Embed Size (px)

Citation preview

Challenges and Opportunities of the North American Petroleum Renaissance

Trisha Curtis, Director of Research, Upstream and Midstream Lou Pugliaresi, President Energy Policy Research Foundation, Inc. (EPRINC) Imperial College November 21st, 2013

Justin Kringstad Trisha Curtis

EPRINC Overview

• Established in 1944

• Publishes original research on oil and gas developments

• Routinely testifies before Congress, consults with U.S. and other Gov’t officials

• Brief policymakers, Hill staff on relevant energy topics

• Presents finding through industry and public forums, universities and think tanks

• Engagement with Washington Diplomatic Community – EPRINC Embassy Series

EPRINC’s PRIMARY MISSION IS TO EVALUATE THE INTERACTION OF PETROLEUM ECONOMICS AND PUBLIC POLICY

2

EPRINC Embassy Series

3

Photo by Yulan Guo

4

0

2

4

6

8

10

12

14

16

18

20

2013 2015 2017 2019 2021 2023

Mill

ion

Bar

rels

p

er

Day

Importance of the North American Lens

Saudi Arabia

Russia

USA

Iraq

Canada

N. America

Source: Wood Mackenzie (includes NGLs)

5

Source: EIA, EPRINC Calculations

U.S. Imports of Crude Oil and Petroleum Products as a Percent of GNP

6

Major Global Challenge: Managing OPEC Spare Capacity millions of barrels/day

Tight oil and Iraq are wild cards

here Regional Rivalries

and Downside Price Risk

Outline

7

Source: EIA

1. Breakdown of U.S. and Canadian Oil Production

2. Infrastructure Challenges in Moving Rising Volumes of North American Crude Oil

3. Regulatory Concerns and Conclusions

North American Oil Production

8

Source: EIA

0

2000

4000

6000

8000

10000

12000

Tho

usa

nd

Bar

rels

Pe

r D

ay

CanadianProduction ofCrude Oil

U.S. FieldProduction ofCrude Oil

August U.S. Oil Production 7.5 mbd

June Canadian Oil Production 3.7 mbd

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Mill

ion

Bar

rels

Per

Day

Periphery

Permian

Eagle Ford

Bakken

EPRINC’s Forecast for Major U.S. Shale Plays

Source: HPDI data with EPRINC forecast estimates

EPRINC forecasts an additional 1.5 mbd by 2022

9

CAPP 2013 Updated Production Forecast

10

Source: CAPP

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Tho

usa

nd

s o

f B

arre

ls p

er

Day

Mining

In Situ

Conventional Light

Conventional Heavy

Over 3 mbd increase by 2030

0

2000

4000

6000

8000

10000

12000

Tho

usa

nd

Bar

rels

Pe

r D

ay

U.S. Importsfrom Canada ofCrude Oil

U.S. FieldProduction ofCrude Oil

U.S. Imports ofCrude Oil

11

U.S. Total Imports, U.S. Production, U.S. Canadian Imports

Source: EIA

U.S. Imports 7.8 mbd U.S. Production 7.5 mbd

Canadian Imports 2.6 mbd

12

U.S. Activity

Source: HPDI September 2013, Past 90 Days

Williston

Basin

Powder River

Basin

Uinta

Basin

DJ Basin (Niobrara Reservoir)

Anadarko Basin

(Mississippian, Granite

Wash, Mississippi Lime

and other stacked plays)

Permian

Basin

Eagle Ford

Reservoir

Utica

Permit Activity

13

14

Drilling Then and Now

Source: From PIECE Course Workbook, Mark J Kaiser, Houston, July 2008, “Introduction to USA Petroleum Industry”

Source Rocks

14

15

North American Potential…Shale Oil Plays

15

16

So how much oil is there…?

Source: EPRINC

16

State Production Trends

17

Source: EIA

0

500

1000

1500

2000

2500

3000

Jan

-81

Ap

r-8

2

Jul-

83

Oct

-84

Jan

-86

Ap

r-8

7

Jul-

88

Oct

-89

Jan

-91

Ap

r-9

2

Jul-

93

Oct

-94

Jan

-96

Ap

r-9

7

Jul-

98

Oct

-99

Jan

-01

Ap

r-0

2

Jul-

03

Oct

-04

Jan

-06

Ap

r-0

7

Jul-

08

Oct

-09

Jan

-11

Ap

r-1

2

Jul-

13

Tho

usa

nd

Bar

rels

Per

Day

North Dakota FieldProduction of CrudeOil Mbbl/d

Alaska FieldProduction of CrudeOil Mbbl/d

Colorado FieldProduction of CrudeOil Mbbl/d

California FieldProduction of CrudeOil Mbbl/d

New Mexico FieldProduction of CrudeOil Mbbl/d

Texas FieldProduction of CrudeOil Mbbl/d

Source: Baker Hughes

18

U.S. Rig Count

0

500

1000

1500

2000

2500

# o

f R

igs

Oil

Gas

Total

U.S. Rig Activity by Drill Type

19

Source: HPDI Nov 2013 – Not 100% Complete

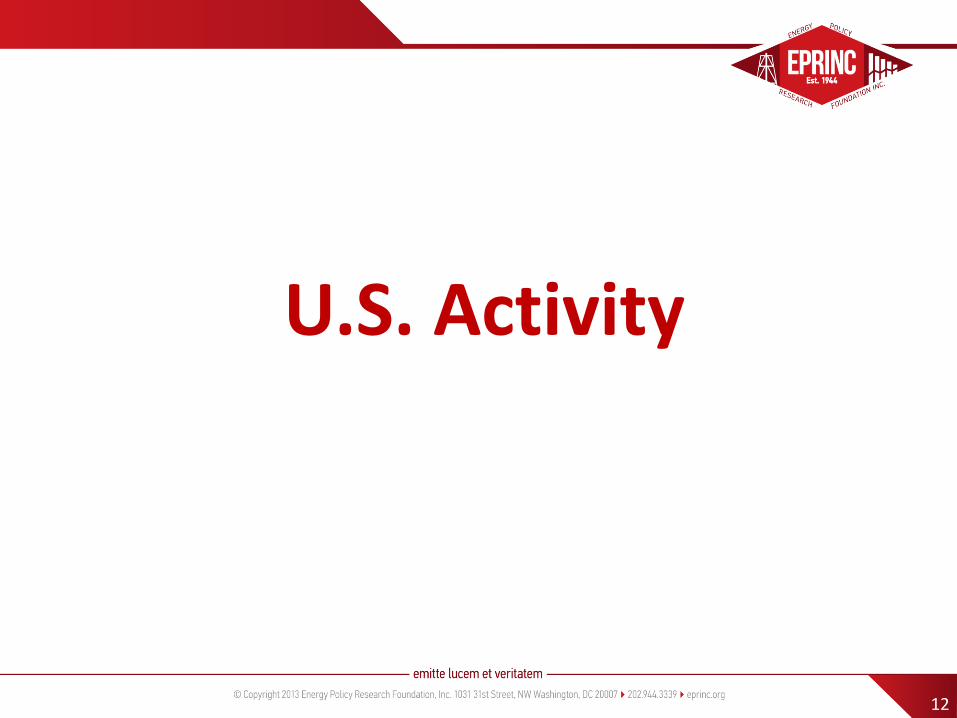

20

Source: ITG Investment Presentation Nov 2012

Shale Oil Play Break Even Costs

20

Source: NationalAtlas.gov

21

U.S. Federal Land Map

22

The Soaring Eagle Ford

23

Geology of the Eagle Ford

Source: Momentum Oil and Gas LLC, DUG Eagle Ford Conference Presentation Oct 2011

24

Source: HPDI Nov 2013

Eagle Ford Wells

25

Eagle Ford Production

Source: HPDI Nov 2013

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

0

200000

400000

600000

800000

1000000

1200000

12

/1/1

999

7/1

/20

00

2/1

/20

01

9/1

/20

01

4/1

/20

02

11

/1/2

002

6/1

/20

03

1/1

/20

04

8/1

/20

04

3/1

/20

05

10

/1/2

005

5/1

/20

06

12

/1/2

006

7/1

/20

07

2/1

/20

08

9/1

/20

08

4/1

/20

09

11

/1/2

009

6/1

/20

10

1/1

/20

11

8/1

/20

11

3/1

/20

12

10

/1/2

012

5/1

/20

13

Bar

rels

Per

Day

LIQ

GAS

26

The Prolific Permian Basin

27

Breakdown of the Permian Basin Province

Source: Permian Basin. Map. Encyclopædia Britannica Online. Web. 17 Jan. 2012. <http://www.britannica.com/EBchecked/media/94328/Map-of-the-

basins-reefs-and-platforms-that-make-up>.

Permian Basin Stratigraphy

28

Source: Concho Resources 2nd Quarter 2013 Investor Presentation

Permian Basin Production 1.3 mbd

29

Source: HPDI Oct 2013

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

1/1

/19

80

1/1

/19

81

1/1

/19

82

1/1

/19

83

1/1

/19

84

1/1

/19

85

1/1

/19

86

1/1

/19

87

1/1

/19

88

1/1

/19

89

1/1

/19

90

1/1

/19

91

1/1

/19

92

1/1

/19

93

1/1

/19

94

1/1

/19

95

1/1

/19

96

1/1

/19

97

1/1

/19

98

1/1

/19

99

1/1

/20

00

1/1

/20

01

1/1

/20

02

1/1

/20

03

1/1

/20

04

1/1

/20

05

1/1

/20

06

1/1

/20

07

1/1

/20

08

1/1

/20

09

1/1

/20

10

1/1

/20

11

1/1

/20

12

1/1

/20

13

mcf

/day

Bar

rels

Pe

r D

ay

LIQ

GAS

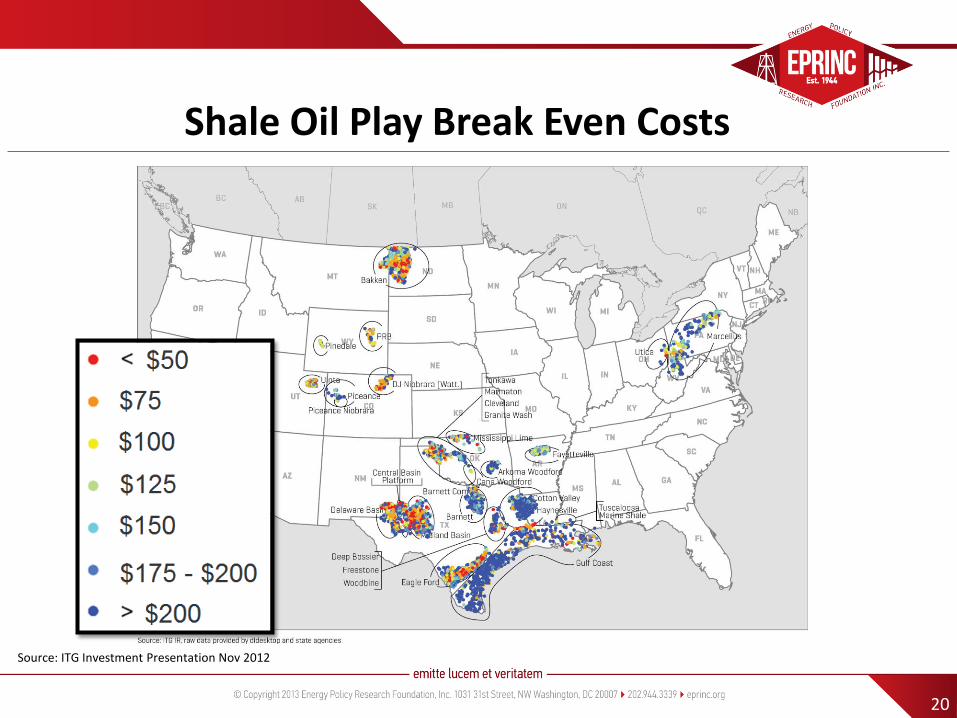

Vertical and Horizontal Progression

30

Source: Pioneer Natural Resources Oct 2013 Investor Presentation

EPRINC November Revised Permian Forecast

31

Source: EPRINC

32

Bakken: The Case Study

33

Long History of the Williston Basin

Source: Time Magazine 1952

34

Bakken Basics

Source: EPRINC Diagram

Source: Julie LeFever Presentation

35

Bakken Geology

36

Bakken Drilling

Source: Triangle Petroleum Corporation, Presentation Bakken Product Markets and Take-Away Denver Jan 31-Feb 1 2012

37

Williston Basin Production

Source: NDIC

North Dakota accounts for almost 10% of US Production Almost all new production is from the Bakken/Three Forks

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Tho

usa

nd

Bar

rels

Per

Day

North Dakota

Eastern Montana

South Dakota

TOTAL

38

Possible Production Figures

Source: NDPA

39

Decline Rates

Source: Lynn Helms, ND Dept. of Mineral Resources, NDPC Meeting Sept. 2011 Medora ND

40

Unlocking the Rocks

Source: Brigham Exploration via World Oil

Combining longer laterals with an increasing number of frac stages yields higher EURs is a short time period.

41

Infrastructure Challenges

Pipeline Choke Points

Source: EPRINC Choke Point Map using Hart ArcGIS Mapping software

42

All Canadian Pipeline Export Options are Full

Source: Canadian Energy Pipeline Association

43

Market Saturation

Source: CAPP Crude Oil Forecast June 2013

44

0

10

20

30

40

50

60

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

PADD 1East Coast

PADD 2Midwest

PADD 3Gulf Coast

PADD 4Rockies

PADD 5West Coast

Nu

mb

er

of

Re

fin

eri

es

Bar

rels

Pe

r C

ale

nd

ar D

ay

OperableAtmosphericCrude OilDistillationCapacity

ThermalCrackingCokingDownstreamChargeCapacity

OperatingRefineries

Where light sweet Bakken and heavy (blended bitumen) needs to go…

Source: AFPM map, EIA data for graph

Total Coking Capacity vs. Atmospheric Crude Distillation Capacity by PADD

Cokers = Heavy refining capability

45

Regional Pricing Disparities

Source: Flint Hills, EIA, CME Group, and estimates

• Western Canadian Select -$41 to WTI

46

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

Jan

-08

Jun

-08

No

v-0

8

Ap

r-0

9

Sep

-09

Feb

-10

Jul-

10

De

c-1

0

May

-11

Oct

-11

Mar

-12

Au

g-1

2

Jan

-13

Jun

-13

WTI

Bakken (NorthDakota LightSweet Flint Hills)

WCS (WesternCanadian Select)

Brent

47

The Rise of Rail

48

North Dakota Crude Oil Transport

Source: North Dakota Pipeline Authority

August 2013 Estimates January 2012 Estimates

49

Daily Crude by Rail Shipment in U.S. and Canada

Source: AAR; Crude and petroleum product includes liquefied gases, asphalt, fuel oil, lubricating oil, jet fuel, etc. U.S. operations exclude U.S. operations of CN and CP. Canadian operations include CN and CP and their U.S. operations. One carload holds 30,000 gallons (or 714.3 barrels).

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Jan

08

Ap

r 0

8

Jul 0

8

Oct

08

Jan

09

Ap

r 0

9

Jul 0

9

Oct

09

Jan

10

Ap

r 1

0

Jul 1

0

Oct

10

Jan

11

Ap

r 1

1

Jul 1

1

Oct

11

Jan

12

Ap

r 1

2

Jul 1

2

Oct

12

Jan

13

Ap

r 1

3

Jul 1

3

Bar

rels

Per

Day

U.S. Average BarrelsPer Day of Petroleumand Petroleum Product

Canadian AverageBarrels Per Day ofPetroleum andPetroleum Product

EPRINC's U.S. DailyCrude by Rail Estimate- 770,000 b/d

EPRINC's Canada DailyCrude by Rail Estimate- 130,000 b/d

50

Pipeline and Rail

Source: EPRINC Maps using Hart Energy data and ArcGIS Mapping software

• Severely limited due to lack of Keystone XL and lack of historical build out to the coasts – system designed to import into the Gulf and move up

50

• New markets • Diversification • Neat Barrels • Nimble - Quickly adjustable • Optionality for Canadian and U.S. crude, NGLS,

and other petroleum products

51

Refineries Benefit

Refinery Acquisition Cost of Crude Oil

Source: EIA

52

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

East Coast (PADD 1) Crude OilComposite Acquisition Cost by Refiners$/bbl

Midwest (PADD 2) Crude Oil CompositeAcquisition Cost by Refiners $/bbl

Rocky Mountain (PADD 4) Crude OilComposite Acquisition Cost by Refiners$/bbl

West Coast (PADD 5) Crude OilComposite Acquisition Cost by Refiners$/bbl

Gulf Coast (PADD 3) Crude OilComposite Acquisition Cost by Refiners$/bbl

Brent

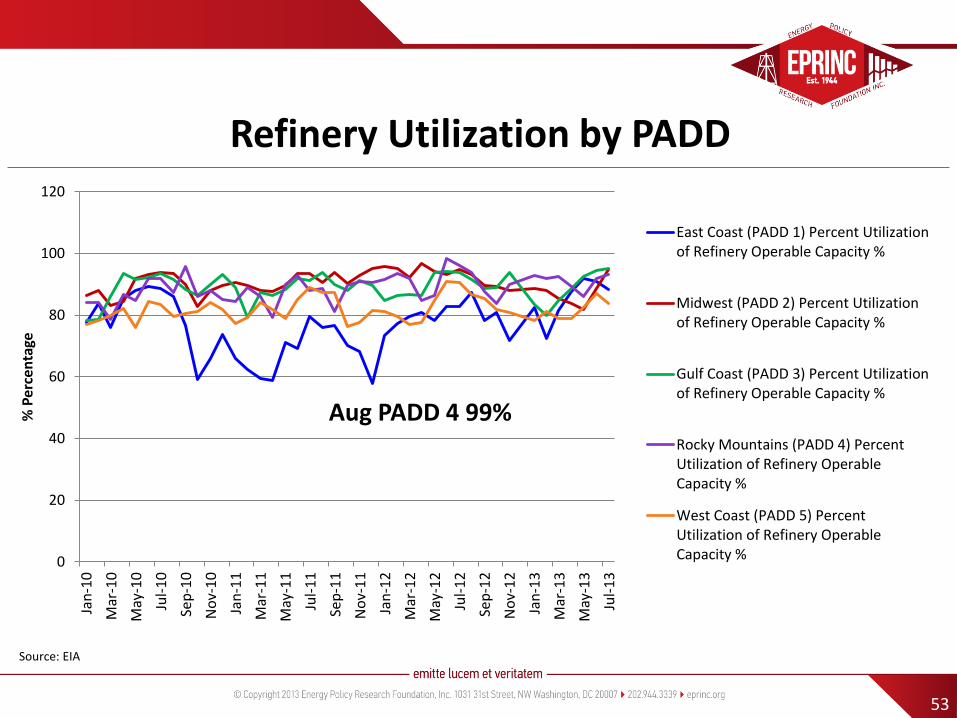

Refinery Utilization by PADD

Source: EIA

53

0

20

40

60

80

100

120

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

% P

erce

nta

ge

East Coast (PADD 1) Percent Utilizationof Refinery Operable Capacity %

Midwest (PADD 2) Percent Utilizationof Refinery Operable Capacity %

Gulf Coast (PADD 3) Percent Utilizationof Refinery Operable Capacity %

Rocky Mountains (PADD 4) PercentUtilization of Refinery OperableCapacity %

West Coast (PADD 5) PercentUtilization of Refinery OperableCapacity %

Aug PADD 4 99%

54

Regulatory Concerns and Conclusions

Potential Issues, Hurdles, and Regulatory Concerns

• Oil prices • Water Usage – Fracking and

Recycling • Oil spills (rail and pipeline) • Environmental Concerns • Regs on Federal Land-Fracking • Infrastructure Delays-PERMITTING • Lack of prudent policy making:

failing to connect what is happening on the ground to what is understood in Washington

• Costs incurred

55

Conclusions • Since 2008 the U.S. and Canada have added over 3 mbd of crude to global production,

helping offset issues in Libya and the Middle East. • Pipelines are being built, but right now their is tightness in the system and an

increasing need for Gateway, XL, and other Coastal options for US and Canadian crude. • Bakken crude has to get to the U.S. East and West Coasts (via rail) and heavy Canadian

needs to get to the Gulf and West Coast (via pipeline and rail). • Roughly 7.7 mbd of new capacity (as estimated by EPRINC) is comprised of pipeline

reversals, expansions, twinning, repurposing, and retrofitting. There are serious regulatory and permitting hurdles which deserve consideration.

• Even with a narrowing spread, rail is a serious option for US producers distanced from refining centers, especially Bakken and Canadian crude—markets exist where pipelines do not (especially with XL delay and Gateway uncertainty).

• Market has changes for producers and refiners with optionality, market and regulatory uncertainty

• Rail will be here in the long term, the question is simply how much and where. • Refineries are going to play a vital role in this renaissance as they adapt to high

volumes of light sweet and heavy crude oils.

56

57

APPENDIX

58

Source: NDPA

Natural Gas Flaring

59

Source: NDPA

Why?

60

Value of an Oil Well in North Dakota

Typical 2012 North Dakota Bakken well will produce for 29 years (enhanced oil recovery efforts could extend the life of the well) In those 29 years the average Bakken well: • Produces approximately 580,000 barrels of oil • Generates over $22 million net profit • Cost $8,500,000 to drill and complete (up from 7.3 last year)

• Pays approximately $4,610,000 in taxes

• $2,200,000 gross production taxes • $2,000,000 extraction tax • $410,000 sales tax • Pays royalties of $7,925,000 to mineral owners • Pays salaries and wages of $1,500,000 • Pays operating expenses of $2,300,000

Source: ND Department of Mineral Resources 2012 Presentation

61

Source: PacWest Consulting

Cost of Oil Sands Production

Source: “Canada’s Energy Future: Energy Supply and Demand Projections to 2035.” Nov 2011. NEB

61