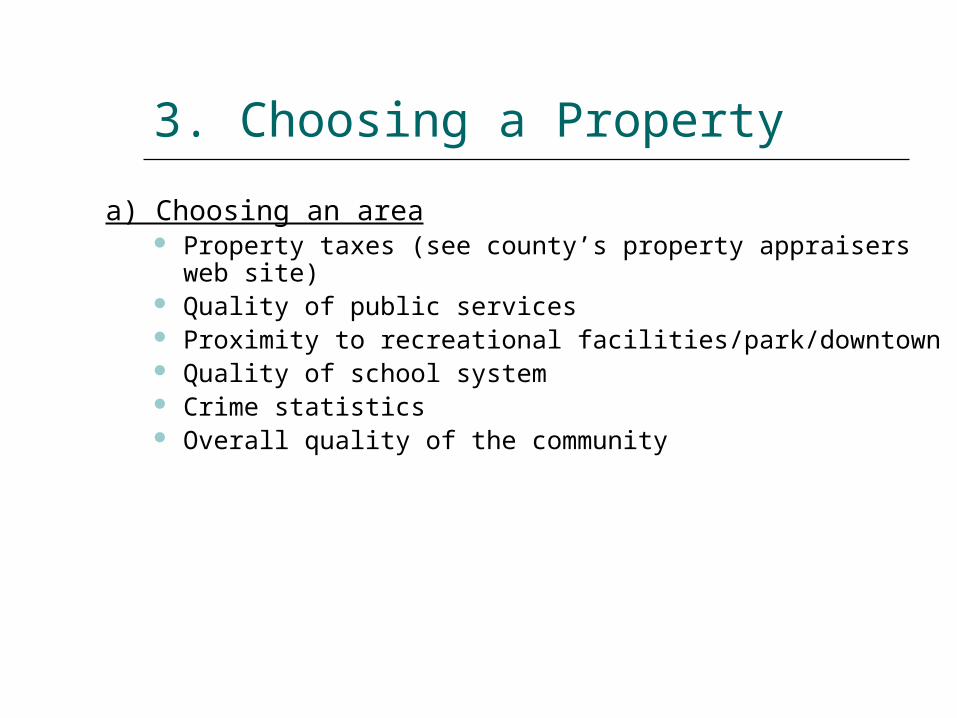

3. Choosing a Property

a) Choosing an area Property taxes (see county’s property appraisers web site) Quality of public services Proximity to recreational facilities/park/downtown Quality of school system Crime statistics Overall quality of the community

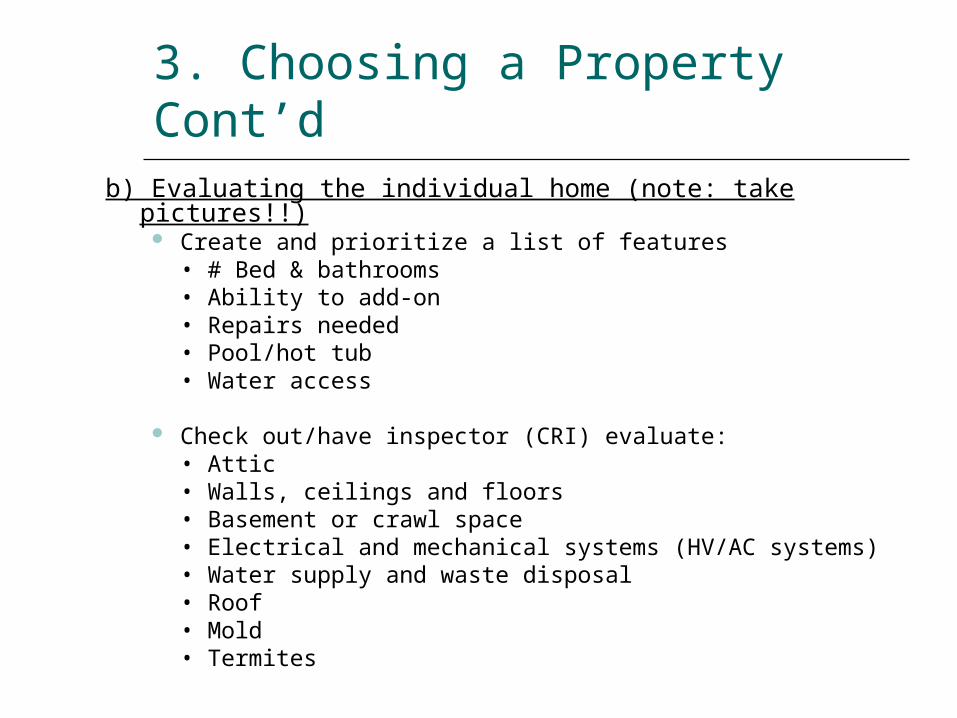

3. Choosing a Property Cont’db) Evaluating the individual home (note: take pictures!!)

Create and prioritize a list of features • # Bed & bathrooms• Ability to add-on• Repairs needed• Pool/hot tub• Water access

Check out/have inspector (CRI) evaluate: • Attic• Walls, ceilings and floors• Basement or crawl space• Electrical and mechanical systems (HV/AC systems)• Water supply and waste disposal • Roof• Mold• Termites

3. Choosing a Property Cont’d

c) Making and Closing the Deal - Real estate agents- Negotiating the price (remember: no emotions!)- Dealing with the lender

- Closing attorneys and escrow agents